Embed Size (px)

Citation preview

The opinions expressed in this presentation are those of the speaker. The International Society and International Foundation disclaim responsibility for views expressed and statements made by the program speakers.

Current Trends in Employee Health Plans:

How Does Your Plan Compare?

David Cooke, CEBSPrincipal

MercerChicago, Illinois

9A-1

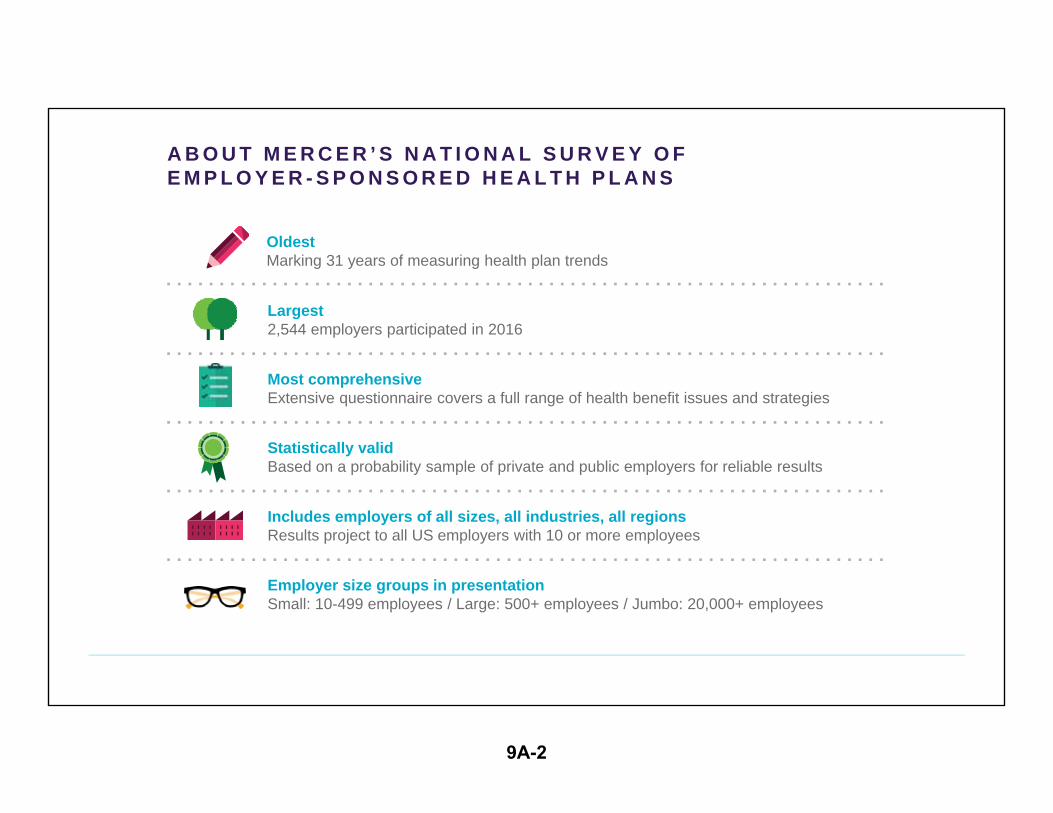

A B O U T M E R C E R ’ S N A T I O N A L S U R V E Y O F E M P L O Y E R - S P O N S O R E D H E A L T H P L A N S

Oldest Marking 31 years of measuring health plan trends

Largest2,544 employers participated in 2016

Statistically valid Based on a probability sample of private and public employers for reliable results

Includes employers of all sizes, all industries, all regions Results project to all US employers with 10 or more employees

Most comprehensiveExtensive questionnaire covers a full range of health benefit issues and strategies

Employer size groups in presentationSmall: 10-499 employees / Large: 500+ employees / Jumbo: 20,000+ employees

9A-2

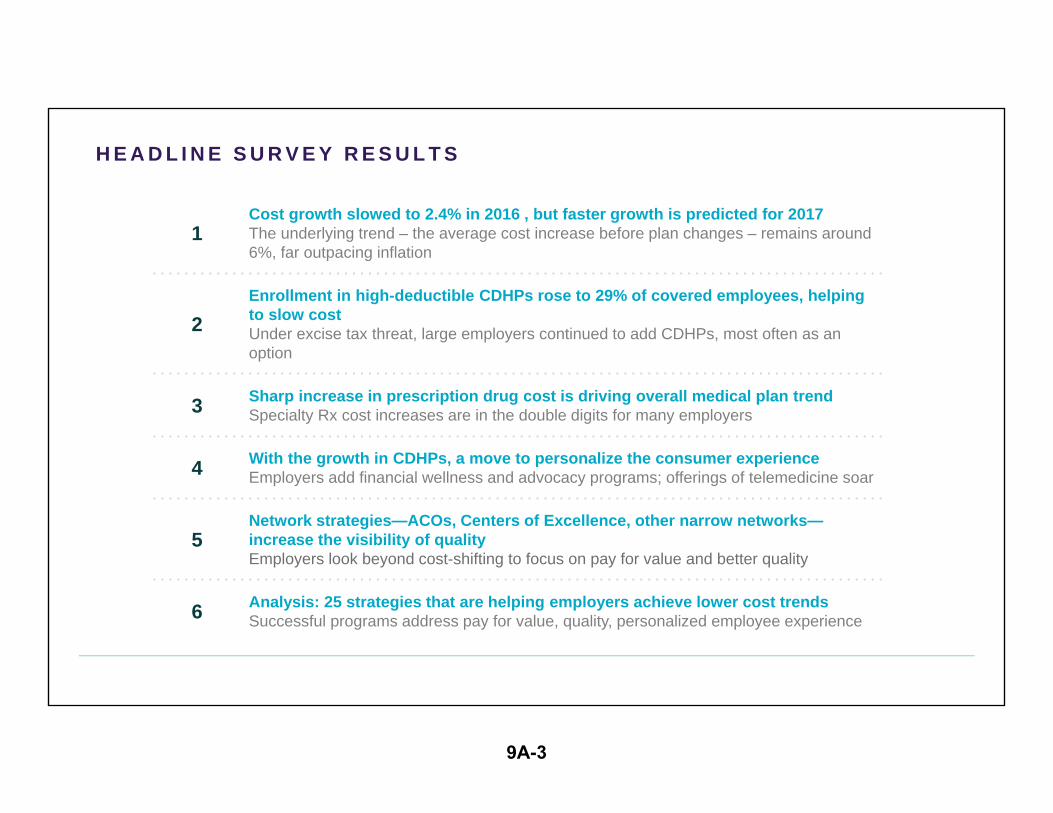

1Cost growth slowed to 2.4% in 2016 , but faster growth is predicted for 2017The underlying trend – the average cost increase before plan changes – remains around 6%, far outpacing inflation

2Enrollment in high-deductible CDHPs rose to 29% of covered employees, helping to slow cost Under excise tax threat, large employers continued to add CDHPs, most often as an option

3 Sharp increase in prescription drug cost is driving overall medical plan trendSpecialty Rx cost increases are in the double digits for many employers

4 With the growth in CDHPs, a move to personalize the consumer experienceEmployers add financial wellness and advocacy programs; offerings of telemedicine soar

5Network strategies—ACOs, Centers of Excellence, other narrow networks—increase the visibility of qualityEmployers look beyond cost-shifting to focus on pay for value and better quality

6 Analysis: 25 strategies that are helping employers achieve lower cost trendsSuccessful programs address pay for value, quality, personalized employee experience

