Embed Size (px)

Citation preview

DISTRICT COUNCIL OF ELLISTON

Audit Committee

Notice is hereby given that a meeting of the District Council of Elliston‟s Audit Committee will be held on Tuesday 3rd August 2010 at the DC Elliston Council Chambers at 12.30pm.

Kuntal Goswami Corporate Service Manager District Council of Elliston

AGENDA 1.0 PRESENT. 2.0 APOLOGIES. 3.0 WELCOME.

4.0 CONFIRMATION OF PREVIOUS MINUTES.

5.0 RESIGNATION OF MRS DIANA DAVIS–INDEPENDENT MEMBER OF THE AUDIT COMMITTEE. 6.0 SECTION – 90(3) CONFIDENTIAL ITEM- APPOINTMENT OF THE COUNCIL’S AUDITOR FOR PERIOD OF 1st

JULY 2010- 30th JUNE 2015.

7.0 PROGRESS REPORT ON DRAFT INTERNAL CONTROL POLICY.

8.0 DISCUSSION ON PARAMETERS AND ASSUMPTION OF LONG TERM FINANCIAL PLAN (LTFP).

9.0 DISCUSSION DRAFT RISK MANAGEMENT POLICY.

10.0 INFORMATION ONLY

2009/10 BUDGET REVIEW (4th QUARTER).

2010/11 BROUGHT FORWARD GRANT.

IMPLICATION OF OH&W COST. GENERAL BUSINESS

11.0 NEXT MEETING. 12.0 CLOSURE.

DISTRICT COUNCIL OF ELLISTON

MINUTES

of the Audit Committee Meeting held

Wednesday 3 March 2010 at Elliston Council Chambers

PRESENT: Cr K Burrows (Deputy Chairman of DC Elliston/Chairman of Audit Committee), Cr P Hitchcock (Councillor & Audit Committee Member Of DC Elliston), Mr Allen Bolaffi (Independent Member / Chartered Accountant- UHY Haines Norton), Kuntal Goswami (CSM /Minute Clerk- No Voting Right) and Mr Wayne Scholz (Works Co-Coordinators of the DC of Elliston -No Voting Right). APOLOGY: Mrs Diane Davis, Corporate Service Manager DC Streaky Bay - Independent Member. WELCOME: The Chairman presided over the meeting and declared the Audit Committee Meeting open at 9.30 am and welcomed Councillor, Committee member and staff to the meeting. CONFIRMATION OF MINUTES:

8.0910 That the minutes of the Audit Committee Meeting of Council held on 15th December

2009 as circulate and tabled in the minute book be taken as read and confirmed. Cr Hitchcock / Mr Bolaffi

CARRIED RESOLUTIONS OF THE MEETING: Progress Report on Implementation of May 2009 Interim (External) Audit Report

9.0910 That the Committee receives the report and requests the Councillor’s Auditor to provide a comment on the report in the next meeting and be invited to participate by telephone if available.

Cr Hitchcock / Mr Bolaffi CARRIED

Discussion on Parameters and Assumption of Long Term Financial Plan (LTFP) and Consideration of External Assistance

10.0910 That the Committee recommends the Council:

To prepare and adopt LTFP as priority one project in the next financial year

Allocate about $ 5000 for this project in the next Financial year (The Council may require external assistance to prepare this document.)

Seek Grant / Financial Assistance from LGA to prepare this document and

Mr Allen Bolaffi to provide copies of LTFP of other Councils to assist CSM and offers to provide assistance if required.

Cr Hitchcock / Mr Bolaffi CARRIED

Review of 2nd Draft Internal Control Policy and Consideration of Mr Allen Bolaffi ’S Comments

11.0910 That the Committee, having discussed all the points, clarified all the points as follows:

1. The Committee directs CSM to concentrate on financial issues of the Internal Control Policy in the 1st phase and advises the Council to adopt it once the financial issues of the draft policy are resolved. Non-financial issues shall be addressed in the 2nd phase.

2. Point 2 shall be clarified by Mr Allen Bolaffi later on. 3. The Committee advises the Council to seek legal advice on the role and

authority of the Chairman of Council being involved in administrative operations of Council.

4. The Committee directs CSM to develop a system in consultation with other

senior staff. 5. The Committee advises Council to select EFT as preferred mode of payment

to all Creditors and for efficiencies to be developed around credit payments. 6. The Committee advises the Council to seek legal advice. 7. The Committee directs CSM to define “the action of transfer of fund between

the bank accounts” and seek more explanation on use & protection of bank passwords. It was felt that appropriate controls are required around the transfer of funds should be implemented in the policy document.

8. The Committee advises the Council to formalise a Debt Recovery Policy. 9. Mr Allen Bolaffi will review the “Private Works and Plant Hire Policy”.

10. The Committee is not so concerned with issue mentioned in the point since

the Committee feels the major revenue transaction has checks and balances.

Cr Hitchcock / Mr Bolaffi CARRIED

Discussion on how to Conduct Internal Audit Quarterly and how to Prepare Progress Report (Consideration of what Internal Controls need to be Reviewed)

12.0910 That the Committee recommends the Council to allocate about $5000 for Internal Audit Project in the next Financial Year Budget. The Internal Audit process will concentrate on payroll / procurement / other internal control issues. Mr Bolaffi is able to assist with the determination of the scope of works that would be appropriate for the Council.

Cr Hitchcock / Mr Bolaffi CARRIED

Update on Draft Risk Register Template Preparation

13.0910 That the Committee adopts function based Risk Register Template and recommends the Council to allocate a budget in the next financial year so that a workshop can be organised with Councillors and Staff to develop a risk register for Council.

Cr Hitchcock / Mr Bolaffi CARRIED

Budget Review Report and Explanation of Changes to the 2010 Budget 14.0910 That the Committee received the Budget Review Report and endorsed the format.

The Committee congratulated management over the new format which was very easy to read and understand.

Cr Hitchcock / Mr Bolaffi CARRIED

Discussion on 2010/11 Council Asset Revaluation and Asset Management Plan Development

15.0910 That the Committee advise the Council that, a proper Asset Management Plan is important for good financial decision making in regard to Council’s Yearly Capital Budget and general management operations, it needs to be developed in the next Financial year .The Committee also advised the Council to undertake a Valuation of all Council assets in the next financial year so as to have an accurate and proper understanding of assets and consequent depreciation charges.

Cr Hitchcock / Mr Bolaffi CARRIED

Works Co-ordinator’s explanation to the Audit Committee on a) Why road construction cost is less than other Councils? b) Method of finalising Council’s Road Re-sheeting Schedule “ The main reasons are as follows:

DC Elliston strictly follow the Australian Road Design standards. The standards recommend minimising the width of the roads to reduce “wastage of materials” and excessive maintenance costs. (for example a wider road requires additional runs with the grader during maintenance using additional fuel, equipment, time, blades and labour) Minimising the width also reduces traffic speed thus reducing the impact of heavy vehicles.

DC Elliston uses contractors to crush and cart rubble onto the roads. As a result Council does not require too maintain a bulldozer to this job. (one of the most costly items of equipment a Council can own). It also improved operating performance as one employee of Council is no longer required to purely sit in a loader all day waiting to load a truck and his time is more effectively utilised.

The staff operate on a 10 hr day shift and have their RDO’s on every second Friday and Monday giving them a 4 day weekend every fortnight, this is a comfortable arrangement for the staff and during this period the grader can be utilised for additional patrol grading using Contract staff or for carrying out maintenance on the machinery (reducing downtime during working time).

The contracting out of the mechanical repairs and maintenance has also been an important cost factor.

Council has less works staff that reduces the fixed cost.

The Councils roads are categorised from 1 to 4 depending on function and volumes, the higher priority roads have a higher build standard than the lower category roads (the material quality remains the same) and this has allowed more higher priority roads to be better maintained throughout the district.”

The Council also strictly follow “ Road Infrastructure Policy ” before finalising Council’s annual Road Resheeting program”

Discussion on “Road to Recovery (R2R) Depreciation- Circular 47.7” 16.0910 That the Committee noted the circular and it will be discussed in the next meeting.

Cr Hitchcock / Mr Bolaffi CARRIED

Discussion on “Review of Audit Committee Operation” Survey Conducted By LGA

17.0910 That the Committee noted the Survey Questionnaire. Cr Hitchcock / Mr Bolaffi

CARRIED Financial Help for Council “Local Government Disaster Fund – Circular 5.2”

18.0910 That the Committee requests that CSM to apply for a grant from the Local Government Disaster Fund to assist with Storm damage repairs.

Cr Hitchcock / Mr Bolaffi CARRIED

Approval of 2009/2010 RlCIP Projects The Committee noted the information. 2008/09 Audited Annual Report The Committee noted the information. Audit Committee Work Plan The Committee noted the Audit Committee Work Plan. Corporate Services Manager’s Report

19.0910 That the Corporate Services Manager Report as printed in the Agenda circulated and tabled be accepted.

Cr Hitchcock / Mr Bolaffi CARRIED

QUESTIONS WITHOUT NOTICE: Cr Burrows - wants to discuss the implication of OHS&W cost in the next Audit Committee Meeting. K Goswami, CSM - is to prepare a briefing note for the Committee to discuss. DATE OF NEXT MEETING: The next Audit Committee Meeting will be held on 2nd June 2010 at 12.30 pm at the Elliston Council Chambers.

CLOSE: The meeting closed at 11.45am after the Chairman thanked all for attending.

