Embed Size (px)

Citation preview

European Private Equity Buyout Review

First Quarter 2017

Fabrizio Bensch REUTERS

Table of Contents

Europe’s PE Buyout Market in Q1 2017 3

€ Invested and # Companies Financed 4

Top PE Buyout Deals 6

Investment by Company Location 7

Investment by Transaction Type 9

PE Investment vs. all European M&A 10

Investment by Company Sector 11

Buyout Funds Raised 12

Public and M&A Exits 13

Private Equity Returns 14

Explanatory Notes & Contacts 15

European Private Equity Buyout Market Activity in Q1 2017

European Buyout-PE Market Trends

Deal-making activity in Europe’s buyout and related private equity market showed a marked decline in the first quarter of 2017. With a total of 206

transactions valued at €12.0 billion, deal values did increase by 22% from Q1 2016. However, deal volumes decreased 36% from the same period last

year, marking the fewest deals done since Q3 2009.

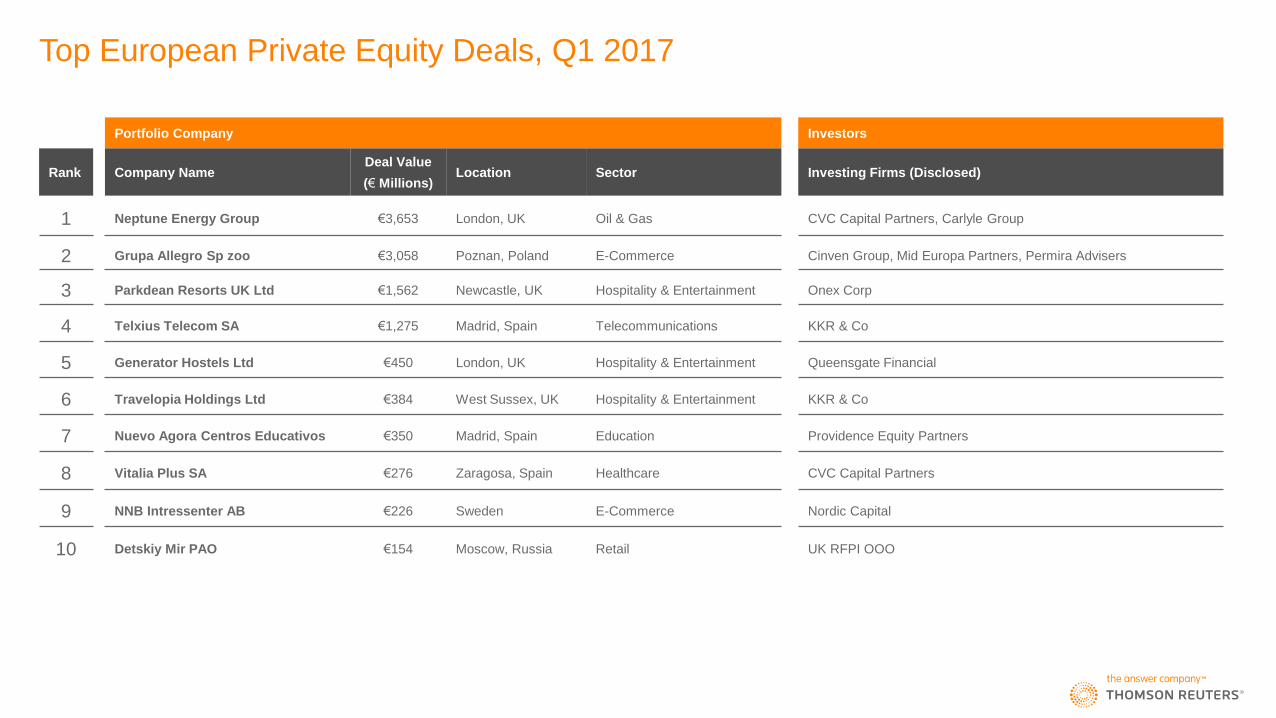

The European top deals list was dominated by UK-based Neptune Energy Group, which received a €3.7 billion investment from CVC Capital Partners

and Carlyle Group; and Poland-based Grupa Allegro, which secured €3.7 billion investment from Cinven Group, Mid Europa Partners, and Permira

Advisers.

