Embed Size (px)

Citation preview

© 2008 Northern Trust Corporation northerntrust.com

N O R T H E R N T R U S T

Aaron OveryHead of Pooling Business DevelopmentEmail: [email protected]

European Pensions Netherlands Summit: The Strive for Excellence

Cross Border Pension Pooling

12 March 2008 - NH Grand Hotel Krasnapolsky, Amsterdam, Netherlands

3

Enterprise Risk Management

For Multinationals, they get back control

4

It Simply Comes Down To Performance

“Gain and Retain”

“Pooling is the cheapest and easiest way to achieve superior performance”

5

Vehicle Options - Pooling

Pooling is the aggregation of assets of different entities into a single portfolio

Assets pooled together as a single portfolio.Entities may be within the same client, or of different clients.Pooled portfolio may be a single custody account or, more usually, a vehicle established for pooling purposes. The investment manager can manage a single, large portfolio rather than multiple smaller, separate portfolios.

POOLING

ABC group assets

XYZ group assets

Single Portfolio

6

Vehicle Options – Cross-Border Pension Pooling

Cross-border pension pooling is the aggregation of assets of different pension funds, which are domiciled in different countries, into a single portfolio

Assets of all participants pooled in a single portfolio.Pooling usually takes place within a vehicle.Pension funds may be of different domiciles with different tax rates applicable.Withholding tax will be applied at the rate applicable to the vehicle.System tracks by participant:

Units held

Cross-Border Pension Pooling

Irish Pension

Fund

Pooled Vehicle(Opaque)

NetherlandsPension

Fund

7

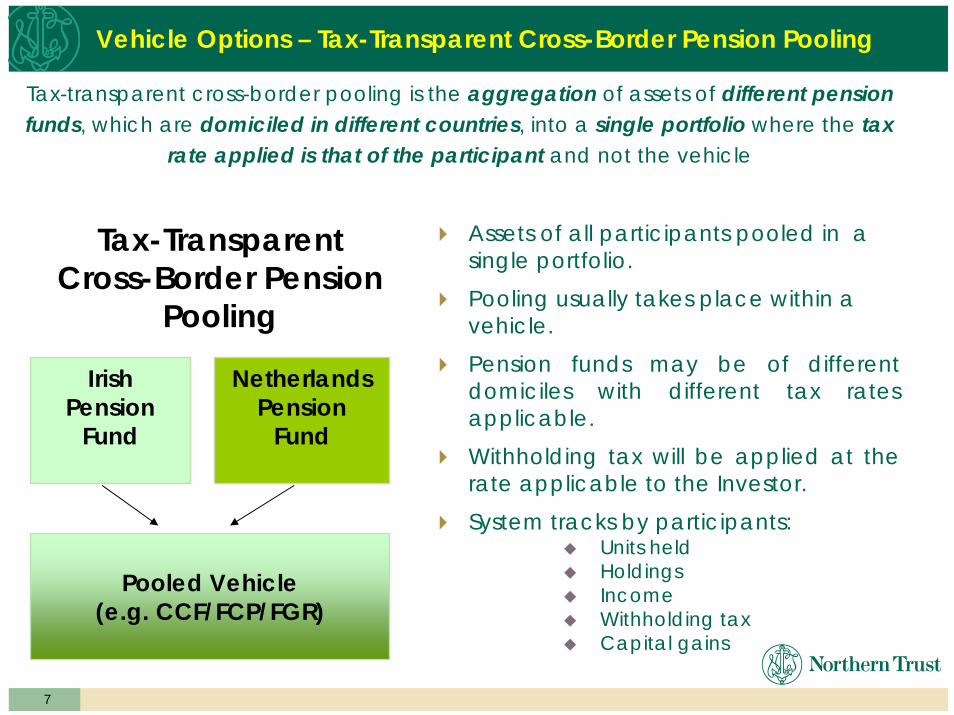

Vehicle Options – Tax-Transparent Cross-Border Pension Pooling

Tax-transparent cross-border pooling is the aggregation of assets of different pension funds, which are domiciled in different countries, into a single portfolio where the tax

rate applied is that of the participant and not the vehicle

Assets of all participants pooled in a single portfolio.Pooling usually takes place within a vehicle.Pension funds may be of different domiciles with different tax rates applicable.Withholding tax will be applied at the rate applicable to the Investor. System tracks by participants:

Units heldHoldingsIncomeWithholding taxCapital gains

Tax-Transparent Cross-Border Pension

Pooling

Irish Pension

Fund

NetherlandsPension

Fund

Pooled Vehicle(e.g. CCF/FCP/FGR)

