Embed Size (px)

Citation preview

Distributed Generation (Solar PV)

Date: 1st March, 2015 Vishal PANDYA

The Energy Solutions Company

2

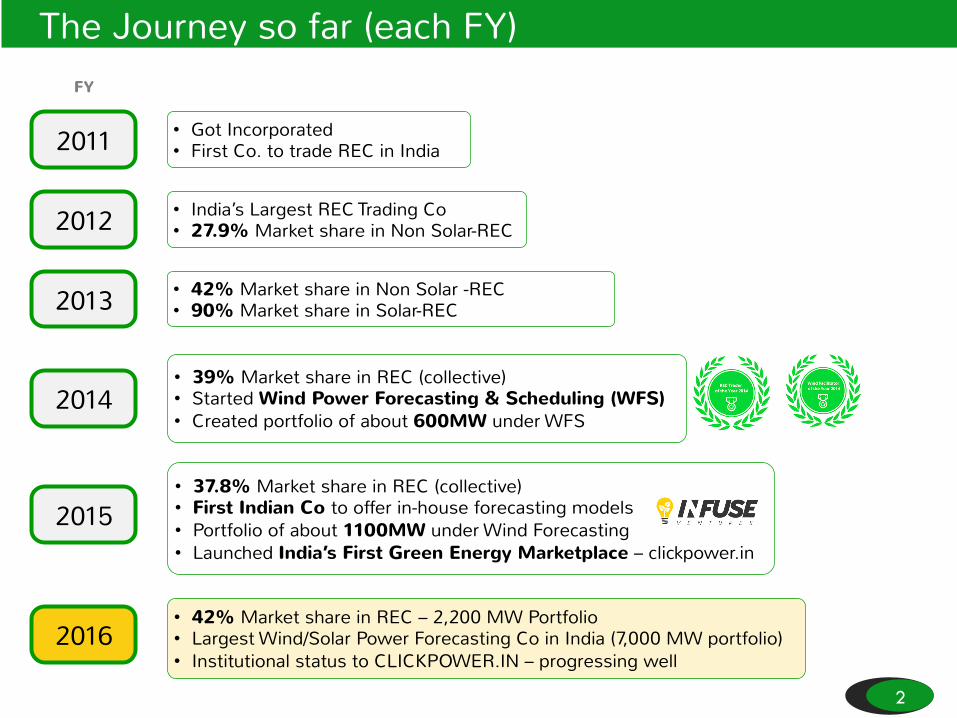

The Journey so far (each FY)

2011

2012

2013

2014

2015

• Got Incorporated • First Co. to trade REC in India

• India’s Largest REC Trading Co • 27.9% Market share in Non Solar-REC

• 42% Market share in Non Solar -REC • 90% Market share in Solar-REC

• 39% Market share in REC (collective) • Started Wind Power Forecasting & Scheduling (WFS) • Created portfolio of about 600MW under WFS

• 37.8% Market share in REC (collective) • First Indian Co to offer in-house forecasting models • Portfolio of about 1100MW under Wind Forecasting • Launched India’s First Green Energy Marketplace – clickpower.in

2016 • 42% Market share in REC – 2,200 MW Portfolio • Largest Wind/Solar Power Forecasting Co in India (7,000 MW portfolio) • Institutional status to CLICKPOWER.IN – progressing well

FY

3

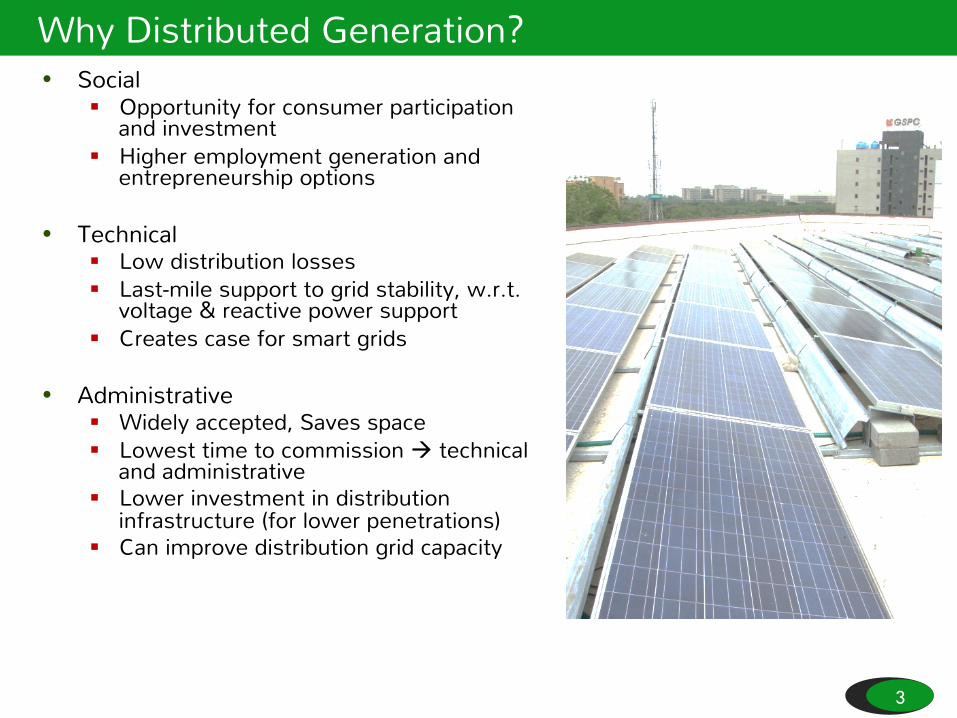

Why Distributed Generation? • Social

§ Opportunity for consumer participation and investment

§ Higher employment generation and entrepreneurship options

• Technical § Low distribution losses § Last-mile support to grid stability, w.r.t.