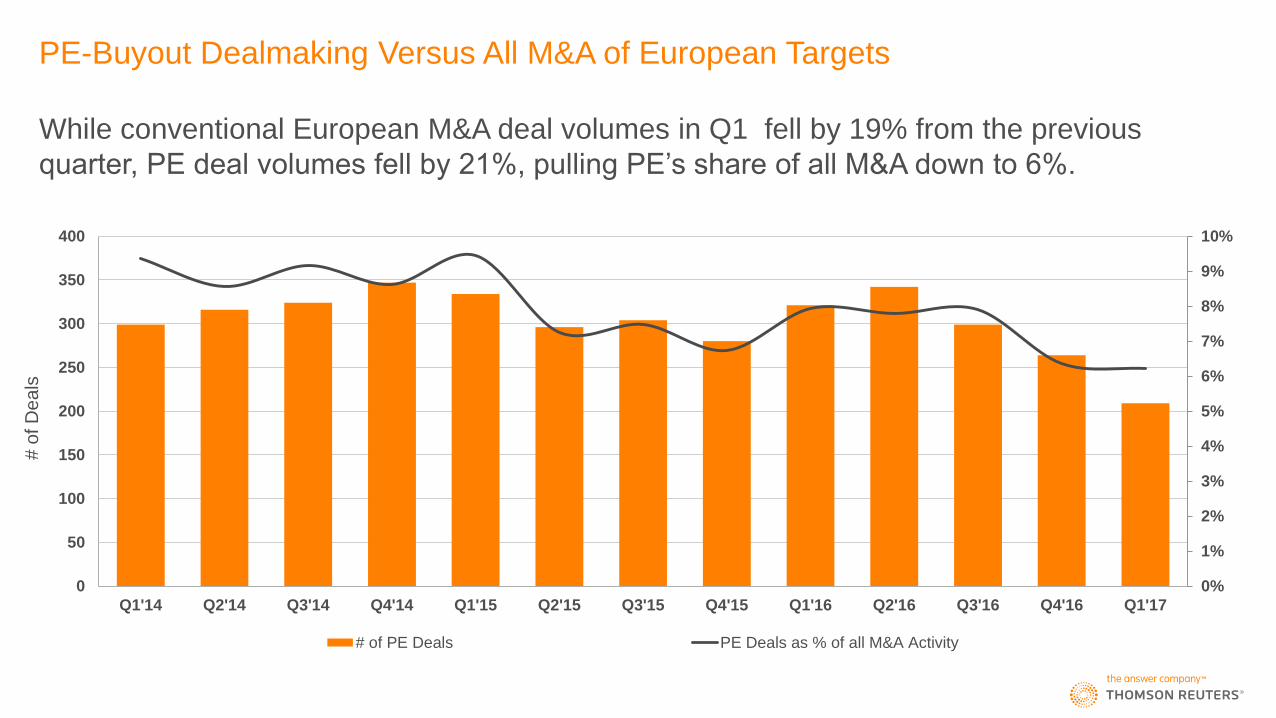

In addition to a decline in private equity deal volumes in European companies on a year-over-year basis, investment activity also continued to decline

as compared to European merger & acquisition activity overall. While the number of private equity deals reached a peak of 9% of the number of

traditional merger & acquisition deals in Q1 2015, this percentage had declined to only 6% in the first quarter of 2017, a three-year low.

European Buyout Fundraising

A total of 13 European private equity buyout funds raised a total of just €3.5 billion in Q1 2017, the weakest quarter since Q3 2012. This represented a

slow start to 2017, considering that European buyout funds raised no less than €34 billion in each of the past four years.

