Embed Size (px)

Citation preview

E-mobility opportunities & challengesy g1st Green Manufacturing Summit – Sectoral Case Automotive

New Dehli, 18 March, 2011

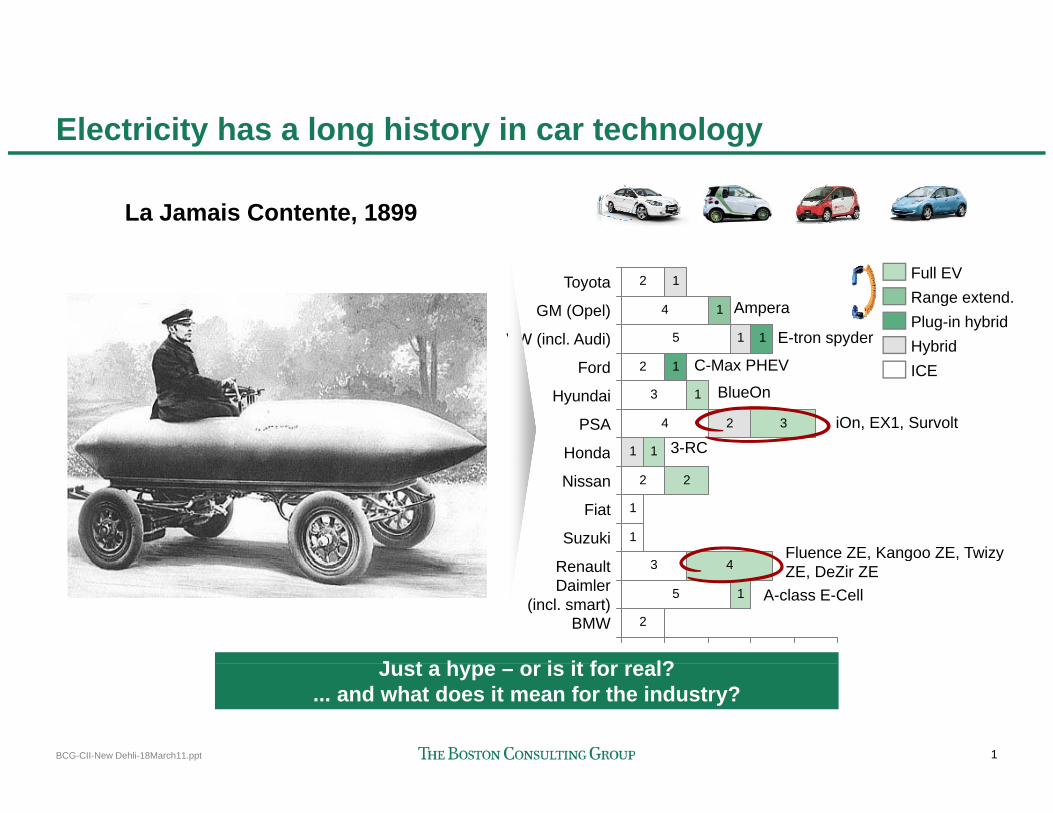

Electricity has a long history in car technology

La Jamais Contente, 1899La Jamais Contente, 1899

2

4

5 1

1

1

1

VW (incl. Audi)

GM (Opel)

Toyota

HybridPlug-in hybridRange extend.Full EV

Ampera

E-tron spyder

2

3

4

1

2

1

1

3

1

Honda

PSA

Hyundai

Ford ICEC-Max PHEV

BlueOn

iOn, EX1, Survolt3-RC

2

1

1

3 4

2

R l

Suzuki

Fiat

Nissan

Honda

Fluence ZE, Kangoo ZE, Twizy 3

5

2

1

4

BMW

Daimler(incl. smart)

Renaultg y

ZE, DeZir ZEA-class E-Cell

J t h i it f l?

1BCG-CII-New Dehli-18March11.ppt

Just a hype – or is it for real?... and what does it mean for the industry?

