Embed Size (px)

Citation preview

Ethical Issues When Working with Startups

What’s a Startup?

Everyone has their own definition. Here’s mine.

All businesses start as a startup.

But they phase out when:

>$50MM revenue (12 month, forward run rate);

>100 employees; or

>$500MM (on paper or otherwise).

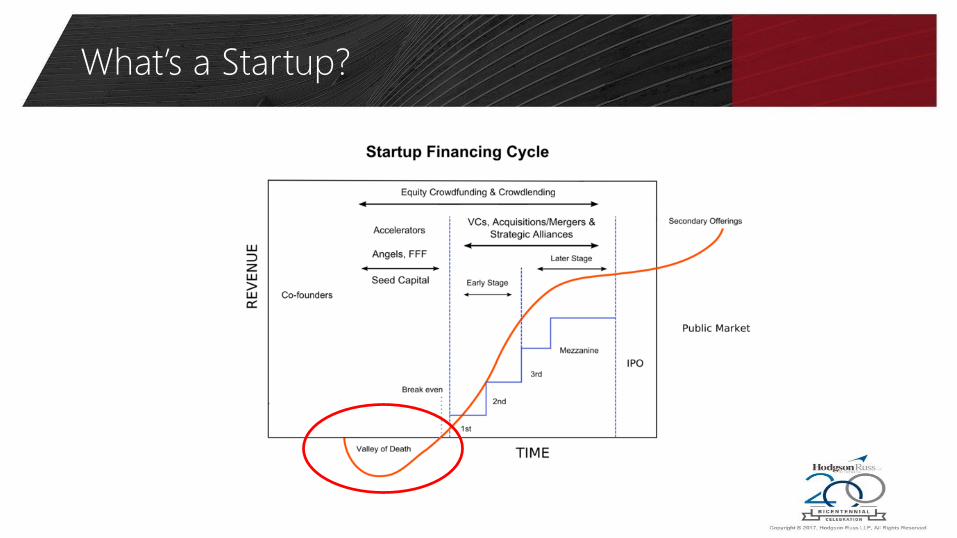

What’s a Startup?

What’s a Startup?

Startup Mentality

Lawyers tend to think too much like, well, lawyers.

Startups don’t really need lawyers.

Most startups would list legal documents last on the list

of their priorities.

Startup founders are DIY-ers.

Startup founders play fast and loose with the rules.

Startup Mentality

Cash is king, queen, and the rest of the royal family.

Lawyers as counselors and connectors.

Startups want your help to raise money.

Venture capital industry still relies on lawyers to introduce

founders to investors.

Startup Mentality

Entrepreneurs are usually a (toxic) mix of super

cocky and insecure.

While confident, they usually hear “no” much more than

“yes.”

They invest in their startup because they think they know

something that everyone else does not.

Startups and Their Lawyers

Traditional

the lone (possibly unsophisticated) founder who turns to

a lawyer to assist in forming a company, protecting

intellectual property and obtaining funding from outside

investors

Startups and Their Lawyers

New Normal

founders (often in groups) utilize form agreements and

software to set up companies and turn to lawyers later in

the process

companies may obtain funding through crowd funding

websites or angel investors, often without the

involvement of counsel

Lawyers and Then Some

As a startup lawyer, you might end up doing quite a

bit of work that is not technically legal, but still adds

value.

Reviewing pitch decks

Making introductions

Experiential advice

Lawyers as Investors

Investments of time and energy.

Deferred fees plus everything you can to keep costs low.

Some lawyers ask for warrants or options in the company

and my experience is that most startups find that request

flattering.

If someone wants equity in a startup company, it’s

because they believe in the idea and the team.

Duties, Representation, and

Scope

Duties as a Lawyer

A lawyer owes certain duties to a client, including

duties of confidentiality, loyalty, communication,

and competence.

These duties typically arise at the commencement

of an attorney-client relationship.

When Representation Begins

When the circumstances are relatively informal or

the commencement of the relationship is not clearly

defined, it can be difficult to determine exactly

when the representation began.

The lawyer’s understanding of when that occurred

may be different than the client’s.

When Representation Begins

Attorney-client relationship can start well before any agreement is reached between the attorney and client.

