Embed Size (px)

Citation preview

Department of Public Instruction March - 2015 1

SPRING FINANCE WORKSHOP

Wednesday, March 11, 20153:30 – 4:45 p.m.

Department of Public InstructionSchool Financial Services Team

Department of Public Instruction March - 2015 2

SPRING FINANCE WORKSHOP Agenda

Revenue Limit -- Levy Chargebacks Counting Part Time Pupils Revenue Limit -- Line 7B Hold Harmless Revenue Limit -- Transfer of Service Community Programs and Services – Fund 80 PI 1500 District Contact Report Revenue Limit -- Energy Efficiency Exemption Long Term Capital Improvement Trust Fund

(Fund 46) 2015-17 Governor’s Budget Review

Department of Public Instruction March - 2015 3

Levy Chargebacks2 Types

1. Line 10D Non-Recurring Exemption Refunded or Rescinded Taxes

2. Line 15C Prior-Year Levy Chargebacks (Uncollectible)

Distinction was clarified in Act 32(State Biennial Budget for 2011-13)

Department of Public Instruction March - 2015 4

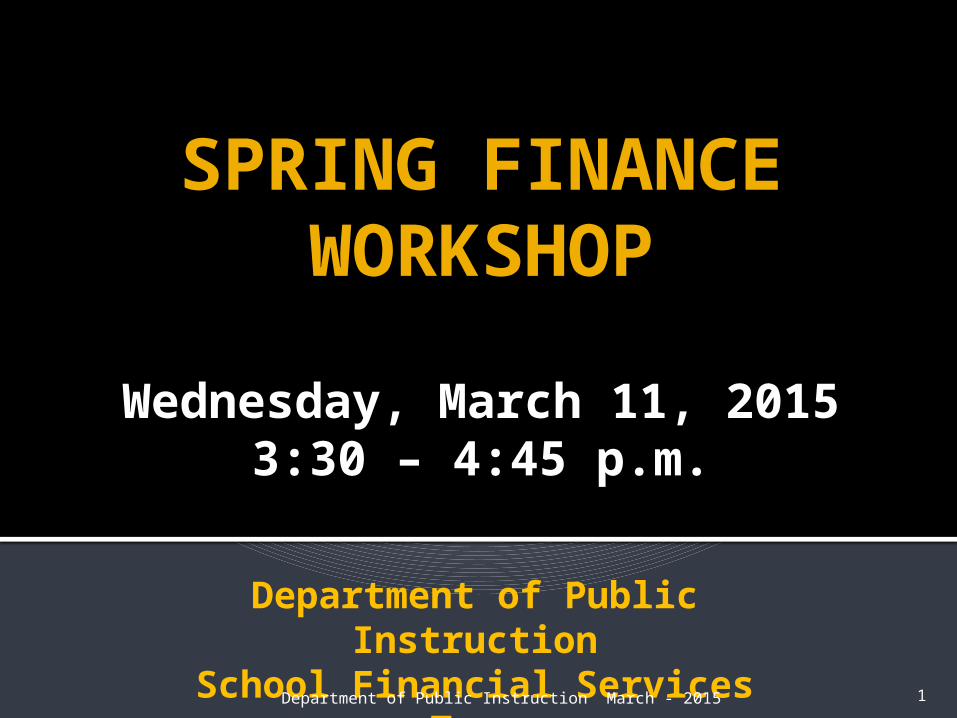

Line 10D Non-Recurring Exemption Refunded/Rescinded

Assessment for a property is reduced (via court case or reviewing authority….can be a multi-year process and usually involves large settlements)

Property owner can request of the Department of Revenue (DOR) a refund of taxes previously paid on the higher value.

Department of Public Instruction March - 2015 5

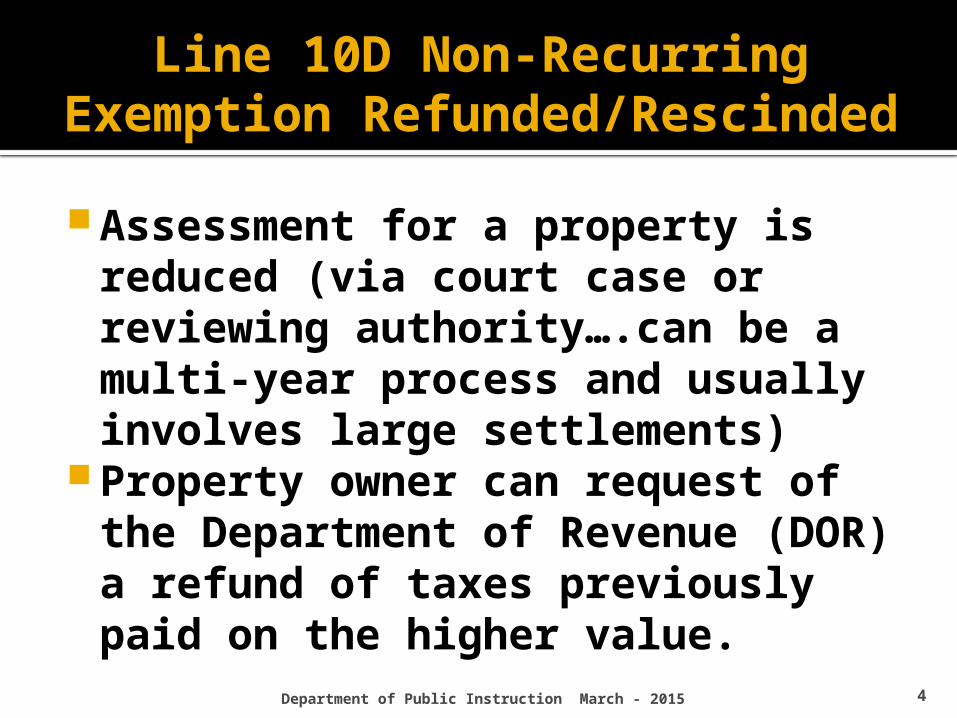

Line 10D Non-Recurring Exemption Refunded/Rescinded

School district is notified by DOR via letter referencing “palpable error that would affect the equalized value.” DOR issues all rescinded letters at once - in November, usually the 15th.

