Embed Size (px)

Citation preview

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 1/43

THE COMPLETE BOOK OF EQUITIESTrading, Investing, Analysis and Arbitrage

© 2012 by Steven I. Dym

My motivation for writing this book is simple. I’ve taught thousans of market pra!titioners " from investors an traes to !omplian!e offi!ers an !omputer professionals " over the past e!aes# an I know what they nee to know. $o myknowlege# most books on the sto!k market spen most of their time on what market pra!titioners o %&$ nee to know# an pre!ious little on what they must know in orerto get their 'ob one (an oes it well). $herefore# I e!ie to write this book.

*ra!titioners nee to know what sto!ks are an how they relate to the !ompany whosename is on the !ertifi!ate. $hey have to unerstan investment management styles ante!hni+ues. $hey must be!ome familiar with the ynami!s of long an short positions#in!luing finan!ing an !ollateral. $hey’ve got to be!ome knowlegeable of the

prin!ipal e+uity erivatives an# !ru!ially# how they are employe. $hey nee to learnthe reasons an the me!hani!s of relative value traing# with an without erivatives.$hey nee to be e,pose to what is known toay as e+uity alternatives. -inally# theyhave to gain a working knowlege of how the ma!roe!onomy influen!es an intera!tswith the sto!k market. $hey o %&$ nee to know e,a!tly how to !al!ulate the /valueof a sto!k or a !ompany. $hey o %&$ nee to be taught formulas for pri!ingerivatives. n they o %&$ nee to learn any proofs of a !apital asset pri!ing orrelate moel.

Similar to my first book# this volume is a !ross between a te,tbook an a book on market pra!ti!e. $hat is# it goes !arefully through funamental prin!iples an is full of real

market appli!ations. It is written intuitively without sa!rifi!ing rigor. hat oes it offerthat others on’t3 ell# besies the previous two senten!es# no other book# to myknowlege# begins at the true /beginning. It’s truly /soup to nuts. *art &ne proviesthe ne!essary a!!ounting basi!s without taking an a!!ounting !ourse4 n the book buils logi!ally from there. $here’s a self!ontaine !hapter on unerstaning thee!onomy (any e!onomy " not 'ust the 5S)# whi!h then is employe in making investinge!isions. 6an you fin this anypla!e else3 $opi!s that are treate (!orre!tly) no pla!eelse are foun here# for e,ample# how to short sto!ks# margin !alls# e+uitylinke notes#effe!t of the e!onomy on sto!ks pri!es. n !ertainly not in one pla!e4 So many termsan market 'argon are e,plaine " it’s almost an en!y!lopeia# but written in an easygoing language. $here’s even a !hapter on mergers 7 a!+uisitions " without having to

buy a separate book4 I think there’s a gaping hole on bookshelves toay# whi!h !alls for a book of this sort. I myself sear!he for su!h a book when tea!hing at business s!hoolsan when giving seminars to market parti!ipants# with no su!!ess.

%ote8 $his book may be tilte a bit more towar a te,tbook than my first one. Inee#sin!e I am 'ust beginning the writing# I !an tilt in the ire!tion an to the egreere!ommene by the publisher’s marketing e,perts. $o this en# I !an appen review+uestions at the en of ea!h !hapter to make it more te,tbooklike an stuentfrienly.

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 2/43

9ou’ll noti!e below I haven’t flushe out many of the !hapters. n some of the /*artsmay be!ome !hapters# an some !hapters may be !ombine. $he part on Derivativesmay be ivie into two. n the orering may well !hange. It’s all flui.

*:$ &%;

5%D;:S$%DI%< 6&M*%98 66&5%$I%< %D -I%%6I= S$$;M;%$%=9SIS I% &%; SI$$I%<

0 >asi!s8 Sto!ks an Shareholers

6ommon sto!k? resiuals? !ash flow /waterfall? preferre shares? leners another outsiers? role of government

I In!ome Statements# >alan!e Sheets an -inan!ial :atios

:evenue an !osts? profit? ta,es? iviens an retaine earnings? ;>I$ 7;>I$D? losses? inventory? :&;? Dupont analysis

II van!e8 Mergers# >uyouts# Spinoffs an 6arveouts

!+uirer 7 target? hege fun marktomarket? goowill? share buyba!ks?leverage buyouts

*:$ $&

S$&6@ *:I6;S %D A=5;S

III >ook Aalue vs. Market Aalue

III’ Divien Dis!ount Moels? <rowth 7 :&68 ;nterprise Aalue

IA ;+uity *ri!e Multiples an *ri!e Dynami!s

A />eta an Measures of :isk

AI Sto!k Ini!es

*:$ $B:;;

I%A;S$M;%$ M%<;M;%$

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 3/43

AII *ortfolio Management Styles

<rowth vs. value? momentum? small# mi 7 large !apitaliCation# +uantitiesstrategies

AIII *erforman!e Measurement

I *assive Management 7 Ine,ing

*:$ -&5:

B& $B; ;6&%&M9 --;6$S S$&6@ *:I6;S

Bow the ;!onomy orks in &ne 6hapter

>usiness !y!les an the sto!k market? the -eeral :eserve an finan!ial markets?effe!ts of inflation

I Bow the Sto!k Market :ea!ts to the ;!onomy’s Dynami!s

*:$ -IA;

$:DI%< D9%MI6S

II :ate of :eturn 6al!ulations? =everage an -inan!ing

IIII Margin an Margin 6alls

IA Shorting Sto!ks? Se!urities =ening by Investors

*:$ SI

;E5I$9 D;:IA$IA;S

A Sto!k Ine, -utures

Intro to forwars an futures !ontra!ts? ine, futures? heging# spe!ulating 7leverage? a'usting beta? /slippage

AI $otal :eturn Swaps

;+uity swaps8 single name# basket an ine,linke? enhan!e passive investing?/portable alpha

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 4/43

AII Ine,linke %otes

*lain an funky alternatives

AIII ;,!hange $rae -uns

Stru!ture an ynami!s of ;$-s? leverage an inverse ;$-s

I &ptions

&ption !ontra!t? plain vanilla puts 7 !alls? payoffs an !ombos? optionsemploye to synthesiCe# to hege# to !reate in!ome? all the /<reeks

;,oti! &ptions an Stru!ture *rou!ts

>inary an barrier options? managing e+uity portfolios with options? ne,tgeneration options? yiel enhan!ement an prin!ipal prote!te notes

I 6onvertible >ons

Stru!ture an attra!tion of !onvertibles? unerstaning the options? reverse!onvertibles

*:$ S;A;%

B;D<; -5%DS %D :;=$IA; A=5; $:DI%<

II Bege -un Stru!ture an &perations

III rbitrage an :elative Aalue $raes

*air traes? ine, traes? statisti!al arbitrage? event riven traing? !ashfutures basis? strippe !onvertibles

*:$ ;I<B$

I%$;:%$I&%= I%A;S$I%<

IA -oreign ;,!hange an ;,!hange rates

hat etermines e,!hange rates? ;ffe!ts of !urren!y movements on sto!k portfolios? emerging markets

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 5/43

A Multinational ;nterprises

*:$ %I%;

M;:<;:S 7 6E5ISI$I&%S

AI hat M7 is ll bout

Motivation for mergers? types of mergers? !ontrol premium? finan!ing

AII Impli!ations for Investors

*:$ $;%

;E5I$9 =$;:%$IA;S

AIII *rivate ;+uity

$ypes of *; investments? venture !apital? e,it strategies? !apital !alls an/F !urve

I =everage >uyouts

Motivation? importan!e of finan!ing? !lawba!k arrangements

:eal ;state Investment $rusts

%ature of :;I$s? favorable ta, treatment? attra!tion to investors

5%I$ &%;

5%D;:S$%DI%< 6&M*%9866&5%$I%< %D -I%%6I= S$$;M;%$ %=9SIS I% &%; SI$$I%<

$his unit provies the basi!s for you to get starte in unerstaning what e+uities ane+uity investing are all about. $he first !hapter provies you with efinitions. >ut that’snot all. It gives you the proper intuition for the e+uity holer’s share in a !ompany’s !ashflow.

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 6/43

$he se!on !hapter !ontains a terse introu!tion to all the a!!ounting !on!epts you’llnee to unerstan an invest in sto!ks. It is brief# to the point an absolutely !ru!ial. Ifyou have an a!!ounting ba!kgroun# you !an skip the basi!s# but make sure youunerstan all the ratios is!usse. nyway# you might want to rea the !hapter +ui!klyin orer to appre!iate the perspe!tive of an investor !ompare to that of an a!!ountant.

hile not funamental to unerstaning the basi!s of e+uities# the final !hapter of thisgroup belongs here be!ause it applies the basi! balan!e sheet ieas to situations that arenot /plain vanilla. Mergers# buyouts# et!. are interesting appli!ations an e,tensions ofwhat you’ll learn in the se!on !hapter# they are important in their own right# an you’ll probably nee to return to this !hapter when these situations are introu!e later on in the book. $he !hapter also is!usses the !ru!ial iea of /markingtomarket in the !onte,tof a hege fun pur!hasing sto!k.

