Embed Size (px)

Citation preview

# A d d i s T a x I n i t i a t i v e

ATI partner country inputs

Essa JallowDeputy Commissioner General and Commissioner Domestic Taxes,

Gambia Revenue Authority

Partner Country Input at ATI Meeting, 18 Feb 2018

Essa Jallow,

Deputy Commissioner General and Commissioner Domestic Taxes,

Gambia Revenue Authority

1. What are current and future challenges with regards to DRM in your country?

a. Large informal sector

b. Predominantly cash based economy

c. Inadequate human and technological capacity to handle telecoms and natural

resources sector

d. The need to review and modernize legislation

e. Poor compliance culture

2. What is your cou try’s strategic focus ith regards to further de elopi g your DRM syste ?

a. Consolidate gains realized in the current Stategic Plan 2015-2019 such as human

capacity building, modernizing GRA infrastructure, data exchange between Tax and

Customs Departments, improving risk management, audit and taxpayer services,

strengthen capacity in the natural resources and specialized sectors, invest in

technology and interface ASYCUDA++ with Gamtaxnet

b. Strengthen bilateral and multilateral cooperation to increase exchange of

information, experiences and to join the crusade to end BEPS which is a leading treat

to DRM on the African continent

3. How can the ATI contribute to leveraging your efforts in this respect?

a. To continue lobbying development partners on behalf of its members to increase

their technical assistance for the latter anchored on country specific TADAT Reports

and Strategic Plans which are aligned to the ATI Commitments

b. Ensure the implementation of the broadly agreed 2017/2018 ATI plan which

symbolizes our collective aspirations for improved DRM

c. Strengthen the dialogue and sharing of country experiences on DRM

# A d d i s T a x I n i t i a t i v e

ATI partner country inputs

Marine KhurtsidzeMinistry of Finance, Georgia

International Taxation Division

Ministry of Finance of Georgia

February, 2017

Achievements of Georgia

In 2017 doing Business ranks Georgia 16th place in the world.

The index of economic freedom of the Heritage Foundation ranks

Georgia 13th.

The Rule of Law Index published under the World Justice Project in

2016 ranks Georgia as the leader country in the Eastern Europe and

Central Asia.

•

Tax System of Georgia 2

Challenges In Georgia

Implementation of BEPS project

Addressing TADAT ASSESSMENT

Tax System of Georgia 3

Action 5

Harmful Tax Practice

Action 6

Prevention of Treaty Abuse

Action 13

Country-by- Country Reporting

Action 14

Dispute Resolution

Georgia and BEPS project

On June 16 2016, Georgia became an associate member of the

inclusive framework for the implementation of the BEPS package

(minimum standards).

This became a unique opportunity for us to work closely with OECD

and G20 member states on equal footing in respect of shaping and

implementation of BEPS outcomes in order to tackle tax avoidance

efficiently.

As a BEPS associate Georgia undertook the

obligation to implement BEPS minimum

standards in timely manner.

Tax System of Georgia 4

Georgia is an elected

member of the Steering

Group of IF, composed of

22 member jurisdictions

and chaired by Germany.

Implementation of BEPS Minimum Standards

Harmful Tax Practices – BEPS Action 5In 2017, preferential tax regimes existing in Georgia have been

reviewed by the FHTP against the compliance with the Action 5 minimum

standards.

• ა ა ა• აე აშ ა ა ა

Tax System of Georgia 5

•Potentially harmful but not actually harmful

•Out of scope for FHTP purposes

•Out of scope for FHTP purposes

•Potentially harmful but not actually harmful

International Financial Company

Free Industrial

Zone

Virtual Zone Person

Special Trade Company

Implementation of BEPS Minimum Standards

Prevention of Treaty Abuse – BEPS Action 6

On 7 June 2017, together with 70 Ministers and other

high-level representatives Georgia signed the Multilateral

Convention to Implement Tax Treaty Related Measures to

Prevent Base Erosion and Profit Shifting

("Multilateral Instrument" or "MLI").

Following our international tax policy line, 34 out of 54 active treaties will bemodified under the MLI, upon the conclusion of domestic proceduresrequired to bring the instrument into effect.

With respect to the remaining jurisdictions, Georgia will be working closelywith them on a bilateral basis.