8

DB Pension Plans

Global DB Plans

9

Pension Pooling

10

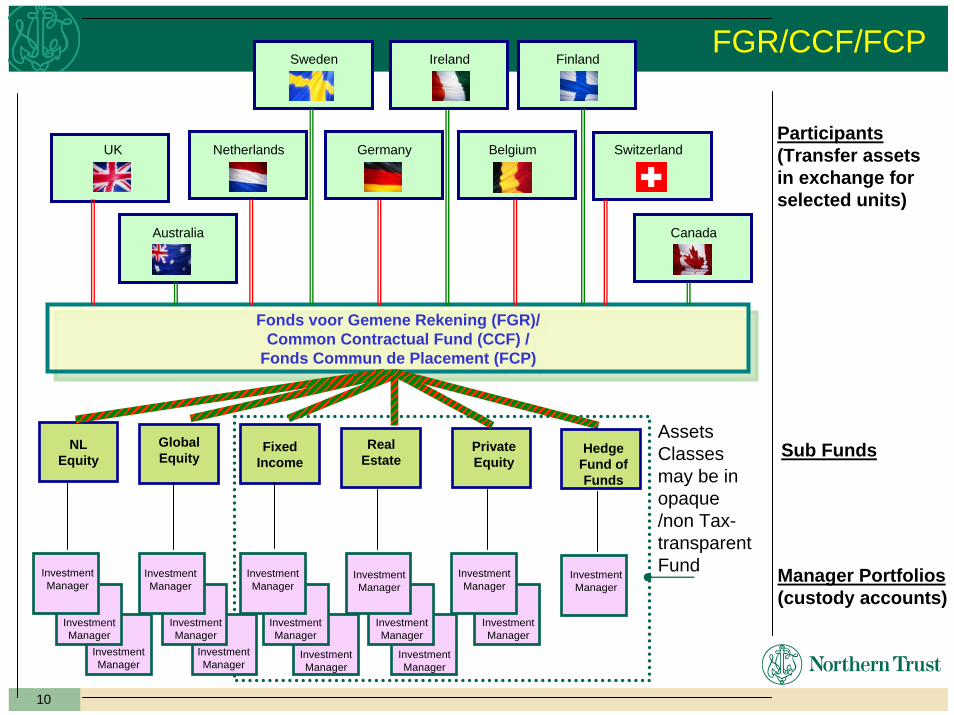

UK

Global Equity

Fixed Income

Real Estate

NL Equity

Fonds voor Gemene Rekening (FGR)/Common Contractual Fund (CCF) /

Fonds Commun de Placement (FCP)

Fonds voor Gemene Rekening (FGR)/Common Contractual Fund (CCF) /

Fonds Commun de Placement (FCP)

Participants(Transfer assets in exchange for selected units)

Manager Portfolios(custody accounts)

Private Equity

Sub Funds

Investment Manager

Netherlands Germany Belgium Switzerland

Sweden Ireland Finland

Australia Canada

FGR/CCF/FCP

HedgeFund of Funds

Assets Classes may be in opaque/non Tax-transparent Fund

Investment Manager

Investment Manager

Investment Manager

Investment Manager

Investment Manager

Investment Manager

Investment Manager

Investment Manager

Investment Manager

Investment Manager

Investment Manager

Investment Manager

Investment Manager

Investment Manager

11

The Pooling Value Proposition - Multinationals

Pooling Value PropositionEnhanced governance and risk management

Administrative efficiencies

Potential cost reductions

Potential Alternatives to PoolingSingle or minimal number of global custodians

Consolidated reporting (HQ Reporting)

Recommended list of investment managers with negotiated fees

IM pooling solution

12

The Pooling Value Proposition – Investment Managers

Pooling Value PropositionTax efficiencies

Enhanced fund performance

Competitive advantage

Potential Alternatives to PoolingNon-tax transparent vehicles (may or may not be characterized by tax drag)

13

IM Structure

Proprietary products

Multi-manager Provide platform/infrastructure so that multinationals do not have to set up their own vehicles but provide manager selection and diversification

Move segregated mandates and pooled funds into new tax-transparent fund run by single investment manager

Guided architecture Implemented consulting, retain control

14

Pooling Today – Timeline

‘01

Consortium formed with two clients Mercer and

GSAM

Northern Trust launches first tax-

transparent multinational CCF

and FCP and global FCP for

manager

Northern Trust launches first

non-tax-transparent cross-

border pension pooling vehicles for multinationals

Ireland creates

CCF

Luxembourg exempts

multinationals from taxe

d’abonnementfor FCP

Ireland extends

CCF eligible investors

and allows non-UCITS

CCF

IMA issues white

paper on pooling

Dutch government promotes the use of FGR

as a tax-transparent

vehicle

EC issues white paper

on investment

funds

‘02

Consortium identifies FCP

as most appropriate tax-

transparent vehicle

Northern Trust undertakes tax, legal and systems work to carry concept

through to implementation

Northern Trust

announces ERISA solution

Northern Trust applies for

patent on tax-transparent

pooling

Operations Management

names Northern Trust’s Univest

launch ‘Best Operations

Innovation’ for 2006

‘03 ‘04 ‘05 ‘06

15

Northern Trust’s Innovative Pooling Process

Unique features…Utilizes investors correct tax rate, enabling them to take advantage of tax treaty benefits

