Embed Size (px)

Citation preview

CONTENTS

EXECUTIVE SUMMARY………………………………………………………………………i

COUNTRY CONTEXT AND DEVELOPMENT CHALLENGES ......................................... 1

A. POLITICAL, SOCIAL AND ECONOMIC CONTEXT AND CHALLENGES ......................................... 1

B. INDONESIA’S NEW ECONOMIC POLICY PACKAGE: THE SHORT-TERM AGENDA ...................... 5

C. THE EMERGING PRSP: A MEDIUM-TERM FRAMEWORK FOR POVERTY REDUCTION ............... 8

D. ECONOMIC OUTLOOK, EXTERNAL ENVIRONMENT AND FINANCING NEEDS ............................ 8

THE WORLD BANK IN INDONESIA: LEARNING FROM RECENT EXPERIENCE.. 10

A. LESSONS FROM THE TRANSITION PERIOD .............................................................................. 10

B. THE SPECIAL PROBLEM OF CORRUPTION............................................................................... 11

THE BANK GROUP’S ASSISTANCE PROGRAM .............................................................. 16

A. THE WORLD BANK GROUP’S STRATEGIC FOCUS .................................................................. 16

Objective I: Improving the Climate for High Quality Investment.................................... 16

Objective II: Making Service Delivery Responsive to the Needs of the Poor.................. 21

The Core Issue of Governance—Defining Selectivity ..................................................... 25

B. BUSINESS PLATFORMS—HOW THE WORLD BANK WILL DELIVER .................................. 27

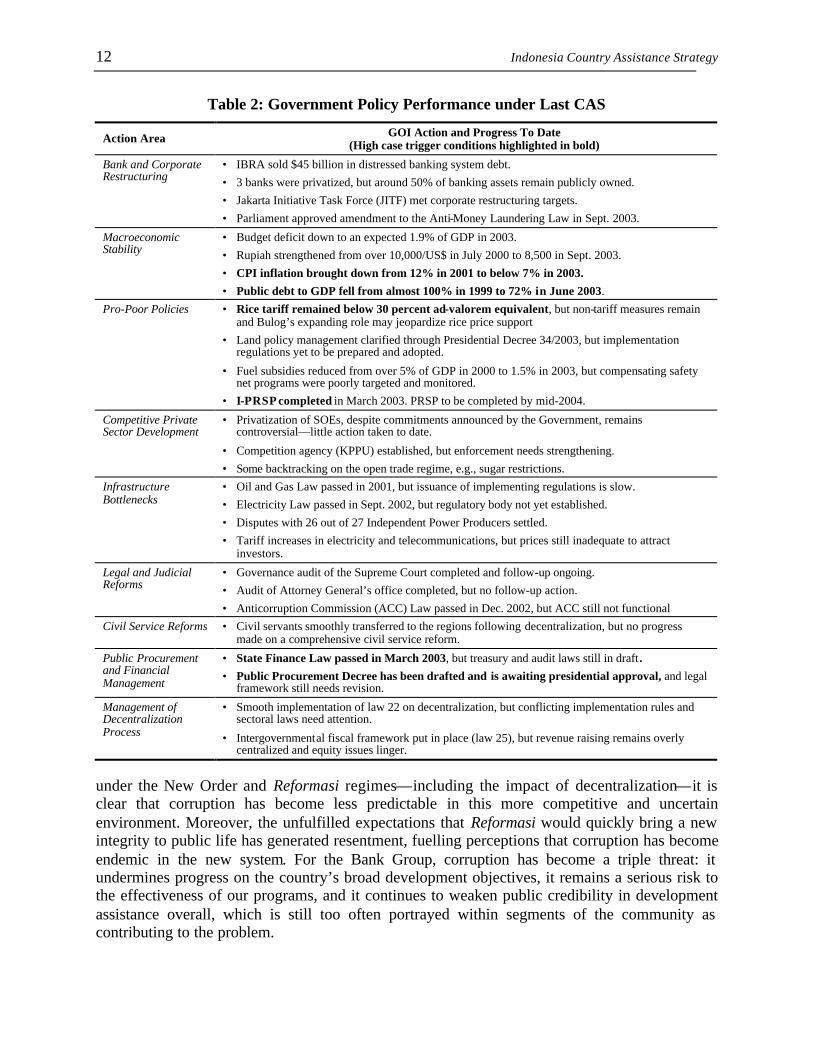

The Community Driven Development Platform............................................................... 28

The Local Services Platform............................................................................................. 30

The Public Utility Platform............................................................................................... 31

The “National” Lending Platform..................................................................................... 32

DELIVERING THE WORLD BANK PROGRAM ................................................................ 33

A. MANAGING THE PORTFOLIO AND MONITORING FOR RESULTS .............................................. 33

B. BUILDING CAPACITY AND INFORMING DECISION MAKING .................................................... 34

C. LENDING SCENARIOS, TRIGGERS AND BANK EXPOSURE ....................................................... 37

D. IFC AND MIGA PROGRAMS................................................................................................. 42

E. PARTNERSHIPS....................................................................................................................... 43

MANAGING RISKS .................................................................................................................. 45

Indonesia Country Assistance Strategy

ANNEXES

A1: Key Economic and Program Indicators A2: Indonesia at a Glance B2: Selected Indicators of Bank Portfolio Performance and Management B3: Bank Group Program Summary—Base Case Lending Program B3: Bank Group Fact Sheet—IFC and MIGA Program B4: Summary of Non-lending Services B5: Social Indicators B6: Key Economic Indicators B7: Key Exposure Indicators B8: Operations Portfolio B8: Statement of IFC’s Held and Disbursed Portfolio B9: CAS Program Matrix B10: CAS Summary of Development Priorities B11: Key Environmental Indicators C. Macroeconomic Performance and Prospects D. Poverty Profile & Analytical Agenda E. Summary of CAS Consultations F. Environment G. Proposed Program of IFC & MIGA

TABLES

Table 1: Progress towards Achieving the Millennium Development Goals....................................4 Table 2: Government Policy Performance under Last CAS ..........................................................12 Table 3: Improving Investment Climate for Poverty Reduction: Targeted Results ......................17 Table 4: Making Services Work for the Poor: Targeted Results ...................................................23 Table 5: Governance: Targeted Results.........................................................................................25 Table 6: Indonesia CAS FY04--FY07: Expected Lending (US$ million) ....................................29 Table 7: The Performance of the Bank's Portfolio during the Last CAS Period (percentages)....33 Table 8: AAA Indicative Key Outputs By Theme .........................................................................36 Table 9: Indonesia CAS Trigger Matrix FY04—FY06 .................................................................38 Table 10: Expected Lending FY04-07...........................................................................................42

BOXES

Box 1: Lessons from OED Reviews and the Last CAS .................................................................11 Box 2: CAS Consultations Highlight Indonesia’s Development Challenges ................................13 Box 3. The Program for Eastern Indonesia SME Assistance (PENSA) ........................................19 Box 4: Support for Poor Rural Households and Farmers ..............................................................21 Box 5: Improving Service Delivery Through Greater Accountability .........................................22 Box 6: The Challenge of Forest Resources Management in Indonesia .........................................29 Box 7: Framework for Achievement of the “Enhanced” Base Case .............................................39 Box 8: Fiduciary Environment: Progress and Next Steps .............................................................40

Indonesia Country Assistance Strategy

FIGURES

Figure 1: A Snapshot of Indonesia’s Economy ...............................................................................2 Figure 2: Indonesia Country Policy and Institutional Assessment ..................................................6 Figure 3: The CAS Framework......................................................................................................16 Figure 4: Total External and IBRD Debt Outstanding ..................................................................41 MAP (IBRD No. 30903R4)

Indonesia Country Assistance Strategy

ABBREVIATIONS AND ACRONYMS

AAA Analytical and Advisory Activities ACC Anti-corruption Commission ADB Asian Development Bank ASEM Asia-Europe Meetings AusAID Australian International Development

