Embed Size (px)

Citation preview

Transportation Fuels Assessments ‐Policy

Economic Demographic and Energy Price InputsEconomic, Demographic, and Energy Price Inputs for Electricity,

Natural Gas and Transportation Fuel DemandNatural Gas, and Transportation Fuel Demand Forecasts

Joint Committee Workshop

February 24, 2011February 24, 2011

Gordon Schremp

Fuels and Transportation Division

California Energy Commission

DATE FEB 24 2011

RECD. FEB 25 2011

DOCKET11-IEP-1L

Topics

• Transportation Energy Demand – Federal and State Policies– Federal ‐ Renewable Fuels Standard (RFS2)– State ‐ Low Carbon Fuel Standard (LCFS)( )

• Transportation Energy Demand – Infrastructure Assessments– Historical & forecast demand– Infrastructure needs – petroleum & renewable fuelsInfrastructure needs petroleum & renewable fuels

• Advanced Biofuel Technologies• Crude Oil

l & f d d– Historical & forecast import demand– Refining capacity scenario & infrastructure needs– Crude oil “screening”

• Other Issues– MOTEMS status, new ozone standards, agricultural commodities,

ethanol import tariffs, blending credits, Macondo oil spill, and energy security

22/24/2011

Federal & State Regulations – More Biofuels

32/24/2011

Renewable Fuels Standard (RFS2) – Increased Demand for Ethanol and BiodieselDemand for Ethanol and Biodiesel

• Federal standard (RFS2) mandates increased use of renewable fuel – both ethanol and biodiesel

• Obligated parties include refiners, importers, and blenders

C i t R bl Id tifi ti N b• Companies can generate Renewable Identification Number (RIN) credits for excess renewable fuel use or purchase credits

• Program is not a “per‐gallon” regulationg p g g

• Regulation impacts can include:– Increased demand for & production of ethanol

– Increased demand for ethanol feedstock such as corn

– Displacement of gasoline

– Need for expanded renewable fuel infrastructure

2/24/2011 4

Renewable Fuels Standard (RFS2)

Total Starch Other Biomass TotalRenewable Fuel Derived Cellulosic Advanced Based Advanced

Requirement Biofuel Biofuels Biofuels Diesel BiofuelsYear Bil Gallons Bil Gallons Bil Gallons Bil Gallons Bil Gallons Bil Gallons

Advanced Biofuels

Year Bil. Gallons Bil. Gallons Bil. Gallons Bil. Gallons Bil. Gallons Bil. Gallons2008 9.00 9.00 0.002009 11.10 10.50 0.10 0.50 0.602010 12.95 12.00 0.10 0.20 0.65 0.952011 13 95 12 60 0 25 0 30 0 80 1 352011 13.95 12.60 0.25 0.30 0.80 1.352012 15.20 13.20 0.50 0.50 1.00 2.002013 16.55 13.80 1.00 0.75 1.00 2.752014 18.15 14.40 1.75 1.00 1.00 3.752015 20.50 15.00 3.00 1.50 1.00 5.502016 22.25 15.00 4.25 2.00 1.00 7.252017 24.00 15.00 5.50 2.50 1.00 9.002018 26.00 15.00 7.00 3.00 1.00 11.002019 28.00 15.00 8.50 3.50 1.00 13.002020 30.00 15.00 10.50 3.50 1.00 15.002021 33.00 15.00 13.50 3.50 1.00 18.002022 36.00 15.00 16.00 4.00 1.00 21.00

Cellulosic requirement downgraded to 6 0 million gallons for 2011

52/24/2011

Cellulosic requirement downgraded to 6.0 million gallons for 2011.

RFS2 Impact on CA Gasoline Demand Forecast2009 Results Will Be Updated2009 Results Will Be Updated

16,000

18,000

Source: Energy Commission analysis.

12,000

14,000

ons

8,000

10,000

Millions of G

allo

Initial Low Gasoline Demand Forecast

Revised Low Gasoline Demand ‐ RFS2 Scenario

4,000

6,000M

Revised E85 Low Demand ‐ RFS2 Scenario

Initial E85 Forecast

0

2,000

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

62/24/2011

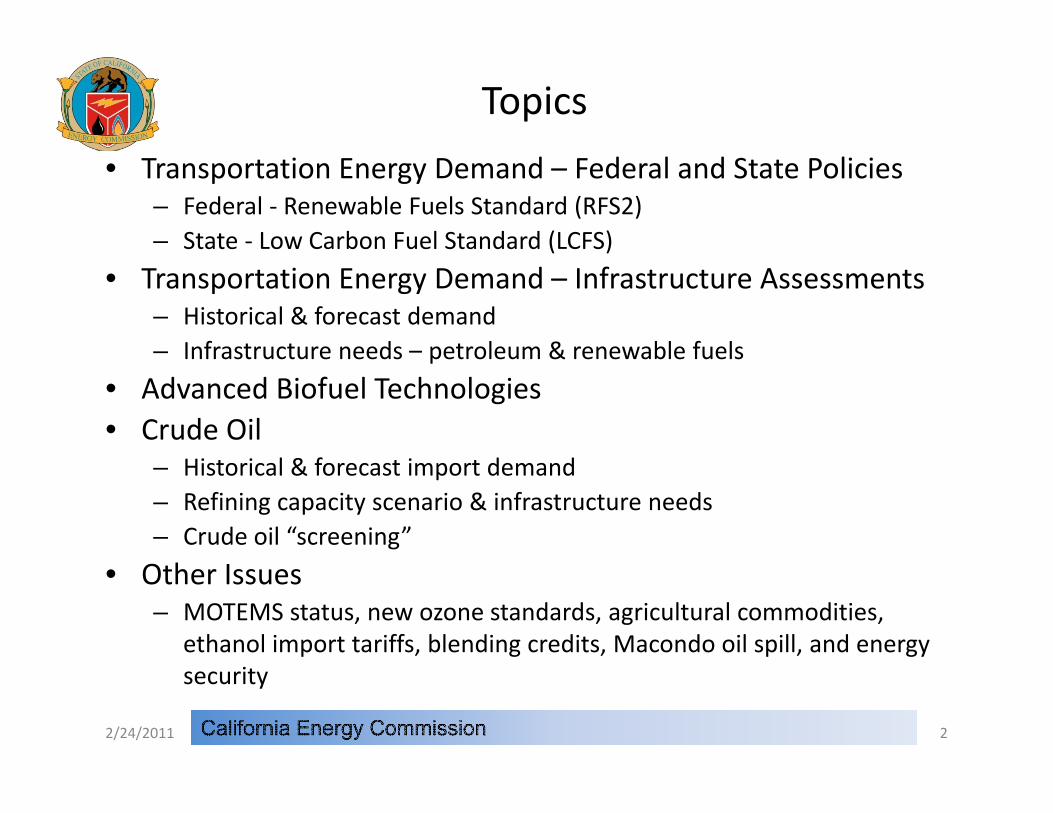

Can contribute to refinery overcapacity & E85 infrastructure constraints.

12%

U.S. Ethanol Concentration in Finished Gasoline

10%

Approaching 10 percent blend “wall.”

