Embed Size (px)

Citation preview

Page 1 of 9

London, 21st June 2019

EU Sugar Market Report and Update

Contents EU sugar production seen 1 million tonnes higher in 2019/20 ......................................................................... 1

Eurostat shows modest increase in in sugar imports so far ............................................................................... 2

EU exports slow to 120,000 tonnes in April 2019............................................................................................. 3

Intra-EU sugar import prices rise above EUR400/tonne while intra-EU export prices fall .............................. 4

Mixed feedback to the EC’s Market Transparency Initiative ............................................................................ 5

High level group on sugar recommends no policy change ................................................................................ 7

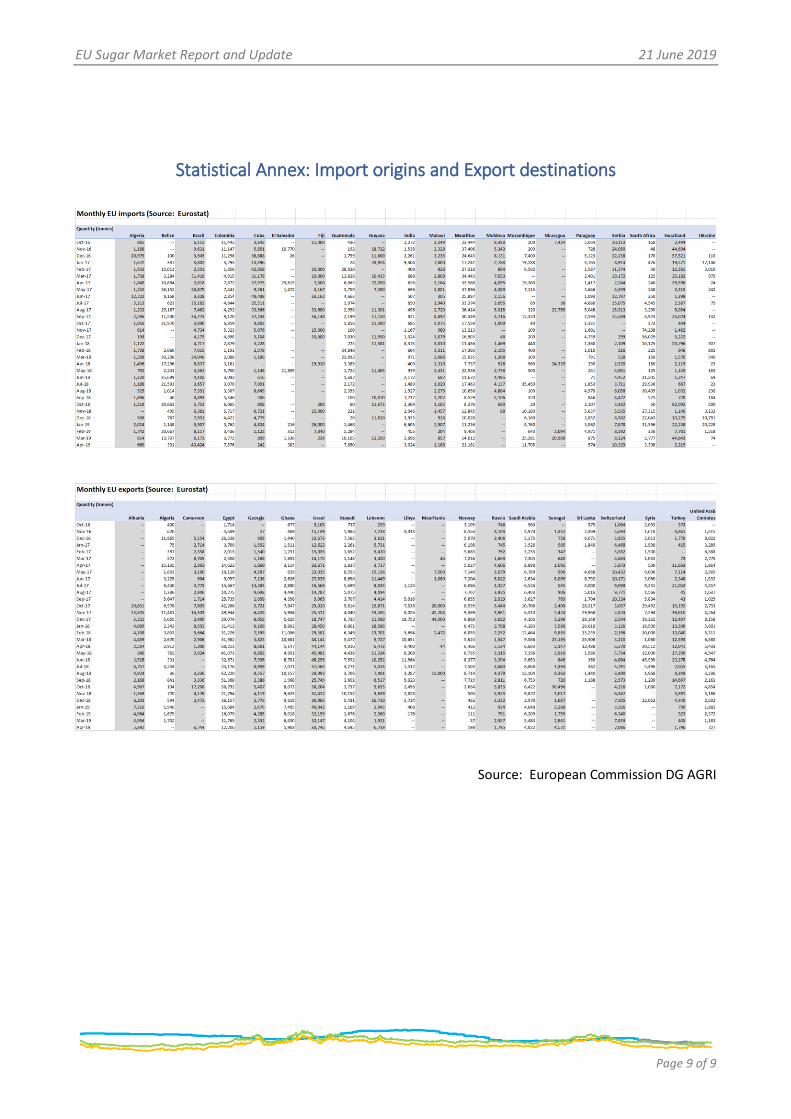

Statistical Annex: Import origins and Export destinations ................................................................................ 9

