Embed Size (px)

Citation preview

1

CAMRI Global Perspectives Monthly digest of market research & views Issue 41, February 2017

Does Macro Policy Diverge or Converge?

By Brian Fabbri

Visiting Senior Research Fellow, CAMRI & President, FABBRI Global Economics

Policy mavens are advocating divergence

Recently economic commentators and

professional economists have opined that

the Federal Reserve should tighten

monetary policy faster in light of the US

president’s proposed plans to stimulate the

economy through aggressive use of fiscal

policy. Some have even thoughtlessly argued

that the Fed has already begun to tighten

policy because of the president’s promises

to increase fiscal stimulus.

History reveals that the Fed began to raise

interest rates in December 2015 and then

again in December 2016. The FOMC began

advising financial markets of their intent to

raise interest rates in June 2015, long before

anyone dreamed that Mr. Trump would

even run for election. In recent years,

normalizing the level of interest rates at an

appropriate time has long been the Fed’s

major motivation in increasing interest

rates.

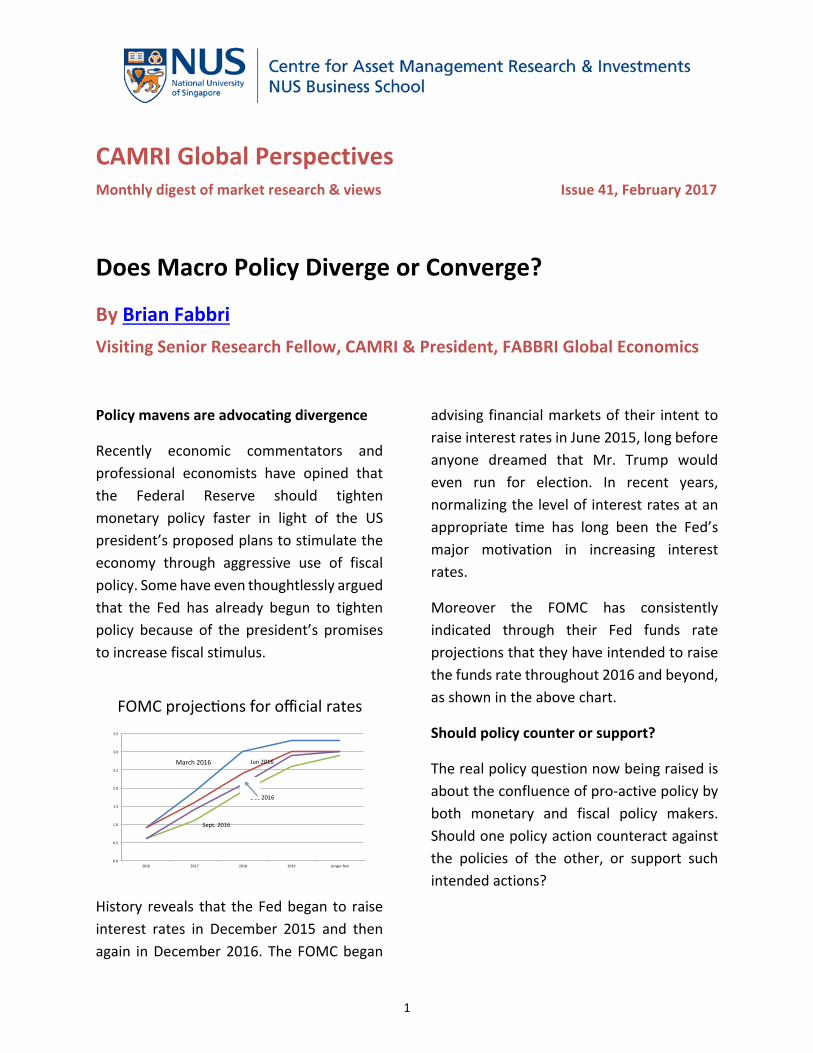

Moreover the FOMC has consistently

indicated through their Fed funds rate

projections that they have intended to raise

the funds rate throughout 2016 and beyond,

as shown in the above chart.

Should policy counter or support?

The real policy question now being raised is

about the confluence of pro‐active policy by

both monetary and fiscal policy makers.

Should one policy action counteract against

the policies of the other, or support such

intended actions?