Georgia will be reviewed under Action 6.

Tax System of Georgia 6

Implementation of BEPS Minimum Standards

Transfer Pricing and County-by-country reporting – BEPS Action 13

On 30 June 2016 in the framework of the first meeting of the Inclusive Framework on

BEPS Georgia signed the Multilateral Competent Authority Agreement on the

Exchange of Country-by-Country (CbC) Reports. Currently Georgia is in the process

of implementation of the CbC Reporting.

Peer review process of Georgia is scheduled.

Mechanisms for Improved Dispute Resolution – BEPS Action 14

The Peer Review of Georgia on Action 14 - Mutual

Agreement Procedures (MAP) is scheduled for 2020.

Tax System of Georgia 7

In May 2017, Georgia

was elected as a

member of the FTA

MAP Forum Steering

Group.

Global Forum on Transparency and Exchange of Information

Global Forum for Transparency and Exchange of Information for Tax Purposes

On April 11, 2011 Georgia became a member of the GlobalForum on Transparency and Exchange of Information for TaxPurposes

In 2013 Global Forum has launched a peer review of Georgia. Asa result of a three-year assessment, it has been recognized thatGeorgia’s legal and regulatory framework, as well as practice forexchange of information is line with international standards ontransparency and exchange of information for tax purposes.Georgia has been granted a rating – Largely Compliant.

In 2017-2018 Global Forum is launching new phase of reviews oflegal and regulatory practice in the framework of 2016 GlobalForum methodology. Georgia’s assessment is scheduled for 2020.

8

Tax System of Georgia 9

In 2016 TADAT assessment was conducted by IMF

Georgia Revenue Service has been working on addressing the

shortcomings identified by TADAT assessment

Some of the weaknesses have already improved

- Introducing simplified value-added tax (VAT) refund process

- analysis and prioritization of debt and write-off of uncollectible debt

Actively working on improvement of other identified areas - GRS

Strategic Plan 2017-2020

TADAT Assessment

Thank you for your attention!

Mari Khurtsidze - Head of International Taxation Division

Tax System of Georgia 10

# A d d i s T a x I n i t i a t i v e

ATI partner country inputs

Daniel Nuer Head of Tax Policy Unit, Ministry of Finance, Ghana

Partner Country Input at ATI Meeting, 18 Feb 2018

Daniel Nuer,

Head of Tax Policy Unit,

Ministry of Finance, Ghana

FOCUS

1. To use revenue policy to support production

2. To build a reliable database

3. To enhance revenue mobilisation through improved compliance instead of introducing

new taxes.

2017 Activities

1. Underwent TADAT

2. Underwent Post-TADAT review on policy and administration with IMF TA.

3. Rolled out tripsTM Domestic tax revenue administration software to 57 GRA offices

4. Commenced review of import exemptions regime

5. Shortfall of 3.4% of targeted revenue even though about 17 lines of taxes were either

abolished or reduced.

2018 Focus

1. Joint needs assessment with USAID to consolidate and synthesis TADAT and all other

Policy and Administration TA reports to develop a revenue policy and MTRS

2. To complete tripsTM roll out to ten outstanding offices and ensure usage of the system

3. To introduce tax amnesty to encourage filing of returns

4. To introduce an alternative independent arbitration mechanism for tax disputes.

5. To automate exemptions processing

6. Introduction of Fiscal Electronic Devices and Excise Tax Stamps to improve VAT and

Excise compliance.

7. To build a data warehouse to provide reliable data and for data matching and mining.

8. Passage of AEOI legislation to aid in tracking transactions of taxpayers completed.

Ghana will be ready to provide information from January 2019.

# A d d i s T a x I n i t i a t i v e

ATI partner country inputs

Elfrieda Stewart TambaCommissioner General, Liberia Revenue Authority

PCT Global Conference

on

Taxation and SDGs

Response to Questions

Elfrieda Stewart Tamba (Mrs.)

