Embed Size (px)

Citation preview

EXECUTIVE COMMITTEE MEETING July 21, 2016

(4:00 P.M. until business is concluded) 2536 Countryside Blvd, Suite 500

Clearwater, FL 33763

PROPOSED AGENDA

I. CALL TO ORDER A. Approval of July 21, 2016 Agenda Page 1 B. Approval of May 19, 2016 Executive Committee Minutes Page 2

II. ACTION ITEMS A. Accounting & Finance Policies 16.07.01E Page 4 B. Supplemental Sliding Fee Scale 16.07.02E Page 174 C. CCEP Taskforce Committee Appointment 16.07.03E Page 176 D. Continuity of Operations Plan (COOP) 16.07.04E Page 177 E. 2016-2017 Tactical Plan 16.07.05E Page 211

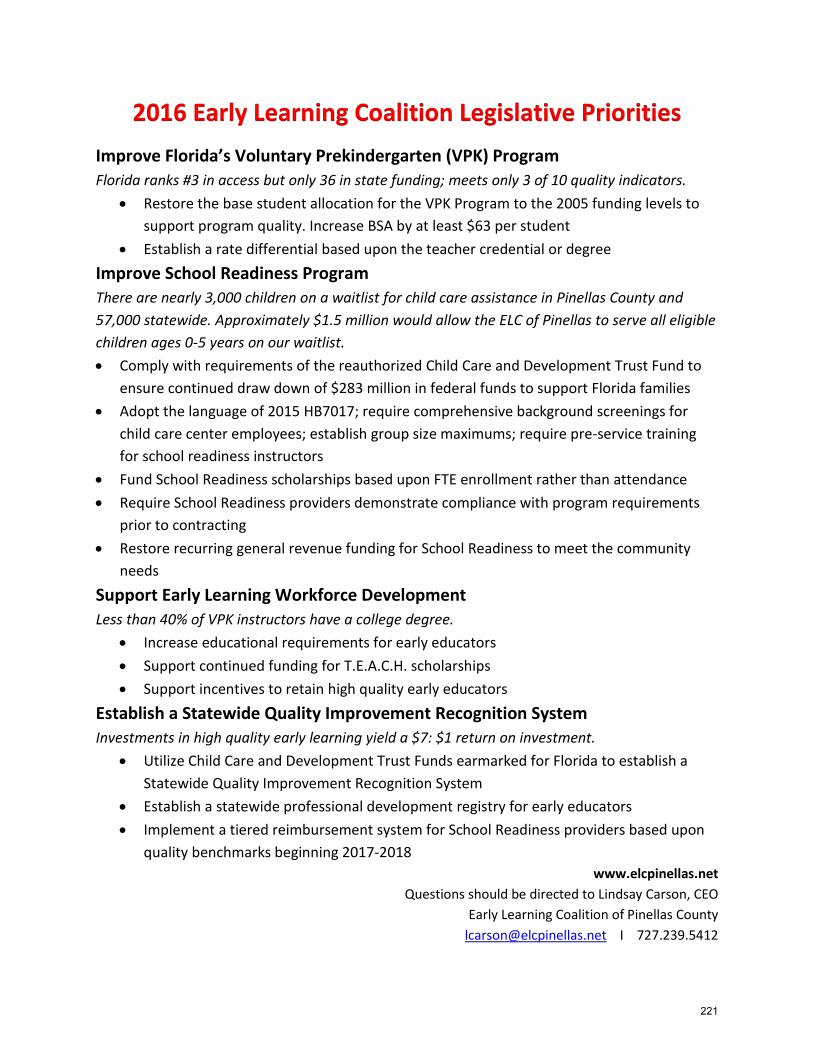

III. DISCUSSION A. Legislative Agenda Page 220 B. Advancement Committee

IV. PUBLIC COMMENT In accordance with the Florida Government in the Sunshine, all meetings of the Early Learning Coalition of Pinellas County, Inc. and its committees are open to the public. Those in attendance who wish to address the Coalition must submit a public comment card to the recorder prior to addressing the Coalition.

V. ADJOURNMENT

Next scheduled Executive Committee meeting: September 15, 2016 at 4:00 p.m. ELC, Countryside Towers 2536 Countryside Blvd. Suite 500 Clearwater, FL 33763

*This meeting will be recorded for the purpose of composing the meeting minutes. A copy of the recording can be made available, please contact Eva Mathews at 727.400.4446

1

EXECUTIVE COMITTEE MEETING May 19, 2016

Approved Minutes 4:00 P.M. until business is concluded

2536 Countryside Blvd., Suite 500 Clearwater, FL 33763

In Attendance: Craig Phillips, Chair; Patsy Buker, Jack Geller, Jim Madden, Yvonne Malague and Elliott Stern

Coalition Staff: Lindsay Carson, Merita Kafexhiu, Eva Mathews

I. CALL TO ORDER:

Chair Craig Phillips called the meeting to order at 4:15 p.m.

A. Chair Craig Phillips called for the approval of the May 19, 2016 agenda.

A motion was made by Jack Geller and seconded by Elliott Stern to:

Approve the May 19, 2016 agenda

The motion passed unanimously.

B. Chair Craig Phillips called for the approval of the March 17, minutes.

A motion was made by Jack Geller and seconded by Elliott Stern to:

Approve the March 17, 2016 minutes

The motion passed unanimously.

2

II. ACTION ITEMS:

A. CCEP Application FY 2016-2017

A motion was made by Jack Geller and seconded by Elliott Stern to:

Approve the CCEP Application FY 2016-2017 as presented.

The motion passed unanimously.

B. Anti-Fraud Plan

A motion was made by Jack Geller and seconded by Elliott Stern to:

Approve the Anti-Fraud Plan as presented.

The motion passed unanimously.

C. Proposed Budget FY 2016-2017

A motion was made by Jack Geller and seconded by Elliott Stern to:

To approve the Proposed Budget FY 2016-1017 as presented.

The motion passed unanimously.

III. DISCUSSION:

A. Tactical Plan 2016-2017 – Role in the Community

IV. PUBLIC COMMENT:

No public comments were made.

V. ADJOURNMENT: The meeting adjourned at 5:00 p.m.

Next meeting: Scheduled for Thursday, July 21, 2016 at 4:00 p.m. ELC, Countryside Towers 2536 Countryside Blvd., Clearwater, FL 33763