8%

4%

6%

2%

4%

0%

‐05

‐05

‐05

‐05

‐06

‐06

‐06

‐06

‐07

‐07

‐07

‐07

‐08

‐08

‐08

‐08

‐09

‐09

‐09

‐09

‐10

‐10

‐10

‐10

Source: Energy Information Administration

Jan

Apr‐

Jul‐

Oct‐

Jan

Apr‐

Jul‐

Oct‐

Jan

Apr‐

Jul‐

Oct‐

Jan

Apr‐

Jul‐

Oct‐

Jan

Apr‐

Jul‐

Oct‐

Jan

Apr‐

Jul‐

Oct‐

72/24/2011

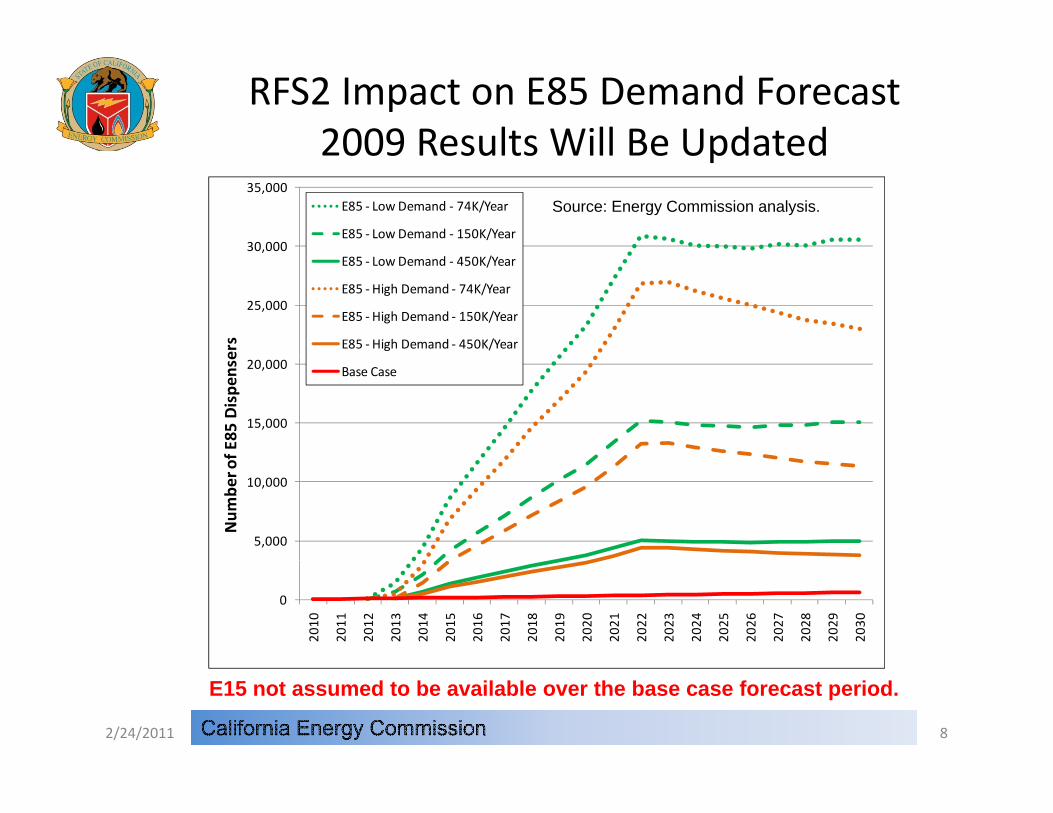

RFS2 Impact on E85 Demand Forecast2009 Results Will Be Updated2009 Results Will Be Updated

30,000

35,000E85 ‐ Low Demand ‐ 74K/Year

E85 ‐ Low Demand ‐ 150K/Year

Source: Energy Commission analysis.

25,000

,ers

E85 ‐ Low Demand ‐ 450K/Year

E85 ‐High Demand ‐ 74K/Year

E85 ‐High Demand ‐ 150K/Year

E85 ‐High Demand ‐ 450K/Year

15,000

20,000

f E85

Dispe

nse

Base Case

5,000

10,000

Num

ber o

f

0

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

82/24/2011

E15 not assumed to be available over the base case forecast period.

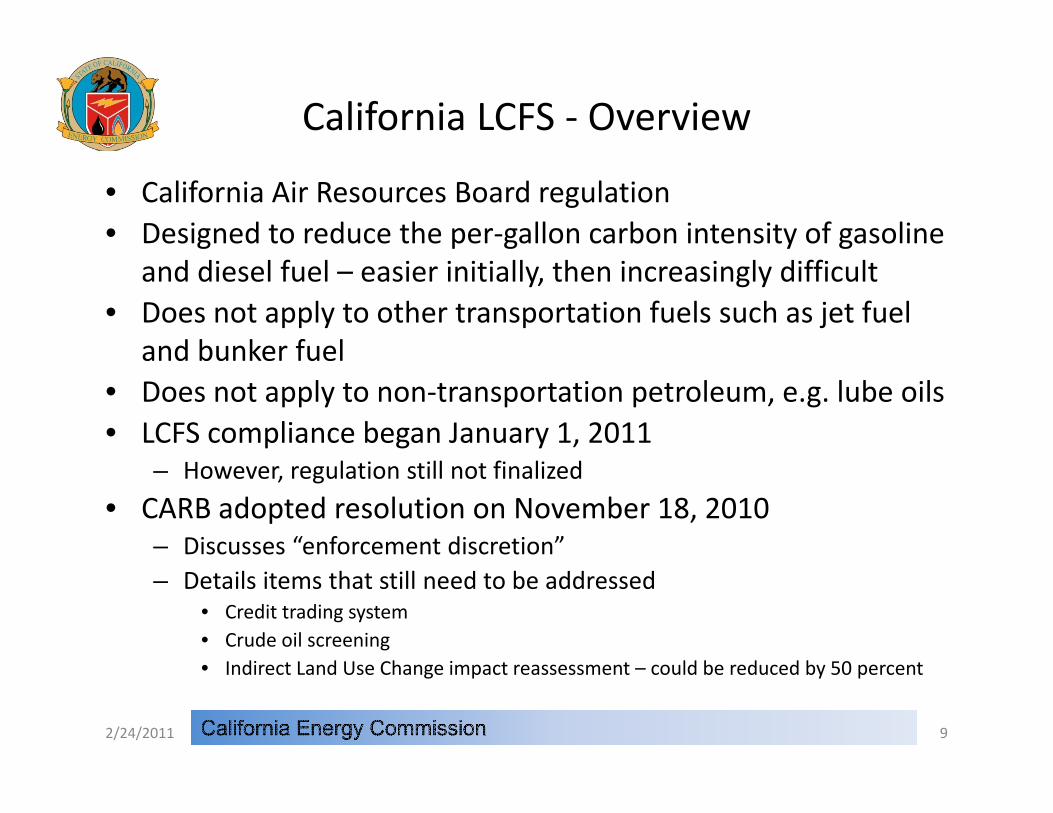

California LCFS ‐ Overview

• California Air Resources Board regulation• Designed to reduce the per‐gallon carbon intensity of gasoline

and diesel fuel – easier initially, then increasingly difficult• Does not apply to other transportation fuels such as jet fuel

and bunker fueland bunker fuel• Does not apply to non‐transportation petroleum, e.g. lube oils• LCFS compliance began January 1, 2011

– However, regulation still not finalized

• CARB adopted resolution on November 18, 2010– Discusses “enforcement discretion”– Details items that still need to be addressed

• Credit trading system• Crude oil screening

I di t L d U Ch i t t ld b d d b 50 t• Indirect Land Use Change impact reassessment – could be reduced by 50 percent

