Embed Size (px)

Citation preview

March, 2014

Investment Thesis

1

Investment Thesis

One of the largest private sector power generators in Brazil

ENEVA currently operates 2.4GW in coal and gas-fired power plants (2.9 GW until the end of year)

Integrated energy platform, with privileged access to natural resources

Only private power generator in Brazil with access to onshore gas

Short-term value triggers

- Reorganization of the company’s structure and continuous TPP’s operation stabilization

- Stronger role of E.ON, bringing technical expertise and cost discipline to ENEVA

Competitive greenfield portfolio

Licensed coal, gas and wind power generation projects

3

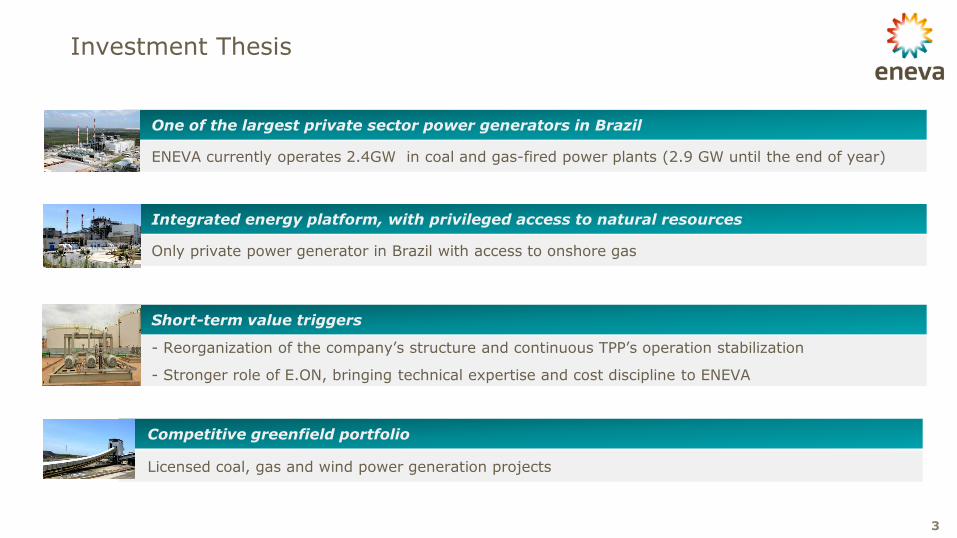

A Brazilian thermal generator with asset exposure to energy fossil fuels (natural gas and coal)

ENEVA at a Glance

2.9GW inflation-protected, long-term PPAs

o 2.4GW in operation

o 517MW under construction

Long-term PPAs guarantee R$2.2 billion in annual inflation-adjusted

capacity payments

PPAs provide hedge against commodity price exposure

Integrated gas E&P assets supply up to 8.4MM m³/day to ENEVA’s power

plants

Competitive portfolio of licensed greenfield wind, coal and gas fired

capacity

Company Description

4

ENEVA ownership structure

Geographic Footprint

Parnaíba I ENEVA 70% / Petra 30% Natural Gas - 676MW

Amapari Energia ENEVA 51% / Eletronorte 49% Diesel - 23MW

Itaqui ENEVA 100% Coal - 360MW

Natural Gas Exploratory

blocks Contracted production

of 8.4MM m3/day

Pecém I ENEVA 50% / EDP 50% Coal - 720MW

Pecém II ENEVA 100% Coal - 365MW

Parnaíba II ENEVA 100% Natural Gas - 517MW

Parnaíba III¹ ENEVA 70% / Petra 30%

Natural Gas - 176MW

Parnaíba IV¹ ENEVA 70% / Petra 30% Natural Gas - 56MW

Free Float (38.2%)

37.9% 23.9%

Other

MPX / E.ON Partipações Joint Venture

50%

50%

BNDES

10.3%

Eike Batista

Controlling Block

27.9%

Solar Tauá ENEVA 100% Solar - 1MW

Note: 1) Ownership structure assumes future MPX / E.ON Participações JV incorporation, as disclosed on the Material Fact Notice as of July 3, 2013

Company Overview

2

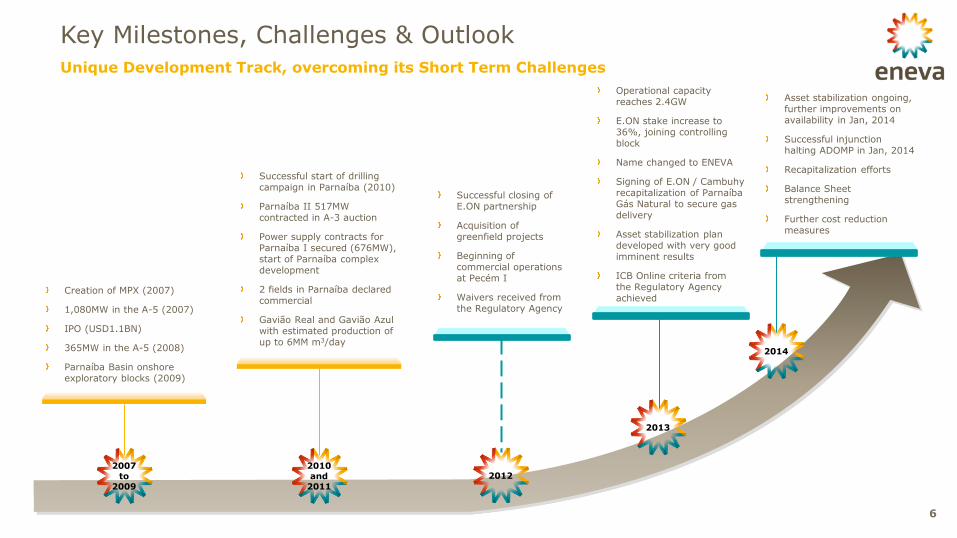

6

Creation of MPX (2007)

