Embed Size (px)

Citation preview

Essar Ports Ltd.Essar Ports Ltd.

Performance Update

Q1 FY2015

Industry Update

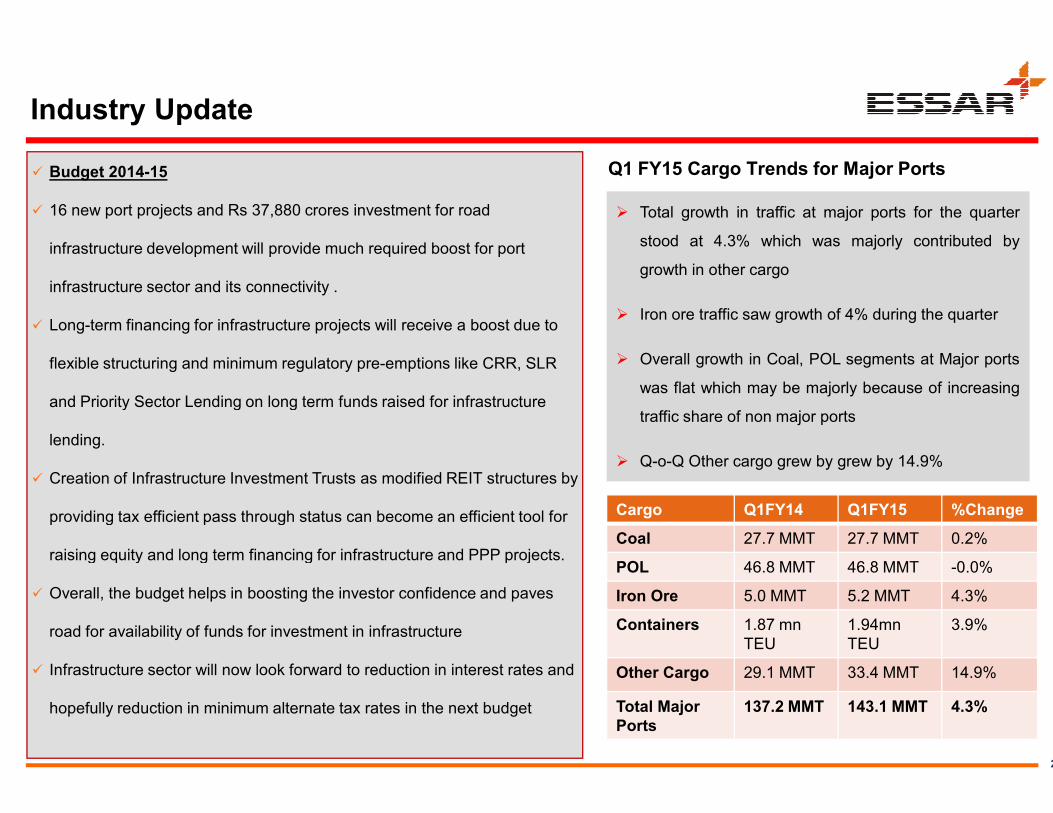

� Budget 2014-15

� 16 new port projects and Rs 37,880 crores investment for road

infrastructure development will provide much required boost for port

infrastructure sector and its connectivity .

� Long-term financing for infrastructure projects will receive a boost due to

flexible structuring and minimum regulatory pre-emptions like CRR, SLR

and Priority Sector Lending on long term funds raised for infrastructure and Priority Sector Lending on long term funds raised for infrastructure

lending.

� Creation of Infrastructure Investment Trusts as modified REIT structures by

providing tax efficient pass through status can become an efficient tool for

raising equity and long term financing for infrastructure and PPP projects.

� Overall, the budget helps in boosting the investor confidence and paves

road for availability of funds for investment in infrastructure

� Infrastructure sector will now look forward to reduction in interest rates and

hopefully reduction in minimum alternate tax rates in the next budget

� Total growth in traffic at major ports for the quarter

stood at 4.3% which was majorly contributed by

growth in other cargo

� Iron ore traffic saw growth of 4% during the quarter

� Overall growth in Coal, POL segments at Major ports

was flat which may be majorly because of increasing

Q1 FY15 Cargo Trends for Major Ports

infrastructure development will provide much required boost for port

receive a boost due to

emptions like CRR, SLR

infrastructure

2

traffic share of non major ports

� Q-o-Q Other cargo grew by grew by 14.9%

Cargo Q1FY14 Q1FY15 %Change

Coal 27.7 MMT 27.7 MMT 0.2%

POL 46.8 MMT 46.8 MMT -0.0%

Iron Ore 5.0 MMT 5.2 MMT 4.3%

Containers 1.87 mn

TEU

1.94mn

TEU

3.9%

Other Cargo 29.1 MMT 33.4 MMT 14.9%

Total Major

Ports

137.2 MMT 143.1 MMT 4.3%

infrastructure

of Infrastructure Investment Trusts as modified REIT structures by

providing tax efficient pass through status can become an efficient tool for

raising equity and long term financing for infrastructure and PPP projects.

