Embed Size (px)

Citation preview

A

COUNTRY STUDY AND REPORT AND COMBINED SUMMARY OF

SEMESTER IV WORK

ON

Different Industries and Sectors of Singapore

Submitted to

Gujarat Technological University

IN PARTIAL FULFILLMENT OF THE

REQUIREMENT OF THE AWARD FOR THE DEGREE OF

MASTER OF BUSINESS ASMINISTRATION

Submitted by

___________________________________________________________________________

___

Marwadi Education Foundation’s Group of Institutions

MBA PROGRAMME

Affiliated to Gujarat Technological University Ahmedabad

May, 2012

SUMMARY OF WORK DONE IN SEM-4

AVIATION IN SINGAPORE

MEANING

Aviation is the design, development, production, operation, and use of aircraft,

especially heavier-than-air aircraft. Aviation is derived from avis, the Latin word for

bird.

HISTORY

There are early legends of human flight such as the story of Icarus, and Jamshid in

Persian myth, and later, somewhat more credible claims of short-distance human

flights appear, such as the flying automaton of Archytas of Tarentum (428–347 BC),

the winged flights of Abbas IbnFirnas (810–887), Eilmer of Malmesbury (11th

century), and the hot-air Passarola of BartolomeuLourenço de Gusmão (1685–

1724).

The modern age of aviation began with the first untethered human lighter-than-air

flight on November 21, 1783, in a hot air balloon designed by the Montgolfier

brothers.

In 1799 Sir George Cayley set forth the concept of the modern airplane as a fixed-

wing flying machine with separate systems for lift, propulsion, and control. Early

dirigible developments included machine-powered propulsion (Henri Giffard, 1852),

rigid frames (David Schwarz, 1896), and improved speed and maneuverability

(Alberto Santos-Dumont, 1901).

Great progress was made in the field of aviation during the 1920s and 1930s, such

as Charles Lindbergh's solo transatlantic flight in 1927, and Charles Kingsford

Smith's transpacific flight the following year. One of the most successful designs of

this period was the Douglas DC-3, which became the first airliner that was profitable

carrying passengers exclusively, starting the modern era of passenger airline

service.

By the 1950s, the development of civil jets grew, beginning with the de Havilland

Comet, though the first widely-used passenger jet was the Boeing 707, because it

was much more economical than other planes at the time.

Since the 1960s, composite airframes and quieter, more efficient engines have

become available, and Concorde provided supersonic passenger service for more

than two decades, but the most important lasting innovations have taken place in

instrumentation and control. The arrival of solid-state electronics, the Global

Positioning System, satellite communications, and increasingly small and powerful

computers and LED displays, have dramatically changed the cockpits of airliners

and, increasingly, of smaller aircraft as well.

On June 21, 2004, SpaceShipOne became the first privately funded aircraft to make

a spaceflight, opening the possibility of an aviation market capable of leaving the

Earth's atmosphere.

BRANCHES OF AVIATION

Civil Aviation is one of two major categories of flying, representing all non-military

aviation, both private and commercial. Most of the countries in the world are

Aviation

Civil Aviation

General Aviation

Civil Transport

Military Aviation

members of the International Civil Aviation Organization (ICAO) and work together to

establish common standards and recommended practices for civil aviation through

that agency.

Civil aviation includes two major categories:

Scheduled Air Transport, including all passenger and cargo flights operating

on regularly scheduled routes; and

General Aviation (GA), including all other civil flights, private or commercial

General Aviation includes all non-scheduled civil flying, both private and

commercial. General aviation may include business flights, air charter, private

aviation, flight training, ballooning, parachuting, gliding, hang gliding, aerial

photography, foot-launched powered hang gliders, air ambulance, crop dusting,

charter flights, traffic reporting, police air patrols and forest fire fighting.

Each country regulates aviation differently, but general aviation usually falls under

different regulations depending on whether it is private or commercial and on the

type of equipment involved.

Many small aircraft manufacturers serve the general aviation market, with a focus on

private aviation and flight training.

Military Aviation is the use of aircraft and other flying machines for the purposes of

conducting or enabling warfare, including national airlift (cargo) capacity to provide

logistical supply to forces stationed in a theater or along a front.

Air power includes the national means of conducting such warfare including the

intersection of transport and war craft. The wide variety of military aircraft includes

bombers, fighters, fighter bombers, transports, trainers, and reconnaissance aircraft.

These varied types of aircraft allow for the completion of a wide variety of objectives.

Types of military aviation

Fighter aircraft's primary function is to destroy other aircraft. (e.g. Sopwith

Camel, A6M Zero, F-15, MiG-29, Su-27, and F-22).

Ground attack aircraft are used against tactical earth-bound targets. (e.g.

Junkers Stuka, A-10, Il-2, J-22 Orao, AH-64 and Su-25).

Bombers are generally used against more strategic targets, such as factories

and oil fields. (e.g. Zeppelin, Tu-95, Mirage IV, and B-52).

Transport aircraft are used to transport hardware and personnel. (e.g. C-17

Globemaster III, C-130 Hercules and Mil Mi-26).

Surveillance and reconnaissance aircraft obtain information about enemy

forces. (e.g. Rumpler Taube, Mosquito, U-2, OH-58 and MiG-25R).

Unmanned aerial vehicles (UAVs) are used primarily as reconnaissance fixed-

wing aircraft, though many also carry payloads. Cargo aircraft are in

development. (e.g. RQ-7B Shadow, MQ-8 Fire Scout, and MQ-1C Gray

Eagle).

Missiles deliver warheads, normally explosives, but also things like leaflets.

AVIATION IN SINGAPORE

Aviation in Singapore is a key component of the Singaporean economy in its quest to

be a transport hub of the Asian region. Besides currently the sixth busiest airport and

the fourth busiest air cargo hub in Asia, the Singaporean aviation industry is also a

significant aerospace maintenance, repair and overhaul centre.

Pre War

In 1937, the Wearne Brothers launched the first commercial air service between

Singapore and Malaya. It was called Wearne Air Services. On 28 June 1937, a de

Havilland Dragon Rapide aircraft, the Governor Raffles, took off from Singapore to

Kuala Lumpur and Penang.

Post War

Malayan Airways Limited (MAL)was established on 1 May 1947, by the Ocean

Steamship Company of Liverpool, the Straits Steamship Company of Singapore and

Imperial Airways. The airline's first flight was a chartered flight from the British Straits

Settlement of Singapore to Kuala Lumpur on 2 April 1947 using an Airspeed Consul

twin-engined airplane.

Federation (1963)

When Malaya, Singapore, Sabah and Sarawak formed the Federation of Malaysia in

1963, the airline's name was changed, from "Malayan Airways" to "Malaysian

Airways". MAL also took over Borneo Airways. In 1966, following Singapore's

separation from the federation, the airline's name was changed again, to Malaysia-

Singapore Airlines (MSA).

Split (1972)

MSA ceased operations in 1972, when political disagreements between Singapore

and Malaysia resulted in the formation of two entities: Singapore Airlines and

Malaysian Airlines System.

A study conducted in 2001 showed the aviation industry contributing about 5.5%, or

S$7.9 billion, to Singapore’s gross domestic product. It provided one in 20 jobs in the

country, or one in 17 jobs if the indirect impact of the sector on the rest of the

economy is taken into account. A different set of measures by the Economic

Development Board showed the industry having an output of S$3.8 billion in 2003,

contributing 1.2% to the GDP and employing over 11,000 people. In 2004, the

industry grew 16% to hit a record high of S$4.5 billion.

AVIATION IN INDIA

The Indian Aviation Industry is among the world’s fastest growing industries. It has

undergone huge transformation following the liberalization of the aviation industry in

India. Once owned by the Government, the aviation sector of India is now privately

owned with full service airways and affordable carriers. Almost 75% of the domestic

aviation sector consists of the private airlines.

Indian aviation industry ranks 4th in the world after USA, China, and Japan in terms

of domestic passenger volume, as per statistics released by Ministry of Civil Aviation.

Industry experts have predicted that not less than 50 million passengers will be

served by the India aviation industry by 2015. Widening opportunities in India will

create room for over 69 foreign airlines entering the Indian aviation sector from about

49 countries.

History/Evolution

The Aviation industry in India began with the birth of Tata Airlines, through the

business relationship between Mr. NevillVintcent, a Royal Air Force pilot and Mr.

JRD Tata, the first Indian to get an A-license. Tata Airlines became Air India in

August 1946. In 1953, the Air Corporation Act nationalized all existing airline assets

and established the Indian Airline Corporation and Air India International for

domestic and international air services respectively.