____________________________ _______________ Craig Phillips, Committee Chair Date

3

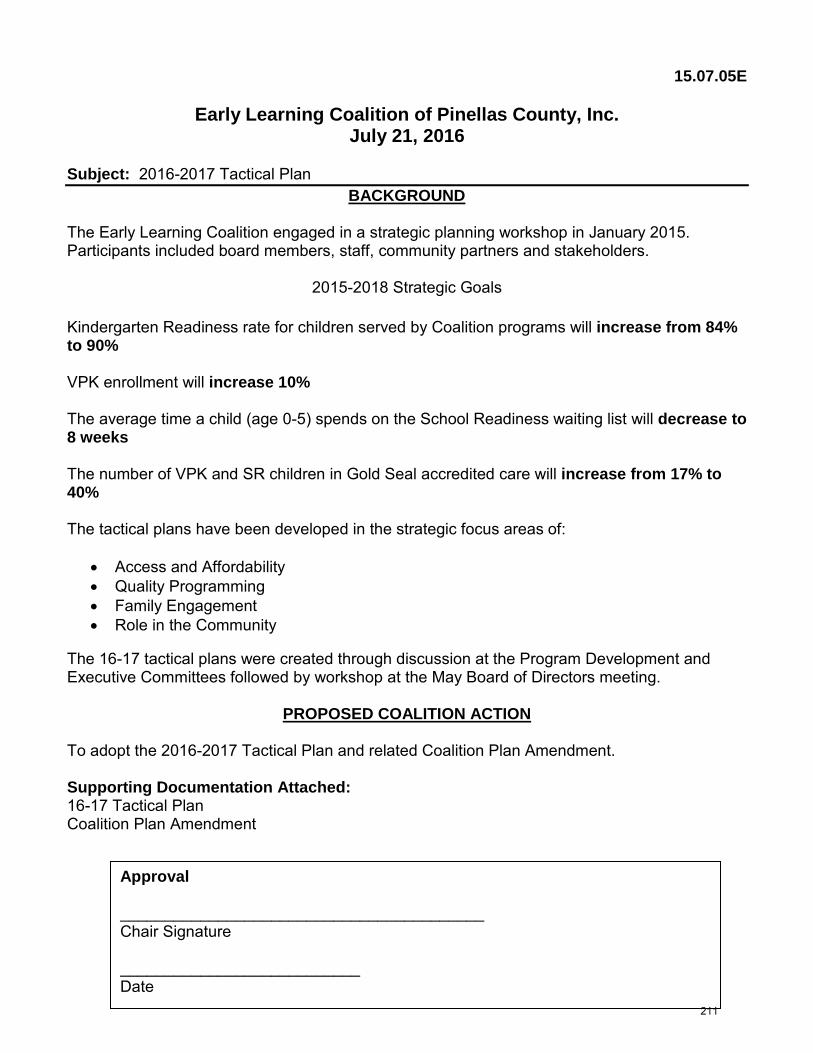

16.07.01E

Early Learning Coalition of Pinellas County, Inc. July 21, 2016

Subject: Fiscal Policy & Procedures

BACKGROUND

The Fiscal Policy and Procedures are part of the Coalition’s Standard Operating procedures. They summarize the fiscal policies and procedures of the Coalition.

The policies are consistent with the accounting principles prescribed by the American Institute of Certified Public Accountants.

Sections are designed to give a comprehensive overview of the Coalition organization, nature authority, accounting system, internal controls, and fiscal policies and procedures. The Coalition has updated the fiscal policy and procedures to align them with new federal regulations. The Office of Management and Budget (OMB) released final guidance, “Uniform Administrative Requirements, Cost Principles and Audit Requirements for Federal Awards also known as Uniform Grant Guidance or 2 CFR Part (200).

PROPOSED COALITION ACTION To approve the Coalition’s Fiscal Policy & Procedures. Supporting Documents:

• Fiscal Policy and Procedures Manual

Approval ______________________________ Chair Signature ______________________________ Date

4

EARLY LEARNING COALITION OF

PINELLAS COUNTY, INC.

Accounting & Financial

Policies and Procedures Manual

5

Effective Date(s) of Accounting Policies

The effective date of all accounting policies described in this manual is JULY 1, 2016. If a policy is added or modified subsequent to this date, the effective date of the new/revised policy will be indicated parenthetically immediately following the policy heading.

Policy: ELCPC 400.01

Effective Date of Policy: July 1, 2016

Date Last Amended: June 30, 2016

Date of Next Review (if policy requires periodic review): July 1, 2017

6

TABLE OF CONTENTS

SECTION 1: POLICIES

INTRODUCTION ..................................................................................................................................... 1

GENERAL POLICIES

ORGANIZATIONAL STRUCTURE .......................................................................................................... 2

The Role of the Board of Directors ........................................................................................................ 2

Committee Structure .............................................................................................................................. 2

Finance Committee Responsibilities ...................................................................................................... 3

Audit Committee Responsibilities .......................................................................................................... 3

The Roles of the Chief Executive Officer and Staff ................................................................................ 3

Example Organization Chart .................................................................................................................. 4

ACCOUNTING DEPARTMENT OVERVIEW ........................................................................................... 5

Organization .......................................................................................................................................... 5

Responsibilities ..................................................................................................................................... 5

Standards for Financial Management Systems ...................................................................................... 6

BUSINESS CONDUCT ............................................................................................................................ 7

Practice of Ethical Behavior ................................................................................................................... 7

Compliance with Laws, Regulations, and Organization Policies ............................................................ 7

CONFLICTS OF INTEREST .................................................................................................................... 8

Introduction ........................................................................................................................................... 8

What Constitutes a Conflict of Interest ................................................................................................... 8

Honoraria Acceptance ........................................................................................................................... 9

Disclosure Requirements..................................................................................................................... 10

Resolution of Conflicts of Interest ........................................................................................................ 11

Disciplinary Action for Violations of This Policy .................................................................................... 11

POLICY ON SUSPECTED MISCONDUCT ........................................................................................... 13

Introduction ......................................................................................................................................... 13

Definitions ........................................................................................................................................... 13

Reporting Responsibilities ................................................................................................................... 14

Whistleblower Protection ..................................................................................................................... 15

Investigative Responsibilities ............................................................................................................... 15

Protection of Records – Federal Matters ............................................................................................. 16

Disciplinary Action ............................................................................................................................... 16

Confidentiality ...................................................................................................................................... 16

Disclosure to Outside Parties .............................................................................................................. 17

SECURITY ............................................................................................................................................ 18

Accounting Department ....................................................................................................................... 18

Access to Electronically Stored Accounting Data ................................................................................. 18

Storage of Sensitive Data .................................................................................................................... 19

7

Destruction of Consumer Information .................................................................................................. 19

General Office Security ....................................................................................................................... 19

GENERAL LEDGER AND CHART OF ACCOUNTS............................................................................. 20

Chart of Accounts Overview ................................................................................................................ 20

Distribution of Chart of Accounts ......................................................................................................... 20

Control of Chart of Accounts ................................................................................................................ 20

Fiscal Year of Organization ................................................................................................................. 21

Accounting Estimates .......................................................................................................................... 21

Journal Entries .................................................................................................................................... 21

POLICIES ASSOCIATED WITH REVENUES & CASH RECEIPTS

REVENUE ............................................................................................................................................. 22

Revenue Recognition Policies ............................................................................................................. 22

Definitions ........................................................................................................................................... 22

ADMINISTRATION OF FEDERAL AWARDS ....................................................................................... 24

Definitions ........................................................................................................................................... 24

Preparation and Review of Proposals .................................................................................................. 24

Post-Award Procedures ....................................................................................................................... 24

Compliance with Laws, Regulations, and Provisions of Awards .......................................................... 25

Document Administration..................................................................................................................... 26

Closeout of Federal Awards ................................................................................................................ 27

COST SHARING AND MATCHING… ................................................................................................... 28

FUND RAISING ..................................................................................................................................... 29

Overview ............................................................................................................................................. 29

Receipt of Donations ........................................................................................................................... 30

Disclosures .......................................................................................................................................... 30 Credit Card Donations ......................................................................................................................... 31

State Registrations .............................................................................................................................. 31

