Embed Size (px)

Citation preview

Please see Disclosures and Disclaimers at the end of this report. A division of Dundee Securities Ltd.

Dundee Capital Markets is a registered trademark of Dundee Corporation, used under license.

Diamond Producers

July 17, 2014

Lucara Diamond & Dominion Diamond - Miners at the Extremes

Source: Diavik Diamond Mine

Matthew O'Keefe / (647) 253-1131

[email protected] Erik Bermel / (647) 253-1112

We are initiating coverage of Dominion Diamond Corp and Lucara Diamond Corp, two diamond producers listed in Canada. Dominion recently consolidated Canada's first two diamond mines, Ekati and Diavik and is looking at opportunities to extend the lives at these maturing operations. Lucara recently started producing from its Karowe Mine in Botswana and has exceeded expectations consistently producing large, high value diamonds.

Diamond Prices on the Rise Provide Tailwind. Diamond prices have risen steadily over the past 2-years on increased global demand driven by growth in China and India and the economic recovery in the United States. Demand growth is expected to continue in line with the global economy while diamond supply remains limited and set to decrease in the medium and longer term.

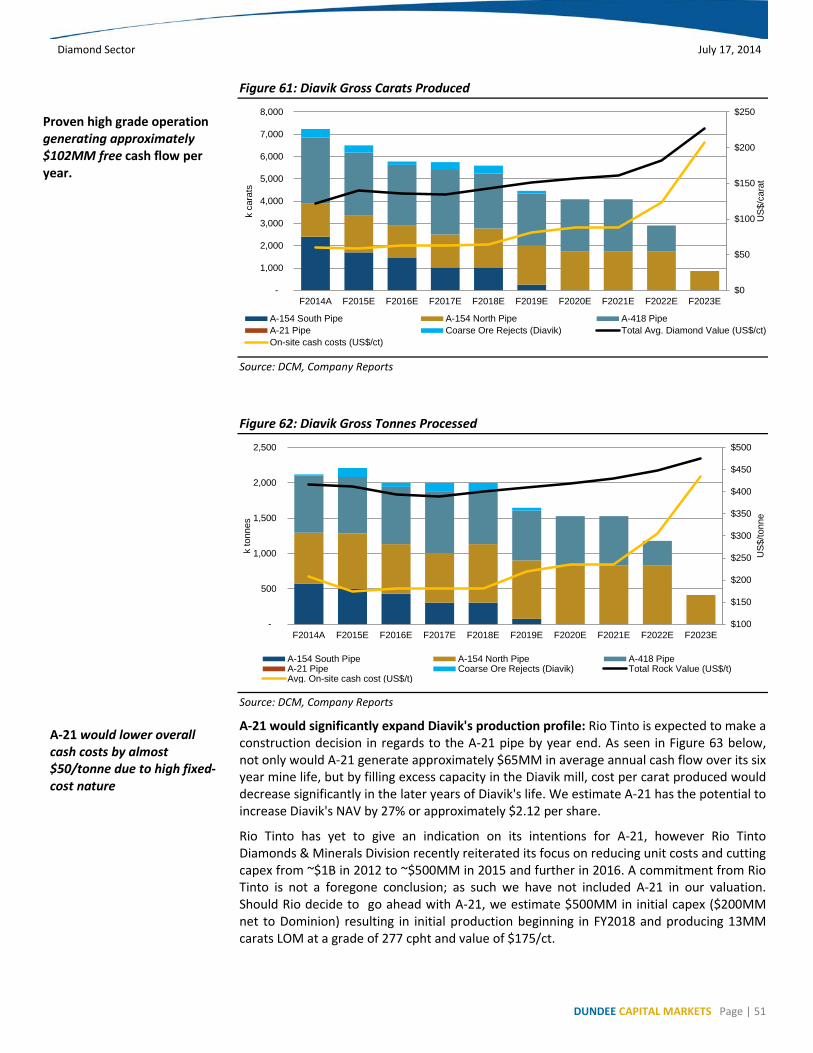

Dominion Diamond Corp - A Pretty Kettle of Fish. The recent consolidation of production in Canada's premier diamond district at Lac de Gras has provided DDC investors with great opportunity but also elevated levels of risk. The high grade Diavik Mine is set for a steady decline in production in its remaining eight-years unless partner Rio Tinto approves the construction of A-21. At Ekati, permitting of Jay is needed to extend the mine life and make the acquisition meaningful. Uncertainty also surrounds the magnitude and structure of growing reclamation bond requirements. Meanwhile operations are marginal until new ore from the Misery pipe can boost production and cash flow in 2016. If Jay is a "go", DDC represents excellent value trading at 0.59x NAV. If neither Jay nor A-21 are approved, DDC is likely fully valued. We initiate coverage on Dominion Diamond Corp. with a BUY, High Risk rating and C$20.50 target price on the assumption that Jay, the game-changing project, will go ahead.

Lucara Diamond Corp - The Biggest Stones in Botswana. In its second year of operation Karowe has proven to be an exceptional mine allowing Lucara to eliminate debt, build cash and attract a premium valuation. While longer-term growth is available on-site, we expect Lucara to use its big stones to grow by acquisition. We initiate coverage on Lucara Diamond Corp. with a BUY, High Risk rating and C$3.00 target price.

Valuations At Each Extreme: DDC appears cheap trading at 0.59x NAV whereas LUC appears expensive at 1.18x NAV vs peers at 0.95x NAV. LUC's large stones, longer-term upside and accretive M&A potential all merit a premium valuation, whereas DDC's discount is attributable to permitting risk around Jay, a capital intensive next two years and an uncertain production profile at both mines.

Rating & Target Methodology: Our valuations for producers DDC and LUC are driven by a DCF analysis to our mine models based on recent feasibility studies, technical reports and discussions with management. We use a 5% discount rate to arrive at our NAV estimates which is in-line with precious metals producers. Our target prices are based on multiples to NAV which capture construction, financing and execution risk.

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 2

Contents

Investment Thesis: .....................................................................................................................................................3

Investing In Canadian Diamonds: Targeting Producers ..................................................................................................... 3

Investment Summaries ...................................................................................................................................................... 5

DDC and LUC - Canadian Listed Producers at the Extremes ..........................................................................................6

Lucara Diamond Corp ...................................................................................................................................................... 10

Dominion Diamond Corp. ................................................................................................................................................ 29

Appendix A - The Diamond Market ........................................................................................................................... 57

Supply & Demand: Expecting Steady Growth Ahead ...................................................................................................... 61

Diamond Prices - Stability Returning ............................................................................................................................... 64

Appendix B: Canadian Diamonds: A Short & Successful History ................................................................................. 66

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 3

INVESTMENT THESIS:

INVESTING IN CANADIAN DIAMONDS: TARGETING PRODUCERS

In our May 2014 report Canadian Diamond Developers & Explorers - Catching the Next Wave of Discovery and Production we focused on what we see as the top explorer-developers in the Canadian diamond space. In this report we extend coverage to include the Canadian producers.

Strengthening Diamond Market: Diamond prices have resumed their steady upward movement after a period of volatility touched off by the credit crisis in 2008 (Figure 1), as outlined in detail in Appendix A. Prices are expected to resume growing at 2-4% annually driven by steady demand growth in the traditional markets of North America, Europe and Japan and higher growth from the emerging and very large markets of China and India. Diamond supply is also growing but should top out in 2017, below previous 2008 highs and start to decline as older and depleted mines are not replaced (Figure 2).

Figure 1: Diamond Prices

Source: PolishedPrices.com, Bain and Co., DCM

Figure 2: Diamond Supply-Demand

Source: Bain and Co., DCM

Globally, the equity market for diamonds is relatively small, dominated by a few large players including Alrosa, De Beers (owned by diversified miner Anglo American) and diversified miner Rio Tinto.

0

20

40

60

80

100

120

140

160

180

200

Inde

x

Historic Rough PricesDCM Rough EstimatePolished Diamond Prices

+5% CAGR +13% CAGR

+2.5% CAGR Est

Rough diamond prices have increased at a CAGR of 13% since 2009 and 5% over the longer term.

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 4

For investors looking for pure play diamond producers, there are few publically traded names to choose from. The main current pure-play producers are Dominion Diamond (BUY, High Risk, C$20.50 target), Petra Diamond (PDL-LON, not rated), Gem Diamonds (GEMD-LN, not rated) and Lucara Diamond (LUC-T, BUY, High Risk, C$3.00 target) (Figure 3). While UK-listed Petra and Gem have shown good performance over the last 12-months, we believe Canadian-listed producers offer excellent opportunities in top performer Lucara Diamond and renewing producer Dominion Diamond.

Figure 3: Comparable Diamond Companies

*Consensus estimates unless covered by DCM; **DDC adjusted for Jan 31 year end; Source: DCM, Company Reports, Intierra, Factset, Bloomberg

INITIATING COVERAGE

As a way to gain exposure to strengthening diamond markets, we are initiating coverage on Dominion Diamond Corp with a BUY, High Risk rating and C$20.50 target and Lucara Diamond Corp. with a BUY, High Risk rating and C$3.00 target. This rounds out our coverage of the top names in the Canadian diamond universe (Figure 4).

Figure 4: Dundee Diamond Coverage List

Source: DCM, *SWY-CA is DCM June 2014 top pick

Valuation Methodology:

Our valuations are based on a net asset value per share approach, based on our estimated pro-forma share structure. For diamond prices, we apply a 2.5% annual real growth rate to our base case price assumptions, as discussed in Appendix A.