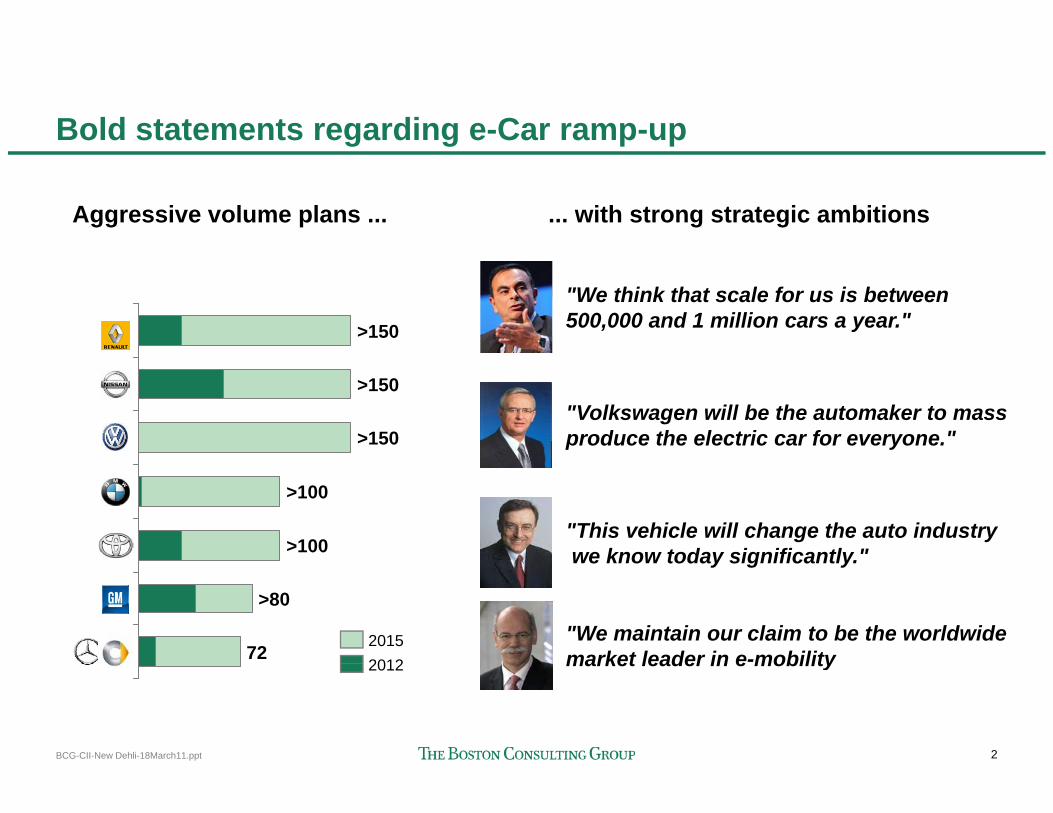

Bold statements regarding e-Car ramp-up

... with strong strategic ambitions... with strong strategic ambitionsAggressive volume plans ...Aggressive volume plans ...

"We think that scale for us is between 500,000 and 1 million cars a year.">150

>150

>150"Volkswagen will be the automaker to massproduce the electric car for everyone."

>100

>100

"This vehicle will change the auto industrywe know today significantly."

72

>80

we know today significantly.