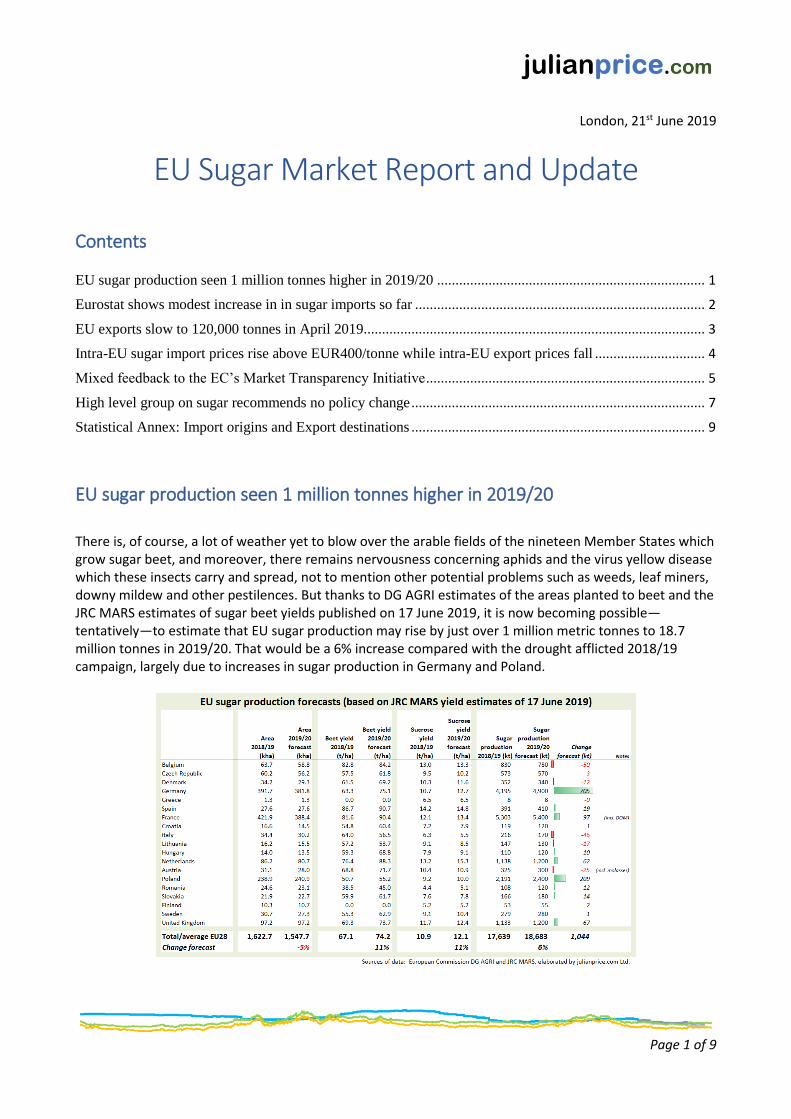

EU sugar production seen 1 million tonnes higher in 2019/20

There is, of course, a lot of weather yet to blow over the arable fields of the nineteen Member States which grow sugar beet, and moreover, there remains nervousness concerning aphids and the virus yellow disease which these insects carry and spread, not to mention other potential problems such as weeds, leaf miners, downy mildew and other pestilences. But thanks to DG AGRI estimates of the areas planted to beet and the JRC MARS estimates of sugar beet yields published on 17 June 2019, it is now becoming possible—tentatively—to estimate that EU sugar production may rise by just over 1 million metric tonnes to 18.7 million tonnes in 2019/20. That would be a 6% increase compared with the drought afflicted 2018/19 campaign, largely due to increases in sugar production in Germany and Poland.