<1953 Nine Airlines existed including Indian Airlines & Air India

1953 Nationalization of all private airlines through Air Corporations Act;

1986 Private players permitted to operate as air taxi operators

1994 Air Corporation act repealed; Private players can operate schedule

services

1995 Jet, Sahara, Modiluft, Damania, East West granted scheduled carrier

status

1997 4 out of 6 operators shut down; Jet & Sahara continue

2001 Aviation Turbine Fuel (ATF) prices decontrolled

2003 Air Deccan starts operations as India’s first LCC

2005 Kingfisher, SpiceJet, Indigo, Go Air, Paramount start operations

2007 Industry consolidates; Jet acquired Sahara; Kingfisher acquired Air

Deccan

2010 SpiceJet starts international operations 2011 Indigo starts international

operations, Kingfisher exits LCC segment

2012 Government allows direct ATF imports, FDI proposal for allowing foreign

carriers to pick up to 49% stake under consideration

GLOBAL AVIATION CHALLENGES 21ST CENTURY

Employee shortage

There is clearly a shortage of trained and skilled manpower in the aviation sector as

a consequence of which there is cut-throat competition for employees which, in turn,

is driving wages to unsustainable levels. Moreover, the industry is unable to retain

talented employees.

Rising fuel prices

As fuel prices have climbed, the inverse relationship between fuel prices and airline

stock prices has been demonstrated. Moreover, the rising fuel prices have led to

increase in the air fares.

Poor infrastructure

Infrastructure remains a major obstacle for the Indian airline industry today, which

was aggravated further due to the excess capacity created in good times.

Maintenance and traffic control (ATC) infrastructure is completely inadequate, if the

industry is expected to grow further. While steps are taken on this front in order to

upgrade the major airports of Mumbai, Delhi and Hyderabad remain security

concerns. Attract private sector investment will go a long way in the development

and maintenance of the infrastructure is crumbling because of the built up excess

capacity.

Regional connectivity

Although the industry is burdened with excess capacity, regional connectivity

continues to be poor, mainly because of lack of infrastructure. Industry experts

speculate that the increase in regional networking, concentrating instead in the

subways and the reallocation of the current fleet of routes where the demand to help

airlines manage their excess capacity.

High input costs

Apart from the above-mentioned factors, the input costs are also high. Some of the

reasons for high input costs are:-

Withholding tax on interest repayments on foreign currency loans for aircraft

acquisition. Increasing manpower costs due to shortage of technical personnel.

GLOBAL AVIATION STRATEGIES 21ST CENTURY

Understand reality of change and become “flexible”

Revitalize strategy

LCC, LC/HV, “Virtual” carriers

Customer focus (ask what they want)

Eliminate duplication

Organizational accountability

Staff relations into strength

Updating of airline systems

Build partnerships (alliances, interactive marketing)

Act decisively

Diversify the business (core and non-core)

Airlines “inventing” new ways to reduce future

costs and spending of capital

Increased efficiency

Dependent upon aviation (links local, national

and international economies)

Airlines must take control of business issues and

work in partnership (first time in history)

COST / EXPENSES FOR AIRLINES

The main 3 cost for the airlines are:

Fuel

Labor

Maintenance

EMPLOYMENT OPPORTUNTIES

The boom in the aviation sector is likely to generate nearly 2.5 lakh jobs by

the year 2014.

The study says that the civil aviation sector is also set to become a Rs

55,000-crore industry by the same time.

The industry is expected to add 130 airliners to its current fleet of 270

airliners, which would, in turn, increase manpower demand

The aviation industry employs about 3000 pilots and there is an immediate shortage

of 450 planes that will be added to the activity expanding Indian fleet in the next five

years and a shortage of additional 4,500 pilots stares us in the face (Total

requirement: 7500 pilots by2010)

Training to be a pilot can be a pretty expensive affair that can push you into a

financial air pocket! From April 2001 all DGCA-subsidized rates have been

discontinued. However, various states offer separate subsidies of varying amounts

up to the PPL stage. Considering the high cost of aviation fuel, you have to pay the

steep commercial rate, which is in the region of Rs.2750-3500 per hour. 40 free

flying scholarships are awarded to SC/ST trainee pilots every year. Under this

scheme, apart from free flying training, student pilots receive financialaid.

While a private school may charge as much as Rs.15-20 lakh, the cost of obtaining a

CPL in a government-sponsored school works out to Rs.10 lakh plus boarding and

lodging, which add up to another Rs.1,500/-p.m.

Salaries for commercial pilots are very attractive, ranging anywhere from Rs.40,

000/- to whopping Rs.4 lakh p.m., depending on the airline. Besides the obvious thrill

of going places and seeing the world in five-star comfort, there are several attractive

perks that go with the job.

QUALIFICATION NEEDED

Helicopter Pilots

Aptitude

There are certain attributes to be a Pilot. First of all, one should not be afraid of

heights and should have a passion to fly those machines.

A Pilot has to be quick thinker as he is the one who is responsible for the lives of

many. One should have patience, commitment, responsibility and self-confidence. A

lot of hard work, stamina, adaptability to follow difficult time schedules, good team

spirit etc., are also required in an aspirant. Most importantly, one must have

emotional stability in crisis situations.

Eligibility

To get a CPL, one should have passed 10+2 examination with Physics and

Mathematics and must be between the age of 18-30 years. The minimum height

should be 5 feet and eyesight 6/6.

Air Hostess / Flight Steward

The trouble free, comfortable and safe journey of a passenger is of prime importance

to the aviation sector. In this regard, it is an Air Hostess / Flight Steward whose role

becomes really crucial as they are the first one to welcome passengers aboard an

aircraft.

By the count, the various airlines in the country have almost 10,207 Cabin Crew

members in 2007-08 and the number is expected to grow to almost 20,284 by 2011-

12.

Aptitude:

To be an Air Hostess or a Flight Steward, one should have common sense, sense of

responsibility, initiative quality, friendly outgoing personality, politeness, physical

stamina and the capacity to work for long hours on the feet.

Eligibility

The educational qualification for an Air Hostess / Flight Steward training programme

is 10+2 or a graduate degree with a diploma / degree in Hotel Management or

Tourism Management.

Flight Purser

After three to five years, depending upon your performance, Flight Steward/Air

Hostess is eligible to become a Flight Purser. Your responsibilities increase as you

take over the charge of the Cabin Crew on board. Salaries generally get double up.

Ground Job:

You can join here directly or after having served on the flight for long, you can opt for

ground jobs in sections like staff-training and human resource management in the

corporate office.

Remuneration

The Cabin Crew can get up to Rs.40, 000 per month for domestic flights whereas

upto Rs.1, 50,000 for international flights on wide-bodied aircrafts. The ground staff

can also earn Rs.20, 000 - Rs.30, 000 per month.

TRENDS IN AVIATION

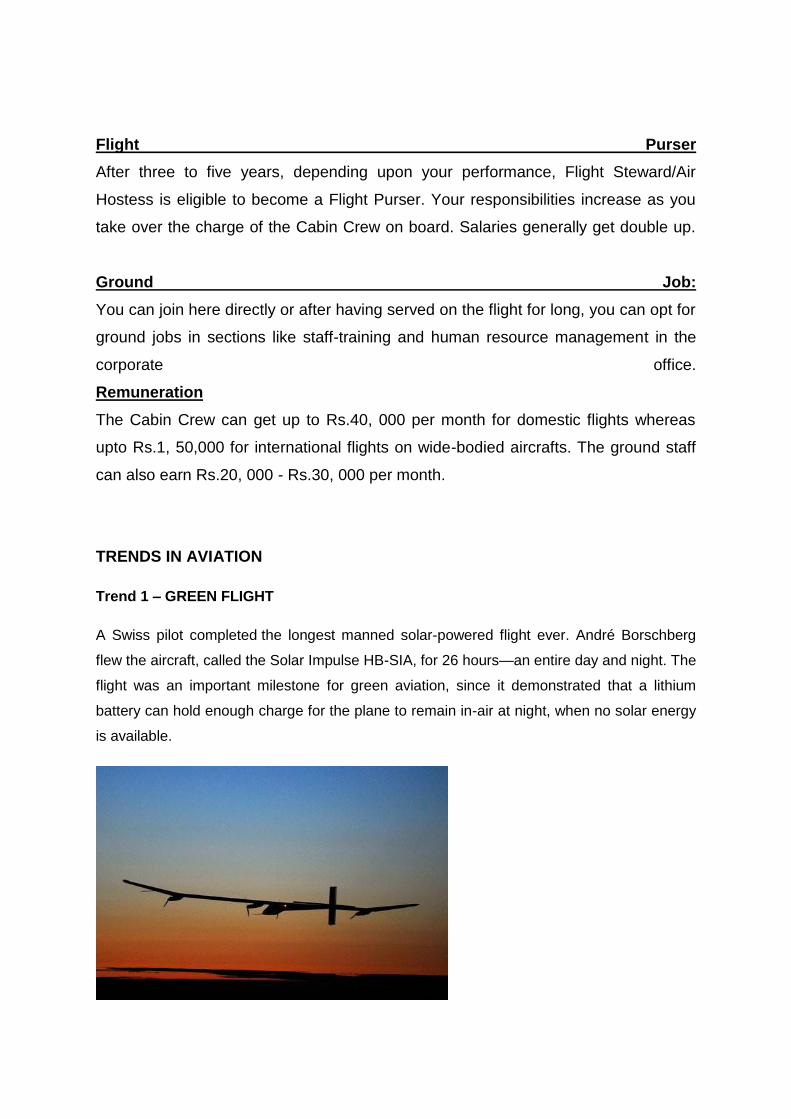

Trend 1 – GREEN FLIGHT

A Swiss pilot completed the longest manned solar-powered flight ever. André Borschberg

flew the aircraft, called the Solar Impulse HB-SIA, for 26 hours—an entire day and night. The

flight was an important milestone for green aviation, since it demonstrated that a lithium

battery can hold enough charge for the plane to remain in-air at night, when no solar energy

is available.