voltage & reactive power support § Creates case for smart grids

• Administrative § Widely accepted, Saves space § Lowest time to commission à technical

and administrative § Lower investment in distribution

infrastructure (for lower penetrations) § Can improve distribution grid capacity

4

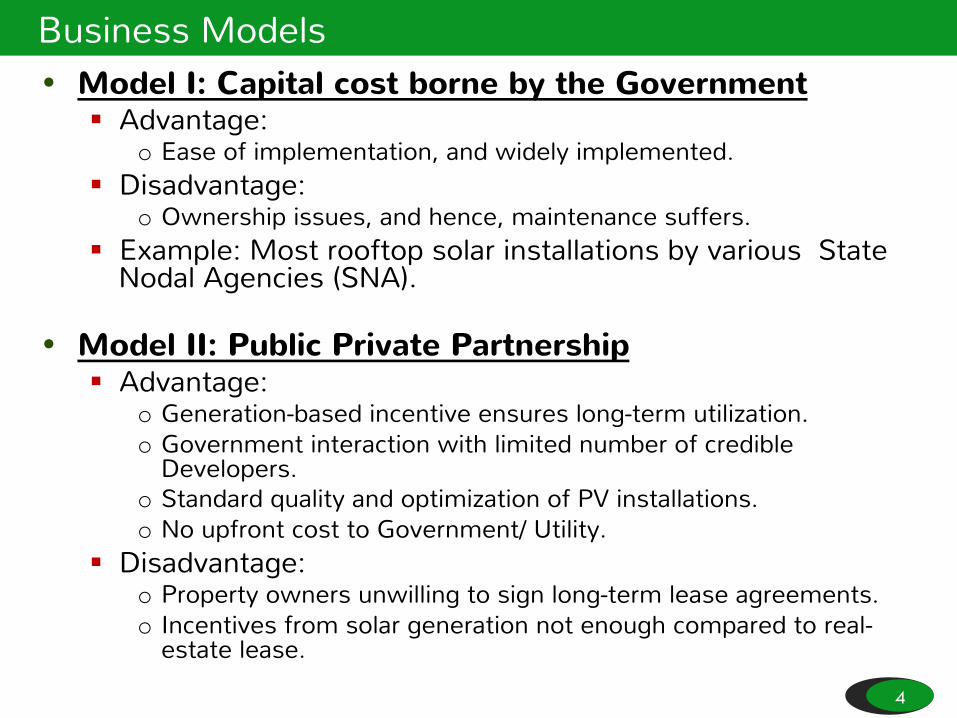

Business Models • Model I: Capital cost borne by the Government

§ Advantage: o Ease of implementation, and widely implemented.

§ Disadvantage: o Ownership issues, and hence, maintenance suffers.

§ Example: Most rooftop solar installations by various State Nodal Agencies (SNA).

• Model II: Public Private Partnership § Advantage:

o Generation-based incentive ensures long-term utilization. o Government interaction with limited number of credible

Developers. o Standard quality and optimization of PV installations. o No upfront cost to Government/ Utility.

§ Disadvantage: o Property owners unwilling to sign long-term lease agreements. o Incentives from solar generation not enough compared to real-

estate lease.