EU Sugar Market Report and Update 21 June 2019

Page 2 of 9

Sugar production in the largest EU sugar producer, France, seems on course to reach 5.4 million tonnes, including 200,000 tonnes produced in the French Overseas Departments (DOM). The beets are reported to be in good condition, having benefited from recent rainfall and warm temperatures which ought to favour rapid growth over the summer. Sugar production in Germany may increase considerably, by around 700,000 tonnes, and reach 4.9 million tonnes; the area sown to beet in Germany is forecast just 3% lower than last year and yield prospects are reported to be “average to good”, clearly above last year’s disappointing yields and close to the five-year average. In Poland, although MARS forecasts below-average yields owing to the adverse conditions at the beginning of the season, sugar production may increase by 200,000 tonnes to 2.4 million tonnes thanks to a small (1%) increase in the area sown and the warm weather during June. Sugar beets in the United Kingdom are generally faring well, with crops reaching 10 to 12 true leaves according to the British Beet Research Organisation on 14 June; British sugar production may increase to 1.2 million tonnes this year. The weather in Spain was very dry and warm in May, but good beet yields are still possible if water reservoir levels allow and irrigation restrictions are not applied. The area sown to beet in Italy is forecast down 12%, and the cold weather in the Po valley did not favour beet, the sowing of which was delayed by wet conditions this spring; production in Italy is forecast down nearly 50,000 tonnes to 170,000 tonnes this year. Although sugar beet is somewhat behind in development in the Benelux countries despite the average sowing date being 10 days earlier than in 2018, sugar production in the Netherlands may reach 1.2 million tonnes, up 60,000 tonnes from last year, whilst production in Belgium is expected to be some 50,000 tonnes lower at 780,000 tonnes this year. Sugar beet planting in Lithuania was satisfactory and crops emerged well; yields are forecast close to the five-year average, but sugar production is forecast down 17,000 tonnes to 130,000 tonnes owing to a smaller area being planted. Overall for the EU of 28 Member States, the area is estimated down just 5% after earlier estimates of a reduction of 8%, but average beet yields are now estimated up 11% giving rise to an estimated sugar production increase of 6% to around 18.7 million tonnes in 2019/20 after around 17.7 million tonnes in 2018/19.

