Embed Size (px)

Citation preview

Debt Issuance Primer

1

Outline

Introduction to Debt Financing

Security and Credit Considerations

Forms of Indebtedness

Underwriting and Marketing Securities

2

Introduction to Debt Financing

3

A Municipal Bond Issue

Issuer's Project Issuer

Investors

Bank Trusts

Investment Advisors

Individuals

Bond Trustee

&

Paying Agent

Bond Proceeds

Monthly Principal and Interest

Payments

BondsBond

ProceedsSemiannual Interest

and Annual Principal

Monies

from

Pledged

Source

4

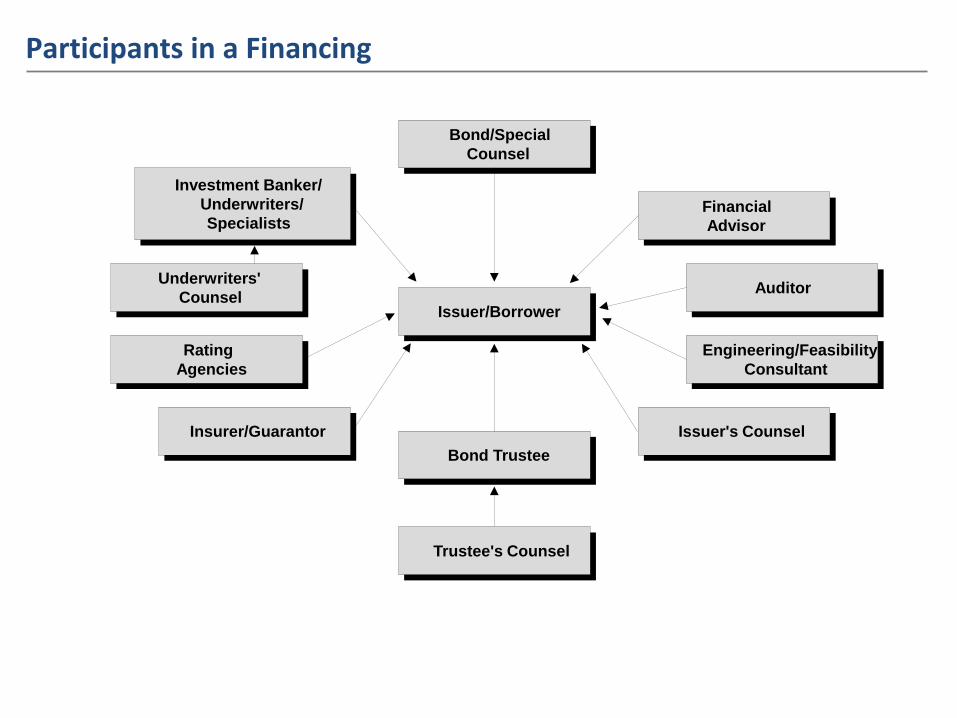

Participants in a Financing

Bond/Special

Counsel

Bond Trustee

Investment Banker/

Underwriters/

Specialists

Underwriters'

Counsel

Rating

Agencies

Insurer/Guarantor

Trustee's Counsel

Issuer/Borrower

Financial

Advisor

Auditor

Engineering/Feasibility

Consultant

Issuer's Counsel

5

Issuers/Borrowers - City or Airport Authority serving as issuer of the debt. Responsible for the repayment of the debt and the accuracy of the Offering Statement Bond Counsel - Law firm working on behalf of the issuer and bondholders. Primary responsibility is preparation of legal documents and rendering of an opinion concerning the validity of the bonds with respect to statutory authority and tax status

Financial Advisor - Acts on behalf of Issuer advising on wide range of financial management issues. Reviews pricing and advises issuer on fairness of rates and fees.

Underwriter - Investment bank responsible for the pricing/marketing of the bonds and often involved with the plan of financing, credit rating process, and shaping of the legal documents

Underwriter’s Counsel - Law firm responsible for drafting the Offering Statement. Prepares underwriting documents (Agreement Among Underwriters, Bond Purchase Contract, etc.)

Feasibility Consultant - Performs economic and financial study covering new project construction and viability of undertaking. Feasibility typically includes an aviation forecast

Primary Participants in a Financing

6

Secondary Participants in a Financing

Issuer’s Counsel - Reviews all legal documents on behalf of issuer and assists in drafting documents

Auditor - Provides most recent annual Audited Financial Statements for the Official Statement for the assessment of the issuer’s financial condition and historical performance

Bond Insurer/Guarantor - Financial services company or bank that may provide credit enhancement through a municipal bond Insurance policy or letter of credit

Rating Agencies - National organizations (S&P, Moody’s, Fitch) that provide ratings on debt and an assessment of a borrower’s ability to repay. Issues credit reports detailing credit strengths and weaknesses.

Bond Trustee - Retained by Issuer, but represents Bondholders’ interests. Manages bond funds, reserves and construction funds. Receives interest and principal payments from Issuer/Borrower and distributes to Bondholders.

