Embed Size (px)

Citation preview

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

Dynamic Asset AllocationChapter 10: Stochastic interest rates

Claus Munk

August 2012

AARHUS UNIVERSITY AU

1 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

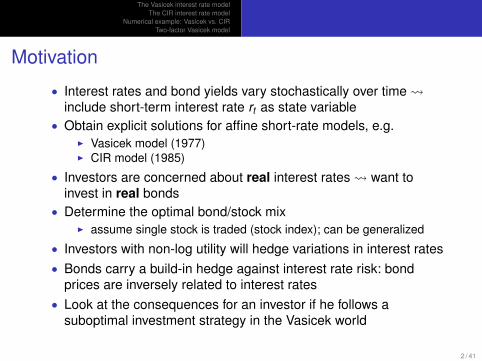

Motivation

• Interest rates and bond yields vary stochastically over time include short-term interest rate rt as state variable

• Obtain explicit solutions for affine short-rate models, e.g.I Vasicek model (1977)I CIR model (1985)

• Investors are concerned about real interest rates want toinvest in real bonds

• Determine the optimal bond/stock mixI assume single stock is traded (stock index); can be generalized

• Investors with non-log utility will hedge variations in interest rates• Bonds carry a build-in hedge against interest rate risk: bond

prices are inversely related to interest rates• Look at the consequences for an investor if he follows a

suboptimal investment strategy in the Vasicek world

2 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

Outline

1 The Vasicek interest rate model

2 The CIR interest rate model

3 Numerical example: Vasicek vs. CIR

4 Two-factor Vasicek model

3 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

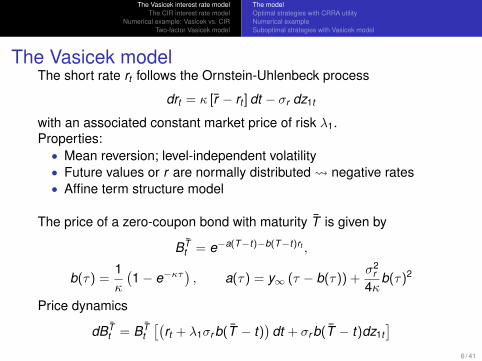

The Vasicek modelThe short rate rt follows the Ornstein-Uhlenbeck process

drt = κ [r − rt ] dt − σr dz1t

with an associated constant market price of risk λ1.Properties:• Mean reversion; level-independent volatility• Future values or r are normally distributed negative rates• Affine term structure model

The price of a zero-coupon bond with maturity T is given by

BTt = e−a(T−t)−b(T−t)rt ,

b(τ) =1κ

(1− e−κτ

), a(τ) = y∞ (τ − b(τ)) +

σ2r

4κb(τ)2

Price dynamics

dBTt = BT

t[(

rt + λ1σr b(T − t))

dt + σr b(T − t)dz1t]

6 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

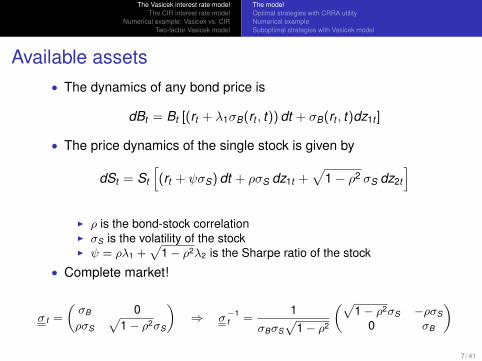

Available assets• The dynamics of any bond price is

dBt = Bt [(rt + λ1σB(rt , t)) dt + σB(rt , t)dz1t ]

• The price dynamics of the single stock is given by

dSt = St

[(rt + ψσS) dt + ρσS dz1t +

√1− ρ2 σS dz2t

]I ρ is the bond-stock correlationI σS is the volatility of the stockI ψ = ρλ1 +

√1− ρ2λ2 is the Sharpe ratio of the stock

• Complete market!

σ t =

(σB 0ρσS

√1− ρ2σS

)⇒ σ−1

t =1

σBσS

√1− ρ2

(√1− ρ2σS −ρσS

0 σB

)7 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

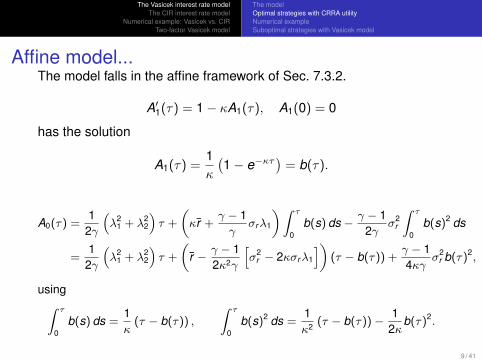

Affine model...The model falls in the affine framework of Sec. 7.3.2.

A′1(τ) = 1− κA1(τ), A1(0) = 0

has the solution

A1(τ) =1κ

(1− e−κτ

)= b(τ).

A0(τ) =1

2γ

(λ2

1 + λ22

)τ +

(κr +

γ − 1γ

σrλ1

)∫ τ

0b(s) ds − γ − 1

2γσ2

r

∫ τ

0b(s)2 ds

=1

2γ

(λ2

1 + λ22

)τ +

(r − γ − 1

2κ2γ

[σ2

r − 2κσrλ1

])(τ − b(τ)) +

γ − 14κγ

σ2r b(τ)2,

using∫ τ

0b(s) ds =

1κ

(τ − b(τ)) ,

∫ τ

0b(s)2 ds =

1κ2 (τ − b(τ))− 1

2κb(τ)2.

9 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

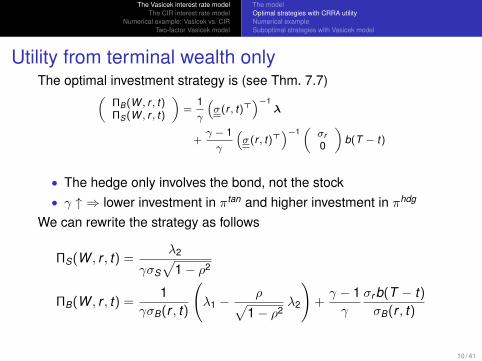

Utility from terminal wealth onlyThe optimal investment strategy is (see Thm. 7.7)(

ΠB(W , r , t)ΠS(W , r , t)

)=

1γ

(σ (r , t)>

)−1λ

+γ − 1γ

(σ (r , t)>

)−1(

σr0

)b(T − t)

• The hedge only involves the bond, not the stock• γ ↑ ⇒ lower investment in πtan and higher investment in πhdg

We can rewrite the strategy as follows

ΠS(W , r , t) =λ2

γσS√

1− ρ2

ΠB(W , r , t) =1

γσB(r , t)

(λ1 −

ρ√1− ρ2

λ2

)+γ − 1γ

σr b(T − t)σB(r , t)

10 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

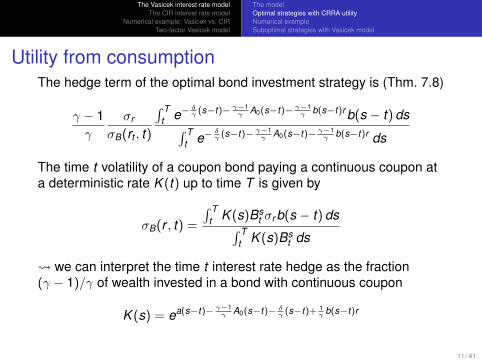

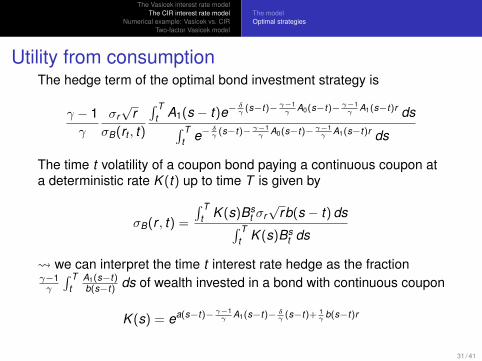

Utility from consumptionThe hedge term of the optimal bond investment strategy is (Thm. 7.8)

γ − 1γ

σr

σB(rt , t)

∫ Tt e−

δγ (s−t)− γ−1

γ A0(s−t)− γ−1γ b(s−t)r b(s − t) ds∫ T

t e−δγ (s−t)− γ−1

γ A0(s−t)− γ−1γ b(s−t)r ds

The time t volatility of a coupon bond paying a continuous coupon ata deterministic rate K (t) up to time T is given by

σB(r , t) =

∫ Tt K (s)Bs

t σr b(s − t) ds∫ Tt K (s)Bs

t ds

we can interpret the time t interest rate hedge as the fraction(γ − 1)/γ of wealth invested in a bond with continuous coupon

K (s) = ea(s−t)− γ−1γ A0(s−t)− δ

γ (s−t)+ 1γ b(s−t)r

11 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

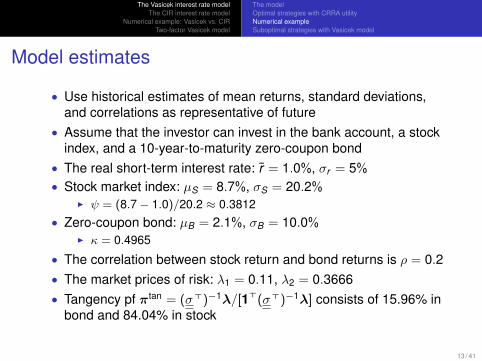

Model estimates

• Use historical estimates of mean returns, standard deviations,and correlations as representative of future

• Assume that the investor can invest in the bank account, a stockindex, and a 10-year-to-maturity zero-coupon bond

• The real short-term interest rate: r = 1.0%, σr = 5%

• Stock market index: µS = 8.7%, σS = 20.2%I ψ = (8.7− 1.0)/20.2 ≈ 0.3812

• Zero-coupon bond: µB = 2.1%, σB = 10.0%I κ = 0.4965

• The correlation between stock return and bond returns is ρ = 0.2• The market prices of risk: λ1 = 0.11, λ2 = 0.3666• Tangency pf πtan = (σ>)−1λ/[1>(σ>)−1λ] consists of 15.96% in

bond and 84.04% in stock

13 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

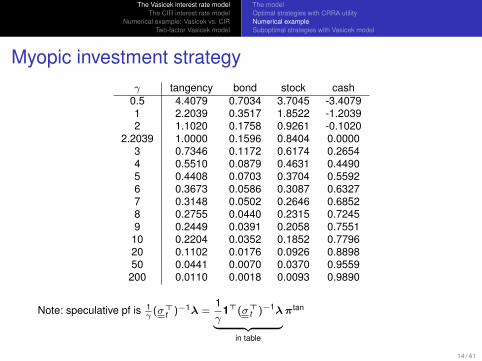

Myopic investment strategyγ tangency bond stock cash

0.5 4.4079 0.7034 3.7045 -3.40791 2.2039 0.3517 1.8522 -1.20392 1.1020 0.1758 0.9261 -0.1020

2.2039 1.0000 0.1596 0.8404 0.00003 0.7346 0.1172 0.6174 0.26544 0.5510 0.0879 0.4631 0.44905 0.4408 0.0703 0.3704 0.55926 0.3673 0.0586 0.3087 0.63277 0.3148 0.0502 0.2646 0.68528 0.2755 0.0440 0.2315 0.72459 0.2449 0.0391 0.2058 0.755110 0.2204 0.0352 0.1852 0.779620 0.1102 0.0176 0.0926 0.889850 0.0441 0.0070 0.0370 0.9559

200 0.0110 0.0018 0.0093 0.9890

Note: speculative pf is 1γ

(σ>t )−1λ =

1γ

1>(σ>t )−1λ︸ ︷︷ ︸

in table

πtan

14 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

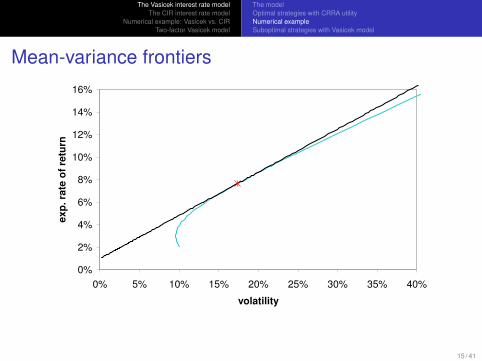

Mean-variance frontiers

0%

2%

4%

6%

8%

10%

12%

14%

16%

0% 5% 10% 15% 20% 25% 30% 35% 40%

volatility

ex

p.

rate

of

retu

rn

15 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

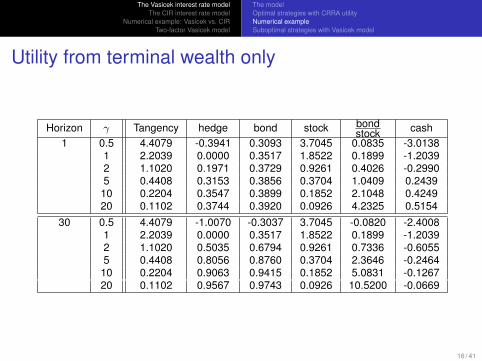

Utility from terminal wealth only

Horizon γ Tangency hedge bond stock bondstock cash

1 0.5 4.4079 -0.3941 0.3093 3.7045 0.0835 -3.01381 2.2039 0.0000 0.3517 1.8522 0.1899 -1.20392 1.1020 0.1971 0.3729 0.9261 0.4026 -0.29905 0.4408 0.3153 0.3856 0.3704 1.0409 0.243910 0.2204 0.3547 0.3899 0.1852 2.1048 0.424920 0.1102 0.3744 0.3920 0.0926 4.2325 0.5154

30 0.5 4.4079 -1.0070 -0.3037 3.7045 -0.0820 -2.40081 2.2039 0.0000 0.3517 1.8522 0.1899 -1.20392 1.1020 0.5035 0.6794 0.9261 0.7336 -0.60555 0.4408 0.8056 0.8760 0.3704 2.3646 -0.246410 0.2204 0.9063 0.9415 0.1852 5.0831 -0.126720 0.1102 0.9567 0.9743 0.0926 10.5200 -0.0669

16 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

Utility from terminal wealth only

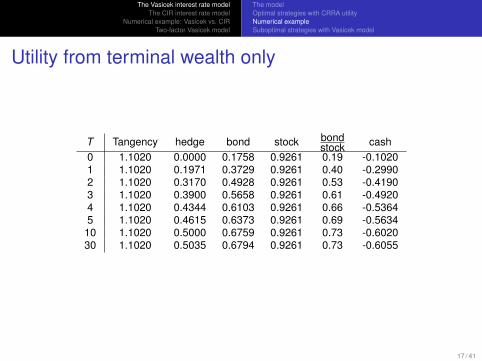

T Tangency hedge bond stock bondstock cash

0 1.1020 0.0000 0.1758 0.9261 0.19 -0.10201 1.1020 0.1971 0.3729 0.9261 0.40 -0.29902 1.1020 0.3170 0.4928 0.9261 0.53 -0.41903 1.1020 0.3900 0.5658 0.9261 0.61 -0.49204 1.1020 0.4344 0.6103 0.9261 0.66 -0.53645 1.1020 0.4615 0.6373 0.9261 0.69 -0.563410 1.1020 0.5000 0.6759 0.9261 0.73 -0.602030 1.1020 0.5035 0.6794 0.9261 0.73 -0.6055

