Embed Size (px)

Citation preview

1Oando PLC

Developing Domestic Gas Infrastructure...a private sector approach

The Nigerian Infrastructure Summit

Transcorp Hilton, Abuja

6th -8th August 2008

Wale Tinubu

2

Outline

1.0 Background

• Nigerian Gas Industry

2.0 Current Realities / Challenges

• Funding and Infrastructural Issues

• Government Intervention

3.0 Practical Way Forward

• A suggested revised path

4.0 Role of private enterprise such as Oando

3

Background

• Nigeria, has the world’s 7th largest proven reserves of gas with 182 TCF already discovered

– The gas is rich in natural gas liquids and have little or no sulphur

• Over the years, there has been a steady growth in reserves with recent discoveries coming from the deepwater basin

• To date, all gas discoveries in Nigeria have been incidental; resulting from the search for oil

– There is a significant potential for reserves growth with focused gas exploration

– The reserve potential has been put at up to 600TCF which will make Nigeria the 4th largest gas reservoir after Russia, Iran and Qatar

• Nigeria currently flares 35 - 39% of total gas exports

– Put another way, the gas flared in Nigeria is sufficient to generate 15GW of electricity; this in a country with 6GW of installed and only 3GW of available power generation.

4

Nigeria’s Gas Sector is predominantly government-controlled

• Government is the dominant gas resource owner but has limited operatorship

– Most of the production is by Major Oil Companies which although are about 60 % owned by NNPC are commercially driven

• The export market is growing

– With train 6 now operational, NLNG’s capacity has reached 22MTPA

– Other LNG plants (Olokola and Brass) are under evaluation

– The West African Gas Pipeline Project is continuing apace and there is evidence of increasing demand

• The domestic demand is also growing

– The power sector reform and the attendant government funded Gas Power Plant developments of over 10GW is driving domestic demand

– Oil prices are driving up the cost of alternative fuels and industries are turning to gas where available

5

The government-led investment in domestic gas

infrastructure is no longer adequate

• The Escravos to Lagos Pipeline System (ELPS),

completed in the nineties is the main transmission

pipeline system dedicated to domestic consumption in

the country

– This pipeline system is the only source of supply to the

industrial and utility sectors of the domestic market

– ELPS also serves as the source of gas supply for the West

African Gas Pipeline System

– As with many other oil and gas facilities, repeated sabotage

of this and feeder systems has led to frequent supply

disruptions of recent

• The other major downstream pipeline systems are

dedicated to single projects leading to sub optimal

pipeline configurations

– These pipelines are mainly to export oriented projects and

cover areas already served by other single project

pipelines.

6

The private sector will feel the brunt of any long term gas

unavailability

• The dearth of investment in major domestic pipeline

infrastructure has lead to a short fall in the pipeline

capacities required to sustain the growing economy

• In addition, there is no pipeline connection between the

gas supply fields of the East and the growing markets of

the West and North.