7

Legal Authority for the Issuance of Debt

Legislation or

Incorporation

Issuer

General CounselBond Counsel

Bond Documents

Bondholders

Create legal, valid and binding

pledge and security for

8

Municipalities and Other Political Subdivisions A state political subdivision (a municipality) possesses only those powers which are expressly delegated to it by its state government and those powers which are necessarily implied in order for the political subdivision to carry out its expressly delegated powers.

The power to issue debt (i.e., to borrow money) is a fundamental power which must be expressly delegated — it can not be implied.

Issuing debt (i.e., borrowing money) can occur in different forms, including without limitation: the public sale of bonds or notes to investors the execution of a loan agreement, typically with a bank the execution of a lease with an entity such as an airline or a group such as the rental car operators

Interest on municipal obligations is exempt from federal income taxation and often from state taxation.

Legal Authority for the Issuance of Debt

9

Various federal (primarily the Securities Acts of 1933 and 1934) and state (also known as “blue sky”) laws exist to protect the investing public.

Basic objectives of securities laws: require disclosure of material information about securities to allow investors to make informed investment decisions; and prohibit misrepresentation or other fraudulent

conduct.

The issuer has a “continuing obligation” to provide material information to the public under Rule 15c2-12.

Bottom line: the Official Statement must not contain any untrue statement of a material fact or omit to state any material facts.

The Disclosure Document (Official Statement)

10

Security and Credit Considerations

11

The Security Question

High

Flexibility

Weak

Covenants

Strict

Covenants

Low

Flexibility

12

The Security

Pledge all project net revenues Net revenues (with rate covenant > 125%

of debt service) after payment of O&M expenses

Airport Revenues Landing Fees Terminal Rents Parking Rental Car Revenues Concessions

Other funds often pledged to repay the debt

Debt Service Fund Debt Service Reserve Fund

Security Sources and Funds

13

The Flow of Funds

Revenue Fund

O&M Expense Fund

Debt Service Fund

Debt Service Reserve Fund

Coverage Fund

Maintenance Reserve Fund

Surplus Fund

14

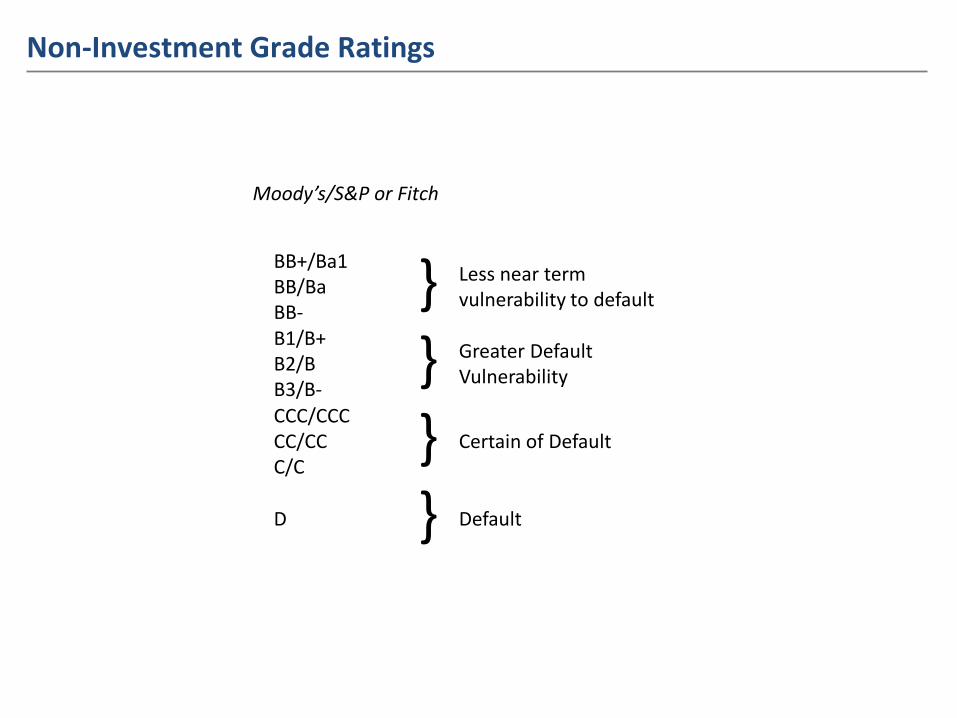

What is a Credit Rating?

A rating is an opinion by a rating agency as to the willingness and ability of an issuer to repay principal and interest in full on a timely basis.