"We maintain our claim to be the worldwide market leader in e-mobility2012

2015

2BCG-CII-New Dehli-18March11.ppt

market leader in e mobility2012

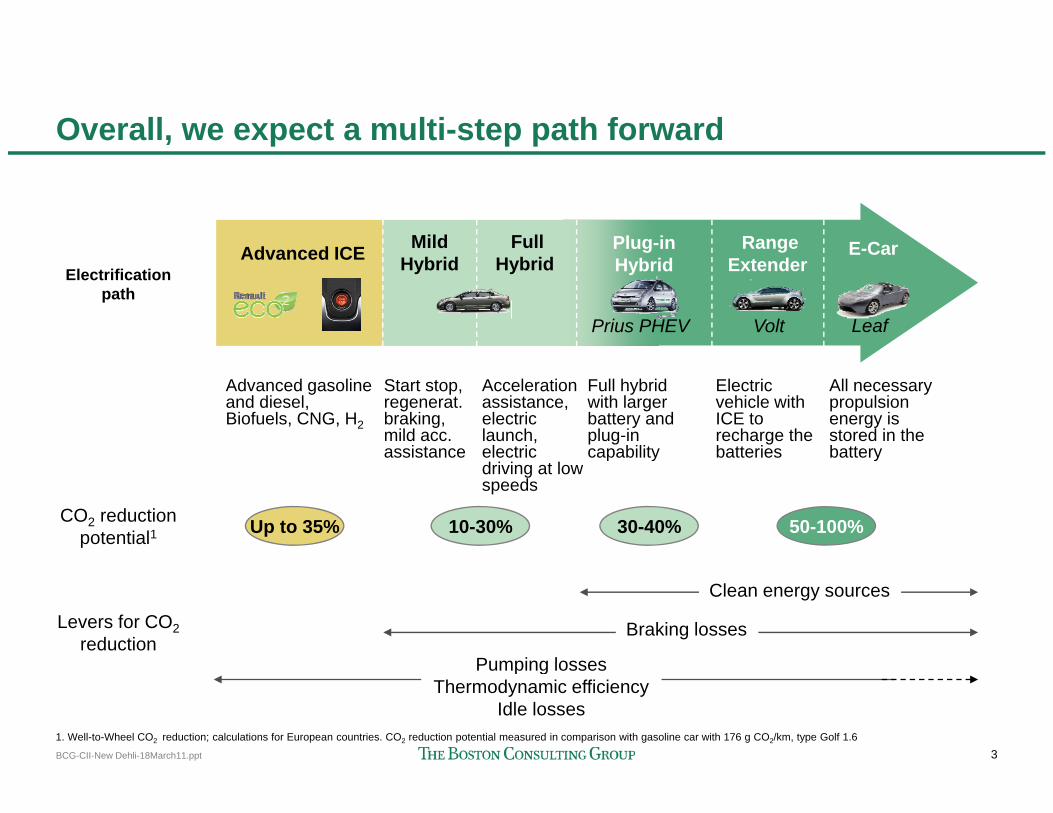

Overall, we expect a multi-step path forward

RangeAdvanced ICE Mild Plug-in E-CarFullExtenderAdvanced ICE Hybrid Hybrid

E CarElectrification

path

Prius PHEV Volt Leaf

Hybrid

Advanced gasoline and diesel, Biofuels, CNG, H2

Start stop, regenerat.braking, mild acc. assistance

Acceleration assistance, electric launch, electric

Full hybrid with larger battery and plug-in capability

Electric vehicle with ICE to recharge the batteries

All necessary propulsion energy is stored in the battery

Up to 35% 10-30% 30-40% 50-100%CO2 reduction potential1

driving at low speeds

p y y

Clean energy sources

Pumping losses

Levers for CO2 reduction

Braking losses

3BCG-CII-New Dehli-18March11.ppt

Pumping lossesThermodynamic efficiency

Idle losses1. Well-to-Wheel CO2 reduction; calculations for European countries. CO2 reduction potential measured in comparison with gasoline car with 176 g CO2/km, type Golf 1.6

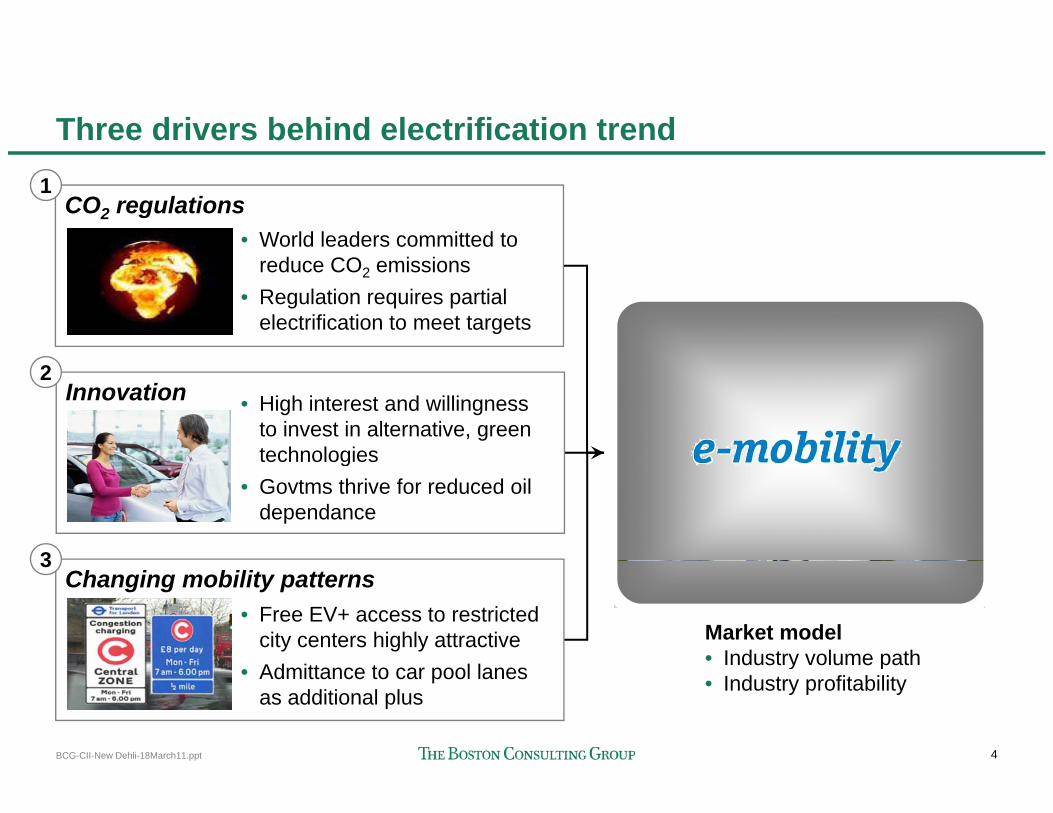

Three drivers behind electrification trend

CO2 regulations• World leaders committed to

1

reduce CO2 emissions• Regulation requires partial

electrification to meet targets

Innovation • High interest and willingness to invest in alternative, green technologies