– This has led to led to a shortage of gas availability for the

newly commissioned power plants in the Western parts of

the country

• Significant and Urgent pipeline Infrastructure has now

become imperative if the country is to benefit from the

gas resource

7

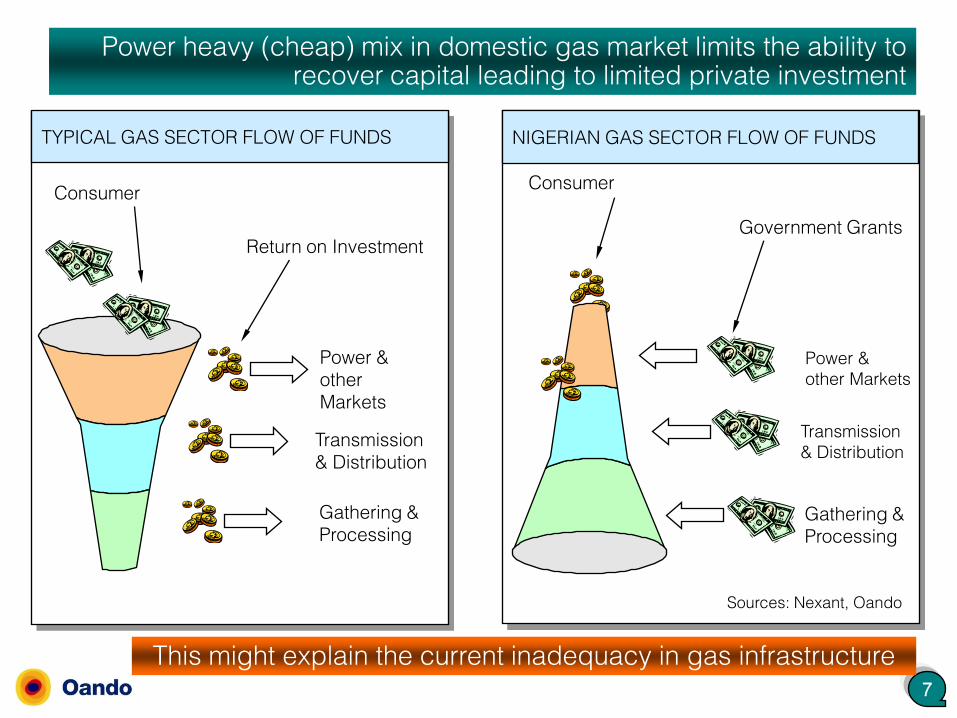

Power heavy (cheap) mix in domestic gas market limits the ability to recover capital leading to limited private investment

Power &

other Markets

Government Grants

Transmission

& Distribution

Gathering &

Processing

Consumer

NIGERIAN GAS SECTOR FLOW OF FUNDS

This might explain the current inadequacy in gas infrastructure

Sources: Nexant, Oando

TYPICAL GAS SECTOR FLOW OF FUNDS

Transmission

& Distribution

Gathering &

Processing

Power &

other

Markets

Return on Investment

Consumer

8

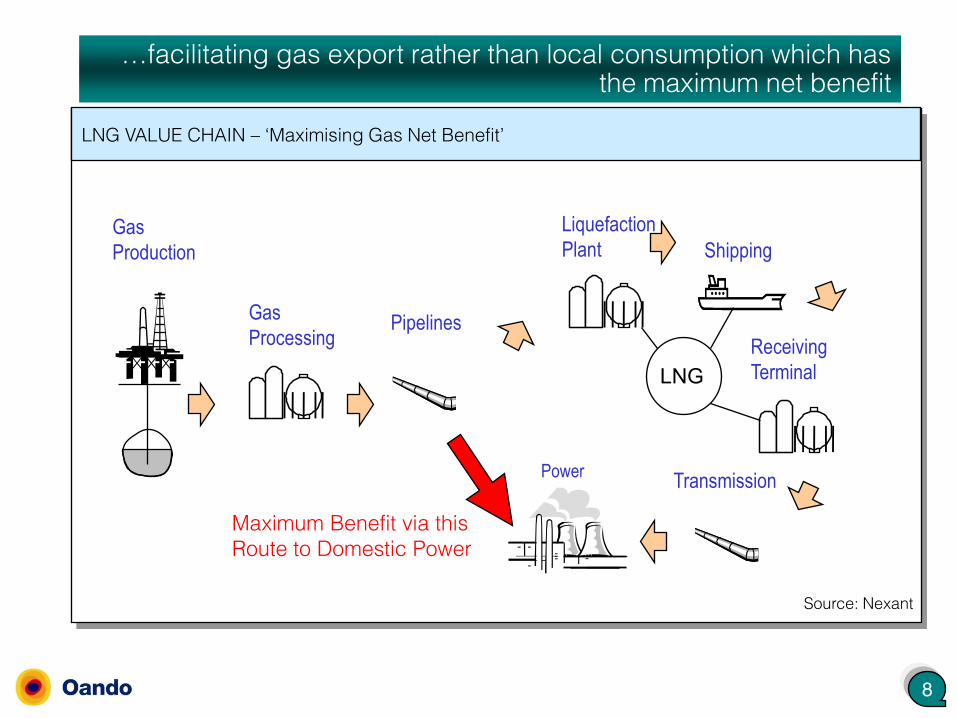

LNG VALUE CHAIN – ‘Maximising Gas Net Benefit’

PipelinesGas

Processing

Shipping

Power

Liquefaction

Plant

Receiving

Terminal

Gas

Production

LNG

Transmission

Maximum Benefit via this

Route to Domestic Power

Source: Nexant

…facilitating gas export rather than local consumption which has the maximum net benefit