Commissioner General/CEO

Liberia Revenue Authority

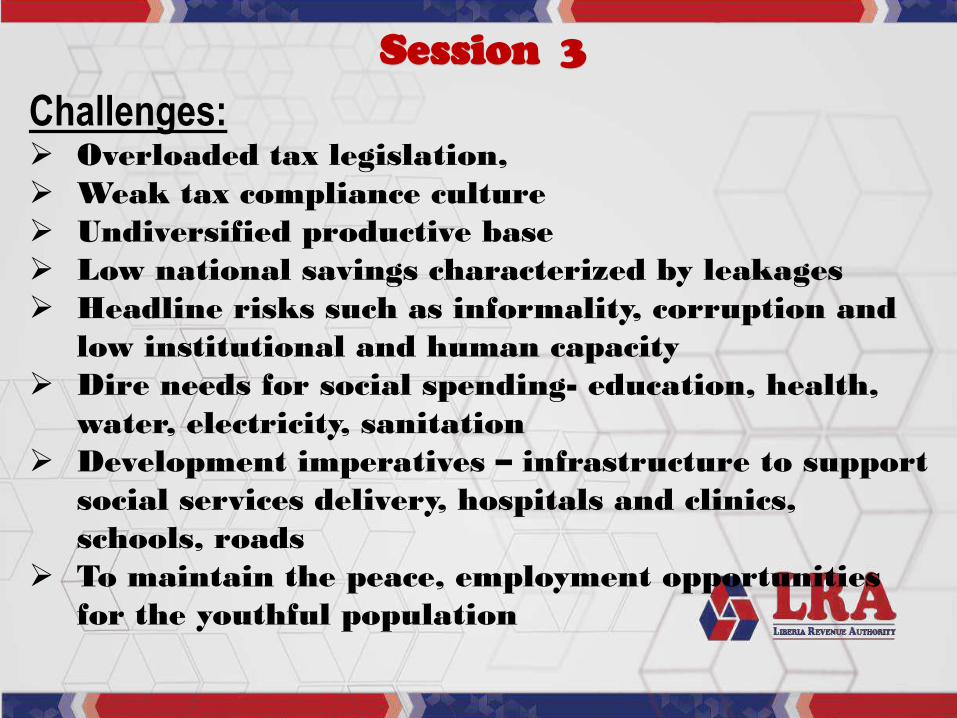

Session 3

1. Liberia has taken a major political set in successfully

transitioning with the elections of George Weah as

president and Madam Sirleaf winning the 2017 Mo Ibrahim

African Leadership Awards.

2. Key for the Weah’s Led Government is to develop a

successor National Development Agenda to address

couple of growing national concerns

Session 3

Challenges: Overloaded tax legislation, Weak tax compliance culture Undiversified productive base Low national savings characterized by leakages Headline risks such as informality, corruption and

low institutional and human capacity Dire needs for social spending- education, health,

water, electricity, sanitation Development imperatives – infrastructure to support

social services delivery, hospitals and clinics, schools, roads

To maintain the peace, employment opportunities for the youthful population

Addressing the problems (DRM Strategy)

1. Under the framework of SGDs target 17.1 and its attaining operational structures like

the ATI and most recently the PCT. LRA set forth DRM Strategy

Specific objective of the DRM Strategy Increase tax revenue for financing recurrent expenditure including education

and health services, public capital formation and first charge in emergencies;

Engender effective and efficient administration of taxes;

Grow private savings through financial deepening in the money and capital markets for public and private investment in the physical and human stocks for inclusive and poverty reduction;

Identify significant leakages in national savings and propose mitigating treatments;

Draw on synergies between domestic and foreign resources flows; and

Provide a strategic basis for setting national targets for measuring and monitoring SDG 17.1.

DRM Strategy (Major Tenants) Expanding the Tax Base and Minimizing Revenue

Loss

- E-registration, Tax law simplification, compliance and audit,

Others: Turning Discount Sectors into Premium Sectors

Taxing the informal sectorTaxing real estate sectorTaxing high wealth individuals

Closing Sources of Revenue LossTax expendituresCorruptionLow capacity in tax administrationCapital flight

DRM Strategy (Major Tenants)

Mobilizing Private Savings: Expand value chain and modernize agriculture, tourism and mining,

The Nexus between DRM and FRM (ODA, FDI, PI & Loans: Tackling illicit flows and issues around international taxation.

