Embed Size (px)

Citation preview

Engineering Economics in Canada

Chapter 8 Taxes

(Important Chapter)

Copyright © 2006 Pearson Education Canada Inc. 8-2

Introduction

• In Canada, the federal and provincial governments levy taxes on both individuals and corporations.

• Taxes can have a significant impact on the economic viability of a project

• This chapter provides an introduction to the tax environment in Canada and shows how it can affect engineering decisions.

Copyright © 2006 Pearson Education Canada Inc. 8-3

8.1 Introduction…

• The most significant kind of tax for economic comparisons is income tax.

• Income taxes provide governments a portion of net income received by an individual or corporation.

• Income taxes are the main source of revenue for federal and provincial governments and pay for social services, health services, infrastructure such as highways and dams, the military and other government services.

Copyright © 2006 Pearson Education Canada Inc. 8-4

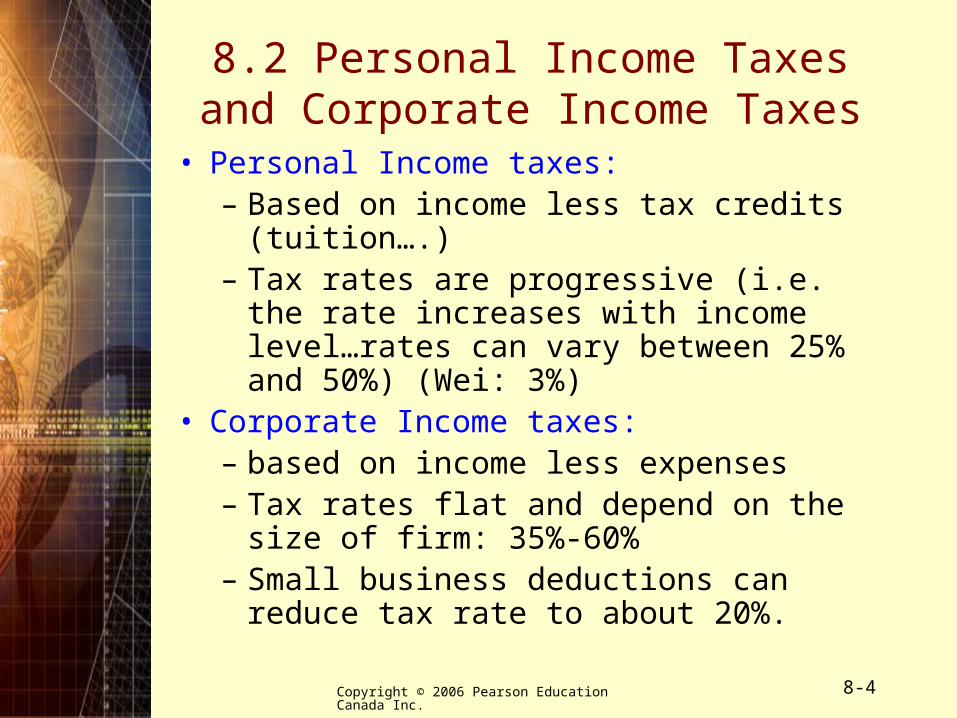

8.2 Personal Income Taxes and Corporate Income Taxes

• Personal Income taxes:– Based on income less tax credits

(tuition….)– Tax rates are progressive (i.e. the rate

increases with income level…rates can vary between 25% and 50%) (Wei: 3%)

• Corporate Income taxes:– based on income less expenses– Tax rates flat and depend on the size of

firm: 35%-60%– Small business deductions can reduce

tax rate to about 20%.

Copyright © 2006 Pearson Education Canada Inc. 8-5

8.3 Corporate Tax Rates

• Corporate taxes have provincial and federal components.

• Rates can depend on factors such as what the corporation does, where it is located, and how large it is.

• Tax rates generally range from 17% to 52%• Small Business Deductions apply to small

companies and give tax credits to provide higher after tax income for reinvestment and expansion.

