Embed Size (px)

Citation preview

Journal ofComparative Corporate Law and Securities Regulation 3 (1981) 373-391 175North-Holland Publisting Company

DEVELOPMENTS IN HARMONIZATION OF

ACCOUNTING STANDARDS

LeRoy J. Herbert

MR. HAWES: We are now going to shift gears a bit and talkabout special legal and accounting problems in multinational activity.The first talk in that field will be on the harmonization of account-ing standards, and the second will be about comparative disclosureand possibilities of harmonization in that area. We should listento Roy Herbert's discussion of accounting harmonization in order tosee what it portends for other kinds of harmonization, because cer-tainly the accountants have been at harmonization efforts as long asanyone.

1. HARMONIZATION

MR. HERBERT: The issue of harmonization of accounting stand-ards has received growing attention over the last decade. The pro-cess has been speeded up by a variety of interest groups, including(1) The users of financial statements. The impact of many companieson capital markets, commodity markets, on labor, etc., goes beyondnational borders. Information included in the financial statementsof these companies is, however, of only limited value to users inother countries if they are not familiar with the accounting standardsunderlying these statements.(2) International and multinational companies operating in severalcountries and having their shares quoted on several stock exchanges.These companies must comply with the different accounting rules andstandards applicable in countries in which they operate, which makestheir financial reporting increasingly difficult and costly.(3) Groups making efforts to harmonize accounting standards and com-pany-law in connection with a greater economic and political integra-tion of a given geographic area, e.g., the EEC.(4) Other national interest groups in various countries who are pri-marily interested in more stringent reporting requirements for inter-national companies, with the objective of exercising more controlover multinational companies.

As you can see from the background material that I have in-cluded as an Appendix to this Chapter, there are basically two dif-ferent types of international organizations working to harmonizeaccounting standards. First, there are the bodies organized by gov-ernments, such as the United Nations, the OECD, and the EEC. Second,there are the international organizations set up by independent pro-fessional accounting bodies, such as the International AccountingStandards Committee and the International Federation of Accountants.

I would like to concentrate for the next few moments on theefforts of, and problems encountered by, the two organizations thathave so far produced the most tangible results: the EEC and the In-ternational Accounting Standards Committee.

0378-7214/8110000-0000/S02.75 0 1981 North-Holland [ 3731

L.J. IHerbert / Hannonization of accounting standards

2. THE EUROPEAN ECONOMIC COMMJUNITY [EEC]

The EEC is striving to create a common market with a freeflow of capital, labor, and merchandise within its boundaries. Inthat context, company-law is being harmonized, and this involvesharmonization of company financial reporting. The vehicles for har-monization are directives issued by the Council of Ministers to beincorporated in national laws of the member states. The FourthDirective (on company accounts) was promulgated in 1978, and theSeventh Directive (on consolidated accounts) is in preparation.These directives have a significant impact on company reporting inthe member states (the Fourth Directive will affect more than 1.5million companies) and they are a considerable contribution toharmonization within, and probably outside, the EEC.

At the same time, the directives demonstrate the difficultiesencountered in the harmonization process. It took more than tenyears from the time that the Fourth Directive was first conceivedto its final approval. In order to achieve agreement between memberstates on a number of issues, options had to be allowed to memberstates in enacting their national legislation and also certain op-tions were left to companies. With such wide latitude given, theFourth Directive is more of a guideline than an agreed standard.The directive had to accept the fact that in some member states,financial statements are influenced by tax considerations, since inthose countries taxation is based on statutory accounts. Further-more, the Fourth Directive does not deal with all accounting issues,especially in the field of measurement. For example, there isnothing specific in it on translation of foreign currencies, on ac-counting for the effects of changing prices, or on deferred taxation.

It is expected that with the passage of time the gaps willbe filled and the options will gradually be reduced. For the timebeing, however, financial statements of companies operating in dif-ferent countries in Europe will still differ significantly. As anexample, the proposed new national accounting legislation in Germany,resulting from the Fourth Directive, is likely to leave German com-panies out of line with other European and international practicesin several key areas. (1) German company accounts will continue toincorporate tax-based rather than commercial valuations. (2) Con-solidation will continue to be required on a domestic basis only,although this will change when legislation to comply with the EEC'sSeventh Directive is introduced. (3) It is expected that Germanywill continue to adopt a hostile approach to any form of accountingfor changing prices, and the government will not propose the enabl-ing legislation which would make inflation accounting compatiblewith the Fourth Directive.

3. INTERNATIONAL ACCOUNTING STANDARDS COmMITTEE [IASC]

Compared to the EEC the IASC has undertaken an even biggertask--the harmonization of accounting standards on a worldwide basis.The IASC was formed in 1973 by the leading accounting bodies of tencountries: Australia, Canada, France, Germany, Japan, Mexico, TheNetherlands, the U.K., Ireland, and the U.S. Today it representsfifty-nine professional accounting bodies in forty-seven countries.Its objectives are "to formulate and publish, in the public interest,standards to be observed in the presentation of audited financialstatements and to promote their worldwide acceptance."

L.J. Herbert / Harmonization of accounting standards

So far the IASC has issued thirteen Accounting Standards andsix Exposure Drafts. A number of additional topics are presentlyunder study. The standards are similar in format to the pronounce-ments issued by the Financial Accounting Standards Board [FASB] herein the U.S., and they cover topics such as inventories, consolida-tion, contingencies, and income taxes. Due to the variety of ac-cepted accounting treatments worldwide, the international standardsare, in general, broadly phrased and they allow options, i.e., dif-ferent treatments for the same type of transactions.

Options are considered necessary in order to account fordifferences in economic conditions and for differences in nationalobjectives for financial reporting around the world. Obviously,when options are allowed they reduce the degree of uniformity infinancial reporting. As a result, the International AccountingStandards [IAS] represent an attempt to find common ground amongnational standards in areas where the standards of reporting arealready highly developed, as opposed to an effort to standardizefinancial reporting. The degree of harmonization greatly dependson the degree of compliance with the IAS.

In this regard it is important to consider the authority ofthe IAS. Within each country local regulations govern, to a greateror lesser degree, the issue of financial statements. The IAS pro-mulgated by the IASC do not override these local regulations. TheIASC pronouncements are somewhat in the nature of recommendationsand lack direct or supranational authority.

