Embed Size (px)

Citation preview

GST370 – 1

GST370 E (20)Protected B when completed

NOTE: In this form, the text inserted between square brackets represents the regular print information.

Employee and Partner GST/HST Rebate Application

You do not quali fy for this rebate i f your employer is a l isted f inancial insti tut ion (for example, a person that was, at any t ime during the year, a bank, an investment dealer, a trust company, an insurance company, a credit union, or a corporation whose principal business is lending money).

For detai ls on how to complete this form, see Guide T4044, Employment Expenses (for employees) or go to our webpage "GST/HST rebate for employees and partners". This form applies to 2014 and later tax years.

continue on next pageè

GST370 – 2

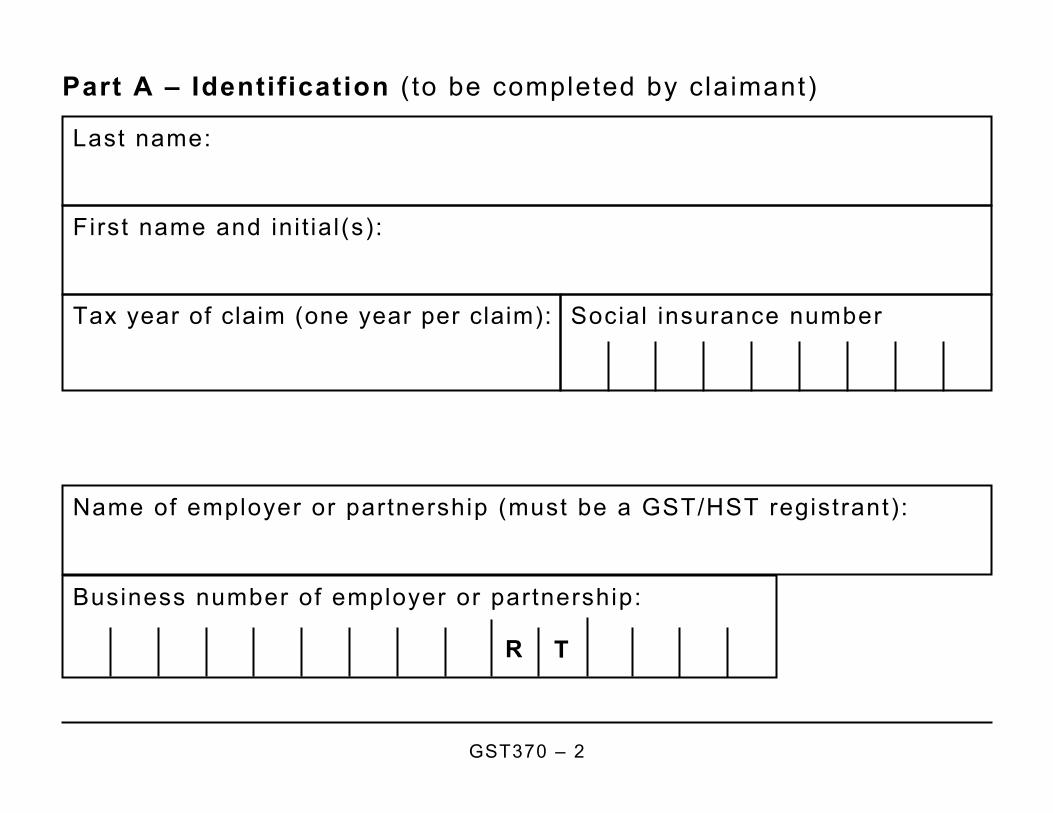

Last name:

Part A – Identification ( to be completed by claimant)

First name and init ial(s):

Tax year of claim (one year per claim): Social insurance number

Name of employer or partnership (must be a GST/HST registrant):

Business number of employer or partnership:

R T

GST370 – 3

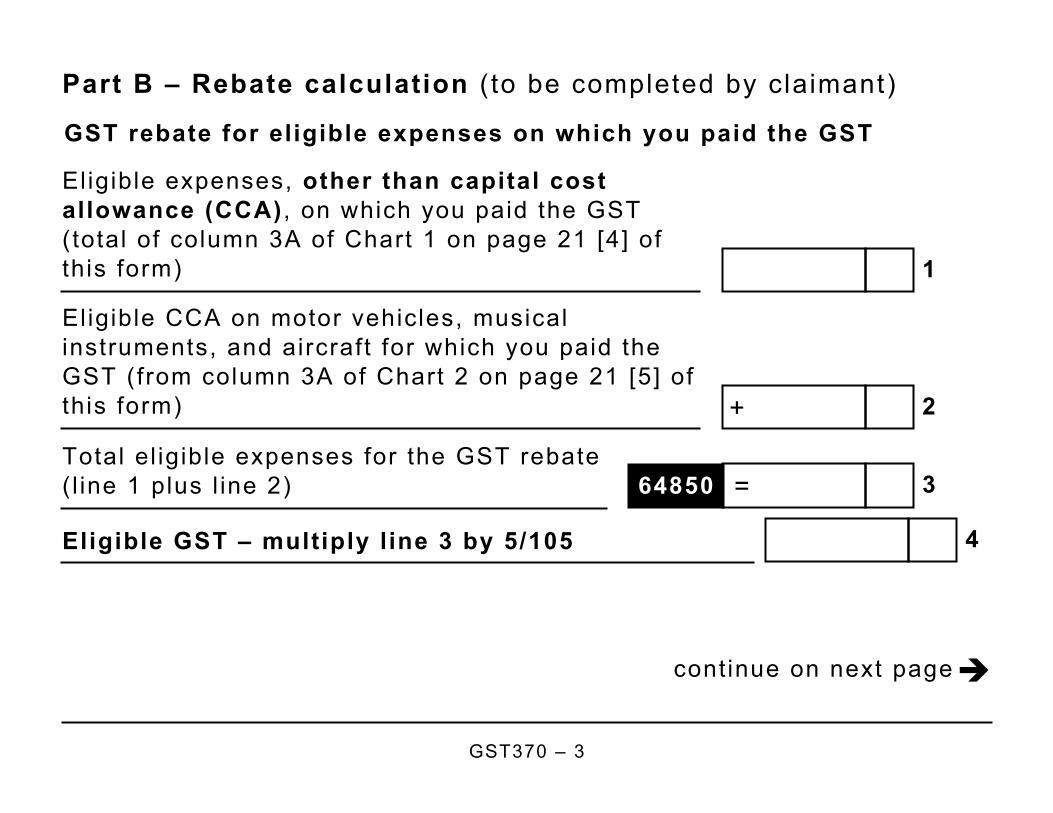

Part B – Rebate calculation (to be completed by claimant)

1

Eligible expenses, other than capital cost allowance (CCA) , on which you paid the GST (total of column 3A of Chart 1 on page 21 [4] of this form)

GST rebate for eligible expenses on which you paid the GST

2+

Eligible CCA on motor vehicles, musical instruments, and aircraft for which you paid the GST (from column 3A of Chart 2 on page 21 [5] of this form)

3=Total el igible expenses for the GST rebate ( l ine 1 plus l ine 2) 64850

4Eligible GST – multiply line 3 by 5/105

continue on next pageè

GST370 – 4

Eligible expenses, other than CCA , on which you paid the HST (totals of each of columns 3B , 3C , and 3D of Chart 1 on page 21 [4] of this form)

Eligible CCA on motor vehicles, musical instruments, and aircraft for which you paid the HST (columns 3B , 3C , and 3D of Chart 2 on page 21 [5] of this form)

HST rebate for eligible expenses on which you paid the HST

3D – 15% HST3B – 13% HST 3C – 14% HST

5

3D – 15% HST3B – 13% HST 3C – 14% HST

6+

Total (add l ines 5 and 6 in each of columns 3B , 3C , and 3D)

3D – 15% HST3B – 13% HST 3C – 14% HST

7=

GST370 – 5

9Mult iply Column 3B l ine 7 by 13/113

8

Total el igible expenses for the HST rebate (add the totals of column 3B , 3C , and 3D together from l ine 7) 64857

10Mult iply Column 3C l ine 7 by 14/114

11Mult iply Column 3D l ine 7 by 15/115

12

Total (add lines 9, 10, and 11). For more information to complete this section, see Guide T4044 go to our webpage "GST/HST rebate for employees and partners".