The HB-SIA is able to store solar energy for nighttime flight (source: Solar Impulse).

Trend 2 – DRONE FLIGHT

Watch out—that plane flying overhead soon might have no one in its cockpit. Unmanned

aircraft aren't a particularly new idea. The first was built in 1916, and remote-controlled

planes were becoming widely used by World War I. Today, unmanned aircrafts are

commonly used for war operations in many countries. But as drone planes grow more

capable of performing complex tasks and carrying passengers, unmanned commercial flight

seems to be on the horizon. In June, the Federal Aviation Administration announced its two-

year plan to bring unmanned flight to the American skies, possibly in a commercial form.

Commercial drone crafts could mean cheaper—and possibly safer—flights.

The search-and-rescue drone plane can find lost hikers more accurately than human-

controlled helicopters (source: Brigham Young University)

Trend 3 – FUTURISTIC FLIGHT

One of the trendiest topics in aviation is futuristic design and innovation. While green

energy and drone technology are often incorporated into futuristic plans, more

outlandish design quirks are also exciting engineers. A prime example is Airbus'

2030 Concept Plane, which features elements that airplanes might have 20 to 40

years from now. Conceptual components include self-cleaning cabins, smart seats

that form to passengers' bodies, and see-through walls, floors and ceilings.

Engineers even imagine holographic projections that could turn the cabin into a

home office or Zen garden.

Airbus conceptual plane features extra-long wings, a U-shaped tail and a highly

efficient fuselage.

REGULATORY AGENCIES& AUTHORITIES, Singapore

Singapore has mainly two regulatory i.e.:

CAAS – Civil Aviation Authority of Singapore

ICAO – International Civil Aviation Organization

Civil Aviation Authority of Singapore

The Civil Aviation Authority of Singapore is Singapore's Civil Aviation Authority

and a statutory board under the Ministry of Transport of the Singapore Government.

Its head office is located on the fourth storey of Terminal 2 of Changi Airport

inChangi.

The CAAS regulates civilian air traffic within the airspace jurisdiction of the Republic;

it is also the sole government agency to maintain the operational efficiency of the

airports in Singapore and to engage civilian air-service agreements with air-service

operators.

CAAS also operates the CAAS Air Traffic Control Service, which serves to ensure

faultless movements of civilian aircraft at Singapore’s airports and in the Singapore

Flight Information Region (FIR).

International Civil Aviation Organization

The International Civil Aviation Organization (ICAO) is a specialized agency of the

United Nations. It codifies the principles and techniques of international air

navigation and fosters the planning and development of international air transport to

ensure safe and orderly growth. Its headquarters are located in the Quartier

International of Montreal, Quebec, Canada.

Aviation LegislationIn Singapore

List of Legislation for the are described below:

Civil Aviation Authority of Singapore Act

Air Navigation Act

Carriage by Air Act

Carriage by Air (Montreal Convention, 1999) Act

Tokyo Convention Act

Hijacking of Aircraft and Protection of Aircraft and International Airports Act

International Interests in Aircraft Equipment Act 2009

The SINCAIR Programme

Ministry of Singapore has developed a program for aviation safety according to

international standards named, SINCAIR

The key objective of SINCAIR is to enhance aviation safety through the collection of

feedback on incidents that would otherwise not be reported through other channels,

or that may appear minor but may be useful for others to learn from the reporter's

experience and may even lead to changes in procedures or design. But it does not

eliminate the need for mandatory reporting of aircraft accidents and incidents to the

relevant authorities under the existing law.

The Singapore Confidential Aviation Incident Reporting (SINCAIR) programme is a

voluntary, non-punitive confidential incident reporting system established by the

AAIB. It provides a channel for the reporting of aviation incidents and safety

deficiencies while protecting the reporter's identity.

What does the SINCAIR Programme cover?

The SINCAIR Programme covers the following areas:

a. Flight Operations:

i. Departure/en route/approach landing

ii. Aircraft cabin operations

iii. Air proximity events

iv. Weight and balance and Performance

b. Ground Operations:

i. Aircraft ground operations

ii. Movement on the airport

iii. Fuelling operations

iv. Airport conditions or services

v. Cargo Loading

c. Air Traffic Management:

i. ATC operations

ii. ATC equipment and navigation aids

iii. Crew and ATC communications

d. Maintenance:

i. Aircraft maintenance

ii. Record keeping

e. Miscellaneous:

i. Passenger handling operations related to safety

REGULATORY AGENCIES & AUTHORITIES, India

Indian Regulatory agencies for the aviation are described below:

Director General of Civil Aviation

Bureau of Civil Aviation Security

Airports Authority of India

International Air Transport Association (IATA)

International Civil Aviation Organization

Directorate General of Civil Aviation (India)

The Directorate General of Civil Aviation is the Indian governmental regulatory body

for civil aviation under the Ministry of Civil Aviation. This directorate investigates

aviation accidents and incidents. It is headquartered along Sri Aurobindo Marg,

opposite Safdarjung Airport, in New Delhi.

Bureau of Civil Aviation Security

The Bureau of Civil Aviation Security was initially set up as a Cell in the

Directorate General of Civil Aviation (DGCA) in January 1978 on the

recommendation of the Pande Committee constituted in the wake of the hijacking

of the Indian Airlines flight on 10th September , 1976. The role of the Cell was to

coordinate, monitor, inspect and train personnel in Civil Aviation Security matters.

The BCAS was reorganized into an independent department on 1st April , 1987

under the Ministry of Civil Aviation as a sequel to the Kanishka Tragedy in June

1985. The main responsibility of BCAS are lay down standards and measures in

respect of security of civil flights at International and domestic airports in India.

Airports Authority of India

The Airports Authority of India (AAI) is an organization working under the Ministry of

Civil Aviation that manages most of the airports in India. The AAI manages and

operates 126 airports and 329 airstrips including 16 international airports, 89

domestic airports and 26 civil enclaves. The corporate headquarters(CHQ) are at

Rajiv Gandhi Bhawan, Safdarjung Airport, New Delhi. A V.P Agrawal is the current

chairman of the AAI.

International Air Transport Association

The International Air Transport Association (IATA) is an international industry trade

group of airlines headquartered in Montreal, Quebec, Canada, where the

International Civil Aviation Organization is also headquartered. The executive offices

are at the Geneva Airport in Switzerland.

IATA's mission is to represent, lead, and serve the airline industry. IATA represents

some 240 airlines comprising 84% of scheduled international air traffic. The Director

General and Chief Executive Officer is Tony Tyler. Currently, IATA is present in over

150 countries covered through 101 offices around the globe.

Legislations

Aviation Security (AVSEC) Law & Policy of India are as below:

The Aircraft Act, 1934

The Aircraft Rules, 1937

The Air Corporation Act, 1953

The Air Corporation Act, 1953,

The International Airports Authority Act, 1971,

The Carriage by Air Act, 1972,

The Tokyo Convention Act, 1975,

The Anti-Hijacking Act, 1982,

The National Airports Authority Act, 1985,

The Airports Authority of India Act,1994

Major Player of Singapore Aviation

Jetstar Asia Airways

Jett8 Airlines

Scoot

SilkAir

Singapore Airlines

Singapore Airlines Cargo

Tiger Airways

Valuair

Major Player of India Aviation

Air India

Blue Dart Aviation

Deccan Aviation

GoAir

IndiGo

Jet Airways

Kingfisher Airlines

SpiceJet

Marketing Strategies of Singapore Airlines

Singapore Airline

Cutting-edge quality Service strategy

o More cabin staff per seat than other airlines

o Free of charge amenities to Economy class passengers

o Singapore girl promotion – a sense of style and sophistication,

romance of travel

Aircraft Replacement Strategy

o Replacing new aircraft by every six year

o The youngest and modernist fleet in the industry

o Advanced, fuel-efficient version aircraft

Demographics strategy: Singapore Airlines offers premium flight fares

targeted to businessmen and the wealthy folks., who are willing to fork out

tens of thousands of dollars for a one-way First Class trip from Singapore to

Los Angeles

Air Asia

Social Media:AirAsia has taken giant and successful leaps on the social

media sphere, especially on Facebook and Twitter. The Malaysia-based

low-cost airline has a whopping 835,00 fans on their Facebook page and

100,000 followers on Twitter.

