Embed Size (px)

Citation preview

Agenda

9.00 – 9.30 New ambitions for profitable growth Rune Bjerke

9.30 – 10.10 Financial ambitions and new regulations Bjørn Erik Næss

10.10 – 10.35 Break

10.35 – 11.20 Growth in Norway Karin B. Orgland

11.20 – 11.50 International growth in the large corporate segment

Leif Teksum

11.50 – 12.15 Break

12.15 – 12.40 The Baltics – Raising the bar Terje Turnes

12.40 – 13.40 Q&A

13.40 – 14.00 Concluding Remarks Rune Bjerke

2

Financial ambitions towards 2015

Return on equity above 14 per cent

NOK 30 billion in pre-tax operating profits before write-downs

Cost/income ratio below 45 per cent

2

Untapped opportunities

Strong platform

Robust strategy for profitable growth

3

Strong development in operating profit

4

9.4

12.5

14.115.1 15.6

18.7

21.1

2004 2005 2006 2007 2008 2009 2010

Development in pre-tax operating profit before write-downs (NOK billion)

CAGR 14.4%

Significant growth in income

5

13 306 13 610

15 289

17 866

21 910 22 633

23 436

10 486

11 725

13 204

13 732

12 438

14 994 16 156

2004 2005 2006 2007 2008 2009 2010

Net interest income Net other operating income

CAGR

NII: 9.9%

NOOI: 7.5%

NOK million

6

Improved cost efficiency

NOK million

14 402

12 864

14 427

16 450

18 721 18 911 18 511

56.0%

50.2% 50.1% 50.6% 51.4%

48.1% 47.6%

0.0 %

10.0 %

20.0 %

30.0 %

40.0 %

50.0 %

60.0 %

70.0 %

80.0 %

90.0 %

100.0 %

2004 2005 2006 2007 2008 2009 2010

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

20 000

Operating expenses Ordinary Cost/income ratio

Sharp decline in loan losses after a peak in 2009

( 179)

137

( 258)

220

3 509

7 710

2 997

2004 2005 2006 2007 2008 2009 2010

NOK million

1) Pro forma figures including effects resulting from the implementation of IAS 39

1)

7

Strong ROE also in post-crisis environment

8

39.5

46.8

53.5

62.4

70.1

89.6

94.9

17.7% 18.8%

19.5%

22.0%

12.4%

10.6%

13.6%

2004 2005 2006 2007 2008 2009 2010

Equity Tier 1 capital Return on equity

NOK billion

Strong share price development relative to peers

9 Source: Bloomberg

Untapped opportunities

Strong platform

Robust strategy for profitable growth

10

The Norwegian bank

Norway

Share of group income

Photo: Erik Berg

11

Norwegians - The most attractive customers

12

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

USA EU12 Denmark Sweden Norway

GDP per capita in USD (PPP adjusted)

Source: Thomson Datastream/EIU/DnB NOR Markets

Among the fastest growing populations in Europe

13

Annual population growth in urban areas

> 750 000 inhabitants, 2005-2010

Estimated population growth in Europe

2010-2030*

Source: United Nations population division, World population prospects: The 2010 revision

Oslo

Norway

Istanbul

Turkey

Madrid

Spain

Toulouse

France

Munich

Germany

90

95

100

105

110

115

120

2010 2014 2018 2022 2026 2030

Norway

UK

Sweden

France

Denmark

Germany

Per cent

*Indexed, 2010 = 100

Stable low unemployment rates

14

Unemployment rates (in per cent of labour force)

Source: DnB NOR Markets and OECD, Economic Outlook NO 89

0 %

2 %

4 %

6 %

8 %

10 %

12 %

2004 2005 2006 2007 2008 2009 2010 F2011 F2012

Norway Sweden Euro Area Denmark Finland

Norway - An economy in a unique position

15

Public net wealth, per cent of GDP (2011)

Source: IMF (World Economic Outlook) and DnB NOR Markets

The Sovereign Wealth Fund (based on DnB NOR's oil price estimates)

-200

-150

-100

-50

0

50

100

150

200 USD billion

In per cent of GDP

0

50

100

150

200

250

0

200

400

600

800

1 000

1 200

1 400

1 600

2001 2005 2009 2013 2017

in USD billion in per cent of GDP

Still rich in natural resources

16

Norwegian exports by sector in 2010

50 %

6 %7 %

9 %

28 %

Oil/gas Food/seafood

Shipping Other commodities

Other

Source: Statistics Norway

The Norwegian bank – also internationally

International

Share of group income

17

Increasing international activity – presence in 20 countries

18 Source: IMF, World Economic Outlook

Global growth

about 4%

Oil demand exceeding supply - greater investment required

19

Global oil supply vs demand E&P spending among 70 oil companies

Source: DnB NOR Markets

75

80

85

90

95

100

105

110

2002 2004 2006 2008 2010 2012 2014

Global supply* Global demand

* Assuming OPEC producing at current level

Million b/d

0

25

50

75

100

125

0

100 000

200 000

300 000

400 000

500 000

600 000

1975

1980

1990

2000

2005

2010

2011e

2012e

E&P spending WTI crude price

USD million USD/bbl

Global trade is back on track

20

20

40

60

80

100

120

140

160

180

80-90 per cent of global trade goes by sea

2-3 per cent higher growth in global exports

than in global GDP

Source: CPB - Netherlands Bureau for Economic Policy Analysis

Total global trade (Seasonally adjusted volume, average exports and imports)

Indexed, 2000 = 100

Population growth and health focus drive demand for seafood

21

Population growth

Increased consumption per capita

0

50

100

150

200

250

300

350

World fisheries and fish farming production (In million tonnes)

Wild catch Fish farming scenario 1 Fish farming scenario 2 Fish farming

Source: FAO and DnB NOR Markets

Untapped opportunities

Strong platform

Robust strategy for profitable growth

22

How to grow?