13

Total expenses el igible for the HST rebate (from l ine 4 in Chart 3 on page 26 [5] ). 64860

continue on next pageè

GST370 – 6

14

Rebate for property and services brought into a participating province. Enter the result from l ine 10 in Chart 3 on page 26 [5] of this form.

15

Employee and partner GST/HST rebate (add l ines 4, 12, and 14). Enter the result on l ine 15, and enter that amount on l ine 45700 of your income tax and benefi t return.

Part C – Declaration by claimant's employer or partnership

An authorized off icer of your employer or partnership must complete this part only i f you are claiming a rebate for any expenses included on l ines 4, 12, or 14 in Part B (pages 3, 5 and 6 [pages 1 and 2] ) for which you were paid an unreasonable al lowance.

continue on next pageèGST370 – 7

Al lowance paid:

I cert i fy that for the tax year stated in Part A, the claimant was paid the fol lowing al lowance(s), which at the t ime i t was paid, I did not consider to be reasonable for the purposes of subparagraphs 6(1)(b)(v), (vi), (vi i) , or (vi i .1) of the Income Tax Act. I wi l l not include an amount equal to this al lowance when determining my input tax credit or rebate.

$

Reason for al lowance(s) ( l ist act ivi t ies):

Name of employer or partnership

Signature of employer or authorized off icer

Posit ion of authorized off icer Year Month Day

GST370 – 8

Part D – Certification (to be completed by claimant)I cert i fy that the information given on this form is correct and complete and that I am el igible for the employee and partner GST/HST rebate for the tax year stated in Part A.

Signature Year Month Day

continue on next pageèGST370 – 9

Chart 1 – Eligible expenses (other than CCA) on which you paid GST/HST

Type of expenses

(1) Total expenses

5% GST A

13% HST B

14% HST C

◄

Accounting and legal feesAdvert ising and promotion

Food, beverages, and entertainment

Lodging

Parking

Supplies

15% HST D

GST370 – 10◄

Type of expenses

(1) Total expenses

5% GST A

13% HST B

14% HST C

◄

Tradesperson's tools expenses (for employees)Apprentice mechanic tools expenses (for employees)Musical instrument expenses other than CCAArtists' employment expensesUnion, professional, or similar dues

15% HST D

continue on next pageèGST370 – 11◄

Type of expenses

(1) Total expenses

5% GST A

13% HST B

14% HST C

◄

Other expenses (please specify)

Fuel

Maintenance and repairsInsurance, l icence, registrat ion, and interest

Leasing

15% HST D

Motor vehicle expenses:

Other expenses (please specify)

GST370 – 12

Work space in home:

◄

Type of expenses

(1) Total expenses

5% GST A

13% HST B

14% HST C

◄

15% HST D

Electr ici ty, heat, and water

Maintenance

Insurance and property taxesOther expenses (please specify)