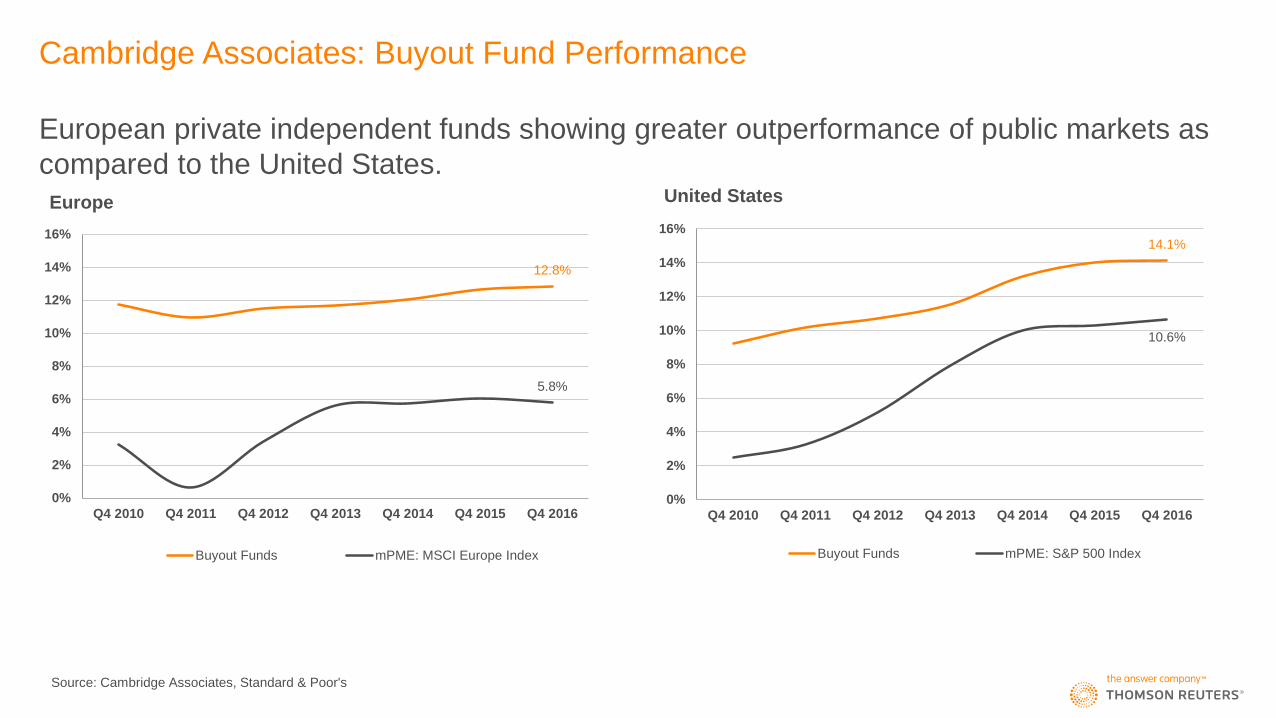

European Fund Performance

While investment activity was on the wane in 2016, the performance of European buyout funds showed steady positive performance, significantly

exceeding public market comparators. Final data provided by Cambridge Associates shows European buyout funds with vintage years of 2000 or

greater returned a since inception IRR of 12.8% as of year-end 2016. While this did lag behind these funds’ US counterparts, European buyout funds

outperformed their public markets by a greater margin.

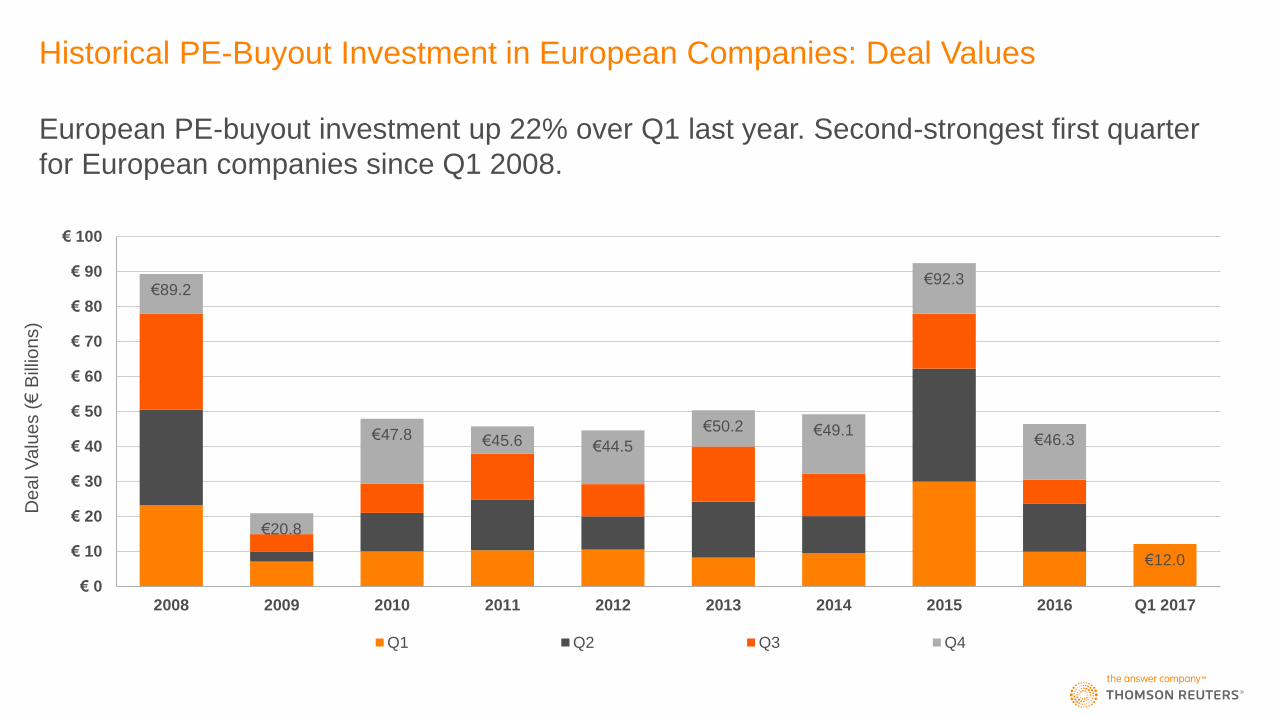

Historical PE-Buyout Investment in European Companies: Deal Values

European PE-buyout investment up 22% over Q1 last year. Second-strongest first quarter

for European companies since Q1 2008.

€12.0

€89.2

€20.8

€47.8 €45.6 €44.5

€50.2 €49.1

€92.3

€46.3

€ 0

€ 10

€ 20

€ 30

€ 40

€ 50

€ 60

€ 70

€ 80

€ 90

€ 100

2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 2017

Q1 Q2 Q3 Q4

De

al V

alu

es (

€ B

illio

ns)

