Embed Size (px)

Citation preview

Imprint

URBACT-Network ECO-FIN-NET

SMEs’ Access to Finance – Cities’ actions in disadvantaged urban areas

Leipzig/Brussels, June 2006

PublisherLead Partner City of Leipzig Business Development AgencyNeues Rathaus, Martin-Luther-Ring 4-604092 Leipzig, GermanyTel +49 (0)341 123 58 41, Fax +49 (0)341 123 58 25e-mail: [email protected]

EditorThematic Coordinator German Association for Housing, Urban and Spatial Development (DV e.V.) 47-51, Rue du Luxembourg1050 Brussels, BelgiumTel +32 (0)2 550 16 13, Fax +32 (0)2 503 56 06e-mail: [email protected]

This report is the fi nal output of the URBACT-network ECO-FIN-NET: City of Leipzig (Lead Partner), German Association for Housing, Urban and Spatial Development (Thematic Coordina-tor), City of Birmingham (GB), City of Evosmos (GR), City of Gdansk (PL), City of Gera (D), City of Gijon (E), Communauté d’Agglomération Grenoble Alpes Métropole (La Métro) (F), City of Marseille (F), City of Rotterdam (NL), City of Venice (I), City of Vienna (A), City of Vilnius (LT), Association for the Development of West Athens (ASDA) (GR)

The report has been compiled with assistance from experts Silke Brocks (German Association for Housing, Urban and Spatial Development), Jeroen den Uyl (City of Amsterdam) and Patrick Fourguette (expert with GIP ADETEF - French Minis-try of Economy, Finance and Industry).

Layout: comcores, Leipzig

Contents

Executive Summary ............................................................................................................................................ 5

1 Cities’ actions in favour for SMEs ....................................................................................... 13

1.1 The ECO-FIN-NET network rationale ..................................................................................................... 14

1.1.1 Background ............................................................................................................................. 14

1.1.2 SMEs‘ as one of the main motors for economic development ................................................. 14

1.1.3 The ECO-FIN-NET’s view on businesses ...................................................................................15

1.2 SME Support – a core task for local governments .................................................................................16

1.3 SMEs’ needs and requirements .............................................................................................................16

1.4 Need of an integrated local SME strategy ............................................................................................ 18

1.4.1 Three main support pillars ...................................................................................................... 18

1.4.2 Different local contexts ............................................................................................................19

1.4.3 Strong local partnership ..........................................................................................................19

2 Fostering the SMEs’ Access to Finance by fi nancial incentives .......................................... 21

2.1 Private Financing .................................................................................................................................. 23

2.1.1 High level of risk assessed by the banks for SME loans .......................................................... 23

2.1.2 Costs of small loan applications .............................................................................................. 25

2.1.3 Lack of information .................................................................................................................. 26

2.2 Public Financial Support ....................................................................................................................... 27

2.2.1 General framework for city involvement ................................................................................. 28

2.2.2 Grants ...................................................................................................................................... 32

2.2.3 Micro-credit ............................................................................................................................. 35

2.2.4 Venture and seed capital ......................................................................................................... 40

2.3 Advisory services and training schemes .............................................................................................. 44

3 Fostering the SMEs’ Access to Finance by non-fi nancial services and network support ....45

3.1 Variety of support services .................................................................................................................. 45

3.2 Existing problems seen by the entrepreneurs ...................................................................................... 47

3.3 Challenges from a city perspective ...................................................................................................... 50

3.4 Suggestions ......................................................................................................................................... 53

4 Recommendations .............................................................................................................65

5 The ECO-FIN-NET network .................................................................................................. 74

15.1 The European Programme URBACT .......................................................................................................71

5.2 The URBACT-network ECO-FIN-NET ...................................................................................................... 72

5.2.1 Work groups / Sub themes ...................................................................................................... 72

5.2.2 Working approach .................................................................................................................... 72

5.2.3 External expertise ................................................................................................................... 73

Appendix ..................................................................................................................................75

I Partner Cities / Contact Persons .......................................................................................................... 75

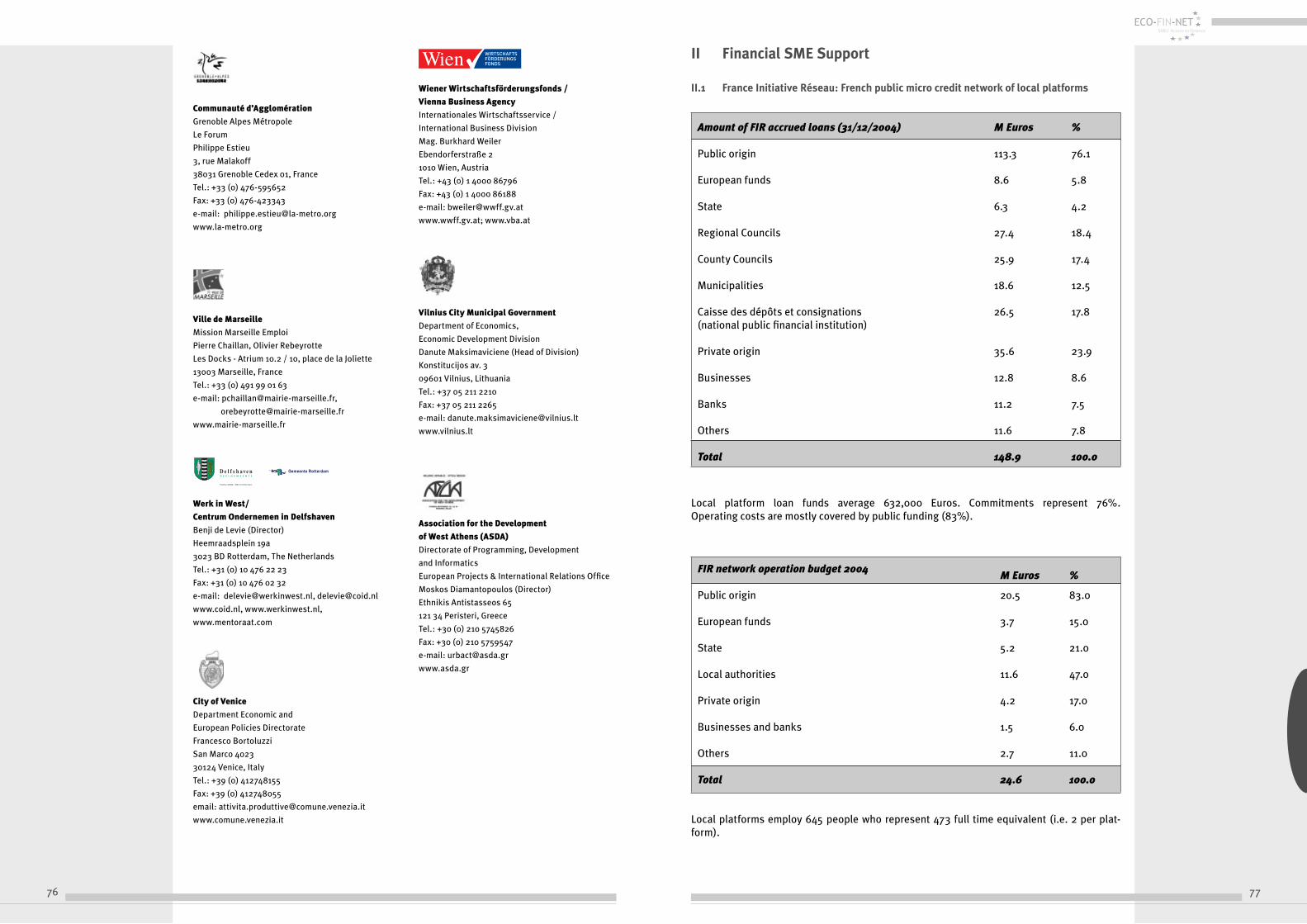

II Financial SME Support ......................................................................................................................... 77

III Non-Financial SME Support ..................................................................................................................81

IV Sources ................................................................................................................................................. 85

V Partners‘ Practice Examples Questionnaire Results ............................................................................ 87

Executive Summary

The URBACT-network ECO-FIN-NET

The EU Initiative URBAN

The far-reaching structural economic changes in Europe during the past decades have had a negative effect on cities and urban areas in general. These changes are particularly apparent in the inner cities and surrounding areas, and also in the large mono-structural housing estates on the outskirts of cities – even in prosperous regions. In these deprived urban neighbourhoods the economic outlook is bad, the buildings are generally in poor structural condition and the quality of life is very low. And where these areas also suffer from high crime rates, they are frequently referred to as “social hotspots”. These signifi cant disparities in economic and social opportunities damage the attractiveness, competitiveness, social in-clusiveness and safety of cities. Thus the situation also impacts negatively on the economic growth and wealth of a city. Unless appropriate countermeasures are taken, in the medium and long term these tendencies will affect more prosperous parts of our cities or regions, since they radiate negative signals with regard to relocation and development.