15

Moody’s/S&P or Fitch

Investment Grade Ratings

Aaa/AAA } Highest Quality

Aa1/AA+ Aa2/AA Aa3/AA-

} Very Strong Capacity

A1/A+ A2/A A3/A-

} Strong Capacity

Baa1/BBB+ Baa2/BBB Baa3/BBB-

} Adequate

16

Moody’s/S&P or Fitch

Non-Investment Grade Ratings

BB+/Ba1 BB/Ba BB-

} Less near term vulnerability to default

B1/B+ B2/B B3/B-

} Greater Default Vulnerability

CCC/CCC CC/CC C/C

} Certain of Default

D } Default

17

Key Covenants

Security: 1st Lien on Gross or Net Revenues of System

Rate Covenant: Net Revenues > 1.25x Annual Debt Service

Flow of Funds: Open or Closed

Additional Bonds Test: Historic: Net Revenues in the Prior Year > 1.25x Maximum Annual Debt Service Proposed & Outstanding Debt

Projected: Net Revenues for 5 Years After Issuance > 1.25x Maximum Annual Debt Service Proposed & Outstanding Debt

18

Population growth, income levels, unemployment and the labor mix

Size of the capital plan and other outstanding debt/obligations The terms of the Airline Use Agreement and the rate-making provisions

Rate Setting Mechanism

The Strength of the Service Area

Other Rating Factors

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

19

Forms of Indebtedness

20

Short-term products Uses: Cash flow, deficit, bridge financings Commercial Paper: 1-270 days Variable rate notes: 6-13 month final maturity Fixed or variable rate bank loans

Medium term notes: 1-10 years with rolling maturities

Long-term issues Uses: long-term project financing Fixed rate bonds: 1-40 year final maturity

Forms of Indebtedness/Financial Products

0.0325

0.035

0.0375

0.04

0.0425

0.045

0.0475

1 6 11 16 21 26

Yie

ld

Year

Interest Rates

21

Short-term debt may require bank credit enhancement/liquidity (“put”) facility

Are the amounts and the dates when money is needed known?

Can the debt easily be converted to another mode such as a fixed rate term?

What is the best adjustable rate period: daily, weekly, monthly, quarterly, semi-annually, multi-annually, commercial paper (1-270 days)

Does the short-term debt need to be remarketed?

If a bank loan, are the bank covenants acceptable to both the issuer and to outstanding bondholders?

Considerations for Short-Term Products

22

Considerations for Long-Term Debt Products

What is the appropriate call feature - 10-years at par?

What is the best mix of serial bonds and term bonds?

Can we match the debt term with the asset life?

Should the debt service be level or are there reasons for a non-level debt structure?

Does bond insurance provide an economic advantage?

How can we attract retail buyers in addition to the larger, institutional investors?

What are the best days to price and close the bonds?

Par Amount of Bonds 85,045,000$

Reoffering Premium 7,249,315

Transfers from Prior Issue DSF 3,596,620

Issuer Equity Contribution 768,589

Total Sources 96,659,524$

Cost of Issuance* 1,281,469$

Refunding Escrow 95,378,055

Total Uses 96,659,524$

* Includes Insurance Premium and Surety Bond Fee

Series 2010B&C Sources and Uses

23

Underwriting and Marketing Securities

24

Underwriters Develop marketing strategy Coordinate input from co-managers and sales Help finalize bond sales/structure Establish price/yield levels on the bonds

Sales Professionals: Institutional and Retail Help coordinate marketing strategy Obtain input from investors Solicit orders for the bonds

Internal Credit/Research Staff Write credit report and assist institutional sales force

Bond Investors: Institutional and Retail Submit orders for new issues Buy and sell bonds in secondary market

Underwriting and Marketing Participants

MATURITY MMD Scale Principal Coupon Spread Yield 7/1/2014 0.20 45,000 2.000 0.250 0.450

7/1/2015 0.29 45,000 2.000 0.350 0.640

7/1/2016 0.42 1,850,000 3.000 0.350 0.770

7/1/2017 0.56 1,985,000 3.000 0.450 1.010

7/1/2018 0.75 2,020,000 4.000 0.500 1.250

7/1/2019 0.93 2,075,000 4.000 0.550 1.480

7/1/2020 1.15 2,145,000 5.000 0.600 1.750

7/1/2021 1.36 2,245,000 4.250 0.650 2.010

7/1/2022 1.55 2,250,000 5.000 0.700 2.250

7/1/2023 1.71 2,635,000 5.000 0.750 2.460

7/1/2024 1.85 2,600,000 4.000 0.900 2.750

7/1/2025 1.98 2,200,000 3.000 1.070 3.050

25

The Bond Market Interest rates Supply of bonds Financial Outlook Economic Releases Federal Reserve Policy The yield where similar bonds are trading in the secondary market

Investor demand depends on Federal and State Income Taxes Where are the bonds on the yield curve Coupons: premiums and discount Underlying Credit Rating and Credit Enhancement Size Serials versus terms bonds

How Securities are Priced

26

Key Components of the Pricing

The Wire

Priority of Orders

Takedowns

Yields

The Order Book

Re-Pricing

The Award Date

The Closing

Investors Amount ($) Amount (%)

Capital Reinsurance Co. 10,690 28.9%

Oppenheimer & Co. 5,825 15.7%

Brown Brothers Harriman 5,000 13.5%

Eaton Vance 5,000 13.5%

Wellington Mgt Co. 4,000 10.8%

Goldman Sachs Asset Mgt 2,000 5.4%

Chubb Insurance 2,000 5.4%

Goldman Arb 1,480 4.0%

Fidelity 1,000 2.7%

Total 36,995 100.0%

27