Embed Size (px)

Citation preview

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

0

Introduction

In June 2008, the Israeli Insurance Association (R.A) appointed KPMG as their official advisors to the Israeli market in relation the new Solvency II regime being introduced by the Insurance Regulator in Israel. The engagement required that KPMG provide professional support for QIS4 in the form of the following actions:

1. Support the work of the Solvency II Committee with respect to the implementation of the quantitative pillar of Solvency II

2. Enable insurance companies to ask questions throughout the QIS4 exercise

and provide timely expert answers

3. Evaluate spreadsheets by insurance companies on behalf of the Committee This document outlines KPMG’s answers to questions posed by the insurance companies. As part of the introduction, it is felt important to explain the process by which the questions arrived to KPMG and the manner in which they have been tackled. After the announcement that Israel is to take up the Solvency II Regulation, four committees were established to deal with the various areas that will be affected by the new rules:

Credit Market

General Insurance

Accounting

Life and Health After a number of meetings, the heads of the committees and in some cases committee members submitted questions either through Magie Braun of the Ministry of Finance, or directly to a member of the Somekh Chaikin ……………. These questions were then collated, translated where necessary, and sent to the various KPMG experts who have been appointed to support the above action points. Once all questions were answered, each was reviewed for accuracy and consistency with the other answers and changes were made where necessary.

Introduction Introduction

ABCD

Draft Response

to the Solvency II Committee

February 2009

Version 2.0

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

1

Introduction In June 2008, the Israeli Insurance Association (R.A) appointed KPMG as their official advisors to the Israeli market in relation the new Solvency II regime being introduced by the Insurance Regulator in Israel. The engagement required that KPMG provide professional support for QIS4 in the form of the following actions:

1. Support the work of the Solvency II Committee with respect to the implementation of the quantitative pillar of Solvency II

2. Enable insurance companies to ask questions throughout the QIS4

exercise and provide timely expert answers

3. Evaluate spreadsheets by insurance companies on behalf of the Committee

It is with this therefore that we are pleased to present this initial draft of our answers for the remarks of the committee.

Please find following the questions received from Mrs. Magie Braum on behalf of the Solvency II Committee and the answers according to the common practice as at December 2008. Before releasing this document to the market, it was reviewed by Mrs. Magie Braum and her team.

Note on Abbreviations

We have included a list of abbreviations and their meanings. This can be found on the following page. Please note that full definitions of these and other terms can be found in the Solvency II Glossary accompanying this response.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

2

Abbreviations (in Order of Use) Abbreviation Meaning

QIS Quantitative Impact Study

EU European Union LGD Loss Given Default BE Best Estimate SCR Solvency Capital Requirement CEE Central and Eastern Europe RM Risk Margin OECD Organization of Economic Co-operation and Development EEA European Economic Area CEIOPS Committee of European Insurance and Occupational Pensions ORSA Own Risk Solvency Assessment VaR Value at Risk VIF Value in Force VNB Value of New Business ASM Available Solvency Margin PVFP Present Value of Future Profits EV Embedded Value PD Probability of Default CDO Collateralized Debt Obligation CDS Credit Default Swap SPV Special Purpose Vehicle MBS Mortgage Backed Security AMC Asset Management Company LoB Line of Business LR Loss Ratio IEULR Initial Expected Ultimate Loss Ratio GAAP Generally Accepted Accounting Principles CoC Cost of Capital IFRS International Financial Reporting Standards LTC Long Term Care PHI Permanent Health Insurance CIC Critical Illness Cover ICA Individual Capital Assessment

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

3

Table of Contents

General ....................................................................................................... 6

Correlations of primary risk and secondary risk categories ...................................... 7

Counterparty default risk ................................................................................................. 8

Credit & Market Risk ................................................................................. 9

Participating policies ...................................................................................................... 10

Pre-1991 Israeli guaranteed-return life assurance policies ..................................... 12

Spread risk and market concentration risk ................................................................. 13

Determination of extreme scenarios – part 1 ............................................................. 14

Determination of extreme scenarios – part 2 ............................................................. 15

Embedded value ............................................................................................................ 16

Inflation risk…… ............................................................................................................. 17

Interest rate risk – part 1 ............................................................................................... 18

Interest rate risk – part 2 ............................................................................................... 19

Spread risk…… .............................................................................................................. 20

Property risk……… ........................................................................................................ 21

Equity risk…………. ....................................................................................................... 22

Counterparty default risk ............................................................................................... 23

Classification of debt instruments for the spread and counterparty model. .......... 24

Investment funds ............................................................................................................ 26

General Insurance ................................................................................... 28

Line of business classification ...................................................................................... 29

Correlations between lines of business ...................................................................... 30

Database for the period of the actuarial calculation ................................................. 31

Standard deviation ......................................................................................................... 34

Risk of catastrophe ........................................................................................................ 35

Adjustment to catastrophe risk ..................................................................................... 36

Use of internal models ................................................................................................... 37

Adjustment to standard factors .................................................................................... 40

Appropriateness of market factors .............................................................................. 42

Market factor confirmation for CMBI ........................................................................... 43

Definition of “Best Estimate” ........................................................................................ 45

Calculation of the risk margin ....................................................................................... 46

Catastrophe risk factors ................................................................................................ 49

Underwriting risk module .............................................................................................. 50

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

4

Accounting ............................................................................................... 51

Insurance groupings ...................................................................................................... 52

Data requirements for Solvency I ................................................................................ 53

Fair value calculation ..................................................................................................... 54

Currency for reporting .................................................................................................... 55

Goodwill…………. .......................................................................................................... 56

Life and Health ......................................................................................... 57

Use of EV assumptions for QIS4 ................................................................................. 58

Operational Risk ............................................................................................................. 59

Alternative information ................................................................................................... 60

Calculation of “Best Estimate” ...................................................................................... 61

Grouping of contracts .................................................................................................... 62

Life mortality scenario .................................................................................................... 63

Catastrophe risk ............................................................................................................. 64

Classification of business lines for life and health .................................................... 65

Approval of premium increases ................................................................................... 66

Hedgeable contracts ...................................................................................................... 67

Counterparty default risk ............................................................................................... 68

Recoverables .................................................................................................................. 69

Taxation…….. ................................................................................................................. 70

Best estimate for special risks ...................................................................................... 71