2/24/2011 9

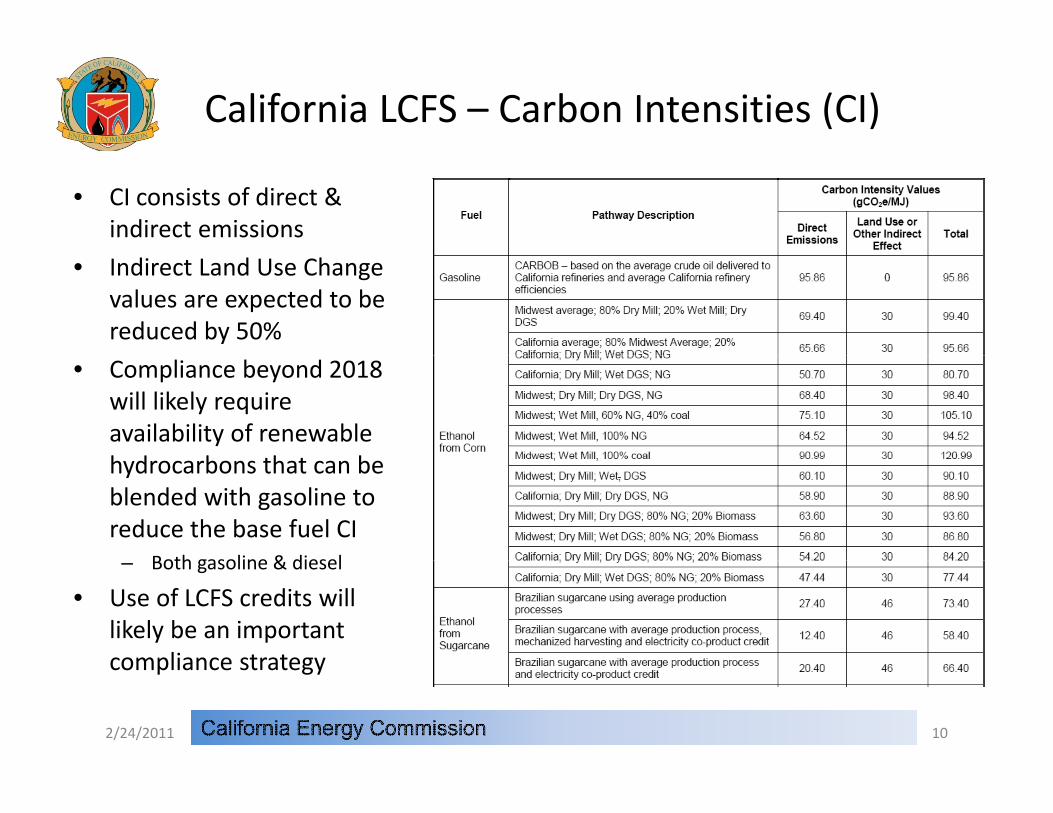

California LCFS – Carbon Intensities (CI)

• CI consists of direct & indirect emissions

• Indirect Land Use Change values are expected to be reduced by 50%

• Compliance beyond 2018 will likely require availability of renewable h d b th t bhydrocarbons that can be blended with gasoline to reduce the base fuel CI

Both gasoline & diesel– Both gasoline & diesel

• Use of LCFS credits will likely be an important compliance strategycompliance strategy