Large corporate

customers

32%

Small and

medium-sized

enterprises

20%

Personal

banking

customers

48%

Share of net lending Q1 2011

23

Maintain an even balance between personal

banking customers and corporates

Where to grow?

Internationally - Strategic core industries

DnB

NORD

5%

Norwegian units 82%

International units 13%

Share of group income Q1 2011 Norway

- Personal banking customers and corporates

Nordics and the Baltics - Selective retail growth

24

Consider sale of Polish division

25

• Modest position

• Highly competitive market

• Costly to achieve a favourable strategic position

• Safeguard interests of both customers and employees

26

Stronger and united – one group, one brand

27

Sustainable strategy

Growth opportunities

More of the same

30

New financial ambitions

Drivers for growth

New regulations

Funding

2

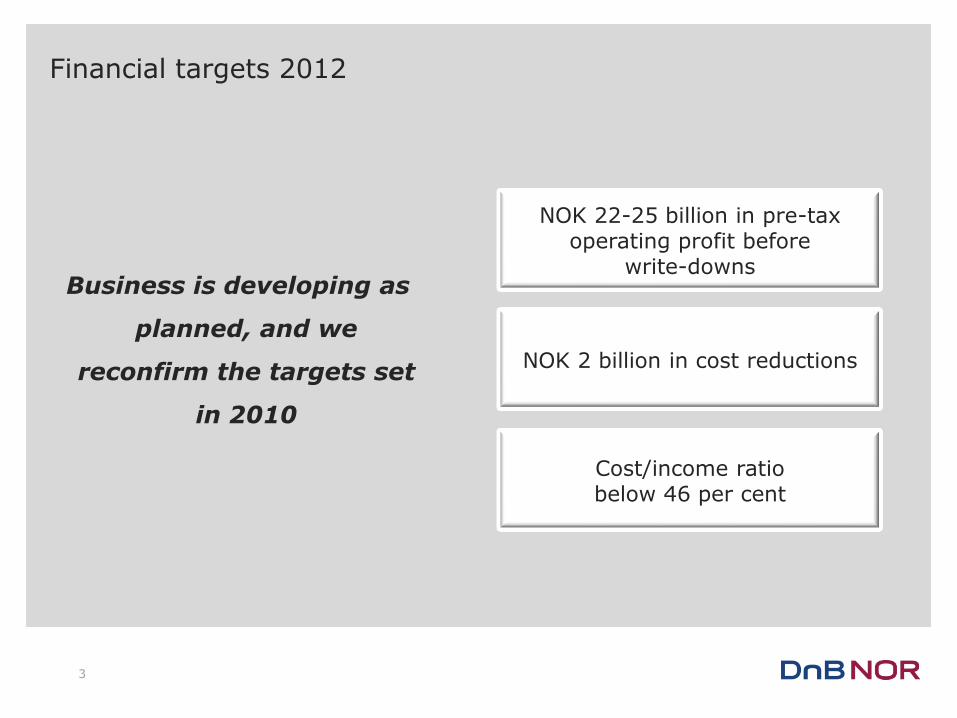

Financial targets 2012

Business is developing as

planned, and we

reconfirm the targets set

in 2010

NOK 22-25 billion in pre-tax operating profit before

write-downs

NOK 2 billion in cost reductions

Cost/income ratio below 46 per cent

3

Financial ambitions towards 2015

Return on equity above 14 per cent

NOK 30 billion in pre-tax operating profit before write-downs

NOK 1 billion in new cost reductions

Cost/income ratio below 45 per cent

4

No change in capital strategy and dividend policy

Be among the best capitalised banks in the Nordic region

Long-term AA rating for the bank

Approximately 50% dividend payout ratio

5

Assumptions underlying our financial ambitions

• Basel III will be implemented according to the schedule presented in December 2010

Basel III

• The Norwegian authorities will not introduce additional regulations or taxes/fees for the Norwegian financial sector

Norwegian regulations

• Increasing economic growth in Norway

• Stable international growth

• NOK money market rates of 5% in 2014

Macroeconomic developments

6

Robust macroeconomic development in Norway

0

1

2

3

4

5

2010 2011 2012 2013 2014

0

1

2

3

4

5

6

2010 2011 2012 2013 2014

0

1

2

3

4

2010 2011 2012 2013 2014

4

5

6

7

2010 2011 2012 2013 2014

GDP growth, per cent excluding the oil and gas sector

3-month NIBOR, per cent

Unemployment rate (In per cent of labour force)

Exchange rate NOK/USD

7

New financial ambitions

Drivers for growth

New regulations

Funding

8

Drivers for profitable growth

• Increase in volume above market

growth

• Higher interest rates

• Wider combined spreads

• Improvement programmes and

cost reductions

• Low write-downs

9

Additional NOK 1 billion in targeted annual cost savings by year-end 2014

10

Streamlining of business processes

Consolidation and centralisation

Improving procurement routines

Reorganising IT operations

350-400

300-400

200-250

NOK million

Increased cost savings (NOK million)