H E A D L I N E S U R V E Y R E S U L T S

9A-3

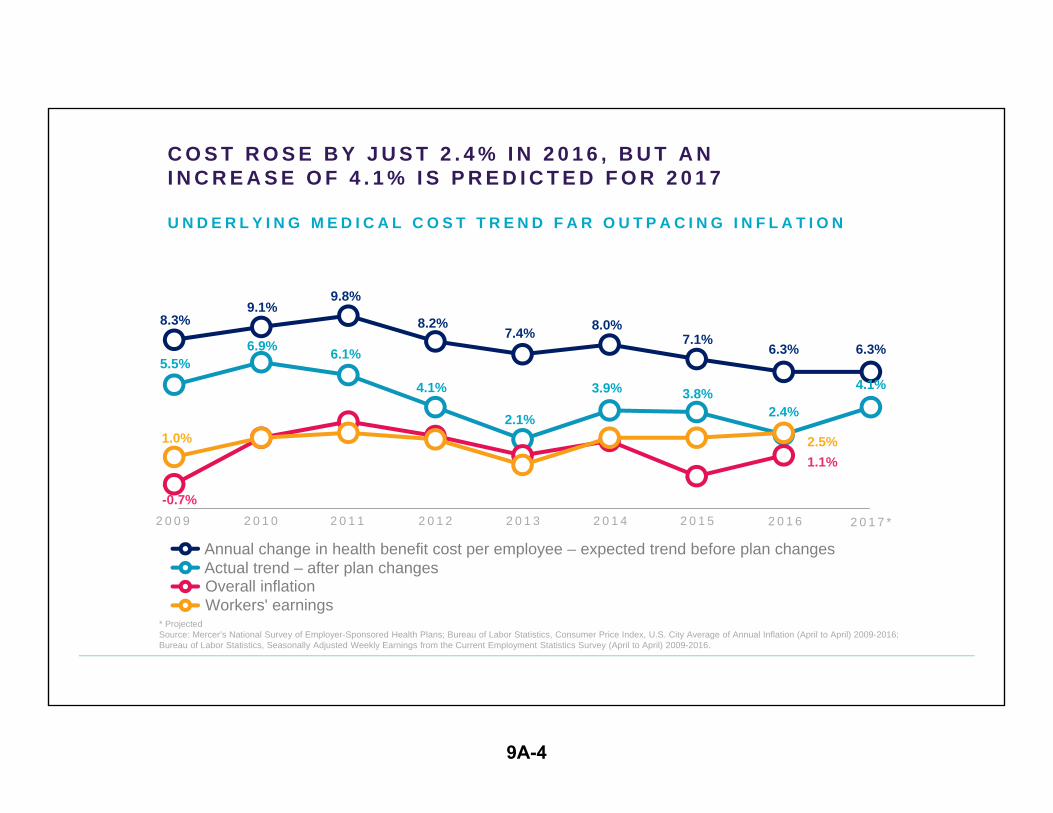

8.3%9.1%

9.8%

8.2%7.4% 8.0%

7.1%6.3% 6.3%

5.5%6.9% 6.1%

4.1%

2.1%

3.9% 3.8%2.4%

4.1%

-0.7%

1.1%

1.0% 2.5%

Annual change in health benefit cost per employee – expected trend before plan changesActual trend – after plan changes Overall inflation Workers' earnings

2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5

C O S T R O S E B Y J U S T 2 . 4 % I N 2 0 1 6 , B U T A NI N C R E A S E O F 4 . 1 % I S P R E D I C T E D F O R 2 0 1 7

U N D E R L Y I N G M E D I C A L C O S T T R E N D F A R O U T P A C I N G I N F L A T I O N

2 0 1 6 2 0 1 7 *

* ProjectedSource: Mercer’s National Survey of Employer-Sponsored Health Plans; Bureau of Labor Statistics, Consumer Price Index, U.S. City Average of Annual Inflation (April to April) 2009-2016; Bureau of Labor Statistics, Seasonally Adjusted Weekly Earnings from the Current Employment Statistics Survey (April to April) 2009-2016.

9A-4

$11,271 $12,173 $12,423 $12,147

$13,074 $11,697

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

10-499 500-999 1,000-4,999 5,000-9,999 10,000-19,999 20,000 ormore

C O S T R I S E S W I T H E M P L O Y E R S I Z E –E X C E P T F O R T H E V E R Y L A R G E S T E M P L O Y E R S

Average total health benefit cost per employee, by employer size

N U M B E R O F E M P L O Y E E S

9A-5

V

$1,113 $1,192

$1,410 $1,452

$1,663 $1,681 $1,738 $1,805

$511 $565 $587 $666 $684 $785 $833 $883

2009 2010 2011 2012 2013 2014 2015 2016

Small employersLarge employers

E M P L O Y E R S H A V E R E L I E D O N C O S T - S H I F T I N G T O C U R T A I L C O S T G R O W T H I N T H E H E A L T H R E F O R M E R A

Average PPO deductible for individual, in-network coverage

9A-6

v

11.5%

9.9% 9.3%

7.6% 7.6%6.3%

5.1% 5.2% 5.5% 5.4%

8.0% 7.4% 7.9%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

A K E Y C O S T D R I V E R I N 2 0 1 6 :A J U M P I N P R E S C R I P T I O N D R U G B E N E F I T C O S T

Cost change in prescription drug benefit offered throughprimary medical plan for large employers

3 2 % O F L A R G E E M P L O Y E R S R E P O R T E D A N I N C R E A S E I N T H E P E R - E M P L O Y E EC O S T O F S P E C I A L T Y D R U G S A T T H E L A S T R E N E W A L – O N A V E R A G E

2 4 % . 4 1 % D I D N ’ T K N O W , A N D 2 4 % S A I D C O S T S T A Y E D A B O U T T H E S A M E .

9A-7

63%

49%

35%

22%

13%

1,000 – 4,999 employees

500 - 999 employees

5,000 – 9,999 employees

D R U G B E N E F I T S H AV E B E E N C A R V E D O U T O F P R I M A RY M E D I C A L P L A N , B Y E M P L O Y E R S I Z E

10,000 – 19,999 employees

20,000 or more employees

9A-8

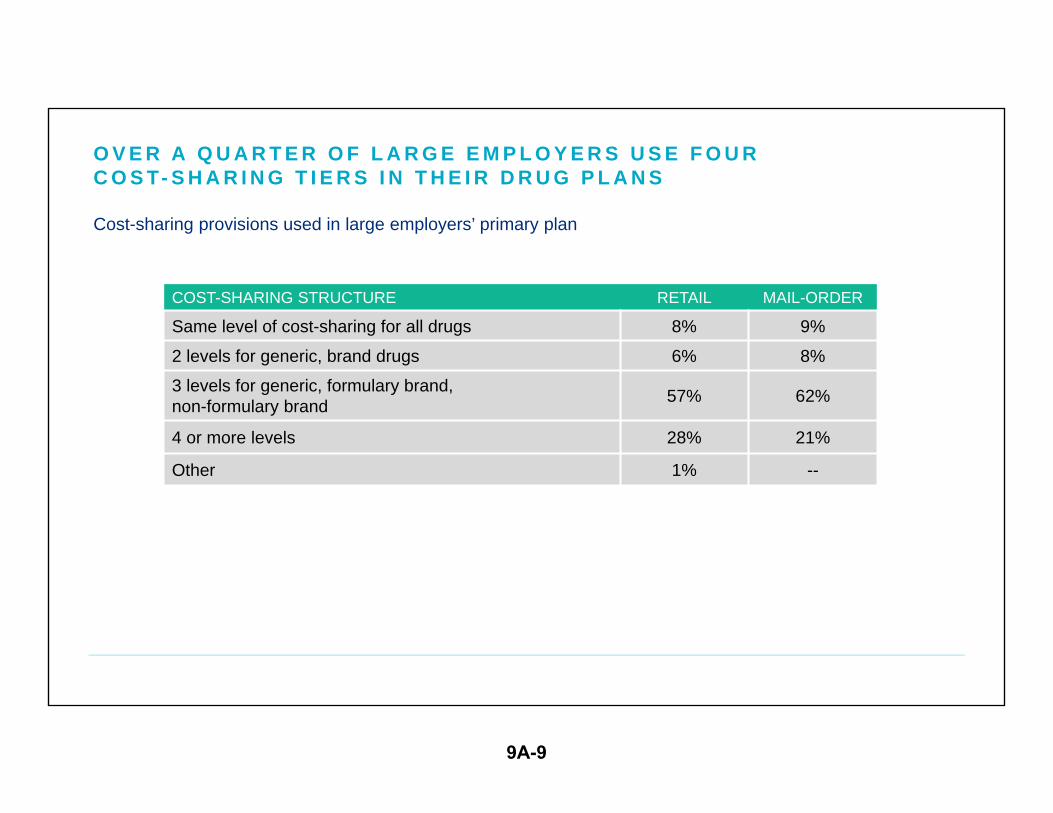

O V E R A Q U A R T E R O F L A R G E E M P L O Y E R S U S E F O U RC O S T- S H A R I N G T I E R S I N T H E I R D R U G P L A N S