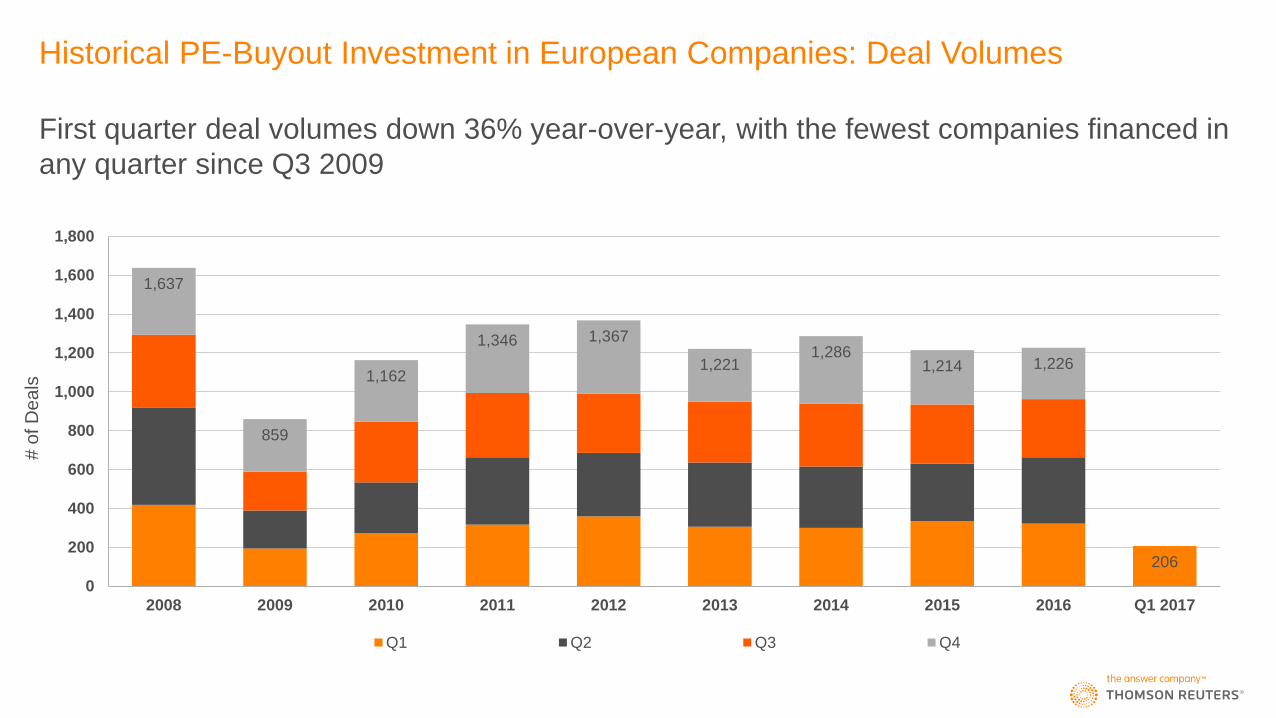

Historical PE-Buyout Investment in European Companies: Deal Volumes

First quarter deal volumes down 36% year-over-year, with the fewest companies financed in

any quarter since Q3 2009

206

1,637

859

1,162

1,346 1,367

1,221 1,286

1,214 1,226

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 2017

Q1 Q2 Q3 Q4

# o

f D

ea

ls

Top European Private Equity Deals, Q1 2017

Portfolio Company Investors

Rank Company Name Deal Value

(€ Millions) Location Sector Investing Firms (Disclosed)