In order to respond appropriately to these trends, in 1990 the European Commission launched the URBAN Pilot Projects (UPP) and in 1994 the URBAN I Community Initiative. Innovative approaches were put to the test in a sort of European experimental ground for urban regeneration. In more than ten years of its existence, using the fi eld-tested integrated development approach, the URBAN Community Initiative has contributed signifi cantly to the sustainable stabilisation and revitalisation of urban areas that are experiencing diffi culties. Measures to strengthen the

local economy, promote employment and social integration and address urban planning, infrastructure and environmental issues have signifi cantly improved the quality of life of local residents. As a result of these positive experiences and evalu-ations, the URBAN programme was carried forward in 2000 as URBAN II.

The URBACT programme

Since 2003 the European Commission has been supporting the Europe-wide exchange between cities in the fi eld of inte-grated urban development within the framework of its URBACT programme. The programme supports• the exchange of innovative ideas and approaches in the notion of „good practices“, • the improvement of methods of integrated urban development, • the preparation of political recommendations concerning urban development in the context of the EU Cohesion Policy

post-2006.

The URBACT programme focuses on all cities that have already been funded within the framework of Urban Pilot Projects (UPP) or the Community Initiatives URBAN I and/or URBAN II and have therefore been able to gain a lot of experience with integrated concepts for the regeneration and revitalisation of disadvantaged districts. Furthermore, cities from the new member states with a population of more than 20,000 are being invited to participate in the programme.

URBACT is not just a straightforward summary of the experiences of the URBAN cities but has acquired an additional dimen-sion as the result of shared discussion between various cities in different European countries and on several issues and approaches which was implemented by URBACT.

The URBACT partner cities have made a signifi cant contribution:

The cities felt that they were in debt because they were receiving URBAN funding, and they have delivered information on their experiences. They have sent representatives to working group discussions in order to set up suitable recommenda-tions and have also made a major fi nancial contribution (50% of the budget of the URBACT networks).

And they have expectations. In an integrated approach, the experiences of the other partner cities are of interest to them because they can represent added value for their own experiences. Consequently they wish this programme to be contin-ued.

The method used within URBACT consists mainly of thematic networks between partner cities, covering the main issues of integrated urban development. Within these networks the partner cities discuss comparable problems of urban revitalisa-tion with other cities from other member states, thereby establishing a knowledge base which is generally accessible. Each network deals with a specifi c topic – e.g. urban regeneration, citizen participation or economic activity.

55

ECO-FIN-NET

The ECO-FIN-NET network dealt with the issue of support to small and medium-sized en-terprises (SMEs). It focused on the access of SMEs to fi nance through innovative fi nancial instruments and in particular on the access of the smallest companies in the less favoured urban areas. The network is led by the City of Leipzig in Germany and consists of 13 cities from 10 European member states.

The rationale of the ECO-FIN-NET network

Economic growth generates additional wealth which in return helps to enhance the whole area, increasing its attractiveness and image, and fi nally strengthens the commitment of the residents to their neighbourhood.

The cities have turned their attention to the SMEs located in their regions because the SMEs are one of the main motors for economic development. Over 95% of all companies in the European Union are micro, small and medium-sized enterprises, and this percentage is even higher in the disadvantaged areas. These areas are characterised by a below-average rate of entrepreneurship and this is motivating the cities to pay particular attention to all sorts of business and entrepreneurial projects – even the very smallest business projects.

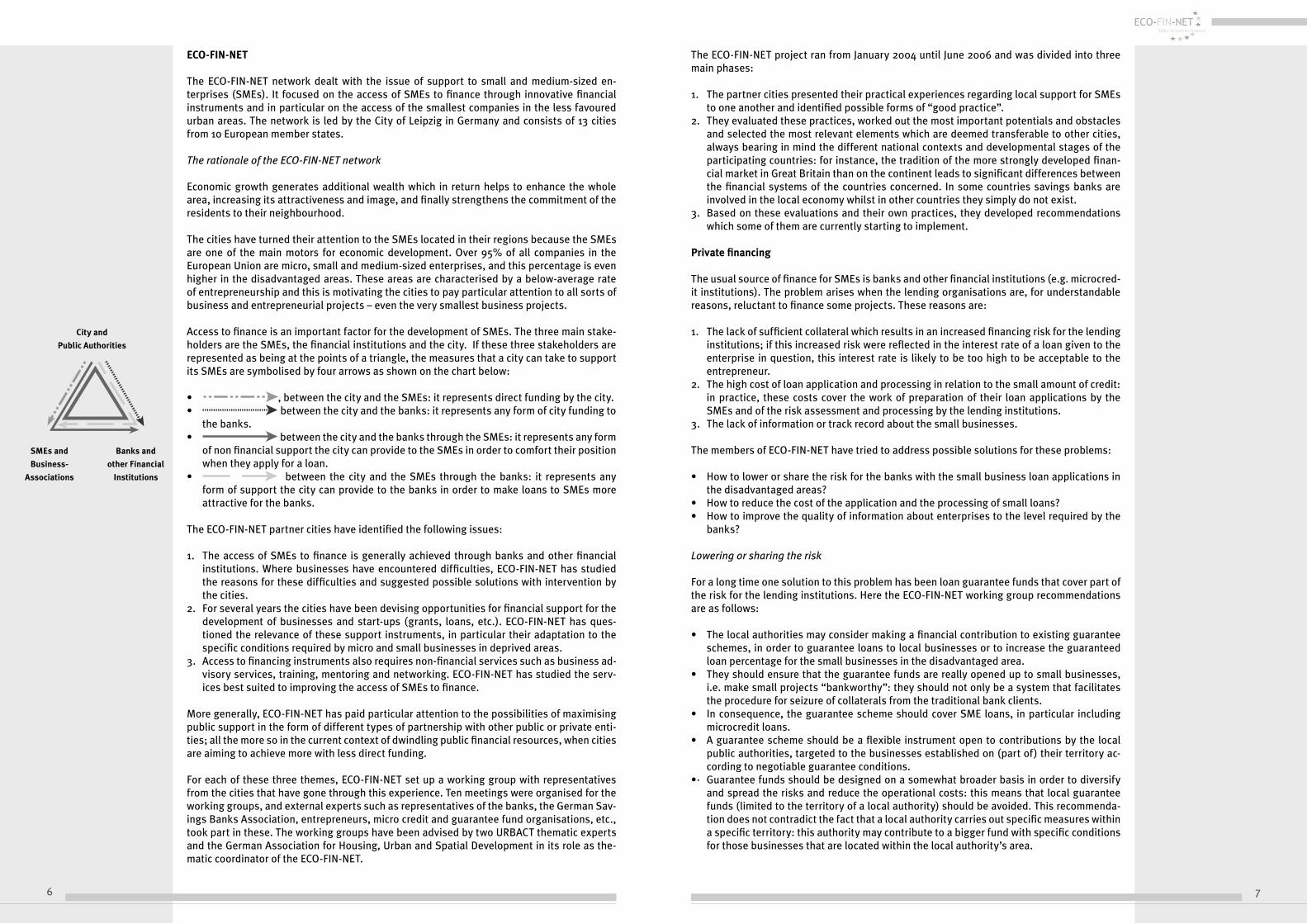

Access to fi nance is an important factor for the development of SMEs. The three main stake-holders are the SMEs, the fi nancial institutions and the city. If these three stakeholders are represented as being at the points of a triangle, the measures that a city can take to support its SMEs are symbolised by four arrows as shown on the chart below:

• , between the city and the SMEs: it represents direct funding by the city.• between the city and the banks: it represents any form of city funding to

the banks.• between the city and the banks through the SMEs: it represents any form

of non fi nancial support the city can provide to the SMEs in order to comfort their position when they apply for a loan.

• between the city and the SMEs through the banks: it represents any form of support the city can provide to the banks in order to make loans to SMEs more attractive for the banks.

The ECO-FIN-NET partner cities have identifi ed the following issues:

1. The access of SMEs to fi nance is generally achieved through banks and other fi nancial institutions. Where businesses have encountered diffi culties, ECO-FIN-NET has studied the reasons for these diffi culties and suggested possible solutions with intervention by the cities.

2. For several years the cities have been devising opportunities for fi nancial support for the development of businesses and start-ups (grants, loans, etc.). ECO-FIN-NET has ques-tioned the relevance of these support instruments, in particular their adaptation to the specifi c conditions required by micro and small businesses in deprived areas.

3. Access to fi nancing instruments also requires non-fi nancial services such as business ad-visory services, training, mentoring and networking. ECO-FIN-NET has studied the serv-ices best suited to improving the access of SMEs to fi nance.

More generally, ECO-FIN-NET has paid particular attention to the possibilities of maximising public support in the form of different types of partnership with other public or private enti-ties; all the more so in the current context of dwindling public fi nancial resources, when cities are aiming to achieve more with less direct funding.

For each of these three themes, ECO-FIN-NET set up a working group with representatives from the cities that have gone through this experience. Ten meetings were organised for the working groups, and external experts such as representatives of the banks, the German Sav-ings Banks Association, entrepreneurs, micro credit and guarantee fund organisations, etc., took part in these. The working groups have been advised by two URBACT thematic experts and the German Association for Housing, Urban and Spatial Development in its role as the-matic coordinator of the ECO-FIN-NET.

The ECO-FIN-NET project ran from January 2004 until June 2006 and was divided into three main phases:

1. The partner cities presented their practical experiences regarding local support for SMEs to one another and identifi ed possible forms of “good practice”.