Demographics strategy: Air Asia’ key customer group are those who are

looking for cheap flights to countries located in Southeast Asia, and young

adults looking for a short weekend getaway trip to Thailand will most likely

choose budget airlines such as Air Asia due to their limited budget and choice

of destination.

ISSUES AND CHALLENGES IN SINGAPORE AVIATION:

Growth

We used to grow about 20% a year 20 years ago, and about 15 years ago in themid

teens. And as we mature, we grow at 6 to 8%. So, how do we continue toget high

growth? Acquisition is one of the strategies. But, we can’t expect to getthat kind of

high rate of growth by simply acquiring any airline. We must belooking for airlines

that are firstly in the growth stage, as we were, say 20 yearsago. That kind of airline

must have a very good product, in terms ofsustainability, and good management. So

in a sense we are trying to look forwhat we were like 20 years ago, and to invest in

that airline so that, with a strongmanagement, we don’t have to be distracted or

divert a lot of our managerialfocus and attention on the acquired airline. Then we can

focus on our ownorganic growth. So in that way we are not compromising or taking

awayanything from ourselves.

Managing Alliances

When you get into investment situations with your alliance or equity partners,how do

you deal with partners that are so different from your own company? Forexample,

Virgin,5 it’s a totally different relationship that you have to manage.It’s very new. How

do you get more people to be familiar with dealing withalliance and equity partners?

Because of growing numbers and working withpeople coming from different cultures

and backgrounds, we have to find betterways to manage these relationships. So we

have a new division, Alliance andPartnerships, just to cater to those relationship

issues that we want to get involvedwith.

Product Decisions

[The terrorist attacks of] 9/11 require us to think about our service classes: firstclass,

business class, two classes, three classes, two-and-one-half classes! What5 Virgin

Atlantic, in which SIA had acquired a 49% stake for S$1.6 billion in December,

1999.is it going to be? We still have to think about it. It may not stay three

classesforever.

Globalization

The nature of flying is different now. In some instances, we haven’t realized thatwe

are a global airline and we operated as though we were still a regional airline.Our

systems were arranged to support regional operations rather than global ones,for

example. We now realize the need for the company to review all aspects

ofoperations and for the organizational structure to support a global airline.

Managing Discontinuous Change

The need for us to respond quickly is greater now. It’s not what is happening, it’show

you respond to what is happening 90% of the time. Your response to it isgoing to

make the material difference. So we need more agility, greaterflexibility, and yet how

do we communicate within the more complexorganization? In the past, we could all

go into a room and discuss it and that wasit. So all this has changed and we have to

respond to it, because we are aninternational company.

EXTERNAL ENVIRONMENT OF AIRLINE INDUSTRY

We have analyzed the external factors for Singapore airlines using PESTEL

Framework and to identify strategic challenge of external environment and have

been using Five Forces of Framework and SWOT for Singapore airlines.

PESTEL FRAMEWORK

The PEST analysis is one of them that are merely a framework that categorizes

environmental influences as political, economical, social and technological forces.

Sometimes two additional factors environmental and legal, will be added to make a

PESTEL analysis, but these themes can be easily subsumed in the others. This

classification distinguished between:

Political

This refers to government policy as such degree of intervention in the economy. To

what extent does it believe in finance firms such as Singapore Airlines has withdrawn

its bid for a stake in Air India, dealing a heavy blow to the Indian government’s

privatization programmed. This is political barrier for Singapore Airlines.

Economical

These include interest rates, taxation charges, economic growth, inflation and

exchange rates. The SA offer to buy 24% stake in China Eastern Airlines for 7.2

billion Hong Kong dollars appeared in trouble Wednesday after a major shareholder

criticized the deal as unfair.

Social

Changes in social trends can impact on a demand for a firm’s product and availability

and willingness of individuals to work. In the year 2002, there was a fatal crash of

Singapore Airline flight SQ006 at Taipei’s Chiang Kai-Shek International Airport.

Authorities blamed “pilot error” for the accident.

Technological

New technologies create new products and new processes. SA is the first airline to

install a productivity suite for the benefit of its passengers who can now continue to

work after boarding the plane without having to power up their laptops.

INTERNAL ANALYSIS

Strategic Capability of SA

Strategic capability identifies the capacity of a business to deliver future value to his

end user i.e. competitive advantage. It includes the following

Resources & Competence Of SA:

SA is the strongest brand from Asia and its long serving is almost iconic. SA has

consistently been one of the most profitable airlines globally. One of the factor is

strong brand management and healthy brand equity. As a result of a dedicated

professional brand strategy throughout diversified global organization.

Unique & Core Competence Of SA:

SA is first to introduce hot meals, free alcoholic and non-alcoholic beverages and hot

towels with a unique and patented scent, personal entertainment systems and video-

on-demand in all cabins.

Competitive Advantage of SA

One key element of SIA’s competitive success is that it manages to navigate skillfully

between poles that most companies think as distinct.

STRATEGIC CHOICES OF SINGAPORE AIRLINES:

Business Level Strategy

o Strategy for competitive advantage

o Meet economical expectations of shareholders

o Strategy for Singapore government satisfaction

Corporate Level Strategy

o Market diversification

o Value creation

SWOT ANALYIS

(1) STRENGHTS

Brand name

Cabin crews

Cuisine

Technology

Innovation

Timings

(2) WEAKNESSES:

Connected with few destinations.

Pricing policy

(3) OPPORTUNITIES:

Demand

Growing Asia Pacific market

Increase in trans-pacific cargo

Global airline market

(4) THREATS:

Competition increase in low cost airlines

Terrorism

Taxation

Increase in prices

Accidents

Instability in the Middle-East

Fuel prices

FIVE FORCES AFFECTING AIRLINE INDUSTRY PROFITABILITY

THREAT OF NEW ENTRANTS

Deregulated

Freedom of entry/exit

Availability of aircraft etc.

THREAT OF SUBSTITUTES

Telecommunications

Video Conferencing

High Speed Railroads etc.

Availability of aircraft etc.

BARGAINING

POWER OF

SUPPLIERS

Supply

concentration

Excess to

Capital

Etc.

BARGAINING

POWER OF BUYERS

Bargaining

Leverage

Buyer

Information

Substitute

Products etc.

RIVALRY AMONG

EXISTING AIRLINES

Competing for

growth, market

share etc.

FUTURE TRENDS IN AVIATION:

The travel and hospitality industries are amongst the most vulnerable to global or

local shocks. That means contingencies, cash reserves, hedging of major risks such

as oil prices. But most of all it means agile and bold leadership who think ahead,

with more than one strategy depending on how events unfold.

Airline manufacturers and airlines themselves will continue to exploit significant

energy savings over the next 20 years from a wide range of new technologies,

including better airline engine design, lighter composite fuselage, more direct aircraft

routing. Efficiencies will also be gained from fuller planes, faster turnaround,

economies of scale (consolidation of smaller airlines). For more on greener aviation,

see below.

Passengers will segment further into budget (bus quality), premium budget

(especially older travelers), traditional economy, right up to premier business class in

the largest long haul routes.

Despite energy price rises, our world’s population will continue to want to fly, and will

sacrifice other spending to do so, cushioning the adjustment for the airline industry.

Burning food in plane engines will become very controversial – as it connects energy

and food prices, with potentially disastrous consequences for the poorest citizens

around the globe.

Most planes will continue to burn carbon-based fuel for decades to come – because

the average life expectancy of a new plane today is at least 30 years.

FINDINGS AND SUGGESTIONS:

Singapore airline is the national airline of Singapore and one of the leading

aviation companies in the world.

At present, they operate in South East Asia, East Asia, Europe and Australia

route.

After analyzing external factors we find that SIA’s has some major barriers in

international political and economical sector.

As we are familiar that oil price is sensitive issue worldwide and day by day

it’s in receipt of more unstable. For those reasons the supplier power is very

high.

In the internal capability shows high brand attributes and strong brand

management as their core competence.

To maintain the current positioning company should concern their internal and

external surroundings.

SUMMARY OF BANKING SECTOR OF SINGAPORE AND INDIA

RESERVE BANK OF INDIA

The Reserve Bank of India was established on April 1, 1935 in accordance with the

provisions of the Reserve Bank Of India Act, 1934. The Central Office of the Reserve Bank

was initially established in Calcutta but was permanently moved to Mumbai in 1937. The

Central Office is where the Governor sits and where policies are formulated. Though

originally privately owned, since nationalization in 1949, the Reserve Bank is fully owned by

the Government of India.

Main Functions of RBI:

It acts as the Monetary Authority.

It regulates and supervises the Financial System.