Cost-sharing provisions used in large employers’ primary plan

COST-SHARING STRUCTURE RETAIL MAIL-ORDER

Same level of cost-sharing for all drugs 8% 9%

2 levels for generic, brand drugs 6% 8%

3 levels for generic, formulary brand, non-formulary brand 57% 62%

4 or more levels 28% 21%

Other 1% --

9A-9

AV E R A G E C O PAY M E N T A M O U N T S I N P R E S C R I P T I O N D R U G P L A N S

In large employers’ primary medical plan

RETAIL MAIL-ORDER

Generic $11 $22

Brand-name $32 $66

Non-formulary brand $55 $114

Specialty / biotech, when separate $115 $179

9A-10

28%

41%

25%

47%

51%

82%

13%

16%

17%

21%

35%

60%

Employers with 500+employeesEmployers with 20,000+employees

Step therapy

Mandatory generics with or without physician override

P R E S C R I P T I O N D R U G P L A N C O S T- M A N A G E M E N T F E AT U R E S

Mandatory mail order (after 2-4 retail fills)

Retail penalty program

Mandatory drug exclusions

Members may fill 90-day maintenance drugs at a specific retail pharmacy

9A-11

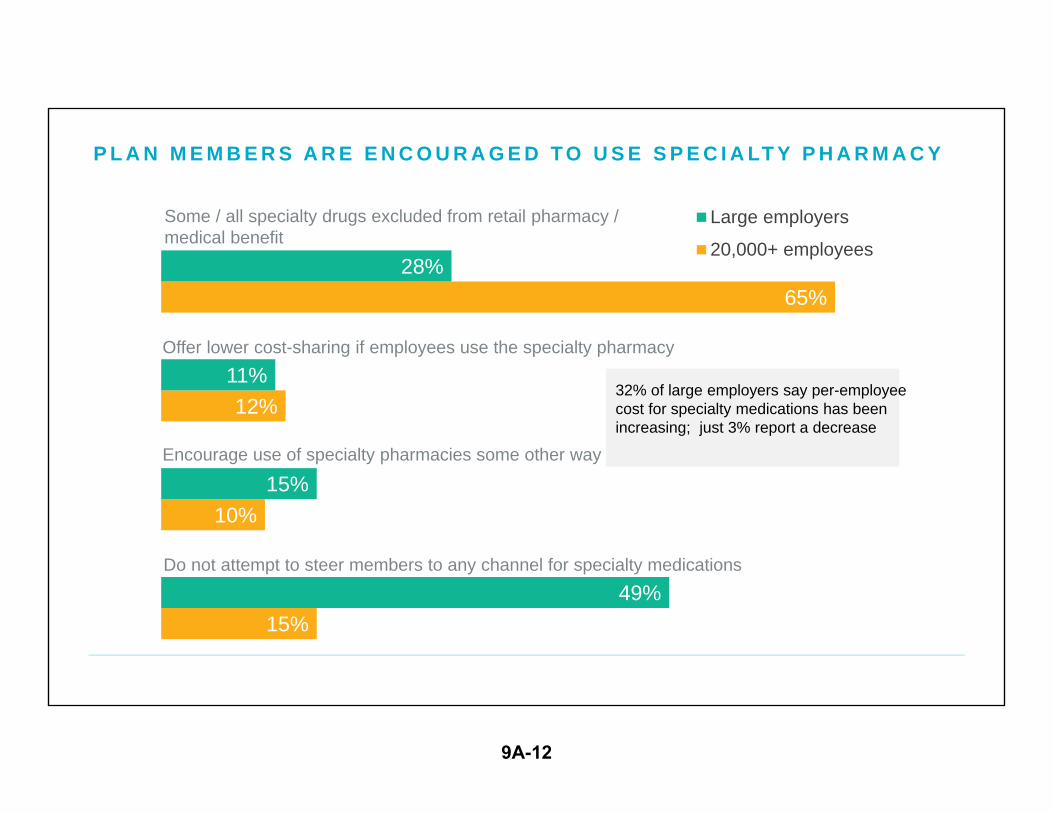

15%

10%

12%

65%

49%

15%

11%

28%

Large employers

20,000+ employees

Offer lower cost-sharing if employees use the specialty pharmacy

Some / all specialty drugs excluded from retail pharmacy / medical benefit

P L A N M E M B E R S A R E E N C O U R A G E D T O U S E S P E C I A LT Y P H A R M A C Y

Encourage use of specialty pharmacies some other way

Do not attempt to steer members to any channel for specialty medications

32% of large employers say per-employee cost for specialty medications has been increasing; just 3% report a decrease

9A-12

v

v

L I M I T I N G D E P E N D E N T C O V E R A G E : S O M E G R O W T H I N S P O U S A L S U R C H A R G E S A N D E X C L U S I O N S

Special provisions for employees’ spouses with other coverage available

8%12%11%

14%

2015

2016

E M P L O Y E R S W I T H 5 0 0 O R M O R E E M P L O Y E E S

Spouses with other coverageare not eligible

Spouses with other coverage mustpay surcharge

5%

26%

8%

27%

2015

2016

Spouses with other coverageare not eligible

Spouses with othercoverage mustpay surcharge

E M P L O Y E R S W I T H 2 0 , 0 0 0 O R M O R E E M P L O Y E E S

Median monthly surcharge: $100

Median monthly surcharge: $100

9A-13

T H E T O P C O S T - M A N A G E M E N T S T R A T E G Y :C O N S U M E R - D I R E C T E D H E A L T H P L A N S

Large employers

20%23%

32%36%

39%

48%

59% 61%

72%

8% 10%13% 15%

18%23%

28%33%

2009 2010 2011 2012 2013 2014 2015 2016 By 2019(projected)

Percent of employers offering CDHPs

Percent of covered employees enrolled inCDHPs

By 2019, 72% of large employers expect to offer a CDHP

9A-14

S L O W D O W N I N N E W C D H P I M P L E M E N T A T I O N S I N 2 0 1 6 –C H A L L E N G E I S T O G R O W E N R O L L M E N T I N E X I S T I N G P L A N SPercent of employers offering / likely to offer CDHP, by employer size

N U M B E R O F E M P L O Y E E S 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6

