Embed Size (px)

Citation preview

Custom duty is imposed on imports into INDIA and export out of INDIA.The Custom Act was first passed in1962 replacing Sea Customs Act ,1878 while the Custom Tariff Act was passed in 1975. In 1985, the Custom Tariff Act was amended by Custom Tariff(amendment) Act , 1985.

NATURE OF CUSTOM DUTY

The rate at which the duty is to be imposed is specified under “ THE CUSTOM TARIFF ACT 1975”.

Article 266 of the constitution provides that the proceeds from the Customs duty are to be kept by union only & are not to be shared between union and any states.

Collection of custom duty on exports & imports. Enforcement of provisions governing imports &

exports of cargo, baggage etc. Enforcement various prohibitions & restrictions. Prevention of smuggling. International passenger processing . Discharge of various agency function's

OBJECTIVES OF THE ACT

SOME IMPORTANT DEFINITION

SOF CUSTOM

LAW

“Baggage”[sec2(3)]: it includes unaccompanied baggage but does not include motor vehicles.

“Board”[sec2(6)] : it means the central board of Excise and Customs;

DEFINITIONS…….

“Coastal goods”[sec2(7)]: It means goods other than imported goods , transported in a vessel from one port in India to another;

“Custom area”[sec2(11)]: It means the area of a custom station & includes any area in which imported goods or exported goods are ordinary kept before clearance by customs authorities.

W“Dutiable goods”[sec2(14)]: It means any goods which are chargeable to duty &on which duty has not been paid.

W“Export goods”[sec2(19)]: It means the goods which are to be taken out of India to a place outside India.

Continued………

W“IMPORT”[SEC2(23)]: with its grammatical variations and cognate expressions means bringing goods into India from a place outside India.

W“IMPORTED GOODS”[SEC2(25)]: means any goods brought into India from a place outside India.

Continued………

W“Warehouse”[sec2(43)]: means a public warehouse appointed u/s 57 or private warehouse licensed u/s 58.

W“Warehouse Goods”[sec2(44)]: means goods

deposited in a warehouse.

CONTINUED…..

TYPES OF DUTIES

Under sec 12 of Custom Act, duties of customs shall be levied at such rates as may be specified under the CTA, 1975 or any other law for the time being in force.

The implications of section 12 are:-1. Duties of customs shall be levied on goods

imported into, or exported from India.2. The levy shall be at such a rate as

specified in the Customs Tariff Act 1975 or any other law for the time being in force.

3. The saving from the import, or exceptions thereto is only provided under the Custom Act, 1962 or any other law for the time being in force.

4. Government goods shall be treated on par with the non-governmental goods for the purpose of levy of the custom duty.

Standard Rate of Duty.

Effective Rate Of Duty.

Preferential Rate of Duty

The different types of Custom duties are explained below:-1. BASIC CUSTOM DUTY : The authority

for the levy of basic custom duty is under section 2 of C.T.A, 1975. BCD is levied as % of value determined under section 14(1). The rates are given in First schedule to CTA 1975. Different articles have different rates but general rate w.e.f. 1.3.2007 is 10%.

BASIC CUSTOM DUTY IS FURTHER DIVIDED INTO THREE PARTS.

2. Auxiliary Customs Duty : The Finance Act , 1999 has imposed a 10% levy called surcharge on all goods except :- Crude oil & petroleum Gold & silver Certain GATT bound items.The surcharge continued up to March 31,2000. Such a surcharge form part of Union Revenue only

3. Additional Duty Of Customs : This is popularly known as Countervailing Duty. (CVD) The levy of this duty is authorised under section 3(1) of Custom Tariff Act.Any article which is imported into India shall be in addition to the basic duty, liable to a duty equal to excise duty for the time being in force on a like articles if produced or manufactured in India. The basic purpose of this duty is to equalise the price of home manufactured article and imported articles and to rule out the difference of price in lieu of excise duty.

To calculate , the value of the imported articles for the calculation of Additional duty of customs :

1. The aggregate of the following is considered :

Assessable Value Basic Customs Duty Surcharge (if any) Protective Duty is levied under

section 6 of the CTA, 19752. If any article is leviable with

different rates of duty, highest among them will be considered for calculation.