It was realized when the IASC was established that the IAScould not be imposed with the authority of law or of professionalrequirements; but it was hoped that compliance could be achieved byIASC member bodies influencing the business community. IASC memberbodies committed themselves to the support of the IAS, to the useof their best endeavors in persuading all parties concerned thatfinancial statements should comply with international standards, andto the requirement that auditors report non-compliance in their opin-ions. It now appears that these pressures are insufficient. TheIASC has realized that compliance with its standards is, in fact,poor.

There are a number of reasons for these unsatisfactory results.In some countries the profession is not, or is no longer, in controlof the standard-setting process--the FASB for example is not a memberof the IASC. In other countries the professional body has no powerto prescribe what auditors should state in their opinion; and in yetother countries, auditors are not allowed to say anything in theiropinions beyond what is required by law. So the road is obviouslymore difficult than it was thought to be in 1973.

In an effort to improve its standing and to increase the levelof compliance with its pronouncements, the IASC has approached theU.N. and the OECD with a suggestion for greater cooperation in thearea of standard setting. In addition, the IASC is trying to in-crease its liaison with national standard-setting bodies, and it iscalling on business interests, in particular the international andmultinational companies, to give more support to the work of theIASC by making reference to compliance with the IAS in their annualreports.

One result of the IASC's work which should be mentioned isthat many developing countries that have no established professionand no standards of their own are adopting the IAS as a nationalstandard. The harmonization of accounting standards in these areas

[375 1

L.J. Herbert / Hannonizatlion of accounting standards

is a significant step forward, but in the final analysis, full com-pliance with the IAS can be achived only if (1) the various profes-sional bodies in the industrialized countries of the world giveactive support to the quest for international harmonization ofaccounting standards, (2) governments support the recommendationsof the professional bodies and initiate the necessary legal changes,and last but not least, (3) the IAS enjoy the support of the inter-national business community.

4. FOREIGN CURRENCY TRANSLATION

I have identified certain of the efforts made so far and theproblems encountered by some of the organizations active in harmoniz-ing accounting standards. Next, I would like to discuss the latestdevelopments and some open questions relating to an important andcontroversial accounting issue: foreign currency translation.

Recent developments concerning foreign currency translationcan serve as a good example of a truly international effort tospeed up the harmonization process in a controversial area. In theU.S., the FASB has had its statement FASB No. 8 under review for thepast two years. Since FASB No. 8 was issued in 1975, the statementhas been criticized both by management of U.S. companies and by theaccounting profession. Although some accountants believe FASB No. 8is technically sound, many believe it produces unrealistic results.

Without going into technical details, FASB No. 8 is based onthe temporal method, which uses a mixture of historical and currentexchange rates for the translation of assets, liabilities, income,and expense items of foreign-based operations. The underlying as-sumption for the use of a mixture of exchange rates is that the unitof measurement for the performance of foreign-based operations isthe currency of the ultimate reporting entity, i.e., the U.S. dollar.As a result, in times of widely fluctuating exchange rates the per-formance of a foreign-based operation measured in U.S. dollars mayshow unsatisfactory results, although the performance reflected inthe local (foreign) currency financial statements is exceptionallygood--or vice versa.

During the time the FASB had its statement No. 8 under recon-sideration, the U.K. and Canadian institutes were also consideringthe issuance of standards on the subject. In 1980 a number of meet-ings were held among the FASB and the U.K. and Canadian institutesin order to exchange views on developments in each country and toexplore ways to achieve a degree of harmonization in the standardsto be published in each country. These meetinqs and what followedmarked a significant step forward toward achieving international har-monization. It was the first time, to my knowledge, that the stand-ard-setting bodies of these three countries (as contrasted with theIASC) had met with the objective of arriving at a common standard.

The exposure drafts that were issued by the FASB and the U.K.Accounting Standards Committee in October 1980 demonstrated thisintention to agree. These two proposals are considered to be similarin all important aspects, although there are some material differ-ences in the exceptions provided by the two drafts. Both draftsrequire the current-rate method; and for the U.S. this would be arevolutionary change from the presently applicable temporal methodunder FASB No. 8.

L.J. Iferbert /l lannonization of accounting standards

Canada and Ireland are presently holding back on issuance ofstandards, awaiting the outcome of these proposals in the U.S. andthe U.K. Should the U.S. and U.K. approve the proposed statements,the current-rate method would, in all probability, also be used byother countries influenced by the U.K. and the U.S.

5. THE INTERNATIONAL ACCOUNTING FIRMS

I shall close with a few remarks about the modus operandi ofthe major international accounting firms and about the role they canplay in the process of harmonizing accounting standards. With theirexperience in the multinational environment, members of these firmscan and do make significant contributions, either by participatingin or by commenting on the work of various organizations active inthe field of harmonization. In order to maintain a high profession-al standard throughout their worldwide practice, these firms encour-age their clients to adopt the highest standards for accounting andreporting procedures in their financial statements. In certainareas or countries where such standards are not stringent, however,the influence of the international accounting firms is limited.

The international financial press has suggested that inter-national firms should contribute to the upgrading of accounting andreporting standards by not allowing their names to be associated,without qualification, with financial statements that do not meetcertain minimum standards. In my view this suggestion is not fea-sible or practical because the firms cannot and should not attemptto move themselves into a quasi standard-setting position. Settingof standards is clearly the responsibility of the professional orgovernmental accounting bodies in the various countries--not that ofthe accounting firms themselves.

Furthermore, international firms cannot easily step out ofline with the legal and professional requirements of the countrywhere the financial statements are being drawn up. They are boundto observe the accounting and reporting standards required in eachcountry. Where there is an established local profession, the in-ternational firms are normally members of this group, and they mustfollow its conventions. A deterioration in relations with the localprofession could result in jeopardizing a firm's right to practicein the country or to practice in its own name.

The international firms can and will continue to make theircontributions to the harmonization process by participating invarious organizations, by rendering their professional expertise,and by using their best efforts to encourage their clients to domore on a voluntary basis.

MR. HAWES: The New York Stock Exchange says there are threehundred companies worldwide that would comply with its alternatelisting standards. Using those standards, would investors (and Iam talking of sophisticated analysts) have a problem comparing thosethree hundred companies today--any significant problem?

MR. HERBERT: If those companies are audited by what I referto as one of the major international firms, the investors would nothave a problem. I am not denigrating my professional colleagues inother countries. We have different standards; it is as simple asthat. But if the audit is performed according to some local account-

1377 1

L.J. Herbert / Hanonization of accounting standards

ing systems in those foreign countries, I strongly suggest that in-vestors should look very, very carefully at what is taking place.

