Embed Size (px)

Citation preview

Deferred Compensation Outside of the UnitedStates

Friday, 28 April 2006, 12:00 - 13:00

Narendra AcharyaBaker & McKenzie (Chicago)

Agnes CharpenetBaker & McKenzie (Paris)

Monika DietrichBaker & McKenzie (Zurich)

Luc MeeusBaker & McKenzie (Brussels)

Overview of Presentation

• Introduction to deferred compensation concept

•Background – changing US rules

•Belgium/France/Switzerland

•Example to illustrate differences

•Other considerations

•Takeaways – key implementation questions

What is “Deferred Compensation”?

•Case 1 – No deferral

• Employee receives EUR 1000 on 1/08/06 and issubject to income tax and social insurance in2006.

•Case 2 – Deferral for 3 years

• Employee makes a timely election to receiveEUR 1000 on 1/08/09 instead of 1/8/06 and issubject to income tax and social insurance in2009 (rather than in 2006).

What is “Deferred Compensation”?

•Why? – amounts grow at pre-tax yields, expect lowerbracket at time of payout

• Base salary generally not deferred

•More typical examples include:

• Incentive bonus plans which permit participants to deferreceipt (and taxation) of payout

• Restricted Stock Unit (“RSU”) plans which containdeferral election to receive shares at some later date(i.e., even after vesting)

• “U.S.-centric” models

Valid Deferrals/Timing of Elections

•At what point is it too late for participants to electto defer payment?

•Other factors

• Invalid deferral leads to taxation ofparticipant/employer withholding before cashreceived ◊No longer an incentive

Substantial Changes to U.S. Rules

•Section 409A

•Guidance under Notice 2005-1 & Proposed Regs.

•Generally effective January 1, 2005 but transitionrules

•Penalties include: (i) accelerated income inclusion,(ii) 20% excise tax, and (iii) interest and penalties.

International (Non-U.S.) Aspects of 409A

• US expatriates may participate in non-US retirement andother plans which do not comply with 409A.

• Non-US employees working in the US may continue toparticipate in their home country retirement and other planswhich do not comply with 409A.

• Proposed Regulations provide exceptions for foreignbroad-based plans in both cases.

• In many cases, funding of non-US trusts will trigger 409Aincome recognition where the trusts have US tax residentbeneficiaries.

But Also Consider Non-US Rules

•How are deferred compensation plans treatedoutside of the United States?

•These rules would apply to individuals subject toincome tax in the host jurisdiction

• Both local residents in the jurisdiction as well asexpatriates on assignment in the jurisdiction.

Let’s Look at Some Specific Jurisdictions

•Belgium, France and Switzerland (canton ofZurich)

• Is the issue specifically addressed under local taxlaws or “inferred” by applying general principlesunder local law?

•Generally, an absence of specific guidance inmost jurisdictions.

Belgium - General

•Domestic deferral programs are not common.

•US deferral programs are being “imported”increasingly.

•No specific domestic tax or social insurance rulesavailable in Belgium.

•Analysis is thus based on general tax and socialinsurance rules and is very fact driven.

Belgium – Income Qualification – Tax Rates

•The deferred bonus or deferred award is taxed asprofessional income at the normal progressiveincome tax rates (between 25% and 50%, notincluding local taxes) (Article 31 ITC).

•Discretionary nature of the award does not changethe aforementioned.

• Irrelevant that the grant is made by US parentcompany and not by the local employer (Com. IB30/1).

Belgium – Taxable Moment

•No specific rules regarding deferral of income.

•General rules:

- Professional income is taxed when “paid” or“attributed” (Article 360 ITC – Article 204, 3°,b) RD/ITC).

- “Attribution”: the date upon which thebeneficiary can effectively dispose of theincome or the date upon which it is availablefor payment .

Belgium – Taxable Moment

- If the income is not available for payment due to anelection of the employee made after the income waspaid or attributed, there will be no deferral of thetaxable moment.

- Tax authorities tend to have a strict view and tend toconsider that compensation is taxable if it is creditedfor the benefit of the employee in the books of thecompany, whether or not it is actually paid, if theemployee has an unconditional right to thecompensation even though such compensation is notpayable until some future time. Majority of the caselaw tends, however, to disagree with this strict view.

Belgium – Deferral Programs

•Possible on the basis of the aforementioned rules.

•Should relate to discretionary grant and not tobase salary provided for in an employmentagreement (discussion on “attributed”).

• Ideally performance based, but time based is notexcluded.

Belgium – Deferral Programs

Moment to elect deferral:•Before there is “payment” or “attribution”.

•Preferably before the “performance /measurement period”.

•To be phrased as a hypothetical question: “if wewere to grant you a discretionary bonus whencertain conditions are met, would you like toreceive the bonus in 2008 or in 2010?”