Agency BCP Business Continuity Plan BKPM Chairman of Investment Coordinating Board BPK Supreme Audit Board BPS Indonesian Bureau of Statistics BRI Bank Rakyat Indonesia CAS Country Assistance Strategy CDD Community Demand Driven CGI Consultative Group on Indonesia CFAA Country Financial Accountability

Assessment COREMAP Coral Reef Rehabilitation and Management

Project CPAR Country Procurement Assessment Report CPI Consumer Price Index CPIA Country Performance Institutional

Assessment CPPR Country Portfolio Performance Review DFID Department for International Development

(United Kingdom) DPRDs Local Parliaments EFF Extended Fund Facility ESW Economic Sector Work FATF Financial Action Task Force FDI Foreign Direct Investment FEATI Farmer Empowerment through Agriculture

Technology & Information Project FY Fiscal Year GDP Gross Domestic Product GDS Governance and Decentralization Survey GEG Good Environmental Governance GOI Government of Indonesia IAIS International Association of Insurance

Supervisors IBRA Indonesian Bank Restructuring Agency IBRD International Bank for Reconstruction And

Development ICRG International Country Risk Guide IDA International Development Association IEDF Indonesia Eastern Development Facility IFC International Finance Corporation ILGRP Initiative for Local Governance Reform

Project IMF International Monetary Fund INT Dep. of Institutional Integrity IOSCO International Organization of Securities

Commissions IPO Initial Public Offering I-PRSP Indonesian Poverty Reduction Strategy

Paper

JBIC Japan Bank for International Cooperation JICA Japan International Cooperation Agency JITF Jakarta Initiative Task Force KDP Kecamatan Development Project KKN Corruption, Collusion, Nepotism KPPU Business Competition Supervisory

Commission LOI Letter of Intent MDG Millennium Development Goals M & E Monitoring and Evaluation MFA Multi Fiber Agreement MIGA Multilateral Investment Guarantee Agency MOF Ministry of Finance NGO Non Government Organization NPPO National Public Procurement Office OED Operations Evaluation Department PDAM Water Utility PENSA Program for Eastern Indonesia SME

Assistance PER Public Expenditure Review PERDAs Peraturan Daerah (local regulations) PERPAMSI Association of Water Enterprises PGN State Gas Company PHP Provincial Health Projects PLN State Electricity Company PPA Participatory Poverty Assessments PROPENAS GOI five-year plan PROPER Program for Pollution Control Evaluation

and Rating PRSP Poverty Reduction Strategy Paper QAE Quality Assessment Evaluation QAG Quality Assurance Group REPETA Annual Development Plan ROSC Report on Observance of Standards and

Codes SME Small- and Medium-size Enterprise SOEs State-owned Enterprises STPDN Public Administration Institute of the

Ministry of Home Affairs TA Technical Assistance TIMMS Third International Mathematics and Science

Study UNDP United Nations Development Fund UPP Urban Poverty Project USDRP Urban Sector Development Reform Program WASPOLA Water Supply and Sanitation Policy

Formulation and Action Planning Project WBI World Bank Institute WDR World Development Report WHO World Health Organization WISMP Water Resources and Irrigation Reform

Implementation Project WSSLIC The Water Supply and Sanitation for Low-

Income Communities

Indonesia Country Assistance Strategy i

EXECUTIVE SUMMARY

i. Country Context. Indonesia continues its transition from an autocratic, centralized state to a democratic, decentralized one. It has successfully regained macroeconomic and political stability, but economic growth remains below 4 percent, poverty reduction remains a challenge, and governance concerns continue to cloud its achievements. Public debt has declined from 100 percent of GDP to 72 percent, inflation is now below 7 percent, and income poverty has fallen from 27 percent in 1999 to 16 percent today. However, 110 million people still live on less than $2 a day, and remain vulnerable to falling back into severe poverty. Indonesia continues to under-perform its neighbors in access to quality health, education and other basic services, as reflected in the MDG indicators. Weak governance institutions are keeping investors away and undermining service provision, especially to the poor. Indonesia has undertaken reforms that could lead to a more effective and accountable government, and a restoration of growth. But sound implementation is now needed to turn the promise into reality.

ii. The Government’s Reform Program. Following its decision not to renew the IMF program after 2003,1 the Government prepared a comprehensive package of policy reforms through the end of 2004. This “letter of intent to the Indonesian people” provides an agenda of time-bound actions, covering macroeconomic management, financial sector reform, and policies to help raise investment and reduce poverty. The package is ambitious – especially for an election year -- but represents an important effort to spur the momentum of reforms, and serves as a mechanism to monitor the Government’s progress on the basis of its own stated benchmarks. With steady progress on this reform package, and an effective PRSP,2 growth over the CAS period is expected to reach 5 percent by 2006, enabling poverty to decline to 11 percent by 2007.

iii. The Bank Group Strategy. Further progress in reducing poverty is prevented by two major factors—low investment, and weak service provision—which in turn are caused primarily by problems of governance. The Bank Group’s entire efforts -- in the form of analytical and advisory services, lending, IFC and MIGA activities, and donor coordination -- will be to help address these problems.

• Improving the Climate for High Quality Investment. Bank Group support will be directed to address five key areas that are essential to raise the rate of investment from its current level of 20 percent of GDP: deepening macroeconomic stability, building a stronger financial sector, fostering a competitive private sector, building Indonesia’s infrastructure, and creating income opportunities for poor households and farmers.

• Making Service Delivery Responsive to the Needs of the Poor. Weak service delivery is undermining Indonesia’s goal of improving the quality of life of its citizens and the attainment of its MDGs. Bank Group support will thus be devoted to help revamp the management and accountability systems for service delivery to make providers more directly accountable to their clients. Focus will be given to implementing the principles of the World Development Report 2004, especially in health and education, but also in agricultural research, extension and irrigation, and in public services in general.

• The Core Issue of Governance. Advances in governance will be needed to address both CAS objectives. Four areas will be given priority: (i) making development planning more responsive to

1The IMF will engage in post-program monitoring beginning in 2004. 2As a blend country, Indonesia’s PRSP preparation is not directly linked to IDA access and was therefore not a pre-requisite for Bank CAS preparation. Indonesia’s I-PRSP was circulated to the Board in March 2003, and its full PRSP is due to be completed in mid-2004.

ii Indonesia Country Assistance Strategy

constituents; (ii) improving public financial management; (iii) strengthening the accountability of local governments under a more coherent decentralization framework; and (iv) enhancing the public credibility, impartiality and accessibility of the justice sector. Selectivity in the Bank’s activities will be determined less by sectoral priorities than by the opportunity to make progress in these areas. Corruption poses a special problem in Indonesia, and the country team aims to integrate governance and corruption issues through the entire Indonesia program, shaping how projects are selected, designed, implemented and monitored.