2. They evaluated these practices, worked out the most important potentials and obstacles and selected the most relevant elements which are deemed transferable to other cities, always bearing in mind the different national contexts and developmental stages of the participating countries: for instance, the tradition of the more strongly developed fi nan-cial market in Great Britain than on the continent leads to signifi cant differences between the fi nancial systems of the countries concerned. In some countries savings banks are involved in the local economy whilst in other countries they simply do not exist.

3. Based on these evaluations and their own practices, they developed recommendations which some of them are currently starting to implement.

Private fi nancing

The usual source of fi nance for SMEs is banks and other fi nancial institutions (e.g. microcred-it institutions). The problem arises when the lending organisations are, for understandable reasons, reluctant to fi nance some projects. These reasons are:

1. The lack of suffi cient collateral which results in an increased fi nancing risk for the lending institutions; if this increased risk were refl ected in the interest rate of a loan given to the enterprise in question, this interest rate is likely to be too high to be acceptable to the entrepreneur.

2. The high cost of loan application and processing in relation to the small amount of credit: in practice, these costs cover the work of preparation of their loan applications by the SMEs and of the risk assessment and processing by the lending institutions.

3. The lack of information or track record about the small businesses.

The members of ECO-FIN-NET have tried to address possible solutions for these problems:

• How to lower or share the risk for the banks with the small business loan applications in the disadvantaged areas?

• How to reduce the cost of the application and the processing of small loans?• How to improve the quality of information about enterprises to the level required by the

banks?

Lowering or sharing the risk

For a long time one solution to this problem has been loan guarantee funds that cover part of the risk for the lending institutions. Here the ECO-FIN-NET working group recommendations are as follows:

• The local authorities may consider making a fi nancial contribution to existing guarantee schemes, in order to guarantee loans to local businesses or to increase the guaranteed loan percentage for the small businesses in the disadvantaged area.

• They should ensure that the guarantee funds are really opened up to small businesses, i.e. make small projects “bankworthy”: they should not only be a system that facilitates the procedure for seizure of collaterals from the traditional bank clients.

• In consequence, the guarantee scheme should cover SME loans, in particular including microcredit loans.

• A guarantee scheme should be a fl exible instrument open to contributions by the local public authorities, targeted to the businesses established on (part of) their territory ac-cording to negotiable guarantee conditions.

•· Guarantee funds should be designed on a somewhat broader basis in order to diversify and spread the risks and reduce the operational costs: this means that local guarantee funds (limited to the territory of a local authority) should be avoided. This recommenda-tion does not contradict the fact that a local authority carries out specifi c measures within a specifi c territory: this authority may contribute to a bigger fund with specifi c conditions for those businesses that are located within the local authority’s area.

6

1

7

City and

Public Authorities

SMEs and

Business-

Associations

Banks and

other Financial

Institutions

• The guarantee funds should be managed by specialised fi nancial institutions in order to increase the leverage ratio and lower the operational costs.

• Where the strengthening of links within a local / sectoral business community is an issue, mutual guarantee schemes should be considered.

• At the national level, counter-guarantee systems should be developed in addition to the European counter-guarantees delivered by the European Investment Fund (EIF).

Reducing the costs of small loan applications and improving the quality of information

When small businesses apply for a loan, they have to prepare a loan application which some-times includes business data, a business plan and a list of all their available securities, etc. Small loans are not assessed in the same way as large ones, but well-prepared applications are easier (and less time-consuming) for the fi nancial institutions to process.

The ECO-FIN-NET recommendation is to deliver advisory services to the applicant businesses in how to prepare their loan applications and to add such fi nancial expertise to the list of other types of expertise eligible to the (regional) advisory support schemes like other types of advisory services.

Another possibility is to also make the cost to the fi nancial institutions of processing loan ap-plications eligible for support from the existing business advisory support schemes.

The procedure for processing loan applications should be designed in such a way as to avoid duplication of work. As a fi rst step in this direction, credit check results could be communi-cated between banks and guarantee funds with the consent of the companies concerned. This cooperation with the aim of leaner and cheaper processes can be further developed and intensifi ed:

• Institutional cooperation between lending and guarantee institutions, giving enterprises the option of a one-stop application point.

• Designing lending products with a “built-in” guarantee (“exemption from liability”) which is “automatically” applied for at the same time as the loan product.

Public fi nancial support

General framework for city involvement

It seems obvious that public SME support measures have to be in line with the expectations and requirements of the businesses. As a general rule, SMEs need stable, visible and effi cient procedures. They also prefer the local level (city). For the cities, these conditions are met by partnerships. The ECO-FIN-NET recommendations are as follows:

• Stable support means sustained access to fi nancial resources. But the current trend, at least in the old member states, shows that public resources are dwindling. For the cit-ies, securing these support procedures can be achieved by partnership either with other public entities that run multi-annual programmes (regions, national level, EU Structural Funds...), or, as it is being developed in some countries, with the private sector.

• Visibility means that the support schemes have to be promoted to the SMEs. This promo-tion can usefully be achieved by business representative organisations, and the cities should organise a partnership with these organisations for this purpose.

• Effi ciency requires technical expertise that as a rule is developed by specialist institu-tions. In order to design and offer effi cient instruments, ECO-FIN-NET recommends that the cities organise a partnership with specialist fi nancial institutions.

Instruments of public fi nancial support

Instruments of public fi nancial support include grants, loans, guarantees and venture capi-tal. The ECO-FIN-NET recommendations on guarantees have already been presented in the section on “Lowering or sharing the risk”.

Grants

• Grants are a very successful support instrument for new projects that require consolida-tion of the entrepreneur’s equity: they bring more confi dence to the projects and give them access to other forms of funding.

• Grants should be considered as part of a fi nancial package aiming at making small projects bank worthy.

• In situations where there are scarce public fi nancial resources, grant funds should be re-served to the consolidation of equity for new projects, irrespective of the investments and the number of new jobs.

• Priorities may be set for grant allocation by the local authorities, but automatic sectoral support associated with specifi c investments (for instance investment in IT equipment) should be avoided, since the main priority for grants in disadvantaged areas is to pro-mote new projects (and new economic activity) and develop these in the long term.

Loans

• There is no reason for local authorities to be involved in the operation of schemes that require particular expertise, but rather what is needed is to create incentives for existing schemes so that they are more active for micro and small businesses in disadvantaged areas.

• These incentives must be negotiated in such a way that the public support can be strictly applied to the businesses concerned within the area.

• The cities can consider making a fi nancial contribution to cover the preparation and/or administration costs of these loans to small businesses.

• They can also consider making a contribution to fi nancial institutions (microcredit) in or-der to cover specifi c local costs (within the disadvantaged area that is being targeted).

• They should always negotiate with the private fi nancial institutions so that the public grants and loans are an incentive for private fi nancing (leverage effect).

Venture capital

• Local authorities should not raise unfounded expectations within the SME community by publicising the possibility of venture capital that will apply only to a very small minority of businesses, in particular in those disadvantaged areas where the vast majority of projects are in the traditional sector.

• So far as this is necessary, and if this is a requirement of local businesses (ad hoc case-by-case agreement), they could act as partners of specialist venture capital organisations. They may consider a fi nancial contribution in order to capitalise investment funds (seed and venture capital) for investments in local businesses and also/fi rst to cover the admin-istrative costs of applications processing and management.

Effi cient implementation of these instruments requires additional advisory services, training and promotion as generally offered by service providers and business representative organi-sations. ECO-FIN-NET recommends that the cities provide fi nancial support to these organi-sations for this purpose.

Non-fi nancial services and network support

Non-fi nancial services are an important complementary part of the measures taken by cities to improve the access to fi nance for SMEs. There are four main types of non-fi nancial services:

• Information / Orientation: SMEs are supplied with information about a number of aspects of their activities and entrepreneurship, such as tax regulations, how to get access to fi nance etc. Advice is given on the viability of a business idea.

• Training / Qualifi cation: Training and qualifi cation services are intended to deliver a high-er level of entrepreneurial skills in the fi elds of promotion, bookkeeping, use of IT, e-com-merce etc.

• Coaching / Mentoring: Coaching and mentoring are services where the entrepreneurs are helped by a mentor, often a retired entrepreneur with a great deal of experience. The entrepreneurs are helped to refl ect on their problems. Coaching and mentoring require a relationship of trust between the mentor and the mentee.

8

1

9

• Network support: Network support is a specifi c form of service intended to set up busi-ness networks between entrepreneurs in order to create a better environment for the en-trepreneurs, opportunities for business-to-business transactions, joint advertising etc.

However, service providers are frequently faced with a whole series of obstacles:

There is a low participation rate. Many entrepreneurs do not take up the services offered to them. In an in-depth survey amongst entrepreneurs in EU member states, the following reasons were given:

• Lack of awareness of what is needed. Entrepreneurs do not know that they may require support and services.

• Diffi culties in fi nding a service provider. Entrepreneurs do not know about all the service providers that exist.

• The content of the service offered. There is often an asymmetry between the type and quality of the service as delivered and the actual requirements of the entrepreneur.

• The conditions of service delivery. Entrepreneurs are not satisfi ed with the timing and price of what is being delivered.