It acts as the Manager of Foreign Currency

It issues Currency

It has the developmental role to support the National Objectives

It is the banker to the Government

It’s the banker to the Banks

(Reserve Bank of India)

2.2: MONETARY AUTHORITY OF SINGAPORE

2.2.1: INTRODUCTION OF MONETARY AUTHORITY OF

SINGAPORE

The Central Bank of Singapore is the Monetary Authority of Singapore. It was established in

1971 in order to regulate Singapore’s financial industry to aid in its development as an

international financial centre. Its primary function is to ensure that the financial markets

operate in an efficient and smooth manner, in line with national economic goals. The MAS is

responsible for the following:

Main Functions of MAS:

It is concerned with implementing the Monetary Policy

It supervises the Banking Systems

It’s banker to the Government

It’s banker to the Banks

It controls the International Reserves

It issues currency

It issues licences to Banks Issuer of banking licences

It’s the lender of the last resort

(Monitory Autority of Sinapore)

2.2.2: TYPES OF BANKS IN SINGAPORE

Most Banks in Singapore cater to different types of clients – individuals, corporations or

government agencies.

Commercial Banking (catering to Businesses and Corporations),

Retail Banking (catering to individual members of the Public)

Private banking (catering to HNWIs) services. Banks can be classified into two

categories:

1. Local Banks

1.7.1 Six local banks in Singapore

2. Foreign Banks

2.7.1 108 Foreign banks in Singapore

a. Full Banks

a. 26 full license banks in Singapore.

b. They provide whole range of banking business approved under the

Banking Act.

c. Six of the foreign banks operating in Singapore have been awarded

Qualifying Full Bank (QFB) privileges.

d. These Banks include:

i. HSBC, Citibank, Standard Chartered, Maybank, ABN AMRO

and BNP Paribas.

b. Wholesale Banks

a. 42 wholesale banks in Singapore

b. They are engaged in the same range of banking activities as full banks,

except Singapore Dollar retail banking activities.

c. All wholesale banks in Singapore operate as branches of foreign banks.

d. Examples:

i. ING bank, National Australia Bank, Barclays Bank, Fortis

Bank, Deutsche Bank etc.

c. Offshore Banks

a. 40 offshore banks in Singapore

b. They are engaged in the same activities as full and wholesale Banks for

businesses transacted through their Asian Currency Units (an

accounting unit, which banks use to book all foreign currency

transactions conducted in the Asian Dollar Market).

c. The banks’ Singapore dollar transactions are separately booked in the

Domestic Banking Unit (DBU).

d. All these.

e. Operate as branches of foreign banks.

f. Examples:

i. ICICI Bank Ltd, Korea Development Bank, Bank of Taiwan,

Bank of New Zealand, Canadian Imperial Bank of Commerce

etc.

d. Merchant Banks

a. 50 merchant banks in Singapore

b. They provide:

i. corporate finance, underwriting of share and bond issues,

mergers and acquisitions, portfolio investment management,

management consultancy and other fee-based activities.

ii. Examples:

1. Credit Suisse Singapore Ltd, Barclays Merchant Bank

Singapore Ltd, ANZ Singapore Ltd, Axis Bank Ltd etc.

(GUIDE ME

SINGAPORE)

2.2.3: MAJOR BANKS IN SINGAPORE

Major Local Banks

DBS (Development Bank Of Singapore)

o Established in 1968.

o It is considered the largest bank in Singapore and Southeast Asia, as measured

by assets.

o It is a leading consumer bank in Singapore and Hong Kong, serving over 4

million and 1 million retail customers respectively.

o It also has the largest retail network in Singapore, with 80 branches at present.

o It ranked 14th in The Banker’s “Top 200 Asian Banks 2008″.

OCBC (Overseas Chinese Banking Corporation)

o Established in 1912

o It is one of the largest financial institutions in the Singapore-Malaysia market

with total assets of S$184 billion.

o It ranked 1st in “Top 5 Regional Banks”, Asia Risk End-User Survey 2008.

UOB (United Overseas Bank)

o Established in 1935

o It is a leading bank in Singapore with a strong presence in the Asia-Pacific

region.

o As at 31 December 2007, the UOB Group had total assets of S$175.0 billion.

o It was awarded the “Best Overall Fund Group in Singapore” during The Edge-

Lipper Singapore Fund Awards 2008.

Major Foreign Banks

HSBC

o In Singapore, The Hong Kong and Shanghai Banking Corporation Limited

first opened its doors in December 1877.

o HSBC is an approved Primary Dealer in the Singapore Government Securities

Market and an Approved Bond Intermediary (ABI).

o It is a QFB honoured with 33 awards at Global Finance Awards 2006

by Global Finance. (Monetary Authority Of Singapore)

Standard Chartered

o Standard Chartered’s Singapore operation began in 1859 and today boasts of a

largest branch network (20) among international banks in the Republic.

o It is the Group’s second largest consumer banking market and was awarded a

Qualifying Full Bank (QFB) license in 1999.

o It is the largest custodian bank in Singapore for foreign institutions, rated top

for the past seven years in Global Custodian’s Agent Bank Survey.

ABN-AMRO Singapore

o ABN AMRO is now owned by RBS, Santander and the Dutch government.

o Its various businesses around the globe are currently being separated from

ABN AMRO and integrated in line with each owner’s plans.

Maybank

o Maybank’s presence in Singapore began in 1960 as a full-licensed commercial

bank.

o Maybank is currently among the top five banks in ASEAN and is a Qualifying

Full Bank in Singapore.

o As of June 2008, Maybank’s total assets amounted to S$22.7 billion in

Singapore.

BNP Paribas

o BNP Paribas has been at the forefront of banking in Singapore since 1968 and

was awarded a QFB status in 1999.

o Today, BNP Paribas Singapore assumes a prominent presence in the region by

acting as the Group’s regional hub for its business in Corporate and

Investment Banking as well as Private Banking.

Citibank

o Citibank was the first American bank to set up a branch in Singapore in 1902.

o Although a relative latecomer to the retail-banking sector.

o The bank has grown into a formidable market player with major market share

in key businesses including unsecured lending, deposits and investments and

secured assets.

o Citibank was among the first four foreign banks to be awarded the Qualifying

Full Bank (QFB) license in 1999.

(GUIDE ME

SINGAPORE)

2.3: BANK REGULATIONS AND LEGISLATION

In Singapore, the laws regulating Banking are found in the relevant Acts passed by

Parliament (and other related subsidiary legislation), the common law and principles and

rules of Equity which are derived from the case law. These legislations not only regulates the

Banking Sector in Singapore, but also ensure that the legal framework for Banking in

Singapore and keeps pace with the latest developments in the financial World. The relevant

acts pertaining to the Banking Industry include:

1. Banking Act – The Banking Act is the legislation that governs commercial banks in

Singapore.

2. Monetary Authority Of Singapore Act – It governs all matters related to MAS in it’s

operations.

3. Anti Money Laundering Regulations

4. Payment and Settlement System Guidelines

5. Securities and Futures Act

2.4 ANALYSIS: INDIA V/S SINGAPORE

2.4.1: DOMESTIC CREDIT PROVIDED BY BANKING SECTOR (% OF GDP)

(WorldBank)

From the above chart, it can be analysed that India has been very competitive when compared

to Singapore and the domestic credit provided by Banking Sector in both the countries is

continuously rising, which is a good sign.

2.4.2: GDP (CURRENT US$)

(WorldBank)

62 63 70

77

91 86

58 61 61 68 69 71

2005 2006 2007 2008 2009 2010

Singapore India

0.00

500000000000.00

1000000000000.00

1500000000000.00

2000000000000.00

2005 2006 2007 2008 2009 2010

Singapore

India

From the above chart, it can be analyzed that the GDP of both the countries are continuously

rising, for India, the change is very nominal but it’s a pretty good rise for Singapore, except

for the year 2008 where it was stable. The reason for this is recession in India during the year

2008 which affected both the countries, as far as their GDP is concerned.

2.4.3: GDP GROWTH (ANNUAL %)

(WorldBank)

The above chart clearly defines that annual GDP growth of Singapore and India. When

compared to India, the change in the GDP Growth Rate of Singapore is significant.

2.4.4: COMMERCIAL BANK BRANCHES (PER 100,000 ADULTS)

(WorldBank)

From the above chart we can conclude the Singapore has more bank branches rather than

India in the year 2005, 2006, and 2007 and at par in the year 2008 and 2009 but fortunately,

7 9 9

1 -1

14

9 9 10

5

9 9

2005 2006 2007 2008 2009 2010

Singapore India

9

9.5

10

10.5

11

11.5

12

12.5

2005 2006 2007 2008 2009 2010

Singapore

India

in India, the number of Bank Branches has increased the banking sector growth because of

formation of new banking policy in the year 2010. (Per 1,00,000 adults)

2.4.5: BANK CAPITAL TO ASSETS RATIO (%)

(WorldBank)

According to World Bank data, the overall bank capital to assets ratio of Singapore is higher

than that of India year on year. Due, to Global Crisis, the ratio for both the countries is less

for the year 2008.

