Embed Size (px)

Citation preview

presents

Non-Profit Cost Allocation Plan Strategies

presents

Crafting an Effective Plan to Distribute Direct and Indirect Expenses

A Live 110-Minute Teleconference/Webinar with Interactive Q&A

Today's panel features:Sharron O'Donnell, Senior Manager, Bader Martin, Seattle, Wash.Colette Kamps, Senior Manager, Henry & Horne, Scottsdale, Ariz.

Q&

Wednesday, June 30, 2010

The conference begins at:The conference begins at:1 pm Eastern12 pm Central

11 am Mountain10 am Pacific10 am Pacific

You can access the audio portion of the conference on the telephone or by using your computer's speakers.Please refer to the dial in/ log in instructions emailed to registrations.

For Continuing Education purposes, gplease let us know how many people are listening at your location by g y y

• closing the notification box • and typing in the chat box your• and typing in the chat box your

company name and the number of attendeesattendees.

• Then click the blue icon beside the box to sendto send.

For live event only

• If the sound quality is not satisfactory• If the sound quality is not satisfactory and you are listening via your computer speakers please dial 1-866-873-1442speakers, please dial 1 866 873 1442 and enter your PIN when prompted. Otherwise, please send us a chat or e-, pmail [email protected] so we can address the problem.

• If you dialed in and have any difficulties during the call, press *0 for assistance.

Non Profit Cost AllocationNon-Profit Cost Allocation Plan Strategies

June 30, 2010

Sharron O’Donnell, Bader [email protected]

Colette Kamps, Henry & Horne [email protected]

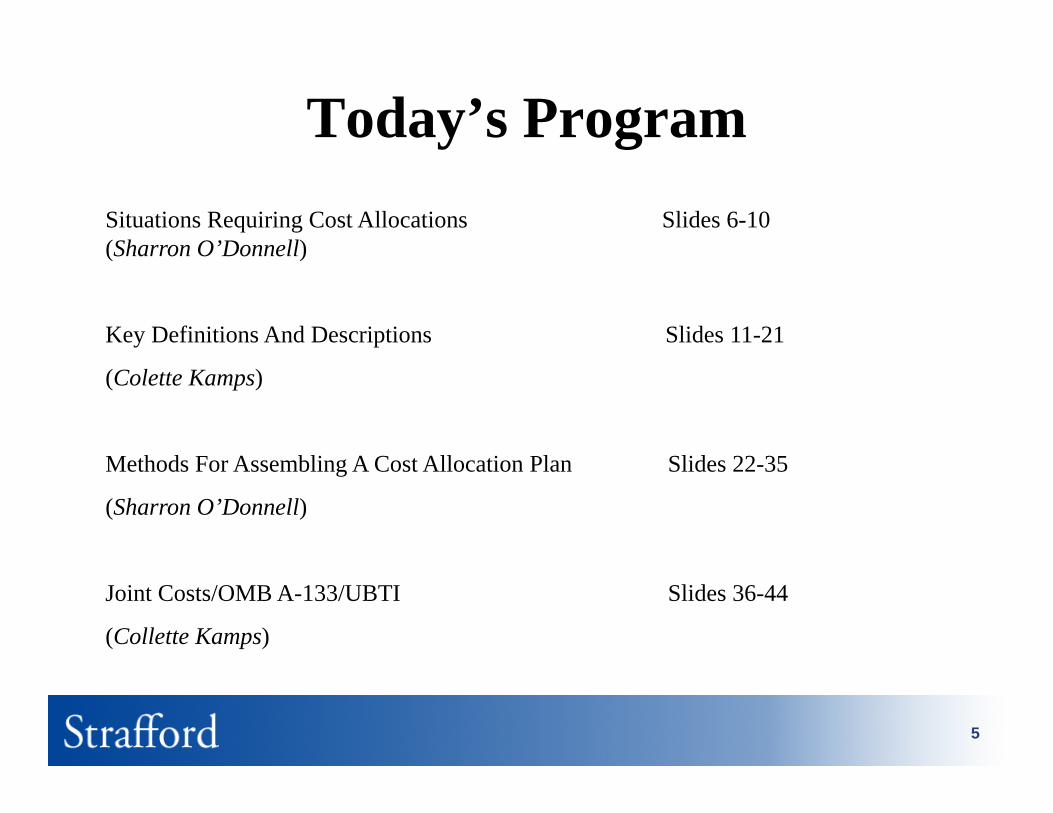

Today’s ProgramSituations Requiring Cost Allocations Slides 6-10 (Sharron O’Donnell)(Sharron O Donnell)

Key Definitions And Descriptions Slides 11-21

(Colette Kamps)

M th d F A bli A C t All ti Pl Slid 22 35Methods For Assembling A Cost Allocation Plan Slides 22-35

(Sharron O’Donnell)

Joint Costs/OMB A-133/UBTI Slides 36-44

(Collette Kamps)

5

Situations Requiring Cost All tiAllocations

Sharron O’Donnell, Bader MartinSharron O Donnell, Bader Martin

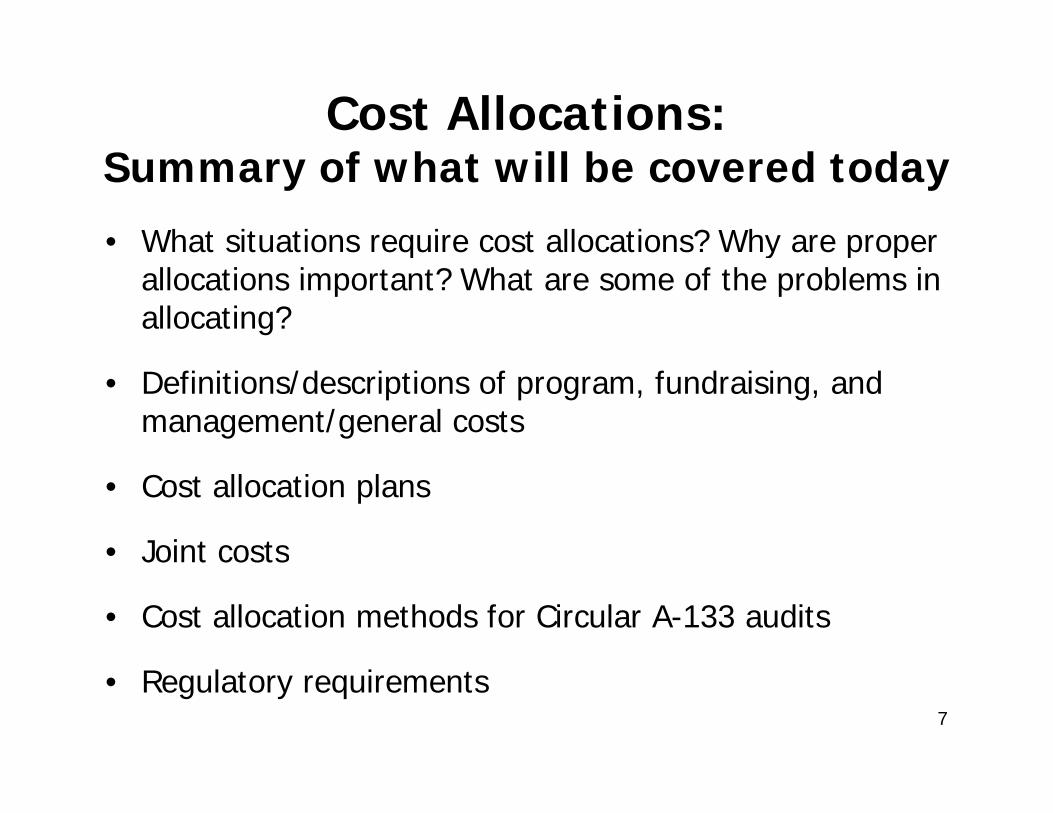

Cost Allocations: f h ill b d dSummary of what will be covered today

• What situations require cost allocations? Why are proper q y p pallocations important? What are some of the problems in allocating?

