Embed Size (px)

Citation preview

ElectionWatch

ab

Perspectives on the 2014 US midterm elections from UBS CIO Wealth Management Research

A clear winner?

27 October 2014

Page

01 Introduction

03 Political dynamics

06 Interview with John Savercool

09 Policy issues for the 114th Congress

1 2 Market implications

15 Disclaimer

ElectionWatch

Publication details

PublisherUBS Financial Services Inc. 1285 avenue of the americas, 20th Floor New York, NY 10019

This report has been prepared by UBS Financial Services Inc. (“UBS FS”). Please see important disclaimer and disclosures at the end of the document.

This report was published on 27 October 2014.

Editor in ChiefTom McLoughlin

Authors (in alphabetical order)Jerry BrimeyerNicole DeckerMichael DionLeslie FalconioKatherine KlingensmithDavid LefkowitzJames RhodesDean UngarJonathan Woloshin

Research AssistantJoseph Vittoria

Desktop Publishing george StilabowerCognizant Group – Basavaraj Gudihal, Srinivas addugula and Virender Negi

Project ManagementPaul LeemingDrew gilmorealyssa Vu

UBS CIO Wealth Management Research gratefully acknowledges the guidance and assistance provided by John Savercool and his colleagues in the UBS US Office of Public Policy in the preparation of this report.

electionWatch 1

Popular interest in midterm elections pales in comparison to presidential contests. Based on a recent survey by the Pew Research Center, this year appears no different. Only 15% of americans are following campaign developments in the news very closely, a lower percentage than was re-corded in 2010 (25%) and 2006 (21%).1 Conversely, almost two-thirds of the respondents are either ignoring the bal-lot coverage or not paying much attention to it. We suspect that other events around the world have contributed to the higher degree of apathy regarding the midterm elections. geopolitical uncertainty has increased with the Russian an-nexation of Crimea and the disintegration of Iraq as a uni-fied country. Media coverage of these developments, along with the outbreak of ebola, has displaced the election from the top of the news cycle.

We do expect interest in the midterm elections to increase in this, the final week of the campaign. Many Senate races are highly competitive and will pivot on the ability of the Demo-cratic candidate to stake out a political position independent of President Barack Obama. election night will be a nail-biting

Introduction

Thomas McLoughlin

affair for the supporters of Senate candidates in a dozen dif-ferent states. The UBS US Office of Public Policy believes the Republicans will eke out enough victories to assume major-ity control of the Senate, something they failed to do two years ago. President Obama’s approval ratings have declined and Democratic candidates in conservative-leaning states are struggling to distance themselves from the chief executive.

If our base case is correct, the net result will still be a divided government and a political stalemate. While Republicans will set the legislative agenda, the chamber’s Democrats will hold enough seats to impede the passage of legislation to which its members strenuously object. Some legislation, such as an in-crease in the debt ceiling and a reauthorization of the highway bill, will be enacted after extended debate. Other initiatives,

The UBS US Office of Public Policy expects the GOP to assume majority control of the US Senate and to increase the size of their majority in the House of Representatives. But the net result remains a divided government.

ElectionWatch

Republicans are trying to nationalize the Senate races while Democrats are trying to keep them focused on more local concerns.– Erika Franklin Fowler, Wesleyan Media Project

Fig. 1: Congressional seats by party affiliation

165

8 15 18 5 16

208

Republican Toss Up

Leans Republican

Likely Republican

Democrat

Likely Democrat

Leans Democrat

199 233

Source: RealClearPolitics, UBS CIO WMR, as of 20 October 2014

Republican Toss Up

Leans Republican

Likely Republican

Democrat

Likely Democrat

Leans Democrat

38

6 1 10 1 2

42

55 45

Fig. 1: Congressional seats by party afffiliation

188

18

229

House seats projected (outer crescent) and current (inside crescent) Senate seats projected (outer crescent) and current (inside crescent)

House seats projected and current Senate seats projected and current

Republican

UndecidedDemocrat

Republican

UndecidedDemocrat

199 233

Source: Real Clear Politics, UBS CIO WMR, as of 20 October 2014

45

10

45

55 45

ProjectedProjected

Current Current

2 electionWatch

such as a repeal of the Affordable Care Act and a stab at com-prehensive tax reform, have little chance of enactment.

Regardless of the likelihood of passage, many legislative initia-tives will be aired out on the floor by members of Congress eager to motivate their political base. Committee hearings and floor debates will serve as a prelude to the presidential campaign that will begin in earnest in 2015. We expect the Obama administration to acknowledge its limited influence over the GOP majorities in Congress next year and instead to focus on administrative actions. The process by which federal rules are made can be long and tedious, so expect the execu-tive departments to get an early start after the election. The new committee chairs will respond with hearings on the rela-tive merits of various administration actions, all of which will be used as fodder for both parties in the run-up to the presi-dential election.

In the countdown to this year’s election, both political parties are expected to use social media to promote their platforms among likely voters. The importance of social networking sites became apparent in the wake of the 2008 presidential elec-tion when the Obama campaign skillfully used the new medi-um to increase the turnout among young voters. His decisive victory altered the traditional approach to both presidential and congressional campaigns. Today, both parties employ net-working to communicate with supporters and to sway inde-pendent voters. The midterms are just the opening act of the main event in 2016.

Introduction

Social media’s role in elections

Jesse Unruh, former Speaker of the California assembly and State Treasurer, was reported to have said that money was the “mother’s milk of politics.” Most candidates in highly contested elections would likely agree. Newspaper adver-tisements and radio broadcasts are no longer quite as influ-ential as they once were and television commercials are notoriously expensive. Political campaigns often involve ef-forts to capture the attention of nonaligned prospective vot-ers. and the cost of doing so can be staggering. according to the Brookings Institution, successful candidates for the US Senate spent an average of USD 10.4 million in 2012 on their statewide campaigns.1

The rise of social networking has begun to transform politi-cal campaigns by increasing the ability of candidates to reach prospective voters at a fraction of the cost associated with traditional advertisement through mass media channels. Based on recent surveys, the Pew Research Center has con-cluded that half of americans now use social networking sites. and contrary to popular belief, the age of users varies considerably. according to Pew’s data, more than one-third of individuals 65 years or older are using social networking sites to maintain relationships with friends and relatives.