# A d d i s T a x I n i t i a t i v e

ATI partner country inputs

Amadou A. BadianeDirector of Tax Legislation and International Cooperation,

Direction Générale des Impôts et des Domaines, Senegal

Oumar Diop DiagneHead of Specialized Tax Audit Unit of Large Taxpayers Department,

Direction Générale des Impôts et des Domaines, Senegal

SENEGAL DRMMOBILISATION DES RESSOURCES DOMESTIQUES AU SENEGAL

Presented byAmadou A. Badiane | Oumar Diop Diagne

Director of tax Legislation| Head of Specialized Taxand International Cooperation | Audit Unit of Large Taxpayers

([email protected]) | Departement ([email protected])

CHALLENGESDEFI

● Increase tax efforts from 18%(2014) to 21% (2018) of GDPin order to finance economicdevelopment plan

● To alleviate public debtpressure

● To enhance tax justice and taxtransparence

● Hisser l'effort fiscal de 18 %(en 2014) à 21 % (en 2018) duPIB afin de financer le PlanSénégal Emergent

● Alléger le poids de la dettepublique

● Assurer l'équité et latransparence fiscales

CHALLENGES (continued)DEFI (suite)

● Prominence of undergroundeconomy

● Narrow and non diversified taxbase (mainly, telecommunica-tion and finance sectors)

● Costly tax expenditures (≈7%of GDP)

● Difficulties in tracking sometechnical activities(telecommunication, finance,extractive sectors, etc.) oroperations (transfer pricing,treaty abuse, etc.)

● Dominance de l'économieinformelle

● Dépendance vis-à-vis dequelques secteurs (télécoms,finance, etc.)

● Poids des dépenses fiscales(≈7% du PIB)

● Difficultés de maîtrisetechnique de certains secteurs(Télécoms, finances, mines,pétrole, etc.) ou opérations(prix de transfert, usage abusifdes conventions fiscales, etc.)

STRATEGIC FOCUSAXES STRATEGIQUES

● To get tax base under controland to secure a more resilientGov't revenue

● To simplify tax rules whilekeeping them in phase ofmodern economy

● To increase tax conscent

● To keep tax burden balancedover taxpayers

● Reduce tax expenditures cost

● Automation of procedures

● Maîtriser l'assiette et rendreles recettes de l'Etat plusrésiliante aux chocs

● Simplifier les règles tout en lesrendant en phase avecl'économie moderne

● Améliorer le consentement àl'impôt

● Mieux répartir la charge fiscaleentre les contribuables

● Rationaliser les dépensesfiscales

● Automatisation des procédures

WHAT AND HOW ATI SUPPORT SENEGAL?EN QUOI ET COMMENT l'ATI PEUT AIDER LE SENEGAL ?

● I. Capacity Building (in bothhuman and technicalresources)

● More tax personnel

● Better skilled personnel ...

● ... in particular in some sectorsthat have great tax revenuepotentials : telecommunication,financial sectors, extractiveindustry, etc.

● I. Renforcement des capacitéshumaines et techniques

● Plus de personnel

● Mieux formé ...

● ... notamment dans domainesà fort potentiel de recettes :télécoms, finance, industriesextractives, etc.

WHAT AND HOW ATI SUPPORT SENEGAL?EN QUOI ET COMMENT l'ATI PEUT AIDER LE SENEGAL ?

● Transfer pricing, includingaccess to and use ofcomparables

● Treaty negociation andprotection against treatyshopping

● Taxation of indirect transfer ofassets

● Prix de transfert, y comprisl'accès et l'utilisation de basesde données de comparables

● Techniques de négociation deconventions et lutte contrel'usage abusif des conventions

● Les cessions indirectes d'actifs

WHAT AND HOW ATI SUPPORT SENEGAL?EN QUOI ET COMMENT l'ATI PEUT AIDER LE SENEGAL ?

● II. Modernization of taxadministration: IT use

● III. Domestic and internationalexchange of information (Taxinformation data base andautomatic exchange)

● Etc.

● II. Modernisation des outils degestion : informatisation desprocédures

● III Echange national etinternational derenseignements (banque dedonnées fiscales et échangeautomatique)

● Etc.