• Definitions/descriptions of program, fundraising, and management/general costs

• Cost allocation plans

• Joint costsJoint costs

• Cost allocation methods for Circular A-133 audits

• Regulatory requirements7

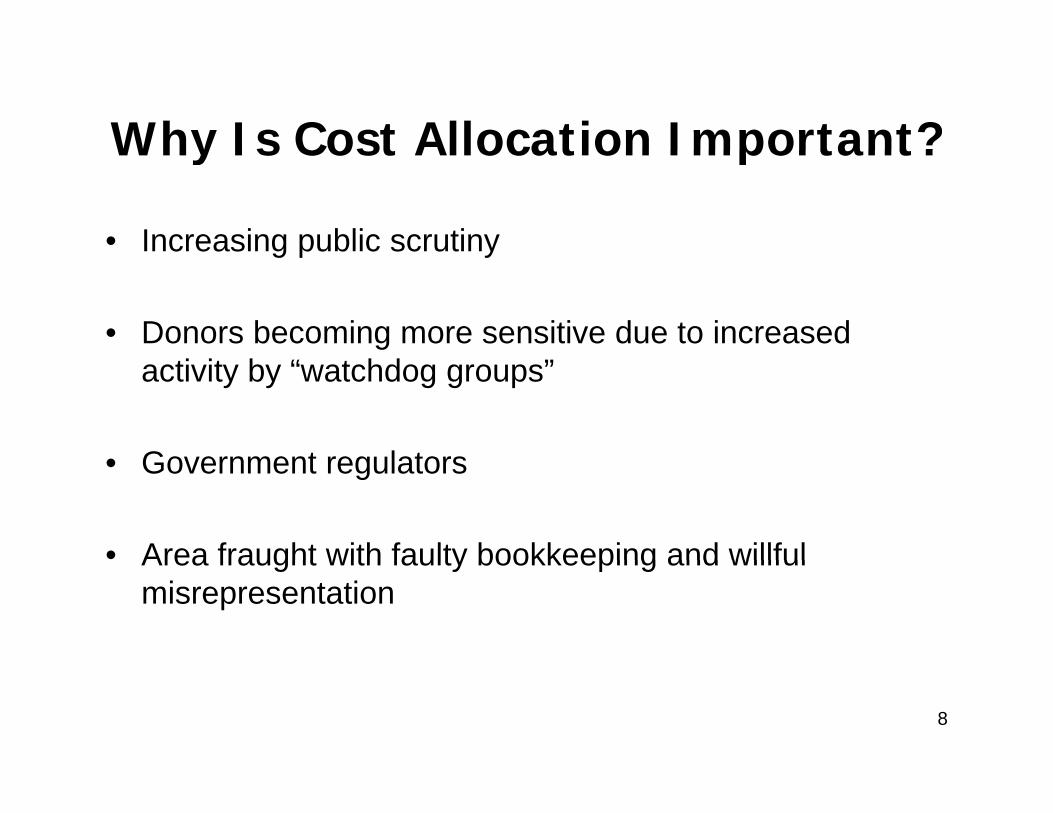

Why Is Cost Allocation Important?Why Is Cost Allocation Important?

• Increasing public scrutinyg p y

• Donors becoming more sensitive due to increased activity by “watchdog groups”

Government regulators• Government regulators

• Area fraught with faulty bookkeeping and willfulArea fraught with faulty bookkeeping and willful misrepresentation

8

Allocating Costs:h i i i ll iWhat situations require cost allocations?

An allocation plan that properly assigns costs toAn allocation plan that properly assigns costs to programs is essential when making decisions.

Reliable and consistent financial reporting

Users of your financial information can make informed decisions.

9

How Much Is Enough?How Much Is Enough?

• Is there a percentage or a range of percentages that is correct?

Do you know how much it costs to run a program?• Do you know how much it costs to run a program?

10

Key Definitions And D i tiDescriptions

Colette Kamps, Henry & HorneColette Kamps, Henry & Horne

Allocating Costs:h i i i ll iWhat situations require cost allocations?

• Natural vs. functional• Accounting standards

– Require nonprofits to report expenses by functional classificationclassification

– Voluntary health and welfare organizations are required to present a Statement of Functional EExpenses• Voluntary health and welfare organization:

Formed for the purpose of performing voluntary p p p g yservices for various segments of society; organized for the benefit of the public. It concentrates efforts in attempt to solve health and welfare problems.p p

12

Allocating Costs:fi i i d d i iDefinitions and descriptions

• Program expenses

• Supporting services expenses– Management and general expenses– Fundraising expenses

13

Allocating Costs:fi i i d d i i ( )Definitions and descriptions (Cont.)

• Program expenses: Expenses related to activities carried g p pout to fulfill the mission; include both direct and indirect expenses

• Reporting by functional classification includes reporting by major program and supporting expenses

N d t d t i th i ti ’ j– Need to determine the organization’s major programs– Requires judgment and knowledge of the organization

14

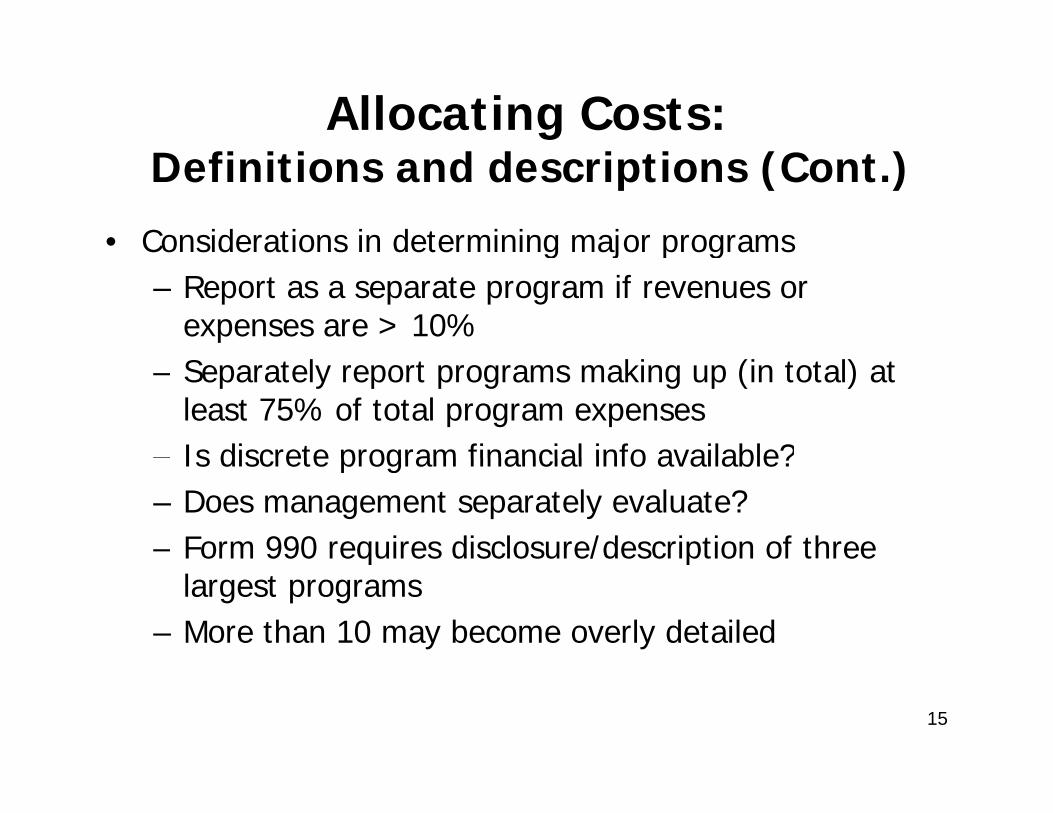

Allocating Costs:fi i i d d i i ( )Definitions and descriptions (Cont.)