Candidates have gotten the message. After the watershed presidential election in 2008, when the Obama campaign skillfully leveraged the Internet to generate voter enthusiasm, candidates in both parties have increasingly turned to social media to raise their profiles and to spread their message. according to one recent survey, 30% of registered voters were encouraged to vote for either former governor Mitt Romney or President Obama via posts on social media sites such as Facebook and Twitter.2

Social media offers another important advantage for the cost-conscious campaign. as an interactive forum for ideas and opinions, social media allows the candidate to engage in a dialogue with supporters and thereby determine which is-sues motivate them the most. The ability to gauge voter opinions based on an individual’s gender, race and ethnicity is a veritable gold mine for campaigns seeking to maximize voter turnout or for candidates to distinguish themselves from their opponent. as smart-phones become ubiquitous among the voting public, the speed with which the online di-alogue occurs will only increase.

electionWatch 3

Midterm elections generate less enthusiasm among american voters than do elections in which we also choose a president. While this shouldn’t be too surprising given the degree of influ-ence a chief executive wields and the amount of media atten-tion devoted to presidential elections, the disparity in voter turnout is stark. While approximately 133 million people partici-pated in the presidential elections in 2008, only 90 million went to the polls in the Congressional elections two years later.1

The decline in voter participation in the 2010 midterm elec-tion was not unusual but will have a material impact on the outcome this year – if the pattern repeats itself. Younger and less affluent voters, a core constituency of the Democratic Party, are more likely to skip the midterm election than are older voters. The latter group has reliably favored Republican candidates for some time now, which explains why Democrats are so focused on convincing registered voters to show up at the polls this November.

Both political parties, and the organizations that support their candidates, are opening the checkbook to pay for advertise-ments. While social networking is increasingly important to

both parties, neither has abandoned more established media channels. According to the Wesleyan Media Project, US Sen-ate candidates have spent USD 337 million for traditional air-time in the run-up to this election. By election Day, the two sides will have squared off and spent more than USD 1 billion in Senate, House, and gubernotatorial races.2

The approach taken by the two political parties in their re-spective advertisements is altogether not too surprising. Republicans are delivering a more uniform message focused on the shortcomings of the Affordable Care Act and the slow pace of economic growth. Democrats are taking a more tar-geted approach by emphasizing local issues important to vot-ers in different parts of the country. Education, Medicare, and Social Security are among the most prominent.3 The commu-nication strategies employed by Democrats are logical given the vulnerable position occupied by members of any presi-dent’s political party in off-year elections.

The six-year itchMidterm elections pose a particular challenge for the presi-dential incumbent’s political party. Opponents often cite

Political dynamics

Thomas McLoughlin

We expect lower voter turnout in a midyear election that favors the GOP. However, increasing polarization means that even with one party controlling both chambers, major legislation is still unlikely.

ElectionWatch

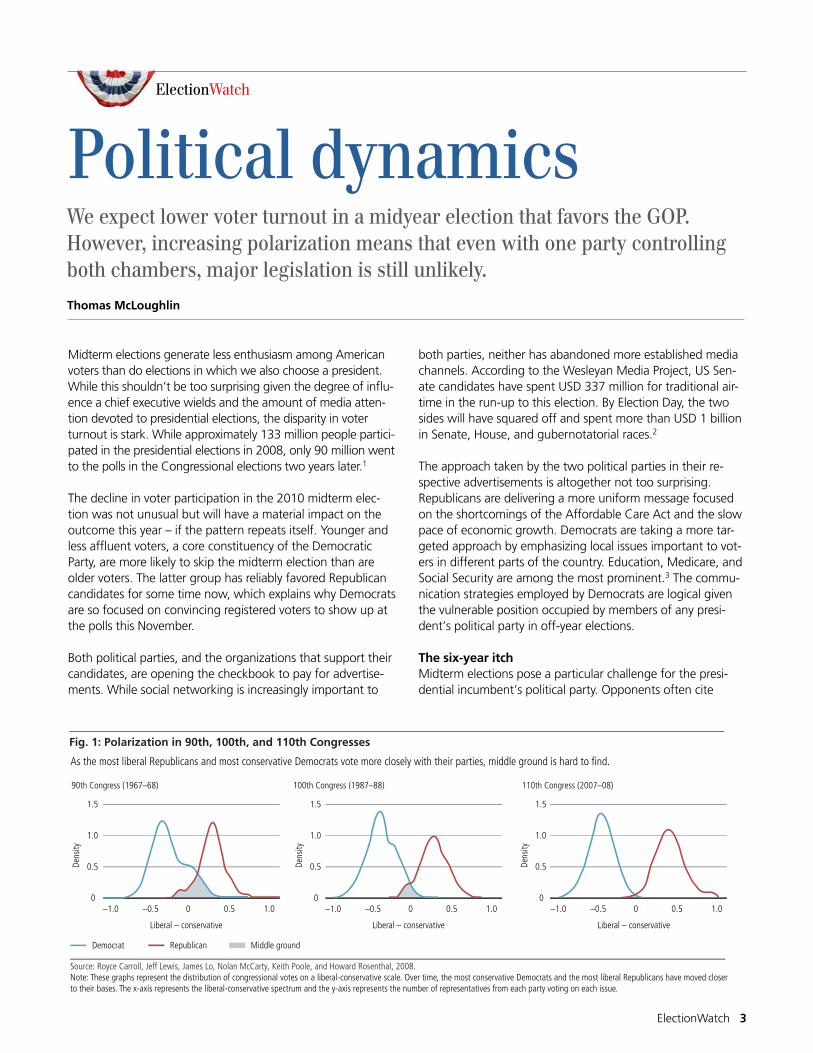

Fig. 1: Polarization in 90th, 100th, and 110th Congresses

–1.0 –0.5 0 0.5 1.00

0.5

1.0

1.5

90th Congress (1967–68)

Liberal – conservative

–1.0 –0.5 0 0.5 1.0

Liberal – conservative

–1.0 –0.5 0 0.5 1.0

Liberal – conservative

Dens

ity

0

0.5

1.0

1.5

Dens

ity

0

0.5

1.0

1.5

Dens

ity

100th Congress (1987–88) 110th Congress (2007–08)

RepublicanDemocrat

Source: Royce Carroll, Jeff Lewis, James Lo, Nolan McCarty, Keith Poole, and Howard Rosenthal, 2008.Note: These graphs represent the distribution of congressional votes on a liberal-conservative scale. Over time, the most conservative Democrats and the most liberal Republicans have moved closer to their bases. The x-axis represents the liberal-conservative spectrum and the y-axis represents the number of representatives from each party voting on each issue.

As the most liberal Republicans and most conservative Democrats vote more closely with their parties, middle ground is hard to find.

Middle ground

4 electionWatch

have contributed to the rejection of GOP challengers in 1998. Devotion to the flag and support for the nation’s chief execu-tive in the wake of 9/11 probably were instrumental in avoid-ing a loss of House seats in 2002.

according to the political analyst Charlie Cook, the pattern is replicated in the Senate. Since the direct election of senators was made possible through a constitutional amendment in 1913, the president’s party has often lost seats in the Senate following midterm campaigns. The record is only slightly

policy errors and adverse economic news as reasons for new representation in Washington. Congressional candidates from the president’s own party – this year it will be the Democrats – are obliged to either defend the actions of the administra-tion or to distance themselves from its actions. The degree to which this maxim holds true is remarkable. The president’s political party has lost seats in the House of Representatives in every midterm election for the past 150 years except for those held in 1934, 1998, and 2002.4 Voter fatigue over the im-peachment of former President Bill Clinton may

Demographic trends

French sociologist auguste Comte is widely credited with the phrase “demography is destiny.” In terms of electoral poli-tics, we believe the term aptly describes the changes under way in the United States. Three broad trends are likely to have a profound impact on Congressional voting patterns and composition.