Belgium – Deferral Programs

•Election during the performance or measurementperiod should still be possible if done before theactual payment or attribution date - however lesscertain (unpublished private letter ruling: electdeferral before the employee is informed of theamount that is due to him).

•Strengthen the deferral by adding a contingencyelement (e.g., forfeiture if dismissed for cause), butshould not be strictly necessary.

Belgium – Deferral Programs

•Social insurance: generally follows the sameanalysis with respect to triggering event as forincome tax purposes.

•Social insurance contributions (± 35% for theemployer and 13,07% for the employee) are,however, only due if the remuneration is “borne”by the local employer (i.e., directly or indirectlycharged back to local employer or granted uponthe instruction /on behalf of the local employer).

Belgium – Conclusion

•Deferral should be possible (recent informalruling)- risk of requalification

• Moment of election is crucial

• Documents are crucial

• Avoid provision in the books

• Ideally provide contingency element

• Consider applying for a tax ruling

France - General

•Deferral plans are not common in France.

•No specific rules available in France.

•General principles apply for both personal incometax and social insurance purposes.

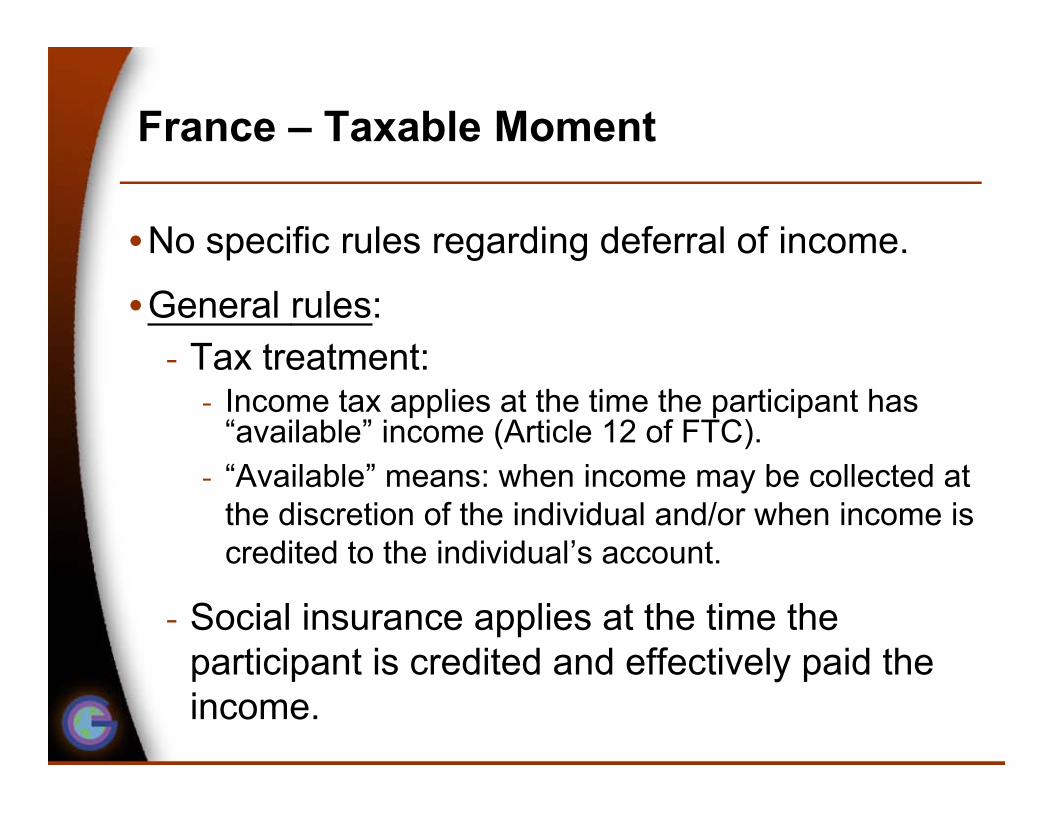

France – Taxable Moment

•No specific rules regarding deferral of income.

•General rules:- Tax treatment:- Income tax applies at the time the participant has

“available” income (Article 12 of FTC).- “Available” means: when income may be collected at

the discretion of the individual and/or when income iscredited to the individual’s account.

- Social insurance applies at the time theparticipant is credited and effectively paid theincome.