17 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

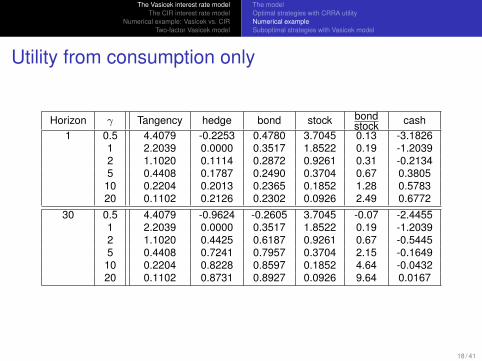

Utility from consumption only

Horizon γ Tangency hedge bond stock bondstock cash

1 0.5 4.4079 -0.2253 0.4780 3.7045 0.13 -3.18261 2.2039 0.0000 0.3517 1.8522 0.19 -1.20392 1.1020 0.1114 0.2872 0.9261 0.31 -0.21345 0.4408 0.1787 0.2490 0.3704 0.67 0.3805

10 0.2204 0.2013 0.2365 0.1852 1.28 0.578320 0.1102 0.2126 0.2302 0.0926 2.49 0.6772

30 0.5 4.4079 -0.9624 -0.2605 3.7045 -0.07 -2.44551 2.2039 0.0000 0.3517 1.8522 0.19 -1.20392 1.1020 0.4425 0.6187 0.9261 0.67 -0.54455 0.4408 0.7241 0.7957 0.3704 2.15 -0.1649

10 0.2204 0.8228 0.8597 0.1852 4.64 -0.043220 0.1102 0.8731 0.8927 0.0926 9.64 0.0167

18 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

Optimal frontiers with Vasicek interest rates

0%

2%

4%

6%

8%

10%

12%

14%

16%

0% 5% 10% 15% 20% 25% 30% 35% 40%

volatility

ex

p.

rate

of

retu

rn

19 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

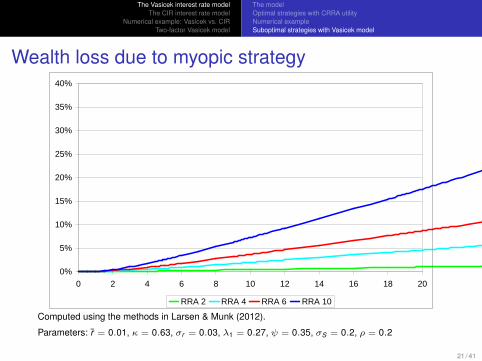

Wealth loss due to myopic strategy

0%

5%

10%

15%

20%

25%

30%

35%

40%

0 2 4 6 8 10 12 14 16 18 20

RRA 2 RRA 4 RRA 6 RRA 10

Computed using the methods in Larsen & Munk (2012).

Parameters: r = 0.01, κ = 0.63, σr = 0.03, λ1 = 0.27, ψ = 0.35, σS = 0.2, ρ = 0.2

21 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

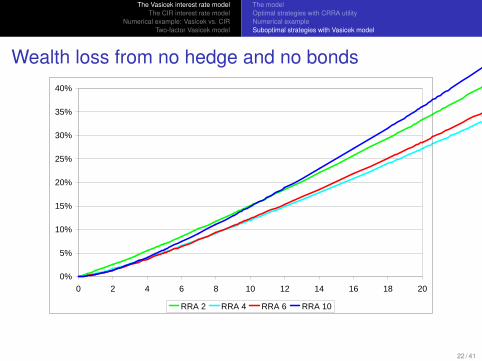

Wealth loss from no hedge and no bonds

0%

5%

10%

15%

20%

25%

30%

35%

40%

0 2 4 6 8 10 12 14 16 18 20

RRA 2 RRA 4 RRA 6 RRA 10

22 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

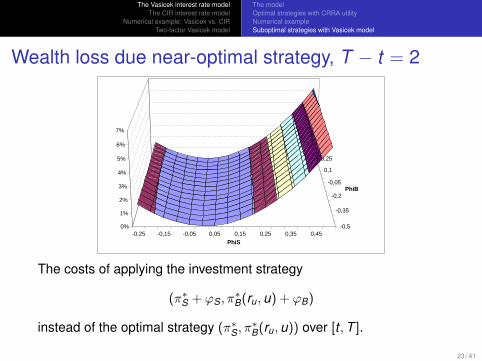

Wealth loss due near-optimal strategy, T − t = 2

-0,25 -0,15 -0,05 0,05 0,15 0,25 0,35 0,45-0,5

-0,35

-0,2

-0,05

0,1

0,25

0%

1%

2%

3%

4%

5%

6%

7%

PhiS

PhiB

The costs of applying the investment strategy

(π∗S + ϕS, π∗B(ru,u) + ϕB)

instead of the optimal strategy (π∗S, π∗B(ru,u)) over [t ,T ].

23 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies with CRRA utilityNumerical exampleSuboptimal strategies with Vasicek model

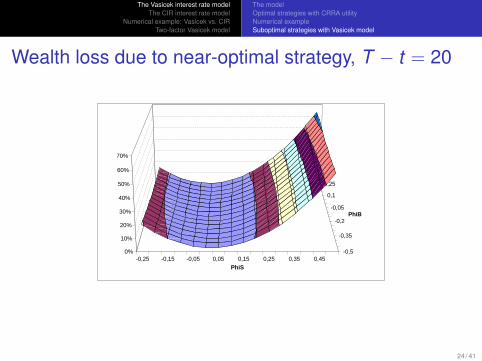

Wealth loss due to near-optimal strategy, T − t = 20

-0,25 -0,15 -0,05 0,05 0,15 0,25 0,35 0,45-0,5

-0,35

-0,2

-0,05

0,1

0,25

0%

10%

20%

30%

40%

50%

60%

70%

PhiS

PhiB

24 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies

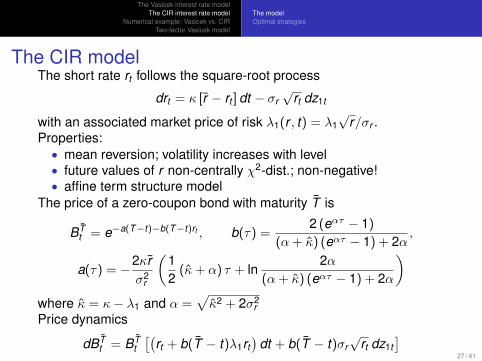

The CIR modelThe short rate rt follows the square-root process

drt = κ [r − rt ] dt − σr√

rt dz1t

with an associated market price of risk λ1(r , t) = λ1√

r/σr .Properties:• mean reversion; volatility increases with level• future values of r non-centrally χ2-dist.; non-negative!• affine term structure model

The price of a zero-coupon bond with maturity T is

BTt = e−a(T−t)−b(T−t)rt , b(τ) =

2 (eατ − 1)

(α + κ) (eατ − 1) + 2α,

a(τ) = −2κrσ2

r

(12

(κ+ α) τ + ln2α

(α + κ) (eατ − 1) + 2α

)where κ = κ− λ1 and α =

√κ2 + 2σ2

rPrice dynamics

dBTt = BT

t[(

rt + b(T − t)λ1rt)

dt + b(T − t)σr√

rt dz1t]

27 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies

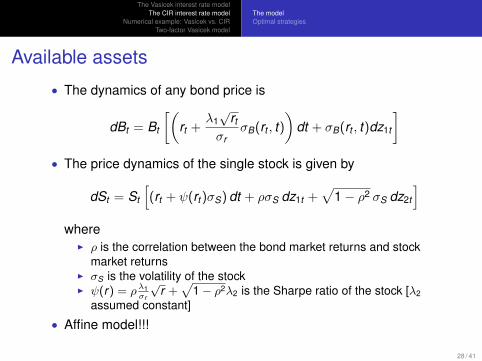

Available assets

• The dynamics of any bond price is

dBt = Bt

[(rt +

λ1√

rt

σrσB(rt , t)

)dt + σB(rt , t)dz1t

]• The price dynamics of the single stock is given by

dSt = St

[(rt + ψ(rt )σS) dt + ρσS dz1t +

√1− ρ2 σS dz2t

]where

I ρ is the correlation between the bond market returns and stockmarket returns

I σS is the volatility of the stockI ψ(r) = ρλ1

σr

√r +

√1− ρ2λ2 is the Sharpe ratio of the stock [λ2

assumed constant]

• Affine model!!!

28 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies

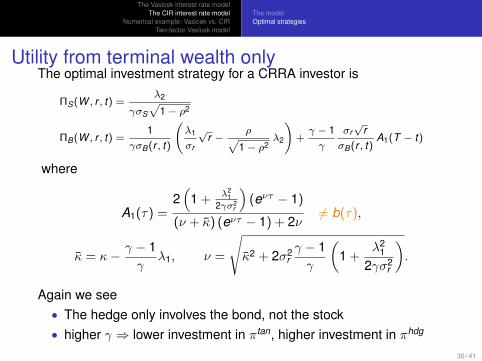

Utility from terminal wealth onlyThe optimal investment strategy for a CRRA investor is

ΠS(W , r , t) =λ2

γσS√

1− ρ2

ΠB(W , r , t) =1

γσB(r , t)

(λ1

σr

√r −

ρ√1− ρ2

λ2

)+γ − 1γ

σr√

rσB(r , t)

A1(T − t)

where

A1(τ) =2(

1 +λ2

12γσ2

r

)(eντ − 1)

(ν + κ) (eντ − 1) + 2ν6= b(τ),

κ = κ− γ − 1γ

λ1, ν =

√κ2 + 2σ2

rγ − 1γ

(1 +

λ21

2γσ2r

).

Again we see• The hedge only involves the bond, not the stock• higher γ ⇒ lower investment in πtan, higher investment in πhdg

30 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

The modelOptimal strategies

Utility from consumptionThe hedge term of the optimal bond investment strategy is

γ − 1γ

σr√

rσB(rt , t)

∫ Tt A1(s − t)e−

δγ (s−t)− γ−1

γ A0(s−t)− γ−1γ A1(s−t)r ds∫ T

t e−δγ (s−t)− γ−1

γ A0(s−t)− γ−1γ A1(s−t)r ds

The time t volatility of a coupon bond paying a continuous coupon ata deterministic rate K (t) up to time T is given by

σB(r , t) =

∫ Tt K (s)Bs

t σr√

rb(s − t) ds∫ Tt K (s)Bs

t ds

we can interpret the time t interest rate hedge as the fractionγ−1γ

∫ Tt

A1(s−t)b(s−t) ds of wealth invested in a bond with continuous coupon

K (s) = ea(s−t)− γ−1γ A1(s−t)− δ

γ (s−t)+ 1γ b(s−t)r

31 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

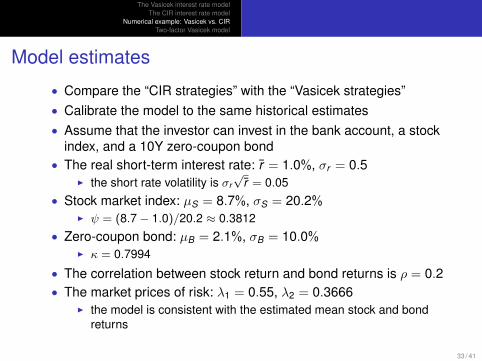

Model estimates

• Compare the “CIR strategies” with the “Vasicek strategies”• Calibrate the model to the same historical estimates• Assume that the investor can invest in the bank account, a stock

index, and a 10Y zero-coupon bond• The real short-term interest rate: r = 1.0%, σr = 0.5

I the short rate volatility is σr√

r = 0.05• Stock market index: µS = 8.7%, σS = 20.2%

I ψ = (8.7− 1.0)/20.2 ≈ 0.3812• Zero-coupon bond: µB = 2.1%, σB = 10.0%

I κ = 0.7994

• The correlation between stock return and bond returns is ρ = 0.2• The market prices of risk: λ1 = 0.55, λ2 = 0.3666

I the model is consistent with the estimated mean stock and bondreturns

33 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

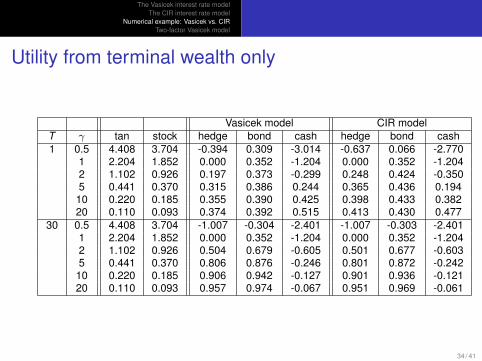

Utility from terminal wealth only

Vasicek model CIR modelT γ tan stock hedge bond cash hedge bond cash1 0.5 4.408 3.704 -0.394 0.309 -3.014 -0.637 0.066 -2.770

1 2.204 1.852 0.000 0.352 -1.204 0.000 0.352 -1.2042 1.102 0.926 0.197 0.373 -0.299 0.248 0.424 -0.3505 0.441 0.370 0.315 0.386 0.244 0.365 0.436 0.19410 0.220 0.185 0.355 0.390 0.425 0.398 0.433 0.38220 0.110 0.093 0.374 0.392 0.515 0.413 0.430 0.477

30 0.5 4.408 3.704 -1.007 -0.304 -2.401 -1.007 -0.303 -2.4011 2.204 1.852 0.000 0.352 -1.204 0.000 0.352 -1.2042 1.102 0.926 0.504 0.679 -0.605 0.501 0.677 -0.6035 0.441 0.370 0.806 0.876 -0.246 0.801 0.872 -0.24210 0.220 0.185 0.906 0.942 -0.127 0.901 0.936 -0.12120 0.110 0.093 0.957 0.974 -0.067 0.951 0.969 -0.061

34 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

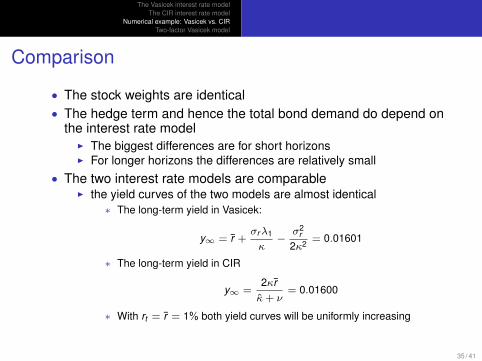

Comparison

• The stock weights are identical• The hedge term and hence the total bond demand do depend on

the interest rate modelI The biggest differences are for short horizonsI For longer horizons the differences are relatively small

• The two interest rate models are comparableI the yield curves of the two models are almost identical

∗ The long-term yield in Vasicek:

y∞ = r +σrλ1

κ−

σ2r

2κ2= 0.01601

∗ The long-term yield in CIR

y∞ =2κrκ+ ν

= 0.01600

∗ With rt = r = 1% both yield curves will be uniformly increasing

35 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

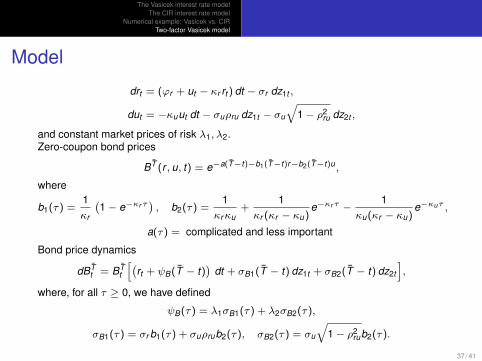

Model

drt = (ϕr + ut − κr rt ) dt − σr dz1t ,

dut = −κuut dt − σuρru dz1t − σu

√1− ρ2

ru dz2t ,

and constant market prices of risk λ1, λ2.Zero-coupon bond prices

BT (r , u, t) = e−a(T−t)−b1(T−t)r−b2(T−t)u ,

where

b1(τ) =1κr

(1− e−κr τ

), b2(τ) =

1κrκu

+1

κr (κr − κu)e−κr τ −

1κu(κr − κu)

e−κuτ ,

a(τ) = complicated and less important

Bond price dynamics

dBTt = BT

t

[(rt + ψB(T − t)

)dt + σB1(T − t) dz1t + σB2(T − t) dz2t

],

where, for all τ ≥ 0, we have defined

ψB(τ) = λ1σB1(τ) + λ2σB2(τ),

σB1(τ) = σr b1(τ) + σuρrub2(τ), σB2(τ) = σu

√1− ρ2

rub2(τ).