School district refunds (sends back) overpaid taxes + interest by February 15, 3 months later. (code to 10E 972 492000)

Department of Public Instruction March - 2015 6

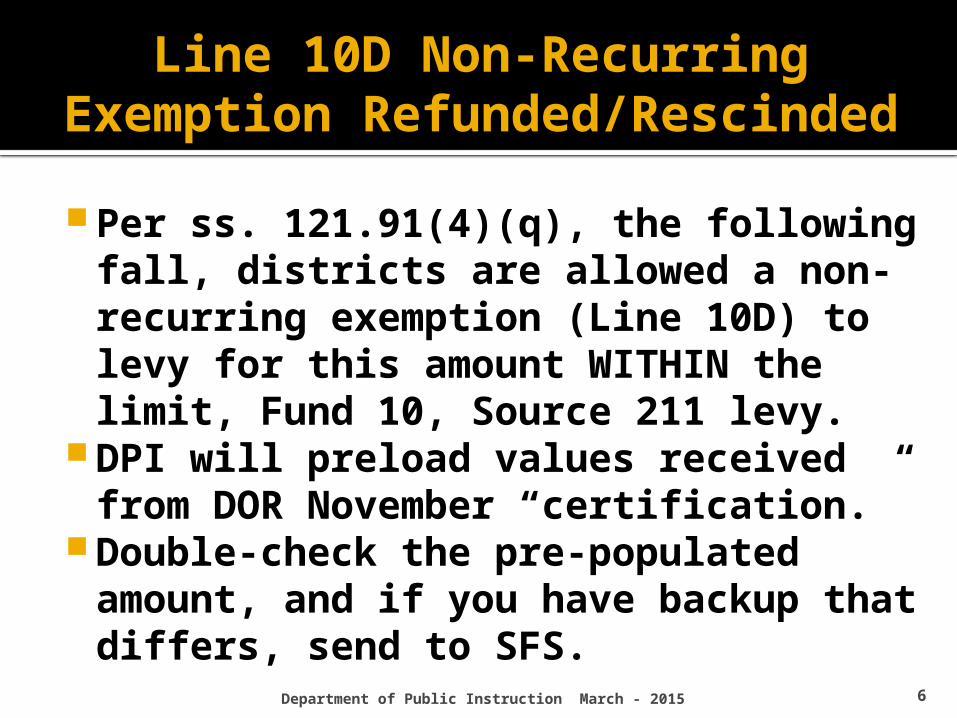

Line 10D Non-Recurring Exemption Refunded/Rescinded

Per ss. 121.91(4)(q), the following fall, districts are allowed a non-recurring exemption (Line 10D) to levy for this amount WITHIN the limit, Fund 10, Source 211 levy.

DPI will preload values received from DOR November “certification.”

Double-check the pre-populated amount, and if you have backup that differs, send to SFS.