E X P E C T T O O F F E R

I N 2 0 1 9

Small employers (10-499 employees) 20% 22% 23% 26% 28% 25% 34%

All large employers (500+ employees) 32% 36% 39% 48% 59% 61% 72%

Jumbo employers (20,000+ employees) 48% 59% 63% 72% 73% 80% 87%

9A-15

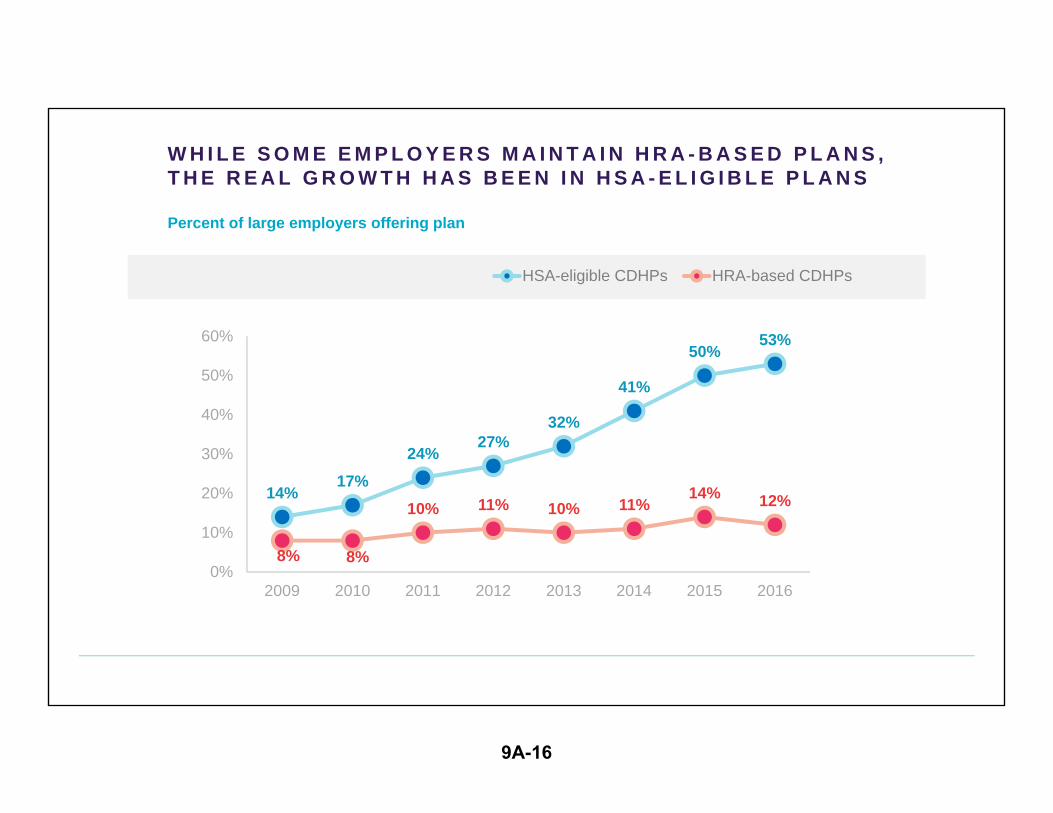

v

14%17%

24%27%

32%

41%

50%53%

8% 8%

10% 11% 10% 11%14% 12%

0%

10%

20%

30%

40%

50%

60%

2009 2010 2011 2012 2013 2014 2015 2016

HSA-eligible CDHPs HRA-based CDHPs

W H I L E S O M E E M P L O Y E R S M A I N T A I N H R A - B A S E D P L A N S , T H E R E A L G R O W T H H A S B E E N I N H S A - E L I G I B L E P L A N S

Percent of large employers offering plan

9A-16

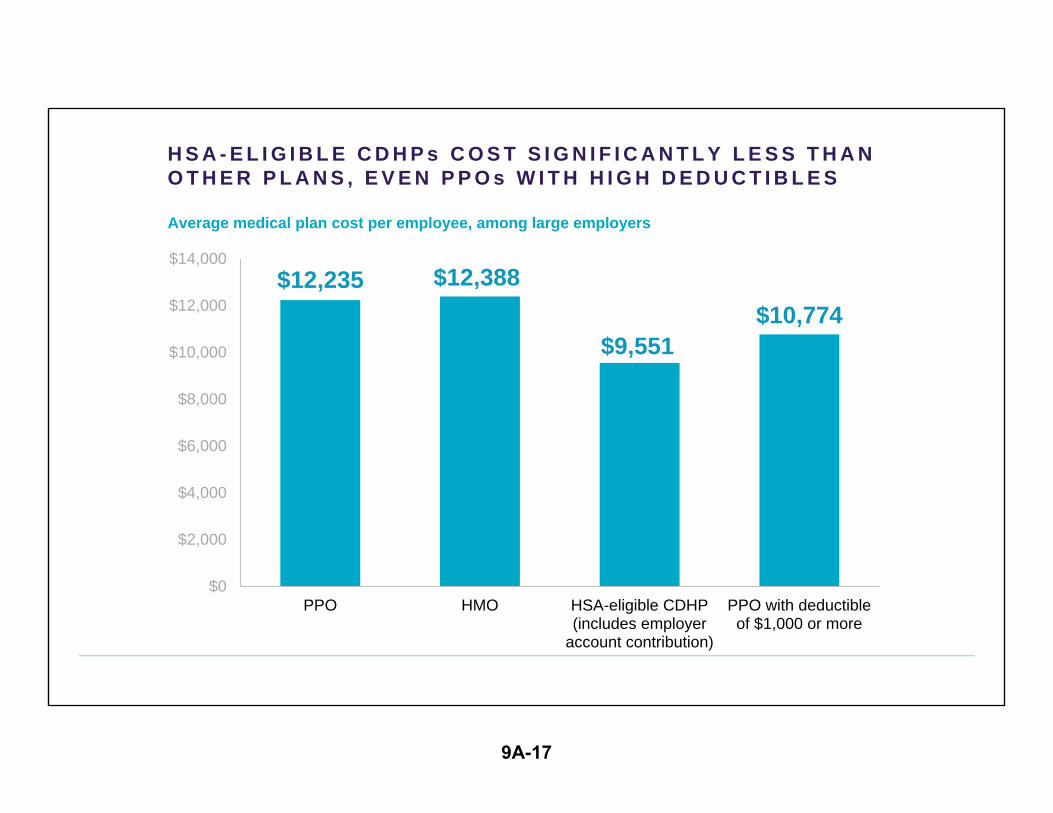

H S A - E L I G I B L E C D H P s C O S T S I G N I F I C A N T L Y L E S S T H A N O T H E R P L A N S , E V E N P P O s W I T H H I G H D E D U C T I B L E S

Average medical plan cost per employee, among large employers

$12,235 $12,388

$9,551$10,774

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

PPO HMO HSA-eligible CDHP(includes employer

account contribution)