37 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

Asset allocationIndividual with CRRA utility of terminal wealth, who can invest in

1 the locally risk-free asset (=bank account; cash deposits) with rate of return rt ,

2 a zero-coupon bond maturing at time T1,

3 a zero-coupon bond maturing at time T2 6= T1,

4 the stock with

dSt = St [(rt + ψSσS) dt + σSk1 dz1t + σSk2 dz2t + σSk3 dz3t ] .

Two-dimensional affine asset allocation model

J(W , r , u, t) =1

1− γg(r , u, t)γW 1−γ ,

g(r , u, t) = exp{−γ − 1γ

A0(T − t)−γ − 1γ

A1r (T − t)r −γ − 1γ

A1u(T − t)u},

A1r (τ) ≡ b1(τ), A1u(τ) ≡ b2(τ).

Optimal investment strategy isπB1(t)πB2(t)πS

=1γ

(σ (t)>

)−1λ−

γ − 1γ

(σ (t)>

)−1

−σr −σuρru

0 −σu

√1− ρ2

ru0 0

(A1r (T − t)A1u(T − t)

)

38 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

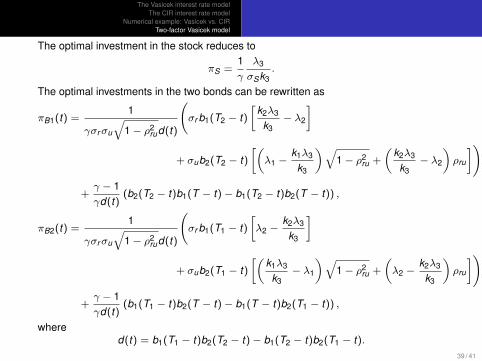

The optimal investment in the stock reduces to

πS =1γ

λ3

σSk3.

The optimal investments in the two bonds can be rewritten as

πB1(t) =1

γσrσu

√1− ρ2

rud(t)

(σr b1(T2 − t)

[k2λ3

k3− λ2

]

+ σub2(T2 − t)[(λ1 −

k1λ3

k3

)√1− ρ2

ru +

(k2λ3

k3− λ2

)ρru

])

+γ − 1γd(t)

(b2(T2 − t)b1(T − t)− b1(T2 − t)b2(T − t)) ,

πB2(t) =1

γσrσu

√1− ρ2

rud(t)

(σr b1(T1 − t)

[λ2 −

k2λ3

k3

]

+ σub2(T1 − t)[(

k1λ3

k3− λ1

)√1− ρ2

ru +

(λ2 −

k2λ3

k3

)ρru

])

+γ − 1γd(t)

(b1(T1 − t)b2(T − t)− b1(T − t)b2(T1 − t)) ,

whered(t) = b1(T1 − t)b2(T2 − t)− b1(T2 − t)b2(T1 − t).

39 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

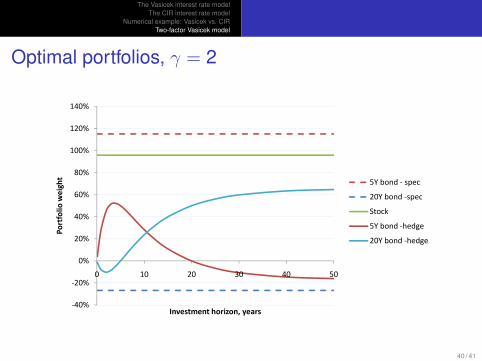

Optimal portfolios, γ = 2

20%

40%

60%

80%

100%

120%

140%

Po

rtfo

lio

we

igh

t

5Y bond - spec

20Y bond -spec

Stock

5Y bond -hedge

20Y bond -hedge

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

0 10 20 30 40 50

Po

rtfo

lio

we

igh

t

Investment horizon, years

5Y bond - spec

20Y bond -spec

Stock

5Y bond -hedge

20Y bond -hedge

40 / 41

The Vasicek interest rate modelThe CIR interest rate model

Numerical example: Vasicek vs. CIRTwo-factor Vasicek model

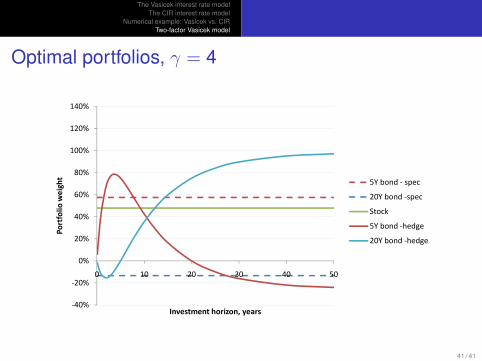

Optimal portfolios, γ = 4

20%

40%

60%

80%

100%

120%

140%

Po

rtfo

lio

we

igh

t

5Y bond - spec

20Y bond -spec

Stock

5Y bond -hedge

20Y bond -hedge

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

0 10 20 30 40 50

Po

rtfo

lio

we

igh

t

Investment horizon, years

5Y bond - spec

20Y bond -spec

Stock

5Y bond -hedge

20Y bond -hedge

41 / 41

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Dynamic Asset AllocationChapter 11: Stochastic market prices of risk

Claus Munk

August 2012

AARHUS UNIVERSITY AU

1 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Outline

1 Stochastic market price of riskThe basic modelDistribution of future pricesOptimal investment strategy

2 Value/growth tilts and mean reversionThe modelOptimal strategiesSuboptimal strategies

3 Stochastic volatilityModel without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

2 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The basic modelDistribution of future pricesOptimal investment strategy

Motivation• Numerous studies have reported empirical evidence of mean

reversion in stock returnsI stock returns are high after a period of low realized returns and

vice versaI average stock returns seem predictable via dividend/price,

earnings/price, or short-term interest rate; still highly debated,though

• Among others Kim and Omberg (1996) and Wachter (2002) havestudied the implications for portfolio decisions

• Both papers obtain closed-form solutions for the optimalinvestment strategies

• The investment strategy is consistent with the typicalrecommendation of investment advisors

I lower variance of long-term stock returns than in the standardmodel

I an investor with a long horizon should invest a larger fraction ofwealth in stocks than an investor with a shorter horizon

5 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The basic modelDistribution of future pricesOptimal investment strategy

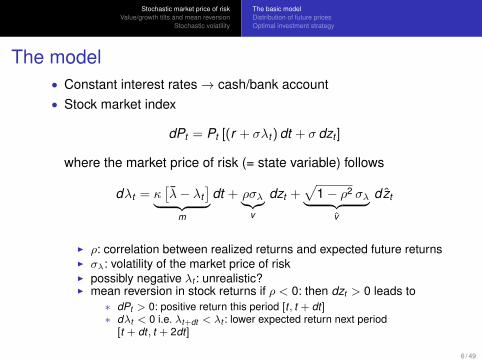

The model• Constant interest rates→ cash/bank account• Stock market index

dPt = Pt [(r + σλt ) dt + σ dzt ]

where the market price of risk (= state variable) follows

dλt = κ[λ− λt

]︸ ︷︷ ︸m

dt + ρσλ︸︷︷︸v

dzt +√

1− ρ2 σλ︸ ︷︷ ︸v

dzt

I ρ: correlation between realized returns and expected future returnsI σλ: volatility of the market price of riskI possibly negative λt : unrealistic?I mean reversion in stock returns if ρ < 0: then dzt > 0 leads to

∗ dPt > 0: positive return this period [t , t + dt]∗ dλt < 0 i.e. λt+dt < λt : lower expected return next period

[t + dt , t + 2dt]

6 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The basic modelDistribution of future pricesOptimal investment strategy

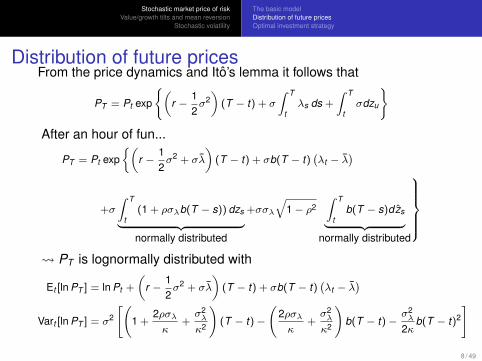

Distribution of future pricesFrom the price dynamics and Ito’s lemma it follows that

PT = Pt exp

{(r −

12σ2)

(T − t) + σ

∫ T

tλs ds +

∫ T

tσdzu

}

After an hour of fun...

PT = Pt exp{(

r −12σ2 + σλ

)(T − t) + σb(T − t)

(λt − λ

)

+σ

∫ T

t(1 + ρσλb(T − s)) dzs︸ ︷︷ ︸normally distributed

+σσλ

√1− ρ2

∫ T

tb(T − s)dzs︸ ︷︷ ︸

normally distributed

PT is lognormally distributed with

Et [ln PT ] = ln Pt +

(r −

12σ2 + σλ

)(T − t) + σb(T − t)

(λt − λ

)Vart [ln PT ] = σ2

[(1 +

2ρσλκ

+σ2λ

κ2

)(T − t)−

(2ρσλκ

+σ2λ

κ2

)b(T − t)−

σ2λ

2κb(T − t)2

]

8 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The basic modelDistribution of future pricesOptimal investment strategy

Distribution of future prices, cont’d

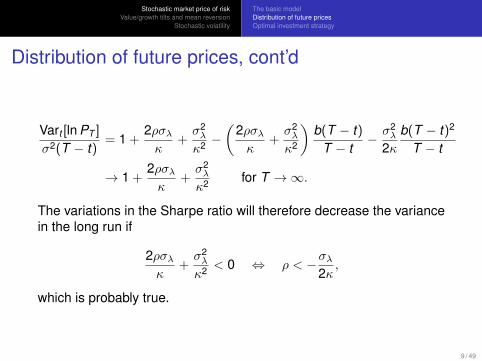

Vart [ln PT ]

σ2(T − t)= 1 +

2ρσλκ

+σ2λ

κ2 −(

2ρσλκ

+σ2λ

κ2

)b(T − t)

T − t− σ2

λ

2κb(T − t)2

T − t

→ 1 +2ρσλκ

+σ2λ

κ2 for T →∞.

The variations in the Sharpe ratio will therefore decrease the variancein the long run if

2ρσλκ

+σ2λ

κ2 < 0 ⇔ ρ < −σλ2κ,

which is probably true.

9 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The basic modelDistribution of future pricesOptimal investment strategy

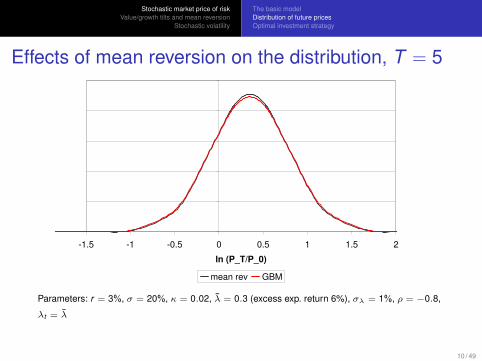

Effects of mean reversion on the distribution, T = 5

-1.5 -1 -0.5 0 0.5 1 1.5 2

ln (P_T/P_0)

mean rev GBM

Parameters: r = 3%, σ = 20%, κ = 0.02, λ = 0.3 (excess exp. return 6%), σλ = 1%, ρ = −0.8,

λt = λ

10 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The basic modelDistribution of future pricesOptimal investment strategy

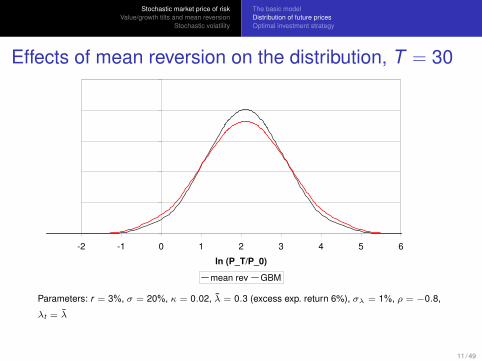

Effects of mean reversion on the distribution, T = 30

-2 -1 0 1 2 3 4 5 6

ln (P_T/P_0)

mean rev GBM

Parameters: r = 3%, σ = 20%, κ = 0.02, λ = 0.3 (excess exp. return 6%), σλ = 1%, ρ = −0.8,

λt = λ

11 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The basic modelDistribution of future pricesOptimal investment strategy

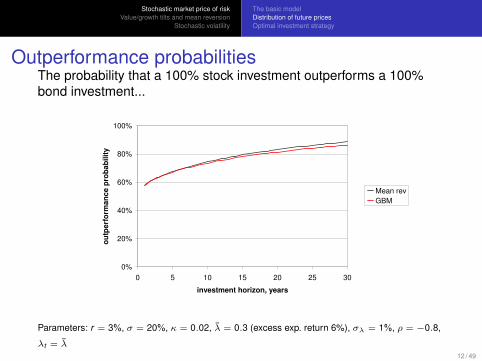

Outperformance probabilitiesThe probability that a 100% stock investment outperforms a 100%bond investment...

0%

20%

40%

60%

80%

100%

0 5 10 15 20 25 30

investment horizon, years

ou

tpe

rfo

rma

nc

e p

rob

ab

ilit

y

Mean rev

GBM

Parameters: r = 3%, σ = 20%, κ = 0.02, λ = 0.3 (excess exp. return 6%), σλ = 1%, ρ = −0.8,

λt = λ12 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The basic modelDistribution of future pricesOptimal investment strategy

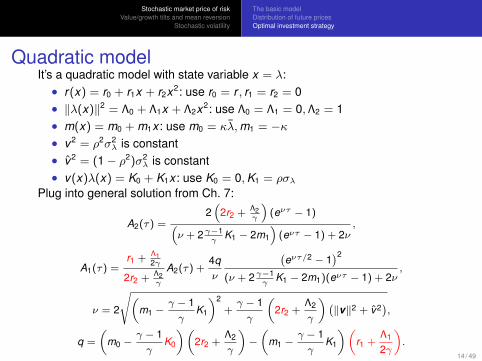

Quadratic modelIt’s a quadratic model with state variable x = λ:• r(x) = r0 + r1x + r2x2: use r0 = r , r1 = r2 = 0• ‖λ(x)‖2 = Λ0 + Λ1x + Λ2x2: use Λ0 = Λ1 = 0,Λ2 = 1• m(x) = m0 + m1x : use m0 = κλ,m1 = −κ• v2 = ρ2σ2

λ is constant• v2 = (1− ρ2)σ2

λ is constant• v(x)λ(x) = K0 + K1x : use K0 = 0,K1 = ρσλ

Plug into general solution from Ch. 7:

A2(τ) =2(

2r2 + Λ2γ

)(eντ − 1)(

ν + 2 γ−1γ

K1 − 2m1

)(eντ − 1) + 2ν

,

A1(τ) =r1 + Λ1

2γ

2r2 + Λ2γ

A2(τ) +4qν

(eντ/2 − 1

)2

(ν + 2 γ−1γ

K1 − 2m1)(eντ − 1) + 2ν,

ν = 2

√(m1 −

γ − 1γ

K1

)2+γ − 1γ

(2r2 +

Λ2

γ

)(‖v‖2 + v2

),

q =

(m0 −

γ − 1γ

K0

)(2r2 +

Λ2

γ

)−(

m1 −γ − 1γ

K1

)(r1 +

Λ1

2γ

).