France – Deferral Programs

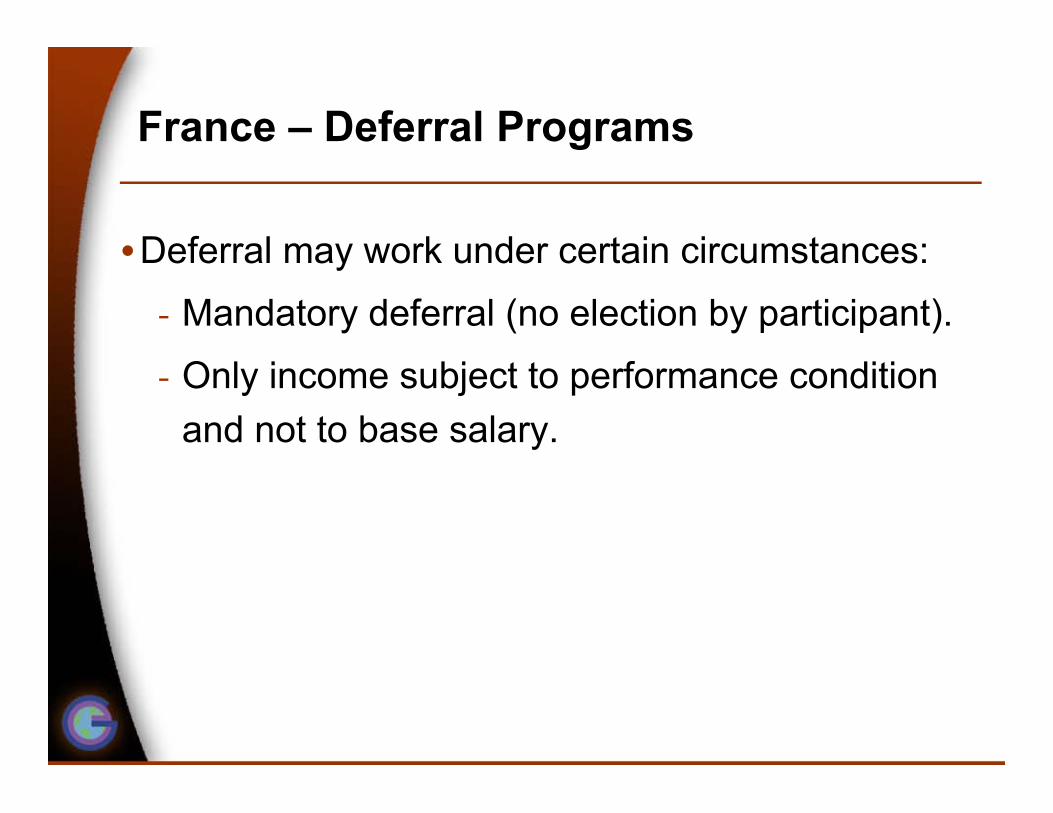

•Deferral may work under certain circumstances:

- Mandatory deferral (no election by participant).

- Only income subject to performance condition

and not to base salary.

France – Deferral Programs

Moment to elect deferral:

• Election is made prior to the date the participanthas available income and prior to the date theparticipant knows he is entitled to the payment(i.e., when satisfaction of performance conditionis known or measured).

France - Conclusion

•Limit to the deferral program

- Risks to substitute (a) amount fully taxable andfully subject to social insurance with (b) afavorable taxed award not subject to socialinsurance: disqualification of French qualifiedawards (options /RSUs).

•Unlikely to see legal or other changes on thistopic.

Switzerland

•Federal vs. Canton rules

•Domestic deferral programs are not common butUS deferral programs are being importedincreasingly.

•No specific rules in Switzerland with respect todeferral – therefore, general principles apply.