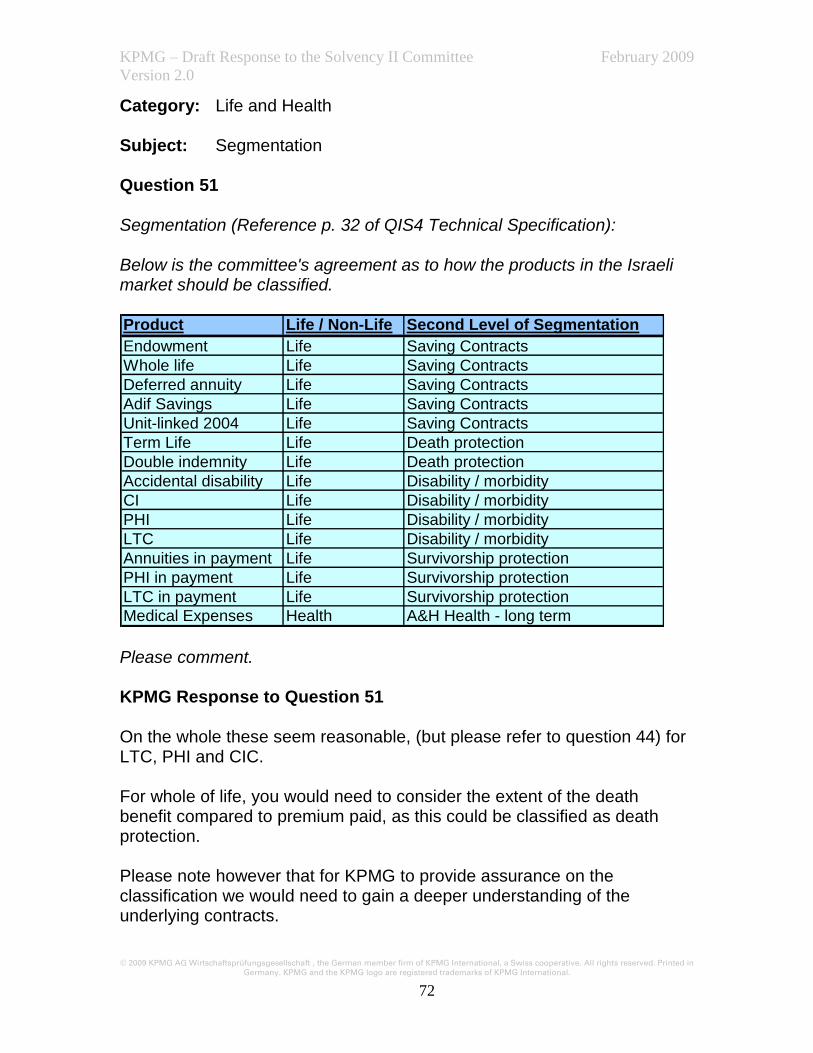

Segmentation .................................................................................................................. 72

Comments on worked example ................................................................................... 73

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

5

Response from Ministry of Finance ...................................................... 74

Re: Question 1 ................................................................................................................ 75

Re: Question 3 ................................................................................................................ 76

Re: Question 4 ................................................................................................................ 78

Re: Question 7 ................................................................................................................ 80

Re: Question 8 ................................................................................................................ 81

Re: Question 10 .............................................................................................................. 82

Re: Question 17 .............................................................................................................. 83

Re: Question 18 .............................................................................................................. 84

Re: Question 22 .............................................................................................................. 85

Re: Question 23 .............................................................................................................. 86

Re: Question 27 .............................................................................................................. 88

Re: Question 31 .............................................................................................................. 89

Re: Question 37 .............................................................................................................. 90

Re: Question 39 .............................................................................................................. 91

Re: Question 40 .............................................................................................................. 92

Re: Question 43 .............................................................................................................. 93

Re: Question 45 .............................................................................................................. 94

Re: Question 47 .............................................................................................................. 95

Re: Question 48 .............................................................................................................. 96

References: .............................................................................................. 97

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

6

General

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

7

Category: General Subject: Correlations of primary risk and secondary risk categories Question 1

a) Are there countries who defined different correlations between primary risk categories and secondary risk categories? If so, please indicate the newly established correlations and the reasons for the change.

b) Please pay special attention to the correlation between life

assurance business and general insurance business. In Israel a large proportion of companies deal in both areas. For countries in which insurance companies are authorized to deal in both sectors, were the correlations set down in QIS4 taken into account or were they changed?

KPMG Response to Question 1

a) We do not know of any countries that have defined different correlations between primary and secondary risk. Generally the correlations cannot be adjusted and are set so that a standard and consistent approach is applied across the EU, but comments on the appropriateness of them are welcome (i.e. via the factors that have been used within a company's internal models). These comments are then used to calibrate the standard formula factors should it be required.

b) Again no changes have been made and the correlations between Life and General Insurance as set down in QIS4 were used, but appropriateness of these can be commented upon also.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

8

Category: General

Subject: Counterparty default risk Question 2 To our understanding of the counterparty default risk, the capital savings and the expected loss must be taken into account in the framework of the Loss Given Default (LGD) calculation and the expected loss should be taken into account in the framework of the Best Estimate (BE) calculation of the recoverable from reinsurance contracts (see p.22 & p.23 of the QIS4 Technical Specification). We request your treatment of the issue. KPMG Response to Question 2 KPMG agrees with your understanding. For the counterparty default risk, you are trying to calculate the reinsurance default risk charge under the stressed scenario, should your gross claims reach the 99.5 percentile level, i.e. the reinsurance recoverable if gross claims reach the 99.5 percentile level (£X). To calculate this default risk charge, the £X will need to be allocated to each counterparty (i), and the relevant probability of default applied. Under the QIS4 LGD calculation, in principle one has to calculate both the gross and net BE, with the difference being the BE of reinsurance recoverable (£Y). Then under QIS4, the underwriting SCR (Solvency Capital Requirement) is calculated for both gross and net, the difference between them being the underwriting reinsurance SCR (£Z). So the LGD is (Y+Z) = X. This is calculated, for each counterparty (i). The factor of 50% takes into account the fact that even in case of default the reinsurer will usually be able to meet a larger part of its obligations.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

9

Credit & Market Risk

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

10

Category: Credit & Market Risk

Subject: Participating policies Question 3 In Israel there exist participating policies (i.e. in investment profits), which do not contain embedded options or guarantees. In these policies, it is the policyholder who bears the investment risk (similar to unit-linked) Until 2004, fixed management fees (0.6% of assets) and variable management fees which are a function of the return (company participation in 15% of the investments) were customary in policies of this type. 1.

a) What is the treatment of policies in which the investment risk is imposed upon the policyholders of the type customary in Israel for each of the market risk models? (It should be noted that in models relating to the spread risk and concentration risk only, there is specific treatment to unit linked policies which contain embedded options and guarantees. We request your treatment of this type as well).

b) What is the method of treating the risks deriving from the profit-participation (for policies with variable management fees)?

2. We request a survey of the treatment methods, in various countries, of unit-linked type policies, where policies similar to those in Israel are customary.