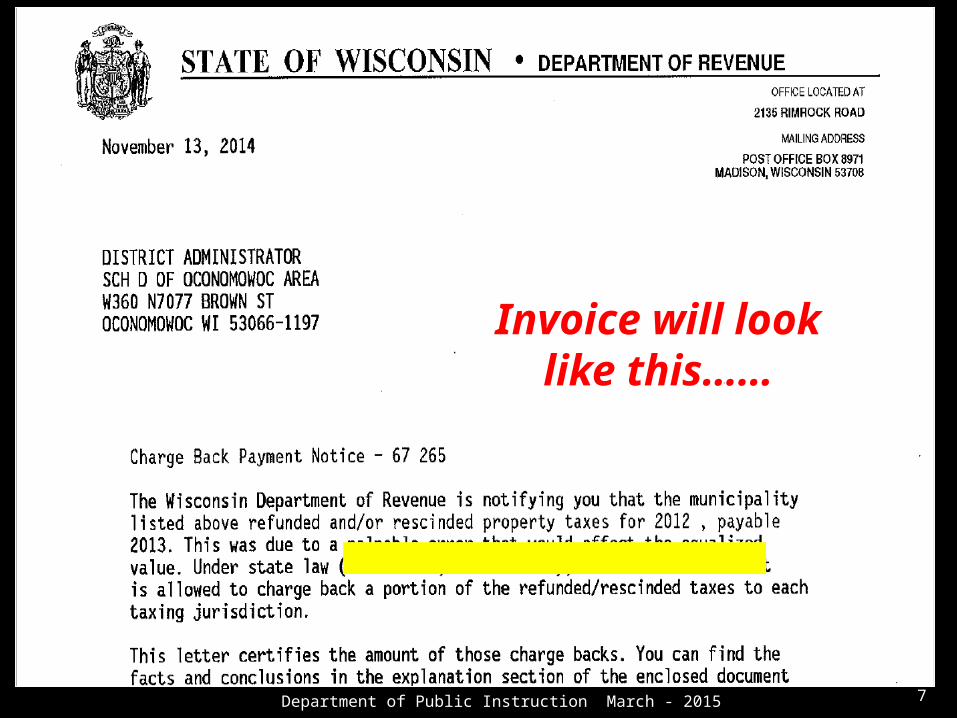

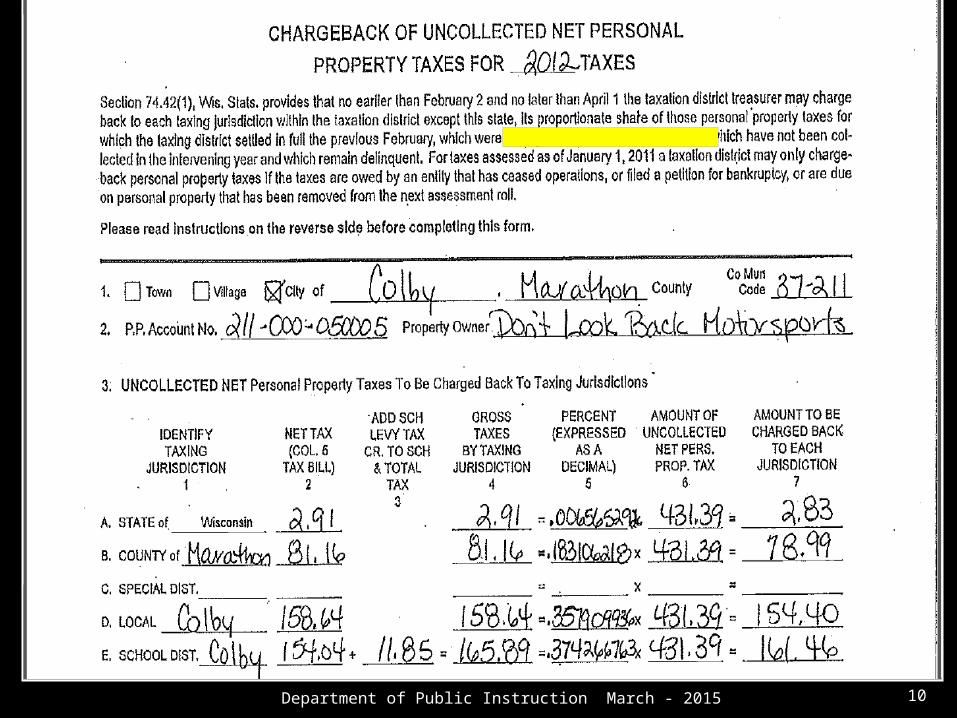

7

Invoice will look like this……

Department of Public Instruction March - 2015

Department of Public Instruction March - 2015 8

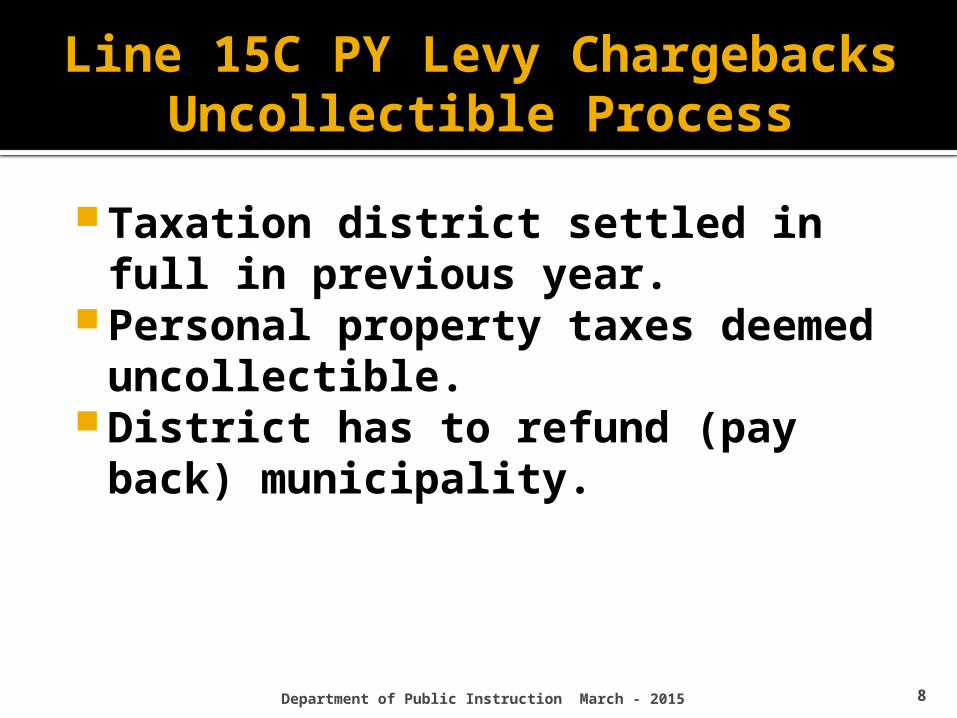

Line 15C PY Levy Chargebacks Uncollectible Process

Taxation district settled in full in previous year.

Personal property taxes deemed uncollectible.

District has to refund (pay back) municipality.