First, the population is aging. The US Census Bureau esti-mates that the nation’s population of senior citizens, defined as those 65 years or older, will reach 83.7 million by the year 2050, double the number in 2012. Older americans vote in larger numbers than do younger citizens. The voting rate of senior citizens increased from 66.3% in 1964 to 69.7% in 2012 while voting participation among 25- 44-year-olds dropped. Seniors are highly attuned to any proposed chang-es in the management of the nation’s Medicare and Social Security programs. While members of Congress may bemoan the growth in entitlement spending, federal funding for these programs is only likely to grow.

Second, America is moving again. After a temporary lull in the rate of internal migration, the US population is on the move. economic recession and lower housing values discour-aged many families from relocating. Jobs were not as plenti-ful and mortgages often exceeded the market value of homes. as the economic recovery has gained traction, the unemployment rate has fallen and housing values have im-proved. according to the National association of Realtors, the median existing single-family home price in the second quarter was USD 212,400, 4.4% higher than the second quarter of 2013. The median price during the first quarter of 2014 rose 8.3% from a year earlier.1 The growth in home prices has already begun to moderate but the current market is still far better than the one prevalent in most communities as recently as three years ago.

The destination for those choosing to relocate is often to points south and west. New York State lost an estimated 136,000 people in 2012, according to the Census Bureau, while Massachusetts lost more than 15,000. The net result is that america’s population is moving to more moderate cli-mates. according to the Census Bureau, cities in the south-ern and western states dominated the list of the 15 fastest-growing municipalities. Seven of those 15 cities are located in Texas, whose favorable tax structure and employ-ment opportunities are encouraging more internal migration from other parts of the country.

Third, the United States is becoming more diverse. according to the State Department, the US minority popula-tion increased by 30% in the decade preceding 2010. Over the same period of time, the non-Hispanic white population increased by just one percent. Hispanic Americans are the single largest minority group in the country, embracing 17% of the population. african americans and asian americans comprise 12% and 5% of the population, respectively.2 Thus far, Hispanic voter participation does not yet mimic popula-tion growth. The population is younger and therefore has a higher percentage of individuals ineligible to vote. But that is likely to change over time. The State Department cites stud-ies which suggest that Hispanic americans will cast more bal-lots in national elections than will african americans by 2020. The Hispanic voting bloc also is not monolithic and runs the gamut from liberal to conservative. However, in some states such as Colorado, their support can be a crucial component in a campaign.

Political dynamics

electionWatch 5

better than in the House. In addition to the three elections de-scribed above, Democrats retained their advantage in 1962 and the gOP did so in 1970.5

The challenge of retaining seats in Congress when the presi-dent hails from the majority party is even greater in the second term of a presidency. Political theorist and author Kevin Phillips coined the phrase “six-year itch” to describe voters’ enthusiasm for change as the curtain begins to de-scend on any president’s final term in office. Republicans lost eight seats in the Senate in 1986 during President Ronald Reagan’s second term and 12 seats in 1958 at the end of the eisenhower presidency.6 To paraphrase Mark Twain, history doesn’t repeat itself but it does rhyme.

A puzzling paradoxA paradox is loosely defined as a self-contradictory statement that appears absurd on the surface but holds some truth. For an example, look no further than the US political arena, where partisan divisions have increased as the number of political in-dependents has grown. More than ever before, individuals of voting age are defining themselves as political independents and express a desire for political compromise. and yet, the political atmosphere in Washington and in state capitals has become highly partisan. each party accuses the other of intran-sigence and a reluctance to bargain in good faith.

An increasing number of Americans have identified them-selves as independent of a political party. The Gallup organiza-tion reports that 42% of Americans identified themselves as political independents in 2013, the highest percentage ever recorded by the polling firm.7 The increase in nonaligned vot-ers has come at the expense of both the Republican and Democratic parties. Respondents identifying themselves as Democrats and Republicans fell to 31% and 25%, respective-ly. gallup also reported that the number of individuals claim-ing they were independent of a political party surged in the fourth quarter of 2013. The polling organization attributes the surge to controversy over government shutdowns and the troubled launch of Obamacare.8

One might reasonably expect that independent voters would reward candidates who exhibited a willingness to compro-mise with political opponents. and yet, the partisan antipathy around the country appears to run deeper than ever. We at-tribute the contradiction to two separate factors. First, inde-pendents usually “lean” in one direction or another. gallup’s results appear to confirm the notion that individuals who de-cline to state a party affiliation still tend to vote for one party

over another. among the roughly 40% of americans who claim to be independents, 16% tend to vote Democratic and an equivalent number usually vote for gOP candidates.9

Second, while a plurality of americans appear to have disen-gaged themselves from active politics, the “party faithful” have become more active than ever. Ideological conformity on both sides of the aisle is on the rise. The Pew Research Center reports that 38% of registered Democrats espouse consistent-ly liberal opinions while 33% of Republicans are consistent in their conservative views. These percentages appear to be at their historical peaks.10 So the net result is that while more and more americans are withdrawing from active politics, those who remain are more highly motivated than ever to support candidates who share their perspectives. and when those candidates are elected to office, they rely upon the party faithful for political support and may be more reluctant to reach across the aisle.

That is why comprehensive tax reform is such an uphill battle. While partisan bickering is a political constant in Washington, personal rancor is more difficult to overcome and makes it more difficult to strike compromises. And tax reform, more than almost any other issue, will require extensive bargaining and numerous concessions. Both parties already recognize the necessity of reforming a tax code that has grown unwieldy but Republicans are highly unlikely to countenance any in-crease in marginal tax rates. as John Savercool suggests on page 8, the gOP prefers that any legislation be revenue neu-tral. Democrats, meanwhile, are likely to resist reductions in entitlement spending and prefer that more revenue be made available for infrastructure investment.

Sooner or later, the need for some reform will drive both par-ties towards the ideological middle ground. and when that happens, we expect may tax shelters (or “tax expenditures” in Washington parlance) to come in for greater scrutiny. These line items are designed to encourage certain types of invest-ments by lowering one’s tax liability or sheltering income. Please refer to Fig. 3 on page 11 for a review of the top 15 largest tax expenditures. Tax reform remains a “big lift” as they say in DC, and the prospects of it happening before the 2016 election are slim according to our colleagues in the US Public Policy Office. The GOP will be defending more seats in the Senate in that presidential election year so the political dynamics already favor the Democrats two years from now. Much will depend on whom each party nominates at the top of the ticket.