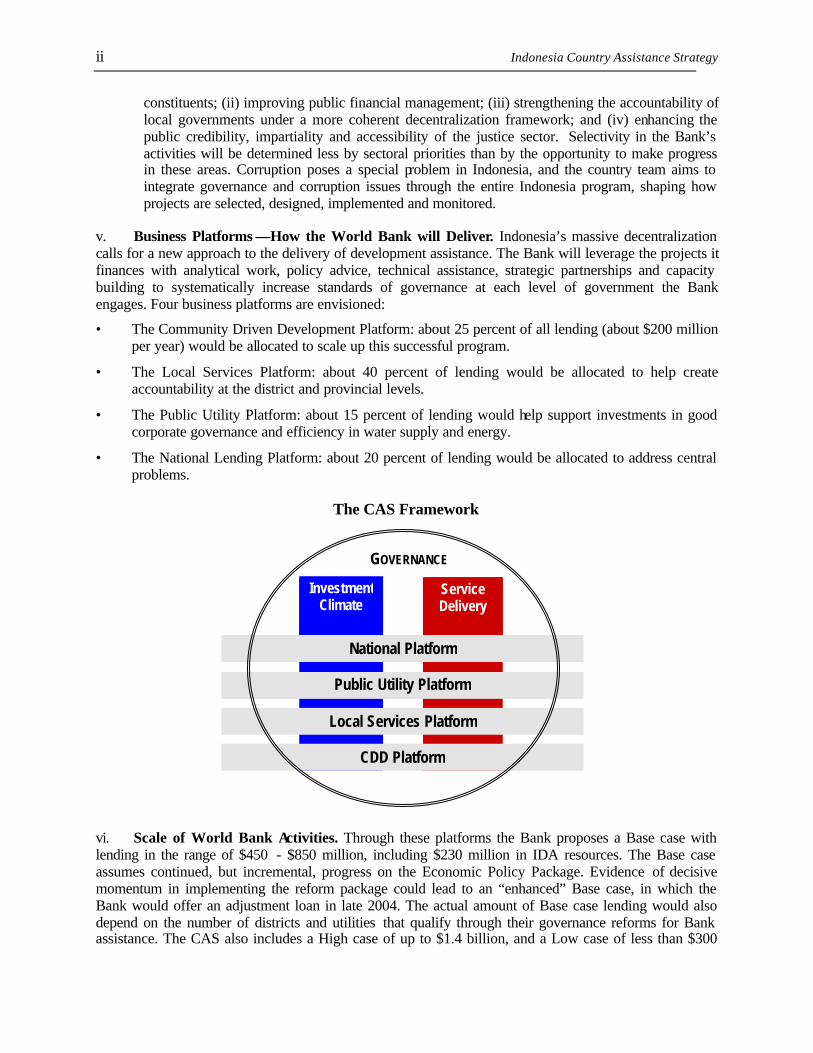

v. Business Platforms —How the World Bank will Deliver. Indonesia’s massive decentralization calls for a new approach to the delivery of development assistance. The Bank will leverage the projects it finances with analytical work, policy advice, technical assistance, strategic partnerships and capacity building to systematically increase standards of governance at each level of government the Bank engages. Four business platforms are envisioned:

• The Community Driven Development Platform: about 25 percent of all lending (about $200 million per year) would be allocated to scale up this successful program.

• The Local Services Platform: about 40 percent of lending would be allocated to help create accountability at the district and provincial levels.

• The Public Utility Platform: about 15 percent of lending would help support investments in good corporate governance and efficiency in water supply and energy.

• The National Lending Platform: about 20 percent of lending would be allocated to address central problems.

The CAS Framework

vi. Scale of World Bank Activities. Through these platforms the Bank proposes a Base case with lending in the range of $450 - $850 million, including $230 million in IDA resources. The Base case assumes continued, but incremental, progress on the Economic Policy Package. Evidence of decisive momentum in implementing the reform package could lead to an “enhanced” Base case, in which the Bank would offer an adjustment loan in late 2004. The actual amount of Base case lending would also depend on the number of districts and utilities that qualify through their governance reforms for Bank assistance. The CAS also includes a High case of up to $1.4 billion, and a Low case of less than $300

Investment Climate Service

Delivery

National Platform

Public Utility Platform

Local Services Platform

CDD Platform

GOVERNANCE

Indonesia Country Assistance Strategy iii

million. The High case triggers have all been selected from the Government’s Economic Policy Package as those most important to achieving target outcomes in the three CAS areas and putting the country on a path to stronger growth and better living standards.

vii. Program Delivery—Portfolio Management, Analytical and Advisory Services (AAA), and Partnerships. Despite challenges of portfolio management across a large country with significant corruption risks, portfolio performance has improved with commitments at risk down from 39 percent (FY02) to 12 percent (FY03), and disbursements remaining above 20 percent. Portfolio risks will be managed by building external monitoring mechanisms into project designs, requiring anti-corruption strategies for each project and using the platform approach to maximize the effectiveness of supervision. The platforms will also bring more coherence to capacity building activities with the World Bank Institute taking a strong role. The AAA program is being thematically developed around the CAS objectives to stay focused on results. Finally, partnerships will play a large role in the success of the platforms, through support for critical analytical, M & E, and capacity building contributions, and in support of specific sectoral reform programs through grant financing, TA and analytical inputs.

viii. International Finance Corporation (IFC) and Multilateral Investment Guarantee Association (MIGA) Programs . IFC’s activities, including the new SME Facility (PENSA), are directed to help the private sector and contribute to sustained economic growth and poverty alleviation, by focusing on: (i) strengthening of banks; (ii) deepening the financial sector; (iii) supporting export-oriented companies, mainly in the agribusiness sector; (iv) supporting infrastructure investments in power and telecommunications; and (v) supporting SMEs. MIGA is proposing to support privatization through the provision of political risk guarantees to foreign investors, to provide support to the investment promotion agency, and to undertake a comprehensive benchmarking study of Indonesia.

ix. Managing Risks. The program is designed to mitigate risks that could limit the effectiveness of Bank support. These risks include, a lack of political will to address governance issues, macroeconomic shocks arising from domestic or international factors, including a financ ial sector crisis; political and security instability threatening a loss of confidence, disruption in Bank activities, and a potential risk to Bank staff; stalled decentralization undermining the effectiveness of local governments; challenges to the Bank’s reputation and credibility stemming from continued public concerns about corruption and the impact of donor assistance. Risk management measures are described for each risk area.

Indonesia Country Assistance Strategy 1

COUNTRY CONTEXT AND DEVELOPMENT CHALLENGES

A. POLITICAL, SOCIAL AND ECONOMIC CONTEXT AND CHALLENGES

1. Indonesia continues its transition from an autocratic, centralized state to a democratic, decentralized one. In the five years since President Soeharto’s resignation and the fall of the New Order regime, Indonesia’s democracy has gained much ground. A multiplicity of voices is being heard from civil society, political parties, and the academic community, and communicated through a burgeoning and relatively free local media. Indonesia’s Parliament has seen its role increase dramatically, and is now actively engaged in the policy debate and providing an institutional check on the executive branch. After a rocky start, the political arena has stabilized over the past two years. Recent constitutional and legal changes have been passed that should further strengthen democratic accountability by paving the way for the first direct election of a President next year and phasing out of the military from Parliament. The successful implementation of the Big Bang decentralization as of 2001 has transferred considerable authority over public expenditures and public service delivery to over 400 local governments in the hopes of improving responsiveness to client needs. There are clear signs that decentralization is enhancing participation in decision-making in the most reform-minded regions.