6B*$;: &%;

>SI6S8 S$&6@S %D SB:;B&=D;:S

>uying a share of sto!k makes you an owner of the !ompany whose name is on the sto!k!ertifi!ate. s an owner# you’re entitle to your share of the profits. 9ou’re alsotypi!ally entitle to vote at shareholers’ meetings# !hoose who will manage the !ompanyan have a say in other /!orporate matters. >ut our !on!ern here is with the money# or/!ash flow aspe!ts of being a shareholer. So# what are /profits3

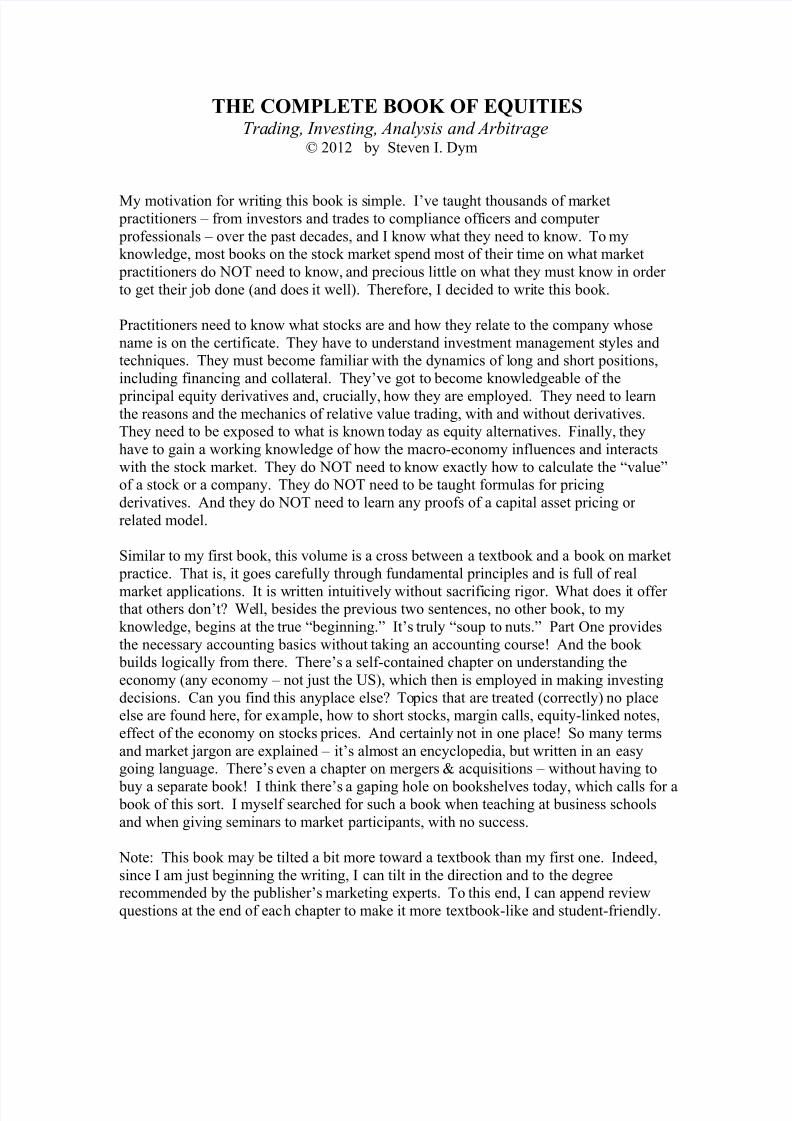

*rofits# :evenue an 6osts

*rofits are what’s /left over from selling the items prou!e (or servi!es provie) aftereveryone else involve in the item’s prou!tion has been pai. -igure &1 sket!hes a!ompany’s !ash flow. lthough a very simplifie pi!ture of a !ompany’s moneyynami!s# the figure is +uite enlightening. It is not an e,haustive listing of the elementsinvolve# but is enough to illustrate the prin!iple !on!epts. =et’s take it stepbystep.

-I<5:; &1

:evenue8 pri!e per unit , units sol

=ess !osts8

Aariable -i,e

labor rentmaterials aministrativeenergy e+uipment epre!iation

ebt servi!e

;+uals profits

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 7/43

=ess ta,es GGGGGGGGGGGGGGGGGGGGGGGGGGGGGGGGGGGG

;+uals %;$ *:&-I$S

!ompany’s revenue e+uals the prou!t of the pri!e it re!eives for ea!h item it sells# anthe number of units sol. e use the wor /units as oppose to /+uantity so that it !anapply to a !ompany proviing servi!es as well as to one prou!ing or selling goos.<oos by nature !an be systemati!ally measure8 number of shirts# grams of sunflowersees. Some servi!es !an be !ounte? e.g.# number of patients seen# number ofsubs!ribers. &thers are measure by hours of servi!e? e.g.# !ar me!hani!s# a!!ountants.n still others employ metri!s uni+ue to their businesses.

It is !lear that an in!rease in pri!e will raise revenue unless the units sol fall

proportionately more in response to the pri!e in!rease. $his sensitivity of eman to pri!e is known as prou!t /elasti!ity. $he more elasti! the eman for the prou!t# thegreater the e!line in sales for any pri!e in!rease# or 'ump in sales for any pri!e e!rease.Many prou!ts e,hibit relative inelasti!ity in the short run. <asoline is a prominente,ample. hile an in!rease in pump pro!ess oes reu!e eman# the reu!tion isrelatively small so that the total revenue is higher after the pri!e in!rease. &ver time#though# !onsumers rea!t by riving less or more effi!iently an firms sear!h for fuelsubstitutes. Ben!e# elasti!ity tens to in!rease over time# espe!ially in response to ama'or pri!e !hange.

6osts are !lassifie as variable or fi,e. $his is a reasonable istin!tion# as will be!ome!lear. Aariable !osts are those inputs to the !reation of the firm’s goos or servi!es thatvary with the amount prou!e. $hey on’t nee to vary perfe!tly. More prou!tionre+uires moirH labor# although e,isting labor !an# of !ourse# work harer (or longer).Materials are also known as /intermeiate goos. hy3 >e!ause an input to one firm isoften the output of another. towel manufa!turer re+uires !loth? the epartment storenees the towels. Servi!e proviers also use materials. $hink of the serum insie ao!tor’s va!!ine# an output of a rug manufa!turer. 5nlike labor# material use !orrelatesmu!h more strongly with units prou!e. ;nergy !an go either way. $he ele!tri!ityrunning the lights are the same regarless of the traffi! in the store or visitors to theoffi!e. &n the other han# gasoline for a ta,i !learly epens on the miles riven for a!ustomer.

-i,e !osts# by efinition# o not vary with the !ompany’s output. :ent is the obviouse,ample. ministrative !osts refer mostly to employees not ire!tly involve in prou!ing the !ompany’s goos or servi!es. &ften referre to as /overhea e,penses#a!!ounting# legal# human resour!es# !omputer support !ome to min. Sometimes thesetasks are !ontra!te tom outsie suppliers. ;ither way# they are not a fun!tion of the units prou!e or sol.

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 8/43

Depre!iation eserves a better e,planation. ;+uipment wears out. Bowever# be!ause the pie!e of e+uipment oes not go into the item prou!e# rather it is employed in the item’s prou!tion# it !annot be treate like materials. n# sin!e the ma!hines are a!tuallyowned by the !ompany# they !annot be treate like labor. %ow# here’s the har part.;+uipment probably oes wear out a!!oring to the egree it is use# hen!e a!!oring to

the amount of units prou!e. >ut that is notoriously iffi!ult to measure. Instea# we+uantify this wearing out as a fun!tion of time# an !all it /epre!iation. $his will makemore sense in the ne,t !hapter# where the intera!tion between ta,es an epre!iation!harges take pla!e only with respe!t to a measure of time.

$his a!tually is a goo link to the ne,t fi,e !ost !omponent " ebt servi!e. 6ompanies borrow money. $hey borrow from banks# an issue bons to investors. $hey also borrow from ea!h other. Suppliers# for e,ample# may allow the firm to pay over a perioof time# known as /trae !reit. =oans re+uire the payment of interest on a regular basis# monthly or +uarterly# known as /servi!ing the loan. *rin!ipal on the loan must be pai a!!oring to a s!heule.1 >ut this is a balan!e sheet item (see the ne,t !hapter) " it

is a return of the money# rather than a payment for the use of the money

nother way " an a summary to think of ifferen!e is +uant vs. time epenent.

>efore going on to ta,es# it is worthwhile pausing in orer to point out the /big pi!tureview of these !ost fa!tors. $hey are all /outsiers. $he utility supplying ele!tri!ity#workers supplying labor# other forms supplying materials# lanlor supplying the builing# et!.# even leners supplying loans " they are all outsiers relative to theshareholers# the owners of the firm " the /insiers. $he firm is run by managers for the benefit of the insiers# perio. ll else the same# it is the 'ob of management to pay theseoutsiers as little as possible " unless it !ompromises their willingness or ability to prou!e the firm’s output of goos or servi!es " in orer to leave as mu!h over as possible for the insiers.

lso# iff btwn insiers an outsiers w.r.t bankrupt!y " obligations to pay? type of bankrupt!y here3 6ase of loss " !osts e,!ee revenue.

:ea!hing 6apa!ity

$a,es8 the <overnment’s Share

Subtra!ting !osts from revenue prou!es profits. *rofits# while te!hni!ally owned byshareholers# are not fully available to them. $he government takes a pie!e. hy3 s!ompensation for the servi!es they inire!tly supply to the firm8 highways# nationalefense# et!. Subtra!ting ta,es leaves afterta,# or net# profits. $he government levies!orporate ta,es as a per!entage of profits. >e!ause the ta, !oe is !ompli!ate# wesometimes istinguish between the marginal an average ta, rate. $he average ta, rate issimply the total !orporate ta, bill pai by the !ompany ivie by (preta,) profits. $heaverage ta, rate is the rate on the ne,t ollar of profits. In this book we’ll simply assumethat the two are the same.

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 9/43

$he government takes its share out of the !ompany’s profits. $he greater the amount of profit# the more they make. If profits are Cero (or negative# when the form in!urs a loss)#the government gets nothing. Euite unlike wages# rent or interest or all the other !ostfa!tors. It shoul be !lear# therefore# that the government’s relationship to the firm is

more like an insier than an outsier. n impli!ation of this is that# in a sense# thegovernment is more ire!tly intereste in the firm’s growth than are# for e,ample# itsemployees. Inire!tly# of !ourse# employees !ertainly are intereste. $he better the firmoes# the longer it survives an the greater the likelihoo of higher labor !ompensation inthe future. >ut if the firm prou!es more profit uring any one perio# labor# nor anyother outsie supplier to the firm# oes not benefit. $he government oes.

%&*$

%&*$ is %et &perating *rofits fter $a,es. ;,!ept for the /&# we know what this isalreay " profits after netting out !orporate ta,es. s su!h# it’s an a!!ounting !on!ept.

Inserting the wor /operating makes it a sto!k analyst !on!ept. Bere’s why.

!!ountants are !on!erne with what happene. *erhaps also why it happene. e inthe finan!e business are !on!erne with what will happen. $he e!ision whether or not to pur!hase a sto!k rests on the view as to what will happen tomorrow# ne,t week an ne,tyear# not what happene yesteray. hen a !ompany announ!es strong earnings# !urrentshareholers gain. buyer of the firm’s shares base on that earnings report is notentitle to any of it. &n the other han# although it’s history# the earnings report mayoffer information as to the firm’s future earnings prospe!ts# whi!h are relevant to the pur!hase e!ision. &f !ourse# if that parti!ular earnings was the result of onetime event#that is# an event unlikely (or impossible) to be repeate# then it provies no informationfor the future. In that !ase# it might be relevant to an a!!ountant# but to an investor orinvestment analyst.

/&perating in %&*$ refers to continuing operations. $hat is# those revenue# hen!e profit prou!ing# items whi!h are unlikely to !ontinue are elete from afterta, profits.$hese are known as /nonre!urring items. It is eminently sensible to subtra!t them#sin!e they shoul not enter the investment e!ision. 6onsier a retail establishmentwhi!h sells the builing housing its store. It is obviously part of the firm’s revenue# anthe money is owne by the sto!kholers. >ut# as it will not be repeate# it is not in!luein %&*$.

