Embed Size (px)

DESCRIPTION

CREDIT MONOTORING

Citation preview

CREDIT MONITORINGCREDIT MONITORING

CREDIT MONITORING IS IMPORTANT CREDIT MONITORING IS IMPORTANT PART OF CREDIT MANAGEMENTPART OF CREDIT MANAGEMENT

CREDIT MANAGEMENT INCLUDES LOAN CREDIT MANAGEMENT INCLUDES LOAN SCRUTINY, SANCTION, DOCUMENTATION, SCRUTINY, SANCTION, DOCUMENTATION, DISBURSEMENT, MONITORING, REVIEW, DISBURSEMENT, MONITORING, REVIEW,

RECOVERYRECOVERY

BROAD CLASSIFICATION OF BROAD CLASSIFICATION OF CREDIT FACILITIESCREDIT FACILITIES

PERIOD-WISE CLASSIFICATIONPERIOD-WISE CLASSIFICATION Short Term Loans 12 MonthsShort Term Loans 12 Months Medium Term Loan > 12 to 60 MonthsMedium Term Loan > 12 to 60 Months Long Term Loans > 60 MonthsLong Term Loans > 60 Months

SECURITY WISE CLASSIFICATIONSECURITY WISE CLASSIFICATION Secured – Cash Credit/Over Draft/Term Secured – Cash Credit/Over Draft/Term

Loan/Home Loan, etc.Loan/Home Loan, etc. Un-Secured – Personal Loans/ Overdrafts.Un-Secured – Personal Loans/ Overdrafts.

Loan RegistersLoan Registers Loan application Inward RegisterLoan application Inward Register Loan Sanction RegisterLoan Sanction Register Documents RegisterDocuments Register Mortgage Security RegisterMortgage Security Register Bill Discount RegisterBill Discount Register Stock Statement RegisterStock Statement Register Drawing Power RegisterDrawing Power Register Insurance RegisterInsurance Register Excess Over Draft/Temp. Over Draft RegisterExcess Over Draft/Temp. Over Draft Register Due Date DairyDue Date Dairy Review/Renewal RegisterReview/Renewal Register Suit Filed RegisterSuit Filed Register

Stages of Credit MonitoringStages of Credit Monitoring

Stock/Book Debt ScrutinyStock/Book Debt Scrutiny Insurance of Assets charged to BankInsurance of Assets charged to Bank Operation in the accountOperation in the account Inspection of securitiesInspection of securities Review/Renewal of accountsReview/Renewal of accounts Notifying irregularities to clients Notifying irregularities to clients Ensuring rectification of regularitiesEnsuring rectification of regularities Follow up for recovery of duesFollow up for recovery of dues

SCRUTINY OF STOCK/BOOK DEBTSSCRUTINY OF STOCK/BOOK DEBTS

Please Ensure that:Please Ensure that:a)a) The statement is as per Bank’s formatThe statement is as per Bank’s formatb)b) Record date of receipt of statementRecord date of receipt of statementc)c) It is complete in all respects It is complete in all respects d)d) Is signed by authorized person of clientIs signed by authorized person of cliente)e) No major deviation in the level of current assets declared by client No major deviation in the level of current assets declared by client

compared to the one assessed by Bank.compared to the one assessed by Bank.f)f) Unpaid stocks and stocks/BDs older than 90 days are shown separately.Unpaid stocks and stocks/BDs older than 90 days are shown separately.g)g) No slow moving/obsolete stocks are foundNo slow moving/obsolete stocks are foundh)h) Stock Opening Balance + Purchases-Sales @ cost equals Closing stock Stock Opening Balance + Purchases-Sales @ cost equals Closing stock i)i) Value of Bills discounted is excluded in Book Debt StatementsValue of Bills discounted is excluded in Book Debt Statementsj)j) Client’s auditor certifies the Book Debt statement periodicallyClient’s auditor certifies the Book Debt statement periodicallyk)k) Stocks are stored in proper addresses and proper insurance is taken for Stocks are stored in proper addresses and proper insurance is taken for

that premises.that premises.