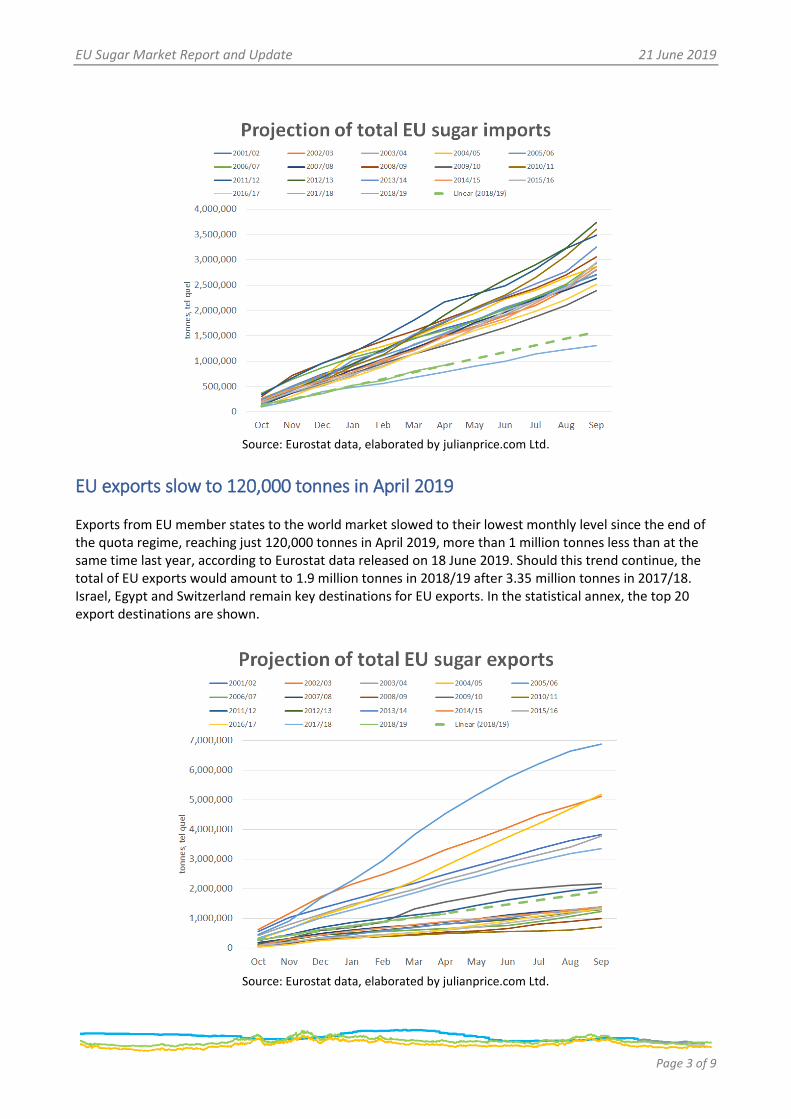

Eurostat shows modest increase in in sugar imports so far According to the latest Eurostat data released on 18 June 2019, imports of all types of sugar into the European Union were nearly 140,000 tonnes ahead of last year, not including imports under IPR arrangements. By April 2019, total imports had reached 920,000 tonnes compared with 781,000 tonnes in April 2018. Should this pace of imports be continued, the total volume of sugar imports into the EU would reach 1.6 million tonnes compared with 1.3 million tonnes in 2017/18, however, there is evidence of an increasing pace of imports and so the total may reach well above 1.6 million, maybe 1.8 million tonnes. The Eurostat data showed a total of 121,000 tonnes of imports in April 2019, of which 43,000 tonnes was imported from Brazil. In the statistical annex hereto, the imports are given for the top 20 import origins.

Picture source: British Beet Research Organization

EU Sugar Market Report and Update 21 June 2019

Page 3 of 9

Source: Eurostat data, elaborated by julianprice.com Ltd.