($CAD) unless otherwise notedTicker Security Name Last Mkt Cap Debt Cash EV P/NAV*

local C $MM C$ MM C$ MM C$ MM 2014 2015 2016 2014 2015 2016Canadian ProducersDDC-CA Dominion Diamond Corporation $15.23 $1,297 $4.8 $273.1 $1,028 4.3x 6.3x 3.3x 2.7x 4.7x 1.9x 0.59x

International ProducersALRS-MIC AC ALROSA OJSC R 44.75 $10,301 $4,481 $300 $14,482 6.2x 5.9x 5.5x nm nm nm 0.98xPDL-LON Petra Diamonds Limited £1.94 $1,832 $224.0 $27.6 $2,028 5.4x 3.9x 3.5x 10.2x 8.2x 6.8x 0.90xLUC-CA Lucara Diamond Corp. $2.72 $1,029 $0.0 $59.2 $970 9.8x 11.1x 11.9x 6.4x 7.0x 7.6x 1.18xGEMD-LON Gem Diamonds Limited £1.75 $446 $0.0 $24.2 $422 4.9x 3.6x 3.5x 4.7x 3.8x 3.6x 0.95xKDL-ASX Kimberley Diamonds Ltd $0.22 $19 $10.7 $8.5 $21 13.8x 11.6x 1.5x 3.2x 0.8x 0.8x 0.10xTSX-JSE Trans Hex Group Limited $3.45 $37 $0.1 $41.7 -$5 nm nm nm nm nm nm nmRDI-CA Rockwell Diamonds Inc. $0.44 $24 $8.6 $1.3 $31 nm nm nm 2.8x nm nm 0.83xAVERAGE 7.4x 7.1x 4.9x 5.0x 4.9x 4.7x 0.95x

Canadian DevelopersMPV-CA Mountain Province Diamonds Inc $5.05 $581 $0.0 $71.3 $510 nm nm nm nm nm nm 0.44xSWY-CA Stornoway Diamond Corporation $0.68 $497 $197.8 $332.0 $363 nm nm nm nm nm nm 0.35xSGF-CA Shore Gold Inc. $0.25 $56 $0.0 $0.8 $55 nm nm nm nm nm nm nmAVERAGE nm nm nm nm nm nm 0.40x

ValuationEV/EBITDA*Price to Cash Flow*

Capital Structure

Company Ticker Rating Risk Target NAVPSDominion Diamond Corporation DDC-CA BUY High C$20.50 C$25.66Lucara Diamond Corp. LUC-CA BUY High C$3.00 C$2.30Mountain Province Diamonds Inc. MPV-CA BUY High C$9.00 C$11.37Stornoway Diamond Corporation SWY-CA BUY High C$1.60 C$1.95Kennady Diamonds, Inc. KDI-CA BUY Speculative N/A N/ANorth Arrow Minerals Inc. NAR-CA BUY Speculative N/A N/APeregrine Diamonds Ltd. PGD-CA BUY Speculative N/A N/A

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 5

INVESTMENT SUMMARIES

Dominion Diamond Corp: Lac de Gras: A Pretty Kettle of Fish. Dominion Diamond is Canada's premier diamond producer currently producing 4MM carats (attributable) annually from its 40%-owned Diavik Mine and 90%-owned and operated Ekati Mine. This mature pair of operations will see current reserves exhaust in 2022. However, the recent consolidation of the Lac de Gras Diamond District has provided Dominion with a great opportunity for expansion. Should permitting of the Jay pipe be approved, the mine life at Ekati would be extended by 10-years while failure would trigger an expensive reclamation from 2022. Given the reduced footprint of Jay, the significant impact to longevity of Ekati and the importance of Ekati to the NWT, we believe Jay will be permitted and constructed. Including Jay, DDC represents excellent value trading at 0.59x NAV. If its future remains uncertain or it is not approved, DDC is fully valued with a final push from the high grade Misery pipe through 2022. We are initiating coverage on Dominion Diamond Corp. with a BUY, High Risk rating and C$20.50 target price. Our target multiple of 0.8x NAV is a discount to similar diamond produces at 0.95x NAV which we feel captures Dominion's lack of clarity and uncertainty surrounding its future mine life and potential commitments. Following resolution of reclamation requirements and clarity surrounding Jay and A-21 construction, we believe Dominion should trade in line with its peers.

Figure 5: Dominion Diamond Modeled Production Profile

Source: Company Reports, DCM

Lucara Diamond Corp: The Biggest Stones in Botswana. Lucara is in its second year of operation at its newly commissioned Karowe which has proven to be an exceptional mine allowing LUC to eliminate debt, build cash and attract a premium valuation. The regular recovery of large (100+ carat) high value diamonds averaging $425 per carat (and $576 in the last 9-months) is well above initial estimates in the DFS. Production is expected to stabilize at 420,000 carats per year but values should continue to climb as mining focuses on the highest value Center and South lobes. While longer-term growth is available on-site, we expect Lucara to use its big stones to grow by acquisition. With an established high margin operation, growing cash, no debt and a premium market value, Lucara is well-positioned to pursue M&A. We expect LUC to maintain its position as a large stone producer, highlighting like-sized producers/developers Gem Diamonds (GEMD-LN, not covered) and Stornoway Diamond (SWY-T; BUY, C$1.60 target, High Risk) as potential acquisition candidates. Gem's Letseng mine in Lesotho would give Lucara tighter control of the large-stone diamond market as well as offer synergies with its Mothae project that could possibly improve the project from marginal to economic. Stornoway's Renard Project in Quebec is also attractive

4.0 4.1 3.9

6.6

7.9 7.7 7.8 7.8

10.5

6.4 6.0 6.0 6.0 6.0 6.0 6.0 6.0 6.0 6.0

0.6

$0

$50

$100

$150

$200

$250

-

2.0

4.0

6.0

8.0

10.0

12.0

US

$/ca

rat

MM

car

ats

Ekati, NWT (~90%) net Jay Jay Diavik, NWT (40%) net A-21 PipeDiamond Value (US$/ct) On site mining costs (k US$)

Trading at a discount due to near term uncertainty. High grade Misery pipe should double cash flow in CY2017

Lucara runs a high margin operation, has growing cash, no debt and a premium market value, positioning itself well to pursue M&A

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 6

as we expect it to yield similar upside as Karowe given its large stone size distribution. We initiate coverage on Lucara Diamond Corp. with a BUY, High Risk rating and C$3.00 target price based on a 1.3x multiple to NAV. The stock is trading at a premium of 1.18x to our NAV estimate which we see as warranted and light given upside potential from an expanded mine life, higher diamond prices and accretive M&A opportunities.

Figure 6: Lucara's Production Profile

Source: Company Reports, DCM

DDC AND LUC - CANADIAN LISTED PRODUCERS AT THE EXTREMES

Although DDC and LUC are both Canadian-listed diamond producers, they are positioned at opposite ends of the diamond producer spectrum, highlighted by several key attributes. In Figures 7 and 8, we compare relevant operation metrics.

1) New versus Renewing: Dominion Diamond has been producing for over a decade and, based on current reserves, has just 8-years of mine life left. Dominion is in the midst of its third renewal moving from discoverer and marketer of rough diamonds (Aber) to top end jeweler (Harry Winston) and now to mature miner scrambling to add reserves (Dominion Diamond). Lucara, by contrast, has the benefit of youth. Its Karowe mine is less than two years in with a 13-year reserve and likely 10 additional years from resource. Some investors may prefer the fresh, clean slate of Lucara over the Dominion. On the other hand, the approval of A-21 and Jay should be significant catalysts for Dominion, extending its life from 8 to 18 years and buying time for additional discoveries on the sizeable land package.

2) Jurisdictions: There are clear differences between the political and operating environments of Canada and Botswana. Both are considered top operating jurisdictions and politically stable. However, Dominion's mines, located in Canada's far north, clearly have the disadvantage with respect to costs and logistics. Water is an issue in both countries, which can lengthen or impede the permitting process, with Canada having too much and Botswana not having enough. Lucara is permitted for Karowe; Dominion has yet to permit Jay.

3) Mining Scope and Scale: Dominion is a large producer of small to medium stones while Lucara is a relatively modest producer of exceptional stones. Annual production from Diavik and Ekati is ~9 MM carats with ~4MM attributable to Dominion. This is almost 10x the carat production of Lucara's Karowe at ~420,000. But both operations move and process similar amounts of material with Diavik processing 2.4MM tpa and Ekati about 4.3MM tpa versus Karowe at 2.5MM tpa. But it's the impact of grade and value is what really drives the difference with modest grades at Karowe in the 20 cpht range significantly lower than the 50 cpht reserves at Ekati and 295 cpht at Diavik. Diamond values are also at opposite ends of

$0

$100

$200

$300

$400

$500

$600

$700

$800

-

50

100

150

200

250

300

350

400

450

500

US

$/ca

rat

k ca

rats

North Lobe Centre Lobe South Lobe

Stockpile Total Avg. Diamond Value (US$/ct) On-site cash costs (US$/ct)

Quantity of stones with Dominion vs quality of stones with Lucara

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 7

the spectrum. Karowe producers large, high value specials with regularity that have pushed average carat values to $425/carat and still climbing while Diavik and Ekati have produced no specials of note with average values in the $118-$150/carat range. The real luxury goods producer in this pair is Lucara but the volume of carats and flexibility of two mines afforded by Dominion also has its appeal.

4) Valuation: Of course, the most relevant measure is valuation; Dominion appears cheap trading at 0.59x NAV whereas Lucara appears expensive at 1.18x NAV. But as we discuss, the large stones, longer-term upside and accretive M&A potential for Lucara all merit a premium valuation supporting our C$3.00 target price. Dominion has more risk predominantly around permitting of Jay for which we apply a lower multiple of 0.8x NAV to achieve our target price of C$20.50 per share. Risk adjusted, they are not that far apart with LUC trading at 0.91x our target and DDC trading at 0.74x our target.

For the more risk adverse investor, LUC is the more appealing stock today given the long life ahead of it and more "bang for the buck" in its large, high value diamonds. However, we believe DDC is poised to "pop" following several key decisions in the short and medium term; namely a "go" decision for A-21, "go" decision & permitting approval for Jay and production start at Misery in 2016.

Figure 7: Lucara - Dominion Diamond Operational Comparison

Source: Company Reports, DCM

LUC-CACapitalizationCurrent Price (C$) $2.72Target Price (C$) $3.00Return To Target 10%NAVPS (C$) $2.30P/NAV 1.18xMarket Cap (C$MM) $1,029EV (C$MM) $970Project Karowe Ekati DiavikProject Ownership 100% ~90% 40%Location Botswana NWT NWTAccess All-Seasoned Winter Road Winter RoadMining Method Open Pit OP & UG UndergroundWater Management Land Based Retention

Dykes Retention

Dykes Operator Lucara Dominion Rio TintoEst. Net Remaining Capex (US$MM) $29 $909 $3Modeled Production MetricsMine Life (years) 13.5 18.5 8.25Throughput (MM tpa) 2.55 4.35 2.40 2014 Production (MM ct, gross/net) 0.4 1.84/1.55 6.5/2.6Grade (cpht) 18 50 294 Base Diamond Value (US$/ct) $560 $302 $137LOM Avg Diamond Value (US$/ct) $583 $118 $148Most Recent QuarterValue Per Tonne (US$/t) $107 $167 $424Operating Cost (US$/t) $19 $80 $160Operating Margin 83% 52% 62%G&A per Tonne (US$) $3.10G&A per Carat (US$) $18.98*~90% ownership assumes Fipke transaction closes

DDC-CA

35%

0.59x$25.66

$20.50$15.23

$7.11$6.05

$1,297$1,028

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 8

Figure 8: Lucara & Dominion Production and Cash Flow Comparison

Source: DCM

We also look at LUC and DDC in the context of the global diamond universe (Figure 9). On a valuation basis, they stack up pretty much where expected with Lucara at a premium to NAV for its top end goods, high margins and expandable mine life and Dominion at a discount given the uncertainty around production growth and funding requirements. Steady-state producers Alrosa (ALRS-MIC, not covered) and Gem (GEMD-LN, not covered) trade at or above NAV, which is typical of established diamond producers.

Figure 9: P/NAV of Covered Diamond Names in Global Context

Source: DCM, Company Reports, Bloomberg

What's worth considering is the steep discount of SWY-CA (BUY C$1.60) and MPV-CA (BUY C$9.00) relative to LUC and DDC. Both are in construction and will have fresh, new mines starting up in 2016; this is about the same timeframe as Dominion is due to start Misery. We perceive the present risk in Dominion to be on par to MPV-CA given that, while both are involved with experienced operators (MPV has De Beers building and operating Gahcho Kué, DDC has Rio Tinto operating Diavik and acquired the Ekati operating team). Both also have permitting and funding risks ahead. SWY lacks operating experience but is permitted and fully financed and trading at the steepest discount and remains the best value in our coverage universe.

