Embed Size (px)

Citation preview

Digitization - The Growth D iDriver

20 March 201520 March 2015

Presented by Ashish GargPresented by Ashish Garg ([email protected])

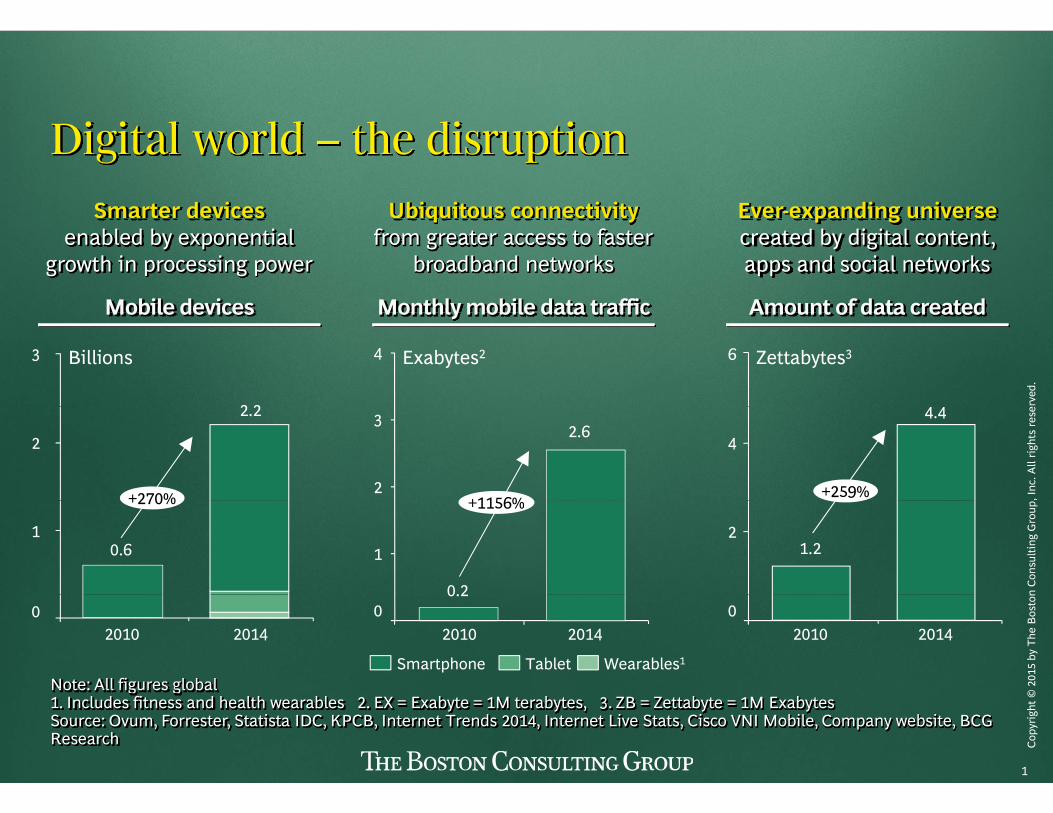

Di i l ld h di iDigital world – the disruptionSmarter devices Ubiquitous connectivity Ever-expanding universe

Mobile devices Monthly mobile data traffic Amount of data created

enabled by exponential growth in processing power

q yfrom greater access to faster

broadband networks

p gcreated by digital content, apps and social networks

rved

.

Mobile devices Monthly mobile data traffic Amount of data created

643

2 2

Zettabytes3Exabytes2Billions

, Inc

. All

right

s re

se

4

4.43

2+1156%

2.62

2.2

+270% +259%

n Co

nsul

ting

Gro

up

21.21

+1156%

0.2

1

+270%

0.6

2015

by

The

Bos

ton

02010 2014

020142010

0.20

20142010

Smartphone Tablet Wearables1

Note: All figures global

IDFC Alternatives Digitzation 20March15 Fin.pptx 1

Copy

right

© Note: All figures global

1. Includes fitness and health wearables 2. EX = Exabyte = 1M terabytes, 3. ZB = Zettabyte = 1M ExabytesSource: Ovum, Forrester, Statista IDC, KPCB, Internet Trends 2014, Internet Live Stats, Cisco VNI Mobile, Company website, BCG Research

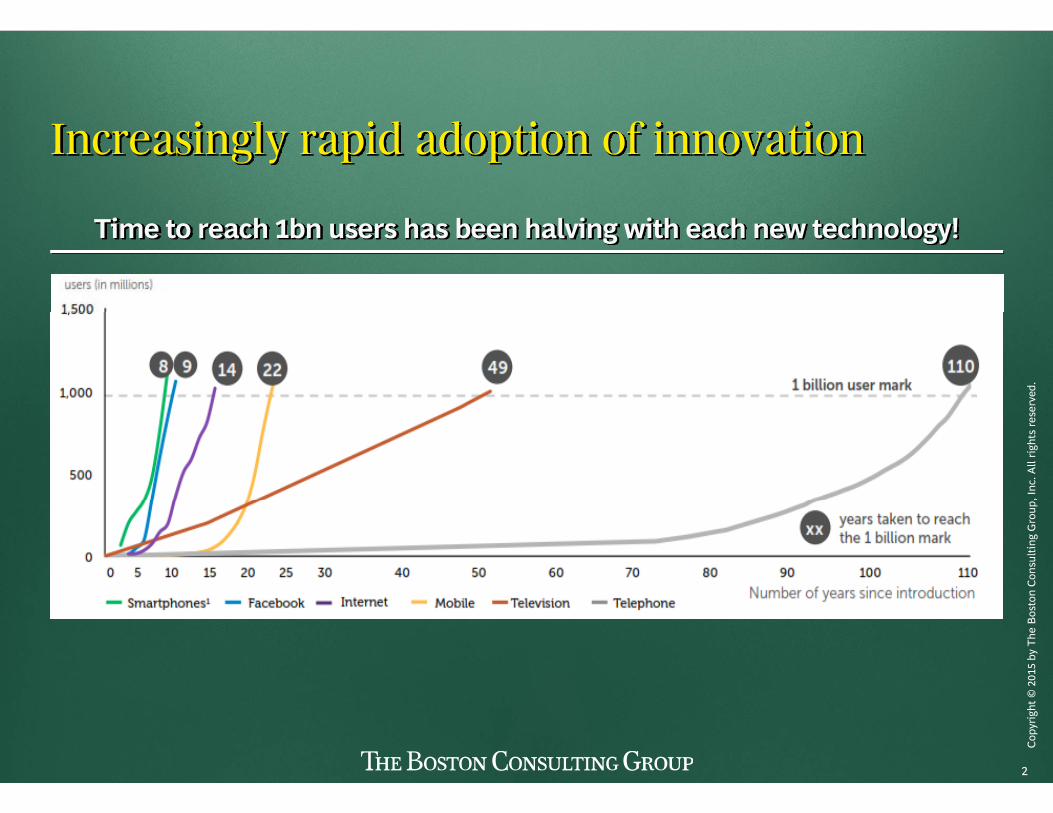

I i l id d i f i iIncreasingly rapid adoption of innovation

i h b h b h l i i h h h l !Time to reach 1bn users has been halving with each new technology!

rved

., I

nc. A

ll rig

hts

rese

n Co

nsul

ting

Gro

up20

15 b

y Th

e B

osto

n

IDFC Alternatives Digitzation 20March15 Fin.pptx 2

Copy

right

©

Th i i h iThe internet is changingSpend/saveSpend/save

rved

.Learn/ Work

, Inc

. All

right

s re

seinform WorkHOW WE

n Co

nsul

ting

Gro

upConnect/ playMove

2015

by

The

Bos

ton

Better our

IDFC Alternatives Digitzation 20March15 Fin.pptx 3

Copy

right

© Better our

world

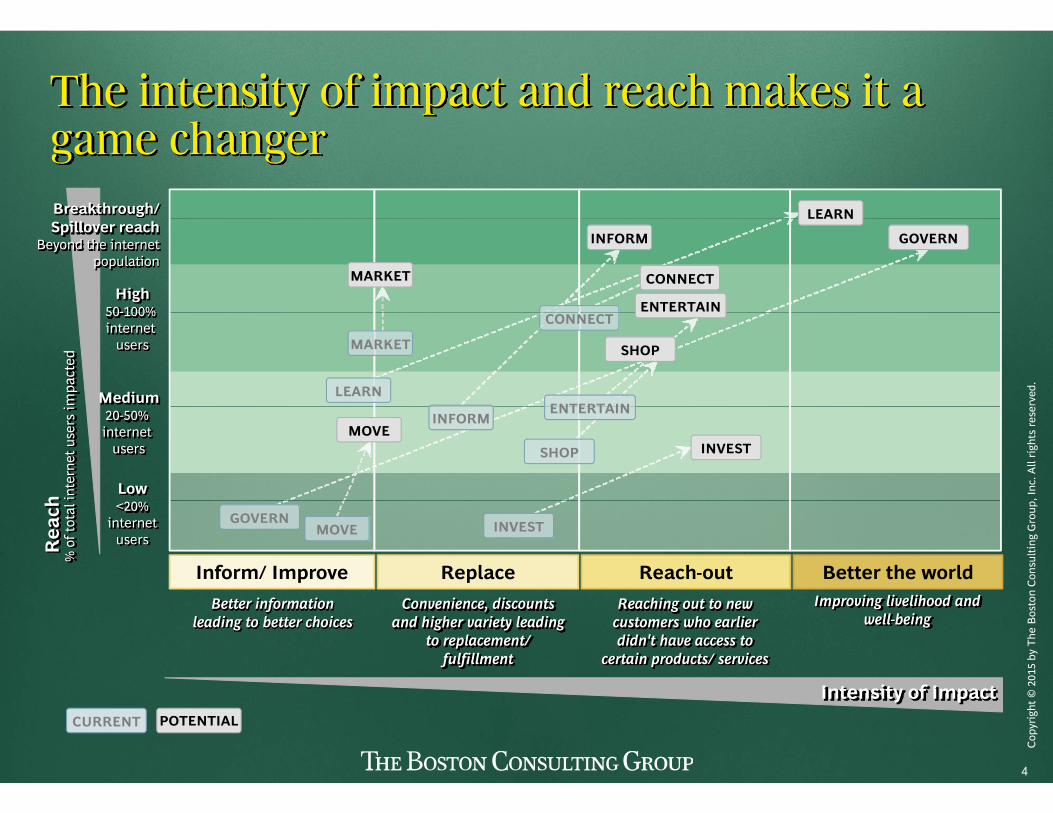

The intensity of impact and reach makes it a hgame changer

Breakthrough/ LEARN

High50-100%

Spillover reachBeyond the internet

population

GOVERN

LEARN

MARKET

INFORM

ENTERTAIN

CONNECT

rved

.