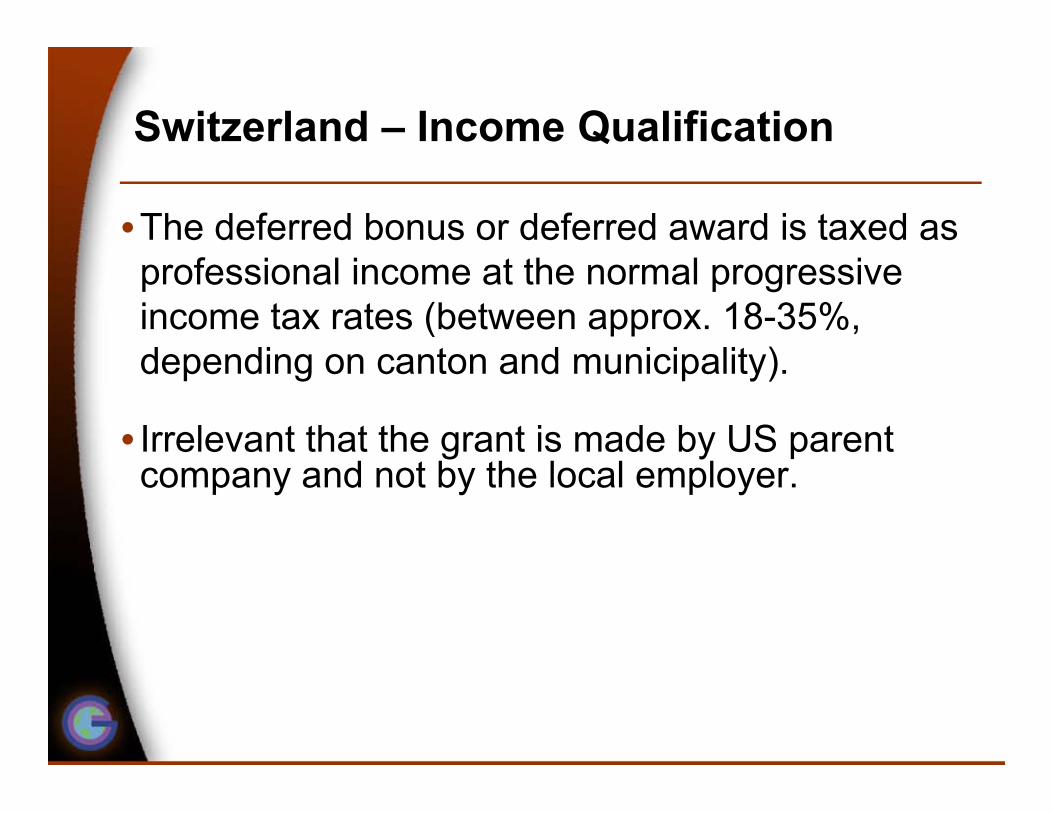

Switzerland – Income Qualification

•The deferred bonus or deferred award is taxed asprofessional income at the normal progressiveincome tax rates (between approx. 18-35%,depending on canton and municipality).

• Irrelevant that the grant is made by US parentcompany and not by the local employer.

•No specific rules regarding deferral of income

•General rules:- Professional income is taxed when participant

has irrevocable right.

- “Irrevocable right”: the date upon which theparticipant can effectively dispose of theincome.

Switzerland – Taxable Moment

Switzerland – Taxable Moment

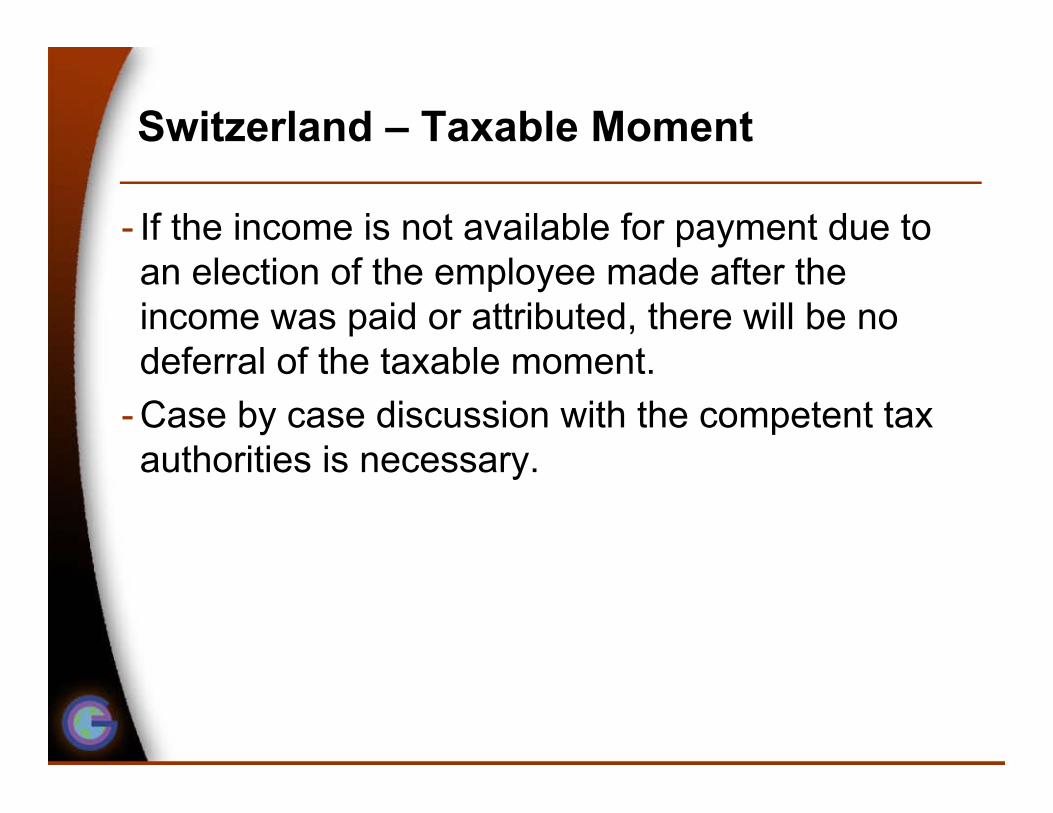

- If the income is not available for payment due toan election of the employee made after theincome was paid or attributed, there will be nodeferral of the taxable moment.