The other aspect that stands out is Lucara's premium valuation and opportunity for accretive acquisition. As discussed in more detail in the Lucara section, the best fits for LUC are Gem Diamonds (GEMD-LN, not covered) and Stornoway Diamond. Both are the rights size, majority own and operate their core assets, trade at discounts to NAV and are large diamond producers (we expect SWY to be) that would allow Lucara to maintain its position as a dominant large stone producer.

Calendar YearLUC-CA DDC-CA LUC-CA DDC-CA LUC-CA DDC-CA

Production (MM ct, net) 0.42 4.15 0.45 3.86 0.43 6.58 Grade (cpht) 18 93 18 82 17 140 Diamond Value (US$/ct) $574 $217 $574 $195 $562 $155Revenue ($MM) $240 $900 $257 $752 $244 $1,019CFO ($MM) $94 $269 $84 $185 $78 $357EBITDA ($MM) $136 $338 $124 $198 $114 $475Free Cash Flow ($MM) $36 $63 $75 -$34 $72 $194P/CF 9.8x 4.3x 11.1x 6.3x 11.9x 3.3xEV/EBITDA 6.4x 2.7x 7.0x 4.7x 7.6x 1.9x

2014 2015 2016

0.35x0.44x

0.59x0.70x

0.83x0.90x 0.95x 0.95x 0.98x

1.18x 1.23x

0.00x

0.20x

0.40x

0.60x

0.80x

1.00x

1.20x

SWY-CA(DCM)

MPV-CA(DCM)

DDC-CA(DCM)

DDC-CA RDI-CA PDL-LON GEMD-LON ProducerAvg.

ALRS-MIC LUC-CA(DCM)

LUC-CA

*Consensus estimate for companies not covered by DCM

DUNDEE CAPITAL MARKETS Page | 9

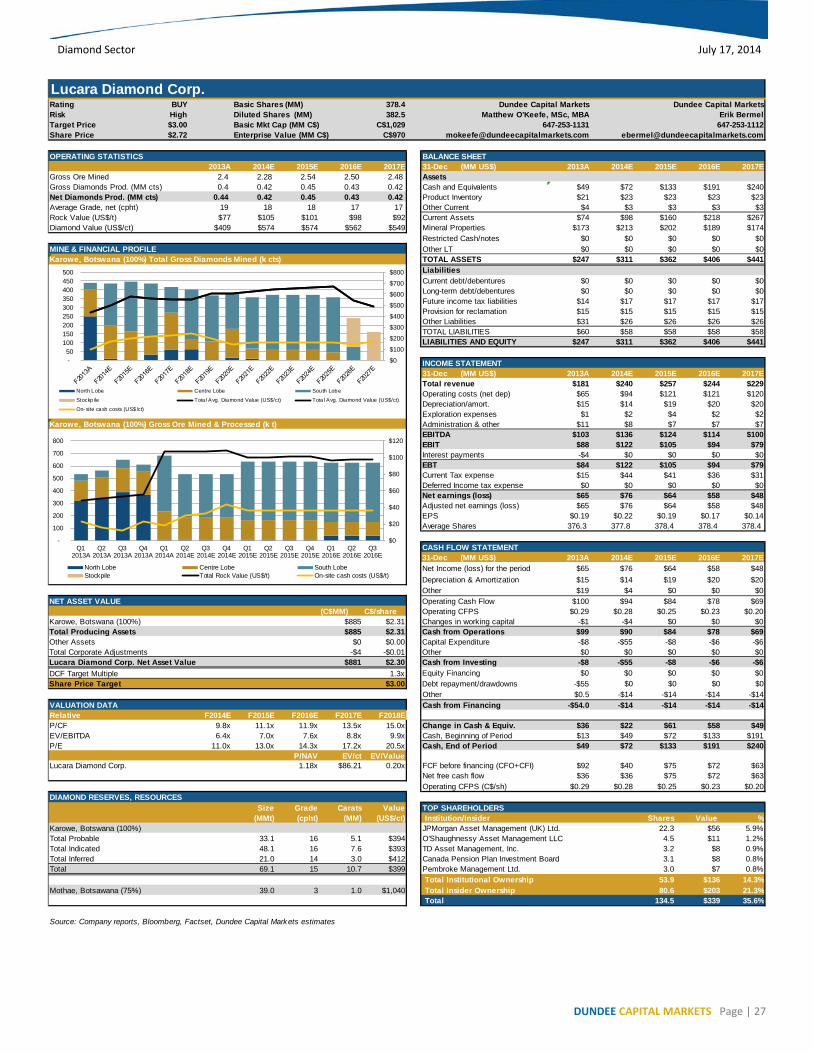

Lucara Diamond Corp. (LUC-T: C$2.72) July 17, 2014

BUY, High Risk Dundee target: C$3.00

Matthew O'Keefe / (647) 253-1131 [email protected]

Erik Bermel / (647) 253-1112 [email protected]

The Biggest Stones in Botswana

We are initiating coverage on Lucara Diamond Corp. with a BUY rating and a 12- month target price of C$3.00 per share. Lucara owns and operates the Karowe diamond mine in Botswana which has developed into a consistent producer of large, high value diamonds since starting production in 2012. Based on the current mine plan, Karowe will produce 420,000 carats annually for 13-years.

• Diamond Success Story: Lucara has quickly developed into a large stone producer routinely recovering +100 carat diamonds. The effect on average diamond price has been dramatic averaging $425/carat versus the $243/carat citied in the 2010 feasibility study.

• Generous Dividend Policy: Lucara has initiated a C$0.02/share semi-annual dividend for a current yield of 1.6% and allowed for a special dividend linked to exceptional stone tenders which could add up to C$0.10/share annually.

• Premium Producer: LUC currently trades at 1.18x our NAV estimate and 0.91x our target price. This is at the top end of comparable producers which we attribute to its operation success, ongoing potential for larger and better diamonds, top management and technical team and aggressive growth potential.

• Ready to Hunt: The aggressive acquisition of Karowe and its subsequent success has put Lucara in a strong position with growing cash, no debt and a premium valuation. As part of the Lundin Group of Companies with active interest from Chairman and major shareholder Lukas Lundin, we expect near-term growth through M&A.

• Resource and exploration upside: The Karowe mine has additional resource at depth which could extend the mine life by up to 10-years. The Orapa district in Botswana remains prospective for additional diamond discoveries and we expect additional properties at various stages to be added and evaluated.

Target Price Valuation Methodology: Our C$3.00 target is based on a 1.3x NAV target multiple. We feel LUC's top operational performance, extended mine life potential, clean balance sheet and further diamond price upside potential justifies the premium 1.3x multiple, compared to other diamond producers which trade at 0.95x. Our target implies a 10.8x 2015E price to cash flow multiple, valuing Lucara towards the top end of comparable diamond producers who trade at an average of 7.1x 2015E cash flow.

LUC: Price/Volume Chart

Source: Factset Company Description Lucara owns and operates the Karowe diamond mine in Botswana which has developed into a consistent producer of large, high value diamonds since starting production in 2012. Karowe is set to produce 420k ct/yr over its 13 year mine life.

LUC-T New LastRating:Target:Risk:NAVPS:

Company DataPrice (07/15/14):52-Week Range:Market Capitalization ($MM):Enterprise Value ($MM):Shares Outstanding - Basic (MM):Shares Outstanding - FD (MM):Avg Daily Volume (3 Mos) (000s):Cash ($MM):Debt ($MM):Dividend YieldFiscal Year-End:Est. (MM) 2013 A 2014 E 2015 ENet Prod. 0.44 0.42 0.45Grade (cpht) 19 18 18Value US$/ct 409 574 574Cost US$/t 19 30 36Revenue ($) 181 240 257CFO ($) 100 94 84EBITDA ($) 103 136 124CFPS (C$) 0.29 0.28 0.25Valuaion 2013 A 2014 E 2015 EP/CF 9.3x 9.8x 11.1xEV/EBITDA 8.5x 6.4x 7.0x

P/NAV EV/ct EV/Value1.18x 86.21 0.20x

All Figures in US$ Unless Otherwise NotedSource: Factset, Company reports, Bloomberg, DCM

C$01.5%

31-Dec

C$1,029C$970

378383523

C$59

C$0.75-2.80

BUYC$3.00

HighC$2.30

C$2.72

Oct-12 Apr-13 Oct-13 Apr-14

0.5

1

1.5

2

2.5

0

4

Lucara Diamond Corp. (LUC-CA)

Volume (Millions) Price (CAD)Volume Lucara Diamond Corp.

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 10

INTRODUCTION

Lucara Diamond Corp. is a Vancouver-headquartered diamond producer that started producing in 2012 from its 100%-owned Karowe Mine located in north-central Botswana (Figure 10). Karowe is part of the Orapa/Letlhakane Kimberlite district which is one of the most prolific diamond producing regions in the world. The Company holds a 75% interested in the Mothae diamond project located in the Maluti Mountains of Lesotho where it is reviewing a number of development options. Both Mothae and Karowe have consistently produced large, "special", Type II stones.

Lucara currently has 378MM shares outstanding, with management and insiders owning ~21%. As of May, 2014, Lorito Holdings Ltd. (8.67%), Zebra Holdings (9.23%), both controlled by the Lundin Trust, and JPMorgan Chase & Co (5.9%) were the largest shareholders of the stock along with Board members Eira Thomas (2.04%) and Lukas Lundin (1.06%). The company has a current cash position of $57MM in the treasury, with no debt. Lucara’s shares trade on the TSX, NASDAQ OMX Stockholm and the Botswana Stock Exchange under the symbol LUC.

Figure 10: Lucara Diamond Properties in Southern African Context

Source: Company Reports

Karowe is part of the most prolific diamond producing regions in the world

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 11

KAROWE - PRODUCER WITH THE BIGGEST STONES IN BOTSWANA

Lucara's 100% owned Karowe Mine in Botswana is the main asset in its portfolio driving our valuation. The new mine started production in mid-2012 and has since exceeded expectations with the consistent recovery of large, high quality diamonds. Average grades are only about 16 carats per hundred tonne (cpht) with pre-production diamond values in the $240/carat range. However, average diamond values to date are tracking $425/carat and $476/carat on a 9-month rolling average at the end of Q1/14 driven by the preponderance of large, high quality diamonds "specials" that have returned values averaging over $40,000 per carat from three "exceptional stone" tenders. Karowe is a modest producer on a total carat basis, yielding only about 420,000 carats per year from an open pit with the current reserve life good for about 13 years of production with an additional 5-8 years potential life in indicated resource below 400 metres. The consistency of large stones suggests that Karowe will be mined for as long as feasible as it is one of the few mines that routinely produces >100 carat gems like the Letseng and Cullinan mines.