9

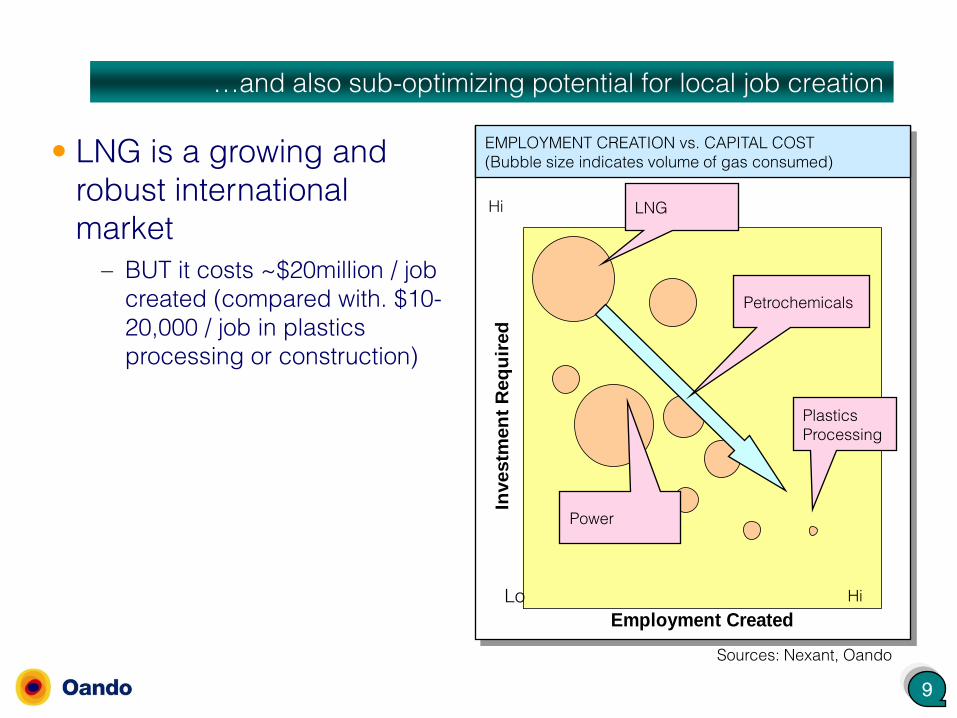

…and also sub-optimizing potential for local job creation

EMPLOYMENT CREATION vs. CAPITAL COST

(Bubble size indicates volume of gas consumed)• LNG is a growing and

robust international

market

– BUT it costs ~$20million / job

created (compared with. $10-

20,000 / job in plastics

processing or construction)