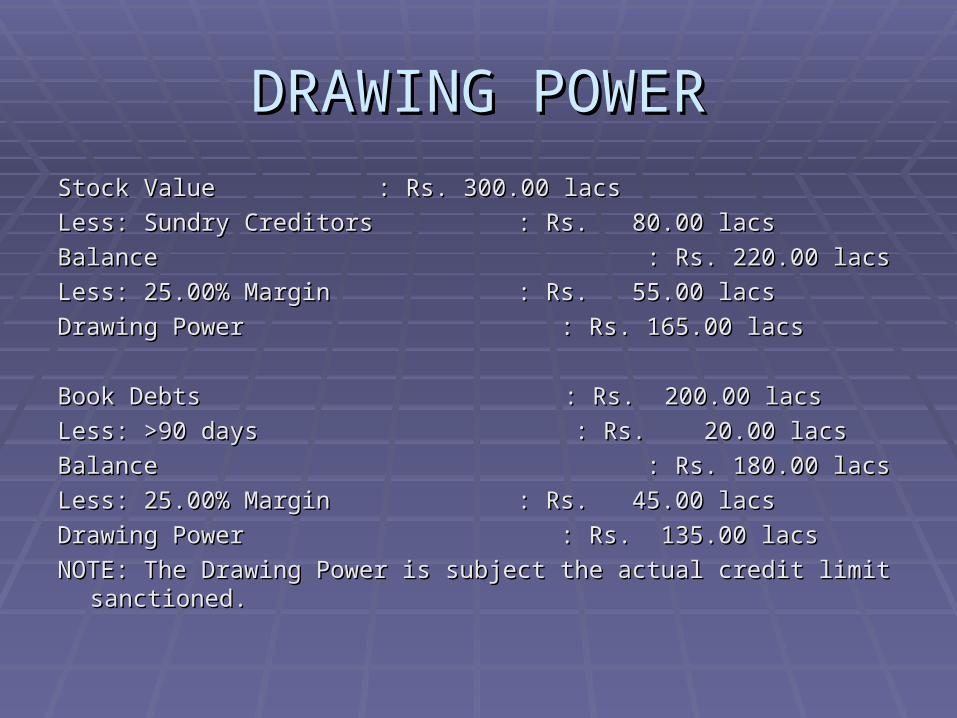

DRAWING POWERDRAWING POWER

Stock ValueStock Value : Rs. 300.00 lacs : Rs. 300.00 lacs

Less: Sundry Creditors : Rs. 80.00 lacsLess: Sundry Creditors : Rs. 80.00 lacs

Balance : Rs. 220.00 lacs Balance : Rs. 220.00 lacs

Less: 25.00% Margin : Rs. 55.00 lacsLess: 25.00% Margin : Rs. 55.00 lacs

Drawing Power : Rs. 165.00 lacsDrawing Power : Rs. 165.00 lacs

Book Debts Book Debts : Rs. 200.00 lacs : Rs. 200.00 lacs

Less: >90 days : Rs. 20.00 lacsLess: >90 days : Rs. 20.00 lacs

Balance : Rs. 180.00 lacs Balance : Rs. 180.00 lacs

Less: 25.00% Margin : Rs. 45.00 lacsLess: 25.00% Margin : Rs. 45.00 lacs

Drawing Power : Rs. 135.00 lacsDrawing Power : Rs. 135.00 lacs

NOTE: The Drawing Power is subject the actual credit limit sanctioned.NOTE: The Drawing Power is subject the actual credit limit sanctioned.

Monitoring of CC/OD AccountMonitoring of CC/OD Account

Account Operations:Account Operations: Turnover to match limit sanctionedTurnover to match limit sanctioned Turnover to match sales realized Turnover to match sales realized Average UtilizationAverage Utilization Minimum Balance Maximum BalanceMinimum Balance Maximum Balance Servicing of Interest charged in timeServicing of Interest charged in time EOL – Rare/sometimes/frequentEOL – Rare/sometimes/frequent Cheque Returns – Rare/FrequentCheque Returns – Rare/Frequent Cash Withdrawals justificationCash Withdrawals justification DP to cover outstanding in accountDP to cover outstanding in account Diversion Internal/External is observedDiversion Internal/External is observed Payments are business related.Payments are business related. Whether OD Bills debited to CC accountWhether OD Bills debited to CC account END USE OF THE FUNDS TO BE ENSUREDEND USE OF THE FUNDS TO BE ENSURED

UNIT INSPECTIONUNIT INSPECTION

Unit inspection is warranted to ensure that the funds Unit inspection is warranted to ensure that the funds lent by Bank is used for the purpose for which it is lent by Bank is used for the purpose for which it is lent.lent.

