Embed Size (px)

Citation preview

Employee Stock Ownership Plans2021

2

Last 17 years – senior East Coast partner of Menke &

Associates, focusing on ownership transitions through

ESOPs. Assisted over 250 companies in designing, adopting

and selling shares to new ESOPs.

Previously 14 years as director of mergers & acquisitions

investment banking for Morgan Stanley and Salomon Smith

Barney.

Previously two year as a research process engineer focusing

on chemical plant scale ups at the Rohm & Haas.

Chemical Engineering from the University of Delaware.

MBA in Finance from UCLA.

Board member - Boy Scouts of America, Del-Mar-Va Council.

Board member - Delaware American Heart Association.

Board member - Delaware Safety Council

Board member - Global Algae Innovations, Inc.

Board member - NY/NJ Employee Ownership Center.

Board member - St Hubert High School for Girls, Philadelphia.

ESOP speaker - ESOP Association, NCEO & CPA Academy.

Managing Director, Investment Banking, Menke & Associates, Inc.

Presenter - Phillip DeDominicis

Chesapeake City, MD(410) [email protected]

3

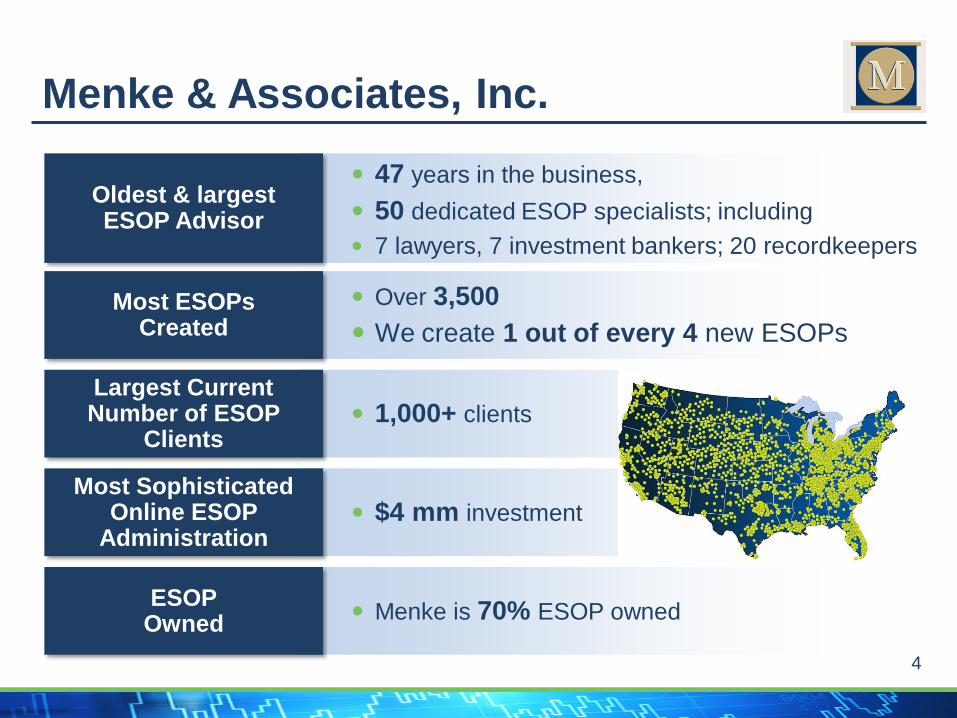

The largest ESOP advisor in the United States

Menke & Associates, Inc.

Chicago

Atlanta

Oakland

Wilmington, DE

Los Angeles

Chesapeake City, MD

Las Vegas

Naples

BurlingameCharlottesville, VA

Aiken, SC

Green Bay

4

Menke & Associates, Inc.

Oldest & largest ESOP Advisor

47 years in the business,

50 dedicated ESOP specialists; including

7 lawyers, 7 investment bankers; 20 recordkeepers

Most ESOPs Created

Over 3,500

We create 1 out of every 4 new ESOPs

Largest Current Number of ESOP

Clients 1,000+ clients

Most Sophisticated Online ESOP

Administration $4 mm investment

ESOP Owned

Menke is 70% ESOP owned

Introduction

6

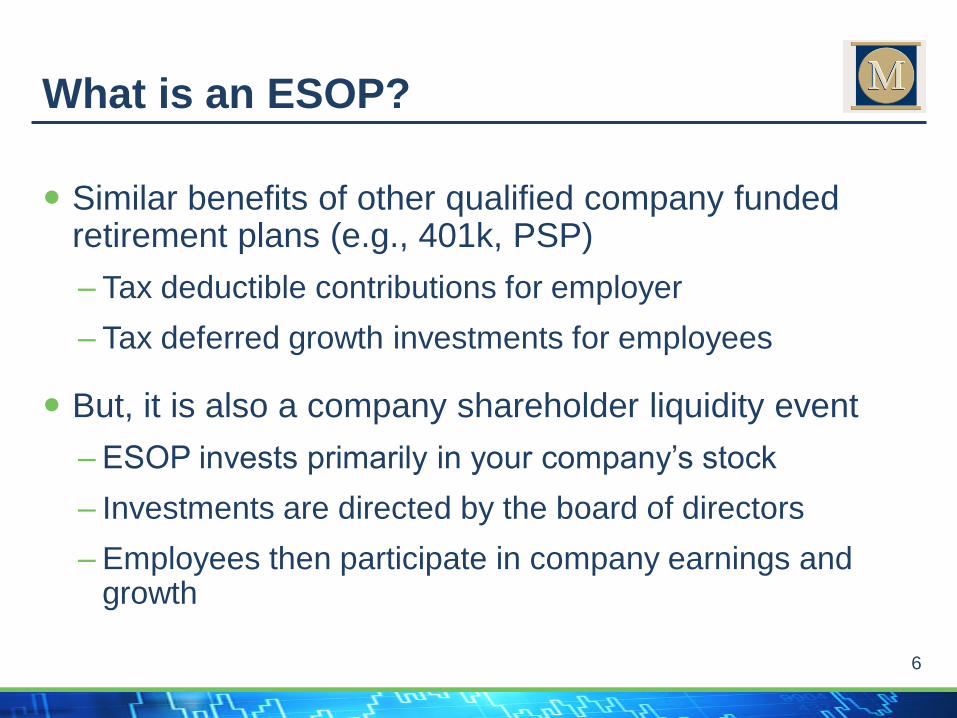

Similar benefits of other qualified company funded retirement plans (e.g., 401k, PSP)

– Tax deductible contributions for employer

– Tax deferred growth investments for employees

But, it is also a company shareholder liquidity event

– ESOP invests primarily in your company’s stock

– Investments are directed by the board of directors

– Employees then participate in company earnings and growth

What is an ESOP?

7

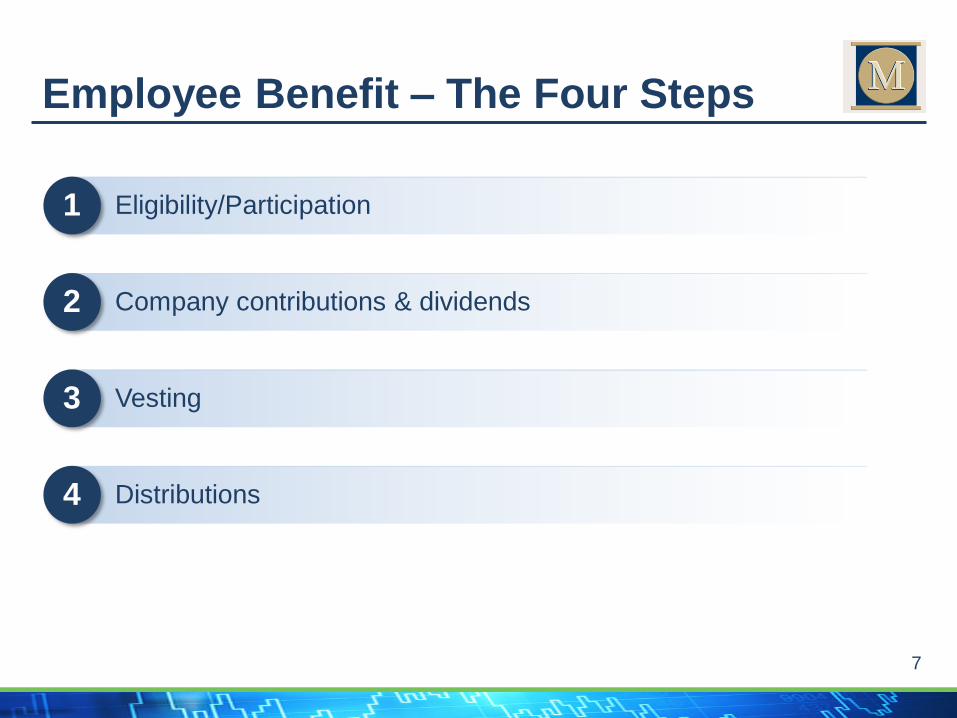

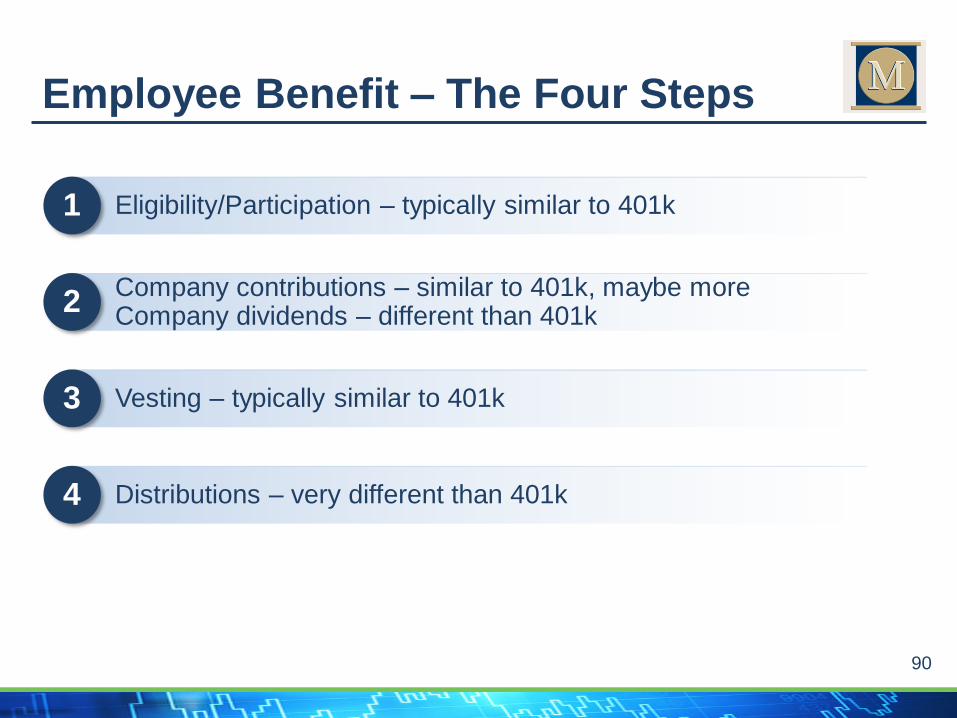

Employee Benefit – The Four Steps

Distributions4

Eligibility/Participation1

Vesting3

Company contributions & dividends2

8

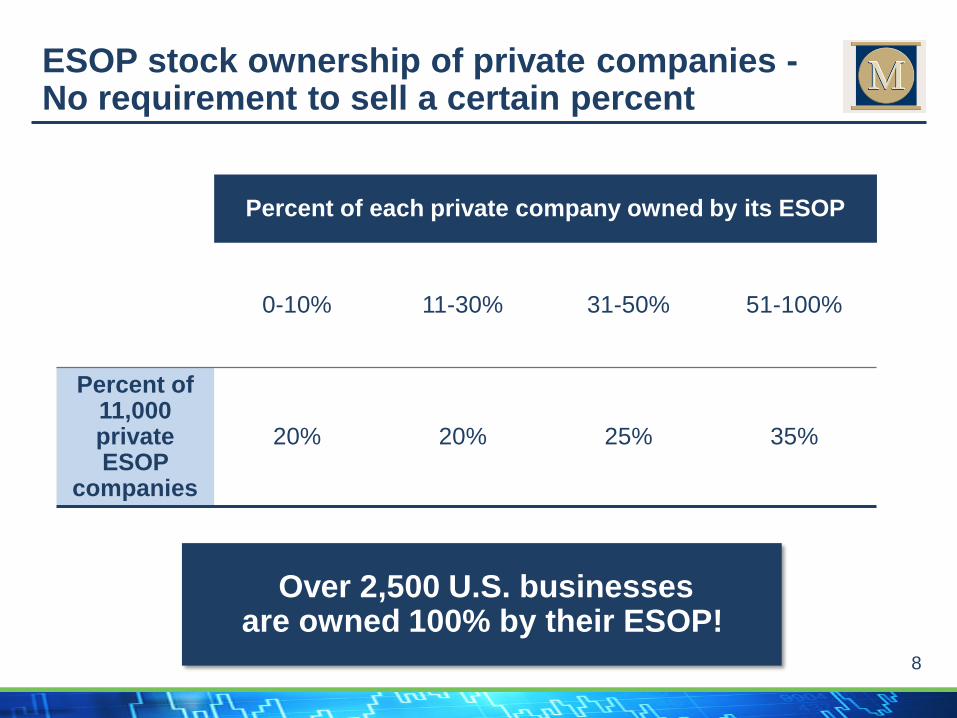

ESOP stock ownership of private companies -No requirement to sell a certain percent

Percent of each private company owned by its ESOP

0-10% 11-30% 31-50% 51-100%

Percent of 11,000 private ESOP

companies

20% 20% 25% 35%

Over 2,500 U.S. businesses are owned 100% by their ESOP!

9

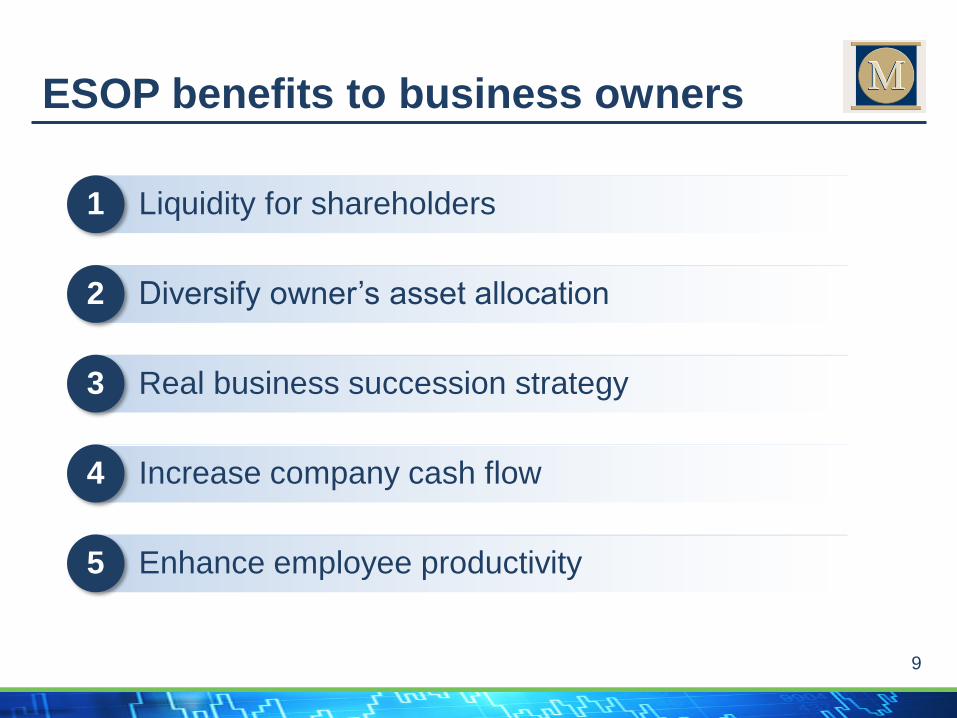

ESOP benefits to business owners

Enhance employee productivity 5

Diversify owner’s asset allocation2

Real business succession strategy3

Increase company cash flow4

Liquidity for shareholders1

10

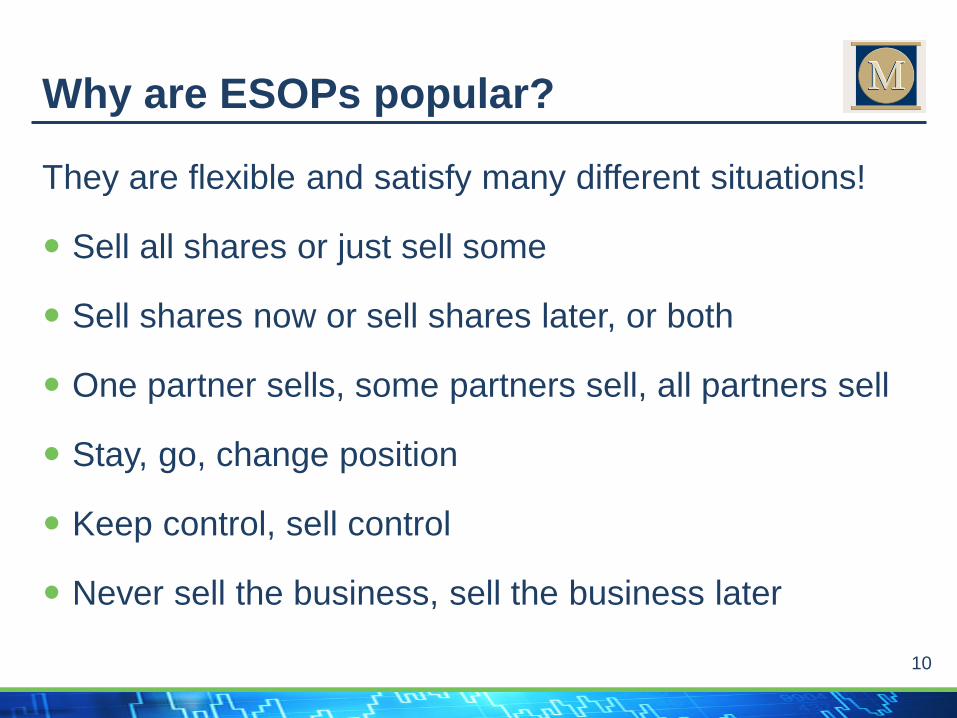

They are flexible and satisfy many different situations!

Sell all shares or just sell some

Sell shares now or sell shares later, or both

One partner sells, some partners sell, all partners sell

Stay, go, change position

Keep control, sell control

Never sell the business, sell the business later

Why are ESOPs popular?