50-100% internet

users

Mediummpa

cted

SHOP

LEARN

MARKET

CONNECT

ENTERTAIN

, Inc

. All

right

s re

se20-50% internet

users

Low

h inte

rnet

use

rs i

MOVEINVEST

INFORM

SHOP

ENTERTAIN

n Co

nsul

ting

Gro

up

Inform/ Improve

<20% internet

users Rea

ch%

of t

otal

Replace Reach-out Better the worldi i i

GOVERNMOVE INVEST

2015

by

The

Bos

ton

Intensity of Impact

Better information leading to better choices

Convenience, discounts and higher variety leading

to replacement/ fulfillment

Reaching out to new customers who earlier didn't have access to

certain products/ services

Improving livelihood and well-being

IDFC Alternatives Digitzation 20March15 Fin.pptx 4

Copy

right

© Intensity of Impact

POTENTIALCURRENT

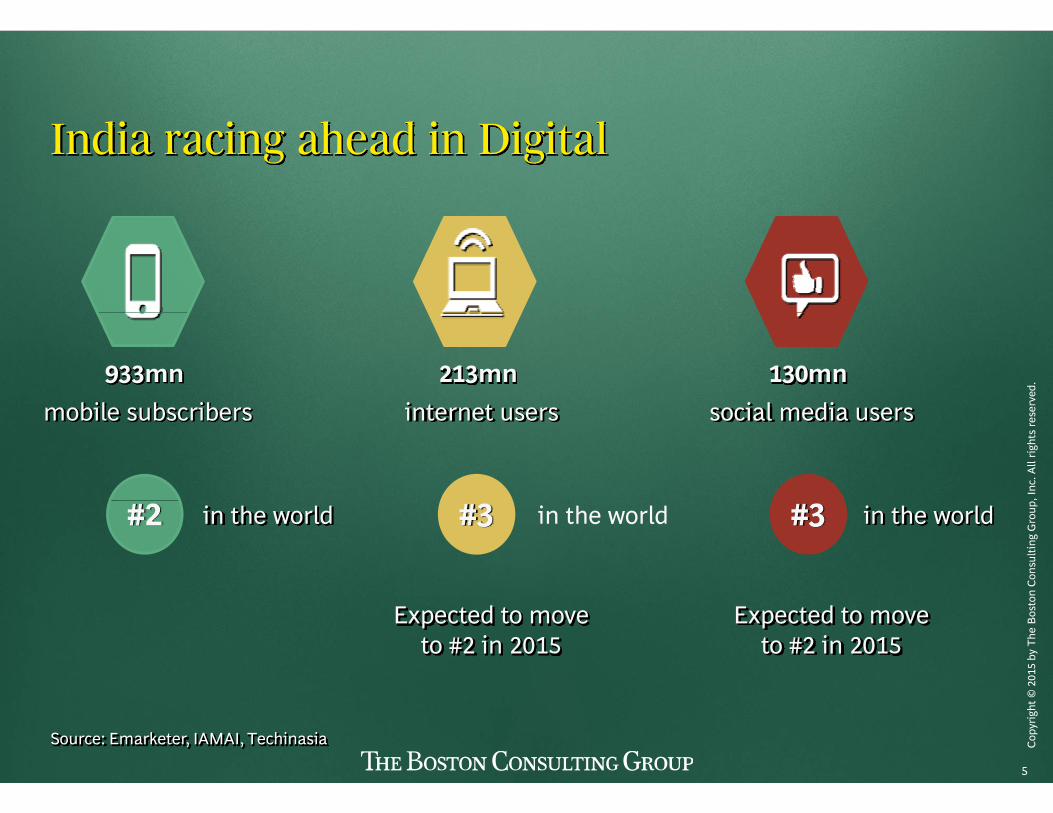

I di i h d i Di i lIndia racing ahead in Digital

rved

.933mn bil b ib

213mn i t t

130mn i l di

, Inc

. All

right

s re

semobile subscribers internet users social media users

n Co

nsul

ting

Gro

up#2 #3 #3in the world in the world in the world

2015

by

The

Bos

ton

Expected to moveto #2 in 2015

Expected to moveto #2 in 2015

IDFC Alternatives Digitzation 20March15 Fin.pptx 5

Copy

right

©

Source: Emarketer, IAMAI, Techinasia

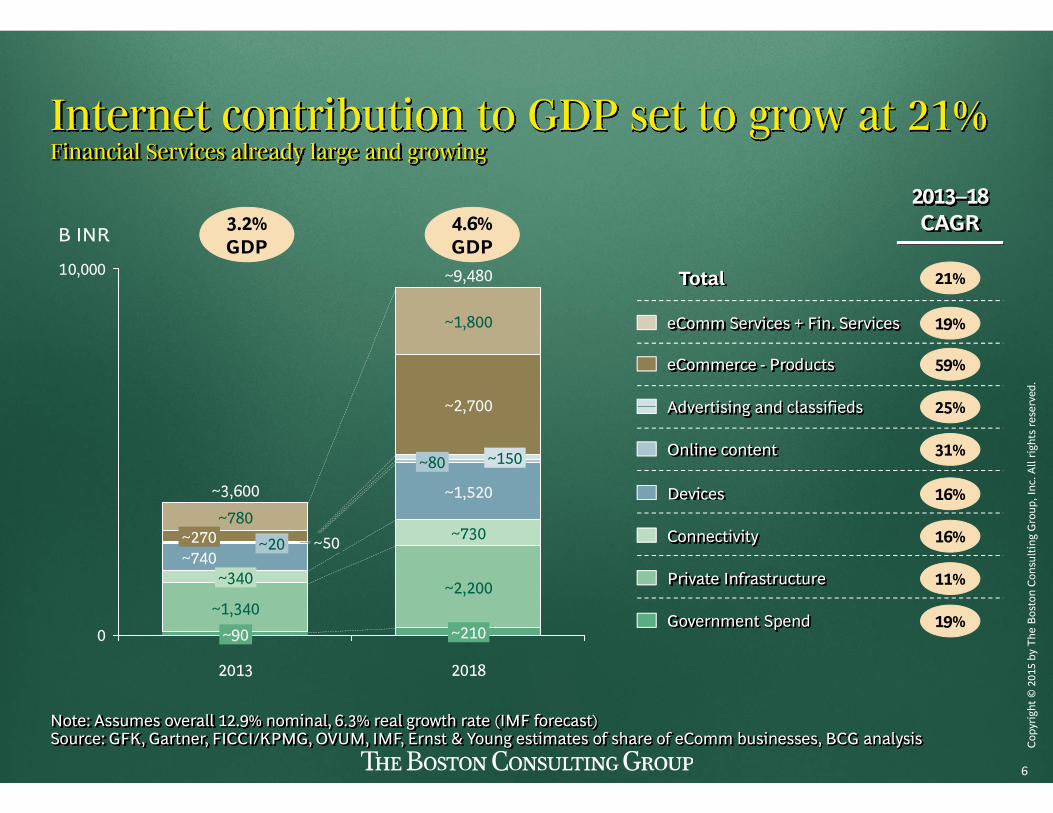

Internet contribution to GDP set to grow at 21%Internet contribution to GDP set to grow at 21%Financial Services already large and growing

3 2% 4 6%2013–18 CAGR

10,000

B INR

~9,480 21%Total

3.2% GDP

4.6% GDP

CAGR

rved

.