Let me give you an example, without naming the country be-cause their representative is here and I do not want to get in anytrouble. We want to continue our practice in that country. A very,very major company--by any standard--employed us to perform an auditin one of the highly industrialized countries of the world becausethey were considering issuing securities through the Frankfurt mar-ket. We spent an enormous amount of time trying to do this engage-ment.

We came down to a relatively simple item called depreciationand we said, "Fellows, you have to take depreciation. That is thename of the game."

And they said, "Well, we had a bad year. Next year we aregoing to have a terrific year, and then you can take five times asmuch depreciation, but you cannot take it this year."

Now, I am not kidding when I tell you that we spent overseventy hours in partner time with the top management of this firm,trying to convince them that they had to take depreciation. In thefinal analysis we said, "If we cannot do it, then we are going toback off this engagement. We will not go ahead." That is the onlyway we got it done.

These were highly sophisticated businessmen in their owncommunity. They truly believed what they said, because that is theway it is done locally. They thought we were out of our minds,telling them that they must further depress earnings by putting inthis crazy thing called depreciation.

MR. HAWES: We will let Steve Friedman have the next question.

MR. FRIEDMAN: Granted the problems with harmonization, isthere a middle ground that would make financial statements preparedin different countries with somewhat different conceptual systemsuseful to investors without a full re-statement? Is there a way todevelop an explanation of differences in accounting treatment thatwould help investors interpret financial statements prepared in adifferent system, or are we on a thousand year journey?

MR. HERBERT: It may not be a thousand years, but it is along journey. The IASC is trying to do what you are describing.But think about it in reverse. Think about explaining LIFO inven-tories and its ramifications to people in a foreign country whonever heard of LIFO and do not have the slightest clue as to whatLIFO means. That is a difficult task. The financial press wouldsay it is simple: you can easily explain a thing like that. Ivery much disagree with their position. But to answer your questiondirectly, I think what you have described--that middle ground--isthe best we can hope for in any short-range period.

[3781

LJ. Herbert / Hannonization of accounting standards

APPENDIX XIII-A

ORGANIZATIONS ACTIVE IN SETTING INTERNATIONAL ACCOUNTING STANDARDS

United Nations (UN)

For many years the UN has been active in the field of internationalaccounting. An intergovernmental working group of experts was established inMay 1979. This group is composed of 34 representatives from the following areas:African States, 9 members; Asian States, 7 members; Latin American States, 6members; Western European and Other States (including the United States), 9 mem-bers; and Eastern European States, 3 members. The group was directed to researchfurther steps to be taken in the field of international standards of accountingand reporting and to formulate priorities. A report to the Commission on Trans-national Corporations is due in May 1981.

Organization for Economic Cooperation and Development (OECD)

The OECD, which is based in Paris, is the world's largest group of in-dustrialized countries and comprises 19 European countries, the United States,Canada, Japan, Australia, and New Zealand. Participation in this organizationis restricted to government representatives.

Based on the recommendations of a previous ad hoc working group, theOECD Committee on International Investment and Multinational Enterprisesestablished an apparently permanent working group on accounting standards.International business and labor interests, the IASC, and the Group of EuropeanAccountants are asked to participate in the work of this working group throughregular consultations. The objective of this group is to seek ways to energizeexisting activities in setting international accounting standards.

European Economic Community (EEC)

Based on a statement of the Council of Ministers of the EEC, one ofthe aims of the common market's industrial policy is the creation of a unifiedbusiness environment. This involves the harmonization of company law andtaxation, and the creation of a community capital market. The Fourth Direc-tive of the EEC Commission provides the framework for a common standard ofaccounting and reporting. It requires adoption by the EEC member countriesby 1982.

A revised Seventh Directive dealing with consolidated financial state-ments was recently proposed. Approval of this Directive by the Commission isexpected in 1981.

African Accounting Council (AAC)

The AAC was formed by 27 African countries in June 1979. Its objectivesare to assist in the establishment of bodies entrusted with accounting standardi-zation in African countries and to promote and carry out studies in the fieldof accounting standardization. This organization is still in the formative stage.

Asian Federation of Accountants (AFA)

The AFA was formed during 1977 jointly by the accountancy bodies ofIndonesia, Malaysia, the Philippines, Singapore, and Thailand. The objectiveof this organization is to improve professional standards in South East Asia.In 1979 the first in a series of accounting standards was issued by the Federa-tion. These standards deal with fundamental accounting principles.

[3791

L.J. Herbert /Harmionization of accounting standards

International Federation of Accountants (IFAC)

The IFAC is an organization of world accountancy bodies engaged indeveloping international auditing, educational, and ethical guidelines.International accounting standards are now issued by the InternationalAccounting Standards Committee (IASC), an organization independent of theIFAC. There is a possibility that IFAC and the IASC may merge and it is forthis reason that IFAC is included in this summary.

IFAC was formed in 1977 and started its operations in 1978. At January1981, the membership of IFAC comprised 76 accountancy bodies in 58 countries.The Federation has formed committees on the subjects of auditing, education,ethics, management accounting, planning, regional organizations, and a com-mittee to organize the 1982 International Congress in Mexico. The AuditingPractices Committee of the Federation has been authorized by the Council toissue guidelines on international auditing matters.

International Accounting Standards Committee (IASC)

The IASC was formed in 1973 by the leading accounting bodies ofAustralia, Canada, France, Germany, Japan, Mexico, The Netherlands, theUnited Kingdom and Ireland, and the United States. The Committee represents59 professional accountancy bodies in 47 countries. Its business is conductedby a board consisting of two representatives of each of the nine founder mem-bers and two representatives each from not more than two other member bodies.The IASC has the responsibility and authority to issue, in its own name, pro-nouncements on International Accounting Standards.