5

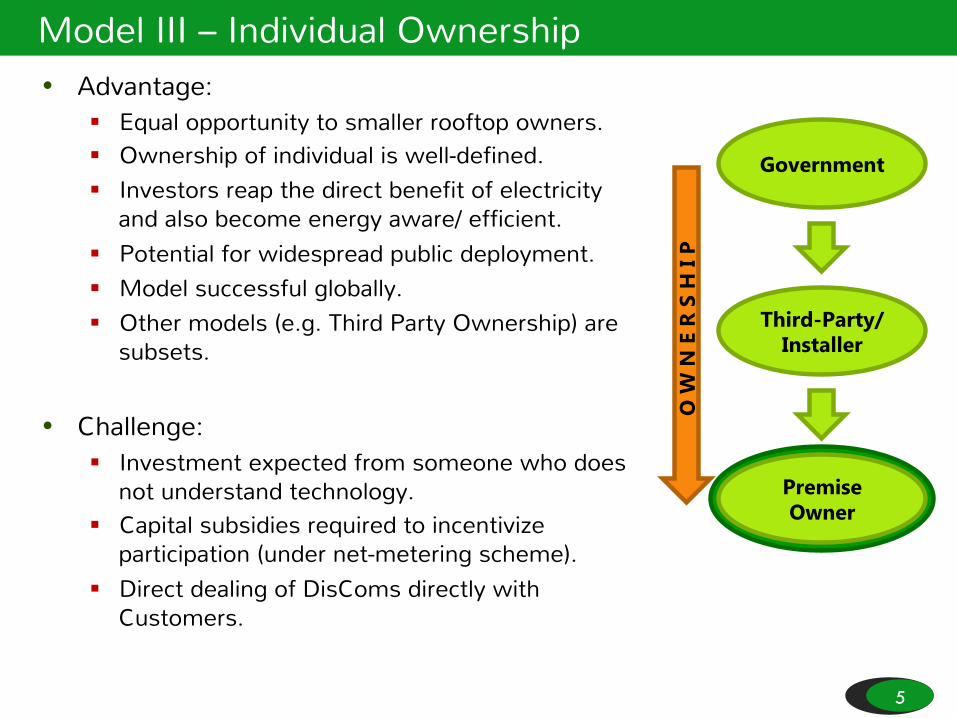

Model III – Individual Ownership • Advantage:

§ Equal opportunity to smaller rooftop owners. § Ownership of individual is well-defined. § Investors reap the direct benefit of electricity

and also become energy aware/ efficient. § Potential for widespread public deployment. § Model successful globally. § Other models (e.g. Third Party Ownership) are

subsets.

• Challenge: § Investment expected from someone who does

not understand technology. § Capital subsidies required to incentivize

participation (under net-metering scheme). § Direct dealing of DisComs directly with

Customers.

Government

Third-Party/ Installer

Premise Owner

O W

N E

R S

H I

P

6

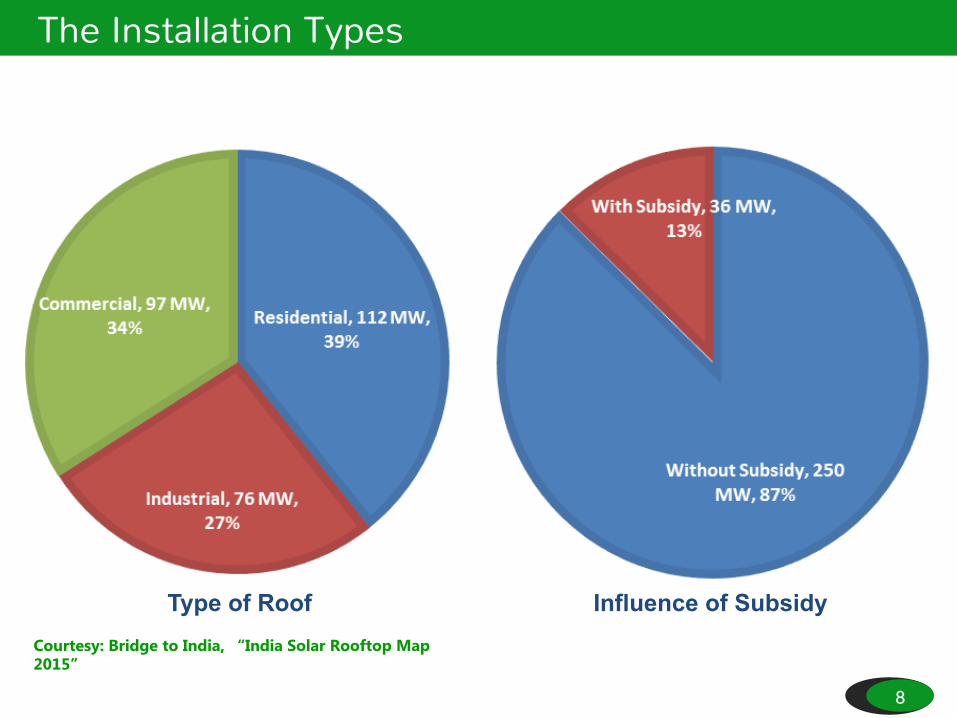

The Present Status (as on Nov 2014) ROOFTOP INSTALLATIONS IN INDIA (NOV. 2014)