~2 700

~1,800

Advertising and classifieds

19%

25%

eCommerce - Products 59%

eComm Services + Fin. Services

, Inc

. All

right

s re

se~2,700

~150

~3,600

~80

~1,520 Devices

Online content

Advertising and classifieds 25%

31%

16%

n Co

nsul

ting

Gro

up

~270 ~50~740

~340

~20 ~730

~2,200

~780

Private Infrastructure

Connectivity 16%

11%

2015

by

The

Bos

ton

0

2013

~90~1,340

,

~210

2018

Government Spend 19%

IDFC Alternatives Digitzation 20March15 Fin.pptx 6

Copy

right

©

Note: Assumes overall 12.9% nominal, 6.3% real growth rate (IMF forecast)Source: GFK, Gartner, FICCI/KPMG, OVUM, IMF, Ernst & Young estimates of share of eComm businesses, BCG analysis

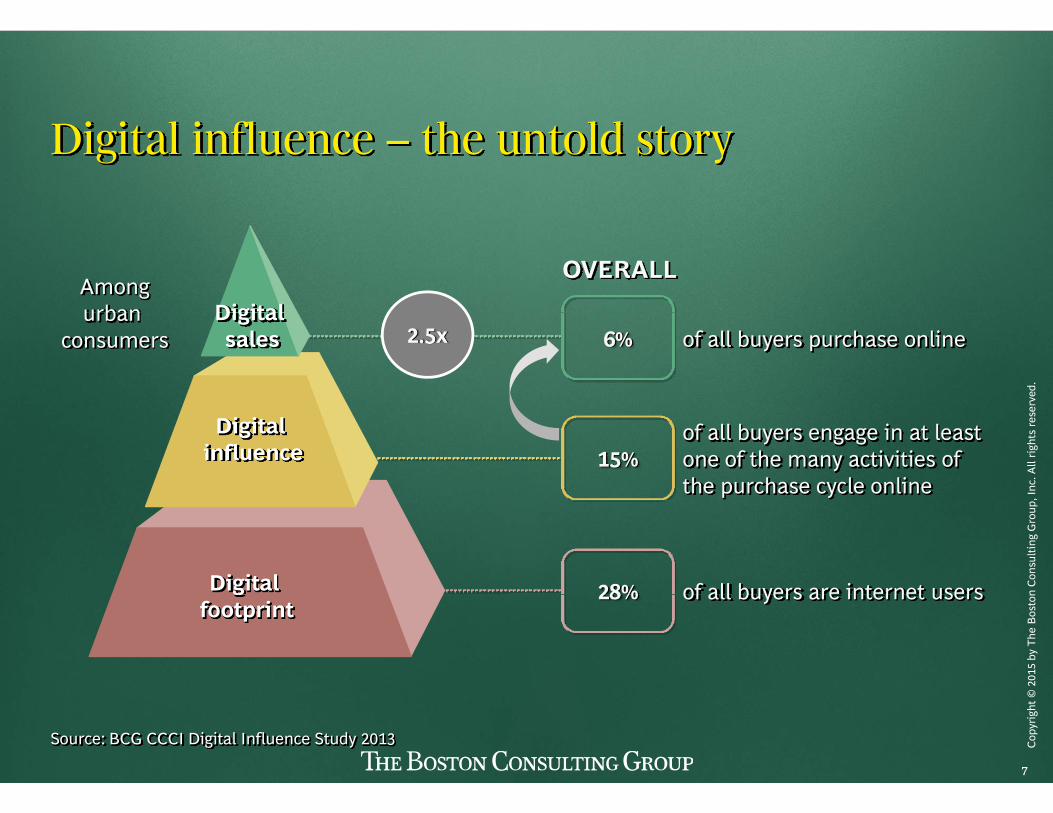

Di i l i fl h ldDigital influence – the untold story

Amongurban

OVERALL

Digital

rved

.

urban consumers of all buyers purchase online 6%2.5x

Digital sales

, Inc

. All

right

s re

se

of all buyers engage in at least one of the many activities of the purchase cycle online

15%Digital

influence

n Co

nsul

ting

Gro

up

of all buyers are internet users28%Digital

2015

by

The

Bos

tonof all buyers are internet users28%g

footprint

IDFC Alternatives Digitzation 20March15 Fin.pptx 7

Copy

right

©

Source: BCG CCCI Digital Influence Study 2013

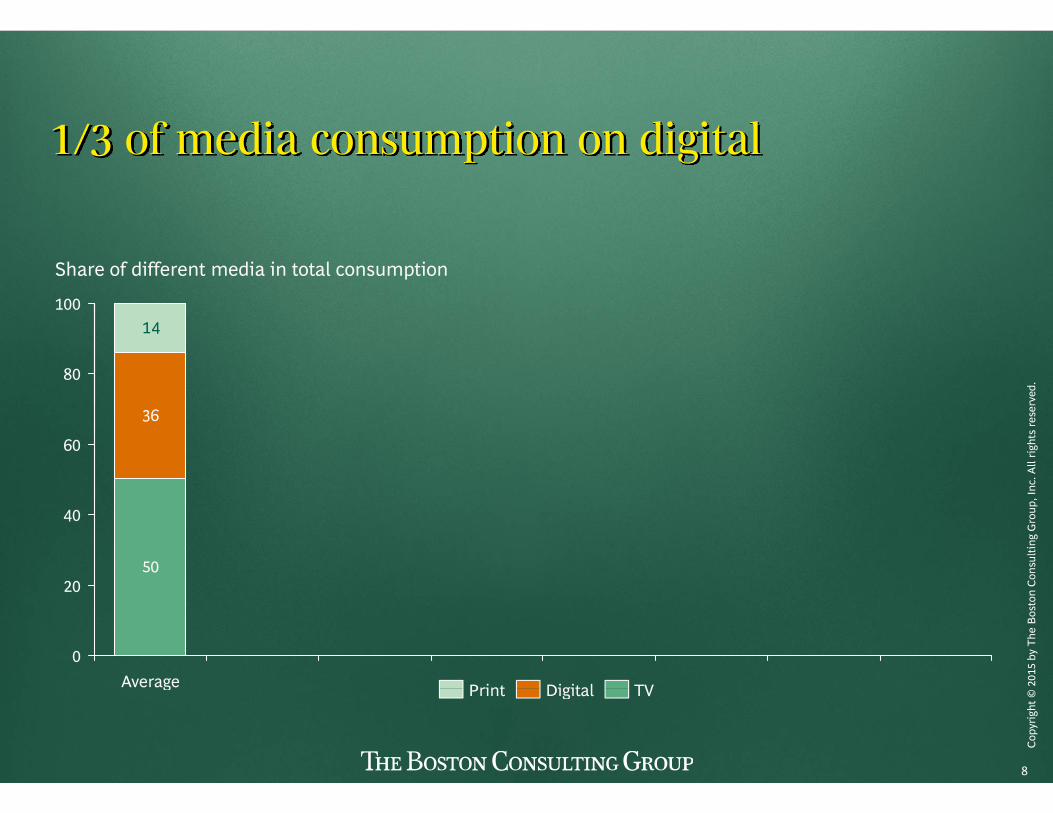

1/3 f di i di i l1/3 of media consumption on digital

100

Share of different media in total consumption

rved

.

14

80

, Inc

. All

right

s re

se36

60

n Co

nsul

ting

Gro

up

50

40

20

2015

by

The

Bos

ton

0Average Print Digital TV

IDFC Alternatives Digitzation 20March15 Fin.pptx 8

Copy

right

© g Print Digital TV

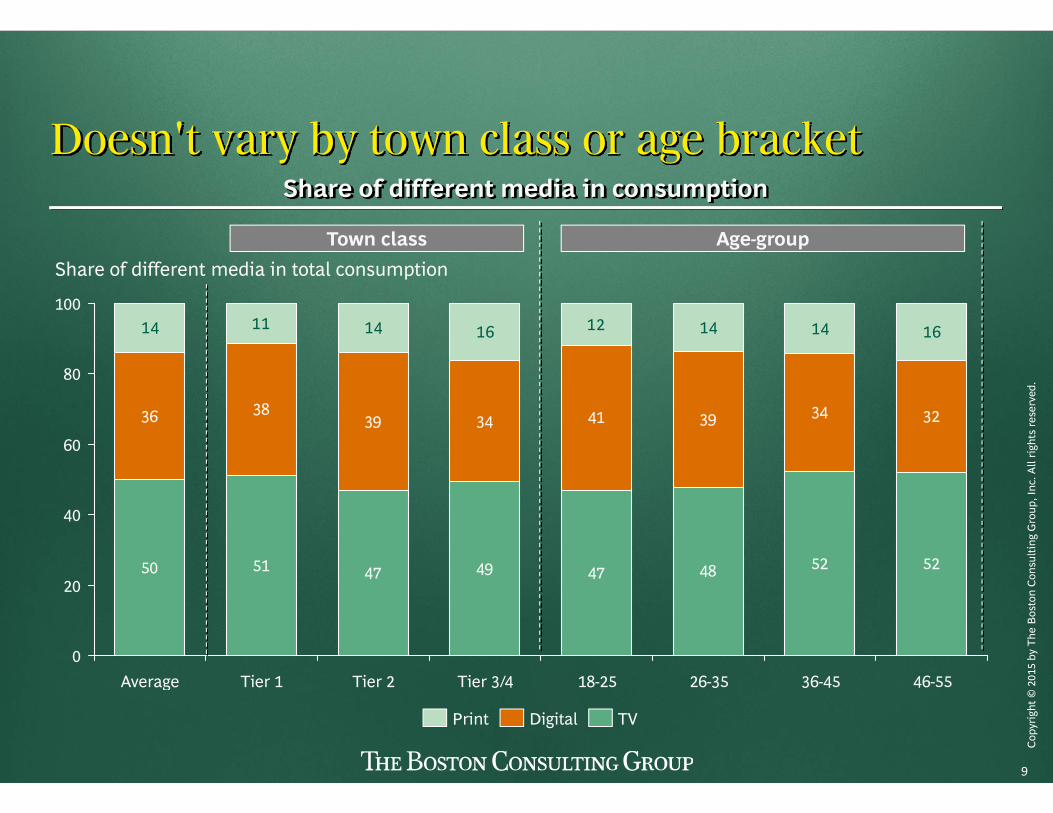

D ' b l b kDoesn't vary by town class or age bracketShare of different media in consumption

100

Share of different media in total consumptionTown class Age-group

rved

.

