Embed Size (px)

Citation preview

Presenting a live 110‐minute teleconference with interactive Q&A

Economic Obsolescence in Property ValuationsEconomic Obsolescence in Property ValuationsLeveraging Market Conditions to Reduce Business Personal and Real Property Assessments and Taxes

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, AUGUST 18, 2011

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Stephen Paul Partner Baker & Daniels IndianapolisStephen Paul, Partner, Baker & Daniels, Indianapolis

Alfred King, Vice Chairman and Director, Marshall & Stevens, Spottsylvania, Va.

C. Stephen Davis, Partner, Cahill Davis & O'Neall, Los Angeles

Scott Tyler, Senior Manager and National Personal Property Tax Practice Leader, Crowe Horwath,

For this program, attendees must listen to the audio over the telephone.

Scott Tyler, Senior Manager and National Personal Property Tax Practice Leader, Crowe Horwath, Tampa, Fla.

Please refer to the instructions emailed to the registrant for the dial-in information.Attendees can still view the presentation slides online. If you have any questions, pleasecontact Customer Service at1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

Attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online but there is no online audio for this program.

Attendees must stay on the line for at least 100 minutes in order to qualify for a full 2 credits of CPE. Attendance is monitored as required by NASBA.

Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.at 1 800 926 7926 ext. 10.

Tips for Optimal Quality

S d Q litSound Quality

For this program, you must listen via the telephone by dialing 1-866-873-1442 and entering your PIN when prompted. There will be no sound over the web connection.co ect o .

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

E i Ob l i P t Economic Obsolescence in Property Valuations Seminar

Aug. 18, 2011

Alfred King, Marshall & [email protected]

Stephen Paul, Baker & [email protected]

C. Stephen Davis, Cahill Davis & O'[email protected]

Scott Tyler, Crowe Horwath [email protected]

Today’s Program

Fundamentals Of Economic Obsolescence[Stephen Paul]

Slide 7 – Slide 18

Quantifying Economic Obsolescence[Alfred King]

Slide 19 – Slide 33

Approaches To Appeals And Litigation[C. Stephen Davis and Scott Tyler]

Slide 34 – Slide 48

FUNDAMENTALS OF Stephen Paul, Baker & Daniels

FUNDAMENTALS OF ECONOMIC OBSOLESCENCE

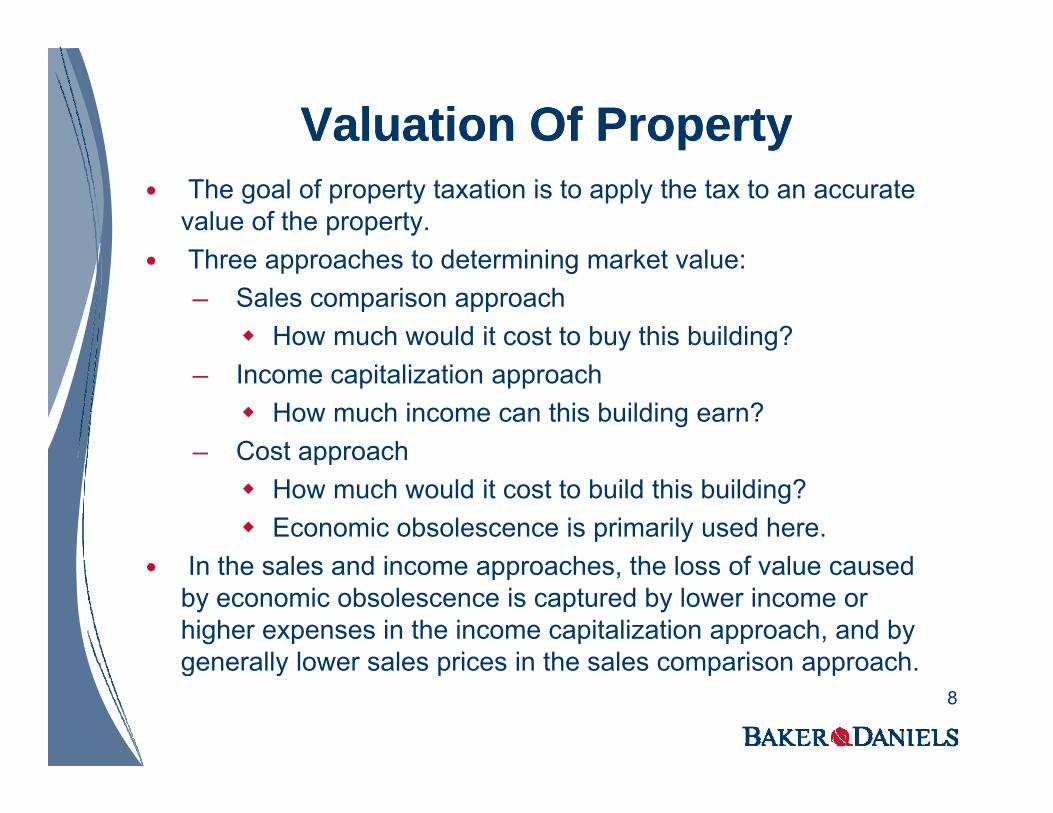

Valuation Of PropertyValuation Of Propertyyy The goal of property taxation is to apply the tax to an accurate

value of the property.Th h t d t i i k t l Three approaches to determining market value:─ Sales comparison approach

How much would it cost to buy this building?─ Income capitalization approach

How much income can this building earn?─ Cost approachCost approach

How much would it cost to build this building? Economic obsolescence is primarily used here.

I th l d i h th l f l d In the sales and income approaches, the loss of value caused by economic obsolescence is captured by lower income or higher expenses in the income capitalization approach, and by generally lower sales prices in the sales comparison approachgenerally lower sales prices in the sales comparison approach.