6 Courtesy: Bridge to India, “India Solar Rooftop Map 2015”

Net Installed Capacity: 285 MW

Residential

Industrial

Commercial

7

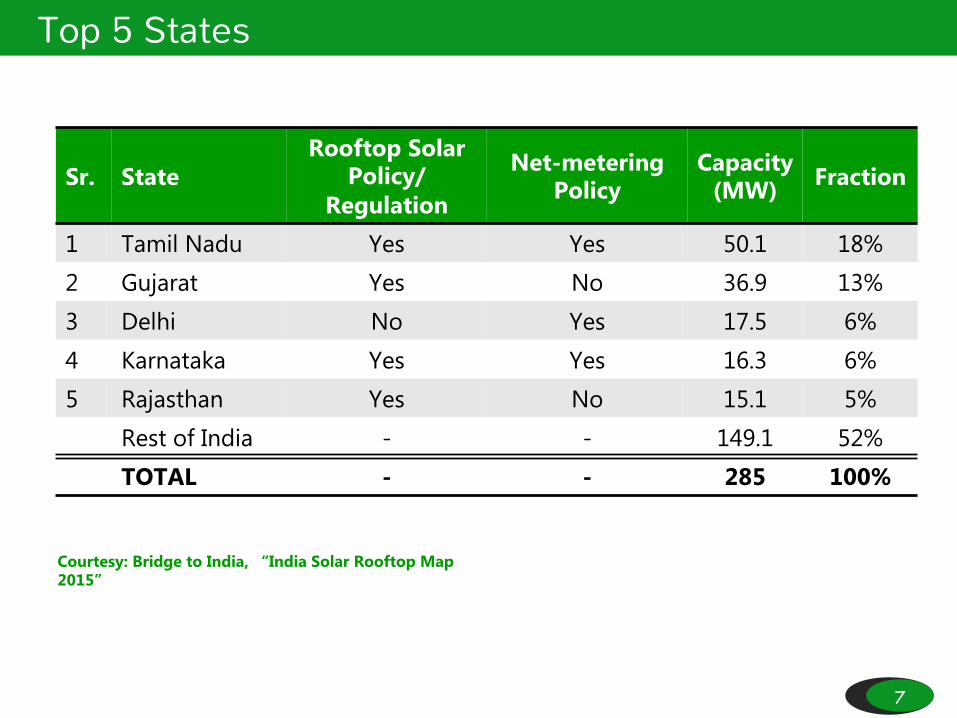

Top 5 States

Sr. State Rooftop Solar

Policy/ Regulation

Net-metering Policy

Capacity (MW) Fraction

1 Tamil Nadu Yes Yes 50.1 18%

2 Gujarat Yes No 36.9 13%

3 Delhi No Yes 17.5 6%

4 Karnataka Yes Yes 16.3 6%

5 Rajasthan Yes No 15.1 5%

Rest of India - - 149.1 52%

TOTAL - - 285 100%

Courtesy: Bridge to India, “India Solar Rooftop Map 2015”

8

The Installation Types

Type of Roof Influence of Subsidy Courtesy: Bridge to India, “India Solar Rooftop Map 2015”

9

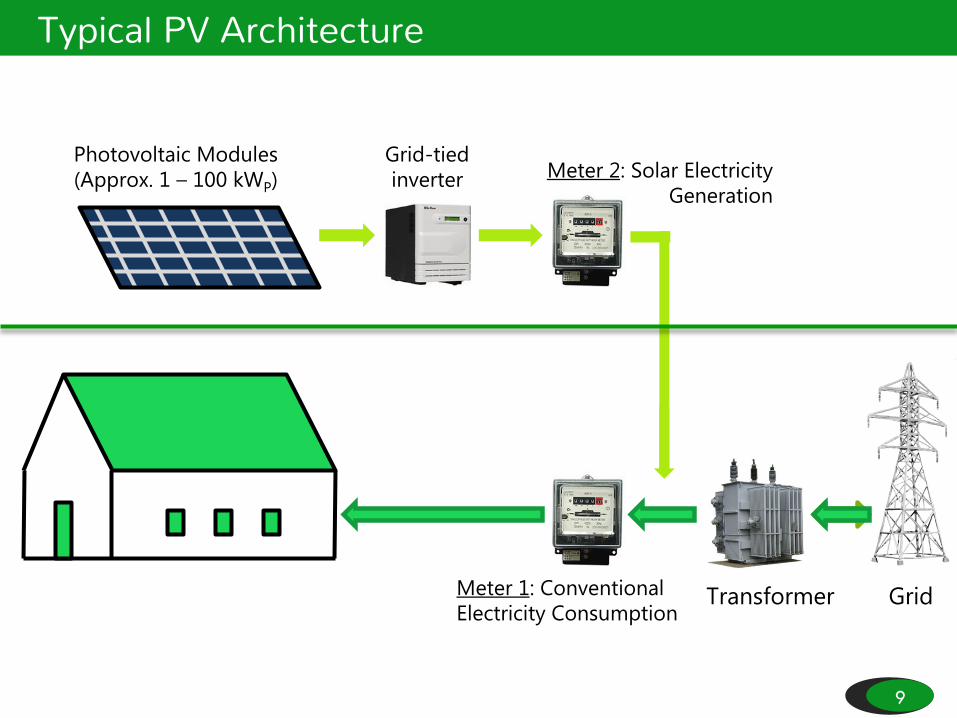

Typical PV Architecture

Photovoltaic Modules (Approx. 1 – 100 kWP)