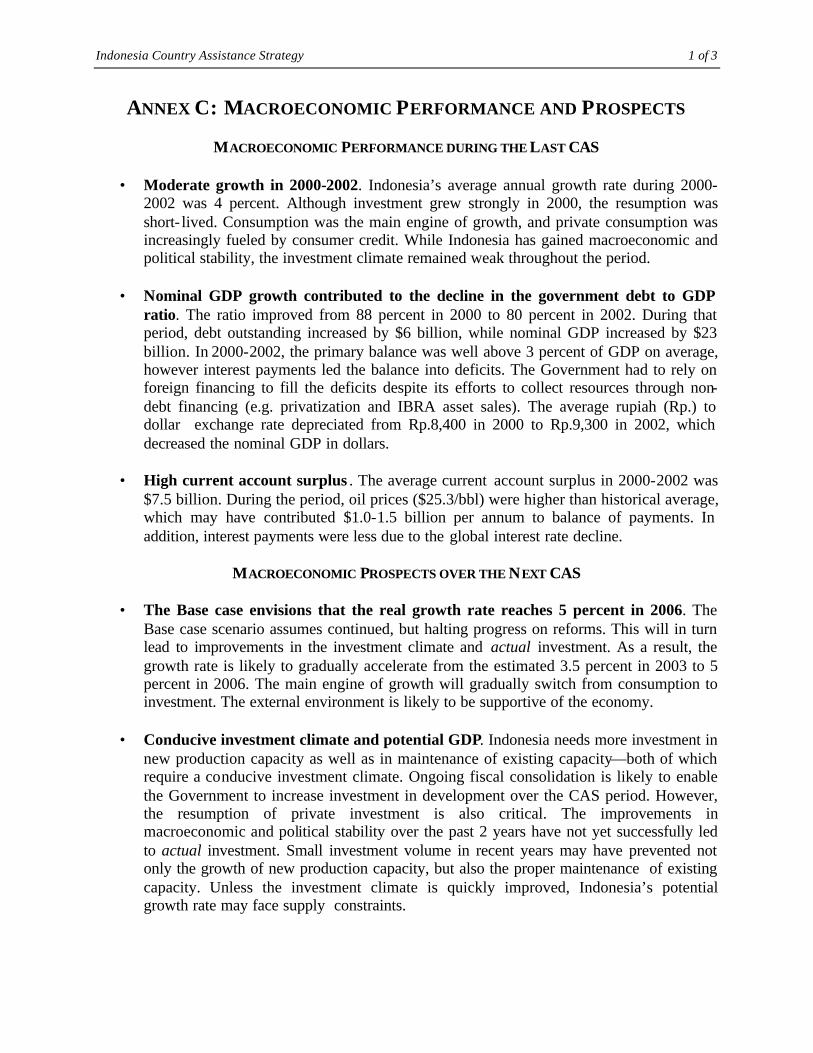

2. Macroeconomic stability has been restored, and poverty has been reduced to near pre-crisis levels (Figure 1). The Rupiah has strengthened from over 10,000 per dollar at the start of the previous CAS period to 8,500 now, inflation has been brought down to below 7 percent, interest rates have fallen accordingly, and the stock market has risen sharply over the past year. Fiscal consolidation has been impressive, as the budget deficit has been reduced by two-thirds to an expected 1.9 percent of GDP in 2003, and 1.3 percent 3 in 2004, primarily through cuts in untargeted fuel subsidies. Government debt to GDP has fallen from almost 100 percent in 1999 to some 72 percent now, and total external debt has shown similar trends. Progress in structural reforms, notably bank sales and asset recoveries by IBRA, the bank restructuring agency, have supported the macroeconomic gains. (See Annex C on macroeconomic performance and prospects.) This stabilization of the economy supported a strong reduction in income poverty,4 which fell from over 27 percent of the population in 1999 to 16 percent in 2002, in part because a stronger Rupiah made key staples, including rice, more affordable after the crisis spike.

3. Nevertheless, the reduction of poverty remains a critical challenge for Indonesia. Despite progress since the crisis, the number of poor in Indonesia continues to be high: currently double that of the entire population of Australia. Moreover, while 6.7 percent of the population live below $1 per day, over 110 million people (53 percent of the population) live on less than $2 per day, and about that many remain highly vulnerable to falling under Indonesia’s poverty line. Eastern Indonesia continues to lag far behind the rest of the country, but there are also pockets of poverty within all regions, and the high population density of Java and Sumatra means that most of the poor in fact live on these islands. Female workers are three times more likely than men to

3 The World Bank estimate of a fiscal deficit of 1.3 percent in 2004, compared to the Government’s estimate of 1.2 percent is due to the World Bank’s projection of nominal GDP being slightly lower than the Government’s projection. 4 As measured through expenditures.

2 Indonesia Country Assistance Strategy

Figure 1: A Snapshot of Indonesia’s Economy Market sentiment continues to improve

(Rupiah/$ exchange rate and Jakarta Stock Exchange index) And inflation and interest rates are falling

(SBI interest rate and CPI inflation)

200

250

300

350

400

450

500

550

600

Feb-01 Jun-01 Oct-01 Feb-02 Jun-02 Oct-02 Feb-03 Jun-038,000

8,500

9,000

9,500

10,000

10,500

11,000

11,500

12,000Stock Index (1983=100) Exchange rate

Stock Index

Exchange rate Rp/US$

4

6

8

10

12

14

16

18

Jan-01 May-01 Sep-01 Jan-02 May-02 Sep-02 Jan-03 May-03

SBI 1 month rate

CPI Inflation (yoy)

(%)

Source: Bank Indonesia, BPS Source: Bank Indonesia, BPS

Fiscal consolidation continues (Government budget deficit, percent of GDP)

And poverty is down from crisis highs (Poverty headcount ratio, percent)

4.8%

3.7%

2.5%

1.8%

1.3%1.6%

2.7%

1.7%1.9%

0%

1%

2%

3%

4%

5%

6%

2000 2001 2002 2003 2004

Budgeted

Actual

draft budget

revised budget

15.7%

27.1%

16.0%

0%

5%

10%

15%

20%

25%

30%

1996 1999 2002

poverty incidence (%)

Source: MOF, staff estimates Source: BPS and staff estimates

But growth remains modest (GDP, Consumption, and Investment growth, percent)

And the investment outlook is subdued (Investment to GDP ratio, percent)

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

GDP Private consumption Investment

2000 2000 20002001 2001 20012002 2002 2002

(growth rate)

15%

17%

19%

21%

23%

25%

27%

29%

31%

1996 1997 1998 1999 2000 2001 2002

Source: BPS Source: BPS

Indonesia Country Assistance Strategy 3

have earnings below one dollar a day and have a lower chance of graduating from low pay jobs. Looking beyond income poverty, Indonesians continue to suffer in many ways. Progress in ensuring access to basic health, education, water, and sanitation services (e.g. as measured by births attended by traditional healers, child enrollment, household access to sanitation and to water), improvements have been slow. These are also reflected in poor MDG outcomes, particularly in health (see Table 1), relative to countries within the region. Women in particular suffer problems of access to quality services and bear the consequences: Indonesia’s maternal mortality rate is two times greater than the Philippines and five times greater than Vietnam. Where public services are available—in education and health, for example—they are often of poor quality as evidenced by student test scores and the high prevalence of communicable diseases such as TB. In addition, while Indonesia is doing well on educating young girls, democratization has so far reduced women’s representation in Parliament, and this trend is also being played out at the local level where local laws are being issued that discriminate against women. (See Annex D for a fuller poverty profile.)

4. The achievements of the past few years continue to be clouded by widespread concerns about governance and corruption across Indonesian society. The high hopes that the Reformasi movement would break the hold of the vested interests and the corruption, collusion, and nepotism that characterized the later years of the Soeharto era have not been realized. Few have been held to account for the theft of public resources, and there are signs that “money politics” is at work allowing old elites to reacquire their previous assets, and new elites to consolidate their positions. While corruption captures headlines, the issues created by Indonesia’s weak institutions have wider implications. The “please your boss”, upward- looking accountability and reward system of Indonesia’s centralized New Order civil service lingers on at the expense of citizen participation and accountability for results. The perception that corruption is still entrenched in the political system has damaged Indonesia’s investment climate and generated popular resentment and resignation. The uneven burden that corruption and poor governance place on poor families raises serious issues of equity and fairness. Indeed, addressing governance was identified in the Bank’s 2001 Poverty Report as the single-most important agenda for reducing poverty in all its dimensions. Many senior Indonesians recognize that the “crisis of governance” is becoming a “crisis of development”, and that a whole new mindset is needed, including tools, instruments and capabilities of a modern, responsive government.