0

100

200

300

400

500

600

700

800

900

1000

2011 2012 2013 2014

50 -100

• Automatisation

• Digitalisation

• Increased use of self-service options

11

NOK million

350-400 Streamlining of business processes

• Postbanken, Vital and other entities united under one brand

in Norway • From 11 marketing units to one • Streamlined distribution • Full integration of DnB NORD, including closing down the

Copenhagen office

Consolidation and centralisation

NOK million 300-400

12

• Better prices and terms • Better allocation of resources • Coordinated processes

Improving procurement routines

Reorganising IT operations

• Simplification and standardisation • From 14 IT units to one

NOK million 50-100

NOK million 200-225

13

Portfolio quality remains strong

836

430

140

22

941

430

101

19

PD 0.01% - 0.75% PD 0.75% - 2.0% PD 2.0% - Net non-performing and net doubtful

commitments 31 March 2010 31 March 2011

Exposure at default (NOK billion)

PD = probability of default

14

Low write-downs

0,00 %

0,10 %

0,20 %

0,30 %

0,40 %

2010 2011 2012 2013 2014

Best estimate of future write-downs in per cent of total lending

15

New financial ambitions

Drivers for growth

New regulations

Funding

16

Basel III – four main issues

• Prepare for the schedule presented in December 2010 Implementation

• Leverage ratio best among Nordic peers Leverage ratio

• Capitalisation above expected requirements Capitalisation

• On track Liquidity

17

Expected implementation schedule

2013 2015 2016 2018 2019

Basel III introduction Solvency II introduction

LCR, minimum

Tier 1 capital

(4.5/6.0%)

Phase-in conservation buffer

NSFR, leverage ratio in pillar 1

Basel III completed

- as of 1 January each year

18

Leverage ratio: best among Nordic peers

3.6%

3.9% 4.0%

4.8% 4.8%

5.2%

Bank 1 Bank 2 Bank 3 Bank 4 Bank 5 DnB NOR

Tier 1 capital/total assets

As of 31 March 2011, from the quartely reports of our Nordic peers 19

DnB NOR is adequately capitalised

9.2 %

11.4 %

Expected range

10.0 – 12.0 %

10.0 %

12.3 %

Expected range 12.0 – 14.0%

CE T1 ratio CE T1 ratio New standard

T1 ratio T1 ratio New standard Full IRB Full IRB

Common Equity T1 and Equity T1 for DnB NOR as of 31 March 2011, including 50 per cent of profit for the period

Capitalisation of DnB NOR as of 31 March 2011 compared to expected new Basel III standards

20

New financial ambitions

Drivers for growth

New regulations

Funding

21

DnB NOR: a strong name in the funding market

Increasing the average residual maturity on

long- term senior debt and covered bonds

Diversifying funding activities to the USA and Australia with good results, both for long and short-

term funding

Stable deposit coverage at about 55%

22

Average residual maturity is increasing

2.0

2.5

3.0

3.5

4.0

4.5

2003 2004 2005 2006 2007 2008 2009 2010

Average residual maturity, long-term senior debt and covered bonds (years)

23

Long-term funding at competitive prices

25

35

45

55

65

75

85

95

105

115

125

aug.10 sep.10 okt.10 nov.10 des.10 jan.11 feb.11 mar.11 apr.11 mai.11

Z s

pread

, b

id levels

Secondary performance large liquid Nordic 5-year transactions over the last six months

DANBNK 4.75 06/04/2014 DNBNOR 4.5 05/29/2014 NBHSS 4.5 05/12/2014

POHBK 4.5 05/22/2014 SEB 5.5 05/06/2014 SHBASS 4.875 03/25/2014

Source: Barclays Capital Research, Time Series Plotter 24

Well positioned

New and strong financial ambitions

Robust and profitable portfolio

Well prepared for new regulations

Good access to funding at competitive prices

25

56

Untapped opportunities for profitable growth

Strong platform in Norway

2

Strong market shares Well positioned in home market – product areas and customer segments

Retail market

28 %

32 %

51 %

29 %

Corporate market

24 %

35 %

26 %

22%

Lending Deposits Policyholders’ funds Mutual fund assets

Lending* Deposits Policyholders’ funds Mutual fund assets

1Q 2011 * = share of lending from credit institutions

3

Stable total income and high return on allocated capital

ROAC is calculated on the basis of internal measurement of risk-adjusted capital. 4

4.7

5.0 5.1

4.8 4.6

4.8 4.7 4.8 4.8

24 %

31 % 27 % 26 %

25 % 23 % 25 %

23 % 25 %

0 %

5 %

10 %

15 %

20 %

25 %

30 %

35 %

40 %

45 %

50 %

1

2

3

4

5

6

1Q 09 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 3Q 10 4Q 10 1Q 11

Total income Return on allocated capital (annualised)

Development in total income and return on allocated capital in Retail Banking

NOK billion

Increasing growth – relatively stable interest spreads

Lending to and deposits from customers. Nominal values, excluding impaired loans. * Volume growth in Retail Banking in the period Jan-May 2011 (annualised)

Development in spreads Volume growth (annualised)