1 Neptune Energy Group €3,653 London, UK Oil & Gas CVC Capital Partners, Carlyle Group

2 Grupa Allegro Sp zoo €3,058 Poznan, Poland E-Commerce Cinven Group, Mid Europa Partners, Permira Advisers

3 Parkdean Resorts UK Ltd €1,562 Newcastle, UK Hospitality & Entertainment Onex Corp

4 Telxius Telecom SA €1,275 Madrid, Spain Telecommunications KKR & Co

5 Generator Hostels Ltd €450 London, UK Hospitality & Entertainment Queensgate Financial

6 Travelopia Holdings Ltd €384 West Sussex, UK Hospitality & Entertainment KKR & Co

7 Nuevo Agora Centros Educativos €350 Madrid, Spain Education Providence Equity Partners

8 Vitalia Plus SA €276 Zaragosa, Spain Healthcare CVC Capital Partners

9 NNB Intressenter AB €226 Sweden E-Commerce Nordic Capital

10 Detskiy Mir PAO €154 Moscow, Russia Retail UK RFPI OOO

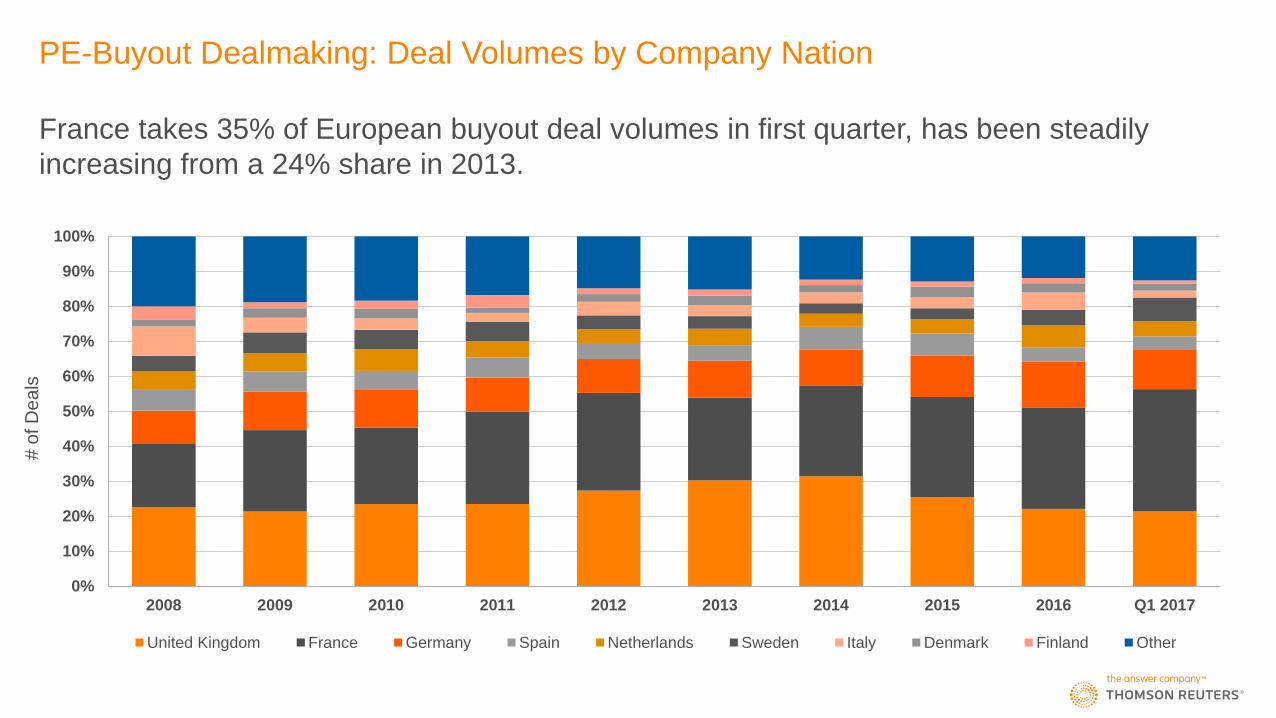

PE-Buyout Dealmaking: Deal Volumes by Company Nation

France takes 35% of European buyout deal volumes in first quarter, has been steadily

increasing from a 24% share in 2013.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 2017

United Kingdom France Germany Spain Netherlands Sweden Italy Denmark Finland Other

# o

f D

ea

ls

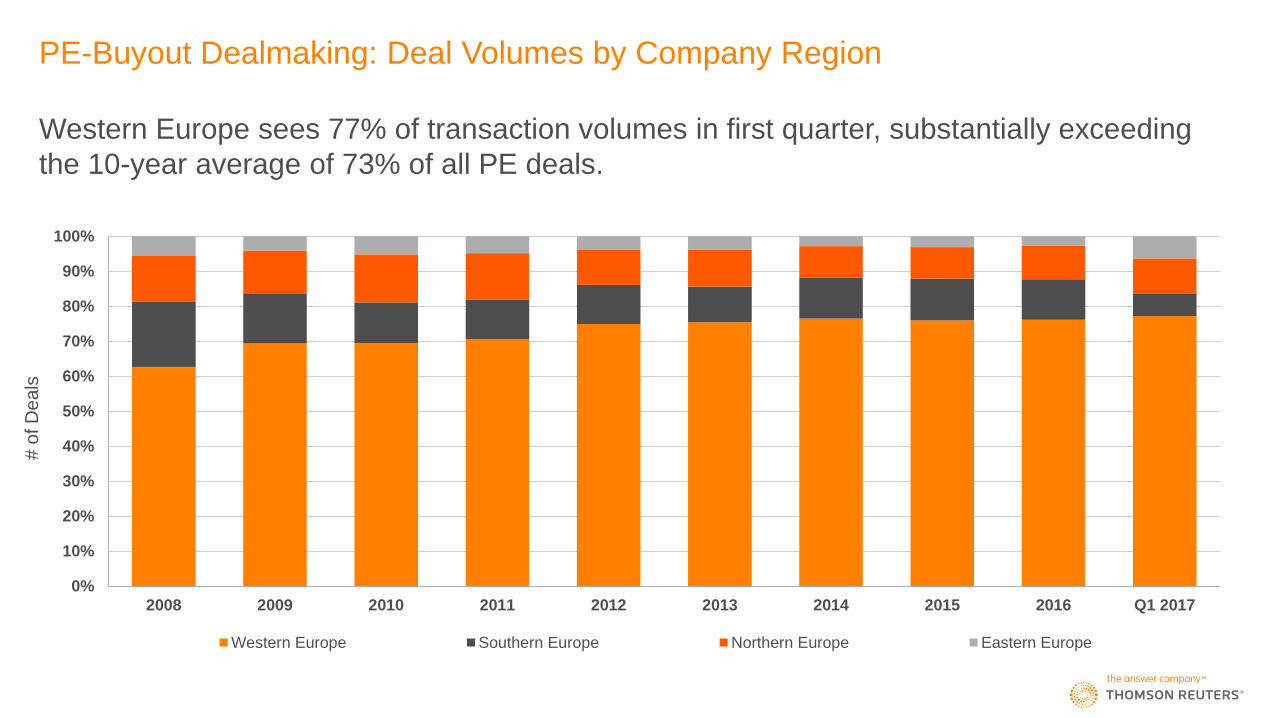

PE-Buyout Dealmaking: Deal Volumes by Company Region

Western Europe sees 77% of transaction volumes in first quarter, substantially exceeding

the 10-year average of 73% of all PE deals.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 2017

