Embed Size (px)

Citation preview

Application No.: A.17-05-XXX

Exhibit No.: SCE-1 Witnesses: S. DiBernardo S. Liu E. Martinez T. Cameron E. Lavik R. Thomas D. Cox K. Seeto S. Lelewer M. Sheriff R. Hite D. Wong A. Wong

(U 338-E)

Energy Resource Recovery Account (ERRA)

2018 Forecast of Operations

Public Version

Before the

Public Utilities Commission of the State of California

Rosemead, California

May 1, 2017

SCE-1: ERRA Resource Recovery Account (ERRA) 2018 Forecast of Operations

Table Of Contents

Section Page Witness

-i-

I. INTRODUCTION .............................................................................................1 S. DiBernardo

II. 2018 ERRA FORECAST PROCEEDING REVIEW REQUIREMENT ...............................................................................................4

A. 2018 ERRA Forecast Proceeding Revenue Requirement ......................4

1. Functionalized ERRA-Related Revenue Requirement ..............5

a) ERRA-Related Generation Service Revenue Requirement ...................................................................6

III. SCE’S BUNDLED ENERGY FORECAST ......................................................8 E. Martinez

A. Retail Sales Forecast Summary .............................................................8

B. Methodology ..........................................................................................9

C. Historical Trends ..................................................................................10

D. Economic Outlook ...............................................................................12

E. Weather Assumptions ..........................................................................13

F. Other Factors Influencing the Forecast ................................................14

G. Total Retail Sales Forecast by Customer Class ...................................15

H. Customer Forecast ...............................................................................16

I. Annual and Monthly Bundled Energy .................................................17

IV. FORECAST ENERGY PRODUCTION AND COSTS FROM SCE’S PORTFOLIO OF RESOURCES .........................................................19 E. Lavik

A. Introduction ..........................................................................................19

B. Energy Production Forecast Methodology ..........................................19

C. Validation of SCE’s Energy Production Forecast ...............................21

D. 2018 Energy and Cost Forecast Summary ...........................................22

SCE-1: ERRA Resource Recovery Account (ERRA) 2018 Forecast of Operations

Table Of Contents (Continued)

Section Page Witness

ii

E. SCE’s Utility-Owned Generation and Purchased Power Contracts ..............................................................................................26

1. Hydro Facilities ........................................................................26

2. SCE Solar Photovoltaic Generation .........................................27

3. CHP and Renewables ...............................................................28

a) Energy Forecast ...........................................................28

b) Payment Forecast .........................................................29

c) Energy and Capacity Prices .........................................29

4. Utility-Owned Natural Gas Facilities ......................................30

a) SCE Peakers .................................................................30

(1) Background and Production .............................30

(2) Costs .................................................................30

b) Mountainview Generating Station ...............................30

5. Interutility Contracts Production ..............................................31 D. Cox

a) WAPA-Reclamation Agreement .................................32

b) Pasadena Corporation Grant Deed ...............................33

c) Interutility Contract Resource Costs ............................34

6. New System Generation CAM Contracts ................................34 E. Lavik

a) Production ....................................................................34

b) Costs .............................................................................34

7. 2013 Bilateral Contracts Production ........................................34

a) Production ....................................................................34

b) Costs .............................................................................35

SCE-1: ERRA Resource Recovery Account (ERRA) 2018 Forecast of Operations

Table Of Contents (Continued)

Section Page Witness

iii

8. Generic and Bilateral RA Contracts ........................................35

a) Production ....................................................................35

9. Local Capacity Requirements (LCR) Contracts ......................35

a) Production ....................................................................36

b) Costs .............................................................................36

10. Preferred Resource Pilot (PRP) ...............................................36

a) Production ....................................................................36

b) Costs .............................................................................36

11. Green Tariff Shared Renewables (GTSR) Program ................37

F. Other SCE Resources and Programs....................................................38 S. Lelewer

1. Nuclear .....................................................................................38

a) Production ....................................................................38

b) Costs .............................................................................38

(1) Introduction ......................................................38

(2) Nuclear Fuel Management ...............................39

(3) SONGS Nuclear Fuel Expense ........................39

(a) Fuel Expense – Generation Related .................................................39

(i) Permanent Disposition of Used Fuel .............................39

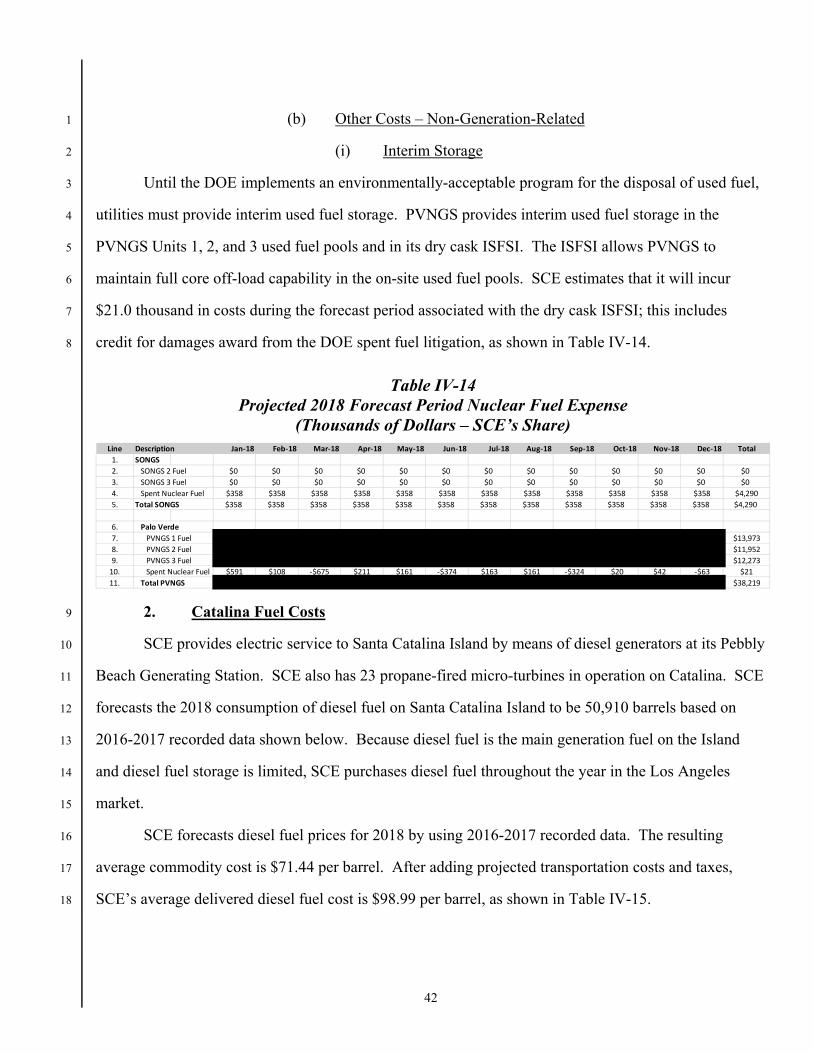

(b) Other Costs – Non-Generation-Related .................................................40

(i) Interim Storage.........................40

(4) PVNGS Nuclear Fuel Expense ........................40

SCE-1: ERRA Resource Recovery Account (ERRA) 2018 Forecast of Operations

Table Of Contents (Continued)

Section Page Witness

iv

(a) Fuel Expense – Generation Related .................................................40

(i) PVNGS Unit 1 .........................40

(ii) PVNGS Unit 2 .........................41

(iii) PVNGS Unit 3 .........................41

(iv) Permanent Disposition of Used Fuel .............................41

(b) Other Costs – Non-Generation-Related .................................................42

(i) Interim Storage.........................42

2. Catalina Fuel Costs ..................................................................42 R. Hite

3. Demand Response ...................................................................44 A. Wong

G. CAISO Costs and Short-Term Market Activity ..................................45 E. Lavik

1. CAISO Costs ............................................................................45

2. Short-Term Market Activity Costs ..........................................46

H. Gas Price Sensitivity ............................................................................46

I. Direct GHG Costs ................................................................................47

J. Gas Hedging Costs ..............................................................................47 S. Liu

1. Transaction Fees ......................................................................47

2. Option Premiums .....................................................................47

K. Gas Transportation and Storage ..........................................................47 D. Cox

1. Transportation ..........................................................................48

a) SoCalGas Transportation Agreement for Mountainview Generating Station ...............................48

SCE-1: ERRA Resource Recovery Account (ERRA) 2018 Forecast of Operations

Table Of Contents (Continued)

Section Page Witness

v

b) SoCalGas Transportation Agreements for UCSB and CSUSB .......................................................48

c) SoCalGas Transportation Agreements for SCE Peakers .........................................................................48

V. FINANCING COSTS .....................................................................................50 T. Cameron

A. Commission Decisions Regarding Financing Costs and Collateral Costs ....................................................................................50

B. SCE’s Current Short-Term Financings ................................................50

1. Credit Facilities (Revolvers) ....................................................50

2. Collateral Requirements ...........................................................51

3. Fixed Rate Bonds Supporting Fuel Inventories .......................52

4. Commercial Paper ....................................................................52

5. Costs of Collateral Issuance .....................................................53

C. Additional Options Supporting Collateral ...........................................53

VI. CARRYING COSTS .......................................................................................54

A. Fuel Inventory Carrying Costs .............................................................54

B. GHG Compliance Carrying Costs .......................................................55

C. Collateral Carrying Costs .....................................................................55

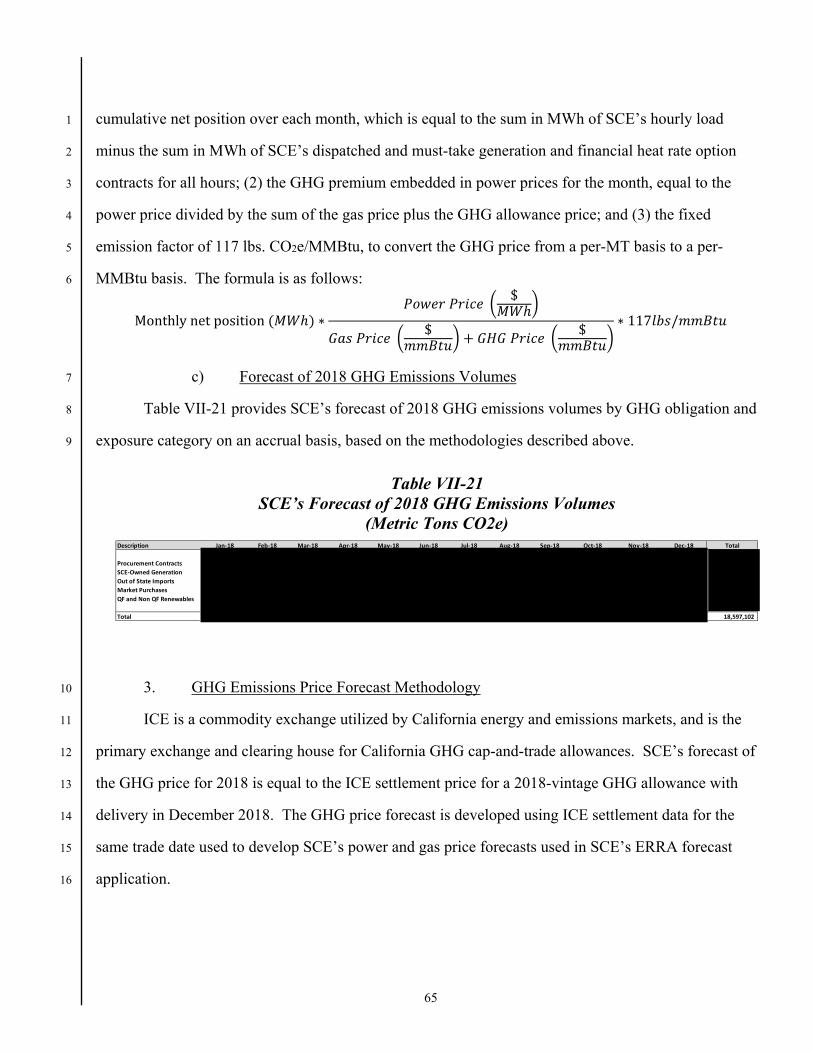

VII. GHG FORECAST COSTS AND REVENUES AND RECONCILIATION .......................................................................................57 M. Sheriff

A. Overview ..............................................................................................57

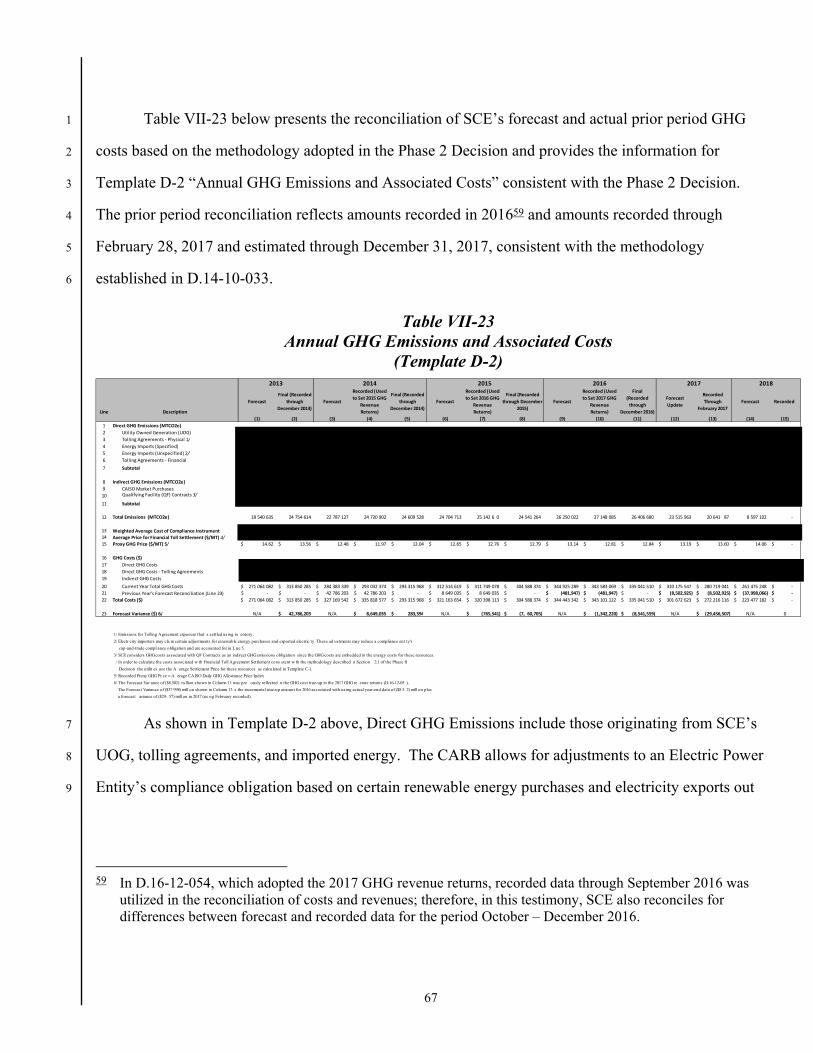

B. 2018 Cap-and-Trade Costs and Reconciliation of Prior Period GHG Costs ..........................................................................................58 K. Seeto

1. Sources of GHG Costs .............................................................59

a) Direct Costs ..................................................................59

SCE-1: ERRA Resource Recovery Account (ERRA) 2018 Forecast of Operations

Table Of Contents (Continued)

Section Page Witness

vi

(1) Compliance Costs ............................................59

(2) Procurement Contract Costs ............................60

b) Indirect Costs ...............................................................60

(1) QF Contract Costs ............................................60

(2) Market Purchase Costs .....................................61

2. GHG Emissions Volume Forecast Methodology ....................61

a) GHG Emissions Associated with Direct Costs ............61

(1) GHG Emissions Associated with Compliance Exposure ......................................62

(2) GHG Emissions Associated with Procurement Contracts .....................................63

b) GHG Emissions Associated with Indirect Costs .............................................................................63

(1) GHG Emissions Associated with QF Contracts ..........................................................63

(2) GHG Emissions Associated with In-State Market Purchases of Electricity ..............64

c) Forecast of 2018 GHG Emissions Volumes ................65

3. GHG Emissions Price Forecast Methodology .........................65

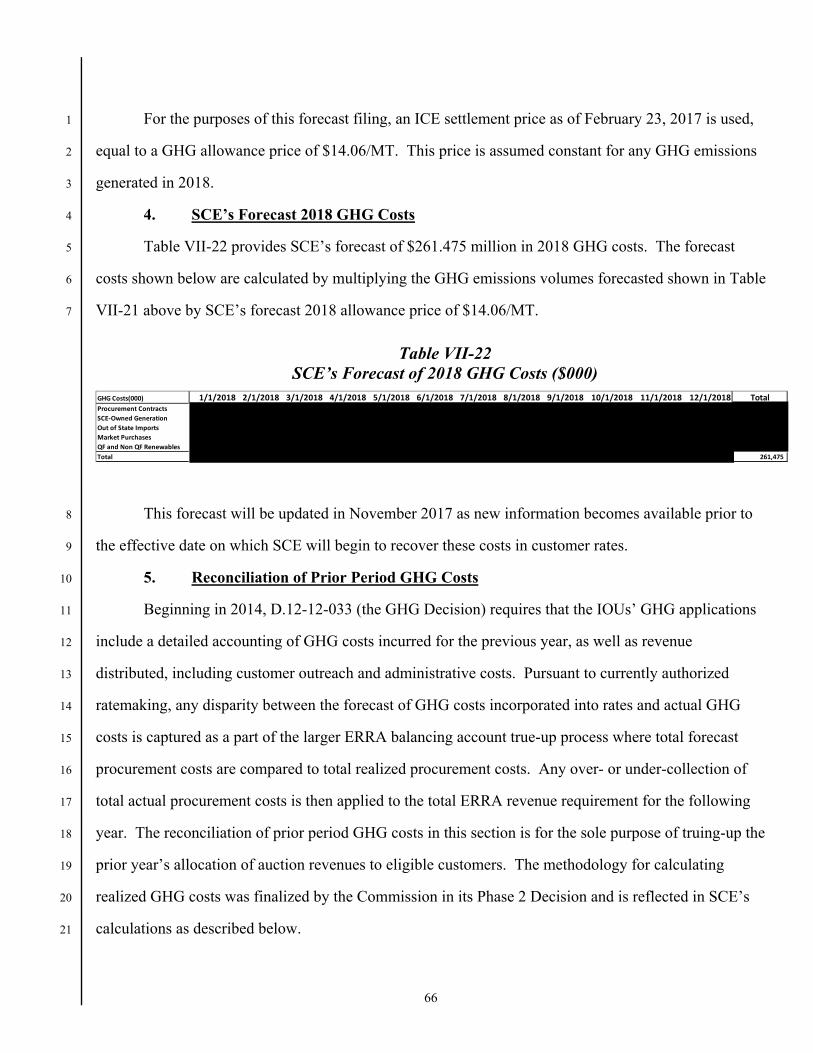

4. SCE’s Forecast 2018 GHG Costs ............................................66

5. Reconciliation of Prior Period GHG Costs ..............................66

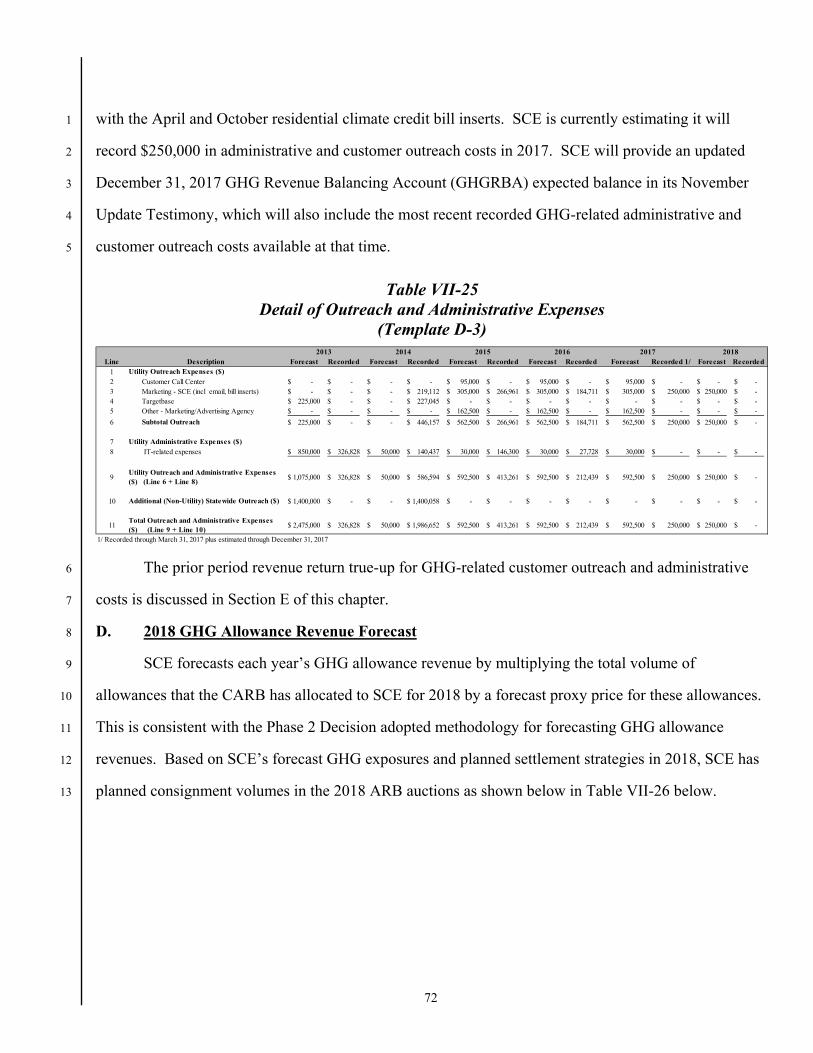

C. 2018 Administrative and Customer Outreach Costs Forecast and Prior Period Reconciliation ...........................................................71 M. Sheriff