Department of Public Instruction March - 2015 9

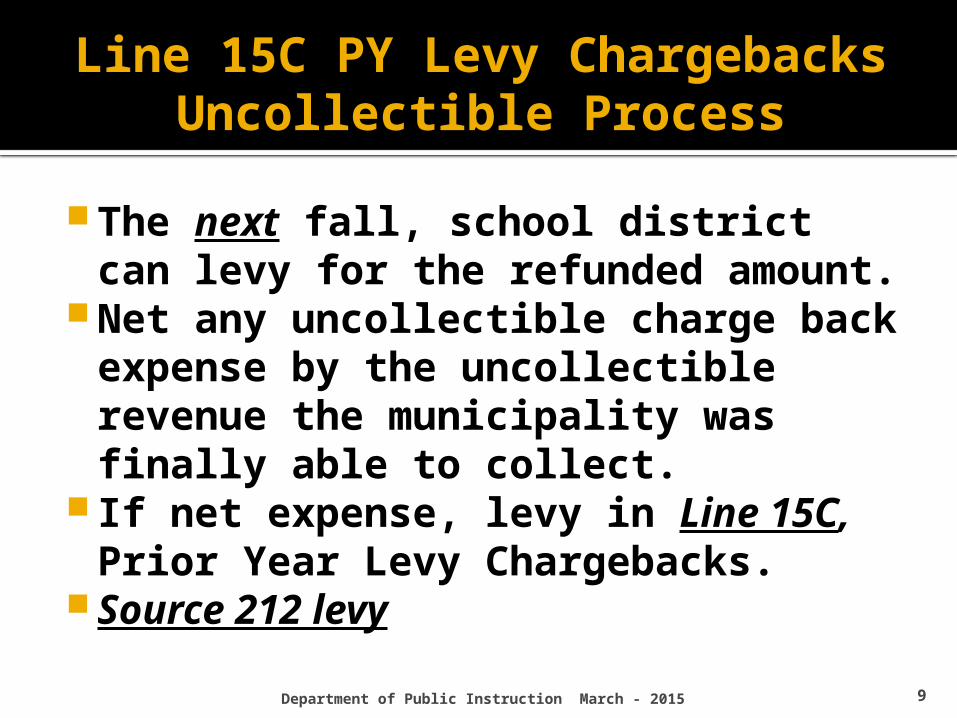

Line 15C PY Levy Chargebacks Uncollectible Process

The next fall, school district can levy for the refunded amount.

Net any uncollectible charge back expense by the uncollectible revenue the municipality was finally able to collect.

If net expense, levy in Line 15C, Prior Year Levy Chargebacks.

Source 212 levy

Department of Public Instruction March - 2015 10

Invoice will look like this……

Department of Public Instruction March - 2015 11

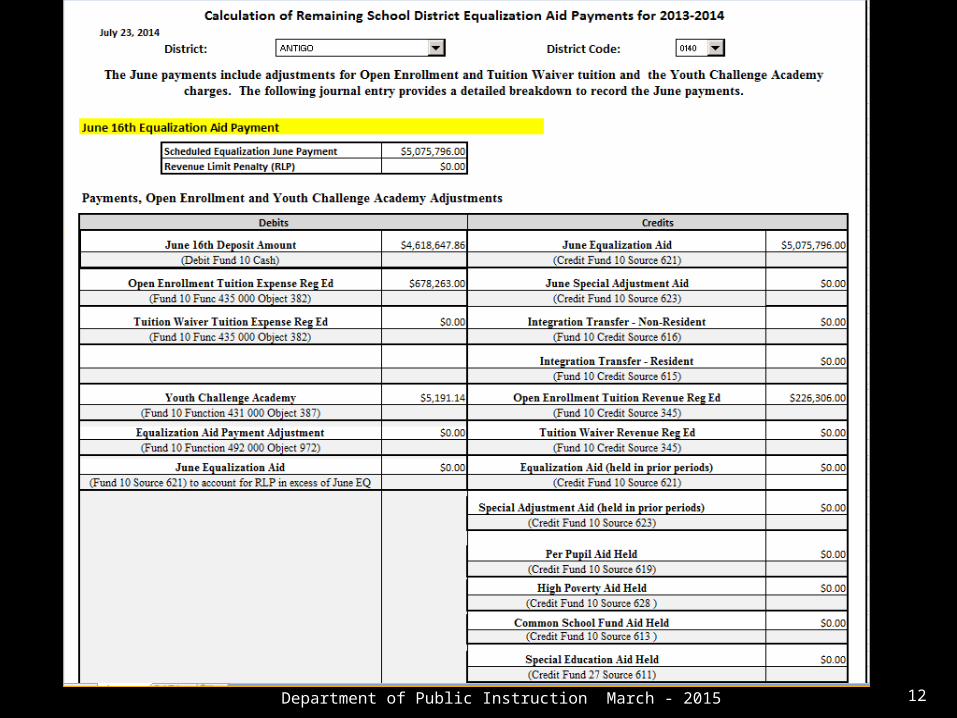

EOY Adjusting Entries Related to June and July Aid Payments

Many calls from districts not able to match the SAFR expected values for State Aid programs or Open Enrollment Revenue/Expense.

Post all adjusting entries – June and July payment in the document found at this address…

http://sfs.dpi.wi.gov/sfs_pay_aid_infoCalculation of Remaining

Equalization Aid Payments for2014-15

Department of Public Instruction March - 2015 12

Department of Public Instruction March - 2015 13

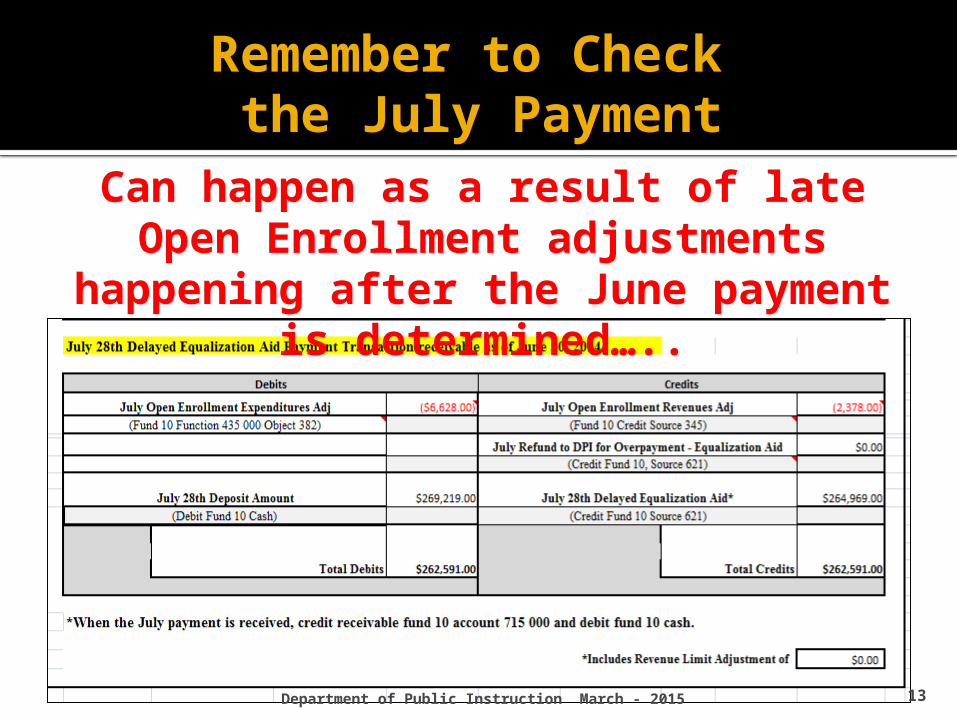

Remember to Check the July Payment

Can happen as a result of late Open Enrollment adjustments happening after

the June payment is determined…..