BILLING/INVOICING POLICIES ........................................................................................................... 32

Overview ............................................................................................................................................. 32

Responsibilities for Billing and Collection ............................................................................................. 32

Billing and Financial Reporting ............................................................................................................ 32

Cash Advances ................................................................................................................................... 33

Accounts Receivable Entry Policies ..................................................................................................... 34

Classification of Income and Net Assets .............................................................................................. 34

CASH RECEIPTS .................................................................................................................................. 35

Overview ............................................................................................................................................. 35

Processing of Checks and Cash Received in the Mail ......................................................................... 35

Endorsement of Checks ...................................................................................................................... 36

Timeliness of Bank Deposits ............................................................................................................... 36

Credit Card Receipts ........................................................................................................................... 36

Reconciliation of Deposits ................................................................................................................... 36

Control Grid – Revenue and Cash Receipts ........................................................................................ 37

8

GRANTS RECEIVABLE MANAGEMENT ............................................................................................. 38

Monitoring and Recognition ................................................................................................................. 38

ACCOUNTS RECEIVABLE MANAGEMENT ........................................................................................ 39

Monitoring and Reconciliations ............................................................................................................ 39

Credits and Other Adjustments to Accounts Receivable ...................................................................... 39

Accounts Receivable Write-Off Authorization Procedures ................................................................... 39

POLICIES ASSOCIATED WITH EXPENDITURES & DISBURSEMENT

PURCHASING POLICIES AND PROCEDURES ................................................................................... 40

Overview ............................................................................................................................................. 40

Responsibility for Purchasing .............................................................................................................. 40

Code of Conduct in Purchasing ........................................................................................................... 40

Competition ......................................................................................................................................... 41

Nondiscrimination Policy ..................................................................................................................... 41

Procurement Procedures ..................................................................................................................... 41

Authorizations and Purchasing Limits .................................................................................................. 43 Approved Vendors ............................................................................................................................... 44 Use of Purchase Orders ...................................................................................................................... 44

Required Solicitation of Quotations from Vendors ............................................................................... 45

Extension of Due Dates and Receipt of Late Proposals ....................................................................... 46

Evaluation of Alternative Vendors ........................................................................................................ 46

Affirmative Consideration of Minority, Small Business, and Women-Owned Businesses ..................... 47

Availability of Procurement Records .................................................................................................... 47

Provisions Included in All Contracts ..................................................................................................... 48

Special Purchasing Conditions ............................................................................................................ 49

Right to Audit Clause ........................................................................................................................... 50

Vendor Files and Required Documentation ......................................................................................... 50

Procurement Grievance Procedures .................................................................................................... 50

Receipt and Acceptance of Goods ...................................................................................................... 50 Contract Administration ....................................................................................................................... 51

SUBRECIPIENTS .................................................................................................................................. 52

Making of Subawards .......................................................................................................................... 52 Monitoring of Subrecipients ................................................................................................................. 52

POLITICAL INTERVENTION ................................................................................................................ 55

Prohibited Expenditures ...................................................................................................................... 55

Endorsements of Candidates .............................................................................................................. 55

Individual vs. Organization Intervention ............................................................................................... 55

Prohibited Use of Organization Assets and Resources ........................................................................ 55

LOBBYING ............................................................................................................................................ 56

Introduction ......................................................................................................................................... 56

Definition of Lobbying Activities ........................................................................................................... 56

Segregation of Lobbying Expenditures ................................................................................................ 56

CHARGING OF COSTS TO FEDERAL AWARDS ................................................................................ 57

Overview ............................................................................................................................................. 57

9

Segregating Unallowable from Allowable Costs ................................................................................... 57

Criteria for Allowability ......................................................................................................................... 57

Indirect Cost Rate ................................................................................................................................ 58

Direct Costs ......................................................................................................................................... 58

Direct Costing Procedures ................................................................................................................... 59

ACCOUNTS PAYABLE MANAGEMENT .............................................................................................. 60

Overview ............................................................................................................................................. 60

Recording of Accounts Payable ........................................................................................................... 60

Accounts Payable Cutoff ..................................................................................................................... 60

Preparation of a Voucher Package ...................................................................................................... 61

Processing of Voucher Packages ........................................................................................................ 61

Payment Discounts.............................................................................................................................. 61

Employee Expense Reports ................................................................................................................ 62

Reconciliation of A/P Subsidiary Ledger to General Ledger ................................................................. 62

Management of Accounts Payable Vendor Master File ....................................................................... 62

Verification of New Contractors ........................................................................................................... 63

TRAVEL AND BUSINESS ENTERTAINMENT ..................................................................................... 63

Travel .................................................................................................................................................. 63

CELL PHONES ..................................................................................................................................... 64

Issuance of Corporate Cell Phones ..................................................................................................... 64

Cell Phone Plans ................................................................................................................................. 64

Employee Cell Phones ........................................................................................................................ 64

Personal Cell Phones or Similar Devices at Work ............................................................................... 64

CASH DISBURSEMENTS (CHECK-WRITING) POLICIES ................................................................... 65

Check Preparation ............................................................................................................................... 65

Check Signing ..................................................................................................................................... 66

Mailing of Checks ................................................................................................................................ 66

Voided Checks and Stop Payments .................................................................................................... 66

Recordkeeping Associated with Independent Contractors ................................................................... 67

Control Grid – Purchasing and Disbursements .................................................................................... 68

CREDIT CARDS/PURCHASING CARDS ............................................................................................. 69

Corporate Credit Cards ....................................................................................................................... 69

Sales Tax ............................................................................................................................................ 69

Card User Responsibilities .................................................................................................................. 70

Revocation of Corporate Credit Cards or Purchasing Cards ................................................................ 70

Employee Credit Cards ....................................................................................................................... 70

PAYROLL AND RELATED POLICIES .................................................................................................. 71

Classification of Workers as Independent Contractors or Employees .................................................. 71

Wage Comparability Study .................................................................................................................. 71

Payroll Administration .......................................................................................................................... 71

Changes in Payroll Data ...................................................................................................................... 72

Payroll Taxes ....................................................................................................................................... 73

Personnel Activity Reports ................................................................................................................... 73

10

Preparation of Timesheets ................................................................................................................... 73

Processing of Timesheets ................................................................................................................... 74

Review of Payroll ................................................................................................................................. 75

Distribution of Payroll ........................................................................................................................... 75

Internal Audit of Payroll Data ............................................................................................................... 75