1. Reconciliation of Prior Period Administrative and Customer Outreach Costs ........................................................71

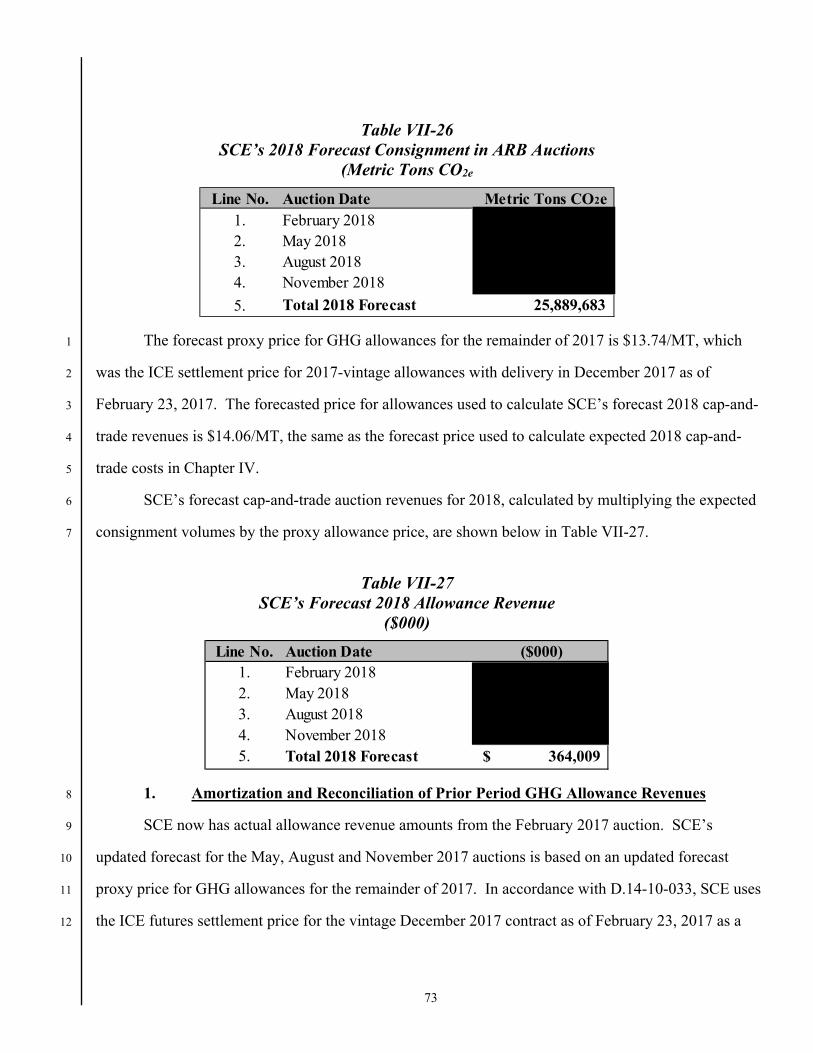

D. 2018 GHG Allowance Revenue Forecast ............................................72 K. Seeto

SCE-1: ERRA Resource Recovery Account (ERRA) 2018 Forecast of Operations

Table Of Contents (Continued)

Section Page Witness

vii

1. Amortization and Reconciliation of Prior Period GHG Allowance Revenues ................................................................73

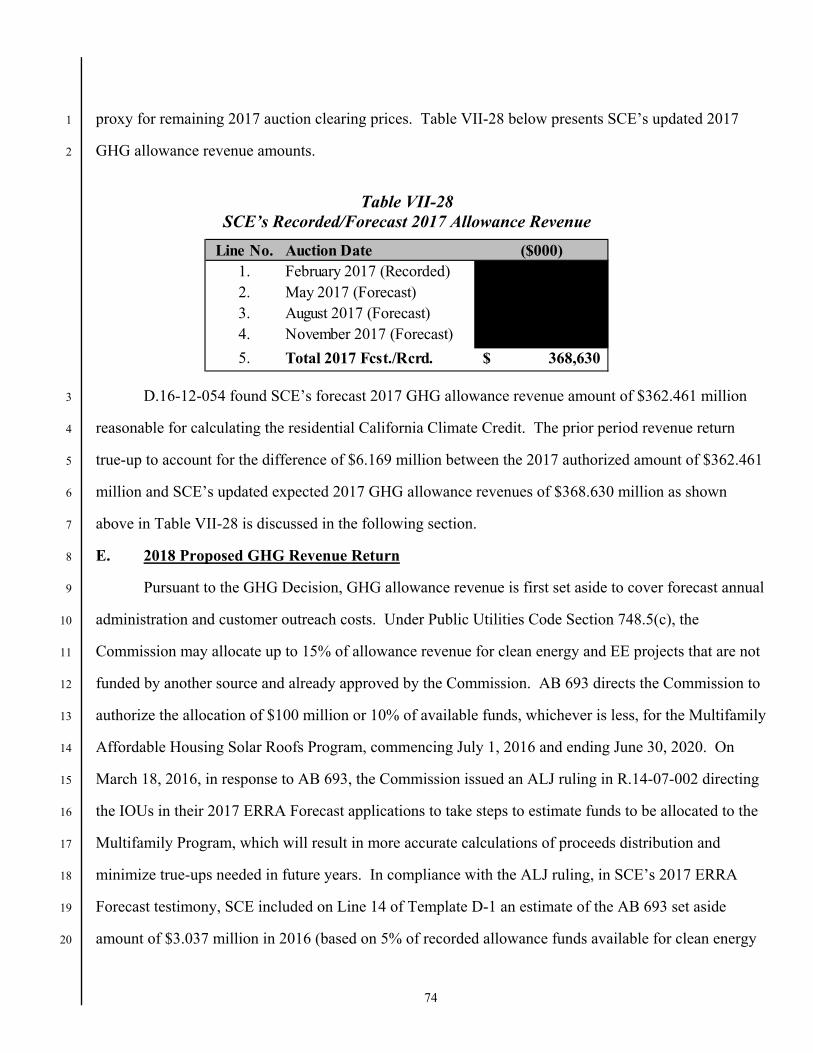

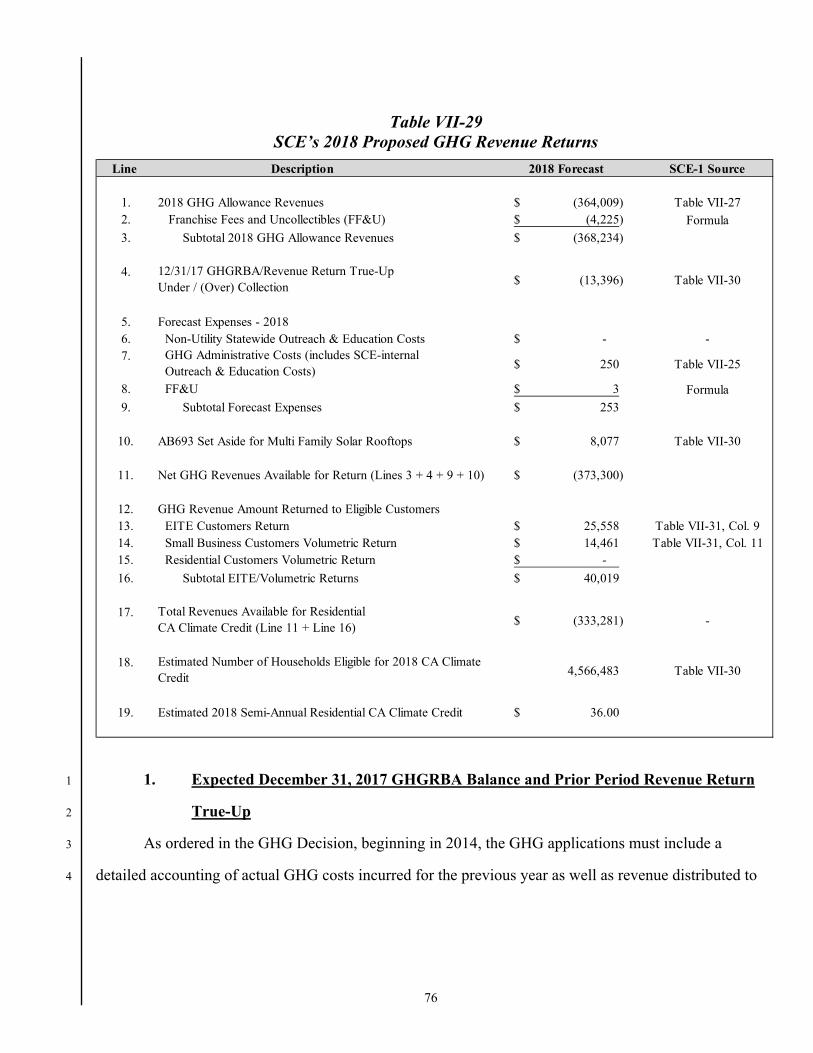

E. 2018 Proposed GHG Revenue Return .................................................74 M. Sheriff

1. Expected December 31, 2017 GHGRBA Balance and Prior Period Revenue Return True-Up ....................................76

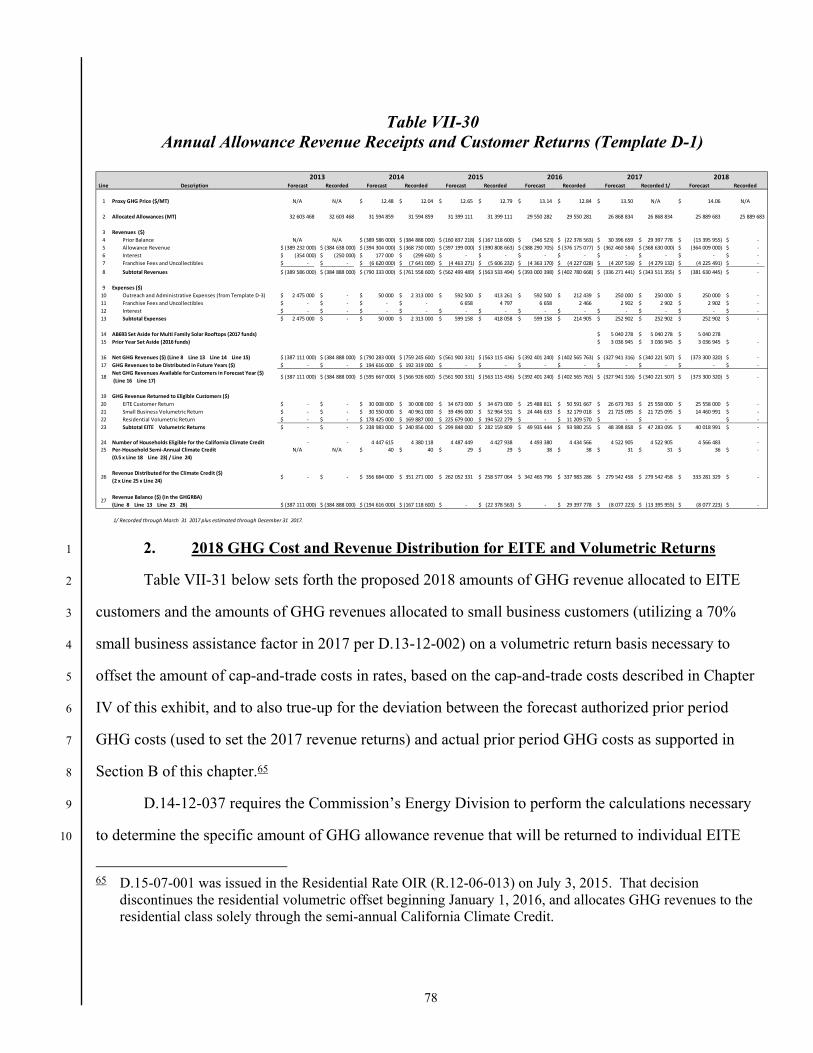

2. 2018 GHG Cost and Revenue Distribution for EITE and Volumetric Returns ...........................................................78 R. Thomas

3. 2018 Residential California Climate Credit .............................80

4. GHG Costs and Revenues by Rate Schedule ...........................81

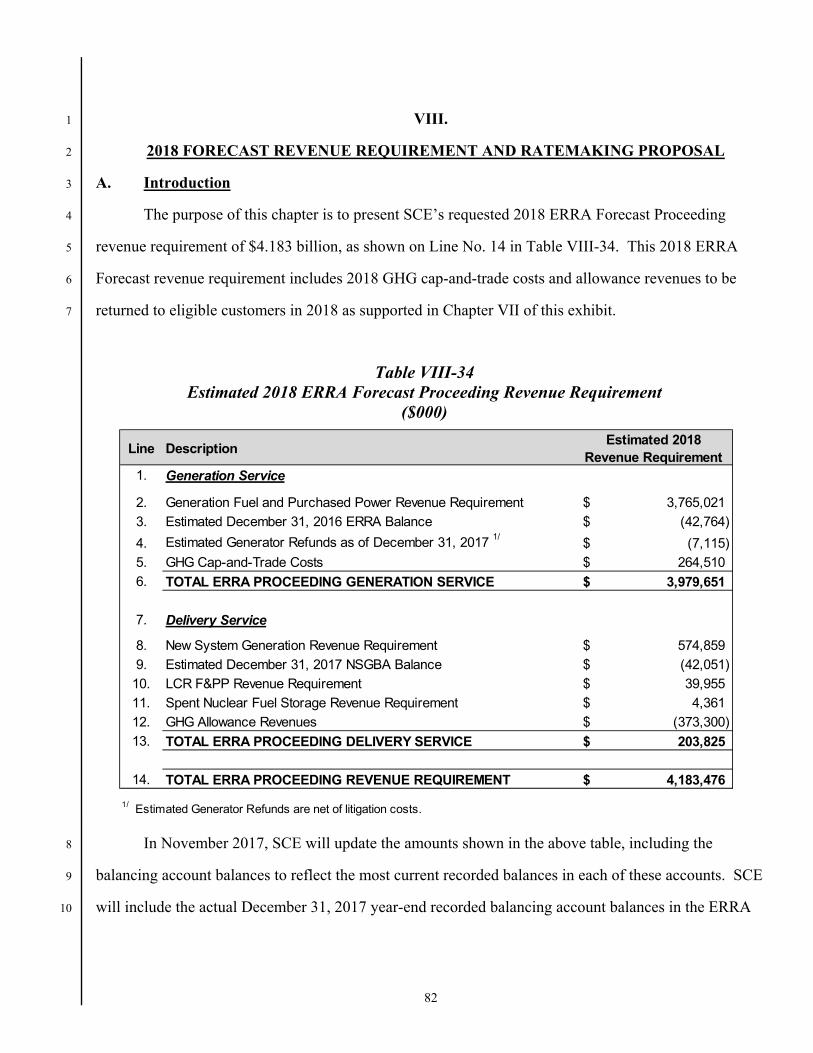

VIII. 2018 FORECAST REVENUE REQUIREMENT AND RATEMAKING PROPOSAL ........................................................................82 S. DiBernardo

A. Introduction ..........................................................................................82

B. Estimated 2018 ERRA-Related Generation Service Revenue Requirement .........................................................................................83

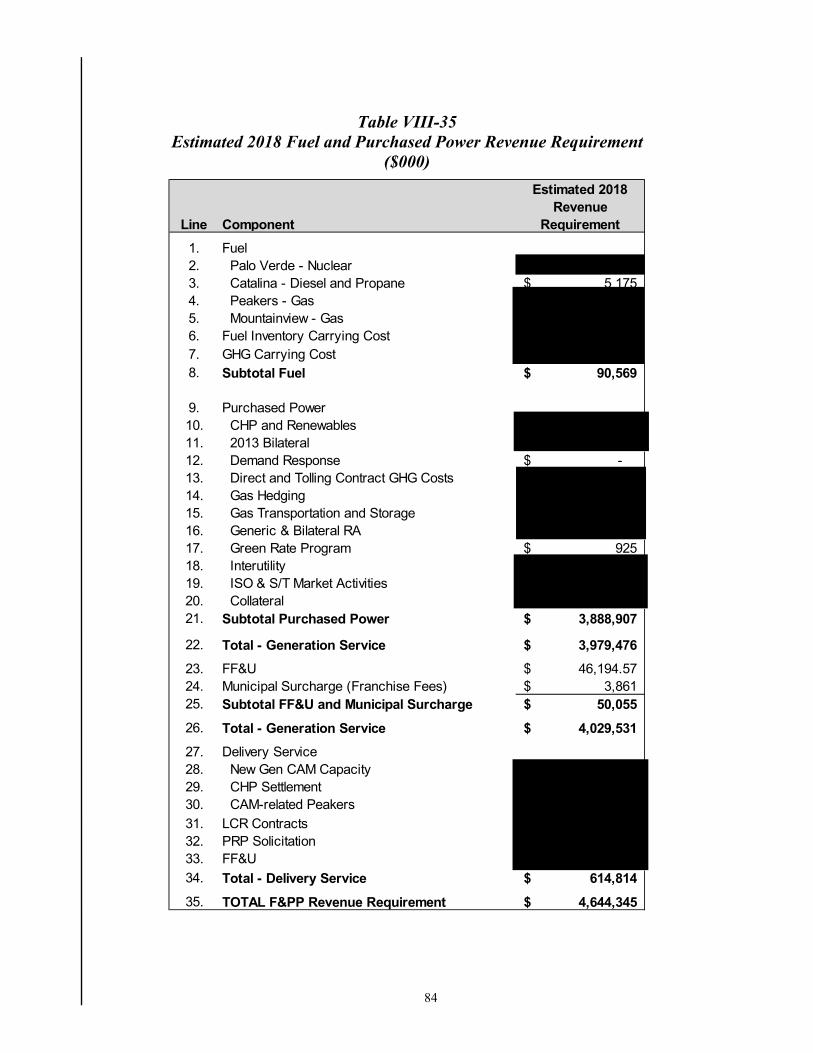

1. Estimated 2018 Fuel and Purchased Power Revenue Requirement .............................................................................83

a) Fuel Expense ................................................................85

b) Purchased Power Expense ...........................................85

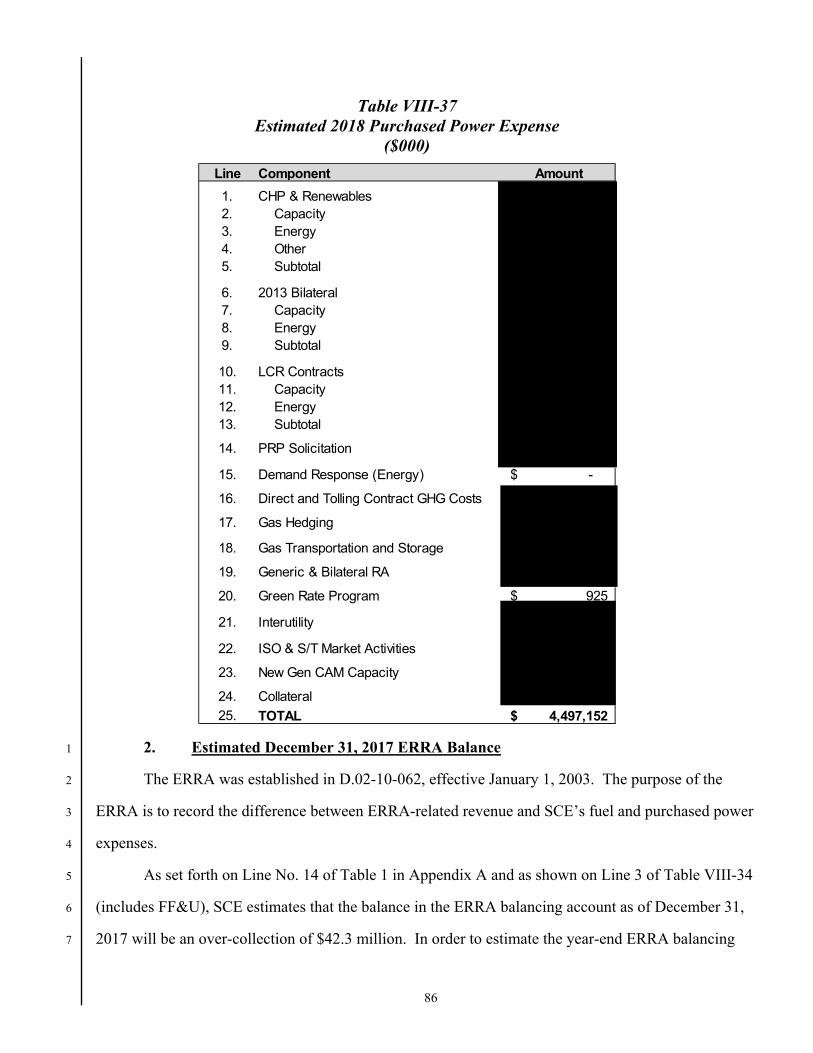

2. Estimated December 31, 2017 ERRA Balance ........................86

3. Estimated Energy Settlement Refunds and Litigation Costs .........................................................................................87