[380 1

LJ. Herbert / Harmonization of accounting standards

APPENDIX XIII-B

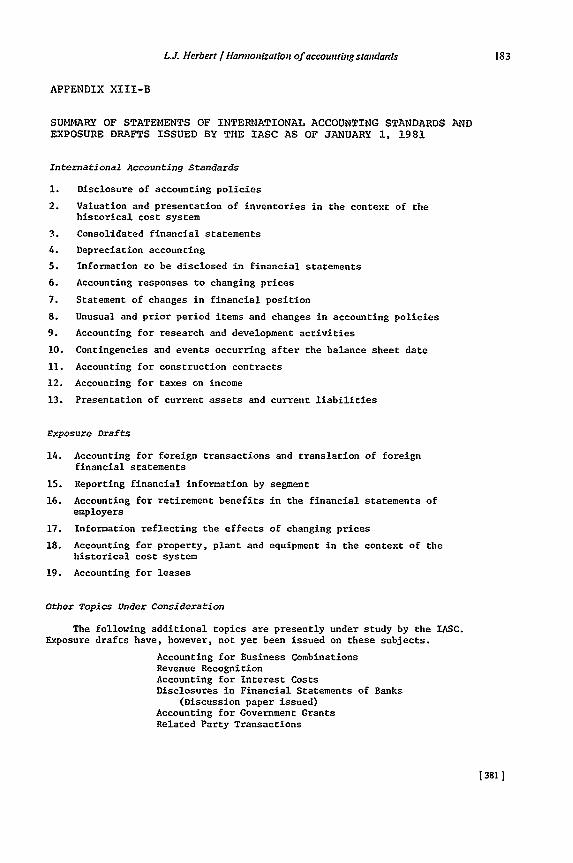

SUMMARY OF STATEMENTS OF INTERNATIONAL ACCOUNTING STANDARDS ANDEXPOSURE DRAFTS ISSUED BY THE IASC AS OF JANUARY 1, 1981

International Accounting Standards

1. Disclosure of accounting policies

2. Valuation and presentation of inventories in the context of thehistorical cost system

3. Consolidated financial statements

4. Depreciation accounting

5. Information to be disclosed in financial statements

6. Accounting responses to changing prices

7. Statement of changes in financial position

8. Unusual and prior period items and changes in accounting policies

9. Accounting for research and development activities

10. Contingencies and events occurring after the balance sheet date

11. Accounting for construction contracts

12. Accounting for taxes on income

13. Presentation of current assets and current liabilities

Exposure Drafts

14. Accounting for foreign transactions and translation of foreign

financial statements

15. Reporting financial information by segment

16. Accounting for retirement benefits in the financial statements ofemployers

17. Information reflecting the effects of changing prices

18. Accounting for property, plant and equipment in the context of thehistorical cost system

19. Accounting for leases

Other Topics Under Consideration

The following additional topics are presently under study by the IASC.Exposure drafts have, however, not yet been issued on these subjects.

Accounting for Business CombinationsRevenue RecognitionAccounting for Interest CostsDisclosures in Financial Statements of Banks

(Discussion paper issued)Accounting for Government GrantsRelated Party Transactions

13811

L.J Herbert / Harnionization of accounting standards

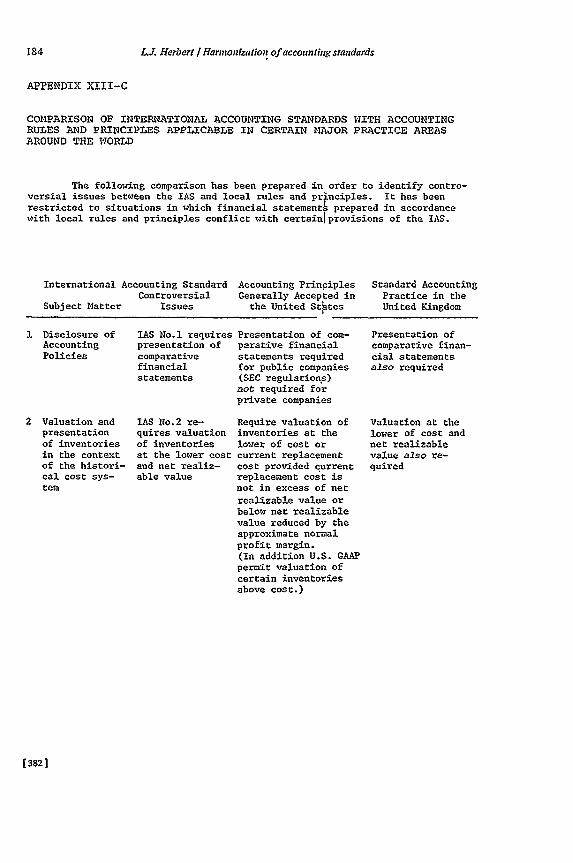

APPENDIX XIII-C

COMPARISON OF INTERNATIONAL ACCOUNTING STANDARDS WITH ACCOUNTINGRULES AND PRINCIPLES APPLICABLE IN CERTAIN MAJOR PRACTICE AREASAROUND THE WORLD

The following comparison has been prepared in order to identify contro-versial issues between the IAS and local rules and principles. It has beenrestricted to situations in which financial statement prepared in accordancewith local rules and principles conflict with certain provisions of the IAS.

International Accounting StandardControversial

Subject Matter Issues

Accounting Principles Standard AccountingGenerally Accepted in Practice in thethe United States United Kingdom

1 Disclosure ofAccountingPolicies

2 Valuation andpresentationof inventoriesin the contextof the histori-cal cost sys-tem

IAS No.1 requirespresentation ofcomparativefinancialstatements

IAS No.2 re-quires valuationof inventoriesat the lower costand net realiz-able value

Presentation of com-parative financialstatements requiredfor public companies(SEC regulations)not required forprivate companies

Require valuation ofinventories at thelower of cost orcurrent replacementcost provided currentreplacement cost isnot in excess of netrealizable value orbelow net realizablevalue reduced by theapproximate normalprofit margin.(In addition U.S. GAAPpermit valuation ofcertain inventoriesabove cost.)