PPO with deductibleof $1,000 or more

9A-17

v

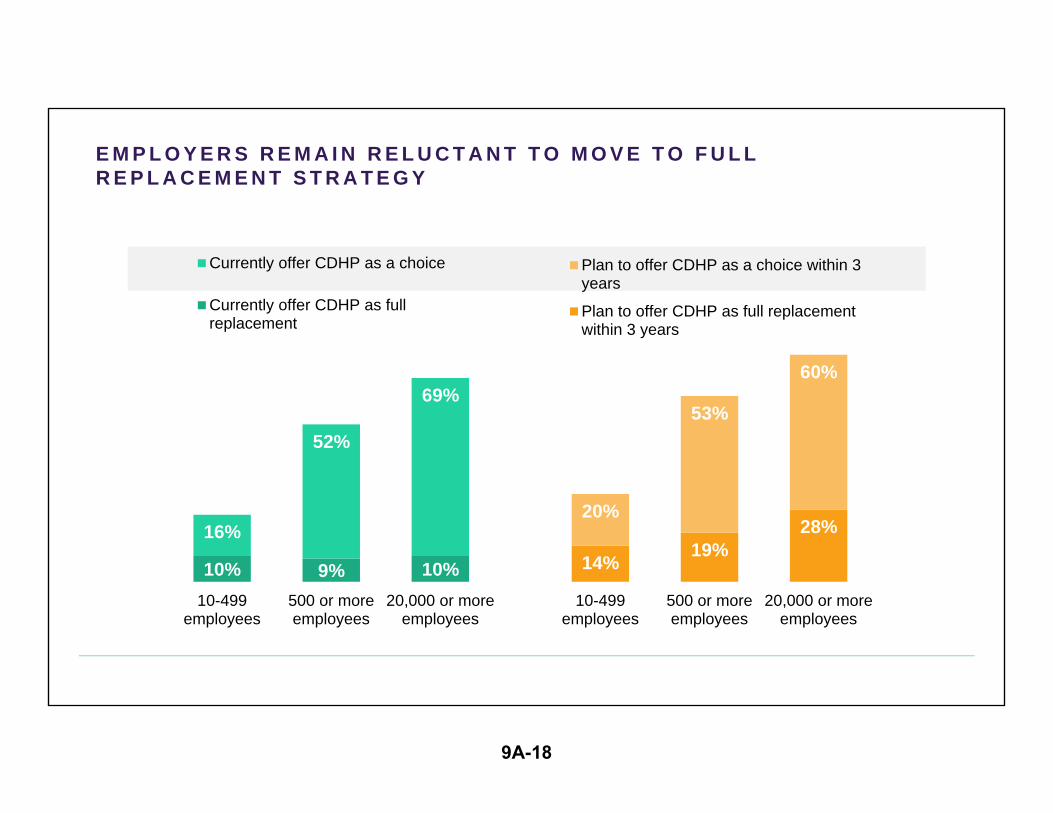

E M P L O Y E R S R E M A I N R E L U C T A N T T O M O V E T O F U L L R E P L A C E M E N T S T R A T E G Y

10% 9% 10%

16%

52%

69%

10-499employees

500 or moreemployees

20,000 or moreemployees

Currently offer CDHP as a choice

Currently offer CDHP as fullreplacement

14% 19%28%

20%

53%

60%

10-499employees

500 or moreemployees

20,000 or moreemployees

Plan to offer CDHP as a choice within 3years

Plan to offer CDHP as full replacementwithin 3 years

9A-18

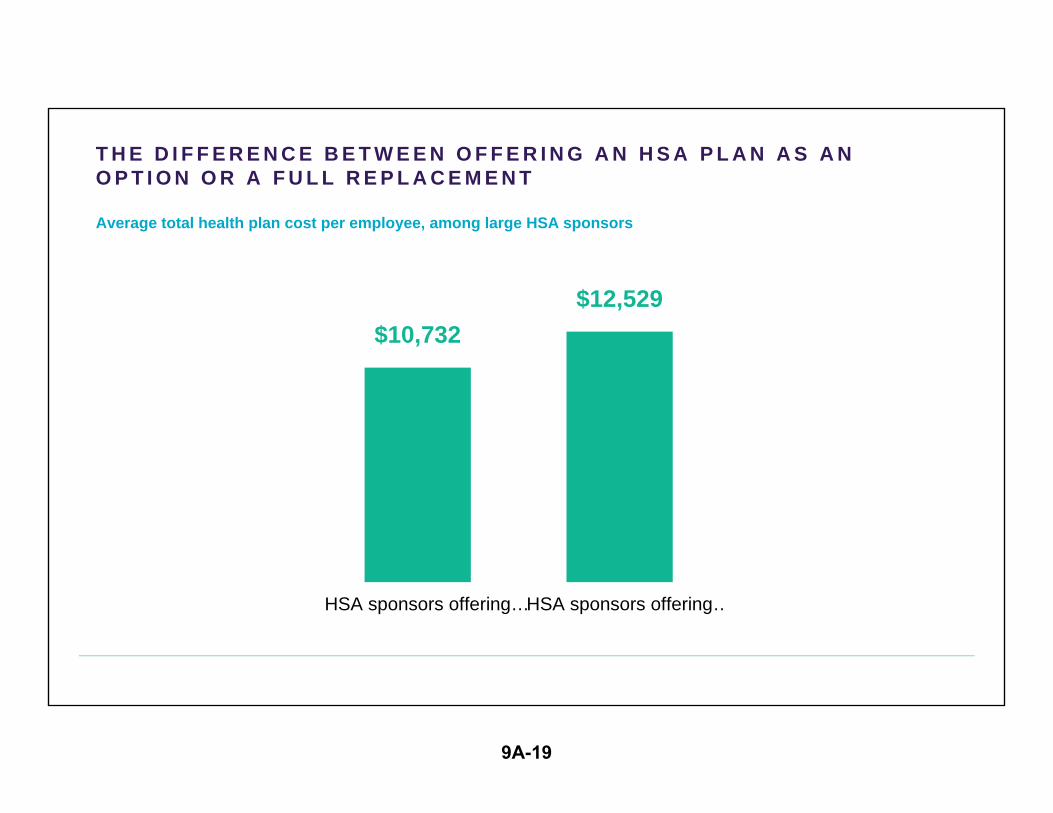

T H E D I F F E R E N C E B E T W E E N O F F E R I N G A N H S A P L A N A S A N O P T I O N O R A F U L L R E P L A C E M E N T

Average total health plan cost per employee, among large HSA sponsors

$10,732 $12,529

HSA sponsors offering…HSA sponsors offering…

9A-19

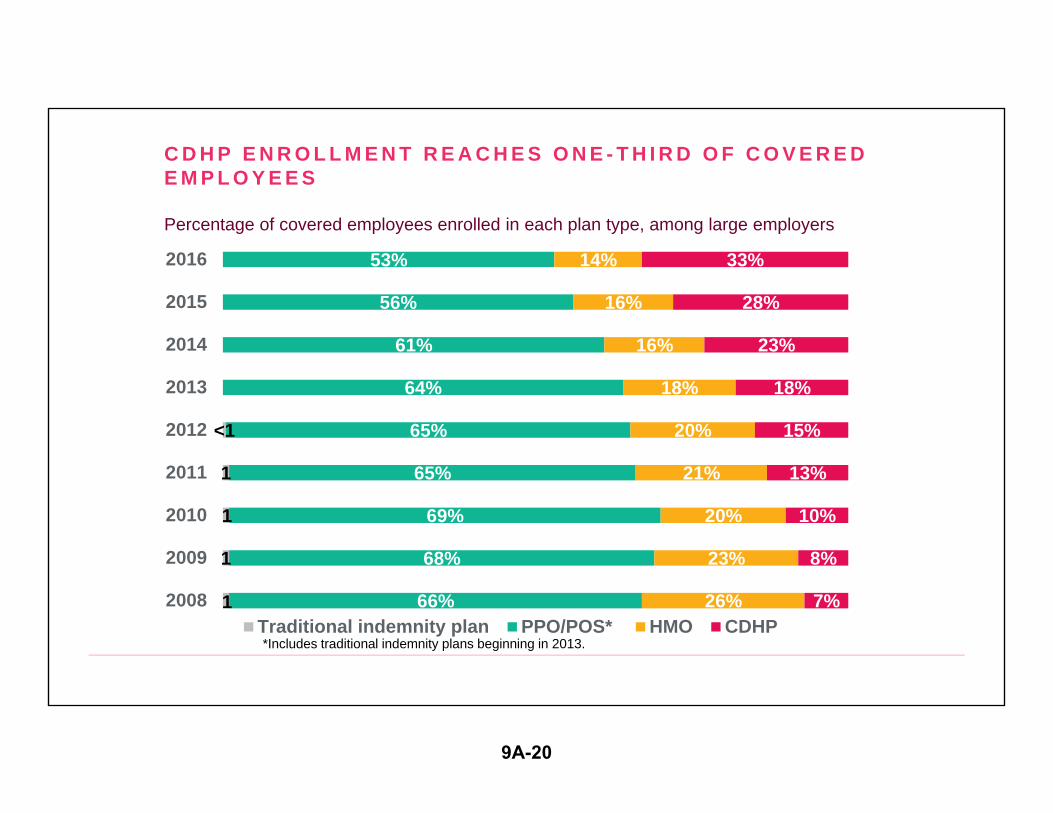

1

1

1

1

<1

66%

68%

69%

65%

65%

64%

61%

56%

53%

26%

23%

20%

21%

20%

18%

16%

16%

14%

7%

8%

10%

13%

15%

18%

23%

28%

33%

2008

2009

2010

2011

2012

2013

2014

2015

2016

Traditional indemnity plan PPO/POS* HMO CDHP*Includes traditional indemnity plans beginning in 2013.

C D H P E N R O L L M E N T R E A C H E S O N E - T H I R D O F C O V E R E D E M P L O Y E E S

Percentage of covered employees enrolled in each plan type, among large employers