C. Estimated 2018 ERRA-Related Delivery Service Revenue Requirement .........................................................................................87

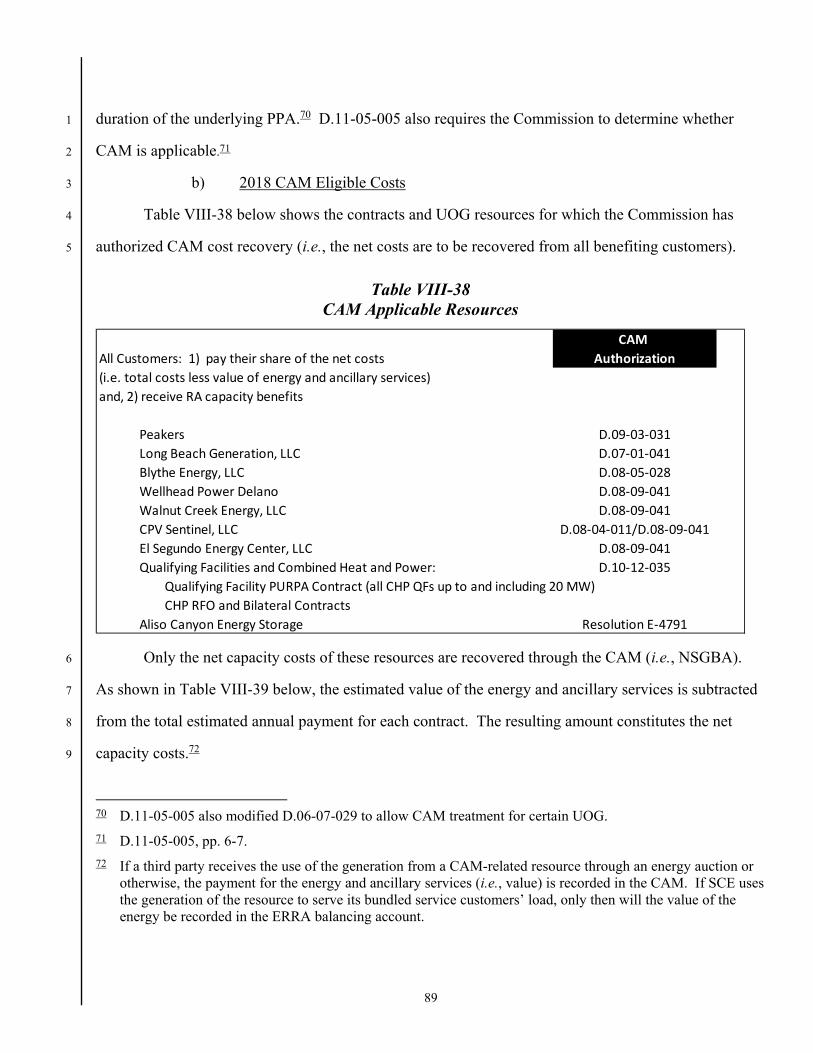

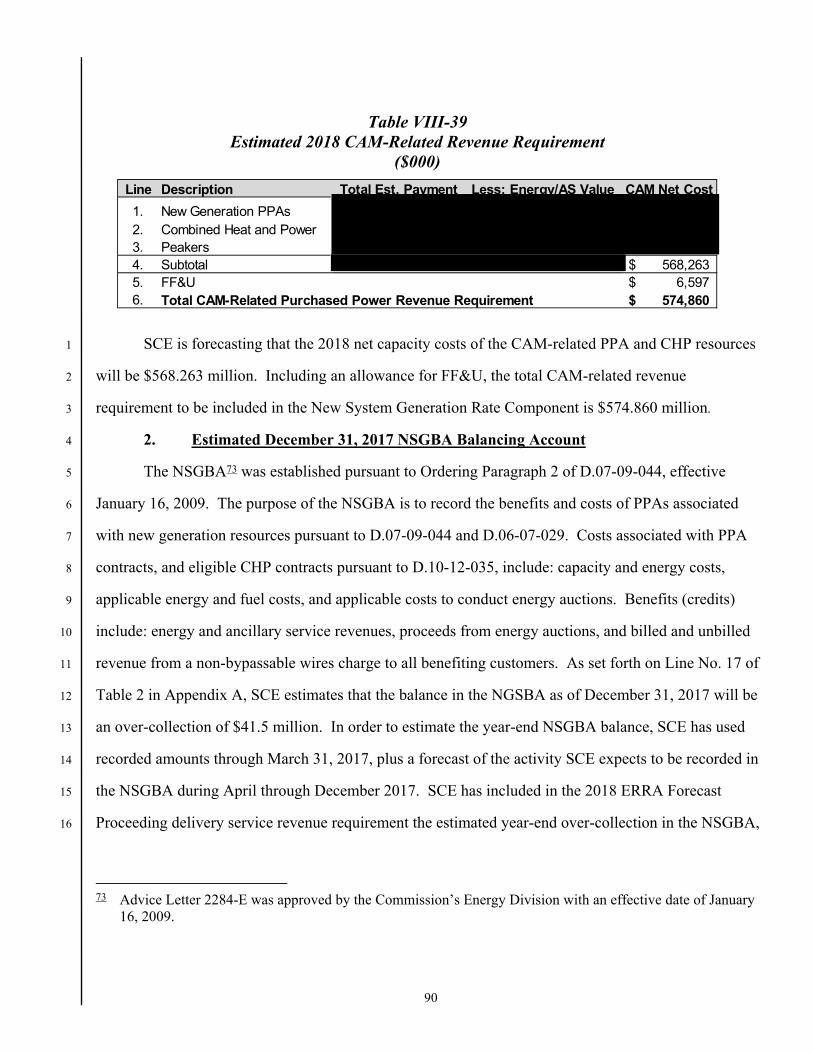

1. Estimated New System Generation Net Capacity CAM-Related Cost...................................................................88

a) Introduction ..................................................................88

b) 2018 CAM Eligible Costs ............................................89

SCE-1: ERRA Resource Recovery Account (ERRA) 2018 Forecast of Operations

Table Of Contents (Continued)

Section Page Witness

viii

2. Estimated December 31, 2017 NSGBA Balancing Account ....................................................................................90

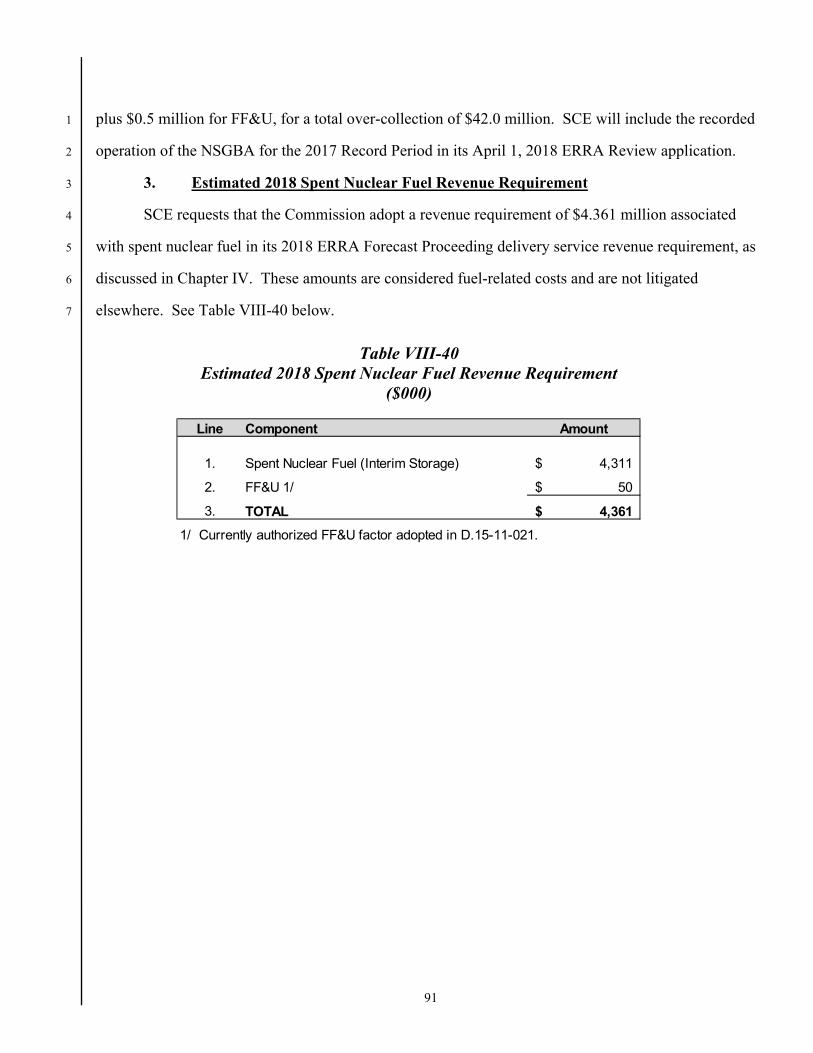

3. Estimated 2018 Spent Nuclear Fuel Revenue Requirement .............................................................................91

IX. DIRECT ACCESS, DEPARTING LOAD AND COMMUNITY CHOICE AGGREGATION COST RESPONSIBILITY SURCHARGES ..............................................................................................92 D. Wong