Grid-tied inverter Meter 2: Solar Electricity

Generation

Meter 1: Conventional Electricity Consumption

Transformer Grid

10

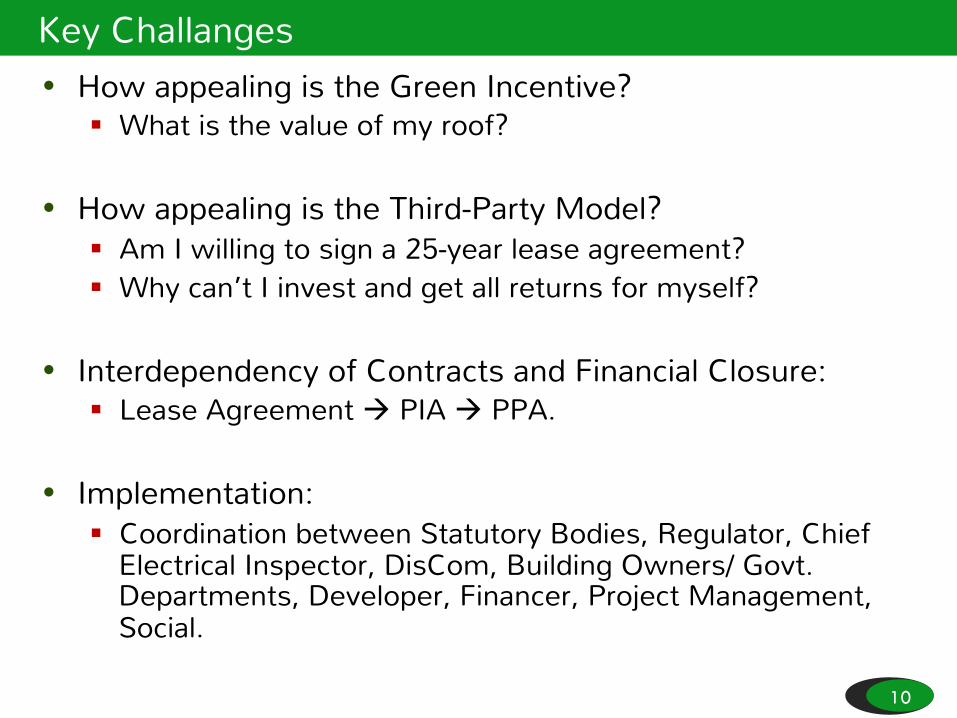

Key Challanges • How appealing is the Green Incentive?

§ What is the value of my roof?

• How appealing is the Third-Party Model? § Am I willing to sign a 25-year lease agreement? § Why can’t I invest and get all returns for myself?

• Interdependency of Contracts and Financial Closure: § Lease Agreement à PIA à PPA.

• Implementation: § Coordination between Statutory Bodies, Regulator, Chief

Electrical Inspector, DisCom, Building Owners/ Govt. Departments, Developer, Financer, Project Management, Social.

11

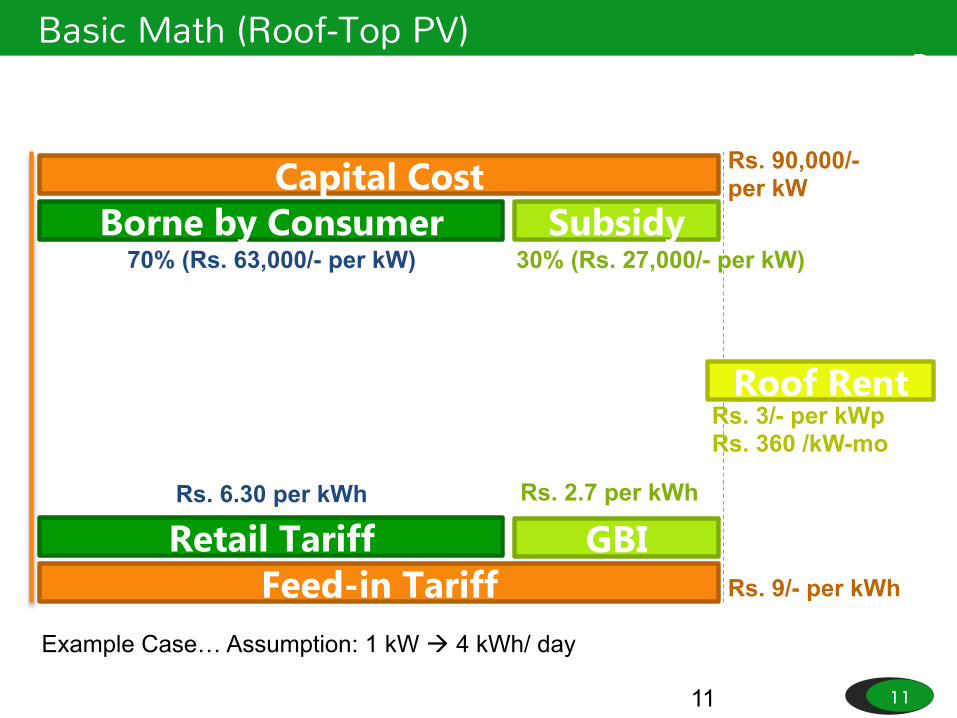

Basic Math (Roof-Top PV) BUILDING BLOCKS OF A BUSINESS MODEL

11

Capital Cost

Feed-in Tariff

Rs. 90,000/- per kW

Subsidy

Rs. 9/- per kWh

Borne by Consumer

Example Case… Assumption: 1 kW à 4 kWh/ day

70% (Rs. 63,000/- per kW) 30% (Rs. 27,000/- per kW)