• Considerations in determining major programsg j p g– Report as a separate program if revenues or

expenses are > 10%– Separately report programs making up (in total) at

least 75% of total program expenses– Is discrete program financial info available?Is discrete program financial info available?– Does management separately evaluate?– Form 990 requires disclosure/description of three q / p

largest programs– More than 10 may become overly detailed

15

Allocating Costs:fi i i d d i i ( )Definitions and descriptions (Cont.)

• Supporting services expenses

– Management and general– Fundraising

b h d l– Membership development

16

Allocating Costs:fi i i d d i i ( )Definitions and descriptions (Cont.)

• Management and general expensesg g p– Relate to the overall direction of the organization

– Although indispensible to the organization, they are not identifiable with a specific program and are not a fundraising activityfundraising activity.

– Include oversight, business management, record g , g ,keeping, budgeting, financing

17

Allocating Costs:fi i i d d i i ( )Definitions and descriptions (Cont.)

• Common types of management/general expenses– Relating to board and committee meetings– Providing executive direction and organization planning (salary

of executive director)– Accounting, auditing, budgeting, financial reporting– Procuring and retaining personnel (human resources)– Office services (receptionist, mail distribution, filing duties)– Preparing the annual report– Disseminating information to the public about the organization’s

use of donated funds– Costs of advertising for ticket sales or admissions of a

performing arts organization, museum, zoo, or similar organization

18

Allocating Costs:fi i i d d i i ( )Definitions and descriptions (Cont.)

• Further consideration of advertising expensesg p– Is the purpose of the advertising primarily to

generate revenue from services/admissions, or is it i il t t th i ti d itprimarily to promote the organization and its

services?

– Is the related fee charged de minimis compared with the actual fair market value?

– Does the related fee help to increase the effectiveness of the organization’s programs?effectiveness of the organization s programs?

19

Allocating Costs:fi i i d d i i ( )Definitions and descriptions (Cont.)

• Fundraising expenses: Costs related to activities that involve i d i i l d ib ( h d h)inducing potential donors to contribute assets (cash and non-cash), services or time

C t• Common types– Conducting of fund-raising campaigns– Conducting special events

M i t i i d li t– Maintaining donor lists– Preparing/distributing fund-raising materials– Recruiting volunteers (even if revenue not recognized)– Conducting solicitations– Professional fund-raiser (do not net with revenue)– Other activities involving soliciting contributions

20

Allocating Costs (Cont.)

• Problems with fundraising costs/ratios– Allocations are often subjective, not objective.– Some contributions do not requiring ongoing fund

raising expenses (bequests, ongoing foundation support)support)

– Highly dependent on nature of the organization– The ratio can be affected by temporary events (stage y p y ( g

of a capital campaign, the economy)

21

Methods For Assembling A C t All ti PlA Cost Allocation Plan

Sharron O’Donnell, Bader MartinSharron O Donnell, Bader Martin

Allocating Costs: ll i lCost allocation plan

• Direct identification: Can be identified with a particular function; only allocate when direct identification is not

ibl ti lpossible or practical

• Indirect expenses: Allocation to more than one function• Indirect expenses: Allocation to more than one function– Need to have a cost allocation plan

23

Allocating Costs: ll i l ( )Cost allocation plan (Cont.)

• Cost allocation planpNeed to have a basis for how costs are allocated

Need to be consistentObjective methods are preferable to subjective.

The plan needs to be documented.

24

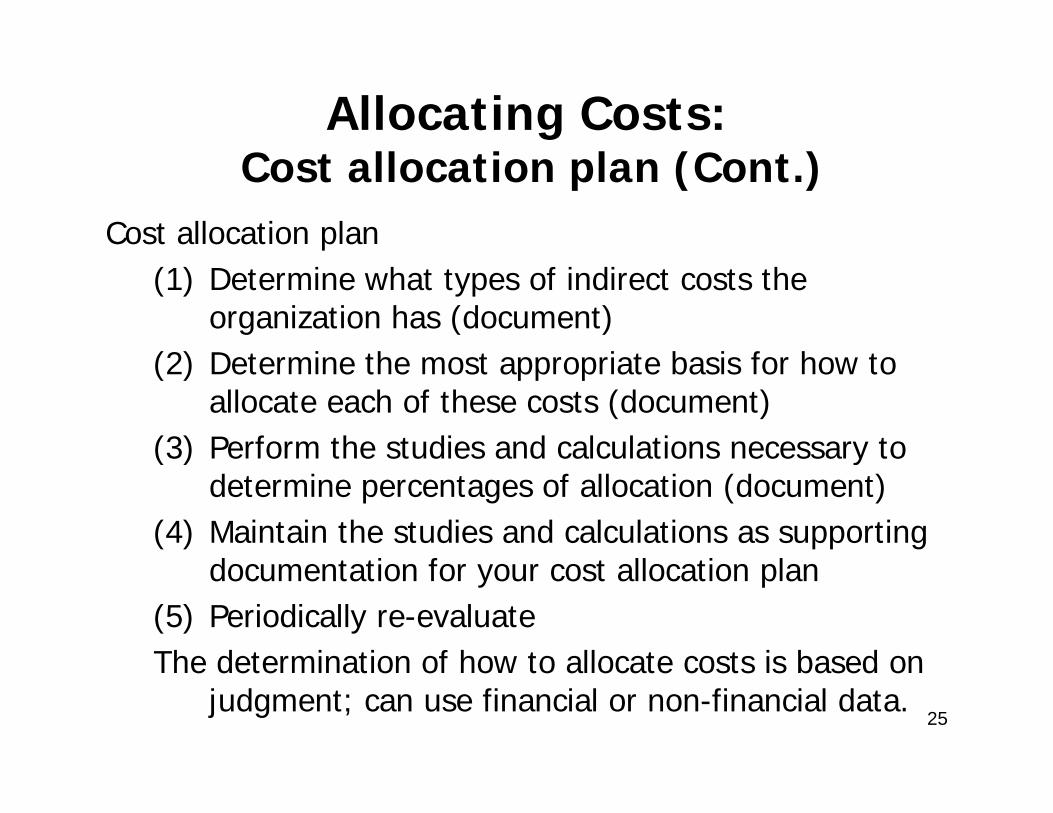

Allocating Costs: ll i l ( )Cost allocation plan (Cont.)