A. Background ..........................................................................................93

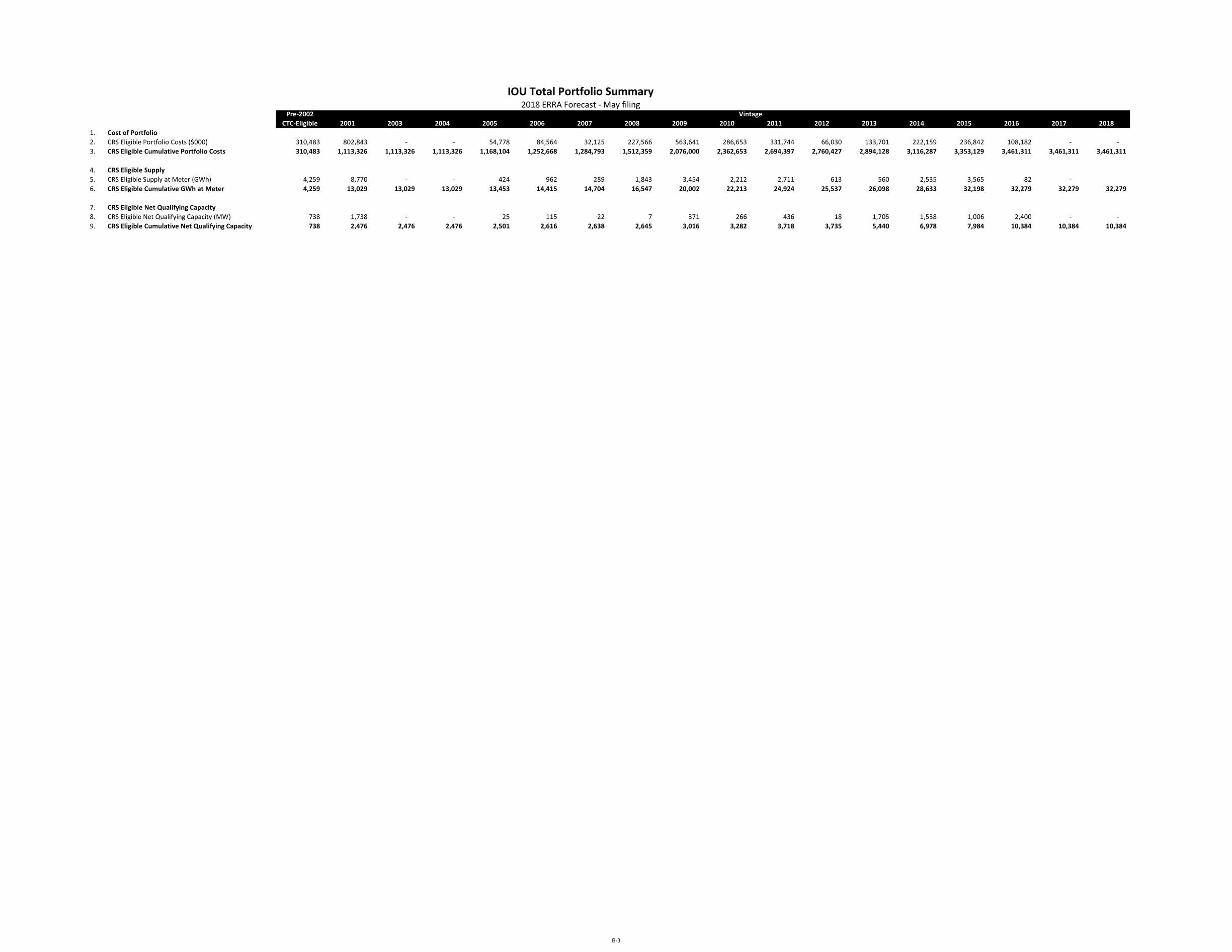

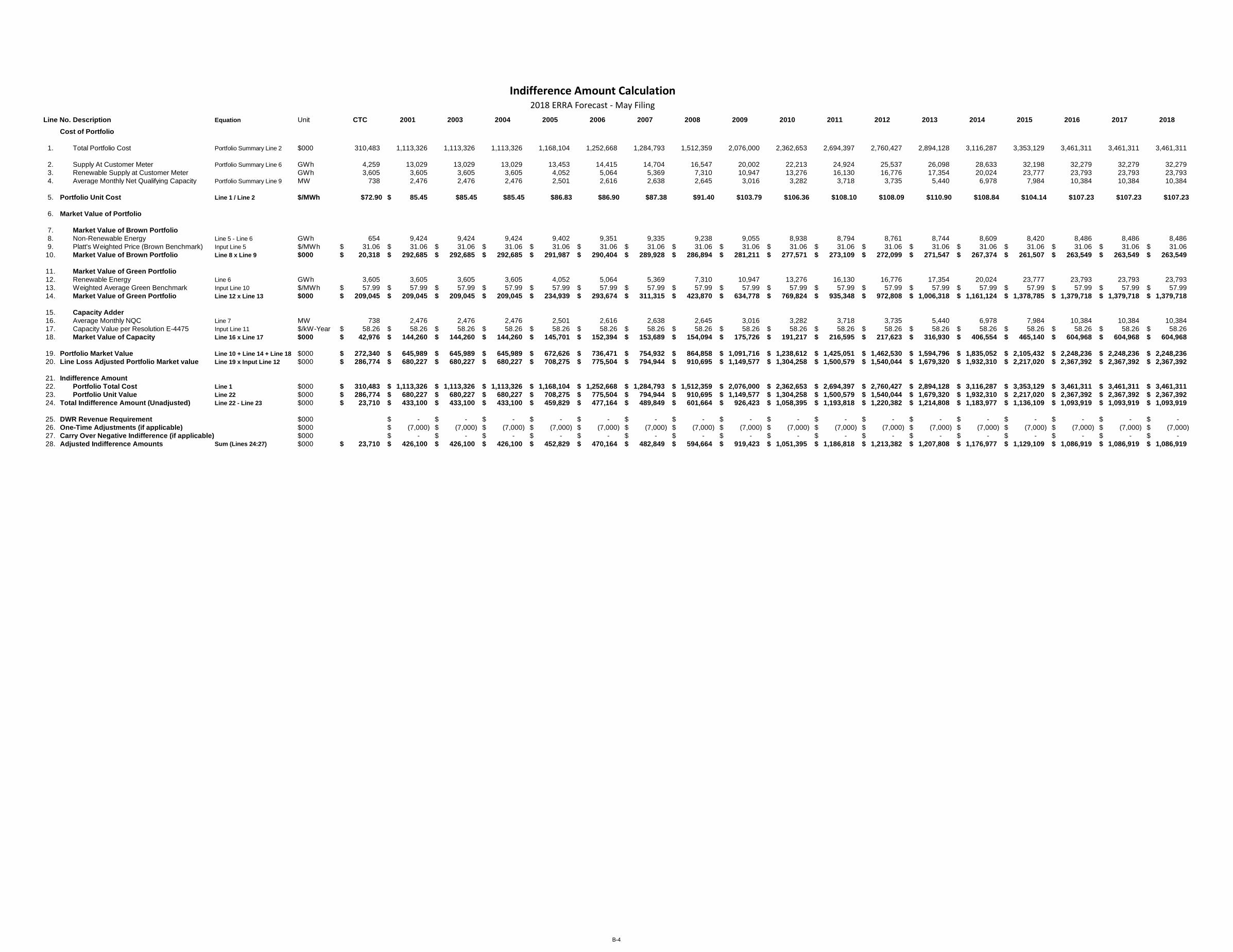

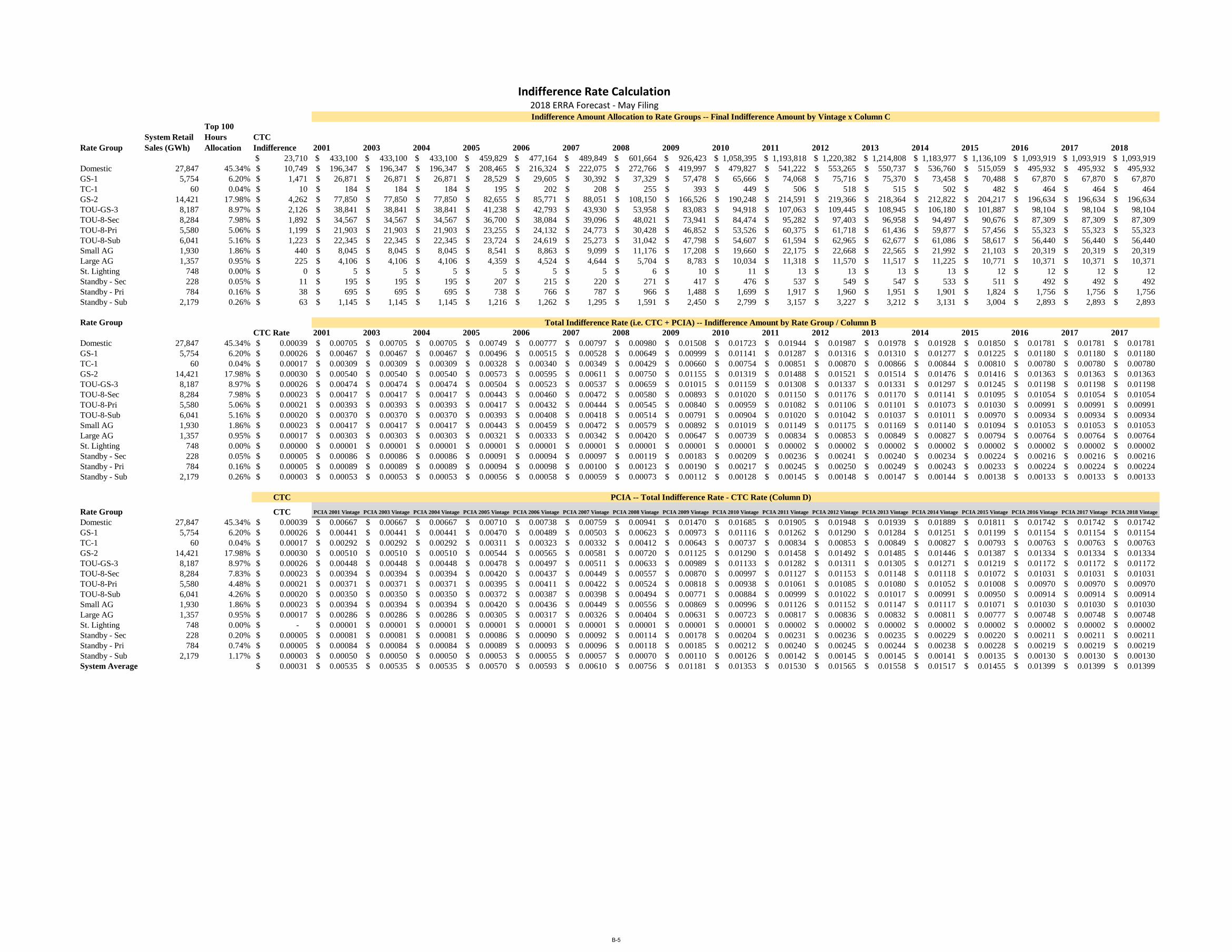

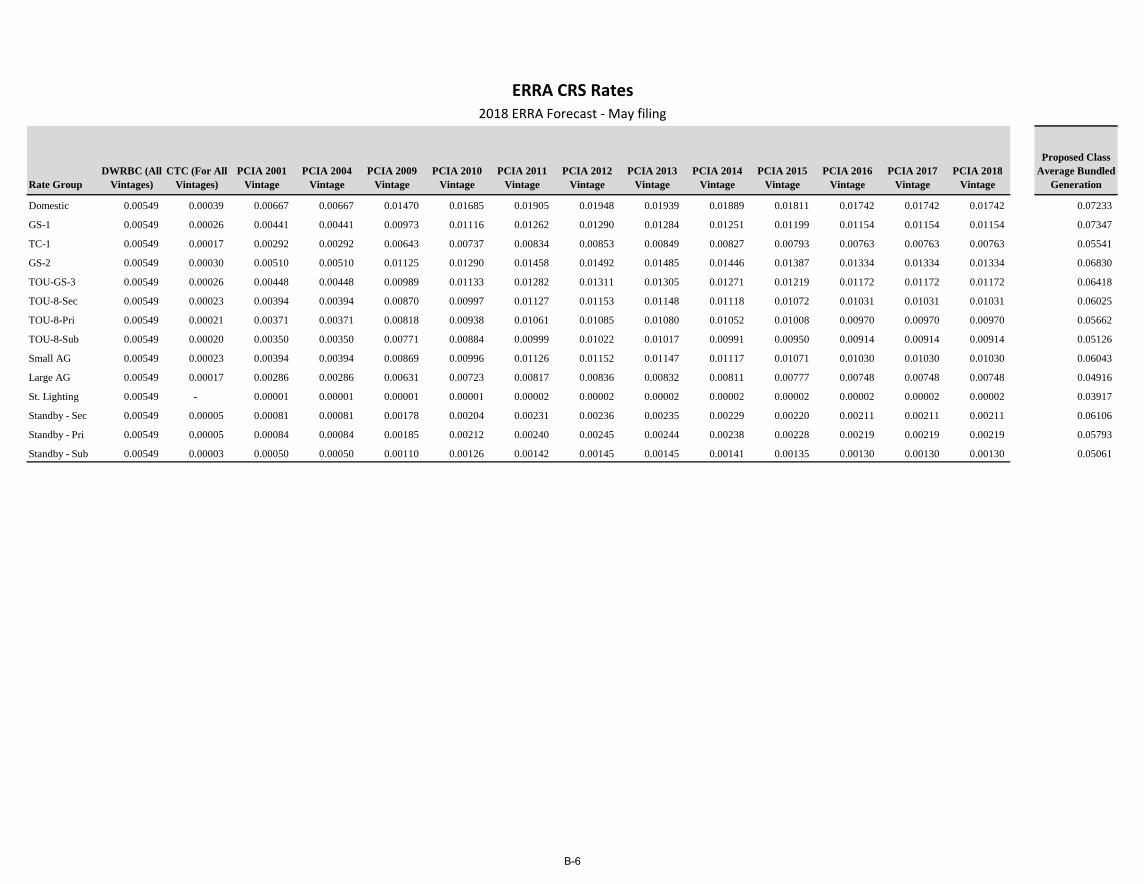

B. Total Portfolio Costs ............................................................................94

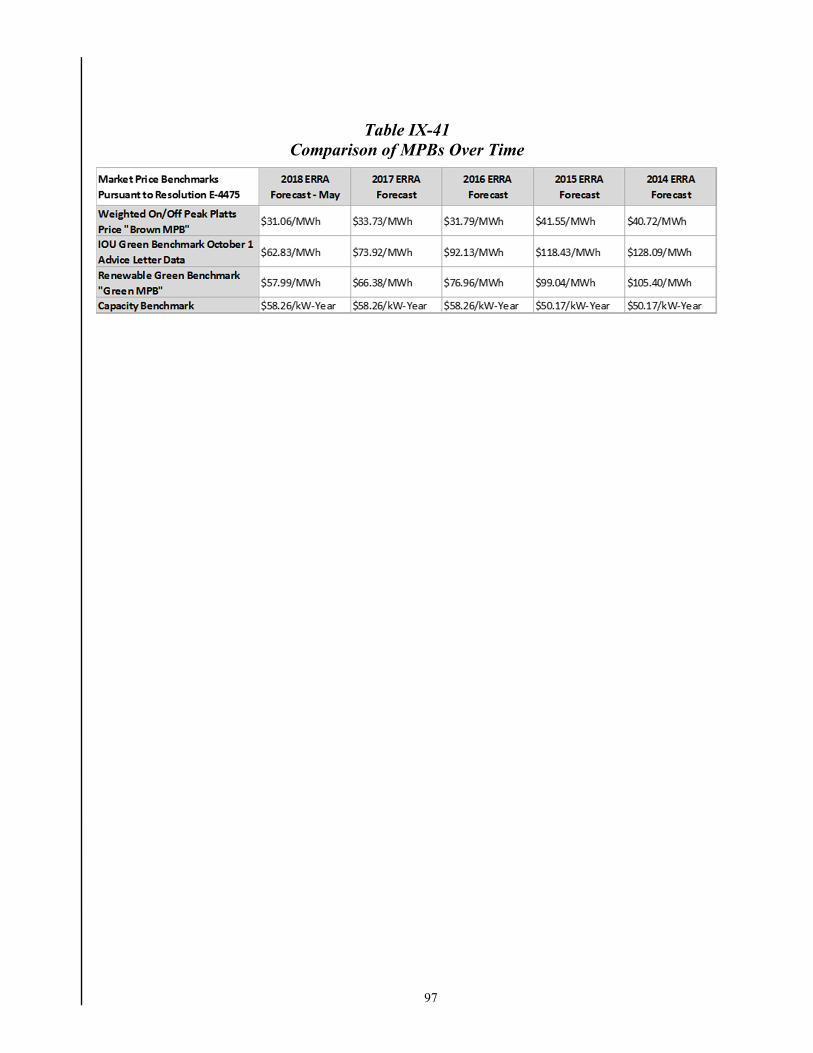

C. 2018 Market Price Benchmark ............................................................95

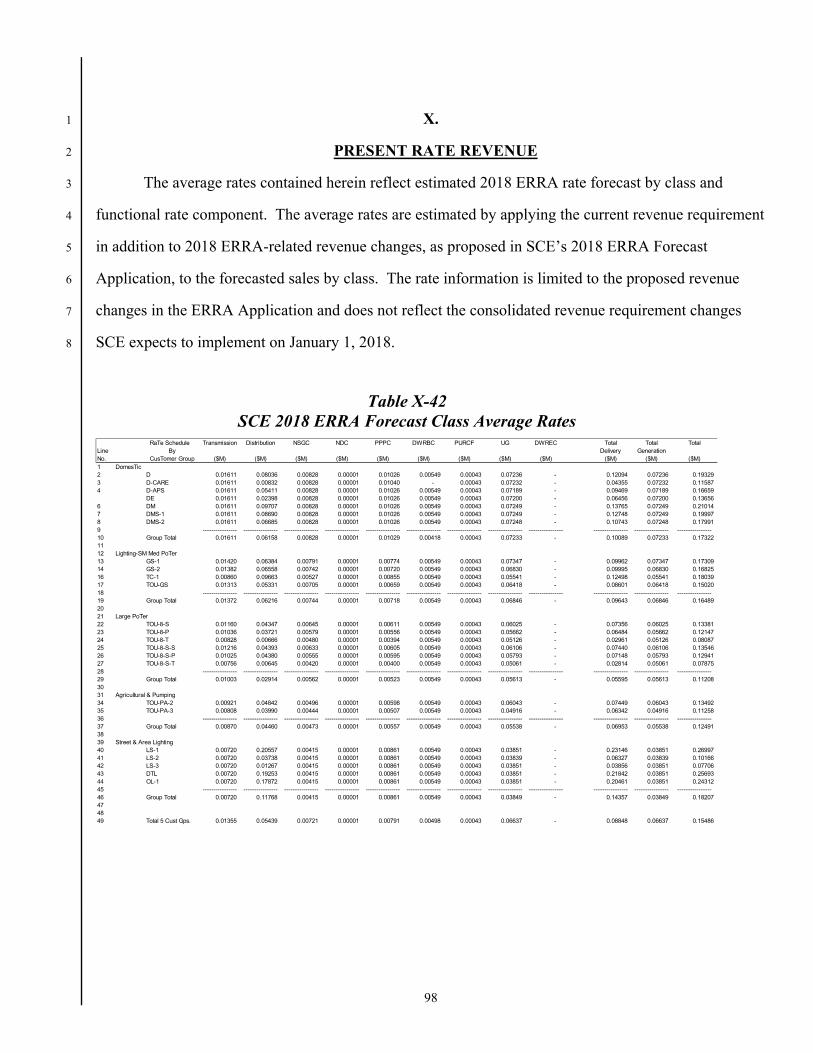

X. PRESENT RATE REVENUE ........................................................................98 R. Thomas

Appendix A Estimated December 31, 2017 Balancing Account Balances

Appendix B Indifference Rate Calculation

SCE-1: ERRA Resource Recovery Account (ERRA) 2018 Forecast of Operations

List Of Tables

Table Page

-ix-

Table II-1 Estimated 2018 ERRA Forecast Revenue Requirement Changes ($000) ..................................4

Table II-2 2018 ERRA Forecast Proceeding Revenue Requirement Changes ($

thousands) ..............................................................................................................................................6

Table III-3 2018 Bundled Customer Load Forecast (GWh) ........................................................................9

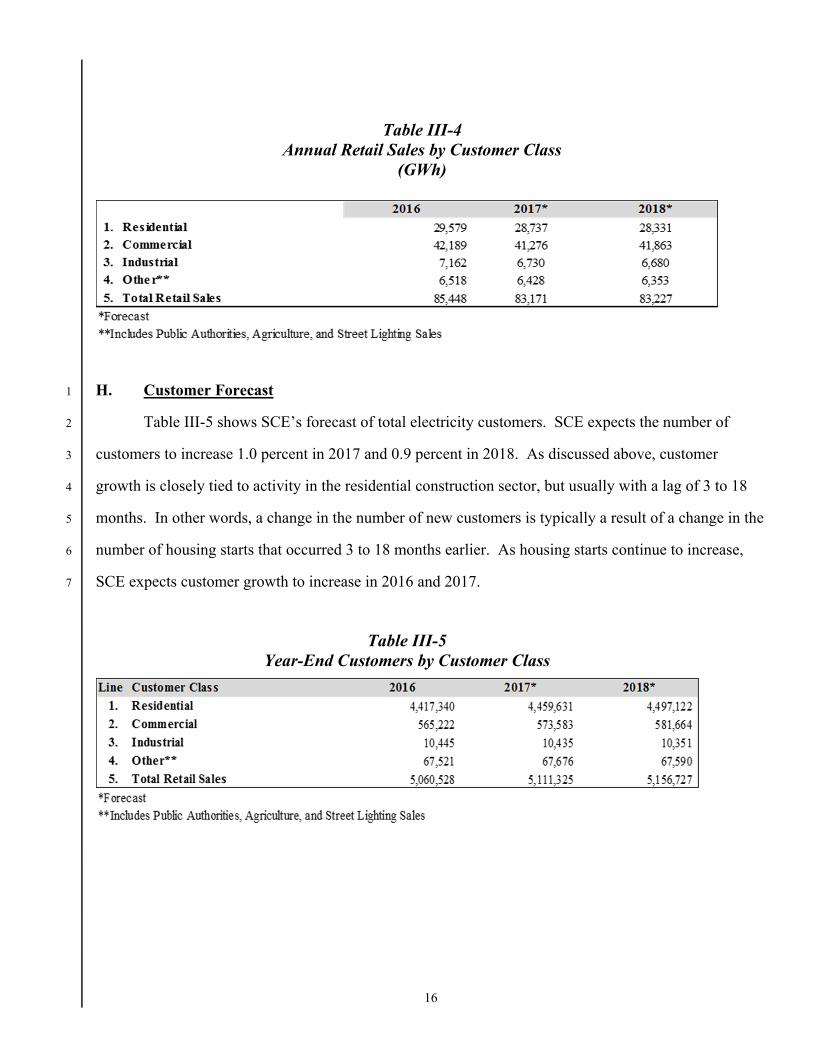

Table III-4 Annual Retail Sales by Customer Class (GWh) ......................................................................16

Table III-5 Year-End Customers by Customer Class ................................................................................16

Table III-6 Bundled Energy at CAISO (GWh) ..........................................................................................18

Table IV-7 2018 Energy Forecast of the SCE Portfolio (GWh) Confidential ...........................................23

Table IV-8 2018 Forecast of Fuel and Purchased Power Costs ($000) Confidential ................................24

Table IV-9 2018 Forecast of SCE SPVP Production (GWh) ....................................................................27

Table IV-10 Annual Capacity Factors by Technology ..............................................................................29

Table IV-11 2018 Forecast of Posted Energy and Capacity Prices ...........................................................30

Table IV-12 Non-Coincident Contract Capacity Quantities and Expiration Dates for

SCE’s Major Interutility Contracts ......................................................................................................31

Table IV-13 SCE Entitlement to Hoover Dam Electrical Output for Year 2017 Source:

Bureau of Reclamation - CRSR 3/2016 Most Probable Inflow ...........................................................33

Table IV-14 Projected 2018 Forecast Period Nuclear Fuel Expense (Thousands of Dollars

– SCE’s Share) .....................................................................................................................................42

Table IV-15 Catalina Diesel Fuel 2018 Forecast Delivered Diesel Cost (2016-2017

Recorded) .............................................................................................................................................43

Table IV-16 2018 Forecast Delivered Propane Cost (MTs) (2016-2017 Recorded) .................................44

Table VI-17 Estimate of 2018 Carrying Costs ($000) ...............................................................................54

Table VI-18 Estimated 2018 Fuel Inventory Carrying Costs ($000) ........................................................55

SCE-1: ERRA Resource Recovery Account (ERRA) 2018 Forecast of Operations

List Of Tables (Continued)

Table Page

-x-

Table VI-19 Estimated 2018 GHG Compliance Carrying Costs ($000) ...................................................55

Table VI-20 Estimated 2018 Procurement Collateral Carrying Costs ($000) ...........................................56

Table VII-21 SCE’s Forecast of 2018 GHG Emissions Volumes (Metric Tons CO2e) ..........................65

Table VII-22 SCE’s Forecast of 2018 GHG Costs ($000) ........................................................................66

Table VII-23 Annual GHG Emissions and Associated Costs (Template D-2) ........................................67

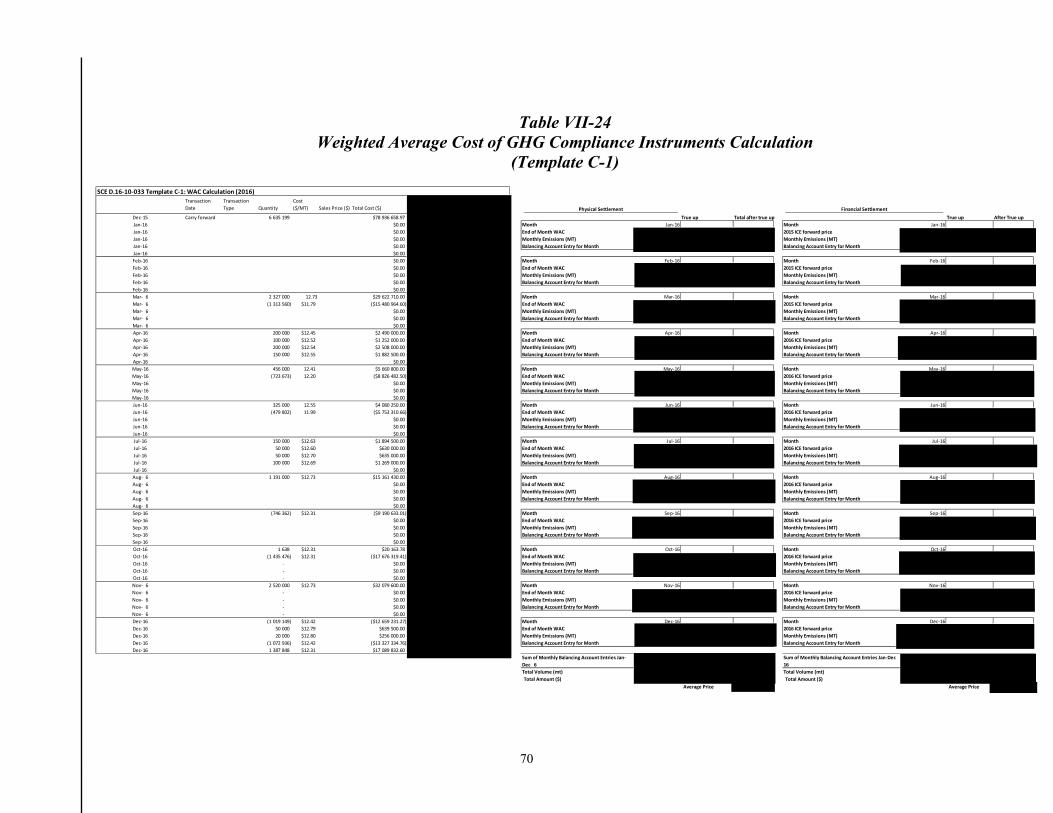

Table VII-24 Weighted Average Cost of GHG Compliance Instruments Calculation

(Template C-1) .....................................................................................................................................70

Table VII-25 Detail of Outreach and Administrative Expenses (Template D-3) .....................................72

Table VII-26 SCE’s 2018 Forecast Consignment in ARB Auctions (Metric Tons CO2e .........................73

Table VII-27 SCE’s Forecast 2018 Allowance Revenue ($000) ..............................................................73

Table VII-28 SCE’s Recorded/Forecast 2017 Allowance Revenue ..........................................................74

Table VII-29 SCE’s 2018 Proposed GHG Revenue Returns ....................................................................76

Table VII-30 Annual Allowance Revenue Receipts and Customer Returns (Template D-

1) ..........................................................................................................................................................78

Table VII-31 GHG Allowance Revenue Allocation by Class ...................................................................80

Table VII-32 GHG Costs and Revenues by Rate Schedule (Template D-4) .............................................81

Table VII-33 History of GHG Revenues, Costs, and Emissions Intensity (Template D-5) ......................81

Table VIII-34 Estimated 2018 ERRA Forecast Proceeding Revenue Requirement ($000) ......................82

Table VIII-35 Estimated 2018 Fuel and Purchased Power Revenue Requirement ($000) .......................84

Table VIII-36 2018 Estimated Fuel Expense ($000) .................................................................................85

Table VIII-37 Estimated 2018 Purchased Power Expense ($000) ............................................................86

Table VIII-38 CAM Applicable Resources ...............................................................................................89

Table VIII-39 Estimated 2018 CAM-Related Revenue Requirement ($000) ...........................................90

Table VIII-40 Estimated 2018 Spent Nuclear Fuel Revenue Requirement ($000) ...................................91

SCE-1: ERRA Resource Recovery Account (ERRA) 2018 Forecast of Operations

List Of Tables (Continued)

Table Page

-xi-

Table IX-41 Comparison of MPBs Over Time..........................................................................................97

Table X-42 SCE 2018 ERRA Forecast Class Average Rates ....................................................................98

Table X-43 Average Generation Rates ......................................................................................................99

SCE-1: ERRA Resource Recovery Account (ERRA) 2018 Forecast of Operations

List Of Figures

Figure Page

-xii-

Figure III-1 Total Non-Farm Employment Growth in the Counties Served by SCE 2006

to 2016 .................................................................................................................................................11

Figure III-2 Residential Housing Starts in Counties Served by SCE ........................................................12

Figure III-3 Total Non-Farm Employment Growth in SCE Service Area Actual and

Forecast ................................................................................................................................................13