GST370 – 13

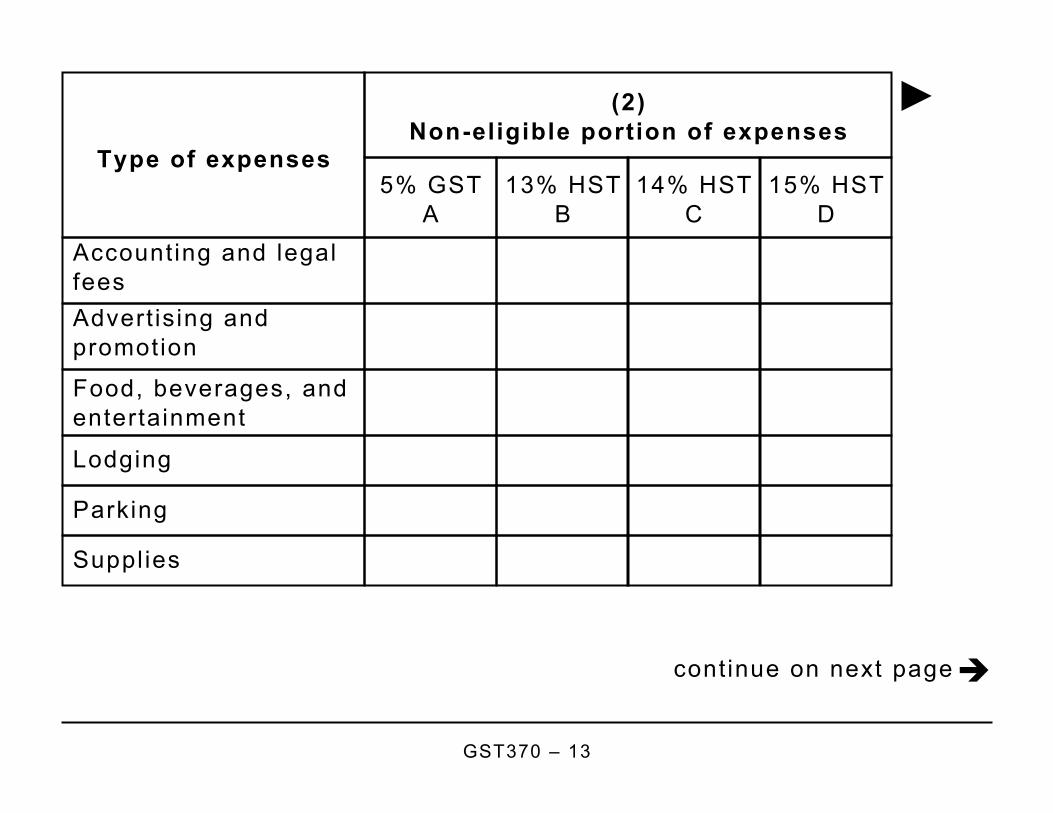

Type of expenses

(2) Non-eligible portion of expenses

5% GST A

13% HST B

14% HST C

◄

Accounting and legal feesAdvert ising and promotion

Food, beverages, and entertainment

Lodging

Parking

Supplies

15% HST D

continue on next pageè

GST370 – 14◄

Type of expenses

(2) Non-eligible portion of expenses

5% GST A

13% HST B

14% HST C

◄

Tradesperson's tools expenses (for employees)Apprentice mechanic tools expenses (for employees)Musical instrument expenses other than CCAArtists' employment expensesUnion, professional, or similar dues

15% HST D

continue on next pageèGST370 – 15

Type of expenses

◄

(2) Non-eligible portion of expenses

5% GST A

13% HST B

14% HST C

◄

Other expenses (please specify)

Fuel

Maintenance and repairsInsurance, l icence, registrat ion, and interest

Leasing

15% HST D

Motor vehicle expenses:

Other expenses (please specify)

GST370 – 16

Work space in home:

◄

Type of expenses

(2) Non-eligible portion of expenses

5% GST A

13% HST B

14% HST C

◄

15% HST D

Electr ici ty, heat, and water

Maintenance

Insurance and property taxesOther expenses (please specify)

GST370 – 17

Type of expenses

(3) Eligible expenses (col. 1 minus col. 2)

5% GST A

13% HST B

14% HST C

◄

Accounting and legal feesAdvert ising and promotion

Food, beverages, and entertainment

Lodging

Parking

Supplies

15% HST D

continue on next pageè

GST370 – 18◄

Type of expenses

(3) Eligible expenses (col. 1 minus col. 2)

5% GST A

13% HST B

14% HST C

◄

Tradesperson's tools expenses (for employees)Apprentice mechanic tools expenses (for employees)Musical instrument expenses other than CCAArtists' employment expensesUnion, professional, or similar dues

15% HST D

continue on next pageèGST370 – 19

Type of expenses

◄

(3) Eligible expenses (col. 1 minus col. 2)

5% GST A

13% HST B

14% HST C

◄

Other expenses (please specify)