38

14 11 14 12 14 14 1616

80

, Inc

. All

right

s re

se36 3839 34 41 39 34 32

60

n Co

nsul

ting

Gro

up

50 51 47 49 47 48 52 52

40

20

2015

by

The

Bos

ton

036-4526-3518-25Tier 3/4Tier 2Tier 1Average 46-55

IDFC Alternatives Digitzation 20March15 Fin.pptx 9

Copy

right

© g

TVPrint Digital

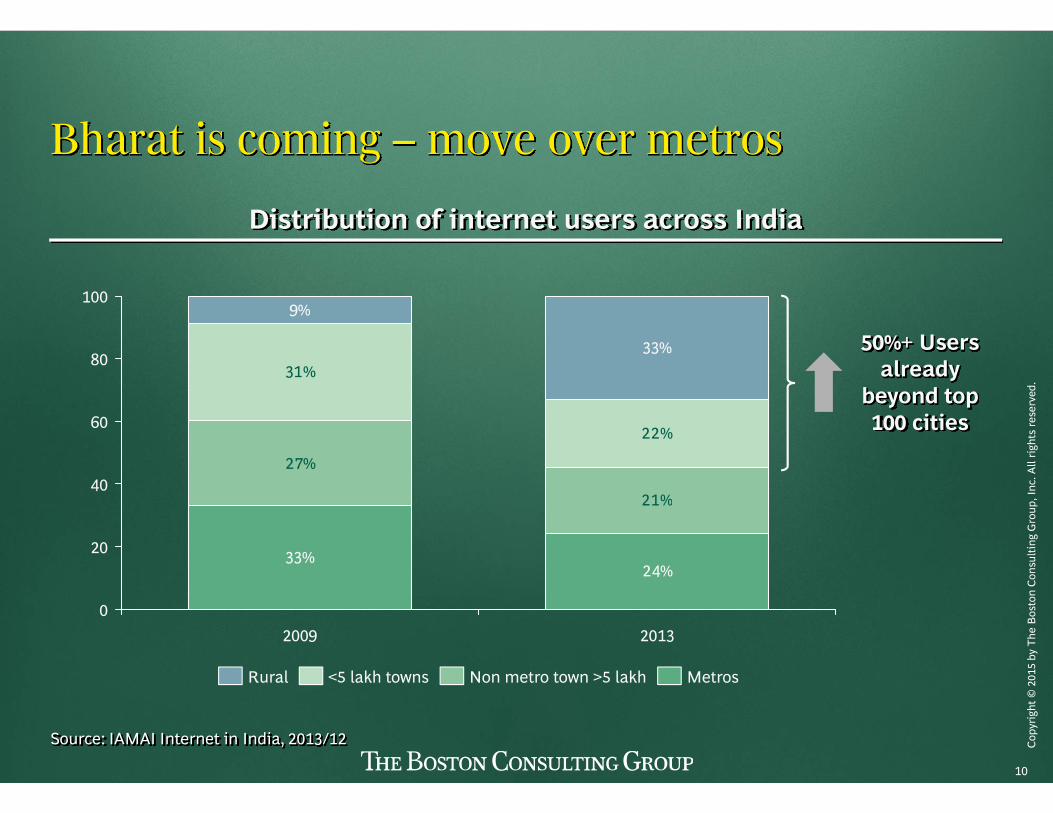

Bh i iBharat is coming – move over metros

Distribution of internet users across India

9%100

Distribution of internet users across India

rved

.

31%33%

9%

8050%+ Users

already beyond top

, Inc

. All

right

s re

se

27%

21%

22%60

40

y p100 cities

n Co

nsul

ting

Gro

up

33%24%

21%

20

2015

by

The

Bos

ton

020132009

Metros<5 lakh towns Non metro town >5 lakhRural

IDFC Alternatives Digitzation 20March15 Fin.pptx 10

Copy

right

©

Source: IAMAI Internet in India, 2013/12

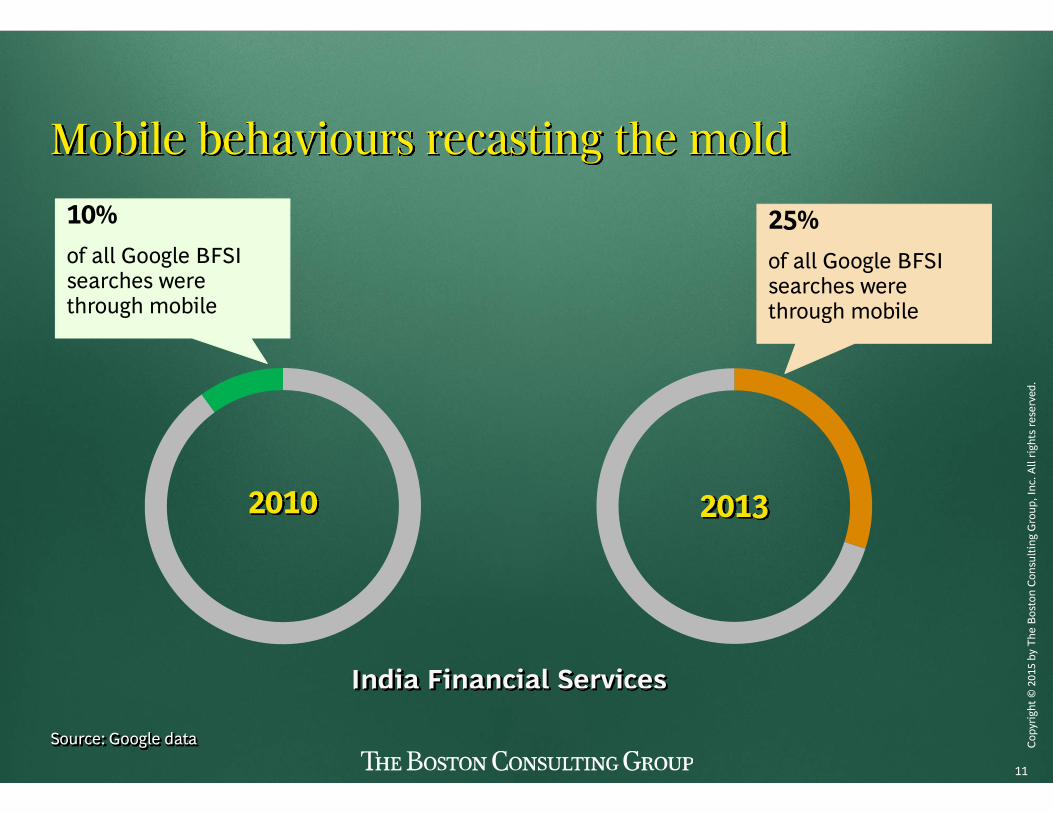

M bil b h i i h ld10% 25%

Mobile behaviours recasting the mold10% of all Google BFSI searches were through mobile

25% of all Google BFSI searches were through mobile

rved

.

through mobile through mobile

, Inc

. All

right

s re

se

2010 2013

n Co

nsul

ting

Gro

up2010 2013

2015

by

The

Bos

ton

India Financial Services

IDFC Alternatives Digitzation 20March15 Fin.pptx 11

Copy

right

© India Financial Services

Source: Google data

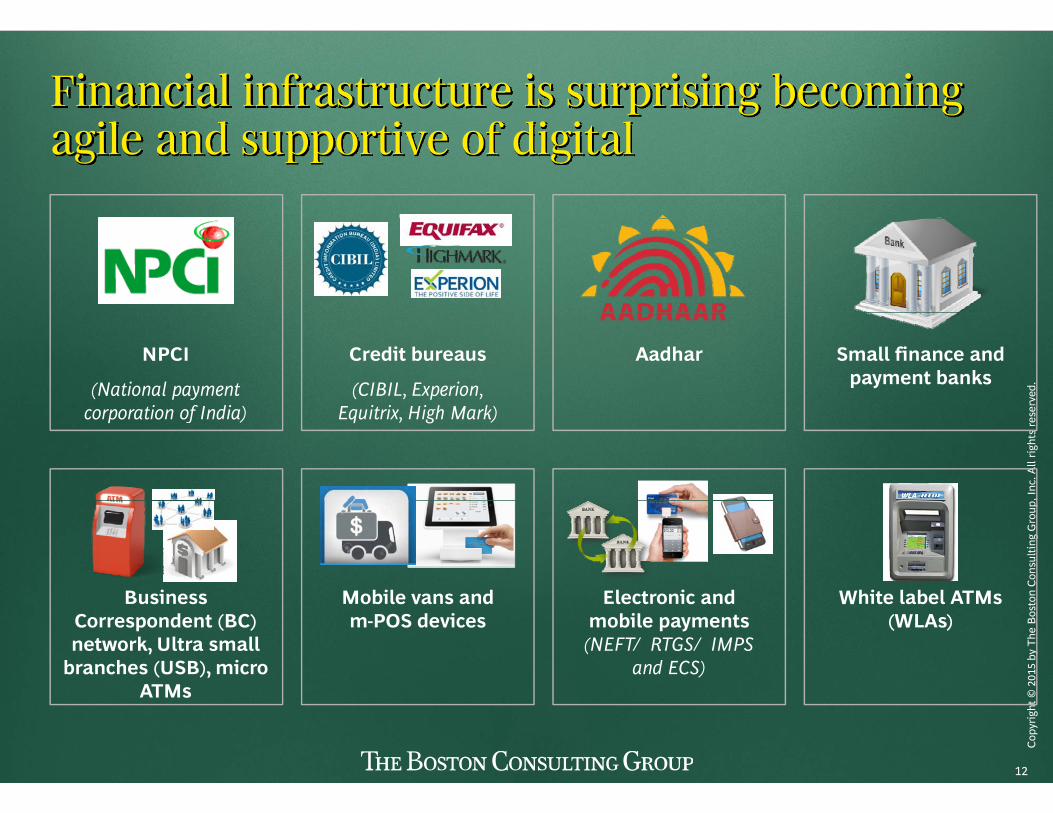

Financial infrastructure is surprising becoming il d i f di i lagile and supportive of digital

rved

.