Based on these fi ndings, their own experience and discussions with entrepreneurs, the ECO-FIN-NET cities addressed the following questions within their working group:

How can we reach the entrepreneurs?How can we meet their demands and requirements?

The ECO-FIN-NET cities have identifi ed many methods of reaching the entrepreneurs. The guiding principles of these methods are: to reach out actively to the entrepreneurs, at the places where they can be found, by people who speak their language, by taking up a (quasi-) autonomous position in order to be as close as possible to the entrepreneur and by encourag-ing entrepreneurs to contact other entrepreneurs.

How can the service / (unity of) supply be improved?

What is the best approach to offering services to entrepreneurs? How can the work of service providers be organised?

Because in many cities the variety of service providers is very wide, the ECO-FIN-NET cities considered what their role would be in improving collaboration between these bodies. The concept of a network covering all service providers and banks and other fi nancial institutions is recommended. This could be further reinforced by developing focal points where informa-tion from all service providers is collected and if necessary can be redirected in order to be able to fulfi l the specifi c requirements of the entrepreneurs with regard to services. Further consolidation of this unit of supply is achieved by the introduction of a business pass show-ing the most important skills of the entrepreneur.

How can cooperation with fi nancial institutions be improved in order to strengthen the ef-fectiveness of non-fi nancial support services?

It is recommended that a stable and trusting relationship of cooperation be built up between banks, service providers and the cities. Such cooperation contributes to the understanding and appreciation of the quality of the services and network support delivered by service pro-viders. It creates a better picture of the entrepreneur’s skills and qualifi cations when s/he applies for a loan. As banks have certain ways of assessing the creditworthiness of an entre-preneur, the service providers must create their services in line with this. Then the banks will be better able to assess the creditworthiness of a loan application. This form of cooperation reduces the costs of information handling and risks, which means that more entrepreneurs will get access to (market) fi nance.

What is the ideal support package and variety of services and network support that is of-fered to entrepreneurs?

Despite the great variety of different requirements by so many entrepreneurs, we cannot avoid the question as to how the best service package offered to the entrepreneurs should look. ECO-FIN-NET cities considered it useful to defi ne the ideal package.

They came to the following conclusion:

• Personal skills: courses on presentation, organisation, bookkeeping etc.• Market access: services concerning market orientation, location issues, permits/regula-

tions, access to business networks etc.• Finance: guidance concerning the information required by banks and fi nancial instru-

ments of support (guarantees, grants).

Together with services in the form of consultations, network support and coaching services can contribute to all of these services mentioned above.

How can we ensure a broader-based integrative support package? What is the best way to approach this?

The ECO-FIN-NET cities know that getting access to fi nance and improving the quality of en-trepreneurs through non-fi nancial services is only part of a broader picture. These services must be rooted in a broader-based scheme.

An integrative policy (like URBAN) is necessary to enforce the effects of (non-)fi nancial sup-port for entrepreneurs. Physical renewal can result in a safer area in places where affordable premises are available, where people are trained and social inclusion measures are taken, where higher-income residents are attracted in order to increase the buying power of the area. These integrative approaches can only work when all the partners work together. In addition to the smaller circle of cities, banks and service providers, house owners, housing associations, schools, social institutions and neighbourhood residents associations are all involved.

How can we attain fi nancial resources for support services?

The ECO-FIN-NET cities are concerned about the fi nancial sustainability of (non-)fi nancial services. Apart from one or two exceptions, external funding is necessary. Over the past few years the infl uence of European programmes such as URBAN has been exceptional. As previ-ously indicated, diminishing funds for the coming budget period are causing dark clouds to appear over these services.

The cities will do their best to reduce costs and create the best conditions for the banks to supply regular market loans, but there remains a considerable need for additional (non-)fi -nancial help.

Conclusions

All the recommendations described above are based on the experiences of the ECO-FIN-NET partner cities with one general framework and two common rules:

The general framework concerns the sustainability of support systems:

It has been indicated that this goal can be achieved by a partnership with other public and private bodies. In particular, the ECO-FIN-NET partner cities wish to emphasize that the “Ac-quis URBAN” is to be integrated in the next programming period and that the appropriate measures will be integrated into EU mainstream funding.

10

1

11

The two rules are:

1. Effi cient support instruments to improve the access of SMEs to fi nance are designed as a package or combination of fi nancial and non-fi nancial services that are well adapted to the requirements of small businesses.

2. Part of the cities’ decision is to take the initiative and build up partnerships between pub-lic and private entities in their environment so that they can deliver these services effi -ciently to small businesses.

The conclusions of ECO-FIN-NET regarding future support for SMEs, both fi nancial and non-fi nancial, form an important part of an integrated urban policy for the disadvantaged urban areas. The suggested measures to strengthen local economy, particularly micro and small businesses, are contributing to a signifi cant stabilisation and revitalisation of disadvantaged urban areas.

13

1 Cities’ actions in favour for SMEs

Today, cities all over Europe are facing huge problems.

The far-reaching structural economic change during the last decades in Europe had nega-tive effects on cities and urban areas in gen-eral that are particularly apparent in the in-ner cities and surrounding areas, but also in the mono-structural large housing estates on the outskirts of the cities – and this even in prosperous regions. In these deprived ur-ban neighbourhoods the economic outlook is bad, generally the buildings are in a struc-turally poor condition and the quality of life is very low. And where these areas also suf-fer from high crime rates, they are frequent-ly referred to as “social hotspots”. These signifi cant disparities in economic and so-cial opportunities damage the attractive-ness, competitiveness, social inclusiveness and safety of cities. Thus the situation also impacts negatively on the economic growth and wealth of a city. Without taking appro-priate countermeasures, in the medium and long term these tendencies will affect more prosperous city regions, since they radiate negative settlement and development in-centives.

The EU Initiative URBAN

In order to respond appropriately to these trends, the European Commission launched the URBAN Pilot Projects (UPP) in 1990 and following this the URBAN I Community Initiative in 1994. In a type of European ex-perimental ground for urban regeneration, innovative approaches were put to the test. The keynote behind URBAN was to take into account all the dimensions of urban life in the context of the urban development pro-grammes and to have all the relevant play-ers participate in their implementation. Spe-cial characteristic of the programmes was their integrated, area based and concen-trated approach: Funds from various public sources as well as different competencies in urban matters are pooled and directed at a relatively small urban area subject to seri-ous problems. And the strong participation and information of local inhabitants is a key element in integrated urban development concepts.

In more than ten years of existence, the UR-BAN Community Initiative, using the fi eld-tested integrated, cross-sector and partici-pative development approach, contributed signifi cantly to the sustainable stabilisation and revitalisation of urban areas in diffi cul-ties. Measures to strengthen local economy, to promote employment and social integra-tion as well as to address urban planning, infrastructure and environmental issues signifi cantly improved the quality of life of local inhabitants. Due to these good experi-ences and evaluations, the programme UR-BAN was continued in 2000 as URBAN II.

The URBACT programme

Taking into consideration the successes of U.P.P. and URBAN, the European Com-mission launched in 2003 the programme URBACT. With this programme, the Europe wide exchange of cities in the fi eld of inte-grated urban development is supported. The programme serves:

• the exchange of innovative ideas and approaches in the notion of “good prac-tices“,

• the improvement of methods for an inte-grated urban development,

• the preparation of political recommen-dations concerning urban development in the context of the EU Cohesion Policy post-2006.

The URBACT programme focuses on all cit-ies that have already been funded within the framework of Urban Pilot Projects (UPP) or the Community Initiatives URBAN I and/or URBAN II and have therefore been able to gain a lot of experience with integrated con-cepts for the regeneration and revitalisation of disadvantaged districts. Furthermore, cities from the new member states with a population of more than 20,000 are being invited to participate in the programme.

URBACT is not just a straightforward sum-mary of the URBAN cities’ experiences, but has acquired an additional dimension as the result of shared discussion between various cities and on several issues and approach-es. URBACT materialised this additional di-mension.

The URBACT partner cities have brought a signifi cant contribution:

The cities felt in debt for receiving URBAN funding and they have delivered information on their experience. They sent representa-tives in work group discussions to prepare

1

15

1

well adapted recommendations. They also contributed fi nancially to an important part (50% of the URBACT networks‘ budget).

And they have expectations. In an integrated approach, the experiences of the other part-ner cities are of interest for them because they may give an added value to their own experiences. Consequently, they wish this programme to be continued.

The method used in URBACT consists main-ly in partner cities’ thematic networks that cover the main issues of integrated urban development. In these networks, the part-ner cities discuss comparable problems concerning urban revitalisation with other cities of other member States and thereby establish a generally accessible knowledge base. Each network is dealing with a specif-ic topic, such as urban regeneration, citizen participation or economic activity.

1.1 The ECO-FIN-NET network rationale

Since the development of local micro, small and medium sized enterprises (SMEs) plays an important role regarding integrated strategies, the network ECO-FIN-NET has been established. It covered the issue of the support of SMEs and focussed on the access to fi nance for SMEs, and particularly the smallest ones, in the less favoured urban areas with innovative fi nancial instruments. 13 cities in 10 European member states, led by the City of Leipzig, Germany, constitute this network.