Attorney-client relationship may be created either through an express agreement or may be implied by the parties’ conduct: whether the attorney volunteered services;

whether the potential client disclosed confidential information;

whether the potential client reasonably believed he or she was consulting the attorney in a professional capacity;

whether the potential client sought legal advice;

whether the attorney indicated that he or she was representing the client; and

the amount of contact between the two.

When Representation Begins

Payment of fees will be a factor supporting the

existence of the relationship, but a fee agreement is

not required to establish an attorney-client

relationship.

However, a would-be client’s consultation of the

lawyer in a non-legal capacity (such as a consultant)

would not create an attorney-client relationship.

When Representation Begins

Discussing legal matters with startup founders or entrepreneurs in relatively informal settings, including through online contacts, should use caution.

While an attorney may provide general information without creating an attorney-client relationship, an attorney’s detailed discussion of the legal implications of a particular person’s (or company’s) situation or options may be enough to create a relationship, depending on the facts.

When Representation Begins

To minimize that risk, attorneys who provide online resources such as formation documents or financing templates should include disclaimers that make clear that by providing the forms, the attorney is not intending to create an attorney-client relationship, is not providing legal advice, that any use of the forms is at the user ’s own risk, and recommend that the user consult an attorney.

Representation Scope

It is ethically permissible for a lawyer to provide a limited scope of representation. Assisting a startup client with intellectual property advice

but not assisting in corporate formation or stock issuance.

However, any such limitation on the scope of a lawyer’s services must be reasonable and must be clearly spelled out to the client.

Representation Scope

Additionally, even in a limited-scope representation,

the attorney has a duty to advise the client of

reasonably apparent legal problems, even if outside

the narrow scope of the services the lawyer has

agreed to provide.

Startup Representation

Two founders may want to hire one attorney to form the corporation, draft a shareholder agreement between them and review a lease that the corporation is about to enter into.

That makes for three clients, each of the founders and the corporation.

Even if all interests are aligned at the moment, conflicts between the parties could arise at any point in time.

Startup Representation

Lawyers representing startups need to be very clear

from the outset whom they represent, and to make

expressly clear the client’s identity to those involved

in the matter.

If the lawyer represents the company, the lawyer’s

duties are owed to the company and not to

individual constituents such as officers or directors.

Startup Representation

This concept may not be clear to a founder who closely identifies with the company, has hired the lawyer and has been the primary contact with the lawyer.

For that reason, lawyers need to make the identity of the client explicit from the outset, including in the representation agreement and other initiation documents.

Startup Representation

The lawyer should explain whenever appropriate that the client is the organization and not the founders (or anyone else).

A lawyer has an obligation to explain the identity of the client when, in dealing with constituents of the organization, it becomes apparent that the organization’s interests may become adverse to the interests of the constituent.

Startup Representation

If a lawyer decides to represent more than one client (for example, joint representation of founders, or a company and its investors), it is very important that the clients are fully informed of the risks of such joint representation, and consent to those risks.

In the formation stage of a startup, the people involved may not understand that they have at least potentially conflicting interests, especially when they believe that they have a shared vision for the new company.

It is important to make clear to such clients that in fact their interests potentially conflict, especially with regard to shareholder plans, allocation of shares and options, and agreements that govern management and control, and they may want separate legal advice to best protect their own individual interests.

Equity in a Startup

Why Take Equity?

In 1999, the well-known Silicon Valley law firm Wilson Sonsini Goodrich & Rosati took stock as part of its compensation for legal services rendered in connection with the initial public offering transactions of thirty-three of the fifty-three companies that the firm represented in IPO transactions that year.

Wilson Sonsini’s holdings in twenty-four of those fifty-three companies were valued in excess of $1 million each at the close of the first day of trading.

This investment practice is not limited to Wilson Sonsini. Indeed, Wilson Sonsini’s cross-town rival, Cooley LLP, also reportedly made lavish returns on its equity investments in law firm clients.

Why Take Equity?

Bill Fenwick of Fenwick & West, who turned down shares in Apple Computer's IPO: [W]e incorporated Apple Computer and represented them

exclusively for a number of years. At one point, at a very young point in their development, they wanted us to take $50,000 off of our fees in stock. And, quite frankly, I had come from the East and . . . there are a host of problems you've got to deal with if you're going to do that. Well, that $50,000 that they wanted us to take in stock was worth $12 million when they went public, so that is a pretty humbling experience.

Equity Positions in Startups

Under certain circumstances, lawyers may have opportunities to invest in their startup clients.