11

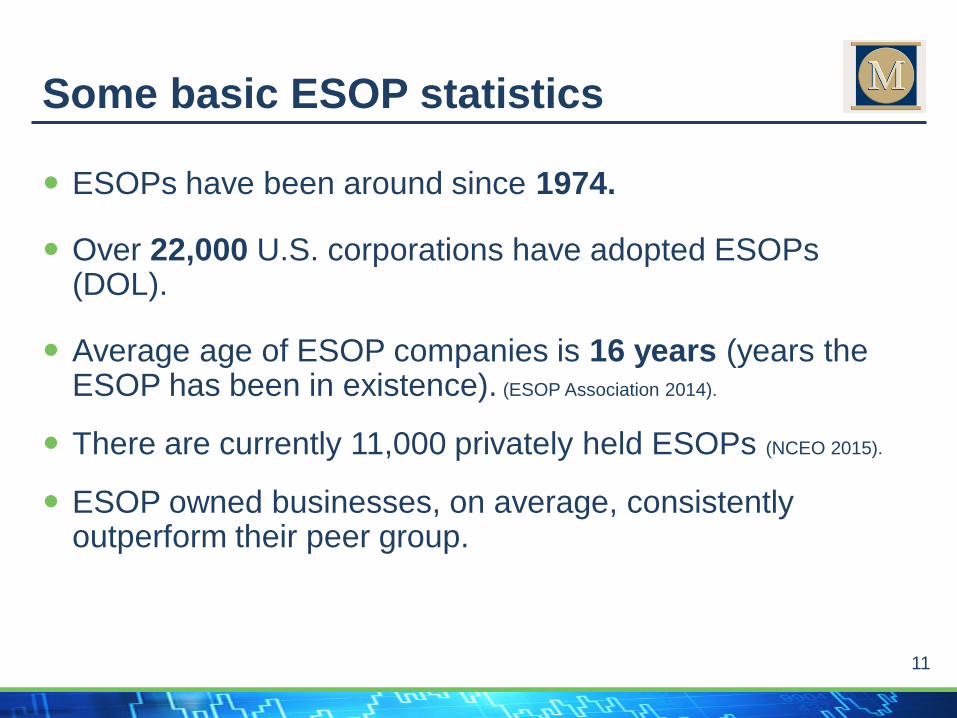

ESOPs have been around since 1974.

Over 22,000 U.S. corporations have adopted ESOPs (DOL).

Average age of ESOP companies is 16 years (years the ESOP has been in existence). (ESOP Association 2014).

There are currently 11,000 privately held ESOPs (NCEO 2015).

ESOP owned businesses, on average, consistently outperform their peer group.

Some basic ESOP statistics

Polling Question #1

13

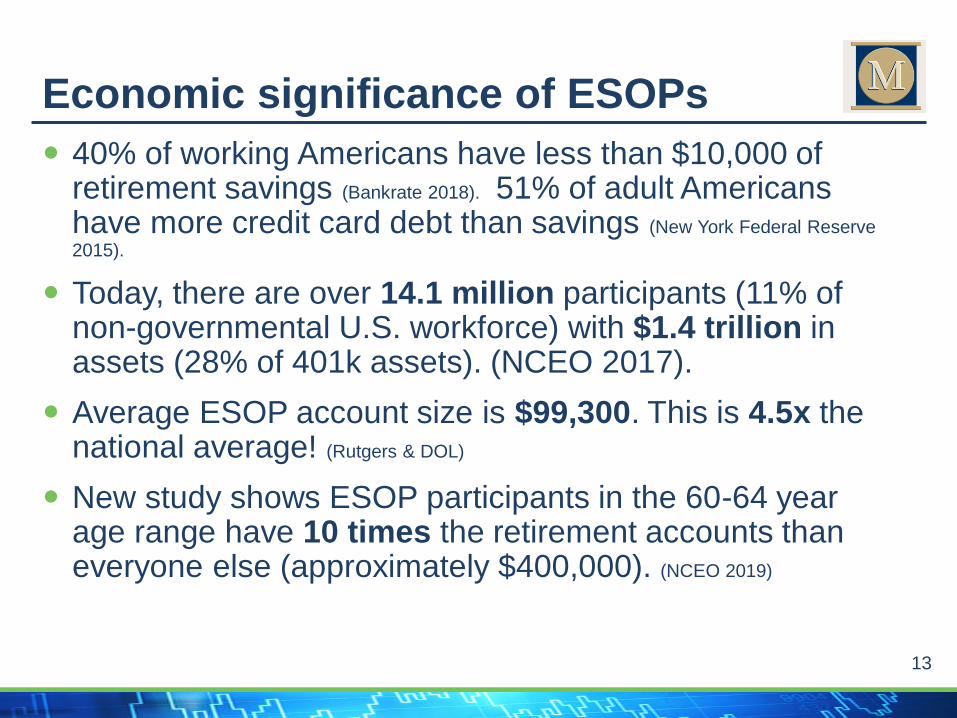

40% of working Americans have less than $10,000 of retirement savings (Bankrate 2018). 51% of adult Americans have more credit card debt than savings (New York Federal Reserve

2015).

Today, there are over 14.1 million participants (11% of non-governmental U.S. workforce) with $1.4 trillion in assets (28% of 401k assets). (NCEO 2017).

Average ESOP account size is $99,300. This is 4.5x the national average! (Rutgers & DOL)

New study shows ESOP participants in the 60-64 year age range have 10 times the retirement accounts than everyone else (approximately $400,000). (NCEO 2019)

Economic significance of ESOPs

14

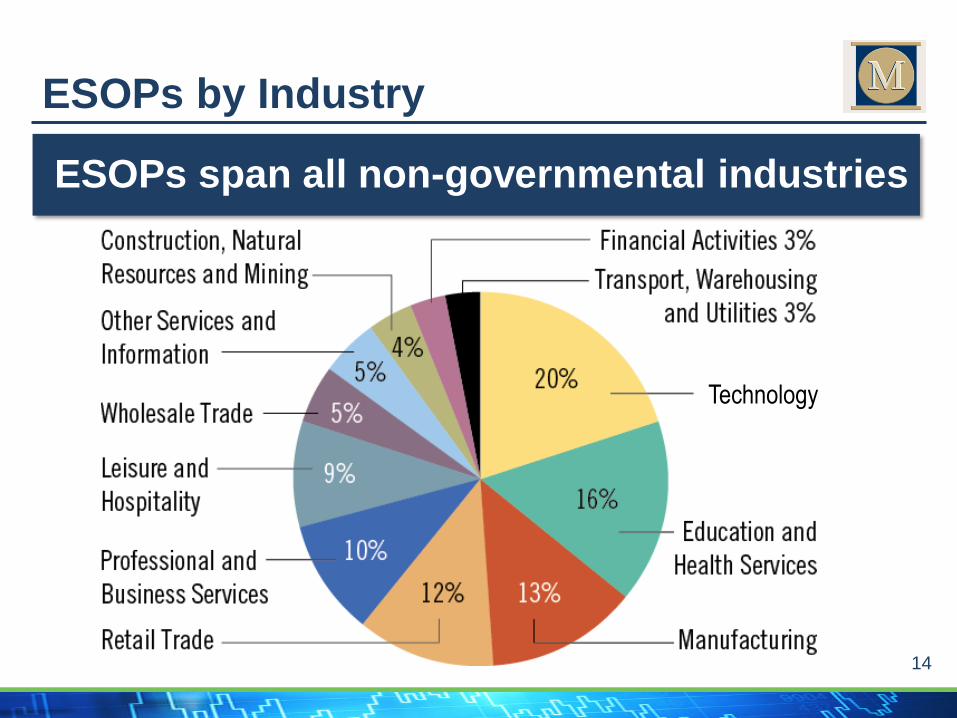

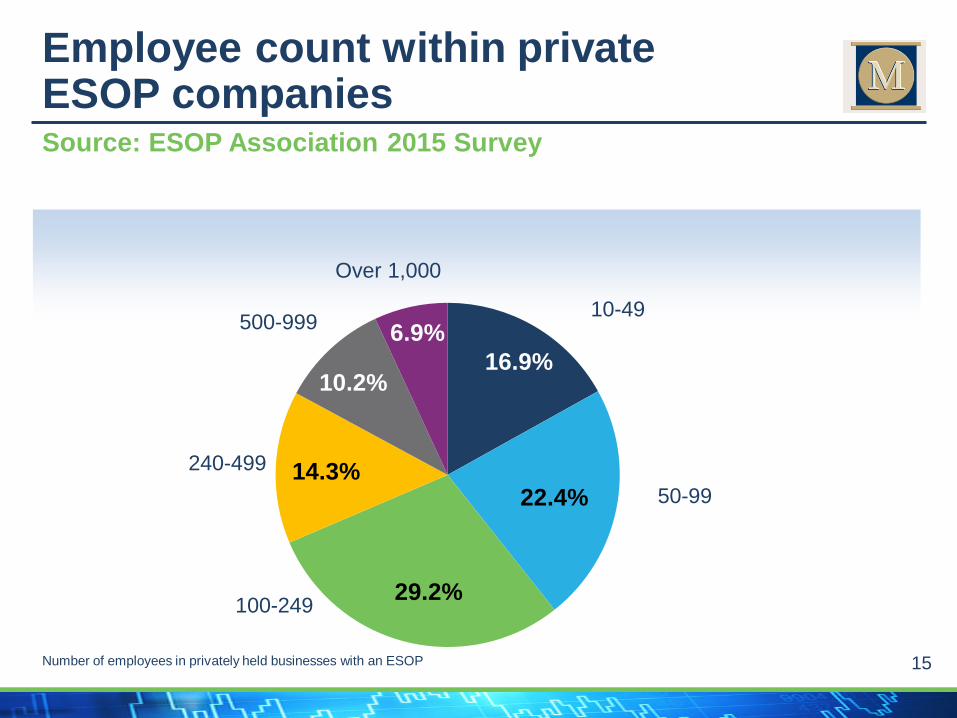

ESOPs by Industry

ESOPs span all non-governmental industries

Technology

15

16.9%

22.4%

29.2%

14.3%

10.2%

6.9%

Number of employees in privately held businesses with an ESOP

Source: ESOP Association 2015 Survey

Employee count within private ESOP companies

50-99

10-49

Over 1,000

500-999

240-499

100-249

16

ESOPs create better companies!

Basic ESOP Structures

18

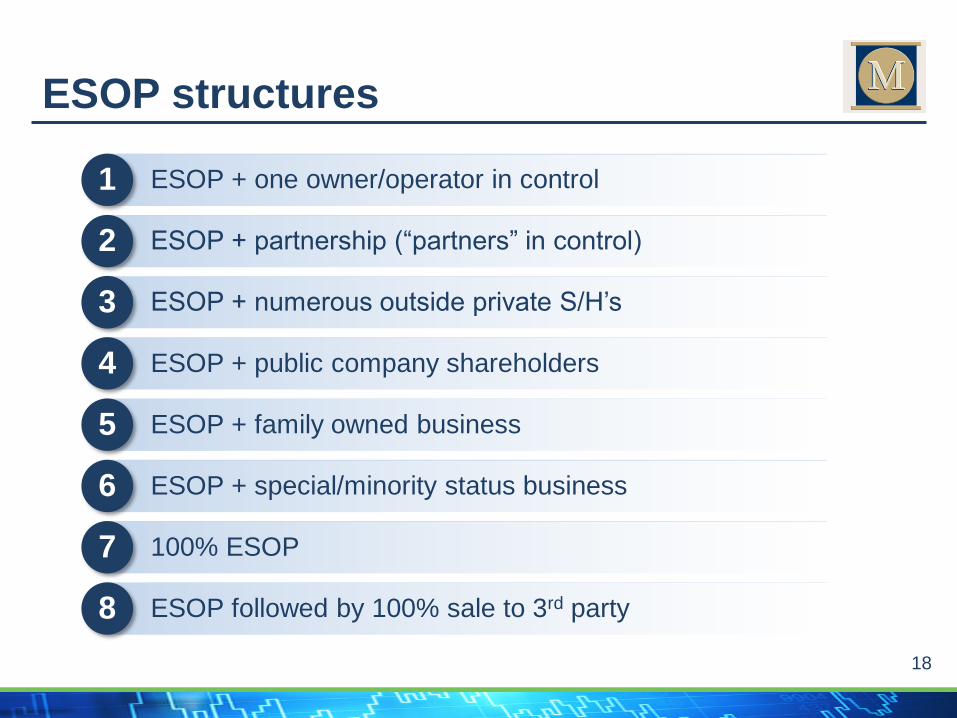

ESOP structures

ESOP + family owned business5

ESOP + partnership (“partners” in control)2

ESOP + numerous outside private S/H’s3

ESOP + public company shareholders4

ESOP + one owner/operator in control1

ESOP + special/minority status business6

100% ESOP7

ESOP followed by 100% sale to 3rd party8

19

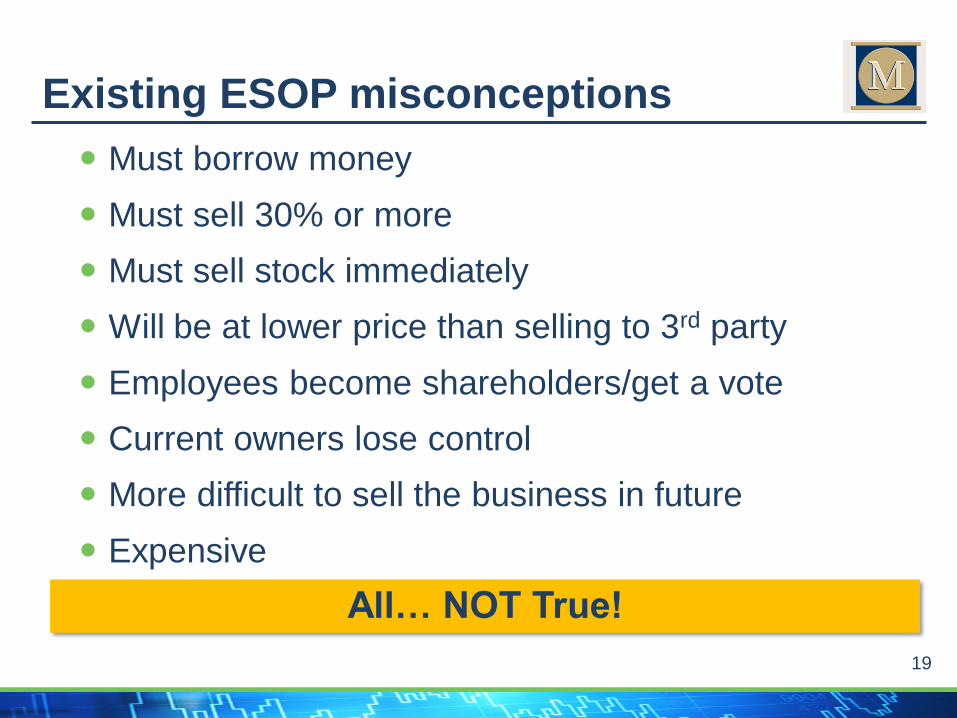

Must borrow money

Must sell 30% or more

Must sell stock immediately

Will be at lower price than selling to 3rd party

Employees become shareholders/get a vote

Current owners lose control

More difficult to sell the business in future

Expensive

Existing ESOP misconceptions

All… NOT True!

20

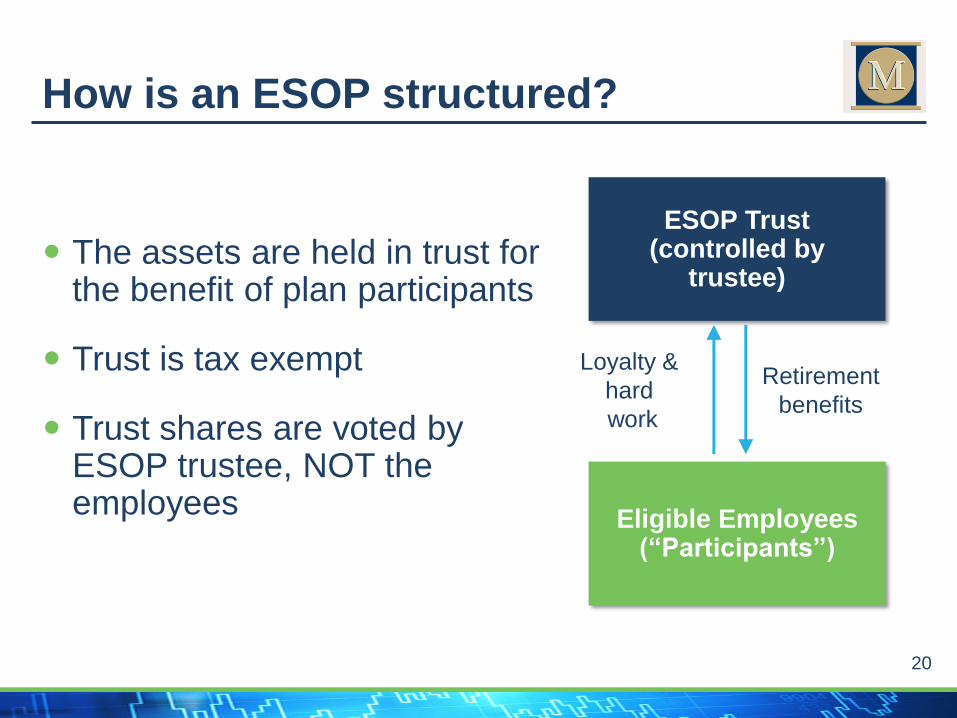

The assets are held in trust for the benefit of plan participants

Trust is tax exempt

Trust shares are voted by ESOP trustee, NOT the employees

How is an ESOP structured?

ESOP Trust(controlled by

trustee)

Eligible Employees(“Participants”)

Loyalty &

hard

work

Retirement

benefits

21

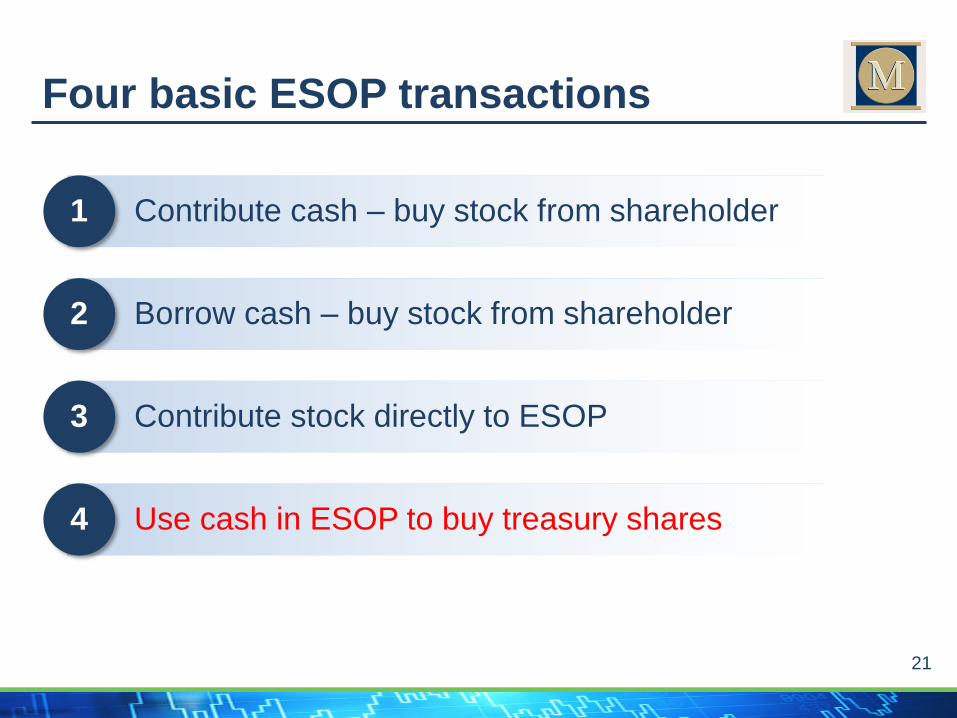

Four basic ESOP transactions

Borrow cash – buy stock from shareholder2

Contribute stock directly to ESOP3

Use cash in ESOP to buy treasury shares4

Contribute cash – buy stock from shareholder1

Polling Question #2

23

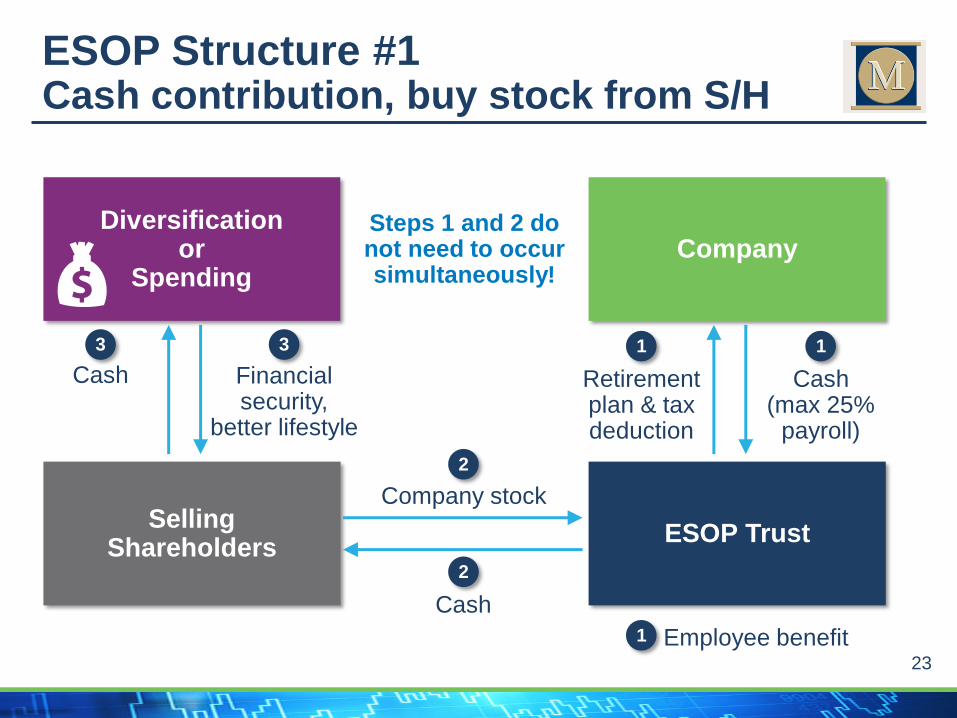

ESOP Structure #1Cash contribution, buy stock from S/H

Company

ESOP Trust

Retirement plan & tax deduction

Cash (max 25%

payroll)

Diversificationor

Spending

SellingShareholders

Steps 1 and 2 do not need to occur simultaneously!