5

1.67% 1.67% 1.61%

1.69% 1.63%

0.42% 0.44% 0.53%

0.37% 0.40%

1.24% 1.26% 1.24% 1.24% 1.21%

1Q 10 2Q 10 3Q 10 4Q 10 1Q 11

Lending spread Deposit spread

Weighted spread

4.9 %

4.2 % 3.7 %

4.2 %

8.0 %

1.2 % 1.1 %

2.3 %

4.2 %

7.7 %

1Q 10 2Q 10 3Q 10 4Q 10 YTD*

Growth lending volumes Growth deposit volumes

Income is well balanced between products and segments

Excluding interest on allocated capital

23%

7%

13%

10% 5%

2%

12%

9%

9%

10% Mortgages lending

Corporate long term lending Consumer finance/ short-term credit Car finance

Investment and equipment finance Autolease/factoring

Other loans

Current account

Demand deposits

Other deposits

6

Net interest income 2010

Improved portfolio quality

Exposure at default (NOK billion) Corporate customers

Exposure at default (NOK billion) Personal banking customers

Low risk Medium risk High risk Low risk Medium risk High risk

7

416

127

45

5

458

132

38

4

PD 0.01% -

0.75 %

PD 0.75% -

2.0%

PD 2.0% - Net non

performing and

net doubtful

commitments

31 Dec 2009 31 March 2011

130

86

44

2

148

89

37

2

PD 0.01% -

0.75 %

PD 0.75% -

2.0%

PD 2.0% - Net non

performing

and net

doubtful

commitments 31 Dec 2009 31 March 2011

PD = Probability at default

Sound asset quality in mortgage loan portfolio in Retail Banking

Mortgage loans (NOK billion)

Mortgage loans based on actual collateral categories 8

397

52 28

430

52 22

Mortgage within 60 per cent of collateral value

Mortgage between 60 and 80 per cent of collateral value

Mortgage above 80 per cent of collateral value

31 Dec 2009 31 March 2011

Actual write-downs on loans significantly below normal levels

Corporate and personal customers - Retail Banking

NOK million

9

207

284

372 362

252

562 556 558 551 545

1Q 2010 2Q 2010 3Q 2010 4Q 2010 1Q 2011

Write-downs on loans and guarantees

Normalized write-downs on loans and guarantees

2.1 million personal

customers

200 000 corporate customers

1 million

insurance policyholders

130 000

non-life insurance

policyholders

600 000

mutual fund customers

400 000

mortgage loan customers

Out of 4 937 000 inhabitants:

Total customer base represents nearly half of the market

10

Estimated 40% of customers uses additional banks

Strong and unique distribution power in Norway

50 corporate advisory services centres

13 regional Markets

sales desks

112 real estate

offices

218

branch offices

208 post offices

2165 in-store

banking and postal outlets

Only bank in Norway with services available on Saturdays

11

1.6 million

online banking

customers

17 000 daily calls

and e-mails from

customers

0.8 million mobile

banking users

24/7

telephone banking

More than 4 million SMS

per month

37 million debit card

transactions per month Share of

households with Internet access and broadband connection

>= 70%

50 - < 70%

< 50%

High Internet and broadband penetration*

Strong and unique distribution power in Norway

Only bank in Norway with customer service open 24 hours a day,

every day

12 *Source: European Commission – Eurostat

Having satisfied customers leads to long-term profitability

DnB NOR customer satisfaction personal banking customers

RepTrak reputation survey - DnB NOR

56.2

64.2

65.8

2009 2010 2011

62

70

72 73

2008 2009 2010 2011

13

Ambitions in Norway

Stable and high return on equity

Lending growth > national credit growth rate

Low and stable losses

14

Untapped opportunities for profitable growth

Strong platform in Norway

15

Opportunities for profitable and sustainable growth

16

Regional variations in growth rates

Growth of new enterprises High growth rate in the four

largest cities in Norway

Source: Statistics Norway Source: The Confederation of Norwegian Enterprises (NHO)

17

We are well positioned for further growth

Low growth rate

High market share Low market share

High growth rate

Smaller cities East and North

Bergen

West coast

Oslo

Smaller cities West Trondheim Stavanger

18 Source: Statistics Norway – number of citizens

Growth on schedule in the four largest cities

Volume growth in Retail Banking in the period Jan-May 2011 (annualised) Banking market annualised based on 1Q 2011

Lending Deposits

Personal Banking

customers

Corporate customers

19

Banking market = 5.7%

Banking market = 6.4%

Banking market = 9.1%

Banking market = 3.8%

Opportunities for profitable and sustainable growth

20

High focus on selected segments with substantial potential

Young adults:

High net present value

Academics:

High potential segment

Affluent:

Very high potential segment

SME: Business offering

tailored to industry needs

1 2

3 4

21

Population growth among young adults ‒ increasing need for new housing

Source: Statistics Norway /DnB NOR Markets

-20 000

-10 000

0

10 000

20 000

30 000

40 000

50 000

1980 1988 1996 2004 2012 2020 2028 2036 2044 2052 2060

Population 20-34: y/y Completed homes

Highly competitive mortgage loan interest

rates

NOK 33 billion in ‘BLU’ loans

Cross-selling between a number of products

1

Distribution advantages home-university-work

Marketing and sponsorships

22

Development in young population vs completed homes

Exclusive distribution to academics – attractive customer segment with high growth

Best market terms – also for self-employed persons and SMEs

Product range to suit both professional and private

needs

Exclusive distribution agreement with the

Federation of Norwegian Professional Associations

2

Source: Norwegian Professional Associations

128

133

139

126

131

137

144

148

154

2003 2004 2005 2006 2007 2008 2009 2010 2011

Increasing number of members joining the Federation of Norwegian Professional Associations (in 1000)

23

Well positioned to be the natural choice for Norway’s most affluent bank customers