Political dynamics

6 electionWatch

Tom McLoughlin: President Obama’s overall popularity rating has declined as the midterm election approaches. and yet, vot-ers’ opinion of Congress is even lower. To what extent will the President’s poll numbers influence the midterm elections? Or, to borrow Tip O’Neill’s famous phrase, “is all politics local”?

John Savercool: Most midterm elections will be determined by national influences so the President’s lower approval rating will indeed be a factor. This is certainly true of US Senate elec-tions, which are really the key contests this year.

There are a few exceptions, of course. But most of the impor-tant Senate races appear to be influenced largely by national events and whether voters think that the nation is on the right track when it comes to policymaking. Keep in mind that the President’s approval ratings are much lower in states with the most competitive Senate seats.

If you’ll forgive the pun, the elephant in the room is whether the gOP will win enough Senate seats to take control of both houses of Congress. earlier this year, you believed the odds were in Republicans’ favor. Do you still believe they are well positioned to assume majority control of the Senate?

Savercool: I do. I still believe the odds are in their favor. Having said that, this will be a very close election. There are probably six or seven seats that are too close to call and it’s still possible that Democrats could retain control of the Senate. But the re-ality is, Tom, that whoever or whichever party wins, they will have a very, very slight governing majority. It will be more of a mathematical majority than a governing majority.

It’s still quite important, of course, because whoever does win has the power to control the legislative agenda and decide which bills go to the floor for a vote. The majority, however slight, become the committee chairs and receive more media attention, allowing them to frame the debate. So you always want to be in the majority, however slight that advantage might be. But in this case, regardless of who wins, it will be a muted majority for the next two years.

and there’s another twist in this year’s election. as I under-stand it, there are two Senate races where the results may not be known on November 5.

Savercool: Yes, there are a few asterisks next to various races. The most important asterisk is probably the runoff dates; there are runoff dates in both Louisiana and Georgia. So we could see one runoff election in December and another in January. So it’s possible that we’re not going to know which party is in control of the Senate until after the start of the year and well after this year’s lame-duck session.

If there is a change of control of the Senate, you’ll get new committee chairs and perhaps a different direction in terms of legislative initiatives. But does the change in majority control herald an even more contentious relationship between the President Obama and the Congress? Does it change the tenor of the discussion in Washington?

Savercool: It does. The President will be placed in a position where he will have to work with Republicans and find com-mon ground in order to get anything done in Congress. It’s really not so difficult to talk to people and to identify common ground. But in the current era, members of Congress and the President are much more philosophical and less pragmatic. So whether they’re conservative or liberal, it is much harder to forge a compromise.

And the President will have a difficult time striking an agree-ment with a Republican Senate because the 2016 presidential election will be looming. Both parties will be seeking to con-trast their own positions with their opponents. So compro-mise will be difficult. Legislative gridlock, which we’ve seen over the last few years, is likely to continue in 2015 and 2016 but the cause will be different. Instead of a divided Congress, the House and Senate will be more united in opposition to the President’s policies.

Interview with John Savercool

In our ElectionWatch interview, Tom McLoughlin sits down with Head of the UBS US Office of Public Policy John Savercool to discuss election dynamics, the balance of power, and prospects for the post-election legislative agenda.

ElectionWatch

electionWatch 7

So if there’s anything getting done at all next year, is it more likely to be accomplished through administrative rule-making?

Savercool: Yes. I think most of the activity will revolve around executive branch rule-making, which is likely to escalate. To some degree, that’s because the president will want to cir-cumvent Congress. and in larger part, it’s because the President wants to leave behind a regulatory agenda that he thinks is good for the country. and to do so, he really needs to commence that rule-making soon because the bureaucrat-ic journey is often a long and tedious affair and needs to be finalized before his term of office ends in early 2017.

So you will see a very robust regulatory agenda. Most of the legislative battles that could be resolved will be kind of “small-ball” issues that don’t engender a lot of opposition.

But you’ll see a handful of issues that must be addressed due to a looming deadline. For in-stance, the debt ceiling has to be resolved some-time in the first or second quarter, the reauthorization of the Export-Import Bank is scheduled for June, and the highway bill has to be reauthorized in May. Those things will all be subject to legislative action – not because there’s a will between the President and House and Senate Republicans to solve them – but because there’s a deadline that requires an actual vote.

We’ve talked a lot about the Senate so let’s turn briefly to the House. The Republicans are expect-ed to retain control of the House of Representa-tives. Do you expect the gOP to pick up any seats and strengthen their majority during this midyear election?

Savercool: Yes, I do. But I think that the pickup will be very small, maybe five or six seats. Ten seats would be a high-water mark. I doubt the gOP will lose any seats and will certainly add to their majority. That should allow them to govern if their members are on the same page, which isn’t always the case.

Is the economy still the dominant issue in Congressional campaigns or has foreign policy dominated the discussions?

Savercool: I think the economy is still the issue for most peo-ple. Certainly, there are other issues now on the radar screen. But I think if you asked most americans, they still care about their own job security. That would still be number one. The economy is improving but at a personal level, they still don’t appear too optimistic. So I think there’s still a disconnect be-tween the recovery, as economists cite it and document it, and the reality in the street among people whose wages are not increasing and whose monthly bills are still a worry.

Has the Affordable Care Act diminished in importance as an election issue?

Savercool: I don’t think it’s really diminished among conserva-tive voters, particularly those who are the most likely to vote.

“Whichever party wins, it will be more of a mathematical majority than a governing majority.”

Interview

8 electionWatch

For them, it is the number one issue. and it will be the reason why they vote. But for most other voters, it no longer repre-sents the dominant issue.

Let’s turn to fiscal policy. How is the debate over corporate tax inversions playing out in Washington?

Savercool: Well, it’s playing out as most issues have over the last couple of years and it’s turned into a political contest. On the one hand, Democrats believe that corporations that choose to relocate lack economic patriotism and should pay what the government thinks is their fair share of taxes. Re-publicans believe that inversions pose a problem but want to use the energy surrounding the issue to reform the tax code.

Which leads us right into the prospects for comprehensive tax reform. Must we await the next presidential election to get any traction there?

Savercool: Well, I think that there will be some serious legisla-tors in Washington who really and earnestly want to push tax reform next year. and, by tax reform, I mean a fairly thorough revision of the tax code, which is a major feat. It only happens once every 30 years or so. There will be people on both the Republican and Democratic sides of the aisle who are capable of sitting down and trying to work something out. But politics will make it difficult.

I’m not optimistic that a tax reform measure will pass next year, or the following year, but I think there will be a lot of work done on both sides of the aisle from people who want, more than anything, to simplify the tax code, which I think is what most americans want. So you’ll see a lot of stops and starts next year, but I don’t think you’ll see anything pulled over the goal line.

Will a Republican majority in the Senate affect national energy policy?

Savercool: If Republicans have a majority in the Senate next year, energy policy will be a big area of focus. Republicans be-lieve that america should expand exports of crude oil and nat-ural gas, and would make this a big legislative priority almost immediately. Democrats historically have been more con-cerned about the impact of such policies on climate change.