Department of Public Instruction March - 2015

Counting Part Time Pupils

14

2013 Act 20 – A Change

District of attendance may count non-resident, home-schooled pupils enrolled part-time

Different method to count resident vs. non-resident part-time pupils

Residents are reported in Step 3 in PI-1563 Non-Residents are reported via paper. See

Membership Link on SFS scanbar.

Department of Public Instruction March - 2015

Counting Part Time Pupils

15

Pupil comes from:

Home School[All grades]

Private School[Grade 9-12]

RESIDENT NON-RESIDENT

0.25 FTE per course (max of 2

courses)

# PT Pupil Hours / FT Hours for

Grade = FTE

# PT Pupil Hours / FT Hours for

Grade = FTE

Cannot be counted

Report residents in the portal. Report non-residents via Excel

Spreadsheet found at:http://sfs.dpi.wi.gov/sfs_membrpt2

Department of Public Instruction March - 2015 16

Revenue Limit Line 7B Hold Harmless

…and how membership adjustments made AFTER the levy is set can cause some unexpected

consequences….

Department of Public Instruction March - 2015 17

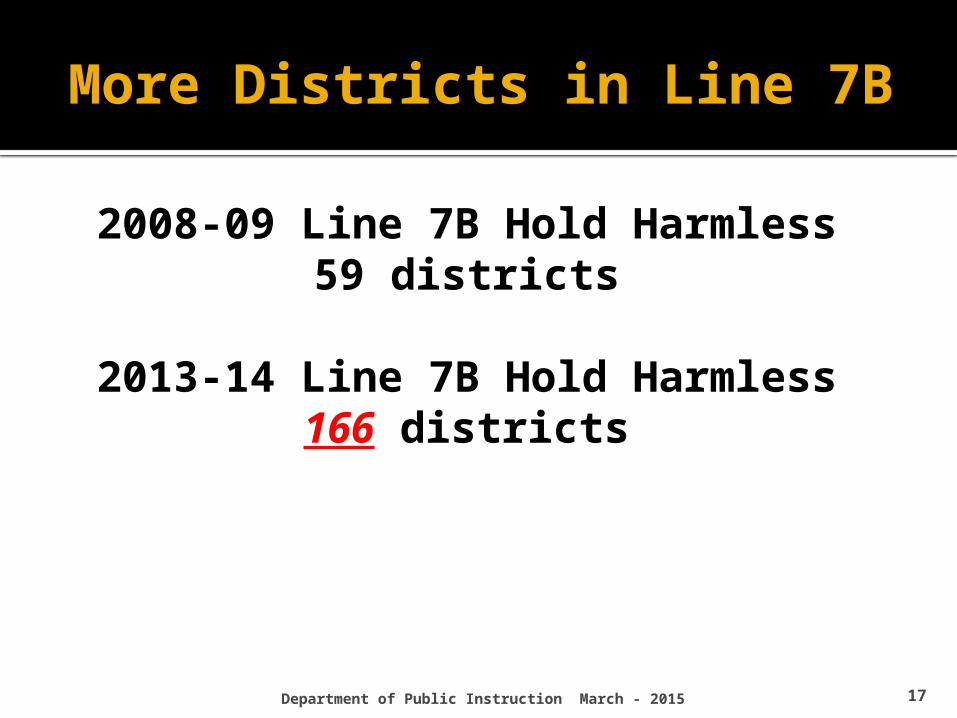

More Districts in Line 7B

2008-09 Line 7B Hold Harmless59 districts

2013-14 Line 7B Hold Harmless166 districts

Department of Public Instruction March - 2015 18

Unintended Consequence

Non-recurring exemption that ensures Line 7 is at least as much as Line 1.

Subsequent membership change will not alter your total in Line 7 (includes Line 7B) unless change is significant.

Likely that membership changes will not alter what your Line 7B is.

Department of Public Instruction March - 2015 19

Unintended Consequence

Increasing membership will reduce the declining enrollment exemption, reducing your limit. (possible into penalty)Decreasing membership will increase your declining enrollment exemption, increasing your limit. (possibly underlevy)

Department of Public Instruction March - 2015 20

Transfer of Service (TOS)

Each TOS request is to be based on providing services to meet a student’s educational needs that are beyond the district’s current program.

The PI 5000 TOS portal opened on Monday, February 23, 2015.

The PI 5000 will close on Tuesday, August 31, 2015.