Presentation ofcomparative finan-cial statementsalso required

Valuation at the

lower of cost andnet realizablevalue also re-quired

[3821

U-J. Herbert / Harmonization of accounting standards

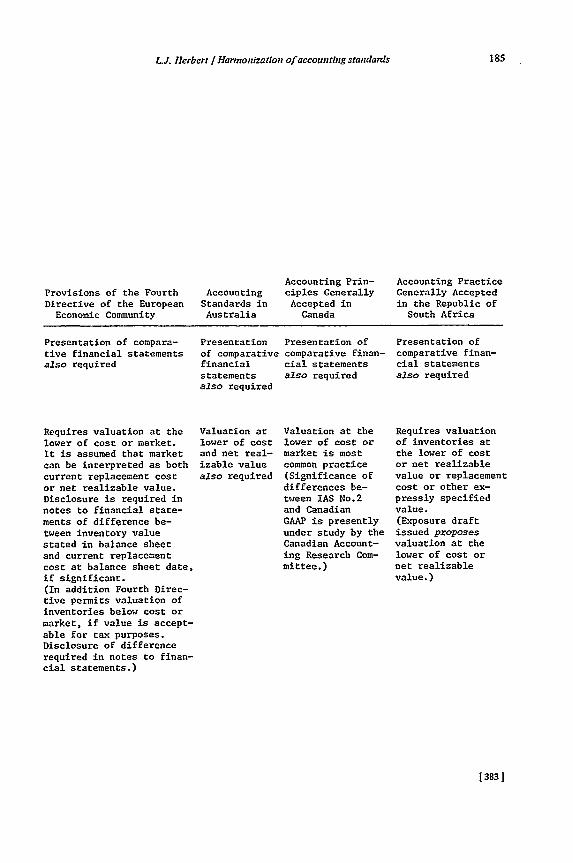

Provisions of the FourthDirective of the EuropeanEconomic Community

AccountingStandards inAustralia

Accounting Prin-ciples GenerallyAccepted in

Canada

Accounting PracticeGenerally Acceptedin the Republic ofSouth Africa

Presentation of compara-

tive financial statementsalso required

Requires valuation at thelower of cost or market.It is assumed that marketcan be interpreted as bothcurrent replacement costor net realizable value.Disclosure is required in

notes to financial state-ments of difference be-tween inventory valuestated in balance sheetand current replacementcost at balance sheet date,if significant.(In addition Fourth Direc-tive permits valuation ofinventories below cost ormarket, if value is accept-able for tax purposes.Disclosure of differencerequired in notes to finan-cial statements.)

Presentationof comparativefinancialstatementsalso required

Valuation atlower of costand net real-izable valuealso required

Presentation ofcomparative finan-cial statementsalso required

Valuation at thelower of cost ormarket is mostcommon practice(Significance ofdifferences be-tween IAS No.2and CanadianGAAP is presentlyunder study by theCanadian Account-ing Research Com-mittee.)

Presentation ofcomparative finan-cial statementsalso required

Requires valuationof inventories atthe lower of costor net realizablevalue or replacementcost or other ex-pressly specifiedvalue.(Exposure draftissued proposesvaluation at thelower of cost ornet realizablevalue.)

[ 3831

L.J. Herbert / Harmonization of accounting standards

International Accounting StandardControversial

Subject Matter Issues

Accounting PrinciplesGenerally Accepted in

the United States

Standard AccountingPractice in theUnited Kingdom

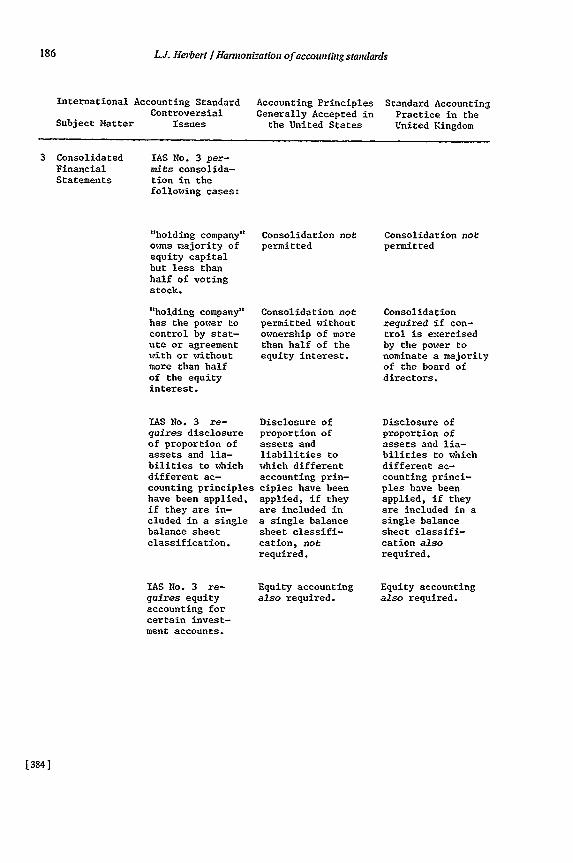

3 ConsolidatedFinancialStatements

IAS No. 3 per-mits consolida-tion in thefollowing cases:

"holding company"owns majority ofequity capitalbut less thanhalf of votingstock.

"holding company"has the power tocontrol by stat-ute or agreementwith or withoutmore than halfof the equityinterest.

Consolidation notpermitted

Consolidation notpermitted withoutownership of morethan half of theequity interest.

IAS No. 3 re- Disclosure ofquires disclosure proportion ofof proportion of assets andassets and lia- liabilities tobilities to which which differentdifferent ac- accounting prin-counting principles ciples have beenhave been applied, applied, if theyif they are in- are included included in a single a single balancebalance sheet sheet classifi-classification, cation, not

required.

IAS No. 3 re-quires equityaccounting forcertain invest-ment accounts.

Equity accountingalso required.

Consolidation notpermitted

Consolidationrequired if con-trol is exercisedby the power tonominate a majorityof the board ofdirectors.

Disclosure ofproportion ofassets and lia-bilities to whichdifferent ac-counting princi-ples have beenapplied, if theyare included in asingle balancesheet classifi-cation alsorequired.

Equity accountingalso required.

[384]

LJ. Herbert / Harmonization of accounting standards

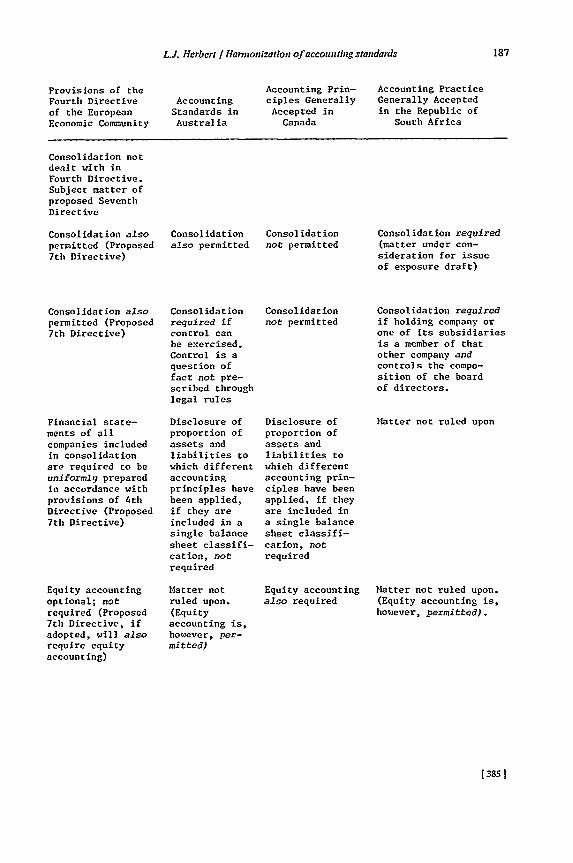

Provisions of theFourth Directiveof the EuropeanEconomic Community

AccountingStandards inAustralia

Accounting Prin-ciples GenerallyAccepted in

Canada

Accounting PracticeGenerally Acceptedin the Republic of

South Africa

Consolidation notdealt with inFourth Directive.Subject matter ofproposed SeventhDirective