2.4.6: BANK NONPERFORMING LOANS TO TOTAL GROSS LOANS (%)

(WorldBank)

10 10 9

8

10 10

6 7

6 7 7 7

2005 2006 2007 2008 2009 2010

Singapore India

4

3

2 2 2 2

5

3 3

2 2 2

2005 2006 2007 2008 2009 2010

Singapore India

The above graph shows the relation between bank nonperforming loans to total gross loans

ratio of last five year. In the year 2005 and 2007, the ratio is higher of India than that of

Singapore and for the year 2006, 2008, 2009 and 2010, it is constant for both the countries.

2.4.7: BANK CAPITAL TO ASSETS RATIO (%)

(WorldBank)

The above graph represents Bank Capital to Asset Ratio in percentage. It can be analysed that

it’s increasing for both the countries except in the year 2007 where it’s declining for both the

countries by 1% and again decrease of 1% in the year 2008 for Singapore.

2.4.8: LENDING INTEREST RATE (%)

(WorldBank)

10 10 9

8

10 10

6 7

6 7 7 7

2005 2006 2007 2008 2009 2010

Singapore India

5 5 5 5 5 5

11 11

13 13 12

11

2005 2006 2007 2008 2009 2010

Singapore India

The above graph represents the Lending Rates in percentage. The lending rates of India are

significantly higher of India than that of Singapore. For, India the rates are fluctuating to

regulate the money supply in the economy which was a major focus for India in recent years,

whereas for Singapore it’s stable.

2.4.9: OFFICIAL EXCHANGE RATE (US$, PERIOD AVERAGE)

(WorldBank)

The above graph represents the exchange rates between India and US and Singapore and US.

The exchange rates between Singapore and US are stable over the time and changes are not

major whereas, the exchange rate between India and US is fluctuating and the major change

can be seen from the year 2006 to 2009. This is because of Global crisis and again the

imports are more for India than exports. The fluctuating exchange rates for India results in

huge loss for companies associated in Exports and Imports.

44 45 41

44 48 46 47

2 2 2 1 1 1 1

2005 2006 2007 2008 2009 2010 2011

INDIA SINGAPORE

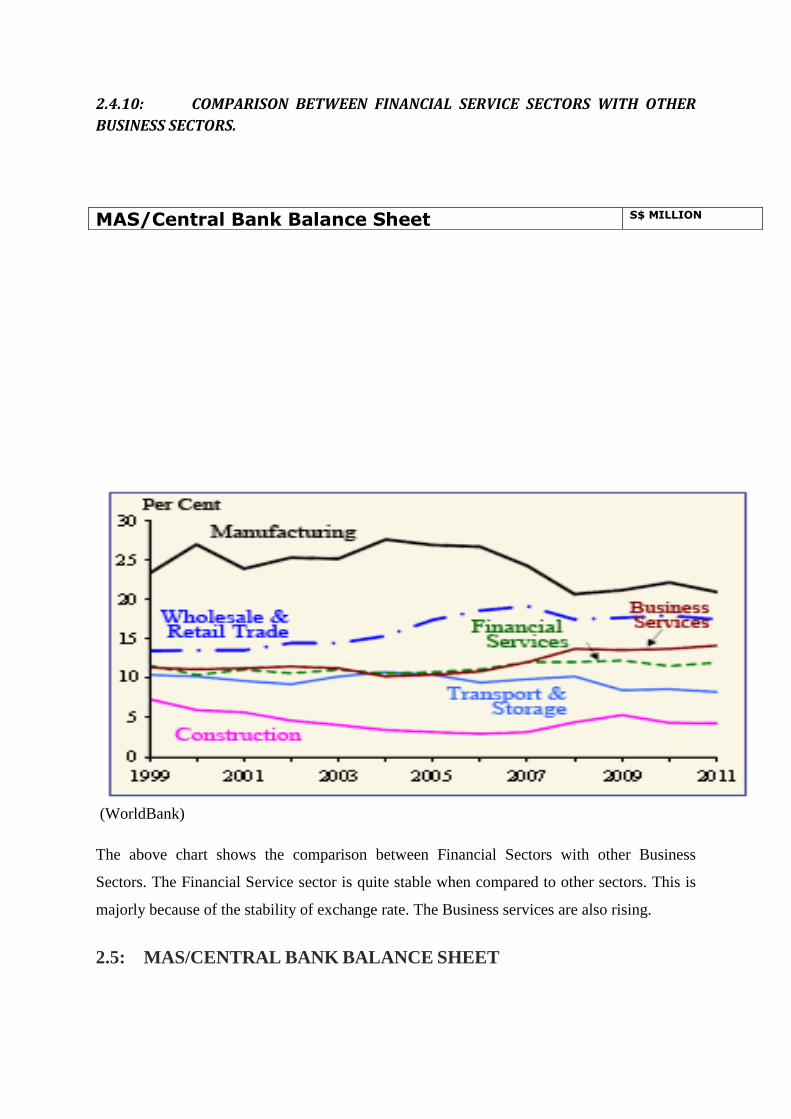

2.4.10: COMPARISON BETWEEN FINANCIAL SERVICE SECTORS WITH OTHER

BUSINESS SECTORS.

(WorldBank)

The above chart shows the comparison between Financial Sectors with other Business

Sectors. The Financial Service sector is quite stable when compared to other sectors. This is

majorly because of the stability of exchange rate. The Business services are also rising.

2.5: MAS/CENTRAL BANK BALANCE SHEET

MAS/Central Bank Balance Sheet S$ MILLION

2.6: STRENGTHS OF BANKING IN SINGAPORE:

Economic resilience is "very low risk", supported by the highly competitive, diverse,

and resilient economy-factors which provide buffers against external shocks.

The institutional framework is "very low risk", benefiting from prudent banking

regulations and supervision, a strong regulatory track record, and supportive

governance framework which is benefiting at long term.

Competitive dynamics are "low risk", reflecting the banking industry's restrained risk

appetite, stable competitive environment as well as a healthy market and absence of

market distortions.

Liberalization in the domestic banking market.

Local banks are strengthened by their regional presence through mergers and

acquisitions.

Increased competition spurred the development of innovative products and more

competitive pricing models.

Provision of sophisticated banking services like corporate and investment banking

activities, apart from traditional lending and deposit-taking functions.

Strict banking secrecy laws, tax friendly policies and a suite of wealth management

services created a private banking boom.

Recognizing the needs of SME’s which comprise a sizable Banking Market in

Singapore.

(Monetary Authority Of Singapore) (WorldBank)

END OF PERIOD

ASSETS LIABILITIES OTHER ITEMS (NET)

TOTAL

DOMESTIC CREDIT RESERVE MONEY

FOREIGN LIABILITIES

GOVERNMENT DEPOSITS

FOREIGN ASSETS

TOTAL

GOVERNMENT

PRIVATE SECTOR

1 2=3+4

3 4 5 6 7 8 9

2007

235691.6 6501.9 6501.7 0.2 28061.0 1865.0 108948.1 103319.4 242193.5

2008

251318.2 6860.3 6860.1 0.2 34122.7 1732.3 132711.3 89,612.2 168566.3

2009

264533.2 7381.8 7381.6 0.2 36344.0 3238.6 117077.7 115254.7 271915.0

2010

289376.6 7480.8 7480.7 0.1 40529.7 2770.3 130490.2 123,067.2

173790.2

2011

308530.8 6813.8 6813.7 0.1 45431.8 3409.8 144112.9 122390.1 315344.6

2.7 GROWTH OF PRIVATE BANKING INDUSTRY

Singapore has capitalized on the growing no. of high net worth individuals in Asia and other

regions like Europe and the Middle East, emerging as an attractive hub for global investors.

Singapore has earned the title “Switzerland of Asia”, attributable to:

Strict banking secrecy laws– Sec. (47) of the Banking Act states that consumer details

shall not, in any way, be disclosed by an any bank or any of its officers, to any other

person except as expressly provided in the Banking Act.

Non-recognition of the 2005 European Tax Directive– Singapore is one of the few

remaining offshore centers that has not signed up to the EU;s saving tax Directive,

whose country members can transit private details regarding to individuals who bank

and invest in these countries.

Generous tax incentives– capital gains and interest income from outside Singapore are

not taxed here

Private Banks such as Credit Suisse, UBS, standard chartered and Citigroup to name a few,

provides the following facilities:

Global wealth management services

Wealth and lifestyle consulting services

Investment strategies

Asset and tax planning

Asset security

Credit Services

2.8 KEY FINDINGS:

The key findings from this report are presented as under:

Domestic credit provided by Banking in Singapore (% of GDP) is significantly rising

for both the countries. Singapore saw a decline in the same in the year 2010 by 5% as

compared to 2009, whereas, it has increased for India.

The lending rates of in India are reducing where as for Singapore; it is stable and

significantly lesser than that of India. From this, it can be analysed that there are

Arbitrage opportunities possible from the same and Market for taking loan in

Singapore would be quite high.

The exchange rates of Singapore are quite stable than that of India.

The Strengths of Banking in Singapore is in large quantum which shows that the

feasibility of Banking in Singapore is high.

The foreign assets of MAS are significantly rising over the period of years.