, the budget helps in boosting the investor confidence and paves

forward to reduction in interest rates and

budget

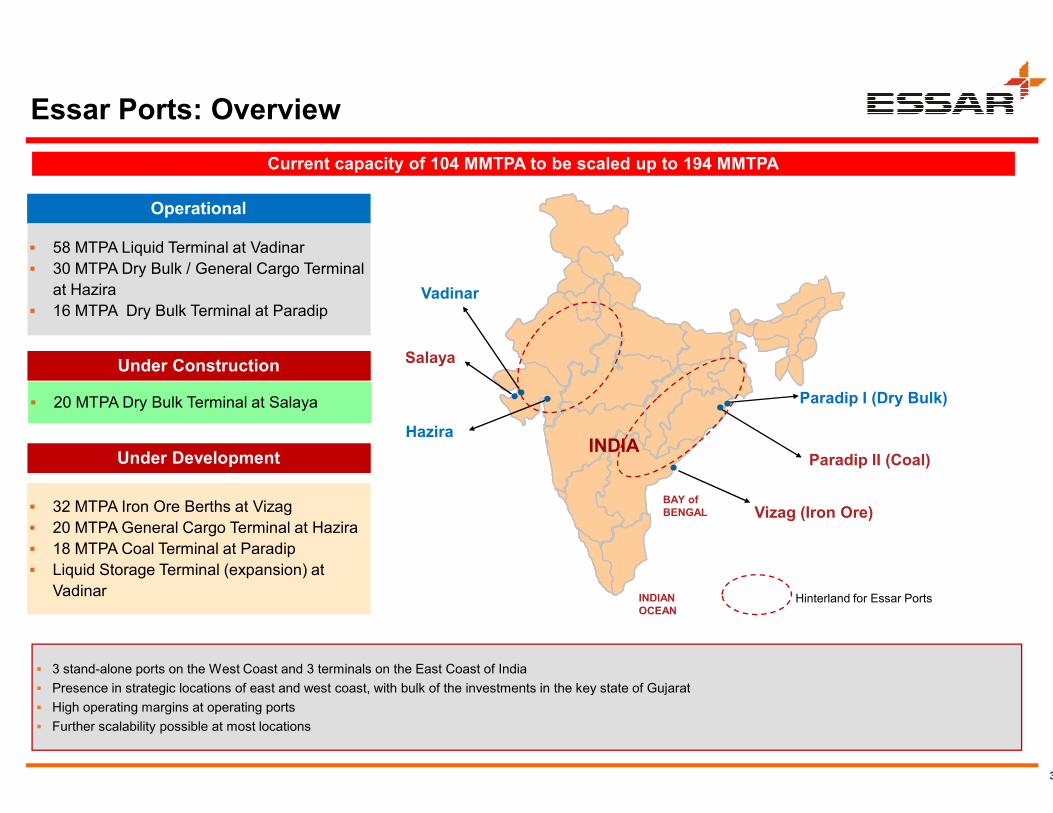

Salaya

Vadinar

� 20 MTPA Dry Bulk Terminal at Salaya

Operational

Under Construction

� 58 MTPA Liquid Terminal at Vadinar

� 30 MTPA Dry Bulk / General Cargo Terminal

at Hazira

� 16 MTPA Dry Bulk Terminal at Paradip

Current capacity of 104 MMTPA

Essar Ports: Overview

Hazira

� 20 MTPA Dry Bulk Terminal at Salaya

� 32 MTPA Iron Ore Berths at Vizag

� 20 MTPA General Cargo Terminal at Hazira

� 18 MTPA Coal Terminal at Paradip

� Liquid Storage Terminal (expansion) at

Vadinar

Under Development

� 3 stand-alone ports on the West Coast and 3 terminals on the East Coast of India

� Presence in strategic locations of east and west coast, with bulk of the investments in the key state of Gujarat

� High operating margins at operating ports

� Further scalability possible at most locations

Paradip I (Dry Bulk)

to be scaled up to 194 MMTPA

INDIA

BAY of

BENGAL

INDIAN

OCEAN

Paradip II (Coal)

Hinterland for Essar Ports

Vizag (Iron Ore)

3

alone ports on the West Coast and 3 terminals on the East Coast of India

Presence in strategic locations of east and west coast, with bulk of the investments in the key state of Gujarat

Performance Summary

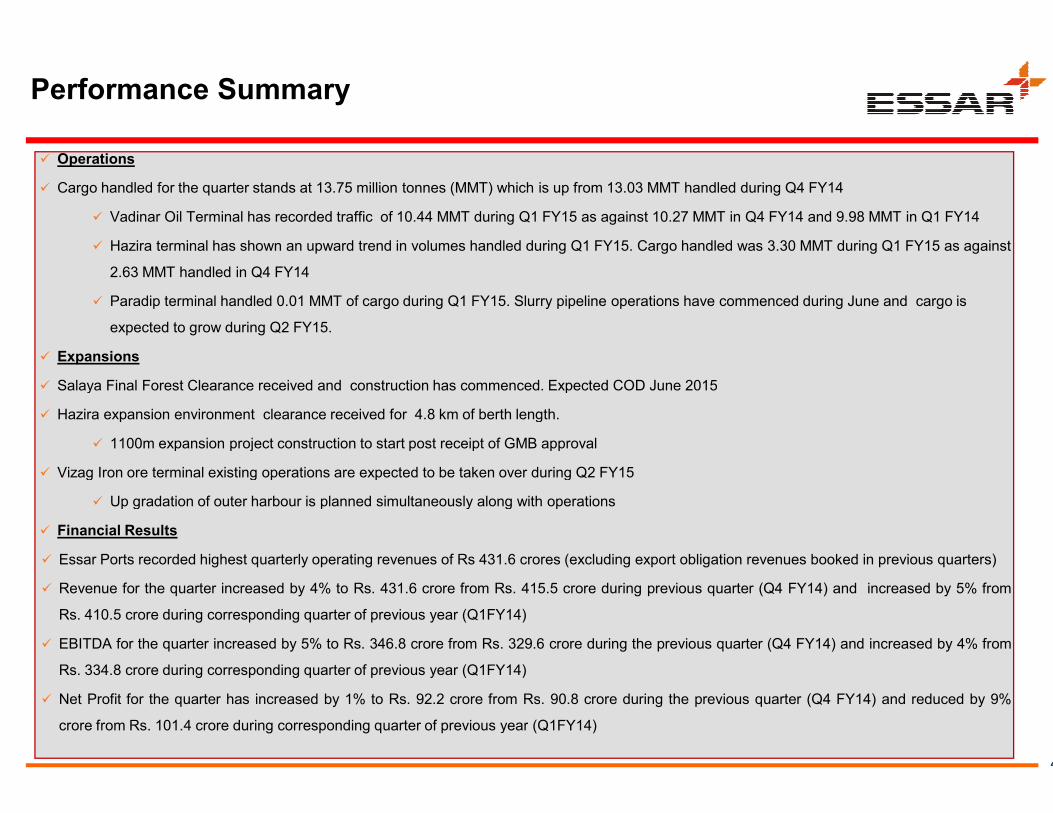

� Operations

� Cargo handled for the quarter stands at 13.75 million tonnes (MMT) which is up from 13.03 MMT handled during Q4 FY14

� Vadinar Oil Terminal has recorded traffic of 10.44 MMT during Q1

� Hazira terminal has shown an upward trend in volumes handled during

2.63 MMT handled in Q4 FY14

� Paradip terminal handled 0.01 MMT of cargo during Q1 FY15. Slurry pipeline operations have commenced during June and cargo i

expected to grow during Q2 FY15.

� Expansions

� Salaya Final Forest Clearance received and construction has commenced. Expected COD June 2015

Hazira expansion environment clearance received for 4.8 km of berth length.� Hazira expansion environment clearance received for 4.8 km of berth length.

� 1100m expansion project construction to start post receipt of GMB approval

� Vizag Iron ore terminal existing operations are expected to be taken over during Q2 FY15