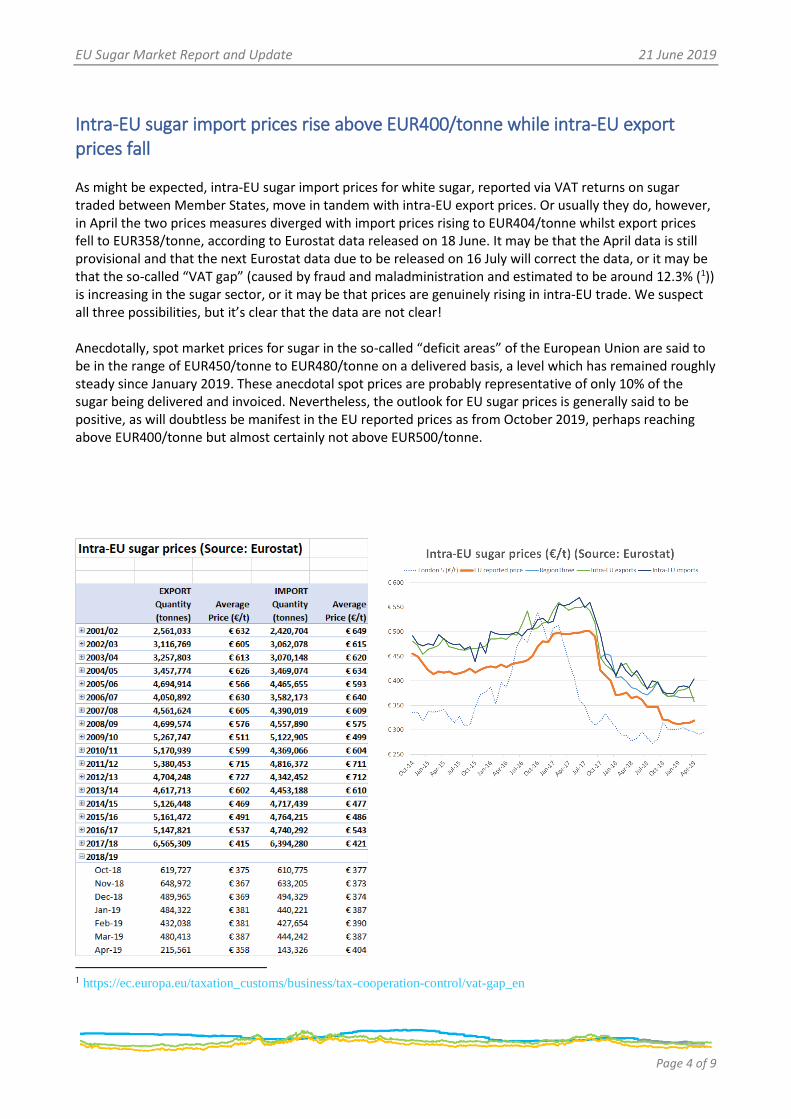

EU exports slow to 120,000 tonnes in April 2019 Exports from EU member states to the world market slowed to their lowest monthly level since the end of the quota regime, reaching just 120,000 tonnes in April 2019, more than 1 million tonnes less than at the same time last year, according to Eurostat data released on 18 June 2019. Should this trend continue, the total of EU exports would amount to 1.9 million tonnes in 2018/19 after 3.35 million tonnes in 2017/18. Israel, Egypt and Switzerland remain key destinations for EU exports. In the statistical annex, the top 20 export destinations are shown.

Source: Eurostat data, elaborated by julianprice.com Ltd.