FOMC projec ons for official rates

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2016 2017 2018 2019 Longer Run

Sept. 2016

Jun 2016

Dec 2016

March 2016

2

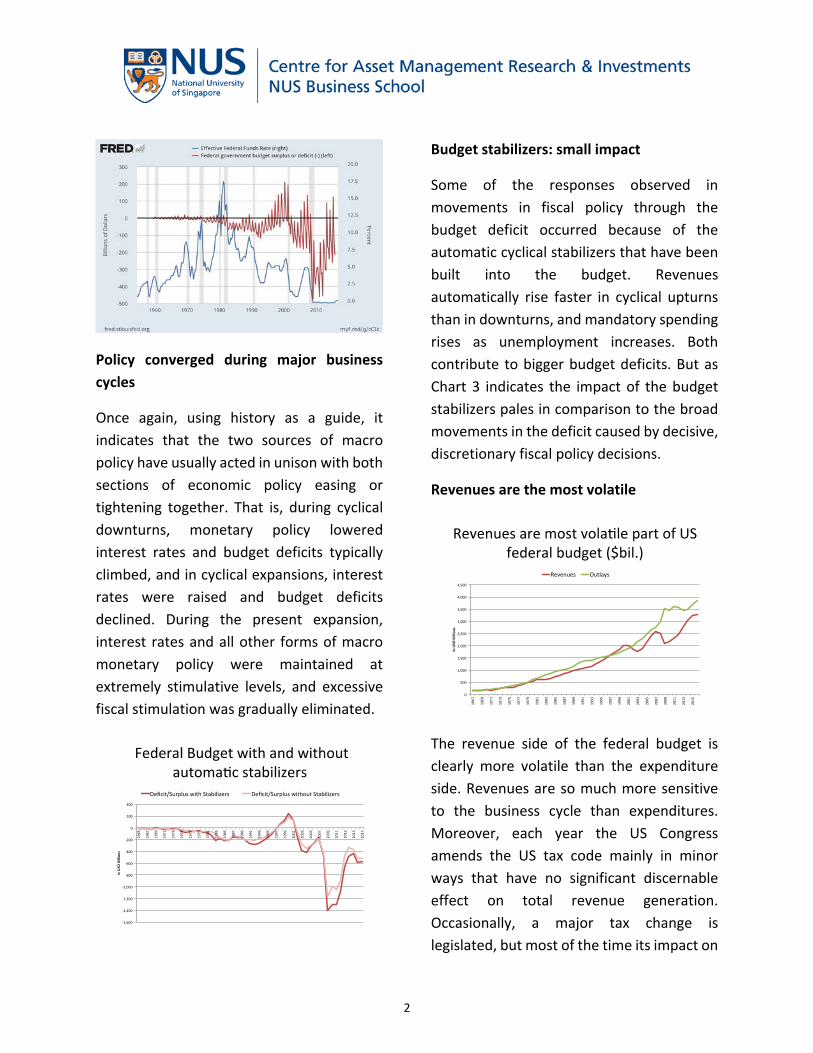

Policy converged during major business

cycles

Once again, using history as a guide, it

indicates that the two sources of macro

policy have usually acted in unison with both

sections of economic policy easing or

tightening together. That is, during cyclical

downturns, monetary policy lowered

interest rates and budget deficits typically

climbed, and in cyclical expansions, interest

rates were raised and budget deficits

declined. During the present expansion,

interest rates and all other forms of macro

monetary policy were maintained at

extremely stimulative levels, and excessive

fiscal stimulation was gradually eliminated.

Budget stabilizers: small impact

Some of the responses observed in

movements in fiscal policy through the

budget deficit occurred because of the

automatic cyclical stabilizers that have been

built into the budget. Revenues

automatically rise faster in cyclical upturns

than in downturns, and mandatory spending

rises as unemployment increases. Both

contribute to bigger budget deficits. But as

Chart 3 indicates the impact of the budget

stabilizers pales in comparison to the broad

movements in the deficit caused by decisive,

discretionary fiscal policy decisions.

Revenues are the most volatile

The revenue side of the federal budget is

clearly more volatile than the expenditure

side. Revenues are so much more sensitive

to the business cycle than expenditures.

Moreover, each year the US Congress

amends the US tax code mainly in minor

ways that have no significant discernable

effect on total revenue generation.

Occasionally, a major tax change is

legislated, but most of the time its impact on

3

total revenue is not intuitively obvious. For

instance, a major tax cut reduces revenue,

but stimulates more economic growth,

which pushes tax revenues upward,

although not necessarily exactly by the same

amounts, nor in the same annual time

periods. However, the divergent effects on

total revenue are muted over time.

Non‐mandatory spending has recently

declined.

Following the years during and immediately

after the great recession discretionary fiscal

policy was extensively used to bail out the

failing parts of the US economy and to

provide financial supports to other sagging

sectors in concert with the Federal Reserve’s

aggressive policies to shore up the weakest

financial institutions. Thus, the two branches

of the government charged with economic

development acted together to support the

economy.