NPCI

(National payment i f I di )

Credit bureaus

(CIBIL, Experion, E i i Hi h M k)

Aadhar Small finance and payment banks

, Inc

. All

right

s re

secorporation of India) Equitrix, High Mark)

n Co

nsul

ting

Gro

up

Business Mobile vans and Electronic and White label ATMs

2015

by

The

Bos

tonBusiness

Correspondent (BC) network, Ultra small

branches (USB), micro ATMs

Mobile vans and m-POS devices

Electronic and mobile payments (NEFT/ RTGS/ IMPS

and ECS)

White label ATMs (WLAs)

IDFC Alternatives Digitzation 20March15 Fin.pptx 12

Copy

right

© ATMs

A dAgenda

rved

.More examples and learning

, Inc

. All

right

s re

se

How to win

n Co

nsul

ting

Gro

up20

15 b

y Th

e B

osto

n

IDFC Alternatives Digitzation 20March15 Fin.pptx 13

Copy

right

©

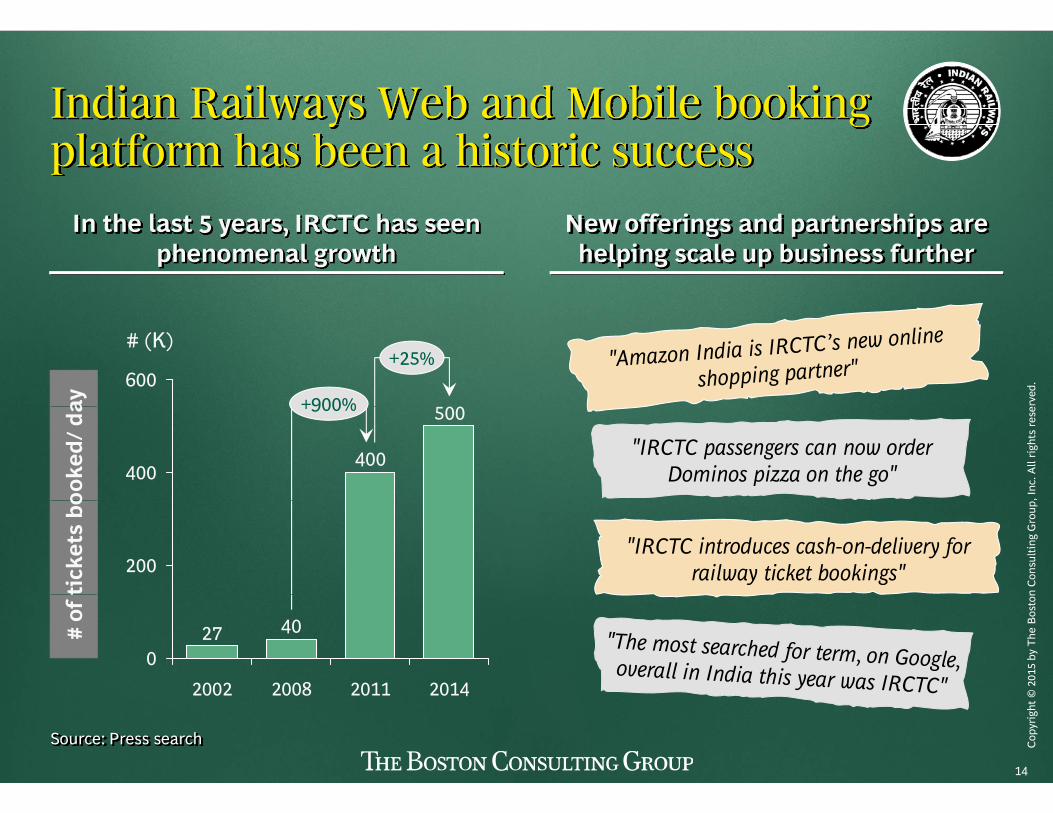

Indian Railways Web and Mobile booking y gplatform has been a historic success

In the last 5 ears IRCTC has seen Ne offerings and partnerships areIn the last 5 years, IRCTC has seen phenomenal growth

New offerings and partnerships are helping scale up business further

rved

.

00

600+900%

# (K)+25%

ay

, Inc

. All

right

s re

se500

400400

+900%

ooke

d/ d

a

"IRCTC passengers can now order Dominos pizza on the go"

n Co

nsul

ting

Gro

up

200

tick

ets

bo

"IRCTC introduces cash-on-delivery for railway ticket bookings"

2015

by

The

Bos

ton

40270

201120082002 2014

# of

t

IDFC Alternatives Digitzation 20March15 Fin.pptx 14

Copy

right

© 201120082002 2014

Source: Press search

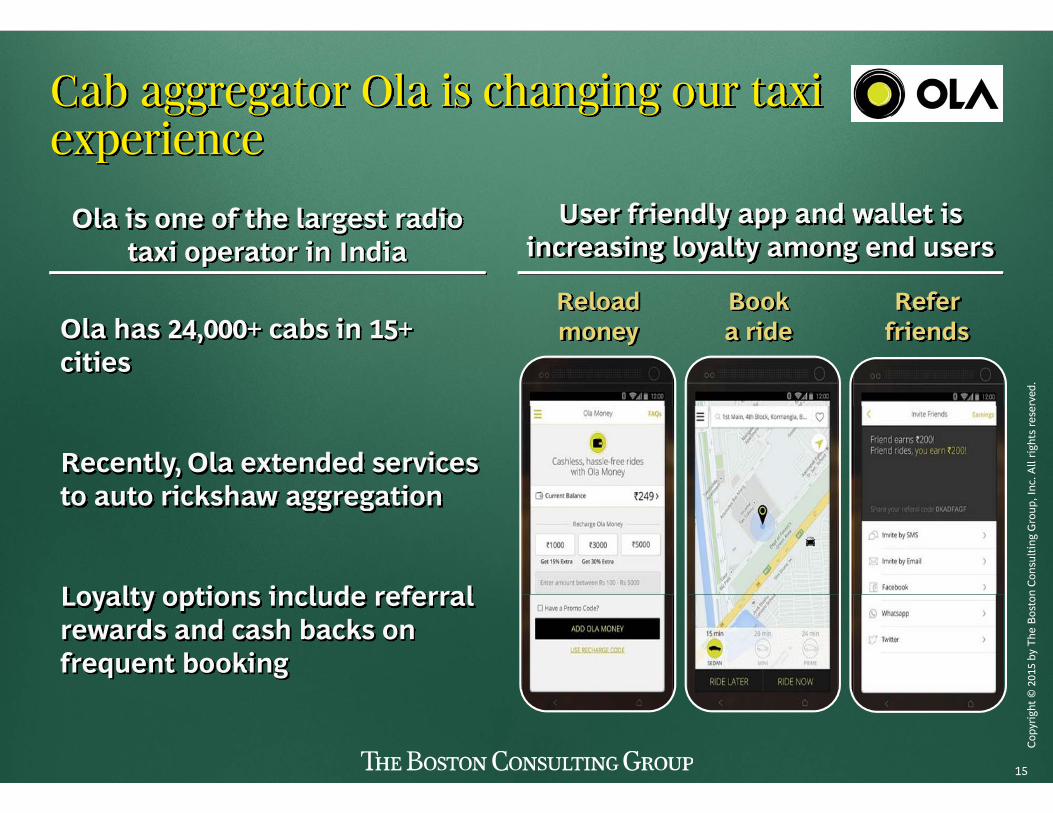

Cab aggregator Ola is changing our taxi iexperience

Ola is one of the largest radio User friendly app and wallet isOla is one of the largest radio taxi operator in India

User friendly app and wallet is increasing loyalty among end users

Reload Book Refer

rved

.

Ola has 24,000+ cabs in 15+ cities

money a ride friends

, Inc

. All

right

s re

se

Recently, Ola extended services to auto rickshaw aggregation

n Co

nsul

ting

Gro

up

to auto rickshaw aggregation

Loyalty options include referral

2015

by

The

Bos

tonLoyalty options include referral

rewards and cash backs on frequent booking

IDFC Alternatives Digitzation 20March15 Fin.pptx 15

Copy

right

©

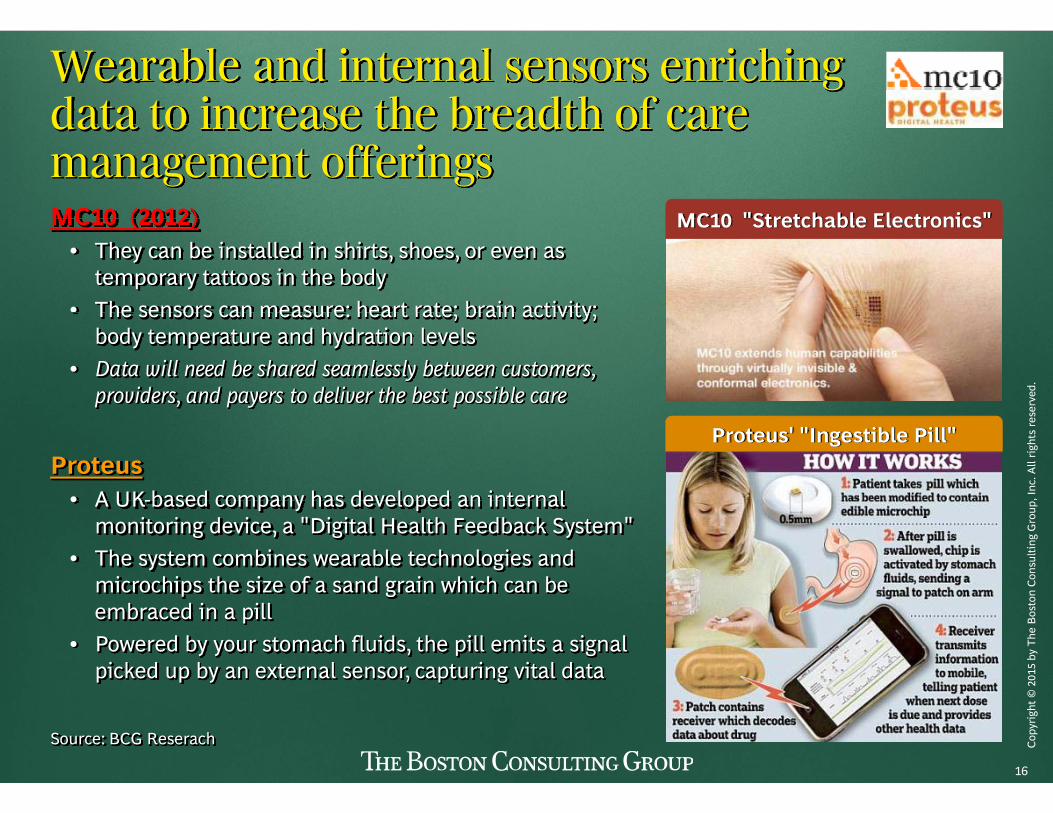

Wearable and internal sensors enrichingdata to increase the breadth of caredata to increase the breadth of care management offeringsMC10 (2012) MC10 "Stretchable Electronics"MC10 (2012)