The lending rates of India are significantly higher of India than that of Singapore. For,

India the rates are fluctuating to regulate the money supply in the economy which was

a major focus for India in recent years, whereas for Singapore it’s stable.

The overall bank capital to assets ratio of Singapore is higher than that of India year

on year. Due, to Global Crisis, the ratio for both the countries is less for the year

2008.

The scope of Banking in India is also high with special reference to Rural Area as

there the large quantum of Market is untapped, especially in developing states.

The employment opportunities in Singapore and India are high as the feasibility for

Banking in both the countries is high.

The norms of Banking in India are more complex than that of Singapore.

The Banking System is much more protective in India as during crisis in 2008-09, the

GDP of India didn’t let to breakdown much.

The overall bank capital to assets ratio is Singapore higher then India in every

consecutive year in the same proportion. The year 2008 is lower in all year because of

Global crisis.

SUMMARY OF ELECTRONICS SECTOR OF SINGAPORE

ECONOMIC AND INDUSTRIES OVERVIEWS:

The electronics industry today plays a vital role in the development of most nations as it has

grown substantially and strongly over the past decades. This industry moves closer to the

centre and drives rapid economic development of the world, taking its place in the heart of

one country after another.

INDIAN ELECTRONIC INDUSTRY:

India is the fifth largest economy in the world and has the second largest GDP among

emerging economies. Owing to its large population, the potential consumer demand is almost

unlimited and consequently under appropriate conditions, strong growth performance can be

expected. The electronics industry, in particular, is emerging as one of the most important

industry in the Indian market.

The electronics industry in India dates back to the early 1960s. Electronics was initially

restricted to the development and maintenance of fundamental communication systems

including radio-broadcasting, telephonic and telegraphic communication, and augmentation

of defence capabilities. Until 1984, the electronics sector was primarily government owned.

The late 1980s witnessed a rapid growth of the electronics industry due to sweeping

economic changes, resulting in the liberalization and globalization of the economy. The

economic transformation was motivated by two compelling factors - the determination to

boost economic growth, and to accelerate the development of export-oriented industries, like

the electronics industry.

SINGAPORE ELECTRONIC INDUSTRY:

Electronics is the major industry underpinning Singapore’s economic growth. Singapore aims

to be a world-class electronics hub, creating manufacturing solutions and producing high

value-added components for the global market. This is the choice location for companies and

talent to create and manage new markets, advanced products and processes, technologies and

applications.

The Singapore's semiconductor industry has grown from humble beginnings as an assembly-

and test-subcontracting supplier to a fully integrated, cutting-edge technology wafer

fabrication hub. With about 13 state-of-the-art wafer fabs nationwide, the small island of

Singapore is way ahead of its Southeast Asia neighbours in the development of the region's

chip-making infrastructure. Semiconductors, as well as related production equipment and

materials, are a key focus of the Singapore’s Industry initiative. An important advantage for

investors is that the government is a significant shareholder in most of the island's wafer fabs.

TRADE AND COMMERCE

INDIA

The electronics industry has recorded very high growth in subsequent years. By 1991, private

investments - both foreign and domestic - were encouraged. The easing of foreign investment

norms, allowance of 100 percent foreign equity, reduction in custom tariffs, and delicensing

of several consumer electronic products attracted remarkable amount of foreign collaboration

and investment. The domestic industry also responded favorably to the politic policies of the

government. The opening of the electronics field to private sector enabled entrepreneurs to

establish industries to meet hitherto suppressed demand. The Indian Electronics Industry is a

text for investors who are seeing India as a potential investment opportunity.

Improvements in the electronics industry have not been limited to a particular segment, but

encompass all its sectors. Strides have been made in the areas of commercial electronics,

software, telecommunications, instrumentation, positioning and networking systems, and

defence. The result has been a significant trade growth that began in the late 1990s.

Despite commendable achievements in the sphere of electronics, considerable infrastructural

improvements remain a priority. Water, power, telecommunications, and transportation

sectors must still be amplified so that high economic growth can be sustained.

Due to liberalization policies of 1980’s, Output from electronics plants in India grew from

Rs1.8 billion in FY 1970 to Rs8.1 billion in FY 1980 and to Rs123 billion in FY 1992. Most

of the expansion too

k place in the production of computers and consumer electronics. Indian Production of

Computer rose from 7,500 units in 1985 to 60,000 units in 1988 and to an estimated 200,000

units in 1992. During this period, major advances were made in the domestic computer

industry that led to more sales. Consumer electronics in India account for about 30% of total

electronics production of the country.

SINGAPORE

With good physical infrastructure support, such as specialized power and water supplies,

waste treatment and other ancillary services already in place, Singapore’s Economic

Development Board (EDB) is hostilely courting investments from both multinational

corporations and local companies. It is offering incentives such as research and development

funding and tax rebates. The key aspect of the "Silicon Valley concept" for Singapore is its

ability to capture the entire value chain of semiconductor production. Industry specific

supporting facilities that have come on line include silicon wafer production, photo-masking

and a high-purity hydrogen peroxide plant.

EDB reports that there are more than 40 semiconductor companies and 160 supporting

organizations operating at all levels of the value chain. The Association of Electronics

Industries of Singapore (AEIS) and the Singapore Manufacturers’ Federation/EEAIIG are the

two organizations working for the development of electronics industry in Singapore. Most

ASEAN countries are not in direct competition with Singapore, as Singapore has decided to

target sectors with higher technologies.

In 2009, electronics contributed an output of almost S$63 billion and employed more than

76,000 workers. Of the S$11.8 billion in fixed asset investment Singapore received that year,

electronics was the largest contributor, accounting for 41.5%.

The charts above, showing India’s trade with Singapore since 2002-03, shows a remarkable trend

of upward movement. From the trade figures, it is quite specious that Indian exports to and

imports from Singapore have been rising substantially since CECA. Indian exports nearly

doubled from Rs. 9,764 crore in 2003-04 to Rs. 17,975 crore in 2004-05. A major reason for this

probably was the anticipation for CECA’s signing, which was in its final stages of negotiation at

the time. Total trade has gone up from Rs. 13,823.6 crore in 2002-03 to Rs. 62,344.4 crore in

2007-08, a nearly five-fold increase.

OVERVIEW OF BUSINESS AND TRADE AT INTERNATIONAL

LEVEL

INDIA

As the market of India is rising like plant growing in the garden in electronics sectors the

demand for the Indian market is expected to reach at the peak point in 2020 by US $ 400

billion. Manufacturing has been recognized as the main engine for economic growth and

exciting target of taking the share of ICT and electronics hardware manufacturing to around

25% within the reach of 2025 has been setup by National Manufacturing Policy. As the India

is second largest peopled country in the world, there are many coupled with strong growth,

India will remain one of the largest consumers of electronics products globally.

The industry is composed to ride the wave of domestic demand for electronic products.

Developing core areas of design and application development will only help totoss the Indian

electronics and manufacturing industry towards greater innovation.

In 2011 the US trade deficit in relation with the India goods is US $ 14.5 billion which is

been increased from 2010 by $ 4.3 billion. In 2010 the US goods shortfall was increased by

12.4% that is in US $ 21.6 billion. As per the above data India is the 17th

largest export maker

for US goods. Export of US towards the private commercial service which eliminates military

and government. In 2010 the US exports to India was 10.3 billion and vice versa the US

import from India was 13.7 billion. Majority of sale service affiliated by US in India was 13.9

billion in 2009 & vice versa of that the majority of sale service affiliated by India’s owned

firm in US was 7.2 billion.

The industry constitutes less than 1% of the global market. However, demand for these

products is growing quickly and investments are smooth in to augment manufacturing

capacity.

a) India remains a major importer of electronic materials, components and finished

equipment amounting to around $20 billion in 2007. The country imports electronic goods

mainly from China

b) In the last four years, production of computers has grown at a compounded annual growth

rate (CAGR) of 31%, the highest among the various electronic products in India. This has

been followed by communication and broadcast equipment (25%), strategic electronics

(20%) and industrial electronics (17%).

c) The consumer electronics segment, which has grown at a CAGR of 10% in the last five

years, includes a wide range of products such as DVD, VCD/MP3 players, television sets and

microwave ovens.

d) The growth in demand for telecom products has been high, with India adding two million

mobile phone users every month, which is one of the main reasons for the growth in

production of electronic goods. This growth is expected to continue over the next decade, too.

e) The government has recognized electronics and IT hardware manufacturing as one of the

thrust areas for development. A special incentive package scheme (SIPS) was announced in

March 2007 to appeal investments for semiconductor fabrication and other micro and

nanotechnology manufacturing industries in India.

f) In the case of exports, the largest share was taken by electronic components, with 47% of

total electronic exports. Exports of electronic components have grown at a CAGR of 25% in

the last five years.

g) India’s main destination for electronic goods is the US.