1,080MW in the A-5 (2007)

IPO (USD1.1BN)

365MW in the A-5 (2008)

Parnaíba Basin onshore exploratory blocks (2009)

Successful closing of E.ON partnership

Acquisition of greenfield projects

Beginning of commercial operations at Pecém I

Waivers received from the Regulatory Agency

Operational capacity reaches 2.4GW

E.ON stake increase to 36%, joining controlling block

Name changed to ENEVA

Signing of E.ON / Cambuhy recapitalization of Parnaíba Gás Natural to secure gas delivery

Asset stabilization plan developed with very good imminent results

ICB Online criteria from the Regulatory Agency achieved

2007 to

2009

2012

2013

2014

Asset stabilization ongoing, further improvements on availability in Jan, 2014

Successful injunction halting ADOMP in Jan, 2014

Recapitalization efforts

Balance Sheet strengthening

Further cost reduction measures

Successful start of drilling campaign in Parnaíba (2010)

Parnaíba II 517MW contracted in A-3 auction

Power supply contracts for Parnaíba I secured (676MW), start of Parnaíba complex development

2 fields in Parnaíba declared commercial

Gavião Real and Gavião Azul with estimated production of up to 6MM m3/day

2010 and

2011

Unique Development Track, overcoming its Short Term Challenges

Key Milestones, Challenges & Outlook

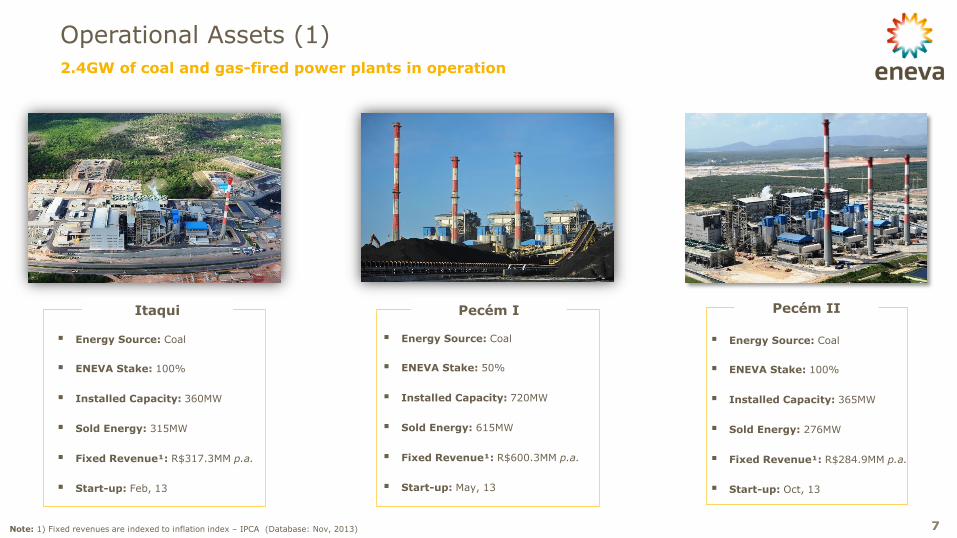

2.4GW of coal and gas-fired power plants in operation

Operational Assets (1)

7

Pecém I

Energy Source: Coal

ENEVA Stake: 50%

Installed Capacity: 720MW

Sold Energy: 615MW

Fixed Revenue¹: R$600.3MM p.a.

Start-up: May, 13

Energy Source: Coal

ENEVA Stake: 100%

Installed Capacity: 360MW

Sold Energy: 315MW

Fixed Revenue¹: R$317.3MM p.a.

Start-up: Feb, 13

Itaqui

Note: 1) Fixed revenues are indexed to inflation index – IPCA (Database: Nov, 2013)

Energy Source: Coal

ENEVA Stake: 100%

Installed Capacity: 365MW

Sold Energy: 276MW

Fixed Revenue¹: R$284.9MM p.a.

Start-up: Oct, 13

Pecém II

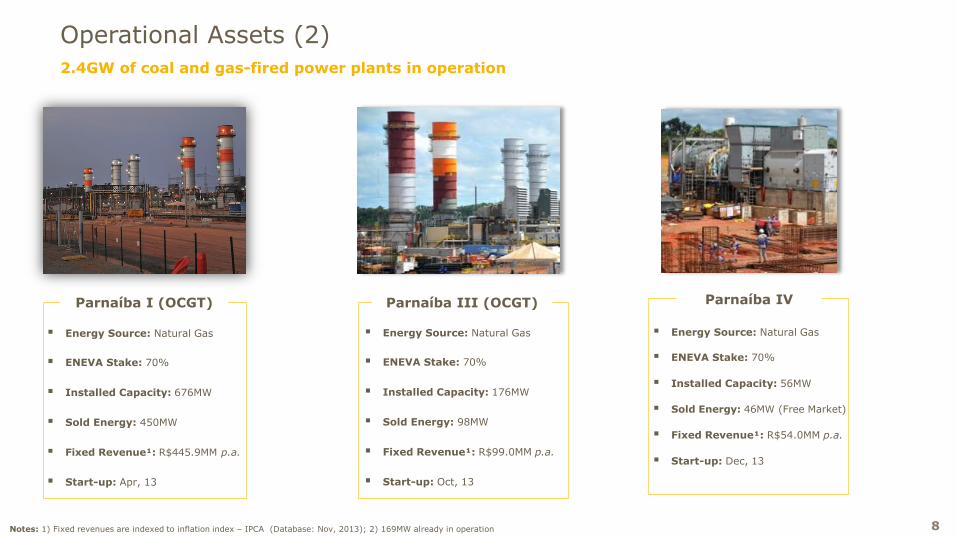

8

Parnaíba I (OCGT)

Energy Source: Natural Gas

ENEVA Stake: 70%

Installed Capacity: 676MW

Sold Energy: 450MW

Fixed Revenue¹: R$445.9MM p.a.