9A-20

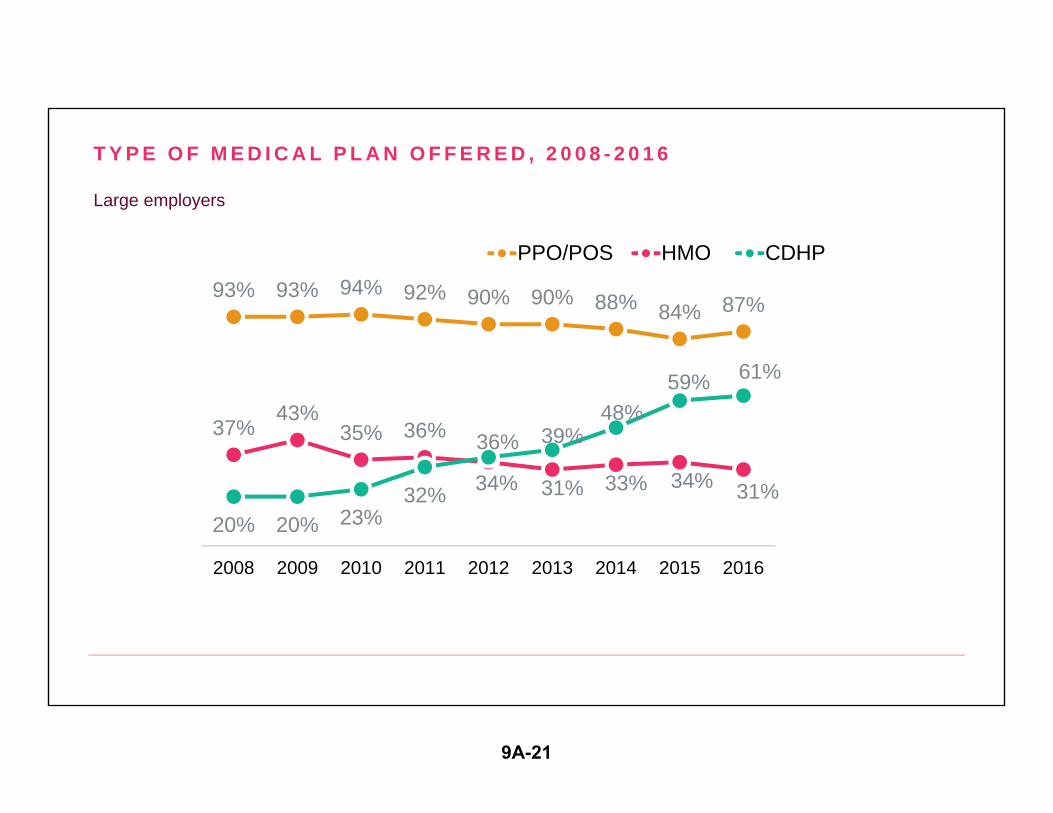

T Y P E O F M E D I C A L P L A N O F F E R E D , 2 0 0 8 - 2 0 1 6

Large employers

93% 93% 94% 92% 90% 90% 88% 84% 87%

37%43%

35% 36%

34% 31% 33% 34% 31%20% 20% 23%

32%

36% 39%48%

59% 61%

2008 2009 2010 2011 2012 2013 2014 2015 2016

PPO/POS HMO CDHP

9A-21

v

60%

v

v

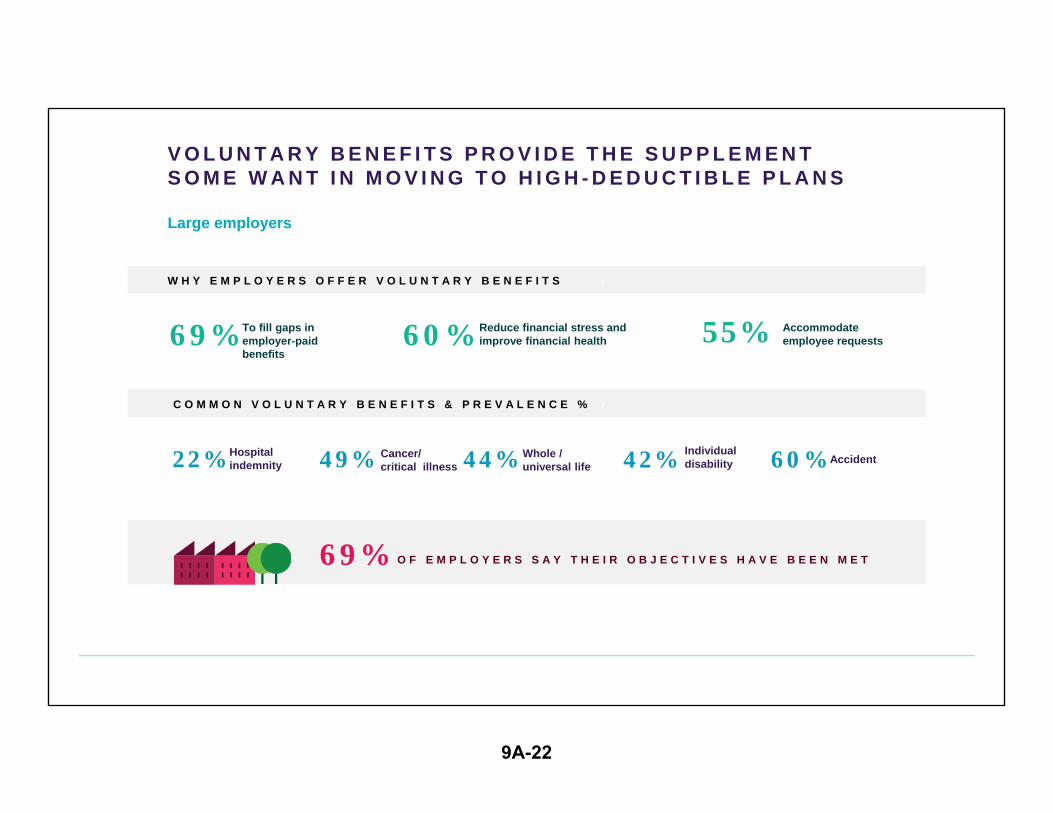

V O L U N T A R Y B E N E F I T S P R O V I D E T H E S U P P L E M E N T S O M E W A N T I N M O V I N G T O H I G H - D E D U C T I B L E P L A N S

Large employers

Cancer/critical illness Accident

Individual disability

Whole /universal life

Hospital indemnity

To fill gaps in employer-paid benefits

Reduce financial stress and improve financial health

Accommodateemployee requests

W H Y E M P L O Y E R S O F F E R V O L U N T A R Y B E N E F I T S

O F E M P L O Y E R S S A Y T H E I R O B J E C T I V E S H A V E B E E N M E T

C O M M O N V O L U N T A R Y B E N E F I T S & P R E V A L E N C E %

69% 60% 55%

22% 49% 44% 42%

69%

9A-22

v

v

H E L P I N G E M P L O Y E E S S A V E O N O F F I C E V I S I T S : T E L E M E D I C I N E I S F A S T - G R O W I N G T R E N D

Percent of employers offering telemedicine

11%18%

30%

59%

18%34%

44%

70%

2013 2014 2015 2016

All large employers Employers with 20,000+ employees

A M O N G L A R G E E M P L O Y E R S O F F E R I N G T E L E M E D I C I N E

13%Require coinsurance

64%Require a copay

$25Is the median copay

9A-23

v

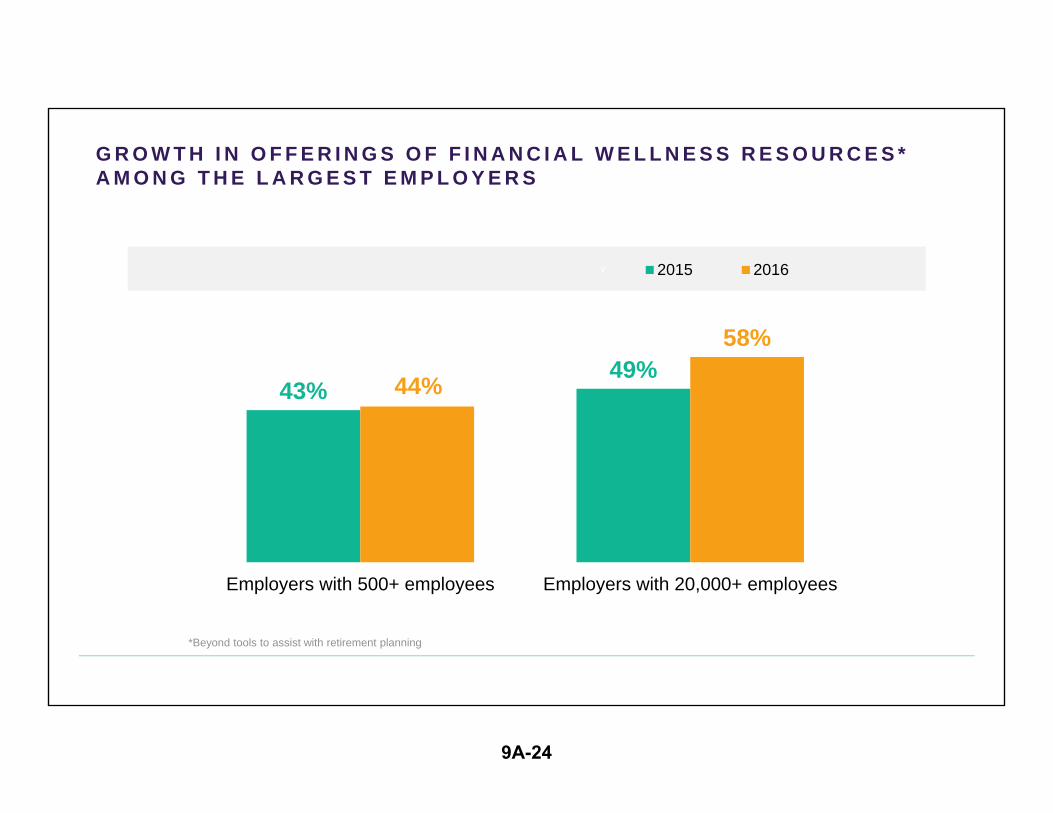

G R O W T H I N O F F E R I N G S O F F I N A N C I A L W E L L N E S S R E S O U R C E S * A M O N G T H E L A R G E S T E M P L O Y E R S

43%49%44%

58%

Employers with 500+ employees Employers with 20,000+ employees

2015 2016

*Beyond tools to assist with retirement planning

9A-24

B U T W H I L E C O S T - S H I F T I N G A N D C O N S U M E R I S M H A V E H E L P E D H O L D D O W N C O S T G R O W T H , I T ’ S N O T E N O U G H

Only about 30% of healthcare cost is “shoppable”

• Healthcare consumers may be able to compare costs for non-urgent care like a physician office visit or MRI, but not in the face of an emergency or critical illness

• A range of options for healthcare services doesn’t exist in all markets

Research shows CDHP enrollees spend more out of pocket and use fewer services

• Concerns remain about whether, or at what point, lower utilization adversely affects health

Once everyone is in a high-deductible health plan, where do cost-savings come from?