Retail Tariff Rs. 6.30 per kWh

Roof Rent Rs. 3/- per kWp Rs. 360 /kW-mo

GBI Rs. 2.7 per kWh

12

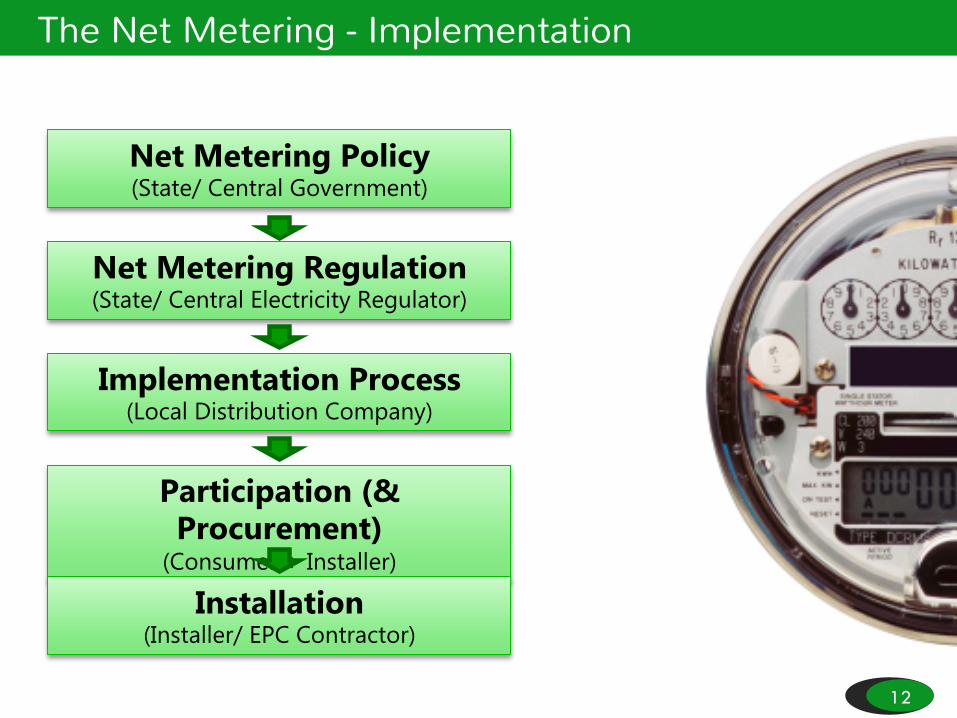

The Net Metering - Implementation

Net Metering Policy (State/ Central Government)

Net Metering Regulation (State/ Central Electricity Regulator)

Implementation Process (Local Distribution Company)

Participation (& Procurement)

(Consumer + Installer)

Installation (Installer/ EPC Contractor)

13

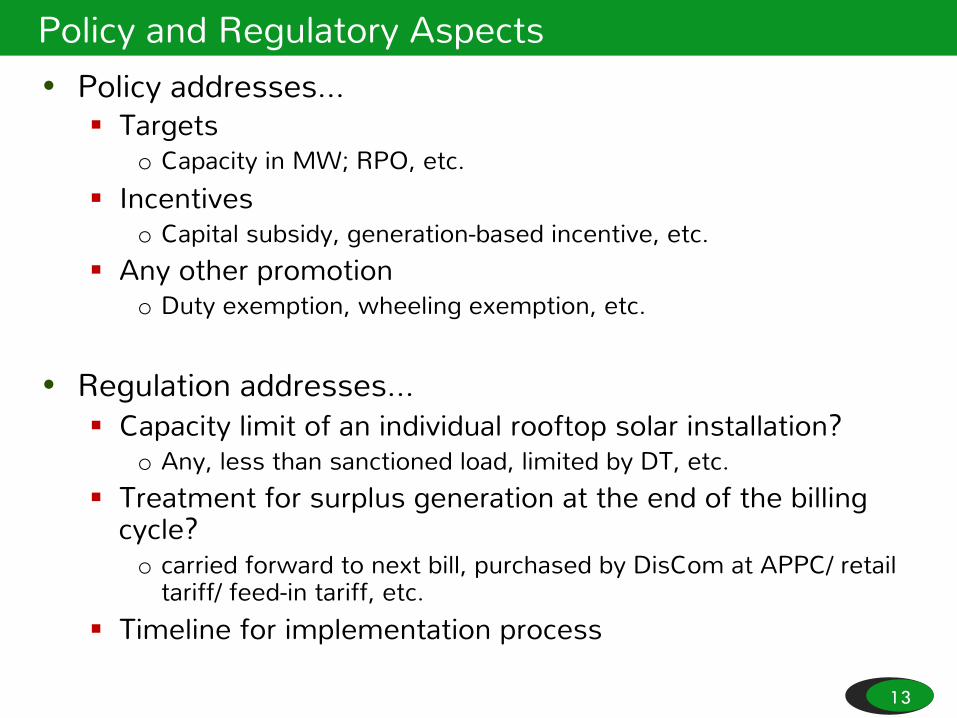

Policy and Regulatory Aspects • Policy addresses…

§ Targets o Capacity in MW; RPO, etc.

§ Incentives o Capital subsidy, generation-based incentive, etc.

§ Any other promotion o Duty exemption, wheeling exemption, etc.