KPMG Response to Question 3 A capital charge for market risk is not required in relation to investment risk for policies where the investment risk is transferred to the policyholder. However, if under these policies a management charge is levied, then companies have a negative reserve (i.e. the expected future management fees, assuming no death benefit payable in excess of return of funds). So companies have to consider, under the stressed market risk components, what the impact on the future management fees is likely to be, for this reduction in future fees is set up as an additional capital charge under the

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

11

Question 3 (continued) market risk component. The key risks for the unit-linked products are market risk (to a lesser extent, arising from the reduction in the fees the issuer of the policy is receiving when there is a fall in the value of the assets backing the unit-linked policies), and expense risk (to a larger extent). Lapse risk needs to be considered through operational risk in a unit-linked product as one should expect, for example, higher lapses when the issuer of the policy gets the unit price wrong to the public. Sensitivity testing on lapse risk is quite common in the UK, but not so in countries located in Central and Eastern Europe (CEE) (e.g. Romania). A possible approach is to test for shocks to market risk, expense risk and the lapse risk, and to test under various scenarios the operational risk. Where policies have either a guaranteed minimum death benefit or a minimum investment return option, the impact of these options on the likely future benefits to the policyholders are considered under each of the market risk stress tests. If under the stressed conditions these options bite then a capital charge is set up equal to the value of the option under the stressed situation. Under with-profit polices, the situation is similar. Companies calculated their insurance liability on a realistic basis (expected future payments, except in Germany where only guaranteed contractible obligations are taken into account), so under the market risk stress tests the impact on any variable management fees would be considered and any reduction set aside as an additional capital charge. Additionally, the net asset movement (assets less liabilities) is adjusted for any anticipated reduction in future profit share (in-so-much as allowed for within the insurance liability above).

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

12

Category: Credit & Market Risk

Subject: Pre-1991 Israeli guaranteed-return life assurance policies Question 4 Until 1991, guaranteed-return life assurance policies issued in Israel were backed by unquoted Government-issued bonds, bearing excess yield compared with the return guaranteed by the policy. The designated bonds fully backed the company’s liability for the guaranteed return until the company’s liability ceased. We request a clarification of how to treat such bonds in all of the models. KPMG Response to Question 4 This has not been seen in the EU, but KPMG’s thoughts are that one needs to follow the accounting treatment. The actual treatment will depend on the relationship between contractual liability under the insurance contract and the return from the unquoted Government bonds. If the contractual liabilities are directly linked to the return on the bonds, then the liability under the insurance contract can be treated as a hedgeable liability and one does not need to calculate a BE plus a Risk Margin (RM). The market risk component for the bonds would then not need to be calculated as the asset less liability would be zero. However, if there is a liability floor under the contact (i.e. Liability at time t > Assets at time t under certain scenarios) then a capital charge needs to be calculated when the floor bites. If the situation is such that the contractual liability is not linked to the return on the bond (i.e. it is a non-hedgeable risk), then a BE + RM needs to be assessed. Additionally the resulting capital charge has to be allocated under the insurance risk. On the market risk side, it would need to be treated as a bond (i.e. interest rate risk) with the market value as per in the accounts (if fair value). One then also needs to consider the spread risk and concentration risk assuming the Government credit rating, if these are guaranteed by the Government though unquoted.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

13

Category: Credit & Market Risk

Subject: Spread risk and market concentration risk

Question 5 The State of Israel is rated at international rating A. We would like to know, in countries rated similar to Israel or lower, were Government bonds treated similarly to the treatment method in countries rated AAA (for example, were they excluded from concentration risk and spread risk)? KPMG Response to Question 5 For both concentration and spread risk calculations, Government bonds are exempt. This relates to borrowings by the national Government, or guaranteed by the national Government, of an OECD or EEA state, issued in the currency of the Government. Currently there are 30 members of the OECD (Israel is not a full member - they have been invited to discussion for membership). For Government bonds not exempt, allowance for the credit rating will need to be applied. For Israel this is likely to mean assuming an “A” rating. Generally, companies have applied this rule in their calculations.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

14

Category: Credit & Market Risk Subject: Determination of extreme scenarios – part 1 Question 6 Are the extreme scenarios under QIS4 fixed over time? If not, are they updated according to a fixed timetable or as a reaction to specific events? Who is the updating party, CEIOPS or the local regulator? KPMG Response to Question 6

1. Nothing definitive has been stated, but KPMG’s view is that:

a) The extreme events would be intended to be largely fixed over time (to prevent arbitrary changes). However, this would not be a permanent fix. As we are looking at extreme tail events, it should be fairly hard to identify new extremes, but clearly external events can occur to change our understanding of the extremities (for example, Sept. 11 changed our views on correlations and the current credit crisis identified a run on a bank as a bigger risk). It is our view therefore that this will always be more of an 'in response to' type review, rather than a review at fixed intervals.

b) As to who would do it! The current thinking is that it would work

similarly to the initial list of catastrophe risks, in that regulators would identify their own changes and CEIOPS would then issue a summary. This seems consistent with the way catastrophe risks are handled within QIS4. Since there might be scenarios having specific impact on individual insurance companies there should be the possibility that insurance companies also add their "own" scenarios, but through the ORSA requirements if not initially within the standard formula.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

15

Category: Credit & Market Risk Subject: Determination of extreme scenarios – part 2 Question 7 What is the manner of calculation of the extreme scenarios under each of the models? Please address the holding periods and whether the average is taken into account in the framework of the calculation of the Value at Risk (VaR)? KPMG Response to Question 7 Generally, the SCR calculations are made either on an extreme scenario or a factor basis. These have been attained by considering data from a few European insurers (i.e. insurance risk) and either modeling these to obtain the capital charge at a 99.5 percentile to obtain a factor to gross up the Best Estimate to the 99.5% level, or economic scenario generators to obtain the factor (32% for equity) or scenarios over historical averages. With regards to Catastrophe risk there are three methods:

1. Calculated as per the factor calculation, 2. Standard scenarios from local regulators, and

3. Company specific scenarios, (though there is potential for double

counting as averages are not deducted). In obtaining the scenarios, or factors, how long the assets or liabilities will be held for, has not been considered, as assets are valued on a market consistent economic basis and liability provisions implicitly allow for the duration.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