2/24/2011 10

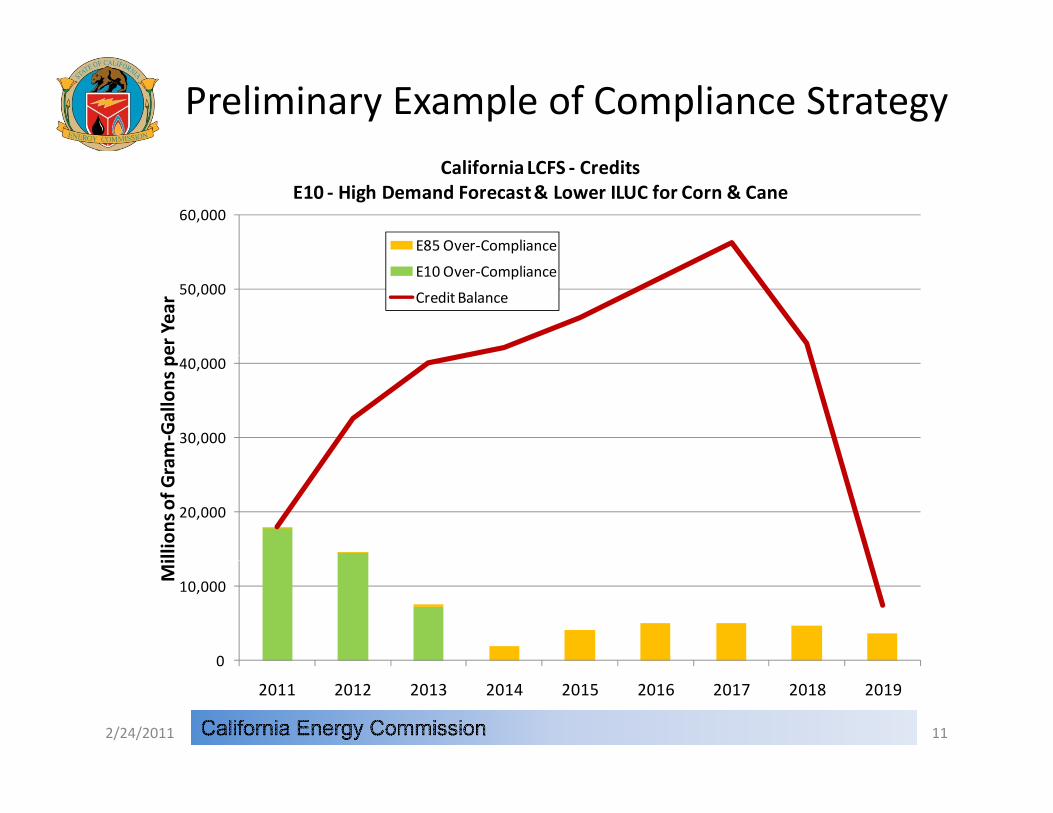

Preliminary Example of Compliance Strategy

60,000

California LCFS ‐ CreditsE10 ‐ High Demand Forecast & Lower ILUC for Corn & Cane

E85 Over‐Compliance

50,000

er Year

p

E10 Over‐Compliance

Credit Balance

30,000

40,000

m‐Gallons p

20,000

illions of G

ra

0

10,000

Mi

112/24/2011

0

2011 2012 2013 2014 2015 2016 2017 2018 2019

Transportation Energy DemandInfrastructure AssessmentsInfrastructure Assessments

122/24/2011

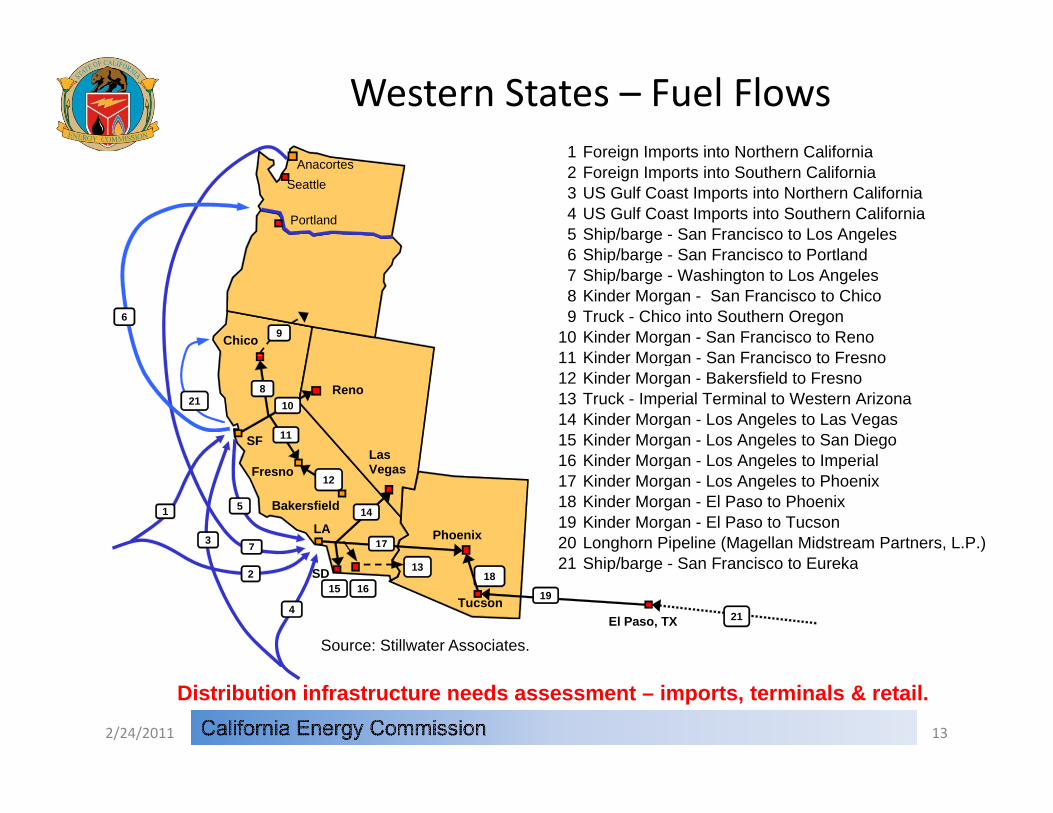

Western States – Fuel Flows1 Foreign Imports into Northern California

AnacortesSeattle

Portland

1 Foreign Imports into Northern California2 Foreign Imports into Southern California3 US Gulf Coast Imports into Northern California4 US Gulf Coast Imports into Southern California5 Ship/barge - San Francisco to Los Angeles6 Ship/barge San Francisco to Portland

Chico 96

6 Ship/barge - San Francisco to Portland7 Ship/barge - Washington to Los Angeles8 Kinder Morgan - San Francisco to Chico9 Truck - Chico into Southern Oregon

10 Kinder Morgan - San Francisco to Reno11 Kinder Morgan San Francisco to Fresno

SFLas

Reno810

11

21

11 Kinder Morgan - San Francisco to Fresno12 Kinder Morgan - Bakersfield to Fresno13 Truck - Imperial Terminal to Western Arizona14 Kinder Morgan - Los Angeles to Las Vegas15 Kinder Morgan - Los Angeles to San Diego16 Kinder Morgan Los Angeles to Imperial

LA

Bakersfield

LasVegas

Phoenix7

1

3

5 14

17

12Fresno

16 Kinder Morgan - Los Angeles to Imperial17 Kinder Morgan - Los Angeles to Phoenix18 Kinder Morgan - El Paso to Phoenix19 Kinder Morgan - El Paso to Tucson20 Longhorn Pipeline (Magellan Midstream Partners, L.P.)21 Ship/barge San Francisco to Eureka

TucsonEl Paso, TX

15SD

21

2

4

1816 19

13 21 Ship/barge - San Francisco to Eureka

Source: Stillwater Associates.

132/24/2011

Distribution infrastructure needs assessment – imports, terminals & retail.

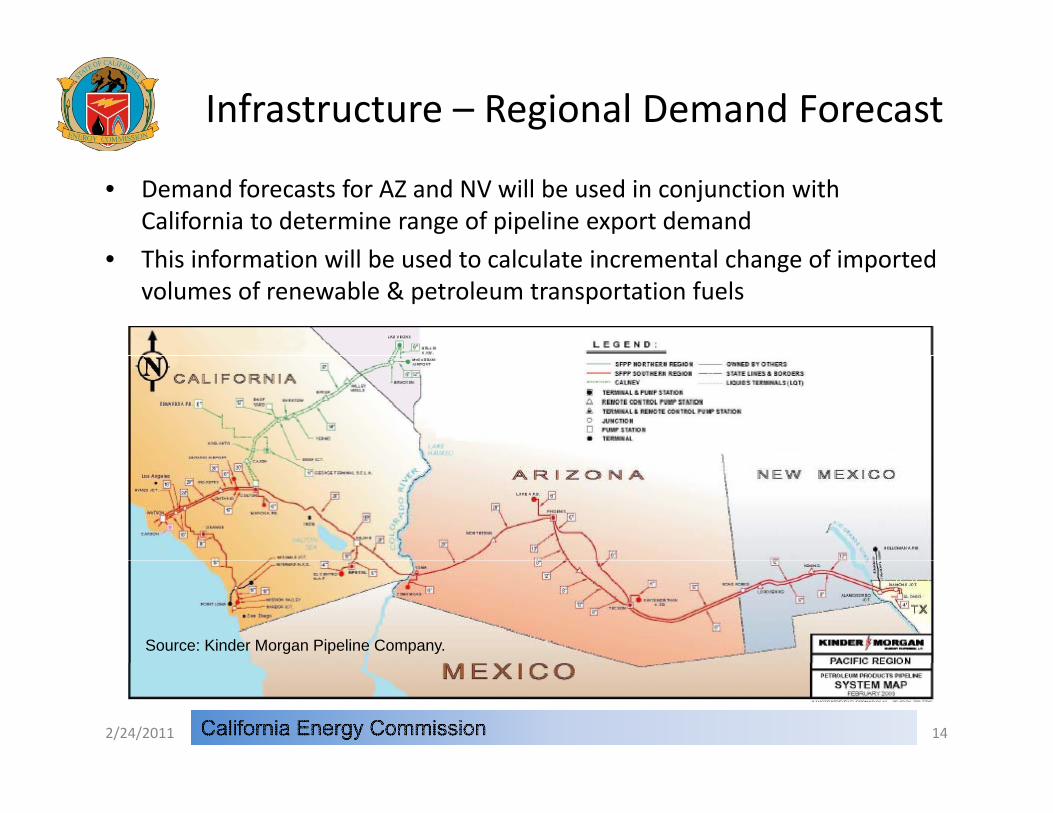

Infrastructure – Regional Demand Forecast

• Demand forecasts for AZ and NV will be used in conjunction with California to determine range of pipeline export demand

Thi i f ti ill b d t l l t i t l h f i t d• This information will be used to calculate incremental change of imported volumes of renewable & petroleum transportation fuels

Source: Kinder Morgan Pipeline Company.

2/24/2011 14

Infrastructure – Regional Pipeline Projects

• UNEV pipeline could become operational as early as the 2nd Q of 2011 with an initial pumping capacity of 30,000 BPD

• Over time, the pipeline system could be expanded to a maximum pumping capacity of up to

8 000118,000 BPD

• Will displace an undetermined portion of the forecasted pipeline d li i L V fdeliveries to Las Vegas from California