Figure 11: Lucara at a Glance

Source: DCM, Company Reports

LUNDIN'S DIAMOND VEHICLE

Lucara began in its present form in 2007 with the acquisition of the Mothae project in Lesotho for a staged earn-in of $8MM with principal contributions and new Board including members of the Lundin Group, Catherine McLeod Selzer and Eira Thomas. In 2009 Lucara acquired a 70.3% interest in the Karowe project (then known as AK6) from then operator De Beers for $49MM, eventually consolidating the balance from African Diamonds plc (28.4%) and Wati Ventures Ltd. (1.4%) in December 2010. The mine went into construction the following year and was officially opened on August 17, 2012. As part of the Lundin Group of Companies, Lucara sees active involvement from Chairman and major shareholder Lukas Lundin who, as discussed above, controls about 17.9% of the Company's stock.

Lucara Diamond Corp. Key StatisticsF2013A F2014E F2015E F2016E F2017E F2018E

Production (MM ct) 0.441 0.418 0.447 0.435 0.417 0.402 Average Grade, net (cpht) 19 18 18 17 17 16 Diamond Value (US$/ct) $409 $574 $574 $562 $549 $552Rock Value (US$/t) $77 $105 $101 $98 $92 $89Cost per Tonne (US$/t) $19 $30 $36 $37 $37 $39Revenue (MM US$) $181 $240 $257 $244 $229 $222CFO (MM US$) $99 $90 $84 $78 $69 $62EBITDA (MM US$) $103 $136 $124 $114 $100 $89Free Cash Flow (MM US$) $36 $36 $75 $72 $63 $56EPS (C$/sh) $0.19 $0.22 $0.19 $0.17 $0.14 $0.12CFPS (C$/sh) $0.29 $0.28 $0.25 $0.23 $0.20 $0.18Current Valuation MetricsP/CF 9.3x 9.8x 11.1x 11.9x 13.5x 15.0xEV/EBITDA 8.5x 6.4x 7.0x 7.6x 8.8x 9.9xP/E 12.8x 11.0x 13.0x 14.3x 17.2x 20.5x

Karowe started production in mid-2012 and has since exceeded expectations

Part of the Lundin Group of Companies, Lucara sees active involvement from Lukas Lundin who controls about 18% of the stock.

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 12

WELL SITUATED IN A TOP MINING JURISDICTION

The Karowe Mine is located in north-central Botswana and is part of the Orapa kimberlite field, one of the world's most prolific diamond producing areas with over 80 kimberlites, five of which (AK1, BK9, DK1, DK2 and AK6) are currently being mined (Figure 12). Letlhakane village is the closest settlement and offers basic facilities, including fuel and connects to the major cities of Gaborone by good quality paved roads. There is an airstrip in the Karowe Mine lease area for light aircraft and the closest airport with commercial flights is Francistown, 200km to the east. Electrical power is provided by Botswana Power Corporation's national grid and water comes from aquifers in the area.

Figure 12: Karowe Well Located in Orapa Kimberlite Field

Source: Company Reports

The AK6 Kimberlite was discovered by De Beers in 1969, but was initially considered to be small and low grade based on early work. Reassessment led by De Beers from 2003 revealed that the Kimberlite was larger and had a higher grade than previously estimated. In June 2010, a definitive feasibility study updating previous work to a confidence level to support project approval was completed. A formal decision was made in 2010 to proceed with the construction of the diamond mine which was estimated to require a capital investment of approximately $120MM to $130MM, which included the process plant and all mine site and off-site infrastructure. It was commissioned on-time and on-budget in June 2012. The low capex compared to North American projects and indeed De Beers original budget demonstrates the quality operating team and the benefit of operating in Botswana, with low labour costs and having the benefit of working within an established diamond district.

The country of Botswana is currently the world’s largest diamond producer, accounting for 23% by value. Access and infrastructure within the country are very good and the semi-arid climate allows exploration and development work to continue year-round in most places. The country’s economy relies heavily on diamond mining, which has taken it from one of the poorest nations in Africa in the 1950s to one of the richest. Botswana has established high-quality public institutions and legal systems with very low corruption. As a result, Botswana rates among the top countries in the world for mining investment, such that Standard and Poor’s has assigned the country an “A” credit rating. The Government of Botswana (GoB) has a 10% gross overriding royalty on Karowe as it does with other diamond projects in the country.

Botswana is the world’s largest diamond producer, by value and rates among the top countries in the world for mining investment

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 13

KAROWE KIMBERLITE - THE BEST IS YET TO COME

The Karowe kimberlite is a three-lobed body with primarily composed of volcaniclastic kimberlite with lesser hypabyssal facies kimberlite (Figure 13). The three lobes are distinguished based on textural characteristics, relative proportion of internal country-rock dilution and degree of weathering. The South Lobe is distinctly different from the North and Centre Lobes which are similar to each other in terms of their geological characteristics. The North and Centre Lobes exhibit internal textural complexity whereas the bulk of the South Lobe is more massive and internally homogeneous.

Figure 13: Karowe Geologic Model

Source: Company Reports

The current mineral reserve estimate which includes mineable material by open pit to 324 metres, is 33.1MM tonnes grading 15.5 cpht for a total of 5.1MM contained carats (Figure 14). The bulk of this reserve (75%) is contained in the high value South Lobe and 18% in the Centre Lobe with the remainder comprising of the North Lobe and low grade stockpile. At the current processing rate of about 2.5MM tpa this is sufficient for 13-years of mine life. However, considerable resource exists with depth with a global resource (indicated and inferred) of 69.1MM tonnes averaging 16 cpht for a total of 10.7MM contained carats to 750 meters which has the potential to nearly double the mine life.

Considerable resource exists with depth which has the potential to nearly double the mine life

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 14

Figure 14: Karowe Mineral Reserves & Estimated Minable Material

Source: Company Reports, DCM

The North Zone is the shallowest, most weathered and has largely been mined out as it was the focus of production in the first 18-months. A large part of the weathered material in the Centre Lobe has also been mined out but it will continue to contribute material for much of the mine life. The Company has recently started mining the South Lobe, the largest portion of the resource and the main source of the large, +100 carat diamonds (Figure 15). The consistency of the recovery of these stones in the South Lobe points to a much higher average diamond value than that of the North and Centre Lobes.

Figure 15: Long Section Showing Consistent Recovery of Very Large Stones

Source: Company Reports

Karowe Reserve Statement - December 2013 DCM EstimateCategory Lobe/facies Tonnes Grade Carats Value Value (2014)

(MMt) (cpht) (MMct) US$/ct US$/ctProbable (to 324m) North 1.0 18.4 0.2 $217 $250

Centre 6.0 18.4 1.1 $351 $565South 25.3 15.1 3.8 $413 $565

Probable LOM Stockpile 0.9 5.7 0.0 $350 $350Total Probable 33.1 15.5 5.1 $394 $552*Mining recovery of 97% and dilution of 4.5% applied, 1.25mm cutoff screen

Karowe Resource Estimate - December 2013 DCM EstimateLobe/facies Tonnes Grade Carats Value Value (2014)

(MMt) (cpht) (MMct) US$/ct US$/ctIndicated (to 400 m) North 1.8 16 0.3 $217 $250

Centre 6.5 20 1.3 $351 $565South 37.9 16 5.9 $413 $565Working SP 0.6 13 0.1 $333 $333LOM SP 1.2 6 0.1 $350 $350

Total Indicated 48.1 16 7.6 $393 $548Inferred (400m to 750m)Centre 0.2 15 0.0 $351 $565

South 20.8 14 3.0 $413 $565Total Inferred 21.0 14 3.0 $412 $565

Total 69.1 15 10.7 $399 $553* 1.25mm cutoff screen

The consistent recovery of +100 carat stones from the South Lobe points to a much higher average diamond value than that of the North and Centre Lobes.

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 15

DIAMOND VALUE - GOOD STONES WITH UPSIDE POTENTIAL

Diamond recoveries from Karowe have exceeded expectations eclipsing the original valuations in the 2010 feasibility study with a reserve value of $243/carat. The values summarized in Figure 16 below and applied in the 2013 resource are based on three production parcels totaling 161,500 carats with about 1/3 from each lobe. The authors of the technical report note that the valuation process is considered to have generated reliable value estimates for all size ranges with the exception of the +10.8 carat size class (above this threshold are "specials"). These +10.8 carat stones are particularly relevant to the Centre and South Lobes for which +10.8 carat diamonds comprise a significant proportion of the total diamond population and contribute substantially to the average value. They also noted that due to blending of material from different lobes during most production periods it was noted that the diamond values for the +10.8 carat stones for the South Lobe and Centre Lobe are not conclusive. As such, the value applied to the +10.8 carat fraction is flattened at $6,063 per carat for an average modeled price of $413/carat (Figure 17).

Figure 16: Karowe Diamond Valuation Estimates

Source: Company Reports

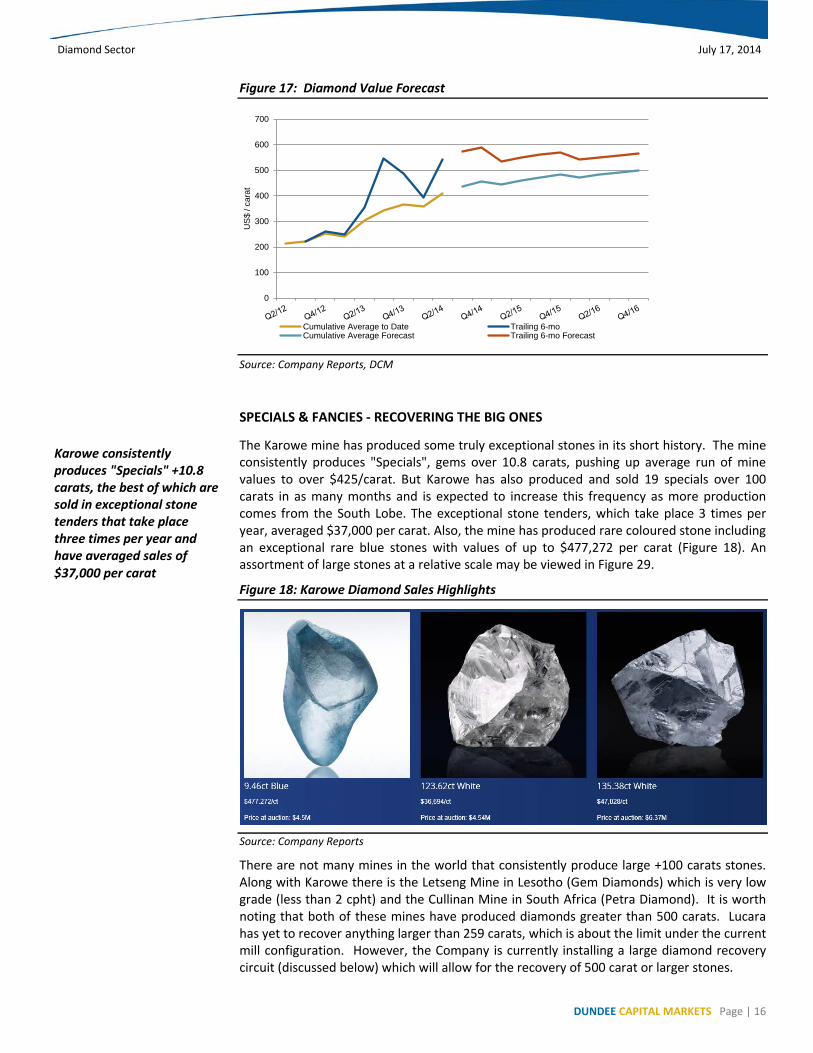

Sales since the updated resource diamond values have continued to rise on a per carat basis with each successive tender as more diamonds are recovered. To date over 730,000 carats have been sold pushing the cumulative average value to $425 per carat. As more material comes from the South and Centre Lobes (the focus of current and future mining) we expect that average values to rise higher, continuing the trend. Projecting forward we expect average diamond values to settle out in the $525/carat range. Ongoing mining in the South Lobe should continue to contribute more large stones and eventually flatten out the cumulative price curve at which point we will be more confident in the forecast. Quarter over quarter diamond values will remain volatile due to the presence or absence of exceptional stone tenders (we expect three per year) and the occurrence of truly exceptional stones like the 167 carat stone that sold in the April tender for $12.7MM (or $76,011 per carat) or the 9.6 carat blue that sold for $4.5MM or $477,072 per carat. But over the longer term, we expect prices for the Centre and South Lobes to average $565 per carat.