8

Valuation Of Property (Cont.)Valuation Of Property (Cont.)y ( )y ( )

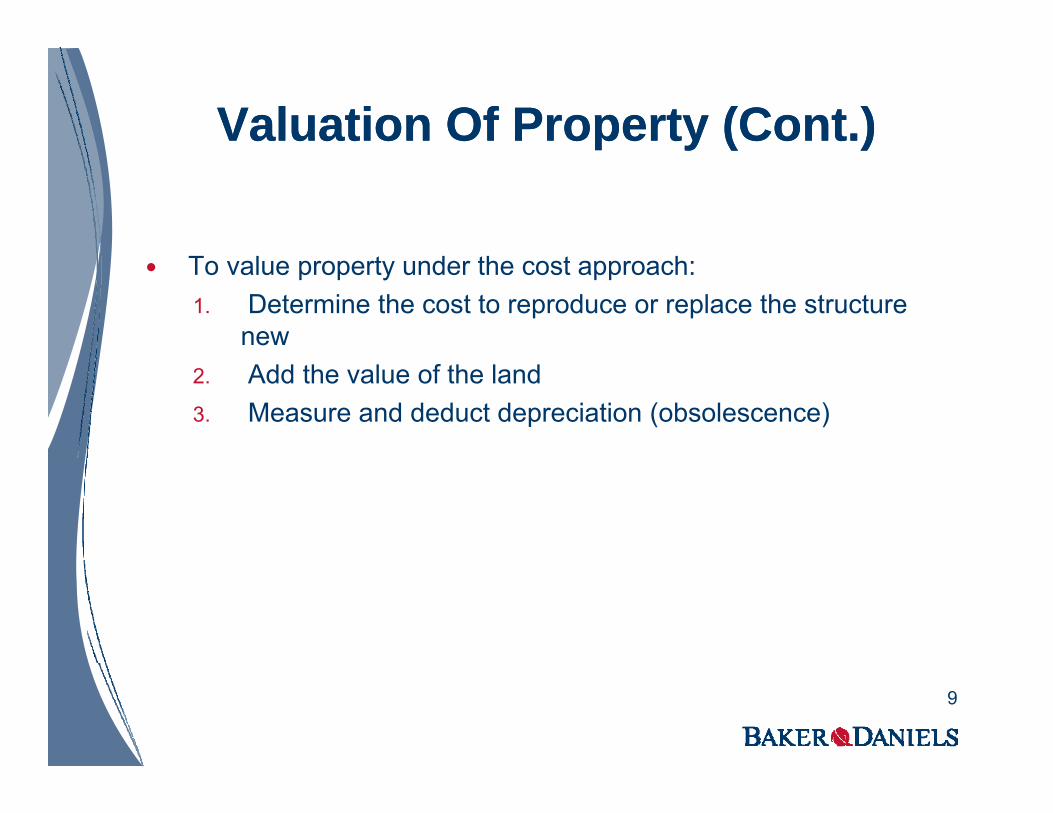

To value property under the cost approach:1. Determine the cost to reproduce or replace the structure

new2. Add the value of the land3. Measure and deduct depreciation (obsolescence)

9

Primary Types Of ObsolescencePrimary Types Of Obsolescencey yy y

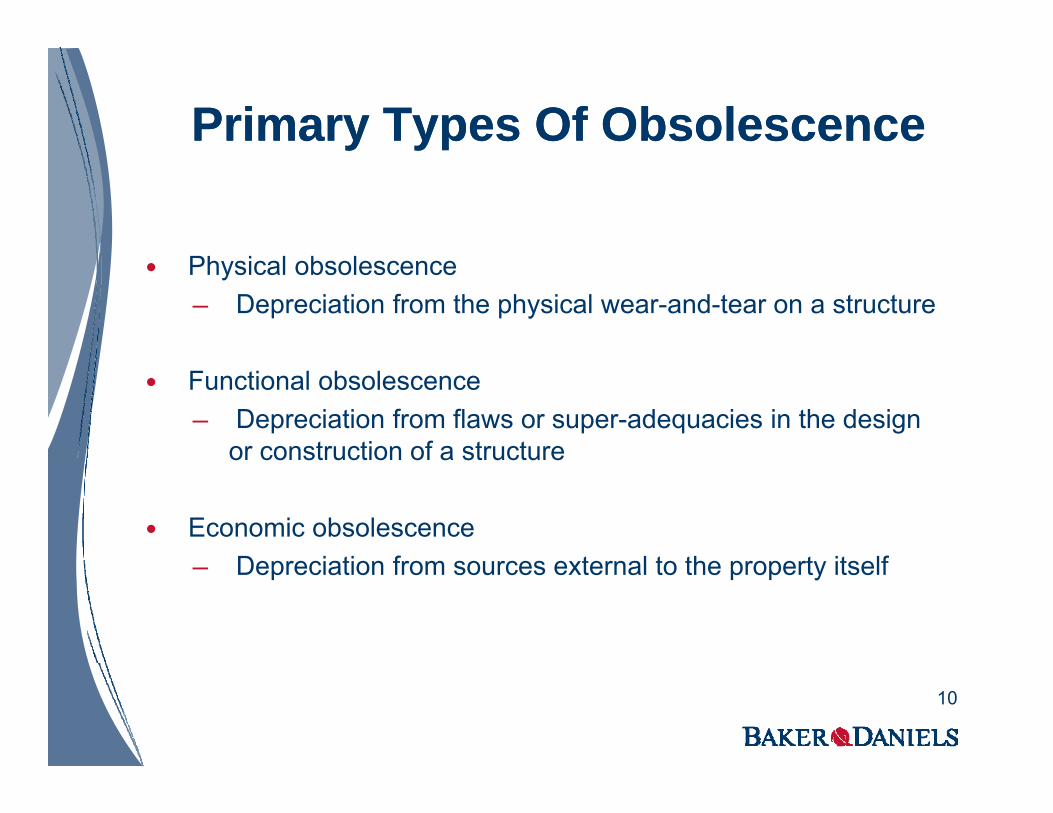

Physical obsolescence─ Depreciation from the physical wear-and-tear on a structure

Functional obsolescence─ Depreciation from flaws or super-adequacies in the design

or construction of a structureor construction of a structure

Economic obsolescenceD i ti f t l t th t it lf─ Depreciation from sources external to the property itself

10

What Is Economic Obsolescence?What Is Economic Obsolescence?

The impairment of desirability or useful life arising from factors external to the property, such as economic forces that affect the supply-demand relationship in the market

May be international, national, industry-based, or local in origin

Economic obsolescence is present when better economic opportunities exist for an investment.