2/24/2011 15

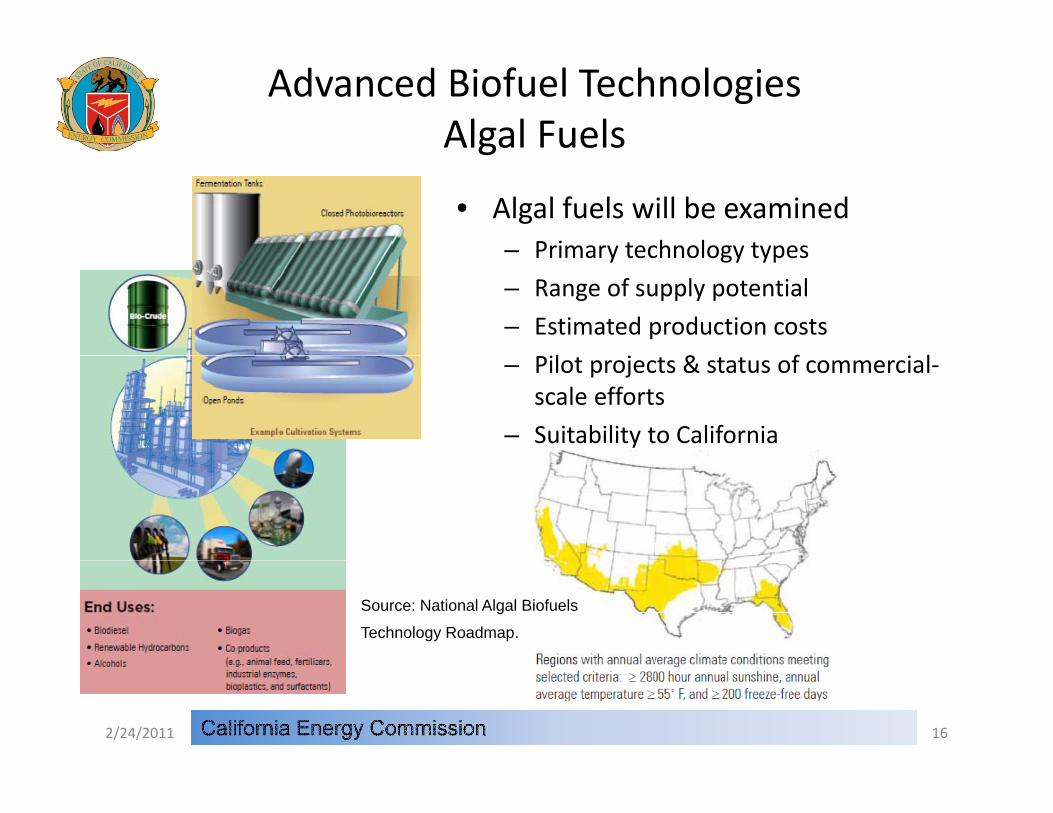

Advanced Biofuel TechnologiesAlgal Fuelsg

• Algal fuels will be examined– Primary technology typesPrimary technology types

– Range of supply potential

– Estimated production costs

l & f l– Pilot projects & status of commercial‐scale efforts

– Suitability to California

Source: National Algal Biofuels

Technology Roadmap.

2/24/2011 16

Advanced Biofuel TechnologiesRenewable Hydrocarbonsy

• Renewable hydrocarbon fuels will be examinedexamined– Primary technology types

– Range of supply potential

d d– Estimated production costs

– Pilot projects & status of commercial‐scale efforts

• Demand will increase for “drop in” blending components that can be used to decrease CI of gasoline diesel & jetto decrease CI of gasoline, diesel & jet fuel– Will likely be necessary to achieve

compliance with LCFS regulationNExBTL-diesel started at the Porvoo refinery in 2007.compliance with LCFS regulation

2/24/2011 17

y

Crude Oil

182/24/2011

Crude Oil – Import Forecast

• Crude Oil Import Forecast – Several Elements– California oil production – historical & forecast rate of decline– Demand forecast for petroleum‐based transportation fuels

450Production Peaked in 1985424 Million Barrels

p p• California, Nevada & Arizona

– California refining capacity – level or declining?

300

350

400

r Yea

r

424 Million Barrels

150

200

250

s of

Bar

rels

per

Cumulative CrudeOil Production

28.2 Billion Barrels, Equivalent to 10.7

Months of 2010 Global Demand of87 7 Milli B l

0

50

100

Mill

ions 87.7 Million Barrels

Per Day

0

1876

1883

1890

1897

1904

1911

1918

1925

1932

1939

1946

1953

1960

1967

1974

1981

1988

1995

2002

2009

192/24/2011

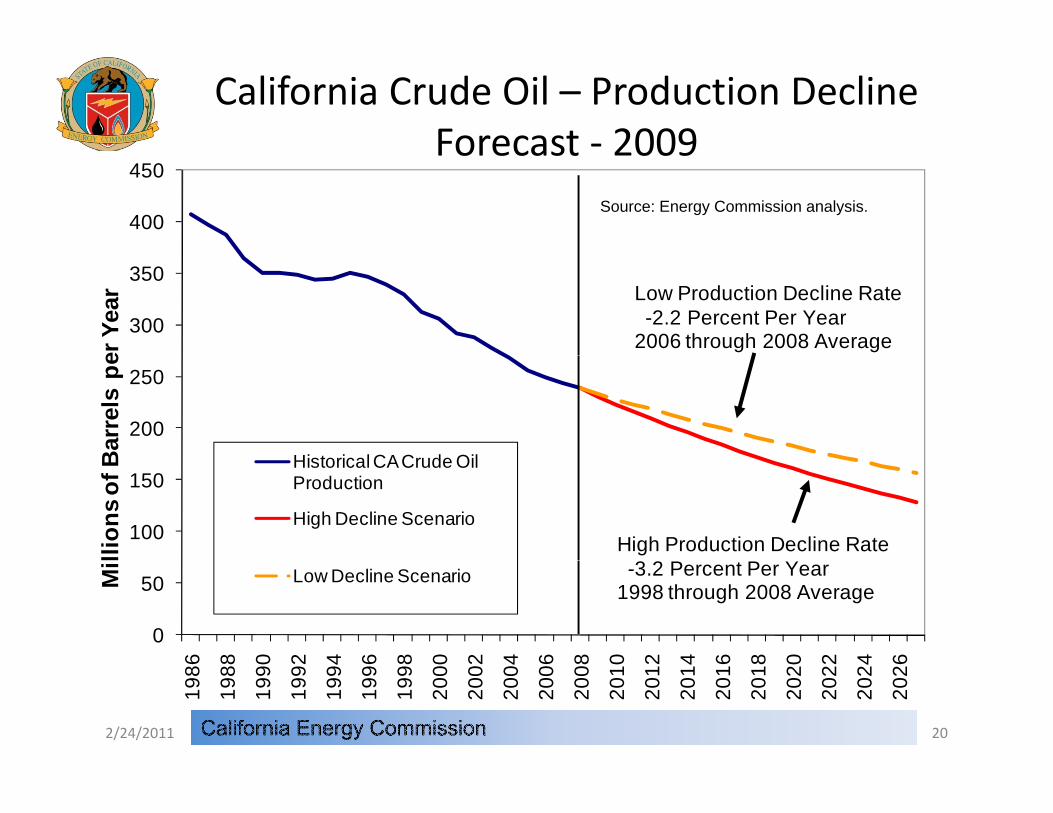

California Crude Oil – Production Decline Forecast ‐ 2009

400

450Forecast 2009

Source: Energy Commission analysis.