� Up gradation of outer harbour is planned simultaneously along with operations

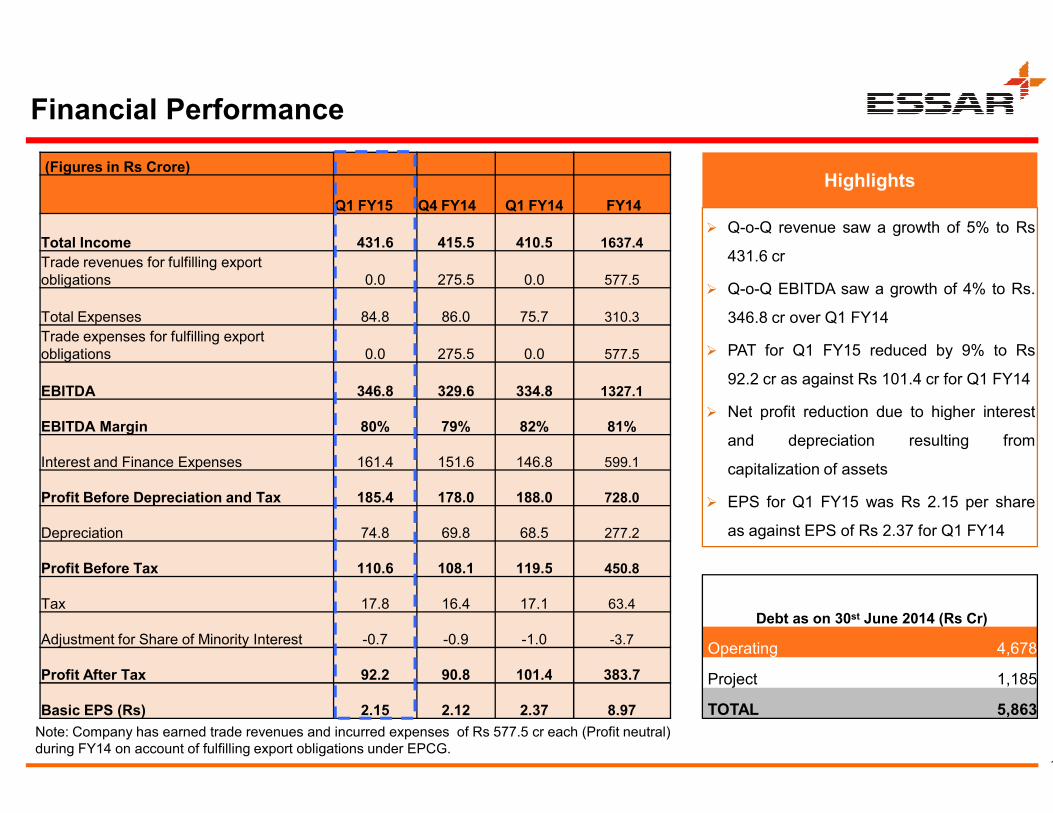

� Financial Results

� Essar Ports recorded highest quarterly operating revenues of Rs 431.6 crores

� Revenue for the quarter increased by 4% to Rs. 431.6 crore from Rs. 415

Rs. 410.5 crore during corresponding quarter of previous year (Q1FY14)

� EBITDA for the quarter increased by 5% to Rs. 346.8 crore from Rs. 329

Rs. 334.8 crore during corresponding quarter of previous year (Q1FY14)

� Net Profit for the quarter has increased by 1% to Rs. 92.2 crore from Rs

crore from Rs. 101.4 crore during corresponding quarter of previous year

Cargo handled for the quarter stands at 13.75 million tonnes (MMT) which is up from 13.03 MMT handled during Q4 FY14

during Q1 FY15 as against 10.27 MMT in Q4 FY14 and 9.98 MMT in Q1 FY14

has shown an upward trend in volumes handled during Q1 FY15. Cargo handled was 3.30 MMT during Q1 FY15 as against

Paradip terminal handled 0.01 MMT of cargo during Q1 FY15. Slurry pipeline operations have commenced during June and cargo is

Salaya Final Forest Clearance received and construction has commenced. Expected COD June 2015

Hazira expansion environment clearance received for 4.8 km of berth length.

4

Hazira expansion environment clearance received for 4.8 km of berth length.

1100m expansion project construction to start post receipt of GMB approval

Vizag Iron ore terminal existing operations are expected to be taken over during Q2 FY15

Up gradation of outer harbour is planned simultaneously along with operations

crores (excluding export obligation revenues booked in previous quarters)

415.5 crore during previous quarter (Q4 FY14) and increased by 5% from

329.6 crore during the previous quarter (Q4 FY14) and increased by 4% from

Rs. 90.8 crore during the previous quarter (Q4 FY14) and reduced by 9%

year (Q1FY14)

Key Highlights

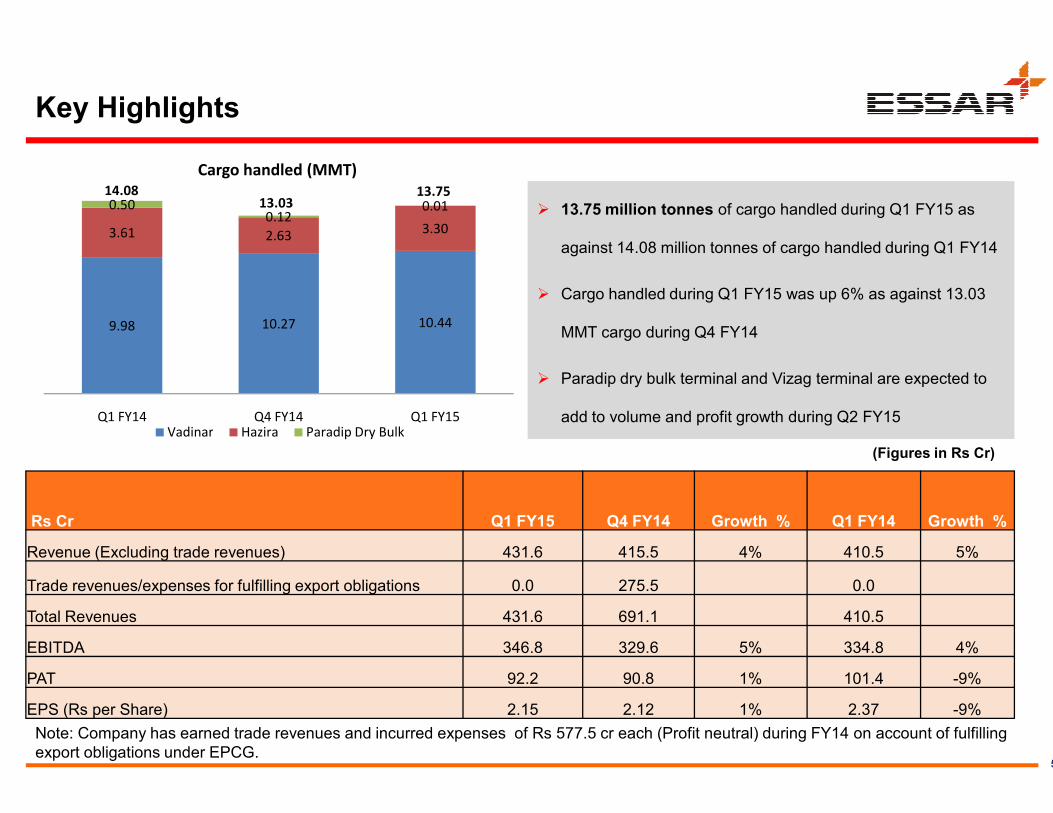

9.98 10.27 10.44

3.61 2.633.30

0.500.12

0.01

Cargo handled (MMT)

14.0813.03

13.75

Note: Company has earned trade revenues and incurred expenses of

export obligations under EPCG.

Rs Cr Q1 FY15

Revenue (Excluding trade revenues) 431.6

Trade revenues/expenses for fulfilling export obligations 0.0

Total Revenues 431.6

EBITDA 346.8

PAT 92.2

EPS (Rs per Share) 2.15

Q1 FY14 Q4 FY14 Q1 FY15Vadinar Hazira Paradip Dry Bulk

� 13.75 million tonnes of cargo handled during Q1 FY15 as

against 14.08 million tonnes of cargo handled during Q1 FY14

� Cargo handled during Q1 FY15 was up 6% as against 13.03

MMT cargo during Q4 FY14

� Paradip dry bulk terminal and Vizag terminal are expected to

5

(Figures in Rs Cr)