11

What Is Economic Obsolescence? (Cont.)What Is Economic Obsolescence? (Cont.)( )( )

Economic obsolescence is typically incurable, meaning that it t b d d b it l i t t ( d tcannot be reduced by capital investments (as compared to

physical and functional obsolescence).

Sub-categories of economic obsolescence include:─ Market obsolescence─ Locational obsolescence─ Political obsolescence─ Environmental obsolescence

The common theme: External to the property itself─ The common theme: External to the property itself

12

Example Of Economic ObsolescenceExample Of Economic Obsolescence The recent housing crisis provides an excellent example of the

effects of economic obsolescence.

New homes in distressed markets throughout the U.S. are being heavily discounted.

These homes are new, so there is no physical deterioration.

They incorporate modern designs and technologies, so there is no functional obsolescence.

Therefore, all of the value loss is due to factors external to the properties themselves (in this case, market obsolescence).

13

Other Examples OfOther Examples OfEconomic ObsolescenceEconomic ObsolescenceEconomic ObsolescenceEconomic Obsolescence

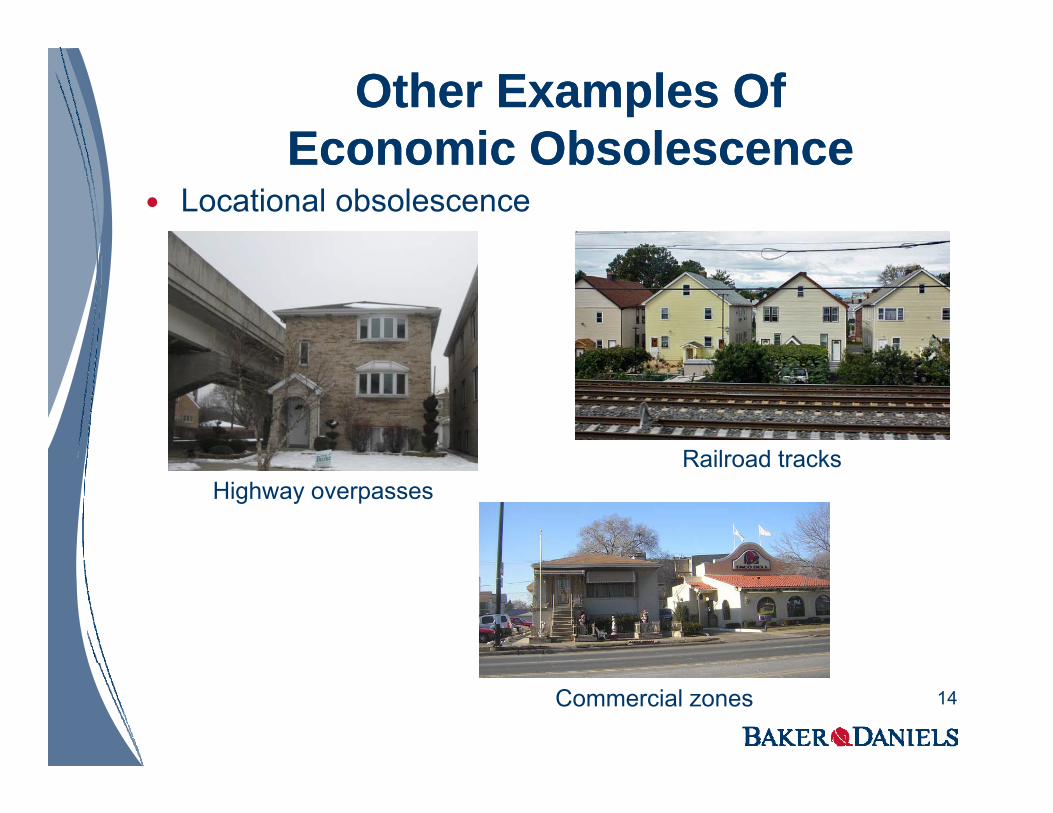

Locational obsolescence

Railroad tracksHighway overpasses

Railroad tracks

Commercial zones 14

Other Examples Of EconomicOther Examples Of EconomicObsolescence (Cont )Obsolescence (Cont )Obsolescence (Cont.)Obsolescence (Cont.)