• Tax rules change periodically

Copyright © 2006 Pearson Education Canada Inc. 8-6

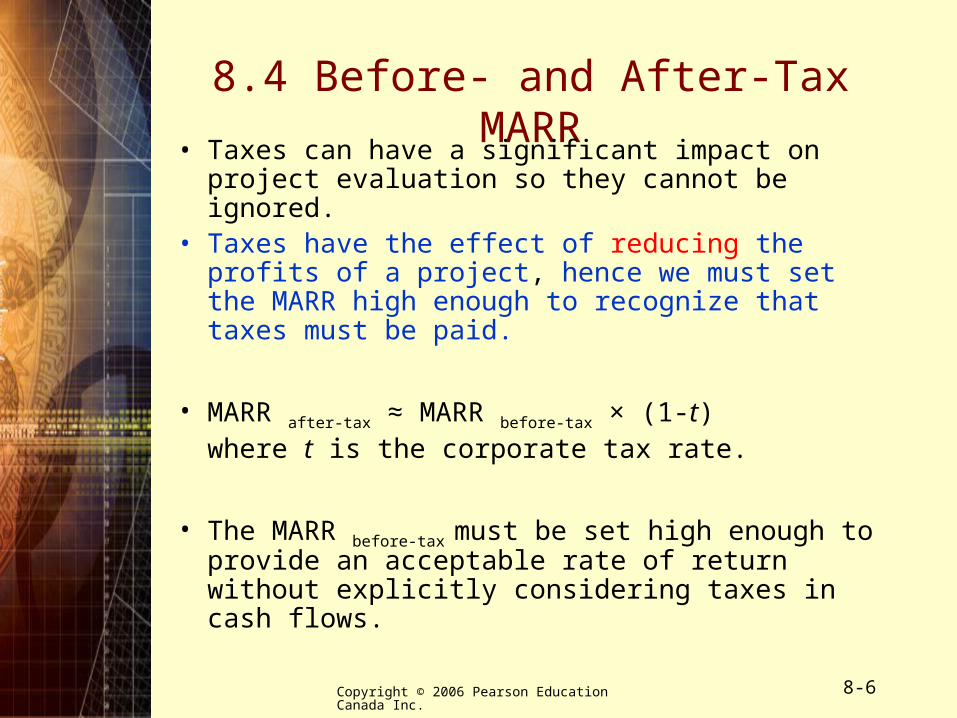

8.4 Before- and After-Tax MARR• Taxes can have a significant impact on project

evaluation so they cannot be ignored.• Taxes have the effect of reducing the profits of

a project, hence we must set the MARR high enough to recognize that taxes must be paid.

• MARR after-tax ≈ MARR before-tax × (1-t) where t is the corporate tax rate.

• The MARR before-tax must be set high enough to provide an acceptable rate of return without explicitly considering taxes in cash flows.

Copyright © 2006 Pearson Education Canada Inc. 8-7

Before- and After-Tax MARR (con’t)

• It appears that we have ignored the impact of taxes so far – no specific tax calculations have been done.

• In fact, taxes have been incorporated into the computations – we have been using a before- tax MARR.

Copyright © 2006 Pearson Education Canada Inc. 8-8

• A capital expense occurs when a firm acquires a depreciable asset.

• Over time, the asset depreciates:– The depreciation is recognized by reducing the

book value of the asset on the firms balance sheet.

– depreciation is also recorded as an expense on the income statement, reducing net income.

• Depreciation reduces net income and thus taxes but it is not an out-of-pocket expense.

• This leads firms to want to depreciate assets as quickly as possible.

8.5 The Capital Cost Allowance (CCA) System

Copyright © 2006 Pearson Education Canada Inc. 8-9

• To control the rate at which firm’s depreciate assets, the Canadian Government has set up rules which limit the amount of depreciation a firm can claim in any one year.

• The maximum level of capital expenses (i.e. depreciation) a firm can claim is called its capital cost allowance (CCA).

• The system established to allow firms to compute their CCA is called the capital cost allowance (CCA) system.

The CCA System (con’t)

Copyright © 2006 Pearson Education Canada Inc. 8-10

• The CCA System requires that the declining-balance method of depreciation be used to claim capital costs

• The CCA System also specifies the maximum depreciation rate that can be used. This is called the CCA rate.

• To implement the CCA system, assets are grouped into CCA asset classes

• Each CCA asset class has a designated CCA Rate assigned

The CCA System (con’t)

Copyright © 2006 Pearson Education Canada Inc. 8-11

CCA CCAClass Rate Description1,3,6 4 – 10 % Buildings and additions8 20% Office furniture and

equipment9 25% Aircraft, aircraft furniture10 30% Passenger vehicles, vans16 40% Taxis, rental cars17 100% Dies, tools, Computer software

Sample CCA Classes and Rates

Copyright © 2006 Pearson Education Canada Inc. 8-12

• The basis for calculating the CCA for assets in a particular class is the total undepreciated capital cost (UCC) for the assets in that class.

• As an asset is used, the undepreciated portion of the original capital cost is tracked through this UCC account.

• Assets belonging to a particular class are pooled and kept track of as a group, not individually.

8.6 Undepreciated Capital Cost (UCC)

Copyright © 2006 Pearson Education Canada Inc. 8-13

• The UCC does not represent market value; but the remaining value for the purposes of computing capital cost allowances.