Cash

Cash Financial security,

better lifestyle

11

2

33

Company stock

2

1 Employee benefit

24

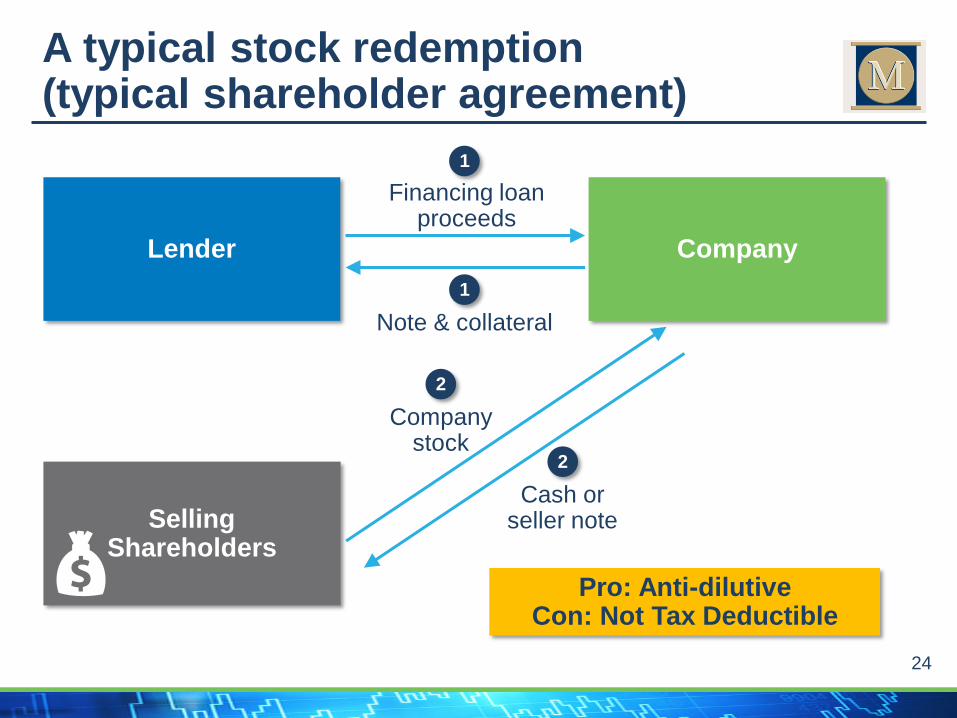

Company

Company stock

Cash or seller note

Lender

SellingShareholders

2

Financing loan proceeds

Note & collateral

1

1

2

A typical stock redemption (typical shareholder agreement)

Pro: Anti-dilutiveCon: Not Tax Deductible

25

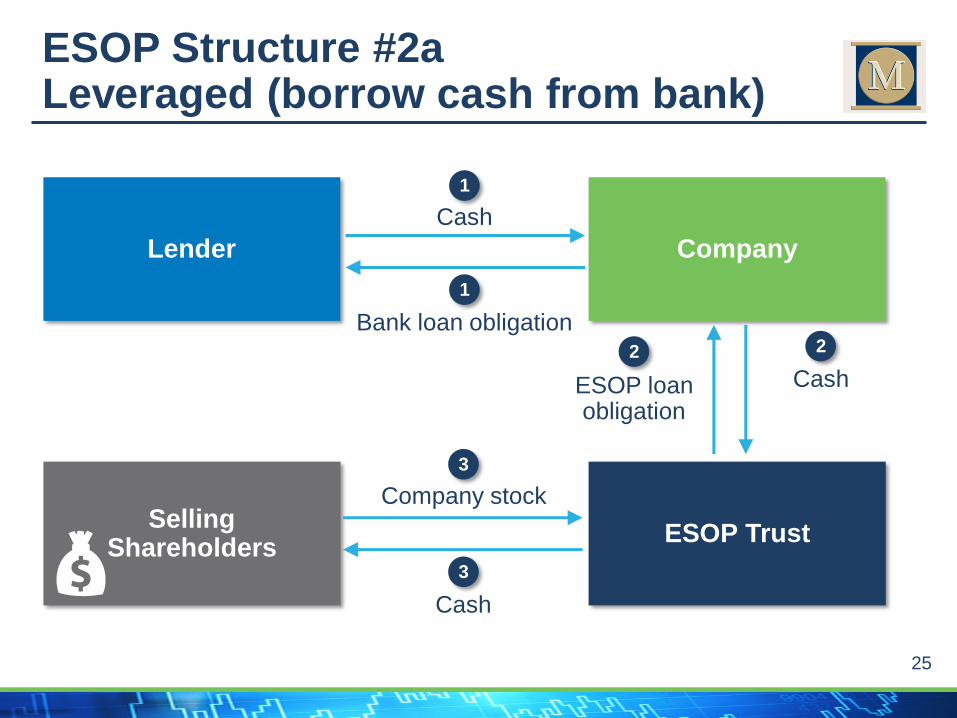

ESOP Structure #2a Leveraged (borrow cash from bank)

Company

ESOP Trust

ESOP loan obligation

Cash

Lender

SellingShareholders

Company stock

Cash

2

3

3

Cash

Bank loan obligation

1

1

2

26

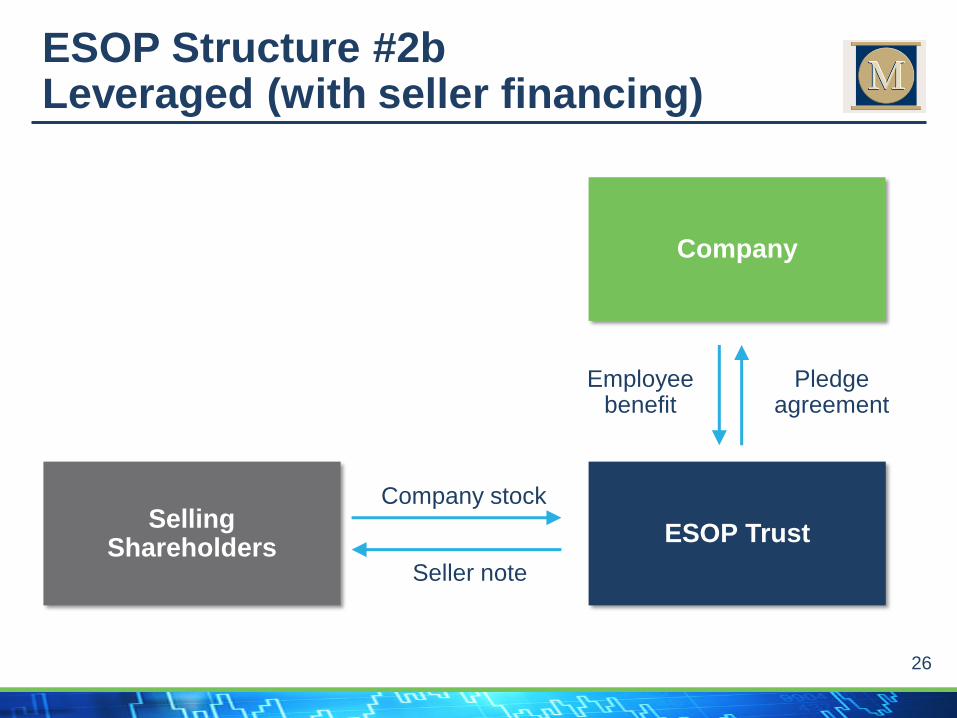

ESOP Structure #2b Leveraged (with seller financing)

Company

ESOP Trust

Employee benefit

Pledge agreement

SellingShareholders

Company stock

Seller note

27

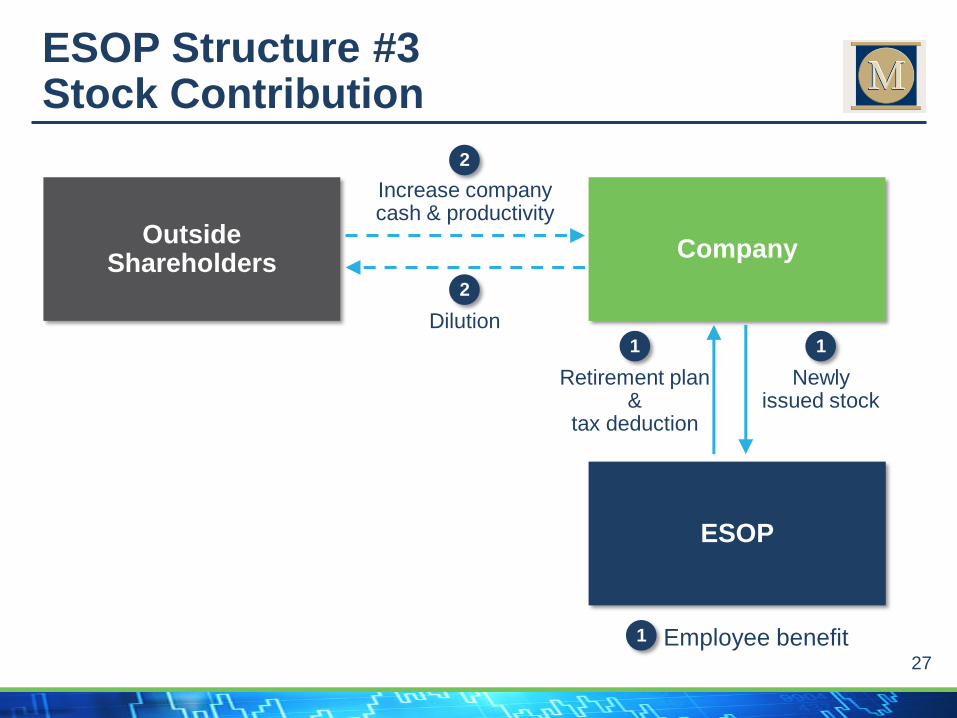

ESOP Structure #3Stock Contribution

Company

ESOP

Retirement plan &

tax deduction

Newly issued stock

OutsideShareholders

1

Increase company cash & productivity

Dilution

2

2

1

1 Employee benefit

Typical ESOP Scenarios

29

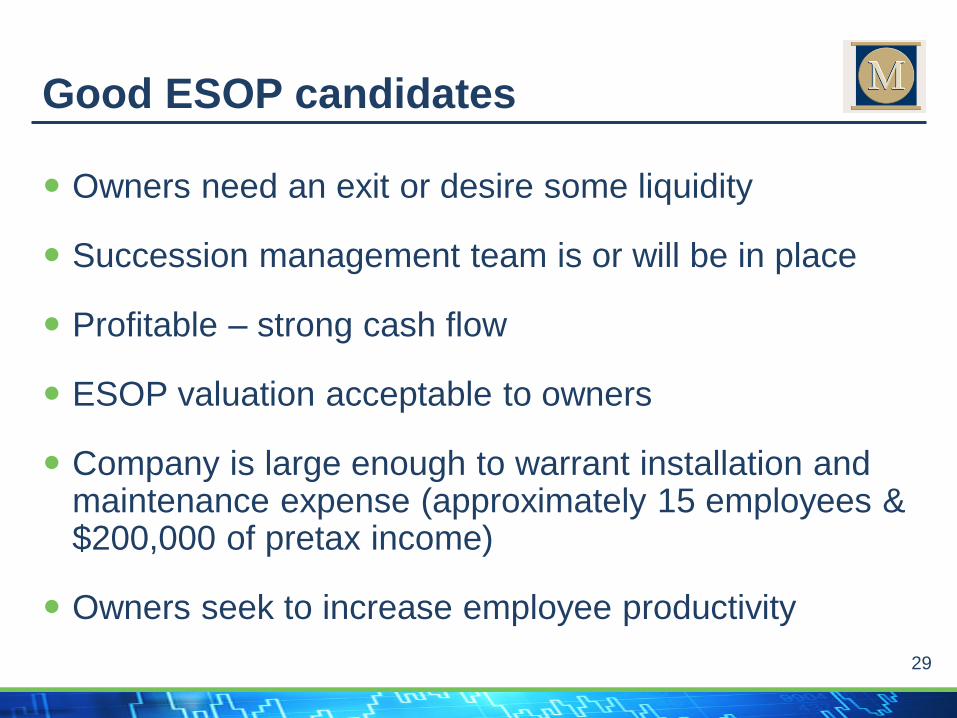

Owners need an exit or desire some liquidity

Succession management team is or will be in place

Profitable – strong cash flow

ESOP valuation acceptable to owners

Company is large enough to warrant installation and maintenance expense (approximately 15 employees & $200,000 of pretax income)

Owners seek to increase employee productivity

Good ESOP candidates

30

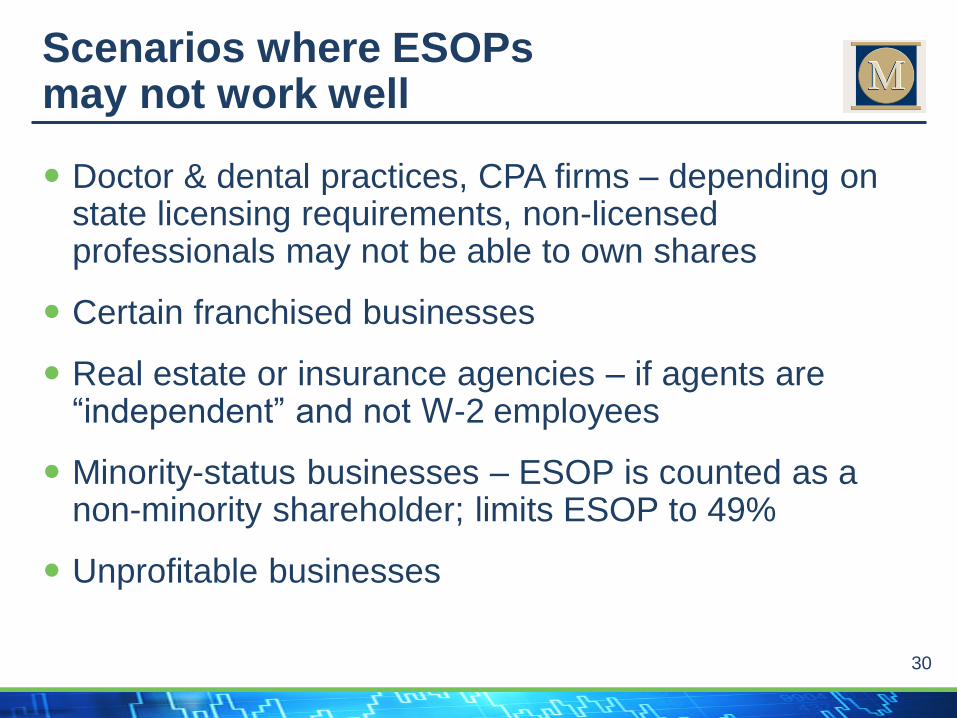

Doctor & dental practices, CPA firms – depending on state licensing requirements, non-licensed professionals may not be able to own shares

Certain franchised businesses

Real estate or insurance agencies – if agents are “independent” and not W-2 employees

Minority-status businesses – ESOP is counted as a non-minority shareholder; limits ESOP to 49%

Unprofitable businesses

Scenarios where ESOPs may not work well

31

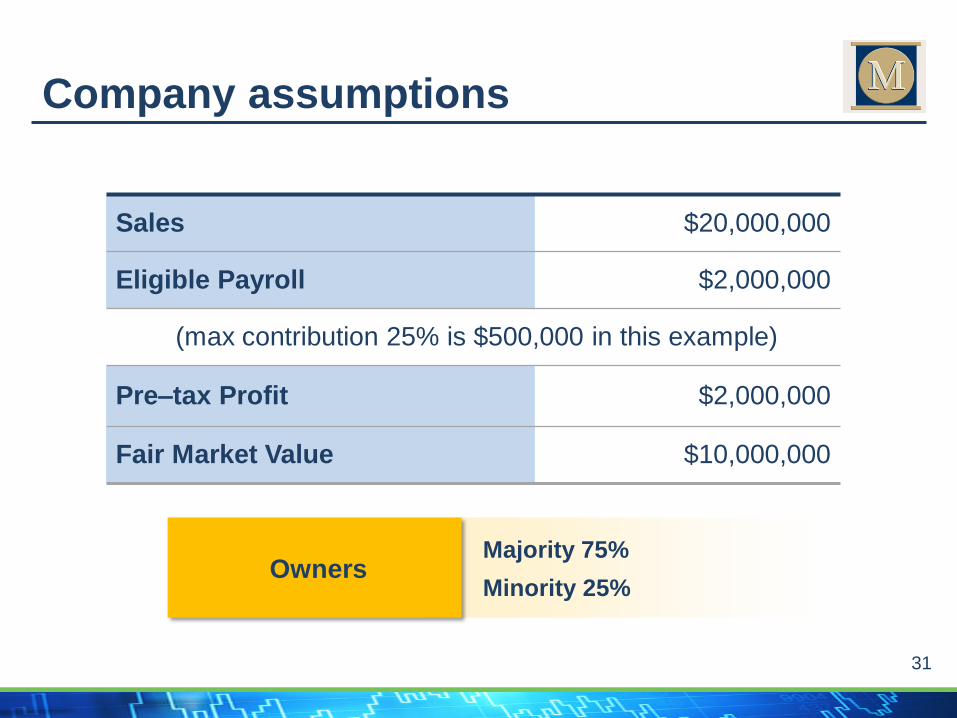

Owners

Company assumptions

Sales $20,000,000

Eligible Payroll $2,000,000

(max contribution 25% is $500,000 in this example)

Pre–tax Profit $2,000,000

Fair Market Value $10,000,000

Majority 75%

Minority 25%

32

Shareholder not ready to sell any stock but wants to create a tax deduction for this year and next year