• Regulation addresses… § Capacity limit of an individual rooftop solar installation?

o Any, less than sanctioned load, limited by DT, etc. § Treatment for surplus generation at the end of the billing

cycle? o carried forward to next bill, purchased by DisCom at APPC/ retail

tariff/ feed-in tariff, etc. § Timeline for implementation process

14

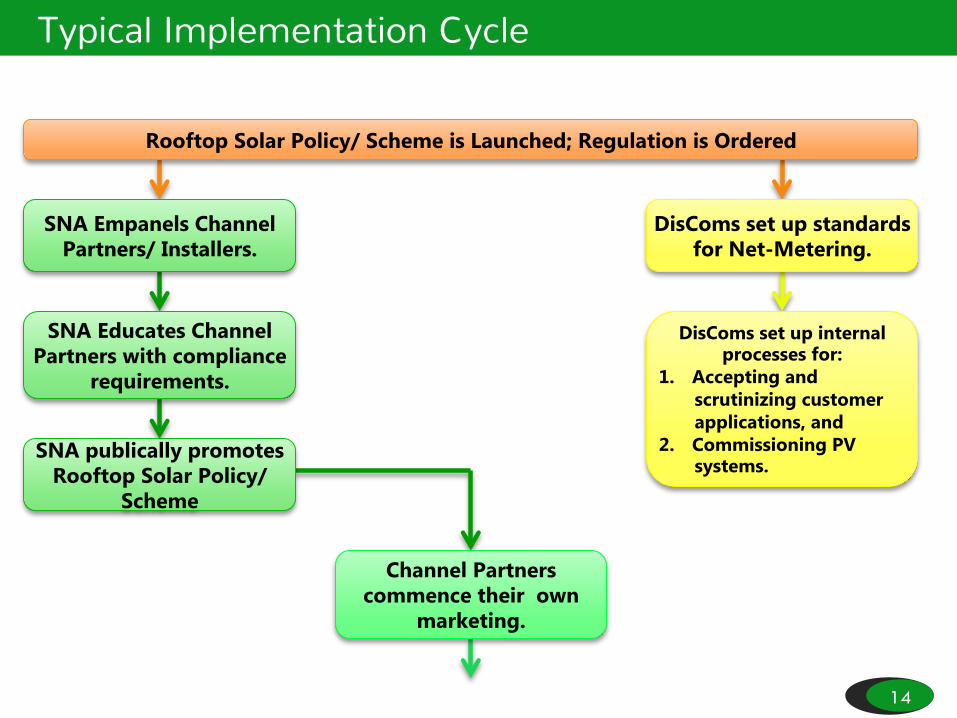

Typical Implementation Cycle

SNA Empanels Channel Partners/ Installers.

DisComs set up standards for Net-Metering.

SNA Educates Channel Partners with compliance

requirements.

SNA publically promotes Rooftop Solar Policy/

Scheme

DisComs set up internal processes for:

1. Accepting and scrutinizing customer applications, and

2. Commissioning PV systems.

Channel Partners commence their own

marketing.

Rooftop Solar Policy/ Scheme is Launched; Regulation is Ordered

15

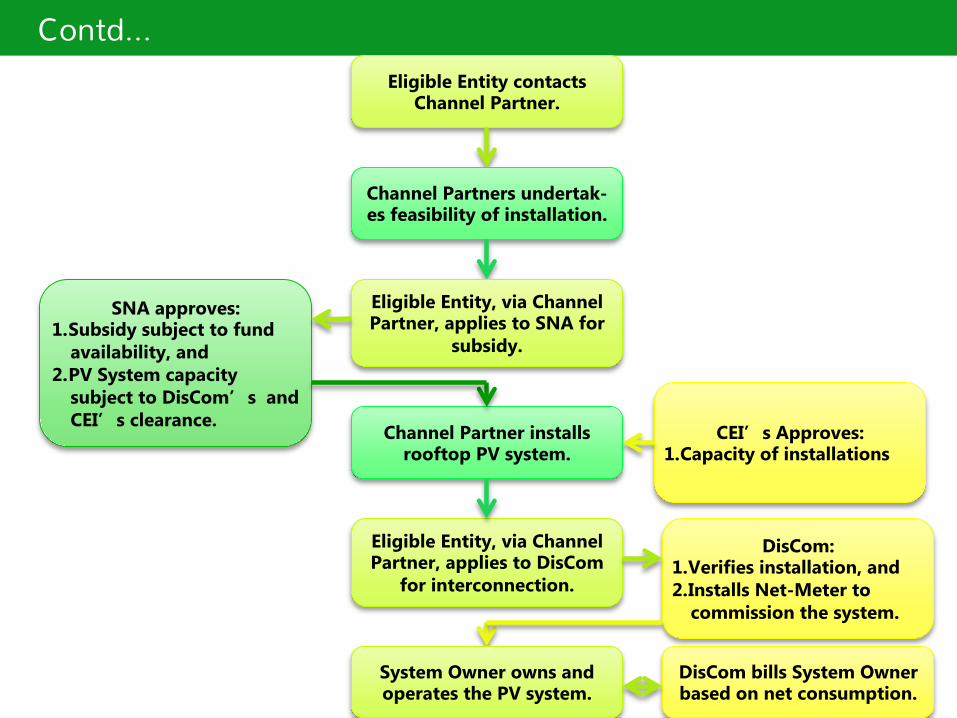

Contd… Eligible Entity contacts

Channel Partner.

Channel Partners undertak-es feasibility of installation.

Eligible Entity, via Channel Partner, applies to SNA for

subsidy.

SNA approves: 1. Subsidy subject to fund

availability, and 2. PV System capacity

subject to DisCom’s and CEI’s clearance.

DisCom: 1. Verifies installation, and 2. Installs Net-Meter to

commission the system.

Channel Partner installs rooftop PV system.

Eligible Entity, via Channel Partner, applies to DisCom

for interconnection.

DisCom bills System Owner based on net consumption.