1.1.1 Background

One of the main goals of the European Agenda, namely increasing growth, com-petitiveness and innovation, has been es-pecially promoted by the U.P.P. and URBAN programmes on the local level. Contrary to most national or regional approaches to ur-ban regeneration, the URBAN programmes place clear emphasis on economic develop-ment. Many cities launched special funding schemes for SMEs through which grants to existing businesses and start-ups are pro-vided for establishing, expanding, modern-ising their business premises or safe-guard-ing their business location. The local econ-omy is also supported through targeted ad-vice and services, the creation of business networks, the establishment of technology, start-up and trade centres as well as city (district) marketing or shopping street man-agement.

There is a fi rm belief that the respective measures not only strengthen local entre-preneurship, but also revitalise the econom-ic and social situation of the districts. This in turn helps to upgrade the whole neighbour-hood, increases the attractiveness and im-age and strengthens the commitment of the inhabitants to their neighbourhood, which fi nally leads to an improvement in the qual-ity of life.

1.1.2 SMEs as one of the main motors for economic development

The cities have therefore put their attention on the SMEs located on their territory be-cause the SMEs are one of the main motor for economic development. Micro, small and medium-sized enterprises represent more than 95% of all enterprises in the European Union and this percentage is even higher in the less favoured areas. These areas are

14

1

The ECO-FIN-NET network

15

To simplify the reading of

this report , the general term

SME is used in the follow-

ing, emphasizing that this

contains for the ECO-FIN-NET

also and specifi cally the

micro businesses.

characterised by a smaller rate of entrepre-neurship than the average and this moti-vates the cities to pay particular attention to all sorts of businesses and entrepreneur-ial projects, even the smallest businesses’ projects. Assistance to SMEs is one vital el-ement to improve the local economy and to create new opportunities in disadvantaged areas. The ECO-FIN-NET focuses on this spe-cifi c dimension.

Micro, small and medium-sized enterprises are playing a socially and economically ma-jor role, not only at local level:

• SMEs are a necessity for a diversifi ed economy: The growth of SMEs is vital for a diversifi ed economy. A great va-riety implies a necessary adaptability of the economy. Many small fi rms can more easily adapt to new chances and challenges. There is a tendency in most European countries that on the one hand large enterprises decrease and on the other hand SMEs increase in numbers and thereby creating more jobs than large businesses.

• SMEs are mainly contributing to equal opportunities: SMEs give also the op-portunity for a city to benefi t optimally of the diversity of the population, includ-ing ethnic minorities. The creation of a sound environment where start-ups can breed and grow is then a relevant part of the policy. The reasons for such a policy lay in the objective of poverty alleviation and empowerment of certain groups in deprived areas.

• SMEs are mainly contributing to upgrad-ing disadvantaged neighbourhoods: SMEs play an important role for the socio-economic stabilisation, the vital structure and function of urban quarters. They provide inhabitants with goods and services and create or secure jobs that are well embedded in the neigh-bourhood. Apart from the vital and ad-equate availability and use of premises, reasonable height of rent levels – often combined with a broader integrated ap-proach of urban regeneration and renew-al, the quality of the entrepreneurs and their possibilities to develop are crucial. This softer side of governmental concern for SMEs is often combined with specifi c targeted measures to uplift the skills of the entrepreneurs. This must lead in the end to a better access of entrepreneurs to fi nance in order to develop their enter-prise in the right direction.

1.1.3 The ECO-FIN-NET’s view on busines-ses

The term of business should be accepted in a broad sense in terms of ownership status (private, public, social economy) and size (big, small, micro, self employed). Very often in less favoured areas it consists in project ideas that some individuals think of implementing to generate some form of income.

The offi cial term used by the European Com-mission is “Micro, Small and Medium Sized Enterprises (SMEs)”. Micro enterprises have less than ten employees and a turnover of maximum two million Euro per year. Small enterprises are defi ned as enterprises with less than 50 employees and an annual turn-over of maximum ten million Euro, whereas medium-sized enterprises have up to 250 employees with a turnover of maximum 50 million Euro per year.

The ECO-FIN-NET rather concentrates its re-fl ection on the micro and small businesses – either formal enterprises or individual projects – as these projects form the biggest part of the local economy in disadvantaged urban areas. Besides, the ECO-FIN-NET part-ners see the support of these businesses as part of their local urban policy. This explains why in some cases the support of a specifi c entrepreneur can make sense for a local au-thority – e.g. in contrary to a fi nancial insti-tution – as its support is seen from a differ-ent angle.

200 km

Evosmos

Gera

GermanHousing

Association

Vilnius

Gdansk

Marseille

Grenoble

Rotterdam

Venezia

Wien

Birmingham

Gijon

LEIPZIG

ASDAASDA

Evosmos

Gera

GermanHousing

Association

Vilnius

Gdansk

Marseille

Grenoble

Rotterdam

Venezia

Wien

Birmingham

Gijon

LEIPZIG

1.2 SME Support – a core task for local governments

As SMEs are contributing to create eco-nomic wealth and growth, the care for SMEs becomes a core task for local governments. And particularly micro and small businesses also expect support services at local level. They prefer that services be delivered to them at local level.1 This can be explained by the fact that the normal environment small businesses are familiar with, is the lo-cal level. This is the level they are naturally in contact with. And it is convenient to have a service provider nearby.

So, cities can do and have to do something in favour for their local businesses. The dis-advantages especially small and micro busi-nesses in derelict areas are facing, call for compensation, which justifi es special pub-lic support. Local authorities have to take action to develop economic activity in the distressed parts of their territory, to render those areas more attractive and to make business opportunities easier to develop.

But the general characteristics of the less favoured areas are that market conditions are not prevalent, and the few projects that may have a local economic impact should have a chance to develop. The fact that market economy conditions are not fully prevalent in these areas, in other terms, the fact that there is a need to compensate the development gap between these areas and other more developed areas, gives ad-ditional legitimacy for public support. This means that the public authorities in charge of these areas have no other choice than providing some form of support for these businesses/projects.

The economic development support should help to activate endogenous potentials, but also attract new businesses from outside. The geographic perspective of local busi-ness promotion should therefore not be lim-ited to the deprived quarter and the small and micro businesses but also show a wider urban or regional focus, as for some branch-es and enterprises the local markets are too limited. Service providers should bear this information in mind very carefully as if, for obvious reasons of critical mass effect or economies of scale, some services need to be designed at regional or national level, they should be delivered at local level for the small businesses to be fully receptive to them (DG Enterprises 2002a).

1.3 SMEs’ needs and requirements

It seems obvious that successful support services should be tailored to their end us-ers, especially the smallest businesses since larger enterprises have a greater capac-ity of adaptation. What are the businesses’ expectations towards local SME support? What are their main concerns?2

Access to fi nance is a very important issue.

One of the main concerns of SMEs is their access to fi nance. All businesses require ac-cess to fi nance for:

• Starting an activity: starting capital is re-quired.

• Financing business growth: investments in premises, equipment, technology, re-search and development, prospecting new markets. All these activities need direct fi nancing.

• Working capital to fi nance the gap be-tween the dates of payments of the purchased goods and services, staff and other costs and the customers’ pay-ments.

• Business transfers.