Start-up: Apr, 13

Energy Source: Natural Gas

ENEVA Stake: 70%

Installed Capacity: 176MW

Sold Energy: 98MW

Fixed Revenue¹: R$99.0MM p.a.

Start-up: Oct, 13

Parnaíba III (OCGT)

Energy Source: Natural Gas

ENEVA Stake: 70%

Installed Capacity: 56MW

Sold Energy: 46MW (Free Market)

Fixed Revenue¹: R$54.0MM p.a.

Start-up: Dec, 13

Parnaíba IV

2.4GW of coal and gas-fired power plants in operation

Operational Assets (2)

Notes: 1) Fixed revenues are indexed to inflation index – IPCA (Database: Nov, 2013); 2) 169MW already in operation

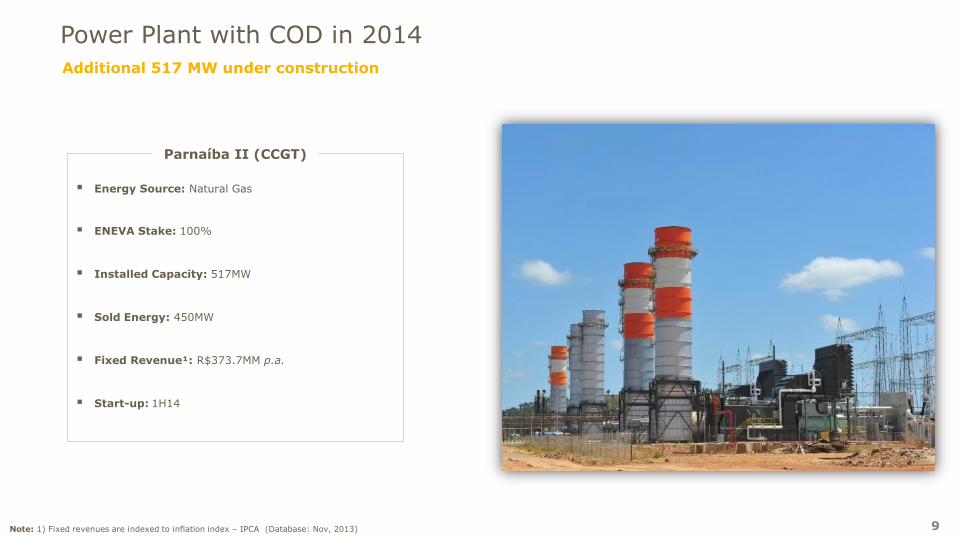

9

Energy Source: Natural Gas

ENEVA Stake: 100%

Installed Capacity: 517MW

Sold Energy: 450MW

Fixed Revenue¹: R$373.7MM p.a.

Start-up: 1H14

Parnaíba II (CCGT)

Note: 1) Fixed revenues are indexed to inflation index – IPCA (Database: Nov, 2013)

Additional 517 MW under construction

Power Plant with COD in 2014

Outstanding management capabilities

Financial strength and discipline

Sector know-how: E.ON E&P looks at a volume delivery of +170k

barrels/day and +60 licenses in GB and Norway

Tried and tested Parnaíba experience, know-how of Parnaíba Complex

rooted within PGN

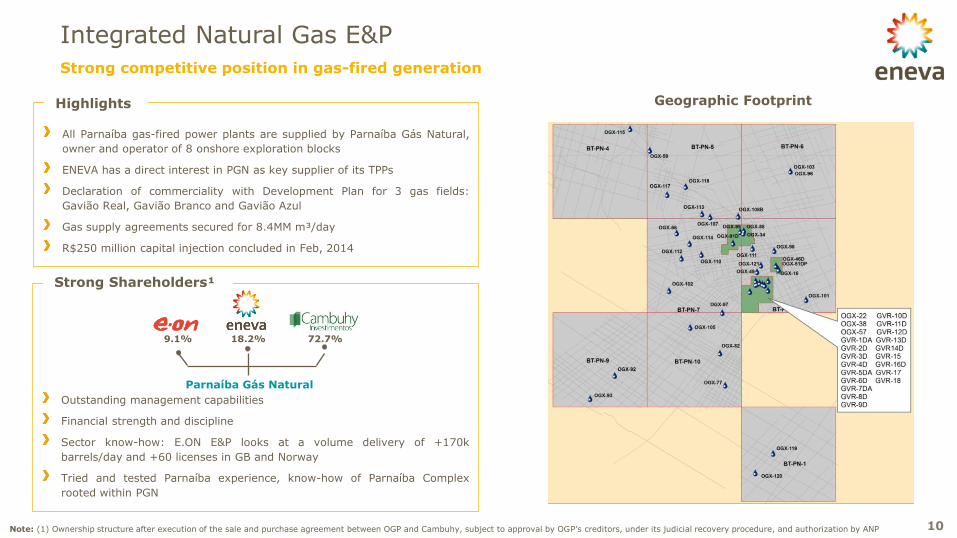

Strong Shareholders¹

All Parnaíba gas-fired power plants are supplied by Parnaíba Gás Natural,

owner and operator of 8 onshore exploration blocks

ENEVA has a direct interest in PGN as key supplier of its TPPs

Declaration of commerciality with Development Plan for 3 gas fields:

Gavião Real, Gavião Branco and Gavião Azul

Gas supply agreements secured for 8.4MM m³/day

R$250 million capital injection concluded in Feb, 2014

Highlights

10

Integrated Natural Gas E&P

Strong competitive position in gas-fired generation

Parnaíba Gás Natural

18.2% 9.1% 72.7%

Geographic Footprint

Note: (1) Ownership structure after execution of the sale and purchase agreement between OGP and Cambuhy, subject to approval by OGP’s creditors, under its judicial recovery procedure, and authorization by ANP

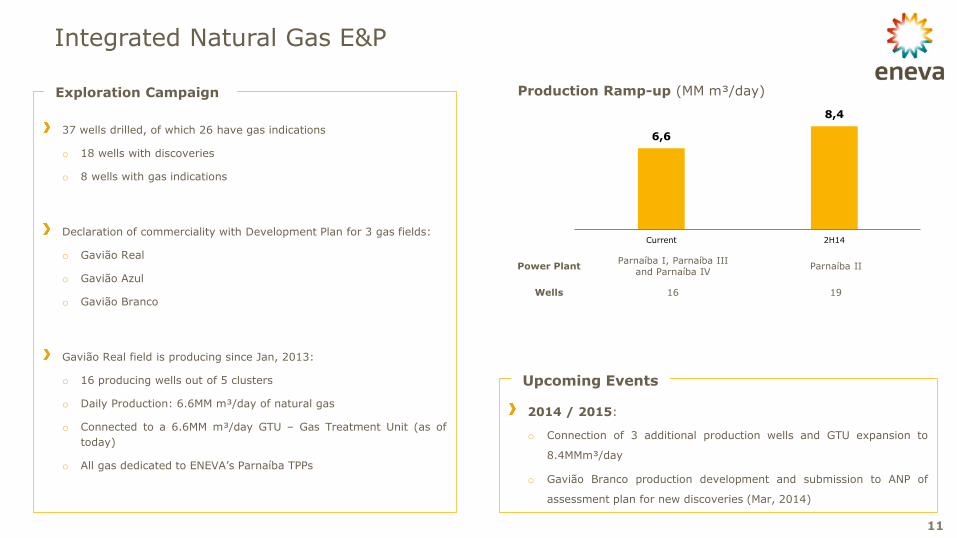

37 wells drilled, of which 26 have gas indications

o 18 wells with discoveries

o 8 wells with gas indications

Declaration of commerciality with Development Plan for 3 gas fields:

o Gavião Real

o Gavião Azul

o Gavião Branco

Gavião Real field is producing since Jan, 2013:

o 16 producing wells out of 5 clusters

o Daily Production: 6.6MM m³/day of natural gas

o Connected to a 6.6MM m³/day GTU – Gas Treatment Unit (as of

today)

o All gas dedicated to ENEVA’s Parnaíba TPPs

Exploration Campaign

11

Integrated Natural Gas E&P

2014 / 2015:

o Connection of 3 additional production wells and GTU expansion to

8.4MMm³/day

o Gavião Branco production development and submission to ANP of

assessment plan for new discoveries (Mar, 2014)

Upcoming Events

Power Plant Parnaíba I, Parnaíba III

and Parnaíba IV Parnaíba II

Wells 16 19

Production Ramp-up (MM m³/day)

6,6

8,4

Current 2H14

Short-Term Value Triggers

3

13

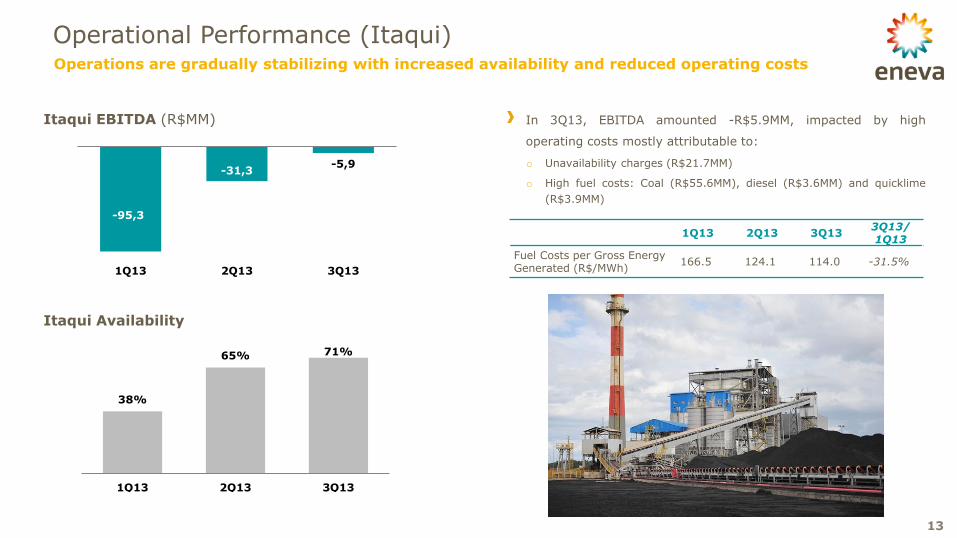

Operational Performance (Itaqui)

