Embed Size (px)

Citation preview

© 2014 Eaton. All Rights Reserved..

Electrical Products Group Conference

Alexander M. Cutler – Chairman and Chief Executive Officer

May 20, 2014

2 © 2014 Eaton. All Rights Reserved..

Forward-looking statements and non-GAAP financial information

The information provided at our conference today will include forward-looking statements relating to our goals and estimates for future years, including statements about expected sales, acquisition synergies, operating earnings per share, cash flow, segment margins, our worldwide markets, our anticipated effective income tax rate, the effects of currency exchange rates, our capital allocation plans and others. These statements should be used with caution and are subject to various risks and uncertainties, many of which are outside the company’s control. The following factors could cause actual results to differ materially from those in the forward-looking statements: unanticipated changes in the markets for the company’s business segments; unanticipated downturns in business relationships with customers or their purchases from us; competitive pressures on sales and pricing; increases in the cost of material and other production costs, or unexpected costs that cannot be recouped in product pricing; the introduction of competing technologies; unexpected technical or marketing difficulties; unexpected claims, charges, litigation or dispute resolutions; the impact of acquisitions and divestitures; unanticipated difficulties integrating acquisitions or realizing expected synergies from the Cooper acquisition; new laws and governmental regulations; interest rate changes; changes in currency exchange rates; stock market fluctuations; and unanticipated deterioration of economic and financial conditions in the United States and around the world. We do not assume any obligation to update these forward-looking statements. This presentation includes certain non-GAAP measures as defined by SEC rules. A reconciliation of those measures to the most directly comparable GAAP equivalent is provided in the investor relations section of our website at www.eaton.com and is contained in your packet.

3 © 2014 Eaton. All rights reserved.

Eaton is a leading global power management company

Uniquely positioned to provide safe, reliable, efficient and sustainable power management solutions for our global customers

Electrical Fluid Mechanical

Cities & Buildings

Industrial & Machinery

Information Technology

Energy & Utilities

Transportation Infrastructure

4 © 2014 Eaton. All rights reserved.

We have created a portfolio capable of delivering stronger growth and more consistent earnings…

61% 14%

8%

17%

2013 Segment Sales

Electrical Hydraulics

Aerospace Vehicle

50%

26%

24%

2013 Sales by Destination

U.S.Int'l DevelopedInt'l Emerging

29%

29%

31%

11%

2013 Cycle Sales

Early Mid Late No

5 5

…and our returns have substantially exceeded those of our peers and the S&P 500

2000 – April, 2014 CAGR* Return

Index

14.8%

Note – ** Peer Group represents an equal weighted index of ABB, DHR, DOV, EMR, HON, IR, ITW, LR, PH, ROK, SIE, SU, UTX *CAGR = Calculated using the End Point Methodology Source Data: Capital IQ, Eaton analysis

0

100

200

300

400

500

600

700

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Apr30,

2014

Cumulative Shareholder Returns

Eaton S&P 500 Peer Group**

12.2%

4.7%

6 © 2014 Eaton. All Rights Reserved.

The Cooper acquisition significantly expanded our electrical solutions

Legacy Eaton

Former Cooper

Data Centers Industrial Utility Commercial / Residential Machinery

7 © 2014 Eaton. All Rights Reserved.