Creates accounting records for individual investors using transaction splitting and rebalancing

Reports capital gains and holdings at the investor level

Supports multiple countries/type of investor and multiple countries of investment

Automated withholding tax processing for both relief-at-source and tax reclaim markets

Accurate calculation of capital gains in those markets that require tax transparency for capital gains

Flexibility to provide regulatory and tax reporting where required at the investor level

Supports securities lending for tax-transparent vehicles

Delivering you a broad range of benefits…

© 2008 Northern Trust Corporation northerntrust.com

Tax Considerations

C O R P O R A T E & I N S T I T U T I O N A L S E R V I C E S

17

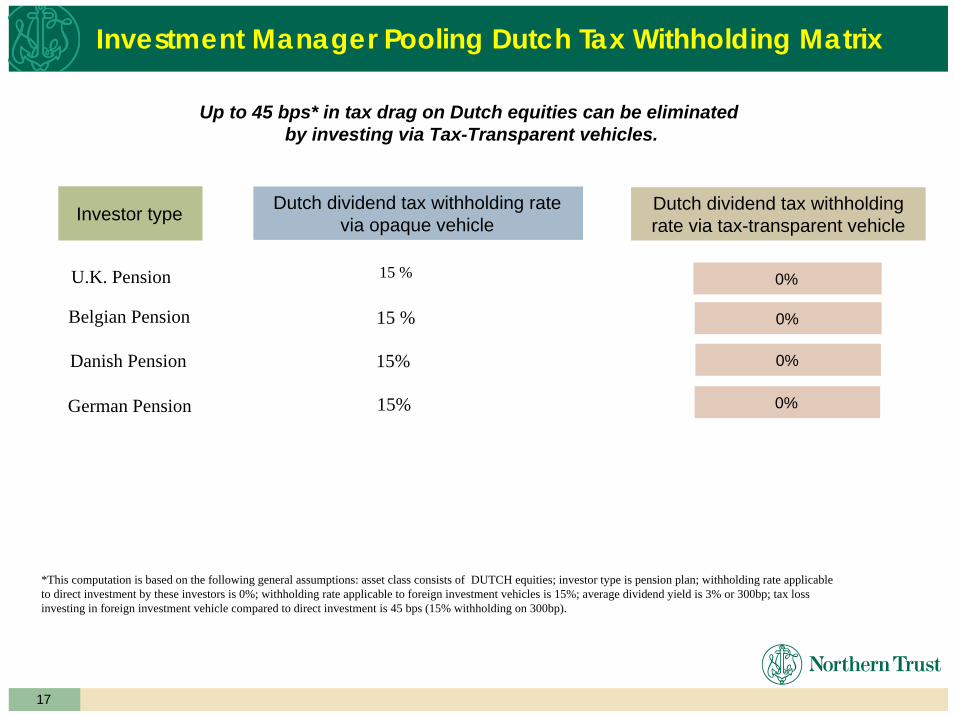

Investment Manager Pooling Dutch Tax Withholding Matrix

Investor type

Danish Pension

Belgian Pension

U.K. Pension 15 %

Dutch dividend tax withholding rate via tax-transparent vehicle

Dutch dividend tax withholding rate via opaque vehicle

15 %

15%

0%

German Pension 15% 0%

0%

0%

*This computation is based on the following general assumptions: asset class consists of DUTCH equities; investor type is pension plan; withholding rate applicable to direct investment by these investors is 0%; withholding rate applicable to foreign investment vehicles is 15%; average dividend yield is 3% or 300bp; tax loss investing in foreign investment vehicle compared to direct investment is 45 bps (15% withholding on 300bp).

Up to 45 bps* in tax drag on Dutch equities can be eliminated by investing via Tax-Transparent vehicles.

18

Systems requirements to support tax-transparent pooling

Normally, all investors in a pooled vehicle are subject to the same withholding tax

Tax-transparent vehicles require (for each sub-fund):

Ability to track income by investor

Ability to withhold or reclaim tax at different rates for different investors

Ability to track percentage ownership by investor at any given time

Ability to track “notional ownership” of shares by each investor

Ability to rebalance shares as percentage ownership changes

Ability to support particular requirements of securities lending

Northern Trust built a systems solution specifically designed to meet the tax and legal requirements for tax transparency

19

Will the Dutch FGR emerge as an alternative to the FCP/CCF?