9A-25

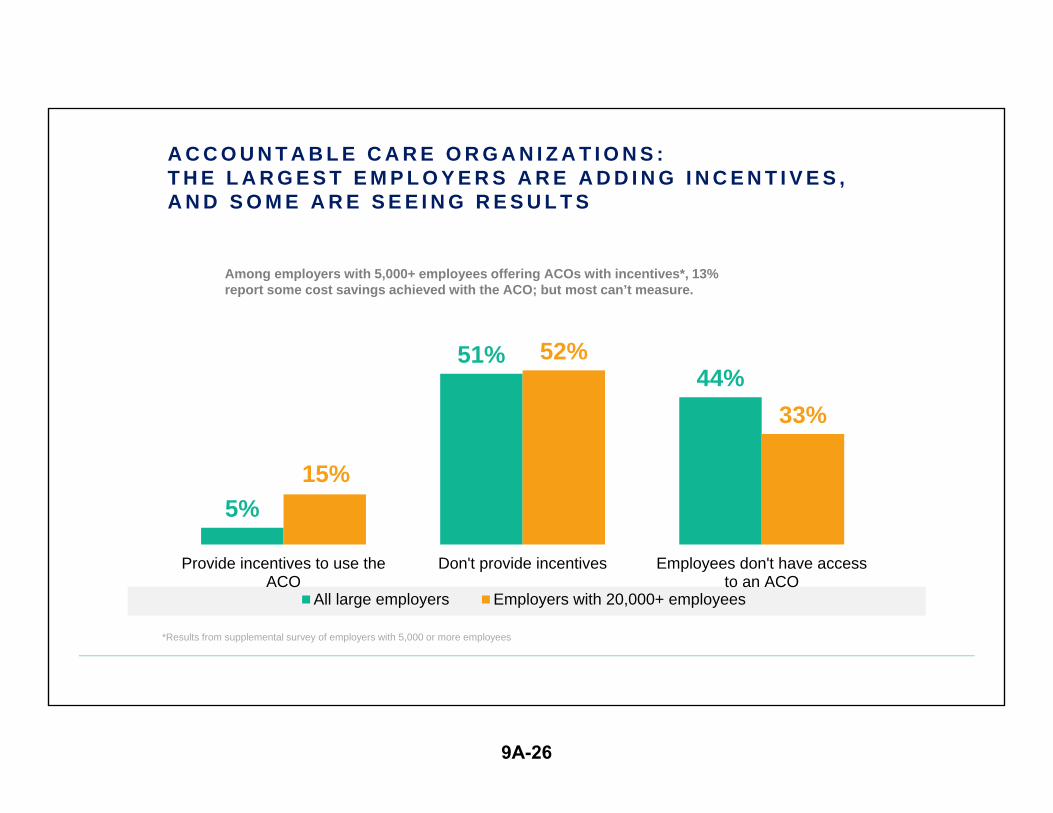

A C C O U N T A B L E C A R E O R G A N I Z A T I O N S :T H E L A R G E S T E M P L O Y E R S A R E A D D I N G I N C E N T I V E S , A N D S O M E A R E S E E I N G R E S U L T S

5%

51%44%

15%

52%

33%

Provide incentives to use theACO

Don't provide incentives Employees don't have accessto an ACO

All large employers Employers with 20,000+ employees

Among employers with 5,000+ employees offering ACOs with incentives*, 13% report some cost savings achieved with the ACO; but most can’t measure.

*Results from supplemental survey of employers with 5,000 or more employees

9A-26

S U R G I C A L C E N T E R S O F E X C E L L E N C E

13%

54%

34%31%

50%

19%

Provide incentives to usesurgical centers of excellence

Don't provide incentives Employees don't have access tosurgical centers of excellence

All large employers Employers with 20,000+ employees

Among employers with 5,000+ employees offering COEs with incentives*, 31% have direct provider contracts or customized carrier arrangement

*Results from supplemental survey of employers with 5,000 or more employees

9A-27

v

P R O V I D E W O R K S I T E O R N E A R - S I T E M E D I C A L C L I N I C F O R P R I M A R Y C A R E S E R V I C E S

24%29% 31% 32%25%

31%36%

40%

0%5%

10%15%20%25%30%35%40%45%

2013 2014 2015 2016

Employers with 5,000 or more employeesEmployers with 20,000 or more employees

* From supplemental survey of employers with 5,000 or more employees

M O R E T H A N H A L F O F R E S P O N D E N T S W I T H A N O N S I T E C L I N I C ( 5 8 % )S A Y T H A T I T I S I N T E G R A T E D W I T H T H E I R P O P U L A T I O N H E A L T H I N I T I A T I V E S *