Size2013 Tech Report North Centre South +3 DTC 38 49 42 +5 DTC 52 54 46 +7 DTC 63 62 61 +9 DTC 84 69 68 +11 DTC 118 86 97 3-6 Gr 235 186 215 8-10 Gr 451 326 433 3-5 ct 753 573 716 6-10 ct 1033 587 1031 +10.8 ct 1425 6063 6063All 217 351 413DCM Adj. 250 565 5652010 values 276 276 231

Average Value ($US/ct)Quarter over quarter diamond values will remain volatile but we expect prices for the Centre and South Lobes to average $565/carat.

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 16

Figure 17: Diamond Value Forecast

Source: Company Reports, DCM

SPECIALS & FANCIES - RECOVERING THE BIG ONES

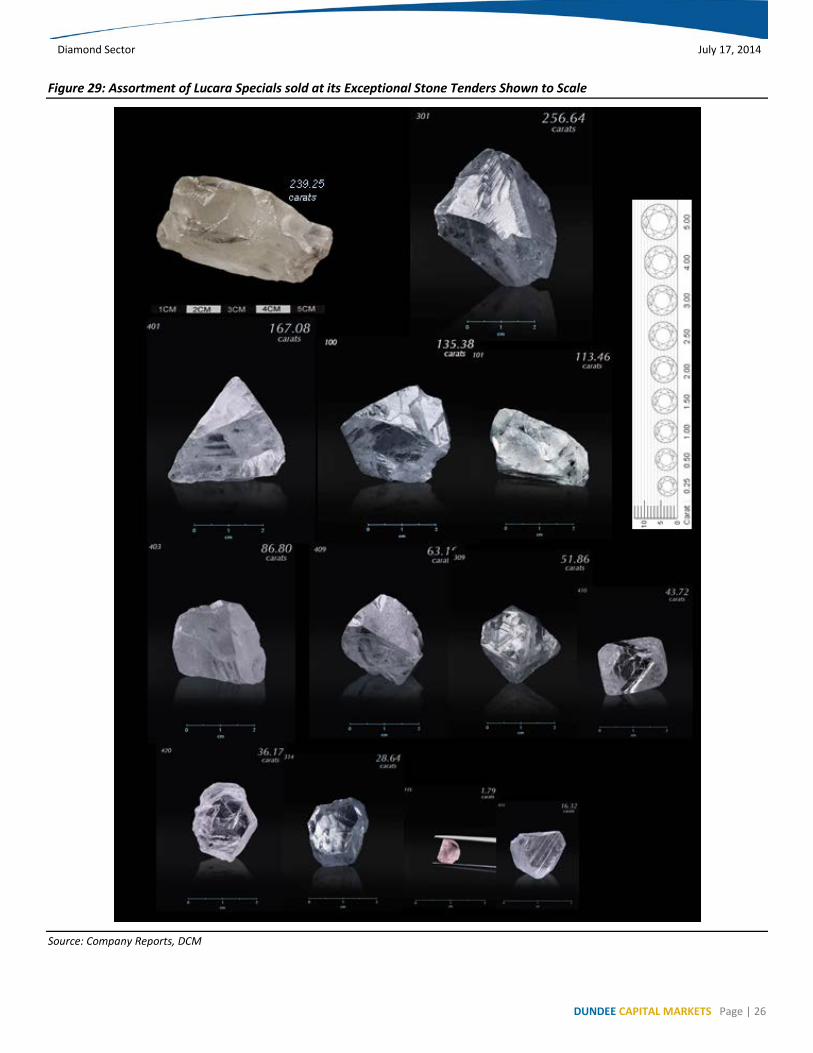

The Karowe mine has produced some truly exceptional stones in its short history. The mine consistently produces "Specials", gems over 10.8 carats, pushing up average run of mine values to over $425/carat. But Karowe has also produced and sold 19 specials over 100 carats in as many months and is expected to increase this frequency as more production comes from the South Lobe. The exceptional stone tenders, which take place 3 times per year, averaged $37,000 per carat. Also, the mine has produced rare coloured stone including an exceptional rare blue stones with values of up to $477,272 per carat (Figure 18). An assortment of large stones at a relative scale may be viewed in Figure 29.

Figure 18: Karowe Diamond Sales Highlights

Source: Company Reports

There are not many mines in the world that consistently produce large +100 carats stones. Along with Karowe there is the Letseng Mine in Lesotho (Gem Diamonds) which is very low grade (less than 2 cpht) and the Cullinan Mine in South Africa (Petra Diamond). It is worth noting that both of these mines have produced diamonds greater than 500 carats. Lucara has yet to recover anything larger than 259 carats, which is about the limit under the current mill configuration. However, the Company is currently installing a large diamond recovery circuit (discussed below) which will allow for the recovery of 500 carat or larger stones.

0

100

200

300

400

500

600

700

US

$ / c

arat

Cumulative Average to Date Trailing 6-moCumulative Average Forecast Trailing 6-mo Forecast

Karowe consistently produces "Specials" +10.8 carats, the best of which are sold in exceptional stone tenders that take place three times per year and have averaged sales of $37,000 per carat

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 17

PLANT UPGRADE - HARDER ORE AND BETTER RECOVERY OF LARGE STONES

In 2014 Lucara is undertaking a capital expenditure program which includes $50MM for optimization of the Karowe plant to improve large diamond recovery and enable sustainable processing of hard ore in the South Lobe. Lucara could afford to wait for this modification as the upper 70 m of the kimberlite (now mostly mined out) is significantly weathered and diamonds liberated easily. To address the harder ore a secondary gyratory crusher will be added to ensure sustainable 2.5MM tpa throughput. The more competent ore is also un-weathered which will result in a higher volume of dense media separates (DMS) reporting to the recovery plant (increasing to 3-7% from 2% in the weathered material). Rather than adding additional DMS capacity Lucara has elected to augment the existing system with X-ray Transmissive technology (XRT). The +1.5, –8 mm material will report to the existing DMS while the other size fractions will report to the new Large Diamond Recovery bulk sorter circuit consisting of high capacity XRT sorting machines. This sensor-based sorting technology uses physical properties such as x-ray luminescence, atomic density and transparency which are inherently different to the gangue minerals present to separate diamonds. The XRT technology along with additional sorting at higher size fractions will also help in the recovery of very large diamonds and Type II diamonds. Orders have been completed for long lead items, and the full upgrade expected to be complete by early 2015. Based on the regular occurrence of large diamonds, the Large Diameter Recovery (LDR) unit will be installed in Q3/14.

CURRENT KAROWE MINE PLAN

Operations are in full swing with the pit excavated across all three lobes down to about 85 meters (Figure 19). The mill has achieved throughput capacity and Karowe is forecast to process 2.2MM to 2.4MM tonnes of ore and to produce and sell 400,000 to 420,000 carats in 2014. Ore mined is forecast between 3.0MM and 3.5MM tonnes and waste mined is expected to be between 10MM to 11MM tonnes for operating cash costs in the $31 to $33 per tonne ore treated range.

Figure 19: Karowe Pit

Source: Company Reports

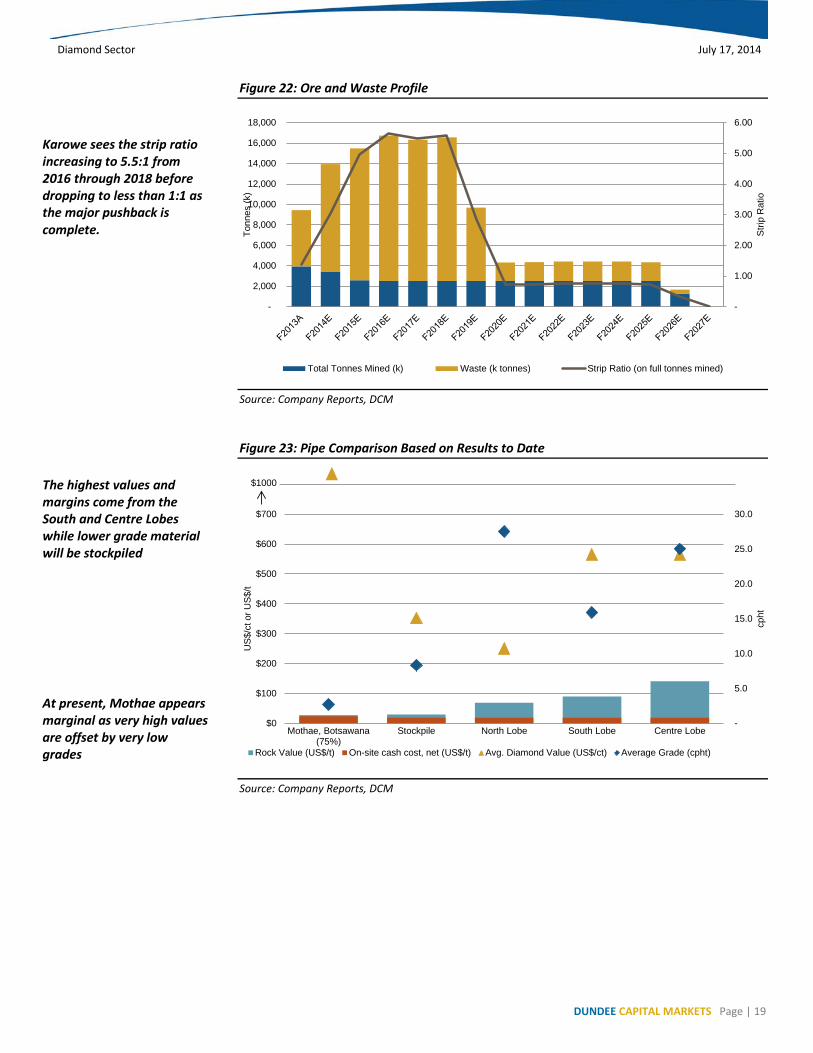

We have modeled Karowe based on the existing resource as outlined in the 2013 independent NI43-101 report. Production will continue in the 400-450k carat range through 2018 peaking at just under 450,000 carats in 2015 (Figure 20 and 21). Production should dip in 2019 and 2020 as lower grade material from the deeper more dilute parts of the North Lobe are extracted. However, margins should expand from this period as the major pushback is completed by 2019 (Figure 22) and mining benefits from lowering strip ratios and greater contribution from the high value South and Central Lobes (Figure 23).