Assets under management – 33% annual growth rate

Proven excellent quality of management of proprietary mutual funds

Wide product range – including non-proprietary products

3

24

The number of newly established enterprises increased over the last 12 months

Corporate and personal needs

Entrepreneurs

Franchises

Academics

Source: Statistics Norway

4

25

Export industries are generating growth in the SME segment 4

Norwegian exports by sector in 2010

50 %

6 %7 %

9 %

28 %

Oil/gas Food/seafood

Shipping Other commodities

Other

Source: The Confederation of Norwegian Enterprises (NHO) Source: Statistics Norway

26

We are the preferred bank for CM solutions in Norway –important driver for stable funding

Products tailored to customer size and

growth

Services available on Saturdays through post

offices

Local and national bank

Source: Large Corporate Banking Survey, Norway

(116) (88)

(110) (91)

(70) (53)

(66) (59)

(48) (39)

(27) (26)

(76) (60)

(73) (63)

(46) (37)

(47) (39)

(34) (22)

(19) (22)

Use bank for domestic cash management

Use bank for overall international cash management

DnB NOR

Bank #2

Bank #3

Bank #4

Bank #5

Bank #6 2010

2009

4

27

Growth in demand and rising interest rates will reduce pressure on spreads

Stable interest rates generate pressure on spreads. Rising interest rates give

opportunities over time

International spread adjustment not fully implemented in the Norwegian corporate

market due to slack in demand

Competitive funding terms compared to local savings banks

3.7

- 3.0

- 1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

Jan 09

Apr Jul Oct Jan 10

Apr Jul Oct Jan 11

Apr Jul Oct

Growth in corporate lending - credit indicator C2

Source: Statistics Norway 28

Opportunities for profitable and sustainable growth

29

Product penetration – leading position compared to European peers

Source: Finalta and DnB NOR - 2010

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

1 4 7 10 13 16 19 22 25 28 31 34

West European Peers

Average 2.27

DnB NOR

30

Average number of products per customer

Still untapped potential – pricing scheme encourages greater product penetration

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

1 4 7 10 13 16 19 22 25 28 31 34

West European Peers

Average 2.27

DnB NOR

DnB NOR loyalty programme customers

31

Average number of products per customer

Source: Finalta and DnB NOR - 2010

Innovative products increase sales

Find your ”home” app Start-up enterprise app

Buy a car app – easier and more efficient

32

New pension reform requires more private savings

Source: Finance Norway (FNO)

Example: Pension payment for a person born in 1963, 40-year service period,

retirement at 67

Pro-active offering of professional advice and savings solutions

New product range and good track record

Discretionary asset management

More than 45% of top-rated mutual funds (Morningstar)

33

150

155

160

165

170

175

180

185

Former national insurance scheme

New national insurance scheme

NOK 1000

Brisk sales of insurance products

Non-life insurance market share up almost 50% in two years*

Number of life insurance policies up from 4 000 in 1Q 2010 to 9 000 in 1Q 2011

More than 90% of our sales people are certified

Development in number of insurance policies sold

* Source: Finance Norway (FNO) 34

-

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

100 000

Jan-May 2010 Jan-May 2011

Strong foothold in the market and high market share within consumer finance, with further growth potential

Source: Datamonitor

Pay Later Card Market Forecasted compound growth rates until 2013

1.0 %

1.6 %

1.6 %

3.4 %

4.0 %

5.7 %

6.0 %

6.1 %

6.4 %

6.7 %

6.7 %

7.6 %

7.8 %

7.9 %

8.8 %

9.3 %

16.3 %

UK

Greece

Ireland

Sweden

Switzerland

Denmark

France

Germany

Portugal

Italy

Spain

Belgium

Norway

Austria

Finland

Netherlands

Turkey

Substantial growth in credit card usage in Norway

Increasing market share within car financing and credit cards

Strong sales from distribution through other retailers

Wider presence in neighbouring countries

35

Close integration between real-estate business and home loan sales, with further growth potential

Increase in number of real estate sales through our real estate agents.

Leads to home loan sales six times greater

than actual housing sales: Increasing hit rate on mortgage

leads – 36 000 leads yearly

New projects – cooperation between brokers, private and corporate

sales

Most satisfied and most loyal customers

Front runner in online solutions

Market leader in Norway – strategy for growth

36

3 901

4 096

4 414

5 234

1Q 2008 1Q 2009 1Q 2010 1Q 2011

Four drivers for sustainable growth in the Norwegian market

37

94

2

Growth opportunities

Proven strategy – solid results

3

Strategy based on long-term relationship-oriented banking and industry expertise

EaD NOK billion

31 March 2011

284

67

163

4

Increasing share of total income from international business*

3 371

4 160

4 555

5 096

9.8%

11.1% 11.5%

13.4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

1 000

2 000

3 000

4 000

5 000

6 000

2008 2009 2010 2011 (annualised)

Total income international units Share of group income

*Baltics & Poland not included Annualisation: Income = Q1-2011 * 4, Share of group income = actual proportion Q1-2011

NOK million

5

Strong and profitable growth in our global industries

Development in profit, losses and RORAC Global industries*

NOK million

*Sum of shipping, offshore, logistics, energy & seafood Annualisation 2011: Profit before write-downs = ytd May/5*12, Actual losses = ytd May/5*12, Normalised losses = ytd May/5*12, RORAC = ytd May/5*12