Cost allocation plan(1) Determine what types of indirect costs the

organization has (document)(2) D t i th t i t b i f h t(2) Determine the most appropriate basis for how to

allocate each of these costs (document)(3) Perform the studies and calculations necessary to(3) Perform the studies and calculations necessary to

determine percentages of allocation (document)(4) Maintain the studies and calculations as supporting

d t ti f t ll ti ldocumentation for your cost allocation plan(5) Periodically re-evaluateThe determination of how to allocate costs is based onThe determination of how to allocate costs is based on

judgment; can use financial or non-financial data.25

Allocating Costs: ll i l ( )Cost allocation plan (Cont.)

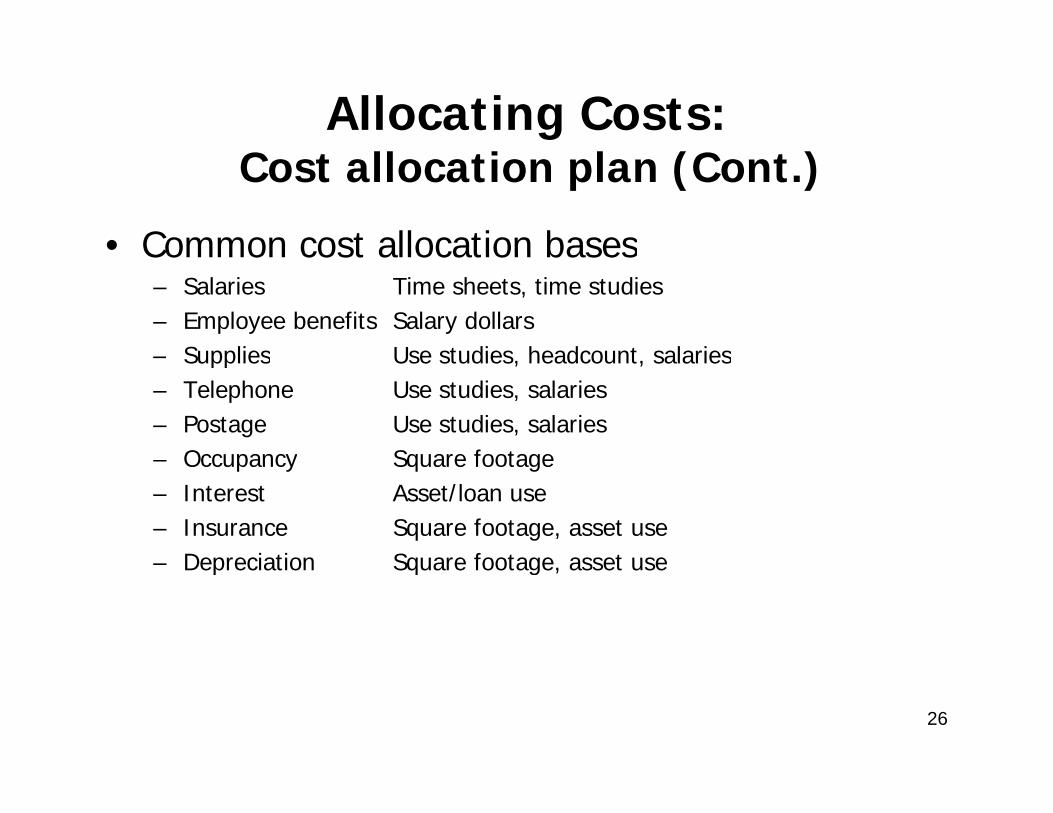

• Common cost allocation basesCommon cost allocation bases– Salaries Time sheets, time studies– Employee benefits Salary dollars– Supplies Use studies headcount salaries– Supplies Use studies, headcount, salaries– Telephone Use studies, salaries– Postage Use studies, salaries

Occupancy Square footage– Occupancy Square footage– Interest Asset/loan use– Insurance Square footage, asset use

Depreciation Square footage asset use– Depreciation Square footage, asset use

26

Allocating Costs: ll i l ( )Cost allocation plan (Cont.)

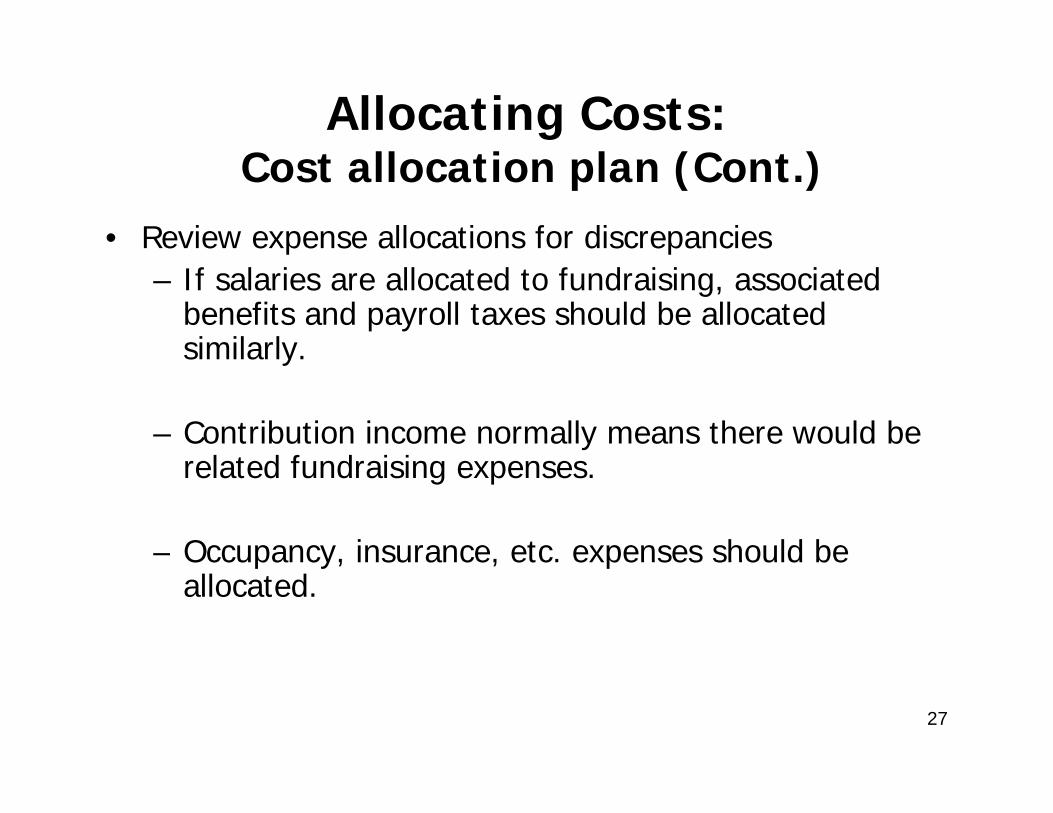

• Review expense allocations for discrepanciesp p– If salaries are allocated to fundraising, associated

benefits and payroll taxes should be allocated similarly.similarly.

– Contribution income normally means there would be l t d f d i irelated fundraising expenses.

– Occupancy, insurance, etc. expenses should beOccupancy, insurance, etc. expenses should be allocated.

27

Allocating Costs: ll i l ( )Cost allocation plan (Cont.)