Employment Created

Investm

en

t R

eq

uir

ed

LNG

Petrochemicals

Plastics

Processing

Power

Sources: Nexant, Oando

HiLo

Hi

10

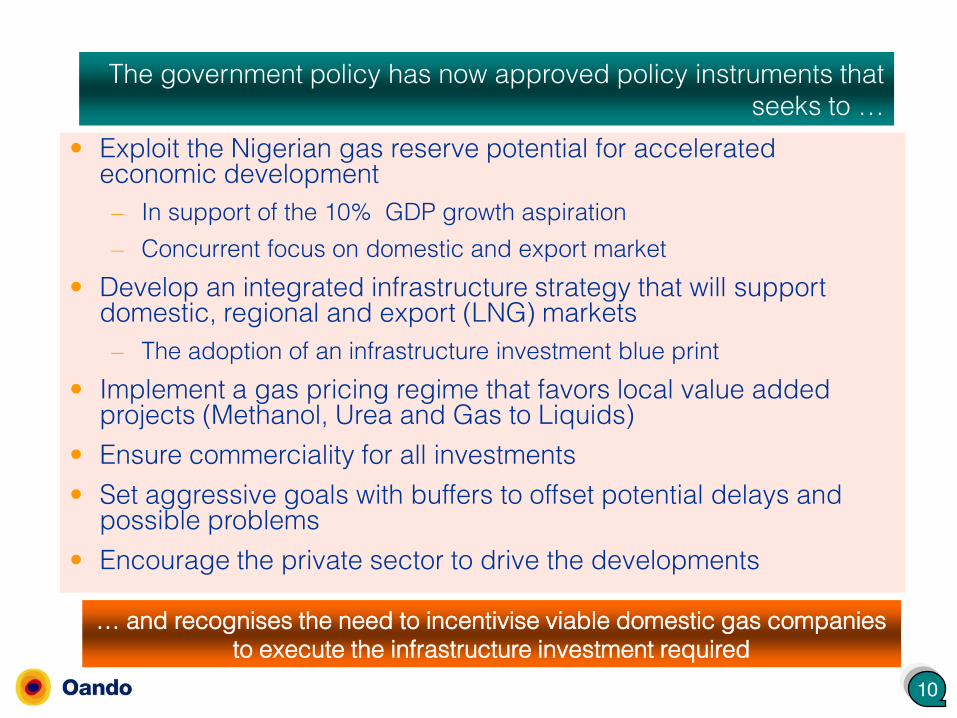

The government policy has now approved policy instruments that

seeks to …

• Exploit the Nigerian gas reserve potential for accelerated economic development

– In support of the 10% GDP growth aspiration

– Concurrent focus on domestic and export market

• Develop an integrated infrastructure strategy that will support domestic, regional and export (LNG) markets

– The adoption of an infrastructure investment blue print

• Implement a gas pricing regime that favors local value added projects (Methanol, Urea and Gas to Liquids)

• Ensure commerciality for all investments

• Set aggressive goals with buffers to offset potential delays and possible problems