-95,3

-31,3 -5,9

1Q13 2Q13 3Q13

Itaqui EBITDA (R$MM)

38%

65% 71%

1Q13 2Q13 3Q13

Itaqui Availability

Operations are gradually stabilizing with increased availability and reduced operating costs

In 3Q13, EBITDA amounted -R$5.9MM, impacted by high

operating costs mostly attributable to:

o Unavailability charges (R$21.7MM)

o High fuel costs: Coal (R$55.6MM), diesel (R$3.6MM) and quicklime

(R$3.9MM)

1Q13 2Q13 3Q13 3Q13/ 1Q13

Fuel Costs per Gross Energy Generated (R$/MWh)

166.5 124.1 114.0 -31.5%

14

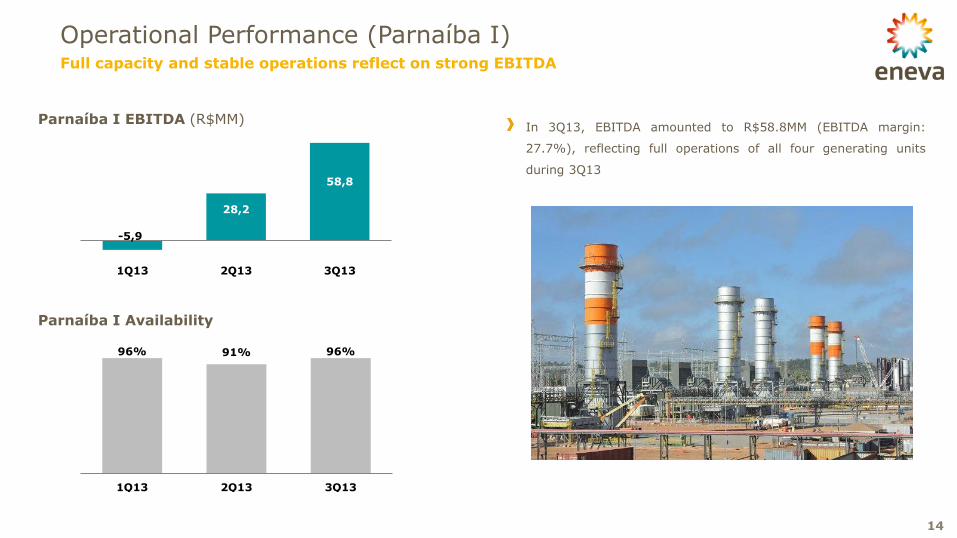

Operational Performance (Parnaíba I)

-5,9

28,2

58,8

1Q13 2Q13 3Q13

Parnaíba I EBITDA (R$MM)

96% 91% 96%

1Q13 2Q13 3Q13

Parnaíba I Availability

Full capacity and stable operations reflect on strong EBITDA

In 3Q13, EBITDA amounted to R$58.8MM (EBITDA margin:

27.7%), reflecting full operations of all four generating units

during 3Q13

15

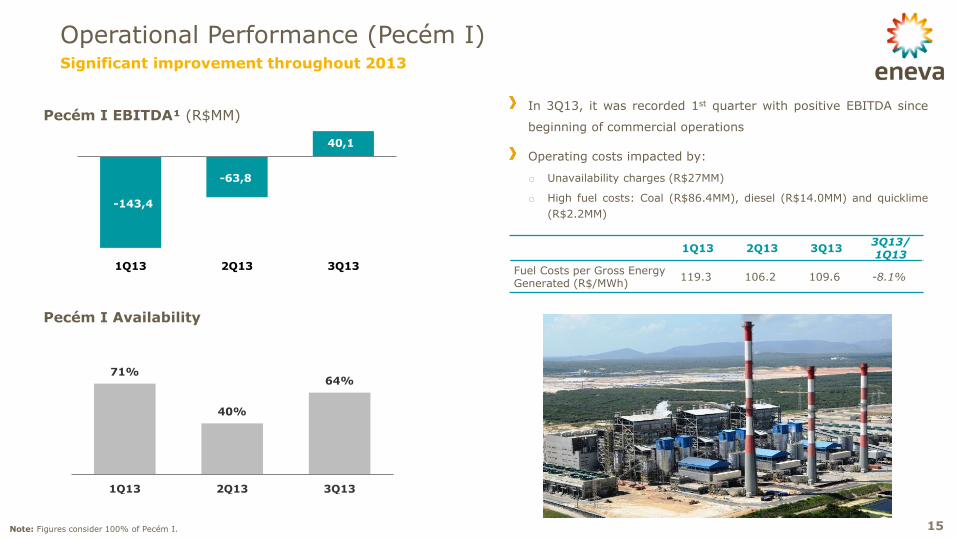

Significant improvement throughout 2013

-143,4

-63,8

40,1

1Q13 2Q13 3Q13

Operational Performance (Pecém I)

Pecém I EBITDA¹ (R$MM)

Pecém I Availability

In 3Q13, it was recorded 1st quarter with positive EBITDA since

beginning of commercial operations

Operating costs impacted by:

o Unavailability charges (R$27MM)

o High fuel costs: Coal (R$86.4MM), diesel (R$14.0MM) and quicklime

(R$2.2MM)

1Q13 2Q13 3Q13 3Q13/ 1Q13

Fuel Costs per Gross Energy Generated (R$/MWh)

119.3 106.2 109.6 -8.1%

71%

40%

64%

1Q13 2Q13 3Q13

Note: Figures consider 100% of Pecém I.