Ongoing plant optimization will improve large diamond recovery and enable sustainable processing of harder ore at depth

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 18

Figure 20: Production Profile (000's tonnes milled)

Source: Company Reports, DCM

Figure 21: Production Profile (000's ct)

Source: Company Reports, DCM

$0

$20

$40

$60

$80

$100

$120

-

500

1,000

1,500

2,000

2,500

3,000

US

$/to

nne

k to

nnes

North Lobe Centre LobeSouth Lobe StockpileTotal Rock Value (US$/t) Cash cost per tonne processed (US$/t)

$0

$100

$200

$300

$400

$500

$600

$700

$800

-

50

100

150

200

250

300

350

400

450

500

US

$/ca

rat

k ca

rats

North Lobe Centre Lobe South Lobe

Stockpile Total Avg. Diamond Value (US$/ct) On-site cash costs (US$/ct)

Production will predominantly come from the high value South and Centre Lobes in the next three years.

Annual production should be above 400,000 carats through 2018 but margins will rise as major pushbacks are complete.

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 19

Figure 22: Ore and Waste Profile

Source: Company Reports, DCM

Figure 23: Pipe Comparison Based on Results to Date

Source: Company Reports, DCM

-

1.00

2.00

3.00

4.00

5.00

6.00

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Stri

p R

atio

Tonn

es (k

)

Total Tonnes Mined (k) Waste (k tonnes) Strip Ratio (on full tonnes mined)

-

5.0

10.0

15.0

20.0

25.0

30.0

$0

$100

$200

$300

$400

$500

$600

$700

Mothae, Botsawana(75%)

Stockpile North Lobe South Lobe Centre Lobe

cpht

US

$/ct

or U

S$/

t

Rock Value (US$/t) On-site cash cost, net (US$/t) Avg. Diamond Value (US$/ct) Average Grade (cpht)

$1000

Karowe sees the strip ratio increasing to 5.5:1 from 2016 through 2018 before dropping to less than 1:1 as the major pushback is complete.

The highest values and margins come from the South and Centre Lobes while lower grade material will be stockpiled

At present, Mothae appears marginal as very high values are offset by very low grades

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 20

MOTHAE - LARGE STONES ON THE SHELF

The Mothae project is located in northeast Lesotho owned 75% indirectly by Lucara and 25% by the Lesotho Government. It hosts a large low grade kimberlite approximately 150km northeast of Maseru, the capital of Lesotho and 6.5 km from Gem Diamonds' (GEMD-LN) Letseng project. Like Letseng, Mothae contains a population of large, high value Type IIa diamonds, but since it is a low grade high value kimberlite, evaluation is particularly difficult because very large bulk samples are required to provide adequate diamond recoveries for grade and revenue estimation. Bulk samples processing of about 700,000 tonnes has shown a very coarse size frequency distribution but work to date has yet to demonstrate its economic potential as data on very large stones (over 60 carats) is still lacking. Average diamond values are modeled at between $615 and $1364 per carat, averaging $1062/carat on the 39MM tonne indicated and inferred resource. The Mothae project remains on temporary care and maintenance as the Company reviews a number of development options. Given the high quality of the work done to date, we believe that Mothae is unlikely to be developed on its own in the near term but could benefit greatly from synergies with another operation such as Letseng that is just 6.5 km to the southeast.

CASH FLOW & DIVIDENDS

Karowe is shaping up to be a strong cash flow generator with our model pointing to an average of $81MM of operating cash flow and $71MM in free cash flow annually. The company plans on holding eight diamond tenders and three exceptional stone tenders during the year. The timing of these tenders will be based on Karowe’s production profile as well as commercial decisions to maximize diamond revenue, however, we expect they will occur in Q2, Q3 and Q4. In February 2014, the Company approved a dividend policy, declaring its first semi-annual dividend of C$0.02 per share. The board has also approved the issuance, from time to time, of a special dividend based on revenues generated from exceptional stone tenders, subject to the Company's overall financial position and other factors existing at the time under consideration. The strong cash flow and low sustaining capital requirements (the mining fleet is contracted) supports a sustained dividend with room to grow. As for special dividends, while our cash flow model could support over C$0.10 per share in additional annual dividends, we expect it to be much more restrained in the short term, allowing Lucara to build a war chest of cash to fuel further growth through M&A.

Figure 24: Cash Flow Profile ($000's)

Source: Company Reports, DCM

($750,000)

($500,000)

($250,000)

$-

$250,000

$500,000

$750,000

$1,000,000

($75,000)

($50,000)

($25,000)

$-

$25,000

$50,000

$75,000

$100,000

k U

S$

k U

S$

Cash from operating activities Cash from investing activitiesCash in financing activities, net of dividend Cash paid as dividendsCash balance @ EOY (RHS)

We believe that Mothae is unlikely to be developed on its own in the near term but could benefit greatly from synergies with Gem's neighboring Letseng Mine

Karowe is shaping up to be a strong cash flow generator with our model pointing to an average of $81MM of operating cash flow and $71MM in free cash flow annually supporting a semi-annual dividend with room to grow

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 21

VALUATION

Our NAV and target price are summarized in Figure 25 below. Now at steady-state commercial production, throughput at Karowe should remain on the order of 2.5MM tonnes per year for an average annual production of 420,000 carats, generating approximately $81MM in free cash flow per year. Sustaining capex should be less than $4MM annually. We value Lucara based on a discounted cash flow analysis of Karowe applying a 5% discount rate resulting in a project NPV of $885MM. The company has no debt. Our diluted shares outstanding number considers all in-the-money options and warrants and we do not expect any equity issues in the near-medium term. As a result we arrive at a net asset value for Lucara of $881MM or $2.30 per share.

Figure 25: Net Asset Value Calculation

Source: Company Reports, DCM

On an operating cash flow basis, we expect Lucara to generate $94MM in 2014 and $84MM in 2015 or C$0.28 and C$0.25 per share respectively. Over the life of mine it should average $81MM or C$0.24 per share. Similar-sized diamond and precious metals producers trade at 4x to 12x 2015 CFPS. Given the 13-year reserve life at Karowe, upside potential from additional tonnes and higher diamond valuations, and special dividend potential we would expect Lucara to trade at the higher end of this range. On a cash flow basis, we would apply a 10x FY2015 CFPS for a target of $2.75 per share.

However, in the context of other diamond producers we see NAV as a more appropriate valuation metric. Lucara currently trades at 1.18x our NAVPS estimate which is a premium compared to other diamond and precious metals peers which trade at 0.6x to 1.1x NAVPS (Figure 26). In our view, a premium is justified given that the high margin, high value operation has ongoing potential for positive surprises in the form of very large stones which increases with the completion of the ongoing plant modifications. In addition, there is good potential to almost double the mine life with existing resource at depth and development potential for Mothae. The premium valuation also affords LUC with valuable stock with which to pursue accretive M&A opportunities. As such, we apply a 1.30x premium multiple to NAV to arrive at a 12-month NAV-based target price of C$3.00 per share.

Lucara Diamond Corp. Net Asset Value BreakdownDiscount

RateNAV

(MM C$)NAV per

shareKarowe, Botswana (100%) 5% $885 $2.31Total Producing Assets $885 $2.31Other Assets 5% $0 $0.00Total Corporate Adjustments 5% -$4 -$0.01Lucara Diamond Corp. Net Asset Value $881 $2.30

Target Price Value Multiple Weight Per ShareNet Asset Value $2.30 1.30x 100% $2.99

In our view, a premium valuation is justified given the high margin, high value operation, ongoing potential for large stones, expansion potential at depth and ability for accretive M&A opportunities

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 22

Figure 26: P/NAV Estimate Relative to Consensus

Source: Company Reports, DCM

To add further context for Karowe we can convert our estimates into gold equivalent ounces, which provides greater familiarity to some investors. On a gold equivalent basis (assuming $1350/oz), the operation at Karowe is the equivalent of a 160k oz per year producer with cash costs of $700/oz from an open pit reserve of 2.4MM oz grading 2.1 g/t.

UPSIDE & SENSITIVITIES

The mine life at Karowe could be almost doubled by moving to an underground operation as an additional 34MM tonnes of material resides in resource below the 324 metre lower level of the pit. We anticipate feasibility work to be conducted in the next couple years but would expect the cost of sinking a production shaft and related development to be less than $200MM. Assuming 30MM additional tonnes, this would add up to 12-years to the mine life and ~$0.80 to our NAVPS. Shorter term growth would have to come from development of Mothae and/or M&A (discussed below).

Additional upside potential to our target could come from higher realized diamond prices. We expect the average diamond price to top out in the $565 per carat range but the recovery of 400-500 carat stones, soon to be a realistic expectation with the ongoing modifications to the plant, could add another step-up to the diamond pricing curve. In Figure 27 below, we show our NAV sensitivity to diamond price, which could see upside from a coarser distribution of stones. It also highlights the sensitivity to major factors such as the diamond price growth assumption and exchange rate. Investors should expect ongoing volatility in diamond values quarter to quarter which is normal for a coarse distribution.

0.59x

0.83x 0.90x 0.95x 0.95x 0.98x

1.18x 1.23x

0.00x

0.20x

0.40x

0.60x

0.80x

1.00x

1.20x

1.40x

DDC-CA(DCM)

RDI-CA PDL-LON GEMD-LON Producer Avg. ALRS-MIC LUC-CA(DCM)

LUC-CA

*Consensus estimate for companies not covered by DCM

The mine life at Karowe could be doubled by moving to an underground operation with additional upside potential from higher realized diamond prices.

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 23

Figure 27: NAVPS Sensitivity to Changes Key Inputs

Source: Company reports, DCM

Our valuation is also sensitive to assumptions regarding annual growth in diamond price and changes in the United States/Canadian currency exchange rate. We currently assume an annual diamond price growth rate of 2.5% per year for the "normal" goods found in the North Lobe, in line with global GDP growth and an USD:CAD exchange rate of 0.9:1. For the Central and South Lobes we apply a lower 1.5% price growth rate on the assumption that the increased availability of these goods may impair the upside somewhat.