2

technologies• Govtms thrive for reduced oil

dependance

3Changing mobility patterns

• Free EV+ access to restricted city centers highly attractive

3

Market model• Industry volume path

4BCG-CII-New Dehli-18March11.ppt

• Admittance to car pool lanes as additional plus

Industry volume path• Industry profitability

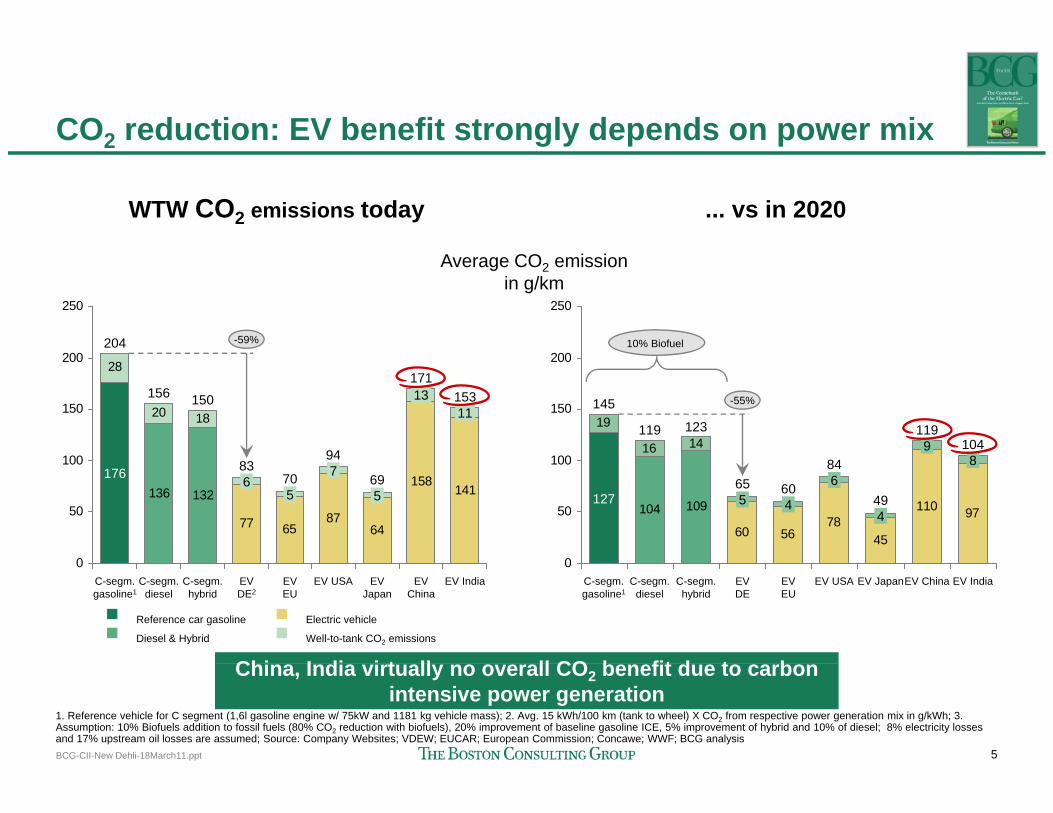

CO2 reduction: EV benefit strongly depends on power mix

WTW CO2 emissions todayWTW CO2 emissions today ... vs in 2020... vs in 2020

200

250

204 -59%

200

250

10% Biofuel

Average CO2 emission in g/km

1820

28

100

150

200

94

15015611

13171

153

1416

19

100

150

200

123119

145

89

119104

-55%

136 132

77 6587

64

158141

0

50

10069

94

7083

5

7

56176

104 109

60 5678

45

110 97

0

50

100 84

6065

8

4

6

45127 49

0C-segm. gasoline1

C-segm. diesel

C-segm. hybrid

EV DE2

EVEU

EV USA EV Japan

EV China

EV India0

EV IndiaC-segm. gasoline1

C-segm. diesel

C-segm. hybrid

EV DE

EVEU

EV USA EV JapanEV China

Chi I di i t ll ll CO b fit d t b

Reference car gasoline

Diesel & Hybrid

Electric vehicle

Well-to-tank CO2 emissions

5BCG-CII-New Dehli-18March11.ppt

China, India virtually no overall CO2 benefit due to carbon intensive power generation

1. Reference vehicle for C segment (1,6l gasoline engine w/ 75kW and 1181 kg vehicle mass); 2. Avg. 15 kWh/100 km (tank to wheel) X CO2 from respective power generation mix in g/kWh; 3. Assumption: 10% Biofuels addition to fossil fuels (80% CO2 reduction with biofuels), 20% improvement of baseline gasoline ICE, 5% improvement of hybrid and 10% of diesel; 8% electricity losses and 17% upstream oil losses are assumed; Source: Company Websites; VDEW; EUCAR; European Commission; Concawe; WWF; BCG analysis