Note: Company has earned trade revenues and incurred expenses of Rs 577.5 cr each (Profit neutral) during FY14 on account of fulfilling

add to volume and profit growth during Q2 FY15

Q1 FY15 Q4 FY14 Growth % Q1 FY14 Growth %

431.6 415.5 4% 410.5 5%

0.0 275.5 0.0

431.6 691.1 410.5

346.8 329.6 5% 334.8 4%

92.2 90.8 1% 101.4 -9%

2.15 2.12 1% 2.37 -9%

Asset-wise Highlights

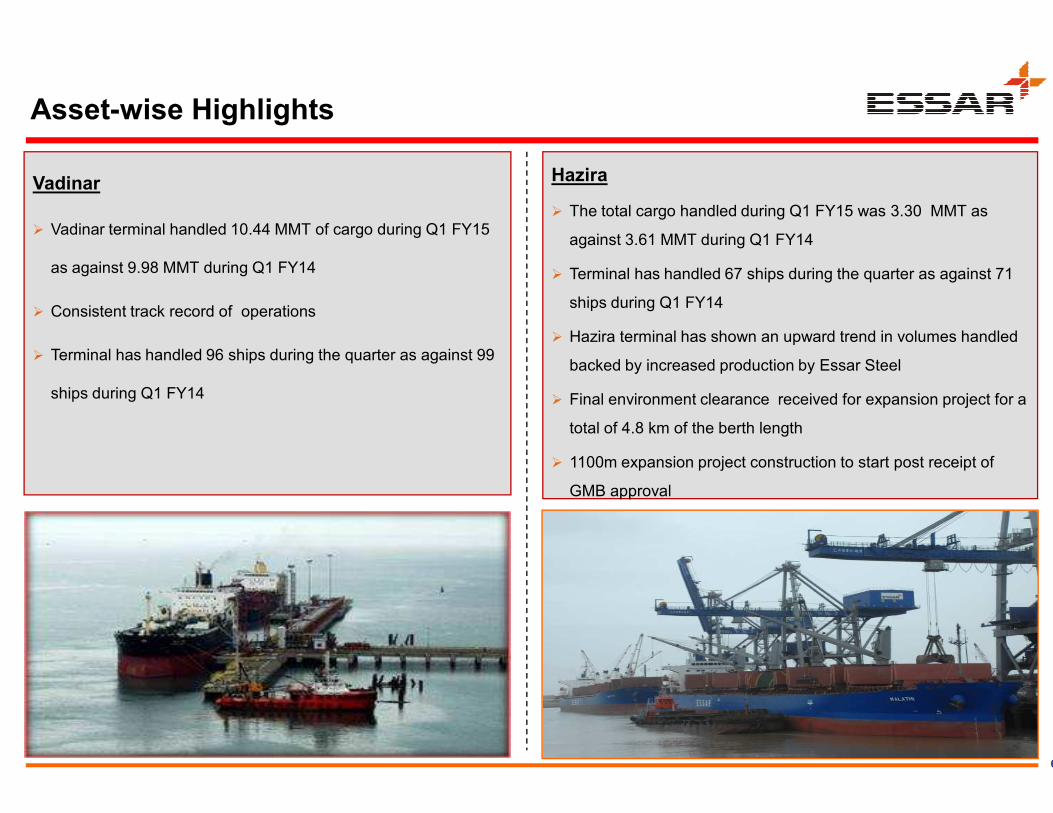

Vadinar

� Vadinar terminal handled 10.44 MMT of cargo during Q1 FY15

as against 9.98 MMT during Q1 FY14

� Consistent track record of operations

� Terminal has handled 96 ships during the quarter as against 99

ships during Q1 FY14

Hazira

� The total cargo handled during Q1 FY15 was 3.30 MMT as

against 3.61 MMT during Q1 FY14

� Terminal has handled 67 ships during the quarter as against 71

ships during Q1 FY14

� Hazira terminal has shown an upward trend in volumes handled

backed by increased production by Essar Steel

� Final environment clearance received for expansion project for a

6

� Final environment clearance received for expansion project for a

total of 4.8 km of the berth length

� 1100m expansion project construction to start post receipt of

GMB approval

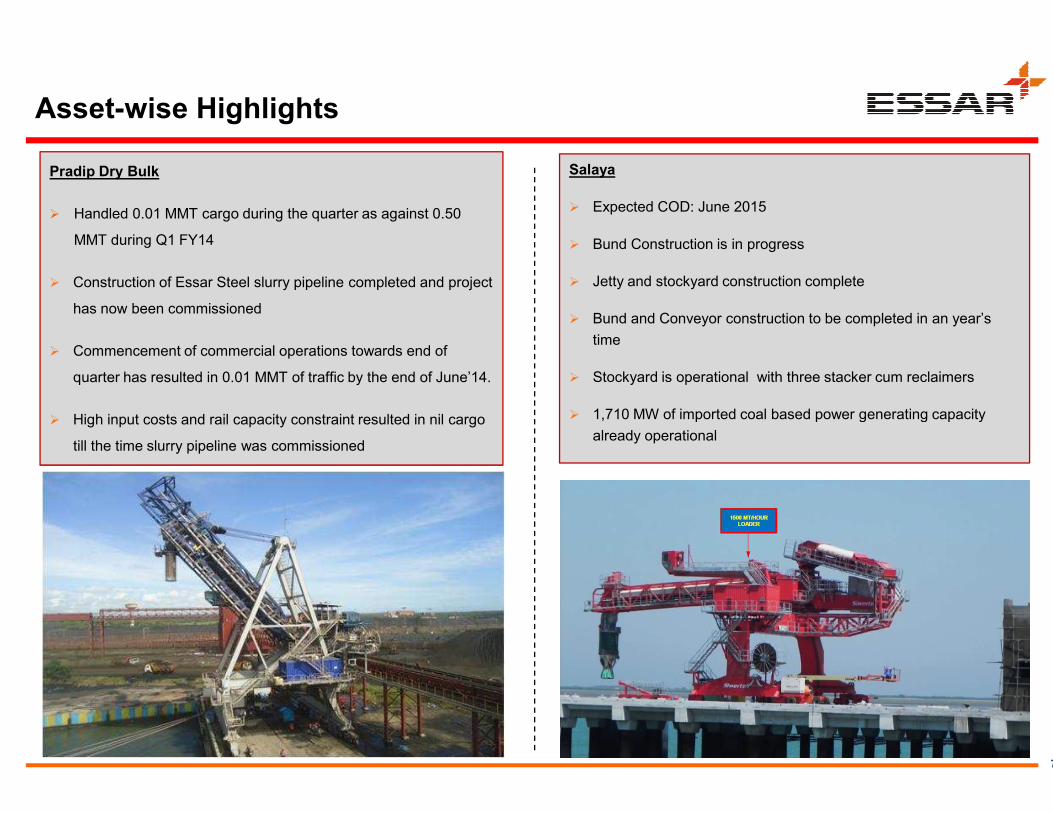

Pradip Dry Bulk

� Handled 0.01 MMT cargo during the quarter as against 0.50

MMT during Q1 FY14

� Construction of Essar Steel slurry pipeline completed and project

has now been commissioned

� Commencement of commercial operations towards end of

quarter has resulted in 0.01 MMT of traffic by the end of June’14.