M&A OPPORTUNITIES

With an established high margin operation, growing cash, no debt and a high market value, Lucara is well-positioned to pursue M&A. Assuming it wants to maintain its position as a large stone producer, like-sized candidates include Gem Diamonds (GEMD-LN, not covered) and Stornoway Diamond (SWY-T; BUY, C$1.60 target, High Risk). Gem is the most obvious candidate, as its Letseng mine in Lesotho would give Lucara tighter control of the large diamond market as well as offer synergies with the Mothae project that could bring it from marginal to economic. Stornoway is attractive for its Renard Project in Quebec which we expect to yield similar upside as Karowe given its large stone size distribution. On the junior side, we see Peregrine Diamonds (PGD-T; BUY, Speculative Risk) and North Arrow (NAR-V; BUY, Speculative Risk) as potential candidates as well. Peregrine's Chidliak Project has demonstrated high grades and high values and over the next 18-months should be ready to move into the development stage similar to where Karowe was when acquired by Lucara. North Arrow's Qilalugaq project could be very attractive and development track ready following a successful bulk-sample program this summer.

Figure 28: Potential Acquisition Targets For LUC

Source: Company reports, DCM

Value NAV NAV Growth NAV NAV FX NAV NAVChange $2.30 Change Rate $2.30 Change Rate $2.30 Change60% $0.83 -64% -1.0% $1.88 -18% 1.04 $1.99 -14%70% $1.20 -48% -0.5% $1.94 -16% 1.02 $2.03 -12%80% $1.57 -32% 0.0% $1.99 -13% 1.00 $2.07 -10%85% $1.75 -24% 0.5% $2.05 -11% 0.98 $2.11 -8%90% $1.93 -16% 1.0% $2.11 -8% 0.96 $2.16 -6%95% $2.12 -8% 1.5% $2.17 -6% 0.94 $2.20 -4%98% $2.23 -3% 2.0% $2.24 -3% 0.92 $2.25 -2%100% $2.30 0% 2.5% $2.30 0% 0.90 $2.30 0%102% $2.38 3% 3.0% $2.37 3% 0.88 $2.35 2%105% $2.49 8% 3.5% $2.44 6% 0.86 $2.41 5%110% $2.67 16% 4.0% $2.51 9% 0.84 $2.47 7%115% $2.85 24% 4.5% $2.58 12% 0.82 $2.53 10%120% $3.04 32% 5.0% $2.65 15% 0.80 $2.59 13%130% $3.41 48% 5.5% $2.73 18% 0.78 $2.66 16%140% $3.77 64% 6.0% $2.81 22% 0.76 $2.73 19%

Diamond Value (US$/ct) Diamond Value Growth USD:CAD Exhange Rate

CompanyEV

($MM)Project of Potential Interest Status

Resource (MMcts)

Grade (cpht)

Value (US$/ct) Rationelle for Acquisition

Capex Estimate

GEM Diamonds $422 Letseng (70%) Production 5.0 1.7 $2,074 large stones, synergies with Mothae Built

Stornoway $363 Renard (100%) Construction 23.8 89.0 $222 large deposit, long life, expected large stones, geographical diversification

Fully Financed

Peregrine $56 Chidliak (100%) Evaluation 7.5 258.0 $213 high grade, high value, large stone potential

$300-600 MM

North Arrow $27 Qilalugaq (40%) Evaluation 26.1 53.6 n/a large resource, potential high value "fancies"

$700-900 MM

With an established high margin operation, growing cash, no debt and a high market value, Lucara is well-positioned to pursue M&A.

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 24

RISKS

• Diamond Price Risk: Diamond prices are sensitive to global diamond supply and demand factors as well as the specific shapes, colours, clarity and carat size of diamonds recovered. Fluctuations in either area may lead to fluctuations in financial performance, and deviation from our expectations. We model a CAGR in global diamond values of 2.5% for regular stones and 1.5% for larger goods, which we deem conservative in context of historic rates and current industry guidance. Historically diamond values have been driven by growth in GDP, disposable income and consumer confidence, all of which are improving. Specific to Lucara, the large high quality stones contribute about 60% to our expected diamond values. As such, any change to this market could have a negative impact on NAV.

• Mineral inventory estimates: For producers and developers, there is a risk that production will not reconcile with resource and reserve estimates. Our valuation is predicated on currently available NI 43-101 technical reports, available bulk sample and drill results, as well as recent sales data. Karowe has so far exceeded expectations based on the repeated occurrence of large high quality stones that contribute about 60% to our estimated diamond value. As a result, the loss of big stones from resource would have a negative impact to our NAV.

• Production risks: Our valuation is based on a variety of assumptions including production and recovery rates, capital costs, operating costs and mine life backed by technical reports and comparable projects. Specific to Lucara, the large high quality stones contribute about 60% to our expected diamond values. As such, the loss of big stones during recovery could have a negative impact on NAV.

• Political Risk: Lucara's main asset, Karowe, is located in Botswana. The country's economy relies heavily on diamond mining, which has taken it from one of the poorest nations in Africa in the 1950s to one of the richest. Botswana rates among the top countries in the world for mining investment, such that Standard and Poor’s has assigned the country an “A” credit rating. Botswana has established high-quality public institutions and legal systems with very low corruption.

• Exploration risk: Lucara has limited exploration but may ramp up exploration or acquire new properties. In some cases, the market may build in expectations for exploration success before the actual exploration work has taken place. In the event that results do not meet with the market’s expectation, the company’s shares may be negatively affected.

• Financing risk: Lucara has a strong balance sheet with growing cash and minimal sustaining capex. New growth plans could be funded out of cash flow and /or new debt. For M&A, the high valuation should be supportive of accretive acquisition.

CONCLUSION

We are initiating coverage on Lucara Diamond Corp. with a BUY rating and a 12-month target price of C$3.00 per share based on a 1.3x multiple to NAV. The startup of its Karowe diamond mine in Botswana has exceeded expectations consistently producing high value "specials" resulting in high margins and strong, sustainable cash flows. Lucara offers investors a semi-annual dividend offering a 1.6% yield and will likely increase this with a special dividend at year-end. With an established high margin operation, growing cash, no debt and a high market value, Lucara is also well-positioned to offer growth through M&A. Additional upside comes from expanded mine life and higher diamond price opportunities.

Initiating coverage with a BUY recommendation, High Risk and twelve month price target of C$3.00 per share

The main risk for Lucara is that Karowe stops yielding large stones.

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 25

MANAGEMENT BIOGRAPHIES

William Lamb, President, CEO & Director has over 20 years' experience in the mining operations and project development including De Beers as their Dense Medium Service Specialist and Metallurgical Superintendent he was responsible for process design and certain project management aspects of Canadian diamond projects. After completing an MBA through the Edinburgh Business School, Mr. Lamb joined the Lundin Group in May 2008 as the General Manager for Lucara Diamond Corp.

Paul Day, Chief Operating Officer is a mining engineer with over 22 years of operational experience in the sub-Saharan African mining industry in senior production and operational management positions within JCI, Anglogold Ashanti and Areva BG Mines.

Anthony George, Vice President Development is a mining engineer with over 27 years of experience in operations, design and construction. In his career with De Beers he was mine general manager on the team that brought the Victor open pit diamond project through feasibility, engineering and construction.

Dr. John Armstrong, Vice President Mineral Resources has over 25 years of combined experience in mineral exploration, mining and government. Dr. Armstrong has been involved in the planning and execution of successful diamond exploration and sampling programs ranging from generative to delineation and valuation.

Glenn Kondo, Chief Financial Officer has senior executive and corporate board experience in the mining industry, including many years with Anglo American. Mr. Kondo is a Chartered Accountant and holds a Bachelor of Commerce degree from the University of Toronto.

DIRECTORS BIOGRAPHIES

Lukas H. Lundin, Chairman graduated from the New Mexico Institute of Mining and Technology (Engineering). Throughout his career, he has been responsible for various resource discoveries, including the multi-million ounce Veladero gold deposit. Mr. Lundin has also led numerous companies through very profitable business acquisitions and mergers; most recently the $9.2 billion sale of Red Back Mining Inc. Mr. Lundin currently sits on the Board of a number of publicly traded companies.

Paul K. Conibear has over 30 years of experience in the mining industry. His background includes 18 years of project and construction management across a diverse range of minerals projects. For the last 12 years he has held public company executive management and director's positions with the Lundin group of companies. Mr. Conibear also serves as President, CEO & Director of Lundin Mining.

Richard P. Clark is a lawyer who practiced mining and securities law in British Columbia from 1987 to 1993. For the past ten years Mr. Clark has been a senior executive with the Lundin Group of Companies.

Brian Edgar has been active in public markets for over 25 years. Mr. Edgar serves on the Board of a number of public companies.

Eira Thomas is a respected Canadian geologist with a highly successful career in the mining industry. She served as a geologist with Aber Resources Ltd. (now Dominion Diamond Corporation) from 1992 to 1997, leading the field exploration team.

Marie Inkster is the Chief Financial Officer of Lundin Mining Corporation and has held positions of increasing responsibility in a number of publicly traded companies.

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 26

Figure 29: Assortment of Lucara Specials sold at its Exceptional Stone Tenders Shown to Scale

Source: Company Reports, DCM

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 27

Lucara Diamond Corp.Rating BUY Basic Shares (MM) 378.4 Dundee Capital Markets Dundee Capital MarketsRisk High Diluted Shares (MM) 382.5 Matthew O'Keefe, MSc, MBA Erik BermelTarget Price $3.00 Basic Mkt Cap (MM C$) C$1,029 647-253-1131 647-253-1112Share Price $2.72 Enterprise Value (MM C$) C$970 [email protected] [email protected]

OPERATING STATISTICS BALANCE SHEET2013A 2014E 2015E 2016E 2017E 31-Dec (MM US$) 2013A 2014E 2015E 2016E 2017E

Gross Ore Mined 2.4 2.28 2.54 2.50 2.48 AssetsGross Diamonds Prod. (MM cts) 0.4 0.42 0.45 0.43 0.42 Cash and Equivalents $49 $72 $133 $191 $240Net Diamonds Prod. (MM cts) 0.44 0.42 0.45 0.43 0.42 Product Inventory $21 $23 $23 $23 $23Average Grade, net (cpht) 19 18 18 17 17 Other Current $4 $3 $3 $3 $3Rock Value (US$/t) $77 $105 $101 $98 $92 Current Assets $74 $98 $160 $218 $267Diamond Value (US$/ct) $409 $574 $574 $562 $549 Mineral Properties $173 $213 $202 $189 $174

Restricted Cash/notes $0 $0 $0 $0 $0MINE & FINANCIAL PROFILE Other LT $0 $0 $0 $0 $0Karowe, Botswana (100%) Total Gross Diamonds Mined (k cts) TOTAL ASSETS $247 $311 $362 $406 $441

LiabilitiesCurrent debt/debentures $0 $0 $0 $0 $0Long-term debt/debentures $0 $0 $0 $0 $0Future income tax liabilities $14 $17 $17 $17 $17Provision for reclamation $15 $15 $15 $15 $15Other Liabilities $31 $26 $26 $26 $26TOTAL LIABILITIES $60 $58 $58 $58 $58LIABILITIES AND EQUITY $247 $311 $362 $406 $441