16

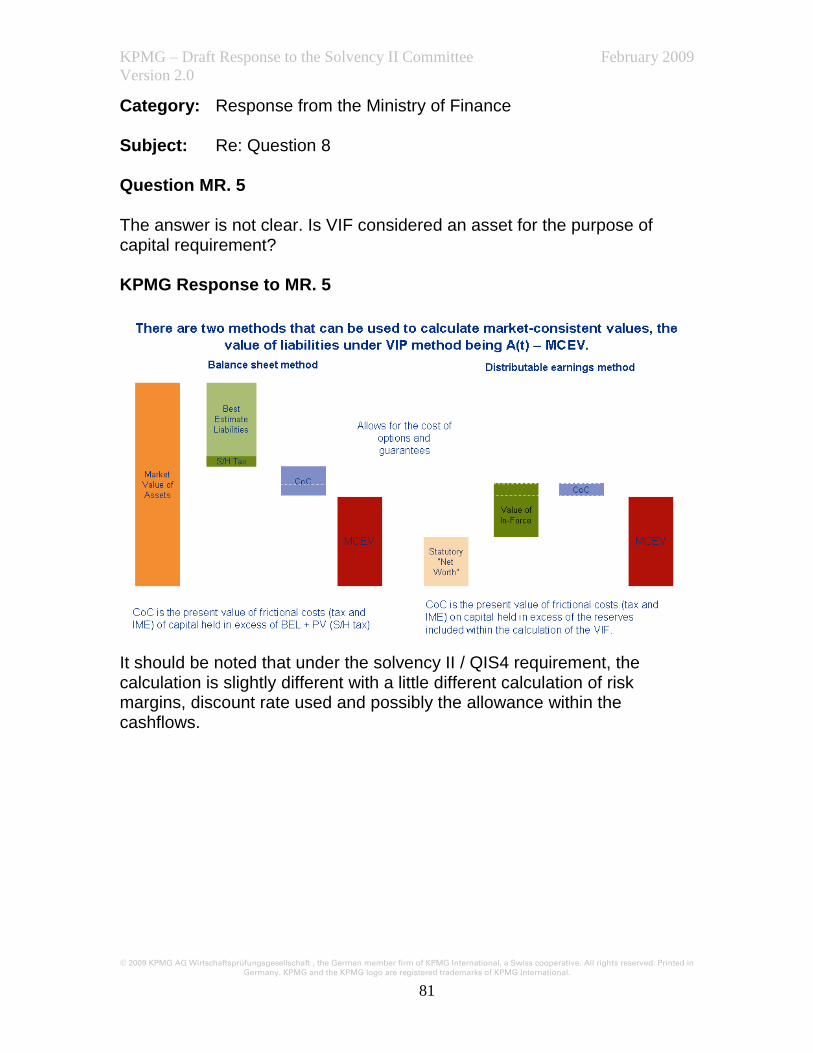

Category: Credit & Market Risk Subject: Embedded value Question 8 How is the Embedded Value (EV) taken into account in the framework of the calculation (please address Value-In-Force (VIF) and Value of New Business (VNB))? KPMG Response to Question 8 Generally, companies have calculated the cash-flows on a best estimate basis for all the business in-force and discounted at the swap rates within QIS4. But you may regard the Available Solvency Margin (ASM) as a form of Embedded Value. (Within Market consistent embedded value in effect the calculation is made up of BE + RM, with the RM containing effectively an allowance for ASM). Of course under the solvency requirement, the calculation is slightly different from that under QIS4 (with a little different calculation of risk margins etc., and no differentiation between net asset value and Present Value of Future Profits (PVFP), or VIF, if you like, and same with the discount rate used and possibly the allowance within the cashflows).

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

17

Category: Credit & Market Risk Subject: Inflation risk Question 9 How was inflation risk dealt with in various countries? KPMG Response to Question 9 Companies have generally built in an allowance for inflation (at the appropriate level, on an expected value) within the cash-flow calculations as outlined in section TS.II.B.9. of the QIS4 Technical Specification. However, there is no specific inflation risk calculation except for expense risk. If inflation risk allowance needs to be made but the QIS exercise (and hence standard formula) has no such allowance within the relevant component then no allocation generally has been made by companies, but they have commented accordingly. Under the solvency II regime this would need to be considered within the ORSA requirements and an additional risk charge calculated and the SCR adjusted accordingly. In countries located in CEE, inflation is assumed to be dealt with implicitly by projecting the claims. However, inflation could be added explicitly to the claim cohorts, for example a loading factor of 10% per annum. When dealt with implicitly however, one could apply a shock of 1% per annum to the claim amounts as a shock test for inflation in the claim cohorts (in line with expense risk as explained), i.e. a 10% shock to inflation per annum. However this would not remove the need to consider this risk under the ORSA requirement. KPMG are aware that in Israel, life insurance premiums for long term business are mostly linked to the cost of living and therefore the expense loading included in the premium will also be linked to the cost of living creating some kind of buffer against inflationary risks.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

18

Category: Credit & Market Risk Subject: Interest rate risk – part 1 Question 10 Is the market stated in percentage points (absolute) or as a percentage of the interest? KPMG Response to Question 10 The up and down shocks are movements to the relative swap risk free curve, i.e.: rfr * (1+shock). Where rfr = risk free rate

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

19

Category: Credit & Market Risk Subject: Interest rate risk – part 2 Question 11 In section TS.IX.B.9 of the QIS4 Technical Specification, it is written that the calculation should be made for assets and liabilities whose cash flows are not influenced by interest rate changes. Is the intent that the calculation be made only for assets / liabilities bearing fixed and not variable interest? KPMG Response to Question 11 This simplification may be used for assets, non-life technical provisions and other liabilities but should not be used for the life technical provisions. It can therefore be used for assets and liabilities bearing variable interest. However, the condition to be met for using the simplification is that the cash-flows of the item are not interest rate sensitive. In particular, the item has no embedded options.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

20

Category: Credit & Market Risk Subject: Spread risk Question 12 In non-AAA rated countries, were adjustments made to the F rating and the G rating? KPMG Response to Question 12 No adjustments have been made when considering the credit risk on Government bonds, but the applicable international rating has been used.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

21

Category: Credit & Market Risk Subject: Property risk Question 13 We request a clarification as to the meaning of indirect “exposures”.

1. To our understanding the model addresses exposure through companies with direct holdings in real estate only and without leverage.

2. To our understanding leveraged companies and venture capitalists

are dealt with using the equity method. KPMG Response to Question 13 This is correct.

1. Participations in real estate companies shall be treated as property as they only give rise to property risk.

2. If the real estate company takes out loans in order to leverage its

investments in properties, the participation should be treated as equity.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

22

Category: Credit & Market Risk Subject: Equity risk Question 14 Which countries used a “Global” classification for the local stock market and which countries used the “Other” classification? Further, did any countries determine a different rate for “Global” and “Other” from that set in the QIS4 Technical Specification? Finally, if you have a calculation of the extreme scenarios of such markets, please could you provide us with it? KPMG Response to Question 14 The classification of “Global” and “Other” is fairly well defined within QIS4, i.e.:

“Global” comprises equity listed in EEA and OECD countries, and

“Other” comprises equity listed only in emerging markets, non-listed equity, hedge funds and other alternative investments.