Reasons for doing this include:

– (1) not ready to diversify

– (2) believe upside in stock price is great

– (3) want to accumulate enough funds to reach 30% threshold for §1042 rollover election

Objective #1

33

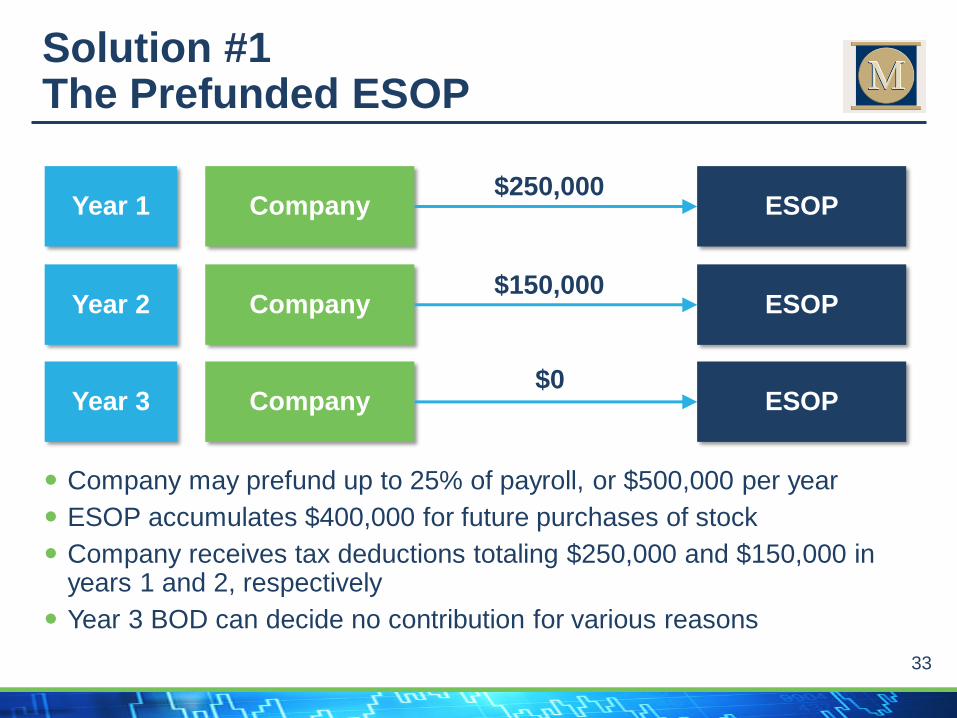

Company may prefund up to 25% of payroll, or $500,000 per year

ESOP accumulates $400,000 for future purchases of stock

Company receives tax deductions totaling $250,000 and $150,000 in years 1 and 2, respectively

Year 3 BOD can decide no contribution for various reasons

$250,000

$150,000

$0

Solution #1 The Prefunded ESOP

ESOP

ESOP

ESOP

Company

Company

Company

Year 1

Year 2

Year 3

34

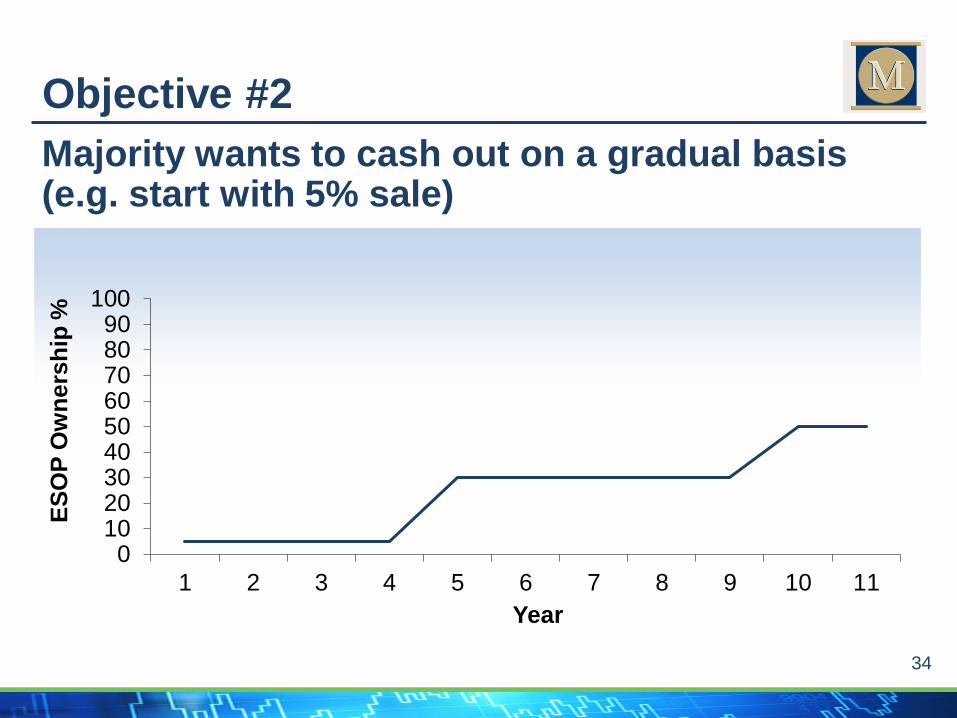

0102030405060708090

100

1 2 3 4 5 6 7 8 9 10 11

ES

OP

Ow

ne

rsh

ip %

Year

Majority wants to cash out on a gradual basis (e.g. start with 5% sale)

Objective #2

35

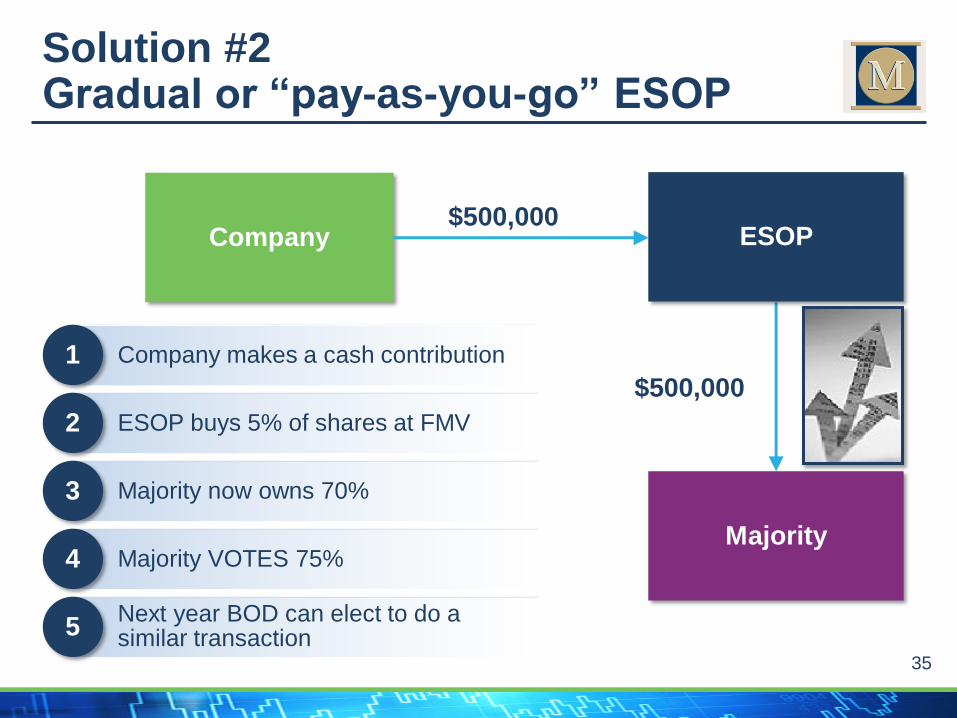

Majority

Company

$500,000

$500,000ESOP

Solution #2Gradual or “pay-as-you-go” ESOP

Majority VOTES 75%4

Majority now owns 70%3

ESOP buys 5% of shares at FMV2

Next year BOD can elect to do a similar transaction5

Company makes a cash contribution1

Polling Question #3

37

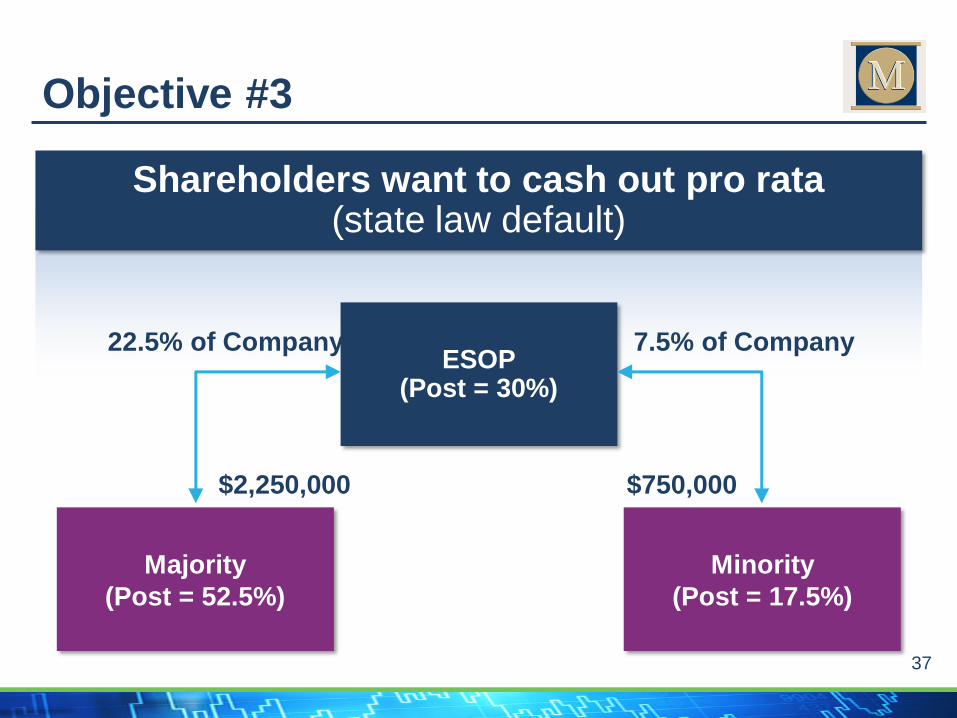

Shareholders want to cash out pro rata(state law default)

Objective #3

7.5% of Company22.5% of CompanyESOP

(Post = 30%)

Minority

(Post = 17.5%)

Majority

(Post = 52.5%)

$2,250,000 $750,000

38

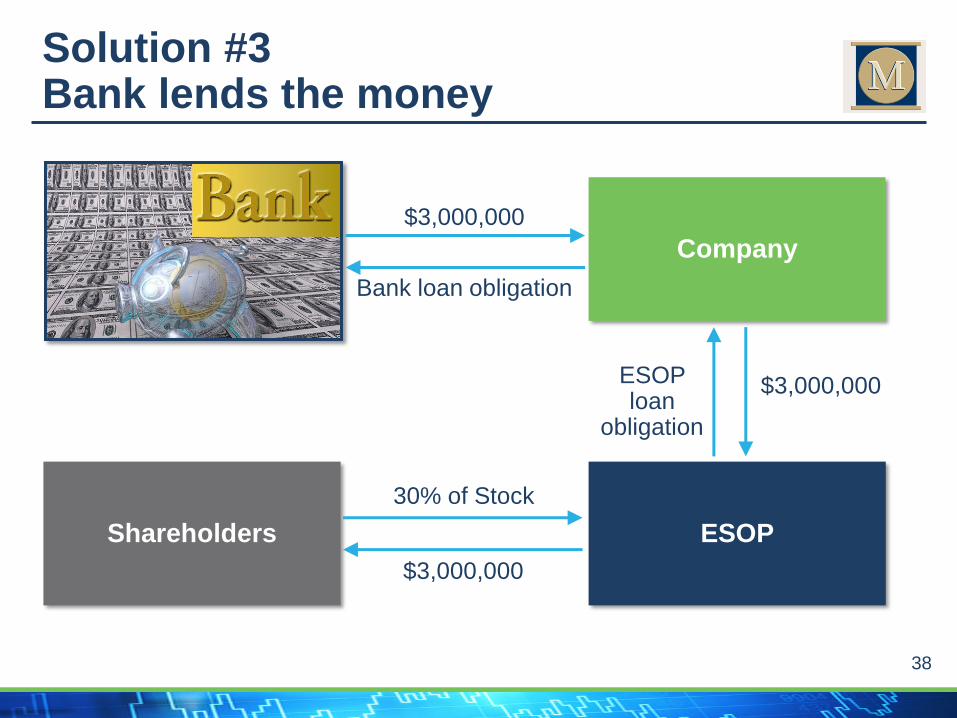

Company

ESOP

ESOP loan

obligation

$3,000,000

Shareholders

30% of Stock

$3,000,000

$3,000,000

Bank loan obligation

Solution #3Bank lends the money

39

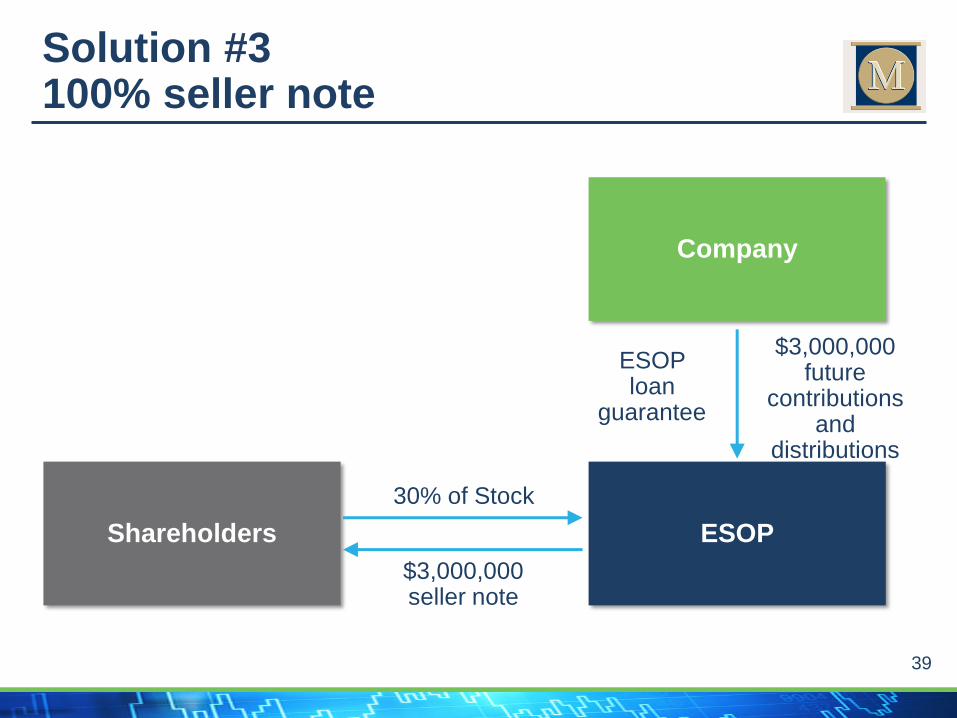

Company

ESOP

ESOP loan

guarantee

$3,000,000 future

contributions and

distributions

Shareholders

30% of Stock

$3,000,000 seller note

Solution #3100% seller note

40

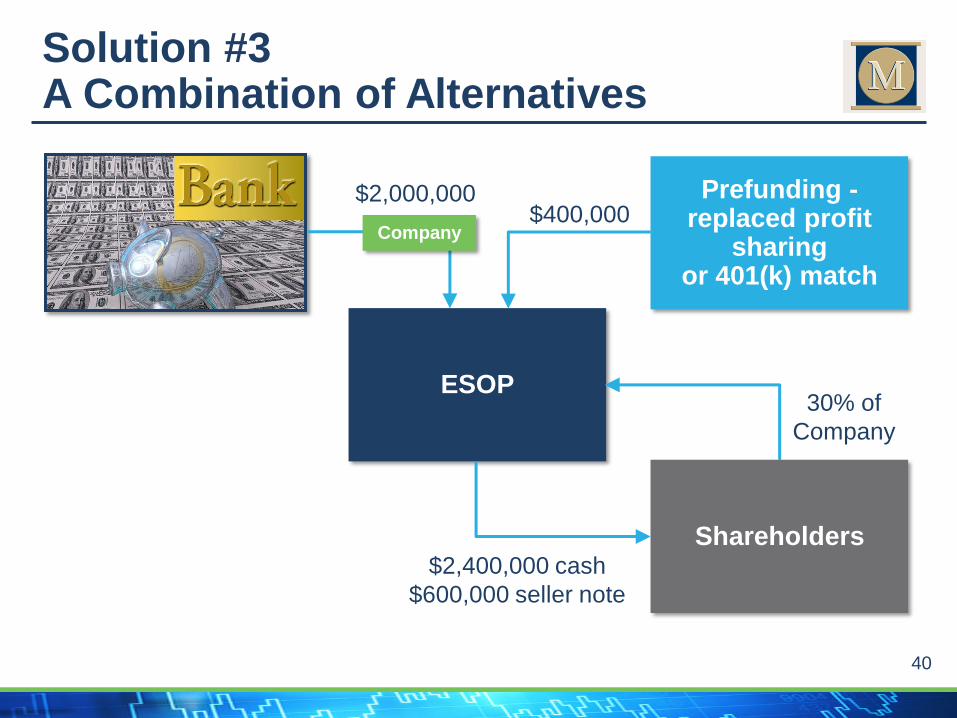

Solution #3 A Combination of Alternatives

ESOP

Shareholders

Prefunding -replaced profit

sharingor 401(k) match

$2,400,000 cash

$600,000 seller note

30% of

Company

$400,000$2,000,000

Company

41

Objective #4

Minority wants to cash out and retire

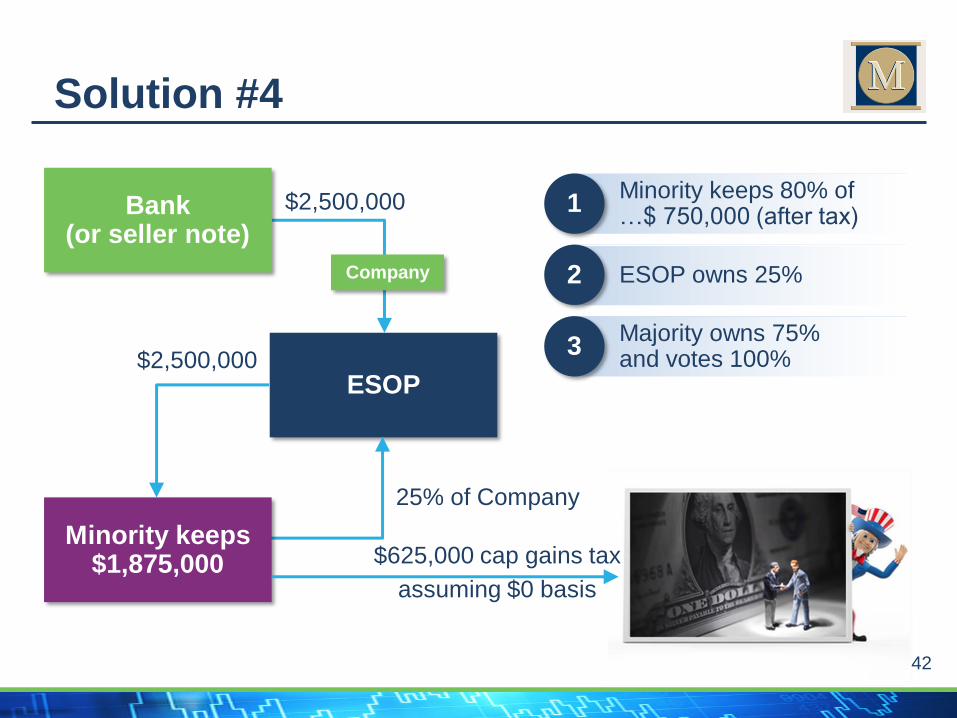

42

$2,500,000

$2,500,000

25% of Company

$625,000 cap gains tax

assuming $0 basis

Solution #4

Majority owns 75%and votes 100%

3

ESOP owns 25%2

Minority keeps 80% of …$ 750,000 (after tax)