16

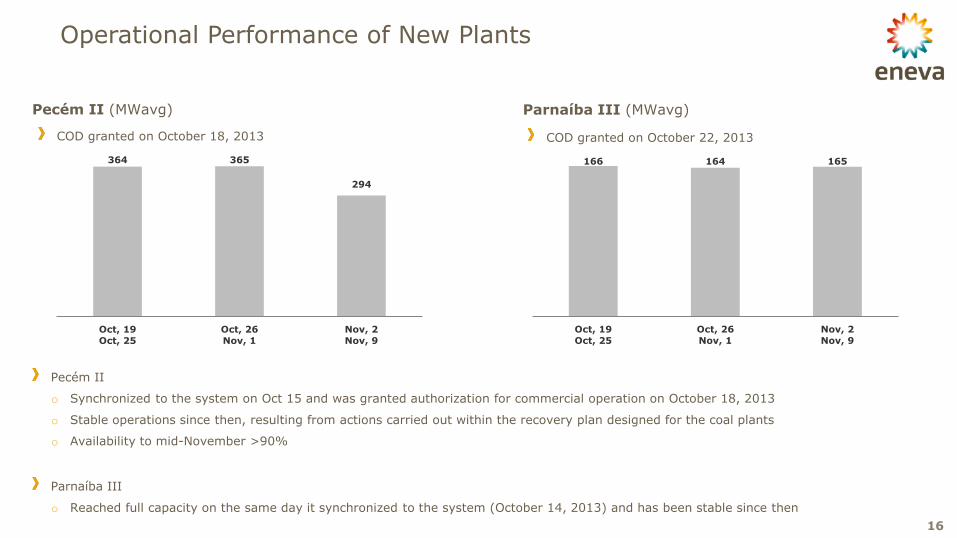

Operational Performance of New Plants

Pecém II (MWavg) Parnaíba III (MWavg)

COD granted on October 22, 2013 COD granted on October 18, 2013

Pecém II

o Synchronized to the system on Oct 15 and was granted authorization for commercial operation on October 18, 2013

o Stable operations since then, resulting from actions carried out within the recovery plan designed for the coal plants

o Availability to mid-November >90%

Parnaíba III

o Reached full capacity on the same day it synchronized to the system (October 14, 2013) and has been stable since then

364 365

294

Oct, 19

Oct, 25

Oct, 26

Nov, 1

Nov, 2

Nov, 9

166 164 165

Oct, 19

Oct, 25

Oct, 26

Nov, 1

Nov, 2

Nov, 9

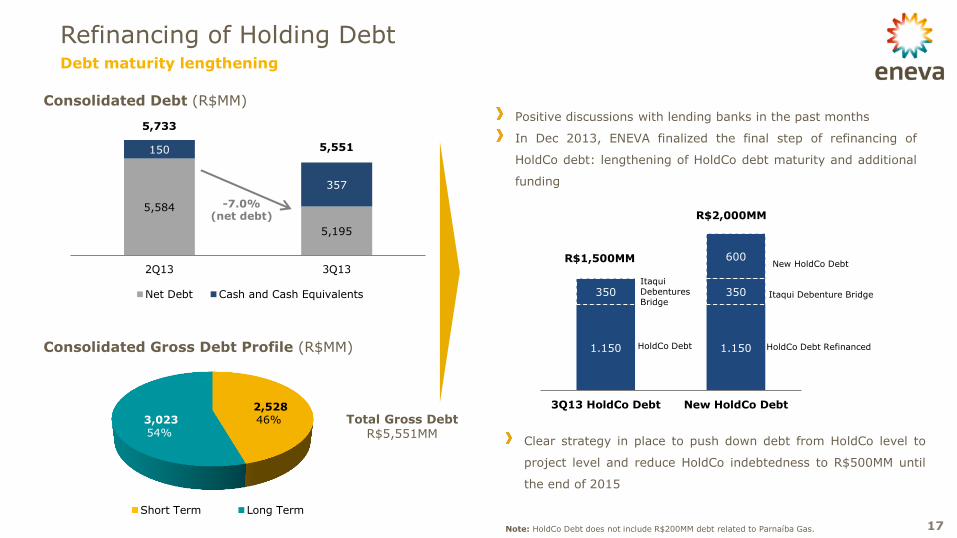

5,584

5,195

150

357

5,733

5,551

2Q13 3Q13

Net Debt Cash and Cash Equivalents

17

Refinancing of Holding Debt Debt maturity lengthening

Consolidated Debt (R$MM)

Total Gross Debt R$5,551MM

Consolidated Gross Debt Profile (R$MM)

Positive discussions with lending banks in the past months

In Dec 2013, ENEVA finalized the final step of refinancing of

HoldCo debt: lengthening of HoldCo debt maturity and additional

funding

2,528 46% 3,023

54%

Short Term Long Term

-7.0% (net debt)

Clear strategy in place to push down debt from HoldCo level to

project level and reduce HoldCo indebtedness to R$500MM until

the end of 2015

1.150 1.150

350 350

600

3Q13 HoldCo Debt New HoldCo Debt

New HoldCo Debt

Itaqui Debenture Bridge

Itaqui Debentures Bridge

HoldCo Debt HoldCo Debt Refinanced

R$1,500MM

R$2,000MM

Note: HoldCo Debt does not include R$200MM debt related to Parnaíba Gas.