All the countries have used these classifications dependent on the underlying investments, e.g. equities on the Israeli market (as non-OECD) would be in the “other” class. Within QIS4 the factors 32% and 45% cannot be adjusted but comments on their appropriateness are welcome. With regards to an example, unfortunately we are unable provide one due to data protection, however if you require us to create one, we will be happy to do so.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

23

Category: Credit & Market Risk Subject: Counterparty default risk Question 15 Was an adjustment to the probability of default made, or another method of calculation determined in the calculation of the exposure to credit risk of re-insurers or counterparties residing in countries rated lower than AAA (rated by a local rating and not an international rating)? KPMG Response to Question 15 Generally, we have not seen this as yet, and the recent CEIOPS paper didn’t make note of anything. However, generally we believe that if the local rating is consistent with that internationally, then that rating and the associated PD would be applied. Where the local rating is not consistent, either, one can request this from rating agencies such as Standard & Poors, Moody’s etc. (who publish PD and LGD estimates based on their statistics), or the lower of the two ratings (country or entity) could be used as a conservative estimate.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

24

Category: Credit & Market Risk Subject: Classification of debt instruments for the spread and

counterparty model. Question 16 We request a clarification of the manner of classification of debt instruments for the two models, the manner of their treatment and these issues:

a) To our understanding re-insurers, market derivatives, and counterparties to securitization carried out by the company are handled under the counterparty model, while bonds (including those of non-OECD governments) CDO’s and CDS’s are handled under the spread model.

b) To which model should mortgage-banked loans, loans backed by life

assurance policies and loans to agents backed by flow of future fees be classified?

c) To our understanding, in the counterparty model, the net exposure

less collateral should be considered. Collateral should be considered in the framework of the relevant models. Please clarify which types of collateral are intended.

KPMG Response to Question 16

a) According to TS.IX.F.9 spread risk comprises of spread risk from bonds, structured credit products and credit derivatives. This includes CDO’s and CDS’s etc. Spread risk covers any financial instruments whose value is affected by interest rate spread above the risk free rate. Compared to counterparty risk which examines the likelihood of default by the counterparty independent of the effect of interest rate on the value of the underlying financial instrument. In particular, securitization is in reference to SPV.

b) MBS’s are usually through an SPV so they should be accounted for

by counterparty risk. However, the spread on these securities are sensitive to interest rates. The latter two loans involve a

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

25

Question 16 (continued)

counterparty, so KPMG’s view is that these should be accounted as counterparty risk.

c) This is defined in TS.VII.I and states "A collaterised transaction is

one in which insurers have a credit exposure or potential credit exposure and it is hedged in whole or in part by collateral posted by a counterparty or by a third party on behalf of the counterparty”.

In addition to the general requirements for legal certainty, the legal mechanism by which collateral is pledged, or transferred must ensure that the insurer has the right to liquidate or take legal possession of it in a timely manner, in case of any event of the counterparty set out in the transaction documentation (and, where applicable, of the custodian holding the collateral). Insurers must have clear and robust procedures for the timely liquidation of collateral to ensure that any legal conditions required for declaring the default of the counterparty and liquidating the collateral are observed, and that collateral can be liquidated promptly. Generally, this means a security or guarantee (usually an asset) pledged for the repayment of a loan if one cannot procure enough funds to repay.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

26

Category: Credit & Market Risk Subject: Investment funds Question 17 Please provide examples of the manner of treatment of investment funds under the look-through approach and of the manner of treatment of investment funds where it is not possible to carry out the look-through approach. KPMG Response to Question 17 Where we have seen the look-through approach being applied is where an insurance company has used, either a sister company, or 3rd party Asset Management Company (AMC) to handle their investment portfolio. These are mainly structured under an investment mandate (legal contract) being put in place, which outlines the type, exposure, duration and volume under each asset category, but usually not the actual asset to be invested in. Depending on the level of reporting agreed with the AMC, participants would either look through to the underlying individual assets or attribute on a best effort basis depending on the investment mandates in place. The other investments that are seen are investment funds or mutual funds which companies had invested, which concentrate either in a specific area of the investment market (i.e. UK small companies, etc) or a general spread of asset classes / territories. For these, if the participants have been able to obtain details of the underlying individual assets then these have been used, but generally this is not available. Here, participants have considered the collective investment fund as an equity investment and applied the global equity risk charge (if the assets within the collective investment scheme are predominately listed in EEA or OECD entities), or the other risk charge (if the assets within the collective investment scheme are predominately unlisted or outside the EEA and OECD). If this was not feasible, the exposure has been attributed on a best effort basis. Furthermore this could be waived if the mutual fund solely invests in European equities with no special individual hedging instruments for

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

27

Question 17 (continued) example. Then it is possible to consider the equity fund as a single equity for the output calculation.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

28

General Insurance

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

29

Category: General Insurance Subject: Line of business classification Question 18

1. How did countries handle the classification of products where the sector classification does not match the classification under QIS4?

2. What was the practice in countries that have no-fault compulsory

motor vehicle insurance? KPMG Response to Question 18 Most of the countries have regulatory returns which are very explicit about classification of business and these have been used. Where there has been an issue, most companies have either asked the local regulator for clarification or looked at the nature, term and volatility of the claims and assigned to a particular class. If a good match has not been available, companies have generally included them in the “other” class explaining why. No adjustments have been made to the factors but comments have been made as to what would be appropriate.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

30

Category: General Insurance Subject: Correlations between lines of business Question 19 Are there countries in which the correlations established were different from the average in QIS4? KPMG Response to Question 19 We do not know of any countries that have used different correlations from the average as stated within the QIS4 outline. The factors have been set in QIS and are there to check the appropriateness of such. CEIOPS are looking at whether the correlations and other factors produce, in aggregate in the EU, reasonable but conservative capital requirements. The aim is for the standard formula to be calibrated to be about 20% to 40% higher than internal models.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

31

Category: General Insurance Subject: Database for the period of the actuarial calculation Question 20 Presently in the liability sector in Israel, most companies calculate the contingent claims on the basis of underwriting year. The QIS4 requirement however is to calculate the contingent claims on the basis of year of damage. Please address the following issues:

1. Are there countries in which it was decided to integrate a calculation on the basis of year of damage and on the basis of underwriting year, according to the method practiced in that country?

2. In cases in which adjustments were made according to underwriting

year, how were the adjustments made with respect to the premium risk, and specifically in dealings not yet signed (in addition to unearned premium)

3. How are companies that account on an underwriting year basis,

dealing with the requirements of section TS.XIII.B.12 of the QIS 4 Technical Specification?

In addition, how do these companies divide the reserve risk between outstanding claims (claims provisions) and unexpired risk (premium provisions) as different factors apply to the different elements?

KPMG Response to Question 20

1. What we have seen a number of Lloyd’s syndicates do, is carry out the calculation on an underwriting year basis and then convert these figures to those required under QIS4. Section TS.II.E.10 of the QIS4 Technical Specification allows companies to ".....use of claims data on an occurrence / accident year basis or an underwriting year basis for the run-off triangles." QIS4 has requested comments / feedback on this matter.

2. The conversions of underwriting figures to earned and unearned

(plus pipeline premium) has been generally to use the underwriting ultimate loss ratio and has been applied to the earned premium. The

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

32

Question 20 (continued)

other methods that have been seen is to consider the expected LR applicable to the unearned + pipeline premium (i.e. IEULR) and then take the balance to the reserve risk, adjusting the underwriting payment pattern to obtain the earned duration of reserves.

3. All companies need to comply with the requirement; however, QIS4

does welcome feedback / comments on the difficulty of moving from an underwriting year basis.