1

ESOP

Bank(or seller note)

Minority keeps$1,875,000

Company

43

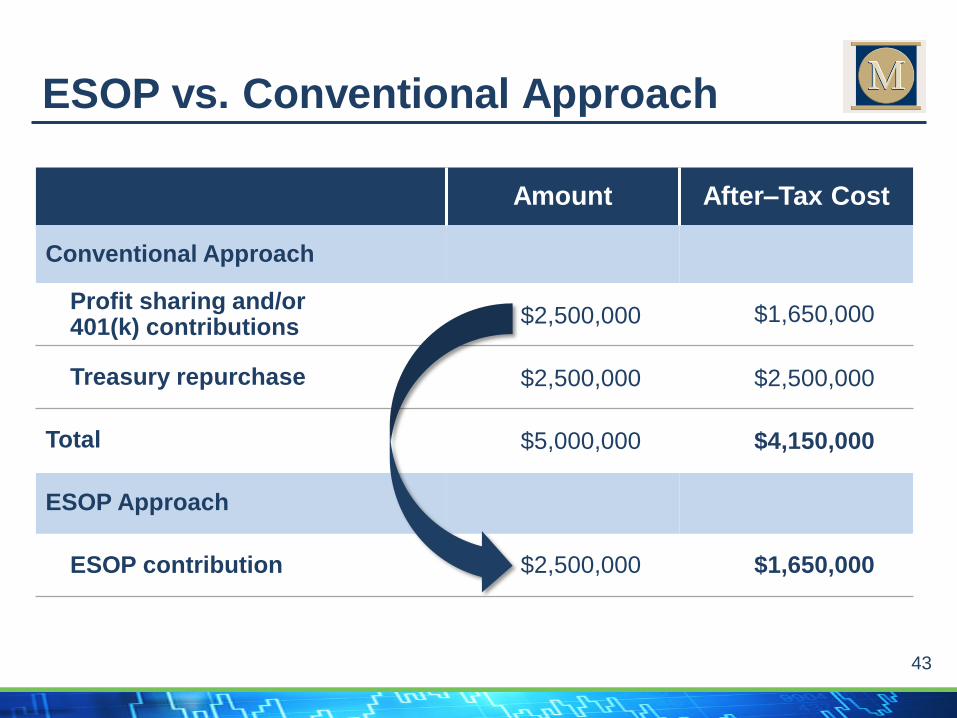

ESOP vs. Conventional Approach

Amount After–Tax Cost

Conventional Approach

Profit sharing and/or401(k) contributions

$2,500,000 $1,650,000

Treasury repurchase $2,500,000 $2,500,000

Total $5,000,000 $4,150,000

ESOP Approach

ESOP contribution $2,500,000 $1,650,000

44

Objective #5

Shareholders want to sell 100% of the company

45

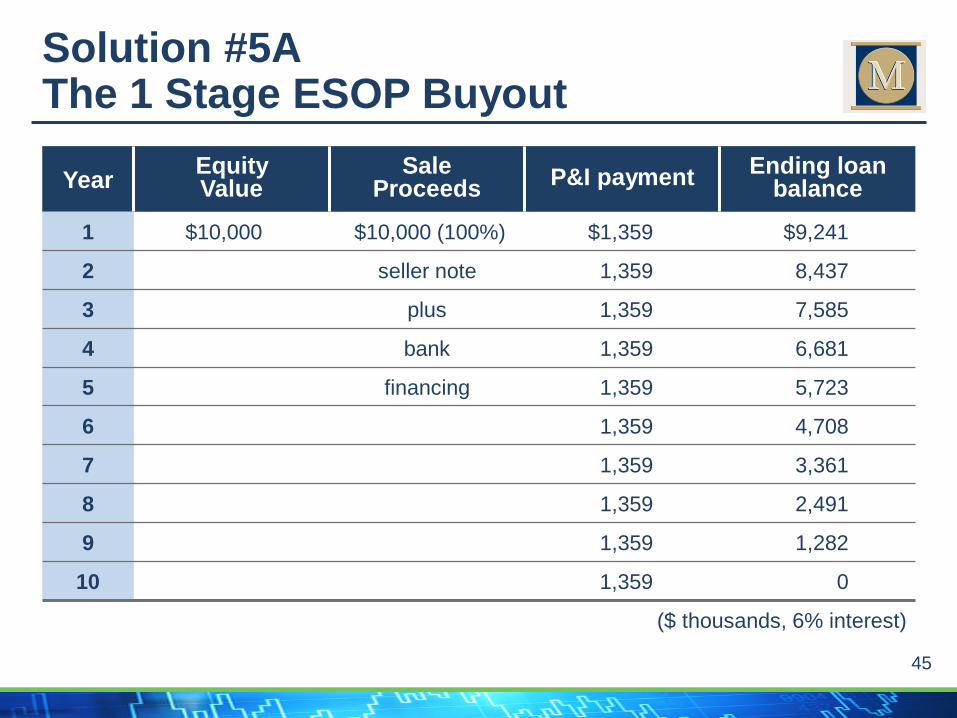

Solution #5A The 1 Stage ESOP Buyout

YearEquityValue

SaleProceeds

P&I paymentEnding loan

balance

1 $10,000 $10,000 (100%) $1,359 $9,241

2 seller note 1,359 8,437

3 plus 1,359 7,585

4 bank 1,359 6,681

5 financing 1,359 5,723

6 1,359 4,708

7 1,359 3,361

8 1,359 2,491

9 1,359 1,282

10 1,359 0

($ thousands, 6% interest)

46

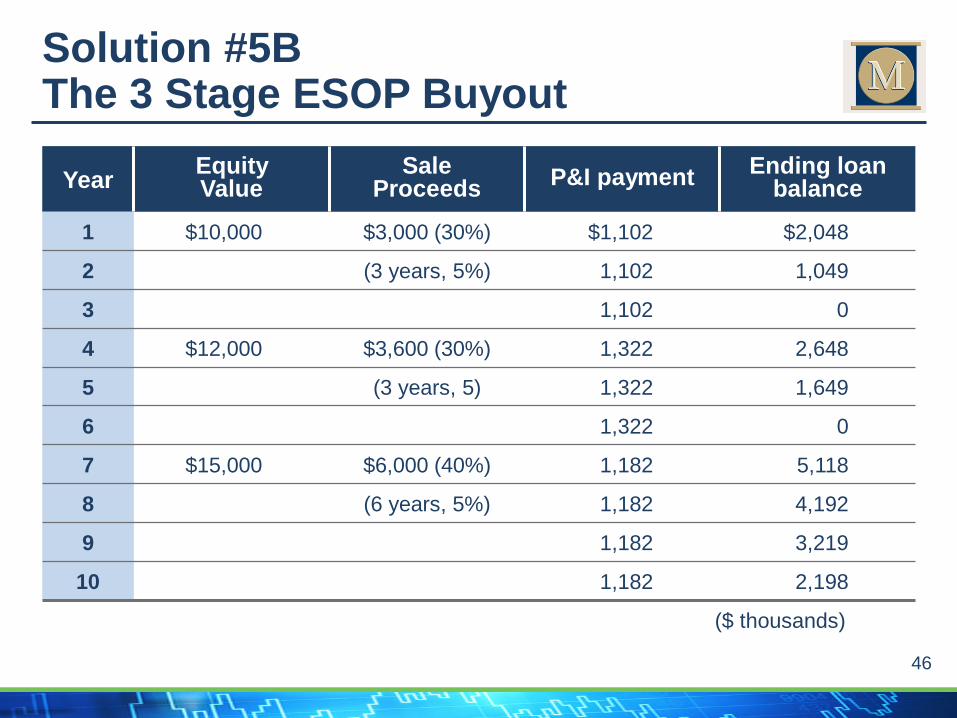

Solution #5B The 3 Stage ESOP Buyout

YearEquityValue

SaleProceeds

P&I paymentEnding loan

balance

1 $10,000 $3,000 (30%) $1,102 $2,048

2 (3 years, 5%) 1,102 1,049

3 1,102 0

4 $12,000 $3,600 (30%) 1,322 2,648

5 (3 years, 5) 1,322 1,649

6 1,322 0

7 $15,000 $6,000 (40%) 1,182 5,118

8 (6 years, 5%) 1,182 4,192

9 1,182 3,219

10 1,182 2,198

($ thousands)

Polling Question #4

48

Create a better incentive plan than the retirement plan or equity plans

the company is already funding

Objective #6

49

Productivity

Cash Compensation High

Low

Low

High

Solution #6 Cash only goes so far

50

Why replace 401(k) match or profit sharing with an ESOP?

– ESOP is a broader based retirement program –matching plans skewed to savers

– Replaces short-term, cash benefit with long-term, stock benefit

– Studies say productivity increases

– By definition, more stable company for employees

Solution #6 “Two Bangs for the Same Buck”

51

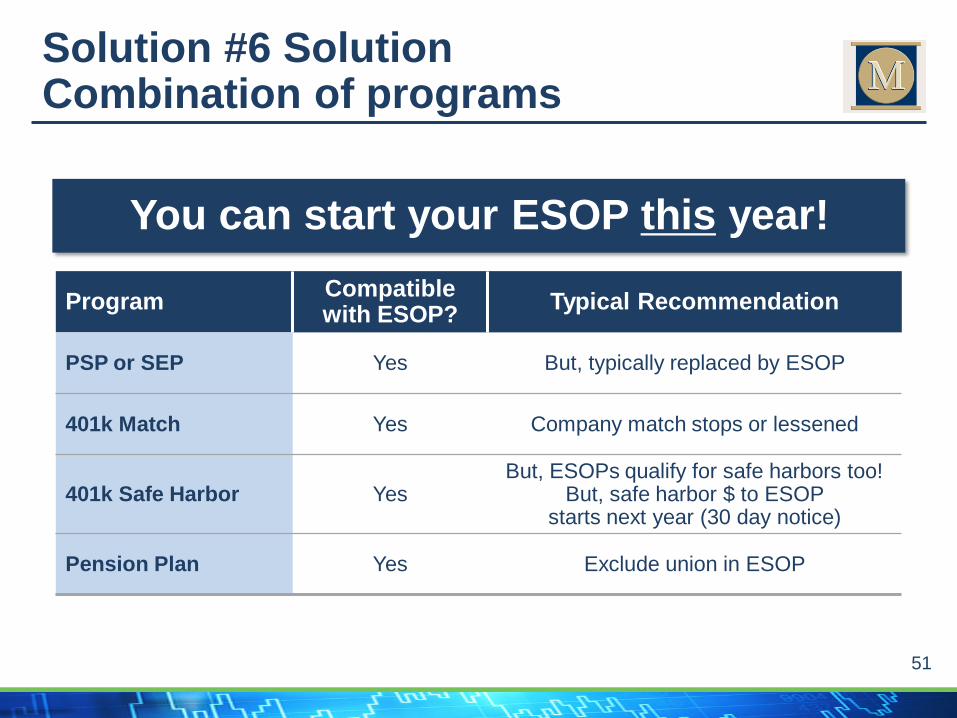

You can start your ESOP this year!

Solution #6 SolutionCombination of programs

ProgramCompatible with ESOP?

Typical Recommendation

PSP or SEP Yes But, typically replaced by ESOP

401k Match Yes Company match stops or lessened

401k Safe Harbor YesBut, ESOPs qualify for safe harbors too!

But, safe harbor $ to ESOP starts next year (30 day notice)

Pension Plan Yes Exclude union in ESOP

52

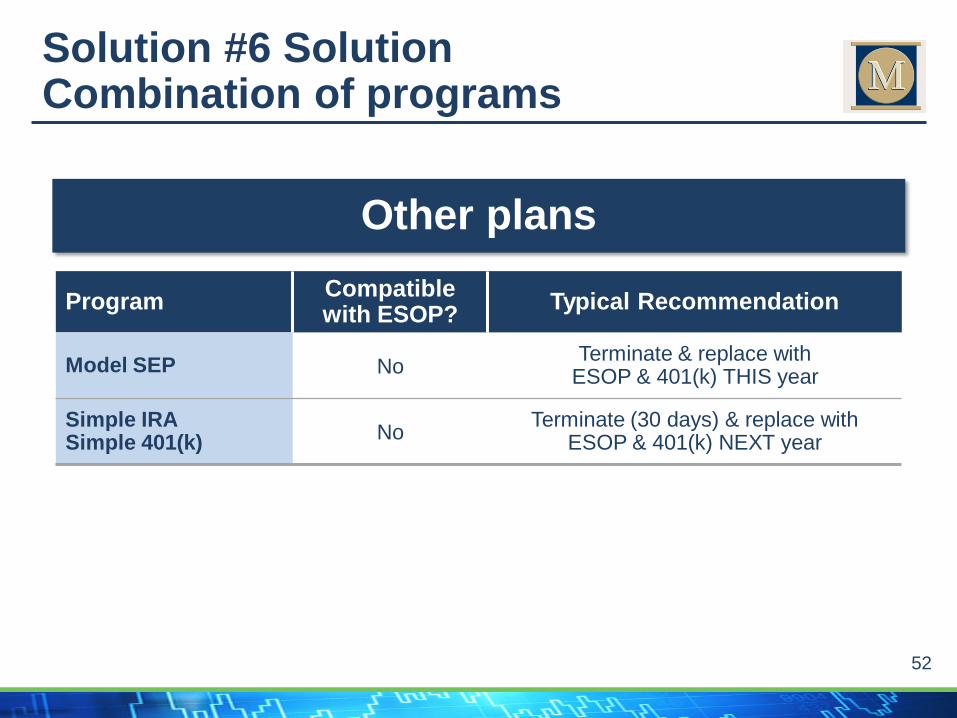

Solution #6 SolutionCombination of programs

Other plans

ProgramCompatible with ESOP?

Typical Recommendation

Model SEP NoTerminate & replace with

ESOP & 401(k) THIS year

Simple IRASimple 401(k)

NoTerminate (30 days) & replace with

ESOP & 401(k) NEXT year

53

MBO – buy shares directly

Sweat equity plans

– Management stock bonus plans

– Phantom stock plans

– Stock options

– Warrants

Solution #6 Other equity plans allowed

54

Objective #7

Raise Capital or Conserve Cash

55

Issue new shares to ESOP

Take tax deduction for fair market value of shares

Company conserves cash by:

– Paying less taxes

– Replacing cash compensation program, like 401k match or profit sharing, with non-cash ESOP

Solution #7The “Cash Flow ESOP”

56

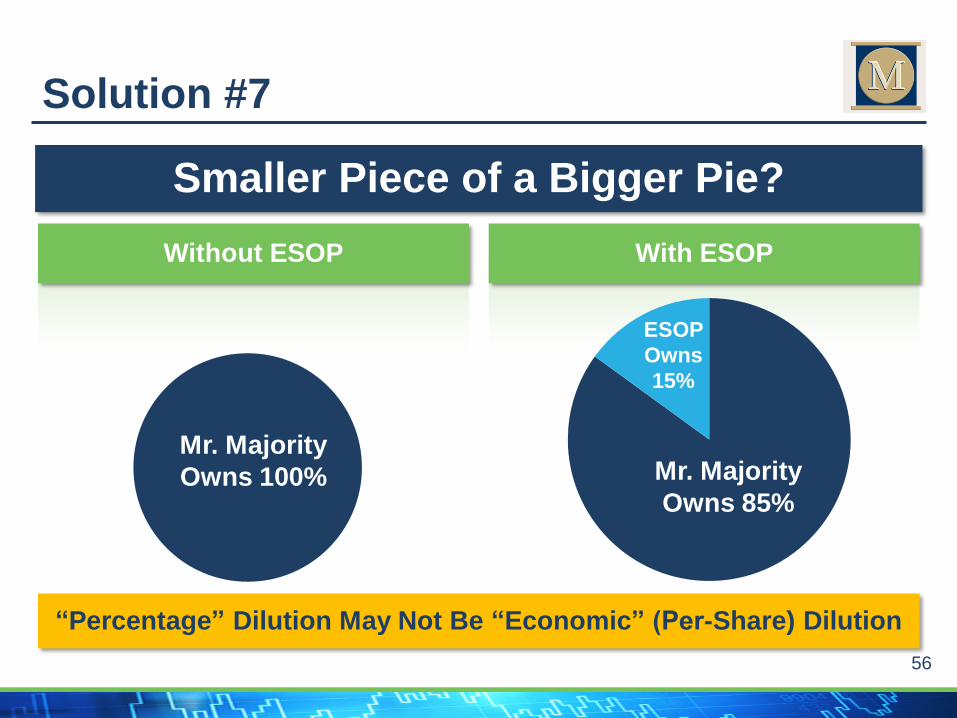

Smaller Piece of a Bigger Pie?