Scope of inspection is beyond mere stock verification.Scope of inspection is beyond mere stock verification. Banker to interact with the client about the present Banker to interact with the client about the present

trend in business and also any problem faced by him trend in business and also any problem faced by him to find solution.to find solution.

To ensure that there is no statutory violation by the To ensure that there is no statutory violation by the borrower.borrower.

It helps to improve client-banker personal It helps to improve client-banker personal relationship.relationship.

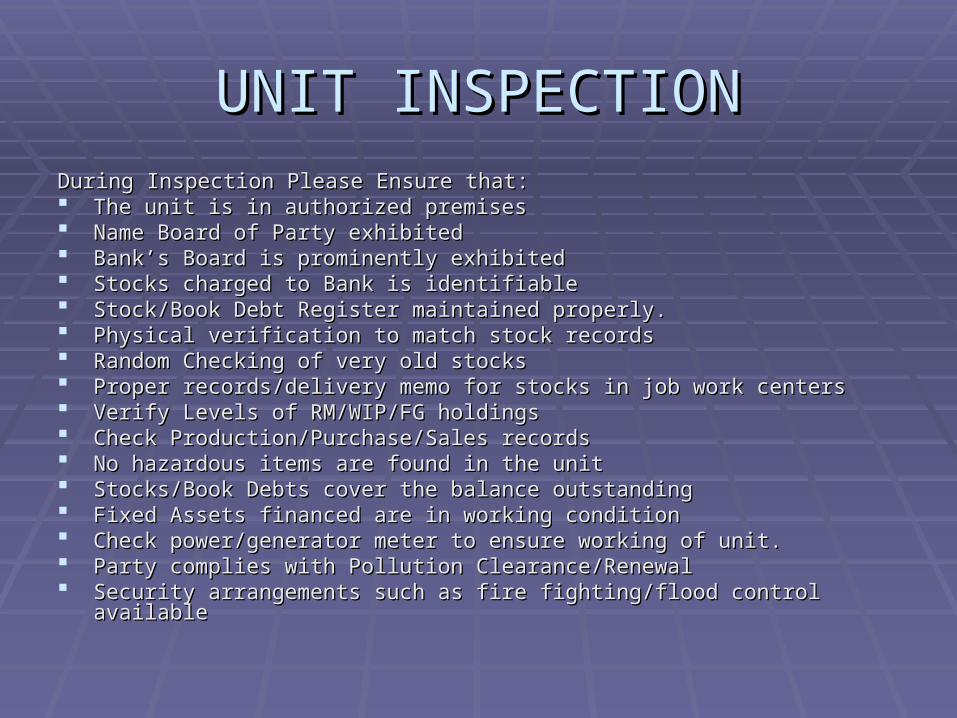

UNIT INSPECTIONUNIT INSPECTIONDuring Inspection Please Ensure that:During Inspection Please Ensure that: The unit is in authorized premisesThe unit is in authorized premises Name Board of Party exhibitedName Board of Party exhibited Bank’s Board is prominently exhibitedBank’s Board is prominently exhibited Stocks charged to Bank is identifiableStocks charged to Bank is identifiable Stock/Book Debt Register maintained properly.Stock/Book Debt Register maintained properly. Physical verification to match stock recordsPhysical verification to match stock records Random Checking of very old stocksRandom Checking of very old stocks Proper records/delivery memo for stocks in job work centersProper records/delivery memo for stocks in job work centers Verify Levels of RM/WIP/FG holdingsVerify Levels of RM/WIP/FG holdings Check Production/Purchase/Sales records Check Production/Purchase/Sales records No hazardous items are found in the unitNo hazardous items are found in the unit Stocks/Book Debts cover the balance outstandingStocks/Book Debts cover the balance outstanding Fixed Assets financed are in working conditionFixed Assets financed are in working condition Check power/generator meter to ensure working of unit.Check power/generator meter to ensure working of unit. Party complies with Pollution Clearance/RenewalParty complies with Pollution Clearance/Renewal Security arrangements such as fire fighting/flood control availableSecurity arrangements such as fire fighting/flood control available

INSPECTION REPORTINSPECTION REPORT

After the Inspection is over compile a report After the Inspection is over compile a report stating date of inspection and observations stating date of inspection and observations made during inspection.made during inspection.