Department of Public Instruction March - 2015 21

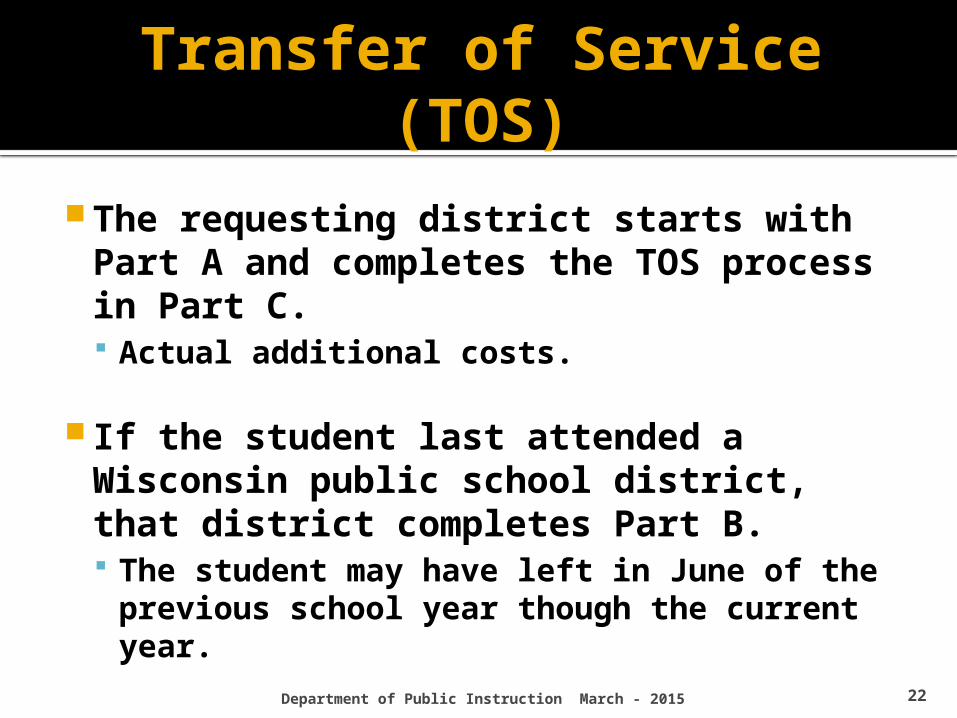

Transfer of Service (TOS)

The requesting district starts with Part A and completes the TOS process in Part C. Actual additional costs.

If the Transfer of Service request is for a student who enrolled later in the school year, the requesting district may make a request by: [Looking forward] estimated and additional

cost in the coming school year.

Department of Public Instruction March - 2015 22

Transfer of Service (TOS)

The requesting district starts with Part A and completes the TOS process in Part C. Actual additional costs.

If the student last attended a Wisconsin

public school district, that district completes Part B. The student may have left in June of the

previous school year though the current year.

Department of Public Instruction March - 2015 23

Transfer of Service (TOS)

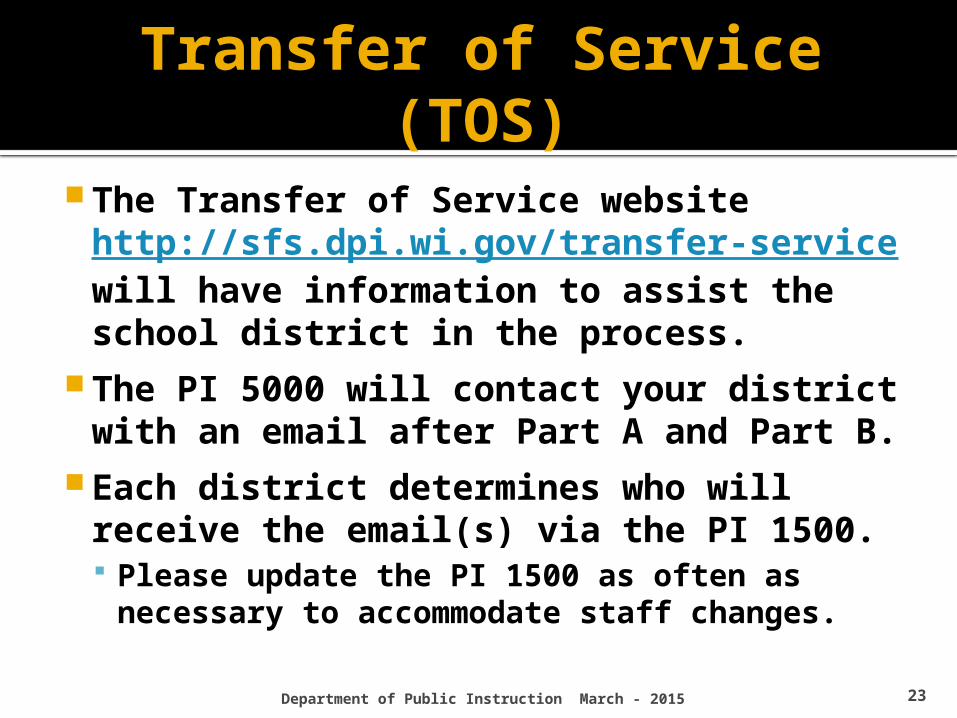

The Transfer of Service website http://sfs.dpi.wi.gov/transfer-service will have information to assist the school district in the process.

The PI 5000 will contact your district with an email after Part A and Part B.

Each district determines who will receive the email(s) via the PI 1500. Please update the PI 1500 as often as

necessary to accommodate staff changes.

Department of Public Instruction March - 2015 24

Community Programs and Services – Fund 80

Statutory authority: 120.13 (19) COMMUNITY PROGRAMS AND SERVICES.

General Outline of Community Service Activities:

Access to Community Service Fund activities cannot be limited to pupils enrolled in the district's K-12 educational programs.

Other funds, such as the General Fund and Special Projects Fund, carry out the day to day K-12 educational operations of the district.

All activities associated with a well-rounded curriculum (curricular and extra-curricular activities) are to be accounted for in these funds (General Fund and Special Projects Fund)and the Pupil Activity Fund (Fund 60).

Department of Public Instruction March - 2015 25

Community Programs and Services – Fund 80

The levy for Fund 80 was removed from revenue limit control starting in the 2000-01 school year [s. 121.91(2m)(e)1.]

As a result, the Fund 80 levy is completely funded by local taxpayers.

It has never been a factor in the equalization aid calculation.

• The Department(DPI) is required to define ineligible costs for Community Programs and Services by administrative rule.

• PI-80 emergency rules took effect on July 1, 2014.