The District Council of Elliston

Report to Audit Committee by

Corporate Services Manager

3rd August 2010

Confirmation of Minutes Recommendation: That the minutes of the Audit Committee Meeting held on 3rd March 2010 as circulated and tabled in the minute book be taken as read & confirmed. Resignation of Mrs Diana Davis–Independent Member of the Audit Committee Mrs Diana Davis has informed the Committee that she will not be able to be on the DC Elliston‟s Audit Committee. Recently she has joined the District Council of Streaky Bay. Her letter of resignation is attached. As a result of Mrs Diana Davis resignation, the Committee will have three members instead of four members with one independent member. The CEO of DC Streaky Bay has indicated that he wishes to continue with the present arrangement of nominating each Council‟s CSM for the post of Independent Member in each other‟s Audit Committee. The present arrangement will continue with once DC Streaky Bay‟s CSM position is filled. Recommendation: That the Committee accepts Mrs Diana Davis‟s (one of the Independent Member of the Committee) resignation from the DC Elliston‟s Audit Committee. Section 90 Briefing: - Appointment of the Council’s Auditor for period of 1st July 2010- 30th June 2015 Confidential Motion – Order to Exclude the Public (Section-90(3)) That pursuant to section 90(2) of the Local Government Act 1999 the Audit Committee orders that all person , with exception of Kuntal Goswami – CSM/Minute Clerk, be excluded from attendance at the meeting for agenda item 6.0 relating to “Appointment of The Council‟s Auditor for period of 1st July 2010- 30th June 2015”. The Audit Committee is satisfied that, pursuant to Section 90(3)(d) & 90(3)(k) of the Act, the information to be received, discussed or considered in relation to this agenda item is related to commercial information of a confidential nature (not being a trade secret) the disclosure of which:

i. Could reasonably be expected to prejudice the commercial position of the person who supplied the information, or to confer a commercial advantage on a third party; and

ii. Tenders for the supply of goods, the provision of services or the carrying out of work The Committee is satisfied that the principle that the meeting be conducted in a place open to the public has been outweighed in the circumstances because such disclosure may compromise the Committee‟s ability to finalise the matters. There was no-one from the public present, except those named above, at xx.xx pm. Section 91(7) Order That having considered Agenda Items – Appointment of The Council‟s Auditor for period of 1st July 2010- 30th June 2015 ,under Section 90(2) and (3)(K) of the Local Government Act 1999, the Committee, pursuant to section 91(7) of that Act orders that all discussions, documents and minutes be retained in confidence for a period of xxx years. This order is subject to Section 91(8)(b) of the Act which provides that details of the identity of the successful tenderer must be released once Council has made a selection . In addition, section 91(8)(ba) of the Act requires details of the amount(s) payable by the Council under a contract for the provision of audit services must be released once the contract has been entered into by all concerned parties.

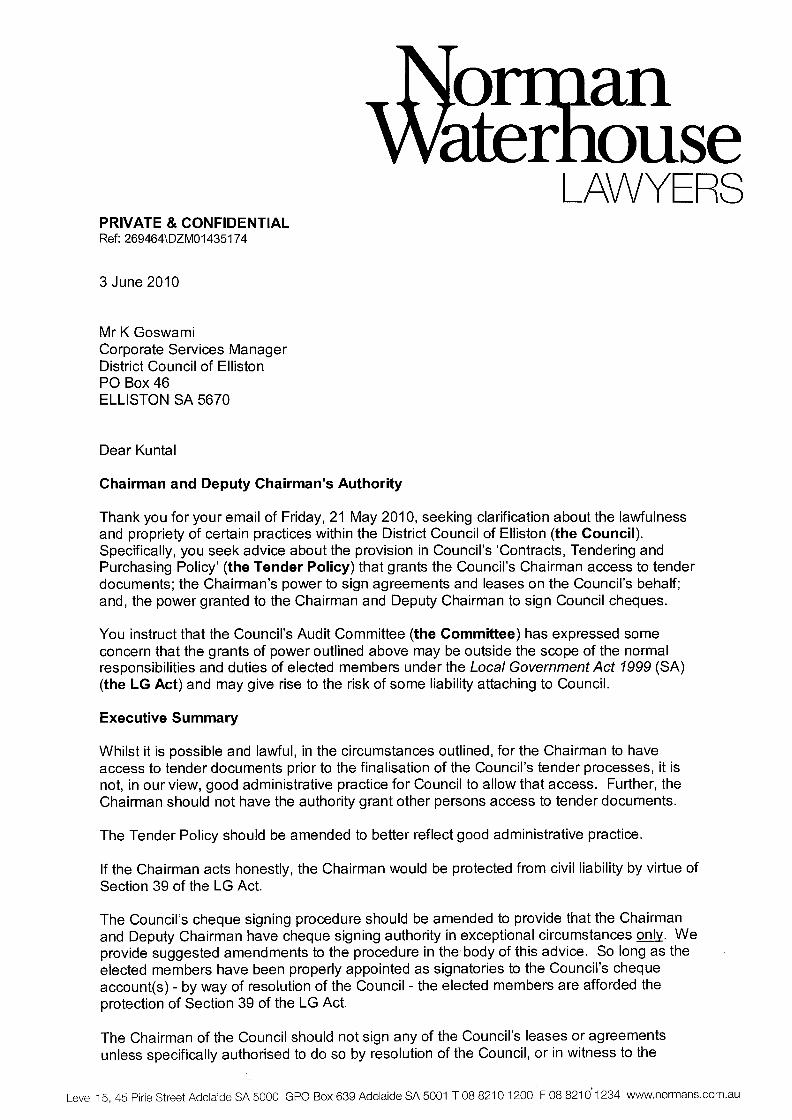

Progress Report on Draft Internal Control Policy In the March 2010 Audit Committee Meeting, it was has recommended that the Council seek legal advice on the “Clarification on Chairman and Deputy Chairman‟s Authority” The brief description of the clarification:- “The role and authority of the Chairman / Deputy Chairman of the Council being involved in administrative operations (such as Cheque Signing authority , custodian of Tender Document, Signing of Agreements and Leases etc) of the Council. The Committee believes that “the Chairman/Deputy Chairman has no authority under Section 58 of the Act [sic] an administrative function. This could lead to issues for the Council and the Chairman/ Deputy Chairman under Section 39 of the Act, in terms of Liability for actions undertaken by the Chairperson.” In brief, the Council‟s legal advisors Norman Water House Lawyers‟ legal advice on this matter as follows:- “In our opinion, the Council should immediately discontinue this present practice. Absent the express authority for the Council to enter into a particular transaction by way of resolution, or the appointment of the Chairman as an agent of the Council for a particular agreement or lease ,the Chairman should not sign agreements or leases on behalf of the Council.” A copy of the letter is attached. Recommendation:- That:

The Committee recommends that the Council immediately discontinue the present practice of providing delegated authority to the Chairman / Deputy Chairman of the Council to sign Cheques, to be the custodian of Tender Documents, or to have any purchasing authority of any limit in accordance with Norman Water House Lawyers‟ legal advice dated 03 June 2010.

The Committee recommends to Council that it amend its draft Internal Control policy and the present Purchasing Policy accordingly.

The Committee believes the Chairman/Deputy Chairman has the authority to sign the Council‟s Agreements and Leases under the Council‟s Common Seal.

The Council should amend its Purchase and Tendering Policy and in corporate same principle in its Draft Internal Control Policy.