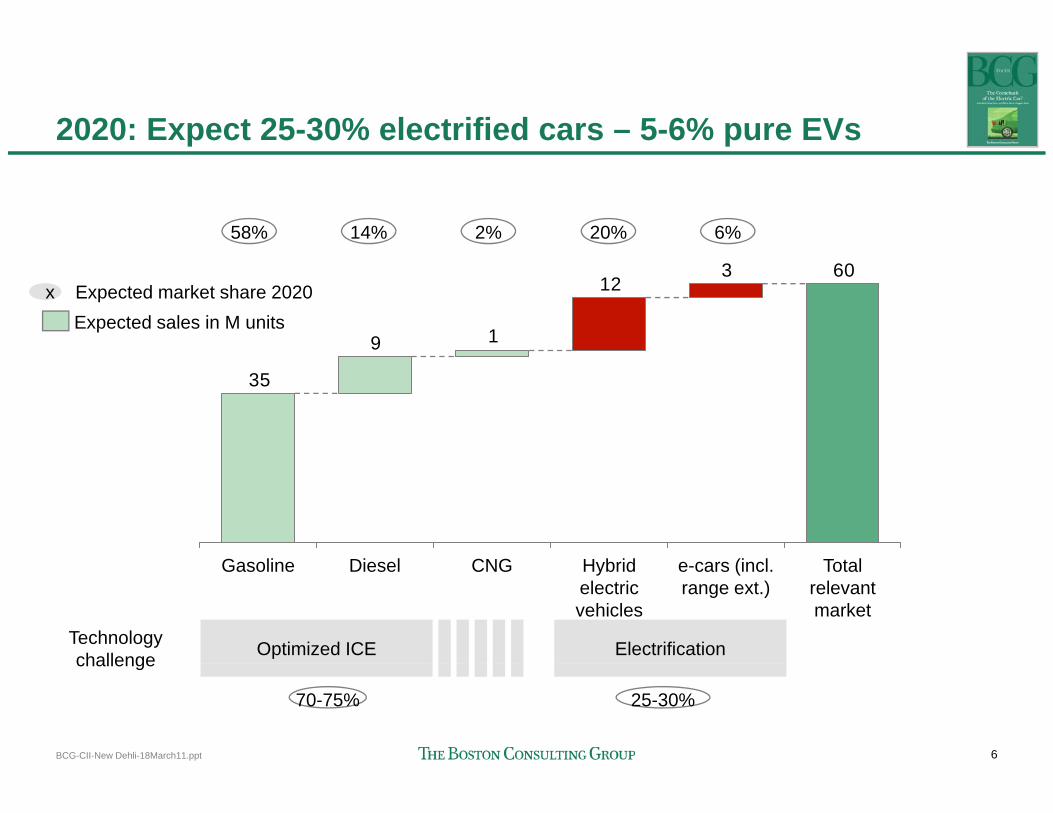

2020: Expect 25-30% electrified cars – 5-6% pure EVs

58% 14% 20% 6%2%

60312

19

x Expected market share 2020Expected sales in M units

35

T t l(i lH b idCNGDi lG li Total relevant market

e-cars (incl. range ext.)

