Embed Size (px)

Citation preview

Digital Revolution: A Case from

Kenyan Banks

Presentation by George Bodo

Head of Banking Research,

Ecobank Capital.

8th September, 2016.

Villa Rosa Kempinsky, Nairobi

Source: Ecobank Research 2

Kenyan Banks: Retail Franchise Strength

0% 2% 4% 6% 8% 10% 12% 14% 16%

KCB

Equity

Co-operative Bank

Barclays

Family Bank

National Bank of Kenya

Diamond Trust Bank Limited

Standard Chartered

Sidian

Bank of Africa

I&M Bank

Ecobank

CBA

NIC

CfC Stanbic

Jamii Bora Bank

Consolidated Bank

First Community Bank

Prime Bank Limited

Trans-National Bank

GTBank

Gulf African Bank Ltd

Credit Bank Limited

Spire Bank

Fidelity Commercial Bank

Bank of Baroda

ABC Bank

Guardian Bank

M Oriental Bank

UBA

Source: Ecobank Research 3

Kenyan Banks: Loan book concentration by key segments

0% 20% 40% 60% 80% 100% 120%

KCB

Equity

Co-operative

Standard Chartered

Barclays

CBA

CfC Stanbic

NIC*

DTB

I&M

Family Bank

Bank of Africa

National Bank

Citi

Ecobank Corporate

SME

Consumer

Source: Ecobank Research 4

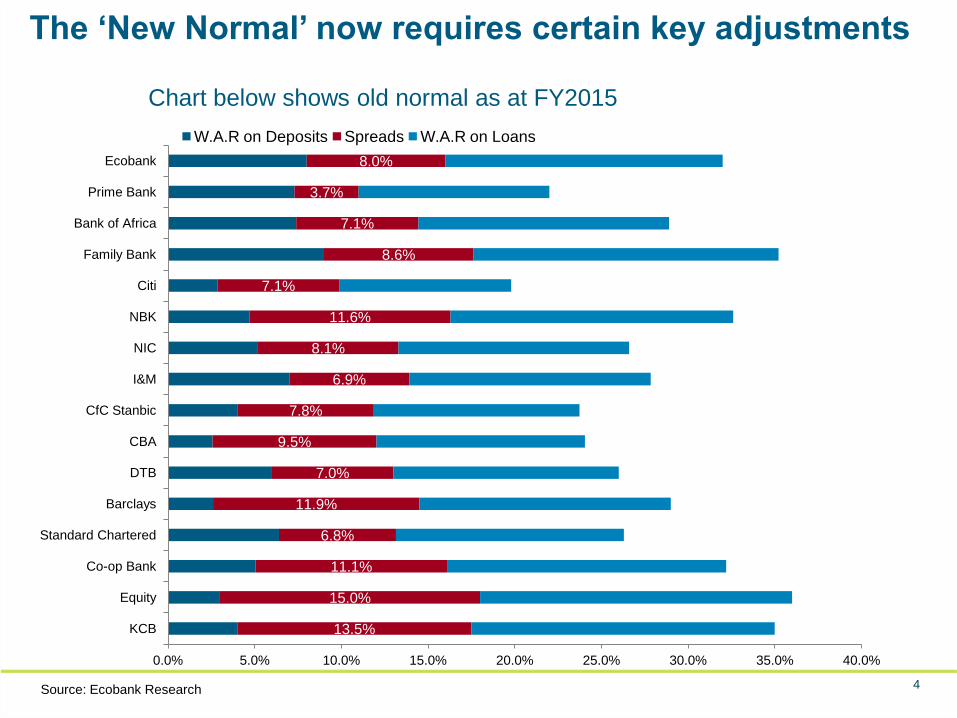

The ‘New Normal’ now requires certain key adjustments

13.5%

15.0%

11.1%

6.8%

11.9%

7.0%

9.5%

7.8%

6.9%

8.1%

11.6%

7.1%

8.6%

7.1%

3.7%

8.0%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0%

KCB

Equity

Co-op Bank

Standard Chartered

Barclays

DTB

CBA

CfC Stanbic

I&M

NIC

NBK

Citi

Family Bank

Bank of Africa

Prime Bank

Ecobank

W.A.R on Deposits Spreads W.A.R on Loans

Chart below shows old normal as at FY2015

Source: Ecobank Research

* Expressed as ratio of total interest expenses to gross interest income

5

New Normal: Key adjustment points

29%

41%

51%

34%

43% 47%

70%

46%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Tier 1 Banks Tier 2 Banks Tier 3 Banks Industry

Cost of Deposits* Efficiency(CIR)

Now that caps on lending rates as well as floors on deposit rates are part of our national laws,

banks will have to make adjustments to their business models-especially around costs (both

funding and non-funding). Technology is likely to be the next game changer in this new battlefront;

and banks will have no choice but to elevate technologization of their businesses.