Consolidation alsopermitted (Proposed7th Directive)

Consolidation alsopermitted (Proposed7th Directive)

Financial state-ments of allcompanies includedin consolidationare required to beuniformly preparedin accordance withprovisions of 4thDirective (Proposed7th Directive)

Equity accountingoptional; notrequired (Proposed7th Directive, ifadopted, will alsorequire equityaccounting)

Consolidationalso permitted

Consolidationrequired ifcontrol canbe exercised.Control is aquestion offact not pre-scribed throughlegal rules

Disclosure ofproportion ofassets andliabilities towhich differentaccountingprinciples havebeen applied,if they areincluded in asingle balancesheet classifi-cation, notrequired

Matter notruled upon.(Equityaccounting is,however, per-mitted)

Consolidationnot permitted

Consolidationnot permitted

Disclosure ofproportion ofassets andliabilities towhich differentaccounting prin-ciples have beenapplied, if theyare included ina single balancesheet classifi-cation, notrequired

Equity accountingalso required

Consolidation required(matter under con-sideration for issueof exposure draft)

Consolidation requiredif holding company orone of its subsidiariesis a member of thatother company andcontrols the compo-sition of the boardof directors.

Matter not ruled upon

Matter not ruled upon.(Equity accounting is,however, permitted).

[ 3851

L.J. Herbert / Harmonization of accounting standards

International Accounting StandardControversial

Subject Matter Issues

Accounting Principles Standard AccountingGenerally Accepted in Practice in the

the United States United Kingdom

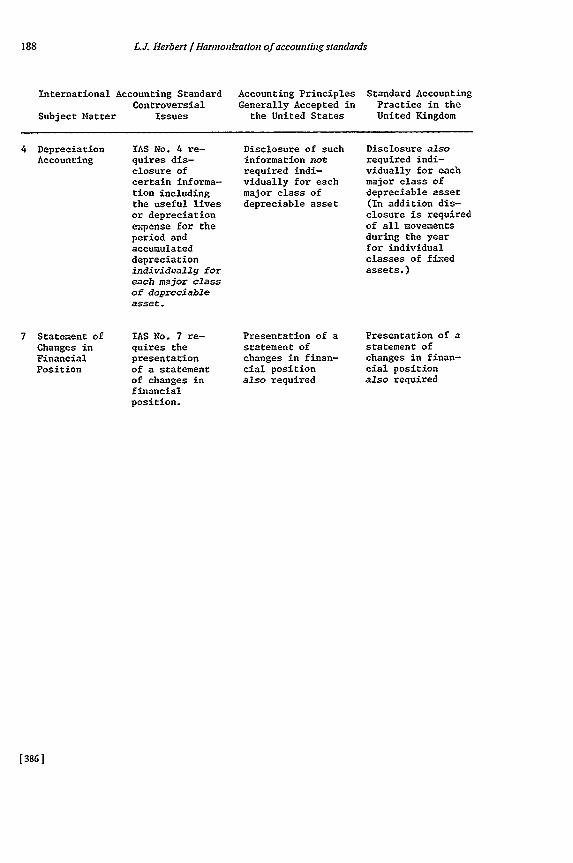

4 DepreciationAccounting

7 Statement ofChanges inFinancialPosition

IAS No. 4 re-quires dis-closure ofcertain informa-tion includingthe useful livesor depreciationexpense for theperiod andaccumulateddepreciationindividually foreach major classof depreciableasset.

IAS No. 7 re-quires thepresentationof a statementof changes infinancialposition.

Disclosure of suchinformation notrequired indi-vidually for eachmajor class ofdepreciable asset

Presentation of astatement ofchanges in finan-cial positionalso required

Disclosure alsorequired indi-vidually for eachmajor class ofdepreciable asset(In addition dis-closure is requiredof all movementsduring the yearfor individualclasses of fixedassets.)

Presentation of astatement ofchanges in finan-cial positionalso required

[3861

LJ. Herbert / Hannonization of accounting standards

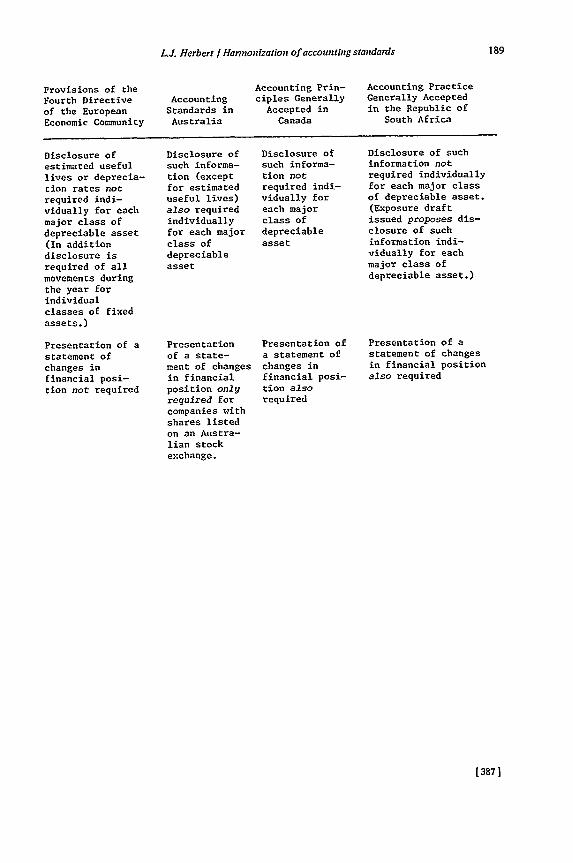

Provisions of theFourth Directiveof the EuropeanEconomic Community

AccountingStandards inAustralia

Accounting Prin-ciples GenerallyAccepted in

Canada

Accounting PracticeGenerally Acceptedin the Republic of

South Africa

Disclosure ofestimated usefullives or deprecia-tion rates notrequired indi-vidually for eachmajor class ofdepreciable asset(In additiondisclosure isrequired of allmovements duringthe year forindividualclasses of fixedassets.)