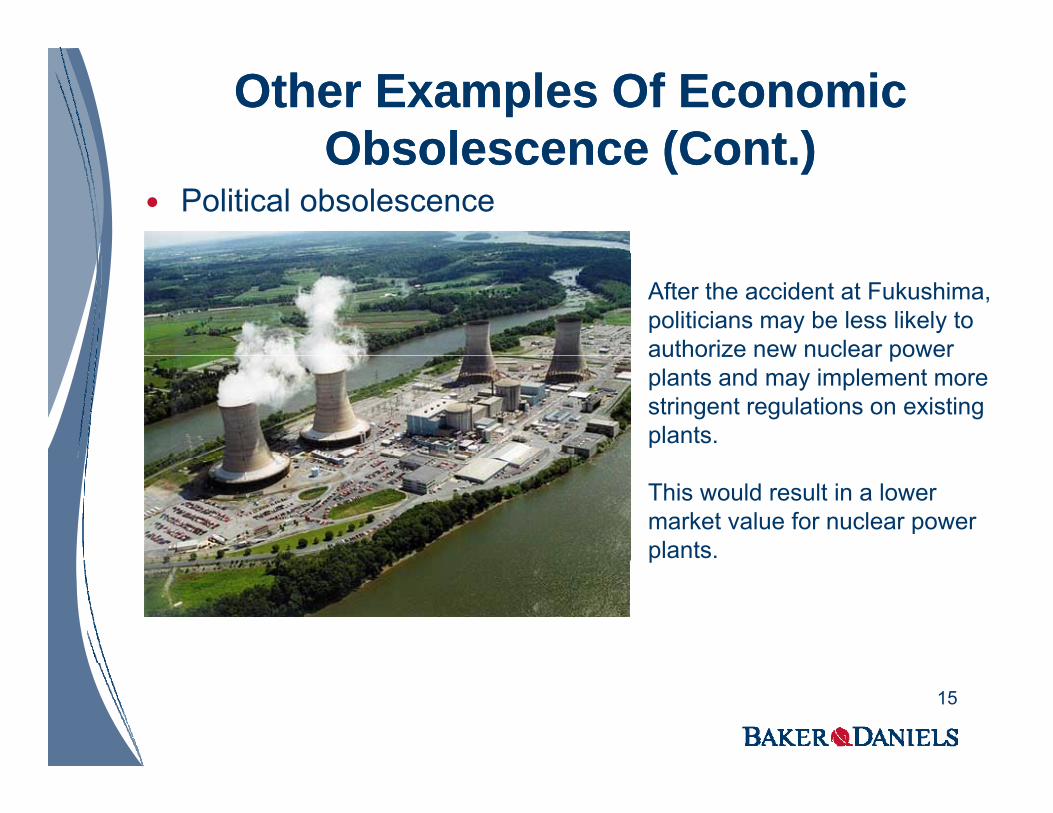

Political obsolescence

After the accident at Fukushima, politicians may be less likely to authorize new nuclear powerauthorize new nuclear power plants and may implement more stringent regulations on existing plants.

This would result in a lower market value for nuclear power plants.p

15

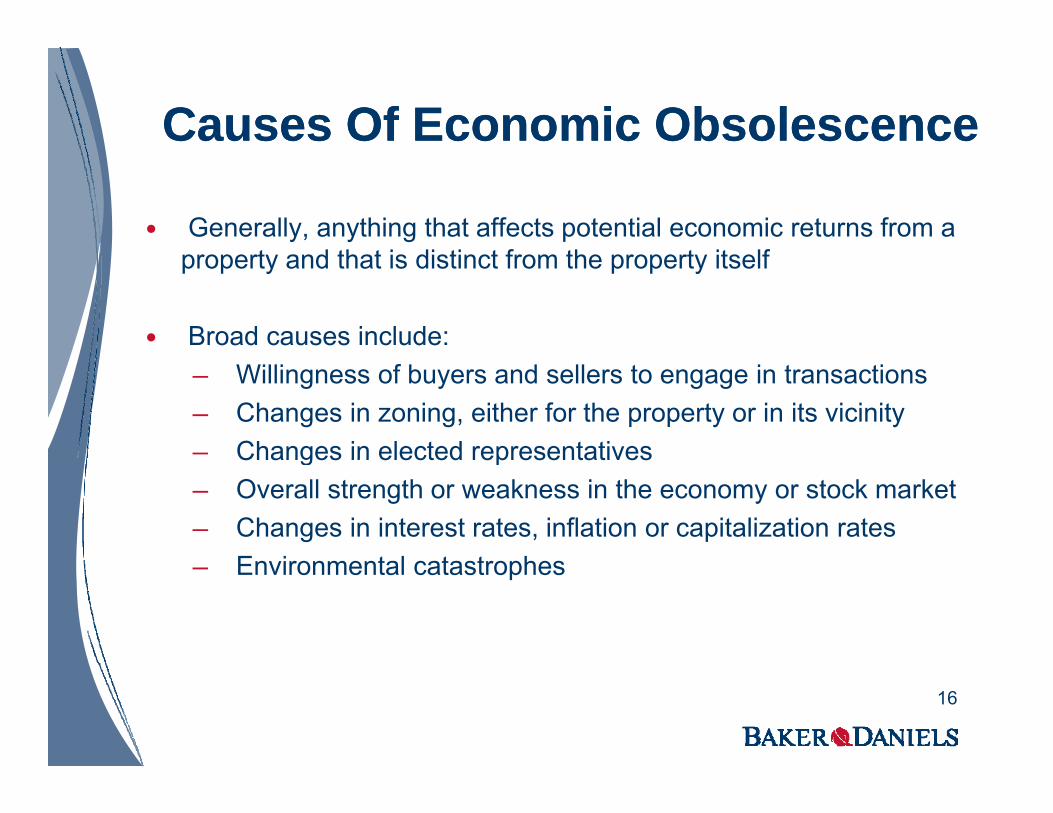

Causes Of Economic ObsolescenceCauses Of Economic Obsolescence

Generally, anything that affects potential economic returns from a t d th t i di ti t f th t it lfproperty and that is distinct from the property itself

Broad causes include:─ Willingness of buyers and sellers to engage in transactions─ Changes in zoning, either for the property or in its vicinity─ Changes in elected representativesChanges in elected representatives─ Overall strength or weakness in the economy or stock market─ Changes in interest rates, inflation or capitalization rates