Fuel

Maintenance and repairsInsurance, l icence, registrat ion, and interest

Leasing

15% HST D

Motor vehicle expenses:

Other expenses (please specify)

GST370 – 20

Work space in home:

◄

Type of expenses

(3) Eligible expenses (col. 1 minus col. 2)

5% GST A

13% HST B

14% HST C

◄

15% HST D

Electr ici ty, heat, and water

Maintenance

Insurance and property taxesOther expenses (please specify)

continue on next pageèGST370 – 21◄

Total eligible expenses (other than CCA) in each of columns 3A, 3B, 3C, and 3D

◄

(3) Eligible expenses (col. 1 minus col. 2)

5% GST A

13% HST B

14% HST C

15% HST D

Chart 2 – GST/HST paid on expenses on which you claimed Capital Cost Allowance (CCA)

Capital cost allowance (CCA) on motor vehicles, musical instruments, and aircraft

◄

(1) Total expenses

5% GST A

13% HST B

14% HST C

15% HST D

GST370 – 22◄

Capital cost allowance (CCA) on motor vehicles, musical instruments, and aircraft

◄

(2) Non-el igible port ion of expenses

5% GST A

13% HST B

14% HST C

15% HST D

◄Capital cost allowance (CCA) on motor vehicles, musical instruments, and aircraft

◄(3)

Eligible expenses (col. 1 minus col. 2)

5% GST A

13% HST B

14% HST C

15% HST D

GST370 – 23

Chart 3 – Rebate for property and services brought into a participating province

Rebate for property and services brought into a participating province. Do not include any expenses for which you paid the HST (federal and provincial component) as i t should be included in Chart 1. For more information, go to Situation 5 on our webpage "GST/HST rebate for employees and partners".

continue on next pageè

GST370 – 24

A – 1% HST

B – 2% HST

C – 8% HST

◄

Eligible expenses, other than CCA , on which you paid the provincial part of the HST separately

Eligible CCA on motor vehicles, musical instruments, and aircraft for which you paid the provincial part of HST separately

1

2+ + +Total (add l ines 1 and 2 in each of columns A , B , C , D and E) 3= = =

GST370 – 25

D – 9% HST

E – 10% HST

◄

Eligible expenses, other than CCA , on which you paid the provincial part of the HST separately

Eligible CCA on motor vehicles, musical instruments, and aircraft for which you paid the provincial part of HST separately

1

2+ +

Total (add l ines 1 and 2 in each of columns A , B , C , D and E) 3= =

continue on next pageè

GST370 – 26◄

4

Total expenses el igible for the HST rebate (add the totals of columns A , B , C , D and E together from l ine 3). Enter the result on l ine 13 of Part B on page 5 [2]. 64860

5Mult iply the amount on l ine 3 of column A by 1/101

6Mult iply the amount on l ine 3 of column B by 2/102

7Mult iply the amount on l ine 3 of column C by 8/108

8Mult iply the amount on l ine 3 of column D by 9/109

9Mult iply the amount on l ine 3 of column E by 10/110

10

Total (add lines 5 , 6 , 7 , 8 and 9) . Enter the result on l ine 14 of Part B on page 6 [2]. For more information to complete this section, go to our webpage "GST/HST rebate for employees and partners".

GST370 – 27

Personal information ( including the SIN) is col lected for purposes of the administrat ion or enforcement of the Excise Tax Act, Part IX, and related programs and activi t ies including administering tax, rebates, elect ions, audit, compliance, and col lect ion. The information col lected may be used or disclosed for the purposes of other federal acts that provide for the imposit ion and col lect ion of a tax or duty. I t may also be disclosed to other federal, provincial, terr i tor ial or foreign government inst i tut ions to the extent authorized by law. Fai lure to provide this information may result in interest payable, penalt ies or other act ions. Under the Privacy Act, individuals have the r ight to: access their personal information, request correction, or f i le a complaint to the Privacy Commissioner of Canada regarding the handling of the individual 's personal information. Refer to Personal Information Bank CRA PPU 241 on Info Source at canada.ca/cra-info-source .