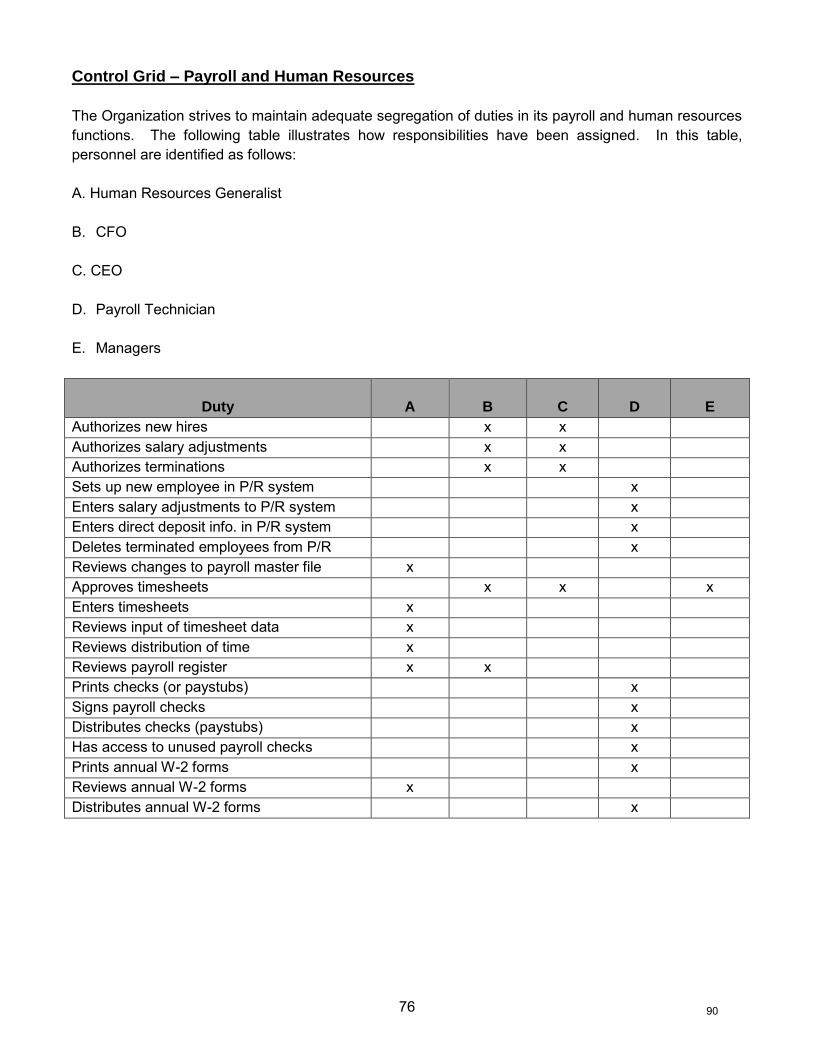

Control Grid – Payroll and Human Resources ..................................................................................... 76

POLICIES PERTAINING TO SPECIFIC ASSET ACCOUNTS

CASH AND CASH MANAGEMENT ...................................................................................................... 77

Cash Accounts .................................................................................................................................... 77

Authorized Signers .............................................................................................................................. 77

Bank Reconciliations ........................................................................................................................... 77

Cash Flow Management ...................................................................................................................... 78

Stale Checks ....................................................................................................................................... 79

Petty Cash ........................................................................................................................................... 79

Wire Transfers ..................................................................................................................................... 79

PREPAID EXPENSES ........................................................................................................................... 80

Accounting Treatment ......................................................................................................................... 80

Procedures .......................................................................................................................................... 80

INVESTMENT POLICIES ...................................................................................................................... 81

Introduction ......................................................................................................................................... 81

Delegation of Authority ........................................................................................................................ 81

Accounting Treatment ......................................................................................................................... 81

Procedures and Reporting ................................................................................................................... 82

PROPERTY AND EQUIPMENT ............................................................................................................ 83

Capitalization Policy ............................................................................................................................ 83

Contributed Assets .............................................................................................................................. 83

Equipment and Furniture Purchased with Federal Funds .................................................................... 83

Establishment and Maintenance of a Fixed Asset Listing .................................................................... 84

Receipt of Newly Purchased Equipment and Furniture ........................................................................ 84

Depreciation and Useful Lives ............................................................................................................. 85

Changes in Estimated Useful Lives ..................................................................................................... 85

Repairs of Property and Equipment ..................................................................................................... 85

Dispositions of Property and Equipment .............................................................................................. 86

Write-Offs of Property and Equipment ................................................................................................. 86

LEASES ................................................................................................................................................ 87

Classification of Leases ....................................................................................................................... 87

Reasonableness of Leases ................................................................................................................. 87

Accounting for Leases ......................................................................................................................... 87

Changes in Lease Terms..................................................................................................................... 88

SOFTWARE ACQUISITION AND DEVELOPMENT COSTS ................................................................ 89

Costs to Be Capitalized ....................................................................................................................... 89

Costs to Be Expensed As Incurred ...................................................................................................... 89

11

INTANGIBLE ASSETS .......................................................................................................................... 90

Acquisition of Intangible Assets ........................................................................................................... 90

Accounting for Intangible Assets.......................................................................................................... 90

Amortization ........................................................................................................................................ 90

FAIR VALUE ACCOUNTING ................................................................................................................ 92

Scope .................................................................................................................................................. 92

Disclosures .......................................................................................................................................... 92

POLICIES PERTAINING TO LIABILITY & NET ASSET ACCOUNTS

ACCRUED LIABILITIES ....................................................................................................................... 93

Identification of Liabilities ..................................................................................................................... 93

Accrued Leave .................................................................................................................................... 93

INCOME TAXES PAYABLE .................................................................................................................. 94

Accrual of Income Taxes ..................................................................................................................... 94

Income Tax Positions .......................................................................................................................... 94

NET ASSETS ........................................................................................................................................ 96

Classification of Net Assets ................................................................................................................. 96

Reclassifications from Restricted to Unrestricted Net Assets ............................................................... 96

Reclassifications from Unrestricted to Restricted Net Assets ............................................................... 96

Disclosures .......................................................................................................................................... 96

POLICIES ASSOCIATED WITH FINANCIAL &TAX REPORTING

FINANCIAL STATEMENTS .................................................................................................................. 98

Standard Financial Statements of the Organization ............................................................................. 98

Frequency of Preparation .................................................................................................................... 98

Review and Distribution ....................................................................................................................... 99

Monthly Distribution ............................................................................................................................. 99

Annual Financial Statements ............................................................................................................... 99

Trend Analysis ..................................................................................................................................... 99

GOVERNMENT RETURNS ................................................................................................................. 100

Overview ........................................................................................................................................... 100

Filing of Returns ................................................................................................................................ 100

Review of Form 990 by Board of Directors ........................................................................................ 101

Public Access to Information Returns ................................................................................................ 101

OTHER TAX CONSIDERATIONS ....................................................................................................... 103

State and Local Property, Sales, Use & Income Taxes ...................................................................... 103

State Charity Registrations ................................................................................................................ 103

TRANSACTIONS WITH INTERESTED PERSONS ............................................................................. 104

Identification of Interested Persons .................................................................................................... 104

Record of Transactions with Interested Persons ................................................................................ 104

UNRELATED BUSINESS ACTIVITIES ............................................................................................... 105

Identification and Classification ......................................................................................................... 105

Allocation of Expenses to Unrelated Activities ................................................................................... 105 12

Reporting ........................................................................................................................................... 105

FINANCIAL MANAGEMENT POLICIES

BUDGETING ....................................................................................................................................... 106

Overview ........................................................................................................................................... 106

Preparation and Adoption .................................................................................................................. 106

Monitoring Performance .................................................................................................................... 106

Budget and Program Revisions ......................................................................................................... 107

Budget Modifications ......................................................................................................................... 107

ANNUAL AUDIT .................................................................................................................................. 108

Role of the Independent Auditor ........................................................................................................ 108

Auditor Independence ....................................................................................................................... 108

How Often to Review the Selection of the Auditor ............................................................................. 109

Selecting an Auditor .......................................................................................................................... 109