E i t l t t h─ Environmental catastrophes

16

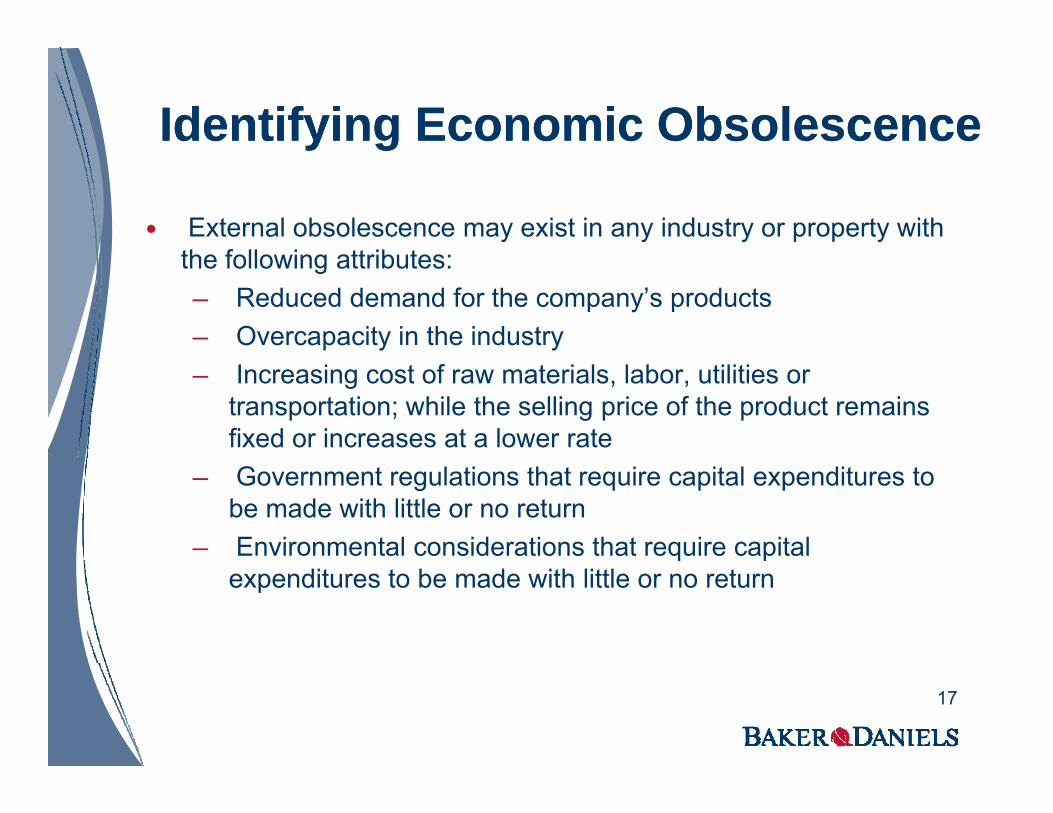

Identifying Economic ObsolescenceIdentifying Economic Obsolescencey gy g

External obsolescence may exist in any industry or property with th f ll i tt ib tthe following attributes:─ Reduced demand for the company’s products─ Overcapacity in the industry─ Increasing cost of raw materials, labor, utilities or

transportation; while the selling price of the product remains fixed or increases at a lower rate

─ Government regulations that require capital expenditures to be made with little or no return

─ Environmental considerations that require capital q pexpenditures to be made with little or no return

17

Identifying Economic Obsolescence (Cont.)Identifying Economic Obsolescence (Cont.)y g ( )y g ( )

External obsolescence may exist in any industry or property with the following attributes:─ Downturns in sales or earnings relative to prior periods─ Inability to control product pricing─ Margin compression due to a contractual agreement or

unfavorable economic conditions─ Increased competition from lower-cost or foreign

competitors

18

QUANTIFYING ECONOMIC Alfred King, Marshall & Stevens

QUANTIFYING ECONOMIC OBSOLESCENCE

Quantifying Economic Obsolescence

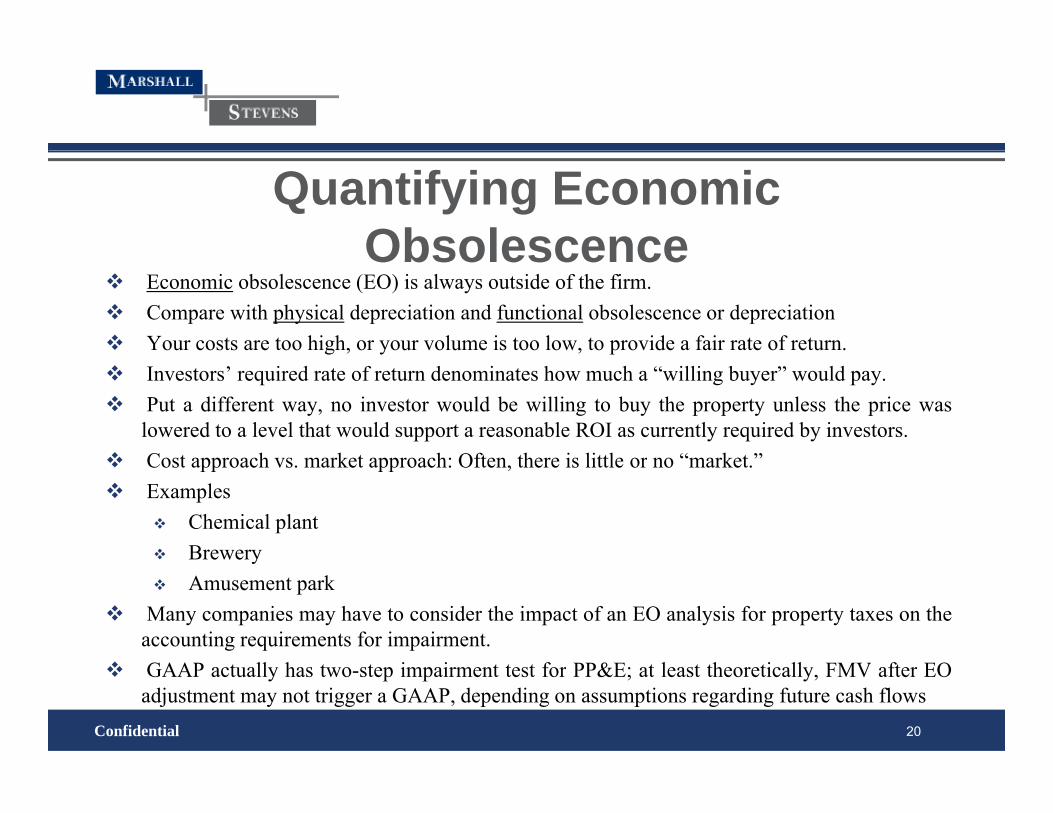

Economic obsolescence (EO) is always outside of the firm. Compare with physical depreciation and functional obsolescence or depreciation Your costs are too high, or your volume is too low, to provide a fair rate of return.

Obsolescence

Investors’ required rate of return denominates how much a “willing buyer” would pay. Put a different way, no investor would be willing to buy the property unless the price was

lowered to a level that would support a reasonable ROI as currently required by investors. Cost approach vs market approach: Often there is little or no “market ” Cost approach vs. market approach: Often, there is little or no “market.” Examples

Chemical plant Breweryy Amusement park

Many companies may have to consider the impact of an EO analysis for property taxes on theaccounting requirements for impairment.