2 436

3 150

3 478 3 605

758

1 251 1 092

735

145

457 307

43

13.5%

10.9%

14.7%

22.4%

0 %

5 %

10 %

15 %

20 %

25 %

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

2008 2009 2010 2011 (annualised)

Profit before write-downs Normalised losses Actual losses RORAC

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

6

Increased profitability driven by volume growth and wider lending spreads

NOK billion

Development in lending, deposits and spreads Global industries*

*Sum of shipping, offshore, logistics, energy & seafood

147

195 179 183

86 103 107 117

0.70 % 0.86 %

0.94 % 0.97 % 1.00%

1.26%

1.49% 1.60%

0.00 %

0.25 %

0.50 %

0.75 %

1.00 %

1.25 %

1.50 %

1.75 %

2.00 %

-

20

40

60

80

100

120

140

160

180

200

2008 2009 2010 1Q2011

Net lending (excl. cred. inst.) Deposits from customers

Combined spread (weighted) Lending spread (weighted)

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

7

Other industries are also important contributors to profitability and diversification

Development in profit, losses and RORAC Other industries*

NOK million

*Sum of telecom, healthcare, forest industries, media, commercial real estate, retail industry, technology, public sector, services, finance

2 169

2 770 2 588

3 273

368 461 419 463

10

621

-41

463

22.6%

19.9%

24.9%

20%

0 %

5 %

10 %

15 %

20 %

25 %

30 %

- 500

0

500

1 000

1 500

2 000

2 500

3 000

3 500

2008 2009 2010 2011 (annualised)

Profit before write-downs Normalised losses Actual losses RORAC

Annualisation 2011: Profit before write-downs = ytd May/5*12, Actual losses = Eguals normalised losses, Normalised losses = ytd May/5*12, RORAC = ytd May/5*12

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

8

Significant increase in lending volume and spreads at the start of 2011

NOK billion

*Sum of telecom, healthcare, forest industries, media, commercial real estate, retail industry, technology, public sector, services, finance

Development in lending, deposits and spreads Other industries*

138

110 111

159

122 93 89 105

0.65% 0.79%

0.84% 0.95% 0.97%

1.31% 1.41%

1.52%

0.00 %

0.25 %

0.50 %

0.75 %

1.00 %

1.25 %

1.50 %

1.75 %

2.00 %

-

20

40

60

80

100

120

140

160

180

200

2008 2009 2010 1Q2011

Net lending (excl. cred. inst.) Deposits from customers

Combined spread (weighted) Lending spread (weighted)

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

244

163

65

4

314

170

30 4

PD 0.01% - 0.75% PD 0.75% - 2.0% PD 2.0% - Net non-performing and net doubtful

commitments

30 Dec. 2009 31 March 2011

9

Improved quality in the large corporate portfolio

Low risk Medium risk High risk

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

PD = Probability of default

Exposure at default (NOK billion)

10

Diversified LBO portfolio

Distribution per risk category

Total portfolio of NOK 51.3 billion,

comprising 92 exposures

Acceptable risk level

Well-diversified sector mix

17 % 70 %

14 % High risk (grade 7.7-10)

Moderate risk (grade 5-

7.7)

Low risk ( grade < 5)

Infrastructure 2 % Energy

12 %

Industrials 11 %

Services 29 %

Consumer 12 %

Healthcare 18 %

Technology 8 %

Media 2 %

Financials 6 %

Distribution per industry segment

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

11

The shipping, offshore and logistics portfolio has been stable since the end of 2008

Loans and guarantees 2006-2010

Portfolio segmentation 31 March 2011 vs 31 March 2010

Offshore

25% (27%)

Crude oil

tankers

10%

(10%)

RoRo/PCC

3% (4%)

Container 11% (9%)

Cruise

4% (5%)

Dry cargo

15%

(15%)

Chemical and

product

tankers

7% (8%)

Other

shipping

2% (3%)

Other non-

shipping

8% (3%)

Gas

9% (10%)

Logistics

6% (7%)

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

89

117

180

143 152

143

0

20

40

60

80

100

120

140

160

180

200

2006 2007 2008 2009 2010 1Q2011

Total loans and guarantees Adj.Loans/guarantees

NOK billion

12

Limited write-downs and improved portfolio quality

Shipping write-downs in NOK and per cent of drawn portfolio past 20 years

Exposure at default Shipping, offshore & logistics

Low risk Medium risk High risk

-1.0 %

-0.5 %

0.0 %

0.5 %

1.0 %

1.5 %

2.0 %

2.5 %

3.0 %

-200

0

200

400

600

800

1000

Net write-downs % of drawn portfolio

PD = Probability of default

NOK million

0

20

40

60

80

100

120

PD 0.01% -

0.75%

PD 0.75% -

2.0%

PD 2.0% -

31 March 2010 31 March 2011

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

NOK billion

13

The dry bulk and tanker segments are showing high volatility

Dry bulk (USD/day)

Spot rates for dry-bulk capesize vessels last 10 years vs. DnB NOR's current estimates

Tankers (USD/day)

Spot rates for VLCC tanker vessels last 10 years vs. DnB NOR's current estimates

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

160 000

180 000

200 000

apr.

01

apr.

02

apr.

03

apr.

04

apr.

05

apr.

06

apr.

07

apr.

08

apr.

09

apr.

10

apr.

11

Spot rates Base Case Risk Case

-20 000

30 000

80 000

130 000

180 000

230 000

apr.

01

apr.

02

apr.

03

apr.

04

apr.

05

apr.

06

apr.

07

apr.

08

apr.