Asset-wise Highlights

� High input costs and rail capacity constraint resulted in nil cargo

till the time slurry pipeline was commissioned

Salaya

� Expected COD: June 2015

� Bund Construction is in progress

� Jetty and stockyard construction complete

� Bund and Conveyor construction to be completed in an year’s

time

� Stockyard is operational with three stacker cum reclaimers

1,710 MW of imported coal based power generating capacity

7

� 1,710 MW of imported coal based power generating capacity

already operational

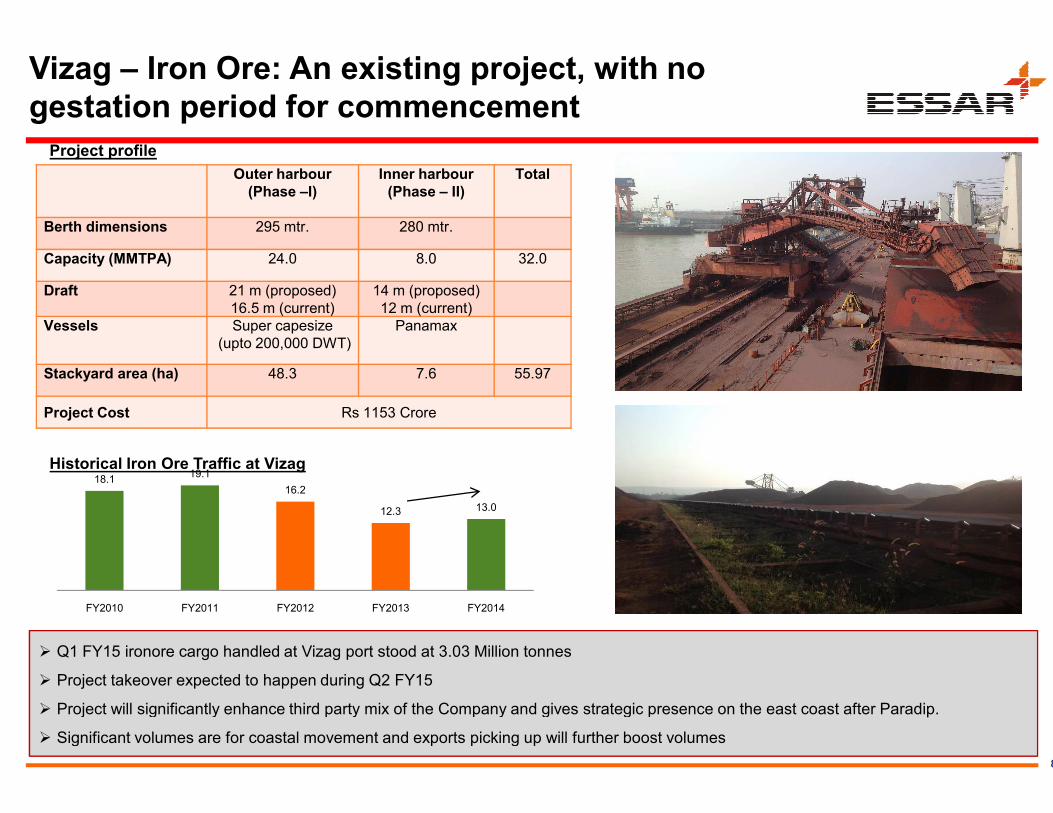

Vizag – Iron Ore: An existing project, with no

gestation period for commencement

Outer harbour

(Phase –I)

Inner harbour

(Phase – II)

Total

Berth dimensions 295 mtr. 280 mtr.

Capacity (MMTPA) 24.0 8.0 32.0

Draft 21 m (proposed)

16.5 m (current)

14 m (proposed)

12 m (current)

Vessels Super capesize

(upto 200,000 DWT)

Panamax

Stackyard area (ha) 48.3 7.6 55.97

Project Cost Rs 1153 Crore

Project profile

Project Cost Rs 1153 Crore

Historical Iron Ore Traffic at Vizag

� Q1 FY15 ironore cargo handled at Vizag port stood at 3.03 Million tonnes

� Project takeover expected to happen during Q2 FY15

� Project will significantly enhance third party mix of the Company and gives strategic presence on the east coast after Paradi

� Significant volumes are for coastal movement and exports picking up will further boost volumes

18.119.1

16.2

12.3 13.0

FY2010 FY2011 FY2012 FY2013 FY2014

Iron Ore: An existing project, with no

gestation period for commencement

Total

32.0

55.97

8

tonnes

Project will significantly enhance third party mix of the Company and gives strategic presence on the east coast after Paradip.

Significant volumes are for coastal movement and exports picking up will further boost volumes

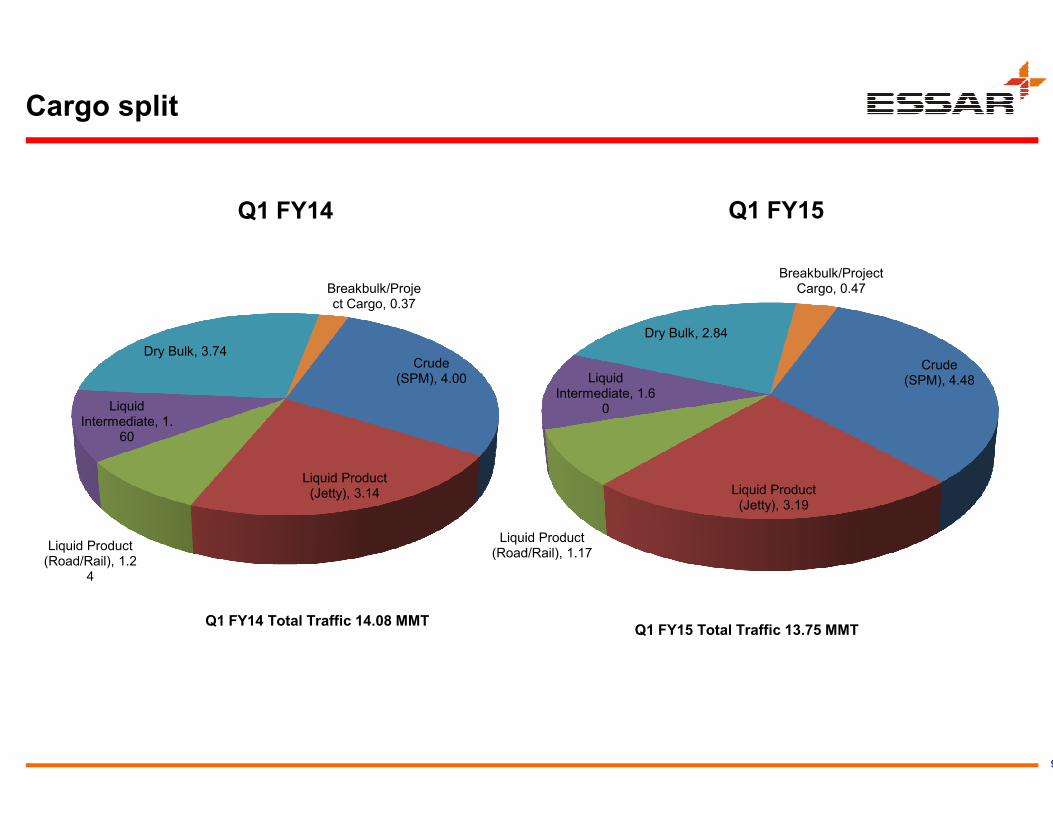

Cargo split

Q1 FY14

Crude (SPM), 4.00

Liquid

Dry Bulk, 3.74

Breakbulk/Project Cargo, 0.37

Liquid Product (Jetty), 3.14

Liquid Product (Road/Rail), 1.2

4

Liquid Intermediate, 1.