Once the economy regained its footing, fiscal

policy went into retreat and massive budget

deficits contracted, while monetary policy

maintained its highly stimulative policy for

years thereafter, providing the impression

that policy was divergent.

During this period the federal government

chose to reduce spending on all non‐

mandatory items from 2011 onwards.

Spending for defense and non‐defense, non‐

mandatory spending was cutback in order to

help shrink the budget deficit to an

acceptable level. It succeeded in reducing

the deficit to around 3% of GDP for the past

three fiscal years. It had touched 10% at the

height of the ‘great recession’ crisis. As Chart

7 reveals, spending for defense and non‐

defense, non‐mandatory spending has

usually moved in synchronization together.

Budget deficit as % of GDP

‐12.0

‐10.0

‐8.0

‐6.0

‐4.0

‐2.0

0.0

2.0

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

(%) o

f GDP

Budget Deficit % of GDP

‐10.0

‐5.0

0.0

5.0

10.0

15.0

20.0

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

(%)

Non‐Mandatory Spending YoY Non‐Mandatory Spending % of GDP

Federal Non Mandatory spending has declined in recent years

Non Mandatory spending

0

200

400

600

800

1,000

1,200

1,400

1,600

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

In USD

Billio

ns

Nondefense Total nonmandatory

4

Looking into the future

It seems that the President and his new

economic team are intent on stimulating the

economy through fiscal policy. They have

repeatedly stated that they will propose

measures to speed up economic growth. For

example, they plan to reduce federal taxes,

to increase federal spending on

infrastructure, to streamline federal

regulations, and to restrict foreign trade.

Assuming these proposals are sent to

Congress for debate and eventually turn into

congressional acts, economic growth will be

boosted in the next year or two and inflation

will accelerate.

The ball is in the Fed’s court

Since the administration is committed to

stimulate economic growth and suffer

through higher inflation, the critical policy

decision on whether to converge, or diverge

will be made by the Federal Reserve. The

decision will be partially influenced by

politics, but mostly influenced by the state of

the business cycle.

The administration’s economic stimulus will

give the present relatively long expansion

another thrust, however, it will come at a

time when the economy is already at full

employment. More growth in final demand

and higher demands for labor will push

wages higher and propel inflation above the

Fed’s tolerance limits. Consequently, the Fed

will be compelled to tighten monetary

policy.

Higher interest rates are inevitable

Higher inflation, tighter monetary policy,

rising market expectations for future

increases in official policy rates, and larger

demands by the federal government and the

Recently Defense and non defense non mandatory spending moved in tandem

0

100

200

300

400

500

600

700

800

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

In USD

Billio

ns

Defense Nondefense

GDP output gap and Unemployment gap closing

‐6.0

‐4.0

‐2.0

0.0

2.0

4.0

6.0

‐1,000

‐800

‐600

‐400

‐200

0

200

400

600

800

1,000

65

67

69

71

73

75

77

79

81

83

85

87

89

91

93

95

97

99

01

03

05

07

09

11

13

15

17

(%)

In USD

Billio

ns

Unemployment Gap (Right) (%) GDP Gap (Le )

Market expecta ons for future policy rates have soared recently

0

0.5

1

1.5

2

2.5

0 1 2 3 4 5 6

Fed Funds Rate (%

)

Fed Funds Market implied rate

Mar 2016

Jun 2016

Dec 2016

Sep 2016

5

private sector for capital will drive longer

term borrowing rates significantly higher.

Eventually the competition for capital by the

public and private sectors will push some

private sector borrowers out of the market

and this will ultimately lead to the beginning

of the end of this very long business cycle

expansion.

Conclusion: Divergence isn’t inevitable

History reveals that the relationship

between fiscal and monetary macro policies

is very inconsistent. It is theorized that one

should offset the effects of the other to

prevent excessive stimulation, or

contraction. This would be consistent with

the checks and balances form of

government, such as the political structure

organized in the United States.

However, it is also posited by many policy

experts that macro and fiscal policy should

be supportive of one another’s intents

rather than to undermine them. This would

be especially true, if it is the government’s

public pledge to stimulate the economy.

Then, monetary policy should act to

complement that policy. Since the elected

government has the option to choose the

Federal Reserve’s chairman, the two

branches of macro policy making should

eventually be of similar views.

Of course, as we have seen, macro policies

have followed both dictums. The pursuit of

complementary macro policy has always

occurred during economic crisis. For

example, during the ‘great recession’ both

policies adopted similar overwhelmingly

stimulative policies. In contrast, during the

early 1980’s monetary policy was intent on

crushing inflation, and the Fed thus raised

interest rates to punishingly high levels while

fiscal policy adopted a very aggressive

stimulative supply side orientation.