Hybrid electricvehicles

CNGDieselGasoline

Optimized ICE ElectrificationTechnology challenge

6BCG-CII-New Dehli-18March11.ppt

70-75% 25-30%

challenge

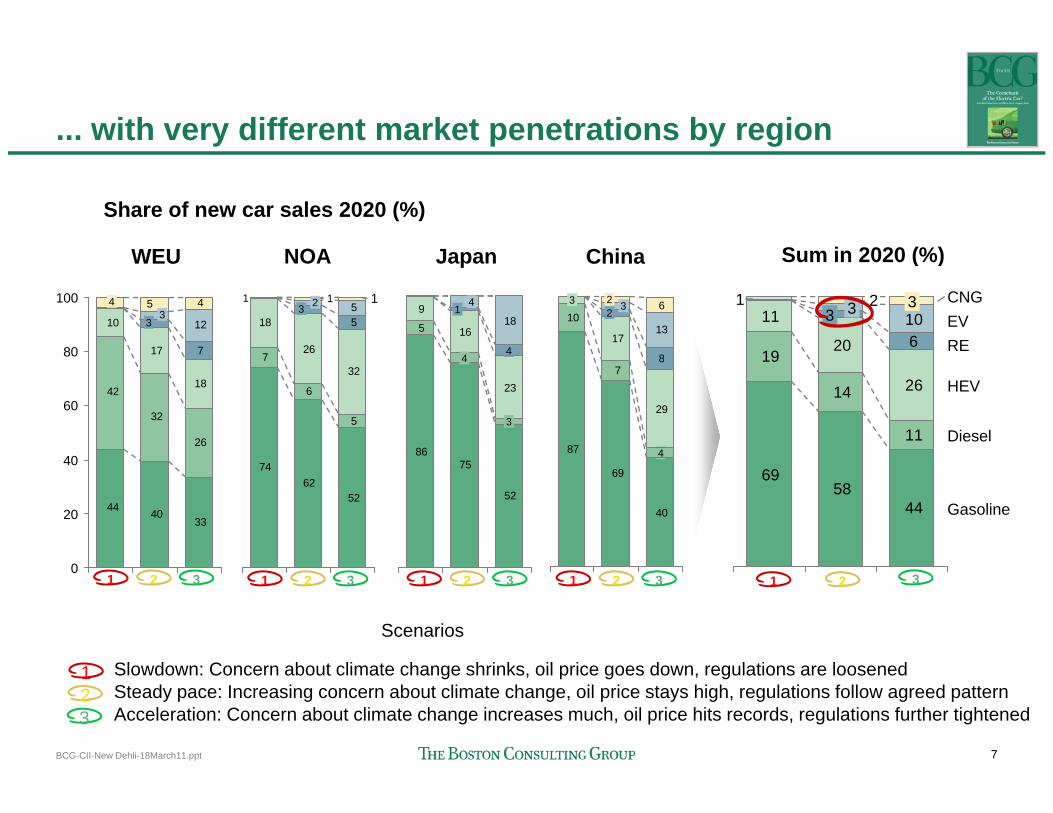

... with very different market penetrations by region

Sum in 2020 (%)Sum in 2020 (%)

Share of new car sales 2020 (%)

WEU NOA Japan China

17

10

7

12

45

80

100

33

4

726

18 55

113 2

5 16

918

44

14

10

17

8

13

62 323

Sum in 2020 (%)Sum in 2020 (%)

1920

11610

213 3

REEVCNG3

WEU NOA Japan China

1

26

32

4218

80

60

40

5

6

732

86

23

3

4

87

7

29

8

411

14

19

26

Diesel

HEV

334044

40

2052

6274

52

75

40

69

4458

69

Gasoline

01 32 1 32 1 32 1 32 1 32

ScenariosScenarios

Sl d C b t li t h h i k il i d l ti l d

7BCG-CII-New Dehli-18March11.ppt

1 Slowdown: Concern about climate change shrinks, oil price goes down, regulations are loosened2 Steady pace: Increasing concern about climate change, oil price stays high, regulations follow agreed pattern3 Acceleration: Concern about climate change increases much, oil price hits records, regulations further tightened