GAAP ll h i i f PP&E l h i ll FMV f EO

Confidential

GAAP actually has two-step impairment test for PP&E; at least theoretically, FMV after EOadjustment may not trigger a GAAP, depending on assumptions regarding future cash flows

20

EO is used only in the cost approach.EO Is “Outside” Of The Firm

EO is used only in the cost approach. Depreciated cost is replacement cost new (RCN) less depreciation from all

causes: Physical depreciation Physical depreciation Functional depreciation Economic obsolescence

“EO has been defined as the loss in value or usefulness of a propertycaused by factors external to the asset. These factors include increasedcost of raw materials, labor or utilities; reduced demand for the

d t i d titi i t l th l tiproduct; increased competition; environmental or other regulations orother regulations; or similar factors.” [ASA - Valuing Machinery &Equipment]

Confidential 21

EO Can Change From Year To Year

B thi i t l t th fi titi d i diti Because this is external to the firm, competition and economic conditions can improve or deteriorate.

Therefore, either the taxpayer or the assessing authority may ask for an update.

Confidential 22

Appraisers Determine Fair Market Value While Assessors Determine Depreciated

Cost Tax assessors work with cost, not FMV. But, the basis of ad valorem is supposed to be FMV. Companies, however, initially report only the “COST” of new additions on

the assumption that initial cost = FMV at the time.p Assessors each subsequent year then “adjust” reported costs from prior

years with depreciation factors. The resultant depreciated cost purports to approximate FMV The resultant depreciated cost purports to approximate FMV. But, if external factors affect the “economics” of the taxpayer’s business,

no depreciation factor can pick this up. Therefore the initial burden is on the taxpayer to prove FMV

Confidential

Therefore, the initial burden is on the taxpayer to prove FMV.

23

FMV Usually Determined By Income Approach And Required Rate Of Return

Must determine projected income anticipated from the asset(s) in question

Reasonable projections of sales and expenses are necessary to ensure that p j p ytaxpayer is not “putting his thumb on the scale.”

If the discount rate used in the present value calculation is that which a If the discount rate used in the present value calculation is that which a third-party investor would use, and the net present value is below the assessor’s depreciated cost, then the case for an EO impairment charge is extremely strong.y g

The discount rate must be supported, usually based on a weighted average cost of capital (WACC)

Confidential

cost of capital (WACC).

24

Example: Chemical Plant Fortune 500 company had a chemical plant that was successful Fortune 500 company had a chemical plant that was successful. Used natural gas as the raw material input Jamaica had a surplus of natural gas that it could not export, and set up its

d ti f ilitown production facility. Jamaica charged its plant $1.00 mcf, while our client was paying upwards

of $4.00. Even adding transportation cost, Jamaican product was priced to customers

at a substantially lower price than client could. We modeled the plant with the competitive selling price that the client had

to meet.

Confidential 25

Example: Chemical Plant (Cont.) Determined the ROI that an outside investor would require say 14% Determined the ROI that an outside investor would require – say, 14%

Determined FMV of plant with projected cash flows, discounted at 14%

That was the true FMV of the plant at that time.

Complications: Largest employer in county Impairment charge on financial statements Impairment charge on financial statements

Result: Negotiated settlement

Confidential 26

GAAP Requirements For PP&E Impairment (ASC 360)

Major differences between GAAP and IFRS, for impairment of PP&E

GAAP has a two-step process.

Step One requires a projection of future net cash flows (including any Step One requires a projection of future net cash flows (including anyrequired capex) [chemical example].

If undiscounted future cash flows are greater than book value or carrying If undiscounted future cash flows are greater than book value or carryingvalue, then you stop.

B d fi iti th i i i t di t th GAAP l

Confidential

By definition, there is no impairment according to the GAAP rules.

27

Future Cash Flows Are LESS Than Book Value If the undiscounted cash flows add up to less than carrying value (book value) then you go to If the undiscounted cash flows add up to less than carrying value (book value), then you go to

Step TWO. In Step Two, you then determine the fair value (FV) of the PP&E, based on what the asset

group could be sold for, either in-use or in-exchange. Th diff b h FV d h i l i h f h i i The difference between the FV and the carrying value is the amount of the impairment

charge, as the FV now becomes the new book value. A question often arises as to whether the future cash flows used in the Step One test must be

used for determination of FV. Answer is that FV definition uses an exit value (what some other investor would pay), while

the cash flows in the Step One test are the expected results for the existing asset owner. Therefore, someone else’s cash flows may differ from yours, and you are allowed to use the

two different assumptionstwo different assumptions. Warning: Be prepared to defend major differences, because this is an area that auditors will

scrutinize closely.

Confidential 28

Example: Brewery

The brewery is a process facility.

I t t d ith ifi d i it Integrated with a specific design capacity

Cannot increase capacity, and hard to run at less than capacity

If you have a 25,000 bbl plant, you can determine that the cost per barrel is $x.xx.

If you have a 50,000 bbl plant, the unit cost per barrel will be 65% to 75% of the smaller plant.

Confidential 29

Example: Brewery (Cont.) Since selling prices of beer are highly competitive owner of smaller plant Since selling prices of beer are highly competitive, owner of smaller plant

must sell at a price determined by the (lower) cost of its larger competitor.

A i j t f t lli i d t t f th ll l t Again, project future selling prices, compared to costs of the smaller plant.

Discount at required rate of return

The result is the actual FMV of plant that an outside investor would pay.

Depreciated original cost is now irrelevant, because it will be above the true FMV.

Confidential 30

Example: Amusement Park Roller coaster rides are very expensive but without the addition of “new” Roller coaster rides are very expensive, but without the addition of new

rides periodically, attendance sags.

S h i f k lit ll “ i ” f k t th Some chains of parks literally move a “winner” from one park to another.

This amusement park has high fixed costs and relatively high capital expenditures.

From the assessor’s records, the depreciated cost of the assets was high.p g

Attendance at the park, in a medium-size city that was not a tourist destination, was insufficient to provide park owners (privately held) with a

Confidential

destination, was insufficient to provide park owners (privately held) with a satisfactory ROI.

31

Summary And Conclusions

Assessors use cost data – usually original cost less depreciation based on t i dcost indexes.

As long as there is little technological change, and no diminution if FMV, then it is hard to challenge assessor.

Indexes cannot handle technological change. Indexes can not handle reduced cash flow. In either situation, it is necessary for an appraiser to develop the true fair y pp p

market value. That should support an EO appeal.