Preparation for the Annual Audit ........................................................................................................ 110

Concluding the Audit ......................................................................................................................... 111

Audit Adjustments ............................................................................................................................. 111

Internal Control Deficiencies Noted During the Audit ......................................................................... 112

Audit Committee Communications with the Auditors .......................................................................... 112

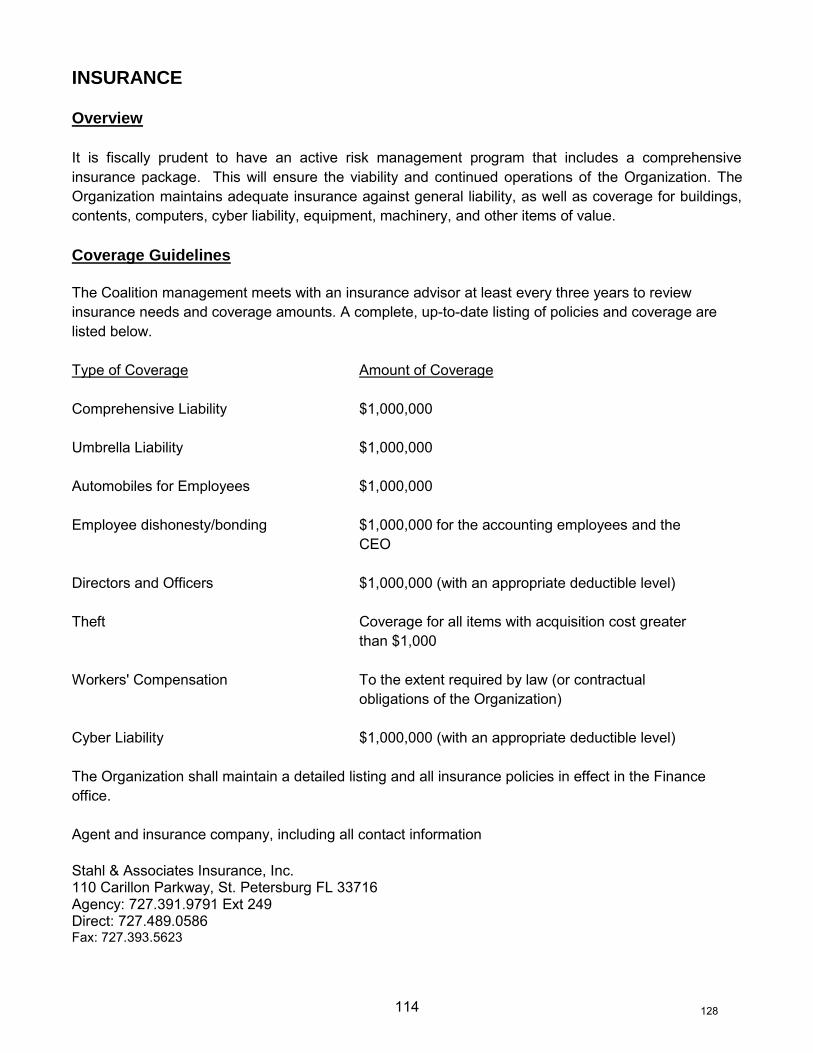

INSURANCE ....................................................................................................................................... 114

Overview ........................................................................................................................................... 114

Coverage Guidelines ......................................................................................................................... 114

Insurance Definitions ......................................................................................................................... 115

13

SECTION 2: FORMS

File Name

Form Name and Content

A01 - Check Request Check Request A02 – Travel Request Form Travel Request Form A03 - Purchase Request Form Purchase Request Form A04 - Purchase Order Purchase Order Form A05 – Bid Request Form Bid Request Form A06 - Journal Entry Form Journal Entry Form A07 - Invoice Form Invoice Form A08 - Travel Forms Travel Forms

14

1

INTRODUCTION

The following manual is intended to provide an overview of the accounting policies and procedures for the Early Learning Coalition of Pinellas County, Inc., which shall be referred to as “the Coalition” or “the Organization” throughout this manual. The Organization is incorporated in the state of Florida and is exempt from federal income taxes under IRS Section [501(c) (3)] as a nonprofit corporation. The Organization’s tax-exempt mission is to: “Lead the community in the development and delivery of a high quality early learning system and family support services that maximize each child's potential and promote the economic self-sufficiency of families”. This manual shall document the financial operations of the Organization. Its primary purpose is to formalize accounting policies and selected procedures for all staff that have a role in accounting processes and to document internal controls. If a particular grant or award has provisions that are more restrictive than those in this manual, the more restrictive provisions will be followed only for that grant or award. The contents of this manual were approved as official policy of the Organization by the Board of Directors, Chief executive Officer, and Chief Financial Officer. All Coalition staff members are bound by the policies herein, and any deviation from established policy is prohibited. The Board of Directors should approve this manual and all updates to it. It is the Coalition practice to present updates to the Finance Committee, and annually to the full Board for its approval.

15

2

GENERAL POLICIES

ORGANIZATIONAL STRUCTURE The Role of the Board of Directors

The Organization is governed by its Board of Directors, which is responsible for the oversight of the Organization by:

1. Planning for the future. 2. Establishing broad policies, including financial and personnel policies and procedures. 3. Approving grant applications. 4. Reviewing and approving the annual audit. 5. Reviewing financial information. 6. Identifying and proactively dealing with emerging issues. 7. Interpreting the Organization’s mission to the public. 8. Soliciting prospective contributors. 9. Hiring, evaluating, and working with the Chief Executive Officer (CEO). 10. Establishing and maintaining programs and systems designed to ensure compliance with terms

of contracts and grants. 11. Authorizing establishment of all bank accounts and check signers.

The CEO shall be responsible for the day-to-day oversight and management of the Organization.

Board of Directors Committee Structure

The Board of Directors shall form committees to assist the board in fulfilling its responsibilities. These committees are responsible for the review of particular programs and providing recommendations to the full board. Standing board-level committees of the Organization consist of the following:

1. Executive Committee 2. Finance Committee 3. Audit Committee 4. Board Development & Nominating Committee 5. Program Development Committee

See the Organization’s bylaws for board and committee details. However, roles of committees with direct responsibilities for the financial affairs of the Organization are further described in this manual. These committees shall be referred to in appropriate sections of this manual.

16

3

Finance Committee Responsibilities

The Finance Committee is responsible for direction and oversight regarding the overall financial management of the Organization. Functions of the Finance Committee include:

1. Review and recommendation of the Organization’s annual budget (prepared by the staff) for final approval by the full board.

2. Long-term financial planning. 3. Establishment of investment policy and monitoring investment performance. 4. Evaluation and approval of facilities decisions (i.e., leasing, purchasing property). 5. Monitoring of actual vs. budgeted financial performance. 6. Oversight of reserve funds. 7. Review of financial procedures.