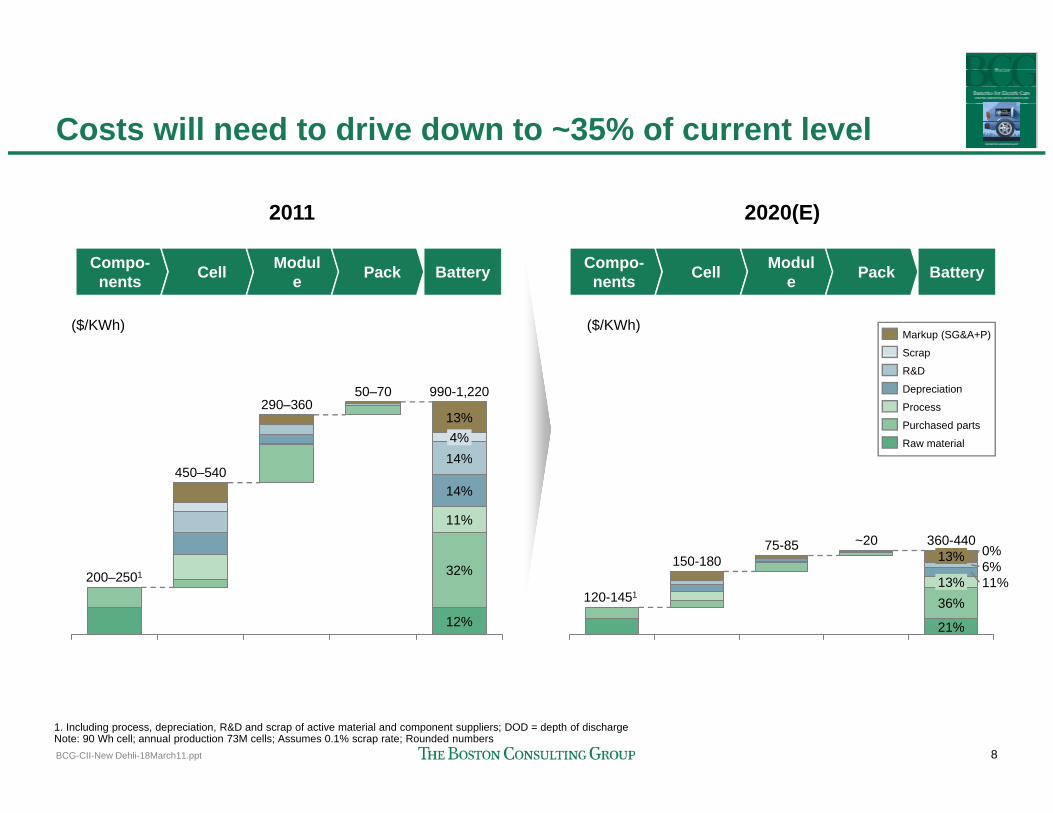

Costs will need to drive down to ~35% of current level

20112011 2020(E)2020(E)

Compo-nents Cell Modul

e Pack Battery Compo-nents Cell Modul

e Pack Battery

($/KWh) ($/KWh)Markup (SG&A+P)

Scrap

990-1,220

14%4%13%

50–70290–360

Purchased parts

Scrap

Raw material

Depreciation

Process

R&D

11%

14%

14%450–540

75-85150 180

360-4400%13%

~20

12%

32%200–2501150-180

120-145113%

21%

36%11%6%

13%

8BCG-CII-New Dehli-18March11.ppt

1. Including process, depreciation, R&D and scrap of active material and component suppliers; DOD = depth of dischargeNote: 90 Wh cell; annual production 73M cells; Assumes 0.1% scrap rate; Rounded numbers