5. Unlike many other countries facing similar governance problems, Indonesia has begun to undertake important structural reforms that could ultimately lead to more transparent and accountable government. An ambitious program of electoral reforms has been introduced that will, over the coming few years make policymakers at all levels of government directly beholden to voters. The mid-2004 national elections will be an important first test. Will “money politics” rule the day? Or will direct election of the President and parliamentarians spark greater responsiveness to public demands for integrity and good governance? In addition, a radical decentralization has brought responsibility for public expenditures and public service provision down to a level where government is likely to be more responsive to client demand. The legal framework for a more transparent system of public expenditure management is making progress with structural reforms soon to follow. And an institutional infrastructure is slowly being put into place to handle corruption cases.

4 Indonesia Country Assistance Strategy

Table 1: Progress towards Achieving the Millennium Development Goals

1990 2002 Poorest quintile Progress towards Goal

1. Halve between 1990 and 2015 the proportion of people who suffer from poverty and hunger Population below 1 dollar a day (%) a 20.6 6.7 33.6 Achieved Share of poorest quintile in National consumption b 0.086 0.0843 n.a. No change Prevalence of underweight children (under 5 years of age, %) c

37 26 n.a. On track, but slipping

Proportion of population below minimum level of energy consumption (less than 2100 Calories per person per day, %) b

70 65 20 Slow progress

2. Achieve universal primary education Ensure that by 2015 everywhere, boys and girls alike will be able to complete a full course of primary education Net enrollment rate in primary school b 93.2d 92.5 88.3 No change Proportion of children aged 16 that have completed primary school. b 88.4 d 94.2 88.1 Improvement

3. Promote Gender Equality and Empower Women Primary 1.06 d 1.08 1.06

Junior secondary 1.13 d 1.04 0.99 Ratio of boys to girls b Senior secondary 1.21 d 1.12 1.14

On track

Share of women in wage employment in non-agricultural sector (%) b 30 d 32 31 No change

Proportion of seats held by women in national parliament (%) e 13 8.8 n.a. Deterioration

4. Reduce Child mortality Under 5 mortality rate f 99 60 n.a. On track Proportion of children of 1 year immunized against measles (%)b 74 d 68 60 Worsening

5. Improve maternal health Maternal mortality ratioc (per 100,000 live births) 425 k 373 l n.a. Improving slowly Proportion of births attended by skilled health personnel b 39.6 d 67 46 Improving but low 6. Combat HIV aids, malaria and other diseases Contraceptive prevalence (% among married women aged 10-50)

52.2 d 53.3 52.2 No change

7. Ensure Environmental Sustainability Proportion of land covered by forest g 63h 57i n.a. Worsening Percent of population that has access to improved water j 63 d 78 65 Improving but low Note: The Government of Indonesia is in the process of preparing a Millennium Development Goals report. In this table we have made an effort to present the indicators as they are likely to feature in the GoI’s report. There are however likely to be differences and this table should not be considered the GoI’s view with respect to progress toward the MDGs. a. World Bank. April 2003. East Asia Update—Looking Beyond Short-term Shocks, Regional Overview. East Asia and Pacific Region, Washington D.C. b. World Bank Staff calculations based on Susenas. c. Health Profile of Indonesia, Ministry of Heatlh 2002. d. 1993 Susenas data. e. International Institute for Democracy and Electoral Assistance. 2000. Democratization in Indonesia: An Assessment. f. BPS publications, using population census, International Demographic and Health Survey and intercensal surveys. g. Holmes, Derek A. 2002. “Indonesia: Where have all the forests gone?” Discussion Paper. Environmental and Social Development, East Asia and Pacific Region. World Bank, Washington D.C. h. 1985 data. i. 1997 data. j. Improved water is derived from bottled, piped or pumped water, protected well or spring and rainwater. k. 1992 data. l. 1995 data.

Indonesia Country Assistance Strategy 5

6. But these bold reforms—in significant respects as far-reaching as any country in transition—have been undermined by weak implementation. As a result, the gap between the promise and the reality of reform in Indonesia has been large. Yet it is important to recognize that there is much to work with in seeking to support Indonesia’s future reform path. The legal framework for necessary structural reforms is in place; the challenge is more narrowly focused on strengthening the incentives for effective implementation. Despite a vibrant arena of political competition, the major parties tend to agree on the basic thrust of reform pointing towards more direct accountability, greater transparency and more responsible financial management. This suggests that there is a strong foundation for reform in the coming years even though there remains much work to be done to harness the bold initiatives of the Reformasi period into effective institutional and behavioral change.

7. This mixed story—of solid progress in economic policy-making, and halting progress on governance issues—is captured in the Country Performance Institutional Assessment (CPIA) ratings. Figure 2 shows that the good progress in macroeconomic policy and reasonable progress in structural policies is only beginning to be matched by progress in social indicators and in indicators of governance. While for most indicators Indonesia is well ahead of the average for IDA countries, performance on property rights and governance, transparency and accountability, and external debt management are lagging. Moreover, the fact that neither investment levels nor (broadly) the quality of public services have returned to their pre-crisis levels—in spite of impressive improvements in the macroeconomic context and opportunities provided by decentralization—is a reflection of the weaknesses of public institutions, a lack of transparency and accountability, and corruption.

8. Finally, Indonesia is not yet free from risks to political and social stability, against which democracy, growth and poverty reduction remain the best weapons. The recent resumption of military action in Aceh demonstrates that so far, decentralization and special autonomy, have not resolved separatist tensions. At the same time, extremist Islamic movements both within Indonesia and across the region, though representing a small minority, continue to pose a heavy burden of terrorism threats. The twin threats of separatism and terrorism raise concerns about security and uncertainty that impose high costs on the population and dampen the response of investors to Indonesia’s strong macroeconomic achievements. At the same time, these twin threats underlie a continued powerful political role for the military that weakens some of the recent gains in establishing greater transparency and accountability in the political system.

B. INDONESIA’S NEW ECONOMIC POLICY PACKAGE: THE SHORT-TERM AGENDA

9. The Government has decided not to renew the IMF program when it expires at the end of 2003, and in its place has announced a package of policy actions for the next eighteen months. Following much discussion among politicians, cabinet members, academic economists and civil society groups, President Megawati Soekarnoputri announced the Government’s decision in her budget speech to the nation on August 15, 2003.5 In place of the

5 The IMF will continue to be strongly engaged through its “Post Program Monitoring” missions.

6 Indonesia Country Assistance Strategy

Figure 2: Indonesia Country Policy and Institutional Assessment

Good progress on macro and structural, but limited progress on governance and social…

1. Macroeconomic Balances

2. Fiscal

3. External Debt

4. Development Program

5. Trade and FX

6. Financial Stability

7. Banking Efficiency

8. Private Sector Environment

9. Markets

10. Environment

11. Gender

12. Equity of Public Resource Use

13. Building HR

14. Social Protection

15. Poverty Analysis

16. Property Rights and Governance

17. Budget Management

18. Revenue Mobilization

19. Public Administration

20. Transparency & Accountability

Indonesia 2003 Indonesia 1999 Maximum

Generally better than the IDA average in all areas but governance and debt…

1. Macroeconomic Balances

2. Fiscal

3. External Debt

4. Development Program

5. Trade and FX

6. Financial Stability

7. Banking Efficiency

8. Private Sector Environment

9. Markets

10. Environment

11. Gender

12. Equity of Public Resource Use

13. Building HR

14. Social Protection

15. Poverty Analysis

16. Property Rights and Governance

17. Budget Management

18. Revenue Mobilization

19. Public Administration

20. Transparency & Accountability

Indonesia 2003 IDA average 2002 Maximum

Indonesia 2003 are preliminary ratings.

Letter Of Intent (LOI) which the Government prepared periodically for the IMF under its program, the Government has prepared a new time-bound package of economic policies, that will guide policy direction through 2004, covering the period of the elections and installation of a new administration. The package, signed by the President on September 15, covers three areas—

Indonesia Country Assistance Strategy 7

macroeconomic management, financial sector reform, and policies to restore investment and growth.