For example, lawyers may take a stake in the venture in lieu of their fees, since the client may be cash-strapped but in need of legal services.

Similarly, lawyers may take an ownership stake in a patent or other intellectual property in lieu of fees, a practice expressly allowed under the newly adopted USPTO rules of professional conduct. See USPTO Rule 11.108(i), 37 C.F.C. §11.108.

Some law firms may invest in their clients by purchasing shares or options on the same terms as other “insider” investors; this may be done through an investment entity or venture fund formed by the law firm.

Equity Positions in Startups

Investing in clients provides a competitive edge for a law firm. “From the client’s perspective, the lawyer’s willingness to invest with entrepreneurs in a startup company frequently is viewed as a vote of confidence in the enterprise’s prospects.” (“ABA Formal Opin. 00-418”).

Further, a law firm’s willingness to invest in an enterprise may provide an additional boost of capital for the firm (if the law firm is investing cash as opposed to providing services in exchange for stock) or as a way to provide legal services the client could not otherwise afford.

Equity Positions in Startups

The most significant ethical concern created by attorneys investing in clients is the potential conflict between the lawyer’s financial interest and the client’s interests: transactions must be “fair and reasonable to the client,” with the

terms fully disclosed in writing in a manner which the client reasonably should understand;

the attorney advise the client of the right to seek the advice of independent counsel, and give the client a reasonable opportunity to do so; and

the client thereafter consent in writing.

Equity Positions in Startups

ABA Formal Ethics Opinion 00-418 looked at the ethics of attorneys investing in clients. The opinion set forth certain conditions that must be satisfied in a stock-for-fees scenario. The lawyer must: explain the transaction so that the client can understand its terms as well as its potential

effect on the lawyer-client relationship;

describe the scope of services to be performed in exchange for the stock, and must set forth whether the lawyer may retain the stock if the attorney-client relationship ends before all the agreed-upon services are performed;

disclose to the client that conflicts could arise that could affect the lawyer’s exercise of independent professional judgment, including where the lawyer’s desire to protect the value of the stock may conflict with the client’s goals;

inform the client that, because of these conflicts, the client should consult an independent lawyer concerning whether to enter into the transaction; and

that should conflicts arise after the stock is issued, that the disclosing lawyer may need to withdraw.

Equity Positions in Startups

The question of the fairness of the transaction is one that requires attention and possible documentation.

Under both sets of rules, the fairness of a transaction between a lawyer and a client is determined as of the time that the transaction was entered into.

In some cases, it may be hard to value the stock (or other interest) at the time it was exchanged.

If the value significantly increases over time, the lawyer may have difficulty later proving the fairness of the deal.

ABA Opinion 00-418 recommends that the lawyer establish a reasonable fee for her services and accept stock that at the time of the transaction is worth the reasonable fee. If possible, the stock should be valued at the amount per share that cash investors agreed to pay about the same time the stock was issued to the lawyer or law firm. If that is not possible, “the percentage of stock agreed upon should reflect the value, as perceived by the client and the lawyer at the time of the transaction, that the legal services will contribute to the potential success of the enterprise.”

Equity Positions in Startups

In certain instances, the required level of disclosure for informed written consent may differ, depending upon the experience and knowledge of the client.

If the law firm pays for stock at the same terms as are offered to other investors, the fairness of the transaction may be presumed. Axiomatically, in such instances, since the firm is not exchanging services for its shares, there is no need to value those services.

Depending on the type of investment vehicle (a separate venture fund, for example) the potential conflicts of interest may be muted, particularly if the investment represents only a small percentage of the total equity of the company or a small percentage of the lawyer’s or law firm’s holdings.

Equity Positions in Startups

Law firms may further minimize ethical risks by adopting guidelines that, for example, limit investment in any one client. Other factors such guidelines should address include: whether to allow individual lawyers to invest or whether to limit investments to the firm as a

whole;

whether the firm should make any investments directly or whether the firm should set up a separate partnership or other entity (such as a venture fund) to make the investments;

who should make investment decisions; and

whether to take investment decisions out of the hands of the lawyers doing the work for the client. Of course, law firms should also adopt policies that minimize the risk of insider trading.

The firm should confirm that its investment will not affect its malpractice coverage.

Lastly, the firm should ensure that a sound process is in place to obtain informed written consent from clients, as applicable.