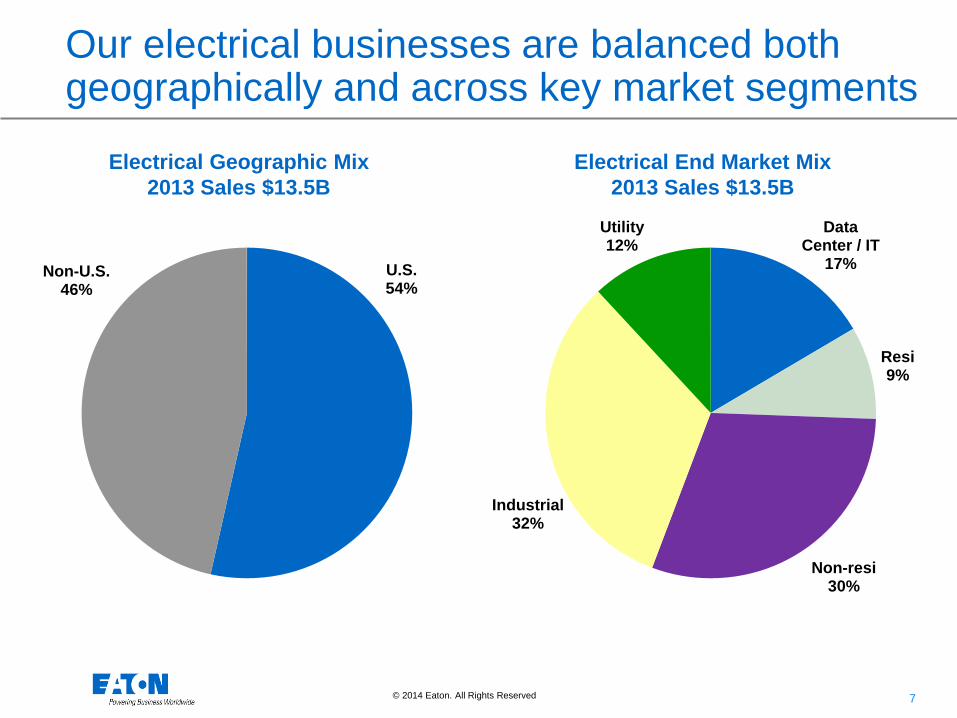

Our electrical businesses are balanced both geographically and across key market segments

Electrical Geographic Mix 2013 Sales $13.5B

U.S. 54%

Non-U.S. 46%

Electrical End Market Mix 2013 Sales $13.5B

Data Center / IT

17%

Resi 9%

Non-resi 30%

Industrial 32%

Utility 12%

8 © 2014 Eaton. All Rights Reserved.

Power distribution and circuit protection Delivers reliable, efficient and safe power where it is needed

Panelboards and switchboards

LV / MV switchgear Transformers Fuses Circuit

breakers

• Eaton is the only company that provides both a full range of circuit breakers and fuses, selling them both stand alone and packaged in NEMA / ANSI or IEC assemblies

• We are extending that position with an innovative power distribution fuse block that uses 50% less panel space and reduces installation time and labor by 33%

• We are a clear leader in arc flash technology

Our expanded electrical business has a number of distinctive capabilities in power distribution…

9 © 2014 Eaton. All Rights Reserved.