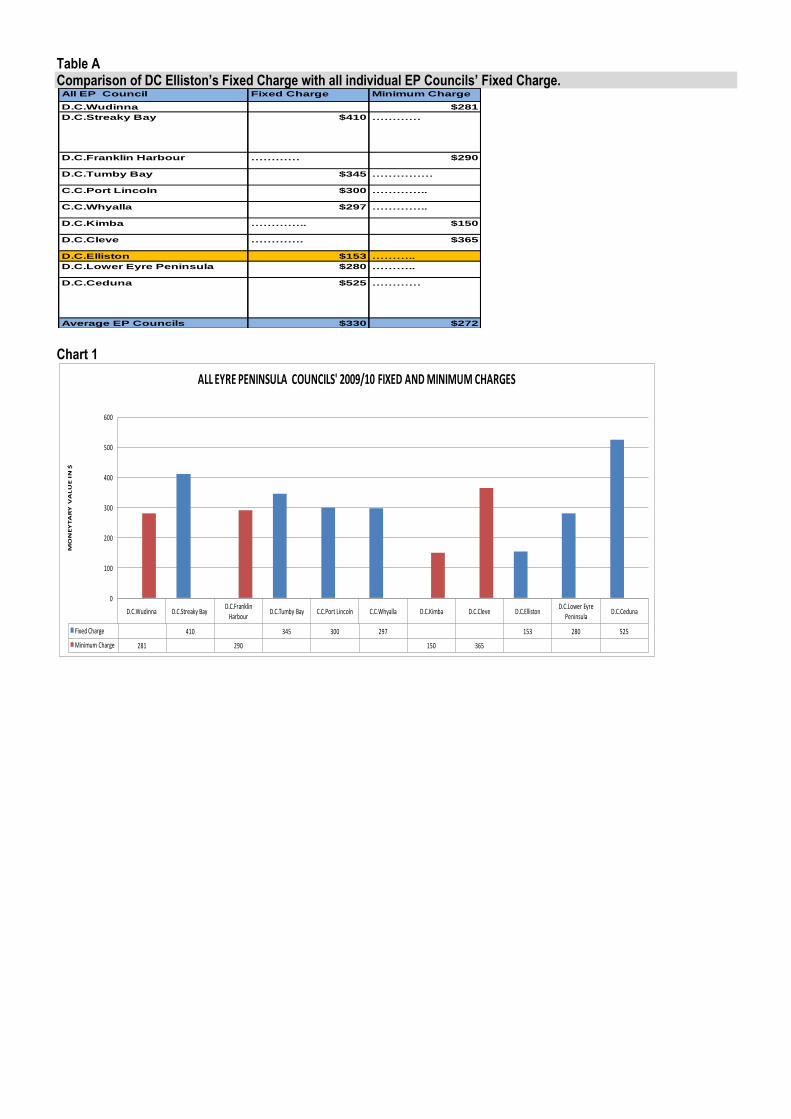

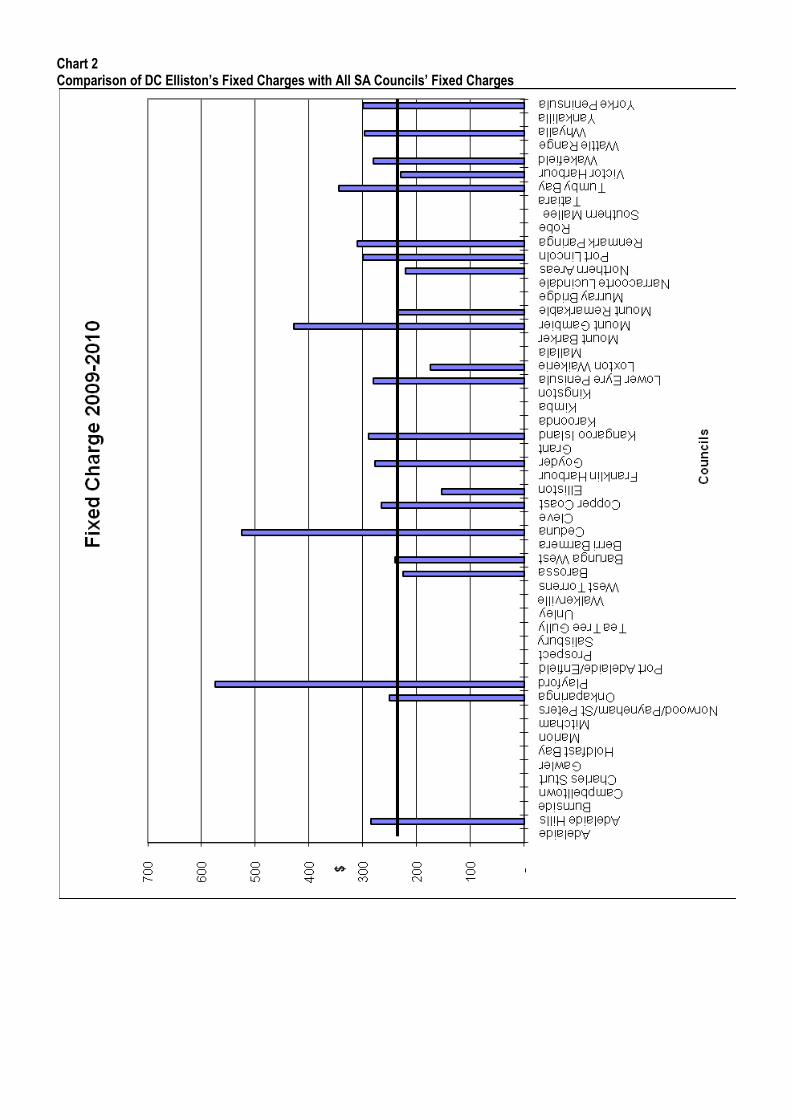

Discussion assumption of Long Term Financial Plan (LTFP) Pursuant to section 122 (1a) of the Local Government Act 1999 the Council must develop and adopt a Long Term Financial Plan (LTFP). LTFP is vital for the Council‟s financial sustainability and upgrading or replacing its aging assets and maintaining its level of service. Without a LTFP Council is at risk of taking on additional services and functions without due consideration of the implication its financial sustainability. As discussed and pointed out during the budget process that the Council‟s fixed charge component of General Rate is the lowest among all EP & SA Councils.

Table A Comparison of DC Elliston’s Fixed Charge with all individual EP Councils’ Fixed Charge.

Chart 1

All EP Council Fixed Charge Minimum Charge

D.C.Wudinna $281

D.C.Streaky Bay $410 …………

D.C.Franklin Harbour ………… $290

D.C.Tumby Bay $345 ……………

C.C.Port Lincoln $300 …………..

C.C.Whyalla $297 …………..

D.C.Kimba ………….. $150

D.C.Cleve …………. $365

D.C.Elliston $153 ………..

D.C.Lower Eyre Peninsula $280 ………..

D.C.Ceduna $525 …………

Average EP Councils $330 $272

D.C.Wudinna D.C.Streaky Bay D.C.Franklin

HarbourD.C.Tumby Bay C.C.Port Lincoln C.C.Whyalla D.C.Kimba D.C.Cleve D.C.Elliston

D.C.Lower Eyre Peninsula

D.C.Ceduna

Fixed Charge 410 345 300 297 153 280 525

Minimum Charge 281 290 150 365

0

100

200

300

400

500

600

MO

NE

YT

AR

Y V

AL

UE

IN

$

ALL EYRE PENINSULA COUNCILS' 2009/10 FIXED AND MINIMUM CHARGES

Chart 2 Comparison of DC Elliston’s Fixed Charges with All SA Councils’ Fixed Charges

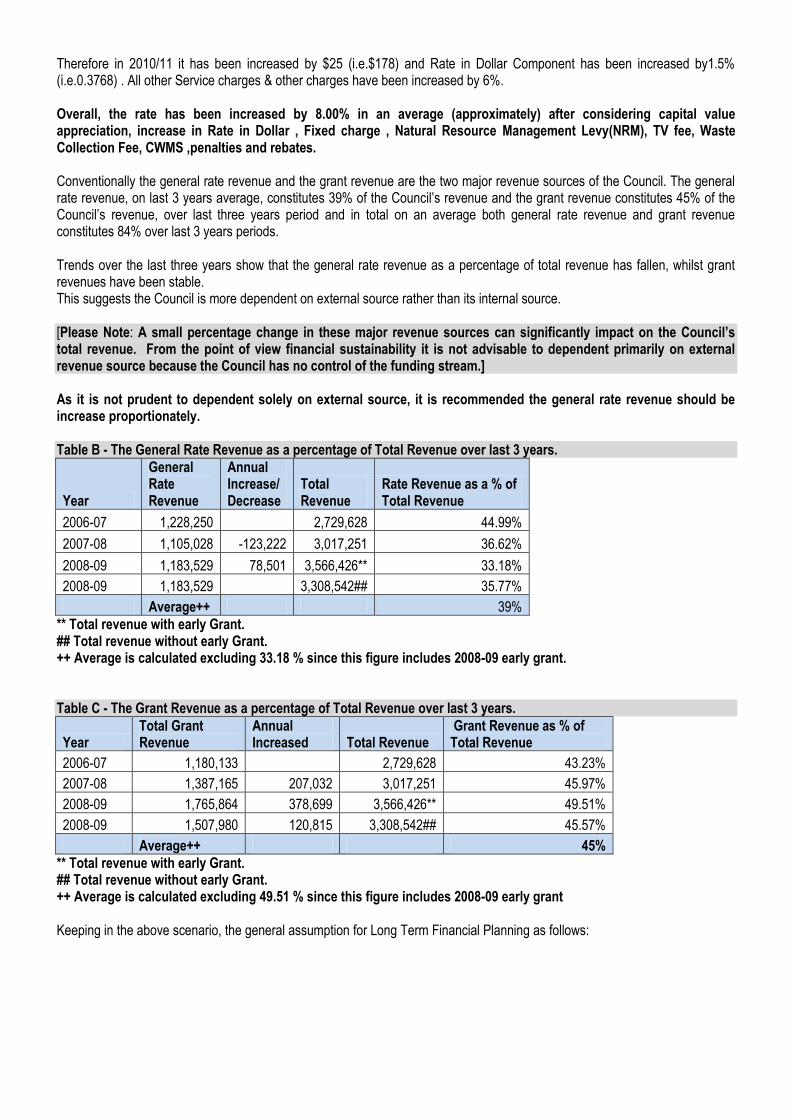

Therefore in 2010/11 it has been increased by $25 (i.e.$178) and Rate in Dollar Component has been increased by1.5% (i.e.0.3768) . All other Service charges & other charges have been increased by 6%. Overall, the rate has been increased by 8.00% in an average (approximately) after considering capital value appreciation, increase in Rate in Dollar , Fixed charge , Natural Resource Management Levy(NRM), TV fee, Waste Collection Fee, CWMS ,penalties and rebates. Conventionally the general rate revenue and the grant revenue are the two major revenue sources of the Council. The general rate revenue, on last 3 years average, constitutes 39% of the Council‟s revenue and the grant revenue constitutes 45% of the Council‟s revenue, over last three years period and in total on an average both general rate revenue and grant revenue constitutes 84% over last 3 years periods. Trends over the last three years show that the general rate revenue as a percentage of total revenue has fallen, whilst grant revenues have been stable. This suggests the Council is more dependent on external source rather than its internal source. [Please Note: A small percentage change in these major revenue sources can significantly impact on the Council’s total revenue. From the point of view financial sustainability it is not advisable to dependent primarily on external revenue source because the Council has no control of the funding stream.] As it is not prudent to dependent solely on external source, it is recommended the general rate revenue should be increase proportionately. Table B - The General Rate Revenue as a percentage of Total Revenue over last 3 years.

Year

General Rate Revenue

Annual Increase/ Decrease

Total Revenue

Rate Revenue as a % of Total Revenue

2006-07 1,228,250 2,729,628 44.99%

2007-08 1,105,028 -123,222 3,017,251 36.62%

2008-09 1,183,529 78,501 3,566,426** 33.18%

2008-09 1,183,529 3,308,542## 35.77%

Average++ 39% ** Total revenue with early Grant. ## Total revenue without early Grant. ++ Average is calculated excluding 33.18 % since this figure includes 2008-09 early grant. Table C - The Grant Revenue as a percentage of Total Revenue over last 3 years.

Year Total Grant Revenue

Annual Increased Total Revenue

Grant Revenue as % of Total Revenue

2006-07 1,180,133 2,729,628 43.23%

2007-08 1,387,165 207,032 3,017,251 45.97%

2008-09 1,765,864 378,699 3,566,426** 49.51%

2008-09 1,507,980 120,815 3,308,542## 45.57%

Average++ 45% ** Total revenue with early Grant. ## Total revenue without early Grant. ++ Average is calculated excluding 49.51 % since this figure includes 2008-09 early grant Keeping in the above scenario, the general assumption for Long Term Financial Planning as follows:

Table D

Assumed Local Government Price Index will be 3.5 % in an average.

Assumed Capital Value appreciation is about 4% in an average. Total Rate Increase :- 7% (including each individual year‟s actual LGPI increase, Actual Capital Value Increase , increase in service charges like TV fee , CWMS fee, Waste Collection Fee , NRM Levy , rebate etc)

Other Revenue will increase by 5.5% (2% over and above assumed LGPI 3.5%)

Operating Expenses increased by 5 %

Depreciation expense increased by 2.5% The financial model shows (table-E) from 2011/12 onwards, the amount of operating deficit is reducing and by 2014/15 onwards the Council will have operating surplus (keeping in mind the given assumptions of this model remain constant). The subsequent table (table-F) also shows that the council‟s liquidity position is also stabile throughout the period. The debt component is also incorporated in this financial modelling (table-G) as directed the minutes number 112.2010, dated 10th May 2010 Special Budget Meeting. The Resolution as follows: “Operating Income Table 1

112.2010 That the Council accepts the Operating Income, proposed for the 2010/2011 financial year as tabled in Table 1 of the 1st Draft Budget Report, and directs for its inclusion into the 2nd Draft Budget Report with the following amendments:

That the anticipated general rate revenue is to be primarily increased via the fixed charge.