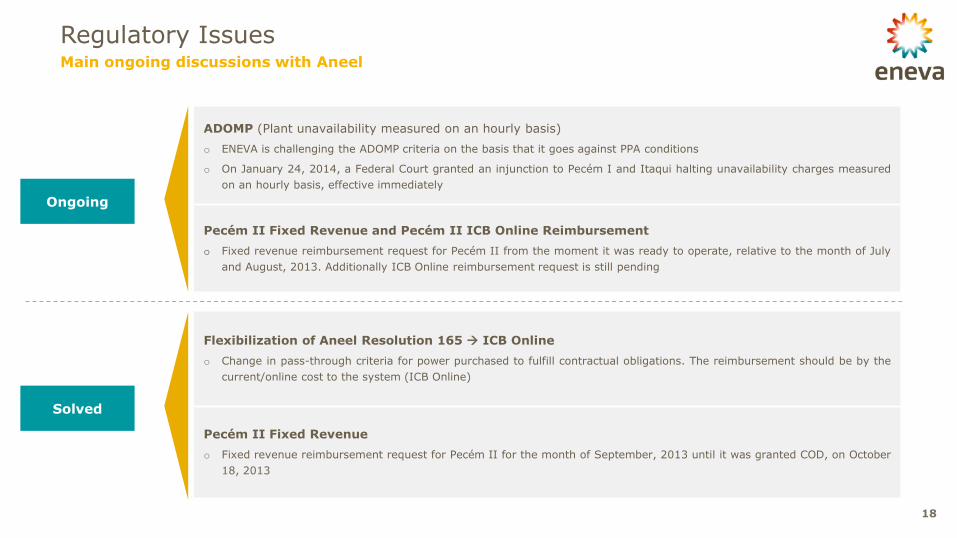

Ongoing

Solved

Flexibilization of Aneel Resolution 165 ICB Online

o Change in pass-through criteria for power purchased to fulfill contractual obligations. The reimbursement should be by the

current/online cost to the system (ICB Online)

Pecém II Fixed Revenue

o Fixed revenue reimbursement request for Pecém II for the month of September, 2013 until it was granted COD, on October

18, 2013

ADOMP (Plant unavailability measured on an hourly basis)

o ENEVA is challenging the ADOMP criteria on the basis that it goes against PPA conditions

o On January 24, 2014, a Federal Court granted an injunction to Pecém I and Itaqui halting unavailability charges measured

on an hourly basis, effective immediately

Pecém II Fixed Revenue and Pecém II ICB Online Reimbursement

o Fixed revenue reimbursement request for Pecém II from the moment it was ready to operate, relative to the month of July

and August, 2013. Additionally ICB Online reimbursement request is still pending

18

Regulatory Issues Main ongoing discussions with Aneel

19

Cost Reduction Program

ENEVA developed a Medium Term Plan 2014-2016 aimed at achieving significant cost reduction at

holding and project level through:

Leaner organizational structure

Headcount reduction

Decrease in third-party services

Reduction of fixed costs at project level

Brazilian Power Market and Greenfield Portfolio

4

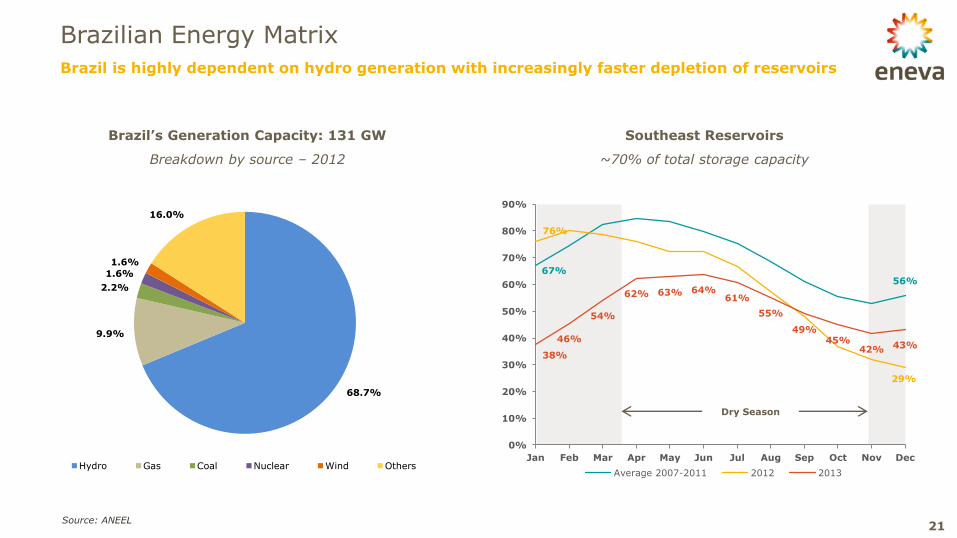

Southeast Reservoirs

~70% of total storage capacity

Source: ANEEL

Brazil’s Generation Capacity: 131 GW

Breakdown by source – 2012

68.7%

9.9%

2.2%

1.6%

1.6%

16.0%

Hydro Gas Coal Nuclear Wind Others

Brazil is highly dependent on hydro generation with increasingly faster depletion of reservoirs

Brazilian Energy Matrix

21

Dry Season

67% 56%

76%

29%

38%

46%

54%

62% 63% 64% 61%

55%

49% 45%

42% 43%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Average 2007-2011 2012 2013