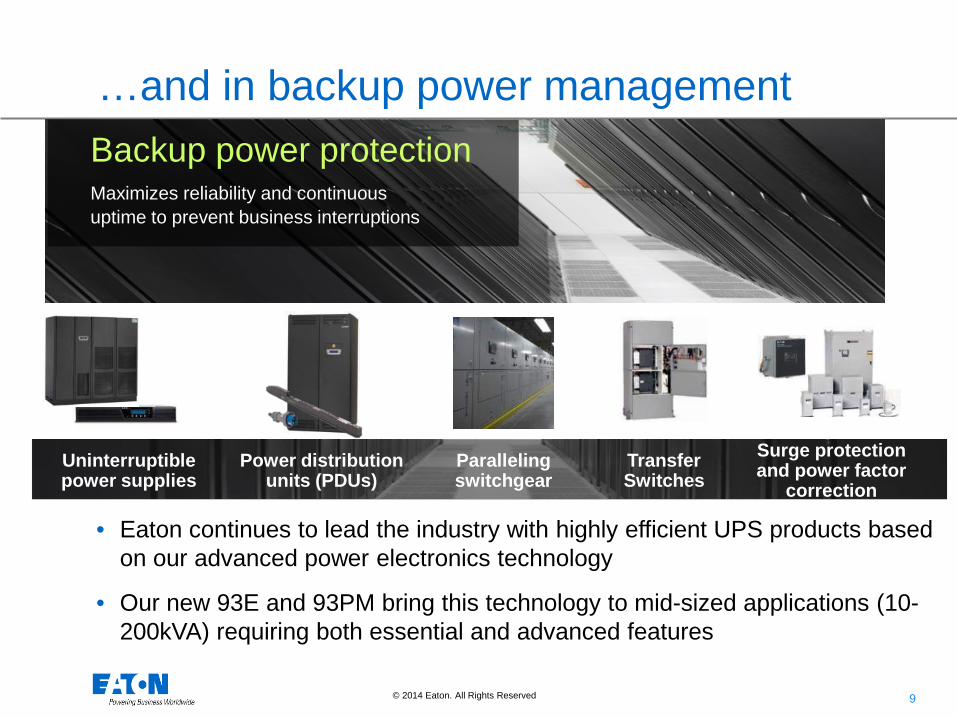

• Eaton continues to lead the industry with highly efficient UPS products based on our advanced power electronics technology

• Our new 93E and 93PM bring this technology to mid-sized applications (10-200kVA) requiring both essential and advanced features

Backup power protection Maximizes reliability and continuous uptime to prevent business interruptions

Uninterruptible power supplies

Surge protection and power factor

correction Power distribution

units (PDUs) Transfer Switches

Paralleling switchgear

…and in backup power management

10 © 2014 Eaton. All Rights Reserved.

Recessed lighting

Ambient lighting

Hazardous area communications

Emergency lighting

Outdoor lighting

Fire systems

Lighting and security Improved efficiency, comfort and safety in the home and the workplace

• Eaton is leading the conversion to LED lighting technology, with 35% of our lighting being LED

• Our new Wavestream technology enables easier installation, better light output and higher efficiency

Cooper acquisition brought lighting and security capabilities to the portfolio…

11 © 2014 Eaton. All Rights Reserved.

Enclosures Industrial control and switchgear Instrumentation Lighting

Solutions for harsh and hazardous environments Delivers reliability and safety to prevent production interruptions

Commercial outlet boxes, wiring and fittings

• Eaton’s Crouse-Hinds unit specializes in packaging products for Class 1 environments

• We have extended our lead with 50+ new product introductions for that environment

• We are the first to determine how to package a drive to work in a Class 1 environment

…along with a range of solutions for harsh and hazardous environments

12 © 2014 Eaton. All Rights Reserved.

Cable tray systems

Bolted framing strut systems

Enclosures and airflow management Safety grating

Structural solutions Improved efficiency and safety during installation with maximum return on investment

• Eaton cable support systems allow for longer spans, resulting in faster installation time and up to 66% less structural steel requirements

• The serrated pattern on Eaton safety grating allows it to be 230% more slip-resistant than other gratings

The Cooper acquisition also increased our range of structural solutions

13 © 2014 Eaton. All Rights Reserved.

Studies Design Build Support • Power quality and reliability audits • Engineering services • Project management • Maintenance / aftermarket • Energy management audits • Consulting services • Turnkey services • 24x7 monitoring • Safety audits • Modeling and analysis • Modernization • Emergency response

Engineering services and project management… through all stages of the application lifecycle

• More than 2,000 field, engineering, management and support professionals in over 20 countries

• Centers of Excellence that specialize in modernization of electrical equipment by upgrading it with the latest technology

We now have the ability to leverage a strong service capability across this expanded portfolio of products

14 © 2014 Eaton. All Rights Reserved.