EU Sugar Market Report and Update 21 June 2019

Page 4 of 9

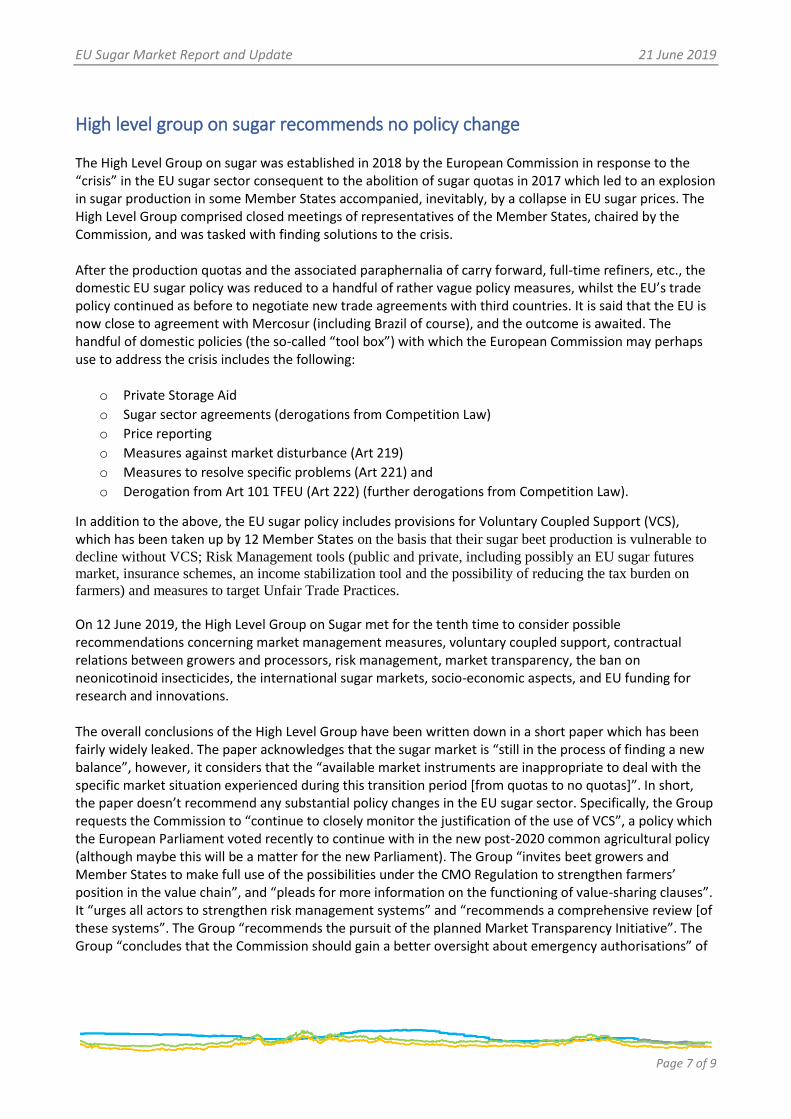

Intra-EU sugar import prices rise above EUR400/tonne while intra-EU export prices fall As might be expected, intra-EU sugar import prices for white sugar, reported via VAT returns on sugar traded between Member States, move in tandem with intra-EU export prices. Or usually they do, however, in April the two prices measures diverged with import prices rising to EUR404/tonne whilst export prices fell to EUR358/tonne, according to Eurostat data released on 18 June. It may be that the April data is still provisional and that the next Eurostat data due to be released on 16 July will correct the data, or it may be that the so-called “VAT gap” (caused by fraud and maladministration and estimated to be around 12.3% (1)) is increasing in the sugar sector, or it may be that prices are genuinely rising in intra-EU trade. We suspect all three possibilities, but it’s clear that the data are not clear! Anecdotally, spot market prices for sugar in the so-called “deficit areas” of the European Union are said to be in the range of EUR450/tonne to EUR480/tonne on a delivered basis, a level which has remained roughly steady since January 2019. These anecdotal spot prices are probably representative of only 10% of the sugar being delivered and invoiced. Nevertheless, the outlook for EU sugar prices is generally said to be positive, as will doubtless be manifest in the EU reported prices as from October 2019, perhaps reaching above EUR400/tonne but almost certainly not above EUR500/tonne.

1 https://ec.europa.eu/taxation_customs/business/tax-cooperation-control/vat-gap_en

EU Sugar Market Report and Update 21 June 2019

Page 5 of 9

Mixed feedback to the EC’s Market Transparency Initiative The European Commission invited comments from stakeholders on its proposal for a Market Transparency Initiative and received a mixed bag of comments before the deadline of 19 June 2019. The Market Transparency Initiative was mooted in 2018 in response to requests by Member States and stakeholders to better understand the food supply chain and agri-food prices at processing and retail stages for key products. The Commission’s idea is that market transparency will help EU farmers achieve higher prices at the farmgate for their produce, and that it is a good thing that information is available as to how prices are formed as agri-food products move along the food supply chain. In short, the Commission believes that better transparency would lead to more rational decision making and hence a better functioning of the markets. Of the 78 responses received from the EU agri-food complex, eleven were from associations of sugar beet growers, cane sugar refiners, sugar beet processors and sugar users. Additionally, responses were received from “umbrella” associations which represent sugar interests amongst others, including associations of agri-food traders, farmers’ cooperatives, food manufacturers, etc. All stakeholders stated that, in one way or another, they welcome the Commission’s initiative. But beyond that window-dressing, all stakeholders expressed grave concerns, especially as regards the specificities in each sector, sugar, milk, meat, grains, etc. Essentially, they divided into two camps: farmers on the one hand and downstream food processors on the other. Farmers’ associations stated there is a lack of transparency in current price developments, complaining that the Commission’s average price reporting schemes do not reflect current price trends and do not permit the calculation of margins all along the food supply chain. The farmers’ groups Copa and Cogeca stated that “without market transparency the necessary tools to curb unfair trade practices, to manage risk and tackle extreme price fluctuations cannot be implemented, will not be efficient, and all this to the detriment of farmers and agricultural cooperatives”. They added that an absence of transparency can lead to a misinterpretation of market signals and therefore a continuation of imbalances in the market, ultimately leading to continued downward pressure on prices and a high risk of market abuse from buyers towards their suppliers. The CGB association of beet growers in France stated that the information available on the European sugar market is the “poorest of all European agricultural sectors” and is “insufficient to provide sufficient visibility for farmers and allow them to adapt their activity”. Another beet growers’ association added that they “are the only link in the chain who do not know prices on time”. The National Union of Sugar Beet Growers of Poland opined that “instruments for monitoring the sugar market should be improved and that at a time when Member States are considering options to reduce sugar consumption, and food companies are reviewing their strategies in this area, it is crucial to closely monitor their impact on the market”. In general, beet farmers urged the Commission to go further with their initiative by gathering and publishing more information, including prices for isoglucose and bioethanol, further improvement of the communication of sugar prices (including other types of sugar and spot values), improvement of the monthly scoreboard on retail price indexes for high-sugar products, monitoring of policies on sugar consumption, and monitoring of the main segments of the market for processed sugar products. Downstream processors, traders and industrial food manufacturers, on the other hand, stated that there is, from their point of view, quite enough market transparency, notably provided via the sectoral Market