300

350

er Y

ear Low Production Decline Rate

-2.2 Percent Per Year2006 through 2008 Average

200

250

Bar

rels

pe

Historical CACr de Oil

100

150

llion

s of

B Historical CA Crude Oil Production

High Decline ScenarioHigh Production Decline Rate

0

50

6 8 0 2 4 6 8 0 2 4 6 8 0 2 4 6 8 0 2 4 6

Mi

Low Decline Scenario -3.2 Percent Per Year1998 through 2008 Average

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

202/24/2011

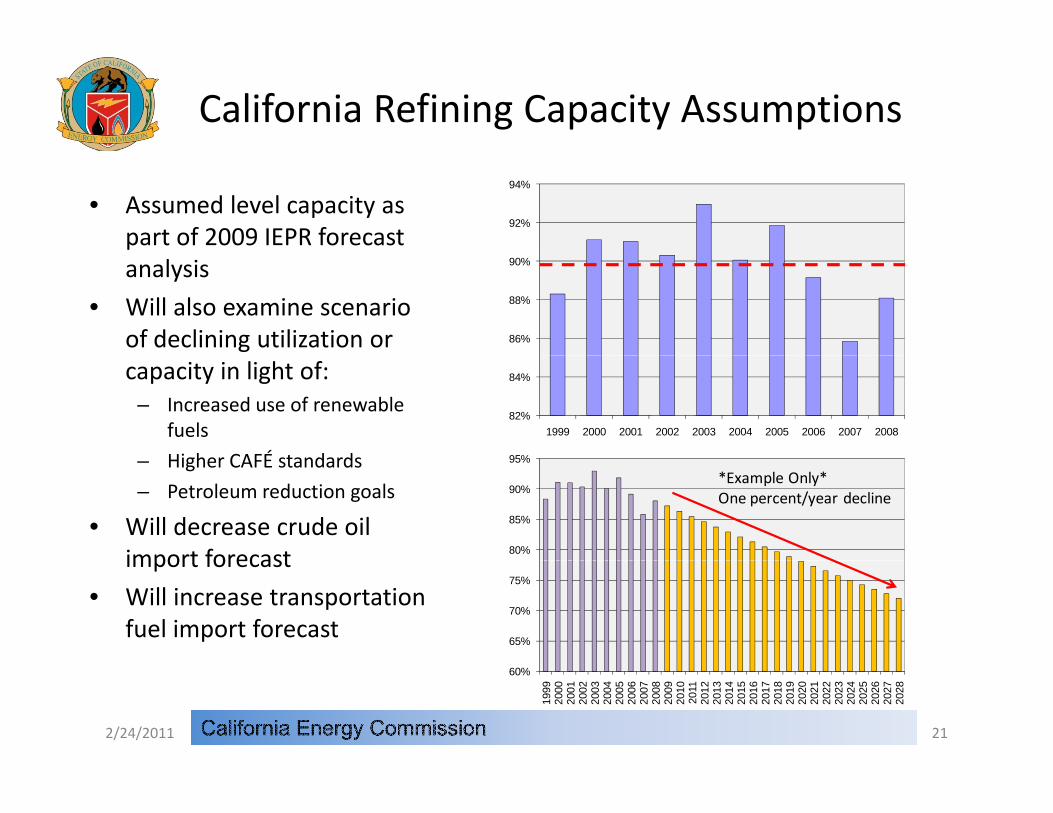

California Refining Capacity Assumptions

92%

94%

• Assumed level capacity as part of 2009 IEPR forecast

86%

88%

90%analysis

• Will also examine scenario of declining utilization or

82%

84%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

capacity in light of:– Increased use of renewable

fuels

Higher CAFÉ standards 95%– Higher CAFÉ standards

– Petroleum reduction goals

• Will decrease crude oil import forecast 80%

85%

90%

95%

*Example Only*One percent/year decline

import forecast

• Will increase transportation fuel import forecast

65%

70%

75%

2/24/2011 21

60%

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

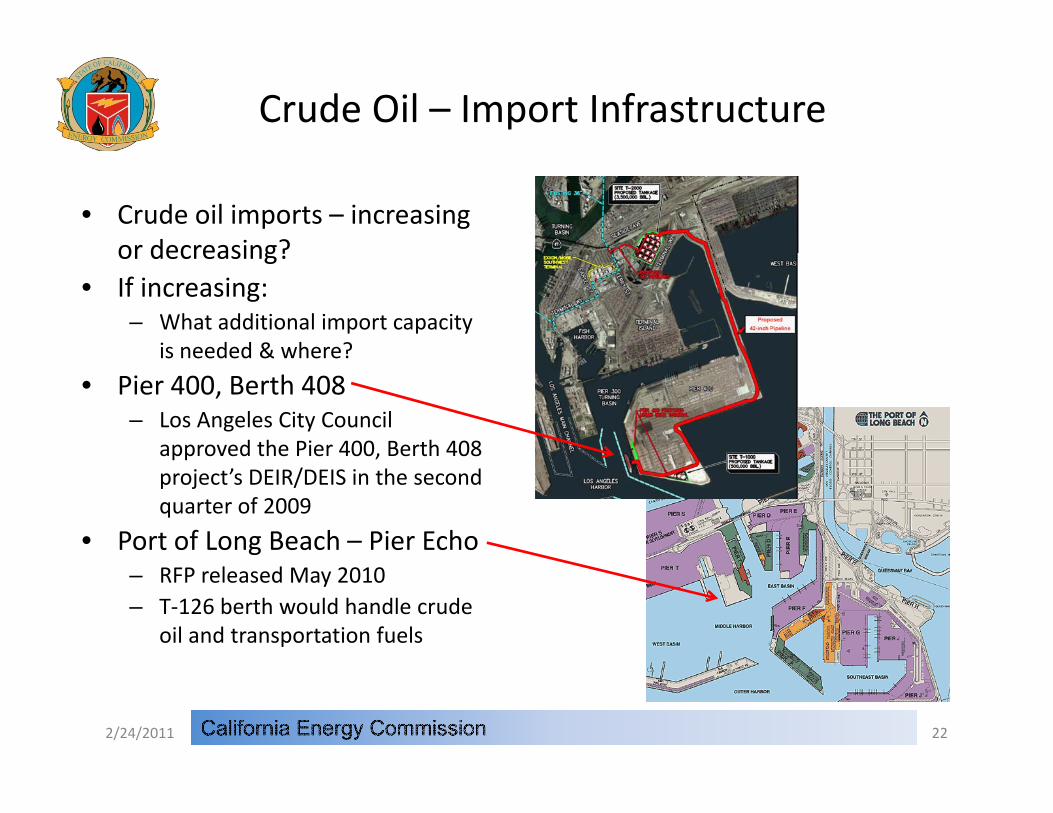

Crude Oil – Import Infrastructure

• Crude oil imports – increasing or decreasing?or decreasing?

• If increasing:– What additional import capacity

is needed & where?is needed & where?

• Pier 400, Berth 408– Los Angeles City Council

approved the Pier 400, Berth 408 pp ,project’s DEIR/DEIS in the second quarter of 2009

• Port of Long Beach – Pier Echo– RFP released May 2010– T‐126 berth would handle crude