• Further Macroeconomic Consolidation. The Government’s aim is to reduce the fiscal deficit to zero by 2006, and the public debt to GDP to “safe levels” (the State Finances law specifies a level below 60 percent of GDP—equal to the so-called “Maastricht” norms). Measures to modernize the tax system include revisions of taxation laws, expanding the large taxpayers’ office, and reforms of the customs office. Measures to increase efficiency in spending include revised procedures on government procurement, establishment of a separate treasury and a treasury single account, and implementing regulations for budget preparation and government accounting standards. The plan calls for further reductions in untargeted fuel subsidies—and limiting these to household kerosene, a fuel mainly used by the poor. The program includes privatization of 10 state enterprises—an ambitious target for an election year—and a revamp of intergovernmental fiscal relations.

• Deeper Financial Sector Reform. Government plans include policies to solidify a financial sector safety net, continue bank restructuring, strengthen state bank governance, and improve capital market supervision. A “white paper” on the financial safety net would be prepared, a deposit insurance law submitted to Parliament, and the “lender of last resort” role of Bank Indonesia would be amended. Specific actions on bank restructuring include further sales of IBRA banks and assets, and introduction of risk-adjusted capital adequacy rules. State banks would be strengthened by appointment of independent commissioners, and by improving credit and risk management systems, and by launching an IPO for Bank BRI. Capital markets would be placed on a firmer footing by enforcement of capital adequacy standards, regulation of the mutual funds business, and consolidation and improved regulation in the insurance and pension sector. The anti-money laundering law has been revised to abide by FATF guidelines, and an anti-money laundering task force will be created.

• An Improved Investment Climate. Actions promised by the Government draw from consultations with the business community, and seek to begin to address deep seated constraints, such as corruption, the lack of a trusted legal system, the lack of access to land tenure, and the lack of adequate physical infrastructure as well as more immediate regulatory and labor issues. The Government will set up an Investment and Trade Team to identify and address constraints, and monitor progress. Specific actions include a revision of the investment law, a review of the negative list of sectors barred for foreign investors, and acceleration of tax refunds for exporters. The Anti-Corruption Commission will begin operation, a judiciary commission in charge of the appointment of judges will be established, and the law on the attorney general’s office will be revised. The bankruptcy law will be revised, and the commercia l court in charge of application of that law will be strengthened. To improve investment and management of physical infrastructure, additional public funds will be allocated; and private investment will be facilitated through revisions to the Transport Law, and the creation of an independent supervisor for the electricity market. The Government commits to improving service delivery to investors by improving tax and customs administration, and by requiring all agencies with services to the public to publish service delivery standards.

8 Indonesia Country Assistance Strategy

10. The Economic Policy Package has been received domestically and internationally as ambitious but welcomed. By announcing actions and dates, the Government has opened itself to public scrutiny and made itself accountable in an unprecedented manner. Existing planning documents, such as the five-year plan (PROPENAS) and annual plan (REPETA), discuss development objectives and list loosely related development spending programs, but do not include concrete time-bound actions, with allocated responsibilities. The new package can be criticized as containing too many items and being unfocused, and its success will only become evident over the coming months. Monitoring units are being established within Government and outside, and the Bank will support the Government’s efforts to refine the program, and will provide support for its implementation. Base and High case triggers for the Bank’s program are taken from the Government’s policy package, and it will also be the focus of the next Consultative Group meeting in December 2003.

C. THE EMERGING PRSP: A MEDIUM-TERM FRAMEWORK FOR POVERTY REDUCTION

11. A Poverty Reduction Strategy Paper (PRSP), scheduled for completion in May 2004, is expected to build on the Economic Package, and lay out a comprehensive medium-term development program for poverty reduction. In early 2003 Indonesia finalized its Interim PRSP, which provided a broad road-map and timetable for developing the full PRSP.6 The I-PRSP (circulated to the Boards of the Bank and Fund in March 2003) was consulted broadly with civil society and across the country. Consensus was developed on four fundamental themes for the national PRSP: (i) creating opportunities; (ii) empowerment; (iii) human capital and capacity development; and (iv) social protection. Four multi-stakeholder Task Forces are charged with putting substance behind these areas through a program of analytics and policy development. A Core PRSP Team, under the leadership of the Coordinating Minister for Social Development, is responsible for the overall strategy, and for seeking to link the strategy to the medium term plan and budgetary framework. A series of district-level poverty-reduction strategies, based on participatory poverty assessments (PPAs), are also being prepared. The CAS has been designed to be fully consistent with the emerging PRSP, and has been prepared in consultation with the PRSP Core Team. The CAS Progress Report, to be prepared at the end of 2004, will propose fine tuning of the CAS, in light of the full PRSP and the concerns of the new Government.

D. ECONOMIC OUTLOOK, EXTERNAL ENVIRONMENT AND FINANCING NEEDS

12. A gradual increase in growth characterizes the Base case economic outlook. Supported by a recovering international economy, and a slow but steady improve ment in the investment climate, Indonesia’s GDP growth rate is expected to reach 5 percent by 2006, up from the 3.5 percent in 2003, and broadly similar rates over the last CAS period. Inflation is expected to drop further to some 5 percent per annum and domestic interest rates to drop in line. Under this scenario, the poverty rate would fall from 16 percent in 2002 to 11 percent in 2007, less than half the 27 percent it was in 1999. The external environment is likely to be slightly more supportive of Indonesia’s growth than over the past years: the most recent World Bank

6 As a blend country, Indonesia’s PRSP preparation is not directly linked to IDA access and was therefore not a pre-requisite for Bank CAS preparation. Indonesia’s I-PRSP was circulated to the Board in March 2003.

Indonesia Country Assistance Strategy 9

projections envision a pick-up in the rate of global GDP growth and of world trade.7 Indonesia will face increasing competition on traditional markets, particularly from China, and that competition will intensify after expiry of the MFA agreement in 2005. At the same time, China will be a rapidly growing export market for Indonesia in the years ahead and, on balance, we therefore expect continued export growth. The real exchange rate, while having appreciated in recent years, remains below its pre-crisis levels. Nevertheless, a competitive exchange rate will be necessary to underpin Indonesia’s trade competitiveness.8 Imports will grow faster, as a result of recovering investment, and the current account surplus is thus expected to gradually decline from the record $7.5 billion, or 4.3 percent of GDP in 2002. (For more detail on macroeconomic performance and prospects, see Annex D.)

13. Our Base case projections include gradual increases in investment rates and factor productivity, which in turn are predicated on continued sound macroeconomic performance and a moderate improvement in the investment climate. We expect the Government to continue fiscal consolidation, although at a more moderate pace than the Government itself projects. We assume a balanced budget by 2007, down from 1.9 percent projected for 2003. Consolidation will not only come from further cuts in fuel subsidies—already down from over 5 percent of GDP in 2001 to 1.4 percent of GDP projected for 2003—but also from an increase in non-oil tax revenues on the back of accelerated revenue administration reforms. The Government debt to GDP ratio will continue to fall through 2007 from 67 percent by the end of this year to below 50 percent by 2007 given the debt repayment schedule, exchange rate assumptions, and nominal GDP growth. Likewise, the total external debt to GDP ratio, which had dropped to 76 percent in 2002 is projected to continue to decline to about 40 percent in 2007. We expect investments as a share of GDP to gradually rise from 20 percent now to 22 percent in 2007.

14. Despite further fiscal consolidation, financing needs will be particularly high in the first two years of the CAS period. With the expiration of the IMF EFF arrangement, Paris Club rescheduling ceases at the end of 2003, adding some $3 billion in additional financing needs. In addition, an increasing share of bank re-capitalization bonds will fall due over the coming years, while IBRA asset recoveries are tailing off, as are privatization receipts. As a result, higher financing is required to support a public investment program that complements private investment. With respect to domestic financing, the Government will look to the domestic bond market and a draw-down in deposits. However, increased foreign-financed disbursement will also be required as one important element in bringing about enhanced investment levels and growth. Foreign financed disbursements on the order of US$3 billion will be required annually over this period, relative to a level of $2.3 billion per annum over the last three years, excluding Paris Club.