The time to act is now

The new administration has promised to

pursue a complex set of economic policies

that are designed to bolster economic

growth over the next several years. One

countervailing consequence, intended or

otherwise, of their promised policies would

be to increase inflation above acceptable

levels. Since the present status of the

economy is on the cusp of full employment

any new added stimulus would most likely

raise the level of inflation. This should cause

the Federal Reserve to act in a countervailing

manner to respond to the increase in

inflation.

Fortuitously, the state of monetary policy is

considered extremely loose by any historic

standard. Therefore, some tightening is

necessary to return monetary policy back to

neutral. Moreover, it will take some time for

the administration’s new economic pledges

to become effective, and it will be time for

economic participants to react to these new

policies. During this interval the Fed would

be wise to act slowly and purposefully to

shore up its relaxed monetary policy before

6

time makes this tightening action appear

divergent to the administration’s policies.

For more information, please contact

7

KEY INDICATORS TABLE (AS OF 31 JANUARY 2017)

INDEX LEVEL (LC) %1MO (LC)

%1MO (USD)

%1YR (LC)

%1YR (USD)

INDEX LEVEL %1YR

S&P500 2278.87 1.90% 1.90% 20.03% 20.03% 3MO LIBOR 1.03 68.79

FTSE 7099.15 ‐0.57% 1.24% 21.49% 7.37% 10YR UST 2.45 27.71

NIKKEI 19041.34 ‐0.37% 2.83% 10.78% 18.57% 10YR BUND 0.44 34.06

HANG SENG 23360.78 6.18% 6.12% 23.28% 23.69% 10YR SPG 1.60 5.69

STI 3046.80 5.85% 8.57% 20.38% 21.54% 10YR SGS 2.30 1.85

EUR 1.08 2.67% ‐0.30% US ISM 54.50 12.14

YEN 112.80 ‐3.56% ‐6.88% EU PMI 55.10 5.35

CMCI 1186.06 2.32% 29.07% JP TANKAN 7.00 ‐22.22

Oil 52.81 ‐1.69% 57.08% CHINA IP 6.00 1.69

Source: Bloomberg

APPENDIX

GLOSSARY OF KEY TERMS (Source: Bloomberg, with tickers in parenthesis. In US$ where applicable) S&P500: capitalization‐weighted index of the prices of 500 US large‐cap stocks (SPX) FTSE: capitalization‐weighted index of the prices of the 100 largest LSE‐listed stocks (UKX) NIKKEI: capitalization‐weighted index of the largest 225 stocks of the Tokyo Stock Exchange (NKY) HANG SENG: capitalization‐weighted index of companies from the Hong Kong Stock Exchange (HSI) STI:cap‐weighted index of the top 30 companies listed on the Singapore Exchange (FSSTI) EUR: USD/EUR exchange rate: 1 EUR = xx USD (EUR) YEN: YEN/USD exchange rate: 1 USD = xx YEN (JPY) CMCI: Constant Maturity Commodity Index (CMCIPI) Oil: West Texas Intermediate prices, $ per barrel (CLK1) 3MO LIBOR: interbank lending rate for 3‐month US dollar loans (US0003M) 10YR UST: 10‐year US Treasury yield (IYC8 – Sovereigns) 10YR BUND: 10‐year German government bond yield (IYC8 – Sovereigns) 10YR SPG: 10‐year Spanish government bond yield, proxy for EU funding problems (IYC8 – Sovereigns) 10YR SGS: 10‐year Singapore government bond yield (IYC8 – Sovereigns) US ISM: US business survey of more than 300 manufacturing firms by the Institute of Supply Management that monitors employment, production inventories, new orders, etc. (NAPMPMI) EU PMI: Purchasing Managers’ index for the 17 country EU region (PMITMEZ) JP TANKAN: Bank of Japan business survey on the outlook of Japanese capital expenditures, employment and the overall economy, quarterly index (JNTGALLI) CHINA IP: China’s Industrial Production index, with 1‐month lag (CHVAIOY) LC: Local Currency Disclaimer:Allresearchdigests,reports,opinions,models,appendicesand/orpresentationslidesintheCAMRIResearchDigestSeriesisproducedstrictlyforacademicpurposes.Anysuchdocumentisnottobeconstruedasanofferorasolicitationofanoffertobuyorsellanysecurities,norisitmeanttoprovideinvestmentadvice.NationalUniversityofSingapore(NUS),NUSBusinessSchool,CAMRI,theparticipatingstudents,facultymembers,researchfellowsandstaffacceptnoliabilitywhatsoeverforanydirectorconsequentiallossarisingfromanyuseofthisdocument,oranycommunicationgiveninrelationtothisdocument.