The review of the Organization’s financial statements shall not be limited to the Finance Committee, but shall involve the entire Board of Directors. Audit Committee Responsibilities

The Audit Committee recommends an independent CPA firm to the full board for its approval. The Audit Committee communicates directly with the CPA firm for an annual audit, as described in the Organization’s bylaws. The full board shall review and approve the final audited financial statements and any other communications received from the auditor regarding internal controls, illegal acts, or fraud. The Audit Committee also serves as the primary point of contact for any employee who suspects that fraud has been committed against the Organization or by one of its employees or board members. The Audit Committee’s role in the annual audit is more fully explained in the section of this manual covering the annual audit. The Roles of the Chief Executive Officer and Staff

The Board of Directors hires the Chief Executive Officer (CEO), who reports directly to the board. The CEO is responsible for hiring and evaluating Department Directors for each of the Organization’s departments. Each Department Director reports to the CEO. All employees within a department shall report directly to their supervisor or to that department’s Department Director, according to the organization chart below. The Director and/or supervisors shall be responsible for managing and evaluating all employees within the department that they direct, manage and/or supervise.

17

4

Organization Chart

Board of Directors

Chief Executive Officer Administration

(Finance, HR, IT, Planning & Communication)

Auditor

Program Operations Quality Programs

Family Services

Provider Services

Resource & Referral Services

Child Screening Development &

Inclusion Services

Targeted TA to Providers

Professional Development

Community Partnership &

Public Relations

Federal State & Local Funding

18

5

ACCOUNTING DEPARTMENT OVERVIEW Organization Structure

The accounting department consists of 5 (five) staff members who manage and process financial information for the Organization. The following positions comprise the accounting department:

Chief Financial Officer Accounting Manager Fiscal Budget Specialist Contract Specialist Purchasing Specialist

Other officers and employees of the Organization who have financial responsibilities are as follows:

Chief Executive Officer Department Directors Human Resources Generalist/Payroll Executive Assistant - Cash Receipts Treasurer – Board level Finance Committee – Board level Audit Committee – Board level Executive Committee – Board level Full Board of Directors

Department Responsibilities

The primary responsibilities of the accounting department consist of:

General ledger Budgeting Cash and investment management Asset management Grants and contracts administration Purchasing Accounts receivable and billing Cash receipts Accounts payable Cash disbursements Payroll Financial statement processing External reporting of financial information Bank reconciliation Reconciliation of subsidiary ledgers Compliance with grant reporting requirements Annual audit Leases Insurance

19

6

Standards for Financial Management Systems

In accordance with 2 CFR Part 200, Uniform Administrative Requirements, Cost Principles, and Audit

Requirements for Federal Awards, the Coalition maintains a financial management system that provides for the following. Specific procedures to carry out these standards are detailed in the appropriate sections of this manual.

1. Identification, in all its accounts, of all Federal awards received and expended and the Federal programs under which they were received.

2. Accurate, current, and complete disclosure of the financial results of each federally-sponsored

project or program in accordance with the reporting requirements of 2 CFR Parts 200.327, Financial Reporting, and 200.328, Monitoring and Reporting Program Performance, and/or the award.

3. Records that identify adequately the source and application of funds for federally-funded

activities. These records must contain information pertaining to federal awards, authorizations, obligations, unobligated balances, assets, expenditures, income, and interest and be fully supported by source documentation.

4. Effective control over and accountability for all funds, property, and other assets. The

Organization must adequately safeguard all such assets and ensure they are used solely for authorized purposes.

5. Comparison of outlays with budget amounts for each award.

6. Information that relates financial data to performance accomplishments and demonstrates cost

effective practices as required by funding sources. (2 CFR Part 301, Performance

Measurement). 7. Written procedures to minimize the time elapsing between the transfer of funds and

disbursement of funds by the Coalition. Advance payments must be limited to the minimum amount needed and be timed to be in accordance with actual, immediate cash requirements (2

CFR Part 200.305 Payment).

8. Written procedures for determining the reasonableness, allocability, and allowability of costs in

accordance with the provisions of the 2 CFR Part 200 Subpart E, Cost Principles, and the terms and conditions of the award.

20

7

BUSINESS CONDUCT Practice of Ethical Behavior

The Organization requires board members, committee members, and employees to observe high standards of business and personal ethics in the conduct of their duties and responsibilities, and all directors, committee members, and employees to comply with all applicable laws and regulatory requirements. Unethical actions, or the appearance of unethical actions, are unacceptable under any conditions. The policies and reputation of the Organization depend to a very large extent on the following considerations. Each employee must apply her or his own sense of personal ethics, which should extend beyond compliance with applicable laws and regulations in business situations, to govern behavior where no existing regulation provides a guideline. Each employee is responsible for applying common sense in business decisions where specific rules do not provide all the answers. In determining compliance with this standard in specific situations, employees should ask themselves the following questions:

1. Is my action legal? 2. Is my action ethical? 3. Does my action comply with the Coalition policy? 4. Am I sure my action does not appear inappropriate? 5. Am I sure that I would not be embarrassed or compromised if my action became known within

the Organization or publicly? 6. Am I sure that my action meets my personal code of ethics and behavior? 7. Would I feel comfortable defending my actions on the 6 o’clock news?

Each employee should be able to answer "yes" to all of these questions before taking action. Each director, manager, and supervisor is responsible for the ethical business behavior of her or his subordinates. Directors, managers, and supervisors must carefully weigh all courses of action suggested in ethical, as well as economic, terms and base their final decisions on the guidelines provided by this policy, as well as their personal sense of right and wrong.

Compliance with Laws, Regulations, and Organization Policies

Our Organization does not tolerate:

The willful violation or circumvention of any federal, state, local, or foreign law by an employee during the course of that person's employment.

The disregard or circumvention of the Coalition policy or engagement in unscrupulous dealings.

Employees should not attempt to accomplish by indirect means, through agents or intermediaries, that which is directly forbidden. The performance of all levels of employees will be measured against implementation of the provisions of these standards.

21

8

CONFLICTS OF INTEREST This section addresses conflict of interest in business dealings. The Coalition has a separate conflict of interest policy: ELCPC 20.2 and shall comply in full with it. Introduction

In the course of business, situations may arise in which a Coalition’s decision maker has a conflict of interest, or in which the process of making a decision may create an appearance of a conflict of interest. All directors and employees have an obligation to:

1. Avoid conflicts of interest, or the appearance of conflicts, between their personal interests and those of the Organization in dealing with outside entities or individuals,

2. Disclose real and apparent conflicts of interest to the Board of Directors, and 3. Refrain from participation in any decisions on matters that involve a real conflict of interest or

the appearance of a conflict. What Constitutes a Conflict of Interest

All employees and directors of the Organization owe a duty of loyalty to the Organization. This duty necessitates that in serving the Organization they act solely in the interests of the Organization, not in their personal interests or in the interests of others. The persons covered under this policy shall hereinafter be referred to as “interested persons.” Interested persons include all members of the Board of Directors and all employees, as well as persons with the following relationships to directors or employees:

1. Spouses or domestic partners 2. Brothers and sisters 3. Parents, children, grandchildren, and great-grandchildren 4. Spouses of individuals listed in 2 and 3

5. Closed friendships 6. Corporations, partnerships, limited liability companies (LLCs), and other forms of businesses in

which an employee or director, either individually or in combination with individuals listed in 1, 2, 3, or 4, collectively possess a 35% or more ownership or beneficial interest.

The above list is not comprehensive. Other relationships may also cause a conflict of interest; however, each situation must be evaluated for potential conflict.