That the administration is to examine the likely Capital Expenditure requirement for the Council over the next 4 years and to provide subsequent revenue increase options to meet this need in the 2nd Draft Budget. This examination should include the option for loan to finance the major capital projects.

The administration is to develop the specific asset categories capital replacement reserves (such as infrastructure, plant and equipment, utility, building and office equipment) for further consideration in the 2nd Budget Meeting.

Cr Burrows / Cr Hitchcock CARRIED”

Table E

BUDGETED INCOME STATEMENT

Revenue Budgeted 2010/11 Budgeted 2011/12 Budgeted 2012/13 Budgeted 2013/14 Budgeted 2014/15

Rate 1744597 1866719 1997389 2137206 2286811

Other Revenue 1808279 1907734 2012660 2123356 2240141

Total Revenue 3552876 3774453 4010049 4260562 4526951

Expenditure

Other Operating Expense 2537146 2664003 2797203 2937064 2995805

Depreciation 1322377 1348825 1375801 1403317 1431383

Total Operating Expense 3859523 4012828 4173004 4340381 4427188

OPERATING SURPLUS/DEFICIT -306647 -238375 -162956 -79818 99763

LOSS DISPOSAL -17000 -17000 -17000 -17000 -17000

NET OPERATING SURPLUS /(DEFICIT) -323647 -255375 -179956 -96818 82763

Table F

Table G

FORCASTED YEARLY NET LOAN BALANCE

YEAR LOAN TAKEN LOAN REPAID NET LOAN BALANCE

2010/11 320,000 -23710 296,290

2011/12 396,290 -33252 363,038

2012/13 438,038 -43400 394,638

2013/14 494,638 -51000 443,638

2014/15 543,638 -55400 488,238

AVERAGE 438521 -41352 397168 Table H

Forecasted Capital Expenditure for coming 5 years Amount

2010/11 Budget 1,634,396

Budgeted 2011/12 1,500,000

Budgeted 2012/13 1,400,000

Budgeted 2013/14 1,400,000

Budgeted 2014/15 1,400,000

Total 7,334,396

Average 1466879 All these above stated assumptions and calculations of LTFP are draft only. Recommendation: I seeks the Audits Committee‟s feedback on the initial assumptions and calculations of LTFP. Discussion 1st Draft Risk Management Policy In order to operate effectively and achieve its corporate and strategic plans in accordance with sound governance principles, Council must be aware of the key risks they face and have strategies in place to manage those risks. Within the Local Government context, risk management requires more than just ensuring footpaths and playgrounds are safe. Risk Management involves all facets and activities of the Council.

BUDGETED CASH FLOW STATEMENT 2010/11 Budget Budgeted 2011/12 Budgeted 2012/13 Budgeted 2013/14 Budgeted 2014/15

CASH FROM OPERATION

RECEIPTS 3552876 3774453 4010049 4260562 4526951

PAYMENT -2537146 -2664003 -2797203 -2937064 -2995805

NET CASH PROVIDED BY OPERATING ACTIVITIES 1015730 1110450 1212845 1323499 1531146

CASH FLOWS FROM INVESTING ACTIVITIES

RECEIPTS (specific Reserves) 688211 688211 688211 688211 688211

PAYMENTS -1634396 -1500000 -1400000 -1400000 -1400000

NET CASH PROVIDED BY INVESTING ACTIVITIES -946185 -811789 -711789 -711789 -711789

CASH FLOWS FROM FINANCING ACTIVITIES

RECEIPTS (Loan) 320000 100000 75000 100000 100000

PAYMENTS -59670 -33252 -43400 -51000 -55400

NET CASH PROVIDED BY FINANCING ACTIVITIES 260330 66748 31600 49000 44600

NET INCREASE (DECREASE ) IN CASH HELD 329875 365409 532656 660710 863957

CASH & CASH EQUIVALENTS AT BEGINNING OF REPORTING PERIOD 1397303 1038967 716165 560610 533109

CASH & CASH EQUIVALENTS AT END OF REPORTING PERIOD 1727178 1404376 1248821 1221320 1397066

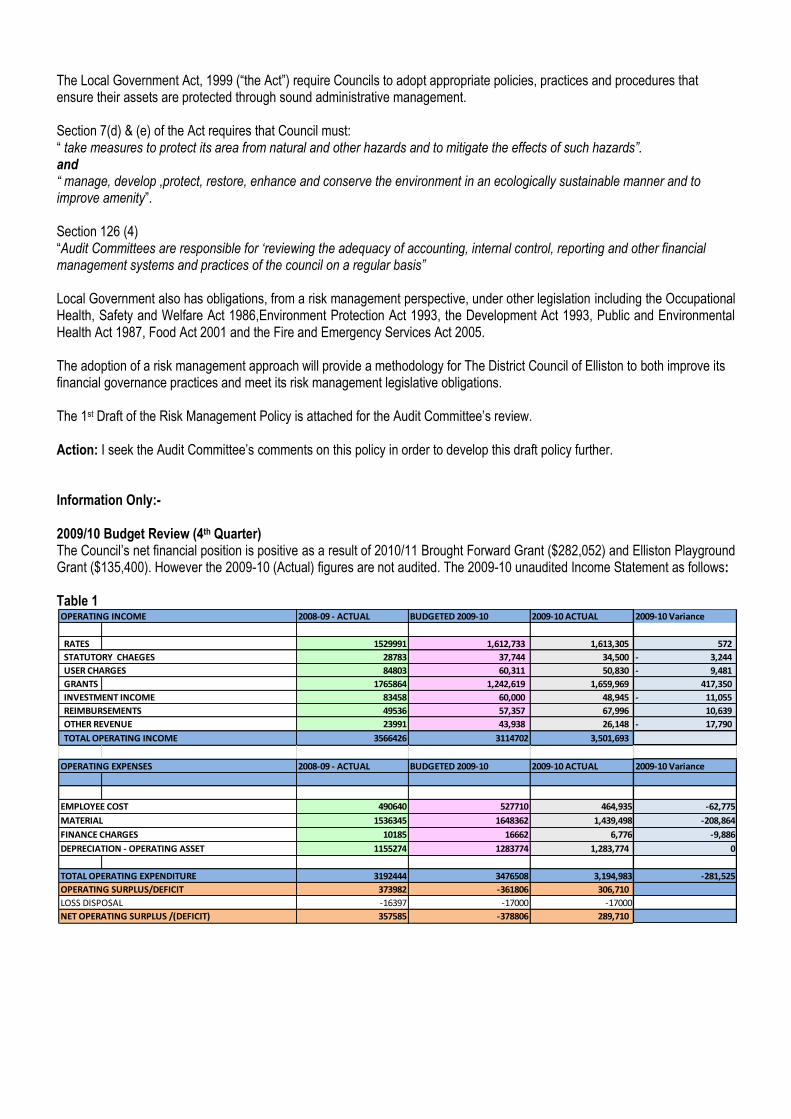

The Local Government Act, 1999 (“the Act”) require Councils to adopt appropriate policies, practices and procedures that ensure their assets are protected through sound administrative management. Section 7(d) & (e) of the Act requires that Council must: “ take measures to protect its area from natural and other hazards and to mitigate the effects of such hazards”. and “ manage, develop ,protect, restore, enhance and conserve the environment in an ecologically sustainable manner and to improve amenity”. Section 126 (4) “Audit Committees are responsible for „reviewing the adequacy of accounting, internal control, reporting and other financial management systems and practices of the council on a regular basis” Local Government also has obligations, from a risk management perspective, under other legislation including the Occupational Health, Safety and Welfare Act 1986,Environment Protection Act 1993, the Development Act 1993, Public and Environmental Health Act 1987, Food Act 2001 and the Fire and Emergency Services Act 2005. The adoption of a risk management approach will provide a methodology for The District Council of Elliston to both improve its financial governance practices and meet its risk management legislative obligations. The 1st Draft of the Risk Management Policy is attached for the Audit Committee‟s review. Action: I seek the Audit Committee‟s comments on this policy in order to develop this draft policy further. Information Only:- 2009/10 Budget Review (4th Quarter) The Council‟s net financial position is positive as a result of 2010/11 Brought Forward Grant ($282,052) and Elliston Playground Grant ($135,400). However the 2009-10 (Actual) figures are not audited. The 2009-10 unaudited Income Statement as follows: Table 1

OPERATING INCOME 2008-09 - ACTUAL BUDGETED 2009-10 2009-10 ACTUAL 2009-10 Variance

RATES 1529991 1,612,733 1,613,305 572

STATUTORY CHAEGES 28783 37,744 34,500 3,244-

USER CHARGES 84803 60,311 50,830 9,481-

GRANTS 1765864 1,242,619 1,659,969 417,350

INVESTMENT INCOME 83458 60,000 48,945 11,055-

REIMBURSEMENTS 49536 57,357 67,996 10,639

OTHER REVENUE 23991 43,938 26,148 17,790-

TOTAL OPERATING INCOME 3566426 3114702 3,501,693

OPERATING EXPENSES 2008-09 - ACTUAL BUDGETED 2009-10 2009-10 ACTUAL 2009-10 Variance

EMPLOYEE COST 490640 527710 464,935 -62,775

MATERIAL 1536345 1648362 1,439,498 -208,864

FINANCE CHARGES 10185 16662 6,776 -9,886

DEPRECIATION - OPERATING ASSET 1155274 1283774 1,283,774 0

TOTAL OPERATING EXPENDITURE 3192444 3476508 3,194,983 -281,525

OPERATING SURPLUS/DEFICIT 373982 -361806 306,710

LOSS DISPOSAL -16397 -17000 -17000

NET OPERATING SURPLUS /(DEFICIT) 357585 -378806 289,710

Table 2 BUDGET COMPARISION – CAPITAL EXPENDITURE 2009/10 AS OF 26-07-2010 BUDGET 2009/10 CAPITAL EXPENDITURE -ROAD BUDGET AMOUNT

(Ex GST) BUDGETED KM

CAT ACTUAL AMOUNT (Ex GST)

Variance $

Comments

136W SHERINGA BEACH ROAD 30,600 1.7 1 144,102 -$16,702 100% Completed

136W SHERINGA BEACH ROAD 21,600 1.2 1

136W SHERINGA BEACH ROAD 70,200 3.9 1

136W SHERINGA BEACH ROAD (Stormwater damaged part)

5,000 1

122R CLIFFTOP ROAD -R2R 247,308 7 1 259,614 -$12306 Completed & Signage to install

138W NO WHERE ELSE ROAD 147,600 8.2 2 172,783 -$25,183 100% completed

162W TOOLIGIE ROAD 135,000 7.5 2 220,147 -$4,147 100% Completed Feb 2010

162W TOOLIGIE ROAD 81,000 4.5 2

TOOLIGIE ROAD - TOTAL 216,000 12 2

203R ROCKY VALLEY ROAD 50,000 2.5 3 17,713 +$32,287 (Roll Over amount) 1.5Km to roll over

172W TERRE DAM 73,010 4.9 3 74,990 -$1980 Over Budget 100% Completed

148W BUZZACOTT ROAD 58,110 3.9 3 55,534 +$ 2576 Under Budget 100% Completed

166W BASCOMBE WELL ROAD Clarification given in the February 2010 Council Meeting – Refer CSM‟s Agenda Report.