09

apr.

10

apr.

11

Spot rates Base Case Risk Case

10 000 15 000

20 000 25 000

USD USD

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

Apr

01

Apr

02

Apr

03

Apr

04

Apr

05

Apr

06

Apr

07

Apr

08

Apr

09

Apr

10

Apr

11

Apr

01

Apr

02

Apr

03

Apr

04

Apr

05

Apr

06

Apr

07

Apr

08

Apr

09

Apr

10

Apr

11

14

Growth opportunities

Proven strategy – solid results

15

We have a clear #1 position in the Norwegian market

DnB NOR Bank #2 Bank #3 Bank #4 Bank #5 Bank #5

Source: Large Corporate Banking Survey, Norway

Market penetration and tier position

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

16

Significant improvement in our pan-Nordic position

-23

-4

52

44

109

-15

11

40

81

94

-40 -20 0 20 40 60 80 100 120

Bank #5

Bank #4

Bank #3

DnB NOR

Bank #2

2010 2009

Overall relationship quality – pan-Nordic

Source: Large Corporate Banking Survey, Pan-Nordic

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

17

Growth in non-lending income

LCI total (NOK million)

Dedicated customer teams drive cross-sales

LCI international units (NOK million)

1 418 1 708

1 995 2 202

669

842

1 142 1 342

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

2008 2009 2010 Q1-2011

annualised

Lending income Non-lending income

3 237 4 354

5 315 5 567

4 077

4 215

4 334 4 869

0

2 000

4 000

6 000

8 000

10 000

12 000

2008 2009 2010 Q1-2011

annualised

Lending income Non-lending income

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

18

We are one of the world’s leading shipping banks

2010 top bookrunner table: syndicated shipping loans

Pos. Bookrunner Deal value $m No. % share

1 DnB NOR Bank 5 714 39 11

2 Nordea Bank 4 622 22 9

3 Mitsubishi UFJ Financial Group 3 576 12 7

4 ING 1 952 9 4

5 Citi 1 679 7 3

6 BNP Paribas 1 156 4 2

7 RBS 1 072 4 2

8 JPMorgen 1 003 4 2

9 Bank of America Merrill Lynch 910 4 2

10 Danske Bank 900 2 2

Source: Dealogic

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

19

We have supported our core clients and remained active throughout the financial crisis

We know the industry and our

clients

We give priority to clients with

cross-sale potential

We finance shipping companies, not

vessels

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

20

US IG Energy Bookrunner

2009

Rank Bank Volume

1 DnB NOR 3 937

2 JP Morgan 3 715

3 Bank of America 3 695

4 Wells Fargo 3 556

5 BNP Paribas 1 960

2010

Rank Bank Volume

1 Wells Fargo 15 694

2 JP Morgan 15 149

3 Bank of America Merril Lynch 12 285

4 Citi 12 195

5 DnB NOR 8 650

EMEA Oil & Gas Bookrunner

2010

Rank Bank Volume

1 BNP Paribas Group 5 769

2 Societe Generale 5 528

3 RBS 3 299

4 Credit Agricole CIB 3 257

5 JP Morgan 3 194

6 ING Groep NV 2 697

7 Standard Chartered PLC 2 541

8 Misubishi UFJ finanncial 2 254

9 Citi 2 214

10 DnB NOR 1 990

We are clearly visible in the major energy league tables

Source: Thomson Reuters Loan Pricing Corporation

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

And well positioned to capitalise on future opportunities

Strong Norwegian platform

Reinforced international standing

during the financial crisis

Energy professionals and products

available worldwide

21

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

Selected transactions 2010 and 2011

22

Our expertise and global presence enable us to capitalise on the opportunities within seafood

Cross-sales to our existing Norwegian customer base

Aquisition of selected customers in Chile and Peru, North-America and

Northern Europe

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

Selected transactions 2009 and 2010

Our international presence supports our strategy

Proven model of control & governance – no business

outside strategy

Organic growth in international network to meet customer needs

Significant industry and product capabilities added

over the years

23

Shipping, Offshore and

LogisticsEnergy Seafood

Telecom

ServiceTech-nology

RetailIndustry

Com-mercial

Real Estate

PublicSector

Finance

Customer value

Healthcare products

Forest

IndustriesMedia

No change in strategy. More of the same. Solid market position in key segments

Strong mega-trends support our growth opportunities within shipping, offshore, energy and seafood

International network with products and expertise adapted to our customers’ needs

Well-positioned to tap into the growth areas of the future

24

Well positioned for the future

119

2

Macroeconomic situation and future outlook

Background

Growth

-20

-15

-10

-5

0

5

10

15

Real GDP growth in per cent

Estonia Latvia Lithuania

From joint venture to 100 per cent ownership

3

“The Baltics...an area with good future earnings potential.”

Evaluation period starts

“Establishing DnB NORD is strategically important to participate in the expected growth in this region, as well as being present for our Nordic customers.”

DnB NOR enters into JV with NORD/LB “The Baltics...higher growth potential than Western Europe, and DnB NOR wishes to grow within the retail banking segment.”