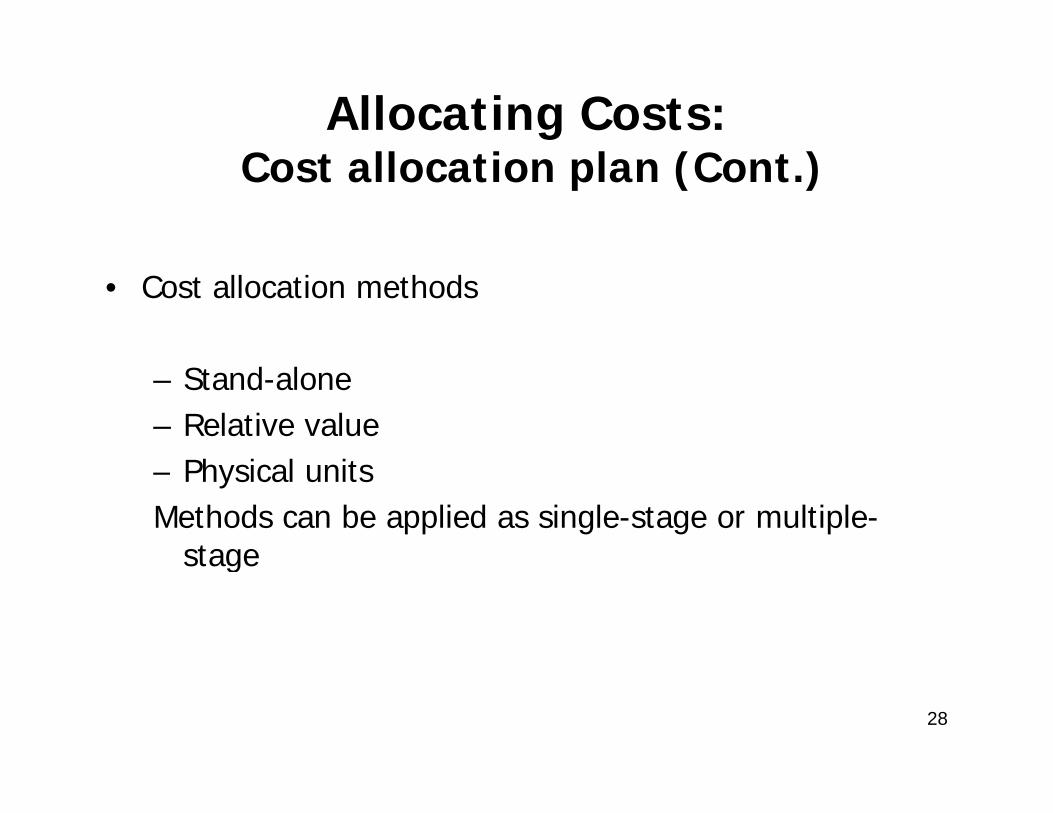

• Cost allocation methods

– Stand-alone– Relative value

h l– Physical unitsMethods can be applied as single-stage or multiple-

stagestage

28

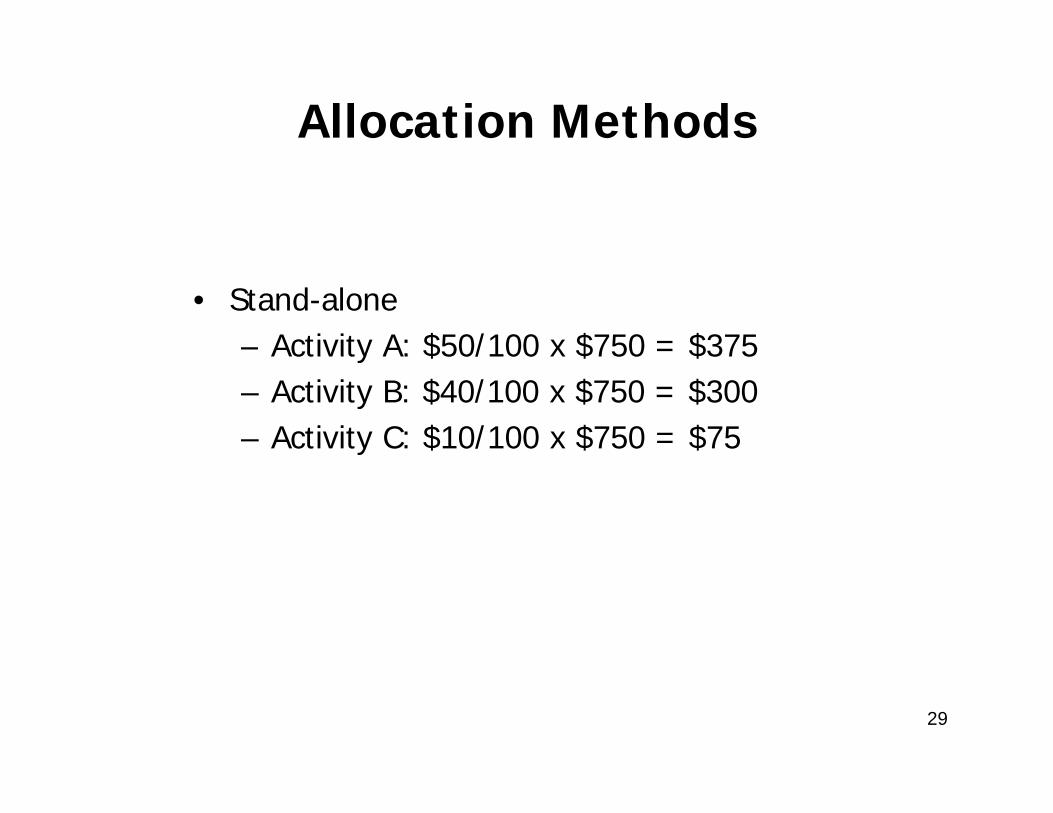

Allocation Methods

• Stand-alone– Activity A: $50/100 x $750 = $375Activity A: $50/100 x $750 $375– Activity B: $40/100 x $750 = $300– Activity C: $10/100 x $750 = $75

29

Allocating Costs: ll i l ( )Cost allocation plan (Cont.)