Western Europe Southern Europe Northern Europe Eastern Europe

# o

f D

ea

ls

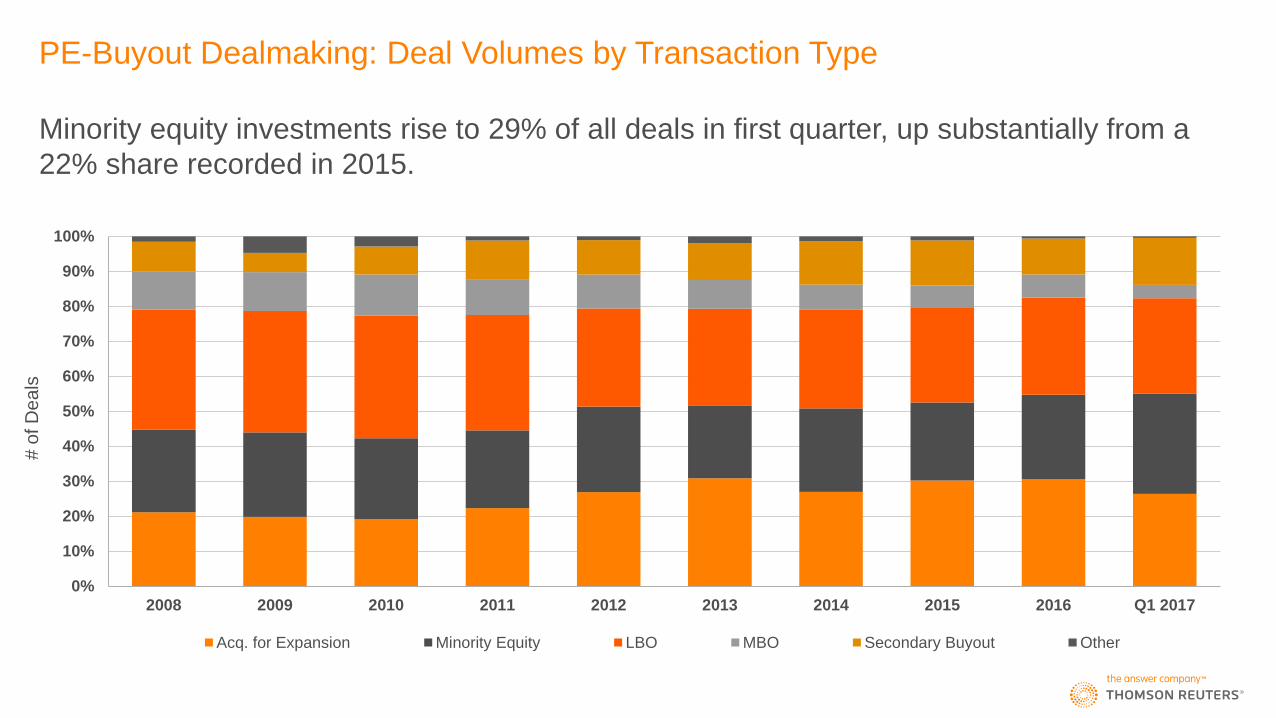

PE-Buyout Dealmaking: Deal Volumes by Transaction Type

Minority equity investments rise to 29% of all deals in first quarter, up substantially from a

22% share recorded in 2015.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 2017

Acq. for Expansion Minority Equity LBO MBO Secondary Buyout Other

# o

f D

ea

ls

PE-Buyout Dealmaking Versus All M&A of European Targets

While conventional European M&A deal volumes in Q1 fell by 19% from the previous

quarter, PE deal volumes fell by 21%, pulling PE’s share of all M&A down to 6%.

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

50

100

150

200

250

300

350

400

Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15 Q4'15 Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