Confidential 32

This Can Be Profitable Work For Appraisers

Confidential

C. Stephen Davis, Cahill Davis & O’Neall

APPROACHES TO APPEALS

C. Stephen Davis, Cahill Davis & ONeallScott Tyler, Crowe Horwath

AND LITIGATION

Strafford Publications WebinarStrafford Publications WebinarEconomic Obsolescence in Property ValuationEconomic Obsolescence in Property Valuation

A 18 2011A 18 2011Aug. 18, 2011Aug. 18, 2011

Economic Obsolescence In Property Economic Obsolescence In Property Val ationVal ationValuation:Valuation:

Appeals And LitigationAppeals And Litigation

C. Stephen DavisCahill, Davis & O’Neall, LLP

Los Angeles CaliforniaLos Angeles, Californiawww.cahilldavis.com | [email protected]

35

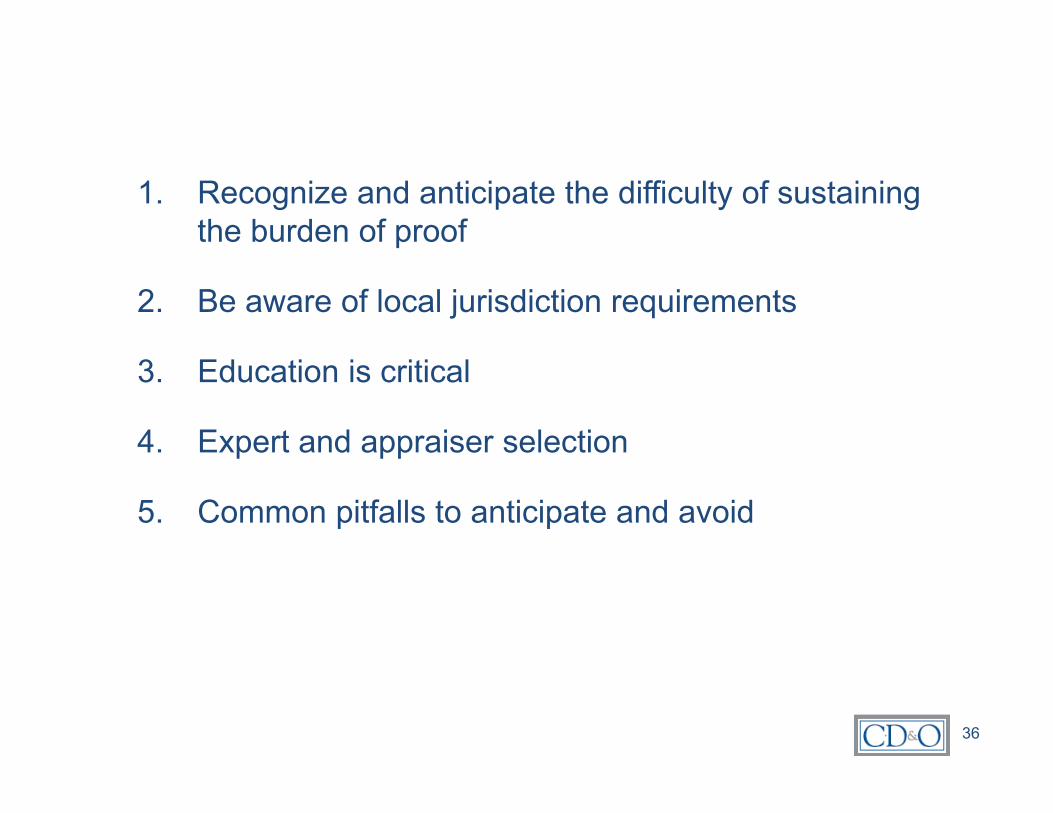

1. Recognize and anticipate the difficulty of sustaining the burden of proof

2. Be aware of local jurisdiction requirements

3. Education is critical

4. Expert and appraiser selection p pp

5. Common pitfalls to anticipate and avoid

3636

1. Recognize And Anticipate DifficultyOf Sustaining Burden Of Proof

• Assessors and AABs are skeptical if not outright hostile to EO adjustments.

Of Sustaining Burden Of Proof

▪ Not familiar with M&E appraisal

▪ Often large % adjustment

I tilit dj t t t i ll t t d b l▪ Inutility adjustments are typically not supported by sales or income data.

▪ The adjustment can be superficially counter-intuitive; the facility may still be operating, perhaps even profitably; perhaps new or recently expanded; and, duration of inutility can be uncertain.

• Burden of proof is not technically different, but burden of persuasion is greater as a practical matter. Do not underestimate the degree of difficulty associated with these cases.

3737

2. Be Aware Of Local Jurisdiction Requirements

• Example: If in California, cite to SBE Rules 2 (value in h ) d 6( ) ( d i i f b lexchange) and 6(e) (mandatory recognition of obsolescence

in the form of over-improvement), the new Guidelines for Substantiating Additional Obsolescence, and Assessors’ Handbook 504 (assessment of fixtures)Handbook 504 (assessment of fixtures)

• Be cognizant of the definition of value prevailing in your j i di ti E if th l t j t l t d d i f lljurisdiction. Even if the plant was just completed and is fully utilized, similar facilities may be selling at steep discounts after long exposure. Value in exchange is very different than value in use under such circumstancesvalue in use, under such circumstances.

3838

3. Education Is Critical• Do not assume the AAB is familiar with personal

property/M&E appraisal concepts.p p y pp p

• Develop the theory/rationale underlying economic obsolescence. Explain why an EO adjustment is fair, reasonable and consistent with the expectations of a reasonable buyer.

E l i th t d ti hi t f th f ilit L• Explain the nature and operating history of the facility. Lay a strong foundation of business reasons explaining “why” a prospective buyer of the subject would discount a cost indicator to determine a purchase priceindicator to determine a purchase price.

3939

4. Expert And Appraiser Selection• All of the usual criteria (testimony experience, qualifications,

familiarity with industry, ethical) apply, but the main point is that the mere opinion of an expert will not usually be sufficient (unless, sadly, it is assessor's expert!). An opinion is only as good as the facts on which it is based. Let the facts talk more than your expert.

• Three or even four witnesses may be required: the plant manager for operating history and current operating conditions, an appraiser to explain the theory, perhaps an industrial economist or the like to review market conditions if such data exist, and an appraiser to present an opinion of value. These categories can be consolidated for consideration in part by a single witness, in some cases.