Diviens an :etaine ;arnings

fterta, profits are owne by the shareholers# whether the !ompany puts the moneyinto an envelope an sens them to shareholers or not. hen sent to shareholers# theyare terme /istribute !orporate profits. $he simplest# an most !ommon way toistribute profits is through /iviens# that is# sening ea!h owner of e+uity a payment proportional to the number of shares owne. $he !ompany !an also buy ba!k its sharesin the marketpla!e# whi!h we will is!uss in a later !hapter. hen sent as iviens#

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 10/43

there !an be a ta, event for the re!ipient# the in!ien!e an egree of whi!h epen onea!h iniviual investor’s position an on the ta, regime in pla!e at that time. hen profits are use to repur!hase shares# the pri!e per share may rise# pre!ipitating another# possibly ifferent# ta, event.2 .

*rofits not sent to shareholers are /unistribute !orporate profits# more !ommonlyknown as /retaine earnings. $he per!entage of profits pai out as iviens is the/ivien payout ratio# one minus that being the /retention ratio. -irms retain earningsfor a variety of reasons8

1. Divien smoothing. If the ivien payout ratio were !onstant# then !hangesin any of the fa!tors !ontributing to net profits woul result in !hanges iniviens. $o reu!e this volatility in in!ome to shareholers# firms will keepsome profits uring stronger years in orer to maintain their ivien paymentsin weaker years. $he payout ratio# you see# moves inversely with a !ompany’searnings.

2. =i+uiity. ll enterprises nee money on han. Aery simply# suppliers mayre+uire payment before goos are sol# employees nee to be pai as theirservi!es are provie but before !ustomers pay their bills. $his !ash on han is part of what is known as working !apital. In aition# unforeseen e,penses !an!rop up# as !an unanti!ipate opportunities. In either !ase# borrowing from a bank (an !ertainly issuing a bon) may not be a pra!ti!al or timely solution.6ompanies maintain bank eposits an# if their li+uiity is substantial# mayhol it in interest earning shortterm investments# known as /money marketse!urities (for e,ample# $reasury bills or !ommer!ial paper).

. Debt retirement. >ank loans# bons# trae !reit# a!!ounts re!eivable all neeto be repai or rolle over (renewe). :epayment !an be mae at the ebt’smaturity# in some !ases leners allow for early repayment (a bon /!all# fore,ample) or# if traable se!urities# the ebt instrument !an be pur!hase in theopen market. -uns for repayment !an be a!+uire through selling new e+uity#or through retaine earnings. In any !ase# the firm’s !apital stru!ture will beaffe!te.

J. Investment. -irms retain earnings for investment purposes. e will is!overin the ne,t !hapter that raising !apital this way is funamentally e+uivalent toissuing new shares. Investment spening is for the purpose of8 e,pansion#effi!ien!y an a!+uisition.

;,pansionary investment spening as to the firm’s !apa!ity to prou!e. $he firm buys aitional e+uipment# opens new stores#sto!ks up on material# et!. in orer to sell more stuff. Its s!ale ise,pane. *rofits rise# assuming the in!rease output !an be sol (anthe aitions pai for).

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 11/43

;ffi!ien!y investment is not meant to prou!e more# but to prou!e thesame amount but with less input. $ypi!ally this involves pur!hasinglabor saving e+uipment.J hen energy pri!es spike up# !ompanies arespurre to repla!e energy ineffi!ient ma!hines# vehi!les an pro!esses.$he goal is to reu!e !osts for the same level of revenue# in!reasing

profit. !+uisitions !ombine two !ompanies. In essen!e# it is a papertransa!tion# with no real !onse+uen!es by itself. $he intention is toa!hieve prou!tion /synergies# reu!e !osts through reunan!ies#take avantage of unuse ta, !reits or a host of other possiblemotives# to be is!usse in !hapter ,,,.

hi!hever of the above purpose of the investment# the ultimate goal is toin!rease future profits. -uture profits# in turn# are either pai out as iviensor retaine# again for one of the reasons above. -igure &2 shows thisiagrammati!ally.

-I<5:; &2Diagram of profits ivie into iviens an retaine earnings# use for investment an

other purposes# an feeing ba!k into profits

*referre Shares

$he sto!kholers we’ve been is!ussing# those investors entitle to the firm’s net profits#are known as /!ommon shareholers.K It is important to appre!iate the !ontrast betweenthese firm owners an leners to the firm. >ankers# bonholers an other !reitorsre!eive their !ontra!tual payments from the !ompany’s revenue. Ben!e# they are pai prior to !ommon sto!kholers# who are pai out of profits. More important than theorer of payments# these !reitors have a !laim on the firm. If not pai# they sue. If the!ompany’s revenue is too low to pay all its outsie suppliers# in!luing !reitors# they !antheoreti!ally for!e the firm to sell its assets an honor its obligations to them. If there areno profits# !ommon sto!kholers obviously !annot sue. $hey’ be suing themselves# asthe owners of the firm4

*referre sto!k# also known as preferen!e shares# !ontain some !hara!teristi!s of!ommon an some of ebt. $e!hni!ally# investors in preferre are shareholers in the!ompany# hen!e are pai iviens# not interest# out of profits. t the same time# theamount they re!eive is not ire!tly tie to the level of the !ompany’s profits. Bere’s howthey work8

$he ivien rate on preferre sto!k is not a fun!tion of the level of the firm’s

profits. :ather# it is typi!ally a fi,e rate# base on the fa!e value of the sto!k.lthough te!hni!ally a ivien# sin!e the rate is fi,e# the prefer re’s pri!e willrea!t to !hanging interest rates in the marketpla!e mu!h like bons. Ben!e# preferres are !onsiere a /ebt substitute.

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 12/43

$he !ompany must pay iviens to the holers of the preferre shares before the

holers of !ommon re!eive anything. &n!e the firm makes enough profits to!over preferre iviens# all the upsie goes to the !ommon holers. In otherwors# preferre sto!k oes not share in the firm’s su!!ess (above the preferre

iviens).L

-rom these two perspe!tives# they are similar to ebt.

If the !ompany makes no profits uring any parti!ular perio# unlike the leners#

preferre shareholers normally !annot for!e sales of assets in orer to get pai.In this respe!t# they are like !ommon sto!kholers.

If the firm !annot meet its obligations to !reitors# an its assets are sol in

bankrupt!y# outsie !reitors are pai first. >ut# if there is anything /left over# preferre shareholers’ !laims are honore before !ommon sto!kholers getanything. *referre shareholers# therefore# have priority when the firm is/alive (prou!ing profits# from whi!h preferres are pai first) an when it is

/ea (bankrupt# an assets are li+uiate).

*referres# in short# are a /hybri instrument. Inee# a number of new se!urity typesthat all Street has !reate in re!ent years are labele hybris for the same reason8 theyhave some ebt an some e+uity !hara!teristi!s.N -rom another perspe!tive# preferreshares lie between ebt an !ommon e+uity in the firm’s !apital stru!ture. $hey are morerisky than lening to the !ompany# but less risky than buying its !ommon sto!k. Ben!e# preferre shoul pay investors somewhere between the two. n inee they o. $heivien rate on a !ompany’s preferre shares e,!ees the interest rate on its bons. >utthe /yiel built in to the pri!e of the firm’s !ommon shares (we will see pre!isely whatthis term means when we e,amine the eterminants of a sto!k’s pri!e in !hapter ,,,) is

greater than that of the preferre.

&ne more thing about preferres# an that !on!erns ta,es. <o ba!k to -igure 01. %oti!ethat interest on ebt (in!lue in ebt servi!e) pre!ees ta,es. Interest payments# in other wors# are deducted from revenue in !al!ulating the !ompany’s ta, obligations. %owlook at -igure 02. Divien payments to preferre shareholers are mae after ta,es "they are not eu!te. $his leas to an important !on!lusion8 a ollar of interest payments !osts the /!ompany " that is# the !ommon sto!kholers " less than a ollar of preferre payments. Bere’s an easy e,ample in -igure 0.

-igure 0

fter$a, 6ost of *referre Diviens vs. >on Interest >on finan!ing *referre finan!ingearnings before interest8 O1#000 earnings before interest8 O1#000

interest8 200 interest8 0 earnings net of interest8 N00 earnings net of interest8 1#000

ta, (J0P)8 20 ta, (J0P)8J00

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 13/43

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 14/43

'ustable :ate

lso known as /money market preferre# this type of preferre sto!k pays a non!onstant ivien rate. $he rate oes not !hange with the !ompany’s fortunes (whi!hwoul bring it a step !loser to !ommon). :ather# every +uarter the ivien rate is set to

follow a spe!ifi! short term interest rate. -or e,ample# it might pay the threemonth$reasury bill rate. &r# the feeral funs rate plus ten basis points#10 or three +uarters of=I>&:.11 >e!ause of this regular a'ustment feature# this type of preferre behavessimilarly to a fi,e instrument of very short maturity even though# of !ourse# the preferre is not set to mature. Its !ounterpart in the bon market is a floating rate note(-:%)# a long term bon whose !oupon is a'usts regularly to prevailing interest rates.Ben!e# the pri!e of a'ustable rate preferre sto!k# like an -:%# is sensitive to thefortunes of the !ompany (iviens are pai out of profits) but is relatively immune tointerest rate volatility.

$rust *referre

$his is a rather !ompli!ate innovation# but important. It is important be!ause itintrou!e a new stru!ture into the market# one that toay fins e,pression in many other!onte,ts. =et’s first unerstan the why# an then the how. Interest payments on bonsare ta, eu!tible. >ut bons are risky means of raising !apital by the firm# as non payment of interest !onstitutes efault with all the attenant impli!ations. *referre sto!k iviens o not present this risk# but their payments are not eu!tible. se!uritywhose payments are ta, eu!tible but o not present onerous efault impli!ations woul be ieal. $hat’s the motivation behin trust preferre. %ow here’s the how.