Europe Some undertakings commented that applying the model seems to be easier when using accounting designed on an accident year basis, or conversely raises practical difficulties for undertakings with accounting systems based on underwriting years. Comments on the difficulties encountered were mainly developed by one supervisor. The problems identified were as follows:

1. Resource intensive - many undertakings commented that while an underwriting year basis can theoretically be converted to an accident year basis, this is difficult in practice as there are many years of account, lines of business, territories and currencies. This exercise was time consuming, requiring a considerable amount of effort; consequently, the information was provided on an underwriting year basis.

2. Underwriting year and local GAAP - undertakings that use an

underwriting basis but publish accounts on a local GAAP basis with differing assumptions stated that the requirements of Solvency II raise a number of new difficulties:

a) Historical loss ratios on an accident year basis will only be

available from the date GAAP accounting was introduced in the undertaking. This may not be a sufficiently long enough period to easily use undertaking-specific parameters.

b) Underwriting year reserves are split between earned and

unearned proportions. This approach implicitly uses the same

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

33

Question 20 (continued)

loss ratio for the earned / unearned portion, but in practice the best estimate loss estimates for the earned / unearned split will be different. Therefore an assumption will have to be made.

c) For discounting purposes, in theory a different run-off pattern

should apply to claims provisions (earned) and the premium provisions (unearned). These run-off patterns are not directly available because claims data on an accident year basis is not collected.

The main conclusion of this supervisor is that providing data on an accident year basis would involve large costs for undertakings accounting for their business on an underwriting year basis if it became a requirement under Solvency II.

Example: German country report

No difficulties have been reported. The QIS4 approach appears to be appropriate to the German market.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

34

Category: General Insurance Subject: Standard deviation Question 21 Are there countries where the standard deviation for premium risk and reserve risk were updated based on local experience? How was the standard deviation calculated, and (as the deviation was calculated according to large companies) was additional conservatism for use of such deviation taken into account for small companies as well? KPMG Response to Question 21 Generally, companies have not updated standard deviations, but have commented on their appropriateness in their case. According to QIS4 a company specific calculation can be done but only in accordance with the formula specified in section TS.XVII.D. of the QIS4 Technical Specification.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

35

Category: General Insurance Subject: Risk of catastrophe Question 22 What is the definition of catastrophe in each sector? Does it relate to the effect of multiple independent events on the level of retention of the company? KPMG Response to Question 22 In relation to catastrophe risk, if regional scenarios are available, provided by the local supervisor (the supervisor of the relevant territory, not necessarily the

insurer's own supervisor), they replace the standard formula of method 1. Regional scenarios include natural and man-made catastrophes. In addition, undertakings may, on an optional basis, use personalized catastrophe scenarios according to the classes of business written and geographic concentration, explaining the appropriate definition for the calculation purposes (method 3). To reflect the effect of multiple independent events on the level of retention of the company, the QIS4 participants will have to use either, scenarios provided by the local regulator, or personalized scenarios on an annual basis.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

36

Category: General Insurance Subject: Adjustment to catastrophe risk Question 23 Since the compulsory motor insurance branch in Israel is no-fault, what adjustments were made to the catastrophe risk in countries in which the same definition exists? In the motor vehicle property branch, there is an option in Israel to purchase insurance against earthquakes, but such insurance is virtually never purchased. Were adjustments made in countries in a similar situation and what were the considerations for making or not making the adjustments? KPMG Response to Question 23 One of the more sophisticated approaches was used in Germany where a specific formula was developed to estimate natural hazard risk in motor comprehensive insurance. Details are available in the guidance notes, however this does not include earthquake. A more relevant example is Portugal where an earthquake scenario has been suggested by the regulator, resulting in an estimated loss of 1.11% of the capital at risk for property insurance policies exposed to seismic perils. This scenario corresponds to an expected 250 year event. Participants are invited to include the estimate of the impact that such an earthquake would have on the other lines of business. Other countries such as France and Belgium have earthquake scenarios affecting all lines of business.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

37

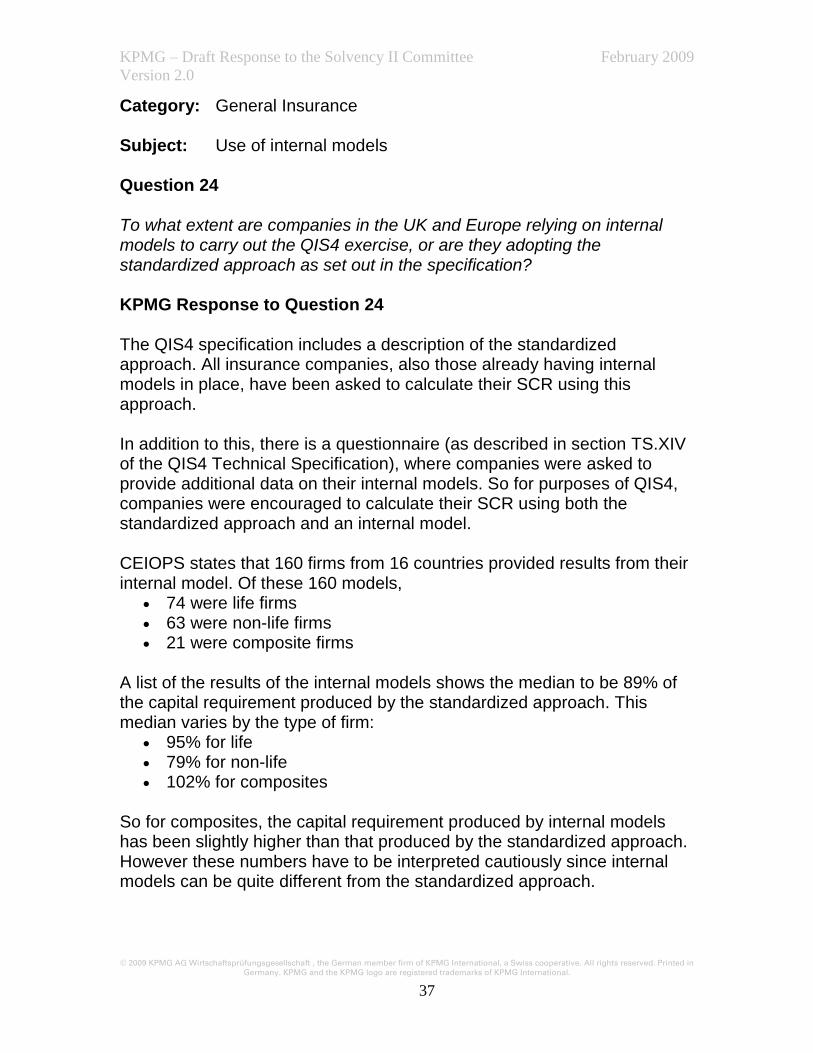

Category: General Insurance Subject: Use of internal models Question 24 To what extent are companies in the UK and Europe relying on internal models to carry out the QIS4 exercise, or are they adopting the standardized approach as set out in the specification? KPMG Response to Question 24 The QIS4 specification includes a description of the standardized approach. All insurance companies, also those already having internal models in place, have been asked to calculate their SCR using this approach. In addition to this, there is a questionnaire (as described in section TS.XIV of the QIS4 Technical Specification), where companies were asked to provide additional data on their internal models. So for purposes of QIS4, companies were encouraged to calculate their SCR using both the standardized approach and an internal model.