Mr. Majority

Owns 100%

Without ESOP

“Percentage” Dilution May Not Be “Economic” (Per-Share) Dilution

Solution #7

With ESOP

Mr. Majority

Owns 85%

ESOP

Owns

15%

57

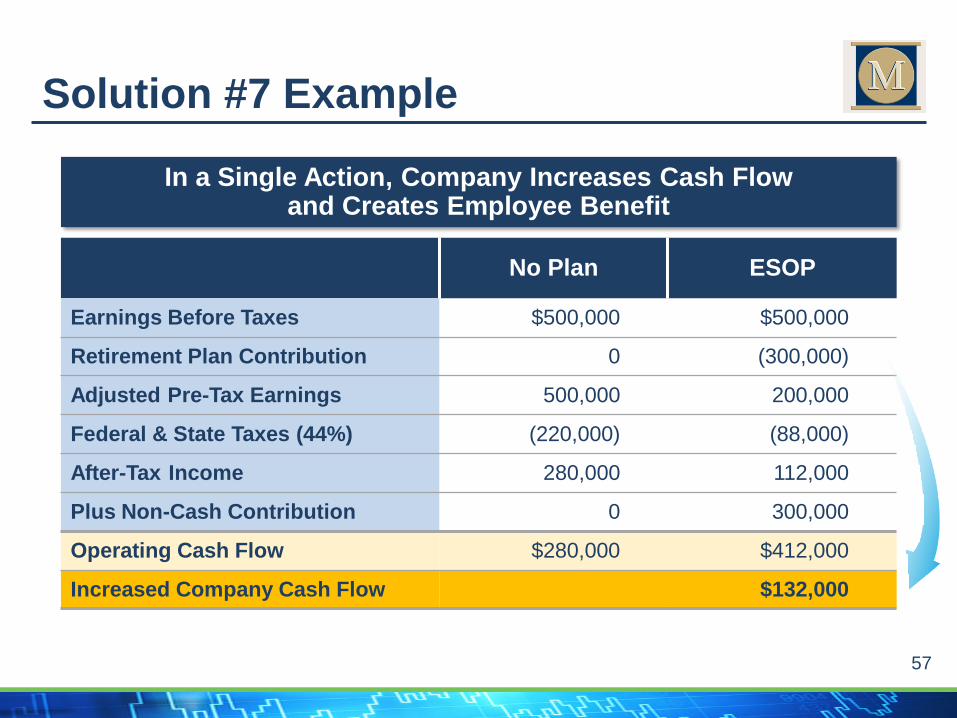

In a Single Action, Company Increases Cash Flow and Creates Employee Benefit

Solution #7 Example

No Plan ESOP

Earnings Before Taxes $500,000 $500,000

Retirement Plan Contribution 0 (300,000)

Adjusted Pre-Tax Earnings 500,000 200,000

Federal & State Taxes (44%) (220,000) (88,000)

After-Tax Income 280,000 112,000

Plus Non-Cash Contribution 0 300,000

Operating Cash Flow $280,000 $412,000

Increased Company Cash Flow $132,000

58

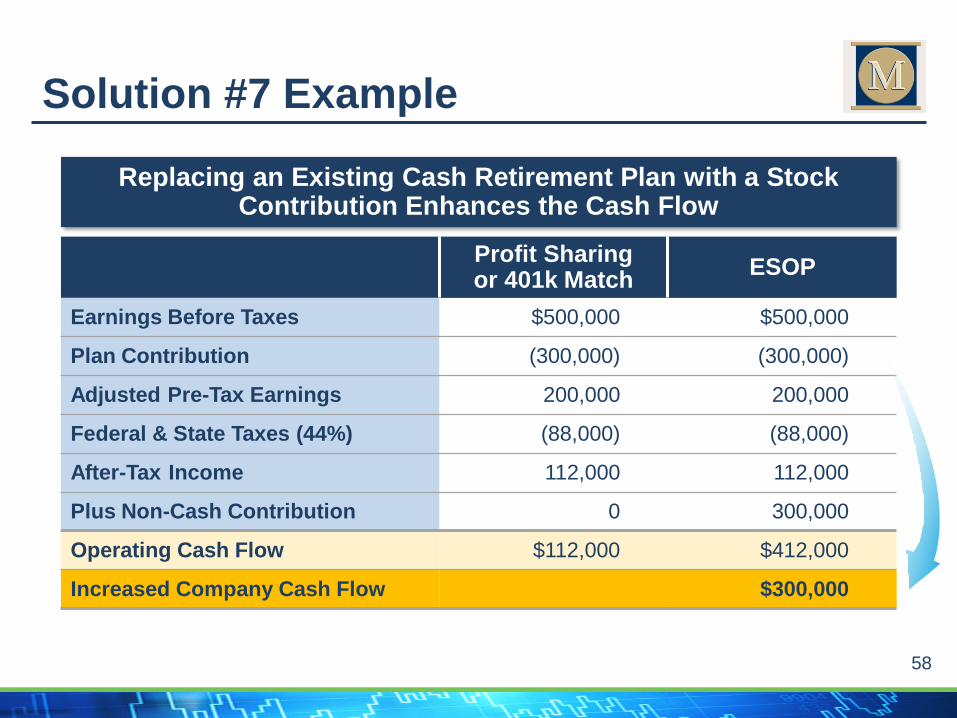

Replacing an Existing Cash Retirement Plan with a Stock Contribution Enhances the Cash Flow

Profit Sharingor 401k Match

ESOP

Earnings Before Taxes $500,000 $500,000

Plan Contribution (300,000) (300,000)

Adjusted Pre-Tax Earnings 200,000 200,000

Federal & State Taxes (44%) (88,000) (88,000)

After-Tax Income 112,000 112,000

Plus Non-Cash Contribution 0 300,000

Operating Cash Flow $112,000 $412,000

Increased Company Cash Flow $300,000

Solution #7 Example

Polling Question #5

S Corporation ESOPs

(Since 1996)

61

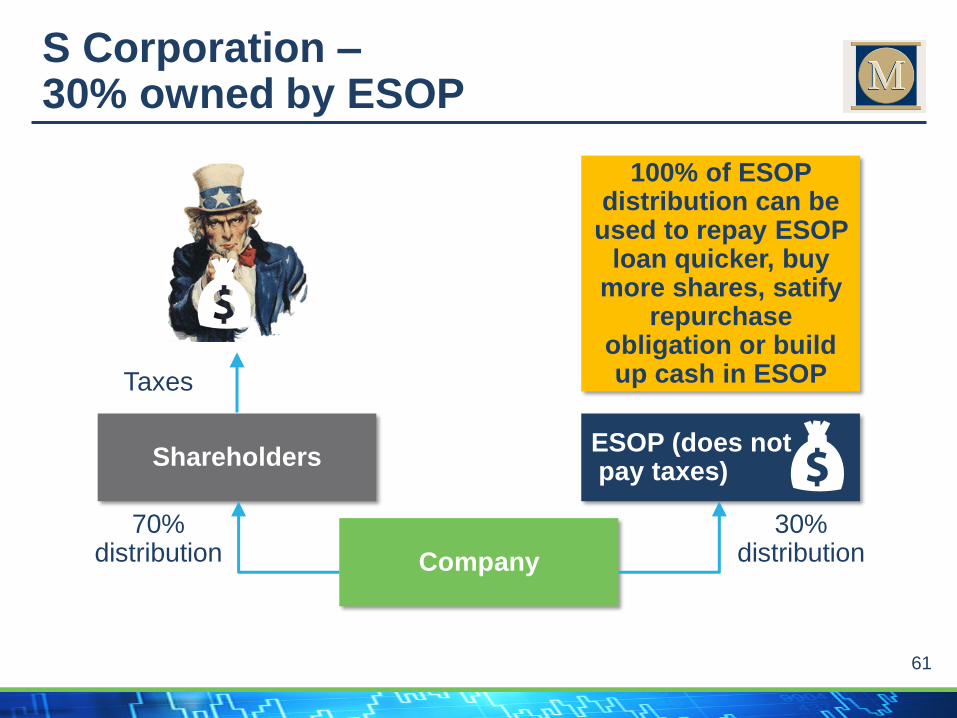

Company

ESOP (does notpay taxes)

Shareholders

30% distribution

Taxes

70% distribution

S Corporation –30% owned by ESOP

100% of ESOP distribution can be

used to repay ESOP loan quicker, buy

more shares, satifyrepurchase

obligation or build up cash in ESOP

62

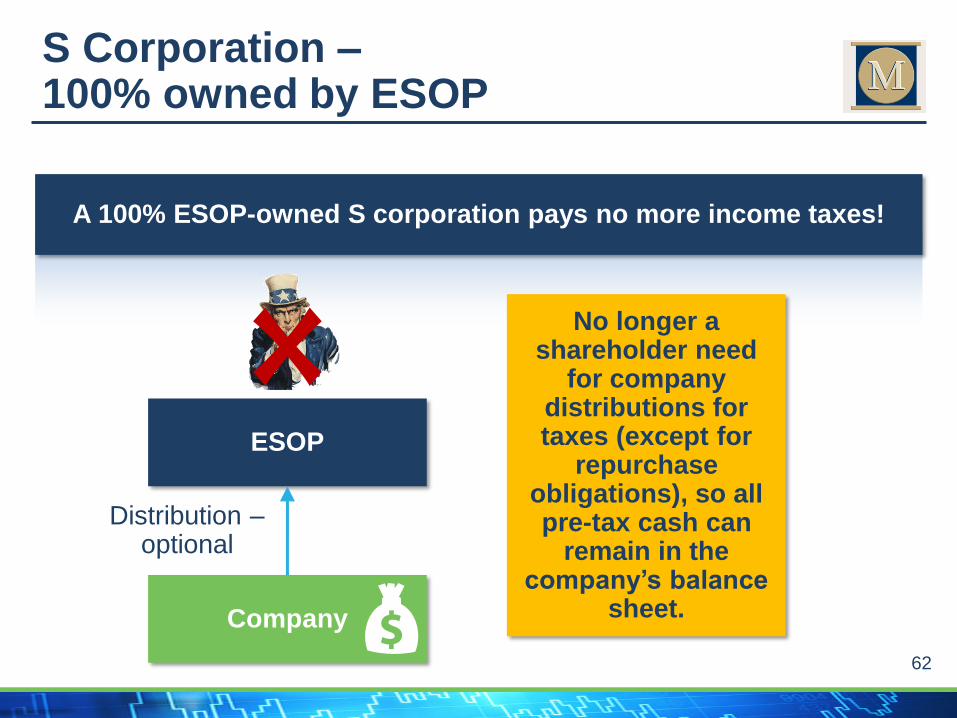

Company

S Corporation –100% owned by ESOP

A 100% ESOP-owned S corporation pays no more income taxes!

ESOP

Distribution –optional

No longer a shareholder need

for company distributions for taxes (except for

repurchase obligations), so all pre-tax cash can

remain in the company’s balance

sheet.

C Corporation ESOPs

(Since 1974)

64

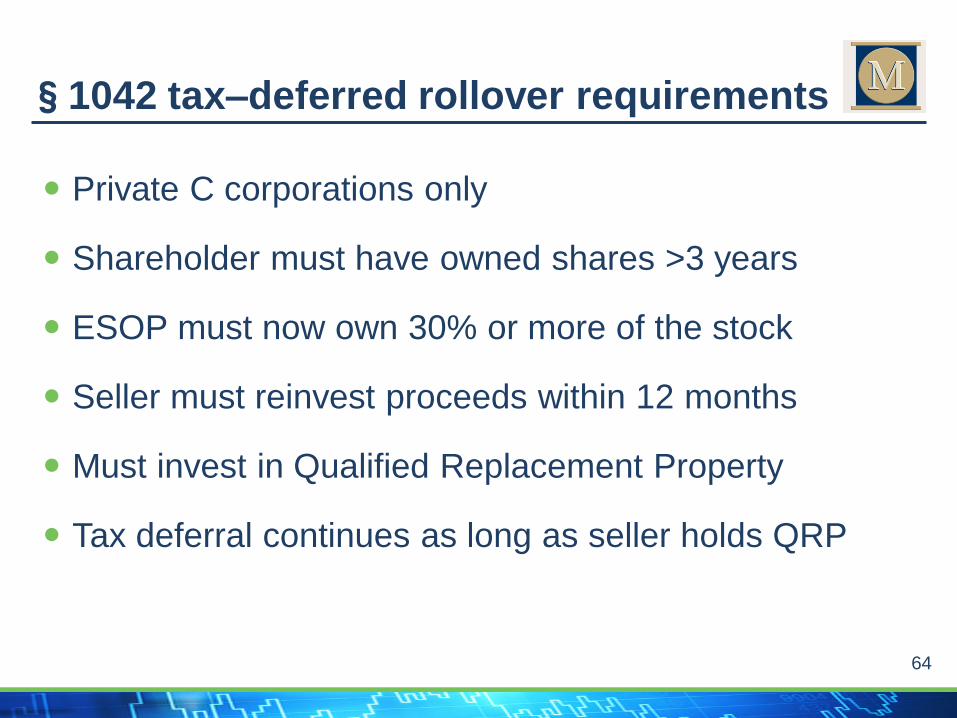

Private C corporations only

Shareholder must have owned shares >3 years

ESOP must now own 30% or more of the stock

Seller must reinvest proceeds within 12 months

Must invest in Qualified Replacement Property

Tax deferral continues as long as seller holds QRP

§1042 tax–deferred rollover requirements

65

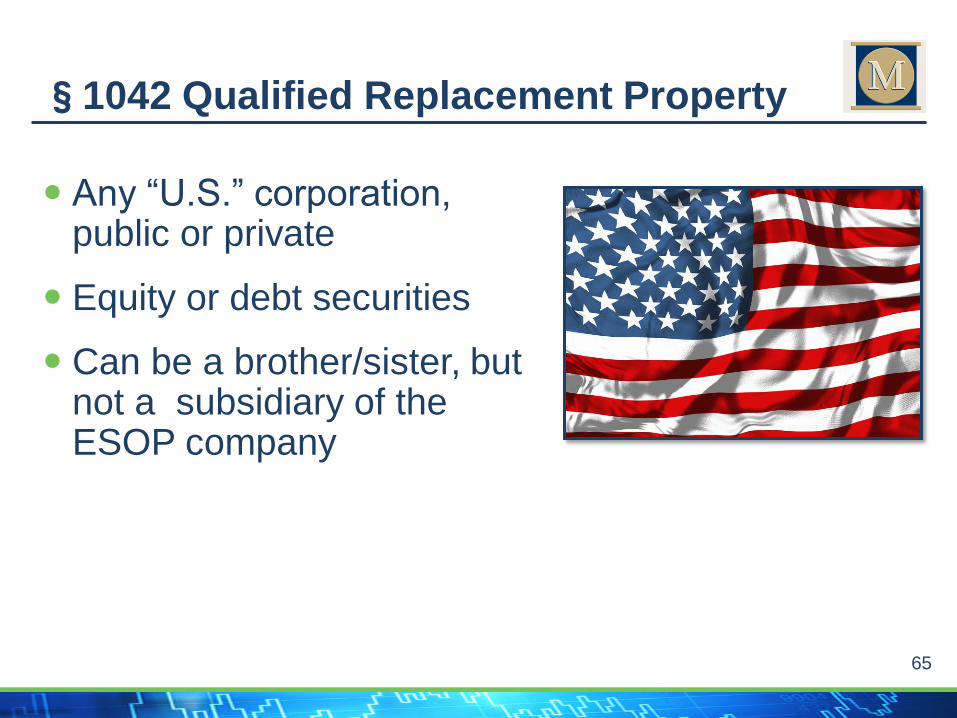

Any “U.S.” corporation, public or private

Equity or debt securities

Can be a brother/sister, but not a subsidiary of the ESOP company

§1042 Qualified Replacement Property

Corporate Status

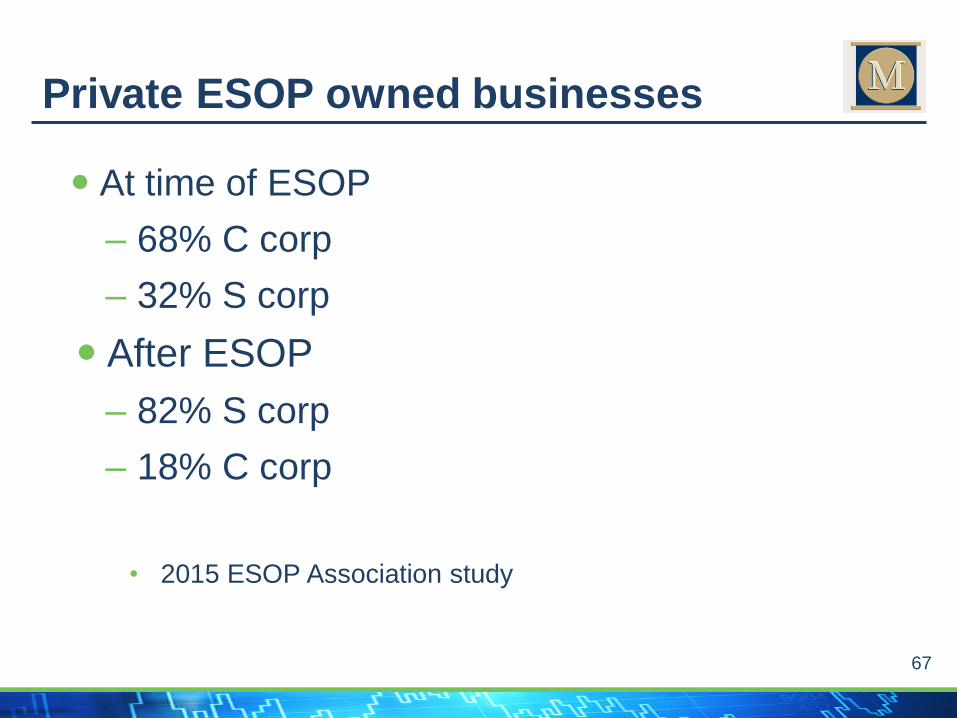

67

At time of ESOP

– 68% C corp

– 32% S corp

After ESOP

– 82% S corp

– 18% C corp

• 2015 ESOP Association study

Private ESOP owned businesses

68

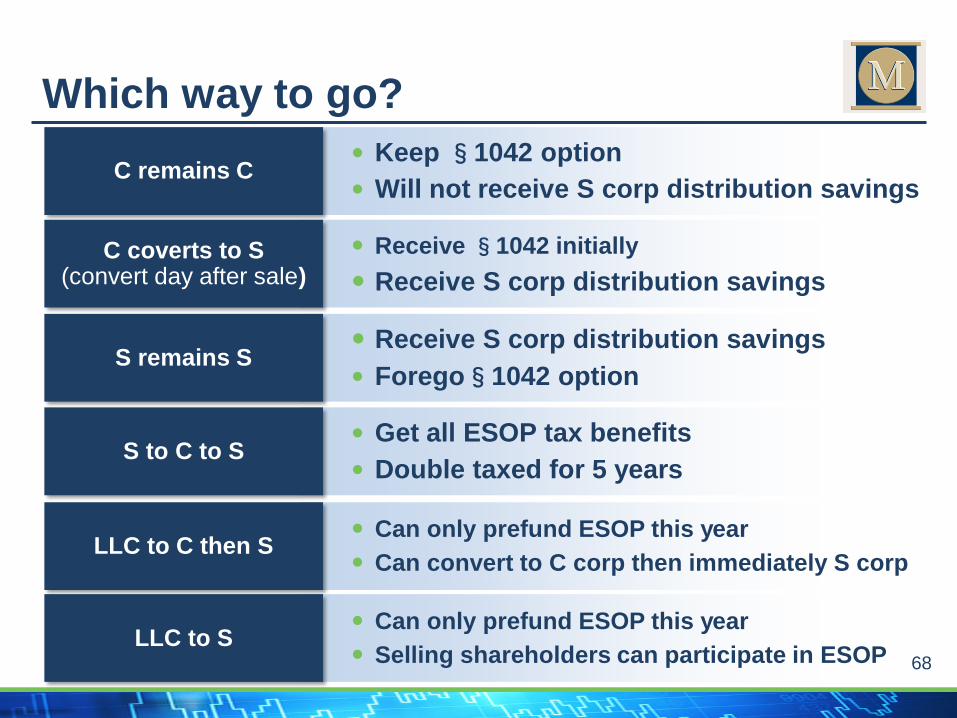

Which way to go?

C remains C Keep §1042 option

Will not receive S corp distribution savings

C coverts to S(convert day after sale)

Receive §1042 initially

Receive S corp distribution savings

S remains S Receive S corp distribution savings

Forego§1042 option

S to C to S Get all ESOP tax benefits

Double taxed for 5 years

LLC to C then S Can only prefund ESOP this year

Can convert to C corp then immediately S corp

LLC to S Can only prefund ESOP this year

Selling shareholders can participate in ESOP

Polling Question #6

ESOP Valuation

71

ESOP can not pay more than FMV

Revenue Ruling 59–60

Fair Market Value (FMV) is the price at which the property would change hands

between a willing buyer and a willing seller when the former is not under any compulsion

to buy and the latter is not under any compulsion to sell, both parties having reasonable knowledge of relevant facts.