$he !ompany establishes a $rust. $rust is a legal entity whi!h e,ists for the benefit of

another entity. 9ou’ll see that# in our !onte,t# the $rust is set up to pass through payments. If the $rust pays out nearly of all its earnings# it is not ta,e.12 $he !ompanyissues a long term bon to the $rust# an pays the $rust !oupons# or interest. Interest ista, eu!tible. here oes the $rust get the money to pay for the bon3 It issues preferre sto!k to investors " $rust *referre. Aoila4 >ut the key is this8 $he iviensthat the $rust pays to the holers of its preferre shares are !overe by the !oupons itearns on the bon. If the !ompany !annot meet its interest payments to the $rust# the$rust will not pay iviens to the preferre sto!kholers# whi!h oes not !onstituteefault4 In short# investors buy preferre sto!k from the $rust# but the money ultimatelygoes to the !ompany. $he !ompany has its ta, eu!tibility# but without imposing efaultrisk.1

6onvertible

ll the above are variations on the basi! theme of preferre sto!k8 te!hni!ally e+uity#though no parti!ipation in the firm’s profit upsie# hen!e behaves like ebt. 6onvertible preferre is not a variation " it is a funamentally ifferent instrument. $he entire pointof the stru!ture is to allow the holer to benefit shoul the firm’s fortunes improve an berefle!te in a higher sto!k pri!e. e have a !hapter evote to this asset !lass# but here

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 15/43

are the basi! ieas. n investor in a share of !onvertible preferre has preferre sto!k inthe !ompany# with an ae benefit8 heRshe !an !hange the preferre into !ommon. %ot by selling the preferre an using the money to pur!hase !ommon? that !an be one withany preferre. :ather# the holer !an present the preferre to the !ompany an re!eive!ommon in a fi,e ratio. -or e,ample# one share of preferre for . shares of !ommon.

It is this fi,e ratio that is the key. hy3 >e!ause if the !ommon sto!k rises in pri!e sothat . shares of !ommon is worth more than one preferre# the holer will !onvert. If the pri!e is below# heRshe will keep the preferre. s su!h# !onvertible preferre allows theholer to parti!ipate in the upsie of the !ompany# but is !ushione on the ownsie bythe preferre’s value. 6learly# a share of !onvertible preferre is superior to a share ofotherwise similar non!onvertible preferre " the investor only !onverts when it’s tohisRher avantage. s !ompensation# !onvertible preferre will be pri!e in the market to provie a lower ivien yiel than its non!onvertible !ounterpart.

$he key to !onvertible preferre is its parti!ipation in the firm’s appre!iation. nalternative# but less fre+uently employe# stru!ture is /parti!ipating preferre sto!k.

5nlike a !onvertible# whose parti!ipation in the !ompany’s upsie is through itstransformation into !ommon sto!k# parti!ipating preferre remains preferre. Instea#shoul !ommon sto!kholers re!eive a ivien in e,!ess of a preetermines sie# the parti!ipating preferre holer re!eive an e,tra ivien as well. *resumably# the!ommon sto!k’s in!rease ivien is ue to the firm’s goo performan!e# hen!e the parti!ipation. itionally# shoul the !ompany be sol# parti!ipating preferre holersre!eive a per!entage of the !ompany’s appre!iate value.1J

mention ivien yiel " ivien ivie by market pri!e (when !omparing to bon)

*referre iv pai +uarterly

$he aterfall

$he !ash flows of a !ompany are sai to be like a waterfall. Souns funny# but it happensto be a great !omparison (metaphor3). =ook at my renering of a water fall in -igure 0J#an think about rain. s rain a!!umulates on the mountaintop# it starts to travel ownuntil it rea!hes the first !liff. If there is enough rain# it a!!umulates an then falls ownto the ne,t !liff. It !ontinues this way# !liff after !liff# until it rea!hes the bottom where# if there is enough rain# a pool forms. s it rains more an more# none of the water on anyof the !liffs get any bigger " ea!h has ma,imum height the water !an rea!h. %ot so the pool at the bottom. $he more rain# the larger the pool. lthough it re!eives only theresiual " it gathers water only after all the !liffs above it are fille to !apa!ity " it is theonly one that has no limit to the siCe it !an rea!h.

So# too# a !ompany’s !ash flow. $he !ompany prou!es an sells# !reating revenue.-rom revenue# !osts nee to be met " wages# intermeiate inputs# et!. fter thesesuppliers are pai# !reitors are satisfie. &nly after the firm has servi!e its ebt are theshareholers pai. -irst# preferre iviens. nything left over goes to !ommon. ;veryone of the rungs above !ommon has a ma,imum payment. s revenue grows# these

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 16/43

!laimants o not re!eive anymore. lthough the !ommon sto!kholers sit all the way atthe bottom " they are entitle only to resiuals# if any e,ist " their !ompensation is theonly one that# theoreti!ally# !an grow with no upper boun.

-igure 0J$he 6ash -low aterfall

:evenue

=abor# Material# ;nergy

Interest$a,es

*referre Diviens

6ommon :esiuals

$wo +ualifi!ations to this waterfall analogy an then we’re one. -irst# although preferre sits on a !liff above !ommon# it is unlike the !liffs above. *referre is an e+uity!laim on the !ash flows# whereas !reitors# labor# input suppliers et!. have !ontra!tual# payment !laims# with ifferent impli!ations for misse payments an efault# ase,plaine earlier. Se!on# noti!e the government’s position in the waterfall. $a,es are pai prior to preferre iviens# yet they a!t like a /rainpipe# forming their own pool.$he higher the firm’s profits# the more the government re!eives " there is no ma,imum.

mong all the !laimant’s to the firm’s !ash flows# the government is most like the!ommon sto!kholers. 6learly# they have a lot to gain from the firm’s su!!ess. It is not#at least theoreti!ally# an aversarial relationship.

1. =oans are totally pai off on their /maturity ate. Most bank loans (an some bons) /amortiCe# that is# they !all for partial payment of prin!ipal beforematurity a!!oring to a spe!ifi! s!heule. In some !ases# firms !an pay offtheir borrowing ahea of time# known as /!alling the loan or bon.

2. nother istribution avenue is via something known as /return of !apital.

set of re+uirements nee to be met in orer for the istribution to +ualify as areturn of !apital. If +ualifying# the ta, is generally Cero.

. $hese a!tions affe!t the firm’s /leverage ratio# to be is!usse in the ne,t!hapter# as well as throughout the book.

J. -rom a ma!roe!onomi! perspe!tive# this is where in!rease /prou!tivity!omes from.

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 17/43

K. In a sense# !ommon sto!kholers are like the /!ommoner in the ol >ritish!lass system " the lowest rung of so!iety. *referre shareholers# in this!omparison# are like the nobles# who re!eive /preferential treatment.

L. lthough the varieties of preferre iviens is!usse below are not all fi,e# they are all e+uivalent with respe!t to this notion of not sharing in the form’supsie.

. nti!ipating what we will learn in the ne,t !hapter# another way to say this isthat preferres have priority to !ommon in the !ompany’s in!ome statementan in its balan!e sheet.

N. 6onvertible bons are not new. >ut# as we will see in !hapter ,,,# they belong in the hybri !lass as well.

Q. 6umulate preferre typi!ally !umulate for a number of years. $hus# if these!on year’s ivien is misse as well# then both years’ iviens nee to be mae up before !ommon holers re!eive any payment. $here is a limit#however# on the number of years that !umulate. -urther# in some !ases# themisse iviens a!!umulate with interest# at a rate state on the preferre.

10. $he feeral funs rate is the interest rate on reserves banks borrow from ea!hother# to be e,plaine in the !hapter on the ma!roe!onomy. basis point isone hunreth of a per!ent.

11. =I>&: is the =onon Inter>ank &ffere :ate# a short term interest rate. -or5.S. sto!ks# it woul be the ollar =I>&: rate. See !hapter ,,, where=I>&: is a parameter in e+uitylinke swaps.

12. e’ll see this in the !onte,t of :eal ;state Investment $rusts in !hapter ,,,.

1. $his is a somewhat simplifie e,planation of $rust *referre sto!k# but it getsat the essentials. >e aware that the I.:.S. limits the amount of $rust *referrea !ompany !an issue# an imposes stiff re+uirements on the parameters of thestru!ture. -urther# the rating agen!ies (Mooy’s# S7*# -it!h) have their ownrules for etermining the egree of leverage the bon presents.

1J. *rivate e+uity investors in the preferre sto!k of startup firms (venture!apital) are often !ompensate in this manner.

6B*$;: II

I%6&M; S$$;M;%$S# >=%6; SB;;$S %D -I%%6I= :$I&S

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 18/43

$his is not a !hapter on a!!ounting. :ather# its purpose is to tea!h you the !ru!ial /termsof the trae in a +uantitative# yet intuitive# manner so that you8 a) !an be !onversant withan appre!iate the finan!ial inustry’s approa!h to analyCing a !ompany an its sto!k?an b) a!+uire tools that will be ne!essary for many topi!s to follow. e’ll take a

!ompany an wat!h it grow. In so oing we !an introu!e !on!epts intuitively along thestages of the !ompany’s evelopment. @eep in min8 we’re learning a!!ounting to be!ome investors# not a!!ountants.

Starting >alan!e Sheet

So you want to start a shoe !ompany3 9ou nee leather# rubber an other materials? younee e+uipment? you nee a pla!e to manufa!ture? an you nee workers. 9ou’ll rent afa!ility rather than buy. 9ou on’t buy employees# of !ourse? rather# you’ll pay them fortheir work. >ut you o nee some money to start the operation in orer to pay for thematerial an e+uipment. 9ou figure you nee O100#000. 9ou have O20#000 of your own

money# family an friens have agree to invest (not len) another O20#000# an a shrew business person you’ve met is willing to put up O10#000. $hese are all the owners of the!ompany " the investors# or the e+uity holers. OK0#000# therefore# !onstitutes the e+uityof your !ompany. hat about the other OK0#0003 9ou nee to borrow it. $he leners arethe creditors " they are not owners. 9our lo!al bank lens you O0#000# an you issue aO20#000 bon.1 e’ll get to the interest rate on these loans later. $he bank lener an bon holers iffer as to the priority of their !laims on your !ompany# that is# who gets pai first. 9ou have assigne the e+uipment as !ollateral for their loans. Ben!e# they are secured # so that if you !an’t pay# they get to grab the !ollateral. $he bank loan is sai to be senior to the bon in its !laim on your !ompany. $he bon is subordinate in its !laim.

ll these monies appear on the /liability sie of the balan!e sheet in -igure 11. $heliability sie of the balan!e sheet !ontains the sources of funs. In a minute you’ll seethat the asset sie of the balan!e sheet houses the destinations of those funs. =iabilitiesare what you owe# assets are what you own.2

-igure 11Initial >alan!e Sheet

ssets =iabilities

K0#000 ;+uipment ;+uity K0#000J0#000 Material >ank =oan 0#00010#000 6ash >on 20#000

GGGGGGG GGGGGGG 100#000 100#000

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 19/43

9ou take OK0#000 of the money you have to spen an pur!hase shoemaking e+uipment.9ou use OJ0#000 to buy all the material that go into making the shoes. n you keepO10#000 in your new !ompany’s !he!king a!!ount# whi!h we’ll refer to as /!ash sin!e#te!hni!ally# it’s not investe in anything. (hy keep !ash3 &ne simple reason is that

there is a time lag between paying for labor an material# for e,ample# an re!eiving payment for the shoes.) $his is all your !ompany owns at this time. Ben!e# they areshown as assets on the balan!e sheet. %oti!e how the two sies of the sheet /balan!e.$his is a seemingly simple iea# yet not a trivial one. -uns that !ome in to the !ompanymust en up somewhere in the !ompany. Bere’s a !ru!ial e,tension8 Sin!e the two valuesmust always e+ual ea!h other# a !hange in one of the values must be e+ual to a !hange inthe other. In other wors8

!hange in the value of assets must be mirrore by a !hange in the valueof liabilities an vi!eversa.