Presentation of astatement ofchanges infinancial posi-tion not required

Disclosure ofsuch informa-tion (exceptfor estimateduseful lives)also requiredindividuallyfor each majorclass ofdepreciableasset

Presentationof a state-ment of changesin financialposition onlyrequired forcompanies withshares listedon an Austra-lian stockexchange.

Disclosure ofsuch informa-tion notrequired indi-vidually foreach majorclass ofdepreciableasset

Presentation ofa statement ofchanges infinancial posi-tion alsorequired

Disclosure of suchinformation notrequired individuallyfor each major classof depreciable asset.(Exposure draftissued proposes dis-closure of suchinformation indi-vidually for eachmajor class ofdepreciable asset.)

Presentation of astatement of changesin financial positionalso required

[ 3871

L.J. Herbert / Hannonization of accounhing standards

International Accounting StandardControversial

Subject Matter Issues

Accounting PrinciplesGenerally Accepted in

the United States

Standard AccountingPractice in theUnited Kingdom

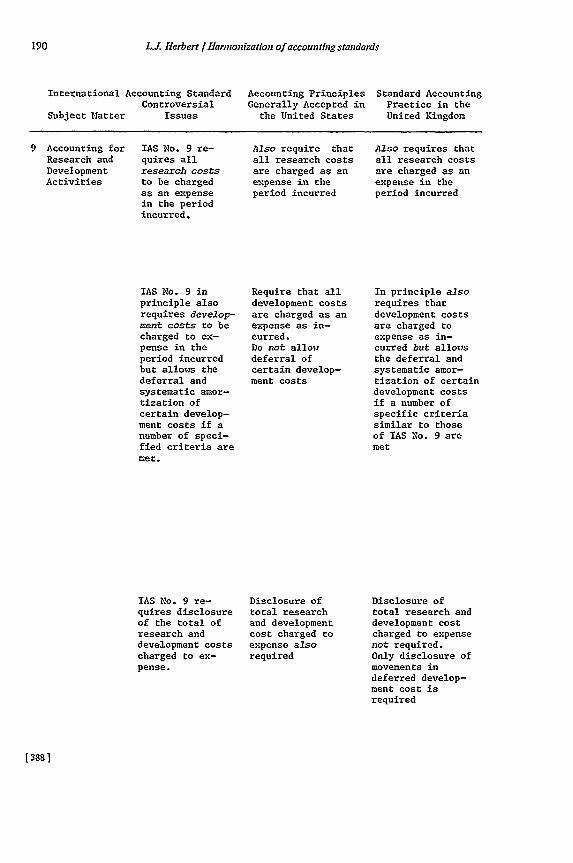

9 Accounting forResearch andDevelopmentActivities

IAS No. 9 re-quires allresearch coststo be chargedas an expensein the periodincurred.

Also require thatall research costsare charged as anexpense in theperiod incurred

Also requires thatall research costsare charged as anexpense in theperiod incurred

IAS No. 9 inprinciple alsorequires develop-ment costs to becharged to ex-pense in theperiod incurredbut allows thedeferral andsystematic amor-tization ofcertain develop-ment costs if anumber of speci-fied criteria aremet.

IAS No. 9 re-quires disclosureof the total ofresearch anddevelopment costscharged to ex-pense.

Require that alldevelopment costsare charged as anexpense as in-curred.Do not allowdeferral ofcertain develop-ment costs

Disclosure oftotal researchand developmentcost charged toexpense alsorequired

In principle alsorequires thatdevelopment costsare charged toexpense as in-curred but allousthe deferral andsystematic amor-tization of certaindevelopment costsif a number ofspecific criteriasimilar to thoseof IAS No. 9 aremet

Disclosure oftotal research anddevelopment costcharged to expensenot required.Only disclosure ofmovements indeferred develop-ment cost isrequired

[3881

L.J. Herbert / larmonization of accounting standards

Provisions of theFourth Directiveof the EuropeanEconomic Community

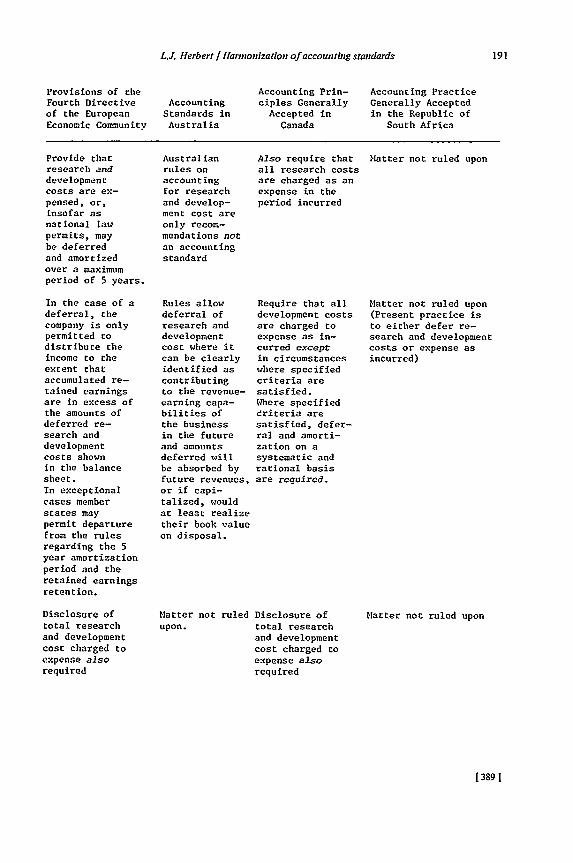

Provide thatresearch anddevelopmentcosts are ex-pensed, or,insofar asnational lawpermits, maybe deferredand amortizedover a maximumperiod of 5 years.

In the case of adeferral, thecompany is onlypermitted todistribute theincome to theextent thataccumulated re-tained earningsare in excess ofthe amounts ofdeferred re-search anddevelopmentcosts shownin the balancesheet.In exceptionalcases memberstates maypermit departurefrom the rulesregarding the 5year amortizationperiod and theretained earningsretention.

Disclosure oftotal researchand developmentcost charged toexpense alsorequired

AccountingStandards inAustralia

Australianrules onaccountingfor researchand develop-ment cost areonly recom-mendations notan accountingstandard

Rules allowdeferral ofresearch anddevelopmentcost where itcan be clearlyidentified ascontributingto the revenue-earning capa-bilities ofthe businessin the futureand amountsdeferred willbe absorbed byfuture revenues,or if capi-talized, wouldat least realizetheir book valueon disposal.