60

Q1 FY14 Total Traffic 14.08 MMT

Liquid Product (Road/Rail), 1.17

Q1 FY15

Crude (SPM), 4.48Liquid

Intermediate, 1.60

Dry Bulk, 2.84

Breakbulk/Project Cargo, 0.47

9

Liquid Product (Jetty), 3.19

Liquid Product (Road/Rail), 1.17

0

Q1 FY15 Total Traffic 13.75 MMT

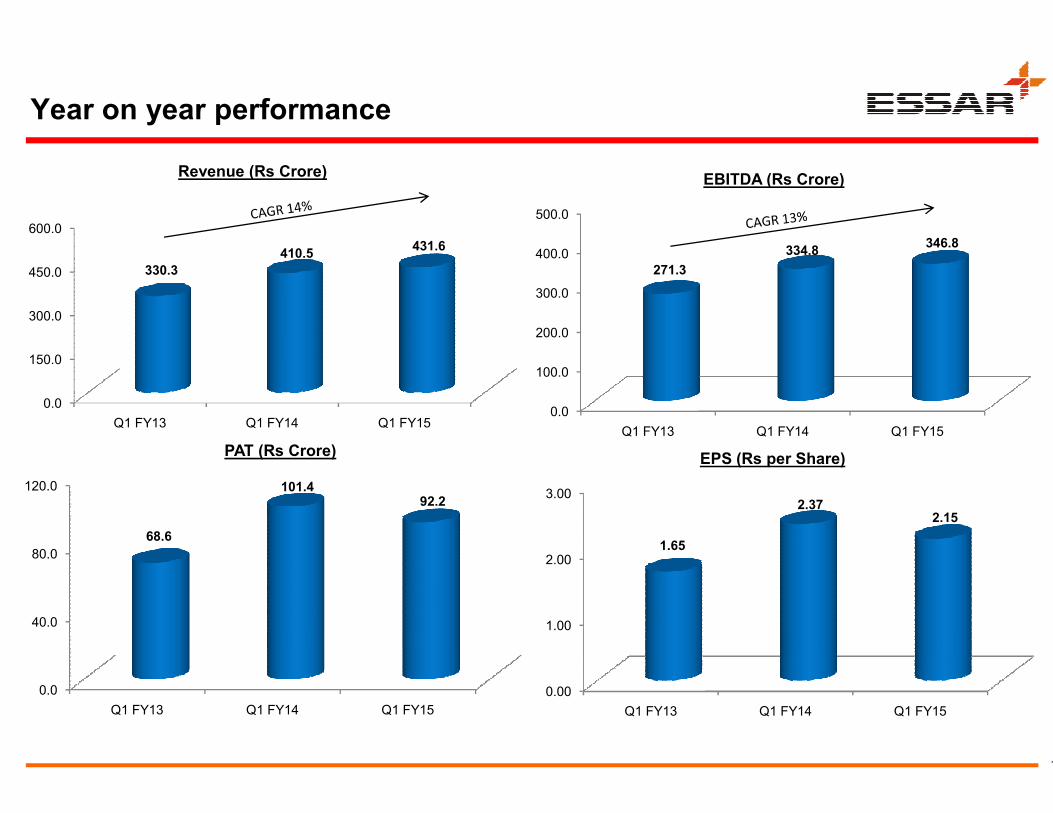

Year on year performance

0.0

150.0

300.0

450.0

600.0

330.3

410.5431.6

Revenue (Rs Crore)

0.0

Q1 FY13 Q1 FY14 Q1 FY15

0.0

40.0

80.0

120.0

Q1 FY13 Q1 FY14 Q1 FY15

68.6

101.492.2

PAT (Rs Crore)

0.0

100.0

200.0

300.0

400.0

500.0

271.3

334.8346.8

EBITDA (Rs Crore)

10

0.0

Q1 FY13 Q1 FY14 Q1 FY15

0.00

1.00

2.00

3.00

Q1 FY13 Q1 FY14 Q1 FY15

1.65

2.372.15

EPS (Rs per Share)

Financial Performance

(Figures in Rs Crore)

Q1 FY15 Q4 FY14 Q1 FY14

Total Income 431.6 415.5 410.5

Trade revenues for fulfilling export

obligations 0.0 275.5 0.0

Total Expenses 84.8 86.0 75.7

Trade expenses for fulfilling export

obligations 0.0 275.5 0.0

EBITDA 346.8 329.6 334.8

EBITDA Margin 80% 79% 82%

Interest and Finance Expenses 161.4 151.6 146.8

Profit Before Depreciation and Tax 185.4 178.0 188.0

Depreciation 74.8 69.8 68.5

Profit Before Tax 110.6 108.1 119.5

Tax 17.8 16.4 17.1

Adjustment for Share of Minority Interest -0.7 -0.9 -1.0

Profit After Tax 92.2 90.8 101.4

Basic EPS (Rs) 2.15 2.12 2.37

Note: Company has earned trade revenues and incurred expenses of Rs 577.5

during FY14 on account of fulfilling export obligations under EPCG.

� Q-o-Q revenue saw a growth of 5% to Rs

431.6 cr

� Q-o-Q EBITDA saw a growth of 4% to Rs.

346.8 cr over Q1 FY14

� PAT for Q1 FY15 reduced by 9% to Rs

92.2 cr as against Rs 101.4 cr for Q1 FY14

� Net profit reduction due to higher interest

Highlights

Q1 FY14 FY14

410.5 1637.4

0.0 577.5

75.7 310.3

0.0 577.5

334.8 1327.1

11

� Net profit reduction due to higher interest

and depreciation resulting from

capitalization of assets

� EPS for Q1 FY15 was Rs 2.15 per share

as against EPS of Rs 2.37 for Q1 FY14

Debt as on 30st June 2014 (Rs Cr)

Operating 4,678

Project 1,185

TOTAL 5,863

82% 81%

146.8 599.1

188.0 728.0

68.5 277.2

119.5 450.8

17.1 63.4

1.0 -3.7

101.4 383.7

2.37 8.97

577.5 cr each (Profit neutral)