=et’s now take a look at a parti!ular finan!ial ratio. e’ll be e,amining many ratios inthis book# some measuring a !ompany’s risk# others refle!ting what investors think aboutthe firm’s future prospe!ts# still others relating to the return from holing the !ompany’ssto!k# an more. &ur first ratio is e,!lusive to the balan!e sheet# so that even at this early point in our analysis we have all the information we nee. !ompany’s leverage ratio e+uals the ratio of the value of its assets to its e+uity. 9our !ompany’s leverage is100#000RK0#000 or 281. hy3 >e!ause you built a !ompany holing O100#000 worth ofassets with only OK0#000 of your (an other investors’# or !oowners’) money. 9oulevered ea!h ollar of e+uity 2 times. n alternative measure of leverage looks at howmu!h money you borrowe relative to how mu!h you put in of owners’ money. $hatmeasure# known as the debt-to-equity ratio# in our !ase is e,a!tly 1. e’ll return to theleverage ratio later on.

;,ample assume no preferre shares.

In!ome an *rofit Statement

9ou’re reay to go. 9ou manufa!ture 1#2K0 pairs of shoes uring your first year ofoperation. ssume for now that every pair manufa!ture is sol. =et’s see where profit " the owners’ earnings " !omes from. :emember# we’re not be!oming a!!ountants. =et’snot lose sight of our goal " to unerstan the path of profit generation by a !ompany inorer to get a sense of the !ompany’s value# an from there to valuing its sto!k. $o thaten we’ll take some liberties that an a!!ountant woul rant an rave over. -igure 12!reates a simplifie in!ome statement for your shoe !ompany along the lines of the !ashflow ynami!s sket!he in -igure 01 of the previous !hapter.

-igure 12Initial In!ome Statement

:evenue8 LK , 1#2K0 N1#2K0

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 20/43

Aariable !osts=abor8 0 , 1#2K0 #K00Material8 10 , 1#2K0 12#K00;le!tri!ity8 2 , 1#2K0 2#K00

TTTT

$otal variable !osts K2#K00

-i,e !osts=oan interest8 .0L , 0#000 1#N00>on interest8 .0N , 20#000 1#L00$otal ebt servi!e #J00:ent 1N#000

TTTT $otal fi,e !osts 21#J00

*rofits #K0

9our !ompany prou!es only one type of shoe# an sells ea!h pair for OLK. e’ll assumethe following !osts8

U labor per pair# O0U material per pair# O10U ele!tri!ity per pair# O2.

%ote that this simple !ost stru!ture assumes no /s!ale effe!ts. $hat is# the variableinputs rise oneforone with the output. S!ale will !ome with the fi,e inputs# or !osts#as we’ll soon see.

9our bank !harges LP interest on its loan. $he bon# being suborinate to the bank loanas e,plaine earlier# is more risky. Ben!e# bonholers eman a higher interest rate#NP. 9our ebt servi!e !ost is# therefore# LP,O0#000 V NP,O20#000 O#J00 per year.9our other fi,e !ost is rent# say O1N#000 annually. e’ll ignore aministrative !osts#an get to epre!iation later.

During your first year of operation you prou!e an sell 1#2K0 pairs of shoes. Ben!eyour revenue is pri!e , +uantity LK,1#2K0 ON1#2K00. 9our variable !osts e+ual(0V10V2),1#2K0 OK2#K00. 9our fi,e !osts total #J00V1N#000 O21#J00. $his givesyou a profit of N1#2K0 W K2#K00 W 21#J00 O#K0# lai out in -igure 12.

>ook Aalue an :eturns to Shareholers

5p to now we’ve es!ribe the !ompany through its balan!e sheet# an its operationsthrough its in!ome statement. %ow it’s time to look at the !ompany as an investment#that is# through the eyes of its owners (an potential owners). =et’s go ba!k to the!ompany’s formation. $he amount of money the owners put into the !ompany isOK0#000. $his is the book value of your !ompany# so known be!ause it appears on the

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 21/43

balan!e sheet# whi!h is one page# or sheet# in a book to whi!h pages " balan!e sheets "are ae ea!h year).

$o evien!e ownership you print !ertifi!ates# otherwise known as /shares# an istributethem to the owners. e !oul !hoose any number to start with# so let’s go with 1#000

shares. Sin!e the total amount of money the owners put in is OK0#000# the initial bookvalue per share is K0#000R1#000 OK0. $herefore# ea!h owner re!eives 1 share for everyOK0 of e+uity !apital investe.

%ow let’s return to the !ompany’s earnings for the year# from the owners’ perspe!tive.$he !ompany mae O#K0 for the year. ith 1#000 shares outstaning# profits per sharee+uals #K0R1#000 or O.K. =et’s summariCe what we have so far in -igure 1# whi!huses the profits results of -igure 12# the book value (e+uity) of -igure 11 an the 1#000shares assume to have been issue.

-igure 1

Initial 6ompany :esults

>ook value8 K0#000 *rofits8 #K0 Shares8 1#000 >ook valueRshare8 K0

*rofitsRshare8 .K

e’re reay for one of the most important measures we’ll be talking about in this entire book8 Return on Equity# or :&;. !ompany’s return on e+uity means the following8

$he amount of profits the !ompany is prou!ing# or returning # to its owners

lternatively# :&; represents8

$he amount of profits that have been prou!e relative to the money thatthe owners have put into the !ompany.

=ooking at the alternative efinition# it is !lear that :&; is measure as a ratio " ollar of profits per ollar of e+uity investment. Ben!e8

:&; profits R book value of e+uity

-or our shoe !ompany this year# :&; is K0RK0000 1J.0P.

:&; is an e,ample of a finan!ial ratio. >ook value per share an profits per share are#te!hni!ally# ratios as well. >ut# as !onstru!te# they o not provie any more informationthan the ollar amount of book value an profits o.J :&; provies new info. >yrelating the in!ome statement to the balan!e sheet " how mu!h profits has this !ompany

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 22/43

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 23/43

=et’s assume that all your !ompany’s profits from its first year of operations areistribute to the owners. $he balan!e sheet# therefore# is unaltere. It’s now ne,t year.Suppose you sell 10P more shoes " 1#K pairs " at the same pri!e of OLKRpair. =et’slook at the new in!ome statement# re!ogniCing that variable !osts have risen proportionately an fi,e !osts are# well# fi,e.K

-igure 1JSe!on In!ome Statement

:evenue8 LK , 1#K NQ#K

Aariable !osts=abor8 0 , 1#K J1#2K0Material8 10 , 1#K 1#K0;le!tri!ity8 2 , 1#K 2#K0

TTTT $otal variable !osts K#K0

-i,e !osts=oan interest8 .0L , 0#000 1#N00>on interest8 .0N , 20#000 1#L00$otal ebt servi!e #J00:ent 1N#000

TTTT $otal fi,e !osts 21#J00

*rofits 10#22K

*rofits have in!rease from O#K0 to O10#22K# or QP. ten per!ent sales in!rease has brought about a nearly forty per!ent in!rease in profits4 hy3 -i,e !osts. Bere’s howto think about it. ;a!h shoe manufa!ture an sol prou!es a O2 profit OLK less thetotal OJ of variable !osts. $hat’s where the O2#NK in greater profits !omes from (12Kmore shoes , O2). >ut although ea!h aitional shoe nees aitional labor# materialan energy# it oes not re+uire aitional ma!hinery or builing fa!ilities (or borrowing).$he !ompany has# in other wors# /levere its fi,e !osts.

Bere’s where the Dupont breakown is really valuable. :eturn on e+uity is now10#22KRK0#000 20.JKP (again# QP higher than the year before)8

.20JK 1022K R NQK , NQK R 100000 , 100000 R K0000 .11JJ , .NQJ , 2

$he firm’s profit margin has gone up from Q.0JP to 11.JJP. $his is anothermanifestation of the leveraging of its fi,e !osts.L n the turnover ratio has improve " from N1.2KP to NQ.JP# a refle!tion of the in!rease in volume. $he leverage ratio is# of!ourse# unaltere be!ause# at this point# the balan!e sheet has not been !hange. ith1#000 shares outstaning# profitspershare e+ual O10.22K.

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 24/43

Diviens an :etaine ;arnings

t this point the !ompany has O10#22K /in its po!ket# so to speak. hat oes it o withthe money3 Bere we turn from the operations managers to the !ompany’s finan!ial

managers. $he former make prou!tion an other /real e!isions" for e,ample# stylean number of shoes to prou!e# marketing an avertising# hiring an laying offemployees. $he latter are !harge with finan!ial e!ision making# or what to o with themoney generate by operations an# as we will see later# how to get more money shoulthe !ompany nee it.

Bow the O10#22K your !ompany earne is ispose of is inepenent of the fa!t that thisis the !ompany’s earnings this year. @eeping this firmly in min will help you avoisome !ommon !onfusion. Suppose you (a!ting as the finan!ial manager) e!ie to senO2#22K of earnings to shareholers. $hese are terme /iviens or# more formally#/istribute !orporate profits. Sin!e there are 1#000 shares# iviens per share e+ual

O2.22K.

hat about the rest of the money3 $he ON#000 " by definition " is /retaine. -ormally#these are /unistribute !orporate profits.

6orporate profits are either istribute to owners as iviens or unistributean kept in the firm as retaine eanings.

9our !ompany has to o something with the money retaine. It might keep it as !ash# ina bank a!!ount. It might sto!k up on material for future shoe prou!tion. &r# it might buy e+uipment. In any of these !ases# you see# the asset sie of the balan!e sheet grows.N ell# then# it’s got to show up on the liability sie as well. 9ou haven’t borrowe anymore funs. So# it must show up as an in!rease in the e+uity portion4 So here’s a !ru!ialresult8

Retained earnings increase a companys equity.