DnB NOR acquires 100 %

Governance model aligned with DnB NOR

4

New legal structure

New operational governance structure implemented

”One Group” in the Baltics

Strong central control of risk

Centralised funding

5

Macroeconomic situation and future outlook

Background

Growth

c

Recession over – strong recovery

6 Source: Eurostat, European Commission, DnB NORD forecasts

Positive credit demand expected

Growth in loans granted to private sector in per cent

Source: Eurostat, ECB Data Warehouse 7

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

Lendin

g

Deposit

Lendin

g

Deposit

Lendin

g

Deposit

Lendin

g

Deposit

Lendin

g

Deposit

2007 2008 2009 2010 Q1

2011

mEUR

Lithuania Latvia Estonia

0

100

200

300

400

500

600

700

800

Private individuals Legal entities

Non-performing portfolio Baltic States 1Q 2008 – 1Q 2011

mEUR

Customers have been safeguarding their financial position

Lending and deposit volumes DnB NORD , Q1 2011

8

Lendin

g

Deposits

Lendin

g

Deposits

Lendin

g

Deposits

Lendin

g

Deposits

Lendin

g

Deposits

2008 2009 2010 1Q 2011

2007

Growth potential in a sizeable market

9

Country Population Market position

No of customers

Lithuania 3.3 mill 3 0.7 mill

Latvia 2.3 mill 4 0.2 mill

Estonia 1.3 mill 5 0.01 mill

Total Baltics

6.9 mill 0.9 mill

Norway 4.9 mill 1 2.1 mill

Lithuania 1.8 %

Latvia 1.4 % Estonia

0.2 %

Rest of the

Group 96.5 %

DnB NOR lending per country Q1 2011

Large corporate

8 %

SME 46 %

Lithuania 52 %

Latvia 41 %

Estonia 7 %

A well diversified retail portfolio

Lending per country - Q1 2011

EUR 5 450 million

Lending per segment - Q1 2011 EUR 5 450 million

10 Definintion large corporate > EUR 50 mill turnover

Private individuals

46%

11

Macroeconomic situation and future outlook

Background

Growth

Good market coverage in Latvia and Lithuania

• Estonia: Mainly a corporate and leasing bank with efficient operations

• Latvia: A universal bank ranked number 2 within lending to private individuals

• Lithuania: A universal bank with an extensive branch network and a top position in rural areas and the public sector

DnB NORD branches in the Baltics

12

Large

corporate 11 %

SME

48 %

Private

individuals 41 %

Lending volumes in Lithuania by segment Q1 2011 EUR 3 171 million

Lithuania: Expecting pick-up in retail market

13

0 %

5 %

10 %

15 %

20 %

25 %

2003 2004 2005 2006 2007 2008 2009 2010

Retail loans Corporate loans Total loans

Market share in Lithuania 2003 - 2010

Definintion large corporate > EUR 50 mill turnover

Lithuania: Customer feedback supports the potential for growth

14

73.6

81

71

78.3

B2B B2C

DnB NORD Industry average

Customer survey index for banking sector in Lithuania 20101

1) EPSI research 2010 2) Survey conducted by Spect-Dive (”Mystery shopping”), December 2010

0 % 50 % 100 %

DnB NORD

Bank 2

Bank 3

Bank 4

Bank 5

2009 2010

99

94

93 94

95

75

92

77

86 69

Mystery shopping ranking Lithuania2

(Top 5 banks 2009 – 2010)

Lithuania: Further develop an already strong position

• Strengthen the position in the five main cities

• Protect the existing strong position in rural areas

• Cross-selling to existing customers

• Target to be number 1 or 2 in selected market segments

15

Large

corporate 5 %

SME

38 % Private

individuals 57 %

Latvia: Second largest financial institution for private individuals

Lending volumes in Latvia by segment 1Q 2011 EUR 2 228 million

16

Market share in Latvia DnB NORD 2002-2010

Definintion large corporate > EUR 50 mill turnover

Latvia: Customer satisfaction increased

17

71.2

74.9

69.8

76.8

B2B B2C

DnB NORD Industry average

Customer survey index for Latvian banking sector 20101

1) EPSI research 2010 2) Mystery shopping, Dorus Ltd, 2010- 2011

0 1 2 3 4

Bank 4

Bank 3

Bank 2

Bank 1

DnB NORD

2011 2010

Mystery shopping ranking in Latvia2 (Top 5 banks, 2010–2011)

Latvia: Increase quality of income

• Capitalise on position as the second largest bank for private individuals

• Focus on cost-efficient operations

• More emphasis on non-lending income

• Competence programme to enhance sales skills

18

Large

corporate 10 %

SME

43 %

Private

individuals 15 %

Leasing

32 %

Estonia: A strong platform for leasing

Lending volumes in Estonia by segment Q1 2011 EUR 372 million

19

Market share DnB NORD 2010

Definintion large corporate > EUR 50 mill turnover

Estonia: Set to grow

• Niche player challenging a consolidated market

• Utilisation of the Group's industry competence

• Increase income from cross-border banking primarily from the Nordic client base

• Re-entry into retail banking to be evaluated

20

Raising the bar in the Baltics

Pick-up in GDP growth

Increased cross-sales and quality of income

Lower write-downs

21

Evaluate organic and structural growth

141

Untapped opportunities

Strong platform

Robust strategy

• Strong track record • Unique distribution power and customer base • Proven industry strategy

• A balanced portfolio • Norway: Four largest cities and selected segments • International: industry strategy • Strengthening position in the Baltics and optimize

integration

• Urbanization and population growth • Increased demand for shipping, energy and

seafood driven by emerging markets growth • Pick up in GDP growth in the Baltics

Well positioned for profitable growth

Financial ambitions towards 2015

Return on equity above 14 per cent

NOK 30 billion in pre-tax operating profits before write-downs

Cost/income ratio below 45 per cent

145