14 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The basic modelDistribution of future pricesOptimal investment strategy

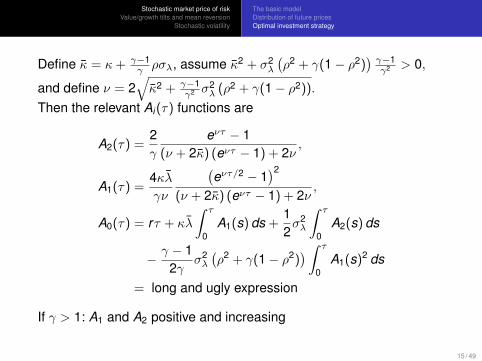

Define κ = κ+ γ−1γ ρσλ, assume κ2 + σ2

λ

(ρ2 + γ(1− ρ2)

)γ−1γ2 > 0,

and define ν = 2√κ2 + γ−1

γ2 σ2λ (ρ2 + γ(1− ρ2)).

Then the relevant Ai (τ) functions are

A2(τ) =2γ

eντ − 1(ν + 2κ) (eντ − 1) + 2ν

,

A1(τ) =4κλγν

(eντ/2 − 1

)2

(ν + 2κ) (eντ − 1) + 2ν,

A0(τ) = rτ + κλ

∫ τ

0A1(s) ds +

12σ2λ

∫ τ

0A2(s) ds

− γ − 12γ

σ2λ

(ρ2 + γ(1− ρ2)

) ∫ τ

0A1(s)2 ds

= long and ugly expression

If γ > 1: A1 and A2 positive and increasing

15 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The basic modelDistribution of future pricesOptimal investment strategy

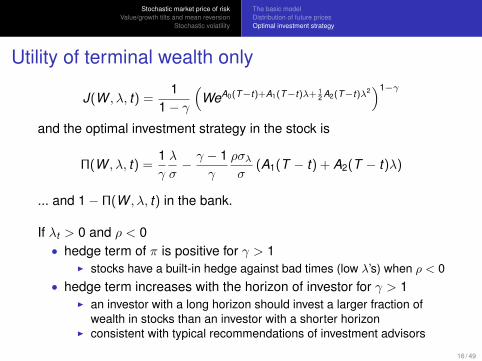

Utility of terminal wealth only

J(W , λ, t) =1

1− γ

(WeA0(T−t)+A1(T−t)λ+ 1

2 A2(T−t)λ2)1−γ

and the optimal investment strategy in the stock is

Π(W , λ, t) =1γ

λ

σ− γ − 1

γ

ρσλσ

(A1(T − t) + A2(T − t)λ)

... and 1− Π(W , λ, t) in the bank.

If λt > 0 and ρ < 0• hedge term of π is positive for γ > 1

I stocks have a built-in hedge against bad times (low λ’s) when ρ < 0• hedge term increases with the horizon of investor for γ > 1

I an investor with a long horizon should invest a larger fraction ofwealth in stocks than an investor with a shorter horizon

I consistent with typical recommendations of investment advisors

16 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The basic modelDistribution of future pricesOptimal investment strategy

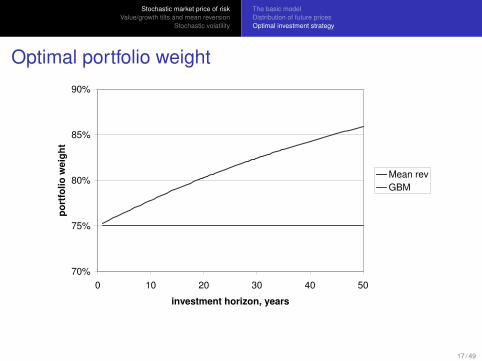

Optimal portfolio weight

70%

75%

80%

85%

90%

0 10 20 30 40 50

investment horizon, years

po

rtfo

lio

we

igh

t

Mean rev

GBM

17 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The basic modelDistribution of future pricesOptimal investment strategy

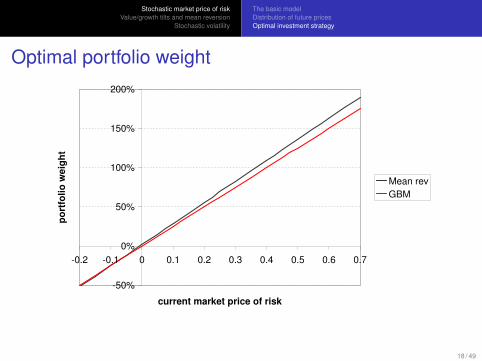

Optimal portfolio weight

-50%

0%

50%

100%

150%

200%

-0.2 -0.1 0 0.1 0.2 0.3 0.4 0.5 0.6 0.7

current market price of risk

po

rtfo

lio

we

igh

t

Mean rev

GBM

18 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The basic modelDistribution of future pricesOptimal investment strategy

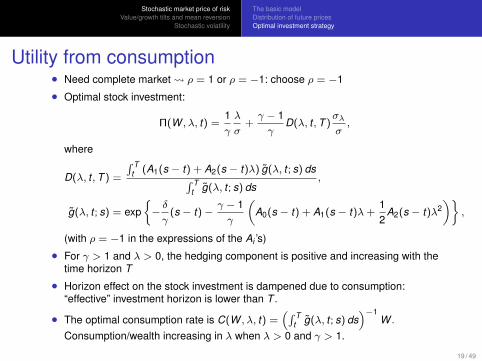

Utility from consumption• Need complete market ρ = 1 or ρ = −1: choose ρ = −1

• Optimal stock investment:

Π(W , λ, t) =1γ

λ

σ+γ − 1γ

D(λ, t ,T )σλ

σ,

where

D(λ, t ,T ) =

∫ Tt (A1(s − t) + A2(s − t)λ) g(λ, t ; s) ds∫ T

t g(λ, t ; s) ds,

g(λ, t ; s) = exp{−δ

γ(s − t)−

γ − 1γ

(A0(s − t) + A1(s − t)λ+

12

A2(s − t)λ2)}

,

(with ρ = −1 in the expressions of the Ai ’s)

• For γ > 1 and λ > 0, the hedging component is positive and increasing with thetime horizon T

• Horizon effect on the stock investment is dampened due to consumption:“effective” investment horizon is lower than T .

• The optimal consumption rate is C(W , λ, t) =(∫ T

t g(λ, t ; s) ds)−1

W .

Consumption/wealth increasing in λ when λ > 0 and γ > 1.

19 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The modelOptimal strategiesSuboptimal strategies

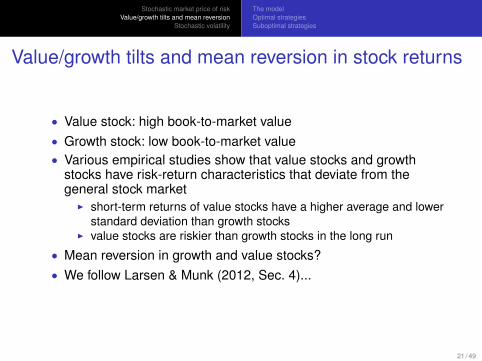

Value/growth tilts and mean reversion in stock returns

• Value stock: high book-to-market value• Growth stock: low book-to-market value• Various empirical studies show that value stocks and growth

stocks have risk-return characteristics that deviate from thegeneral stock market

I short-term returns of value stocks have a higher average and lowerstandard deviation than growth stocks

I value stocks are riskier than growth stocks in the long run

• Mean reversion in growth and value stocks?• We follow Larsen & Munk (2012, Sec. 4)...

21 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The modelOptimal strategiesSuboptimal strategies

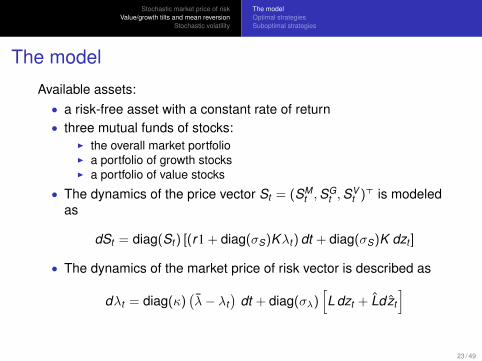

The model

Available assets:• a risk-free asset with a constant rate of return• three mutual funds of stocks:

I the overall market portfolioI a portfolio of growth stocksI a portfolio of value stocks

• The dynamics of the price vector St = (SMt ,S

Gt ,S

Vt )> is modeled

as

dSt = diag(St ) [(r1 + diag(σS)Kλt ) dt + diag(σS)K dzt ]

• The dynamics of the market price of risk vector is described as

dλt = diag(κ)(λ− λt

)dt + diag(σλ)

[L dzt + Ldzt

]

23 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The modelOptimal strategiesSuboptimal strategies

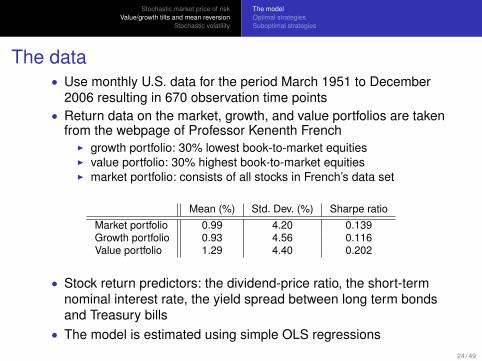

The data• Use monthly U.S. data for the period March 1951 to December

2006 resulting in 670 observation time points• Return data on the market, growth, and value portfolios are taken

from the webpage of Professor Kenenth FrenchI growth portfolio: 30% lowest book-to-market equitiesI value portfolio: 30% highest book-to-market equitiesI market portfolio: consists of all stocks in French’s data set

Mean (%) Std. Dev. (%) Sharpe ratioMarket portfolio 0.99 4.20 0.139Growth portfolio 0.93 4.56 0.116Value portfolio 1.29 4.40 0.202

• Stock return predictors: the dividend-price ratio, the short-termnominal interest rate, the yield spread between long term bondsand Treasury bills

• The model is estimated using simple OLS regressions24 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The modelOptimal strategiesSuboptimal strategies

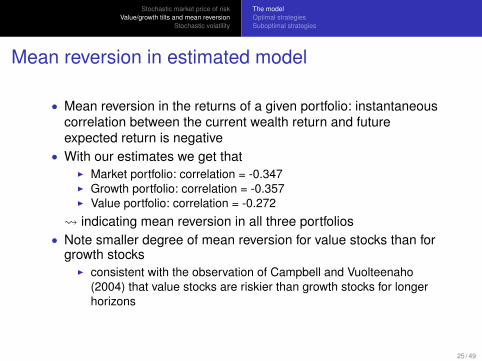

Mean reversion in estimated model

• Mean reversion in the returns of a given portfolio: instantaneouscorrelation between the current wealth return and futureexpected return is negative

• With our estimates we get thatI Market portfolio: correlation = -0.347I Growth portfolio: correlation = -0.357I Value portfolio: correlation = -0.272

indicating mean reversion in all three portfolios• Note smaller degree of mean reversion for value stocks than for

growth stocksI consistent with the observation of Campbell and Vuolteenaho

(2004) that value stocks are riskier than growth stocks for longerhorizons

25 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The modelOptimal strategiesSuboptimal strategies

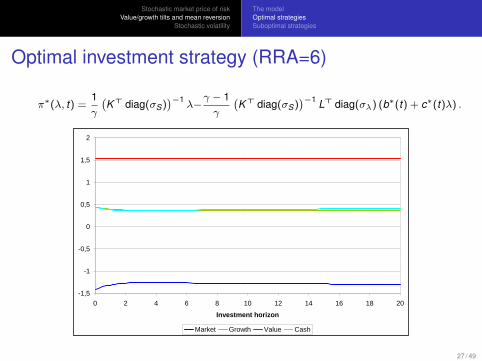

Optimal investment strategy (RRA=6)

π∗(λ, t) =1γ

(K> diag(σS)

)−1λ−

γ − 1γ

(K> diag(σS)

)−1 L> diag(σλ) (b∗(t) + c∗(t)λ) .

-1,5

-1

-0,5

0

0,5

1

1,5

2

0 2 4 6 8 10 12 14 16 18 20

Investment horizon

Market Growth Value Cash

27 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The modelOptimal strategiesSuboptimal strategies

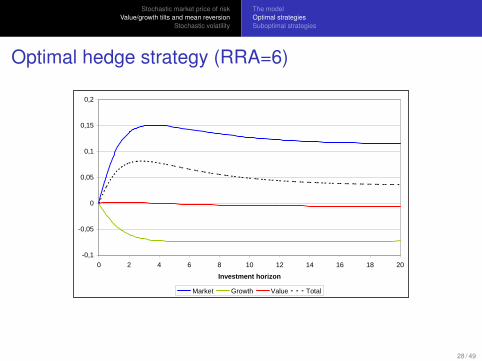

Optimal hedge strategy (RRA=6)

-0,1

-0,05

0

0,05

0,1

0,15

0,2

0 2 4 6 8 10 12 14 16 18 20

Investment horizon

Market Growth Value Total

28 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The modelOptimal strategiesSuboptimal strategies

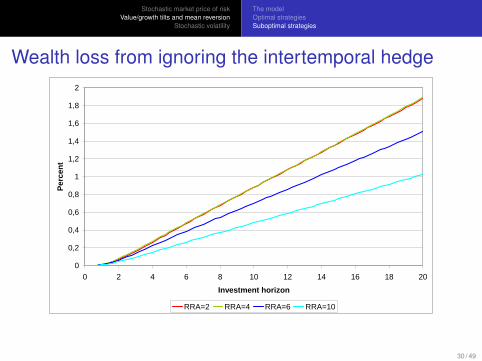

Wealth loss from ignoring the intertemporal hedge

0

0,2

0,4

0,6

0,8

1

1,2

1,4

1,6

1,8

2

0 2 4 6 8 10 12 14 16 18 20

Investment horizon

Per

cen

t

RRA=2 RRA=4 RRA=6 RRA=10

30 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

The modelOptimal strategiesSuboptimal strategies

Wealth loss from omitting assets

• Investors ignoring both value and growth stocks suffer thebiggest loss

I γ = 6, T − t = 10: loss ≈ 38%• Investors ignoring value stocks suffer the second highest loss

I γ = 6, T − t = 10: loss ≈ 28%• Investors ignoring growth stocks suffer the lowest loss

I γ = 6, T − t = 10: loss ≈ 23%

• Hence it is more important to take the special features of valuestocks into account than the features of growth stocks

31 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Model without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

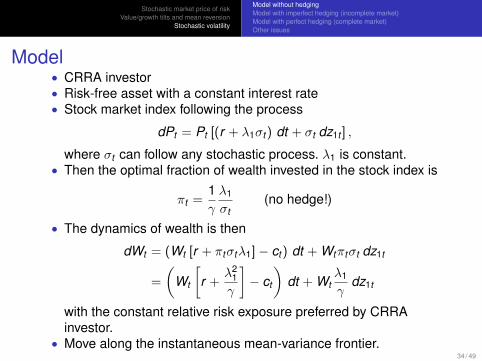

Model• CRRA investor• Risk-free asset with a constant interest rate• Stock market index following the process

dPt = Pt [(r + λ1σt ) dt + σt dz1t ] ,

where σt can follow any stochastic process. λ1 is constant.• Then the optimal fraction of wealth invested in the stock index is

πt =1γ

λ1

σt(no hedge!)

• The dynamics of wealth is then

dWt = (Wt [r + πtσtλ1]− ct ) dt + Wtπtσt dz1t

=

(Wt

[r +

λ21γ

]− ct

)dt + Wt

λ1

γdz1t

with the constant relative risk exposure preferred by CRRAinvestor.