EU Sugar Market Report and Update 21 June 2019

Page 6 of 9

Observatories, and they seem united in their view in that there is no need for additional government instruments. They wonder what purpose might be served by publication of more prices data and what measures might be put in place to respond to any price anomalies which such an enhanced reporting mechanism would potentially reveal? One group stated it would be beneficial instead to make the best possible use of existing public and private sources of data, not only concerning prices but also production trends, consumption and trade volumes, etc., and to work on improving these data, comparing the Commission’s publications less than favourably with those of the US Department of Agriculture. Another opined that the provision of these data is key if private risk management tools such as insurance and derivative markets are to become established or developed. The French beet processors’ group SNFS stated that, “it is easy but dangerous to think that price transparency is likely to provide a solution to the crisis in the sector”. Commenting on operators further downstream in the sugar sector, the primary processors opined that that there is a large information imbalance within the sugar processing chain to the detriment of beet growers and sugar manufacturers. Nordic Sugar noted that sugar processors “have been relieved of around EUR2.75 billion by lower raw material purchase prices and that, as far as we know, information on the extent to which the lower purchase prices have been passed on to the end consumers is not available”. The sugar processors’ group CEFS stated that they support the introduction of notifications downstream in the sugar supply chain, where currently no such obligations exist. “We fully concur with the conclusions of the Agricultural Markets Task Force and the report of the High Level Forum for a Better Functioning of the Food Supply Chain of February 2019, which call for the extension of market transparency downstream to those stems where information is currently lacking, up to an including the retail stage”, CEFS stated. The industrial sugar users’ group CIUS, representing sugar users of the EU food and drink sector, stated that market monitoring and transparency is a key priority for their members, but that “current market information is already available”. Information as regards stocks, spot market prices, inter-company exchanges, export prices, etc., could be improved, but CIUS is against the extension of sugar price monitoring for manufacturers in the food sectors because “price formation/transmission in the food supply chain is very complex and goes far beyond price data for single ingredients”. Nevertheless, CIUS recommends that the current collection of data from sugar producers should be intensified, notably by reducing reporting time lags. The German sugar users’ group IZZ also does not see any need for more price transparency in the downstream chain because public bodies, such as the Federal Statistical Office in Germany, already report on the monthly developments of consumer price indices of various product groups. Many stakeholders also raised concerns over commercial confidentiality and competition amongst operators and stated that the Commission’s market transparency initiative could constitute a threat to arbitrage possibilities and thus reduce operators’ negotiating capacity, and hence could also lead to downward pressure on prices ultimately paid to farmers. Also, some voiced the opinion that excessive price transparency could further restrict competition in the sector.