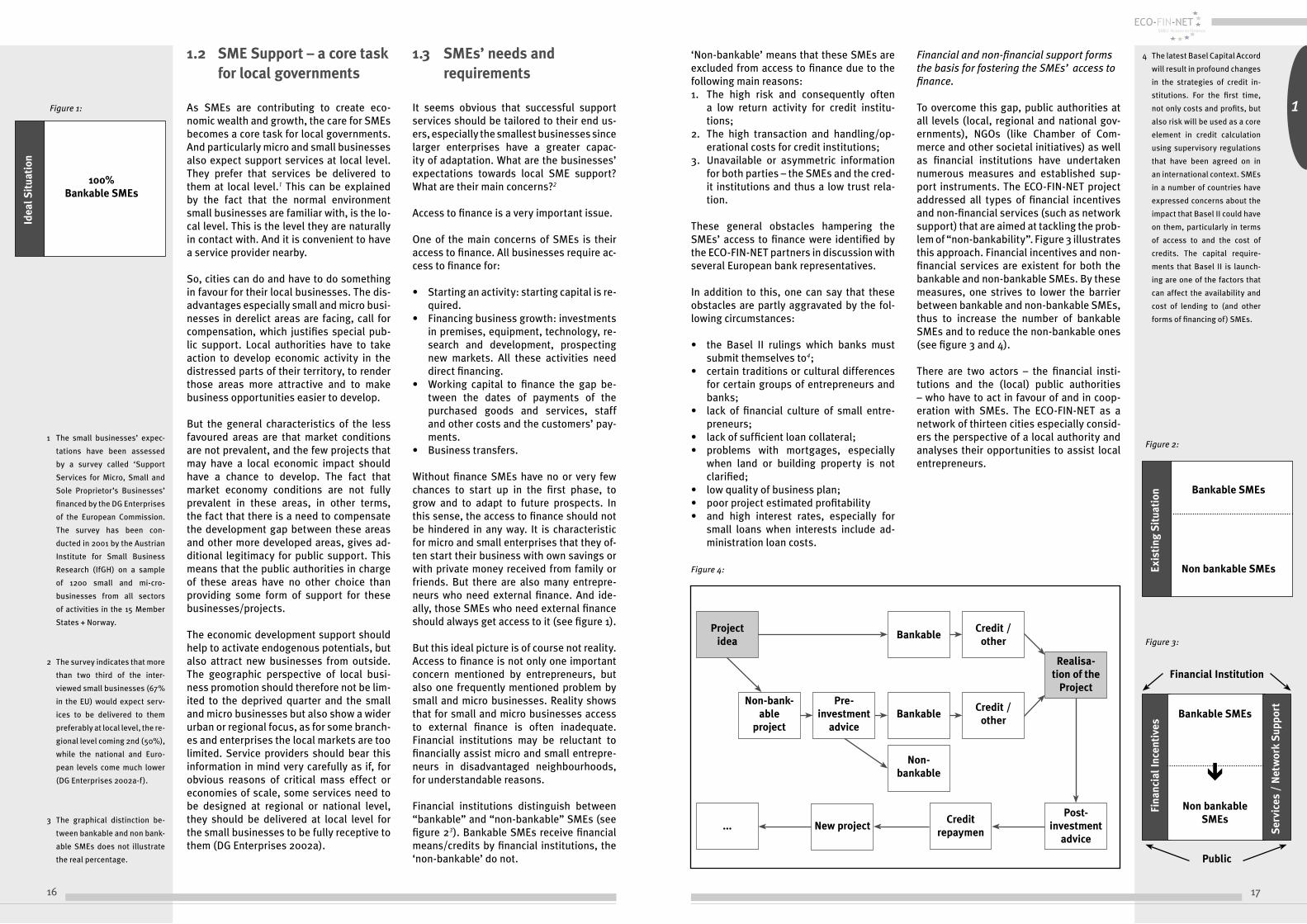

Without fi nance SMEs have no or very few chances to start up in the fi rst phase, to grow and to adapt to future prospects. In this sense, the access to fi nance should not be hindered in any way. It is characteristic for micro and small enterprises that they of-ten start their business with own savings or with private money received from family or friends. But there are also many entrepre-neurs who need external fi nance. And ide-ally, those SMEs who need external fi nance should always get access to it (see fi gure 1).

But this ideal picture is of course not reality. Access to fi nance is not only one important concern mentioned by entrepreneurs, but also one frequently mentioned problem by small and micro businesses. Reality shows that for small and micro businesses access to external fi nance is often inadequate. Financial institutions may be reluctant to fi nancially assist micro and small entrepre-neurs in disadvantaged neighbourhoods, for understandable reasons.

Financial institutions distinguish between “bankable” and “non-bankable” SMEs (see fi gure 23). Bankable SMEs receive fi nancial means/credits by fi nancial institutions, the ‘non-bankable’ do not.

‘Non-bankable’ means that these SMEs are excluded from access to fi nance due to the following main reasons: 1. The high risk and consequently often

a low return activity for credit institu-tions;

2. The high transaction and handling/op-erational costs for credit institutions;

3. Unavailable or asymmetric information for both parties – the SMEs and the cred-it institutions and thus a low trust rela-tion.

These general obstacles hampering the SMEs’ access to fi nance were identifi ed by the ECO-FIN-NET partners in discussion with several European bank representatives.

In addition to this, one can say that these obstacles are partly aggravated by the fol-lowing circumstances:

• the Basel II rulings which banks must submit themselves to4;

• certain traditions or cultural differences for certain groups of entrepreneurs and banks;

• lack of fi nancial culture of small entre-preneurs;

• lack of suffi cient loan collateral;• problems with mortgages, especially

when land or building property is not clarifi ed;

• low quality of business plan;• poor project estimated profi tability• and high interest rates, especially for

small loans when interests include ad-ministration loan costs.

Figure 4:

Financial and non-fi nancial support forms the basis for fostering the SMEs’ access to fi nance.

To overcome this gap, public authorities at all levels (local, regional and national gov-ernments), NGOs (like Chamber of Com-merce and other societal initiatives) as well as fi nancial institutions have undertaken numerous measures and established sup-port instruments. The ECO-FIN-NET project addressed all types of fi nancial incentives and non-fi nancial services (such as network support) that are aimed at tackling the prob-lem of “non-bankability”. Figure 3 illustrates this approach. Financial incentives and non-fi nancial services are existent for both the bankable and non-bankable SMEs. By these measures, one strives to lower the barrier between bankable and non-bankable SMEs, thus to increase the number of bankable SMEs and to reduce the non-bankable ones (see fi gure 3 and 4).

There are two actors – the fi nancial insti-tutions and the (local) public authorities – who have to act in favour of and in coop-eration with SMEs. The ECO-FIN-NET as a network of thirteen cities especially consid-ers the perspective of a local authority and analyses their opportunities to assist local entrepreneurs.

16

1Figure 1:

1 The small businesses’ expec-

tations have been assessed

by a survey called ‘Support

Services for Micro, Small and

Sole Proprietor’s Businesses’

fi nanced by the DG Enterprises

of the European Commission.

The survey has been con-

ducted in 2001 by the Austrian

Institute for Small Business

Research (IfGH) on a sample

of 1200 small and mi-cro-

businesses from all sectors

of activities in the 15 Member

States + Norway.

2 The survey indicates that more

than two third of the inter-

viewed small businesses (67%

in the EU) would expect serv-

ices to be delivered to them

preferably at local level, the re-

gional level coming 2nd (50%),

while the national and Euro-

pean levels come much lower

(DG Enterprises 2002a-f).

3 The graphical distinction be-

tween bankable and non bank-

able SMEs does not illustrate

the real percentage.

17

4 The latest Basel Capital Accord

will result in profound changes

in the strategies of credit in-

stitutions. For the fi rst time,

not only costs and profi ts, but

also risk will be used as a core

element in credit calculation

using supervisory regulations

that have been agreed on in

an international context. SMEs

in a number of countries have

expressed concerns about the

impact that Basel II could have

on them, particularly in terms

of access to and the cost of

credits. The capital require-

ments that Basel II is launch-

ing are one of the factors that

can affect the availability and

cost of lending to (and other

forms of fi nancing of) SMEs.

Figure 2:

Figure 3:

Idea

l Sit

uati

on

100% Bankable SMEs

Fina

ncia

l Inc

enti

ves

Bankable SMEs

Non bankable SMEs

Ser

vice

s /

Net

wor

k S

uppo

rt

Exis

ting

Sit

uati

on

Bankable SMEs

Non bankable SMEs

Bankable

Non-bank-able

projectBankable

Non-bankable

Post-investment

advice

Credit repaymen

New project...

Credit / other

Credit / other

Project idea

Pre-investment

advice

Realisa-tion of the

Project

Public

Financial Institution

1.4 Need of an integrated lo-cal SME strategy

1.4.1 Three main support pillars

In order to solve the various problems that SMEs are facing, the ECO-FIN-NET empha-sizes that the future SME Support Policy must be based on three pillars which at the end form one integrated and consistent support package for the local economy. For each of these three themes, ECO-FIN-NET set up a work group with experienced cities’ representatives and external expertise:

1 Private Financial Support Facilities for SMEs

The usual source of external fi nance for businesses is banks and other fi nancial in-stitutions. SMEs direct themselves fi rst to banks when they need external fi nance. But as the allocation of credits to SMEs involves inherently a high risk of failure, often a low return activity and high handling costs, banks are often very reluctant to fi nancially assist SMEs. Cities have the possibility to help solve these problems.

Work group 1 of the ECO-FIN-NET discussed and developed new approaches on how lo-cal authorities can face these obstacles and how they can foster the SMEs’ Access to Fi-nance (see chapter 2.1).

2 Public SME Support

For several years, the cities have designed fi nancial support for the development of businesses and start-ups (grants, loans etc.). Today there are already various SME support schemes at a local level operating – directly or indirectly – with EU-funding. But with regard to the enlargement of the European Union and the lack of visibility for the Structural Policy from 2007 on, cit-ies are confronted with new challenges, as especially EU-funds will – at least for the former 15 member states – not increase in the future. Thus, it will become more and more crucial for cities to search for other in-novative ways and approaches for support-ing SMEs. Instead of direct public subsidies, the take-up of private fi nancial tools and a strong local partnership between public organisations and fi nancial institutions are more and more needed.

The work group 2 of the ECO-FIN-NET has questioned the relevance of public support instruments, in particular their adaptation

to the specifi c conditions required by micro and small businesses in the less favoured areas. Besides, the partners searched for ways and strategies on how public fi nan-cial means for SME support can be used in a more effi cient and effective way and how the expectations of SMEs towards public sector funds can be met, even in times of di-minishing public means (see chapter 2.2).

3 SME Support Services / SME-networks

In addition to the fi nancial support of SMEs, cities are in many ways in charge of or in-volved in delivering non-fi nancial services and network support to SMEs. These are an important part of local SME Support Policy throughout Europe.

These services often include the organisa-tion of network support or the offer of coach-ing, mentoring or other advisory services. By increasing the “bankability” of entre-preneurs, those non-fi nancial services can have a positive leverage effect for external fi nance and improve the SMEs’ access to fi -nance. Besides, they constitute widespread instruments to create generally a positive environment for businesses.