CEIOPS states that 160 firms from 16 countries provided results from their internal model. Of these 160 models,

74 were life firms 63 were non-life firms 21 were composite firms

A list of the results of the internal models shows the median to be 89% of the capital requirement produced by the standardized approach. This median varies by the type of firm:

95% for life 79% for non-life 102% for composites

So for composites, the capital requirement produced by internal models has been slightly higher than that produced by the standardized approach. However these numbers have to be interpreted cautiously since internal models can be quite different from the standardized approach.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

38

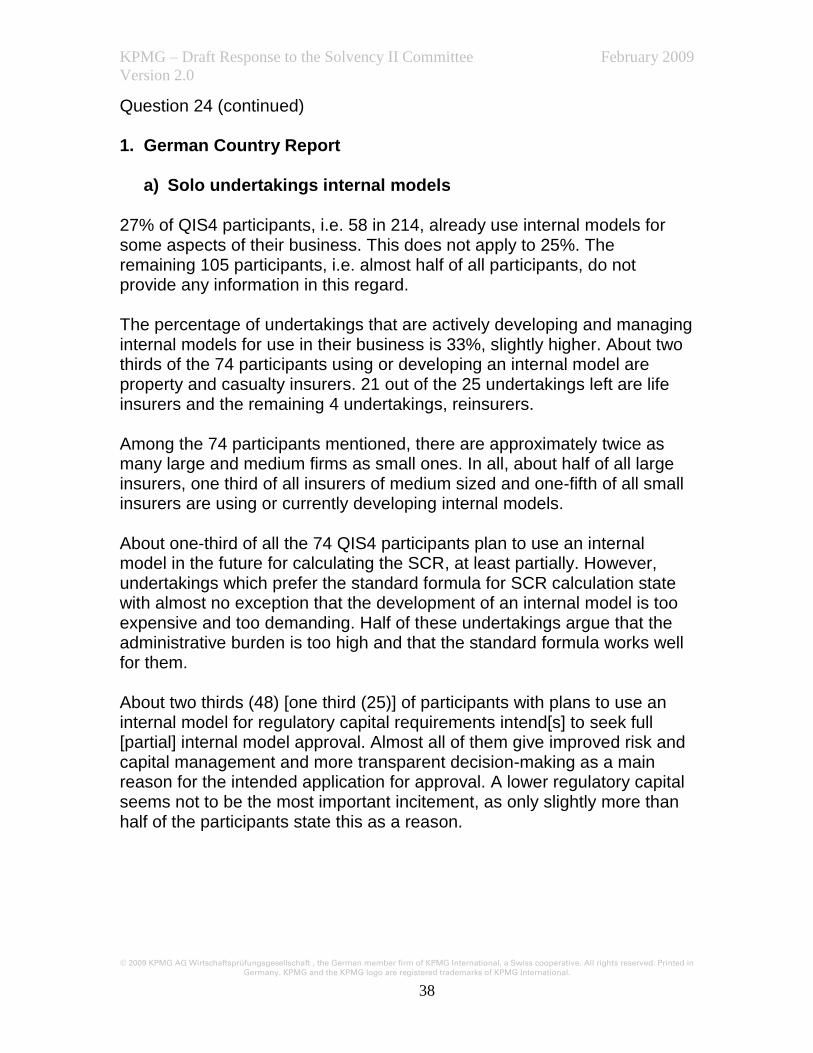

Question 24 (continued) 1. German Country Report

a) Solo undertakings internal models

27% of QIS4 participants, i.e. 58 in 214, already use internal models for some aspects of their business. This does not apply to 25%. The remaining 105 participants, i.e. almost half of all participants, do not provide any information in this regard. The percentage of undertakings that are actively developing and managing internal models for use in their business is 33%, slightly higher. About two thirds of the 74 participants using or developing an internal model are property and casualty insurers. 21 out of the 25 undertakings left are life insurers and the remaining 4 undertakings, reinsurers. Among the 74 participants mentioned, there are approximately twice as many large and medium firms as small ones. In all, about half of all large insurers, one third of all insurers of medium sized and one-fifth of all small insurers are using or currently developing internal models. About one-third of all the 74 QIS4 participants plan to use an internal model in the future for calculating the SCR, at least partially. However, undertakings which prefer the standard formula for SCR calculation state with almost no exception that the development of an internal model is too expensive and too demanding. Half of these undertakings argue that the administrative burden is too high and that the standard formula works well for them. About two thirds (48) [one third (25)] of participants with plans to use an internal model for regulatory capital requirements intend[s] to seek full [partial] internal model approval. Almost all of them give improved risk and capital management and more transparent decision-making as a main reason for the intended application for approval. A lower regulatory capital seems not to be the most important incitement, as only slightly more than half of the participants state this as a reason.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

39

Question 24 (continued) b) Group internal models

6 out of the 19 participating insurance groups, i.e. about one third of the groups, already use internal models for some aspects of their business. 4 other groups stated that the question does not apply to them. One of these groups reported, however, that it is actively developing and managing an internal model for use in its business. The remaining 9 groups did not provide any information on internal model usage or corresponding plans for the future.

Each of the 6 insurance groups that are already using an internal model for some aspects of their business plans to use it in the future for calculating the SCR, at least partially. 5 out of the 6 insurance groups mentioned above intend to seek full model approval. The one remaining group will apply for partial model approval for market risk. All 6 groups stated better capital management and more transparent decision-making as the main reasons for the intended application for full or partial model approval.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

40

Category: General Insurance Subject: Adjustment to standard factors Question 25 Are countries attempting to adjust the standard factors as set out in sections TS.XIII.B.25, TS.XIII.B.27, TS.XIII.B.28 TS.XIII.B.36 and TS.XIII.C.6 of the QIS4 Technical Specification to make them more country specific? KPMG Response to Question 25 Countries are generally allowed to adjust the standard factors yet we are not aware that this has happened up to now. Calibration paper (CEIOPS-DOC-02/2008) issued centrally by CEIOPS states that parameters referred to in TS.XIII.B.25, TS.XIII.B.27 and TS.XIII.C.6 have been re-calibrated from QIS3 to QIS4 for example.

For catastrophe risks however, regional scenarios were generally well accepted nationally when available, but criticised for not being harmonised throughout Europe, and allowing for the possibility of there being an un-level playing field between undertakings in different countries. For natural catastrophes (such as earthquake, floods, storms etc.), regional factors, index tables and scenarios have been used. For example, for Germany there exist regional indices for the calculation of the regional exposure factor for storm property, earthquake property, and natural hazard motor.