7 The World Bank’s Global Development Prospects 2004 publication envisages world GDP growth climbing from 2 percent in 2003 to 3 percent in 2004-2005, and regional (East Asia and Pacific) growth rates rising to 6.6-6.7 percent in 2004-2005. World trade volume is expected to increase from 4.6 percent in 2003 to 8 percent in 2004-2005. 8 Bank projections anticipate a real exchange depreciation of about 1.2 percent annually over the CAS period.

10 Indonesia Country Assistance Strategy

THE WORLD BANK IN INDONESIA: LEARNING FROM RECENT EXPERIENCE

A. LESSONS FROM THE TRANSITION PERIOD

15. In the aftermath of the economic crisis, the World Bank was seen by many as part of the problem rather than the solution. To many Indonesians the Bank was associated with the Soeharto Government, which it had supported through loans and policy advice for 32 years. The Bank was a contributor to Indonesia’s external debt, perhaps the country’s most visible economic problem in the post crisis years, without being able to contribute to debt rescheduling or debt reduction. And the Bank’s reputation was damaged as it was perceived to have failed to take a stand against corruption, while lending large sums of money in support of the Soeharto regime. As of mid-2000, the Bank had $11.8 billion of IBRD funds outstanding to Indonesia. To many NGOs this was a millstone around Indonesia’s neck. And to the Bank’s risk managers, this posed one of the most risky parts of the overall portfolio.

16. Over the last few years, the Bank has sought to actively confront these issues, making progress and learning important lessons. First, our debt exposure to Indonesia has been lowered. In agreement with the Government, lending was reduced dramatically from an average of $ 1.3 billion per year before the crisis, to about $450 million over the last three years. As a result the Bank’s exposure to Indonesia has dropped by some $1.5 billion, and will fall by a further $700 million in FY04. Second, as the Bank’s portfolio has shrunk, portfolio performance has picked up. Consolidation, project restructuring and intensive supervision have helped portfolio performance recover from its FY02 post-decentralization dip. Commitments at risk, which reached 39 percent in FY02, dropped to 12 percent by end FY03. Third, the Bank shifted its focus (and its reputation) towards a major expansion of our work on community-driven development programs, governance and anti-corruption (see Section B), and engagement with civil society.

17. Recent project outcomes have been mixed. Recent OED ratings largely apply to projects that began before the crisis, and thus teach lessons about the need to be flexible at times of stress. Of the 30 projects closed in FY00-02, 60 percent were rated moderately satisfactory or above, while 37 percent were rated moderately unsatisfactory or below. Problems identified understandably included lack of counterpart funding and more generally a lack of ownership on the part of Government during the transition period. Lack of supervision from central Government and from the Bank was identified in several situations, as was more generally the break-down of traditional top-down project design and administration. During the past CAS period, therefore, an effort has been made to introduce a new generation of projects, giving much greater emphasis to participatory approaches, being sensitive to the capacities at local and central levels of Government, and introducing mechanisms for local level accountability. Some of the lessons from the past CAS period are summarized in Box 1.

18. Indonesia remained in the Base case throughout the last CAS period, but has now broadly achieved the High case. Triggers for the High case gave emphasis to the continuation of the post-crisis reforms. Table 2 summarizes progress made over the past three years on both

Indonesia Country Assistance Strategy 11

Box 1: Lessons from OED Reviews and the Last CAS

The lessons from the Operations Evaluation Department (OED) review of the Bank’s role leading up to the crisis,* which informed the last CAS, continue to provide a foundation for the Bank’s program:

In the area of structural reforms, the Country Assistance Note recommended:

• Strengthening Bank support to the Government in improving governance by improving fiscal/budget transparency, strengthening oversight and voice mechanisms, enhancing transparency in the incentive framework, and reforming the civil service.

• Concerted effort, including ESW, to help restore banking sector soundness.

• Updating poverty and distribution data and re-thinking long-term intra-sectoral commitments, with the aim of supporting poverty alleviation more directly.

This CAS has integrated these lessons:

• It calls direct attention to Indonesia’s poor governance and corruption and, through the innovation of operational platforms, is mainstreaming support for improving transparency, oversight and voice while continuing to pursue civil service reform.

• Poverty and income distribution data have been updated, and this CAS puts forward an intensive analytical program on poverty. (See Annex D). Community Driven Development efforts, which comprised over 50 percent of new commitments under the last CAS and channeled funds directly to grass-roots development projects selected by villagers, including the poor, are supporting poverty alleviation more directly. This CAS aims to build from this promising foundation.

• Intensive Bank support, including through ESW, will continue to help strengthen the financial sector.

A more recent OED Project Performance Assessment** which draws lessons from the Bank’s crisis-response adjustment and TA loans, has informed the assumptions which define this CAS: In a country with deeply rooted and widespread governance issues, and where authorities are not committed to deep governance reforms, the ability to affect fundamental reforms with adjustment and technical assistance support has been limited:

• Under this CAS the use of adjustment lending will continue to be very limited and only be employed in support of government-driven reform efforts.

• The overall CAS program and the High case triggers have been aligned to the Government’s program to support ownership and effective implementation.

This CAS also learns from other experience and lessons drawn from the last CAS period:

• Close partnerships with donor partners and civil society, such as through the CGI process and Partnership for Governance Reform, enhances our effectiveness, as does current high quality collaboration with the Fund.

• Decentralization is for real and affects everything we do. It poses real opportunities and real challenges which, going forward, we must address centrally in our strategy.

• More systematic monitoring and evaluation of the impacts of our interventions is essential to an innovative program such as ours. This requires priority going forward.

• Strong analytical work continues to be a strength of the Bank and is appreciated by the client and our partners. Increasing its leverage to better inform the design of operational interventions and affect policy change is key.

____________________ * OED Country Assistance Note, February, 1999

** Draft Project Performance Assessment Report (PPAR), July 31, 2003

the triggers and related measures in which the Bank Group provided technical support. By the end of FY03 only one High case trigger—the issuance of a new Procurement decree—remained unmet. This progress, however, must be tempered by the fact that much still remains to be done on the reform agenda, and implementation of policies and laws remains a serious issue.

B. THE SPECIAL PROBLEM OF CORRUPTION

19. More than 5 years after the fall of Soeharto, the salience of the issue of corruption has not diminished. Though it is nearly impossible to compare the actual levels of corruption

12 Indonesia Country Assistance Strategy

Table 2: Government Policy Performance under Last CAS

Action Area GOI Action and Progress To Date (High case trigger conditions highlighted in bold)

Bank and Corporate Restructuring

• IBRA sold $45 billion in distressed banking system debt. • 3 banks were privatized, but around 50% of banking assets remain publicly owned. • Jakarta Initiative Task Force (JITF) met corporate restructuring targets. • Parliament approved amendment to the Anti-Money Laundering Law in Sept. 2003.

Macroeconomic Stability

• Budget deficit down to an expected 1.9% of GDP in 2003. • Rupiah strengthened from over 10,000/US$ in July 2000 to 8,500 in Sept. 2003. • CPI inflation brought down from 12% in 2001 to below 7% in 2003. • Public debt to GDP fell from almost 100% in 1999 to 72% in June 2003.

Pro-Poor Policies • Rice tariff remained below 30 percent ad-valorem equivalent, but non-tariff measures remain and Bulog’s expanding role may jeopardize rice price support

• Land policy management clarified through Presidential Decree 34/2003, but implementation regulations yet to be prepared and adopted.

• Fuel subsidies reduced from over 5% of GDP in 2000 to 1.5% in 2003, but compensating safety net programs were poorly targeted and monitored.