29,800 2 3 61,919 -$ 32,119 Over Spend

100% Completed

125W MAIN STREET , BRAMFIELD 7,450 0.3 3 3,429 +$4021 (Roll Over amount) 0.2km to be completed

178 100 LINE ROAD- ($ 6300 [09/10]+$23500 [R2R-08/09]+10000[storm damage] = $39800)

178W 100 LINE ROAD-09/10 Budget 6,300 2-a 3 22,002 -$5702 Over Spend

100% complete

178W 100 LINE ROAD-Storm damage 10,000

178R 100 LINE ROAD-08/09 – R2R 23,500 2-b 3 24,243 -$ 743 Over Spend 100% complete

CAPITAL and NON- CAPITAL MAINTENANCE (Replacing ROCKY VALLEY ROAD, $77,480, 5.2 KM)

75,000 5.2 0 -----

164W

DEAR MAN ROAD

12,000

2

4

12,845

Reimbursed by Trevor Pearce $6800, -$749 over spend. Therefore actually -$749 is not overspend

100% complete Part of this expense was reimbursed by Trevor Pearce $6800 100% Completed

Total $1,008,478 51.6 $1,069,321 -$60843 -6.03 % including unbudgeted bonus amount and variance excluding bonus amount ($11,600) is -4.88% and actually completed 49.9km

This variance includes:-

Significant variance in cost Bascombe Well Road Re-sheeting work due to bad weather.

Includes a bonus amount of $11,600 to all works staffs including contractor which was not budgeted in the road re-sheeting costing.

Over run on Clifftop Drive due to Coastal Protection & Native Veg issues and extensive wet weather.

There is a overall expected net over run of about $22,325 for R2R projects. A small part of R2R projects are not completed also . Those unfinished parts are included

in the 2010/11 Budget. The net over run have to fund by the Council.

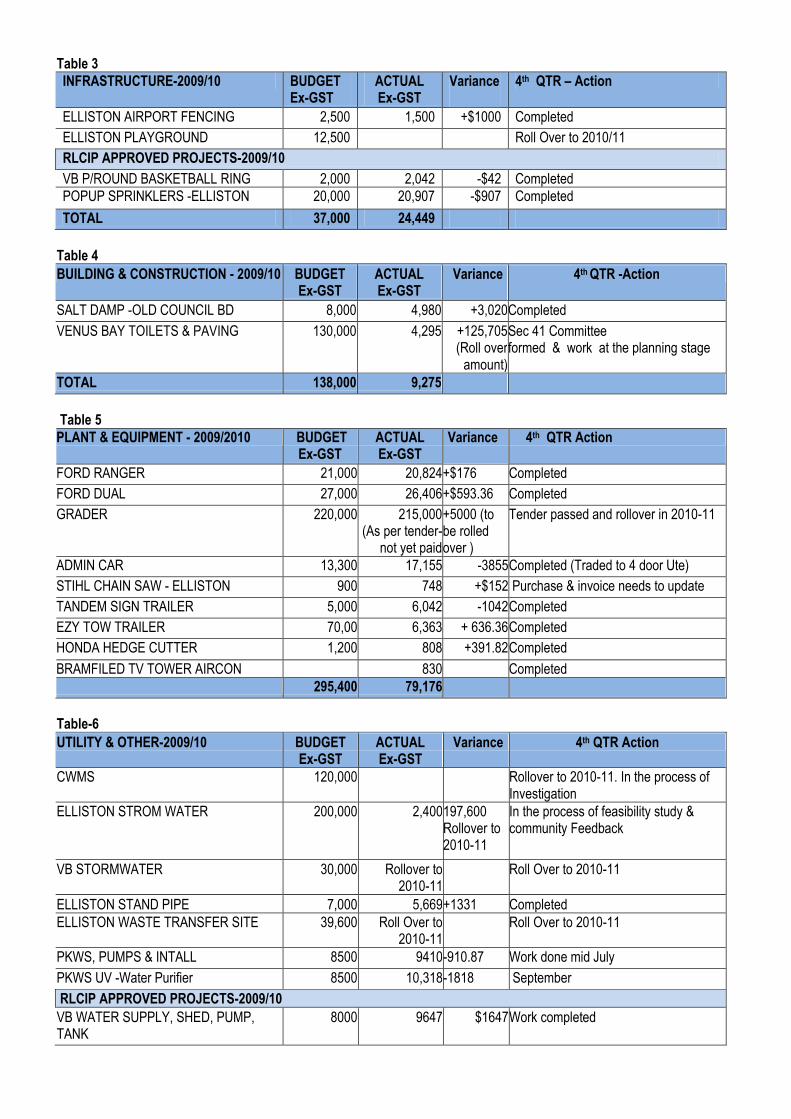

Table 3

INFRASTRUCTURE-2009/10 BUDGET Ex-GST

ACTUAL Ex-GST

Variance

4th QTR – Action

ELLISTON AIRPORT FENCING 2,500 1,500 +$1000 Completed

ELLISTON PLAYGROUND 12,500 Roll Over to 2010/11

RLCIP APPROVED PROJECTS-2009/10

VB P/ROUND BASKETBALL RING 2,000 2,042 -$42 Completed POPUP SPRINKLERS -ELLISTON 20,000 20,907 -$907 Completed

TOTAL 37,000 24,449

Table 4

BUILDING & CONSTRUCTION - 2009/10 BUDGET Ex-GST

ACTUAL Ex-GST

Variance

4th QTR -Action

SALT DAMP -OLD COUNCIL BD 8,000 4,980 +3,020 Completed

VENUS BAY TOILETS & PAVING 130,000 4,295 +125,705 (Roll over

amount)

Sec 41 Committee formed & work at the planning stage

TOTAL 138,000 9,275

Table 5

PLANT & EQUIPMENT - 2009/2010 BUDGET Ex-GST

ACTUAL Ex-GST

Variance

4th QTR Action

FORD RANGER 21,000 20,824 +$176 Completed

FORD DUAL 27,000 26,406 +$593.36 Completed

GRADER 220,000 215,000 (As per tender-

not yet paid

+5000 (to be rolled over )

Tender passed and rollover in 2010-11

ADMIN CAR 13,300 17,155 -3855 Completed (Traded to 4 door Ute)

STIHL CHAIN SAW - ELLISTON 900 748 +$152 Purchase & invoice needs to update

TANDEM SIGN TRAILER 5,000 6,042 -1042 Completed

EZY TOW TRAILER 70,00 6,363 + 636.36 Completed

HONDA HEDGE CUTTER 1,200 808 +391.82 Completed

BRAMFILED TV TOWER AIRCON 830 Completed 295,400 79,176

Table-6

UTILITY & OTHER-2009/10 BUDGET Ex-GST

ACTUAL Ex-GST

Variance 4th QTR Action

CWMS 120,000 Rollover to 2010-11. In the process of Investigation

ELLISTON STROM WATER 200,000 2,400 197,600 Rollover to 2010-11

In the process of feasibility study & community Feedback

VB STORMWATER 30,000 Rollover to 2010-11

Roll Over to 2010-11

ELLISTON STAND PIPE 7,000 5,669 +1331 Completed ELLISTON WASTE TRANSFER SITE 39,600 Roll Over to

2010-11 Roll Over to 2010-11

PKWS, PUMPS & INTALL 8500 9410 -910.87 Work done mid July

PKWS UV -Water Purifier 8500 10,318 -1818 September

RLCIP APPROVED PROJECTS-2009/10 VB WATER SUPPLY, SHED, PUMP, TANK

8000 9647 $1647 Work completed

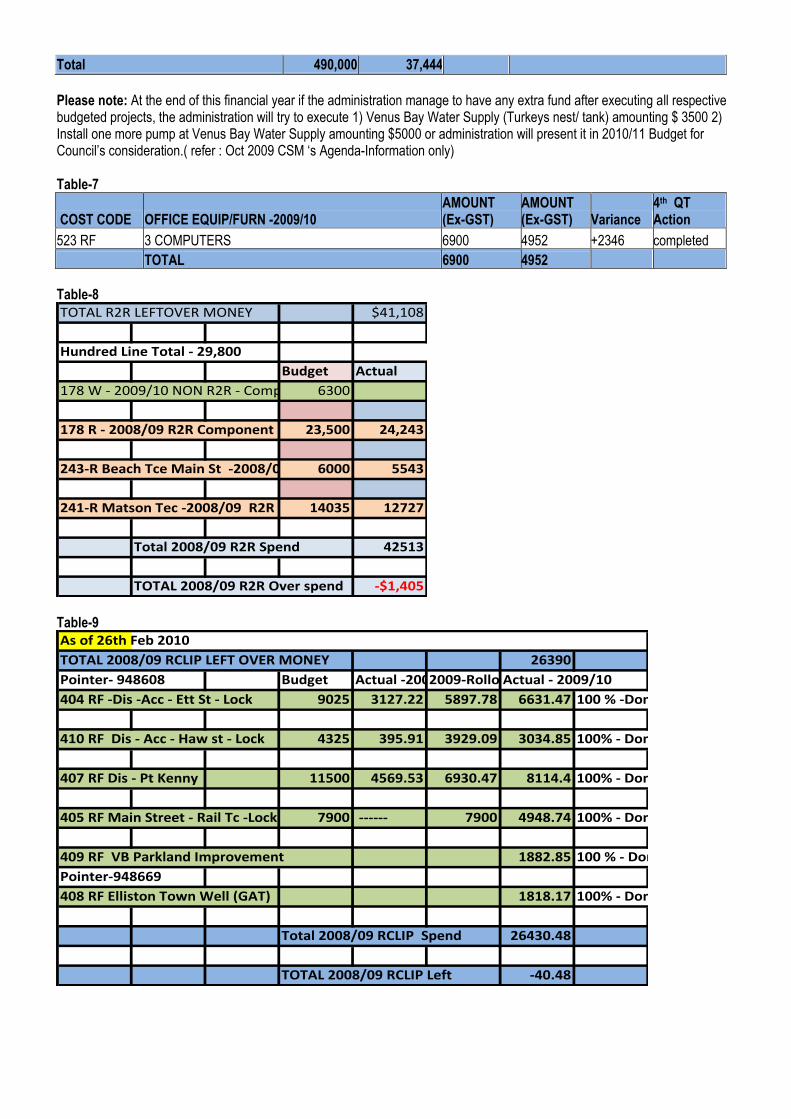

Total 490,000 37,444 Please note: At the end of this financial year if the administration manage to have any extra fund after executing all respective budgeted projects, the administration will try to execute 1) Venus Bay Water Supply (Turkeys nest/ tank) amounting $ 3500 2) Install one more pump at Venus Bay Water Supply amounting $5000 or administration will present it in 2010/11 Budget for Council‟s consideration.( refer : Oct 2009 CSM „s Agenda-Information only) Table-7