72

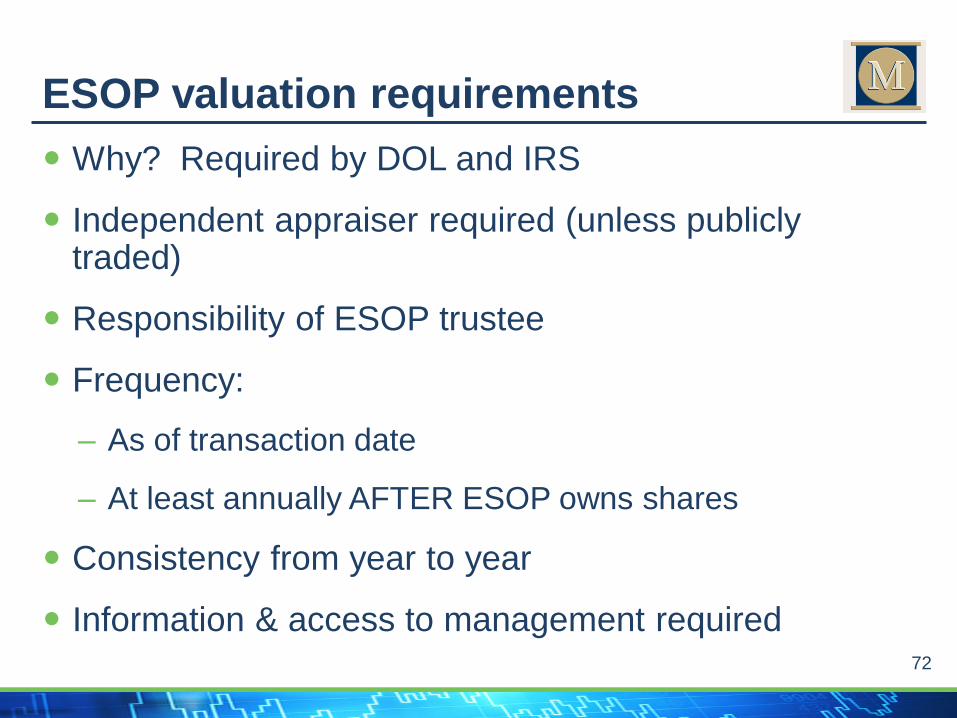

Why? Required by DOL and IRS

Independent appraiser required (unless publicly traded)

Responsibility of ESOP trustee

Frequency:

– As of transaction date

– At least annually AFTER ESOP owns shares

Consistency from year to year

Information & access to management required

ESOP valuation requirements

73

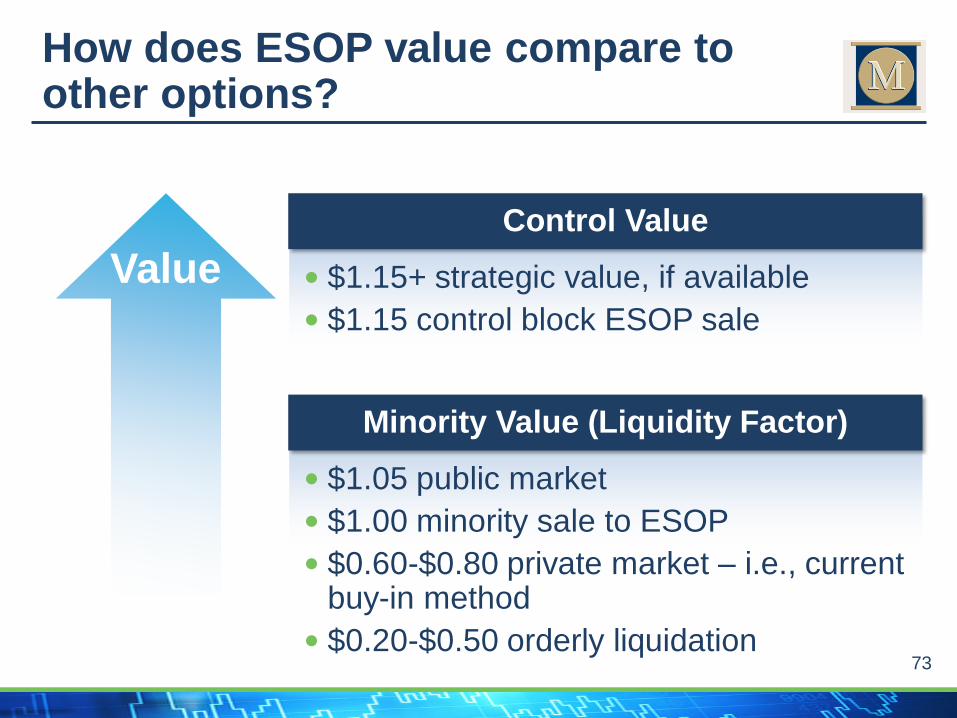

Value

How does ESOP value compare to other options?

Control Value

$1.15+ strategic value, if available

$1.15 control block ESOP sale

Minority Value (Liquidity Factor)

$1.05 public market

$1.00 minority sale to ESOP

$0.60-$0.80 private market – i.e., current buy-in method

$0.20-$0.50 orderly liquidation

74

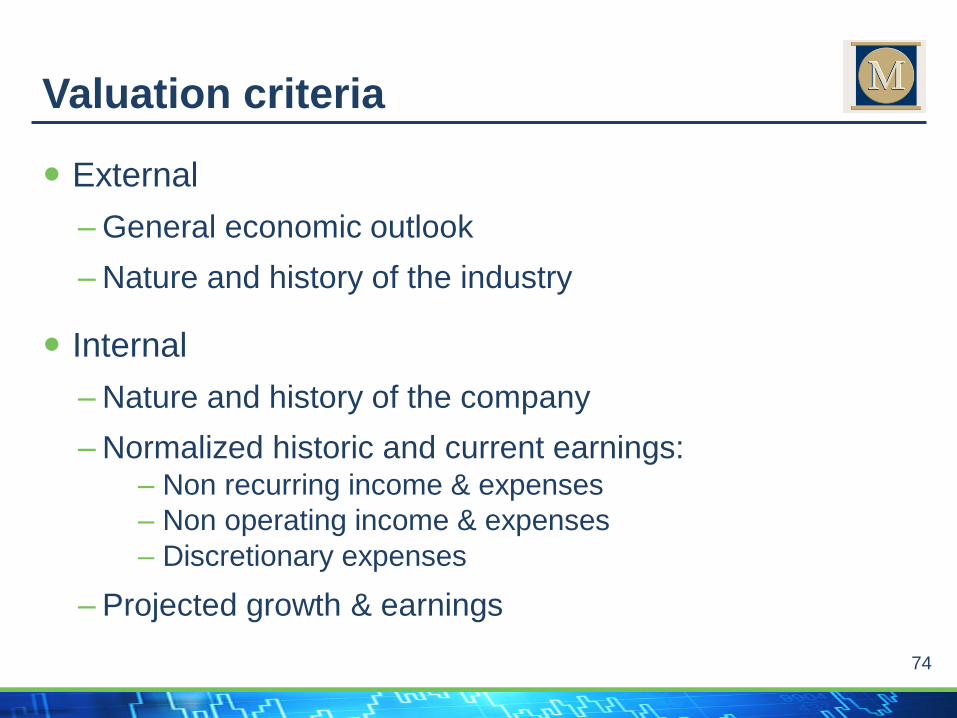

External

– General economic outlook

– Nature and history of the industry

Internal

– Nature and history of the company

– Normalized historic and current earnings:– Non recurring income & expenses

– Non operating income & expenses

– Discretionary expenses

– Projected growth & earnings

Valuation criteria

75

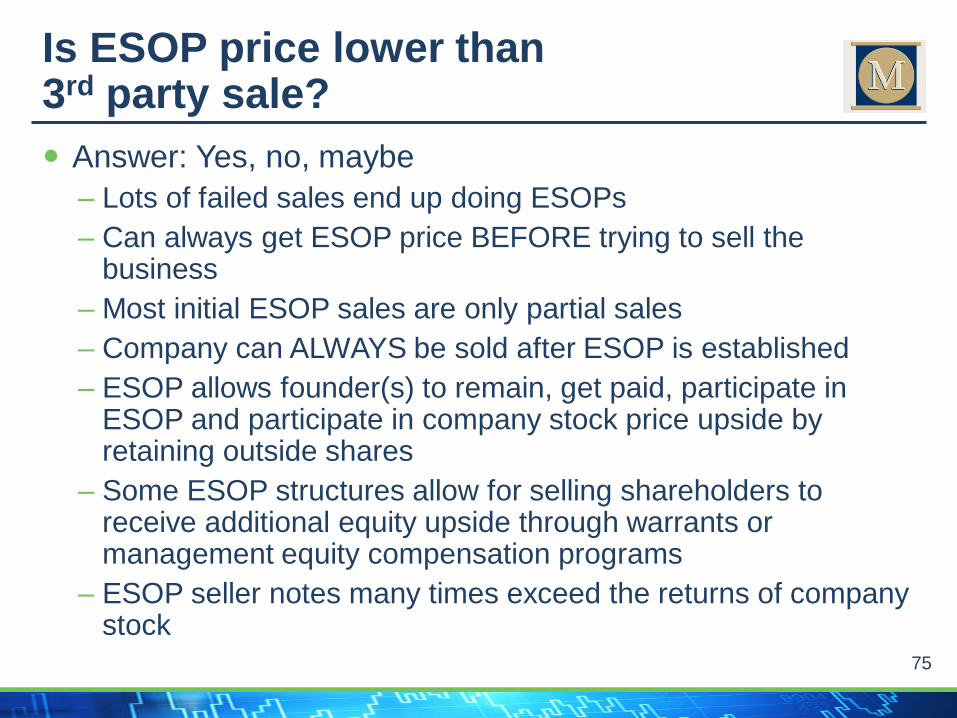

Answer: Yes, no, maybe

– Lots of failed sales end up doing ESOPs

– Can always get ESOP price BEFORE trying to sell the business

– Most initial ESOP sales are only partial sales

– Company can ALWAYS be sold after ESOP is established

– ESOP allows founder(s) to remain, get paid, participate in ESOP and participate in company stock price upside by retaining outside shares

– Some ESOP structures allow for selling shareholders to receive additional equity upside through warrants or management equity compensation programs

– ESOP seller notes many times exceed the returns of company stock

Is ESOP price lower than 3rd party sale?

Control

77

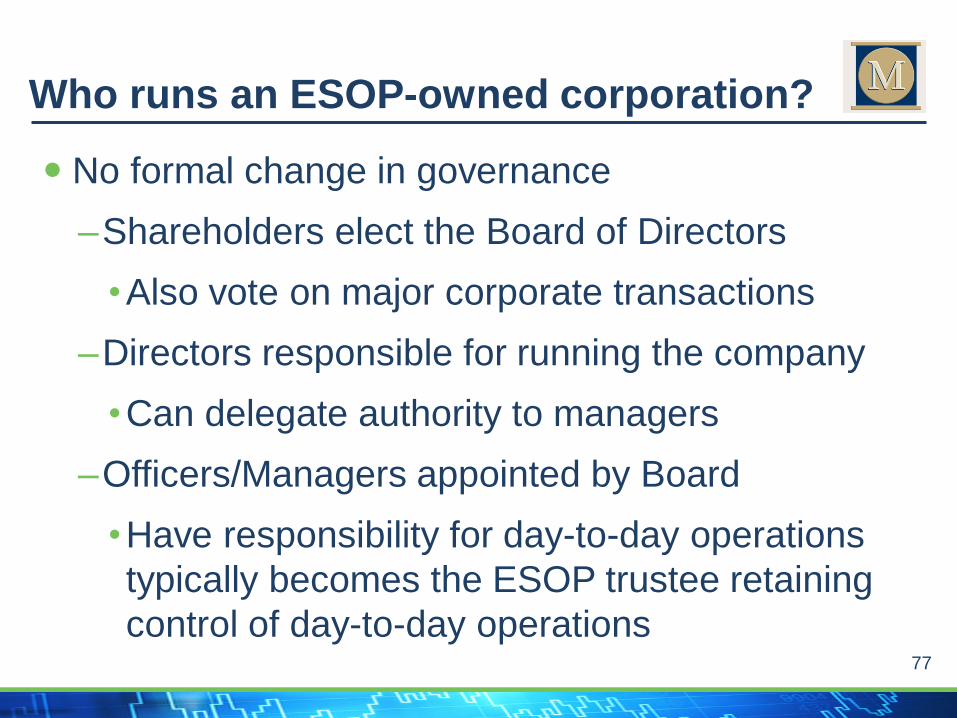

No formal change in governance

–Shareholders elect the Board of Directors

•Also vote on major corporate transactions

–Directors responsible for running the company

•Can delegate authority to managers

–Officers/Managers appointed by Board

•Have responsibility for day-to-day operations

typically becomes the ESOP trustee retaining

control of day-to-day operations

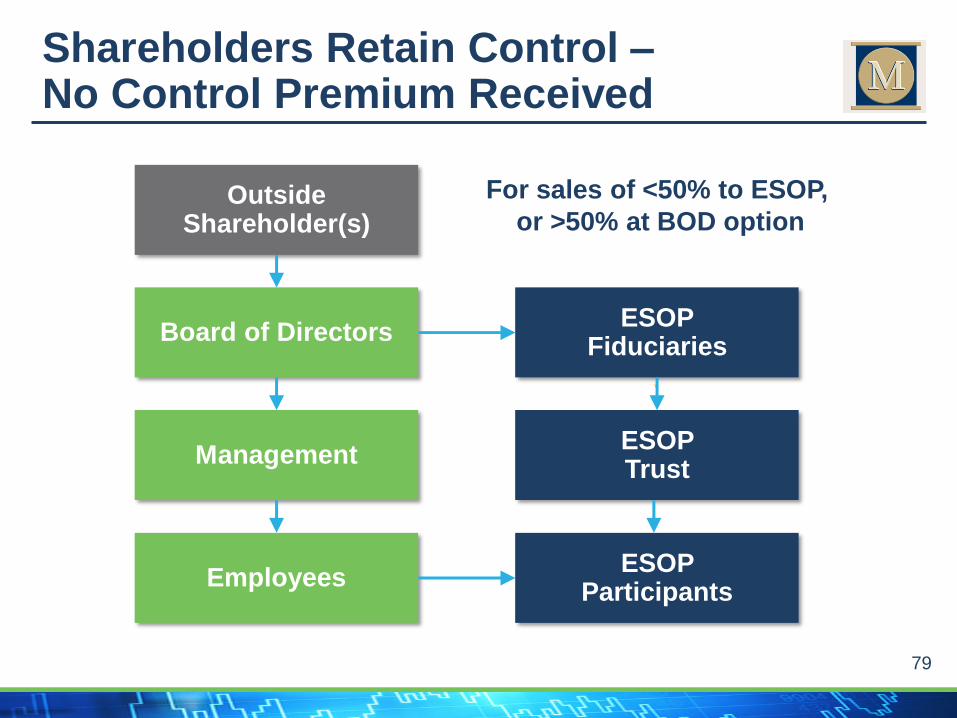

Who runs an ESOP-owned corporation?

78

The ESOP Trust is the DIRECT owner of company stock, NOT the employees

Employees are BENEFICIAL owners, and thus, do not have the same rights as direct owners of stock

But who is the shareholder?

79

ESOPFiduciaries

ESOP Trust

ESOP Participants

Board of Directors

OutsideShareholder(s)

Management

Employees

For sales of <50% to ESOP,

or >50% at BOD option

Shareholders Retain Control –No Control Premium Received

80

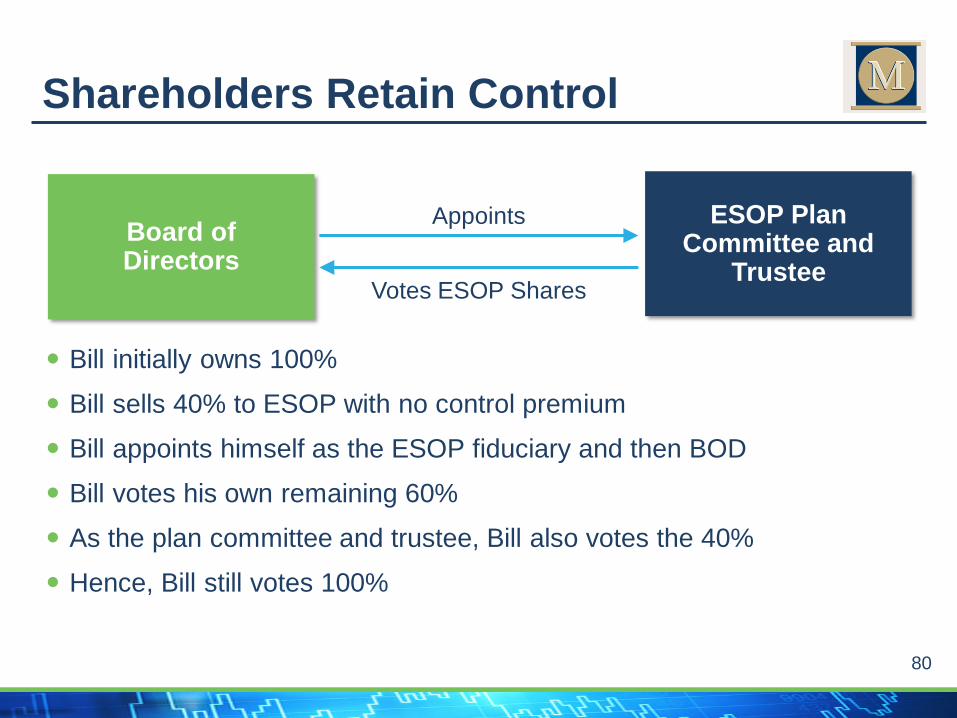

Bill initially owns 100%

Bill sells 40% to ESOP with no control premium

Bill appoints himself as the ESOP fiduciary and then BOD

Bill votes his own remaining 60%

As the plan committee and trustee, Bill also votes the 40%

Hence, Bill still votes 100%

Board ofDirectors

ESOP PlanCommittee and

Trustee

Shareholders Retain Control

Appoints

Votes ESOP Shares

81

At times it may be advisable for the board of directors to hire an Independent Fiduciary to oversee a particular transaction involving the ESOP

Events to consider an Independent Fiduciary include

– 100% sale to an ESOP

– A sale to a third party for stock sales with proceeds greater than $2 million

– Transactions that include other aspects beside a sale of stock, e.g., a new MSBP, seller note with high interest rate or long maturity

Independent Fiduciaries

82

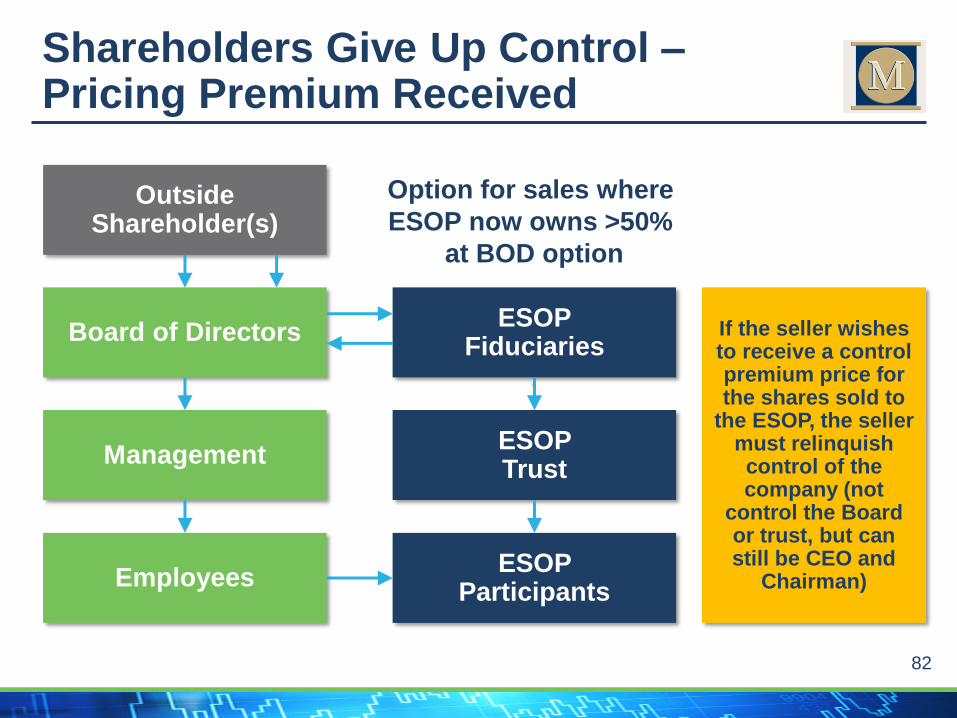

ESOPFiduciaries

ESOP Trust

ESOP Participants

Board of Directors

OutsideShareholder(s)