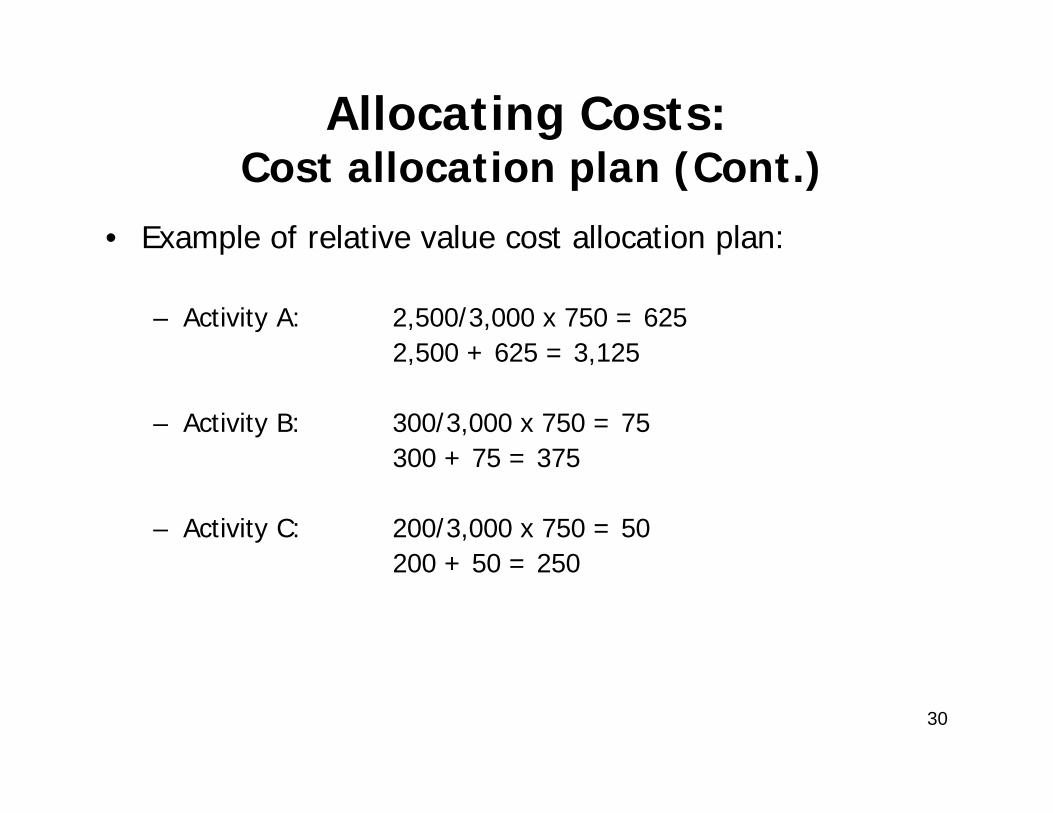

• Example of relative value cost allocation plan:p p

– Activity A: 2,500/3,000 x 750 = 6252 500 + 625 = 3 1252,500 + 625 = 3,125

– Activity B: 300/3,000 x 750 = 75300 + 75 = 375300 + 75 = 375

– Activity C: 200/3,000 x 750 = 50200 + 50 = 250200 + 50 = 250

30

Allocation Methods (Cont.)Allocation Methods (Cont.)Allocation Methods (Cont.)Allocation Methods (Cont.)

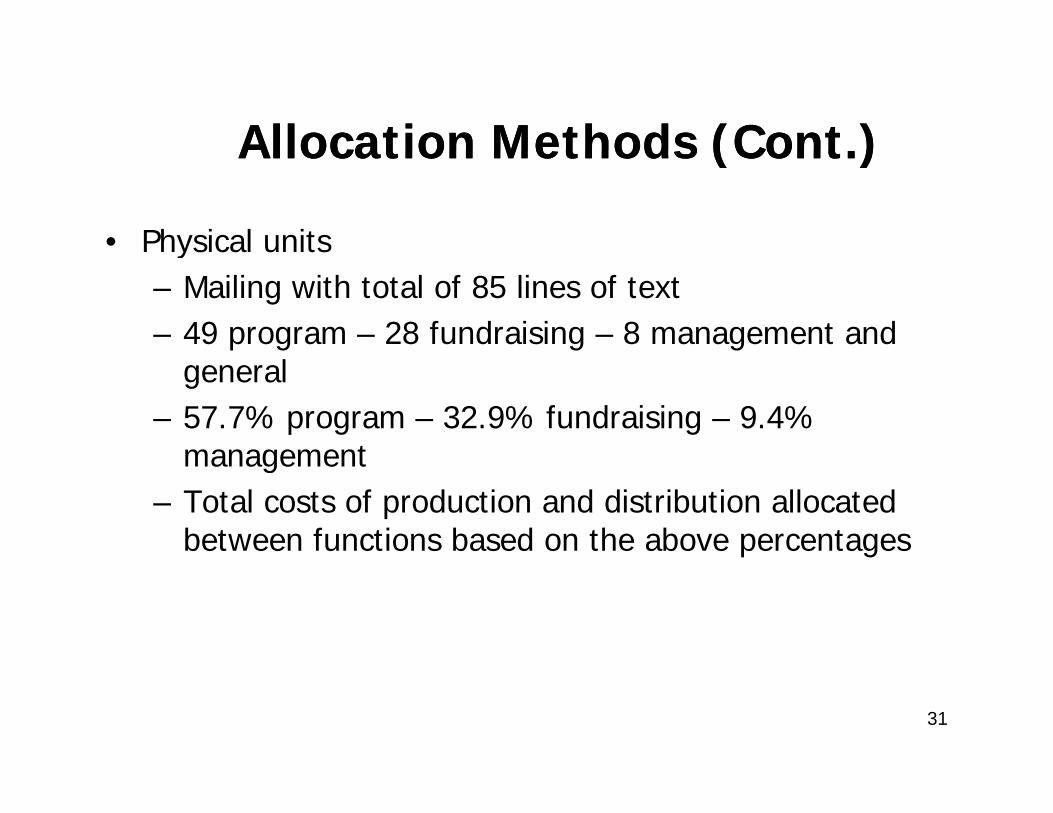

• Physical unitsy– Mailing with total of 85 lines of text– 49 program – 28 fundraising – 8 management and

general– 57.7% program – 32.9% fundraising – 9.4%

managementmanagement– Total costs of production and distribution allocated

between functions based on the above percentages

31

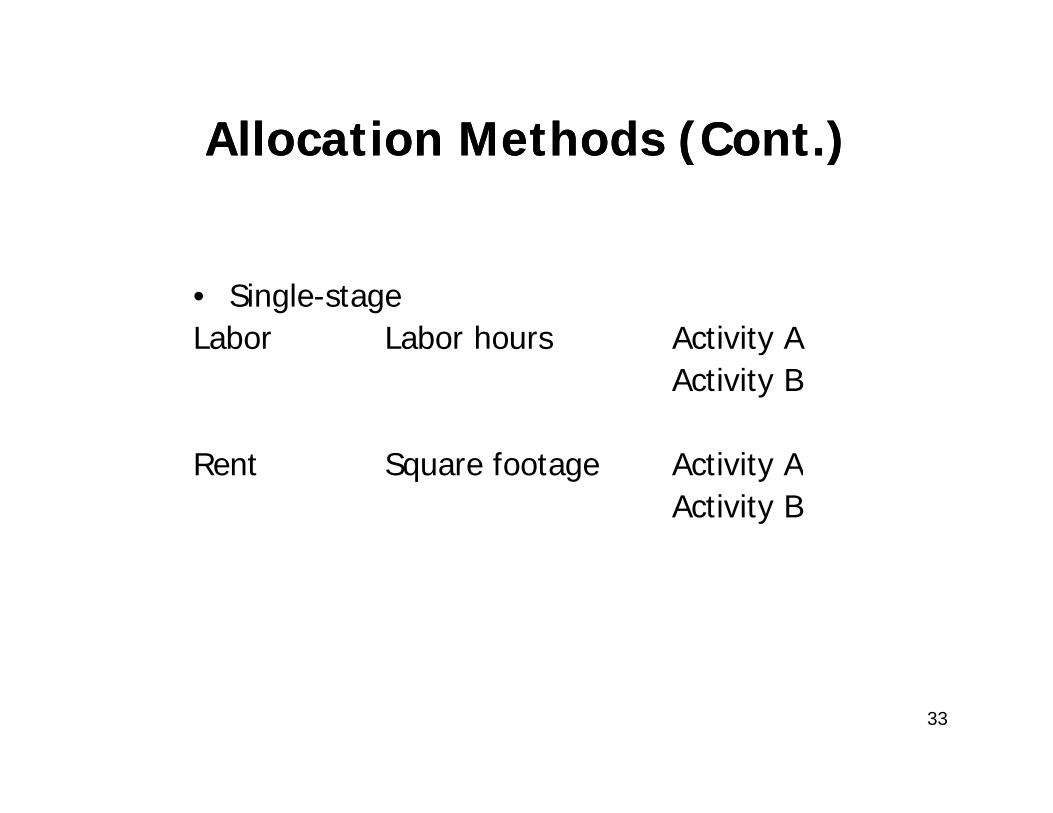

Allocation Methods (Cont.)