4. Countervailing Duty On Raw materials : In addition to countervailing duty u/s 3(1) ,there is another countervailing duty u/s 3(3) to counter balance excise duty leviable on raw materials components etc., similar to those used in production of such article.

Exceptions:1. Where the packaged commodities are imported

into India, value would be MRP less abatement prescribed for the purpose of calculating additional duty of customs provided retail sale price is printed on the package and are notified under section 4A of the Central Excise Act.

2. If the article cannot be subjected to excise levy because it is no manufactured then on import of like articles , no additional duty can be levied.

3. If any concession or exemption is provided under Excise law , the same should be provided while calculating additional duty of customs.

Finance act 2006 had imposed CVD of 4% on all imports with a few exceptions. However , full credit to be allowed to manufacturers of excisable goods.If such or like article is not produced or manufactured in India the excise duty that would be leviable on the articles had it been produced in India constitutes countervailing duty.

4.Special Additional Duty Of Customs( CVD-ST & VAT) : SAD was abolished w.e.f. 9.1.2004 and reintroduced w.e.f.1.3.2006. As countervailing duty of customs u/s 3(1) is imposed to counter balance excise duty charge, this special additional duty is imposed to counter balance sales tax charge on articles so as to provide a legal playing field to indigenous goods.The value for the purpose of calculation of special additional duty of custom used to be aggregate of :(Assessable value + Basic Duty + surcharge + countervailing duty)No drawback of special additional duty of customs is admissible . However nil duty goods, Baggage free allowance, Goods chargeable to additional duty in lieu of sales tax, gold, silver and some other specified goods are exempt from this duty.

5. Protective Duties : Imports can endanger the indigenous industry in two ways : The imported goods could be cheaper. They can be more attractive if a flood of such

things is brought into market . To protect the indigenous industry from the

above dangers, protective duties are imposed . The protection through such duty is intended to ensure that the imported goods are not completely cheaper than the indigenous goods .

The Central Government shall impose such duty on the recommendation of Tariff Commission established under Tariff Commission Act, 1951. If Central Government on such recommendation is satisfied that circumstances exist to take immediate action to provide for the protection of interests of any indigenous industry the Central Government may by notification in the official gazette impose protective duty at a rate which is recommended by Tariff Commission

Under section 7 of Customs Tariff Act following powers are

provided to Central Government.1. Power to specify period upto which

the protective duty shall be in force.2. Power to reduce or extend such

periods.3. Power to reduce or increase the

effective rate of protective duty if the govt. is satisfied that the existing protective duty has become ineffective or excessive.

7. Countervailing duty on subsidized articles [SECTION 9] : if any country pays directly or indirectly any subsidy to its residents for the production and exportation of such produced articles into India then upon the improvement of such articles into india the central govt. may by notification in official gazette impose a countervailing duty not exceeding the amount of such subsidy .If the amount of subsidy cannot be ascertained , the duty can be collected provisionally pending determination of such amount of duty . The difference , if any, can be collected further or refunded as the case may be .

8.ANTI DUMPING DUTY [ SEC 9A] : It provides that where an article is exported from any country or territory at less its normal value then on its importation in india , the central govt. may by notification in the official gazette impose an anti-dumping duty not exceeding margin of dumping . Whenever such a situation arises Central Govt. imposes a duty known as Anti Dumping duty.