India however remains a major importer of electronic materials, components and finished

equipment amounting to over US$12 Billion in 2005.India is also an exporter of a huge range

of electronic components and products for the following segments -

Display technologies

Entertainment electronics

Optical Storage devices

Passive components

Electromechanical components

Telecom equipment

Semiconductor designing

Electronic Manufacturing Services (EMS)

Indian Electronics Industry Exports are given below

Electronics & IT Production (Calendar Year)

(Rs. crore)

Item 2002 2003 2004 2005 2006 2007*

Consumer Electronics 13,580 14,850 16,500 17,500 19,500 21,880

Industrial Electronics 5,400 5,980 8,300 8,600 10,100 11,560

Computers 4,180 6,600 8,680 10,500 12,500 15,500

Communication & Broadcast

Equipment

4,800 5,150 4,770 6,300 9,200 13,150

Strategic Electronics 2,330 2,670 2,850 3,070 4,500 5,700

Components 6,510 7,450 8,700 8,530 8,600 9,320

Sub-Total 36,800 42,700 49,800 54,500 64,400 77,110

Software for Export 44,000 55,000 75,000 97,000 132,025 157,500

Domestic Software 12,000 15,500 20,500 27,000 35,150 44,730

Total 92,800 113,200 145,300 178,500 231,575 279,340

*Estimated

Source: Electronic Industries Association of India

SINGAPORE

Singapore is a major manufacturing and trading centre in the region for electronic products,

components and parts, and supporting services. This section considers Singapore’s position in

the industry value chain, including production, technology development, procurement,

marketing and sales.

Data initiated from the International Economic Database of the Australian National

University (ANU) show that, among the eight economies in this study, Singapore ranked first

as an exporter of office and computing machinery (ISIC 3825) and electrical machinery (ISIC

383) and second only to Hong Kong as an importer. As illustrated, this dominant position can

be accounted for by large domestic production and entrecote trade.

Singapore’s national trade data (excluding trade with Indonesia) illustrate the composition of

domestic exports and re-exports and the product alignment in its total exports. In 1992,

Singapore’s total trade in electronics reached US$74.3 billion, with imports of US$30.8

billion and exports of US$43.5 billion, of which re-exports accounted for 26.5%. The largest

categories of domestic exports were disk drives, computers and subassemblies, integrated

circuits (ICs), television (TV) receivers and subassemblies, and color TV sets. Re-exports

were concentrated in ICs, computers and subassemblies, disk drives, color TV sets, radios

and videocassette recorders (VCRs), and telecommunications equipment.

In 2011, the sector donated an output of US$86.1 billion, accounting for 6.3% of Singapore’s

total GDP, and employed more than 82,000 workers.

Singapore’s domestic exports of electronics still depend on US–EC markets, which immersed

64.1% of such exports in 1992. East Asia accounted for 26.3%, but Japan’s share was only

5.1%. The very small Japanese share is noteworthy in view of the extensive presence of

Japanese electronics firms in Singapore and may be attributed to both Japan’s import barriers

and the corporate strategies of Japanese electronics firms in Singapore.

From the early 1980s to the early 1990s, Singapore became a key manufacturing base for

original equipment manufacturers (OEMs) as production costs increased in the OEMs’ home

base. The Singapore Government stimulated the sector’s development through investments in

state-owned enterprises like Chartered Semiconductor, NatSteel Electronics. A host of

smaller private-sector Singapore firms emerged, many as suppliers to the MNCs, but others

as innovators themselves (Creative Technology and its soundcards). In the 1990s, several

large contract assemblers grew, including Venture and NatSteel Broadway. By the mid-

1990s, electronics was contributing over half the economy’s manufacturing output, up from

23.6% in 1985 and 10.7% in 1975.

TABLE: ECONOMIC CONTRIBUTION BY ELECTRONICS INDUSTRY

Year Real GDP

Growth %

Electronics

Output as

% of Total Output

Manufacturing

% Employment in

Electronics

1988 11.1 38.7 34.8

1990 7.3 39.1 34.9

1995 8.8 51.4 34.3

1996 7.0 50.8 34.9

1997 8.5 50.5 33.8

1998 -0.9 50.1 31.7

1999 6.4 52.1 21.2

2000 9.4 51.3 29.7

2001 -2.4 45.0 28.4

2002 2.2 42.2 26.7

2003 0.8 (est.) 40.0 27.1 (est.)

Source: Research Paper on Foreign Trade Performance of Singapore

The weakness of the dependence on electronics for such a large share of output and exports

was brought home in 2001, when Singapore suffered a sharp economic recession. The 2001-

2002 downturn in global electronics demand (global sales of semiconductors plunged 34% in

2001) saw Singapore’s domestic exports of electronics down 20% to S$59 million (US$32

billion at then current exchange rates) in 2001 (the U.S. absorbs 20% of Singapore’s

electronics shipments). Shipments were down in all segments of the electronics industry.

Exports of electronics fell further in 2002, to S$57 billion (US$32 billion at end-2002

exchange rates), or 25% below their level in 2000 and 10% below the 1997 level.

Electronics Trade

(Percent Share)

Electronics Exports: CY 2001 CY 2002 CY 2003

As a percentage of Total Exports 52.6 52.1 49.7

To U.S. as percentage of Total Exports 11.6 10.9 9.7

To U.S. as percentage of NODX 26.2 24.7 21.5

To U.S. as percentage of Electronics Exports 22.1 20.9 19.6

Electronics NODX as percentage of NODX 61.0 57.9 52.9

Source: Research Paper on Foreign Trade Performance of Singapore

PRESENT TRADE RELATIONS AND BUSINESS VOLUME OF

DIFFERENT PRODUCTS WITH INDIA

A short-term look at trends for some of the main commodities of import/ export will shed some

light on the composition of trade between the two countries. The main commodities exported

and imported by India to/ from Singapore in the last few years are given in the table below:

MINERAL FUELS, MINERAL OILS AND PRODUCTS OF THEIR DISTILLATION;

BITUMINOUS SUBSTANCES; MINERAL WAXES.

SHIPS, BOATS AND FLOATING STRUCTURES.

NUCLEAR REACTORS, BOILERS, MACHINERY AND MECHANICAL APPLIANCES;

PARTS THEREOF.

ELECTRICAL MACHINERY AND EQUIPMENT AND PARTS THEREOF; SOUND

RECORDERS AND REPRODUCERS,

TELEVISION IMAGE AND SOUND RECORDERS AND REPRODUCERS, AND PARTS.

NATURAL OR CULTURED PEARLS,PRECIOUS OR SEMIPRECIOUS

STONES,PRE.METALS,CLAD WITH PRE.METAL AND

ARTCLS THEREOF;IMIT .JEWLRY;COIN.

IRON AND STEEL ALUMINIUM AND ARTICLES THEREOF.

AIRCRAFT, SPACECRAFT, AND PARTS THEREOF.

PRINTED BOOKDS, NEWSPAPERS, PICTURES AND OTHER PRODUCTS OF THE

PRINTING INDUSTRY; MANUSCRIPTS, TYPESCRIPTS AND PLANS.

ORGANIC CHEMICALS

VEHICLES OTHER THAN RAILWAY OR TRAMWAY ROLLING STOCK, AND PARTS

AND ACCESSORIES THEREOF.

Source: Export Import Data Bank, Ministry of Commerce, Government of India

Source: Export Import Data Bank, Ministry of Commerce, Government of India

In the annexure, there are tables analyzing export/ import trends in some of the above

commodities. In exports, there has been a very explosive movement in growth rates of the top

5

commodities. For example, gemstones and precious metals had 2 successive years of more

than 100% growth, which was followed by a 87.46% drop in 2006-07 that brought the value

of export back to around the original level. Mineral oil and fuel products (motor oils, fuel oil,

petroleum products, diesel, ATF, etc.) have increased to become 55% of all exports from

India to Singapore. Shipping and boat goods (such as floating/ submersible drilling/

production platforms, small vessels for transport of persons and goods) registered huge

growth in export around time of CECA’s launch and have grown to 7.3% of India’s exports

to Singapore from 1.14% in 2003-04. Unwrought aluminum, copper wires and diamond are

other important items of export.

India’s Imports Exports from/to Singapore:

India’s main imports from Singapore comprise electronic goods, non-electrical machinery,

organic chemicals, project goods, transport equipment, artificial resins and professional

instruments (non-electronic).

Electronic items are India’s largest imports from Singapore. The value of such imports has

increased from US$1.31 billion in 2005-06 to US$1.65 billion in 2006-07. Out of around 440

different electronic products imported by India from Singapore, some of the leading ones are

photosensitive transistor diodes, electronic integrated circuits, telephones for cellular and

wireless networks, apparatus for control and distribution of electricity, electrical machinery

parts, laser and magnetic discs for reproducing purpose, optical fiber cables, remote control

apparatus (excluding radio), apparatus for switching, static convertors, generating sets with

spark ignition, fixed capacitors, transmission apparatus, digital cameras, smart cards, video

recorders and parts for line telephone apparatus.

Under the ‘Early Harvest Program of the CECA, India eliminated customs duties on 506

items originating from Singapore from 1 August 2005. These include a large number of items