9A-28

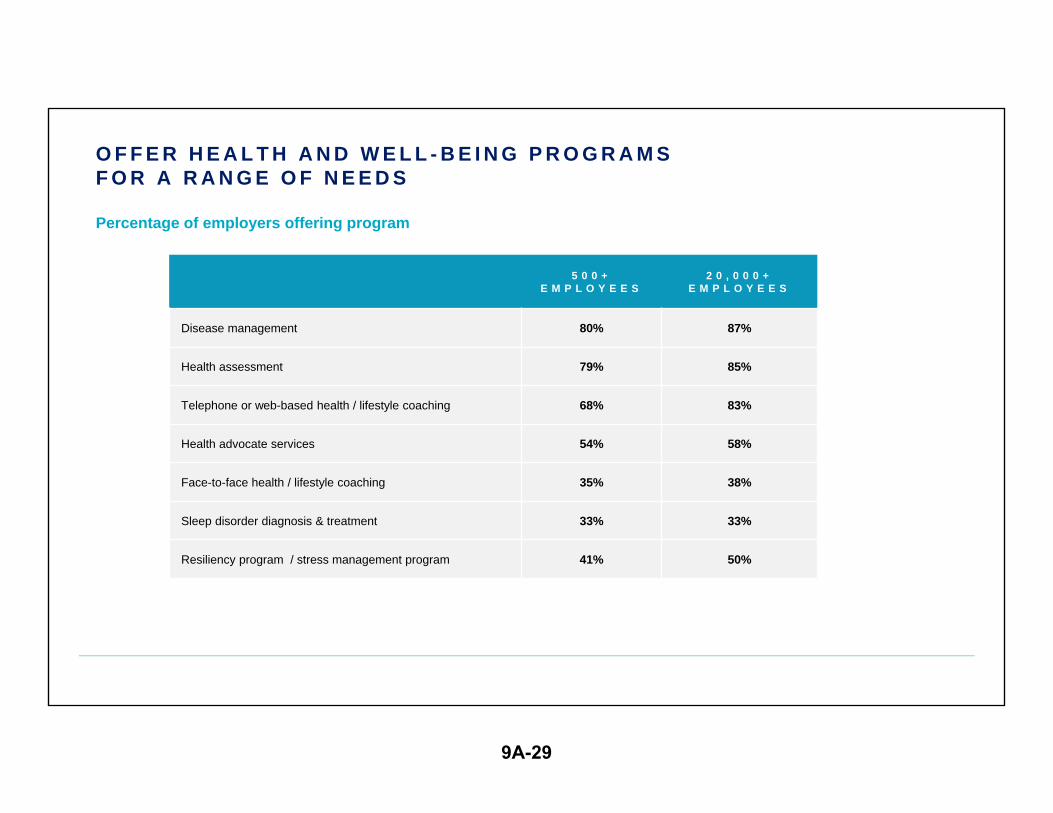

O F F E R H E A L T H A N D W E L L - B E I N G P R O G R A M SF O R A R A N G E O F N E E D S

Percentage of employers offering program

5 0 0 + E M P L O Y E E S

2 0 , 0 0 0 + E M P L O Y E E S

Disease management 80% 87%

Health assessment 79% 85%

Telephone or web-based health / lifestyle coaching 68% 83%

Health advocate services 54% 58%

Face-to-face health / lifestyle coaching 35% 38%

Sleep disorder diagnosis & treatment 33% 33%

Resiliency program / stress management program 41% 50%

9A-29

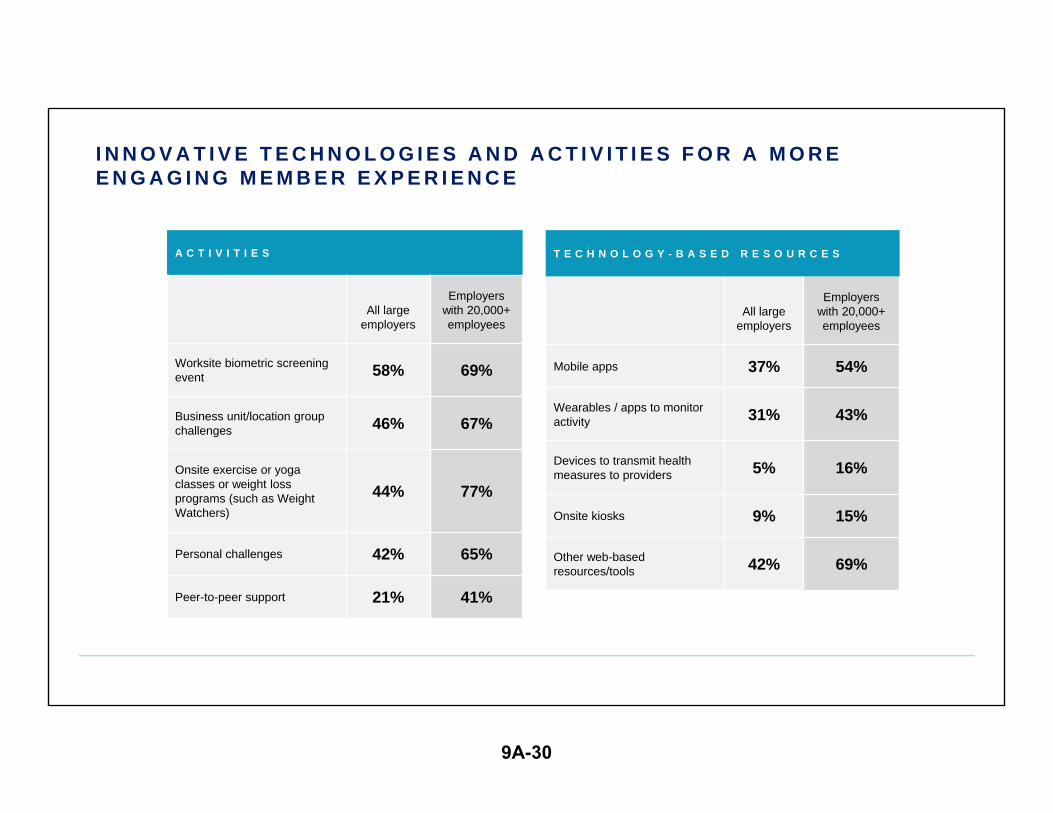

I N N O V A T I V E T E C H N O L O G I E S A N D A C T I V I T I E S F O R A M O R E E N G A G I N G M E M B E R E X P E R I E N C E

A C T I V I T I E S

All large employers

Employers with 20,000+ employees

Worksite biometric screening event 58% 69%

Business unit/location group challenges 46% 67%

Onsite exercise or yoga classes or weight loss programs (such as Weight Watchers)

44% 77%

Personal challenges 42% 65%

Peer-to-peer support 21% 41%

T E C H N O L O G Y - B A S E D R E S O U R C E S

All large employers

Employers with 20,000+ employees

Mobile apps 37% 54%

Wearables / apps to monitor activity 31% 43%

Devices to transmit health measures to providers 5% 16%

Onsite kiosks 9% 15%

Other web-based resources/tools 42% 69%

9A-30

v

4%

17%

24%

64%

Financial penalties, such as higher premiums, loss of plan eligibility

O F F E R I N C E N T I V E S I N C O N N E C T I O N W I T HW E L L - B E I N G P R O G R A M S

Large employers

Financial rewards, such as lower premiums, cash/gift cards

Non-financial rewards, such as lottery, recognition, token gifts

Charitable contributions on behalf of members

E A R N E D F O R

Participation 66%

Outcomes 29%

No incentives provided 25%

M A X I M U MA N N U A L V A L U E

M E D I A N

Participation $300

Outcomes $350

2015 2016

Offer lower premium for non-tobacco use

22% 26%

9A-31

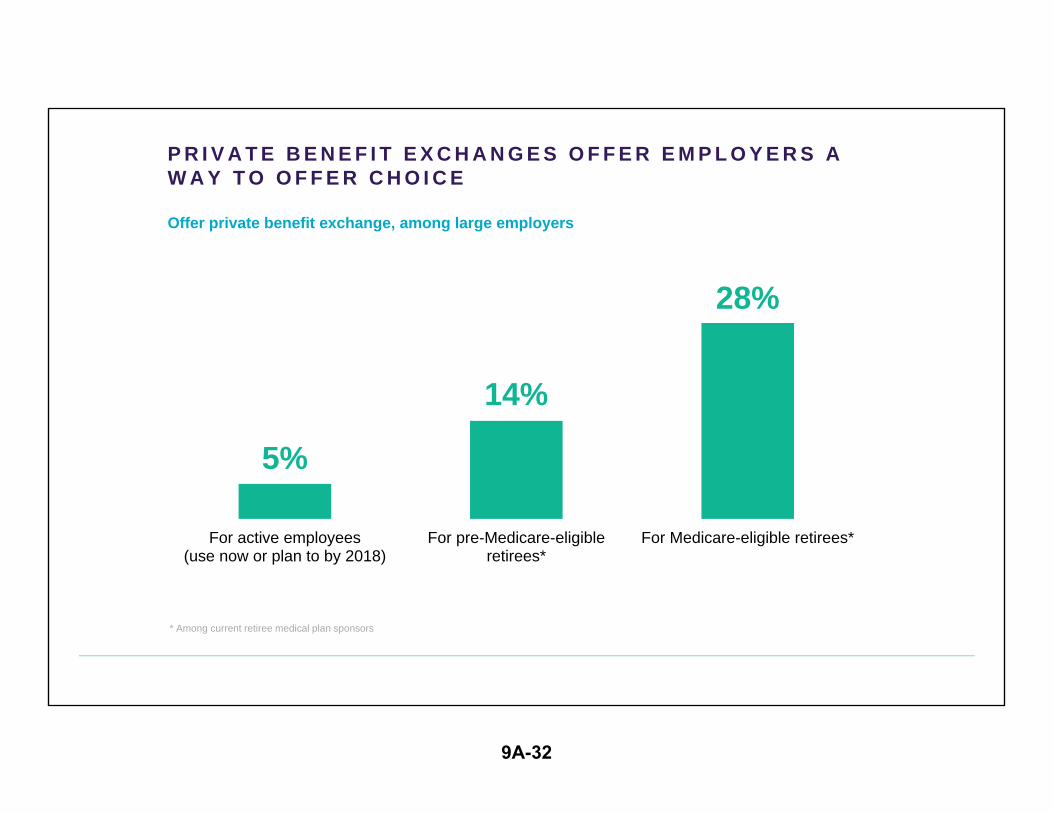

P R I V A T E B E N E F I T E X C H A N G E S O F F E R E M P L O Y E R S A W A Y T O O F F E R C H O I C E

Offer private benefit exchange, among large employers

5%

14%

28%

For active employees(use now or plan to by 2018)

For pre-Medicare-eligibleretirees*

For Medicare-eligible retirees*

* Among current retiree medical plan sponsors

9A-32

39%46% 47%

52% 55%62%

57%

0%

10%

20%

30%

40%

50%

60%

70%

2010 2011 2012 2013 2014 2015 2016

F O L L O W I N G S U P R E M E C O U R T R U L I N G O N M A R R I A G E E Q U A L I T Y, S O M E E M P L O Y E R S A R E D R O P P I N G S A M E - S E X D O M E S T I C PA R T N E R C O V E R A G E

Large employers offering same-sex domestic partner coverage

9A-33

THANK YOU

QUESTIONS?

9A-34