- Case by case discussion with the competent taxauthorities is necessary.

Switzerland – Deferral Programs

•Possible on the basis of the aforementionedrules.

•Should relate to discretionary grant and not tobase salary.

•Again, discussion with tax authorities is highlyrecommended (on a case by case basis).

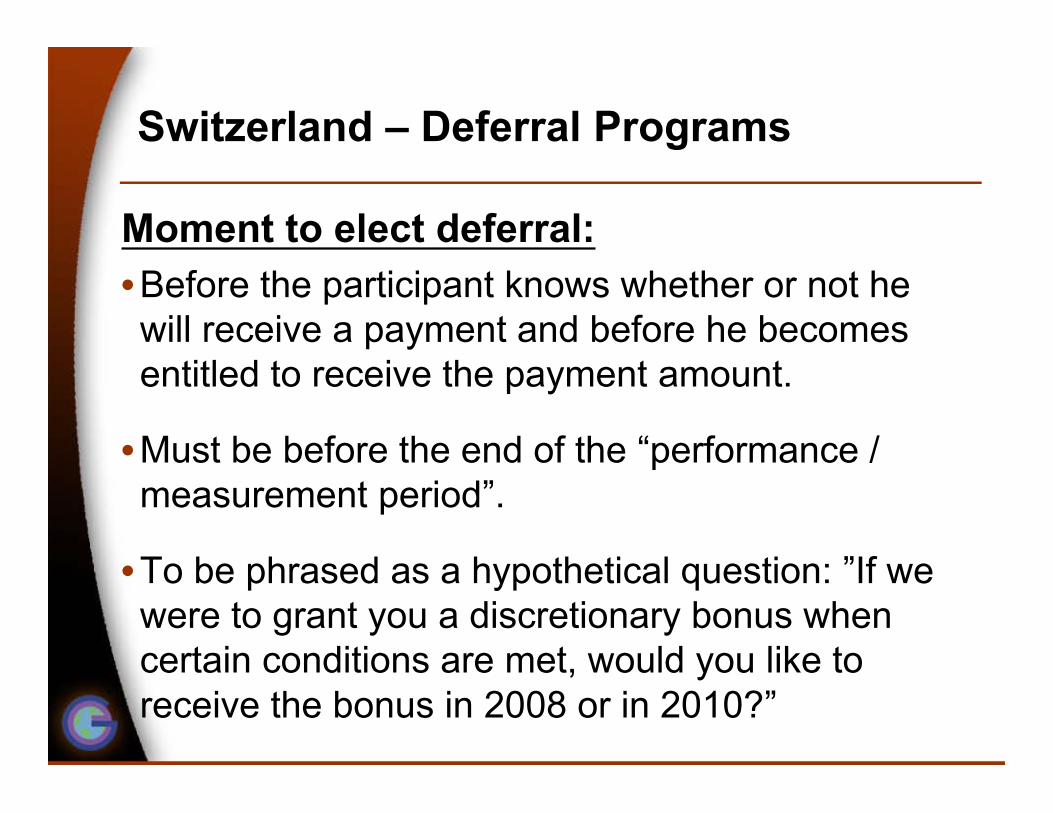

Switzerland – Deferral Programs

Moment to elect deferral:•Before the participant knows whether or not hewill receive a payment and before he becomesentitled to receive the payment amount.

•Must be before the end of the “performance /measurement period”.

•To be phrased as a hypothetical question: ”If wewere to grant you a discretionary bonus whencertain conditions are met, would you like toreceive the bonus in 2008 or in 2010?”

Switzerland – Deferral Programs

•Strengthen the deferral by adding a contingencyelement (e.g., forfeiture if dismissed for cause),but should not be strictly necessary.

•Social insurance: generally follows the sameanalysis with respect to triggering event as forincome tax purposes.

Switzerland – Legal Changes

•Draft of new law with respect to taxation ofemployee benefits. However, the new law doesnot provide any specific rules with respect todeferral.

•As long as new law has not entered into force,advisable to seek ruling from the competent taxauthorities.