• They can be installed in shirts, shoes, or even as temporary tattoos in the body

• The sensors can measure: heart rate; brain activity;

MC10 Stretchable Electronics

rved

.

The sensors can measure: heart rate; brain activity; body temperature and hydration levels

• Data will need be shared seamlessly between customers, providers, and payers to deliver the best possible care

, Inc

. All

right

s re

se

p , p y p

Proteus• A UK-based company has developed an internal

Proteus' "Ingestible Pill"

n Co

nsul

ting

Gro

up• A UK-based company has developed an internal monitoring device, a "Digital Health Feedback System"

• The system combines wearable technologies and microchips the size of a sand grain which can be

2015

by

The

Bos

tonp g

embraced in a pill • Powered by your stomach fluids, the pill emits a signal

picked up by an external sensor, capturing vital data

IDFC Alternatives Digitzation 20March15 Fin.pptx 16

Copy

right

©

Source: BCG Reserach

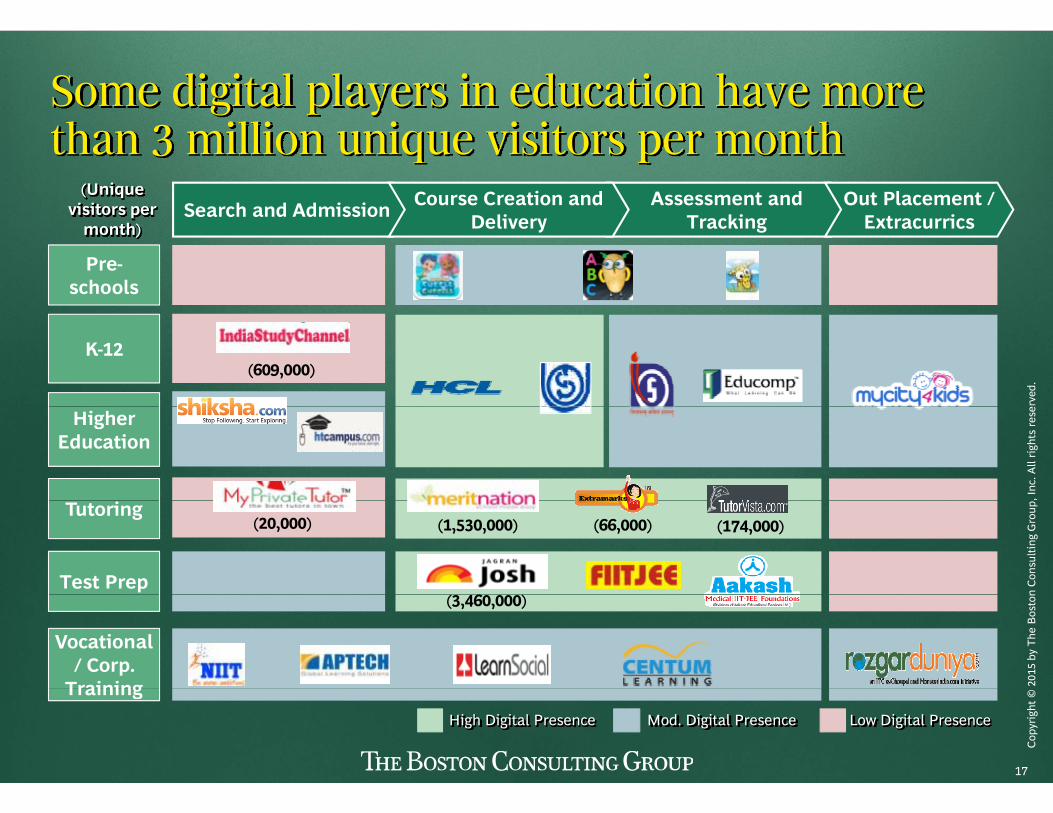

Some digital players in education have more h illi i i i hthan 3 million unique visitors per month

Search and Admission Assessment and Tracking

Course Creation and Delivery

Out Placement / Extracurrics

(Unique visitors per

TrackingDelivery Extracurrics

Pre-schools

month)

rved

.

K-12(609,000)

, Inc

. All

right

s re

seHigher Education

n Co

nsul

ting

Gro

upTutoring

Test Prep

(20,000) (1,530,000)

( 6 )

(66,000) (174,000)

2015

by

The

Bos

ton

Vocational / Corp.

Training

(3,460,000)

IDFC Alternatives Digitzation 20March15 Fin.pptx 17

Copy

right

© Training

High Digital Presence Mod. Digital Presence Low Digital Presence

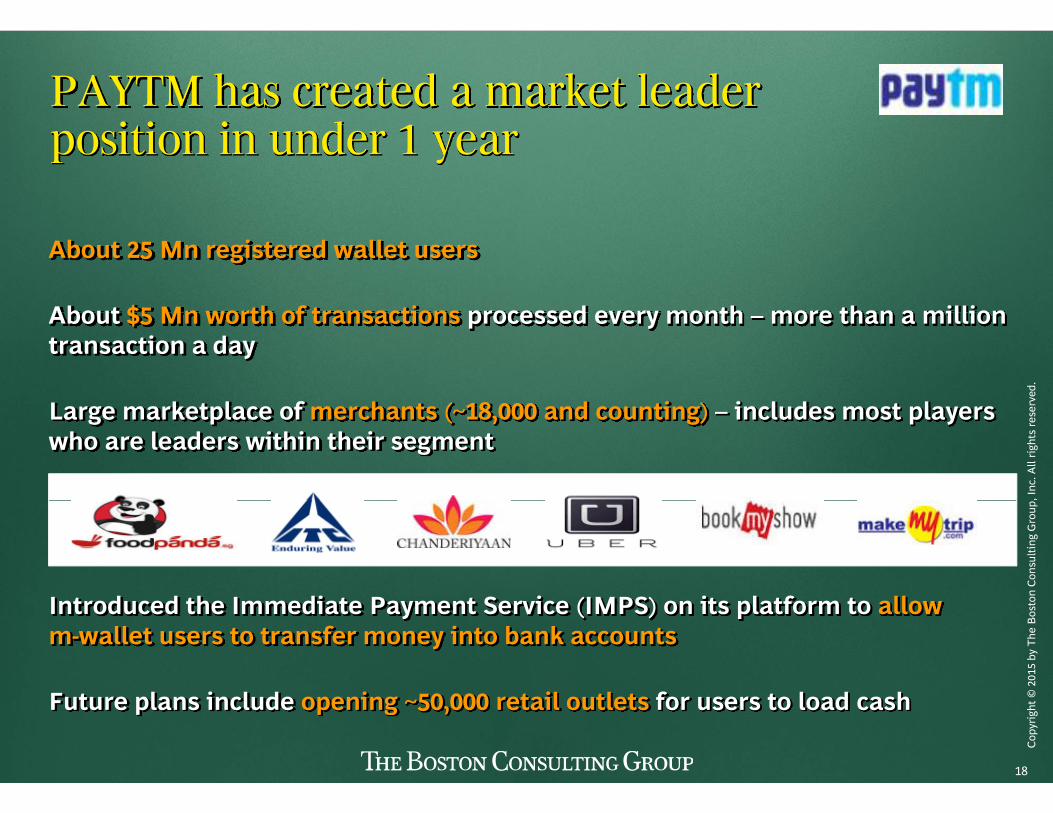

PAYTM has created a market leaderi i i dposition in under 1 year

About 25 Mn registered wallet users

About $5 Mn worth of transactions processed every month more than a million

rved

.