Management

Employees

Option for sales where

ESOP now owns >50%

at BOD option

Shareholders Give Up Control –Pricing Premium Received

If the seller wishes to receive a control premium price for the shares sold to

the ESOP, the seller must relinquish control of the company (not

control the Board or trust, but can still be CEO and

Chairman)

83

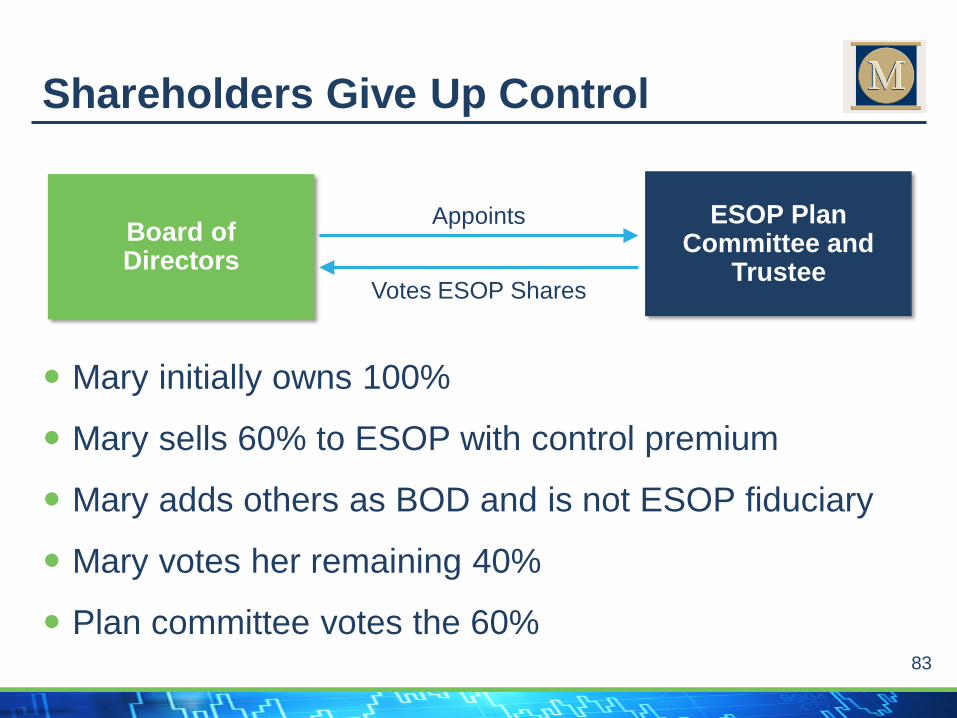

Mary initially owns 100%

Mary sells 60% to ESOP with control premium

Mary adds others as BOD and is not ESOP fiduciary

Mary votes her remaining 40%

Plan committee votes the 60%

Shareholders Give Up Control

Board ofDirectors

ESOP PlanCommittee and

Trustee

Appoints

Votes ESOP Shares

Polling Question #7

Financing Leveraged ESOPs

86

ESOP lending is a mature market and has been around for 40+ years

Most major financial institutions welcome the idea lending to ESOP owned companies

Why?

– ESOP companies tend to more stable

– Cash flow is better – tax deduction for interest AND PRINCIPAL on the loan value, and S Corp ESOPs can use pro rata distributions for loan repayments

ESOP Lenders

87

ESOP loans are normal corporate loans

– Bank debt recorded as employer debt

How is ESOP loan handled?

– Equity is reduced (contra-equity account) for “inside” or “ESOP” loan

– Equity is restored as inside loan is repaid

Bonding issues due to temporary negative impact to shareholders equity?

ESOP Loan Balance Sheet Effects

88

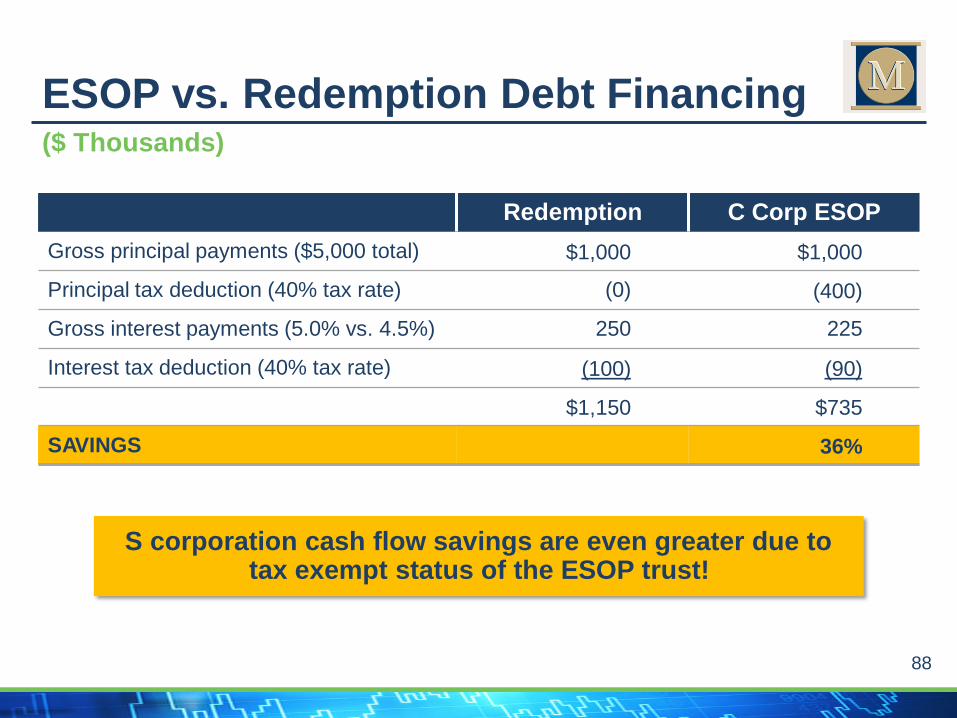

S corporation cash flow savings are even greater due to tax exempt status of the ESOP trust!

($ Thousands)

ESOP vs. Redemption Debt Financing

Redemption C Corp ESOP

Gross principal payments ($5,000 total) $1,000 $1,000

Principal tax deduction (40% tax rate) (0) (400)

Gross interest payments (5.0% vs. 4.5%) 250 225

Interest tax deduction (40% tax rate) (100) (90)

$1,150 $735

SAVINGS 36%

How the ESOP Plan Operates

90

Employee Benefit – The Four Steps

Distributions – very different than 401k4

Eligibility/Participation – typically similar to 401k1

Vesting – typically similar to 401k3

Company contributions – similar to 401k, maybe moreCompany dividends – different than 401k

2

91

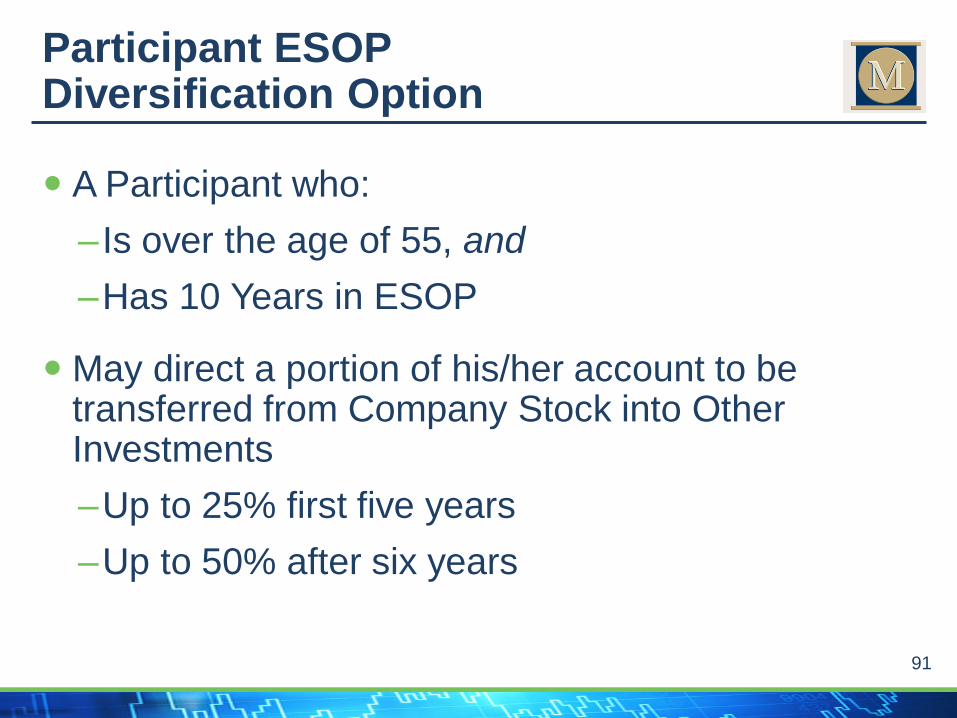

A Participant who:

– Is over the age of 55, and

–Has 10 Years in ESOP

May direct a portion of his/her account to be transferred from Company Stock into Other Investments

–Up to 25% first five years

–Up to 50% after six years

Participant ESOPDiversification Option

92

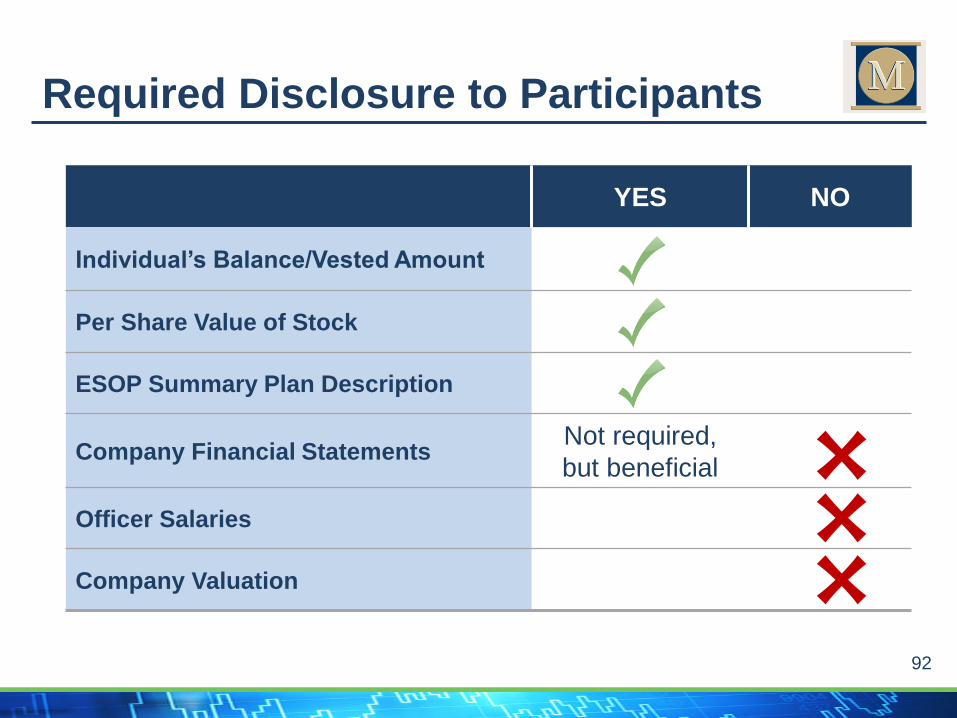

Required Disclosure to Participants

YES NO

Individual’s Balance/Vested Amount

Per Share Value of Stock

ESOP Summary Plan Description

Company Financial StatementsNot required,

but beneficial

Officer Salaries

Company Valuation

93

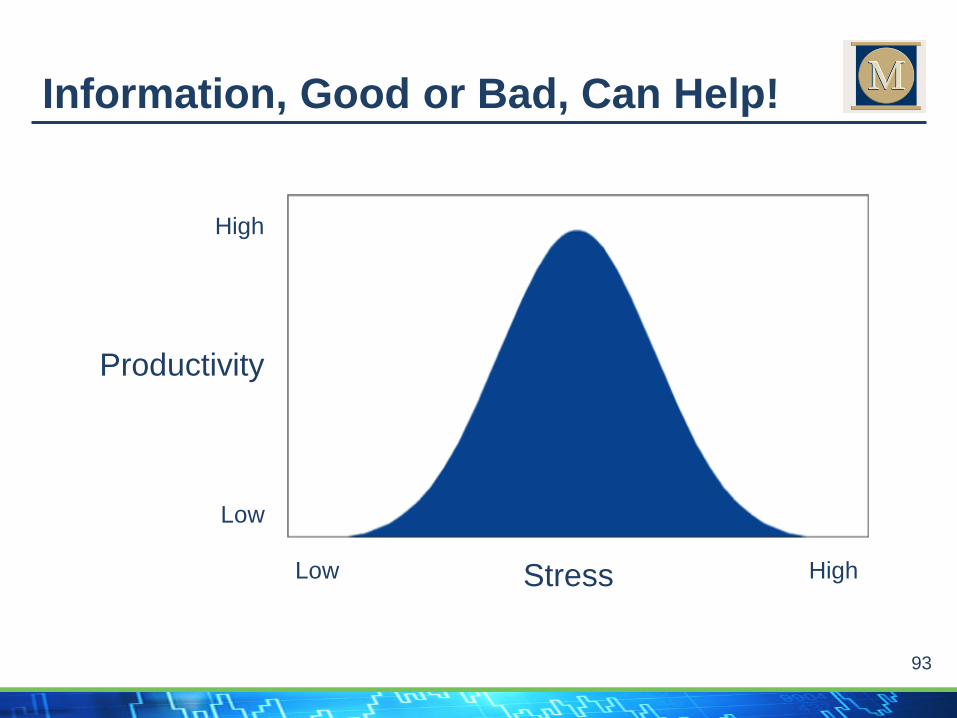

Information, Good or Bad, Can Help!

Productivity

Stress

Low

Low High

High

94

Take care of your company

–Accountability to the company

–Accountability to the client

–Accountability to each other

–Accountability to yourself

Loyalty

Employee Investment

95

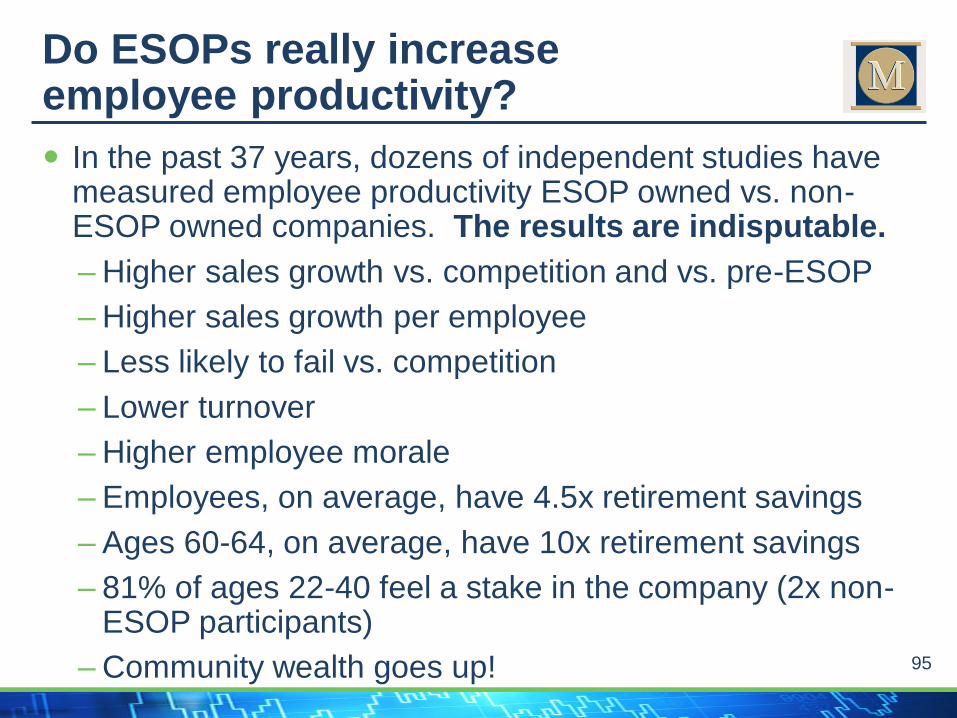

In the past 37 years, dozens of independent studies have measured employee productivity ESOP owned vs. non-ESOP owned companies. The results are indisputable.

– Higher sales growth vs. competition and vs. pre-ESOP

– Higher sales growth per employee

– Less likely to fail vs. competition

– Lower turnover

– Higher employee morale

– Employees, on average, have 4.5x retirement savings

– Ages 60-64, on average, have 10x retirement savings

– 81% of ages 22-40 feel a stake in the company (2x non-ESOP participants)

– Community wealth goes up!

Do ESOPs really increaseemployee productivity?

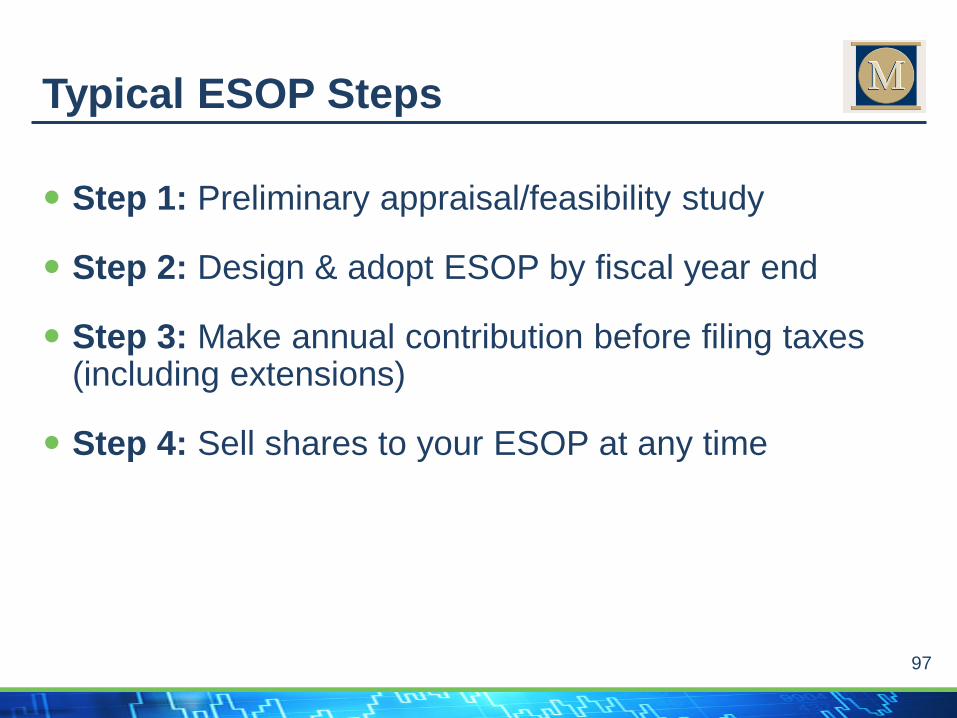

Next Steps

97

Step 1: Preliminary appraisal/feasibility study

Step 2: Design & adopt ESOP by fiscal year end

Step 3: Make annual contribution before filing taxes (including extensions)

Step 4: Sell shares to your ESOP at any time

Typical ESOP Steps

Polling Question #8