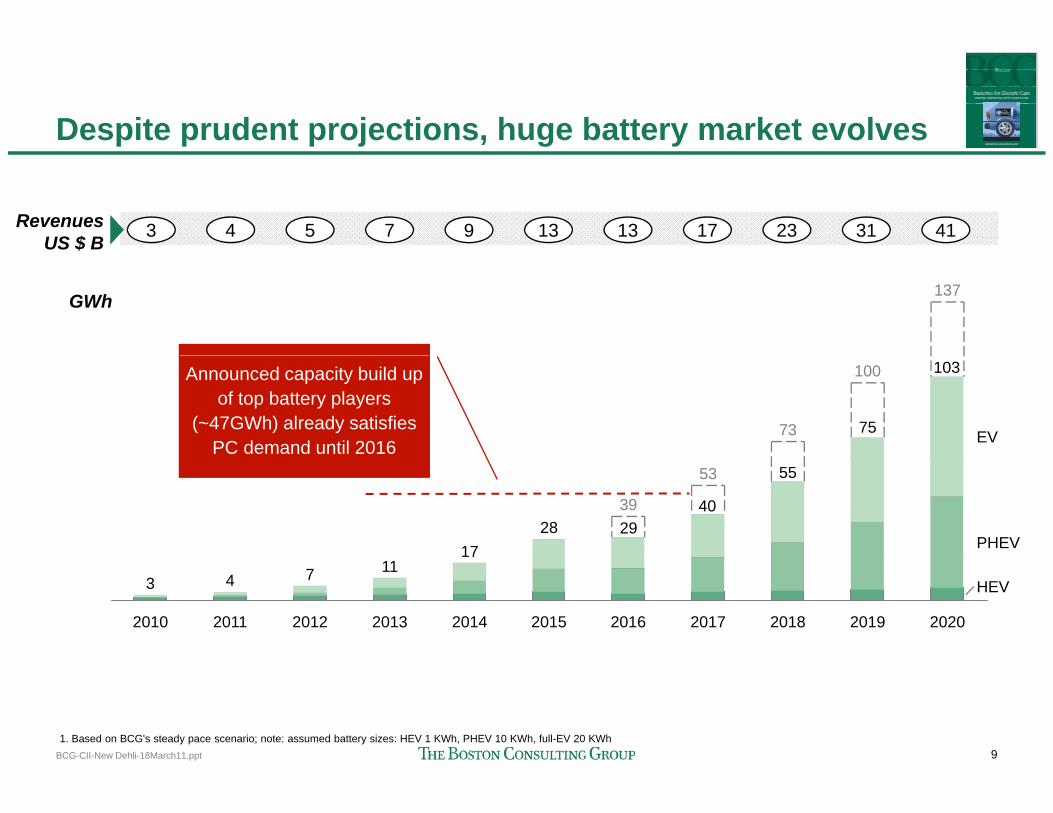

Despite prudent projections, huge battery market evolves

3 4 5 7 9 13 13 17 23 31 41RevenuesUS $ B

137GWh

EV

100

73

Announced capacity build up of top battery players

(~47GWh) already satisfies PC demand until 2016

103

75

PHEV

53

3928

1711

55

4029

HEV

20202019201820172016201520142013

11

2012

7

2011

4

2010

3

9BCG-CII-New Dehli-18March11.ppt

1. Based on BCG's steady pace scenario; note: assumed battery sizes: HEV 1 KWh, PHEV 10 KWh, full-EV 20 KWh

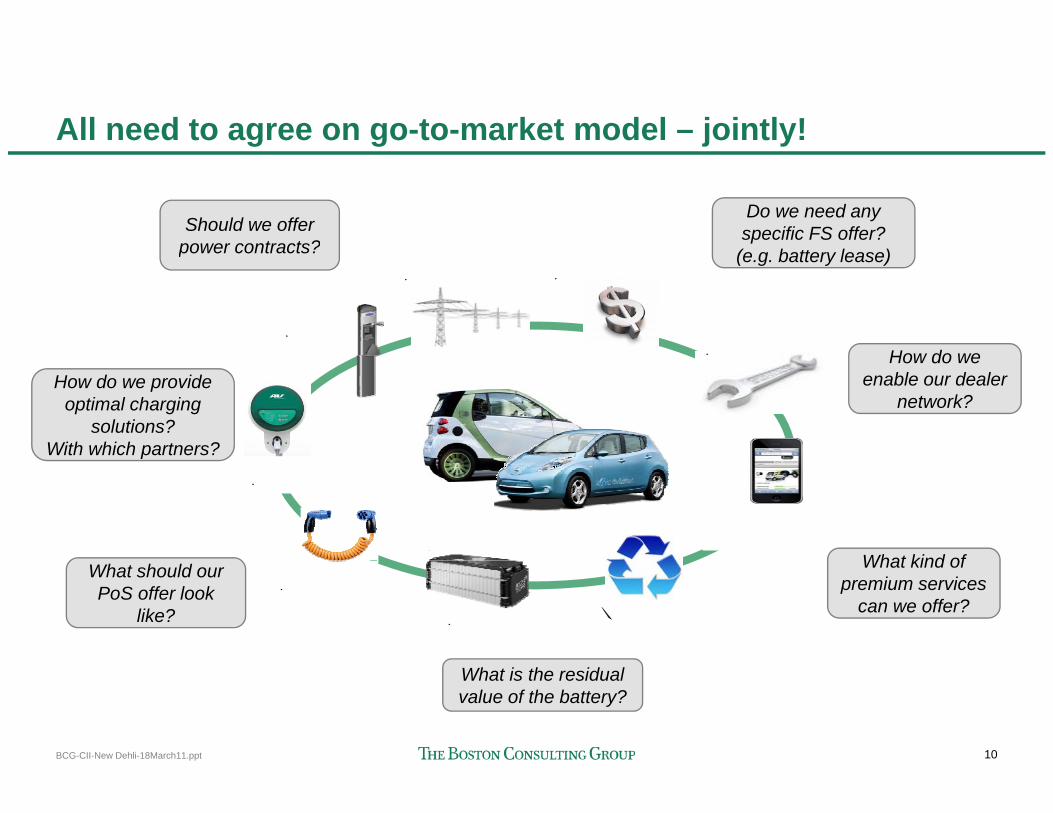

All need to agree on go-to-market model – jointly!

Do we need any specific FS offer?

(e g battery lease)

Should we offer power contracts?

C�������

P���� �������� F�������� ��������

M How do we

(e.g. battery lease)power contracts?

��������������

http://ed.smart.comhttp://ed.smart.com

���������� How do we enable our dealer

network?How do we provide

optimal charging solutions?

With which partners?W������

����������

��������

What kind of

p

C������� ����

B������

R��������

What kind of premium services

can we offer?

What should our PoS offer look

like?

10BCG-CII-New Dehli-18March11.ppt

What is the residual value of the battery?

Some key take aways for all players

Deal with new uncertainties• Act as an entrepreneur: apply trial & error approach to better understand customer e-mobilityAct as an entrepreneur: apply trial & error approach to better understand customer e mobility

requirements• Limit own risks related to unclear battery durability while keeping prices low for customers• Be agile to react to changes in regulation/incentive schemes

Acquire new capabilities• Integrate vehicle periphery into existing processes• Use new technologies to level out e car related inconveniences• Use new technologies to level out e-car-related inconveniences

Profit form changing market environment• Leverage new market entrants as value-adding partnersg g p• Selectively explore new profit pools• Secure customer interface

G t l/ i i l th iti d l t ll

11BCG-CII-New Dehli-18March11.ppt

Governmental/municipal authorities and regulators as well as industry asociations will play a crucial role