Example:

Reference in QIS4: TS.XIII.B.25 and TS.XIII.B.27: “Following feedback from QIS3, the factors used within the SCR non-life underwriting risk module were adjusted to better reflect the relative and overall riskiness of different lines of business. Based on the QIS3 calibration of premium risk in the German market, the recalibration reflects information collected through QIS3 on internal models, the results from current regulatory regimes and other market information from several

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

41

Question 25 (continued) Members States (United Kingdom, Portugal, The Netherlands). Results from over 46 firms were used to recalibrate the factors.”

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

42

Category: General Insurance Subject: Appropriateness of market factors

Question 26

How do the regulators view the use of the market factors which are incorrect for both small and large companies? KPMG Response to Question 26 It is agreed that any model using market factors can only reflect a certain set of companies, i.e. those having characteristics close to the “market average”. As typical examples, large insurance groups and niche players with a special product portfolio do not fall into this category. However, as page 10 of the CEIOPS paper on ORSA (Ref: CEIOPS-IGSRR-09/08) points out, the “Framework Directive Proposal allows undertakings to use entity-specific parameters when calculating the life, non-life and special underwriting risk modules. The use of these specific parameters is subject to supervisory approval.”

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

43

Category: General Insurance Subject: Market factor confirmation for CMBI Question 27 Should the Israeli companies approach ISO-Israel to produce relevant market factors for the reserve and underwriting risk for the Compulsory Motor Bodily Injury sector, as they hold and analyse data for the whole market? In addition, the tariff has been radically reduced over the last 10 years rendering historical loss ratios invalid, how would you suggest that we deal with this problem? KPMG Response to Question 27 It may be a good solution to take data from a reliable source which has a sufficient overview of the Israeli market. As to the trend in the tariffs, two different effects have to be separated:

level change - i.e. the reduction in tariffs over the last 10 years. This effect could be tackled by a trend correction. This effect does not directly reflect the risk within the product. i.e. although the product might be in deficit, the risk might be deemed minor if the fluctuation around this (low) average is small. In this case the results from the product can be estimated quite reliably.

risk - i.e. the possibility that the true losses out of the product deviate strongly from the assumptions used in pricing the product. This risk might, as is done in QIS, be measured by some means based on the standard deviation of loss ratios after trend correction. If you do not correct the inherent trend you would overestimate the risk in the product since the trend produces additional fluctuation.

Another way to look at this is as follows: If the rates have been reduced across the market then the impact should be the same. However, you can analyze the data in two groups: before rate changes

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

44

Question 27 (continued) and after rate changes. Or adjust the historical loss ratio for rate changes to a specific balance date and utilize this for calculations. This will capture any impact of rate changes (or at least dampen the effect on standard deviation).

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

45

Category: General Insurance Subject: Definition of “Best Estimate” Question 28 Is any change to the definition of "Best Estimate" expected, or will any guidelines be published as to the method of calculation? How are companies coping with the current definition? KPMG Response to Question 28 There are no standard guidelines on how the Best Estimate should be calculated as the company can use a wide range of actuarial methods. The consistency is achieved through the definition of Best Estimate as opposed to the method employed. Companies have been producing BE on a best effort basis, but concerns have been raised by CEIOPS that there is inconsistency in Best Estimates (i.e. is it mean, median, etc). In light of this there may be some guidance. It is making the setting of reserves more explicit by splitting out any explicit or implicit margins previously allowed for in the best estimate. It is thought that guidance is more likely to come from Actuarial professional bodies.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

46

Category: General Insurance Subject: Calculation of the risk margin Question 29 What are the latest thoughts regarding the calculation of the risk margin or is the Cost of Capital (CoC) method the most likely approach also in the future? KPMG Response to Question 29 Generally, companies have used the standard method provided within QIS4 (within the helper sheets) to calculate the risk margins. This uses the CoC approach. Currently, it looks as if the CoC method is going to be the approach most likely to be adopted for Solvency II to calculate the RM. German Country report Regarding the data collecting issues, many participants consider the calculation of the risk margin to be too complex. They complained about the effort to derive CoC margins separately for each line of business. Thus most of them used simplifications. The majority of the participants assessed the risk margin using the duration simplification. Many other participants estimated future SCR’s via best estimate ratios. Only one participant stated to have employed a proxy. The assumption defines a situation which is too complex to be modelled in detail. For example, the calculation of the risk margin requires the projection of the SCR until run-off of the liabilities. However, it is usually not feasible to determine in detail the future SCR’s for long time periods.

Risk margin (all insurance types) To determine the CoC margin, most of the participants needed to apply simplifications since a comprehensive projection of all future SCR’s and their allocation to individual LoB’s was not practically feasible for them. For this purpose, some participants followed their own approach, while others used one of the simplifications provided in the specification (which were partly implemented in the helper tab on risk margins contained in the QIS4 package).

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

47

Question 29 (continued) In non-life insurance, some participants also applied the simple risk-margin-proxy which determines the risk margin as a fixed percentage of the best estimate, irrespective of the size of the SCR or the duration of the liability. Some participants drew attention to the fact that in the ordinary course of business, insurance companies will normally retain insurance liabilities and will not transfer them to a third party. Thus, in contrast to the valuation principle set out in part TS.II.C.3 of the QIS4 Technical Specification, they believed it to be more economically faithful to value insurance liabilities on the basis that they are kept in the company’s own portfolio, including the company’s existing servicing platform and cost structure, rather than to base the valuation on a hypothetical transfer. Only few participants found the CoC rate not to be appropriate.

Again, in non-life insurance, some participants applied both the main approach provided by the helper tab, and also the simplified method outlined in formula TS.II.C.25 of the QIS4 Technical Specification, and found that these two approaches yielded materially different results. In view of these technical difficulties, some participants (in particular small insurers) resorted to using the Risk Margin Proxy, arguing that this was justified in view of the immateriality of the risk margin with respect to the size of the best estimate. Concerning the helper tab for the non-life risk margin, a number of participants pointed out that the method implemented in this tab produces separate risk margins for premium provisions and claims provisions, and commented that the computations would lead to unsuitable results with regard to the premium provision risk margin. In the context of the determination of the risk margin, some participants raised the issue of diversification effects and took the view that the risk margin relating to the insurer’s book of business as a whole should reflect diversification benefits across different segments. Quantitatively the risk margin amounted to:

1.1% of the BE provisions in life insurance,

9.3% of the net BE provisions in property & casualties insurance, and

1.5% of the net BE provisions in health insurance.

KPMG – Draft Response to the Solvency II Committee February 2009

Version 2.0

© 2009 KPMG AG Wirtschaftsprüfungsgesellschaft , the German member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in

Germany. KPMG and the KPMG logo are registered trademarks of KPMG International.

48