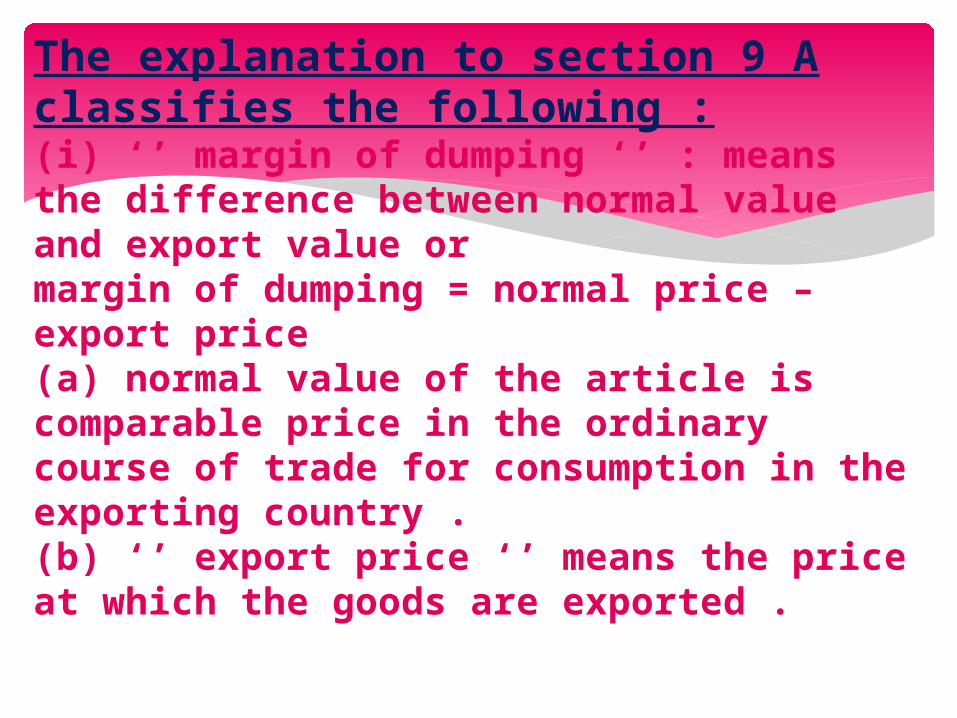

The explanation to section 9 A classifies the following :(i) ‘’ margin of dumping ‘’ : means the difference between normal value and export value or margin of dumping = normal price – export price (a) normal value of the article is comparable price in the ordinary course of trade for consumption in the exporting country .(b) ‘’ export price ‘’ means the price at which the goods are exported .

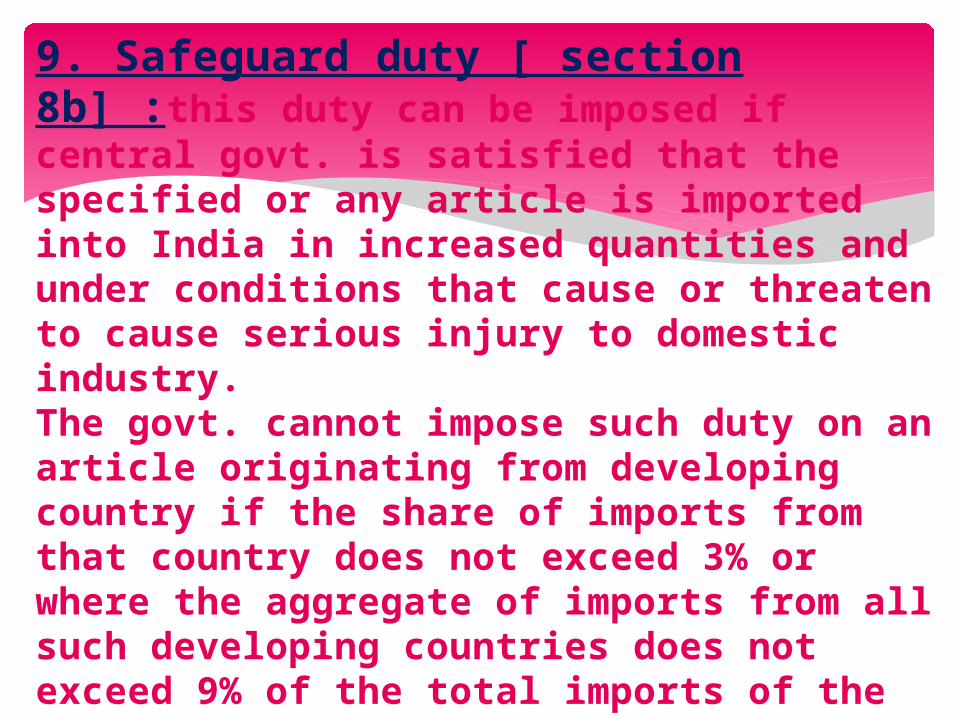

9. Safeguard duty [ section 8b] :this duty can be imposed if central govt. is satisfied that the specified or any article is imported into India in increased quantities and under conditions that cause or threaten to cause serious injury to domestic industry. The govt. cannot impose such duty on an article originating from developing country if the share of imports from that country does not exceed 3% or where the aggregate of imports from all such developing countries does not exceed 9% of the total imports of the article into India.