What about immigration? Would a change in Senate leader-ship allow Congress to present or to pass any sort of sensitive immigration reform?

Savercool: No. I think it would make it harder. There is still a lack of unity among Republicans regarding what to do with the 11 million people already in the country illegally. Most of the other components of an immigration reform bill, such as how to restructure legal immigration practices and establish guest-worker programs, are all very manageable. The big issue is what to do with those who are here illegally now. Do we give them some kind of legal status and allow them to stay or should they be removed from the country? Those are big issues, and I think that Republicans will have a hard time reaching a consensus within their own caucus. You might see President Obama issue executive orders but I am skeptical that you’ll see any new legislation.

Last question. You mentioned the highway bill earlier in our conversation. The nation’s infrastructure is in desperate need of repair and replacement. are the Congressional elections likely to have any meaningful impact on capital spending on highways, airports, water or mass transit? Or must we await the next presidential election?

Savercool: I think this is one issue that could see some action next year. everyone in Washington, from the most liberal to the most conservative member, understands the need to put more money into our nation’s physical infrastructure. So that’s the good news. The bad news is there is no consensus on how you pay for it. We have typically paid for it through the federal gas tax. But Republicans are reluctant to increase the excise tax on gasoline and they don’t want to pay the political price for supporting a tax increase. That’s the primary hurdle right now.

Interview

“Legislative gridlock, which we’ve seen over the last few years, is likely to continue in 2015 and 2016.”

electionWatch 9

The list of policy issues awaiting resolution by the next Congress is long and complex. Political stalemates are likely to prevent the passage of groundbreaking legislation, but that won’t deter members from engaging in robust debate. We focus on five policy areas.

HealthcareVotes on the full repeal of the Affordable Care Act will likely take place in both chambers, passing in the House but getting sidetracked in the Senate. While conservatives in both houses will push for a full repeal of the act, more centrist legislators will likely see that as a fruitless exercise and instead target in-dividual provisions of the healthcare law. We expect the gOP majorities to push for the elimination of the medical device tax (2.3% excise tax on all sales of US medical devices) and an increase in the number of weekly hours worked to qualify for mandatory health insurance coverage.

The GOP is also likely to use its majority to attack the so-called “risk corridors,” where the federal government com-pensates health insurers, regardless of their failure to meet certain financial benchmarks in health plans offered by state health insurance exchanges. A Republican majority is also more likely to pass legislation imposing more restrictive rules for Medicare reimbursement. These changes would be incre-mentally negative for health insurers, as well as health service providers (hospitals and physicians). Congressionally mandat-ed budget cuts are expected to be relatively moderate over the coming year; we don’t foresee major negative implica-tions for healthcare stocks over this period.

EnergyWe believe a Republican majority in both houses of Congress would be modestly positive for the energy industry. a Republi-can-controlled House and Senate would increase the near-term likelihood that the Keystone pipeline is approved, as well as ac-celerate issuance of permits for construction of liquefied natural gas (LNg) export facilities, in our view. We also expect a more

robust debate over the merits of lifting the US crude oil export ban. Discussions regarding oil and gas exploration on federal land and offshore waters will increase but a bipartisan resolu-tion is unlikely. The Obama administration will likely retain sig-nificant influence over policy decisions regarding climate change, water quality, and alternative energy through federal rule-making.

Hydraulic fracturing, a controversial drilling technique that is hotly debated among environmentalists and energy industry supporters, is regulated primarily at the state level. The frack-ing debate has been a lively one in certain producing states, such as Pennsylvania and Colorado. environmentalists are call-ing for stricter regulations, and turnover among top officials in these two states could lead to greater regulatory oversight. In other states such as New York, policy and regulatory deci-sions on development of oil and gas reserves have been post-poned until after the elections. State officials in New York and other states could face heightened pressure to finalize policy decisions after the elections.

FinancialsDesignation as a systemically important financial institution (SIFI) is often unwelcome as it increases the costs associated with regulatory compliance. For the large insurers subject to non-bank SIFI requirements, a Republican Senate increases the odds that the process by which such a designation is made will be subject to great transparency. Asset managers, who thus far have avoided designation as a SIFI despite their size and importance, would no doubt welcome this develop-ment. They have long argued they are merely agents for their clients’ funds.

A Republican majority in the Senate would have a more lim-ited impact on commercial banks and broker dealers. We do not expect any major changes ton the Dodd-Frank Act, which would still require a bipartisan legislative compromise. One potential change, which seems to have broader appeal,

Policy issues for the 114th Congress

Jerry Brimeyer; Nicole Decker; Michael Dion, CFA; Thomas McLoughlin; Dean Ungar, CFA; John Woloshin, CFA

A shift to a Republican-controlled Senate slightly alters our outlook for some issues. Treasury actions make tax inversions less attractive, but legislative reform remains unlikely. A Republican majority in the Senate could spur legislation favorable to the energy industry.

ElectionWatch

10 electionWatch

Policy issues

would be to raise the threshold for a bank to be considered a SIFI. a higher threshold, with a reduced level of regulatory scrutiny for those institutions falling below the threshold, would open the door to increased M&a activity.

Republican control of the Senate also would likely result in greater scrutiny of the Consumer Financial Protection Bureau (CFBP). We would expect legislative oversight to increase, which could ease the pressure on financial activities ranging from auto loans to payday lending.

In the event the gOP recaptures control of the Senate, we ex-pect banks to lobby regulators more aggressively on modifi-cations to the large bank leverage requirement known as the supplementary leverage ratio. This measure has been widely criticized because it fails to distinguish among the risks posed by different types of assets. There is also some pressure to raise the threshold for determining which banks participate in annual Comprehensive Capital analysis and Review (CCaR) stress tests, which is now set at USD 50bn or more. The 2014 CCaR stress tests included 24 US bank holding companies and six US holding company subsidiaries of foreign banks.

What is a tax inversion?

Sovereign nations apply different methods to tax the profits of private corporations and impose different tax rates. A tax inversion occurs when a US corporation acquires a company based in another country and “redomiciles” its headquarters outside the US, partly to attain a lower corporate tax rate. With its top rate at 35%, the US has the highest nominal corporate tax rate of any developed country (although the effective US rate can be lower due to deductions). Several european countries have meaningfully lower corporate tax rates, such as Ireland at 12.5%, the UK at 21%, the Nether-lands at 25%, and Switzerland at 12–24% (depending on the region).