Thank you Merci

ATI partner country inputs

Moses KaggwaAg. Director Economic Affairs

Ministry of Finance, Planning and Economic Development, Uganda

BRIEF ON THE DOMESTIC RESOURCE MOBILIZATION INITIATIVE

IN UGANDA

I. BACKGROUND

For the past few decades, Uganda has struggled to surpass a tax-to-GDP ratio of

14%, short of the medium-term target of 16% and lagging behind both Sub-

Saharan African and East African peers. This suggests significant untapped

potential and Uganda now requires a stronger revenue strategy to finance much-

needed increases in public expenditure, particularly in infrastructure, to help

promote economic growth. Furthermore, Uganda requires improved domestic

resource mobilisation to safeguard fiscal sustainability, accommodate rising

interest payments, and reduce aid dependency.

The Ugandan government aims to increase the tax-to-GDP ratio by 0.5 percentage

points per year, to attain a level of over 16% by 2022/23. This is in line with the

objectives of the Second National Development Plan (SNDP II) and will bring

Uganda closer to the SSA average. In pursuit of this ambition, the government is

currently in the initial stages of a new effort to bolster revenue collection based on

the concept of a Medium-Term Revenue Strategy.

II. MEDIUM-TERM REVENUE STRATEGY

An MTRS consists of four interdependent components: (1) setting a revenue

mobilisation target, by building broad-based consensus within the country for

medium-term revenue goals linked to high-priority public expenditure, (2)

designing comprehensive tax system reform over a five-year time-frame, covering

tax policy and administration, (3) committing stead and sustained whole-of-

government political support to the reforms, and (4) securing adequate resourcing,

both domestically and from donors, as needed, including technical assistance, to

support the implementation. Developing such a strategy has the following benefits:

i. Provides a clearer picture of likely tax revenues and gives certainty to

taxpayers on the tax implications of their decisions and investments

ii. Helps to prioritize medium-term objectives and gives direction to

persistent tax capacity building efforts

iii. Institution building in tax administration is complex and requires

sustained effort over several years

iv. Provides the legal framework to support policy and administration

changes

v. Revenue strategies help to guide external support to where it is most

needed

vi. Provides security when countries suffer instabilities and uncertainties

Adopting an MTRS approach to frame tax system reform will increase the

likelihood of achieving the government’s revenue goals. Such a strategy helps the authorities to credibly commit to sustainable implementation of reform, moving

away from ad hoc reforms done in the pursuit of immediate revenue gains. It will

thus provide an important medium-term anchor, as well as a much more

coordinated approach to reform.

III. STATUS OF FORMULATION OF THE MTRS

The government of Uganda have undertaken the initial steps to adopt an MTRS

approach to tax reform. The Ministry of Finance has established a Domestic

Resource Mobilisation Working Group with senior officials from the Ministry and

the Uganda Revenue Authority, as well as representatives from Development

Partners, including the World Bank Group, USAID, DFID, the IMF, the EU, KFW,

and the IGC. The Ministry of Finance anticipates expanding stakeholder

engagement further to include civil society organisations, key private sector agents,

and other arms of government after the initial drafting process. The overall

objective is to include the drafting process by the end of the Financial Year

2017/18, for implementation from the Financial Year 2018/19.

Thus far, the following steps in the development of the MTRS have been

undertaken:

i. Completed a stock-take of existing technical assistance reports and

analytical work to review recommendations

ii. Introduced internationally-used revenue mobilisation diagnostic tools,

including TADAT and the VAT Gap analysis

iii. Identified focus areas and key challenges to Uganda’s DRM efforts

iv. Identified further diagnostic studies to aid in the identification of

challenges, particularly on ICT infrastructure, Customs Administration,

and an Institutional Assessment

v. Completed a draft matrix of challenges and recommendations, which

was presented to the DRM Working Group for initial comments

Informed by this process, the Secretariat drafting the MTRS has adopted a three-

pronged approach to identifying challenges and interventions for Uganda to

improve its revenue effort: (1) repairing the tax policy, (2) strengthening the

revenue administration, and (3) widening the revenue base. Within each

component, key objectives and actions will be identified. The MTRS will

encompass some of the current reform efforts initiated by the MoFPED and URA,

but will also focus on areas that are currently not considered as central to the

mobilisation reform effort, but that the mission considers are key to achieving the

government’s stated objectives.

Towards a Medium Term Revenue Strategy (MTRS) for

Uganda

Presented by Moses Kaggwa, Ag. Director Economic Affairs

Ministry of Finance, Planning and Economic Development

#DoingMore

Uganda’s tax-to-GDP ratio has not surpassed 14%This places Uganda below many of both EAC and SSA peers. Reforms carried out in tax policy and administration have underpinned steady revenue increases, but a bigger effort is needed to meet targets.