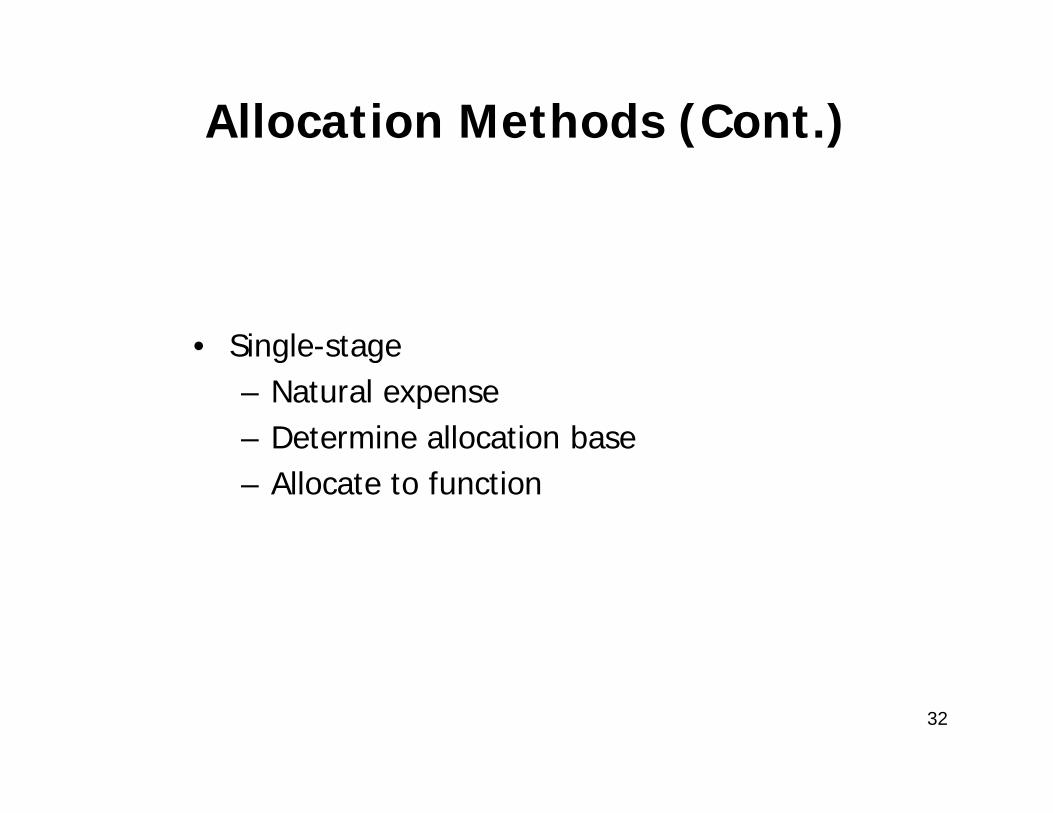

• Single-stageSingle stage– Natural expense – Determine allocation base– Allocate to function

32

AllocationAllocation Methods (Cont.)Methods (Cont.)Allocation Allocation Methods (Cont.)Methods (Cont.)

• Single-stageLabor Labor hours Activity A

Activity B

Rent Square footage Activity ARent Square footage Activity AActivity B

33

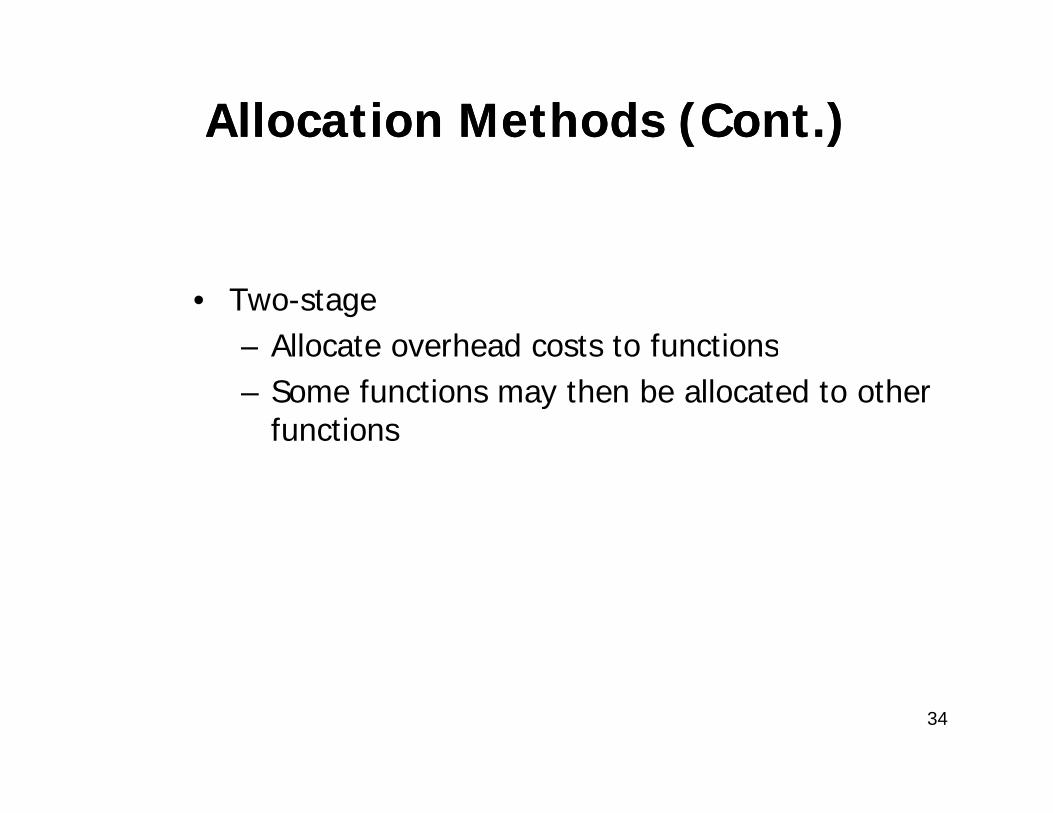

Allocation Methods (Cont.)Allocation Methods (Cont.)

• Two-stage– Allocate overhead costs to functionsAllocate overhead costs to functions– Some functions may then be allocated to other