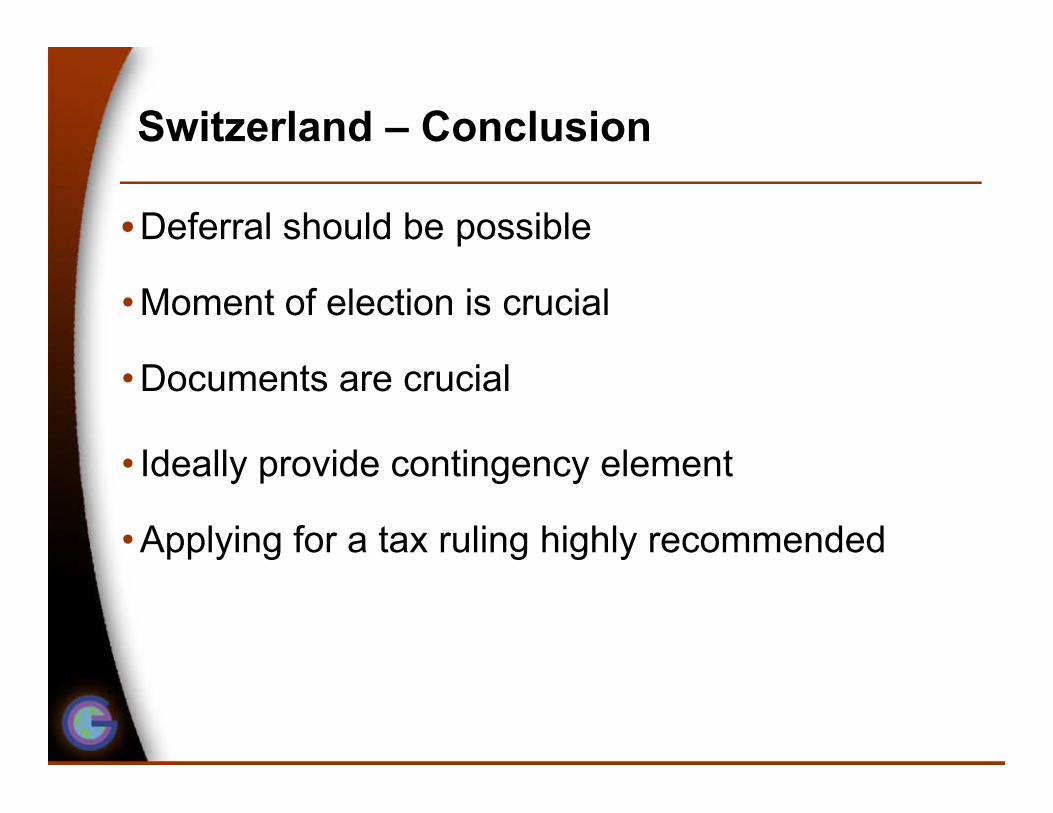

Switzerland – Conclusion

•Deferral should be possible

• Moment of election is crucial

• Documents are crucial

• Ideally provide contingency element

• Applying for a tax ruling highly recommended

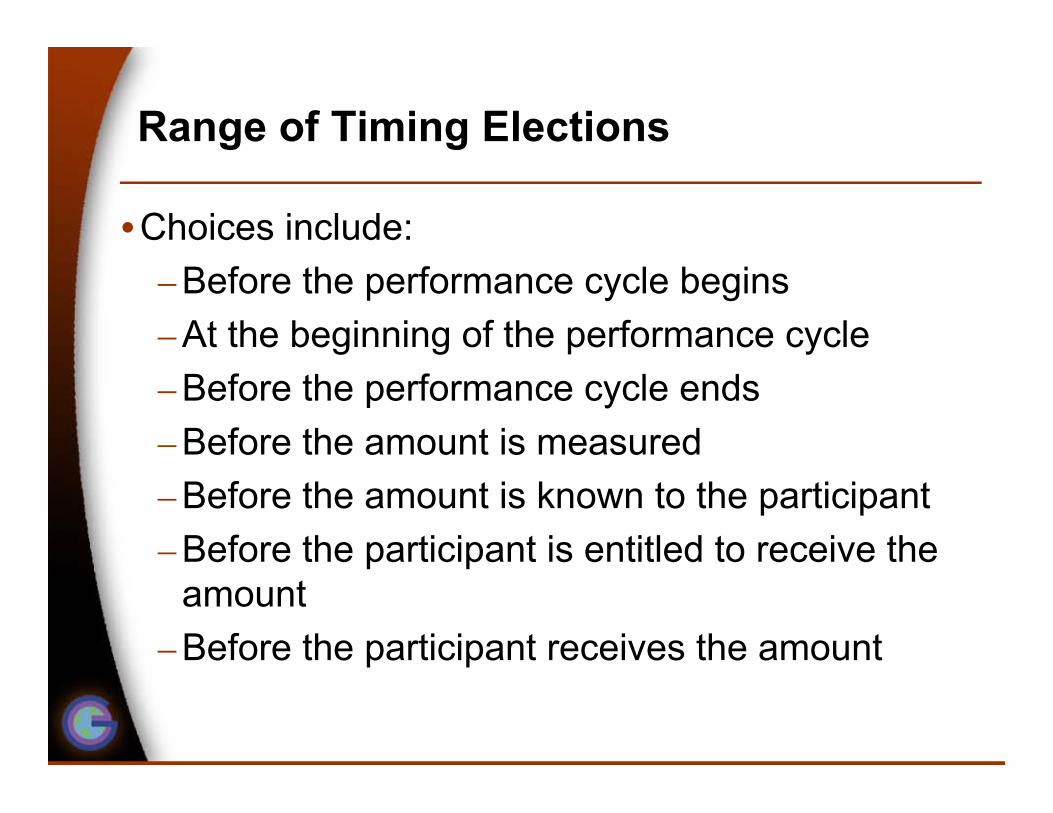

Range of Timing Elections

•Choices include:

–Before the performance cycle begins

–At the beginning of the performance cycle

–Before the performance cycle ends

–Before the amount is measured

–Before the amount is known to the participant

–Before the participant is entitled to receive theamount

–Before the participant receives the amount

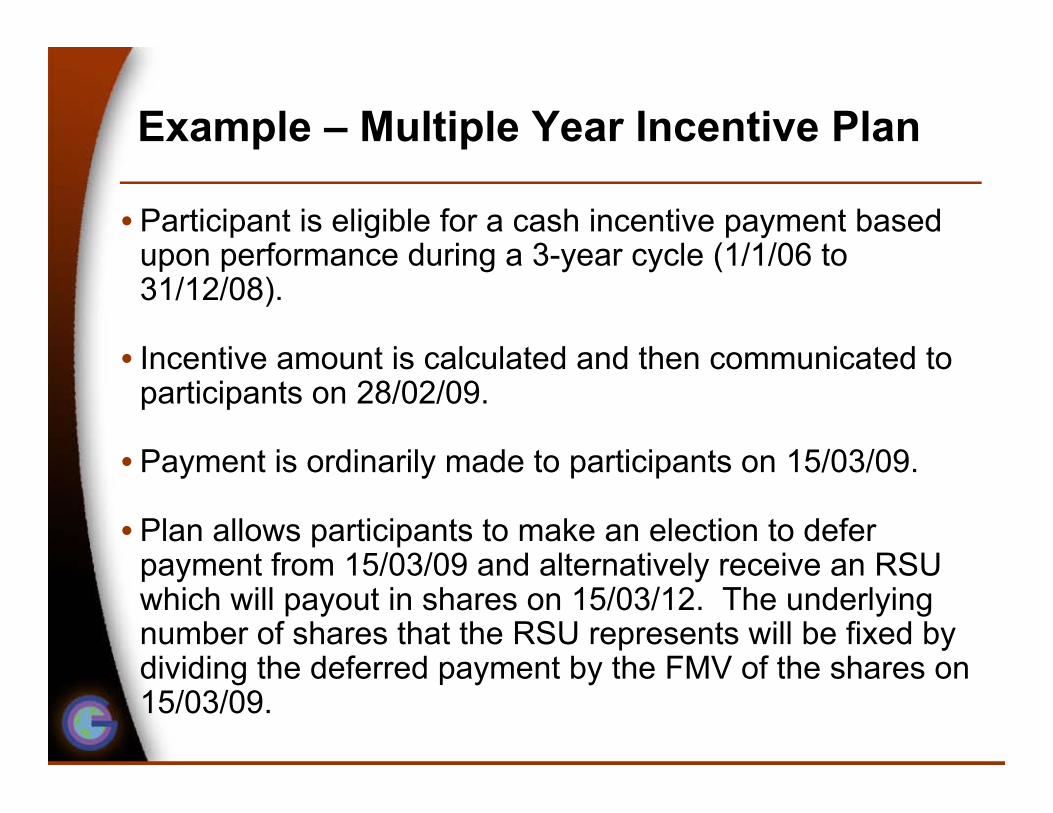

Example – Multiple Year Incentive Plan

• Participant is eligible for a cash incentive payment basedupon performance during a 3-year cycle (1/1/06 to31/12/08).

• Incentive amount is calculated and then communicated toparticipants on 28/02/09.

• Payment is ordinarily made to participants on 15/03/09.

• Plan allows participants to make an election to deferpayment from 15/03/09 and alternatively receive an RSUwhich will payout in shares on 15/03/12. The underlyingnumber of shares that the RSU represents will be fixed bydividing the deferred payment by the FMV of the shares on15/03/09.

Example – Time Line

1/01/06

Performanceperiod

31/12/08 28/02/09 15/03/09 15/03/12

Calculation Payment Deferral

Example – Multiple Year Incentive Plan

•Belgium: election ideally before the performancecycle; to be phrased as a hypothetical question;ideally no provision in the books of the grantor.

•France: election at the beginning of theperformance cycle (or even before theperformance cycle begins) shall be acceptablesince the participant does not know with certaintywhether he will even be entitled to a cash payment(or the RSU grant). Unlikely for the RSU grant tomeet the requirements of a French tax-qualifiedRSU.