INCOME STATEMENT31-Dec (MM US$) 2013A 2014E 2015E 2016E 2017ETotal revenue $181 $240 $257 $244 $229Operating costs (net dep) $65 $94 $121 $121 $120Depreciation/amort. $15 $14 $19 $20 $20Exploration expenses $1 $2 $4 $2 $2

Karowe, Botswana (100%) Gross Ore Mined & Processed (k t) Administration & other $11 $8 $7 $7 $7EBITDA $103 $136 $124 $114 $100EBIT $88 $122 $105 $94 $79Interest payments -$4 $0 $0 $0 $0EBT $84 $122 $105 $94 $79Current Tax expense $15 $44 $41 $36 $31Deferred Income tax expense $0 $0 $0 $0 $0Net earnings (loss) $65 $76 $64 $58 $48Adjusted net earnings (loss) $65 $76 $64 $58 $48EPS $0.19 $0.22 $0.19 $0.17 $0.14Average Shares 376.3 377.8 378.4 378.4 378.4

CASH FLOW STATEMENT31-Dec (MM US$) 2013A 2014E 2015E 2016E 2017ENet Income (loss) for the period $65 $76 $64 $58 $48Depreciation & Amortization $15 $14 $19 $20 $20Other $19 $4 $0 $0 $0

NET ASSET VALUE Operating Cash Flow $100 $94 $84 $78 $69(C$MM) C$/share Operating CFPS $0.29 $0.28 $0.25 $0.23 $0.20

Karowe, Botswana (100%) $885 $2.31 Changes in working capital -$1 -$4 $0 $0 $0Total Producing Assets $885 $2.31 Cash from Operations $99 $90 $84 $78 $69Other Assets $0 $0.00 Capital Expenditure -$8 -$55 -$8 -$6 -$6Total Corporate Adjustments -$4 -$0.01 Other $0 $0 $0 $0 $0Lucara Diamond Corp. Net Asset Value $881 $2.30 Cash from Investing -$8 -$55 -$8 -$6 -$6DCF Target Multiple 1.3x Equity Financing $0 $0 $0 $0 $0Share Price Target $3.00 Debt repayment/drawdowns -$55 $0 $0 $0 $0

Other $0.5 -$14 -$14 -$14 -$14VALUATION DATA Cash from Financing -$54.0 -$14 -$14 -$14 -$14Relative F2014E F2015E F2016E F2017E F2018EP/CF 9.8x 11.1x 11.9x 13.5x 15.0x Change in Cash & Equiv. $36 $22 $61 $58 $49EV/EBITDA 6.4x 7.0x 7.6x 8.8x 9.9x Cash, Beginning of Period $13 $49 $72 $133 $191P/E 11.0x 13.0x 14.3x 17.2x 20.5x Cash, End of Period $49 $72 $133 $191 $240

P/NAV EV/ct EV/ValueLucara Diamond Corp. 1.18x $86.21 0.20x FCF before financing (CFO+CFI) $92 $40 $75 $72 $63

Net free cash flow $36 $36 $75 $72 $63Operating CFPS (C$/sh) $0.29 $0.28 $0.25 $0.23 $0.20

DIAMOND RESERVES, RESOURCESSize Grade Carats Value TOP SHAREHOLDERS

(MMt) (cpht) (MM) (US$/ct) Institution/Insider Shares Value %Karowe, Botswana (100%) JPMorgan Asset Management (UK) Ltd. 22.3 $56 5.9%Total Probable 33.1 16 5.1 $394 O'Shaughnessy Asset Management LLC 4.5 $11 1.2%Total Indicated 48.1 16 7.6 $393 TD Asset Management, Inc. 3.2 $8 0.9%Total Inferred 21.0 14 3.0 $412 Canada Pension Plan Investment Board 3.1 $8 0.8%Total 69.1 15 10.7 $399 Pembroke Management Ltd. 3.0 $7 0.8%

Total Institutional Ownership 53.9 $136 14.3%Mothae, Botsawana (75%) 39.0 3 1.0 $1,040 Total Insider Ownership 80.6 $203 21.3%

Total 134.5 $339 35.6%

Source: Company reports, Bloomberg, Factset, Dundee Capital Markets estimates

$0

$100

$200

$300

$400

$500

$600

$700

$800

- 50

100 150 200 250 300 350 400 450 500

North Lobe Centre Lobe South Lobe

Stockpile Tota l Avg. Diamond Value (US$/ct) Tota l Avg. Diamond Value (US$/ct)

On-site cash costs (US$/ct)

$0

$20

$40

$60

$80

$100

$120

-

100

200

300

400

500

600

700

800

Q12013A

Q22013A

Q32013A

Q42013A

Q12014A

Q22014E

Q32014E

Q42014E

Q12015E

Q22015E

Q32015E

Q42015E

Q12016E

Q22016E

Q32016E

North Lobe Centre Lobe South LobeStockpile Total Rock Value (US$/t) On-site cash costs (US$/t)

DUNDEE CAPITAL MARKETS Page | 28

Dominion Diamond Corp. (DDC-T: C$15.23), (DDC-NYSE: US$14.16)

July 17, 2014

Matthew O'Keefe, MSc, MBA / (647) 253-1131 [email protected]

Erik Bermel / (647) 253-1112 [email protected]

BUY, High Risk Dundee target: C$20.50

Lac de Gras: A Pretty Kettle of Fish

We are initiating coverage on Dominion Diamond Corp. with a Buy rating and a 12- month target price of C$20.50 per share. Dominion recently consolidated the Lac de Gras region, a world class diamond district and now have ownership in two of the largest and richest diamond mines in the world. Both have underappreciated development pipelines which could expand the existing eight year mine life.

• Near Term Uncertainty Clouding Long Term Potential: Dominion’s next two years are filled with several capital intensive but manageable expansion projects and a relatively uninteresting production and cash flow profile. Looking past the next two years, production and cash flow are set to double in FY2017 with the high grade, 75% margin Misery pipe giving boost to operations.

• Jay Will Be A Game Changer: Approval of the high grade, high value Jay pipe would extend Ekati’s mine life from 8 years to 18 years while delivering reasonable 39% margins LOM. In addition, it should push back Ekati’s $435MM reclamation liability by ten years.

• Reclamation Liability Manageable: The Company will likely be required to post an additional $145MM in reclamation collateral for Ekati and its $60MM share for Diavik. In addition to $212MM in cash on hand, the company has only $4.3MM in debt and the possibility to use its ownership in Diavik as collateral. We expect clarity from the territorial government by year end.

• Larger Risk Offers Bigger Reward: Dominion offers compelling value currently trading at 0.59x NAV vs peers at 0.95x should expansion at Ekati go according to plan. Even at a discounted 0.8x target multiple, our C$20.50 target price offers a healthy risk-adjusted return.

• A-21 Provides Additional Upside: Construction of A-21 would rejuvenate an otherwise declining production profile at the Diavik mine, filling mill capacity drastically improving costs and increasing profitability. Diavik’s operator Rio Tinto is expected to make a construction decision on the project by year end.

Target Price Valuation Methodology: Our C$20.50 target price is based on 0.80x our C$25.66 NAVPS, which is a discount to similar diamond producers trading at 0.95x. As uncertainty surrounding its future mine life is resolved, capital and reclamation bond commitments clarified and construction decisions for Jay and A-21 are made, we believe Dominion Diamond stock should trade up, in line with its peers. Our target implies an 8.1x 2015E price to cash flow multiple, valuing Dominion in line with diamond producers who trade at an average of 7.1x 2015E cash flow.

DDC: Price/Volume Chart

Source: Factset

Company Description Dominion has ownership in two high grade diamond operations in the Northwest Territories, Canada. Dominion's share of production from its two world class assets, Ekati & Diavik, is approximately 4MM ct.

DDC-T New LastRating:Target:Risk:NAVPS:

Company DataPrice (07/15/14):52-Week Range:Market Capitalization ($MM):Enterprise Value ($MM):Shares Outstanding - Basic (MM):Shares Outstanding - FD (MM):Avg Daily Volume (3 Mos) (000s):Cash ($MM):Debt ($MM):Dividend YieldFiscal Year-End:Est. (MM) 2014 A 2015 E 2016 ENet Prod. 4.0 4.1 3.9Grade (cpht) 132 93 82Value US$/ct 188 217 195Cost US$/t 128 128 130Revenue ($) 752 900 752CFO ($) 160 269 185EBITDA ($) 681 338 198CFPS (C$) 2.09 3.43 2.36Valuaion 2014 A 2015 E 2016 EP/CF 7.3x 4.4x 6.5xEV/EBITDA 1.4x 2.7x 4.7x

P/NAV EV/ct EV/Value0.59x 6.83 0.03x

All Figures in US$ Unless Otherwise NotedSource: Factset, Company reports, Bloomberg, DCM

C$12.31-16.83

BUYC$20.50

HighC$25.66

C$15.23

C$5n/a

31-Jan

C$1,297C$1,028

8588

110C$273

Oct-12 Apr-13 Oct-13 Apr-14

12

13

14

1516

17

00.8

Dominion Diamond Corporation (DDC-CA)

Volume (Millions) Price (CAD)VolumeDominion Diamond Corporation

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 29

INTRODUCTION

Dominion Diamond Corp. is a Canadian diamond mining company with ownership in two major producing diamond mines located in the Lac De Gras region, approximately 300km northeast of Yellowknife in the Northwest Territories (Figure 30).

Figure 30: Dominion Diamond Project Location

Source: Company Reports, DCM

The company operates its recently acquired Ekati Mine and is in the process of increasing its ownership interest from 80% to 90% in the core zone, which includes the current operating mine and other permitted kimberlite pipes, and the surrounding buffer zone mineral claims, which hold the Jay pipe, from 58.8% to 68.8% (Figure 31). It also has a 40% interest in the high grade nearby Diavik Mine, which is 60%-owned and operated by Rio Tinto (RIO-LON, not covered). The Ekati and Diavik mines produced 8.6MM carats in FY2014 (4MM carats net to Dominion), which was approximately 6.5% of 2013 global production. Of note, Dominion's financial year ends on January 31.

Two world class high grade diamond mines in Canada's Northwest Territories

Diamond Sector July 17, 2014

DUNDEE CAPITAL MARKETS Page | 30

Figure 31: Ownership Interest Breakdown

Source: Company Reports DCM

In 2013, Dominion Diamond transitioned from a diamond marketer and retailer to pure play diamond miner by purchasing the Ekati diamond mine from BHP Billiton for $500MM cash and selling its Harry Winston luxury brand to The Swatch Group for $750MM. The transactions left the company on solid financial footing with two producing assets in a premiere diamond district. The strategy ahead is to optimize existing operations and pursue the prospective expansion opportunities on the large, well-endowed land package (Figure 32).

Figure32: Dominion Diamond Property Map

Source: Company Reports, DCM

Ekati

Core Zone Buffer Zone

10%

Charles Fipke

31.2%

Archon (AC

S-T)

10%

Charles Fipke

10%

Stewart

Blusson

80%

Dom

inion D

iamond

58.8%

Dom

inion D

iamond

Diavik Lac De Gras Exploration JV