The controversy over tax inversions reached a new level in the wake of Burger King’s decision to purchase a controlling interest in Tim Horton’s, a Canadian corporation. although inversions can occur in any sector of the economy, the US pharmaceutical industry has been particularly active. Three major healthcare inversion transactions announced this year include Medtronic acquiring Ireland-based Covidien, abbVie acquiring UK-based pharmaceutical company Shire, and Mylan buying abbott’s developed markets pharmaceutical business and redomiciling in the Netherlands. The major tax inversion transaction announced within the technology space is the applied Materials merger with Tokyo electron.

given the political discord in Washington among Democrats and Republicans, Congress was not prepared to prevent more inversions through legislative action. For this reason, the US Treasury Department issued a formal notice in Sep-tember that will make tax inversions more difficult to ex-ecute. The Treasury notice altered five sections of the US tax code, which will make it more difficult for US companies to use cash from non-US operations to finance inversions. The proposed tax code change precludes use of cash that already

exists overseas without paying US taxes, but does not nec-essarily impact future cash generated overseas after an in-version (a major consideration for companies choosing to invert). The Treasury also plans to tighten the rules around ownership requirements following a merger. If US company ownership is above 80% of the new entity, it is still treated as a US corporation for tax purposes.

These new rules will make inversions less economically attrac-tive and more difficult to execute. Already, AbbVie and Shire have mutually agreed to terminate their tax inversion transac-tion due to the new tax code changes set forth by the US Treasury. Mylan’s proposed transaction is also vulnerable to the new rules. Inversion transactions now rely more heavily on debt financing, resulting in less near-term earnings accre-tion (and more earnings dilution). However, the low cost of capital now available to credit-worthy companies can make the use of debt manageable. The long-term advantages of tax inversions are still appealing for many companies – great-er flexibility of offshore cash and a lower corporate tax rate.

The Treasury’s new rule on inversions does not alter our view regarding the prospects for broader tax reform. In general, Republicans are opposed to stand-alone inversion legislation and believe that a more competitive tax code is the answer to stopping inversions. The gOP wants to move away from the current “worldwide” tax system to a “territorial” tax code, which is more consistent with the procedures followed by other countries. Many Democrats, particularly those with strong union constituents, fear loss of US jobs to other coun-tries under a territorial system and thus favor our current worldwide system and separate inversion legislation. While inversions have captured the attention of Congress, we be-lieve a political consensus on comprehensive tax is unlikely before 2017.

electionWatch 11

The Federal Reserve will impose explicit capital, liquidity, and likely stress testing requirements for bank holding compa-nies. The final form of these rules could be tempered by the shape of the midterm elections, in that a more Republican-influenced Senate Banking Committee could pressure regula-tors to ease the rules to some small degree.

Real estateWe believe TRIa (Terrorism Risk Insurance act) will be re-newed. The legislation is crucial for owners of commercial real estate as the expiration of TRIa would make the cost of ter-rorism insurance prohibitive. The Foreign Investment Real Property Tax act (FIRPTa) is also likely to be back on the agen-da should Republicans succeed in winning control of both houses of Congress. FIRPTa is a withholding tax applied to foreigners on the sale proceeds from real estate. a relaxation or elimination of FIRPTa could spur additional foreign invest-ment in US commercial real estate.

a Republican Senate might well use its control of the legisla-tive agenda to limit the political pressure currently being ap-plied to lending institutions. In an optimistic scenario, this could lead to a further availability of mortgage credit. Reform of government-sponsored enterprises is likely to be on the House agenda, where some Republicans want to pursue priva-tization of Fannie Mae and Freddie Mac. Others within the gOP caucus prefer a more gradual transition, while Democrat-ic House members prefer a more hands-off approach. Our col-leagues in the US Office of Public Policy expect a great deal of debate over this issue, but the chances of legislation are slim.

Policy issues

Source: The staff of the US Congress Joint Committee on Taxation, UBS CIO WMR, as of 5 August 2014

700600500400300200100 8000

Net exclusion of pension contributions and earnings (Keogh, defined benefit, defined contribution)Reduced rates of tax on dividends, long-term capital gains

Controlled foreign corporations – Active Income DeferralMortgage interest deduction on owner-occupied residences

Earned income credit exclusionExclusion of Medicare benefits (Parts A, B and D)

Subsidies for insurance purchased through health benefit exchangesDeduction of nonbusiness state and local government income taxes, sales taxes, and personal property taxes

Social services credit for children under the age of 17Exclusion of untaxed Social Security and railroad retirement benefits

Exclusion of benefits provided under cafeteria plansDeduction for charitable contributions, other than for education and health

Deduction for property taxes on real propertyInterest on public purpose state and local government bonds exclusion

Contributions for healthcare and insurance premiums – Exclusion

Fig. 1: Estimated tax expenditures 2014–2018

In USD bn

785.1699.4

632.8418.0

405.2352.8350.2

285.5209.1

193.0192.0

182.1179.6

318.1316.4

MunicipalsConstitutional protection from federal taxation of interest on state and local government debt was weakened when the US Supreme Court ruled in 1988 that Congress could eliminate the tax exemption on municipal bonds that were not properly reg-istered. In a 7-1 decision, the Court decided that interest pay-ments on state and local government debt were not immune from a non-discriminatory federal tax.11 In its opinion, the Court ruled that state governments must find their protection from Congressional regulation through the national political process rather than through litigation.12

Subsequent legislative initiatives to reduce or to eliminate the tax shelter provided by municipal bonds have recurred with greater frequency in recent years. In 2011, the Obama adminis-tration proposed to limit the amount of interest income that could be excluded from federal taxation.13 The proposal failed to garner enough Congressional support for passage but intro-duced the possibility that Congress might one day impose re-strictions on the ability of individual taxpayers to deduct municipal bond interest from their taxable income.

We do not expect Congress to alter the rules governing mu-nicipal bond tax exemption in the next two years. Such an ef-fort is more likely in the context of comprehensive tax reform, where Congress will set its sights on curtailing the number and breadth of tax shelters found in the Internal Revenue Code. Tax reform is a topic that garners a lot of interest among mem-bers of Congress but is exceptionally difficult to accomplish.

12 electionWatch

Elections have consequences. President Obama’s state-ment in 2009 might well be true for public policy but an elec-tion’s impact on equity markets is rarely so straightforward and is often difficult to measure. With that caveat, we feel comfortable concluding that this year’s election will likely have minimal impact on the equity market. We do not expect many policy shifts in the UBS base case scenario whereby the GOP gains control of the Senate. as we discussed earlier in this re-port, there may be changes to the legislative committee agen-das but more substantive changes in policy must await the next presidential administration. In many respects, the next two years will simply be a continuation of the recent gridlock in Washington.

Gridlock isn’t necessarily bad for financial markets. At a mini-mum, it reduces policy uncertainty. and as we show in Fig. 1, the improvement in policy uncertainty in recent years has like-ly been one of the drivers of higher equity market valuations. With the budget deficit back to normal levels relative to the size of the economy, the need for significant tax and spending changes is low – at least until Medicare expenditures start to ramp up at the end of the decade. But gridlock does mean

that US taxpayers – both business and consumers – will re-main saddled with an inefficient tax code that leaves a moun-tain of corporate cash trapped overseas. and investors are likely to remain hostage to the periodic battles over the bud-get and increases in the federal government debt ceiling.