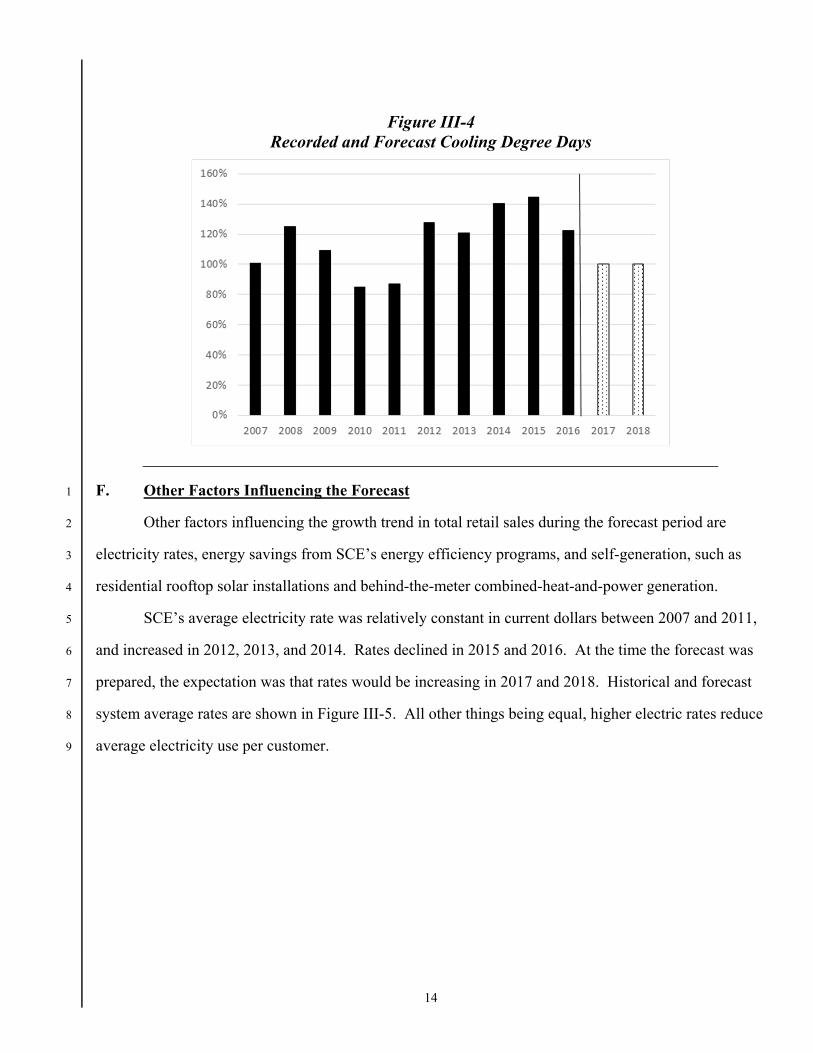

Figure III-4 Recorded and Forecast Cooling Degree Days .......................................................................14

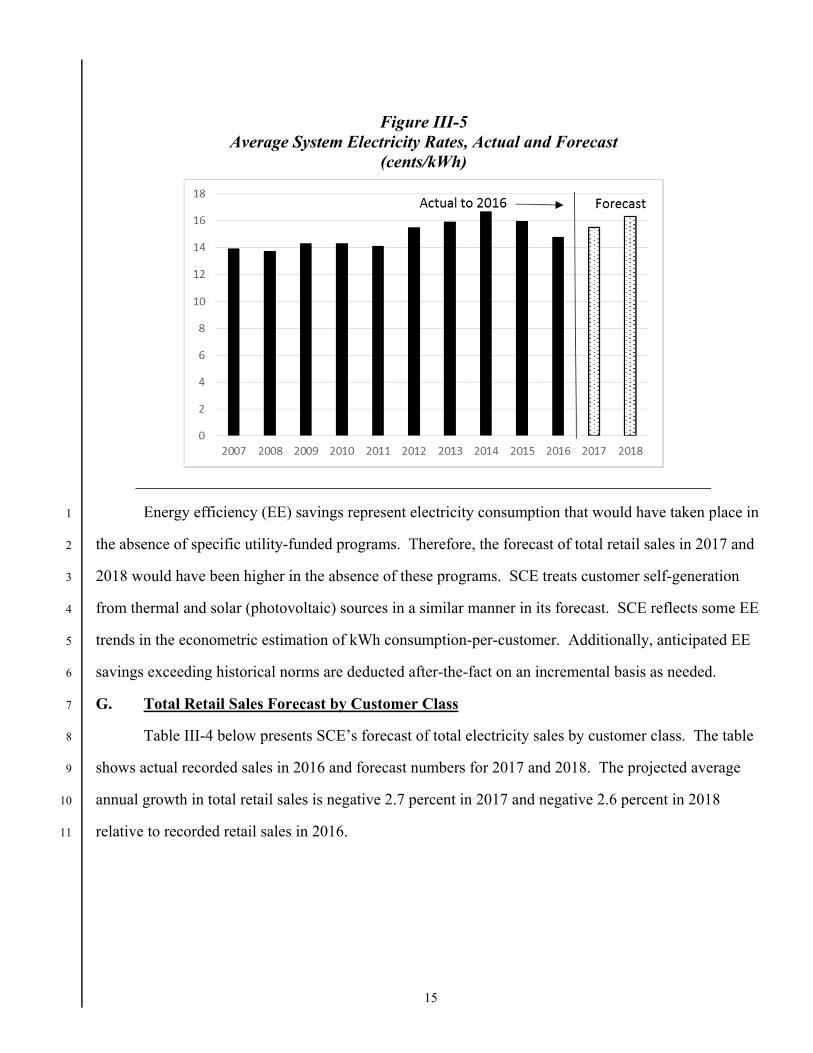

Figure III-5 Average System Electricity Rates, Actual and Forecast ........................................................15

1

I. 1

INTRODUCTION 2

Southern California Edison Company (SCE or Company) files this annual Energy Resource 3

Recovery Account (ERRA) Forecast application to request the Commission to authorize SCE’s 2018 4

ERRA Forecast proceeding revenue requirement in the amount of $4.183 billion. The Commission has 5

established this process for the review and approval of SCE’s forecast of fuel and purchased power 6

expenses for the purpose of setting rates.1 The 2018 ERRA Proceeding revenue requirement forecast of 7

$4.183 billion is supported in the following chapters of this testimony, and is based on SCE’s best 8

estimate of such factors as kWh sales and load, natural gas and power prices, and an estimate of the 9

December 31, 2017 balancing account balances included in this revenue requirement.2 The forecast 10

adopted by the Commission in this proceeding does not determine which procurement-related costs are 11

ultimately eligible for cost recovery, as the actual fuel and purchased power costs must be reviewed by 12

the Commission and found eligible for recovery in a subsequent ERRA Review proceeding or Quarterly 13

Compliance Report (QCR) determination. Consistent with past ERRA Forecast applications, SCE will 14

update its 2018 ERRA Forecast proceeding revenue requirement forecast in November 2017, so that the 15

latest forecast assumptions can be incorporated into SCE’s 2018 rates. 16

As directed by the Commission’s Phase 2 Decision Adopting Standard Procedures for Electric 17

Utilities to File Greenhouse Gas (GHG) Forecast Revenue and Reconciliation (FR&R) Requests (D.14-18

10-033), issued in A.13-08-002 et al., dated October 16, 2014, the investor-owned utilities (IOUs) are to 19

include their Greenhouse Gas (GHG) revenue and reconciliation requests as an additional chapter or 20

section within the annual ERRA Forecast applications.3 In this Application, SCE proposes to return a 21

1 Decision (D.) 04-01-050 and D.04-01-048, and as modified by D.04-03-023.

2 Pursuant to SCE’s 2015 ERRA Forecast D.15-10-037, SCE is including only the ERRA Balancing Account, the Energy Settlements Memorandum Account (ESMA)/Litigation Costs Tracking Account (LCTA) and the New System Generation Balancing Account (NSGBA) forecast year-end 2017 balances in the 2018 ERRA Forecast revenue requirement.

3 D.14-10-033, Ordering Paragraph (OP) 10.

2

total of $373.3 million in GHG allowance revenues to eligible customers in 2018 based on the 1

Commission-adopted methodologies and utilizing GHG revenues and cap-and-trade costs, including 2

administrative and customer outreach costs, as proposed and supported in this testimony. Based on 3

SCE’s estimated GHG allowance revenues available for return to eligible customers in 2018, residential 4

customers can expect a semi-annual, on-bill California Climate Credit of $36.00 in 2018. 5

A discussion of SCE’s estimated 2018 ERRA Forecast proceeding revenue requirement and the 6

resulting rate change are presented in Chapter II, and the remaining chapters of this testimony address 7

the following: 8

• Chapter III, SCE’s Bundled Energy Forecast 9

• Chapter IV, Forecast Energy Production and Costs from SCE’s Portfolio of Resources 10

• Chapter V, Financing Costs 11

• Chapter VI, Carrying Costs 12

• Chapter VII, GHG Forecast Costs and Revenues and Reconciliation 13

• Chapter VIII, 2018 Forecast Revenue Requirement and Ratemaking Issues 14

• Chapter IX, Cost Responsibility Surcharges (Direct Access, Departing Load, and Community 15

Choice Aggregation) 16

• Appendix A, Estimated December 31, 2017 Balancing Account Balances 17

• Appendix B, Indifference Rate Calculation 18

D.16-01-017 approved an amendment to Rule 2.1(c) of the Commission’s Rules of Practice and 19

Procedure (Title 20, Division 1, of the California Code of Regulations) to require all applications to 20

identify all relevant safety considerations implicated by the application. One of SCE’s core values is to 21

assure public and employee safety. As such, the procurement of fuel and purchased power (whether for 22

SCE-owned units, contracted through Power Purchase Agreements, or purchased through CAISO or 23

other power exchanges), inherently assumes that all power providers are fully compliant with laws, 24

rules, regulations and internally-managed controls to assure that their generating facilities are operated 25

and maintained in a safe working condition. Likewise, SCE’s management of air emissions costs (i.e., 26

Greenhouse Gas Cap-and-Trade costs and other similar costs), and transmission capacity procurement 27

activities, also assume the counter-parties to these transactions are fully compliant with laws, rules, 28

3

regulations and internally-managed controls to assure that their facilities are operated and maintained in 1

a safe working condition. 2

The safety performance of the counter-parties involved (once contracted) is not directly related 3

to SCE’s activities at issue in this proceeding, which include the forecast for sales and purchases of 4

power, fuel, transmission capacity and air emissions credits and allowances. Nevertheless, these 5

activities do support public and employee safety, as these transactions are an inherent part of assuring a 6

reliable supply of electricity to SCE customers. Costs incurred by SCE to operate and maintain the SCE 7

office and public spaces, shops, warehouses, transmission and distribution facilities, and utility-owned 8

power plants in a safe condition are reviewed in SCE’s GRC Applications. In addition, per D.14-12-9

025, SCE filed a Safety Model Assessment Proceeding (SMAP) Application “to provide Commission 10

staff and other parties with the opportunity to analyze and understand the various models and 11

methodologies that the energy utilities will be using to prioritize safety in their GRC proceedings. This 12

prioritization of safety is to be achieved through the use of models and methodologies to assess the 13

energy utility’s risk, and the mitigation measures the energy utility plans to take to reduce and minimize 14

such risks.”4 15

4 D.14-12-025, p. 24.

4

II. 1

2018 ERRA FORECAST PROCEEDING REVIEW REQUIREMENT 2

A. 2018 ERRA Forecast Proceeding Revenue Requirement 3

As shown in Table II-1, SCE is forecasting a decrease of approximately $302 million in its 2018 4

ERRA Forecast proceeding revenue requirement 5 as compared to the revenue requirement used to set 5

the rates in effect today.6 6

Table II-1 Estimated 2018 ERRA Forecast Revenue Requirement Changes

($000)

5 In order to estimate the year-end ERRA, ESMA/LCTA and NSGBA balances, SCE has used recorded

amounts through March 31, 2017, plus a forecast of the activity SCE expects to be recorded from April through December 2017.

6 The rates in effect today are based on the revenue requirement approved by D.16-12-054.

Line Description

Estimated 2018 Revenue Requirement In Rates 1/

Rev. Req. Change

(a) (b) (c) (d) (e) = (c) - (d)

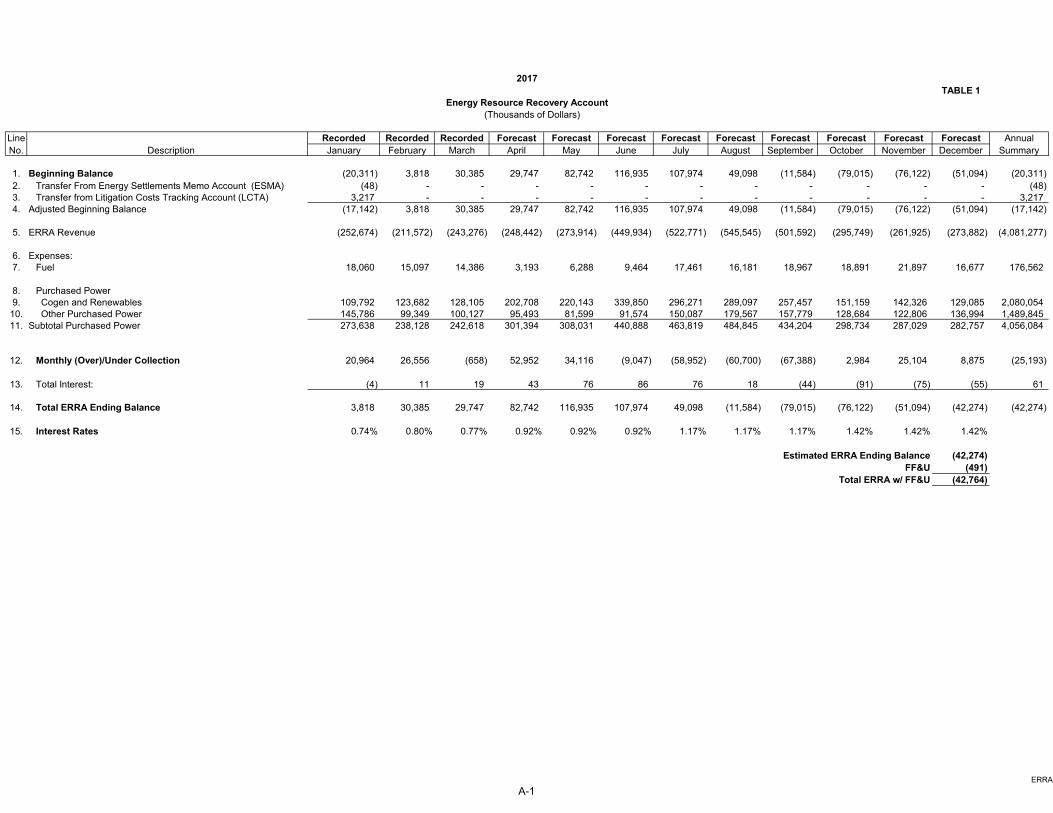

1. Fuel and Purchased Power 2/ 4,384,196$ 4,584,334$ (200,137)$ 2. ERRA Balancing Account (42,764)$ (94,007)$ 51,243$ 3. Energy Settlements Memorandum Account - Net Amount 3/ (7,115)$ -$ (7,115)$ 4. New System Generation Balancing Account (42,051)$ 8,896$ (50,947)$ 5. SUBTOTAL ERRA-RELATED 4,292,266$ 4,499,222$ (206,956)$

6. GHG Cap-and-Trade Costs 264,510$ 313,776$ (49,266)$ 7. GHG Allowance Revenues (373,300)$ (327,941)$ (45,359)$ 8. SUBTOTAL GHG-RELATED (108,790)$ (14,165)$ (94,625)$

9. TOTAL ERRA PROCEEDING REVENUE REQUIREMENT 4,183,476$ 4,485,057$ (301,581)$

1/ D.16-12-054 (2017 ERRA Rev Rqmt) implemented January 1, 2017 (Advice Letter 3515-E-A).2/ Amounts Include Spent Nuclear Fuel.3/ Amount reflects 2017 forecast ESMA refunds less forecast litigation-related costs in the Litigation Cost Tracking Account (LCTA).

5

As discussed in more detail below and in Chapter IV, the primary reasons for the decrease in the 1

estimated 2018 fuel and purchased power expenses from the amounts included in the 2017 Forecast 2

revenue requirement are summarized below: 3

1. SCE expects its sales to be lower than the levels included in current rates; 4

2. SCE expects lower fuel-related costs from its natural gas-fueled UOG and tolling resources 5

due to lower forecast natural gas prices; 6

3. SCE expects lower open market costs due to lower forecast SP-15 forward market power 7

prices; and 8

4. SCE expects lower Short-Run Avoided Cost (SRAC) payments due to lower forecast market 9

prices. 10

1. Functionalized ERRA-Related Revenue Requirement 11

SCE’s ERRA Forecast proceeding revenue requirement is functionalized between “generation 12

service” and “delivery service.” The generation service revenue requirement is recovered from only 13

SCE’s bundled service customers, while the delivery service revenue requirement is recovered from all 14

customers to whom SCE delivers electricity, which includes Direct Access (DA) and Community 15

Choice Aggregation (CCA) customers. SCE’s delivery service revenue requirement also includes the 16

purchased power costs the Commission has deemed to benefit all customers, and is therefore recovered 17

from all customers through a Cost Allocation Mechanism (CAM). The CAM is explained in more detail 18

beginning in Section C.1 of Chapter VIII. 19

As shown on Line No. 23 in Table II-2 and as discussed above, SCE is forecasting a decrease of 20

approximately $302 million in its 2018 ERRA Forecast proceeding revenue requirement from the 21

revenue requirement used to set rates in effect today. This sum includes a decrease of $140 million in its 22

generation service requirement from the rates in effect today, as shown on Line No. 6, and a decrease of 23

$162 million in its delivery service revenue requirement from the rates in effect today, as shown on Line 24

No. 22. The discussion below compares the forecast 2018 ERRA Forecast proceeding revenue 25

requirement with the 2017 authorized ERRA Forecast revenue requirement by function. 26

6

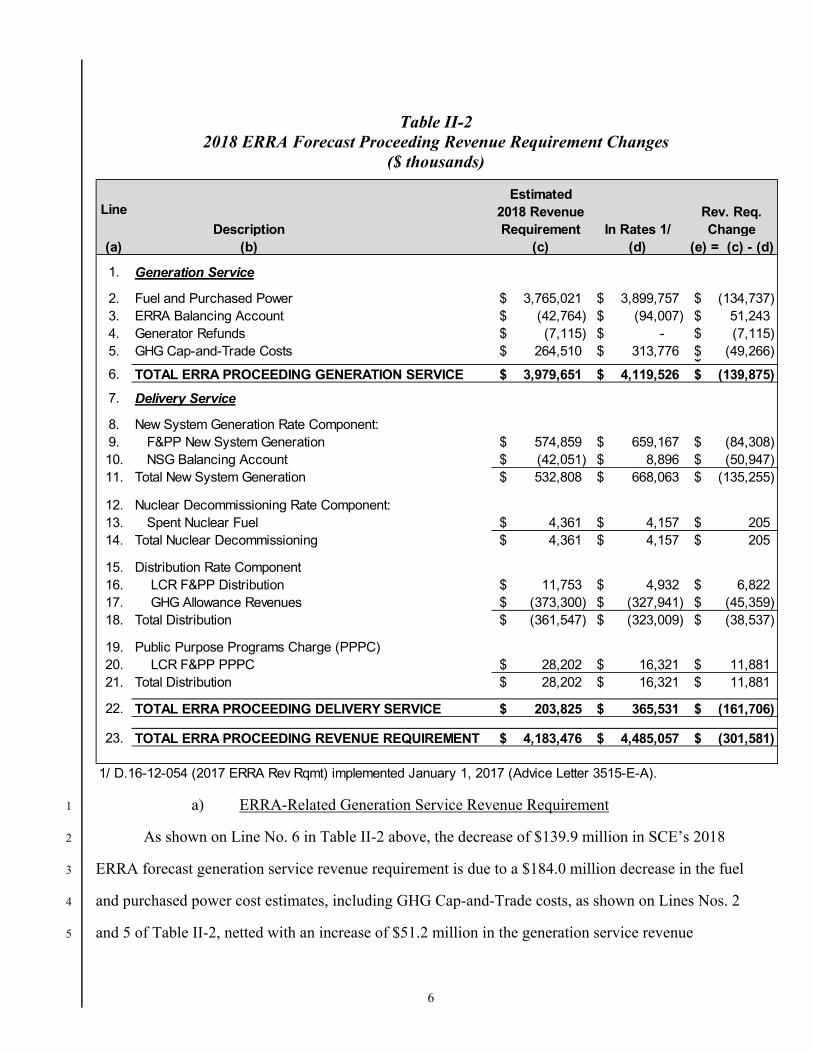

Table II-2 2018 ERRA Forecast Proceeding Revenue Requirement Changes

($ thousands)

a) ERRA-Related Generation Service Revenue Requirement 1

As shown on Line No. 6 in Table II-2 above, the decrease of $139.9 million in SCE’s 2018 2

ERRA forecast generation service revenue requirement is due to a $184.0 million decrease in the fuel 3

and purchased power cost estimates, including GHG Cap-and-Trade costs, as shown on Lines Nos. 2 4

and 5 of Table II-2, netted with an increase of $51.2 million in the generation service revenue 5

Line

Description

Estimated 2018 Revenue Requirement In Rates 1/

Rev. Req. Change

(a) (b) (c) (d) (e) = (c) - (d)

1. Generation Service

2. Fuel and Purchased Power 3,765,021$ 3,899,757$ (134,737)$ 3. ERRA Balancing Account (42,764)$ (94,007)$ 51,243$ 4. Generator Refunds (7,115)$ -$ (7,115)$ 5. GHG Cap-and-Trade Costs 264,510$ 313,776$ (49,266)$ $ 6. TOTAL ERRA PROCEEDING GENERATION SERVICE 3,979,651$ 4,119,526$ (139,875)$

7. Delivery Service

8. New System Generation Rate Component:9. F&PP New System Generation 574,859$ 659,167$ (84,308)$ 10. NSG Balancing Account (42,051)$ 8,896$ (50,947)$ 11. Total New System Generation 532,808$ 668,063$ (135,255)$

12. Nuclear Decommissioning Rate Component:13. Spent Nuclear Fuel 4,361$ 4,157$ 205$ 14. Total Nuclear Decommissioning 4,361$ 4,157$ 205$

15. Distribution Rate Component16. LCR F&PP Distribution 11,753$ 4,932$ 6,822$ 17. GHG Allowance Revenues (373,300)$ (327,941)$ (45,359)$ 18. Total Distribution (361,547)$ (323,009)$ (38,537)$

19. Public Purpose Programs Charge (PPPC)20. LCR F&PP PPPC 28,202$ 16,321$ 11,881$ 21. Total Distribution 28,202$ 16,321$ 11,881$

22. TOTAL ERRA PROCEEDING DELIVERY SERVICE 203,825$ 365,531$ (161,706)$

23. TOTAL ERRA PROCEEDING REVENUE REQUIREMENT 4,183,476$ 4,485,057$ (301,581)$

1/ D.16-12-054 (2017 ERRA Rev Rqmt) implemented January 1, 2017 (Advice Letter 3515-E-A).