Annexures: Terminal PhotographsAnnexures: Terminal Photographs

12

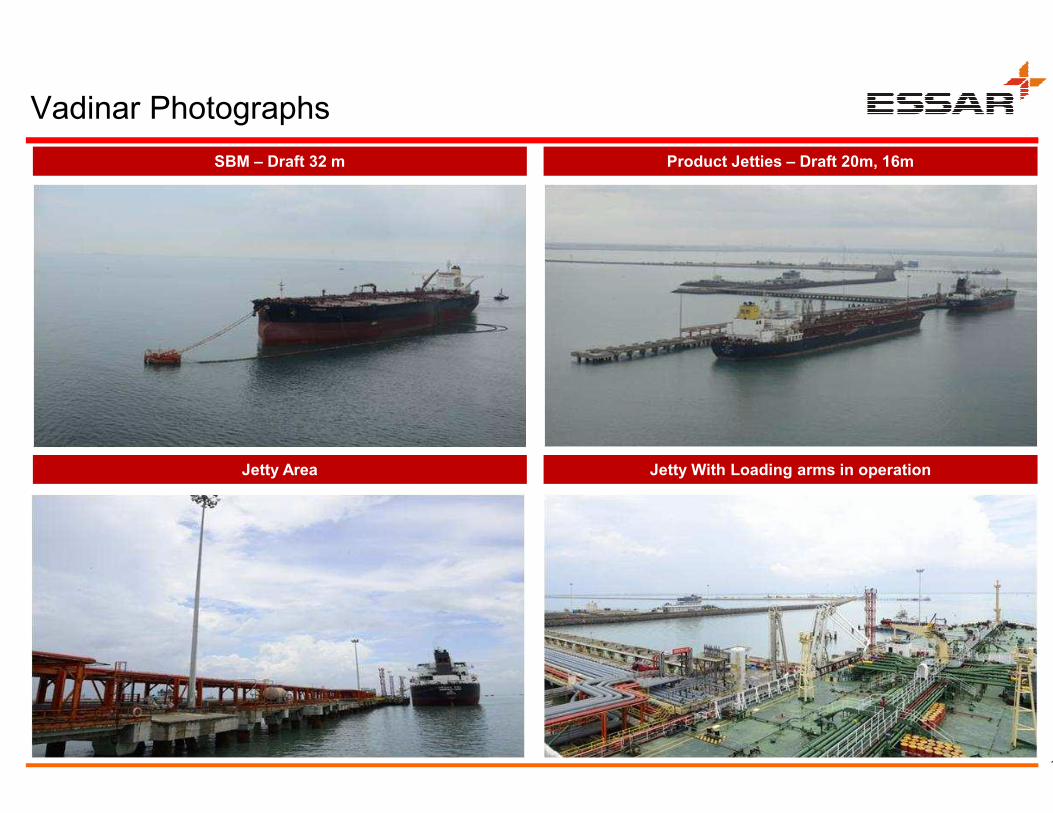

Vadinar Photographs

SBM – Draft 32 m

Jetty Area

Product Jetties – Draft 20m, 16m

Jetty With Loading arms in operation

13

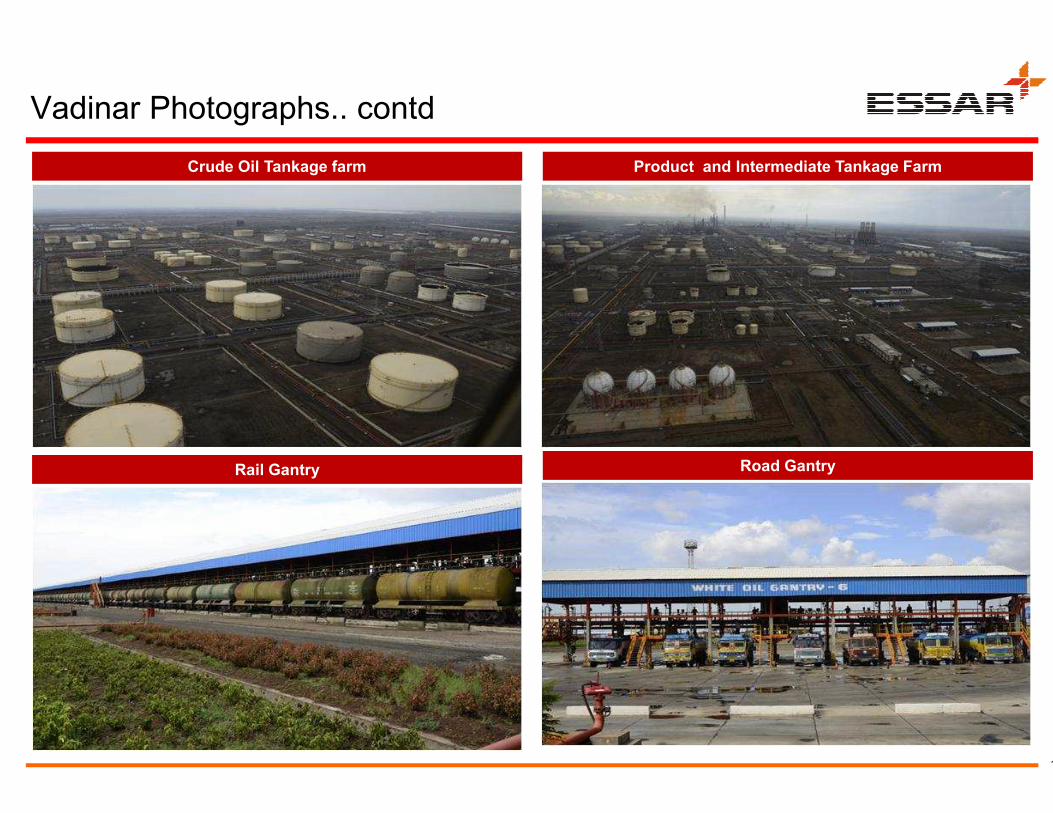

Vadinar Photographs.. contd

Crude Oil Tankage farm

Rail Gantry

Product and Intermediate Tankage Farm

Road Gantry

14

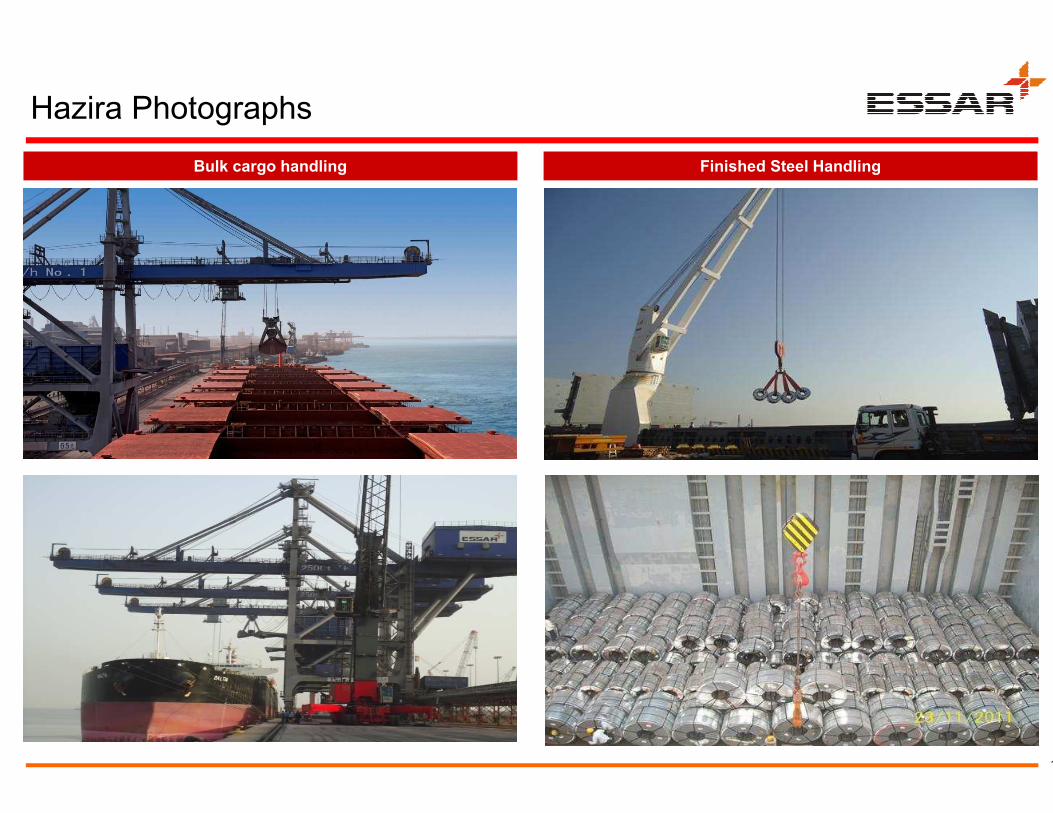

Hazira Photographs

Bulk cargo handling Finished Steel Handling

15

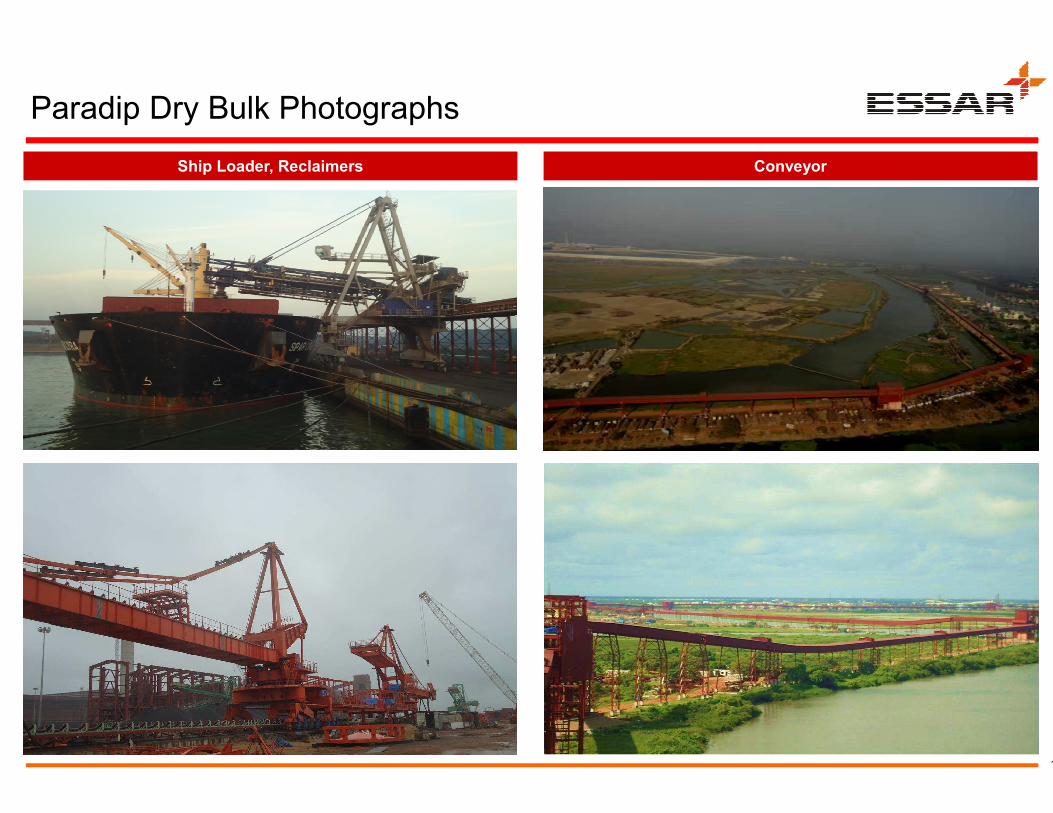

Paradip Dry Bulk Photographs

Ship Loader, Reclaimers Conveyor

16

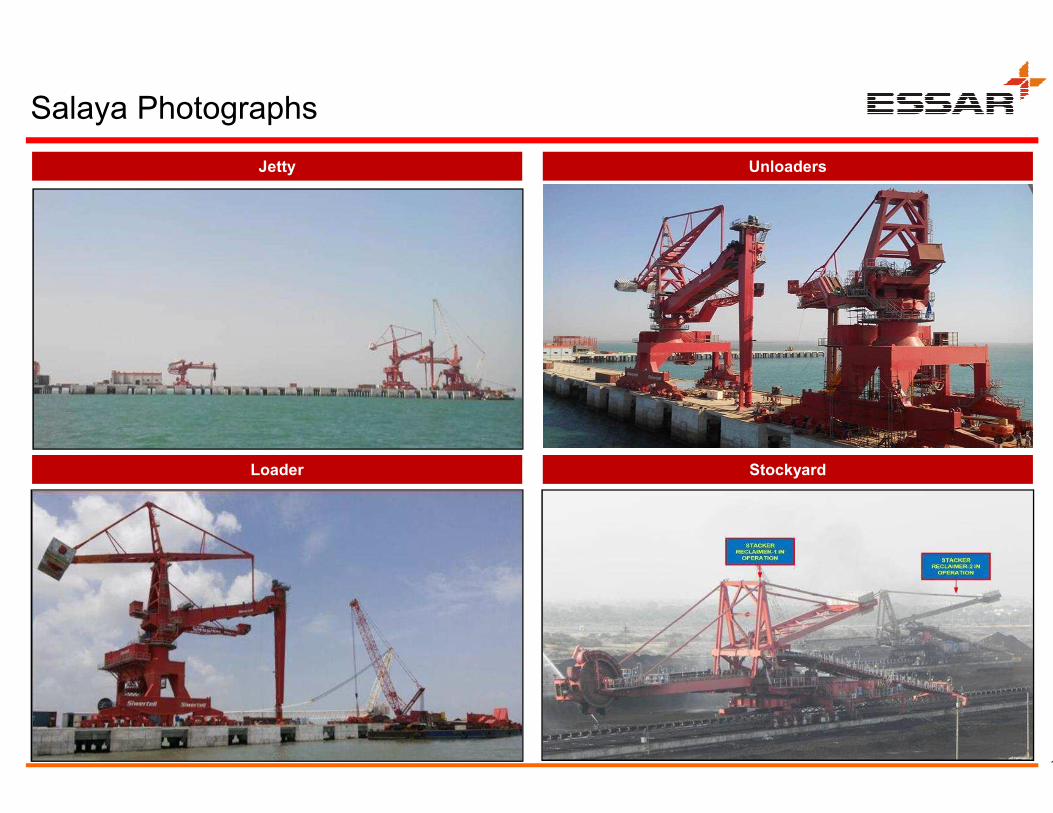

Salaya Photographs

Jetty

Loader

Unloaders

Stockyard

17

Vizag Photographs

Receipt and Wagon Tippling

Conveyors

Stockyard - Stacker

Ship Loading

18

Legal Disclaimer

“This presentation is for information purposes only and doesrespect to the purchase or sale of any security of Essar Portsand no part of it shall form the basis of or be relied upon in connection

This presentation is not a complete description of the Companyphrases that are forward looking statements. All forward-assumptions that could cause actual results to differ materiallystatement. Any opinion, estimate or projection herein constitutescan be no assurance that future results or events will be consistentinformation in this presentation is subject to change without notice,condensed and it may not contain all material information concerningdo not intend to, update or otherwise revise any statementspresentation or to reflect the occurrence of underlying events,

All information contained in this presentation has been preparedhas been independently verified by anyone else. No representationnor is any responsibility or liability of any kind accepted withinformation, projection, representation or warranty (expressedCompany nor anyone else accepts any liability whatsoever forpresentation or its contents or otherwise arising inused, reproduced, copied, distributed, shared or disseminated