• The general approach for computing UCC balances each period (usually a year) is as follows:

UCCending = UCCopening + additions – disposals – CCA

Undepreciated Capital Cost (UCC)

Copyright © 2006 Pearson Education Canada Inc. 8-14

• “Fly-by-Night” charter service purchased two airplanes at $25,000 each. The CCA rate for airplanes is 25%. What will be the UCC balance for each of the next four years, assuming it was zero before the planes were bought?

Example 8-1

Copyright © 2006 Pearson Education Canada Inc. 8-15

Year Adj. to UCC from UCC used for Capital Cost Remaining UCC

purch. and dispos. Cap. Cost Allow. Allowance

1 $50,000.00 $50,000.00 $12,500.00 $37,500.00

2 $0.00 $37,500.00 $12,500.00 $25,000.00

3 $0.00 $25,000.00 $12,500.00 $12,500.00

4 $0.00 $12,500.00 $12,500.00 $0.00

Example 8-1: aNSWER

Copyright © 2006 Pearson Education Canada Inc. 8-16

Year Adj. to UCC from UCC used for Capital Cost Remaining UCC

purch. and dispos. Cap. Cost Allow. Allowance

1 $50,000.00 $50,000.00 $12,500.00 $37,500.00

2 $0.00 $37,500.00 $9,375.00 $28,125.00

3 $0.00 $28,125.00 $7,031.25 $21,093.75

4 $0.00 $21,093.75 $5,273.44 $15,820.31

Example 8-1: Real Answer

Copyright © 2006 Pearson Education Canada Inc. 8-17

• There is a complication in UCC calculation due to the half year rule.

• Assets purchased after November 1981 are subject to this rule.

• Half year rule: only half of the capital cost of acquiring an asset can be claimed in the UCC for the first year. The remaining half is claimed the following year. (%, not value, see example 8-2)

• This rule was created because many businesses would purchase assets at the end of a year and only own them a short time but get to claim a full year’s CCA.

The Half-Year Rule

Copyright © 2006 Pearson Education Canada Inc. 8-18

• “Fly-by-Night” charter service purchased two airplanes at $25,000 each in 1996. The CCA rate for airplanes is 25%. Assuming the equipment was kept for more than 4 years, what will be the UCC balances at year-end for 1996 – 1999?

• The Half-Year Rule means 12.5% first year, then 25%

Example 8-2 (Very important)

Copyright © 2006 Pearson Education Canada Inc. 8-19

Year Adj. to UCC from UCC used for Capital Cost Remaining UCC

purch. and dispos. Cap. Cost Allow. Allowance

1996 50000 25 000.0 6 250.0 43 750.0

1997 0 43 750.0 10 937.5 32 812.5

1998 0 32 812.5 8 203.1 24 609.4

1999 0 24 609.4 6 152.3 18 457.0

Example 8-2: Answer

Copyright © 2006 Pearson Education Canada Inc. 8-20

• The CCA creates tax savings by reducing taxable income over a number of years.

• This reduction of income causes a savings in the amount of tax payable in the future.

• Consider the tax savings if “Fly-by-night” from Example 8-1 purchased two $25,000 airplanes in 1976 (CCA = 25%):Year Adj. to UCC from UCC used for Capital Cost Remaining UCC

purch. and dispos. Cap. Cost Allow. Allowance

1976 50000 50 000.0 12 500.0 37 500.0

1977 0 37 500.0 9 375.0 28 125.0

1978 0 28 125.0 7 031.3 21 093.8

1978 0 21 093.8 5 273.4 15 820.3

8.7 The Capital Cost Tax Factor (very important)

Copyright © 2006 Pearson Education Canada Inc. 8-21

• If ‘Fly-by-night’ has a corporate tax rate of t = 40%, and an after-tax MARR of i, then:

PW(tax savings) = (0.40)(12 500)(P/F, i, 1)

+ (0.40)(9375)(P/F, i, 2)

+ (0.40)(7031.3)(P/F, i, 3) +

• Or, more generally (with d = CCA rate):

d)(itPd

...+i)(

dd)tP(

+i)(

d)dtP(+i)(

tPd =

3

2

2 1

1

1

11

savings)PW(tax

The Old Capital Cost Tax Factor

Copyright © 2006 Pearson Education Canada Inc. 8-22

The Old Capital Cost Tax Factor

oldCCTFP

(i+d)td

P (i+d)Pdt

P

P

1

savings)PW(tax cost) PW(first

(i+d)td1 CCTFold

• Then the after-tax present worth of the first cost becomes:

• Where we have defined:

Copyright © 2006 Pearson Education Canada Inc. 8-23

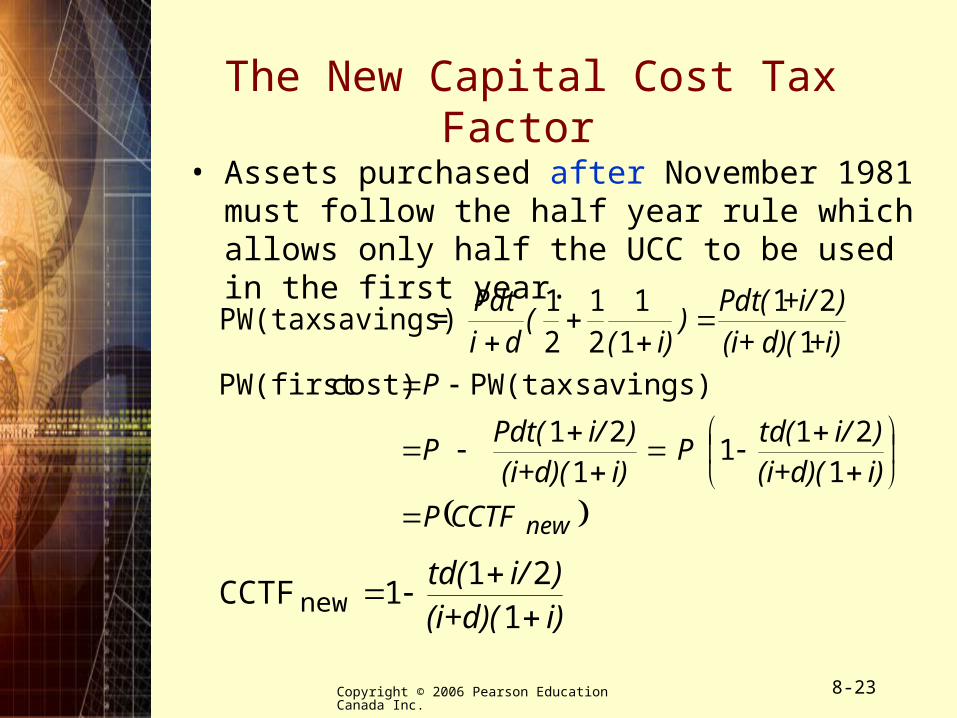

• Assets purchased after November 1981 must follow the half year rule which allows only half the UCC to be used in the first year.

+i)(i+ d)()+i/Pdt(

)i)(

(di

Pdt

121

11

21

21

= savings)PW(tax

newCCTFP

i)(i+d)()i/td(

P i)(i+d)()i/Pdt(

P

P

121

11

21

savings)PW(tax cost) PW(first

The New Capital Cost Tax Factor

i)(i+d)()i/td(

1

211 CCTFnew

Copyright © 2006 Pearson Education Canada Inc. 8-24

• The following summarizes how to treat various cost components in a full after-tax evaluation of a project:

Component Treatment

First cost Multiply by CCTFnew

Revenues, Savings Multiply by (1-t)

or costs

Salvage value Multiply by CCTFold

8.8 Components of a Complete Tax Calculation

Copyright © 2006 Pearson Education Canada Inc. 8-25

• An electric pallet truck costs $12 000. It saves $4000 per year over its 5 year life and is expected to have a $2000 salvage value.

• The after-tax MARR is 8%, taxes are at 50% and the CCA rate for this type of equipment is 20%.

• Is the investment in pallet truck justified?

Example 8-3 (very important)

Copyright © 2006 Pearson Education Canada Inc. 8-26

1) Purchasing the asset starts a stream of tax savings: multiply the first cost by the CCTFNEW:

PW(first cost) = –12 000(0.6561)

= –7873

2) Savings are taxed at 50%:

PW(savings) = PW(savings before taxes) (1 – t)

= 4000(P/A, 8%, 5)(1 – t)

= 7985

Example 8-3: Answer

Copyright © 2006 Pearson Education Canada Inc. 8-27

3) Salvaging the pallet truck terminates the stream of tax savings at the end of 5 years.

CCTFOLD = 1 – (td)/(i+d)

= 1 – (0.5)(0.2)/(0.08 + 0.20) = 0.6429

PW(salvage) = 2000(P/F, 8%, 5)CCTFOLD

= 2000(0.68058)(0.6429) = 875

The after-tax present worth is:

PW(total) = PW(first cost) + PW(savings)

+ PW(salvage)

= –7873 + 7985 + 875

= $987

Example 8-3: Answer

Copyright © 2006 Pearson Education Canada Inc. 8-28

Summary

• Income taxes – personal and corporate• CCA system

– UCC accounts– CCA rates, asset classes– CCTF’s

• Full tax calculations for PW, AW, IRR comparisons