• Move along the instantaneous mean-variance frontier.34 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Model without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

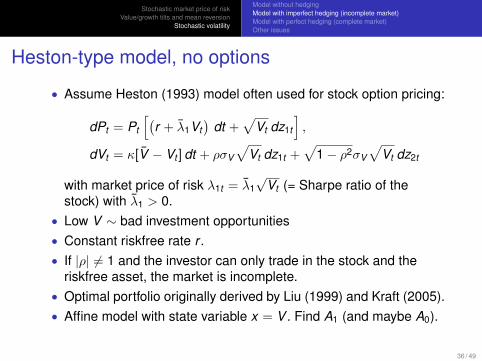

Heston-type model, no options

• Assume Heston (1993) model often used for stock option pricing:

dPt = Pt

[(r + λ1Vt

)dt +

√Vt dz1t

],

dVt = κ[V − Vt ] dt + ρσV

√Vt dz1t +

√1− ρ2σV

√Vt dz2t

with market price of risk λ1t = λ1√

Vt (= Sharpe ratio of thestock) with λ1 > 0.

• Low V ∼ bad investment opportunities• Constant riskfree rate r .• If |ρ| 6= 1 and the investor can only trade in the stock and the

riskfree asset, the market is incomplete.• Optimal portfolio originally derived by Liu (1999) and Kraft (2005).• Affine model with state variable x = V . Find A1 (and maybe A0).

36 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Model without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

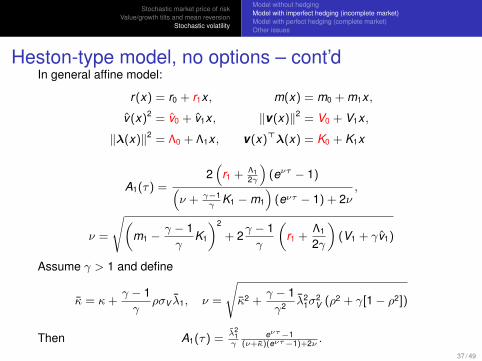

Heston-type model, no options – cont’dIn general affine model:

r(x) = r0 + r1x , m(x) = m0 + m1x ,

v(x)2 = v0 + v1x , ‖v(x)‖2 = V0 + V1x ,

‖λ(x)‖2 = Λ0 + Λ1x , v(x)>λ(x) = K0 + K1x

A1(τ) =2(

r1 + Λ12γ

)(eντ − 1)(

ν + γ−1γ

K1 −m1

)(eντ − 1) + 2ν

,

ν =

√(m1 −

γ − 1γ

K1

)2

+ 2γ − 1γ

(r1 +

Λ1

2γ

)(V1 + γv1)

Assume γ > 1 and define

κ = κ+γ − 1γ

ρσV λ1, ν =

√κ2 +

γ − 1γ2 λ2

1σ2V (ρ2 + γ[1− ρ2])

Then A1(τ) =λ2

1γ

eντ−1(ν+κ)(eντ−1)+2ν .

37 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Model without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

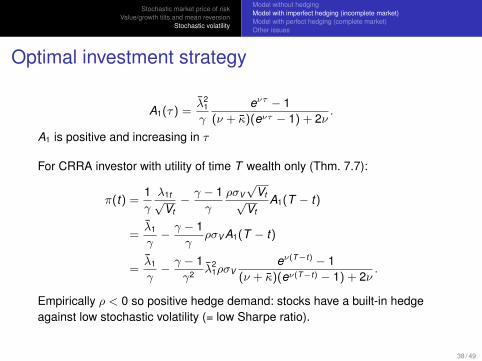

Optimal investment strategy

A1(τ) =λ2

1

γ

eντ − 1(ν + κ)(eντ − 1) + 2ν

.

A1 is positive and increasing in τ

For CRRA investor with utility of time T wealth only (Thm. 7.7):

π(t) =1γ

λ1t√Vt− γ − 1

γ

ρσV√

Vt√Vt

A1(T − t)

=λ1

γ− γ − 1

γρσV A1(T − t)

=λ1

γ− γ − 1

γ2 λ21ρσV

eν(T−t) − 1(ν + κ)(eν(T−t) − 1) + 2ν

.

Empirically ρ < 0 so positive hedge demand: stocks have a built-in hedgeagainst low stochastic volatility (= low Sharpe ratio).

38 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Model without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

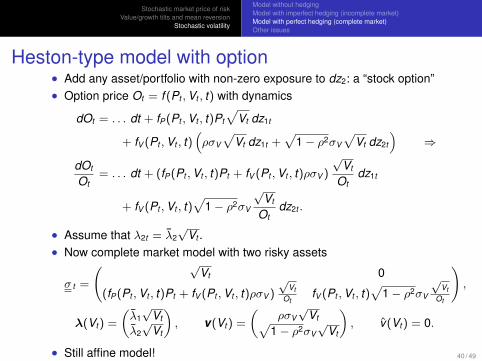

Heston-type model with option• Add any asset/portfolio with non-zero exposure to dz2: a “stock option”• Option price Ot = f (Pt ,Vt , t) with dynamics

dOt = . . . dt + fP(Pt ,Vt , t)Pt

√Vt dz1t

+ fV (Pt ,Vt , t)(ρσV

√Vt dz1t +

√1− ρ2σV

√Vt dz2t

)⇒

dOt

Ot= . . . dt + (fP(Pt ,Vt , t)Pt + fV (Pt ,Vt , t)ρσV )

√Vt

Otdz1t

+ fV (Pt ,Vt , t)√

1− ρ2σV

√Vt

Otdz2t .

• Assume that λ2t = λ2√

Vt .• Now complete market model with two risky assets

σ t =

( √Vt 0

(fP(Pt ,Vt , t)Pt + fV (Pt ,Vt , t)ρσV )

√Vt

OtfV (Pt ,Vt , t)

√1− ρ2σV

√Vt

Ot

),

λ(Vt ) =

(λ1√

Vt

λ2√

Vt

), v(Vt ) =

(ρσV√

Vt√1− ρ2σV

√Vt

), v(Vt ) = 0.

• Still affine model! 40 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Model without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

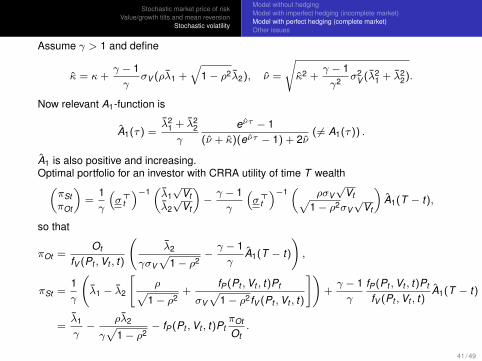

Assume γ > 1 and define

κ = κ+γ − 1γ

σV (ρλ1 +√

1− ρ2λ2), ν =

√κ2 +

γ − 1γ2

σ2V (λ2

1 + λ22).

Now relevant A1-function is

A1(τ) =λ2

1 + λ22

γ

eντ − 1(ν + κ)(eντ − 1) + 2ν

( 6= A1(τ)) .

A1 is also positive and increasing.Optimal portfolio for an investor with CRRA utility of time T wealth(

πStπOt

)=

1γ

(σ>

t

)−1(λ1√

Vtλ2√

Vt

)−γ − 1γ

(σ>

t

)−1(

ρσV√

Vt√1− ρ2σV

√Vt

)A1(T − t),

so that

πOt =Ot

fV (Pt ,Vt , t)

(λ2

γσV√

1− ρ2−γ − 1γ

A1(T − t)

),

πSt =1γ

(λ1 − λ2

[ρ√

1− ρ2+

fP(Pt ,Vt , t)Pt

σV√

1− ρ2fV (Pt ,Vt , t)

])+γ − 1γ

fP(Pt ,Vt , t)Pt

fV (Pt ,Vt , t)A1(T − t)

=λ1

γ−

ρλ2

γ√

1− ρ2− fP(Pt ,Vt , t)Pt

πOt

Ot.

41 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Model without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

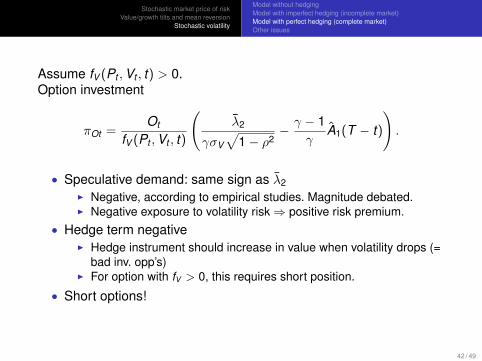

Assume fV (Pt ,Vt , t) > 0.Option investment

πOt =Ot

fV (Pt ,Vt , t)

(λ2

γσV√

1− ρ2− γ − 1

γA1(T − t)

).

• Speculative demand: same sign as λ2I Negative, according to empirical studies. Magnitude debated.I Negative exposure to volatility risk⇒ positive risk premium.

• Hedge term negativeI Hedge instrument should increase in value when volatility drops (=

bad inv. opp’s)I For option with fV > 0, this requires short position.

• Short options!

42 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Model without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

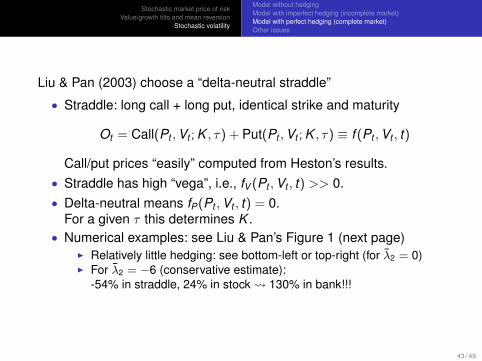

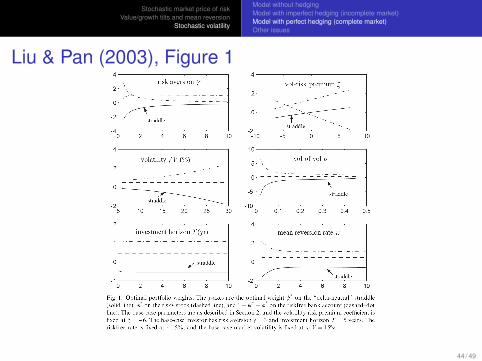

Liu & Pan (2003) choose a “delta-neutral straddle”

• Straddle: long call + long put, identical strike and maturity

Ot = Call(Pt ,Vt ; K , τ) + Put(Pt ,Vt ; K , τ) ≡ f (Pt ,Vt , t)

Call/put prices “easily” computed from Heston’s results.• Straddle has high “vega”, i.e., fV (Pt ,Vt , t) >> 0.• Delta-neutral means fP(Pt ,Vt , t) = 0.

For a given τ this determines K .• Numerical examples: see Liu & Pan’s Figure 1 (next page)

I Relatively little hedging: see bottom-left or top-right (for λ2 = 0)I For λ2 = −6 (conservative estimate):

-54% in straddle, 24% in stock 130% in bank!!!

43 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Model without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

Liu & Pan (2003), Figure 1

44 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Model without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

Losses from suboptimal strategies

See Liu & Pan (2003) and Larsen & Munk (2012)

• Important to include options in the speculative portfolio becauseof the apparently very attractive risk-return tradeoff

I highly depending on the estimate of λ2!• Relatively little is gained by the intertemporal hedge

I highly depending on the functional form assumed for the marketprices of risk

45 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Model without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

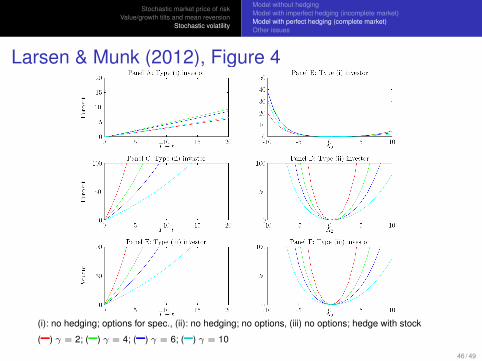

Larsen & Munk (2012), Figure 4

(i): no hedging; options for spec., (ii): no hedging; no options, (iii) no options; hedge with stock

(–) γ = 2; (–) γ = 4; (–) γ = 6; (–) γ = 10

46 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Model without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

Jumps

• Liu & Pan allow for jumps of given size (large negative, “crash”)I Jump arrival intensity proportional to VtI Need estimate of jump risk premium (high?)I Need another jump-sensitive option to complete the market, e.g.,

an out-of-the-money putI Affine jump-diffusion type model closed-form solutionI Their Table 1 shows that the optimal put position is very sensitive to

assumed jump parameters

• Jumps of many possible sizes need more options to completethe market

• Jumps in volatility?Liu, Longstaff & Pan (2003), Branger, Schlag & Schneider (2008)

• Need to learn more about theoretical asset pricing withstochastic volatility and jumps to understand the relevant marketprices of risk!

48 / 49

Stochastic market price of riskValue/growth tilts and mean reversion

Stochastic volatility

Model without hedgingModel with imperfect hedging (incomplete market)Model with perfect hedging (complete market)Other issues

Related issues

• Correlation risk: correlations vary stochasticallyMarkets move together in bad times⇒ diversification lesseffectiveSee Buraschi, Porchia & Trojani (2009, JF)

• Contagion: events in one market may directly influence othermarketsSee Branger, Kraft & Meinerding (2009, InsMathEcon)

• Unspanned stochastic bond volatilitySee Trolle (2009, wp)

49 / 49

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Dynamic Asset AllocationChapter 13: Labor income

Claus Munk

August 2012

AARHUS UNIVERSITY AU

1 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Outline

1 Introduction

2 Merton with income

3 Constraints and better income model

4 Interest rate risk and labor income

2 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Labor income

• Primary source of funds for savings/investments for mostindividuals

• Total wealth = financial wealth + human capital• Human capital is LARGE for young individuals

With a real interest rate of 1% and a constant annual income of300.000 for 30 years, human capital equals 7.7 millions

• The optimal financial investment will depend onI the magnitude of human capital,I the uncertainty of labor income, andI the correlation between labor income and asset prices

• Obvious horizon effects in human capital — life-cycle perspective

4 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

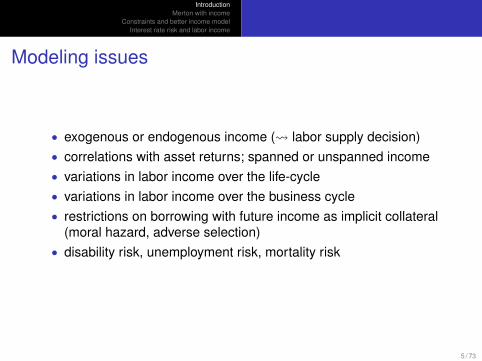

Modeling issues

• exogenous or endogenous income ( labor supply decision)• correlations with asset returns; spanned or unspanned income• variations in labor income over the life-cycle• variations in labor income over the business cycle• restrictions on borrowing with future income as implicit collateral

(moral hazard, adverse selection)• disability risk, unemployment risk, mortality risk

5 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

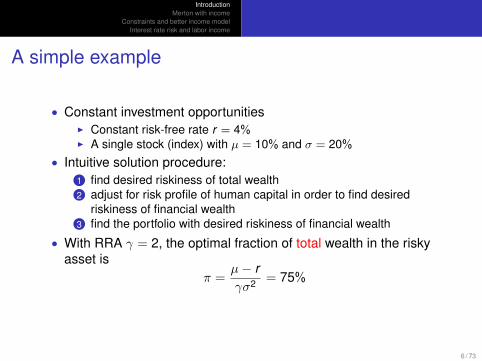

A simple example

• Constant investment opportunitiesI Constant risk-free rate r = 4%I A single stock (index) with µ = 10% and σ = 20%

• Intuitive solution procedure:1 find desired riskiness of total wealth2 adjust for risk profile of human capital in order to find desired

riskiness of financial wealth3 find the portfolio with desired riskiness of financial wealth

• With RRA γ = 2, the optimal fraction of total wealth in the riskyasset is

π =µ− rγσ2 = 75%

6 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

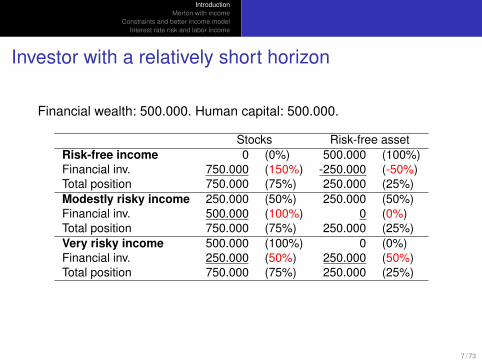

Investor with a relatively short horizon

Financial wealth: 500.000. Human capital: 500.000.