The work group 3 of the ECO-FIN-NET worked out the main challenges as well as success factors of those support services and stud-ied the services best targeted at improving SMEs’ access to fi nance (see chapter 3).

More generally, ECO-FIN-NET paid particular attention to the possibilities of maximising the public support impact by various forms of partnership with other public or private entities; all the more in the current context of dwindling public fi nancial resources, when the cities aim at doing more with less direct funding.

1.4.2 Different local contexts

Besides these three pillars, different con-texts have to be kept in mind whilst look-ing at the ECO-FIN-NET cities’ approaches. SME Support Policy must always respect the local conditions and circumstances un-der which a local authority acts. Firstly, the national, regional and local frameworks are differing much. For instance, the tradition of the more developed fi nancial market in Great Britain than on the continent causes signifi cant differences between the fi nan-cial systems of the concerned countries. In some countries savings banks are involved in local economy whilst they simply do not exist in other countries. These differences

could not be analysed in depth by the ECO-FIN-NET. Therefore, the recommendations drawn in this report are put in a rather general context.

Secondly, there are different types and situ-ations of so called less favoured urban ar-eas. Two main situations have been identi-fi ed by the partner cities:

• Specifi c disadvantaged neighbourhoods located in developed areas (so called “pockets of poverty”) which can be ei-ther in the centre or in the suburbs of the city. Here, there is the necessity for the cities to support even very small individ-ual entrepreneurial projects.

• All the territory of the city is included in an area lagging behind in development (e.g. classifi ed by the European Union as “objective 1”-area) with the main is-sue being access to mainstream support for all the projects including the smallest ones. Unfortunately, the same situation applies in some former objective 1-areas with the additional constraint of dwin-dling fi nancial EU support.

The ECO-FIN-NET underlines that these dif-ferences may imply different approaches to the SME support, the main consequence of which is that in the latter case very small projects (individual entrepreneurs) may not be considered with the same care/attention as in the “pockets of poverty”.

1.4.3 Strong local partnership

In order to face the existing barriers, inte-grated and consistent packages of fi nancial and non-fi nancial support are necessary. Only integrated and coordinated strategies make measures most effective. Besides, every target group should be offered the service that is appropriate for their situa-tion. Those integrated (fi nancial) packages targeted at the specifi c needs of the entre-preneurs can only be offered by a strong and trustful local partnership of different local actors – the banks, the local authority, the Chambers and business associations, the service providers etc. and the SMEs them-selves. They all have to cooperate in order to comfort existing successful schemes and to take over their respective responsibility regarding SME Support.

1

19

A strong and trustful partner-

ship of the local authority,

the banks, the Chambers and

business associations, the

service providers and the

SMEs is needed at local level.

ECO-FIN-NET Partners

Marseille 2006

18

Figure 5:

Three work groups of the

ECO-FIN-NET

WG 1 Private Financial

Support Facilities

for SMEs

Chapter 2.1

WG 2 Public SME Support

Chapter 2.2

WG 3 SME Support Serv-

ices / SME-networks

Chapter 3

2020

2

21

2

21

2

21

2 Fostering the SMEs’ Access to Finance by fi nancial incentives

As the English say, the natural way for small businesses to have access to fi nance is with the three “Fs”: “family, friends and fools”. Unfortunately, this resource is not always suffi cient and access to external fi nance is done by the banks and other fi nancial in-stitutions. But in the less favoured areas, the banks may be reluctant to take commit-ments with entrepreneurs who operate in a diffi cult environment.

On the other hand, in these disadvantaged areas, in order to create wealth for the lo-cal population, no opportunity of business development should be neglected and, if only viable economic development projects should be given a chance to develop, the concept of viability is probably made more fl exible in these areas. As a consequence the projects should be considered with even more care than in other more developed ar-eas, and the public authorities have the ob-ligation to give some incentives to compen-sate for the banks’ possible reluctance.

Among the various public authorities, the local ones, the cities are those that are most accepted (legitimate) by the small busi-nesses.

Of course before imagining any form of di-rect support to their businesses, they should make sure that their general environment is “small business friendly”, which implies at least:

• adequate local taxes, in particular with regard to the neighbouring municipali-ties,

• a good information on the local business community and its expectations: this is the role of the business observatories,

• a possibility of dialogue with the busi-nesses through their representative bodies: this can be problematic in the less favoured areas as it is indicated in chapter 2.2.1.

The cities can also envisage direct support to the businesses located on their territory. The main stakeholders involved in SMEs’ access to fi nance are:

• the SMEs themselves with their business associations,

• the banks and other fi nancial institu-tions,

• and the public authorities including the cities at local level.

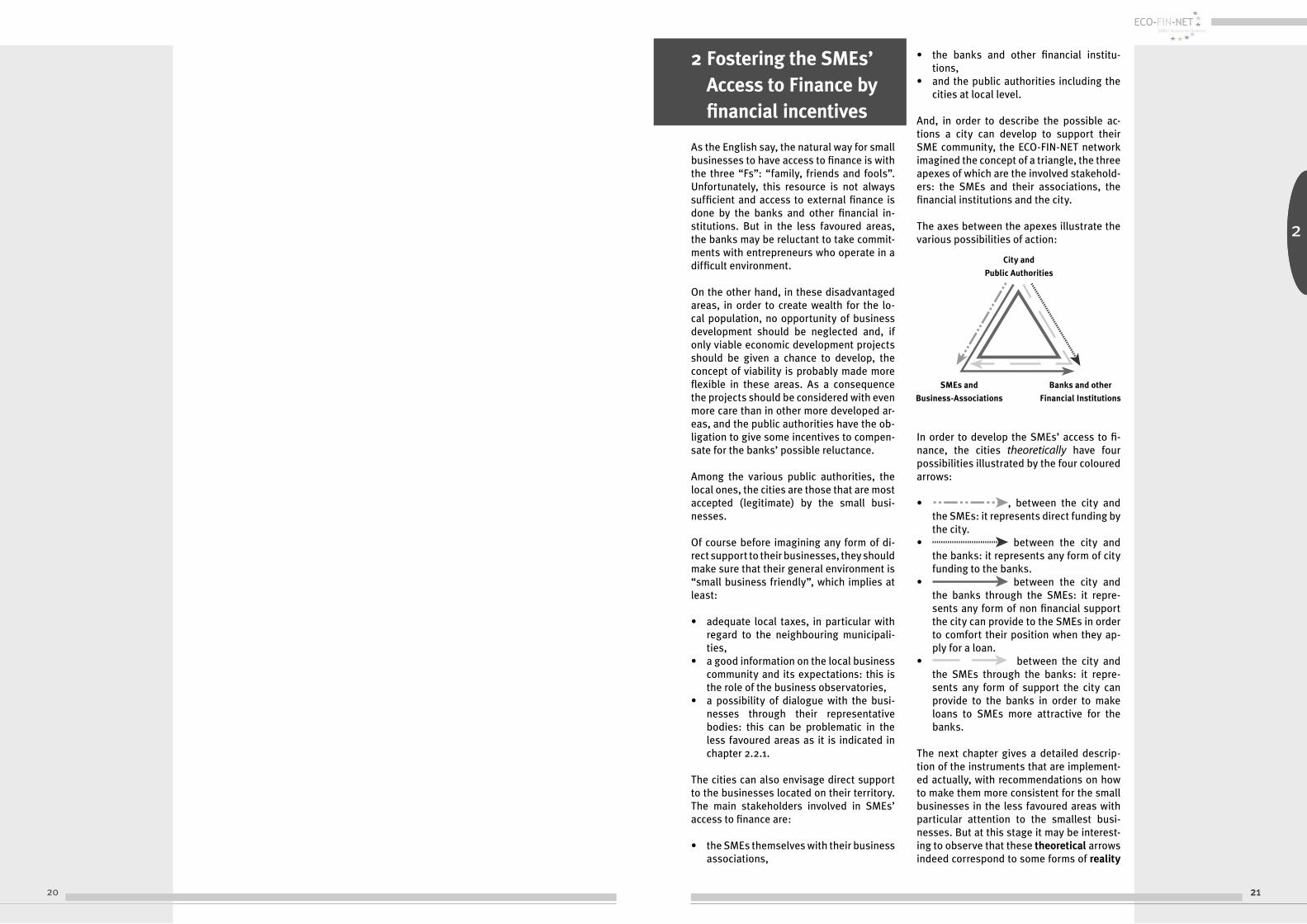

And, in order to describe the possible ac-tions a city can develop to support their SME community, the ECO-FIN-NET network imagined the concept of a triangle, the three apexes of which are the involved stakehold-ers: the SMEs and their associations, the fi nancial institutions and the city.

The axes between the apexes illustrate the various possibilities of action:

In order to develop the SMEs’ access to fi -nance, the cities theoretically have four possibilities illustrated by the four coloured arrows:

• , between the city and the SMEs: it represents direct funding by the city.

• between the city and the banks: it represents any form of city funding to the banks.

• between the city and the banks through the SMEs: it repre-sents any form of non fi nancial support the city can provide to the SMEs in order to comfort their position when they ap-ply for a loan.

• between the city and the SMEs through the banks: it repre-sents any form of support the city can provide to the banks in order to make loans to SMEs more attractive for the banks.