COST CODE OFFICE EQUIP/FURN -2009/10 AMOUNT (Ex-GST)

AMOUNT (Ex-GST) Variance

4th QT Action

523 RF 3 COMPUTERS 6900 4952 +2346 completed

TOTAL 6900 4952 Table-8

TOTAL R2R LEFTOVER MONEY $41,108

Hundred Line Total - 29,800

Budget Actual

178 W - 2009/10 NON R2R - Component 6300

178 R - 2008/09 R2R Component 23,500 24,243

243-R Beach Tce Main St -2008/09 R2R Component6000 5543

241-R Matson Tec -2008/09 R2R Component14035 12727

Total 2008/09 R2R Spend 42513

TOTAL 2008/09 R2R Over spend -$1,405 Table-9

As of 26th Feb 2010

TOTAL 2008/09 RCLIP LEFT OVER MONEY 26390

Pointer- 948608 Budget Actual -2008/092009-Rollover Actual - 2009/10

404 RF -Dis -Acc - Ett St - Lock 9025 3127.22 5897.78 6631.47 100 % -Done

410 RF Dis - Acc - Haw st - Lock 4325 395.91 3929.09 3034.85 100% - Done

407 RF Dis - Pt Kenny 11500 4569.53 6930.47 8114.4 100% - Done

405 RF Main Street - Rail Tc -Lock 7900 ------ 7900 4948.74 100% - Done

409 RF VB Parkland Improvement 1882.85 100 % - Done

Pointer-948669

408 RF Elliston Town Well (GAT) 1818.17 100% - Done

Total 2008/09 RCLIP Spend 26430.48

TOTAL 2008/09 RCLIP Left -40.48

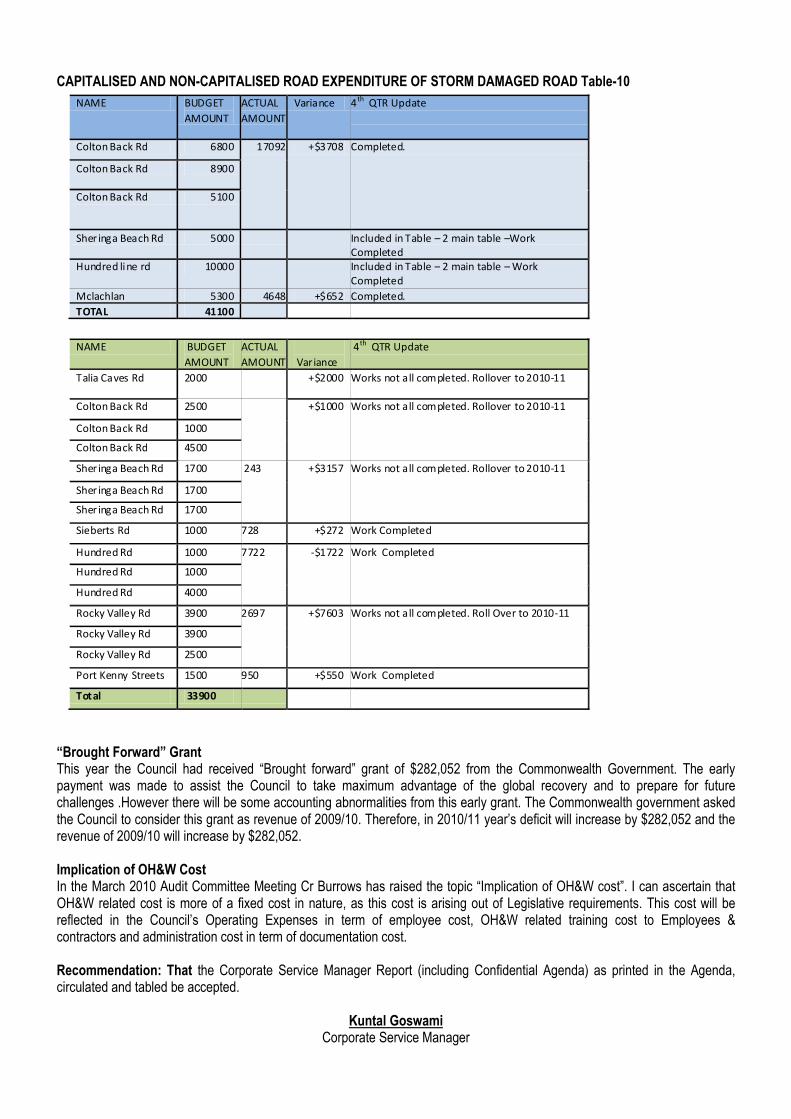

CAPITALISED AND NON-CAPITALISED ROAD EXPENDITURE OF STORM DAMAGED ROAD Table-10

“Brought Forward” Grant This year the Council had received “Brought forward” grant of $282,052 from the Commonwealth Government. The early payment was made to assist the Council to take maximum advantage of the global recovery and to prepare for future challenges .However there will be some accounting abnormalities from this early grant. The Commonwealth government asked the Council to consider this grant as revenue of 2009/10. Therefore, in 2010/11 year’s deficit will increase by $282,052 and the revenue of 2009/10 will increase by $282,052. Implication of OH&W Cost In the March 2010 Audit Committee Meeting Cr Burrows has raised the topic “Implication of OH&W cost”. I can ascertain that OH&W related cost is more of a fixed cost in nature, as this cost is arising out of Legislative requirements. This cost will be reflected in the Council’s Operating Expenses in term of employee cost, OH&W related training cost to Employees & contractors and administration cost in term of documentation cost. Recommendation: That the Corporate Service Manager Report (including Confidential Agenda) as printed in the Agenda, circulated and tabled be accepted.

Kuntal Goswami Corporate Service Manager

NAME BUDGET

AMOUNT

ACTUAL

AMOUNT

Variance

4th QTR Update

Talia Caves Rd 2000 +$2000 Works not all completed. Rollover to 2010-11

Colton Back Rd 2500 +$1000 Works not all completed. Rollover to 2010-11

Colton Back Rd 1000

Colton Back Rd 4500

Sher inga Beach Rd 1700 243 +$3157 Works not all completed. Rollover to 2010-11

Sher inga Beach Rd 1700

Sher inga Beach Rd 1700

Sieberts Rd 1000 728 +$272 Work Completed

Hundred Rd 1000 7722 -$1722 Work Completed

Hundred Rd 1000

Hundred Rd 4000

Rocky Valley Rd 3900 2697 +$7603 Works not all completed. Roll Over to 2010-11

Rocky Valley Rd 3900

Rocky Valley Rd 2500

Port Kenny Streets 1500 950 +$550 Work Completed

Total 33900

NAME BUDGET

AMOUNT

ACTUAL

AMOUNT

Variance 4th QTR Update

Colton Back Rd 6800 17092 +$3708 Completed.

Colton Back Rd 8900

Colton Back Rd 5100

Sher inga Beach Rd 5000 Included in Table – 2 main table –Work

Completed

Hundred line rd 10000 Included in Table – 2 main table – Work

Completed

Mclachlan 5300 4648 +$652 Completed.

TOTAL 41100

\\LGESQL\Data\WPData\NEW FILING STRUCTURE\Governance\Council Meetings Agenda and Minutes\Audit Committee Agenda 2010-2011\Aug 03 Agenda 10 - 11\Agenda 03 August 2010\Attachments\Diana Davis's Letter of Resignation .docx

From: Diane Davis [mailto:[email protected]]

Sent: Monday, 7 June 2010 11:20 AM To: Kuntal Goswami

Subject: RE: Proposed date for Audit Committee Meeting

Hi Kuntal I have accepted a position at Ceduna Council as from the 5th July so unfortunately will not be able to be on your Audit committee. Thanks Di

The District Council

of Elliston

Policy Document

DRAFT RISK MANAGEMENT POLICY

Date Adopted: Review Date: Original Minute Number: Revised Date:

Revised Minute Number:

What is Risk? Risk is the likelihood of an activation of an event that has undesired or unwanted outcomes or consequences or can be expressed as an estimate of the “chance” that an unwanted event will happen within a given period in time. Risk is everywhere and remains everywhere. Overall risk remains the same (the probability of 1 or 100% likelihood. Theoretically and practically when we do manage some risk factors other risk factors either emerge to fill the reduction and/or existing risk factors increase in probability (extent to which an event is likely to occur) or Likelihood. Therefore, risk cannot be created nor destroyed and can only be changed from forms and sources of risk to other forms and sources of risk. This means we can manage risk sources but not really manage risk in the entirety or completeness of risk.

What is Risk Management? Risk management is the process of identifying sources of risk within our environment and then working to reduce or re-direct the source and the event and the consequence of a particular risk. Therefore, risk management involves selecting sources of risk for management and listing the most important sources for risk management and ranking them in term of priorities and importance. In other words risk management is the act of risk balancing activity where cost – benefit approaches can be used to decide which sources or set of risk sources are required to address or which sources/ set of risk sources are required to address before other risk sources.