1. Legal provision

Power to levy above duty u/s 6(1) of CTA, 1975

Power to levy above duty is u/s 8B of CTA 1975

Power to levy is u/s 9A of CTA

2.Conditions

Conditions are left to be determined by Tariff Commission . Normally imported cheaper goods which hinder growth of domestic industry .

If any article is imported into india in increased quantities and causes will threaten to cause serious injury to domestic industry .

If any article is imported into india and its export price is less than its normal value.

3.Power to levy

Power to levy this duty rests with Central Govt. but a recommendation from Tariff Commission is necessary.

Power to levy duty rests with Central Govt. No recommendation from Tariff Commission is must

Power to levy duty rests with Central Govt. . No recommendation from Tariff Commission is must

Basis of difference

Protective duty Safeguard duty Anti Dumping duty

Dissimilarities Among

4. Period The power to decide and specify upto which date such duty shall be in force is with Central Govt.

Unless revoked earlier by Central Govt. , such duty shall cease to have effect on the expiry of 4 years from the date of its imposition.

Unless revoked earlier by Central Govt. , such duty shall cease to have effect on the expiry of 5 years from the date of its imposition.

5. Conditions of Developing Country

No such conditions . Only recommendations of Tariff Commission is necessary.

The Govt. can’t impose such duty if imports from a developing country of that article do not exceed 3% or where the aggregate of imports from such developing countries does not exceed 9% of total imports of that article in india

No such condition but the condition of export price being less than normal value exists

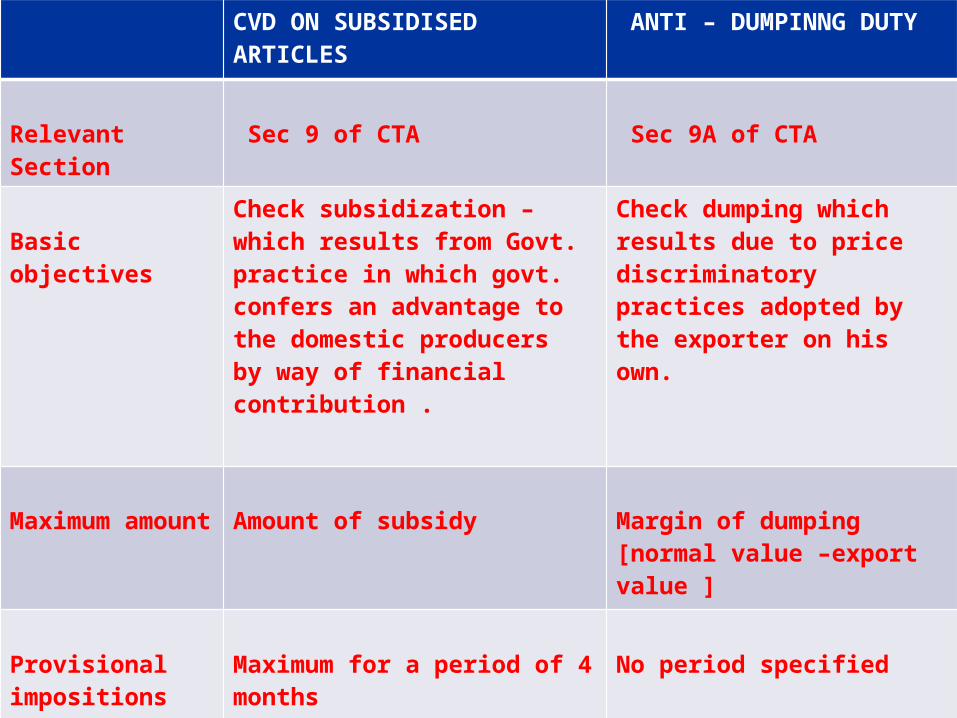

CVD ON SUBSIDISED ARTICLES

ANTI – DUMPINNG DUTY

Relevant Section

Sec 9 of CTA Sec 9A of CTA

Basic objectives

Check subsidization – which results from Govt. practice in which govt. confers an advantage to the domestic producers by way of financial contribution .

Check dumping which results due to price discriminatory practices adopted by the exporter on his own.

Maximum amount

Amount of subsidy Margin of dumping [normal value –export value ]

Provisional impositions

Maximum for a period of 4 months

No period specified