Department of Public Instruction March - 2015 26

Community Programs and Services – Fund 80 and PI 80

Ineligible costs means school district costs that are not the actual, additional costs to operate community programs and services.

First, costs are ineligible if they are not costs to operate community programs and services. Community programs and services do not include any program that is limited to only school district pupils or any program or service whose schedule presents a significant barrier for age-appropriate school district residents to participate in the program or service.

Second, costs must not only be costs to operate community programs and services to be eligible but also must be actual, additional costs. Ineligible costs include costs that would be incurred by the school district if the community programs and services were not provided by the school district.

Department of Public Instruction March - 2015 27

Community Programs and Services – Fund 80 and PI 80

PI 80.02 Definitions. In this chapter: “Community programs and services” does not include:

Any program or service that is limited to only school district pupils.

Any program or service whose schedule presents a significant barrier for age-appropriate school district residents to participate in the program or service.

“Ineligible costs” means school district costs that are not the actual, additional costs to operate community programs and services under s. 120.13 (19), Stats. “Ineligible costs” includes costs that would be incurred by the school district if the community programs and services were not provided by the school district.

Department of Public Instruction March - 2015 28

Community Programs and Services – Fund 80 and PI 80

What does “actual” and “additional” costs mean to a school district?

A cost, that if the ability to operate the Community Service Fund (Fund 80) ended; a school district, would not have to move those costs to the General Fund (Fund 10) to continue the regular curricular and extracurricular programs for its students.

A few examples: Before school and after school childcare open to any

district resident. Adult technology classes held at the local public library. Adult literacy classes held at a township hall within the

school district.

Department of Public Instruction March - 2015 29

Community Programs and Services – Fund 80 and PI 80

What does “actual” and “additional” costs mean to a school district?

A more complex example: The summer baseball program for all interested resident students uses the school district’s ball diamond for games, after the high school season is over. District employees do the mowing, mark the field, and clean

up after the game. The field does not have lights and the concession stand is not operating. ▪ Each District employee logs their time related to this

program and based on past records the total hours/game are determined and charged to Fund 80.

▪ The related costs for mower fuel and field paint is based on past years records and are charged to Fund 80

Department of Public Instruction March - 2015 30

Community Programs and Services – Fund 80 and PI 80

What does “actual” and “additional” costs mean to a school district?

An example of an expense not meeting this standard: An adult ballroom dance class is held one night a week for 6 weeks in the middle school gym. It has the facility for a 3 hour period of time.

The class instructor or a participant sweeps the floor before the class starts.

The custodial staff do not clean the gym or restrooms in this part of the building until after everyone from the class has left the school.

There can be no custodial time or related costs charged to Fund 80 for this class as there was no actual or additional cost incurred.

Department of Public Instruction March - 2015 31

Community Programs and Services – Fund 80 and PI 80

2013 Act 306 requires that Fund 80 expenditures be audited by the school district’s auditor.

NOTE: Current law already directs DPI to exclude from Shared Costs (for General Aid purposes) any CPS expenditures.

▪ If a CPS expenditure audit determines that a district had inappropriately coded CPS expenditures to Fund 10, those expenditures would have to be removed from Fund 10 and would decrease the district’s Shared Costs for General Aid purposes.

Department of Public Instruction March - 2015 32

Community Programs and Services – Fund 80 and PI 80

2013 Act 306 requires DPI to determine if ineligible CPS expenditures exist If so, DPI must reduce the district’s allowable revenue limit

authority the following year by the amount of the ineligible CPS expenditures; structured as a negative exemption rather than a reduction to the district’s base.

This first applies to the Revenue Limit calculation for the 2015-16 school year, based on 2014-15 expenditures. The audit process will be more detailed than it was this past

school year. The independent school auditors will be given formal

procedures after May 15, 2015.

Department of Public Instruction March - 2015 33

Community Programs and Services – Fund 80 and PI 80

Preparing for a CPS audit; Each program or service will need to be documented

within the district’s accounting system. Supporting documentation will be part of the audit

process. Wisconsin Uniform Financial Accounting

Requirements (WUFAR) will assist each district in this process.

Community Service Fund Information http://sfs.dpi.wi.gov/sfs_comm_serv website provides the most recent information regarding Fund 80. Question and Answers Complete Fund 80 PowerPoint

Department of Public Instruction March - 2015 34

PI 1500 District Contact Report

This portal was renovated and became active in early January (2015).

It is time to review this site to confirm it reflects the district’s current staff.

The PI-1500 District Contacts is built around one key piece of individual information, the User ID. Once in the system the User ID cannot be

changed.

Department of Public Instruction March - 2015 35

PI 1500 District Contact Report

It is recommended that your school district establish an IT security policy/protocol with regard to creating an ID and Password.

Normally the superintendent and at least one designee must provide the new employees with their User ID, email address and related duties.

SFS/DPI-1500 District Contacts Report - New Process Will assist anyone who has questions on the

process.

36

PI 1500 District Contact Report

Once an individual has been entered in to the PI 1500 for your district, that individual becomes responsible for retrieving their own ID or Password using the 3 links below the “Log In” button.

Through this portal the district is responsible to assign an individual: a personal ID, their original Password,and which reports this individual will receive information about and/or the authority to enter data in the related portal for the district.