System Owner owns and operates the PV system.

CEI’s Approves: 1. Capacity of installations

16

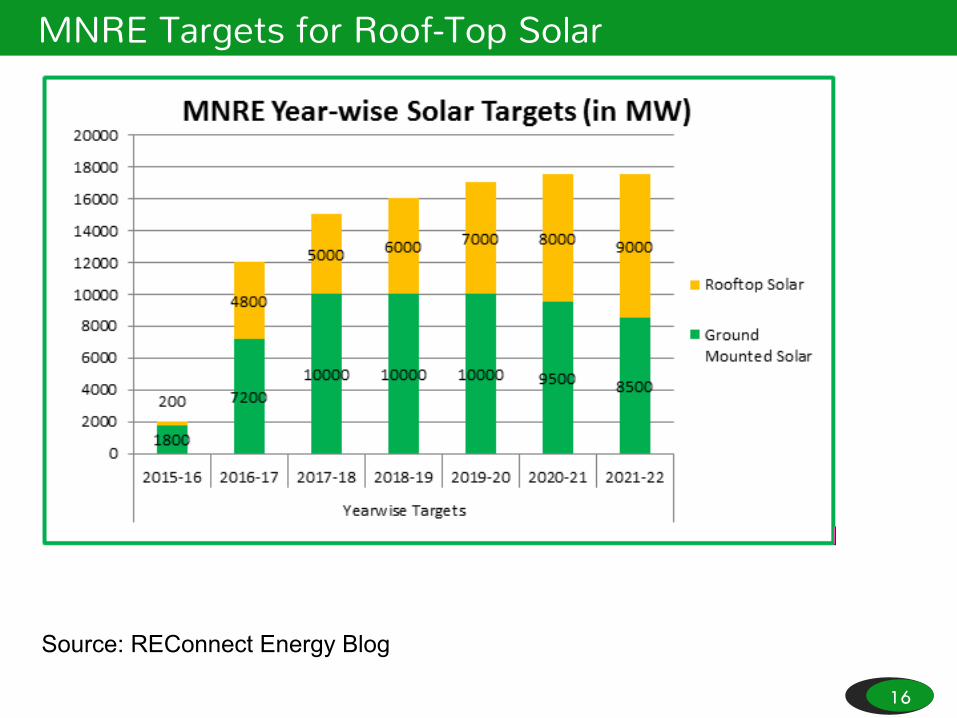

MNRE Targets for Roof-Top Solar

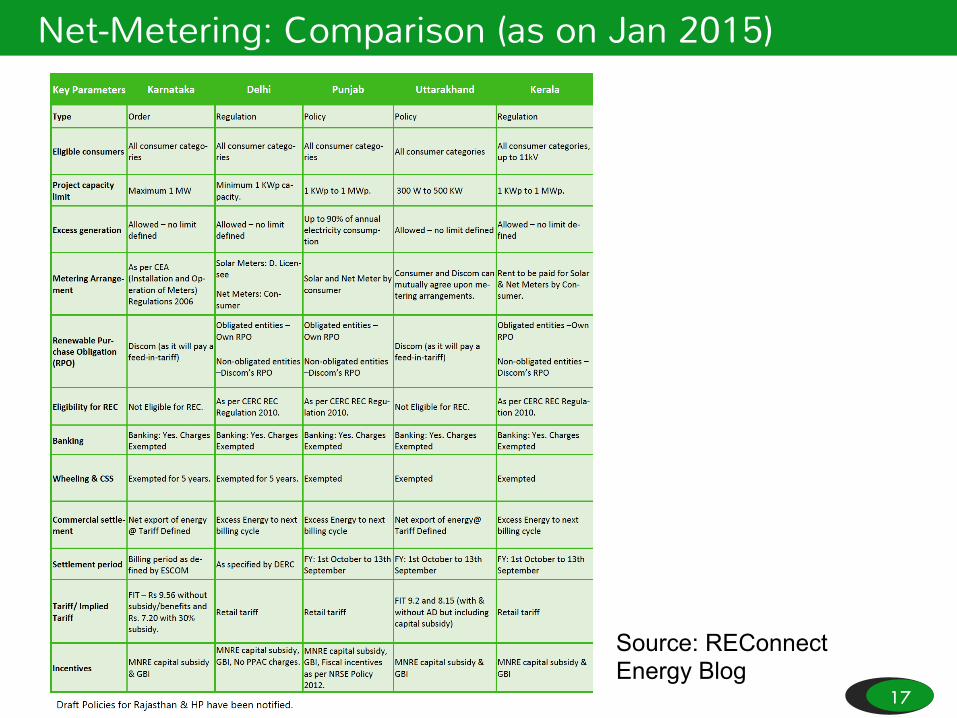

Source: REConnect Energy Blog

17

Net-Metering: Comparison (as on Jan 2015)

Source: REConnect Energy Blog

18

Conclusion • Rooftop PV is simple and well-established globally.

• The objective and scale of any net-metering programme have to be very clear upfront.

• The Electricity Act provides ample provision to undertake a net-metering programme.

• Well-defined implementation is key to success of a net-metering programme.

• 40 GW is GoI & MNRE’s target for Roof-Top Solar by 2022.

• Need – Innovative market models and marketplaces.