Risk Management in Local Government The Local Government Act, 1999 (“The Act”) that require Councils to adopt appropriate policies, practices and procedures that ensure their assets are protected through sound administrative management. Section 7(d) & (e) of the Act requires Council must: “take measures to protect its area from natural and other hazards and to mitigate the effects of such hazards”. “manage, develop ,protect, restore, enhance and conserve the environment in an ecologically sustainable manner and to improve amenity”. Section 126 (4) of the Act States: “Audit Committees are responsible for „reviewing the adequacy of accounting, internal control, reporting and other financial management systems and practices of the council on a regular basis”

Local Government also has obligations, from a risk management perspective, under other legislation including the Occupational Health, Safety and Welfare Act 1986,Environment Protection Act 1993, the Development Act 1993, Public and Environmental Health Act 1987, Food Act 2001 and the Fire and Emergency Services Act 2005. The adoption of a risk management approach will provides a methodology for The District Council of Elliston to improve its financial governance practices and meet its risk management legislative obligations. Definition of Risk in context The District Council of Elliston A risk is defined as: any threat that can potentially prevent the Council from meeting its objectives; any opportunity that is not being maximised by the Council to meet its objectives. To prevent any loss in the value of assets. To prevent any loss of its resources (physical, human, financial and environmental) and communities.

The total risk is the combination of the probability of an event (frequency/ occurrence of a particular set of circumstances) and its consequence (impact /outcome of an event).

Objective of this Policy To ensure that laws, regulations, industry codes and organisational standards are met;and To foster a culture which encourages opportunity and pursuit of best practices;and To have the effective control of financial risk , legal risks and environmental risk in order to ensure that Council complies

with the law.

Risk Management in the context of the District Council of Elliston Council is committed to the continuous process of pursuing coordinated activities to direct and control its exposure to risk. The District Council of Elliston will undertake a structured approach to identifying, evaluating and managing risks and it will undertake a proactive approach to order to minimise exposure to threats and lost opportunities. Risk Management Approach The steps involved in a risk management approach are summarised as follows: 1. Establish the Context. 2. Identify the risks. 3. Analyse the risks. 4. Evaluate the risks. 5. Treat the risks.

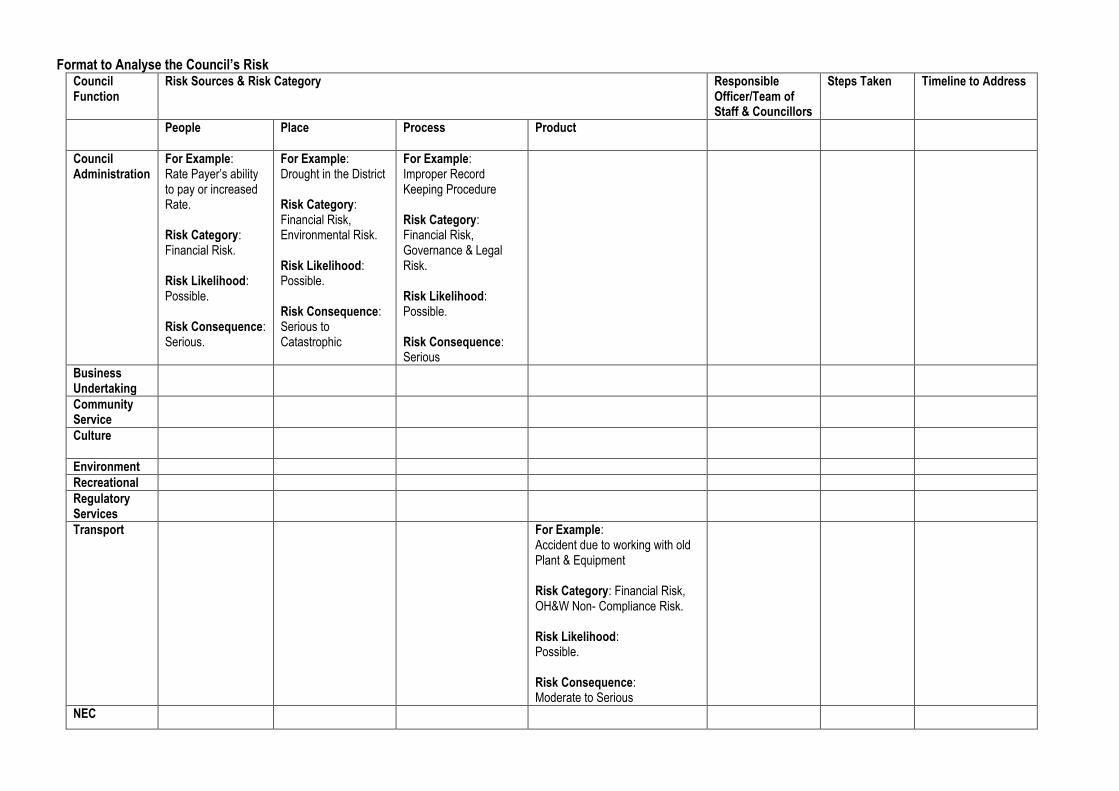

1) Establish the Context The Council should establish its context prior to commencing a risk assessment. Establishing the context requires an examination of its core function in which the risk identification, analysis and treatment options will be considered. This assists in establishing the assessment criteria for risk and the structure of the analysis. The Council’s core functions are as follows:

Council Administration.

Business Undertaking.

Community Service.

Culture.

Environment.

Recreational.

Regulatory Services.

Transport.

2) Identify the Risks In order to identify the risk, the Council have to identify the risk source in its core functions. The risk sources are:

People,

Place,

Process and

Product.

and within these risk sources the Council’s risk can be categorised as

Financial Risk,

Governance & Legal Risk,

Environmental Risk and

Business Continuity Risk.

OH&W Non-Compliance Risk.

Approaches used to identify risks may include:

Brainstorming sessions;

Review of the Council’s Risk Management Audit Report, OH&W Audit Report , Governance Audit ;Report and Annual & Interim financial Audit report;

Review of Internal Audit Report;

OH&W Hazard Management Register.

Assessment of historical incident data;

3) Analyse the Risks Risk analysis describes the process of determining the level of inherent risk associated with a particular issue before taking account of any mitigating factors or controls in place.

Format to Analyse the Council’s Risk Council Function

Risk Sources & Risk Category Responsible Officer/Team of Staff & Councillors

Steps Taken

Timeline to Address

People Place Process Product

Council Administration

For Example: Rate Payer’s ability to pay or increased Rate. Risk Category: Financial Risk. Risk Likelihood: Possible. Risk Consequence: Serious.

For Example: Drought in the District Risk Category: Financial Risk, Environmental Risk. Risk Likelihood: Possible. Risk Consequence: Serious to Catastrophic

For Example: Improper Record Keeping Procedure Risk Category: Financial Risk, Governance & Legal Risk. Risk Likelihood: Possible. Risk Consequence: Serious

Business Undertaking

Community Service

Culture

Environment

Recreational

Regulatory Services

Transport For Example: Accident due to working with old Plant & Equipment Risk Category: Financial Risk, OH&W Non- Compliance Risk. Risk Likelihood: Possible. Risk Consequence: Moderate to Serious

NEC

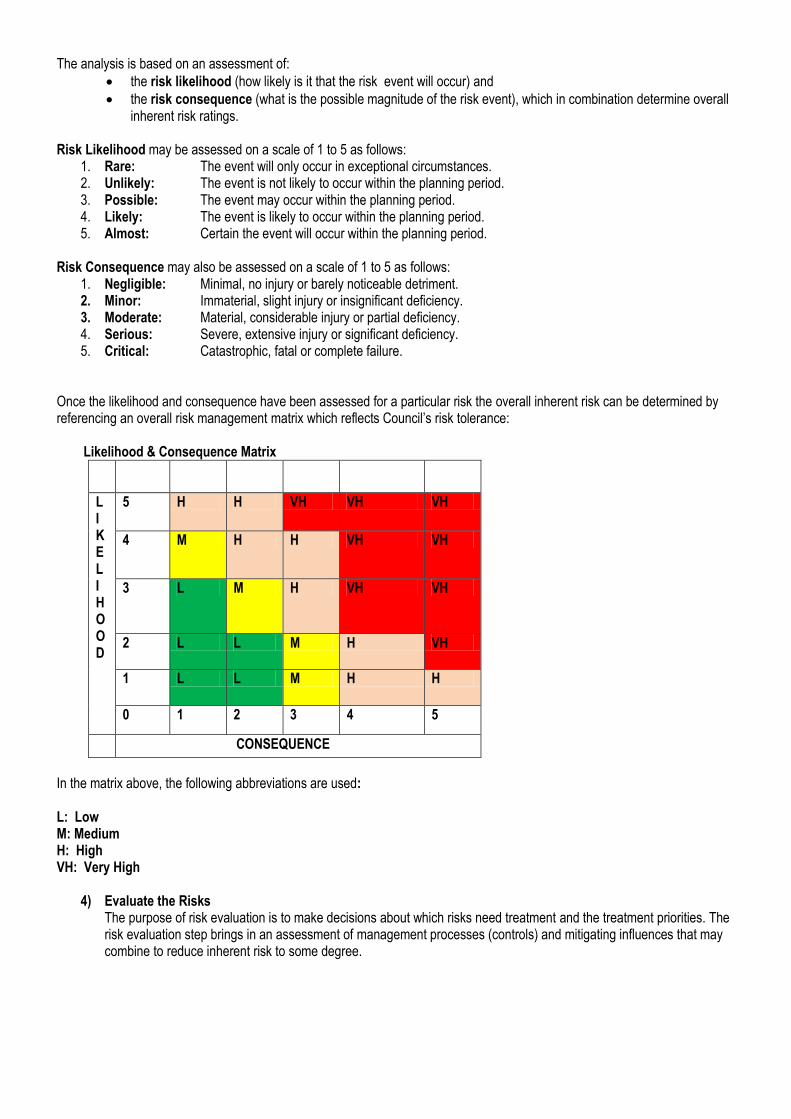

The analysis is based on an assessment of:

the risk likelihood (how likely is it that the risk event will occur) and

the risk consequence (what is the possible magnitude of the risk event), which in combination determine overall inherent risk ratings.