Example – Multiple Year Incentive Plan

•Switzerland: election needs to be made beforeparticipant knows whether or not he will receive abonus payment and before he knows what theamount of the bonus payment will be.If election is made at the “right” time, the grant ofRSU is not a taxable event but only the vesting ofthe RSU. Ruling advisable! Social insuranceusually follows tax treatment

Some Other Jurisdictions

•Canada – Salary Deferral Arrangement rules

– Impact on RSUs

•Brazil

•Many countries do not permit deferrals

Other Considerations

•Are the social insurance rules synchronized withincome tax recognition rules?

•Employer reporting of valid deferrals?

•Employer withholding of valid deferrals.

•Expatriate and cross-border issues.

Takeaways!

• Rules are very specific to jurisdiction.

• Be wary of exporting US plans (even 409A compliant plans) to rest ofthe world.

• At the same time, local rules may be less strict than the new USrequirements.

• Not like stock options (where generally viable in the majority ofjurisdictions)

• Consider the following questions for the initial jurisdictional analysis:

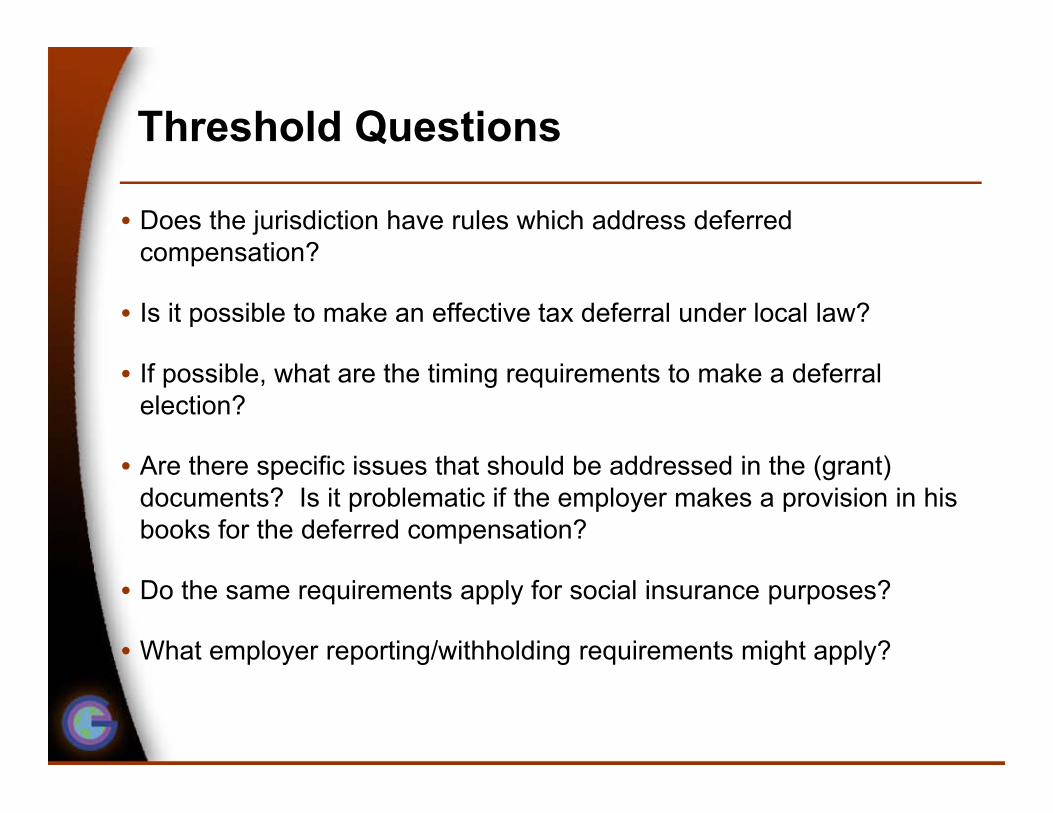

Threshold Questions

• Does the jurisdiction have rules which address deferredcompensation?

• Is it possible to make an effective tax deferral under local law?

• If possible, what are the timing requirements to make a deferralelection?

• Are there specific issues that should be addressed in the (grant)documents? Is it problematic if the employer makes a provision in hisbooks for the deferred compensation?

• Do the same requirements apply for social insurance purposes?

• What employer reporting/withholding requirements might apply?

Questions?

Thank you for your participation

![BENEFITS & COMPENSATION INTERNATIONAL1].pdf · qualified deferred compensation plan”. Deferred compensation arrangements issued by foreign- ... United States will be regarded as](https://img.pdfslide.net/doc/110x75/5b69676e7f8b9ab0128e2dd8/benefits-compensation-international-1pdf-qualified-deferred-compensation.jpg)