Department of Public Instruction March - 2015

37

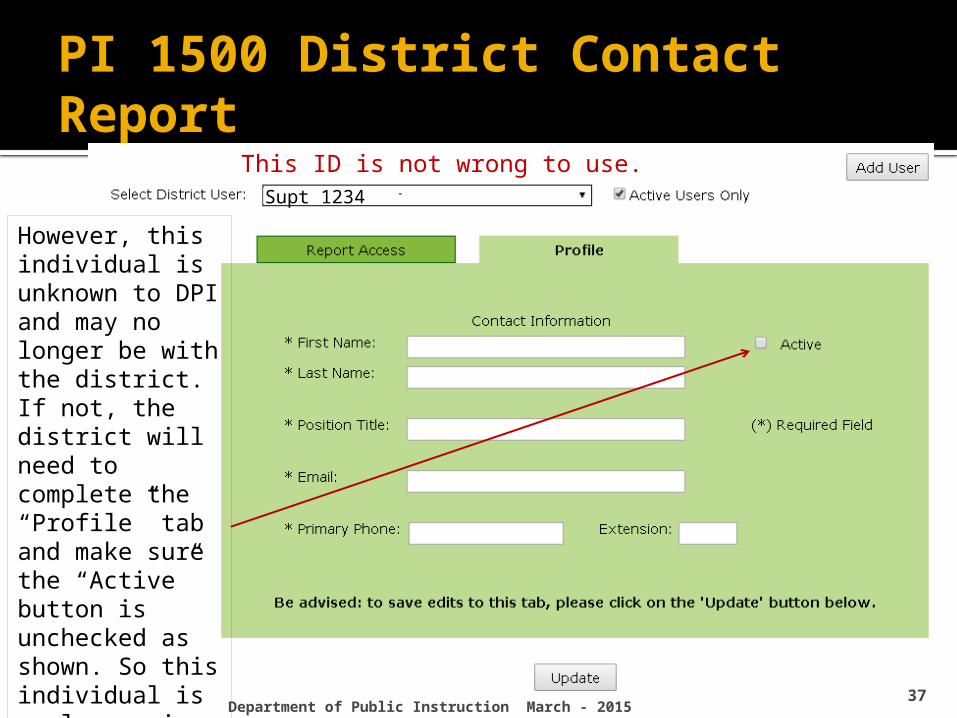

PI 1500 District Contact Report

Supt 1234

However, this individual is unknown to DPI and may no longer be with the district. If not, the district will need to complete the “Profile” tab and make sure the “Active” button is unchecked as shown. So this individual is no longer in the drop down list.

This ID is not wrong to use.

Department of Public Instruction March - 2015

Department of Public Instruction March - 2015 38

Energy Efficiency Exemption

Facility project Per Wisconsin Statute §121.91(4)(o) school districts

may exceed the revenue limit on a non-recurring basis for a project to increase the energy efficiency of a facility.

The project is governed by a performance contract entered into under Wisconsin Statute §66.0133.

Energy Savings Performance Contracting per Wisconsin Statute §66.0133 is broader that the Revenue Limit exemption with regard to nature projects.

Department of Public Instruction March - 2015 39

Energy Efficiency Exemption

Districts are encouraged to consider their options, but know the prudent course is to limit projects to facility

energy efficiency measures.

Administrative Rule PI 15 is currently being reviewed for revision purposes.

Department of Public Instruction March - 2015 40

Energy Efficiency Exemption

Reminders: Publication and Reporting requirements.

▪ Budget Hearing and DPI Energy savings must be used to reduce the

tax levy. Always separate BOE motions for each

levy by fund to the second digit. Separate Fund 38 & Fund 39.

Department of Public Instruction March - 2015 41

A school board may establish a “trust” to fund capital improvement projects per their ten year long-term capital improvement plan.

The trust is funded with a transfer from the general fund.

The contribution (transfer) from Fund 10 to Fund 46 is recorded as the expenditure for shared cost and equalization aid purposes.

Long-term Capital Improvement Trust Fund Wisconsin Statute 120.137

Department of Public Instruction March - 2015 42

Long-term Capital Improvement Trust Fund (46) - REQUIREMENTS

Board approved 10 year capital improvement plan.

Board resolution to establish a trust. Creation of a segregated bank account. Reporting to DPI. http://sfs.dpi.wi.gov/sfs_capital_projects_funds

Department of Public Instruction March - 2015 43

Long-term Capital Improvement Trust Fund (46)

Allows districts to set aside funds for capital projects

Requires planning for capital facility needs and improvements including care and maintenance.

May level out expenses for shared cost (rather than a large project expenditure in Fund 10)

Opportunity for end of fiscal year expenditure

Department of Public Instruction March - 2015 44

Long-term Capital Improvement Trust Fund (46)

Where is the district in the Equalization Aid formula? District/Local Factors

▪ Shared Costs (Spending)▪ Equalized Property Value (Wealth)▪ Membership (Number of Students to Educate)

State Factors▪ Cost Ceilings▪ Guaranteed Valuations▪ Total Amount Of Funding

Consider that shared cost is only one factor to consider when evaluating the Fund 46 option.

Department of Public Instruction March - 2015 45

Long-term Capital Improvement Trust Fund (46)

Is the resolution the same as for the OPEB trust? No – Fund 46 is not a legally established irrevocable trust BUT the funds money be physically segregated in a separate account and only used for the purposes as described in the resolution and 10 year plan.

What if the plan is no longer represents our needs? With board approval, change the plan.

Department of Public Instruction March - 2015 46

Governor’s Budget in review

“2015-17 Biennial Budget Information” is available on the Policy and Budget Team http://pb.dpi.wi.gov/ website.

“DPI Summary of Governor's 2015-17 Budget Proposal for K-12 Education”

Bob’s update and thought of the day.

Department of Public Instruction March - 2015 47

THANK YOU!

Questions? Contact Information (Area Code 608)

Bruce Anderson, Consultant 267-9707 Carey Bradley, Consultant 267-3752 Dan Bush, Consultant 267-9212 Karen Kucharz Robbe, Consultant 266-3464 Victoria Chung, Accountant267-9205 Brian Kahl, Auditor 266-3862 Gene Fornecker, Auditor 267-7882 Vacant, Auditor 267-9218 Debi Towns, Assistant Director 267-9209 Bob Soldner, Director 266-6968 School Financial Services http://sfs.dpi.wi.gov/