• Encourage the private sector to drive the developments

… and recognises the need to incentivise viable domestic gas companies

to execute the infrastructure investment required

11

12

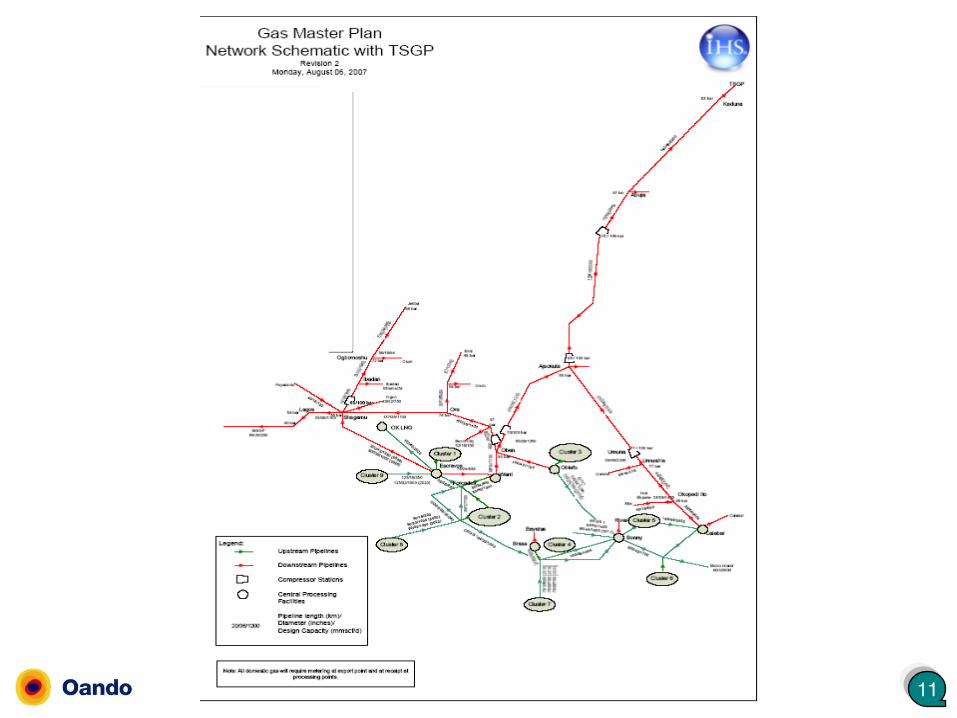

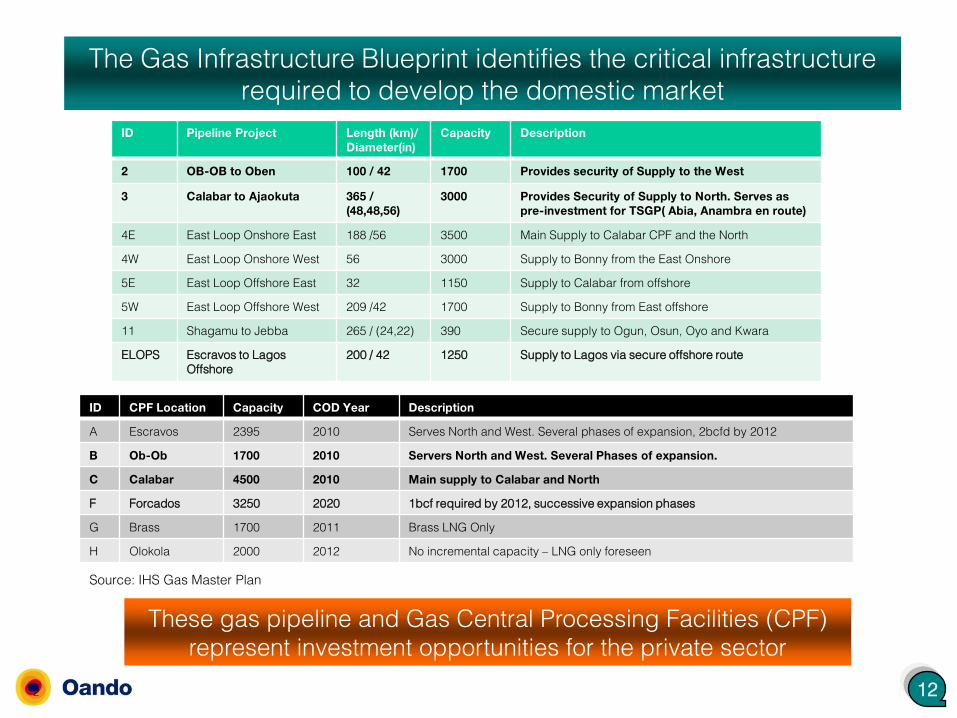

The Gas Infrastructure Blueprint identifies the critical infrastructure

required to develop the domestic market

2

ID Pipeline Project Length (km)/Diameter(in)

Capacity Description

2 OB-OB to Oben 100 / 42 1700 Provides security of Supply to the West

3 Calabar to Ajaokuta 365 / (48,48,56)

3000 Provides Security of Supply to North. Serves as pre-investment for TSGP( Abia, Anambra en route)

4E East Loop Onshore East 188 /56 3500 Main Supply to Calabar CPF and the North

4W East Loop Onshore West 56 3000 Supply to Bonny from the East Onshore

5E East Loop Offshore East 32 1150 Supply to Calabar from offshore

5W East Loop Offshore West 209 /42 1700 Supply to Bonny from East offshore

11 Shagamu to Jebba 265 / (24,22) 390 Secure supply to Ogun, Osun, Oyo and Kwara

ELOPS Escravos to Lagos

Offshore

200 / 42 1250 Supply to Lagos via secure offshore route

ID CPF Location Capacity COD Year Description

A Escravos 2395 2010 Serves North and West. Several phases of expansion, 2bcfd by 2012

B Ob-Ob 1700 2010 Servers North and West. Several Phases of expansion.

C Calabar 4500 2010 Main supply to Calabar and North

F Forcados 3250 2020 1bcf required by 2012, successive expansion phases

G Brass 1700 2011 Brass LNG Only

H Olokola 2000 2012 No incremental capacity – LNG only foreseen

These gas pipeline and Gas Central Processing Facilities (CPF)