6

Sources: Ecobank Research

28%

17%

33%

24% 20%

44% 45%

39% 41% 39% 36%

14%

41%

49%

71%

55% 50%

41% 44% 44% 45%

39%

52%

31%

37%

51%

29% 31%

64%

35%

72%

20%

85%

42%

89%

64%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cost of Deposits Efficiency(CIR)

Tier 1

Tier 2 In the new normal:

•CIR must not exceed 40%;

•Cost of funds must not exceed 30%

Customer Behaviors

8

Regular banking transactions and frequency

Type of Transaction

Daily-

several

times

Daily-

Once

Weekly-

several

times

Weekly-

once

Monthly-

several

times

Monthly-

once

Occassionally

-less than

once a month

117 141 608 484 786 1328 626

Cash Withdrawal 76% 9 12 149 133 260 254 141

Cash Deposit 67% 7 20 142 105 166 272 132

Savings 59% 6 29 73 89 159 293 88

Balance Enquiry 40% 11 15 47 53 88 163 122

Airtime Recharge 26% 76 52 120 29 21 18 9

Funds Transfer 23% 3 4 46 42 47 80 69

Bill Payments 21% 0 1 13 18 20 193 17

Other Payments 5% 0 2 8 2 14 16 19

Purchasing 4% 4 5 7 8 6 15 11

Sources: KBA-Survey on the interplay between Banking and MNOs, 2014

9

Places where cash is withdrawn

ATMs

58%

Mobile Operator Agent

20%

Bank Teller

16%

Bank Agent

5%

Sources: KBA-Survey on the interplay between Banking and MNOs, 2014

10

Payment of Bills

0%

0%

0%

1%

2%

3%

4%

10%

14%

64%

0% 10% 20% 30% 40% 50% 60% 70%

Prepaid

Credit Card

By cheque

Pay outlet by company

ATM

Others

Third party outlets

At the bank teller

Mobile Banking

Cash direct to company

Sources: KBA-Survey on the interplay between Banking and MNOs, 2014

Bank Initiatives: Alternative Channels

12

Channels…

0

50

100

150

200

250

300

350

400

2009 2010 2011 2012 2013 2014 2015 H1 2016

ATMs ATM Cards Debit Cards POS Machines Branches

Sources: Ecobank Research, CBK

13

Payments…

1% 3% 4% 4%

6% 7% 7% 8%

21%

28%

12% 11%

12% 12% 11% 10%

1% 1% 3% 2% 4% 5% 4% 4%

78% 75%

83% 84%

80% 79% 79% 80%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2008 2009 2010 2011 2012 2013 2014 2015

Mobile Payments as % of Total National Payments Cheque&EFT Payments as % of Total National Payments

Card Payments as % of Total National Payments RTGS Payments

Sources: Ecobank Research, CBK

14

Agency Banking…

# of

Banks

# of

Agents

Cash

Withdrawals

(KES'Bn)

Cash

Deposits

(KES'Bn)

Total

Transactions

(Mn)

Value of

Transactions(KES'Bn)

2011 8 9,748 15 28 9 44

2012 10 16,333 50 101 30 152

2013 13 23,477 74 160 42 236

2014 16 35,847 105 236 58 346

2015 17 40,592 133 297 80 442

Sources: Ecobank Research, CBK

15

Initiatives currently in the pipeline: Switches

Sources: Ecobank Research, CBK

• Commercial banks now want to bypass

telcos in the battle for mobile money

wallet.

• Banks are currently on top gear to

launch a common mobile switch to be

used by banks.

• Access to this wallet will be through

USSD or an app.

• This effectively means that banks want

to dominate mobile payments.

• This is definitively a game change and

banks just need to drive its acceptability.

Mobile Switch

Bank

Account

USSD

App

Safaricom/

Airtel

MNO Platform

Customer

Mobile

Wallet

MobilePhone

Bank

Account Customer

Mobile

Wallet

USSD

App

Common Switch

Mobile

Phone

16

Mobile Phone Loans

Sources: Ecobank Research, CBK

Loan

originator

(RM)

No objection from

head of credit

CAD-Availment and

Letter of Offer

Operations-

disbursement

CAD-Monitoring

Credit Analyst

Appraisal (Credit

Factory)

Customer

drawdown

Registering of charge (in case of secured lending)

The normal bank process

17 Sources: Ecobank Research, CBK

The Mobile Process

Loan

origination

by the

customer

Mpesa

usage Airtime

Usage

Okoa

Jahazi Okoa

stima

Airtel

Money

usage

CRB

listing

Limit

setting

Loan

availment

Credit Appraisal by the MNO

• The mobile process is a lot more

cheaper and efficient;

• Less people involved in the

process;

• A very ideal platform going

forward for mass-market focused

banks.

18

Initiatives currently in the pipeline: Switches

Sources: Ecobank Research, CBK

Mobile Switch

Thank you