Stocks Risk-free assetRisk-free income 0 (0%) 500.000 (100%)Financial inv. 750.000 (150%) -250.000 (-50%)Total position 750.000 (75%) 250.000 (25%)Modestly risky income 250.000 (50%) 250.000 (50%)Financial inv. 500.000 (100%) 0 (0%)Total position 750.000 (75%) 250.000 (25%)Very risky income 500.000 (100%) 0 (0%)Financial inv. 250.000 (50%) 250.000 (50%)Total position 750.000 (75%) 250.000 (25%)

7 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

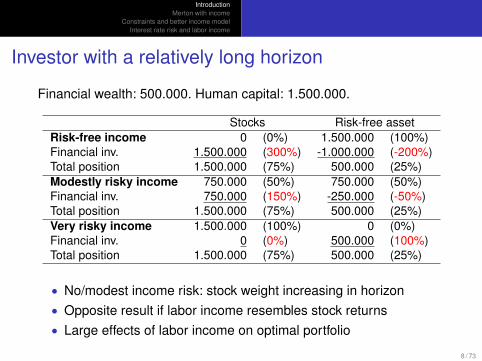

Investor with a relatively long horizon

Financial wealth: 500.000. Human capital: 1.500.000.

Stocks Risk-free assetRisk-free income 0 (0%) 1.500.000 (100%)Financial inv. 1.500.000 (300%) -1.000.000 (-200%)Total position 1.500.000 (75%) 500.000 (25%)Modestly risky income 750.000 (50%) 750.000 (50%)Financial inv. 750.000 (150%) -250.000 (-50%)Total position 1.500.000 (75%) 500.000 (25%)Very risky income 1.500.000 (100%) 0 (0%)Financial inv. 0 (0%) 500.000 (100%)Total position 1.500.000 (75%) 500.000 (25%)

• No/modest income risk: stock weight increasing in horizon• Opposite result if labor income resembles stock returns• Large effects of labor income on optimal portfolio

8 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Exogenous incomeEndogenous income

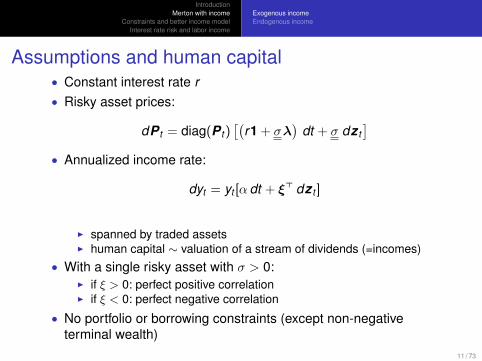

Assumptions and human capital• Constant interest rate r• Risky asset prices:

dP t = diag(P t )[(

r1 + σλ)

dt + σ dz t]

• Annualized income rate:

dyt = yt [α dt + ξ> dz t ]

I spanned by traded assetsI human capital ∼ valuation of a stream of dividends (=incomes)

• With a single risky asset with σ > 0:I if ξ > 0: perfect positive correlationI if ξ < 0: perfect negative correlation

• No portfolio or borrowing constraints (except non-negativeterminal wealth)

11 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Exogenous incomeEndogenous income

Human capital with spanned income

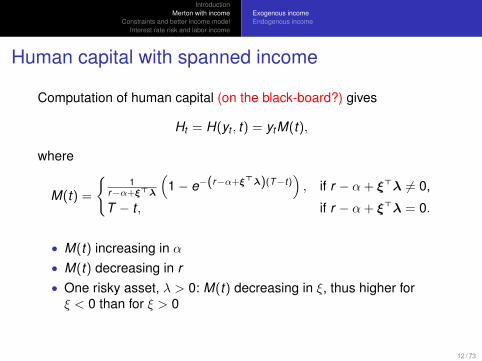

Computation of human capital (on the black-board?) gives

Ht = H(yt , t) = ytM(t),

where

M(t) =

{1

r−α+ξ>λ

(1− e−(r−α+ξ>λ)(T−t)

), if r − α + ξ>λ 6= 0,

T − t , if r − α + ξ>λ = 0.

• M(t) increasing in α• M(t) decreasing in r• One risky asset, λ > 0: M(t) decreasing in ξ, thus higher forξ < 0 than for ξ > 0

12 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Exogenous incomeEndogenous income

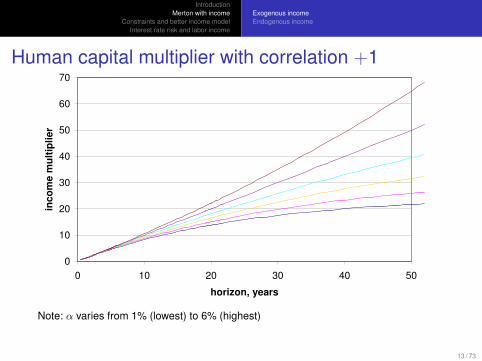

Human capital multiplier with correlation +1

0

10

20

30

40

50

60

70

0 10 20 30 40 50

horizon, years

inco

me m

ult

ipli

er

Note: α varies from 1% (lowest) to 6% (highest)

13 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Exogenous incomeEndogenous income

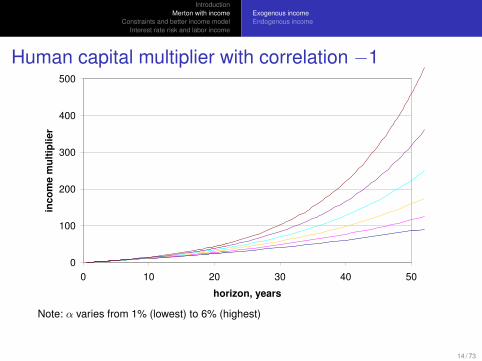

Human capital multiplier with correlation −1

0

100

200

300

400

500

0 10 20 30 40 50

horizon, years

inco

me m

ult

ipli

er

Note: α varies from 1% (lowest) to 6% (highest)

14 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Exogenous incomeEndogenous income

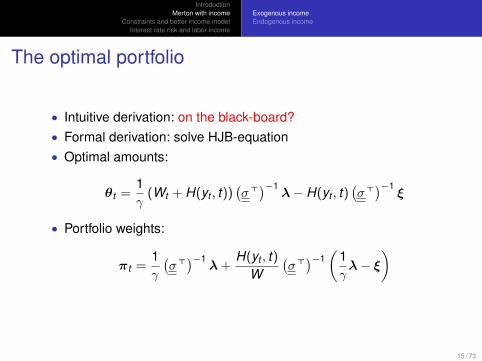

The optimal portfolio

• Intuitive derivation: on the black-board?• Formal derivation: solve HJB-equation• Optimal amounts:

θt =1γ

(Wt + H(yt , t))(σ>)−1

λ− H(yt , t)(σ>)−1

ξ

• Portfolio weights:

πt =1γ

(σ>)−1

λ +H(yt , t)

W(σ>)−1

(1γλ− ξ

)

15 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Exogenous incomeEndogenous income

The optimal portfolio

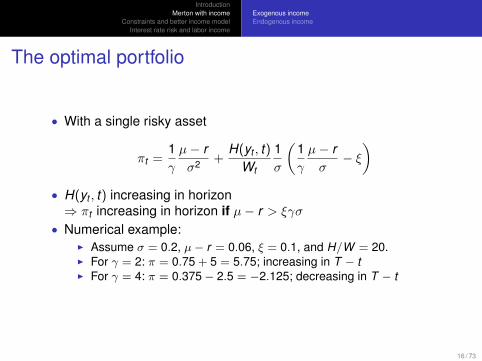

• With a single risky asset

πt =1γ

µ− rσ2 +

H(yt , t)Wt

1σ

(1γ

µ− rσ− ξ)

• H(yt , t) increasing in horizon⇒ πt increasing in horizon if µ− r > ξγσ

• Numerical example:I Assume σ = 0.2, µ− r = 0.06, ξ = 0.1, and H/W = 20.I For γ = 2: π = 0.75 + 5 = 5.75; increasing in T − tI For γ = 4: π = 0.375− 2.5 = −2.125; decreasing in T − t

16 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Exogenous incomeEndogenous income

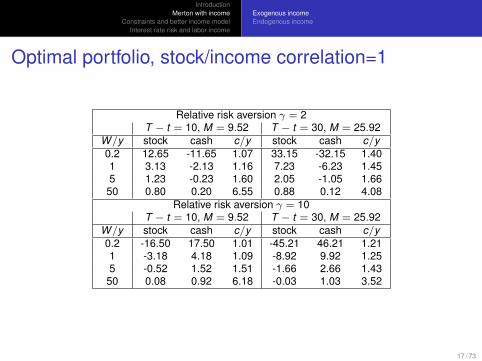

Optimal portfolio, stock/income correlation=1

Relative risk aversion γ = 2T − t = 10, M = 9.52 T − t = 30, M = 25.92

W/y stock cash c/y stock cash c/y0.2 12.65 -11.65 1.07 33.15 -32.15 1.401 3.13 -2.13 1.16 7.23 -6.23 1.455 1.23 -0.23 1.60 2.05 -1.05 1.66

50 0.80 0.20 6.55 0.88 0.12 4.08Relative risk aversion γ = 10

T − t = 10, M = 9.52 T − t = 30, M = 25.92W/y stock cash c/y stock cash c/y0.2 -16.50 17.50 1.01 -45.21 46.21 1.211 -3.18 4.18 1.09 -8.92 9.92 1.255 -0.52 1.52 1.51 -1.66 2.66 1.43

50 0.08 0.92 6.18 -0.03 1.03 3.52

17 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Exogenous incomeEndogenous income

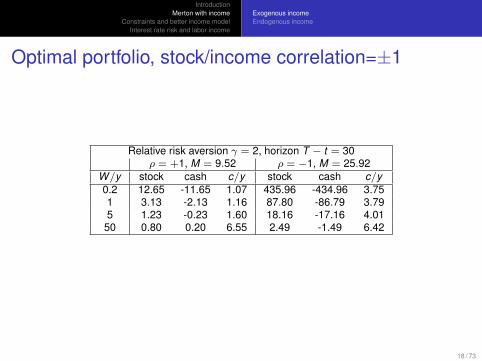

Optimal portfolio, stock/income correlation=±1

Relative risk aversion γ = 2, horizon T − t = 30ρ = +1, M = 9.52 ρ = −1, M = 25.92

W/y stock cash c/y stock cash c/y0.2 12.65 -11.65 1.07 435.96 -434.96 3.751 3.13 -2.13 1.16 87.80 -86.79 3.795 1.23 -0.23 1.60 18.16 -17.16 4.01

50 0.80 0.20 6.55 2.49 -1.49 6.42

18 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Exogenous incomeEndogenous income

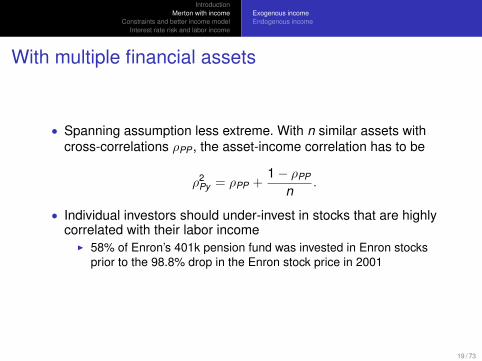

With multiple financial assets

• Spanning assumption less extreme. With n similar assets withcross-correlations ρPP , the asset-income correlation has to be

ρ2Py = ρPP +

1− ρPP

n.

• Individual investors should under-invest in stocks that are highlycorrelated with their labor income

I 58% of Enron’s 401k pension fund was invested in Enron stocksprior to the 98.8% drop in the Enron stock price in 2001

19 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Exogenous incomeEndogenous income

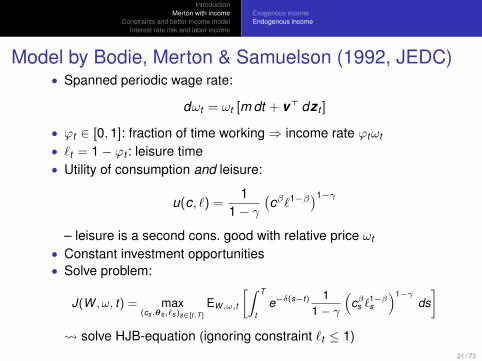

Model by Bodie, Merton & Samuelson (1992, JEDC)• Spanned periodic wage rate:

dωt = ωt [m dt + v> dz t ]

• ϕt ∈ [0,1]: fraction of time working⇒ income rate ϕtωt

• `t = 1− ϕt : leisure time• Utility of consumption and leisure:

u(c, `) =1

1− γ(cβ`1−β)1−γ

– leisure is a second cons. good with relative price ωt

• Constant investment opportunities• Solve problem:

J(W , ω, t) = max(cs,θs,`s)s∈[t,T ]

EW ,ω,t

[∫ T

te−δ(s−t) 1

1− γ

(cβs `

1−βs

)1−γds]

solve HJB-equation (ignoring constraint `t ≤ 1)21 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Exogenous incomeEndogenous income

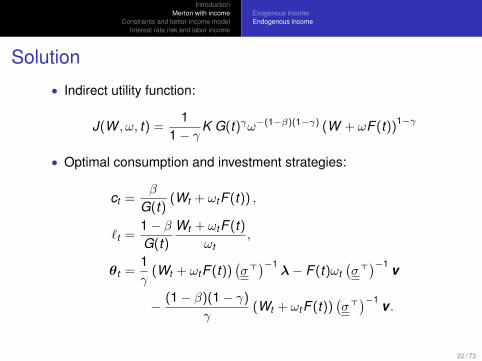

Solution

• Indirect utility function:

J(W , ω, t) =1

1− γK G(t)γω−(1−β)(1−γ) (W + ωF (t))1−γ

• Optimal consumption and investment strategies:

ct =β

G(t)(Wt + ωtF (t)) ,

`t =1− βG(t)

Wt + ωtF (t)ωt

,

θt =1γ

(Wt + ωtF (t))(σ>)−1

λ− F (t)ωt(σ>)−1 v

− (1− β)(1− γ)

γ(Wt + ωtF (t))

(σ>)−1 v .

22 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Exogenous incomeEndogenous income

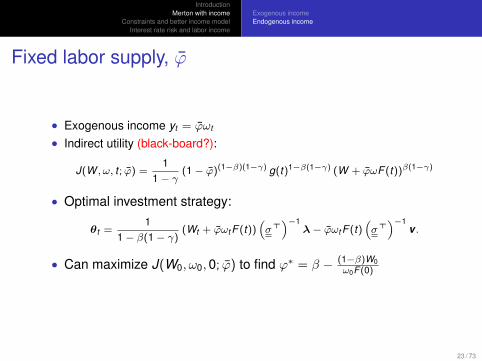

Fixed labor supply, ϕ

• Exogenous income yt = ϕωt

• Indirect utility (black-board?):

J(W , ω, t ; ϕ) =1

1 − γ(1 − ϕ)(1−β)(1−γ) g(t)1−β(1−γ) (W + ϕωF (t))β(1−γ)

• Optimal investment strategy:

θt =1

1 − β(1 − γ)(Wt + ϕωt F (t))

(σ>)−1

λ− ϕωt F (t)(σ>)−1

v .