A new debt ceiling playbook?We don’t view another potential government shutdown as a significant market-moving event – very little economic activ-ity is disrupted by a brief shutdown. However, failure to raise the debt ceiling which leads to a default on US government debt would clearly be very unsettling. By now, investors have become accustomed to the typical debt ceiling playbook. There is a fair amount of political posturing before the dead-line but a solution is found at the last minute to avoid a de-fault. as a result, equity markets have become less sensitive to these episodes.

a gOP-controlled Senate could change the political calculus to some degree as there is some uncertainty as to how a newly empowered Senate leadership would choose to nego-tiate. However, we believe it more likely that the Republican

Market implications

David Lefkowitz, CFA; Leslie Falconio

We believe election results do not affect US equity and fixed income markets materially. Political gridlock is not necessarily bad for markets.

ElectionWatch

Source: US Senate, US House of Representatives, FactSet, as of 27 October 2014

0

6

4

2

8

12

14

10

Democratic Congress Republican CongressDivided Congress

Fig. 2: Returns are higher when Congress is controlled byone party

S&P 500 average annual total return 1928–2014, in %

Source: Bloomberg, FactSet, UBS WMR, as of 25 September 2014

Equity risk premium (right)Economic Policy Uncertainty Index (standardized, le)

2.5

–5.0

–2.5

0.0

5.0

6.0

–3.0

0.0

3.0

9.0

2000 2002 2004 2006 2008 2010 2012 2014

Fig. 1: Policy and market valuations have been linked overthe past decade

Equity risk premium and economic policy uncertainty index

electionWatch 13

Source: US Senate, US House of Representatives, FactSet, as of 27 October 2014

0

642

8

12

181614

20

10

Democratic Congress Republican CongressDivided Congress

Fig. 3: During a Democratic presidency, returns are highestunder a Republican Congress

S&P 500 average annual total return 1928–2014, in %

majority will exercise some restraint in this area because they will be eager to demonstrate their ability to govern responsi-bly before the next presidential election. For that reason, while investors should be prepared for possible financial mar-ket volatility ahead of the next round of debt ceiling negotia-tions, we still believe an outright default is extremely unlikely. The debt limit will likely have to be raised again in mid-2015.

Which party is better for stocks?We have examined past equity market returns through two different “political” lenses: 1) which party controls the White House and Congress; and 2) the presidential election cycle. as we show in Fig. 2, equity markets tend to be strongest when one party controls both chambers of Congress, with returns slightly better when Republicans are in the major-ity. Returns are even better when the president is a Demo-crat and the gOP controls Congress (see Fig. 3). To be clear, we place limited value on this type of analysis because the sample size is so small that the results are not statistically sig-nificant. In addition, at any given time, a wide array of fun-damental drivers impact equity market returns. In our view, it is questionable to narrowly pinpoint a causal link between the party affiliation of the occupants of the White House and Congress and equity market returns.

Presidential election cycle may not holdThe presidential election cycle is another often-cited market dy-namic based on the observation that weaker equity market re-turns in the first two years of a president’s term are generally followed by stronger returns in the third and fourth years (see Fig. 4). The logic behind this pattern rests on the premise that an incumbent president will pursue pro-growth policies more

aggressively in the second half of his/her term in order to boost re-election chances for his/her party. This would suggest that the stock market should enjoy nice gains in the coming two years. However, the political gridlock we described earlier means it will be nearly impossible for any new policies to be implemented, even ones that would boost economic pros-pects. as a result, we tend to downplay the relevance of this historical pattern.

Our favorable view on US equity markets will not likely be meaningfully threatened or further supported by the results of next month’s election. Instead, solid earnings growth, a Federal Reserve that will continue to pursue pro-growth poli-cies and fair equity market valuations – especially relative to bonds – should continue to drive US stocks indexes higher. That being said, we will continue to be vigilant for any gov-ernment policy changes that could “upset the apple cart” and alter our baseline view.

TreasuriesWe have examined the historical relationship between mid-term election results and subsequent changes in Treasury mar-ket yields and are obliged to conclude the relationship is rather tenuous (see Fig. 5). In examining the two-week change in 10-year Treasury rates following all midterm elections back to 1994, we find that Treasury rates rose in the wake of the election four times out of five. The magnitude of the move, however, was not particularly significant. On average, yields in-creased by a mere 10 basis points (bps). The largest move was 32bps in 2010. In short, the Treasury market has treated the midterm elections as a non-event in most cases.

Market implications

Source: Bloomberg, UBS WMR, as of 6 September 2012

0

642

8

12

181614

20

10

Year 1 Year 3 Year 4Year 2

Fig. 4: Markets tend to perform best in the last two years ofa president’s term

S&P 500 returns segmented by year of a presidential term (1929-2012), in %

14 electionWatch

AgenciesWe believe that prospects for comprehensive housing finance reform (e.g., regulatory reform for Fannie Mae and Freddie Mac) are remote. The political gulf between Republicans and Democrats is just too large to bridge in the near term. Just as important, the political risk-reward calculus around this issue is upside down, in our opinion. The potential political reward from being associated with any substantial version of housing finance reform pales in comparison to the potential risk of at-taching oneself politically to reform if housing price apprecia-tion dips considerably. Instead, we believe the most likely outcome is another stalemate. With the apparent failure of some high-profile hedge fund lawsuits recently, Fannie and Freddie may not be going anywhere soon.1

FinancialsFor bond investors, the current stringent requirements have lowered the risk posed by bank bonds and preferred shares. Credit spreads on bank debt and preferred shares have nar-rowed since the financial crisis as banks have rebuilt their bal-ance sheets under the watchful eye of their regulators. The new rules have improved the credit strength of banks and large non-bank financial institutions.

The august 2011 Congressional budget impasse, which contributed to S&P’s decision to reduce the sovereign credit rating of the United States to aa+ from aaa was a rude awakening for the US credit market. The subsequent mar-ket dislocations contributed to dramatic widening of credit spreads in the third quarter of 2011. Investment grade credit

spreads widened by 93bps to 257bps during the quarter and reached a 2-year high of 272bps in early October 2011. High yield spreads also spiked by 300bps, ending the quarter at 842bps. While periodic budgetary crises resurfaced again in 2012 and 2013, none of these had the same impact as the 2011 episode. as in the equity market, we believe the politi-cal risk associated with debates over the debt ceiling and the federal budget has diminished.

In sum, we anticipate a GOP majority in the Senate, which will allow Republicans to set the legislative agenda and to cooperate with colleagues in the House on hot-button issues important to more con-servative members of their caucus. However, Demo-crats are likely to retain enough seats in the Senate to impede legislation to which they object. The prospect of a major legislative breakthrough on issues ranging from banking regulation to the reform of govern-ment-sponsored enterprises is slim.