The distribution of this document in certain jurisdictions maypresentation comes should inform them about, and observe, any

does not constitute an offer, solicitation or advertisement withPorts Limited (the “Company” or “EPL” or “Essar Ports Limited”)connection with any contract or commitment whatsoever.

Company. Certain statements in this presentation contain words orforward-looking statements are subject to risks, uncertainties andmaterially from those contemplated by the relevant forward lookingconstitutes a judgment as of the date of this presentation, and there

consistent with any such opinion, estimate or projection. Thenotice, its accuracy is not guaranteed, it may be incomplete or

concerning the Company. We do not have any obligation to, andstatements reflecting circumstances arising after the date of thisevents, even if the underlying assumptions do not come to fruition.

prepared solely by the Company. No information contained hereinrepresentation or warranty (express or implied) of any nature is made

with respect to the truthfulness, completeness or accuracy of any(expressed or implied) or omissions in this presentation. Neither the

for any loss, howsoever, arising from any use or reliance on thisconnection therewith. This presentation may not be

disseminated in any other manner.

may be restricted by law and persons into whose possession thisany such restrictions.”

19

![431.6 Skálholt Map · Skálholt Map #431.6 2 indigenous population]. Marked vertically on the map’s southwestern edge is the name Promontorium Winlandiae [Promontory of Vinland]](https://img.pdfslide.net/doc/110x75/5fa9700b040d74780a43e882/4316-sklholt-map-sklholt-map-4316-2-indigenous-population-marked-vertically.jpg)