The next chapter gives a detailed descrip-tion of the instruments that are implement-ed actually, with recommendations on how to make them more consistent for the small businesses in the less favoured areas with particular attention to the smallest busi-nesses. But at this stage it may be interest-ing to observe that these theoretical arrows indeed correspond to some forms of reality

City and

Public Authorities

SMEs and

Business-Associations

Banks and other

Financial Institutions

22 23

2

with support instruments that have already been implemented by the ECO-FIN-NET part-ner cities:

Direct relation between the city and the SMEs

These are the instruments with which the cities provide direct funding to their SMEs: it generally consists in grants or loans that can be specifi cally targeted at some busi-nesses and/or in some specifi c areas. In practice, grants are more widely used than direct loans, since the latter require specifi c expertise, longer management procedures and can be contracted with specialised in-stitutions (see next arrow).

Examples:

City of Birmingham: Business Investment

Scheme grants + loans + venture capital),

Enterprise City scheme providing targeted

entrepreneurs with a comprehensive package of

coaching, funding and services, West Midlands

Inclusive Fund targeted at specifi c ethnic and

religious entrepreneurs

City of Gera: grant scheme

City of Gijón: Equal micro credits, entrepreneur

micro credit scheme

City of Leipzig: grant scheme

City of Marseille: public micro credit scheme

with the “platform for local initiative” being a

member of the national network of local micro

credit funds France Initiative Réseau,

City of Vienna: grant schemes for start-ups,

founders’ bonus, for retail shops, for infra-

structure support and for internationalisation

City of Vilnius: grant schemes

Relation between the public author-ity and the bank/fi nancial institution

The cities can provide funding to fi nancial institutions for loans to the local business-es: in some cases the funding is entirely (or almost) public and directed to the business-es as in the case of public micro credit funds funded by the city (see previous arrow), but in some cases, a partnership is developed with private donors or investors to create micro credit funds. The city can contribute to the fund capitalisation and/or to their operational costs, for the business projects located in the areas targeted by the cities.

They also provide funding to loan guarantee schemes (capitalisation and/or operational costs) or venture capital:

Examples:

The City of Birmingham participating in the

capital of the micro credit Arrow Fund

The City of Gdańsk participating in the Regional

Guarantee Scheme

The City of Gijon participating in a micro credit

scheme with the savings banks Caixa

The City of Leipzig with the “concept venture

capital light” with a city subsidy to the venture

capital institution (savings bank) for small

projects

The City of Marseille: public micro credit

scheme, initiated by the City, co-funded by

other public bodies (regional and national) and

private donors (large businesses)

The City of Vienna granting loans in coopera-

tion with the Economic Chamber

City actions directed to the banks through the SMEs

This concerns non-fi nancial support to en-trepreneurs in order to facilitate their access to fi nance with fi nancial institutions (gen-erally for loans). In this respect, two main lines are considered:

a) Pre-investment support is important for the investment readiness of a business proposal. One has to check if a project is viable before fi nancing or funding it.

b) But also post-investment support is very important in order to make sure that the investment remains viable and to ensure that the funding revolves.

Examples:

Advisory support services for the preparation

of loan applications or business plans were

presented by the Cities of Evosmos, Leipzig,

Marseille, Vienna and Vilnius.

The City of Gijon: business network called

“Nautical Station”

The City of Grenoble is partner in the ECTI-or-

ganisation that delivers mentoring services

The City of Leipzig and Gera create business

networks.

The City of Marseille engaged the SAP project

aiming to enforce project ideas to become a real

business idea

The City of Rotterdam-Delfshaven: Mentorraad-

project offering mentoring services

The City of Rotterdam-Delfshaven: voucher

system

The City of Vienna initiated the “Grätzelman-

agement”

West Athens: reached the entrepreneurs effec-

tively by ITC-improvement projects

City actions directed to the SMEs through the banks

These actions are widely used: they concern the loan guarantee schemes and the type of subsidy that has been indicated in the previ-ous chapter. They are described in detail in chapter 2.2.

Examples:

Regional Guarantee Fund with participation of

the city: Gdańsk

Very often SME loan guarantee schemes are op-

erated at regional level as in France, Germany

or Poland or at national level as the national

bank for SMEs BDPME/SOFARIS in France or the

national guarantee scheme in Austria.

2.1 Private Financing

As it has been indicated in the previous chapter, the usual source of external fi nance for businesses is banks and other fi nancial institutions (micro credit institutions). The problem rises when the lending organisa-tions are, for understandable reasons, re-luctant to fi nance some projects. These rea-sons are:

1. The lack of suffi cient collateral which results in an increased fi nancing risk for the lending institutions; if this increased risk is refl ected in the interest rate of a loan given to the enterprise in question, this interest rate is likely to be too high to be accepted by the entrepreneur.

2. The high cost of loan application and processing in relation to the small amount of credit: in practice, these costs cover the work of preparing the loan ap-plications by the SMEs and of the risk assessment and processing by the lend-ing institutions. The former are directly supported by the SMEs, the latter are normally covered by the interests paid by the debtors, in this case the SMEs (charged indirectly). For very small projects, implying small amounts of funding and thus small loans, the entre-preneurs often have a limited fi nancial culture, which results in poor loan appli-cation preparation and additional costs for the lending institutions. Charging these costs through the loan interests’ results in too high rates to be commer-cially acceptable or even illegal rates in countries where the interest rates are capped by law.

3. The lack of information or track record with the small businesses: this informa-tion is the basis for the fi nancial institu-tions to take decisions on business loan applications. Very often in the small businesses, the management informa-tion system is rather primitive and it is not the main priority for the entrepre-neur. This lack of information reinforces the high risk assessment indicated in chapter 1.

The ECO-FIN-NET participants have tried to address possible solutions for these prob-lems:

• How to lower or share the risk for the banks with the small business loan ap-plications in the less favoured areas?

• How to reduce the cost of the application and processing for small loans?

• How to improve the quality of the infor-mation on enterprises to the level re-quired by the banks in the loan applica-tion process without putting a too heavy administrative burden on the small busi-nesses that cannot afford a well staffed administrative structure?

2.1.1 High level of risk assessed by the banks for SME loans

Guarantee funds are an effi cient and widely used instrument aimed at facilitating access to credit for small businesses, at any stage of their development, by sharing the risk with the lending institutions. It has been widely used in most of the EU countries for several decades since the end of the 2nd World War. These funds obviously are the solution for the banks to accept loan appli-cations with a higher level of risk. The cities can usefully participate in these funds for their less favoured areas with some condi-tions that the ECO-FIN-NET partner cities have highlighted.

There is no point in giving a detailed de-scription of the business loan guarantee schemes in this paper, but some features should be underlined:

• Their fi nancial resources come from guarantee fees paid by the borrowers, the income from their investments and the subsidies they may receive.

• A guarantee fund is characterised by its leverage ratio. This ratio depends on two essential factors: the percentage of risk taken by the fund and the probability of borrower’s default. Other factors are also important: the return on investments,

25

2

the recovery of losses and the guarantee fee paid to the guarantee fund.

• The lower the risk and the higher the leverage ratio, the stricter the risk ap-praisal and the higher the ratio, with the possible counter-productive effect that a guarantee fund that would only approve risk-free applications would loose its « raison d’être » which is to encourage banks to be active on a market segment they assess as too risky.

• Fine-tuning this contradiction is not easy. It mostly lies on experience and the eco-nomic situation that condition the risk of business failures. For instance, the lever-age ratio of a guarantee fund dedicated to new businesses is around 6, and 22 for short-term loans that are much less risky.

This is the reason why a critical mass should be reached with guarantee funds (they should not be too small). In fact there are some experiences of cities setting up their own guarantee funds but these experienc-es generated poor results. The guarantee funds should generally operate at national or regional level (not local level that cannot allow for a suffi cient volume).

A good example of this necessary condition of a minimum critical mass is given by the City of Gdańsk (see at the left).

This critical mass effect also applies to the qualifi cations and the corresponding man-agement costs for these organisations and this condition generally implies that these guarantee funds be managed by specialised organisations, possibly with a credit institu-tion agreement: the examples of the French “Banque des PME” (BDPME/SOFARIS- bank for small and medium sized businesses) or the Regional Guarantee Schemes in Germa-ny illustrate this requirement:

In France, at national level, the biggest French company (BDPME/SOFARIS) special-ised in the management of SME guarantee schemes, receives funding from the central level and from French and European fi nancial institutions. They set up a subsidiary that organises partnerships with the regional authorities, to provide sound management of the regional guarantee funds, fi nanced with regional budget resources.

Their regional agencies appraise the appli-cations, prepare and manage the guarantee commitments. The funds’ fi nancial manage-ment is done at national level. There is no need for an additional structure. The re-

gional means are entirely dedicated to guar-antees. The operational costs are borne by the return on investments and part of the guarantee fees paid by the benefi ciary busi-nesses, allowing for a low cost procedure.

Additionally, the experience accumulated on several Regions and a large number of businesses make it possible for this fi nan-cial institution to guarantee the regions against the risk of funds’ shortage: with this procedure the Regions never take a commit-ment that can be higher than their budget allocation. If the risk rose to a higher level, it would be covered with the own resources of the fi nancial institution.