# of PE Deals PE Deals as % of all M&A Activity

# o

f D

ea

ls

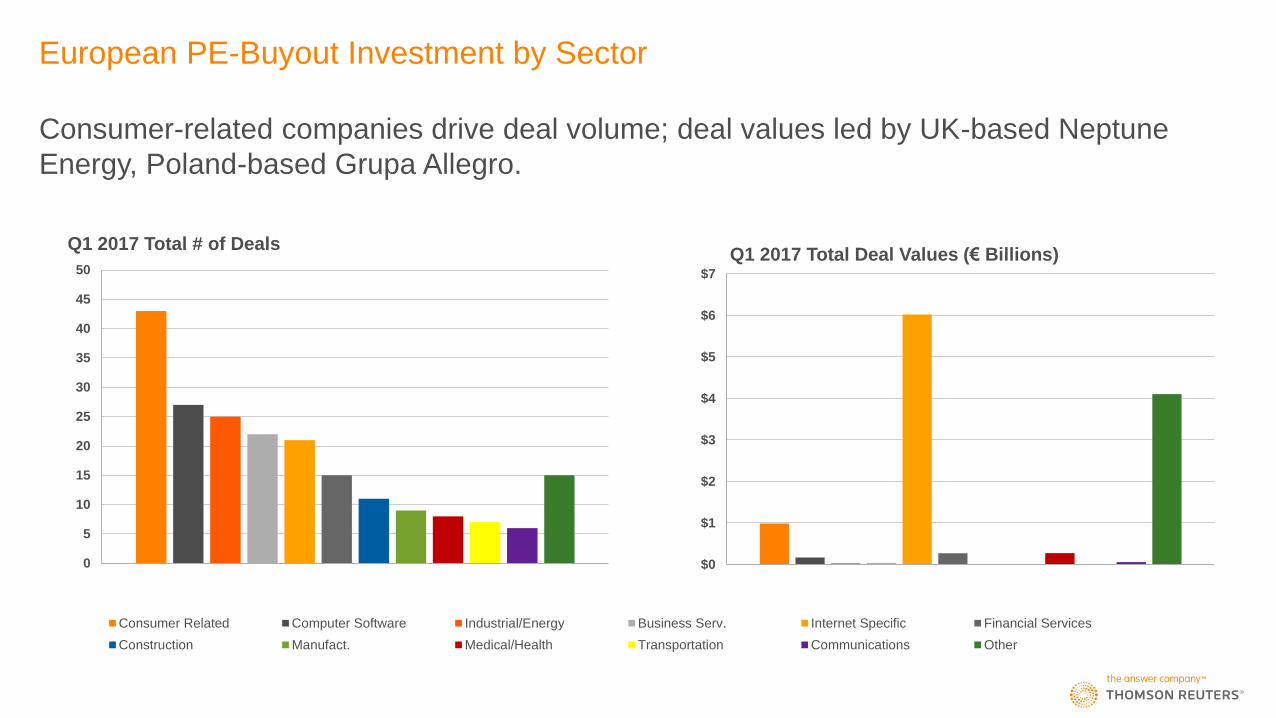

0

5

10

15

20

25

30

35

40

45

50

Q1 2017 Total # of Deals

European PE-Buyout Investment by Sector

Consumer-related companies drive deal volume; deal values led by UK-based Neptune

Energy, Poland-based Grupa Allegro.

$0

$1

$2

$3

$4

$5

$6

$7

Q1 2017 Total Deal Values (€ Billions)

Consumer Related Computer Software Industrial/Energy Business Serv. Internet Specific Financial Services