Source: ONS

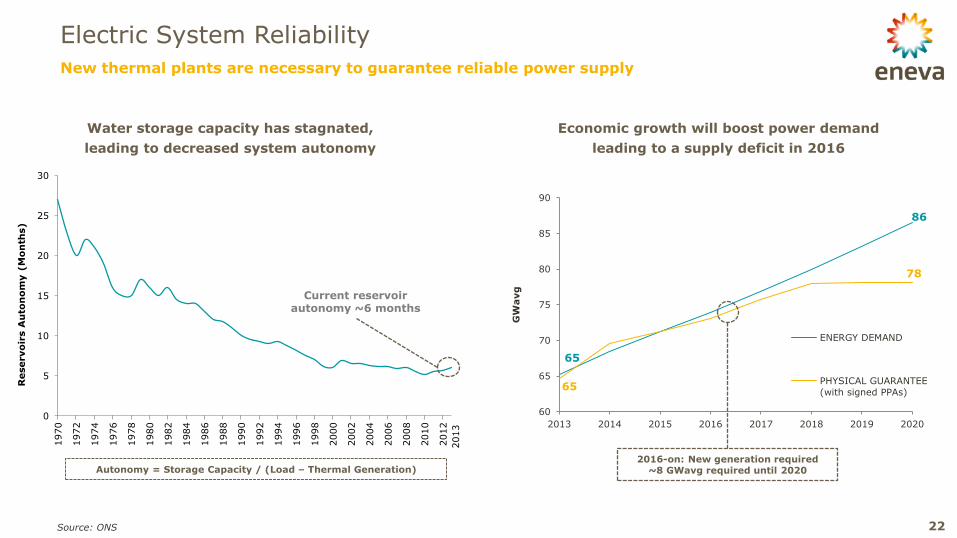

Autonomy = Storage Capacity / (Load – Thermal Generation)

Economic growth will boost power demand

leading to a supply deficit in 2016

Water storage capacity has stagnated,

leading to decreased system autonomy

65

86

65

78

60

65

70

75

80

85

90

2013 2014 2015 2016 2017 2018 2019 2020

GW

avg

ENERGY DEMAND

PHYSICAL GUARANTEE

(with signed PPAs)

2016-on: New generation required ~8 GWavg required until 2020

22

Electric System Reliability

New thermal plants are necessary to guarantee reliable power supply

0

5

10

15

20

25

30

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Reservo

irs A

uto

no

my (

Mo

nth

s)

2013

Current reservoir autonomy ~6 months

Parnaíba Complex

Integrated to natural gas resources

Located in a tax-advantaged region

Ventos Wind Complex

Located in one Brazil’s best wind resource areas

Attractive load factor

Just 30km from grid connection

Land ownership assured

Açu (Coal + Gas)

Located at a port with a regasification terminal build license

150km from Campos Basin natural gas accumulations

Environmental licensed to both coal and gas operations

Sul & Seival Integrated to the Seival Mine (proven reserves: 152 M ton)

Low operation costs

Power

supply-demand

unbalanced

Hydropower

concentrated

matrix

Spot prices at

historical highs

Demand for base-

load generation

Opportunities

for ENEVA’s

growth 2 3 4 5 1

Sul 727 MW

Parnaíba Complex 2,166 MW

Seival 600 MW

Açu 2,100 MW – Coal 3,300 MW – Natural Gas

Solar Tauá 1 MW

Ventos Wind Complex 600 MW

Seival Mine License granted 152 M ton in proven reserves

ENEVA’s Greenfield Portfolio

23

Attractive licensed greenfield projects in various development stages

Appendix | Images

5

Pecém I & II

25

Itaqui

26

Parnaíba Complex

27

Natural Gas: Parnaíba E&P

28

Disclaimer

The material that follows is a presentation of general background information about ENEVA S.A. and its subsidiaries (collectively, “ENEVA” or the “Company”) as of

the date of the presentation. It is information in summary form and does not purport to be complete. No representation or warranty, express or implied, is made

concerning, and no reliance should be placed on, the accuracy, fairness, or completeness of this information.

This presentation may contain certain forward-looking statements and information relating to ENEVA that reflect the current views and/or expectations of the

Company and its management with respect to its performance, business and future events. Forward looking statements include, without limitation, any statement

that may predict, forecast, indicate or imply future results, performance or achievements, and may contain words like “may”, “plan”, “believe”, “anticipate”,

“expect”, “envisages”, “will likely result”, or any other words or phrases of similar meaning. Such statements are subject to a number of risks, uncertainties and

assumptions. We caution you that a number of important factors could cause actual results to differ materially from the plans, objectives, expectations, estimates

and intentions expressed in this presentation. In no event, neither the Company, any of its affiliates, directors, officers, agents or employees nor any of the

placement agents shall be liable before any third party (including investors) for any investment or business decision made or action taken in reliance on the

information and statements contained in this presentation or for any consequential, special or similar damages.

This presentation does not constitute an offer, or invitation, or solicitation of an offer, to subscribe for or purchase any securities.

Neither this presentation nor anything contained herein shall form the basis of any contract or commitment whatsoever.

Recipients of this presentation are not to construe the contents of this summary as legal, tax or investment advice and recipients should consult their own advisors

in this regard.

The market and competitive position data, including market forecasts, used throughout this presentation were obtained from internal surveys, market research,

publicly available information and industry publications. Although we have no reason to believe that any of this information or these reports are inaccurate in any

material respect, we have not independently verified the competitive position, market share, market size, market growth or other data provided by third parties or

by industry or other publications. ENEVA, the placement agents and the underwriters do not make any representation as to the accuracy of such information.

This presentation and its contents are proprietary information and may not be reproduced or otherwise disseminated in whole or in part without ENEVA’s prior

written consent.

Thank you. www.eneva.com.br