About $5 Mn worth of transactions processed every month – more than a million transaction a day

Large marketplace of merchants ( 18 000 and counting) includes most players

, Inc

. All

right

s re

seLarge marketplace of merchants (~18,000 and counting) – includes most players who are leaders within their segment

n Co

nsul

ting

Gro

up20

15 b

y Th

e B

osto

n

Introduced the Immediate Payment Service (IMPS) on its platform to allow m-wallet users to transfer money into bank accounts

IDFC Alternatives Digitzation 20March15 Fin.pptx 18

Copy

right

©

Future plans include opening ~50,000 retail outlets for users to load cash

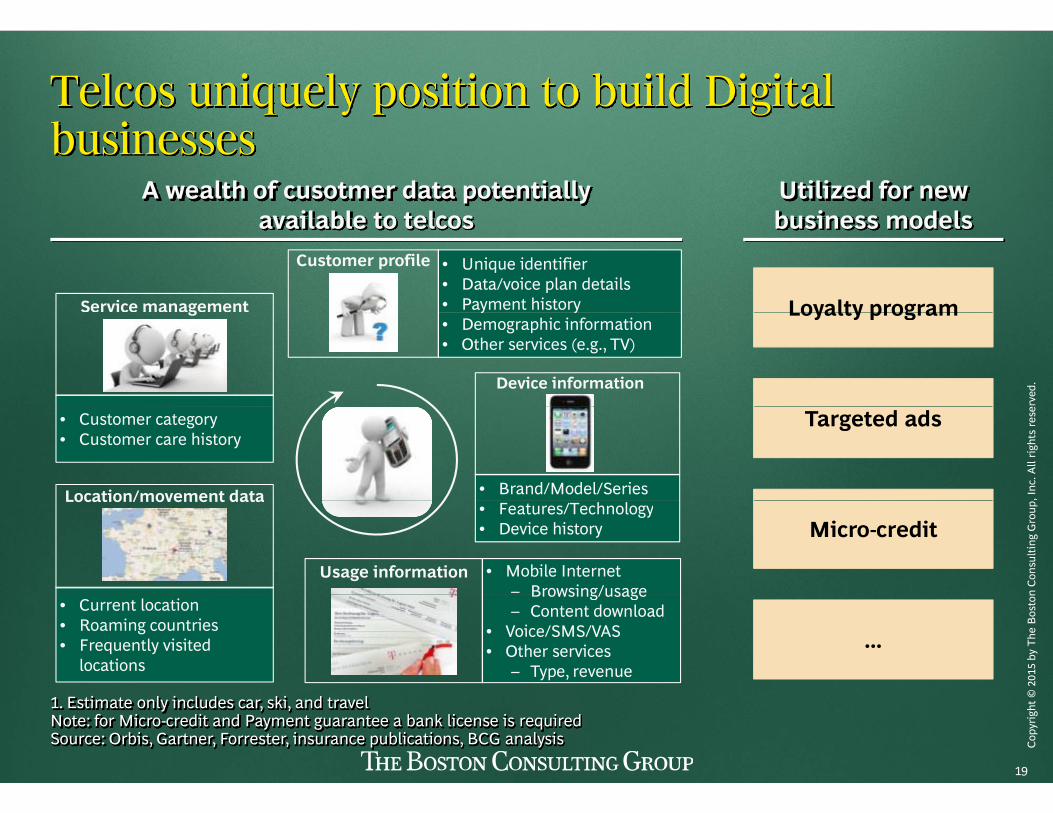

Telcos uniquely position to build Digital b ibusinesses

A wealth of cusotmer data potentially available to telcos

Utilized for new business models

Loyalty programService management

• Unique identifier• Data/voice plan details• Payment history

Customer profile

available to telcos business models

rved

.

Loyalty programg

Device information

y y• Demographic information• Other services (e.g., TV)

, Inc

. All

right

s re

seTargeted ads• Customer category• Customer care history

Location/movement data • Brand/Model/Series

n Co

nsul

ting

Gro

up

Micro-creditLocation/movement data

• Features/Technology• Device history

• Mobile Internet– Browsing/usage

Usage information

2015

by

The

Bos

ton

• Current location• Roaming countries• Frequently visited

locations

Browsing/usage– Content download

• Voice/SMS/VAS• Other services

– Type, revenue

...

IDFC Alternatives Digitzation 20March15 Fin.pptx 19

Copy

right

©

1. Estimate only includes car, ski, and travel Note: for Micro-credit and Payment guarantee a bank license is requiredSource: Orbis, Gartner, Forrester, insurance publications, BCG analysis