oil and transportation fuels

2/24/2011 22

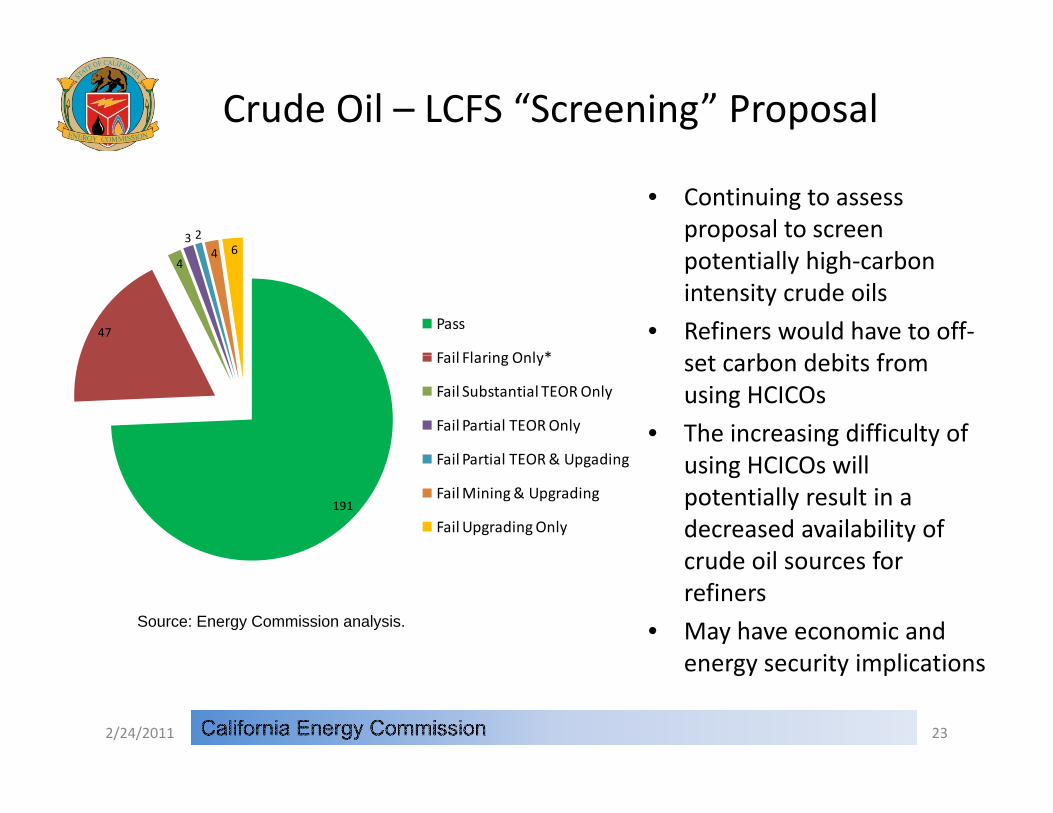

Crude Oil – LCFS “Screening” Proposal

• Continuing to assess proposal to screen

i ll hi h b3 2

4 6 potentially high‐carbon intensity crude oils

• Refiners would have to off‐b d bi f

47

44 6

Pass

Fail Flaring Only* set carbon debits from using HCICOs

• The increasing difficulty of i HCICO ill

Fail Flaring Only*

Fail Substantial TEOR Only

Fail Partial TEOR Only

Fail Partial TEOR& Upgading using HCICOs will potentially result in a decreased availability of crude oil sources for

191

Fail Partial TEOR & Upgading

Fail Mining & Upgrading

Fail Upgrading Only

crude oil sources for refiners

• May have economic and energy security implications

Source: Energy Commission analysis.

energy security implications

2/24/2011 23

Other Issues – MOTEMS Update

• Marine Oil Terminal Engineering & Maintenance Standards (MOTEMS) part of California Business Code – Chapter 31F– Require upgrades to existing marine terminals to reduce the risk of

spill related to earthquakes and tsunamis

• Most, if not all, marine oil terminals with medium or high riskMost, if not all, marine oil terminals with medium or high risk of a potential spill have completed their safety audits– Include assessments of work that needs to be completed to achieve

compliance with the standardscompliance with the standards

• Timing impacted by discussion over who pays

• It is possible that some facilities will not be upgraded and p pgtheir leases not renewed– Forecast for imports (both crude oil and transportation fuels) will have

a direct role in this debatea direct role in this debate

2/24/2011 24

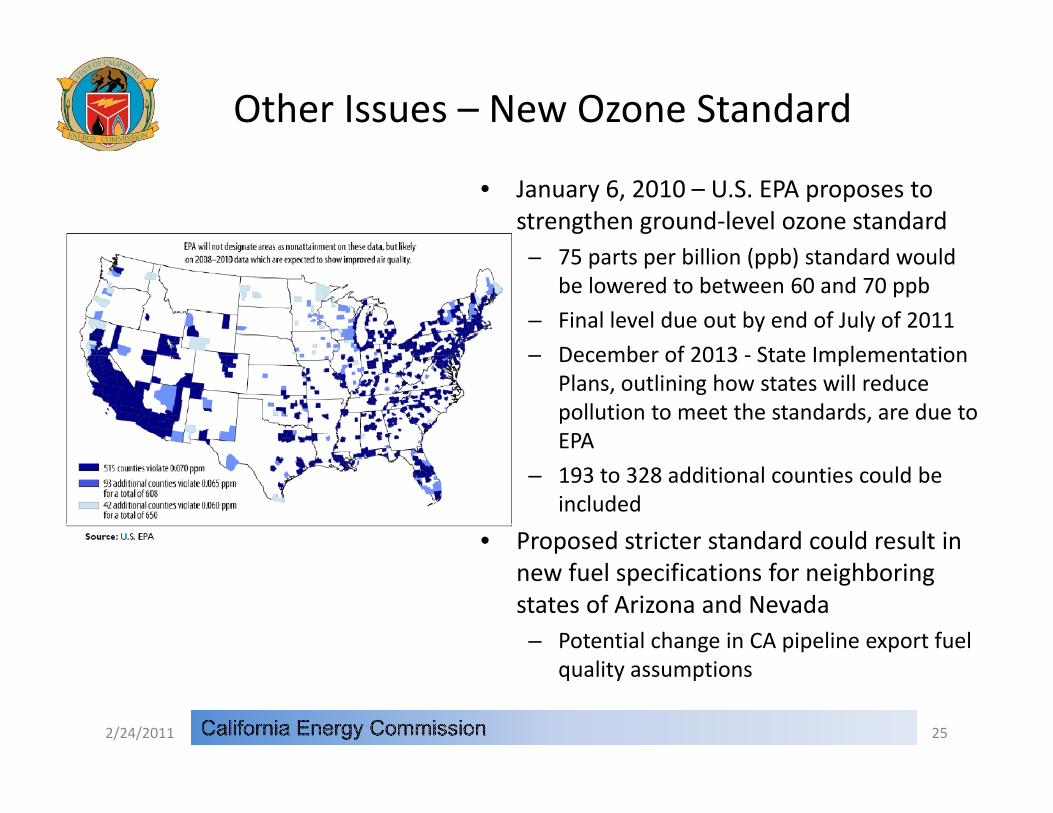

Other Issues – New Ozone Standard

• January 6, 2010 – U.S. EPA proposes to strengthen ground‐level ozone standard

75 t billi ( b) t d d ld– 75 parts per billion (ppb) standard would be lowered to between 60 and 70 ppb

– Final level due out by end of July of 2011

– December of 2013 ‐ State Implementation– December of 2013 ‐ State Implementation Plans, outlining how states will reduce pollution to meet the standards, are due to EPA

– 193 to 328 additional counties could be included

• Proposed stricter standard could result in new fuel specifications for neighboring states of Arizona and Nevada– Potential change in CA pipeline export fuel