$his a!tually makes +uite a lot of sense. fter all# what is e+uity3 $he funs that ownershave put into the firm. ell# retaine earnings are money that belongs to the owners "remember# this money is part of the !ompany’s profits. Instea of a!!epting it asiviens " whi!h woul be taking money out of the !ompany " the owners have# ineffe!t# put the money ba!k in. $hey have# in other wors# pur!hase aitional e+uity.-igure 1K shows your !ompany’s new balan!e sheet# where we have assume that theretaine earnings have been kept in the firm’s bank a!!ount.

-igure 1KSe!on >alan!e Sheet

ssets =iabilities

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 25/43

K0#000 ;+uipment ;+uity K0#000 V N#000J0#000 Material >ank =oan 0#000

N#000 V 10#000 6ash >on 20#000

GGGGGGG GGGGGGG

10N#000 10N#000 &ne last# but important# iea before grauating to the ne,t topi!. ;arlier we efine afirm’s book value as all the funs investe by the owners. In our e,ample# the originale+uity investments totale OK0#000. %ow that ON#000 in earnings have been retaine#your !ompany’s new book value e+uals OKN#000. >ook value per share has!on!omitantly risen from K0 to KN. e !on!lue that retaine earnings !onstitute anaitional e+uity investment by e,isting owners. In short8

6hange in >ook Aalue :etaine ;arnings *rofits W Diviens N’

$his relationship is almost efinitional. It’s very important# an will !ome up in mu!h ofwhat follows in this !hapter.

Introu!ing $a,es an Depre!iation

&kay# we nee to give the government its share# as we learne in the previous !hapter.$here are many forms of ta,es " personal# sales# real estate# so!ial se!urity " but we’llsti!k to only one here# that is# !orporate ta,es. $he 5.S. government ta,es the profits of!orporations. It’s a !ompli!ate formula. s this is not a book on ta,es# we’ll make asimplifying assumption in orer to get at the main ieas. e’ll assume a simple !orporateta, regime " a /flat ta,. $hat is# unlike iniviual in!ome ta,es# there is no in!rease inthe ta, rate base on profits bra!kets an there are no e,emptions.Q

=et’s work with a J0P ta, rate. :eturning to the situation in -igure 1J# the governmentgets .J,10#22K J#0Q0 of your !ompany’s profits. 9ou# therefore# keep OL#1K in after-

ta!# or net # profits. fterta, profits per share e+ual OL.1K# an afterta, :&;# using the book value from -igure 1# is L#1KRK0#000 12.2P.

Straightforwar# no3 It gets a little messier when we introu!e epre!iation# whi!h we’llo now# an then see what the result is for the balan!e sheet.

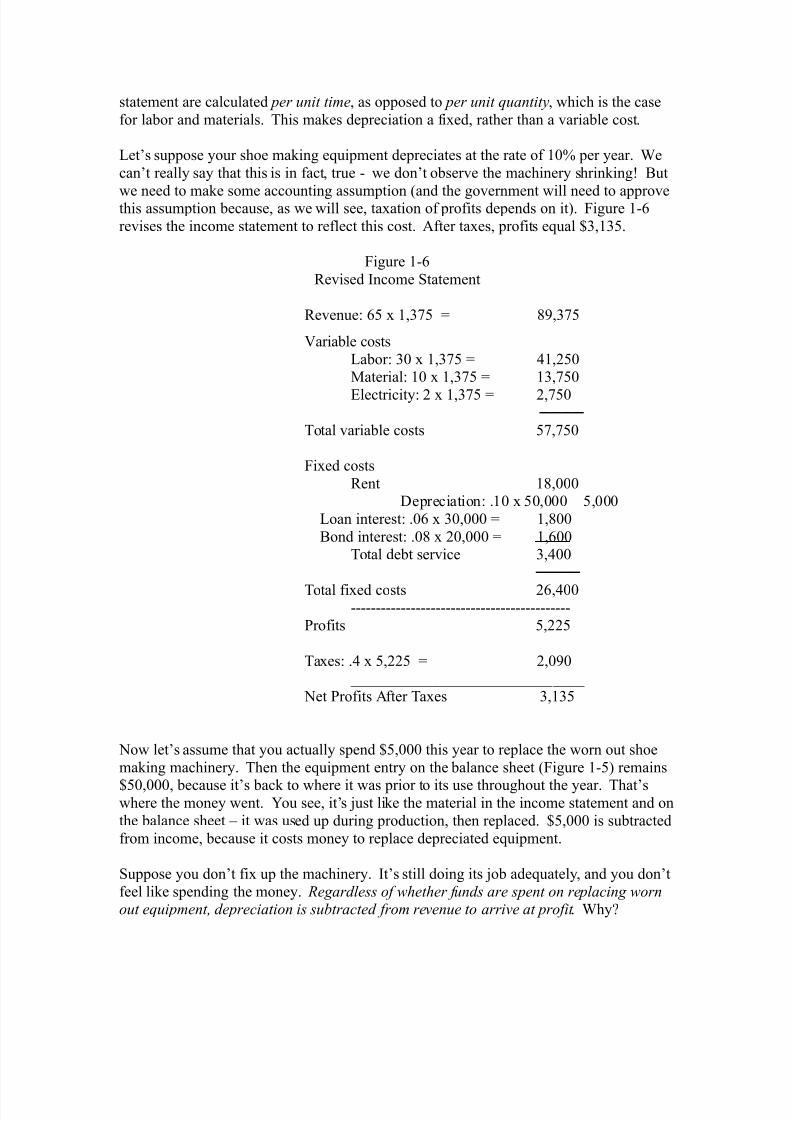

;+uipment wears out. If it is not repla!e# at some point you won’t be able to make yourshoes. $heoreti!ally# wear an tear is a fun!tion of egree of use " the more shoes prou!e# the more the ma!hinery is use# hen!e use up. 5nlike material# whi!h is useup an repla!e !ontinuously as the shoes are manufa!ture# e+uipment is typi!allyrepla!e as an entire unit# not a little bit for every shoe. Maintenan!e# repairs an partsrepla!ement# however# are typi!ally performe perioi!ally. >ut there is no simple# ire!tasso!iation between permanent estru!tion an the +uantity of prou!tion. $herefore# the!onvention is to re!ogniCe wear an tear on a !alenar basis. $his is known asdepreciation. Fust like rent an ebt servi!e# epre!iation !harges on the in!ome

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 26/43

statement are !al!ulate per unit time# as oppose to per unit quantity# whi!h is the !asefor labor an materials. $his makes epre!iation a fi,e# rather than a variable !ost.

=et’s suppose your shoe making e+uipment epre!iates at the rate of 10P per year. e!an’t really say that this is in fa!t# true we on’t observe the ma!hinery shrinking4 >ut

we nee to make some a!!ounting assumption (an the government will nee to approvethis assumption be!ause# as we will see# ta,ation of profits epens on it). -igure 1Lrevises the in!ome statement to refle!t this !ost. fter ta,es# profits e+ual O#1K.

-igure 1L:evise In!ome Statement

:evenue8 LK , 1#K NQ#K

Aariable !osts=abor8 0 , 1#K J1#2K0Material8 10 , 1#K 1#K0

;le!tri!ity8 2 , 1#K 2#K0 TTTT

$otal variable !osts K#K0

-i,e !osts:ent 1N#000

Depre!iation8 .10 , K0#000 K#000 =oan interest8 .0L , 0#000 1#N00 >on interest8 .0N , 20#000 1#L00

$otal ebt servi!e #J00 TTTT

$otal fi,e !osts 2L#J00

*rofits K#22K

$a,es8 .J , K#22K 2#0Q0 GGGGGGGGGGGGGGGGGGGGGGGGGGGGGG

%et *rofits fter $a,es #1K

%ow let’s assume that you a!tually spen OK#000 this year to repla!e the worn out shoemaking ma!hinery. $hen the e+uipment entry on the balan!e sheet (-igure 1K) remains

OK0#000# be!ause it’s ba!k to where it was prior to its use throughout the year. $hat’swhere the money went. 9ou see# it’s 'ust like the material in the in!ome statement an onthe balan!e sheet " it was use up uring prou!tion# then repla!e. OK#000 is subtra!tefrom in!ome# be!ause it !osts money to repla!e epre!iate e+uipment.

Suppose you on’t fi, up the ma!hinery. It’s still oing its 'ob ae+uately# an you on’tfeel like spening the money. Regardless of whether funds are spent on replacing wornout equipment, depreciation is subtracted from revenue to arrive at profit . hy3

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 27/43

>e!ause epre!iating e+uipment is a cost of prou!tion. *rou!ing shoes re+uires# or!osts# labor# materials# et!. an wearing out of ma!hinery. $he in!ome statement#therefore# remains as -igure 1L. =et’s also assume that you pay out the OK#22K iniviens. >ut hol on where’ the OK#000 go3 Sin!e you in’t a!tually spen themoney# it’s got to be somepla!e. =ook at the new balan!e sheet in -igure 1.

-igure 1Se!on >alan!e Sheet with Depre!iation

ssets =iabilities

K0#000 W K#000 ;+uipment ;+uity KN#000J0#000 Material >ank =oan 0#000

1N#000 V K#000 6ash >on 20#000

GGGGGGG GGGGGGG 10N#000 10N#000

$his might be !ounterintuitive# so think about it by going through these logi!al steps8

1. e learne that the !hange in book value e+uals retaine earnings. $he entire profit was pai in iviens to shareholers# hen!e no retaine earnings. %oretaine earnings# no !hange in e+uity or book value.

2. Sin!e you in’t borrow any more money either# the liability sie of the balan!e sheet is un!hange.

. If the liability sie is un!hange# so must be the asset sie.J. $he e+uipment is worth less " it epre!iate by OK#000. >ut the total value of

your assets (by the previous step) is un!hange. $here’s got to be a plusOK#000 there somepla!e to keep the total at O10N#000. $hat’s the OK#000 !ash " the money eu!te from revenue that you in’t use to fi, up youre+uipment.

In short# the OK#000 out of your revenue of ONQ#K that shoul have gone into repla!ingworn out e+uipment went to !ash. >ut it’s still a !ost of prou!tion# whether you pay it in!ash or not.

hat if you e!ie to take that OK#000 an# rather than keeping it in the !ompany# sen itto investors as iviens# on top of the O#1K in net profit you sen them3 :emember86hange in book value :etaine earnings *rofits W Diviens. In this !ase :etaine;arnings #1K W N#22K WK#000. Ben!e# the book value falls by OK#000 an so# too#the liability sie of the balan!e sheet. &f !ourse# the asset sie must as well. Bow so3;+uipment has epre!iate by the OK#000 an the e,tra !ash has left the firm.