We continue to leverage innovation and product vitality to drive organic growth

• CXH - Increased safety and reliability with unmatched arc flash mitigation

• Hazardous location boltless cover reduces installation and maintenance costs

Hazardous Area Boltless Enclosures

CXH Low Voltage Assemblies

Marine Duty Uninterruptable Power Supplies

• Marine certified UPS for marine safety, control, bridge and commercial systems

• Standard and engineered solutions address end user applications

Extending UPS technology to additional markets

General Purpose, Machine & EU Directive Drives

• General purpose and machinery drives expand functionality and increase ease of use

• Simple motor drives meet new European energy savings directive

Drives technology for every application

Creating oil & gas technology to enhance safety and maintenance

WaveStream Architectural Solutions

• Expanded WaveStream LED solutions for more design freedom

• Provides best in class optical control, brightness control and energy efficiency

Utilizing LED technology to increase flexibility

15 © 2014 Eaton. All rights reserved.

0

100

200

300

400

500

2013 2014 2015 2016

Syne

rgy

Prof

it ($

M)

Current Plan Original Plan

$115

$210

$360

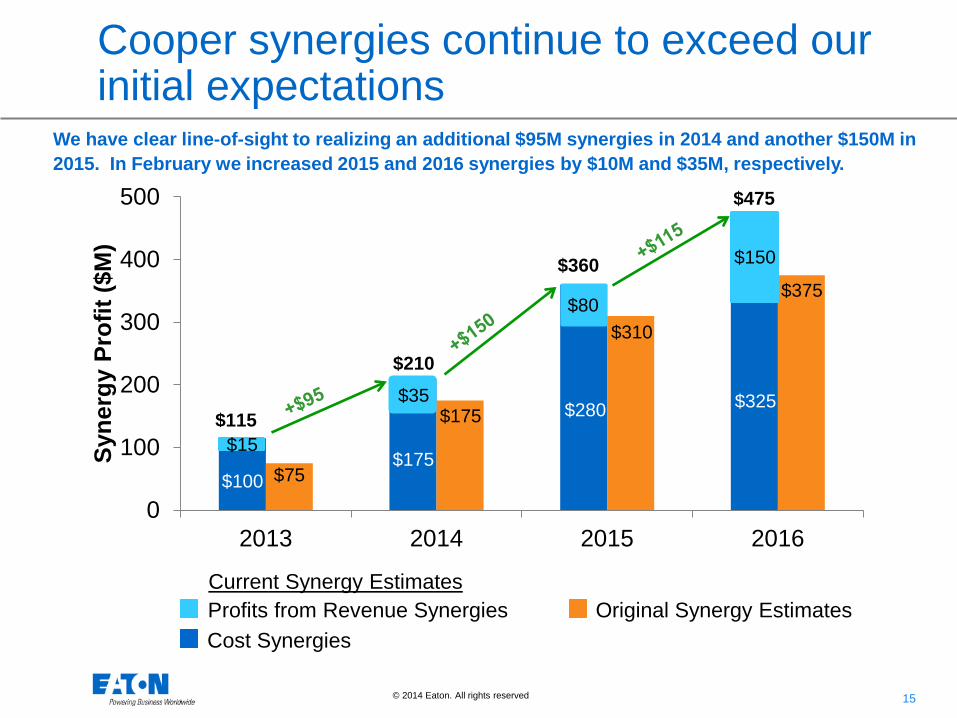

Cooper synergies continue to exceed our initial expectations

We have clear line-of-sight to realizing an additional $95M synergies in 2014 and another $150M in 2015. In February we increased 2015 and 2016 synergies by $10M and $35M, respectively.

$475

$15

$35

$80

$150

$100 $175

$280 $325

$75

$175

$310

$375

Original Synergy Estimates Profits from Revenue Synergies Cost Synergies

Current Synergy Estimates

16 © 2014 Eaton. All Rights Reserved.