• Can maximize J(W0, ω0,0; ϕ) to find ϕ∗ = β − (1−β)W0ω0F (0)

23 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Exogenous incomeEndogenous income

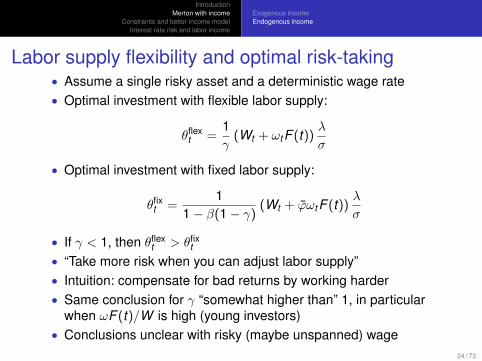

Labor supply flexibility and optimal risk-taking• Assume a single risky asset and a deterministic wage rate• Optimal investment with flexible labor supply:

θflext =

1γ

(Wt + ωtF (t))λ

σ

• Optimal investment with fixed labor supply:

θfixt =

11− β(1− γ)

(Wt + ϕωtF (t))λ

σ

• If γ < 1, then θflext > θfix

t

• “Take more risk when you can adjust labor supply”• Intuition: compensate for bad returns by working harder• Same conclusion for γ “somewhat higher than” 1, in particular

when ωF (t)/W is high (young investors)• Conclusions unclear with risky (maybe unspanned) wage

24 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Models should be improvedThe Cocco-Gomes-Maenhout paper

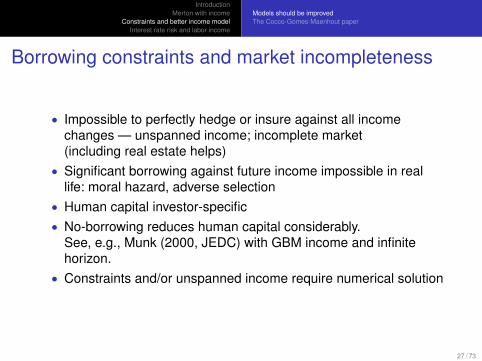

Borrowing constraints and market incompleteness

• Impossible to perfectly hedge or insure against all incomechanges — unspanned income; incomplete market(including real estate helps)

• Significant borrowing against future income impossible in reallife: moral hazard, adverse selection

• Human capital investor-specific• No-borrowing reduces human capital considerably.

See, e.g., Munk (2000, JEDC) with GBM income and infinitehorizon.

• Constraints and/or unspanned income require numerical solution

27 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Models should be improvedThe Cocco-Gomes-Maenhout paper

Income variations over life cycle and business cycle

• Life cycle [discrete time]:Cocco, Gomes & Maenhout, “Consumption and Portfolio Choiceover the Life Cycle”, Review of Financial Studies, 2005.

• Life and business cycle [interest rates, cont. time]:Munk & Sørensen, “Dynamic Asset Allocation with StochasticIncome and Interest Rates”, Journal of Financial Economics,2010.

• Life and business cycle [dividend yield, discrete time]:Lynch & Tan, “Labor Income Dynamics at Business-CycleFrequencies”, Journal of Financial Economics, forthcoming.

28 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Models should be improvedThe Cocco-Gomes-Maenhout paper

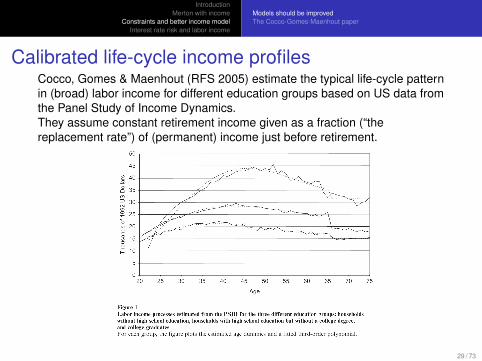

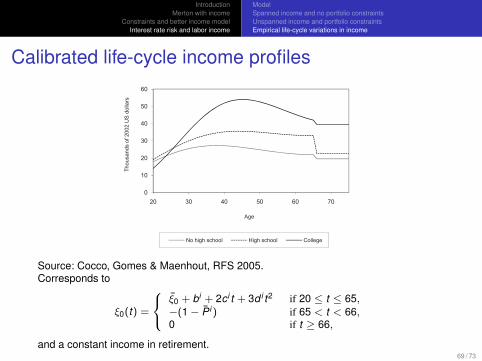

Calibrated life-cycle income profilesCocco, Gomes & Maenhout (RFS 2005) estimate the typical life-cycle patternin (broad) labor income for different education groups based on US data fromthe Panel Study of Income Dynamics.They assume constant retirement income given as a fraction (“thereplacement rate”) of (permanent) income just before retirement.

29 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Models should be improvedThe Cocco-Gomes-Maenhout paper

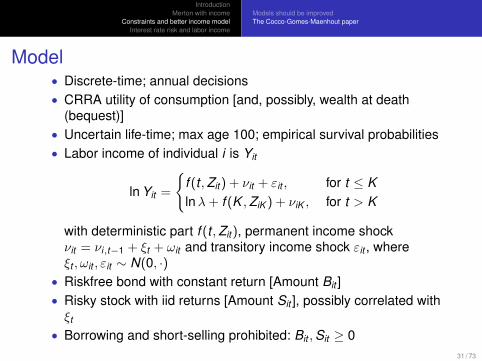

Model• Discrete-time; annual decisions• CRRA utility of consumption [and, possibly, wealth at death

(bequest)]• Uncertain life-time; max age 100; empirical survival probabilities• Labor income of individual i is Yit

ln Yit =

{f (t ,Zit ) + νit + εit , for t ≤ Klnλ+ f (K ,ZiK ) + νiK , for t > K

with deterministic part f (t ,Zit ), permanent income shockνit = νi,t−1 + ξt + ωit and transitory income shock εit , whereξt , ωit , εit ∼ N(0, ·)

• Riskfree bond with constant return [Amount Bit ]• Risky stock with iid returns [Amount Sit ], possibly correlated withξt

• Borrowing and short-selling prohibited: Bit ,Sit ≥ 031 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Models should be improvedThe Cocco-Gomes-Maenhout paper

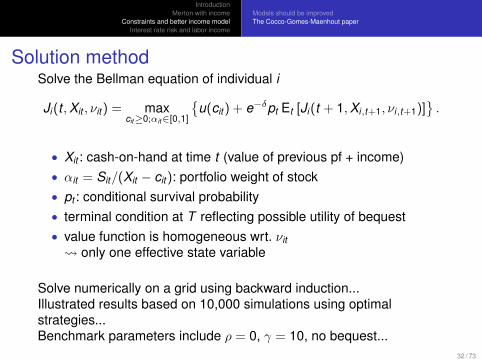

Solution methodSolve the Bellman equation of individual i

Ji (t ,Xit , νit ) = maxcit≥0;αit∈[0,1]

{u(cit ) + e−δpt Et [Ji (t + 1,Xi,t+1, νi,t+1)]

}.

• Xit : cash-on-hand at time t (value of previous pf + income)• αit = Sit/(Xit − cit ): portfolio weight of stock• pt : conditional survival probability• terminal condition at T reflecting possible utility of bequest• value function is homogeneous wrt. νit only one effective state variable

Solve numerically on a grid using backward induction...Illustrated results based on 10,000 simulations using optimalstrategies...Benchmark parameters include ρ = 0, γ = 10, no bequest...

32 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Models should be improvedThe Cocco-Gomes-Maenhout paper

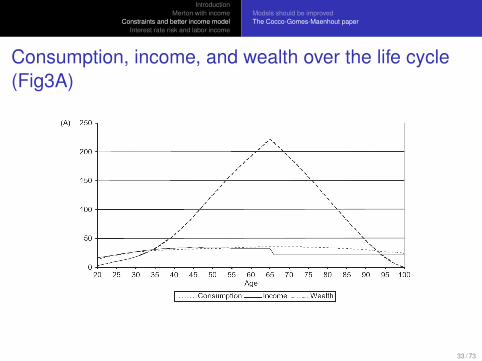

Consumption, income, and wealth over the life cycle(Fig3A)

33 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Models should be improvedThe Cocco-Gomes-Maenhout paper

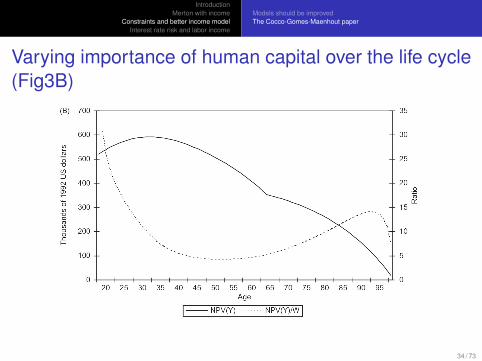

Varying importance of human capital over the life cycle(Fig3B)

34 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Models should be improvedThe Cocco-Gomes-Maenhout paper

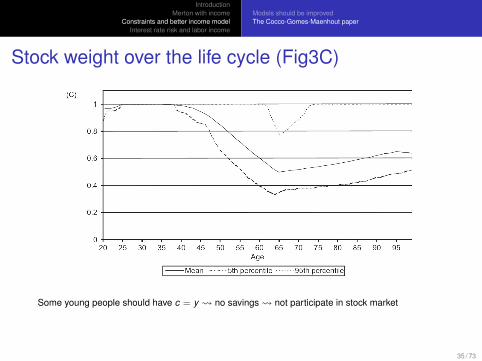

Stock weight over the life cycle (Fig3C)

Some young people should have c = y no savings not participate in stock market

35 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Models should be improvedThe Cocco-Gomes-Maenhout paper

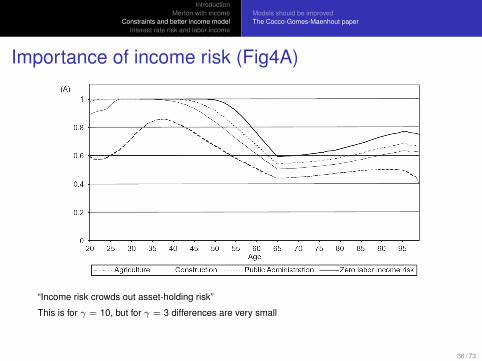

Importance of income risk (Fig4A)

“Income risk crowds out asset-holding risk”

This is for γ = 10, but for γ = 3 differences are very small

36 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Models should be improvedThe Cocco-Gomes-Maenhout paper

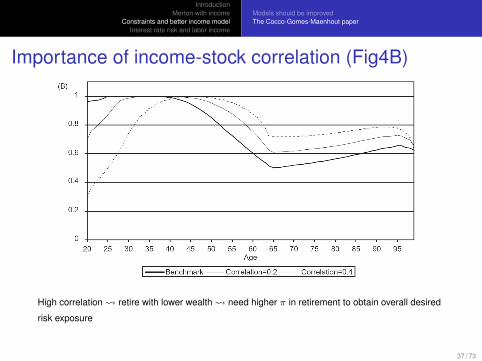

Importance of income-stock correlation (Fig4B)

High correlation retire with lower wealth need higher π in retirement to obtain overall desired

risk exposure

37 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Models should be improvedThe Cocco-Gomes-Maenhout paper

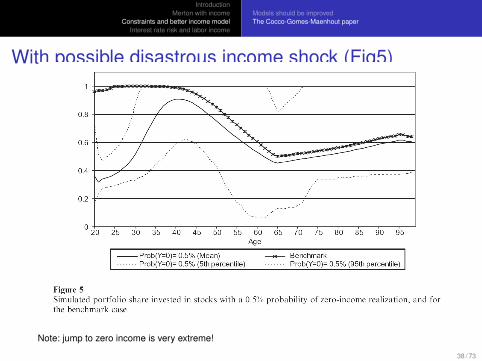

With possible disastrous income shock (Fig5)

Note: jump to zero income is very extreme!

38 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Models should be improvedThe Cocco-Gomes-Maenhout paper

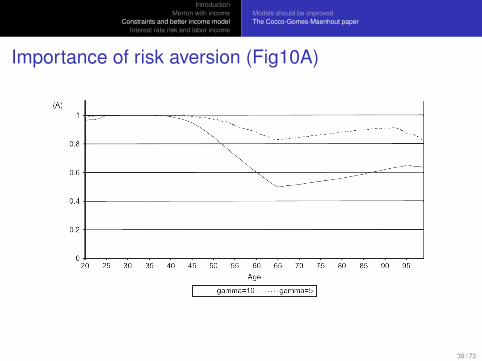

Importance of risk aversion (Fig10A)

39 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

Models should be improvedThe Cocco-Gomes-Maenhout paper

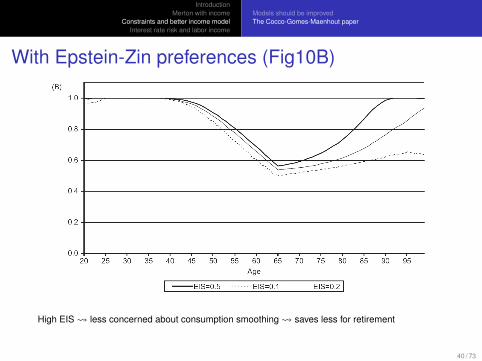

With Epstein-Zin preferences (Fig10B)

High EIS less concerned about consumption smoothing saves less for retirement

40 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

Labor income and interest rate uncertainty

• Reference: Munk & Sørensen (JFE 2010)• The paper combines two important features of long-term portfolio

choiceI labor incomeI business cycle variations in investment opportunities: real interest

rates (fixed market prices of risk)• The paper studies optimal stock/bond/cash allocation with labor

incomeI bonds and stocks correlate differently with labor incomeI invest in bonds to hedge total wealth (including human wealth)

against interest rate riskI labor income growth related to interest rate (business cycle): does

human wealth replace a long-term coupon bond or cash?

42 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

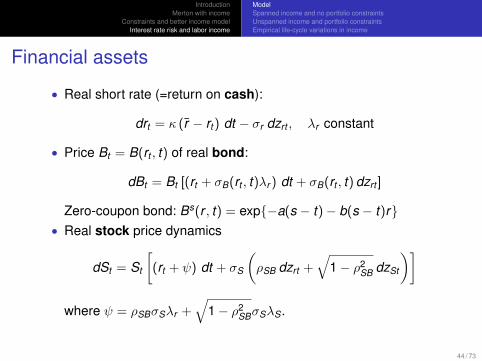

Financial assets

• Real short rate (=return on cash):

drt = κ (r − rt ) dt − σr dzrt , λr constant

• Price Bt = B(rt , t) of real bond:

dBt = Bt [(rt + σB(rt , t)λr ) dt + σB(rt , t) dzrt ]

Zero-coupon bond: Bs(r , t) = exp{−a(s − t)− b(s − t)r}• Real stock price dynamics

dSt = St

[(rt + ψ) dt + σS

(ρSB dzrt +

√1− ρ2

SB dzSt

)]

where ψ = ρSBσSλr +√

1− ρ2SBσSλS.