lit tiquality assumptions

2/24/2011 25

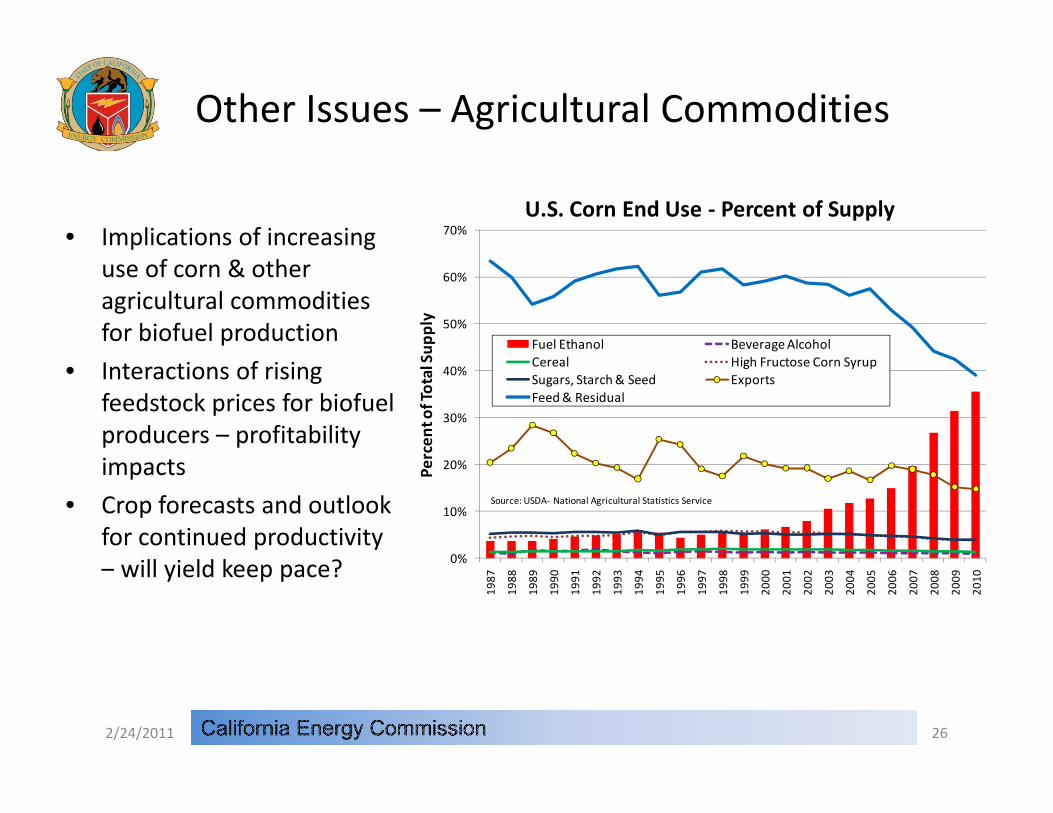

Other Issues – Agricultural Commodities

• Implications of increasing 70%U.S. Corn End Use ‐ Percent of Supply

use of corn & other agricultural commodities for biofuel production 50%

60%

Supp

ly

Fuel Ethanol Beverage Alcohol

• Interactions of rising feedstock prices for biofuel producers – profitability i

30%

40%

rcen

t of Total S Cereal High Fructose Corn Syrup

Sugars, Starch & Seed ExportsFeed & Residual

impacts

• Crop forecasts and outlook for continued productivity

ill i ld k ? 0%

10%

20%Per

Source: USDA‐ National Agricultural Statistics Service

– will yield keep pace? 0%

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2/24/2011 26

Other Issues ‐ Ethanol Import Tariff

• Brazilian exporters of ethanol to the U.S. must pay two types of i t d tiimport duties– Ad valorem tax equivalent to

2.5 percent of the ethanol transaction price

– Secondary import duty of 54 cents per gallon

• California demand for sugarcane‐based ethanol could be significant under LCFS

• Is it time to retire this duty?

• How might the price of ethanol be affected?

Source: José Goldemberg, Biotechnology for Biofuels 2008.

be affected?

2/24/2011 27

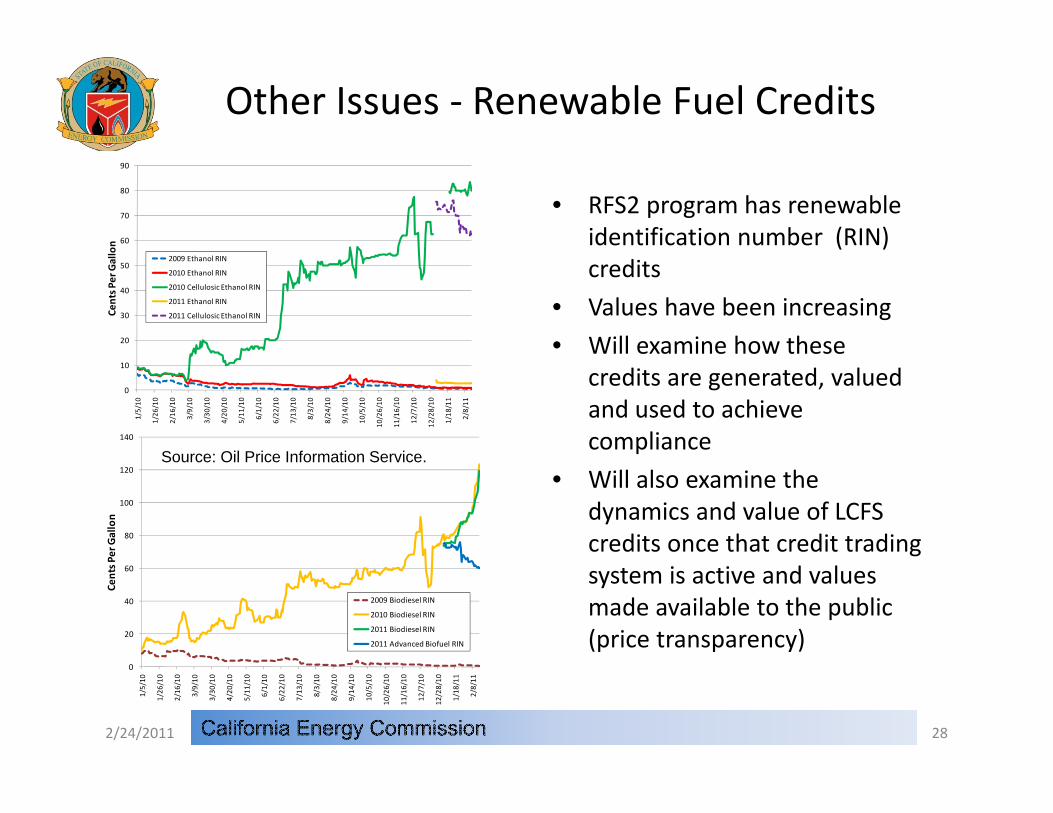

Other Issues ‐ Renewable Fuel Credits

• RFS2 program has renewable identification number (RIN) 60

70

80

90

on

credits

• Values have been increasing

• Will examine how these 20

30

40

50

Cents P

er Gall

2009 Ethanol RIN

2010 Ethanol RIN

2010 Cellulosic Ethanol RIN

2011 Ethanol RIN

2011 Cellulosic Ethanol RIN

140

credits are generated, valued and used to achieve compliance

0

10

1/5/10

1/26

/10

2/16

/10

3/9/10

3/30

/10

4/20

/10

5/11

/10

6/1/10

6/22

/10

7/13

/10

8/3/10

8/24

/10

9/14

/10

10/5/10

10/26/10

11/16/10

12/7/10

12/28/10

1/18

/11

2/8/11

Source: Oil Price Information Service

80

100

120

Per G

allon

• Will also examine the dynamics and value of LCFS credits once that credit trading

Source: Oil Price Information Service.

20

40

60

Cents P

2009 Biodiesel RIN

2010 Biodiesel RIN

2011 Biodiesel RIN

2011 Advanced Biofuel RIN

system is active and values made available to the public (price transparency)

0

1/5/10

1/26

/10

2/16

/10

3/9/10

3/30

/10

4/20

/10

5/11

/10

6/1/10

6/22

/10

7/13

/10

8/3/10

8/24

/10

9/14

/10

10/5/10

10/26/10

11/16/10

12/7/10

12/28/10

1/18

/11

2/8/11

2/24/2011 28

Other Issues ‐Macondo Oil Spill

• 78 to 167 million gallons released to environment

• At higher estimate ‐ largest• At higher estimate ‐ largest volume of accidental release in world history

• Status of U.S. offshore drilling

• California vs. Gulf ‐ comparison of drilling environment & potentialdrilling environment & potential resource base estimates

• Prospects of renewed drilling in California’s offshore watersCalifornia s offshore waters

2/24/2011 29

Other Issues – Energy Security

• The issue of energy security i tt ti dis attracting renewed interest as a policy consideration

• Analysis of transportation fuel issues will include a qualitative energy securityqualitative energy security assessment for specific fuels and crude oil

• Can also be relevant for renewable fuels and even advanced technologiesadvanced technologies

2/24/2011 30

Additional Q & A

Torrent Ducks – Rio Bremajo – Near San Isidro, Eastern Ecuador 10-15-2010

312/24/2011