EU Sugar Market Report and Update 21 June 2019

Page 7 of 9

High level group on sugar recommends no policy change The High Level Group on sugar was established in 2018 by the European Commission in response to the “crisis” in the EU sugar sector consequent to the abolition of sugar quotas in 2017 which led to an explosion in sugar production in some Member States accompanied, inevitably, by a collapse in EU sugar prices. The High Level Group comprised closed meetings of representatives of the Member States, chaired by the Commission, and was tasked with finding solutions to the crisis. After the production quotas and the associated paraphernalia of carry forward, full-time refiners, etc., the domestic EU sugar policy was reduced to a handful of rather vague policy measures, whilst the EU’s trade policy continued as before to negotiate new trade agreements with third countries. It is said that the EU is now close to agreement with Mercosur (including Brazil of course), and the outcome is awaited. The handful of domestic policies (the so-called “tool box”) with which the European Commission may perhaps use to address the crisis includes the following:

o Private Storage Aid

o Sugar sector agreements (derogations from Competition Law)

o Price reporting

o Measures against market disturbance (Art 219)

o Measures to resolve specific problems (Art 221) and

o Derogation from Art 101 TFEU (Art 222) (further derogations from Competition Law).

In addition to the above, the EU sugar policy includes provisions for Voluntary Coupled Support (VCS), which has been taken up by 12 Member States on the basis that their sugar beet production is vulnerable to

decline without VCS; Risk Management tools (public and private, including possibly an EU sugar futures

market, insurance schemes, an income stabilization tool and the possibility of reducing the tax burden on

farmers) and measures to target Unfair Trade Practices.

On 12 June 2019, the High Level Group on Sugar met for the tenth time to consider possible recommendations concerning market management measures, voluntary coupled support, contractual relations between growers and processors, risk management, market transparency, the ban on neonicotinoid insecticides, the international sugar markets, socio-economic aspects, and EU funding for research and innovations. The overall conclusions of the High Level Group have been written down in a short paper which has been fairly widely leaked. The paper acknowledges that the sugar market is “still in the process of finding a new balance”, however, it considers that the “available market instruments are inappropriate to deal with the specific market situation experienced during this transition period [from quotas to no quotas]”. In short, the paper doesn’t recommend any substantial policy changes in the EU sugar sector. Specifically, the Group requests the Commission to “continue to closely monitor the justification of the use of VCS”, a policy which the European Parliament voted recently to continue with in the new post-2020 common agricultural policy (although maybe this will be a matter for the new Parliament). The Group “invites beet growers and Member States to make full use of the possibilities under the CMO Regulation to strengthen farmers’ position in the value chain”, and “pleads for more information on the functioning of value-sharing clauses”. It “urges all actors to strengthen risk management systems” and “recommends a comprehensive review [of these systems”. The Group “recommends the pursuit of the planned Market Transparency Initiative”. The Group “concludes that the Commission should gain a better oversight about emergency authorisations” of

EU Sugar Market Report and Update 21 June 2019

Page 8 of 9

the use of neonicotinoids and “recommends” legal action if justified. And it “stresses the status of ‘sensitive product’ for sugar in [trade] negotiations with major sugar producing countries” (i.e. Brazil). So, lots of recommendations and encouragement to use existing legislative and private mechanisms, but no concrete policy measures to alleviate the crisis in the EU sector. On 14 June, the International Confederation of European Beet Growers, CIBE, reacted in a strongly worded press release which voiced beet growers’ concern over the prolonged inaction of the Commission in addressing the crisis and noting that the draft conclusions of the High Level Group “risk persisting on this path of inaction”. CIBE President Eric Lainé is quoted stating, “we need support to improve our resilience and to stop market access concessions to third countries”, concluding, “It is time to act, to be pragmatic. The Commission and Member States have shown that it is possible to act for other sectors. CIBE and its members will continue to work but would be deeply disappointed and concerned in the event of disengagement from the Commission and Member States”, President Lainé said.

Picture source: https://twitter.com/flanesfordfarm/status/1138326609667272705

EU Sugar Market Report and Update 21 June 2019

Page 9 of 9

Statistical Annex: Import origins and Export destinations

Source: European Commission DG AGRI

![EU Import of main citrus varieties [tonnes] Citrus fruit](https://img.pdfslide.net/doc/110x75/619169f3fec5567b3a417793/eu-import-of-main-citrus-varieties-tonnes-citrus-fruit-.jpg)