7

requirement as shown on Line No. 3 of Table II-2 associated with the estimated year-end 2017 ERRA 1

balance, and a decrease of approximately $7.1 million associated with net Generator refunds related to 2

the 2000-2001 California Energy Crisis settlements approved by the Federal Energy Regulatory 3

Commission (FERC). 4

In addition to the bundled service generation revenue requirement identified in Table II-2 above, 5

SCE’s estimated 2018 ERRA Forecast revenue requirement also includes delivery service amounts. As 6

shown on Line No. 22 in Table II-2 above, the decrease of $161.7 million in SCE’s 2018 ERRA forecast 7

delivery service revenue requirement is due to a decrease in the New System Generation (i.e., CAM-8

related) revenue requirement of $84.3 million, a decrease of $50.9 million associated with SCE’s year-9

end 2017 NSGBA balance, an increase of $0.2 million associated with spent nuclear fuel costs, an 10

increase of $18.7 million associated with Local Capacity Requirement (LCR) contracts and a decrease 11

of $45.4 million associated with GHG allowance revenues to be returned to eligible customers. SCE 12

discusses the background for recovering these costs through CAM in more detail in Chapter VIII. The 13

GHG allowance revenue forecast is discussed in Chapter VII.14

8

III. 1

SCE’S BUNDLED ENERGY FORECAST 2

This chapter presents a summary of SCE’s forecast of 2018 bundled service customer energy 3

load in its service area and a brief description of the methodology used to produce the forecast. A brief 4

discussion of the major factors and assumptions that influence the forecast is also presented. 5

A. Retail Sales Forecast Summary 6

SCE developed its bundled customer energy forecast for this ERRA filing based on a retail 7

customer sales forecast that was completed on December 4, 2016. The retail sales forecast consists of 8

forecast sales to bundled service, DA, and CCA customers measured at the customer meter. Total retail 9

electricity sales in the SCE service area totaled 85,448 GWh in 2016. For 2017 and 2018, SCE is 10

forecasting sales of 83,171 GWh and 83,227 GWh, respectively. The predicted decrease in sales 11

between 2016 and 2017 is about negative 2.7 percent. The primary drivers of the lower forecast are 12

weather and declining average residential usage as a result of energy efficiency savings. Temperatures 13

as measured by Cooling Degree Days were warmer than normal in 2016. Therefore, the transition from 14

an above-normal weather year to a normal weather year assumed in the forecast has a downward impact 15

on predicted sales in 2017 relative to recorded sales in 2016. 16

For the ERRA forecast proceeding, the forecast of retail sales is converted to a forecast of 17

bundled service customer sales, and then converted to a forecast of bundled customer energy at the 18

California Independent System Operator (CAISO) interface (i.e., distribution line losses are accounted 19

for). The difference between bundled sales and bundled energy is that bundled sales represents the 20

energy delivered to and measured at the customer meter as it is billed, while bundled energy consists of 21

the energy delivered to the customer meter plus distribution losses as measured during the hour it is 22

consumed. This definition of load is referred to as “measured at the CAISO interface.” The CAISO 23

interface is where all wholesale energy transactions and settlements take place. 24

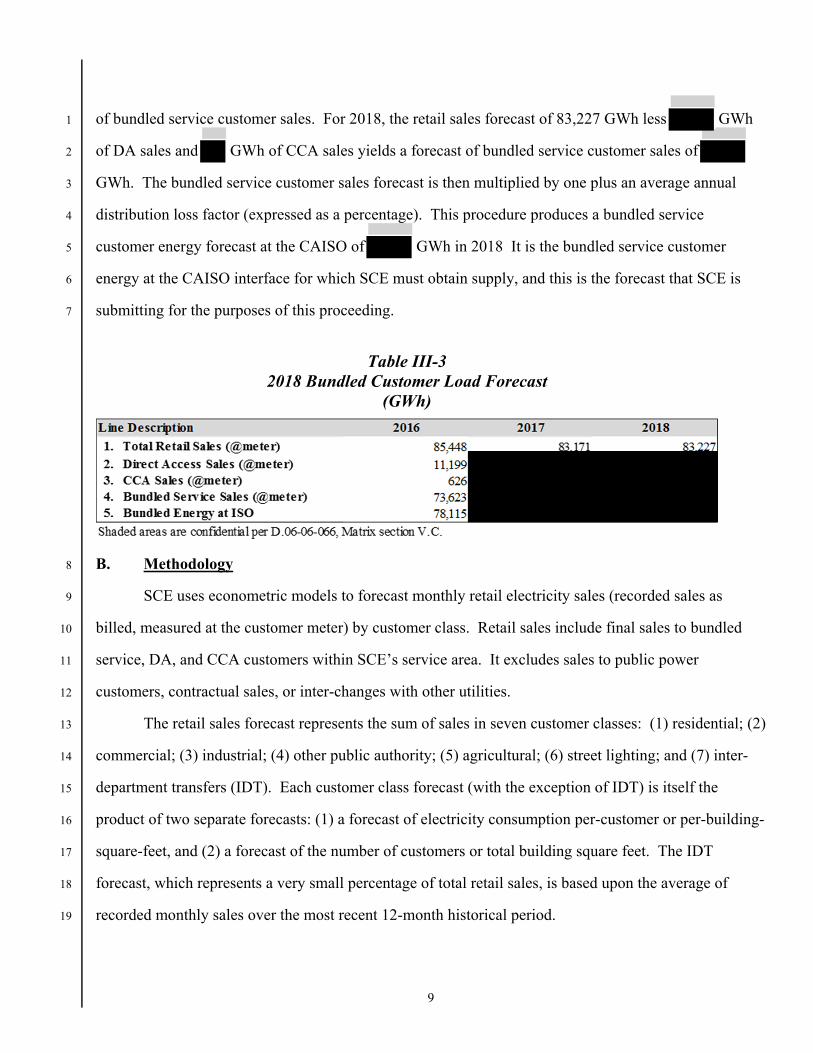

Table III-3 summarizes the steps in converting retail sales to bundled customer energy at the 25

CAISO interface. Retail sales consist of two components: (1) bundled service customer sales and (2) 26

DA and CCA sales. Deducting the forecast of DA and CCA sales from total retail sales yields a forecast 27

9

of bundled service customer sales. For 2018, the retail sales forecast of 83,227 GWh less GWh 1

of DA sales and GWh of CCA sales yields a forecast of bundled service customer sales of 2

GWh. The bundled service customer sales forecast is then multiplied by one plus an average annual 3

distribution loss factor (expressed as a percentage). This procedure produces a bundled service 4

customer energy forecast at the CAISO of GWh in 2018 It is the bundled service customer 5

energy at the CAISO interface for which SCE must obtain supply, and this is the forecast that SCE is 6

submitting for the purposes of this proceeding. 7

Table III-3 2018 Bundled Customer Load Forecast

(GWh)

B. Methodology 8

SCE uses econometric models to forecast monthly retail electricity sales (recorded sales as 9

billed, measured at the customer meter) by customer class. Retail sales include final sales to bundled 10

service, DA, and CCA customers within SCE’s service area. It excludes sales to public power 11

customers, contractual sales, or inter-changes with other utilities. 12

The retail sales forecast represents the sum of sales in seven customer classes: (1) residential; (2) 13

commercial; (3) industrial; (4) other public authority; (5) agricultural; (6) street lighting; and (7) inter-14

department transfers (IDT). Each customer class forecast (with the exception of IDT) is itself the 15

product of two separate forecasts: (1) a forecast of electricity consumption per-customer or per-building-16

square-feet, and (2) a forecast of the number of customers or total building square feet. The IDT 17

forecast, which represents a very small percentage of total retail sales, is based upon the average of 18

recorded monthly sales over the most recent 12-month historical period. 19

10

Econometric models employ statistical techniques to quantify the relationship between electricity 1

consumption and the various economic, demographic, and other factors that influence electricity 2

consumption. Examples of such variables are weather, electricity rates, billing days, energy efficiency 3

program savings, employment, personal income, and building floor stock. Historical data is used to 4

determine these relationships. The typical estimation procedure used to construct the models is ordinary 5

least squares (OLS). Model-generated forecasts may be modified based on current trends, judgment, 6

and events that are not specifically modeled in the econometric equations. 7

Once a satisfactory statistical relationship is established, SCE uses historical average values of 8

weather (cooling and heating degree days) and billing days to represent typical or normal conditions in 9

future periods. Forecasts of economic drivers such as employment, personal income, and building floor 10

stock, along with the typical weather and billing day variables, are then “plugged into” the models in 11

order to derive forecast values of electricity consumption per customer. Moody’s Analytics and Dodge 12

Data & Analytics are the principal sources of employment, personal income, and floor stock data, both 13

historical and forecast. 14

The forecasts of both residential and non-residential customers are based on econometric models 15

that relate changes in the number of customers to a change in economic activity. For example, in the 16

case of residential customers, population growth is used as the leading economic variable to forecast the 17

number of customers. Changes in the number of small commercial customers are assumed to be 18

influenced by changes in the number of residential customers, while changes in the number of industrial 19

customers are dependent upon changes in manufacturing employment. 20

C. Historical Trends 21

On a recorded basis, SCE’s total electricity sales increased at an average annual rate of negative 22

0.6 percent per year between 2009 and 2016. Sales growth has not been consistently negative during 23

this period. For example, annual sales growth surpassed 3 and 2 percent in 2012 and 2014, respectively. 24

However, increased sales in these two years were a result of above-average weather. Customer growth 25

has remained positive during the post-recession period of 2009 to 2016, averaging 0.5% annual growth. 26

11

In 2014 and 2015, annual customer growth reached 0.6%, the highest level since 2007, but still well 1

below the levels reached during the regional housing boom. 2

After the Great Recession and the weak initial recovery, the Southern California economy has 3

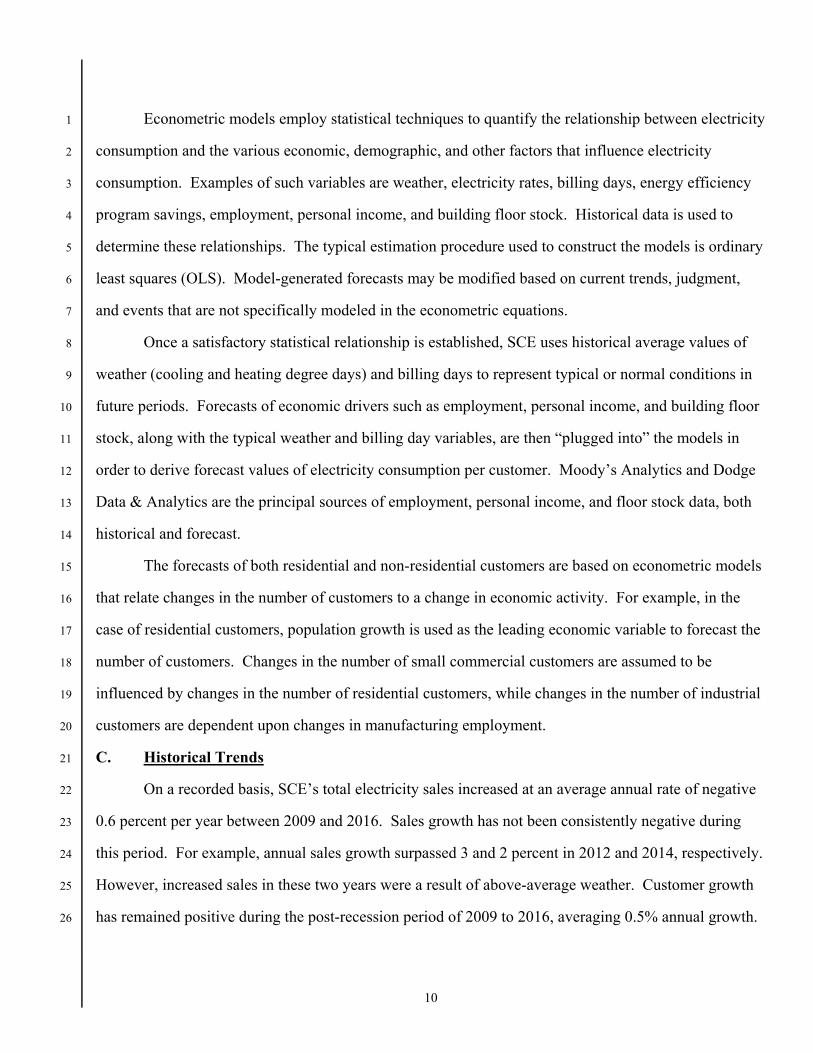

settled into a modest economic expansion as outlined in Figure III-1. The pace of job growth in SCE’s 4

service territory picked up in 2015 before subsiding modestly in 2016. The number of housing starts 5

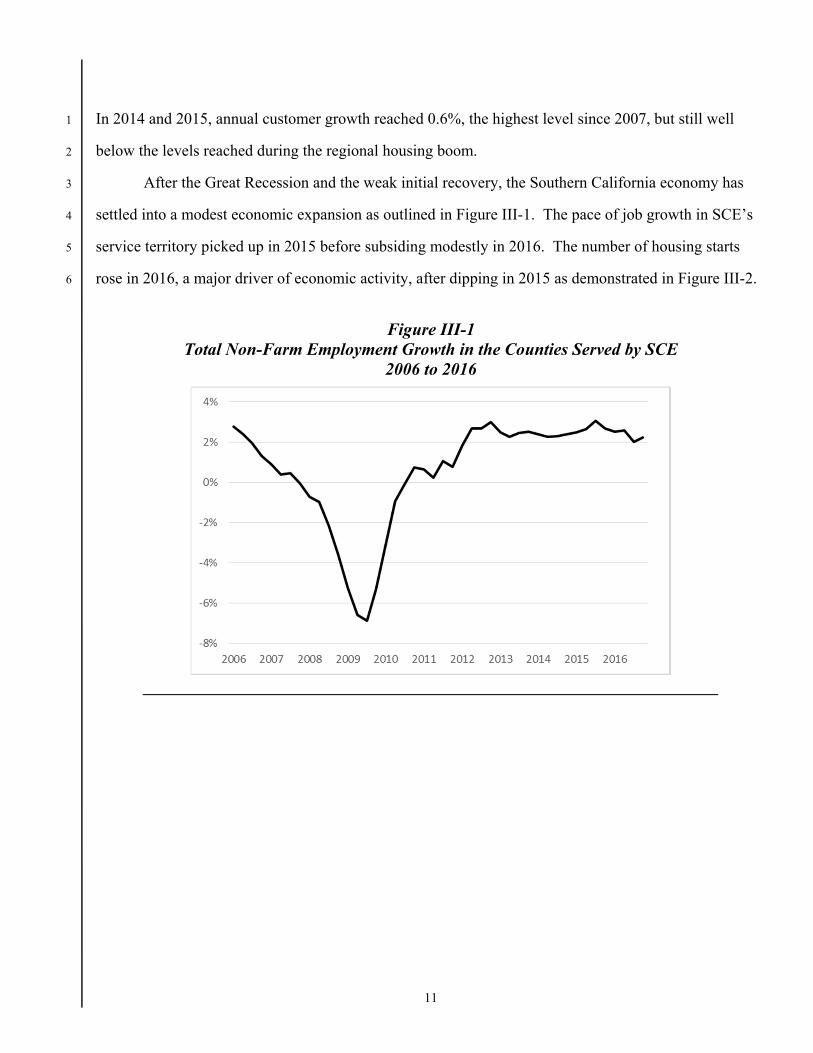

rose in 2016, a major driver of economic activity, after dipping in 2015 as demonstrated in Figure III-2. 6

Figure III-1 Total Non-Farm Employment Growth in the Counties Served by SCE

2006 to 2016

12

Figure III-2 Residential Housing Starts in Counties Served by SCE

D. Economic Outlook 1

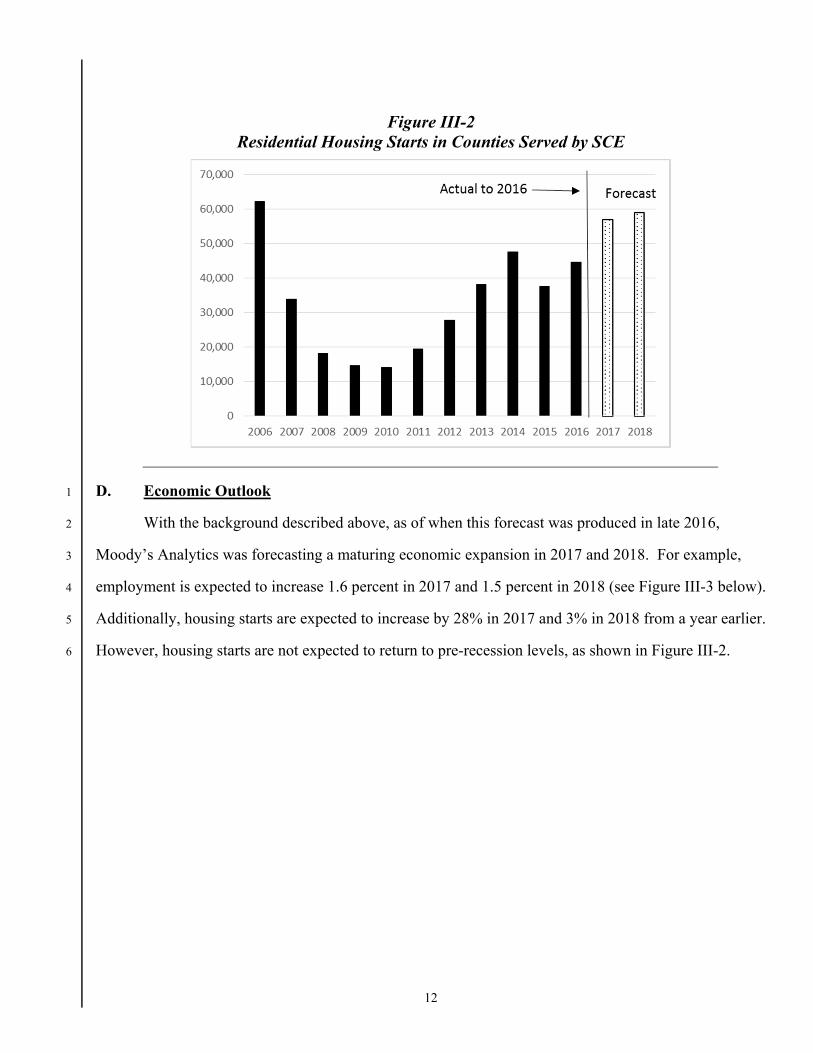

With the background described above, as of when this forecast was produced in late 2016, 2

Moody’s Analytics was forecasting a maturing economic expansion in 2017 and 2018. For example, 3

employment is expected to increase 1.6 percent in 2017 and 1.5 percent in 2018 (see Figure III-3 below). 4