Risk Likelihood may be assessed on a scale of 1 to 5 as follows:

1. Rare: The event will only occur in exceptional circumstances. 2. Unlikely: The event is not likely to occur within the planning period. 3. Possible: The event may occur within the planning period. 4. Likely: The event is likely to occur within the planning period. 5. Almost: Certain the event will occur within the planning period.

Risk Consequence may also be assessed on a scale of 1 to 5 as follows:

1. Negligible: Minimal, no injury or barely noticeable detriment. 2. Minor: Immaterial, slight injury or insignificant deficiency. 3. Moderate: Material, considerable injury or partial deficiency. 4. Serious: Severe, extensive injury or significant deficiency. 5. Critical: Catastrophic, fatal or complete failure.

Once the likelihood and consequence have been assessed for a particular risk the overall inherent risk can be determined by referencing an overall risk management matrix which reflects Council’s risk tolerance: Likelihood & Consequence Matrix

L I K E L I H O O D

5 H H VH VH VH

4 M H H VH VH

3 L M H VH VH

2 L L M H VH

1 L L M H H

0 1 2 3 4 5

CONSEQUENCE

In the matrix above, the following abbreviations are used: L: Low M: Medium H: High VH: Very High

4) Evaluate the Risks The purpose of risk evaluation is to make decisions about which risks need treatment and the treatment priorities. The risk evaluation step brings in an assessment of management processes (controls) and mitigating influences that may combine to reduce inherent risk to some degree.

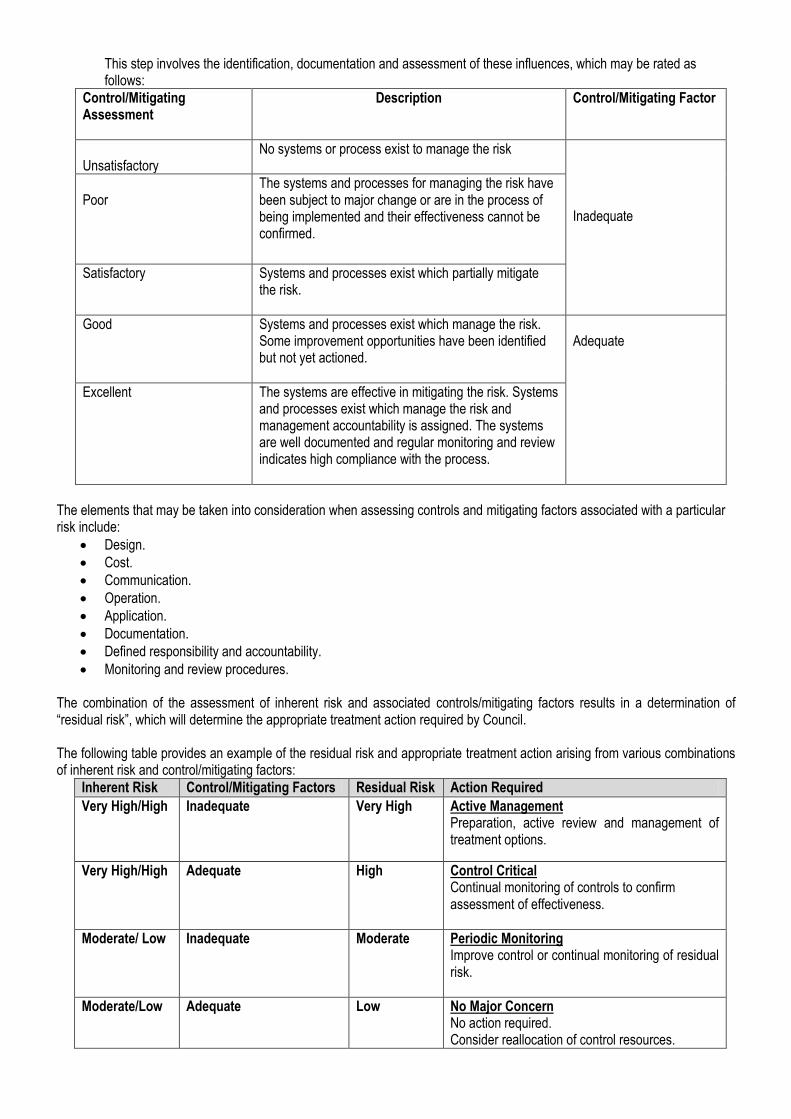

This step involves the identification, documentation and assessment of these influences, which may be rated as follows:

Control/Mitigating Assessment

Description Control/Mitigating Factor

Unsatisfactory

No systems or process exist to manage the risk Inadequate

Poor

The systems and processes for managing the risk have been subject to major change or are in the process of being implemented and their effectiveness cannot be confirmed.

Satisfactory Systems and processes exist which partially mitigate the risk.

Good Systems and processes exist which manage the risk. Some improvement opportunities have been identified but not yet actioned.

Adequate

Excellent The systems are effective in mitigating the risk. Systems and processes exist which manage the risk and management accountability is assigned. The systems are well documented and regular monitoring and review indicates high compliance with the process.

The elements that may be taken into consideration when assessing controls and mitigating factors associated with a particular risk include:

Design.

Cost.

Communication.

Operation.

Application.

Documentation.

Defined responsibility and accountability.

Monitoring and review procedures. The combination of the assessment of inherent risk and associated controls/mitigating factors results in a determination of “residual risk”, which will determine the appropriate treatment action required by Council. The following table provides an example of the residual risk and appropriate treatment action arising from various combinations of inherent risk and control/mitigating factors:

Inherent Risk Control/Mitigating Factors Residual Risk Action Required

Very High/High Inadequate Very High Active Management Preparation, active review and management of treatment options.

Very High/High Adequate High Control Critical Continual monitoring of controls to confirm assessment of effectiveness.

Moderate/ Low Inadequate Moderate Periodic Monitoring Improve control or continual monitoring of residual risk.

Moderate/Low Adequate Low No Major Concern No action required. Consider reallocation of control resources.

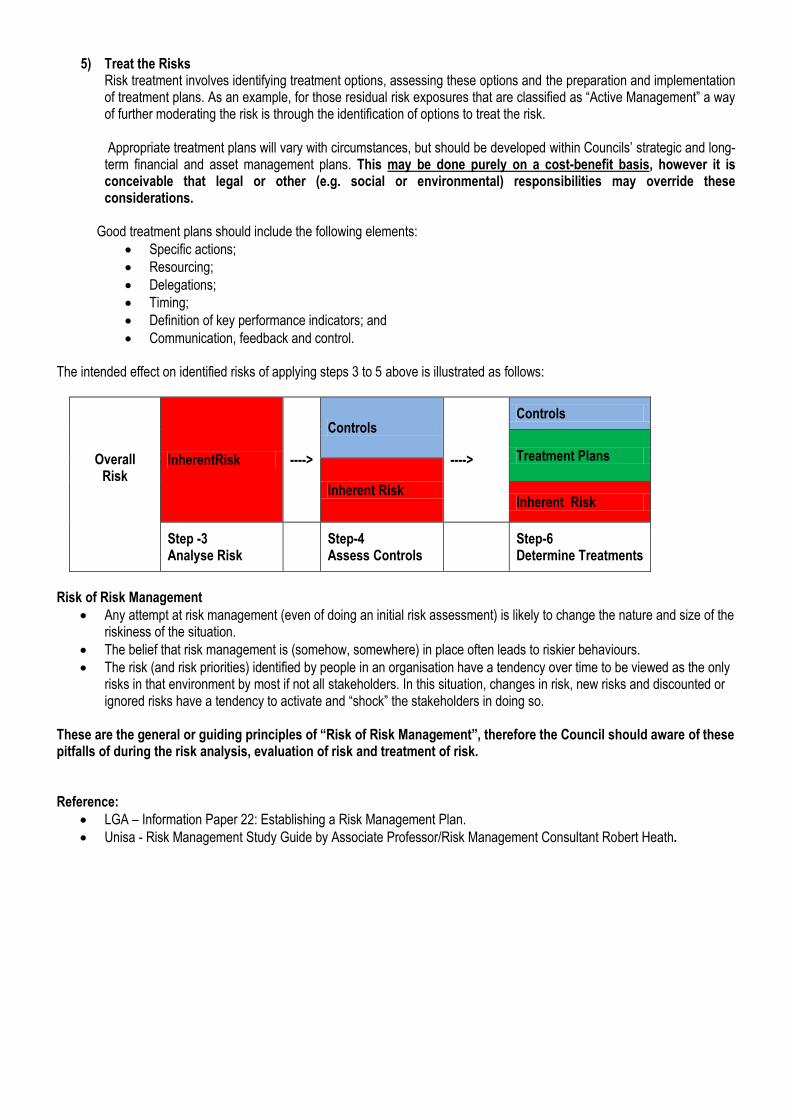

5) Treat the Risks Risk treatment involves identifying treatment options, assessing these options and the preparation and implementation of treatment plans. As an example, for those residual risk exposures that are classified as “Active Management” a way of further moderating the risk is through the identification of options to treat the risk.

Appropriate treatment plans will vary with circumstances, but should be developed within Councils’ strategic and long-term financial and asset management plans. This may be done purely on a cost-benefit basis, however it is conceivable that legal or other (e.g. social or environmental) responsibilities may override these considerations.

Good treatment plans should include the following elements:

Specific actions;

Resourcing;

Delegations;

Timing;

Definition of key performance indicators; and

Communication, feedback and control. The intended effect on identified risks of applying steps 3 to 5 above is illustrated as follows:

Overall Risk

InherentRisk ---->

Controls

---->

Controls

Treatment Plans

Inherent Risk Inherent Risk

Step -3 Analyse Risk

Step-4 Assess Controls

Step-6 Determine Treatments

Risk of Risk Management

Any attempt at risk management (even of doing an initial risk assessment) is likely to change the nature and size of the riskiness of the situation.

The belief that risk management is (somehow, somewhere) in place often leads to riskier behaviours.

The risk (and risk priorities) identified by people in an organisation have a tendency over time to be viewed as the only risks in that environment by most if not all stakeholders. In this situation, changes in risk, new risks and discounted or ignored risks have a tendency to activate and “shock” the stakeholders in doing so.

These are the general or guiding principles of “Risk of Risk Management”, therefore the Council should aware of these pitfalls of during the risk analysis, evaluation of risk and treatment of risk. Reference:

LGA – Information Paper 22: Establishing a Risk Management Plan.

Unisa - Risk Management Study Guide by Associate Professor/Risk Management Consultant Robert Heath.