Accounting Prin-ciples GenerallyAccepted in

Canada

Also require thatall research costsare charged as anexpense in theperiod incurred

Require that alldevelopment costsare charged toexpense as in-curred exceptin circumstanceswhere specifiedcriteria aresatisfied.Where specifieddriteria aresatisfied, defer-ral and amorti-zation on asystematic andrational basisare required.

Matter not ruled Disclosure ofupon. total research

and developmentcost charged toexpense alsorequired

Accounting PracticeGenerally Acceptedin the Republic of

South Africa

Matter not ruled upon

Matter not ruled upon(Present practice isto either defer re-search and developmentcosts or expense asincurred)

Matter not ruled upon

[ 389 1

L. Herbert / Hannonization of accounting standards

International Accounting StandardControversial

Subject Matter Issues

Accounting PrinciplesGenerally Accepted in

the United States

Standard AccountingPractice in theUnited Kingdom

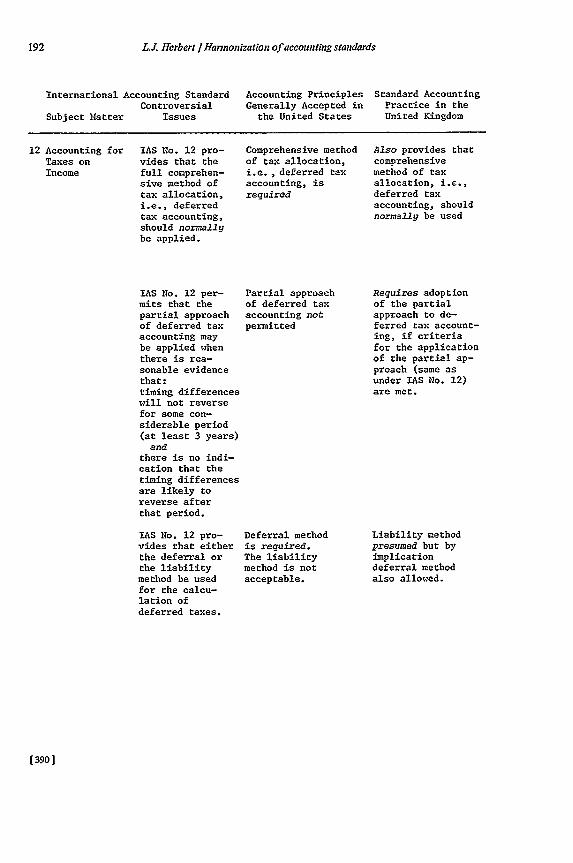

12 Accounting forTaxes onIncome

IAS No. 12 pro-vides that thefull comprehen-sive method oftax allocation,i.e., deferredtax accounting,should normallybe applied.

IAS No. 12 per-mits that thepartial approachof deferred taxaccounting maybe applied whenthere is rea-sonable evidencethat:timing differenceswill not reversefor some con-siderable period(at least 3 years)and

there is no indi-cation that thetiming differencesare likely toreverse afterthat period.

IAS No. 12 pro-vides that eitherthe deferral orthe liabilitymethod be usedfor the calcu-lation ofdeferred taxes.

Comprehensive methodof tax allocation,i.e., deferred taxaccounting, isrequired

Partial approachof deferred taxaccounting notpermitted

Deferral methodis required.The liabilitymethod is notacceptable.

Also provides thatcomprehensivemethod of taxallocation, i.e.,deferred taxaccounting, shouldnormally be used

Requires adoptionof the partialapproach to de-ferred tax account-ing, if criteriafor the applicationof the partial ap-proach (same asunder IAS No. 12)are met.

Liability methodpresumed but byimplicationdeferral methodalso allowed.

Li. Herbert / Harmonization of accounting standards

Provisions of theFourth Directiveof the EuropeanEconomic Community

AccountingStandards inAustralia

Accounting Prin-ciples GenerallyAccepted in

Canada

Accounting PracticeGenerally Acceptedin the Republic of

South Africa

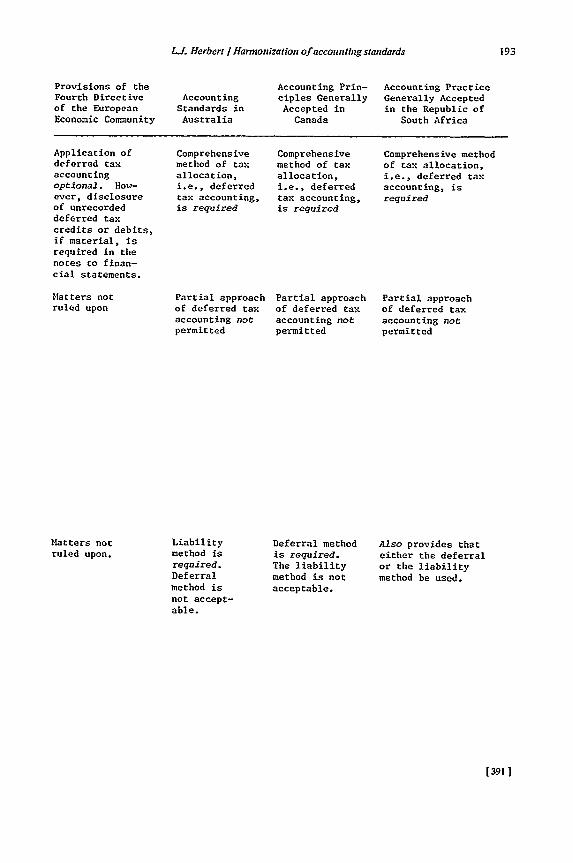

Application ofdeferred taxaccountingoptional. flow-ever, disclosureof unrecordeddeferred taxcredits or debits,if material, isrequired in thenotes to finan-cial statements.

Comprehensivemethod of taxallocation,i.e., deferredtax accounting,is required

Comprehensivemethod of taxallocation,i.e., deferredtax accounting,is required

Comprehensive methodof tax allocation,i.e., deferred taxaccounting, isrequired

Partial approachof deferred taxaccounting notpermitted

Liabilitymethod isrequired.Deferralmethod isnot accept-able.

Partial approachof deferred taxaccounting notpermitted

Deferral methodis required.The liabilitymethod is notacceptable.

Partial approachof deferred taxaccounting notpermitted

Also provides thateither the deferralor the liabilitymethod be used.

Matters notruled upon

Matters notruled upon.

[3911