functions

34

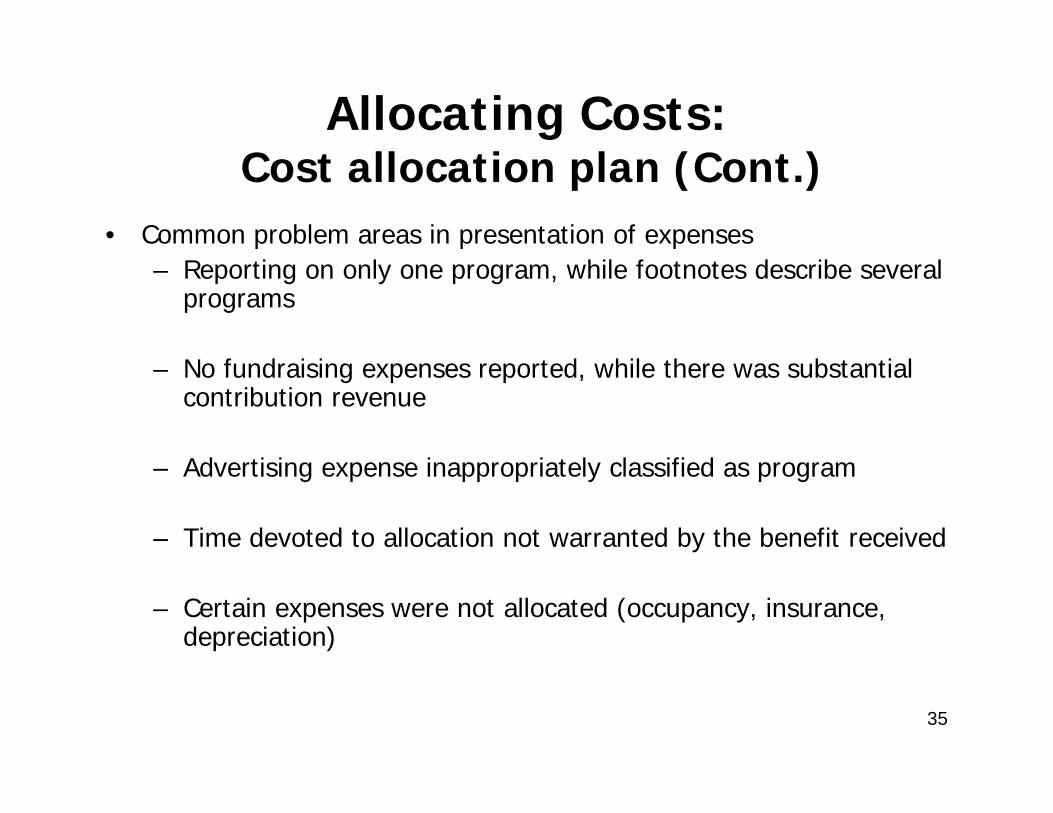

Allocating Costs: ll i l ( )Cost allocation plan (Cont.)

• Common problem areas in presentation of expenses– Reporting on only one program, while footnotes describe several

programs

– No fundraising expenses reported, while there was substantial contribution revenue

Ad ti i i i t l l ifi d– Advertising expense inappropriately classified as program

– Time devoted to allocation not warranted by the benefit received

– Certain expenses were not allocated (occupancy, insurance, depreciation)

35

Joint Costs/OMB A-133/UBTI133/UBTI

Colette Kamps, Henry & HorneColette Kamps, Henry & Horne

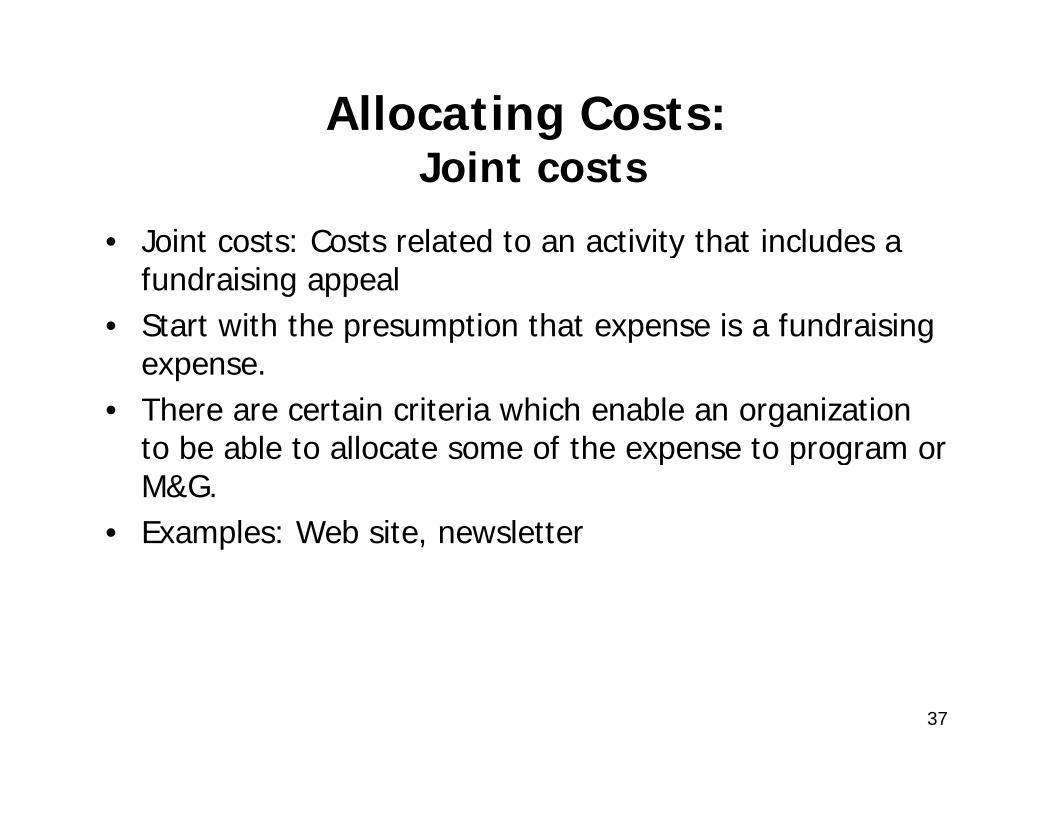

Allocating Costs:iJoint costs

• Joint costs: Costs related to an activity that includes a yfundraising appeal

• Start with the presumption that expense is a fundraising expense.

• There are certain criteria which enable an organization to be able to allocate some of the expense to program orto be able to allocate some of the expense to program or M&G.

• Examples: Web site, newsletter

37

Allocating Costs:i ( )Joint costs (Cont.)

• Criteria to overcome the presumption that the entire cost p pis fundraising– Purpose– Audience– Content

If all three criteria are met, allocate joint costs between fundraising and program (or M&G)g p g ( )

38

Allocating Costs:i ( )Joint costs (Cont.)

• Purpose criteriap

– Purpose of the activity includes accomplishing program activity. Consider:• Call to action (other than call to make a

contribution)contribution)• Compensation or fees test• Separate and similar activity test (doesn’t p y (

automatically disqualify)• Other evidence

39

Allocating Costs:i ( )Joint costs (Cont.)

• Audience criteria

– Easier to meet if audience members do not include former donors and are not selected based on their ability to contribute.

– Must be selected because they can help accomplishMust be selected because they can help accomplish both the program and the fundraising activity.

40

Allocating Costs:i ( )Joint costs (Cont.)

• Content criteria

– Content of the activity must support the program

41

Allocating Costs:i ( )Joint costs (Cont.)

• Disclosures required for joint costs– The types of activities that resulted in joint costs.– The fact that such costs have been allocated– The total amount allocated during the period and the

portion that was allocated to each functional expenseportion that was allocated to each functional expense category

42

Allocating Costs:ll i l ( )Cost allocation plan (Cont.)

• Cost allocation methods permitted by OMB Circular A-122 (federal funds)– Simplified allocation method– Multiple allocation base method

Direct allocation method– Direct allocation method

43

Allocating Costs:UBTI costs

• Allocating costs to unrelated business taxable income g(UBTI)– A cost is indirect only if cannot possibly be allocated

di tldirectly.

– Fundraising expenses are deemed specific to exemptFundraising expenses are deemed specific to exempt purposes and are not allocable to UBTI.

– Methods of allocating should be consistent.

– Maintain documentation of allocation method used44

![Cost allocation joint cost [compatibility mode]](https://img.pdfslide.net/doc/110x75/54448861b1af9f740a8b49b9/cost-allocation-joint-cost-compatibility-mode.jpg)