44 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

Labor income

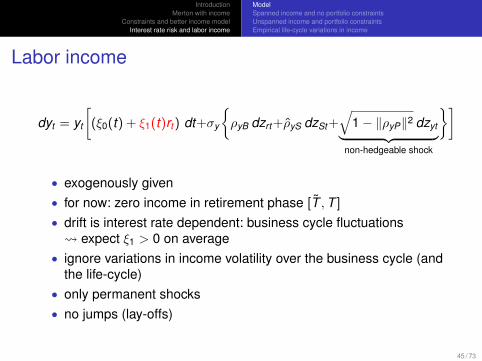

dyt = yt

[(ξ0(t) + ξ1(t)rt ) dt+σy

{ρyB dzrt +ρyS dzSt +

√1− ‖ρyP‖2 dzyt︸ ︷︷ ︸

non-hedgeable shock

}]

• exogenously given• for now: zero income in retirement phase [T ,T ]

• drift is interest rate dependent: business cycle fluctuations expect ξ1 > 0 on average

• ignore variations in income volatility over the business cycle (andthe life-cycle)

• only permanent shocks• no jumps (lay-offs)

45 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

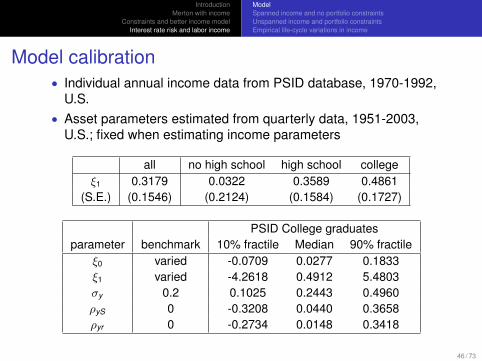

Model calibration• Individual annual income data from PSID database, 1970-1992,

U.S.• Asset parameters estimated from quarterly data, 1951-2003,

U.S.; fixed when estimating income parameters

all no high school high school collegeξ1 0.3179 0.0322 0.3589 0.4861

(S.E.) (0.1546) (0.2124) (0.1584) (0.1727)

PSID College graduatesparameter benchmark 10% fractile Median 90% fractile

ξ0 varied -0.0709 0.0277 0.1833ξ1 varied -4.2618 0.4912 5.4803σy 0.2 0.1025 0.2443 0.4960ρyS 0 -0.3208 0.0440 0.3658ρyr 0 -0.2734 0.0148 0.3418

46 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

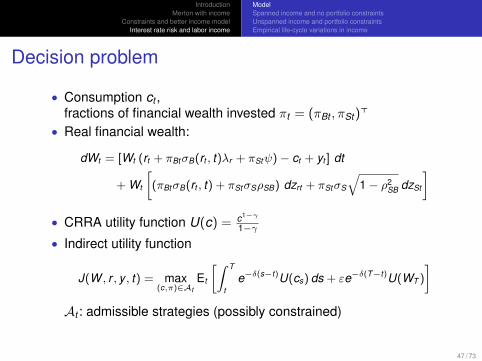

Decision problem

• Consumption ct ,fractions of financial wealth invested πt = (πBt , πSt )

>

• Real financial wealth:

dWt = [Wt (rt + πBtσB(rt , t)λr + πStψ)− ct + yt ] dt

+ Wt

[(πBtσB(rt , t) + πStσSρSB) dzrt + πStσS

√1− ρ2

SB dzSt

]• CRRA utility function U(c) = c1−γ

1−γ

• Indirect utility function

J(W , r , y , t) = max(c,π)∈At

Et

[∫ T

te−δ(s−t)U(cs) ds + εe−δ(T−t)U(WT )

]At : admissible strategies (possibly constrained)

47 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

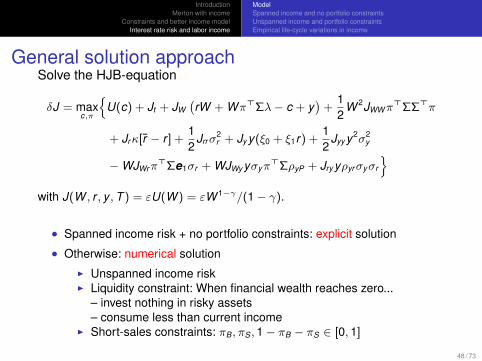

General solution approachSolve the HJB-equation

δJ = maxc,π

{U(c) + Jt + JW

(rW + Wπ>Σλ− c + y

)+

12

W 2JWWπ>ΣΣ>π

+ Jrκ[r − r ] +12

Jrrσ2r + Jy y(ξ0 + ξ1r) +

12

Jyy y2σ2y

−WJWrπ>Σe1σr + WJWy yσyπ

>ΣρyP + Jry yρyrσyσr

}with J(W , r , y ,T ) = εU(W ) = εW 1−γ/(1− γ).

• Spanned income risk + no portfolio constraints: explicit solution

• Otherwise: numerical solutionI Unspanned income riskI Liquidity constraint: When financial wealth reaches zero...

– invest nothing in risky assets– consume less than current income

I Short-sales constraints: πB, πS , 1− πB − πS ∈ [0, 1]

48 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

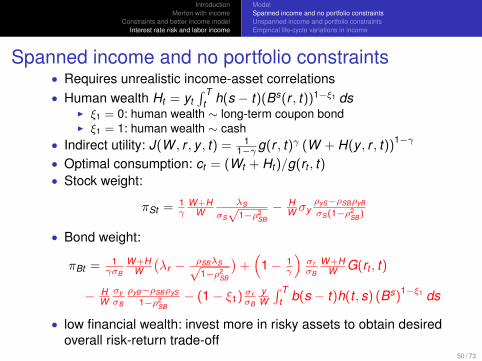

Spanned income and no portfolio constraints• Requires unrealistic income-asset correlations• Human wealth Ht = yt

∫ Tt h(s − t)(Bs(r , t))1−ξ1 ds

I ξ1 = 0: human wealth ∼ long-term coupon bondI ξ1 = 1: human wealth ∼ cash

• Indirect utility: J(W , r , y , t) = 11−γg(r , t)γ (W + H(y , r , t))1−γ

• Optimal consumption: ct = (Wt + Ht )/g(rt , t)• Stock weight:

πSt = 1γ

W +HW

λS

σS

√1−ρ2

SB

− HW σy

ρyS−ρSBρyB

σS(1−ρ2SB)

• Bond weight:

πBt = 1γσB

W +HW

(λr − ρSBλS√

1−ρ2SB

)+(

1− 1γ

)σrσB

W +HW G(rt , t)

− HWσyσB

ρyB−ρSBρyS

1−ρ2SB− (1− ξ1) σr

σB

yW

∫ Tt b(s − t)h(t , s) (Bs)1−ξ1 ds

• low financial wealth: invest more in risky assets to obtain desiredoverall risk-return trade-off

50 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

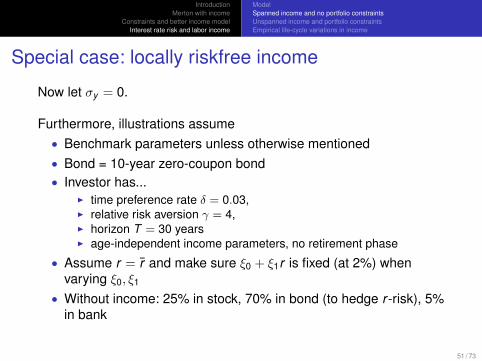

Special case: locally riskfree income

Now let σy = 0.

Furthermore, illustrations assume• Benchmark parameters unless otherwise mentioned• Bond = 10-year zero-coupon bond• Investor has...

I time preference rate δ = 0.03,I relative risk aversion γ = 4,I horizon T = 30 yearsI age-independent income parameters, no retirement phase

• Assume r = r and make sure ξ0 + ξ1r is fixed (at 2%) whenvarying ξ0, ξ1

• Without income: 25% in stock, 70% in bond (to hedge r -risk), 5%in bank

51 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

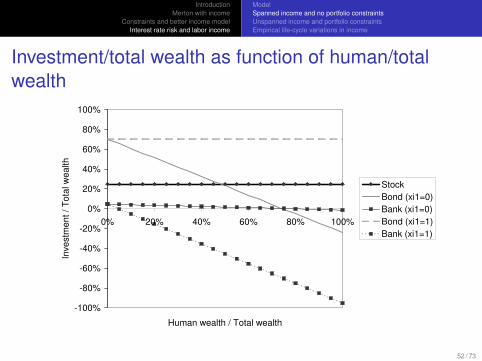

Investment/total wealth as function of human/totalwealth

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

Human wealth / Total wealth

Inve

stm

en

t /

Tota

l w

ealth

Stock

Bond (xi1=0)

Bank (xi1=0)

Bond (xi1=1)

Bank (xi1=1)

52 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

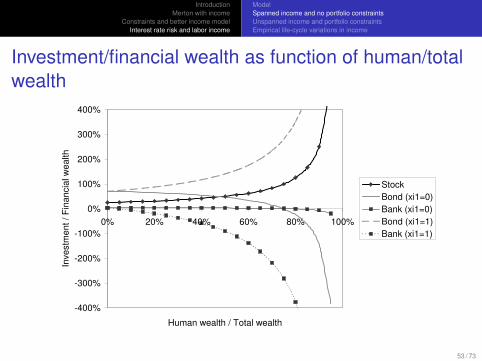

Investment/financial wealth as function of human/totalwealth

-400%

-300%

-200%

-100%

0%

100%

200%

300%

400%

0% 20% 40% 60% 80% 100%

Human wealth / Total wealth

Inve

stm

en

t /

Fin

ancia

l w

ea

lth

Stock

Bond (xi1=0)

Bank (xi1=0)

Bond (xi1=1)

Bank (xi1=1)

53 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

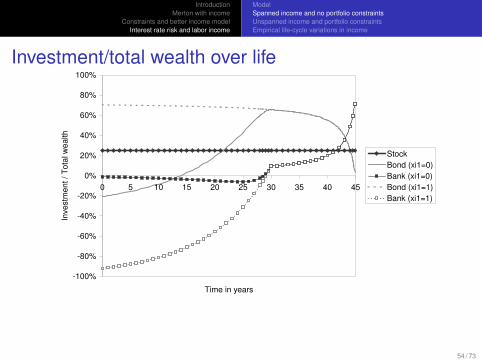

Investment/total wealth over life

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

0 5 10 15 20 25 30 35 40 45

Time in years

Inve

stm

en

t / T

ota

l w

ea

lth

Stock

Bond (xi1=0)

Bank (xi1=0)

Bond (xi1=1)

Bank (xi1=1)

54 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

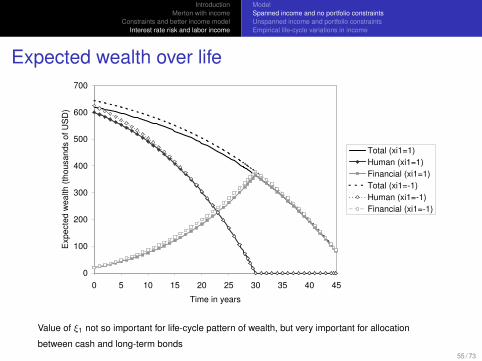

Expected wealth over life

0

100

200

300

400

500

600

700

0 5 10 15 20 25 30 35 40 45

Time in years

Exp

ecte

d w

ea

lth

(th

ou

sa

nd

s o

f U

SD

)

Total (xi1=1)

Human (xi1=1)

Financial (xi1=1)

Total (xi1=-1)

Human (xi1=-1)

Financial (xi1=-1)

Value of ξ1 not so important for life-cycle pattern of wealth, but very important for allocation

between cash and long-term bonds55 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

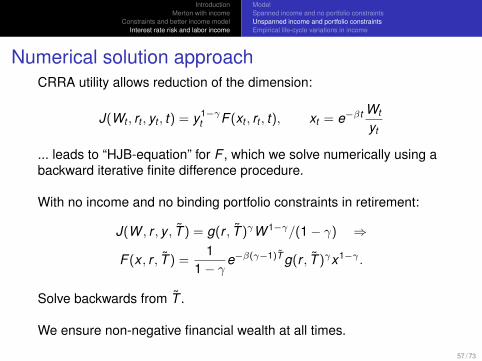

Numerical solution approachCRRA utility allows reduction of the dimension:

J(Wt , rt , yt , t) = y1−γt F (xt , rt , t), xt = e−βt Wt

yt

... leads to “HJB-equation” for F , which we solve numerically using abackward iterative finite difference procedure.

With no income and no binding portfolio constraints in retirement:

J(W , r , y , T ) = g(r , T )γW 1−γ/(1− γ) ⇒

F (x , r , T ) =1

1− γe−β(γ−1)T g(r , T )γx1−γ .

Solve backwards from T .

We ensure non-negative financial wealth at all times.

57 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

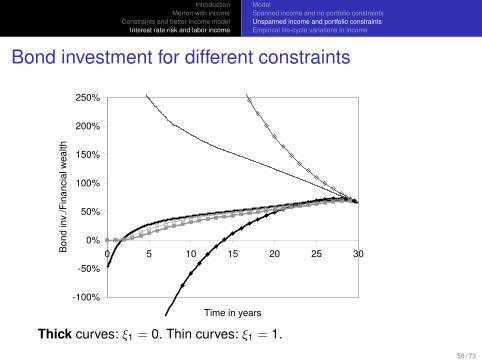

Bond investment for different constraints

-100%

-50%

0%

50%

100%

150%

200%

250%

0 5 10 15 20 25 30

Time in years

Bo

nd

in

v./

Fin

an

cia

l w

ea

lth

Thick curves: ξ1 = 0. Thin curves: ξ1 = 1.58 / 73

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income

ModelSpanned income and no portfolio constraintsUnspanned income and portfolio constraintsEmpirical life-cycle variations in income

Stock investment for different constraints

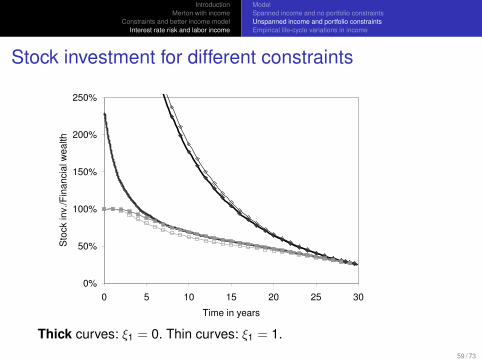

0%

50%

100%

150%

200%

250%

0 5 10 15 20 25 30

Time in years

Sto

ck in

v./

Fin

an

cia

l w

ea

lth

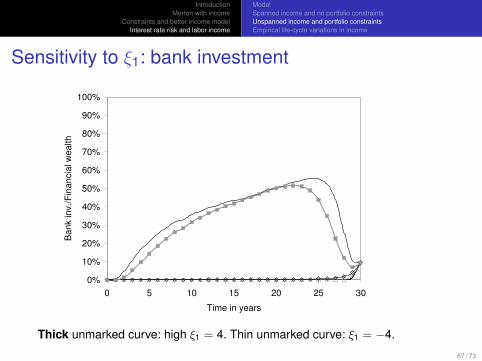

Thick curves: ξ1 = 0. Thin curves: ξ1 = 1.59 / 73

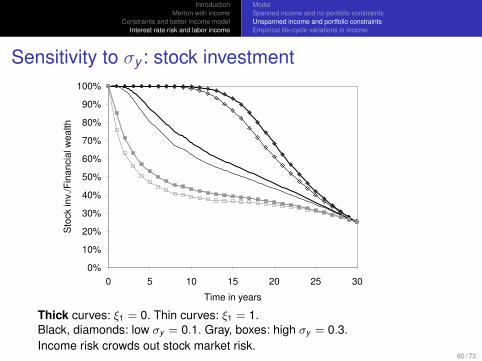

IntroductionMerton with income

Constraints and better income modelInterest rate risk and labor income