Additionally, housing starts are expected to increase by 28% in 2017 and 3% in 2018 from a year earlier. 5

However, housing starts are not expected to return to pre-recession levels, as shown in Figure III-2. 6

13

Figure III-3 Total Non-Farm Employment Growth in SCE Service Area

Actual and Forecast

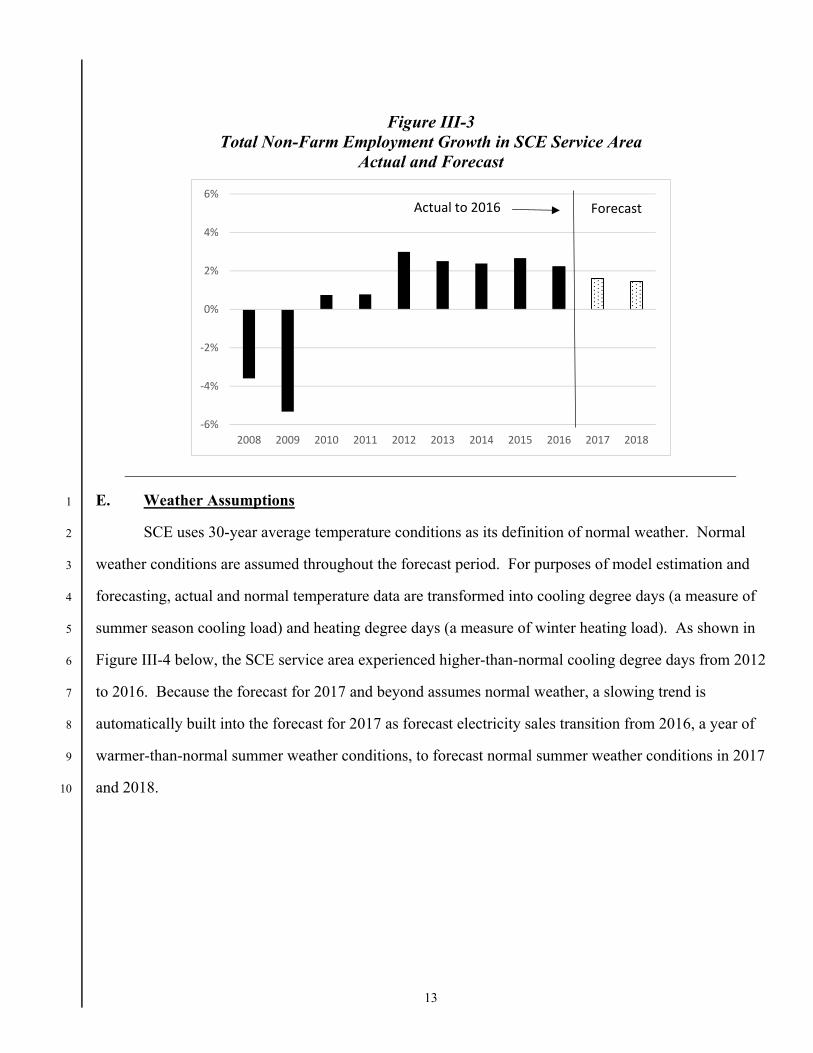

E. Weather Assumptions 1

SCE uses 30-year average temperature conditions as its definition of normal weather. Normal 2

weather conditions are assumed throughout the forecast period. For purposes of model estimation and 3

forecasting, actual and normal temperature data are transformed into cooling degree days (a measure of 4

summer season cooling load) and heating degree days (a measure of winter heating load). As shown in 5

Figure III-4 below, the SCE service area experienced higher-than-normal cooling degree days from 2012 6

to 2016. Because the forecast for 2017 and beyond assumes normal weather, a slowing trend is 7

automatically built into the forecast for 2017 as forecast electricity sales transition from 2016, a year of 8

warmer-than-normal summer weather conditions, to forecast normal summer weather conditions in 2017 9

and 2018. 10

-6%

-4%

-2%

0%

2%

4%

6%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Actual to 2016 Forecast

14

Figure III-4 Recorded and Forecast Cooling Degree Days

F. Other Factors Influencing the Forecast 1

Other factors influencing the growth trend in total retail sales during the forecast period are 2

electricity rates, energy savings from SCE’s energy efficiency programs, and self-generation, such as 3

residential rooftop solar installations and behind-the-meter combined-heat-and-power generation. 4

SCE’s average electricity rate was relatively constant in current dollars between 2007 and 2011, 5

and increased in 2012, 2013, and 2014. Rates declined in 2015 and 2016. At the time the forecast was 6

prepared, the expectation was that rates would be increasing in 2017 and 2018. Historical and forecast 7

system average rates are shown in Figure III-5. All other things being equal, higher electric rates reduce 8

average electricity use per customer. 9

15

Figure III-5 Average System Electricity Rates, Actual and Forecast

(cents/kWh)

Energy efficiency (EE) savings represent electricity consumption that would have taken place in 1

the absence of specific utility-funded programs. Therefore, the forecast of total retail sales in 2017 and 2

2018 would have been higher in the absence of these programs. SCE treats customer self-generation 3

from thermal and solar (photovoltaic) sources in a similar manner in its forecast. SCE reflects some EE 4

trends in the econometric estimation of kWh consumption-per-customer. Additionally, anticipated EE 5

savings exceeding historical norms are deducted after-the-fact on an incremental basis as needed. 6

G. Total Retail Sales Forecast by Customer Class 7

Table III-4 below presents SCE’s forecast of total electricity sales by customer class. The table 8

shows actual recorded sales in 2016 and forecast numbers for 2017 and 2018. The projected average 9

annual growth in total retail sales is negative 2.7 percent in 2017 and negative 2.6 percent in 2018 10

relative to recorded retail sales in 2016. 11

16

Table III-4 Annual Retail Sales by Customer Class

(GWh)

H. Customer Forecast 1

Table III-5 shows SCE’s forecast of total electricity customers. SCE expects the number of 2

customers to increase 1.0 percent in 2017 and 0.9 percent in 2018. As discussed above, customer 3

growth is closely tied to activity in the residential construction sector, but usually with a lag of 3 to 18 4

months. In other words, a change in the number of new customers is typically a result of a change in the 5

number of housing starts that occurred 3 to 18 months earlier. As housing starts continue to increase, 6

SCE expects customer growth to increase in 2016 and 2017. 7

Table III-5 Year-End Customers by Customer Class

17

I. Annual and Monthly Bundled Energy 1

By the end of 2013, DA partial reopening to non-residential customers was completed. In the 2

near term, SCE is expecting increases in DA load to be small or remain flat as the DA phase-in has been 3

completed. SCE had its first departing CCA load starting in May 2015 in the form of Lancaster Choice 4

Energy (LCE). A second CCA, Apple Valley Choice Energy (AVCE) began operations at the beginning 5

of April 2017. As a result, SCE’s bundled sales growth has been reduced relative to retail sales growth. 6

SCE anticipates that additional CCAs may begin operations in SCE’s service territory in 2017 and 2018 7

and will update its CCA forecast in the November ERRA update based on SCE’s internal CCA forecast 8

criteria.7 9

Annual bundled energy at the CAISO delivery point is derived by adjusting the annual bundled 10

sales forecast for distribution losses. Specifically, SCE applies a historical average loss factor to retail 11

sales in the following way: Annual Bundled Energy @ CAISO = Annual Bundled Sales * DLF, where 12

DLF is the ratio of CAISO settlement quality meter data and bundled sales at the customer meter 13

averaged over the years 2012 to 2016. 14

Monthly bundled energy at the CAISO delivery point is derived through a series of steps that 15

begins with the annual bundled energy forecast. Annual bundled energy is first allocated to each hour in 16

a year using a set of hourly load shape equations. The load shape equations were created by 17

econometric methods that relate each hour’s recorded load to daily average temperature, calendar 18

variables such as day of week, month, holidays, and various time trend variables. Monthly energy is 19

then derived by summing the hourly load associated with each calendar month. Finally, monthly 20

bundled customer peak demand is determined by selecting the maximum hourly load in each calendar 21

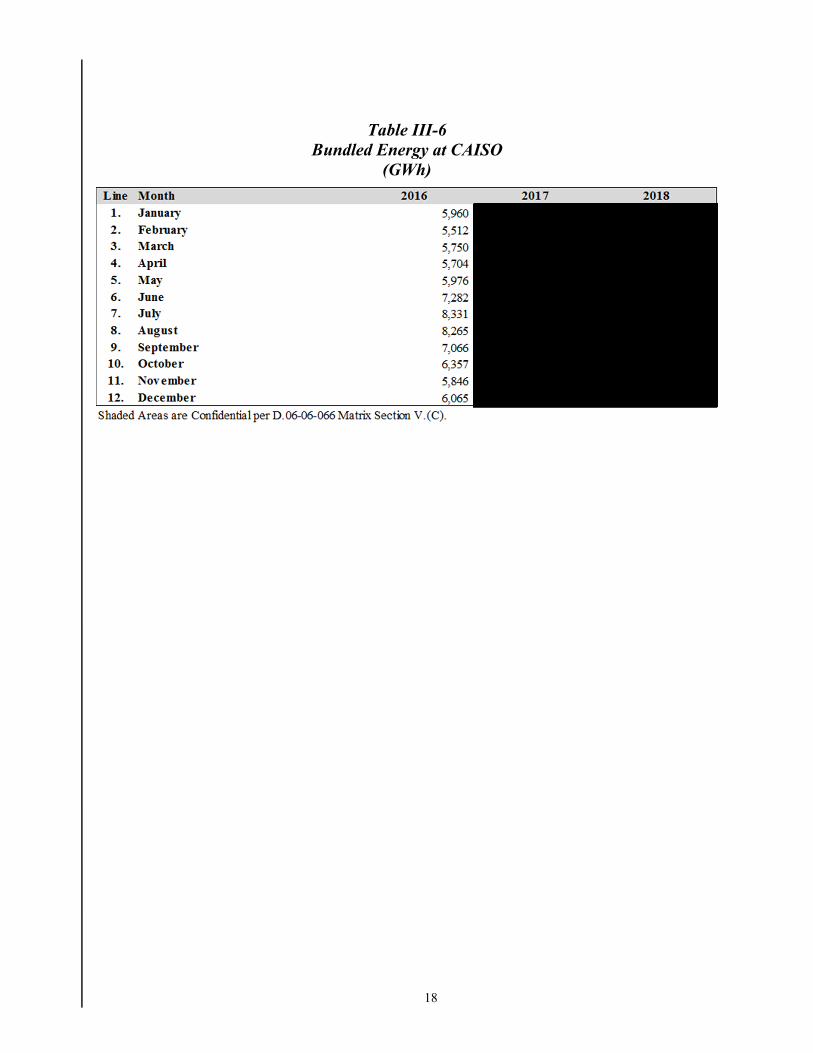

month. Table III-6 presents actual recorded bundled monthly energy at CAISO in 2016 and the forecast 22

of monthly bundled energy at CAISO in 2017 and 2018. 23

7 SCE’s internal criteria for a qualifying governmental entity to be included in the CCA departing load forecast

is: (1) the filing of a binding notice of intent (BNI) to begin CCA service, (2) an initial Resource Adequacy (RA) filing, or (3) the start of CCA service.

18

Table III-6 Bundled Energy at CAISO

(GWh)

19

IV. 1

FORECAST ENERGY PRODUCTION AND COSTS FROM SCE’S PORTFOLIO OF 2

RESOURCES 3

A. Introduction 4

This chapter describes SCE’s resource portfolio and the associated forecast costs that SCE 5

proposes to recover in its ERRA balancing account. SCE’s resource portfolio is comprised of its utility-6

owned generation (UOG), which includes nuclear, natural gas, hydroelectric, fuel cells, and renewable 7

generation resources; SCE’s purchased power resources, including CHP and renewable resources, 8

interutility contracts, and bilateral contracts; and proxy8 (i.e., generic) costs from anticipated future 9

solicitations and market purchases. SCE’s 2018 forecast also includes executed contracts from SCE’s 10

Local Capacity Requirements (LCR) solicitations for the Western Los Angeles (LA) Basin and 11

Moorpark regions, as approved in D.15-11-041 and proposed in A.14-11-016, respectively. 12

The decrease in SCE’s 2018 fuel and purchased power cost forecast can be generally attributed 13

to four major factors. First, SCE expects its sales to be lower than it did for the 2017 ERRA forecast. 14

Second, SCE expects lower fuel-related costs from its natural gas-fueled UOG and tolling resources due 15

to lower forecast natural gas prices. Third, SCE expects lower open market costs due to lower forecast 16

SP-15 forward market power prices. Fourth, SCE expects lower SRAC payments due to lower forecast 17

market prices. SCE used $58.27/kW-year as the proxy price to meet Generic Capacity need as outlined 18

in the 2015 “Estimated Cost of New Renewable and Fossil Generation in California Final Staff Report” 19

study issued by the CEC. 20

B. Energy Production Forecast Methodology 21

In this ERRA Forecast application, as in its past forecast applications, SCE forecasts energy 22

production from its portfolio primarily using the Ventyx Planning and Risk (PROSYM) software.9 The 23

8 The proxy capacity costs are further discussed in Section IV.E.

9 Ventyx is the current owner of the originally developed Henwood PROSYM tool. Ventyx’s Planning and Risk Software is primarily powered by the PROSYM engine.

20

Ventyx models are used to: (1) forecast the least-cost dispatch (LCD) of dispatchable resources in 1

SCE’s portfolio; (2) optimize hydro dispatch; and (3) perform Monte Carlo simulations of forced outage 2

rates of individual units. 3

The simulated dispatch is based on a forecast of power, gas, and GHG prices,10 physical 4

constraints of each generating unit, and contractual limitations. SCE’s forecast methodology 5

economically dispatches resources in a least-cost manner as directed by the Commission, rather than 6

force-dispatching resources to meet SCE’s forecast of bundled customer demand. Under the LCD 7

principle, a generating resource or contract is simulated to dispatch if its marginal operating cost is less 8

than the market price of power, while simultaneously observing all operating constraints.11 For a given 9

hour, the difference between the forecast bundled load and the total forecast economic dispatch of SCE’s 10

resource portfolio constitutes SCE’s projected open position for the hour. 11

SCE based its 2018 power price forecast on the forward power broker quotes for 2018 in effect 12

as of February 23, 2017. The 24-hour flat price as of February 23, 2017, was $28.59/MWh for 2018.12 13

SCE derived its hourly price forecast by applying on-peak and off-peak hourly price profiles to the 14

respective monthly on-peak and off-peak forward quotes for 2018 in effect as of February 23, 2017,13 15

such that the simple averages of the hourly on-peak and off-peak forecast prices for a particular month 16

match the forward on-peak and off-peak power prices for that month. SCE updated its existing MRTU-17

based statistical models to generate hourly price profiles for the SP-15 and NP-15 zones.14 18

10 The Ventyx models were not used to develop forecasts of competitive market power or GHG prices. These

prices were developed independently, as discussed in the following paragraphs. The GHG price forecast was incorporated as part of the resource dispatch cost similar to natural gas prices in order to reflect the additional GHG cost for the generation resources that have GHG emissions.

11 Energy- and use-limited hydroelectric and peaking resources are also dispatched pursuant to LCD; this analysis also incorporates opportunity cost principles regarding water and emissions limitations, respectively, to ensure that such units are dispatched during higher-priced hours, when it is most economic to do so.

12 SCE has contracts in NP-15. SCE used relevant prices to forecast the cost of those contracts.

13 SCE used forward prices from the same trading day for power, GHG, and natural gas price forecasts to maintain the consistency of the forward-market outlook.

14 The statistical models incorporated historical MRTU data from the CAISO’s Integrated Forward Market (IFM).

21

SCE used the Intercontinental Exchange’s (ICE) settlement price of a 2018-vintage GHG 1

allowance as the basis for its 2018 GHG price forecast. The ICE settlement price as of February 23, 2

2017, was $14.06/MT for 2018. This price is assumed to be constant for any GHG emissions produced 3

in 2018.15 Lastly, SCE based its daily natural gas price forecast on monthly NYMEX forward prices at 4

the SoCal Border in effect as of February 23, 2017, plus intrastate transportation charges from Southern 5

California Gas Company (SoCalGas), as applicable.16 The 12-month average NYMEX forward gas 6

price as of February 23, 2017 was $2.78/MMBtu for 2018. Within a given month, SCE assumed that the 7

daily gas price forecast is equal to the monthly forward price. 8

C. Validation of SCE’s Energy Production Forecast 9

SCE follows a consistent process to forecast its energy production and costs for the subsequent 10

calendar year, supported by a robust internal validation process. SCE’s forecast process is discussed 11

below. 12

The first stage of SCE’s forecast process involves developing all forecast inputs. These inputs 13

include, but are not limited to, SCE’s forecast of power, gas, and GHG prices; production from UOG 14

resources (nuclear, hydro, gas, fuel cells and renewable facilities); CHP and renewable energy 15

production and costs; gas hedging costs; CAISO costs, etc. These inputs are developed and vetted by 16

various business groups or divisions responsible for each input and then submitted to senior managers in 17

SCE’s Power Supply Organizational Unit for further review and approval. 18

Once approved, the forecast inputs are utilized in PROSYM, which is an industry-standard 19

production cost model capable of modeling various types of resources with differing constraints. SCE 20

uses PROSYM to forecast its LCD activities. Once the dispatch results are produced, SCE conducts a 21

15 In prior years, direct and indirect GHG costs were reviewed in a separate GHG Cost and Revenue Forecast

application. Pursuant to D.14-10-033, they will now be reviewed in this proceeding, and are discussed in further detail in Chapter VII.

16 Not all generating resources in SCE’s portfolio utilize transportation service from SoCalGas.

22

thorough validation of the dispatch outcomes by resource.17 If necessary, SCE will rerun the previous 1

forecast steps if it believes more accurate dispatch results can be realized. 2

Once dispatch results are validated, all energy and cost forecasts are input into SCE’s ERRA 3

forecasting tool, an internally-developed, automated software program that aggregates the hourly energy 4

production and cost forecast data. The ERRA forecasting tool produces the ERRA forecast tables 5

included in the following section(s). Prior to inclusion in SCE’s ERRA Forecast filing, the forecast 6

tables are reviewed and approved by SCE’s senior management. 7

D. 2018 Energy and Cost Forecast Summary 8

Because this ERRA application is designed to forecast SCE’s energy-related costs that will 9

ultimately be used to establish retail generation rates in 2018, a single expected scenario forecast is 10

utilized. All production and residual open position forecasts provided in this section are reflected at the 11

CAISO system interface. To accomplish this, SCE reduced generation production forecasts by the 12

forecast transmission losses and grossed up the forecast retail load by the forecast distribution losses. 13

Table IV-7 summarizes the monthly forecast production from SCE’s portfolio and SCE’s open energy 14

positions. Table IV-8 summarizes the monthly forecast cost of SCE’s purchased power resources 15

accounted for in the ERRA balancing account. The remainder of this chapter provides detailed 16

descriptions of the resources and the underlying forecast assumptions.17

17 For example, SCE compares its dispatch results against prior ERRA forecasts and reviews any significant

discrepancies to ensure that its results are reasonably justified.