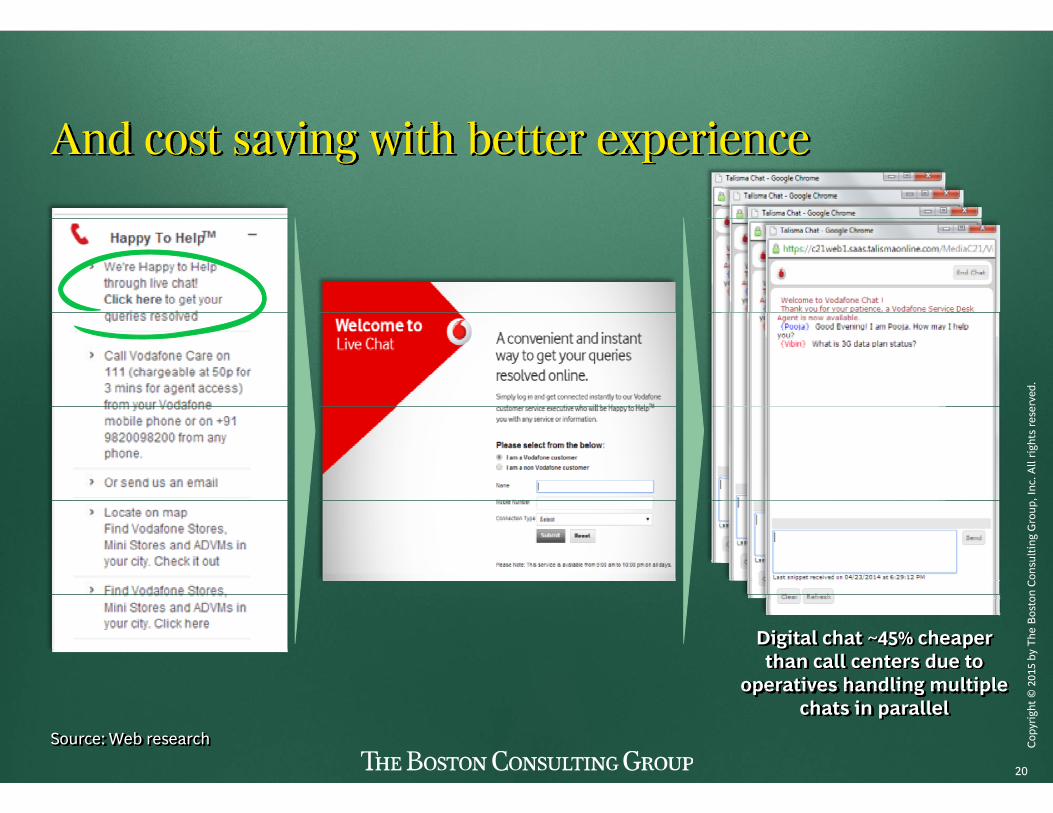

A d i i h b iAnd cost saving with better experience

rved

., I

nc. A

ll rig

hts

rese

n Co

nsul

ting

Gro

up20

15 b

y Th

e B

osto

n

Digital chat ~45% cheaper than call centers due to

operatives handling multiple

IDFC Alternatives Digitzation 20March15 Fin.pptx 20

Copy

right

© operatives handling multiple

chats in parallelSource: Web research

Amazon has translated Digital themein their back endin their back end

rved

., I

nc. A

ll rig

hts

rese

n Co

nsul

ting

Gro

up20

15 b

y Th

e B

osto

n

IDFC Alternatives Digitzation 20March15 Fin.pptx 21

Copy

right

©

BHP BilliBHP Billiton

rved

., I

nc. A

ll rig

hts

rese

n Co

nsul

ting

Gro

up20

15 b

y Th

e B

osto

n

IDFC Alternatives Digitzation 20March15 Fin.pptx 22

Copy

right

©

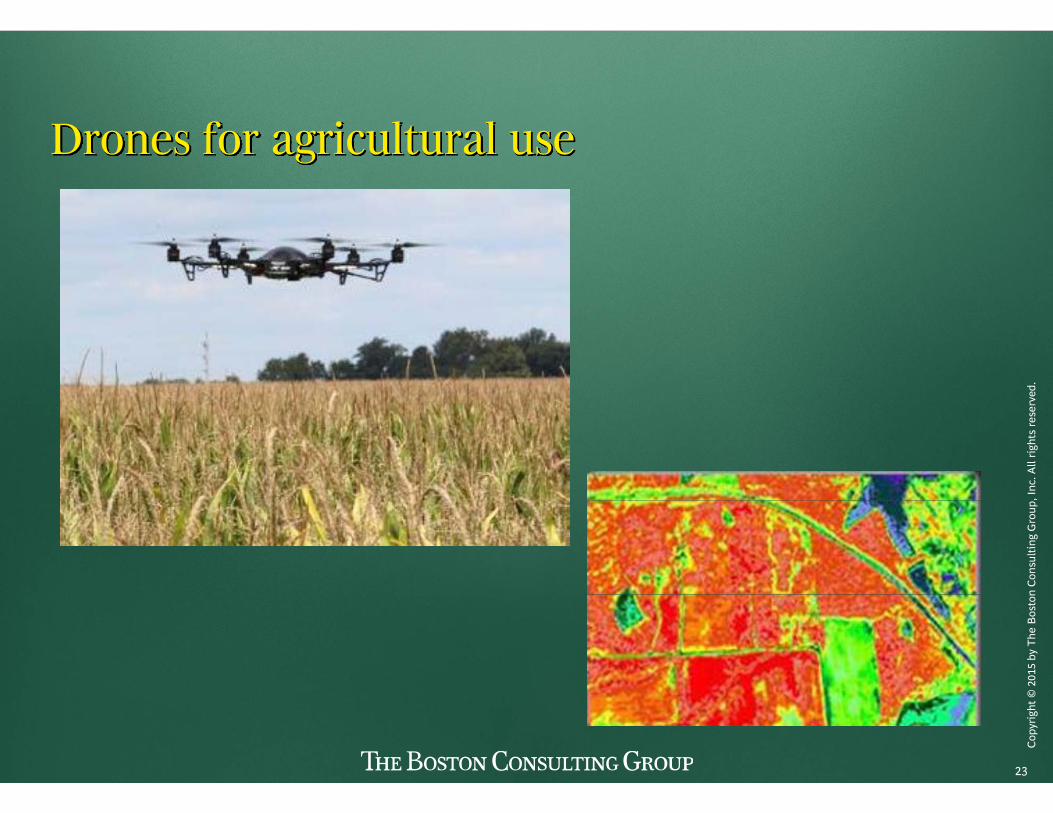

D f i l lDrones for agricultural use

rved

., I

nc. A

ll rig

hts

rese

n Co

nsul

ting

Gro

up20

15 b

y Th

e B

osto

n

IDFC Alternatives Digitzation 20March15 Fin.pptx 23

Copy

right

©

A dAgenda

rved

.More examples and learning

, Inc

. All

right

s re

se

How to win

n Co

nsul

ting

Gro

up20

15 b

y Th

e B

osto

n

IDFC Alternatives Digitzation 20March15 Fin.pptx 24

Copy

right

©

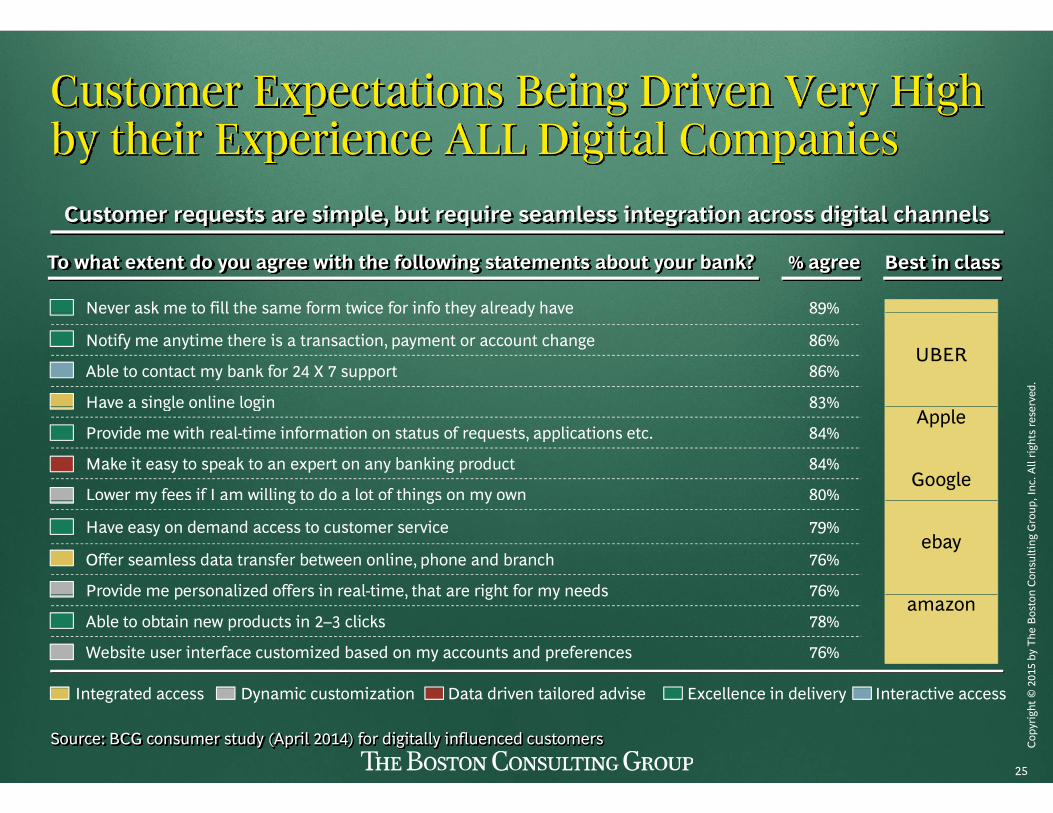

Customer Expectations Being Driven Very High b h i E i ALL Di i l C iby their Experience ALL Digital Companies

Customer requests are simple, but require seamless integration across digital channels

Best in classTo what extent do you agree with the following statements about your bank? % agree

Never ask me to fill the same form twice for info they already have 89%

Customer requests are simple, but require seamless integration across digital channels

rved

.

UBER

Never ask me to fill the same form twice for info they already have 89%

Notify me anytime there is a transaction, payment or account change 86%

Able to contact my bank for 24 X 7 support 86%

Have a single online login 83%

, Inc

. All

right

s re

seApple

Provide me with real-time information on status of requests, applications etc. 84%

Make it easy to speak to an expert on any banking product 84%

Have a single online login 83%

Lower my fees if I am willing to do a lot of things on my own 80%

n Co

nsul

ting

Gro

up

ebay

y g g y

Have easy on demand access to customer service 79%

Provide me personalized offers in real-time, that are right for my needs 76%

Offer seamless data transfer between online, phone and branch 76%

2015

by

The

Bos

ton

amazon

E ll i d li I t tiI t t d D t d i t il d d iD i t i ti

Able to obtain new products in 2–3 clicks 78%

Provide me personalized offers in real time, that are right for my needs 76%

Website user interface customized based on my accounts and preferences 76%

IDFC Alternatives Digitzation 20March15 Fin.pptx 25

Copy

right

©

Source: BCG consumer study (April 2014) for digitally influenced customers

Excellence in delivery Interactive accessIntegrated access Data driven tailored adviseDynamic customization

E i b i DIGITALEvery company is becoming a DIGITAL company

Size of impact

Value x 5-10

Value x 1-∞

rved

.• Enablement of new ecosystems and new business

Business model innovation

2

3

Value x 5-10

Value x 5 10

, Inc

. All

right

s re

se

• Reduction of unit cost of

Cost reduction • Enhancement of business processes

Business transformationecosystems and new business models

• High innovation leading to creation of new products and services

1

2

n Co

nsul

ting

Gro

up

• Reduction of unit cost of Technology services

• Commoditisation and externalisation of Technology

• Improved efficiency, automation and agility

services

2015

by

The

Bos

ton

Nature of

Technology

IDFC Alternatives Digitzation 20March15 Fin.pptx 26

Copy

right

© Nature of

impactSource: BCG experience, cloud analysis

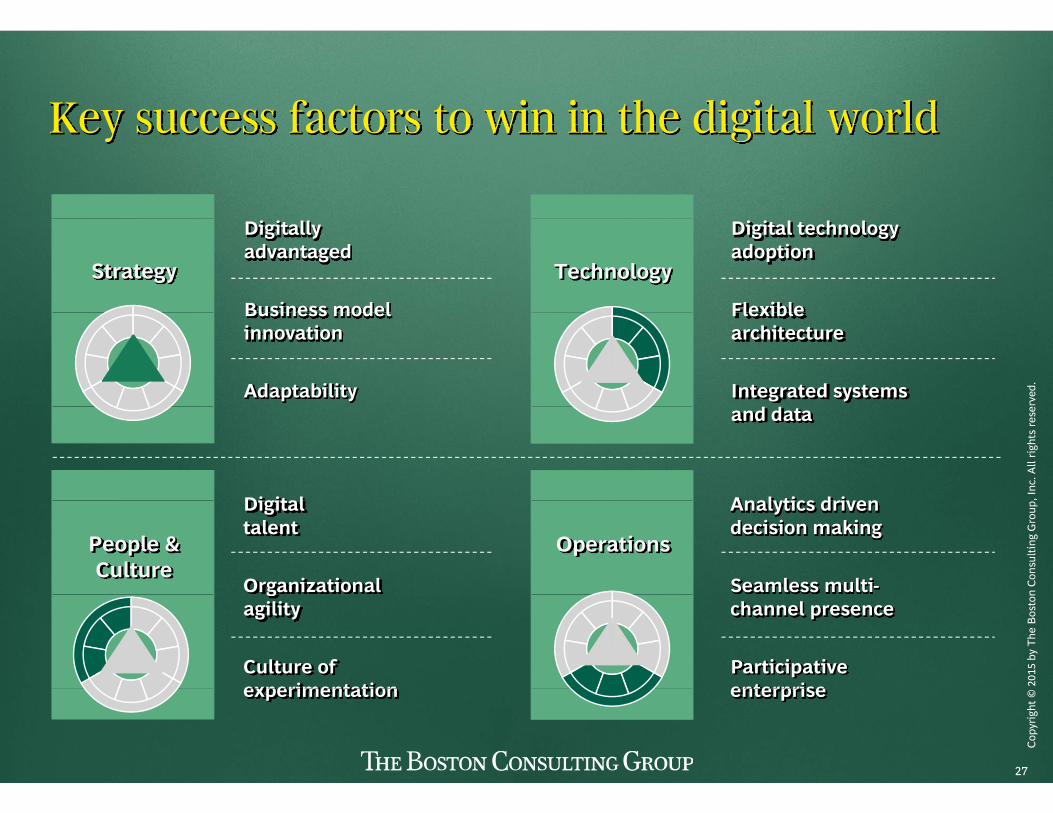

Key success factors to win in the digital worldKey success factors to win in the digital world

Strategy

Digitally advantaged

Business model

Technology

Digital technology adoption

Flexible

rved

.

Business model innovation

Adaptability

Flexible architecture

Integrated systems d d

, Inc

. All

right

s re

se

Digital

and data

Analytics driven

n Co

nsul

ting

Gro

up

People & Culture

Digital talent

Organizational

Operations

Analytics driven decision making

Seamless multi-

2015

by

The

Bos

tong

agility

Culture of experimentation

channel presence

Participative enterprise

IDFC Alternatives Digitzation 20March15 Fin.pptx 27

Copy

right

© experimentation enterprise

Thank you

bcg.com | bcgperspectives.com