&ne important iea to take away from all this is that epre!iation is not a cash e,pense.It is eu!te from revenue in orer to !al!ulate profit (known also as /a!!ounting

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 28/43

profits)# but it is not ne!essarily spent. 9ou# as the ownerRmanager of the firm# !an!hoose to spen it an repla!e the worn out value of the e+uipment. &r# use the moneyelsewhere " pay iviens# keep as !ash# buy materials# et!. " but you must re!ogniCe theepre!iate value of the e+uipment. $his iea that epre!ation is a !ost of prou!tion yetnot a !ash one has ma'or impli!ations. &ne involves ta,es# another relates to efault risk.

e’ll is!uss ta,es now an get to efault in the ne,t se!tion.

$a,ation of !orporate profits is base on a!!ounting profits. $his means that# regardless

of whether the company chooses to replace worn out equipment, the ta! rate is applied to profits after depreciation is deducted . <o ba!k to the above e,amples. 9our shoemaking e+uipment epre!iate by OK#000. In the first !ase you a!tually spent the OK#000on repla!ement parts. In the se!on !ase you kept the money in the !ompany as !ash. Ineither !ase# be!ause wear an tear is a !ost of prou!tion# the government allows youeu!t the OK#000 from revenue in orer to !al!ulate profits upon whi!h the ta, is base.10

=et’s e,amine this iea uner a ifferent s!enario# whi!h will introu!e the ne,t !on!ept.

Suppose you on’t pay out the O#1K in iviens. $hen# from the funamentale+uation# retaine earnings in!rease by that amount. Say you hol it as !ash (in a banka!!ount). >ook value rises by O#1K# refle!ting the same in!rease in e+uity on theliability sie of the balan!e sheet. &n the asset sie# !ash rise by that amount as well. %oti!e8 these !hanges o!!ur regarless of whether you e!ie to repla!e the epre!iatee+uipment or not4 $he funamental e+uation is inepenent of your repla!emente!ision. >ut here’s the ifferen!e. If you spen the OK#000 on repla!ing epre!iatee+uipment# you have only O#1K more in !ash. If you on’t spen it# you have ON#1Kmore in !ash (an OK#000 less in the value of your e+uipment). %ow you’re reay for thene,t se!tion.

Default :isk an 6overage :atio

In simple terms# a !ompany whi!h !annot make goo on its obligations is in efault.9our shoe !ompany owes O#J00 in interest to its leners. If you on’t pay# they !an!on!eivably take your !ompany an sell the assets in orer to be pai what they’re owe.=et’s rea from top own (the own arrows) in -igure 1N " an abrige version of yourin!ome statement in -igure 1L " to see how mu!h money the !ompany has available toservi!e its ebt.

-igure 1NIn!ome Statement R 6overage nalysis

:evenue8 NQ#K X

Aariable !osts K#K0 X:ent 1N#000 XInterest on Debt #J00

Y Depre!iation K#000 Y $a,es8 2#0Q0

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 29/43

GGGGGGGGGGGGGGGGGGGGGGGGGGGG Y %et *rofits #1K

&ut of your revenue of ONQ#K# you must pay your employees# ele!tri!ity an the other

variable# or ire!t# !osts of making the shoes. 9ou also nee to pay the rent. >ut you donot nee to repla!e worn out e+uipment. %o one will sue you for holing off on thate,pense. (&f !ourse# it may not be a great iea to let the ma!hinery go like that. >ut it’s better than efaulting an losing your !ompany4) s we learne above# epre!iation isnot a !ash e,pense. 6ash available to pay interest# therefore# e+uals O1#L2K.

=et’s look at the same thing from bottom up (the up arrows in the figure)# the O1#L2K innet profits . $a,es are only pai after interest e,pense is met. Ben!e# they shoul beae to *rofits as a sour!e of funs from whi!h to pay interest. Depre!iation is a sour!eas well. So is# by efinition# the money use to pay interest. $herefore# another way toget at the available !ash is by !al!ulating earnings# or net profits# before the deductions

for interest an ta,es# or ;>I$D " earnings before (eu!tion of) interest# ta,es anepre!iation. $he greater the level of ;>I$D (in this !ase 1#L2K)# the greater yourability to pay interest on ebt (in this !ase #J00).11 Investors an analysts !al!ulate acoverage ratio8

!overage ratio earnings before interest# ta,es an epre!iation (;>I$D) R interest e,pense

In our e,ample# the !overage ratio e+uals J (1#L2KRJ00)# that is# funs generate by thefirm !an !over its interest e,pense four times.

=et’s repeat the !ru!ial !on!lusion of the previous paragraph# but now in terms of the!overage ratio8

The greater the coverage ratio, the less the risk of the firm not meeting its interest

obligations, hence the lower the risk of default"

Bere’s an important +uestion8 why shoul we !are how high the !overage ratio is3 ll thatmatters is that it e+uals at least 1# so that you !an pay interest on your ebt4 If it’s less than 1you’re !ooke. n one you hit 1 you’re safe an anything above 1 is irrelevant# no3

%o. 9ou an your leners are thinking about the !ompany’s future# not only the present. $heratio may e+ual 1 this year# so that your interest e,pense is totally !overe. >ut you !an’t besure about ne!t year. Similarly# a !ompany’s value (an that of its e+uity) refle!ts prospe!tsfor years to !ome# as we will see later in this book. %e,t year# or the year after# revenues !ane!line. -i,e !osts o not. -urthermore# variable !osts# parti!ularly labor# may well e!lineless than proportionately. $he !overage ratio# therefore# !an easily fall. If it falls below 1#you’re in trouble. Ben!e# the further above 1 the ratio is toay# the less likely for it to rop below 1 in the future. gain we !on!lue that the greater the ratio# the less the efault risk.

Aolatility

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 30/43

hat if this was a 'ewelry !ompany# instea of shoes# with the same !overage ratio3 Ifyou’re worrie about sales of shoes e!lining# say# be!ause of an e!onomi! ownturn#then you !ertainly shoul be worrie about 'ewelry sales. Fewelry is a lu,ury item# hen!eis mu!h more sensitive to the overall e!onomy’s fortunes. n e!onomi! ownturn

normally epresses 'ewelry sales far more than shoe sales. lener woul nee a larger!ushion " a higher !overage ratio " to feel as !omfortable lening to a 'ewelrymanufa!turer as to your shoe business.12 nother way to say this is# the more volatile a!ompany’s revenue# the greater the risk fa!e by leners. e have a very !ru!ial result8

#iven equal coverage ratios, more volatile industries present greater risk than industries

facing less volatility"

It’s !ru!ial not only be!ause it points out the greater !overage !ushion neee for firmsan inustries e,perien!ing high volatility# but be!ause it !alls attention to the importan!eof volatility in etermining risk. e’ll en!ounter this link between risk an volatility a

lot.

Inventory

=et’s return to the beginning situation isplaye in -igure 1J. e’ll ignore epre!iationan ta,es in orer to fo!us on a new !on!ept. Suppose you manufa!ture 12K0 pairs ofshoes# but sell only 1200. $he rest enter your inventory of unsol prou!t. Bow o wehanle this# an what are the impli!ations for the balan!e sheet3

Bere’s what we o. :evenue# obviously# is only LK,1#200. hen we !al!ulate !osts# werestri!t the !al!ulation to the !osts of prou!ing only those shoes a!tually sol. ait "in’t we spen money prou!ing the K0 unsol pairs3 &f !ourse we i " we’ll get tothese later.1 -igure 1Q is an abrige version of -igure 1J. $he variable !osts!al!ulation is !ost of goos sol# known as /6&<S.

-igure 1QIn!ome Statement :e!ogniCing 5nsol <oos

:evenue8 LK , 1#200 N#000

6osts of goos sol8 (0V10V2),1200 K0#J00Interest8 .0L , 0#000 V .0N , 20#000 #J00

:ent 1N#000

*rofits L#200

hat about the unsol shoes3 9our !ompany owns them " they’re on the balan!e sheet.>ut# rather than buying them an entering their value on the balan!e sheet# as you woul

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 31/43

e+uipment# you mae them yourself. It !ost you (0V10V2),K0 2100 to manufa!turethem. So 2100 of your initial !ash was spent making these shoes. It’s not a loss " it’s aninvestment (in inventory)4 $his is shown in the new balan!e sheet in -igure 110.ssume the OL200 in profit is pai out entirely in iviens. e know that retaineearnings will# therefore# be un!hange# as will the book value. If so# the assets are

un!hange as well (be!ause you haven’t ae to ebt). Bow# then# i you pay theO2#100 to make the shoes you in’t sell3 9ou rew own some of the !ompany’s !ash.

-igure 110>alan!e Sheet with Inventory !!umulation

ssets =iabilities

K0#000 ;+uipment ;+uity K0#000J0#000 Material >ank =oan 0#000

V 2#100 Inventory >on 20#000 10#000 " 2#100 6ash GGGGGGG GGGGGGG 100#000 100#000

!ouple of points before we e,amine what happens if you sell more shoes than you prou!e. ere we to re!ogniCe ta,es# they woul be !al!ulate on the L#200 profit. $he!osts of the unsol shoes are not a eu!tion " they’re an investment. If# however# their pri!e has to be marke own in orer to sell# or if they simply lose value be!ause similarshoes that are a!tually sol fet!h a lower pri!e# then that e!line in pri!e is eu!te from profit (as well as in the balan!e sheet). e’ll eal with losses in the last se!tion of this!hapter.

&kay# let’s move on to the reverse situation# taking the balan!e sheet above as the starting point. s you sol only 1200 pairs last year# you e!ie to prou!e that amount this year#with the K0 pairs in inventory there /'ust in !ase. Surprisingly# though# your sales revert ba!k to 12K0. Bow o we hanle this3 ;asy " 'ust the opposite of the previous !ase.:evenue is LK,12K0. 6&<S is base on the 12K0 pairs a!tually sol. So# o the!al!ulations as in -igure 1Q# but with 12K0 units. -i,e !osts are# of !ourse# un!hange#so that profits e+ual #K0. ssuming again no earnings retaine# book value isun!hange. >ut the balan!e sheet !ertainly looks ifferent " the inventory is gone. =et’se,amine what happene by oing something analysts !all /follow the !ash.