Construction Manufact. Medical/Health Transportation Communications Other

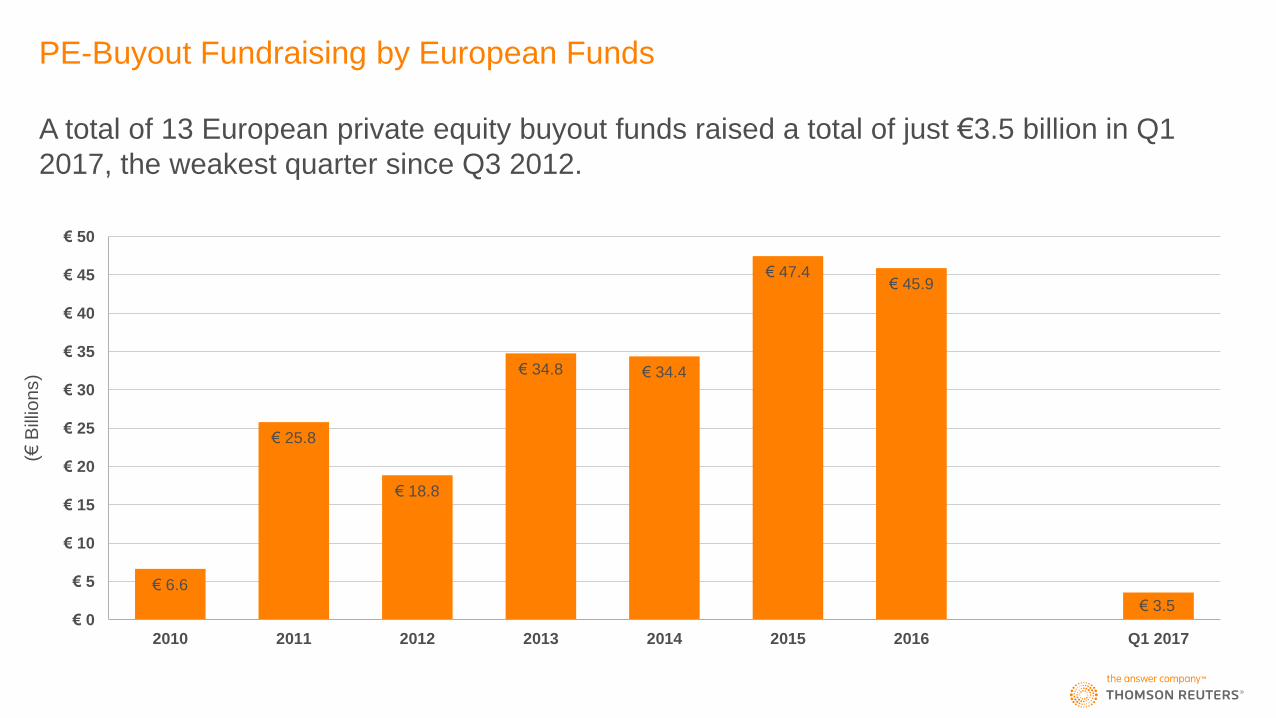

PE-Buyout Fundraising by European Funds

A total of 13 European private equity buyout funds raised a total of just €3.5 billion in Q1

2017, the weakest quarter since Q3 2012.

€ 6.6

€ 25.8

€ 18.8

€ 34.8 € 34.4

€ 47.4 € 45.9

€ 3.5 € 0

€ 5

€ 10

€ 15

€ 20

€ 25

€ 30

€ 35

€ 40

€ 45

€ 50

2010 2011 2012 2013 2014 2015 2016 Q1 2017

(€ B

illio

ns)

European PE-Backed Exits

Portfolio Company Investors

Rank Company Name Deal Value

(€ Millions) Location Sector Investors (Disclosed)

1 Idcsalud SLU €5,763 Madrid, Spain Healthcare CVC Capital Partners

2 Booker Group €4,219 Warwick, UK Consumer-Related 3i Group PLC, Epiris Managers LLP, Montagu Private Equity LLP

3 PointPark Properties sro €2,409 Prague, Czech

Republic Warehousing Logistics

Gic Special Investments Pte Ltd, TPG Capital Management LP,

Ivanhoe Cambridge

4 Cerba Healthcare SASU €1,801 Saint-Ouen

l'Aumone, France Laboratories

Idinvest Partners SA, PAI Partners SAS, Partners Group Holding AG,

Public Sector Pension Investment Board

5 Oasis Dental Care Ltd €979 Bristol, UK Healthcare Bridgepoint Advisers

With only 61 disclosed exits completed in Q1 2017, exit volumes fell 42% as compared to

both Q1 2016 and Q1 2015.

0

50

100

150

Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15 Q4'15 Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

M&A Secondary Sale Public

# o

f E

xits

Cambridge Associates: Buyout Fund Performance

12.8%

5.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Q4 2010 Q4 2011 Q4 2012 Q4 2013 Q4 2014 Q4 2015 Q4 2016

Europe

Buyout Funds mPME: MSCI Europe Index

14.1%

10.6%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Q4 2010 Q4 2011 Q4 2012 Q4 2013 Q4 2014 Q4 2015 Q4 2016

United States

Buyout Funds mPME: S&P 500 Index

Source: Cambridge Associates, Standard & Poor's

European private independent funds showing greater outperformance of public markets as

compared to the United States.

Explanatory Notes

1. Data collected and analyzed by Thomson Reuters for this statistical report were drawn from a variety of sources including Thomson Reuters M&A databases, regulatory filings, press releases, and proprietary investor

reports from European and non-resident fund managers.

2. Key statistical indicators (e.g., total disbursements, per quarter or per annum) are influenced by the fact that a substantial fraction of buyout and other PE deals are not fully disclosed. For instance, “Euros invested” in a

given period pertain only to those deals with values that have been published or confidentially disclosed to Thomson Reuters.

3. Statistical data reflect all essential forms of buyout-PE deal-making, including control-stake acquisitions of businesses, minority equity investments, restructuring and special-situations transactions, mezzanine deals,

acquisitions for expansion and other quasi-equity investments.

4. Fund performance data and public market equivalents are produced via the Cambridge Associates Benchmark Calculator, available through Thomson Reuters Eikon. Returns are for European and US buyout funds with

vintage years of 2001 or greater, on a first cash flow basis, in Euros, from inception to the end of the indicated quarter, under published data mode Q4 2016. Pooled internal rates of return are net of fees, expenses and

carried interest. CA Modified Public Market Equivalent (mPME) replicates private investment performance under public market conditions. The public index’s shares are purchased and sold according to the private fund

cash flow schedule, with distributions calculated in the same proportion as the private fund, and mPME NAV is a function of mPME cash flows and public index returns.

5. All current and previous years data is as of Monday, May 29th, 2017. Data is continuously updated and is therefore subject to change. All figures are in Euros unless otherwise noted.

For further information on Thomson Reuters venture capital and private equity offerings, please visit us at:

• http://thomsonreuters.com/en/products-services/financial/venture-capital-and-private-equity.html

For further reports on private equity, venture capital, and other asset classes, please visit us at:

• http://dmi.thomsonreuters.com

Contributors to this analysis are provided with additional packages of data. If you would like to participate in the submission process, receive quarterly press releases, or have questions about our venture capital criteria, please

contact us at:

Jelena Marinovic

Private Equity European Contributor Relations Lead

E-mail: [email protected]