Corporate Cost

Reduction • Corporate

functions • Data centers • Back office

support

Plant & Distribution

• Facility & product line rationalization

• Distribution center rationalization

Application of EBS Tools

• ELSS • EQS • PROLaunch • VAVE

Supply Chain Economies

of Scale • Direct /

indirect spend • Logistics

Leveraging Eaton’s

Infrastructure • Operating

SG&A • Shared R&D • Shared

service centers

Cost synergies come from five main areas

EBS

60% of total 2016 cost-out synergies

40% of total 2016 cost-out synergies

17 © 2014 Eaton. All Rights Reserved.

Sales synergies come from four main areas

Geographic Expansion

• Pull-through opportunities

• Greater scale opportunities

Boost Channel

Sales • Distributor

conversion • Increased

penetration

Larger Package to Common Customers

• Oil & Gas • Data Centers • Mining • Utility

Service

Business • Large Cooper

installed base & relationships

• Leverage Eaton’s existing service business

70% of total 2016 sales synergies

30% of total 2016 sales synergies

18 © 2014 Eaton. All rights reserved.

15.4% 16.0% 17.0%

2013 2014e 2015e

14.2% 14.0% 15.0%

2013 2014e 2015e

13.1% 13.5% 15.0%

2013 2014e 2015e

14.4% 14.5% 16.0%

2013 2014e 2015e

16.1% 17.75% 19.0%

2013 2014e 2015e

290 bps

160 bps

190 bps

80 bps

160 bps

We are driving significant margin improvement across all five segments

Electrical Systems & Services

2013-2015 Change

Electrical Products

2013-2015 Change

Hydraulics

Aerospace

Vehicle

2013-2015 Change

2013-2015 Change

2013-2015 Change

We remain on track to achieve segment margins of 17% in 2015

19 © 2014 Eaton. All rights reserved.

Our cash earnings are much greater than operating earnings

$3.45 $4.13

$4.80

$0.24

$0.98 $0.86

$3.69

$5.11 $5.66

2007 2013 2014E

Cash Earnings Comparison

Operating EPS Cash Operating EPS

Note: Cash Operating EPS is Operating EPS plus per share after-tax amortization and inventory step-up expense

20 © 2014 Eaton. All rights reserved.

Strong cash flow and a stronger balance sheet provide future financial flexibility

Nea

r-ter

m

Long

er-te

rm

Capital Allocation Plans

Repurchase shares if we become overcapitalized or there is an opportunity to buy the shares at a sudden discount… …we have repurchased $1.9B in the last 10 years

Invest in acquisitions which advance our strategy and return at least 300 bps over our cost of capital… …expect to have capacity to ramp up acquisition program in 2015

Reinvest in the business to drive organic growth… …invest 3% of sales annually in capital expenses

Return cash to shareholders with a growing dividend… …grow dividends in line with earnings growth

Retire debt to strengthen our balance sheet… …committed to repaying $2.1B of term debt by 2016

21 © 2014 Eaton. All rights reserved.

2014 End Market Growth Forecast

(Y-O-Y % Growth)

Electrical 3% Hydraulics 3% Aerospace 3% Vehicle 5% Consolidated Markets 3%

22 © 2014 Eaton. All rights reserved.

2014 Outlook Market Growth 3% Outgrowth $330M Revenues from Divestiture ($80)M Forex ($200)M Incremental Margin 26% Tax Rate 5%

Operating EPS Full Year $4.60 – $5.00

Q2 $1.15 – $1.25 Operating Cash Flow $2.7B – $2.9B Free Cash Flow $2.0B – $2.2B CAPEX $700M

23 © 2014 Eaton. All rights reserved.

Summary

• For the full year 2014, on modest market growth of 3% we are expecting 16% operating EPS growth based upon the midpoint of our guidance at $4.80

• The Cooper integration remains on track to deliver $210M

of synergies in 2014, representing an increase of $95M over 2013 levels

• In 2015, we expect an additional $185M of operating profits

from: An incremental $150M in Cooper synergies over 2014 levels $35M in incremental annual benefits from the $40M restructuring

program undertaken in the Industrial Sector in Q2 of 2014

24 © 2014 Eaton. All rights reserved.