• Be alert to the necessity of presenting a rebuttal case.

4040

5. Common Pitfalls To Anticipate And Avoida. Evidence of actual operating history should be sufficient

to show inadequate demand relative to production capacity 1 but some assessors contend that other orcapacity,1 but some assessors contend that other or different evidence of market conditions is required. Consider offering evidence of industry press, stock analyst reports reports to shareholders transcripts of publicreports, reports to shareholders, transcripts of public telephone conferences discussing acquisitions, facility sales data and/or government statistics to explain or illustrate market conditions.

1 See Spletter Kathy G “Appraising Property with Declining Utility ”1 See Spletter, Kathy G., Appraising Property with Declining Utility, IPT Property Tax Symposium, Fall 2010, p.6.

4141

5. Common Pitfalls To Anticipate And Avoid (Cont.)

b. Recent construction does not disprove EO.*

c. Continued operation does not disprove EO.**

d. Continued profitability does not disprove EO.***

e. Improved utilization does not disprove EO.

f A FAS 144 i i t i t diti f EOf. An FAS 144 impairment is not a condition for EO.

g. An overall inutility adjustment is typical, but if only some production lines are unaffected by excess capacity, consider limiting the adjustment to just those components that are overbuilt.

h. EO is accounted for by standard depreciation tablesh. EO is accounted for by standard depreciation tables (“normal depreciation”).

* SBE Guidelines p 20

42

SBE Guidelines, p. 20** SBE Guidelines, p.9*** SBE Guidelines, p.9 42

The Unique Alternative to the Big Four®

I. Basic formula for winning

II Specifics on building your caseII. Specifics on building your case

III. Common jurisdictional rebuttal points

© 2010 Crowe Horwath LLP 43Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

Basic Formula For WinningA. Approach basics

1 B d t k th1. Be prepared to know the processa. Informal negotiation

• A settlement here is possible, if structured properly.• Success at this stage depends on the capacity of the jurisdiction toSuccess at this stage depends on the capacity of the jurisdiction to

understand the nuances of obsolescence.• Everything here should be done with the thought that the case will

possibly go to formal appeal or beyond.b F l lb. Formal appeal

• Winning at the appeal level can vary by state/jurisdiction.• The likelihood of success depends again on the education level of the

jurisdiction relative to obsolescence, and the ability to formulate their j , yown opinion and analysis.

c. Litigate• Know beforehand if prior appeal testimony will be used within this forum

© 2010 Crowe Horwath LLP 44Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

Basic Formula For Winning (Cont.)B. Strategy for winning informally

1 K th b l t d d f th t j i di ti1. Know the obsolescence standards for that jurisdiction2. Identify that there is economic obsolescence3. Roughly quantify the amount of economic obsolescence4. Have a preliminary discussion with the jurisdictiony j

a. Object isn’t to win anything at this stageb. Object is to lay the groundwork

• Prepare the framework with working with the assessor• Identify the assessor’s educational level and position on the subject• Identify the assessor s educational level and position on the subject• Identify what the assessor believes is a viable approach

4. Build your case based upon the information you collected abovea. Making it conform as closely to what the jurisdiction will accept is importantb. The analysis must be tight – ensure all data has been consideredc. Don’t overinflate figures as a negotiation strategy – present the “right” answer

5. Present your case to the jurisdictiona Know your negotiation limits beforehand

© 2010 Crowe Horwath LLP 45Audit | Tax | Advisory | Risk | Performance

a. Know your negotiation limits beforehand

The Unique Alternative to the Big Four®

Specifics On Building Your CaseA. The reportp

1. Executive summary2. Definition of obsolescence

a. Jurisdiction’s definitionb Generally accepted appraisal definitionsb. Generally accepted appraisal definitions

3. Overview of taxpayer’s circumstancesa. Description of facts that affect the taxpayer in this situationb. Identify the source of the economic obsolescence

4. Quantify the obsolescencea. Preferably use as many different ways to quantify this as possible (minimum of 3

different methods) – 5 to 7 variations is usually optimalb. Use metrics from both the taxpayer AND the taxpayer’s industryb Use e cs o bo e a paye e a paye s dus yc. Use metrics that span multiple years (determine a “business as usual” period)d. Service companies that don’t have typical manufacturing production metrics to

benchmark may need to dive into other data sources (balance sheet, P&L, etc.)5 Summarize your findings

© 2010 Crowe Horwath LLP 46Audit | Tax | Advisory | Risk | Performance

5. Summarize your findings

The Unique Alternative to the Big Four®

Specifics On Building Your Case (Cont.)B. The evidence

1. Taxpayer-specific evidencea. Balance sheetb. P&L statementsc. Site toursd. Written or in-person documentation by company personnely ye. 10-K/annual reportf. Engineering reportsg. Financial budgets/projectionsh. Production statementsh. Production statementsi. Production capacitiesj. Employment recordsk. Newspaper/magazine articles on the company or industry

2 Industry-specific evidence2. Industry-specific evidencea. Any public information for the same information gathered for the taxpayer relative to the

taxpayer’s main competitorsb. Industry periodicals/reportsc Census Bureau or other U S government reports

© 2010 Crowe Horwath LLP 47Audit | Tax | Advisory | Risk | Performance

c. Census Bureau or other U.S. government reportsd. Investment survey reports (e.g., Valueline)

The Unique Alternative to the Big Four®

CCommon Jurisdiction Rebuttal Points

A. The property is brand new, so there is no way there could be obsolescence.

B The company’s revenue has been increasing so there is no basis forB. The company s revenue has been increasing, so there is no basis for obsolescence.

C. The equipment is being utilized, so there is no basis for obsolescence.D Ob l i t h d ill b t dD. Obsolescence is a temporary phenomenon and will be corrected over

time, so there should not be any adjustment.E. The obsolescence is not unique to the taxpayer’s property and is

i d t id th it d t lif f b lindustry-wide; thus, it does not qualify for obsolescence.F. Economic obsolescence is already captured within the jurisdiction’s

depreciation tables and to capture it again would be “double-dipping.”

© 2010 Crowe Horwath LLP 48Audit | Tax | Advisory | Risk | Performance