Market implications

Source: Bloomberg, UBS CIO WMR, as of 13 October 2014

1

0

3

2

5

4

Nov-02Nov-01Nov-00Nov-99 Nov-03 Nov-04 Nov-12Nov-11Nov-10Nov-09Nov-08Nov-07Nov-06Nov-05 Nov-13

6

8

7

9

10-year yield

Nov-98Nov-97Nov-96Nov-95Nov-94

The 10-year yield has averaged +10bps more during the midterm elections since 1994, the highest being in 2010

Change in the 10-year yield during mid-term elections

1994 – Bill Clinton’s first term. Republican party took controlof both houses, first time since1954.

1998 – Clinton’s 2nd term, Democrats in the Senate; gained 5 House seats.

2002 – A first term president’sparty gained power. Republicanparty increased margin in the House. Regained control of the Senate.

2006 – George W. Bush's second term, saw a sweeping victory for the Democratic Party.

2010 – Unemployment is over 9%. Republicans take the House. Largest market response to date at 32bps

Appendix

Endnotes Introduction 1 Seth Motel, “For Many americans, a ‘meh’ midterm,” Pew Research

Center, 8 October 2014.

Rise of social media 1 Vital Statistics on Congress: Chapter 3: Campaign Finance in

Congressional elections, Brookings Institution, 14 March 2013. 2 Politics Fact Sheet, Pew Research Internet Project, 16 October 2014.

Political dynamics 1 Doyle McManus, “The Republican midterm advantage: reliable voters,”

Los Angeles Times, 14 October 2014. 2 “Ad Spending Poised to Break $1 Billion,” Wesleyan Media Project, 14

October 2014. The data is based upon all media purchases from 01 January 2013 through 09 October 2014.

3 Wesleyan Media Project, “Ad Spending Poised to Break $1 billion,” 14 October 2014. The list of issues herein is derived upon research com-pleted by the Wesleyan Media Project based on advertisements in the period from 26 September to 9 October 2014.

4 Charlie Cook, “History shows that midterm elections are usually bad for the president’s party,” National Journal, 6 January 2014. Years in which the size of the House of Representatives was increased are excluded.

5 Charlie Cook, “History shows that midterm elections are usually bad for the president’s party,” National Journal, 6 January 2014.

6 Ibid. 7 Jeffrey M. Jones, “Record-High 42% of Americans Identify as

Independents,” gallup, 8 January 2014. 8 Ibid. 9 Ibid. 10 “Political Polarization in the American Public,” Pew Research Center

for People and the Press, 12 June 2014. Pew’s data is drawn from a

national telephone survey conducted over three months in the first quarter of 2013. The survey contacted 10,013 adults and followed up with subsequent surveys.

11 The registration of municipal bonds was required by the Tax equity and Fiscal Responsibility act of 1982. Please refer to “The Renewed Battle over Tax exemption of Interest on State and Local government Debt Obligations” in government Finance Review, February 2013 for a fur-ther discussion.

12 South Carolina v Baker 485 US 505 (1988). The case was argued on 7 December 1987 and decided on 20 April 1988. See supreme.justia.com

13 The american Jobs act of 2011.

Demographic trends 1 “Home-Price gains Decelerate in Many Metro areas during Second

Quarter,” National association of Realtors, 12 august 2014. 2 Nancy Benac and Connie Cass, “Face of electorate becomes more di-

verse in america,” associated Press, 10 November 2012.

Market implications 1 In simplified terms, these hedge fund lawsuits (e.g., Fairholme, Perry,

arrowood) generally claim that the government overstepped its bounds and treated investors unfairly when it set (and then later revised) the terms of the Senior Preferred Stock Purchase agreement that now sweeps all profits of Fannie Mae and Freddie Mac to the government. Plaintiffs argued that common and preferred stockholders were unfairly deprived of their share of those profits and were thus due damages. These claims were dismissed in district court and are now in different stages of the appeal process.

Chief Investment Office (CIO) Wealth Management (WM) Research is published by UBS Wealth Management and UBS Wealth Management Americas, Business Divisions of UBS AG (UBS) or an affiliate thereof. CIO WM Research reports published outside the US are branded as Chief Investment Office WM. In certain countries UBS AG is referred to as UBS SA. This publication is for your information only and is not intended as an offer, or a solicitation of an offer, to buy or sell any investment or other specific product. The analysis contained herein does not constitute a personal recommendation or take into account the particular investment objectives, investment strategies, financial situation and needs of any specific recipient. It is based on numerous assumptions. Different assumptions could result in materially different results. We recommend that you obtain financial and/or tax advice as to the implications (including tax) of investing in the manner described or in any of the products mentioned herein. Certain services and products are subject to legal restrictions and cannot be offered worldwide on an unrestricted basis and/or may not be eligible for sale to all investors. all information and opinions expressed in this document were obtained from sources believed to be reliable and in good faith, but no representation or warranty, express or implied, is made as to its accuracy or completeness (other than disclosures relating to UBS and its affiliates). All information and opinions as well as any prices indicated are current only as of the date of this report, and are subject to change without notice. Opinions expressed herein may differ or be contrary to those expressed by other business areas or divisions of UBS as a result of using different assumptions and/or criteria. at any time, investment decisions (including whether to buy, sell or hold securities) made by UBS AG, its affiliates, subsidiaries and employees may differ from or be contrary to the opinions expressed in UBS research publications. Some investments may not be readily realizable since the market in the securities is illiquid and therefore valuing the investment and identifying the risk to which you are exposed

may be difficult to quantify. UBS relies on information barriers to control the flow of information contained in one or more areas within UBS, into other areas, units, divisions or affiliates of UBS. Futures and options trading is considered risky. Past performance of an investment is no guarantee for its future performance. Some investments may be subject to sudden and large falls in value and on realization you may receive back less than you invested or may be required to pay more. Changes in FX rates may have an adverse effect on the price, value or income of an investment. This report is for distribution only under such circumstances as may be permitted by applicable law.

Distributed to US persons by UBS Financial Services Inc., a subsidiary of UBS AG. UBS Securities LLC is a subsidiary of UBS AG and an affiliate of UBS Financial Services Inc. UBS Financial Services Inc. accepts responsibility for the content of a report prepared by a non-US affiliate when it distributes reports to US persons. all transactions by a US person in the securities mentioned in this report should be effected through a US-registered broker dealer affiliated with UBS, and not through a non-US affiliate. The contents of this report have not been and will not be approved by any securities or investment authority in the United States or elsewhere.

UBS specifically prohibits the redistribution or reproduction of this material in whole or in part without the prior written permission of UBS and UBS accepts no liability whatsoever for the actions of third parties in this respect.

Version as per May 2014.

© UBS 2014. The key symbol and UBS are among the registered and unregistered trademarks of UBS. all rights reserved.

ab

©2014 UBS Financial Services Inc. all rights reserved.

Member SIPC. all other trademarks, registered trademarks,

service marks and registered service marks are of their

respective companies.

UBS Financial Services Inc.

www.ubs.com/financialservicesinc

UBS Financial Services Inc. is a subsidiary of UBS ag.