Dutch Ministry of Finance announcement regarding the Fund for Joint Account (Fonds voor GemeneRekening) 27 March 06

Promotes the FGR as a vehicle for cross-border asset pooling

Ministry of Finance confirmed the tax transparency of the FGR in the Netherlands

Ministry of Finance offers to assist in gaining confirmation from tax authorities in other countries that the FGR is tax transparent

Holland Financial Centre

Pensions Champion Document

Requirements for a tax-transparent vehicle for multinational investors

Strong support from regulators in the jurisdiction of the vehicle

Multinational client proposes to establish the vehicle

Gain confirmations of tax transparency from a broad array of countries of investor and countries of investment

Dutch tax authorities willing to provide rulings to confirm tax transparency

Working with Dutch Ministry of Finance to gain additional rulings from other countries

Subsidiaries comfortable with regulatory structure of the vehicle

© 2008 Northern Trust Corporation northerntrust.com

Pan European Pensions

C O R P O R A T E & I N S T I T U T I O N A L S E R V I C E S

21

Pan European Pension – OFP/Assep/API/Master Trust

22

Pooling Assets and liabilities

23

Investing Directly?

24

Investing via a Tax Transparent Pool

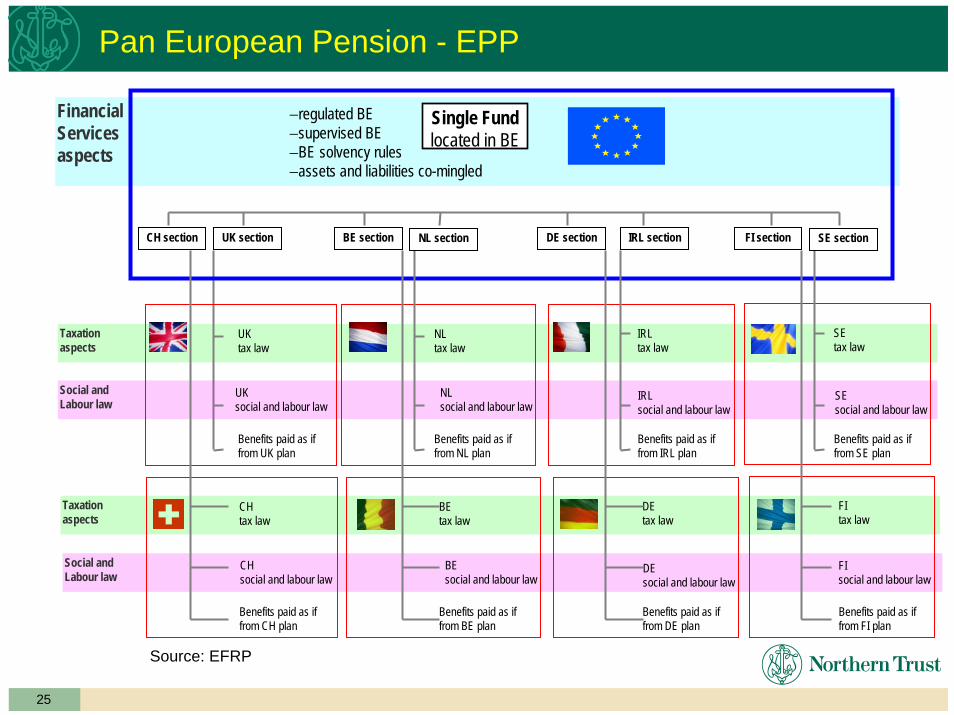

25

Taxationaspects

Financial Servicesaspects

−regulated BE−supervised BE−BE solvency rules−assets and liabilities co-mingled

Benefits paid as iffrom IRL plan

Single Fundlocated in BE

IRL tax law

Social and Labour law

Benefits paid as iffrom NL plan

NL tax law

NL social and labour law

Benefits paid as iffrom UK plan

UK tax law

UK social and labour law

IRL social and labour law

Benefits paid as iffrom SE plan

SE tax law

SEsocial and labour law

Taxationaspects

Benefits paid as iffrom DE plan

DE tax law

Social and Labour law

Benefits paid as iffrom BE plan

BE tax law

BE social and labour law

Benefits paid as iffrom CH plan

CH tax law

CH social and labour law

DE social and labour law

Benefits paid as iffrom FI plan

FI tax law

FIsocial and labour law

CH section UK section BE section NL section DE section IRL section FI section SE section

Pan European Pension - EPP

Source: EFRP

N O R T H E R N T R U S T

![Cap. 173] Pensions CHAPTER 173. PENSIONS. 173.pdf · Pensions, etc., to cease on bankruptcy. 14. Pensions, etc., may cease on sentence to term of imprisonment. 15. Pensions, etc.,](https://img.pdfslide.net/doc/110x75/5f32c41fe2aa25713c052446/cap-173-pensions-chapter-173-173pdf-pensions-etc-to-cease-on-bankruptcy.jpg)