9 February 2018 2

#DoingMore

A strong revenue strategy is needed to:

• Finance much-needed increases in public expenditure, particularly on infrastructure

• Encourage economic growth and reduce aid dependency

• Ensure fiscal sustainability

• Reduce the overall fiscal deficit from 3.5-4% of GDP to the target of 3%

• Accommodate rising interest payments

• Establish a robust non-resource revenue base before the onset of oil revenues

Uganda’s DRM hallengeTax Revenue and Overall Fiscal Deficit (% of GDP)

9 February 2018 3#DoingMore

Why a Medium Term Revenue Strategy • To provide a clearer picture of likely tax revenue and give certainty to taxpayers

on the tax implications of their decisions and investment

• Prioritize medium-term objectives and give direction to tax capacity building efforts

• Building tax administration capacity is complex and requires sustained effort over several years

• To provide the legal framework to support policy and administration changes

• Help guide external support to where it is most needed

• Provide security when in event of instabilities and uncertainties

• Build commitment and trust among a wide range of stakeholders

#DoingMore

Core elements of the proposed Medium Term Revenue Strategy• A broad consensus on revenue goals with due consideration to poverty and the

distributional implications of suggested measures

• Covers a 5 year time frame

• Comprehensive reform plan reflecting Uga da’s circu sta ces and the state of institutional capacity

• Changes to policy measures

• Reform of revenue administration

• Strengthening of the legal framework

• Commitment to steady and sustained implementation, notably political support

• Determining financing and technical assistance required to support Uganda in overcoming domestic constraints to formulation and implementation

9 February 2018 #DoingMore

Diagnostic framework for identifying gaps in DRM

Guidance from national planning

policies (NDP, SDG etc)

Revenue policy formulation

Revenue target setting

Quality assurance

Budget process (interaction with

expenditure programme)

Revenue collection strategy

Identification & registration

Return filing & declaration

Payment AuditDispute

resolutionData analysis &

reportingMonitoring &

evaluation

TAXPAYER SERVICES

OVERARCHING FACTORS

Institutional setting

Legal & regulatory framework

Human resource capacity

Political economy

Research & planning

Accountability &

transparency

Risk management

KEY FUNCTIONS

9 February 2018 6#DoingMore

• Reforms thus far have been erratic and unsustained

• The development of an MTRS can break the short-term focus of measures

• Improving the quality of Uga da’s ta systems is essential to economic growth and the achievement of SDGs

• An MTRS will help make more effective use of external support by promoting coordination among development partners

Development of an MTRS is urgent

9 February 2018 7#DoingMore

O je tives of Uganda’s MTRS• Ensure that the goal of increasing tax-to-GDP by 0.5 percentage

points per year, achieving a level of 16% by 2021/22, is achieved

• Build broad-based consensus on revenue goals

• Design comprehensive tax system reforms, encompassing policy, administration, and legal framework

• Break short-term focus and commit to steady and sustained reforms

• Secure adequate resourcing, domestically and from donors, including technical assistance, to support implementation

9 February 2018 8#DoingMore

Uganda’s MTRS pro ess• The Government of Uganda established a DRM Committee, including representatives

from the Uganda Revenue Authority, the World Bank Group, the EPRC, USAID, DFID, KFW, IMF, the EU delegation, and the IGC

• Methodology:

1. Completed a stock-take of existing technical assistance reports and analytical work to review recommendations

2. Introduced internationally-used revenue mobilisation diagnostic tools, including TADAT and the VAT Gap analysis

3. Ide tified focus areas a d ke challe ges to Uga da’s DRM efforts4. Completed further diagnostic studies, including an excise duty diagnostic, assessment

of URA customs systems, and an IMF mission to draft an MTRS framework

• Cross-cutting approach involves development partners, URA, and the TPD at all stages

9 February 2018 9#DoingMore

Way forward

• The secretariat presented a draft MTRS to the DRM Committee for consideration

• DRM Committee to review the draft and invite other stakeholders for debate

• Anticipated MTRS to be in place by June 30, 2018.

9 February 2018 10#DoingMore