All positive/negative points to be brought out in All positive/negative points to be brought out in the report.the report.

Process of inspection to assess the Process of inspection to assess the merits/weakness of unit and deviation if any, merits/weakness of unit and deviation if any, with justification thereof.with justification thereof.

To address the client of the irregularities seeking To address the client of the irregularities seeking rectification and avoid repetition in future. rectification and avoid repetition in future.

INSURANCEINSURANCE

Assets financed by Bank i.e. stocks, Plant and Assets financed by Bank i.e. stocks, Plant and Machinery, Building to be insured.Machinery, Building to be insured.

Collateral securities wherever required to be insured.Collateral securities wherever required to be insured. Insurance to be done adequately as under insurance will Insurance to be done adequately as under insurance will

result in lower amount of claim being settled.result in lower amount of claim being settled. Bank clause to be incorporated.Bank clause to be incorporated. Insurance Register to be maintained and timely renewal Insurance Register to be maintained and timely renewal

is to be done.is to be done. Party to be advised about the premia being debited to Party to be advised about the premia being debited to

his account and to provide adequate funds.his account and to provide adequate funds.

Review/RenewalReview/Renewal

All credit limits are to be renewed/ reviewed periodically All credit limits are to be renewed/ reviewed periodically normally once a yearnormally once a year

Review is to ensure that the account is in order, Review is to ensure that the account is in order, financials are satisfactory, no change in the owners of financials are satisfactory, no change in the owners of the unit and even if there is any change it does not affect the unit and even if there is any change it does not affect Bank’s interest, no reduction in value of prime/collateral Bank’s interest, no reduction in value of prime/collateral security, conduct of account is satisfactory, no overdue security, conduct of account is satisfactory, no overdue in repayment of installment/interest.in repayment of installment/interest.

Special care to be taken to renew documents.Special care to be taken to renew documents. Acknowledgement of debt to be obtained from the clients Acknowledgement of debt to be obtained from the clients

for all outstanding advances to ensure continuity of for all outstanding advances to ensure continuity of principal documents.principal documents.

MONITORING TOOLSMONITORING TOOLS

FORMSS

Problem areasProblem areas

Diversion of Funds – Payment to non-business related Diversion of Funds – Payment to non-business related purposes, funds being paid to sister concerns/relativespurposes, funds being paid to sister concerns/relatives

Misuse of Funds – Assets not purchased but only Misuse of Funds – Assets not purchased but only invoices are produced.invoices are produced.

Creation of sub-standard fixed assets Creation of sub-standard fixed assets In case of Current Assets – slow / non-moving stocks.In case of Current Assets – slow / non-moving stocks. Parallel operation in another Bank while working capital Parallel operation in another Bank while working capital

is availed from our Bank.is availed from our Bank. Non servicing of interest/installments/continuous EOLNon servicing of interest/installments/continuous EOL Inaccurate stock/book debt details/inflated values.Inaccurate stock/book debt details/inflated values. Frequent cheque returns/inadequate DP/Poor Turnover Frequent cheque returns/inadequate DP/Poor Turnover

ConclusionConclusion

Credit Monitoring is a continuous process.Credit Monitoring is a continuous process. It ensures that quality of assets is It ensures that quality of assets is

maintained and avoid slippage in to NPA.maintained and avoid slippage in to NPA. It is the responsibility of Credit officers of It is the responsibility of Credit officers of

the Bank to undertake systematic credit the Bank to undertake systematic credit monitoring process to protect the interest monitoring process to protect the interest of the Bank.of the Bank.