22

9

Conflicts of interest arise when the interests of an interested party may be seen as competing with those of the Organization. Conflicts of interest may be financial where an interested party benefits financially directly or indirectly or non-financial such as seeking preferential treatment, using confidential information, etc. A conflict of interest arises when a director or employee involved in making a decision is in the position to benefit, directly or indirectly, from his or her dealings with the Organization or person conducting business with the Organization. Examples of conflicts of interest include, but are not limited to, situations in which a director or employee:

1. Negotiates or approves a contract, purchase, or lease on behalf of the Organization and has a direct or indirect interest in, or receives personal benefit from, the entity or individual providing the goods or services.

2. Negotiates or approves a contract, sale, or lease on behalf of the Organization and has a direct

or indirect interest in, or receives personal benefit from, the entity or individual receiving the goods or services.

3. Employs or approves the employment of, or supervises a person who is an immediate family

member of the director or employee. 4. Sells products or services in competition with the Organization. 5. Uses the Organization’s facilities, other assets, employees, or other resources for personal gain. 6. Receives a substantial gift from a vendor, if the director or employee is responsible for initiating

or approving purchases from that vendor.

Honoraria Acceptance

The Organization employee shall not accept an honorarium for an activity conducted where agency-reimbursed travel, work time, or resources are used or where the activity can be construed as having a relationship to the employee's position with the Organization; such activity would be considered official duty on behalf of the Organization. A relationship exists between the activity and the employee's position with the Organization if the employee would not participate in the activity in the same manner or capacity if they did not hold their position with the Organization. The employee should make every attempt to avoid the appearance of impropriety. An employee may receive an honorarium for activities performed during regular non-working hours or while on annual leave if the following conditions are met:

All expenses are the total responsibility of the employee or the sponsor of the activity in which the employee is participating.

The activity has no relationship to the employee's Organization duties.

23

10

Nothing in this policy shall be interpreted as preventing the payment to the Organization by an outside source for actual expenses incurred by an employee in an activity, or the payment of a fee to the Organization (in lieu of an honorarium to the individual) for the services of the employee. Any such payments made to the Organization should be deposited to the Organization account and an appropriate entry should be made coded to the same program or department to which the employee’s corresponding time was charged. Disclosure Requirements

A director or employee who believes that he or she may be perceived as having a conflict of interest in a discussion or decision must disclose that conflict to the group making the decision. Most concerns about conflicts of interest may be resolved and appropriately addressed through prompt and complete disclosure. Therefore, the Organization requires the following:

1. At the inception of employment or volunteer service to the Organization, and on an annual basis thereafter, the accounting department shall distribute a list of all contractors with whom the Organization has transacted business at any time during the preceding year, along with a copy of the disclosure statement to all members of the Board of Directors, the CEO, members of senior management, and employees with purchasing and/or hiring responsibilities or authority. Using the prescribed form, these individuals shall inform, in writing and with a signature, the CEO and the chair of the Audit Committee, of all potential reportable conflicts.

2. During the year, these individuals shall submit a signed, updated disclosure form if any new

potential conflict arises. 3. The CEO shall review all forms completed by employees, and the Audit Committee shall review

all forms completed by directors and the CEO and determine appropriate resolution in accordance with the next section of this policy.

4. Prior to management, board, or committee action on a contract or transaction involving a conflict

of interest, a staff, director, or committee member having a conflict of interest and who is in attendance at the meeting shall disclose all facts material to the conflict of interest. Such disclosure shall be reflected in the minutes of the meeting.

5. A staff, director, or committee member who plans not to attend a meeting at which he or she

has a reason to believe that the management, board, or committee will act on a matter in which the person has a conflict of interest shall disclose to the chair of the meeting all facts material to the conflict of interest. The chair shall report the disclosure at the meeting and the disclosure shall be reflected in the minutes of the meeting.

6. A person who has a conflict of interest shall not participate in or be permitted to hear

management’s, the board’s, or the committee’s discussion of the matter except to disclose material facts and to respond to questions. Such person shall not attempt to exert his or her personal influence with respect to the matter.

24

11

7. A person who has a conflict of interest with respect to a contract or transaction that will be voted on at a meeting shall not be counted in determining a quorum for purposes of the vote. The person having a conflict of interest may not vote on the contract or transaction and shall not be present in the meeting room when the vote is taken, unless the vote is by secret ballot. Such person’s ineligibility to vote and abstention from voting shall be reflected in the minutes of the meeting. For purposes of this paragraph, a member of the Board of Directors of Sample Organization has a conflict of interest when he or she stands for election as an officer or for re-election as a member of the Board of Directors.

8. Board and staff members with procurement responsibilities will annually review a list of vendors to identify potential conflicts of interest.

9. If required by the awarding agencies, the Organization will notify those agencies in writing of any potential conflict of interest (2 CFR Part 200.112, Conflict of interest).

Resolution of Conflicts of Interest

All real or apparent conflicts of interest shall be disclosed to the Audit Committee and the CEO of the Organization. Conflicts shall be resolved as follows:

The Audit Committee shall be responsible for making all decisions concerning resolutions of conflicts involving directors, the CEO, and other members of senior management.

The chair of the committee shall be responsible for making all decisions concerning resolutions of conflicts involving Audit Committee members.

The chair of the Board shall be responsible for making all decisions concerning resolutions of the conflict involving the chair of the Audit Committee.

The CEO shall be responsible for making all decisions concerning resolutions of conflicts involving employees below the senior management level, subject to the approval of the Audit Committee.

An employee or director may appeal the decision that a conflict (or appearance of conflict) exists as follows:

An appeal must be directed to the chair of the board. Appeals must be made within 30 days of the initial determination. Resolution of the appeal shall be made by vote of the full Board of Directors. Board members who are the subject of the appeal, or who have a conflict of interest with

respect to the subject of the appeal, shall abstain from participating in, discussing, or voting on the resolution, unless their discussion is requested by the remaining members of the board.

Disciplinary Action for Violations of This Policy

Failure to comply with the standards contained in this policy will result in disciplinary action that may include termination, referral for criminal prosecution, and reimbursement to the Organization or to the government, for any loss or damage resulting from the violation. As with all matters involving disciplinary action, principles of fairness will apply. Any employee charged with a violation of this policy will be afforded an opportunity to explain her or his actions before disciplinary action is taken.

25

12

Disciplinary action will be taken:

1. Against any employee who authorizes or participates directly in actions that are a violation of this policy.

2. Against any employee who has deliberately failed to report a violation or deliberately withheld

relevant and material information concerning a violation of this policy. 3. Against any director, manager, or supervisor who attempts to retaliate, directly or indirectly, or

encourages others to do so, against any employee who reports a violation of this policy. A Board member who violates this policy will be removed from the Board.

26

13

POLICY ON SUSPECTED MISCONDUCT Introduction

This policy communicates the actions to be taken for suspected misconduct committed, encountered, or observed by employees and volunteers. Like all organizations, the Coalition faces many risks associated with fraud, abuse, and other forms of misconduct. The impact of these acts collectively referred to as misconduct throughout this policy, may include, but not be limited to:

Financial losses and liabilities. Loss of current and future revenue and customers. Negative publicity and damage to the Organization’s good public image. Loss of employees and difficulty in attracting new personnel. Deterioration of employee morale. Harm to relationships with clients, vendors, bankers, and subcontractors. Litigation and related costs of investigations, etc.