23

Tabl

e IV

-7

2018

Ene

rgy

For

ecas

t of t

he S

CE

Por

tfolio

(G

Wh)

C

onfid

entia

l te

mJa

n-18

Feb-

18M

ar-1

8Ap

r-18

May

-18

Jun-

18Ju

l-18

Aug-

18Se

p-18

Oct

-18

Nov

-18

Dec

-18

Tota

l

1SC

E Bu

nded

Loa

d

2 3SC

E Po

rtfo

io

4N

ucea

r

5M

ount

ainv

iew

6SC

E Pe

aker

s

7H

ydro

8U

OG

Sto

rage

9A

iso

Cany

on P

rocu

rem

ents

10SC

EO

wne

d SP

VP

11CH

P &

Ren

ewab

es

12G

reen

Rat

e Pr

ogra

m

13nt

erU

tiit

y Co

ntra

cts

1420

13 B

iat

era

1520

0607

So

icit

atio

n

16LC

R Co

ntra

cts

Sto

rage

17LC

R Co

ntra

cts

Gas

Fir

ed

18D

eman

d Re

spon

se0

00

01

12

22

10

09

19 20To

ta S

CE P

ortf

oio

21 22O

pen

Ener

gy P

ositi

on

24

Table IV-8 2018 Forecast of Fuel and Purchased Power Costs

($000) Confidential

25

Table IV-8 (Con’t) 2018 Forecast of Fuel and Purchased Power Costs

($000) Confidential

26

E. SCE’s Utility-Owned Generation and Purchased Power Contracts 1

1. Hydro Facilities 2

SCE’s hydro resources consist of 33 powerhouses in central and southern California, which 3

provide 1,176 MW of nameplate capacity. SCE’s hydro division is organized into two regions, Northern 4

and Eastern. The Northern Division hydro region, also known as the Big Creek Project, is located in 5

central California about 50 miles east of Fresno in the western Sierra Nevada Mountains. Big Creek’s 6

nine powerhouses provide 1,015 MW of nameplate capacity. The Eastern Division hydro region 7

consists of SCE’s powerhouses located in the eastern and southern Sierra Nevada Mountains, as well as 8

in the San Bernardino and San Gabriel Mountains of southern California. The Eastern Division hydro 9

region’s 24 powerhouses provide 161 MW of nameplate capacity. 10

The Big Creek hydro system is a flexible, dispatchable resource, except during the period of 11

spring run-off. During this period, in a normal water year, the generating units typically need to operate 12

near maximum capacity for 24 hours per day to ensure that spill is minimized. For ERRA forecast 13

purposes, SCE optimizes the Big Creek Project by operating at full capacity (when operationally 14

possible) during the highest economic value hours. When Big Creek does not operate at full capacity, it 15

can generally provide ancillary services to the CAISO market. 16

Eastwood powerhouse is a pump-storage unit providing 199.8 MW of nameplate generating 17

capacity, and is part of the Big Creek Project. The pumpback efficiency is approximately 75 percent, 18

meaning that approximately 1.33 MWh of pumping energy is required to pump enough water back into 19

the forebay to generate 1 MWh of energy at a later time. Pumpback duration generally varies from two 20

to six hours and consumes approximately 180 MWh per hour. Every three hours of pumpback stores 21

enough water to generate for approximately two hours at 199.8 MW. Pumpback and generation 22

dispatch for Eastwood are modeled on an hourly basis assuming economic dispatch. To maximize the 23

value of the resource, pumpback normally takes place during off-peak hours when energy prices are 24

lower, and dispatch normally takes place during peak hours when energy prices are higher. 25

27

SCE’s Eastern Division hydro facilities are predominantly run-of-the-river, non-dispatchable 1

resources and their actual MW output varies based on hydrological conditions. As a result, the forecast 2

energy production is largely deterministic. 3

For 2018, SCE’s forecast of its UOG Hydro production, inclusive of pumpback operations, is 4

shown in Table IV-7. This forecast assumes a slightly-above-normal hydrological year for 2018, and 5

also incorporates SCE’s best estimate of upcoming major planned outages of Big Creek and Eastern 6

Hydro units in 2018. 7

2. SCE Solar Photovoltaic Generation 8

SCE’s Solar Photovoltaic Program (SPVP) is a Commission-approved initiative to install, own, 9

and operate up to 91 MW Direct Current (DC) of utility-owned solar photovoltaic projects on 10

commercial rooftop space and ground-mounts in SCE’s service area.18 SCE estimates that in 2018 that 11

its UOG SPVP solar projects will provide a total of approximately 91 MW DC of capacity, primarily 12

(although not exclusively) located in San Bernardino County. These photovoltaic projects generally 13

provide energy during peak usage times. For 2018, SCE’s forecast of SPVP production, based on the 14

previous year’s project capacity factors, is shown in Table IV-9. 15

Table IV-9 2018 Forecast of SCE SPVP Production

(GWh)

18 The Commission originally approved a 500 MW SPVP program, with 250 MW of projects to be UOG and

250 MW to be owned by independent power producers. See D.09-06-049. SCE’s February 2011 Petition for Modification requested the program be modified to include, among other things, a reduction of both the UOG and the Independent Power Producer portions from 250 MW to 125 MW, and the petition was approved on February 16, 2012. On July 27, 2012, SCE filed a second Petition for Modification to further reduce the UOG portion of the SPVP from 125 MW to 91 MW, given that 18 MW of ground sites were at risk due to interconnection cost and schedule, and 16 MW of formerly-committed rooftops were no longer viable. SCE proposed that the 34 MW reduction from the UOG SPVP Program be transferred to the Renewable RAM Procurement Program. The Commission approved SCE’s petition in D.13-05-033, capping the UOG portion of SPVP at 91 MW. The independent power producer portion of the program maintains its 125 MW program goal.

28

3. CHP and Renewables 1

a) Energy Forecast 2

For the 2018 Forecast Period, SCE expects 19 of energy deliveries at the CAISO 3

interface as shown in Table IV-7 from CHP (combined heat and power) and renewable projects. The 4

energy deliveries from cogeneration and renewable projects are effectively “must take” energy. There 5

are some gas-fired contracts that are dispatched based on market prices. 6

Energy deliveries at the generators’ meters are forecast to be The 319 projects 7

delivering energy have approximately 9,789 MW of contract capacity allocated as follows: 8

• 1,319 MW of CHP capacity; 9

• 8,470 MW of renewable capacity.20 10

In addition and not included in the above capacity numbers, SCE has contracted an additional 11

174 MW of dispatchable capacity through the CHP Program Settlement requests for offers. 12

SCE uses the historical performance of each project to forecast monthly energy deliveries. From 13

March 2017 through December 2018, 31 projects are expected to begin delivering energy. Some of 14

these projects have been delivering energy and signed new contracts. Others are new projects under 15

development and are adjusted by their probability of successful development and commercial operation. 16

The total capacity for these projects is approximately 1,187 MW. The nineteen new projects (15 solar 17

and 4 wind) are expected to begin delivering energy during the period from March 2017 through 18

December 2018. Because there are no historical performance data for these new projects, forecast 19

energy deliveries are based on contractual expectations discounted by their expected probabilities of 20

successful development. 21

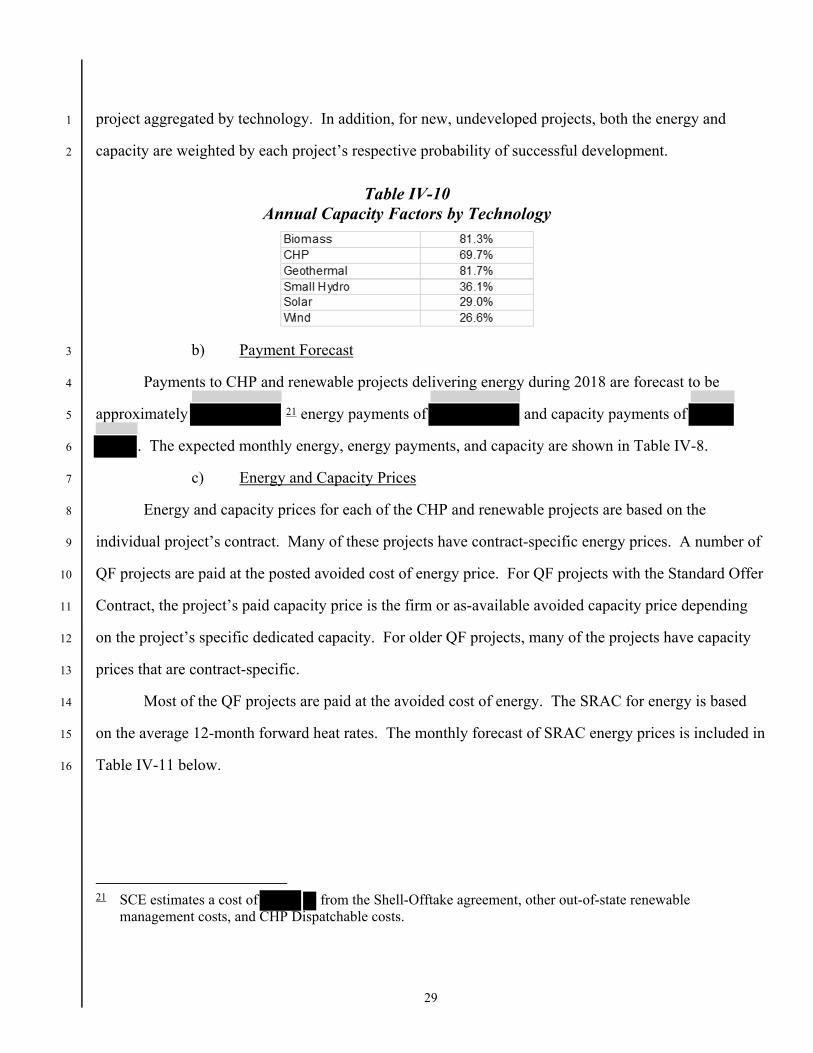

Table IV-10 lists the average annual capacity factors for each of the six technologies. These 22

average annual capacity factors are based on expected annual energy and contract capacity for each 23

19 includes generation loss and the Shell Offtake agreement, and excludes 11 GWh allocated to

serve Green Tariff customers as a part of the GTSR Program described in Section E.10.

20 The contract capacity for a project that is not developed is weighted by the project’s expected commercially-operable success rate.

29

project aggregated by technology. In addition, for new, undeveloped projects, both the energy and 1

capacity are weighted by each project’s respective probability of successful development. 2

Table IV-10 Annual Capacity Factors by Technology

b) Payment Forecast 3

Payments to CHP and renewable projects delivering energy during 2018 are forecast to be 4

approximately 21 energy payments of and capacity payments of 5

. The expected monthly energy, energy payments, and capacity are shown in Table IV-8. 6

c) Energy and Capacity Prices 7

Energy and capacity prices for each of the CHP and renewable projects are based on the 8

individual project’s contract. Many of these projects have contract-specific energy prices. A number of 9

QF projects are paid at the posted avoided cost of energy price. For QF projects with the Standard Offer 10

Contract, the project’s paid capacity price is the firm or as-available avoided capacity price depending 11

on the project’s specific dedicated capacity. For older QF projects, many of the projects have capacity 12

prices that are contract-specific. 13

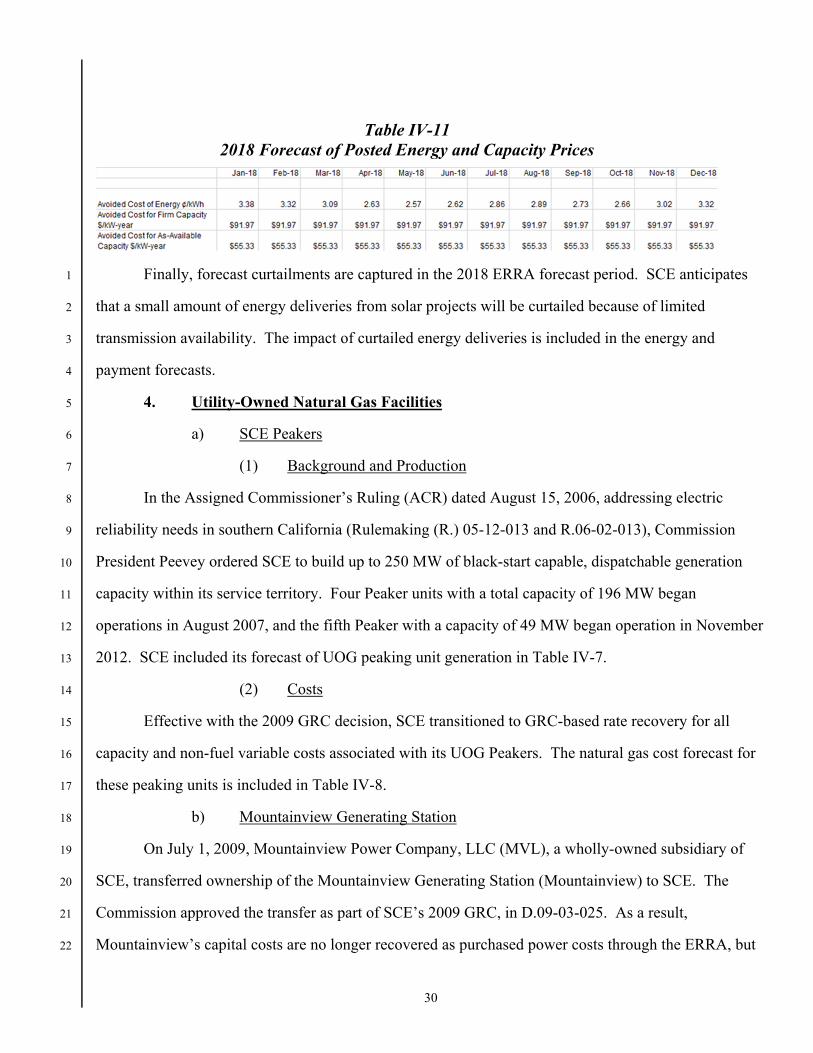

Most of the QF projects are paid at the avoided cost of energy. The SRAC for energy is based 14

on the average 12-month forward heat rates. The monthly forecast of SRAC energy prices is included in 15

Table IV-11 below. 16

21 SCE estimates a cost of from the Shell-Offtake agreement, other out-of-state renewable

management costs, and CHP Dispatchable costs.

30

Table IV-11 2018 Forecast of Posted Energy and Capacity Prices

Finally, forecast curtailments are captured in the 2018 ERRA forecast period. SCE anticipates 1

that a small amount of energy deliveries from solar projects will be curtailed because of limited 2

transmission availability. The impact of curtailed energy deliveries is included in the energy and 3

payment forecasts. 4

4. Utility-Owned Natural Gas Facilities 5

a) SCE Peakers 6

(1) Background and Production 7

In the Assigned Commissioner’s Ruling (ACR) dated August 15, 2006, addressing electric 8

reliability needs in southern California (Rulemaking (R.) 05-12-013 and R.06-02-013), Commission 9

President Peevey ordered SCE to build up to 250 MW of black-start capable, dispatchable generation 10

capacity within its service territory. Four Peaker units with a total capacity of 196 MW began 11

operations in August 2007, and the fifth Peaker with a capacity of 49 MW began operation in November 12

2012. SCE included its forecast of UOG peaking unit generation in Table IV-7. 13

(2) Costs 14

Effective with the 2009 GRC decision, SCE transitioned to GRC-based rate recovery for all 15

capacity and non-fuel variable costs associated with its UOG Peakers. The natural gas cost forecast for 16

these peaking units is included in Table IV-8. 17

b) Mountainview Generating Station 18

On July 1, 2009, Mountainview Power Company, LLC (MVL), a wholly-owned subsidiary of 19

SCE, transferred ownership of the Mountainview Generating Station (Mountainview) to SCE. The 20

Commission approved the transfer as part of SCE’s 2009 GRC, in D.09-03-025. As a result, 21

Mountainview’s capital costs are no longer recovered as purchased power costs through the ERRA, but 22

31

instead are recovered in SCE’s authorized base generation revenue requirement and through base rates. 1

However, Mountainview fuel costs and availability and heat rate incentive payments continue to be 2

recorded in the ERRA balancing account.22 SCE included its Mountainview generation forecast in 3

Table IV-7. The natural gas forecast for Mountainview is included in Table IV-8. 4

5. Interutility Contracts Production 5

SCE is a party to three23 major interutility contracts under which it is expected to purchase and/or 6

exchange capacity and associated energy for various periods through September 2017, except for the 7

City of Pasadena which has no expiration date. These interutility contracts were executed prior to 8

industry restructuring and contain complex terms and conditions that were designed to satisfy the unique 9

needs of SCE and each of the counterparties. The current contracts with 1) Western Area Power 10

Administration (WAPA) and the Bureau of Reclamation (Reclamation), and 2) the Metropolitan Water 11

District of Southern California (MWD) expire at the end of September 2017. SCE executed a new fifty-12

year agreement with WAPA and Reclamation with an initial service date of October 1, 2017. Table IV-13

12 summarizes these major interutility contracts. 14

Table IV-12 Non-Coincident Contract Capacity Quantities and

Expiration Dates for SCE’s Major Interutility Contracts

22 See SCE’s 2009 GRC Application, A.07-11-011, Exhibit SCE-02, Vol. 9, Ch. 1, dated November 2007, in

which SCE proposed to include the concepts of the PPA incentive mechanisms in the ERRA proceeding.

23 Excluded from this total are SCE’s so-called “Fringe Service” agreements, which provide for small amounts of energy exchanges among neighboring utilities. These include two contracts with the Department of Defense for the Air Force that SCE presented to the Commission in Advice Letters 2686-E and 1777-E and contracts associated with retail tariffs.

32

The process of forecasting the level of energy deliveries and receipts for interutility contracts 1

with dispatchability (i.e., with WAPA-Reclamation) is an inherently complex task. SCE is forecasting 2

net interutility contract purchases of 198 GWh in 2018. 3

a) WAPA-Reclamation Agreement 4

For 2018, SCE has an entitlement of 280.245 MW of contingent capacity and 238 GWh of firm 5

energy24 from the Boulder Canyon Project (Hoover), marketed by WAPA. 6

Due to the lowering of the surface elevation of Lake Mead, which is the forebay to the Hoover 7

power plant, the amount of capacity and firm energy available to SCE will be reduced from the amounts 8

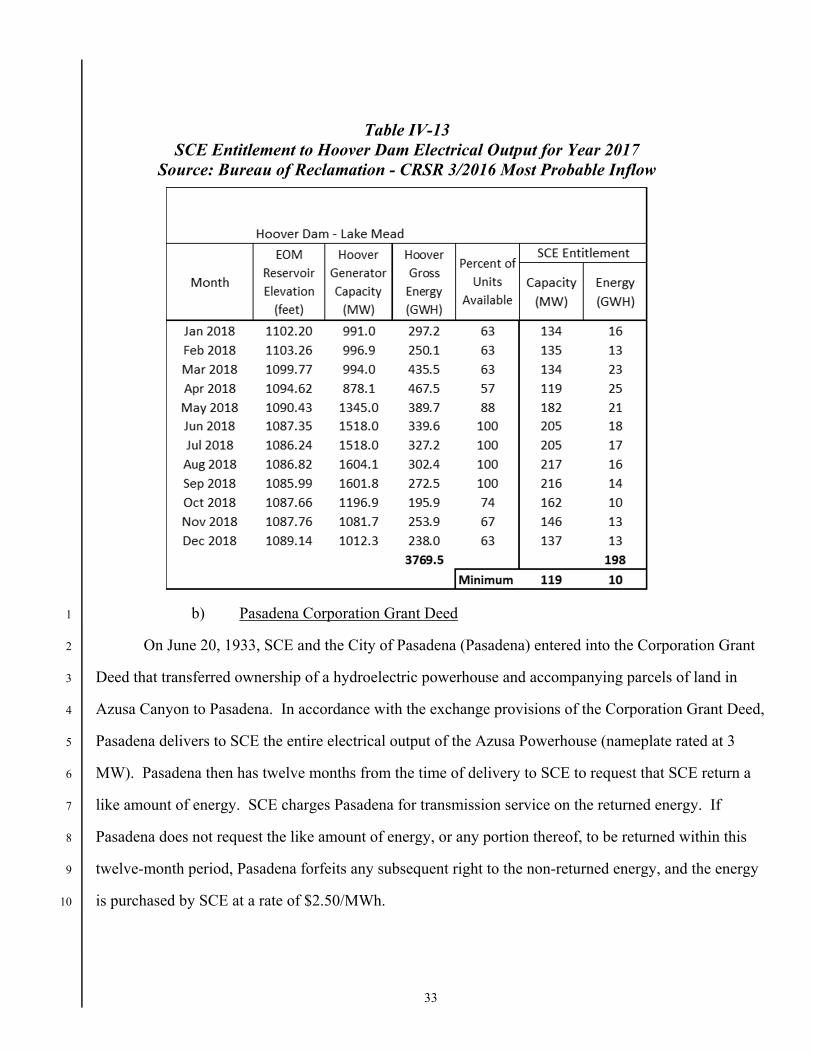

described in the previous paragraph. For the year 2018, the monthly capacity and firm energy available 9

to SCE could range as low as 119 MW and 10 GWh, respectively.25 The forecast amount of capacity 10

and energy available to SCE out of Hoover is shown in Table IV-13. 11

24 Firm energy is energy obligated from Hoover under the Hoover Power Plant Act. During periods when

Hoover is unable to provide energy in amounts equal to the firm energy, WAPA is obligated to provide any deficit, if requested by the purchaser, at a rate equal to WAPA’s cost to acquire.

25 The Bureau of Reclamation, the owner and operator of Hoover Dam, anticipates a low reservoir elevation through 2018 and beyond. The reason for the low elevation is due to low precipitation since 2000.

33

Table IV-13 SCE Entitlement to Hoover Dam Electrical Output for Year 2017

Source: Bureau of Reclamation - CRSR 3/2016 Most Probable Inflow

b) Pasadena Corporation Grant Deed 1

On June 20, 1933, SCE and the City of Pasadena (Pasadena) entered into the Corporation Grant 2

Deed that transferred ownership of a hydroelectric powerhouse and accompanying parcels of land in 3

Azusa Canyon to Pasadena. In accordance with the exchange provisions of the Corporation Grant Deed, 4

Pasadena delivers to SCE the entire electrical output of the Azusa Powerhouse (nameplate rated at 3 5

MW). Pasadena then has twelve months from the time of delivery to SCE to request that SCE return a 6

like amount of energy. SCE charges Pasadena for transmission service on the returned energy. If 7

Pasadena does not request the like amount of energy, or any portion thereof, to be returned within this 8