represent investment opportunities for the private sector

Source: IHS Gas Master Plan

13

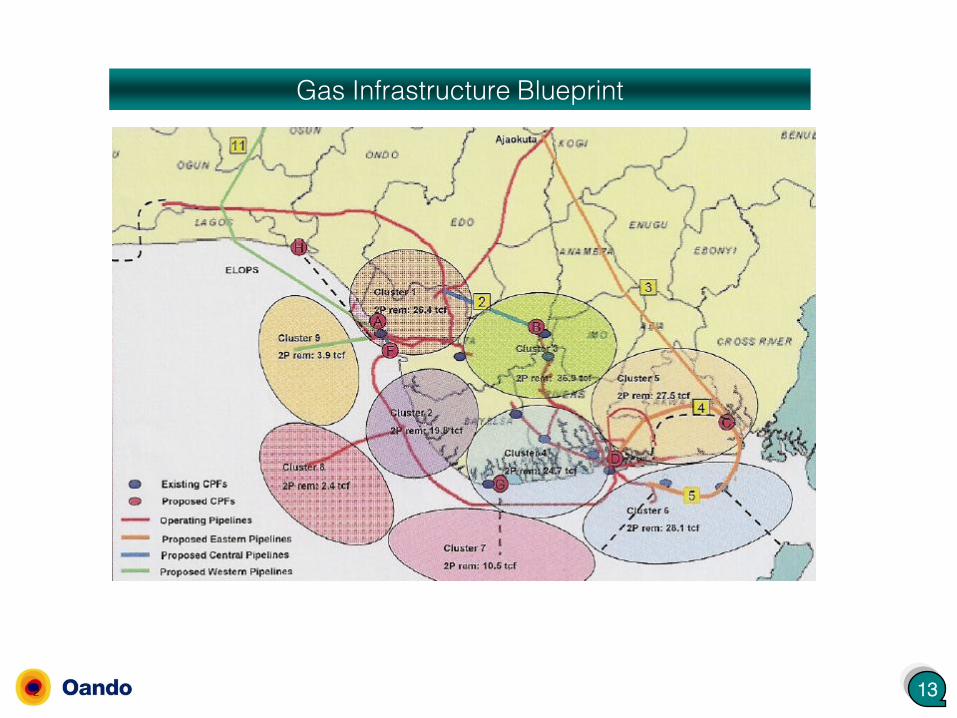

Gas Infrastructure Blueprint

2

14

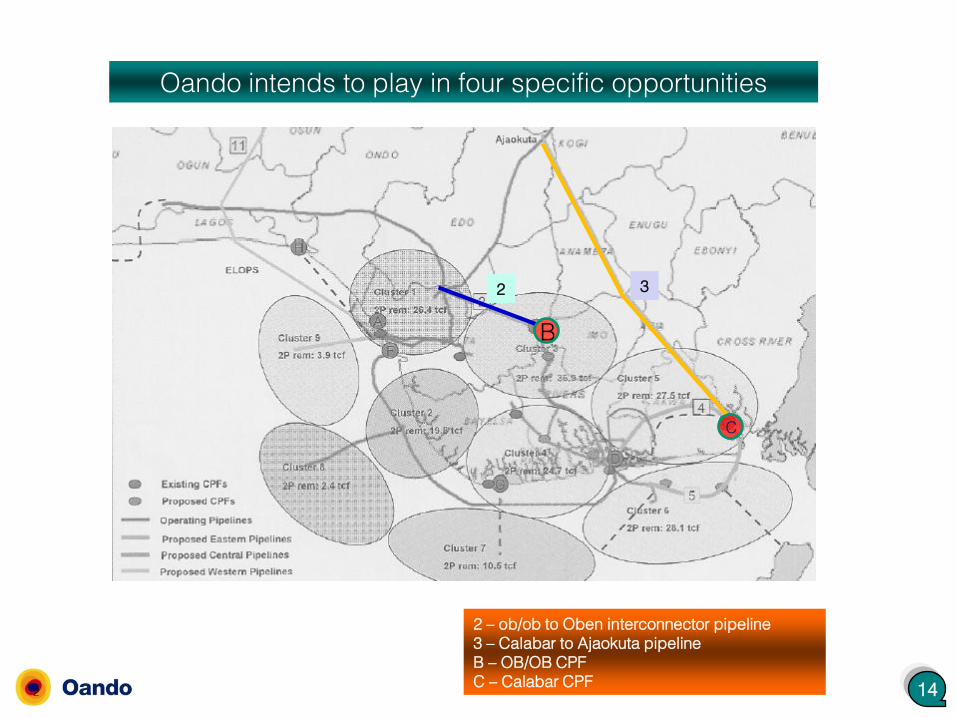

Oando intends to play in four specific opportunities

2

32

C

B

2 – ob/ob to Oben interconnector pipeline

3 – Calabar to Ajaokuta pipeline

B – OB/OB CPF

C – Calabar CPF

15

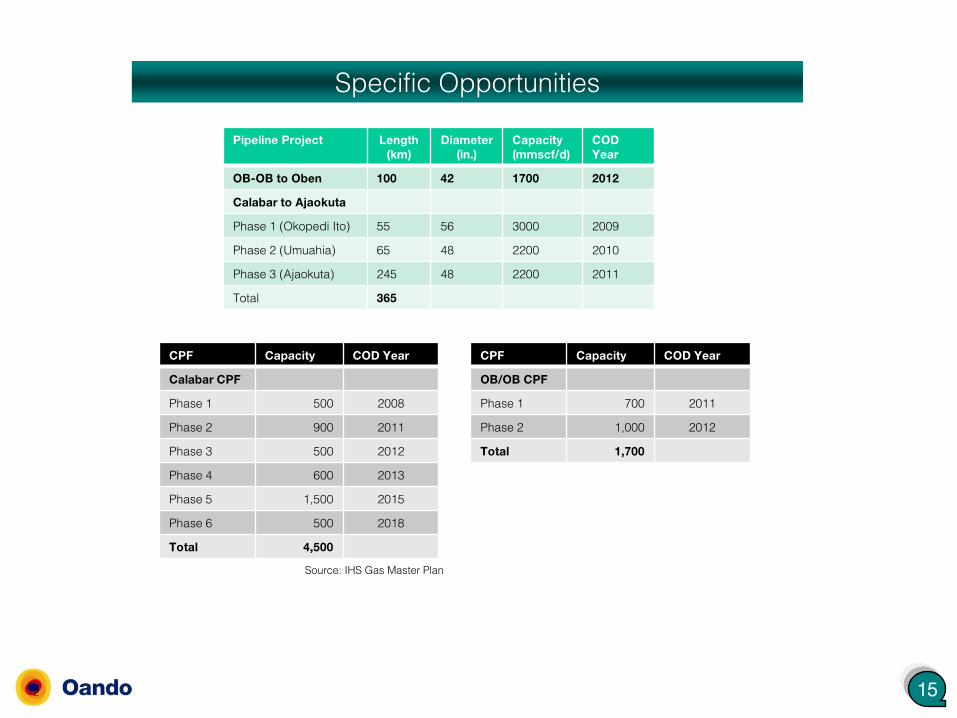

Specific Opportunities

2

Pipeline Project Length(km)

Diameter(in.)

Capacity(mmscf/d)

CODYear

OB-OB to Oben 100 42 1700 2012

Calabar to Ajaokuta

Phase 1 (Okopedi Ito) 55 56 3000 2009

Phase 2 (Umuahia) 65 48 2200 2010

Phase 3 (Ajaokuta) 245 48 2200 2011

Total 365

CPF Capacity COD Year

Calabar CPF

Phase 1 500 2008

Phase 2 900 2011

Phase 3 500 2012

Phase 4 600 2013

Phase 5 1,500 2015

Phase 6 500 2018

Total 4,500

Source: IHS Gas Master Plan

CPF Capacity COD Year

OB/OB CPF

Phase 1 700 2011

Phase 2 1,000 2012

Total 1,700

16

Oando Gas and Power – a local gas company

Oando has had an 8 year history of supplying gas to industries

in the Greater Lagos Area, the success of which is

demonstrated by the following achievements:

– Phased completion of a 99 km distribution network in Lagos

– The development of a 124km gas supply pipeline to the

Cement Plant in Calabar

– Plans include a city gate to supply gas to the Calabar

Industrial Area

– $156m (NGN18.7bn) of investment mobilized by Oando to

construct pipeline infrastructure

– The connection of over 90 industrial customers to the gas

network

Oando is gearing up to play a major role in the

development of the national gas grid

17

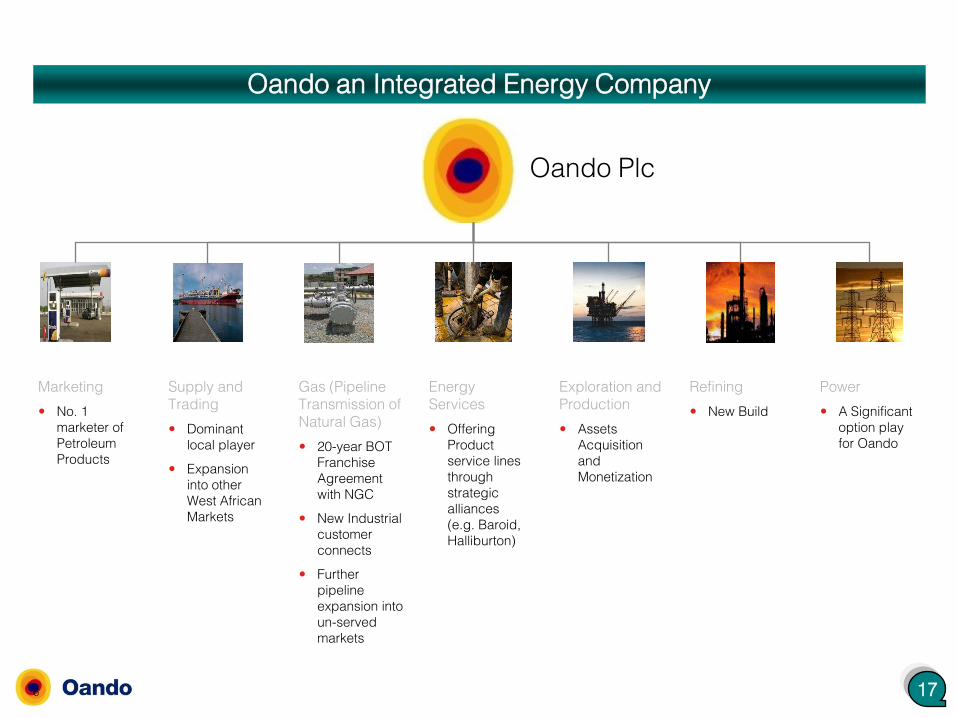

Oando an Integrated Energy Company

Oando Plc

Marketing

No. 1

marketer of

Petroleum

Products

Power

A Significant

option play

for Oando

Energy

Services

Offering

Product

service lines

through

strategic

alliances

(e.g. Baroid,

Halliburton)

Exploration and

Production

Assets

Acquisition

and

Monetization

Refining

New Build

Supply and

Trading

Dominant

local player

Expansion

into other

West African

Markets

Gas (Pipeline

Transmission of

Natural Gas)

20-year BOT

Franchise

Agreement

with NGC

New Industrial

customer

connects

Further

pipeline

expansion into

un-served

markets

6

18

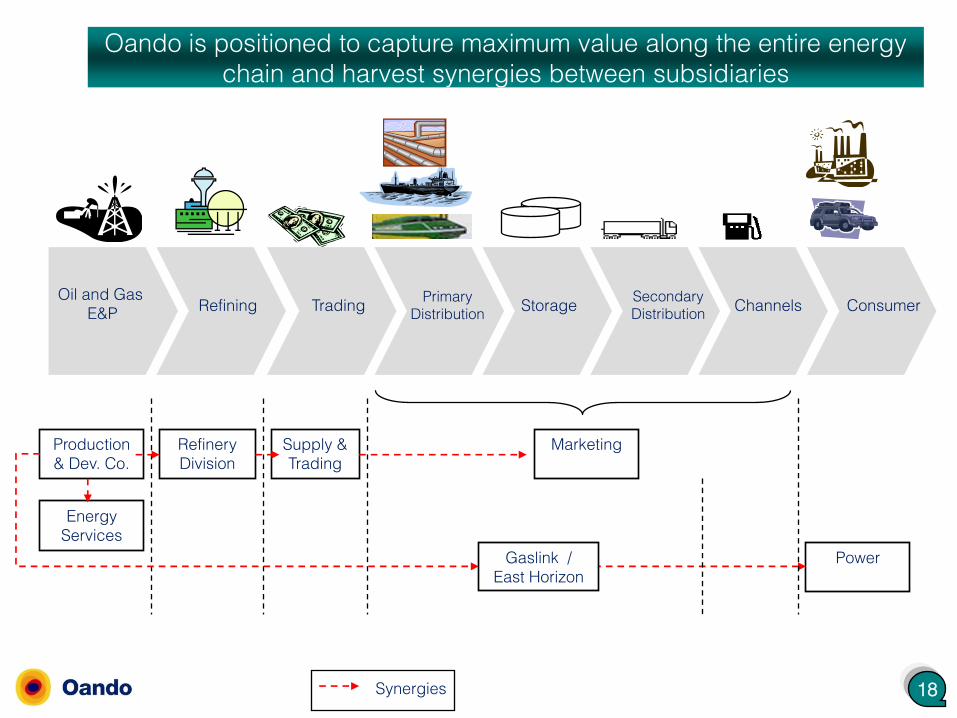

Oando is positioned to capture maximum value along the entire energy

chain and harvest synergies between subsidiaries

MarketingRefinery

Division

Production

& Dev. Co.

Energy

Services

Power

Supply &

Trading

Synergies

RefiningOil and Gas

E&PPrimary

DistributionConsumerStorage

Secondary

DistributionChannelsTrading

Gaslink /

East Horizon

196

Thank you

http://www.oandoplc.com