Bow mu!h !ash !ame in3 LK,12K0 N1#2K0. Bow mu!h !ash went out3 ell# you only pai the variable !osts of J2 on 1200 pairs# or K0#J00. In!luing the 21#J00 in fi,e!osts# 1#N00 went out the oor. $hat leaves N1#2K0 " 1#N00 Q#JK0. >ut there is only#K0 in profit. here’s the 2#1003 $hat !ash is not profit. It’s simply the K0 pairs of

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 32/43

shoes in inventory# value at a !ost of K0,J22#100# that was li+uiate# or turne into!ash. hi!h# you see# is e,a!tly the opposite of how we treate the previous !ase.=ooking at -igure 110# the new balan!e sheet removes the inventory an as ba!k the2#100 in !ash# so that the balan!e sheet is ba!k to where it was.1J

Market Aalue

=et’s return to our !ompany an its analysis before we !ompli!ate things with ta,es#epre!iation# inventory an the like. It’s the en of the se!on year of operations# anyou or one of your partners " the other owners of the shoe !ompany " wants to sell someshares. >ook value per share is OKN# as above (-igure 1K). potential buyer ise,amining the !ompany. She’s looking at the first two years of results " the in!omestatements in -igures 12 an 1J an the returns on e+uity they generate for the owners.$hey look pretty goo !ompare to other investments she’s !onsiering. &ne of theowners wants to sell some or all of his interest in the !ompany. >ase on these past twoyears’ return on e+uity " an# more important# as we will see in later !hapters# base on

her assessment of the !ompany’s future profit potential an return on e+uity " she offersOK per share for the e,isting owner’s shares.1K sale is agree upon# an the shares aretransferre to the new owner. hat matters to us now is this8 the transa!tion hasestablishe a market price for the shares. ;ven though only some of the shares were sol#we know that the market " as manifeste in the most re!ent transa!tion of shares in the!ompany " now values ea!h share at OK. $he !ompany’s book value is OKN#000# whileits market value is OK#000 (the number of shares " 1#000 " has not !hange ue to thetransa!tion). $he ratio of market value to book value is KRKN 1.2Q. e will see in later !hapters that this is an e,tremely important ratio for investors. %ow# though# we’ll!on!entrate on the market value on its own.

itional Share Issuan!e

9ou now want to e,pan your !ompany. $he first two years were goo# an you thinkyou !an sell a lot more shoes. Maybe you want to introu!e a new style# maybe you 'ustwant to open more lo!ations. ;ither way# you nee more e+uipment# material# et!. 9ouissue 1#000 aitional shares. Some are sol to e,isting investors# who are happy withthe performan!e thus far an wish to invest more# some to new investors who see anattra!tive new opportunity. t what pri!e3 %ot OK0Rshare# the original per share pri!e.&f !ourse not " you have two years of profits an retaine earnings to show. %ot even atOKNRshare. :ather# OKRshare# whi!h is the pri!e at whi!h shares !hange hans re!ently " the market price. 9our !ompany now has 1#000,OK OK#000 in aitional e+uity.>efore you spen the money on e,paning your operations# let’s take a look at the new balan!e sheet# -igure 111 (-igure 1K with the aitional shares issue).

-igure 111>alan!e Sheet with itional Share Issuan!e

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 33/43

ssets =iabilities

K0#000 ;+uipment ;+uity KN#000 V K#000

J0#000 Material >ank =oan 0#000 1N#000 V K#000 6ash >on 20#000

GGGGGGG GGGGGGG 1N#000 1N#000

$he new book value is OKN#000VOK#000 O1#000. Market value e+uals 2#000,OK O1K0#000. -igure 112 !ompares the situations prior to an following the aitionale+uity issuan!e# both after your se!on year of operations. %oti!e that although the

number of shares have ouble# book value has more than ouble. hy3 $he originalshares were issue when the !ompany was born# at O1#000Rshare. %ow that the !ompanyhas shown its stuff# the market # e,pe!ting profits to !ontinue as 'ust e,perien!e# isvaluing it at a higher level# allowing the !ompany to issue shares more e,pensively. $henew book value per share is the average of the book an market values per share prior tothe issuan!e of new shares. =ooke at another way# the original investors or shareholershave moneti$ed their shares. Selling new shares has establishe a market value for allshares.1L

-igure 112>ook an Market Aalues8 before an fter itional Share Issuan!e

>efore fterShares 1#000 2#000>ook Aalue KN#000 1#000>ook Aalue per Share KN LL.KMarket Aalue K#000 1K0#000Market Aalue per Share K KMarket AalueR>ook Aalue 1.2Q 1.12N

=et’s look at the key ratio# :&;# now that there is more e+uity in your firm. s your!ompany stans now# that is# base on the past year’s earnings (-igure 1J)# return one+uity is 10#22KR1#000 .LQP# a far !ry from the 20.JKP that the se!on year’sresults returne to the owners. Similarly# earnings per share e+uals OK.11# half of what itwas before you ouble the number of shares. $his is known as /ilution. -ollowingissuan!e of new shares# the !onvention is to take the most re!ent earnings figures an perform !al!ulations base on the new book value or number of shares. hy o we look

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 34/43

at the most re!ent earnings3 It’s the past " isn’t the past over4 >e!ause that’s all we haveto go on. 6learly# the very purpose of issuing aitional shares an raising !apital is toincrease earnings4 So# let’s o some forwar looking# rather than ba!kwar looking#analysis.

9our !ompany now has O1N#000 worth of !apital (e+uity plus ebt) to work with#!ompare to the O100#000 at the start of the year. &bviously# you in’t issue new shares(nor i you retain earnings) in orer to keep all the pro!ees in !ash. =et’s assume you pur!hase aitional shoe manufa!turing e+uipment an buy material proportionately# thatis# NP more of ea!h. 9our assets now !onsist of OQ1#K00 in e+uipment# O#200 ofmaterial an O1N#00 !ash. 9ou also rent more manufa!turing spa!e# so your rent rises toO2#QJ0 from O1N#000. =et’s assume your e,pansion works out 'ust as planne " you sellNP more pairs of shoes (1.N,1K)# at the original pri!e. 9our new in!ome statementis -igure 11 (interest !ost is un!hange as you haven’t in!urre any aitional ebt).

-igure 11

In!ome Statement after ;,pansion

:evenue8 LK , 2#K1L 1L#KJ0

Aariable !osts8 J2 , 2#K1L 10K#L2 Debt servi!e #J00

:ent 2#QJ0

*rofits 21#K2N

*rofits have more than ouble.1 =et’s break this own using the Dupont analysis8

:&; 21#K2N R 1#000 1L.1NP

21#K2N R 1L#KJ0 , 1L#KJ0 R 1N#000 , 1N#000 R 1#000

profit margin turnover leverage

.11L , .NQL , 1.L

:&; the year before the e,pansion before was 20.JKP 11JJ , .NQJ , 2. hy therop3 =et’s !ompare !omponents. *rofit margin is up somewhat be!ause interest payments are un!hange. $he turnover ratio is inta!t# refle!ting our assumption that salese,pane !on!omitantly (NP) with the in!rease in assets. So what i it3 :eu!eleverage. 9ou relie totally on e+uity to e,pan your firm’s operations. >y in!reasingthe e+uity base# the higher profit is sprea over more shareholers. n you i this inthree ways8

1. :etaine earnings. $he ON#000 is effe!tively aitional e+uity issuan!e.

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 35/43

2. %ew shares. Sure profit has risen# but it has to be share by more !laimants.

. ;a!h new share ae OK (market value) in e+uity# not OK0 (original bookvalue). So the /sharing of profits on a ollar basis is even more pronoun!e.

itional >orrowing

n alternative way to e,pan your s!ale of operations is by issuing ebt. :ather than sellnew shares# borrow more from banks or sell aitional bons. $his woul in!reaseleverage an raise :&;. &r# split the !apital raising into ebt an e+uity# keeping theleverage ratio inta!t an preventing the e!line in :&;. In fa!t# were we to re!ogniCeta,es# an ae benefit is the ta, eu!tibility of interest payments to the ebtholers.So# what’s the ownsie in oing it this way3 <reater risk. 9ou !an’t be sure that you’llsell the e,tra shoes you’re prou!ing# hen!e there may not be enough money to payinterest after the variable !osts are met. (9ou on’t fa!e this risk shareholers " you have

no !ontra!tual obligation to pay iviens.) In fa!t# this very possibility " an# as we’veseen above# the more volatile the prou!t the greater the !han!e of this o!!urring " !auses bon investors to eman higher interest rates than you’re paying on the e,isting ebt.-urthermore# to the e,tent the e,isting bank loans an bons nee to be refinan!e ontheir maturity ates# their interest rates will rise as well.1N

=osses

1. It’s unrealisti! to suppose that a startup !ompany su!h as the one we’ve!on!o!te will be able to issue a bon in the market. s a theoreti!ale,er!ise to tea!h you prin!iples# we’ll take that liberty.

2. %ot e,a!tly# be!ause you on’t /owe the e+uity to anyboy other thanyourself (an your e+uityRowner partners).

. $e!hni!ally# this woul be es!ribe as variable !osts rising /linearlywith prou!tion

J. If the number of shares !hange (whi!h we e,amine later)# then iviing by the number of shares is ne!essary.

K. e’re impli!itly assuming that the !ompany’s fi,e resour!es !ana!!ommoate the in!rease in prou!tion? i.e.# that it hasn’t rea!he!apa!ity. e eal with the nee to in!rease !apa!ity later.

L. *rofit margin !al!ulate on a variable !ost basis# revenue less variable!osts ivie by revenue# or (NQ#KTK#K0)RNQ#K K.NP# is thesame as in the first year.

8/9/2019 Equity Book

http://slidepdf.com/reader/full/equity-book 36/43

. $e!hni!ally# profits !an also be istribute to owners via repur!hases ofshares an via return of !apital. e will !ome a!ross share repur!hasesan share repur!hase programs in other !onte,ts in this book. *rofitsistribution +ualifies as return of !apital if stringent re+uirements are met#

an in that !ase are not ta,e as iviens# whi!h we is!uss later in this!hapter.

N. hat about using the money to hire employees# you ask3 :emember "an this is not !ompletely intuitive# so you nee to igest this " hiring (anfiring) is part of the prou!tion pro!ess. It is not a balan!e sheet issue.$he money to pay for labor (as well as for ele!tri!ity an for materialsuse in shoe prou!tion) !omes from the sale of the shoes. e alreaytook !are of that. $his money is what’s left over after that pro!ess is!omplete# in a sense. %ow# be!ause funs spent on labor# materials# et!. isuse before money is re!eive from shoe sales# the finan!ial managers

may e!ie to keep more in !ash. $hat !ash# of !ourse# is on the balan!esheet# as note earlier in the te,t.

N’. $his e+uality hols only if the firm oes not issue new shares. ee,amine this possibility towar the en of the !hapter.

Q. $his means the average ta, rate is e+ual to the marginal rate. ($here areno eu!tions# !reits# !arryforwars# et!.)

10. $his e,plains why firms favor /a!!elerate epre!iation. 5ner su!h ata, regime# the I:S allows a faster rate of epre!iation " for e,ample# 20P per year rather than ten. hether or not the firm a!tually repla!es whate!onomi!ally epre!iate# the ta, bill is reu!e (in the earlier years).