Our Organization is committed to establishing and maintaining a work environment of the highest ethical standards. Achievement of this goal requires the cooperation and assistance of every employee and volunteer at all levels of the Organization. Definitions

For purposes of this policy, misconduct includes, but is not limited to:

1. Actions that violate the Organization’s Code of Conduct (and any underlying policies) or any of the accounting and financial policies included in this manual.

2. Fraud (see below). 3. Forgery or alteration of checks, bank drafts, documents or other records (including electronic

records). 4. Destruction, alteration, mutilation, or concealment of any document or record with the intent to

obstruct or influence an investigation, or potential investigation, carried out by a department or agency of the federal government or by the Organization in connection with this policy.

5. Disclosure to any external party of proprietary information or confidential personal information

obtained in connection with employment with or service to the Organization. 6. Unauthorized personal or other inappropriate (non-business) use of equipment, assets,

services, personnel, or other resources. 7. Acts that violate federal, state, or local laws or regulations.

27

14

8. Accepting or seeking anything of material value from contractors, vendors, or persons providing goods or services to the Organization. Exception: gifts valued at $25 or less.

9. The Organizations may permit employees to accept gifts of nominal value. The definition of “nominal value” is determined by the Management and is set at $25.

10. Impropriety of the handling or reporting of money in financial transactions. 11. Failure to report known instances of misconduct in accordance with the reporting responsibilities

described herein (including tolerance by supervisory employees of misconduct of subordinates). Fraud is further defined to include, but not be limited to:

Theft, embezzlement, or other misappropriation of assets (including assets of or intended for the Organization, as well as those of our clients, subcontractors, vendors, contractors, suppliers, and others with whom the Organization has a business relationship).

Intentional misstatements in the Organization’s records, including intentional misstatements of accounting records or financial statements.

Authorizing or receiving payment for goods not received or services not performed. Authorizing or receiving payments for hours not worked. Forgery or alteration of documents, including but not limited to checks, timesheets, contracts,

purchase orders, receiving reports. The Organization prohibits each of the preceding acts of misconduct on the part of employees, officers, executives, volunteers, and others responsible for carrying out the Organization’s activities. Reporting Responsibilities

All employees, officers, and volunteers are responsible for immediately reporting suspected misconduct to their supervisor, Chief Financial Officer (CFO), or the Chair of the Audit Committee. When supervisors have received a report of suspected misconduct, they must immediately report such acts to their manager, the CFO, or the Chair of the Audit Committee. In addition, the Coalition has set up a telephone hotline that can be accessed 24 hours per day to report suspected misconduct. As a best practice, the Coalition has arranged for some form of anonymous reporting of allegations of violations of the code of conduct. All reporting of allegations of violations can be reported to the Coalition line: 727.400.4458.

28

15

Whistleblower Protection

The Organization will consider any reprisal against a reporting individual an act of misconduct subject to disciplinary procedures. A “reporting individual” is one who, in good faith, reported a suspected act of misconduct in accordance with this policy, or provided to a law enforcement officer any truthful information relating to the commission or possible commission of a federal offense or any other possible violation of the Organization’s Code of Conduct. The final element of the preceding policy, pertaining to protection of whistleblowers reporting possible federal offenses, is a required element of the Sarbanes-Oxley Act of 2002 (SOX). A question regarding whether the organization has a whistleblower policy is also on Form 990. Although the SOX whistleblower requirements apply only to possible federal offenses, the Coalition is advised to expand the policy to cover allegations of any violation of the organization’s code of conduct/ethics. Investigative Responsibilities

Due to the sensitive nature of suspected misconduct, supervisors and managers should not, under any circumstances, perform any investigative procedures. The CFO has the primary responsibility for investigating suspected misconduct involving employees below the CEO and executive management level. The CFO shall provide a summary of all investigative work to the Audit Committee. The Audit Committee has the primary responsibility for investigating suspected misconduct involving CEO and executive level positions, as well as board members and officers. However, the Audit Committee may request the assistance of the CFO in any such investigation. Investigation into suspected misconduct will be performed without regard to the suspected individual’s position, length of service, or relationship with the Organization. In fulfilling its investigative responsibilities, the Audit Committee shall have the authority to seek the advice and/or contract for the services of outside firms, including but not limited to law firms, CPA firms, forensic accountants and investigators, etc. Members of the investigative team (as authorized by the Audit Committee) shall have free and unrestricted access to all Organization records and premises, whether owned or rented, at all times. They shall also have the authority to examine, copy, and remove all or any portion of the contents (in paper or electronic form) of filing cabinets, storage facilities, desks, credenzas and computers without prior knowledge or consent of any individual who might use or have custody of any such items or facilities when it is within the scope of an investigation into suspected misconduct or related follow-up procedures. The existence, the status, or results of investigations into suspected misconduct shall not be disclosed or discussed with any individual other than those with a legitimate need to know in order to perform their duties and fulfill their responsibilities effectively.

29

16

Protection of Records – Federal Matters

The Organization prohibits the knowing destruction, alteration, mutilation, or concealment of any record, document, or tangible object with the intent to obstruct or influence the investigation or proper administration of any matter within the jurisdiction of any department or agency of the United States government, or in relation to or contemplation of any such matter or case. Violations of this policy will be considered violations of the Organization’s Code of Ethics and subject to the investigative, reporting, and disclosure procedures described earlier in this Policy on Suspected Misconduct. Such policy is required in order to comply with the Sarbanes-Oxley Act of 2002. Violators are subject to criminal penalties. Disciplinary Action

Based on the results of investigations into allegations of misconduct, disciplinary action may be taken against violators. Disciplinary action shall be coordinated with appropriate representatives from the Human Resources Department. The seriousness of misconduct will be considered in determining appropriate disciplinary action, which may include:

Reprimand Probation Suspension Demotion Termination Reimbursement of losses or damages Referral for criminal prosecution or civil action

This listing of possible disciplinary actions is for information purposes only and does not bind the Organization to follow any particular policy or procedure. Confidentiality

The Audit Committee and the CFO treat all information received confidentially. Any employee who suspects dishonest or fraudulent activity will notify the CFO or the Audit Committee Chair immediately, and should not attempt to personally conduct investigations or interviews/interrogations related to any suspected fraudulent act (see Reporting Procedures section above). Great care must be taken in the investigation of suspected improprieties or irregularities so as to avoid mistaken accusations or alerting suspected individuals that an investigation is under way. Investigation results will not be disclosed or discussed with anyone other than those who have a legitimate need to know. This is important in order to avoid damaging the reputations of persons suspected but subsequently found innocent of wrongful conduct and to protect the Organization from potential civil liability.

30

17

An employee who discovers or suspects fraudulent activity may remain anonymous. All inquiries concerning the activity under investigation from the suspected individual(s), his or her attorney or representative(s), or any other inquirer should be directed to the Audit Committee or legal counsel. No information concerning the status of an investigation will be given out. The proper response to any inquiry is “I am not at liberty to discuss this matter.” Under no circumstances should any reference be made to “the allegation,” “the crime,” “the fraud,” “the forgery,” “the misappropriation,” or any other specific reference. The reporting individual should be informed of the following:

1. Do not contact the suspected individual in an effort to determine facts or demand restitution. 2. Do not discuss the case, facts, suspicions, or allegations with anyone unless specifically asked

to do so by the Organization’s legal counsel or the Audit Committee.

Disclosure to Outside Parties