• I-PRSP completed in March 2003. PRSP to be completed by mid-2004.

Competitive Private Sector Development

• Privatization of SOEs, despite commitments announced by the Government, remains controversial—little action taken to date.

• Competition agency (KPPU) established, but enforcement needs strengthening. • Some backtracking on the open trade regime, e.g., sugar restrictions.

Infrastructure Bottlenecks

• Oil and Gas Law passed in 2001, but issuance of implementing regulations is slow. • Electricity Law passed in Sept. 2002, but regulatory body not yet established. • Disputes with 26 out of 27 Independent Power Producers settled. • Tariff increases in electricity and telecommunications, but prices still inadequate to attract

investors.

Legal and Judicial Reforms

• Governance audit of the Supreme Court completed and follow-up ongoing. • Audit of Attorney General’s office completed, but no follow-up action. • Anticorruption Commission (ACC) Law passed in Dec. 2002, but ACC still not functional

Civil Service Reforms • Civil servants smoothly transferred to the regions following decentralization, but no progress made on a comprehensive civil service reform.

Public Procurement and Financial Management

• State Finance Law passed in March 2003, but treasury and audit laws still in draft . • Public Procurement Decree has been drafted and is awaiting presidential approval, and legal

framework still needs revision.

Management of Decentralization Process

• Smooth implementation of law 22 on decentralization, but conflicting implementation rules and sectoral laws need attention.

• Intergovernmental fiscal framework put in place (law 25), but revenue raising remains overly centralized and equity issues linger.

under the New Order and Reformasi regimes—including the impact of decentralization—it is clear that corruption has become less predictable in this more competitive and uncertain environment. Moreover, the unfulfilled expectations that Reformasi would quickly bring a new integrity to public life has generated resentment, fuelling perceptions that corruption has become endemic in the new system. For the Bank Group, corruption has become a triple threat: it undermines progress on the country’s broad development objectives, it remains a serious risk to the effectiveness of our programs, and it continues to weaken public credibility in development assistance overall, which is still too often portrayed within segments of the community as contributing to the problem.

Indonesia Country Assistance Strategy 13

20. A central lesson of the Bank Group’s experience in Indonesia is that our entire success will be judged by the contribution that our programs are seen to make towards greater transparency and accountability, and by the standards of integrity with which we implement these programs. This has consistently been one of the main messages of our enhanced CAS consultations with civil society (see Box 2) and the Indonesia Country Team’s own self-assessment of the Bank’s objectives over the next several years. Since the crisis, the Bank has responded to the triple threat of corruption by scaling back our lending, while seeking to build a capacity to act as a catalyst for anti-corruption reforms, cultivating partnerships to promote good governance, and strengthening the team’s own capacity for mitigating corruption risks to our projects. Much has been achieved in each of these areas, providing a stronger foundation for the Bank to respond to Indonesia’s increased need for development assistance.

Box 2: CAS Consultations Highlight Indonesia’s Development Challenges

As part of the preparation of this CAS, extensive consultations with various civil society representatives, both in Jakarta and in the regions, through focus groups, interviews and feedback sessions, highlighted priority development issues that participants thought the Bank should address. (See Annex E). They closely mirror and validate the key challenges posed above. First , participants saw “KKN” (corruption, collusion and nepotism) as the country’s core problem. As it was put by one participant, “corruption is the real root of poverty in this country”. Many called for particular attention to legal reform as a related development priority. Second, participants stressed the need to alleviate poverty, especially through job creation and economic growth. Third, consultations raised the need to improve essential services—especially in education and health—as a key development priority. With regard to service delivery, concerns were raised about corruption and quality. Fourth, related to both growth and governance, Indonesians felt there was a need to pay more attention to improving agriculture and environmental management.

21. Going forward, the Bank Group will integrate four key anti-corruption principles across its entire program in Indonesia:

• A clear and consistent voice raising corruption concerns and promoting feasible responses across all sectors of our operations. In the past three years the Bank invested considerable efforts in assisting the development of the Partnership for Governance Reform—an Indonesian-led, multi-donor supported effort to raise awareness of and devise solutions to governance problems. The Bank is complementing this work by raising its own voice on corruption through analytical and advisory work. In October 2003 a multi-sector Bank report dissecting “how corruption works” in a wide range of areas was launched, and televised nationally.9 This is being followed up by expenditure reviews and expenditure tracking targeted at key breeding grounds of corruption, more core diagnostic reports, and detailed studies of the effects of participation and transparency on corruption outcomes in community level programs. At the same time, the Bank has supported national- level reforms in procurement and financial management (see Table 2). The Bank will help the Government persevere in fending-off special interests to create a national procurement function and modernize its procurement law. We will also support the Government to implement the agenda that has been codified in the recent State Finance Law (and soon to be passed Treasury and Audit laws).

• Project selection to open multiple entry points in the fight against corruption. Instead of relying on the development of an overarching anti-corruption program or anti-

9 Combating corruption in Indonesia: Enhancing Accountability for Development, World Bank, October 20, 2003 Discussion Draft.

14 Indonesia Country Assistance Strategy

corruption institution, the Bank’s projects described in the pages ahead have been chosen to open up multiple anti-corruption entry points at different levels of government and across different sectors. CDD projects promote participatory planning and monitoring to reduce corruption in village level governments. District level projects will seek to select kabupaten (districts) and kota (municipalities) with a demonstrated commitment to greater accountability and transparency and work with them to improve their financial management and pro-poor planning capacity. Justice sector work will target both enhancing access to justice for the poor as well as providing technical assistance to the new central institutions designed to fight corruption. The Bank will respond in particular to partners with a demonstrated track record of commitment to anti-corruption reforms.

• Mechanisms to mitigate corruption risks for all projects through empowerment, participation and transparency. The lessons of our successful CDD projects in Indonesia demonstrate the impact of smart project design for reducing corruption risks and getting more development impact for less investment. Direct client participation in the selection and implementation of projects engages citizens as monitors with a direct incentive to reveal corruption problems. Public disclosure requirements at key stages of the project make asset diversion more difficult and build public credibility behind the project. Enhanced supervision through project facilitators in the community linked to national networks has been particularly successful in revealing corruption allegations. To ensure smart project designs, all projects are required to devise an Anti-Corruption Plan, assessing risks of corruption inherent in the project and proposing design and supervision mechanisms to mitigate those risks.

• Pre-emptive audits, vigorous investigation and follow-up to allegations of corruption in Bank projects, and public disclosure of the results. Having created better mechanisms to detect and handle corruption allegations in our projects, the Bank is now receiving and investigating considerably more corruption complaints. It is also proactively uncovering the methods and systems that allow corruption to flourish in each sector. Professionals from the Department of Institutional Integrity (INT) will continue to be brought in to investigate corruption allegations, and they will be supplemented by local investigative staff. Where misuse of funds has been confirmed, the Bank will declare mis-procurement, seek return of affected funds, blacklist offending contractors, and encourage the pursuit of appropriate disciplinary and legal action. Where satisfactory progress is not being made in responding to corruption allegations the Bank will discontinue further operations in the relevant sector, region, or government agency. Public disclosure of corruption cases will be made on the Bank’s Indonesia website, within the limits of safeguarding the Bank’s investigative and sanctions process, protecting the identity of individuals, and respecting domestic legal due process.

22. The Country Team has invested unprecedented resources into mainstreaming anti-corruption throughout our program. The Indonesia Country Office is the only mission worldwide with a Senior Governance Adviser to coordinate our anti-corruption dialogue, oversee governance-related operations, advise projects on governance and anti-corruption strategies, and develop a comprehensive research agenda and monitoring framework on governance. A strong field-based Operations Services Unit team has been put in place to lead the movement towards a systematic and effective supervision of fiduciary practices during project implementation. An in-

Indonesia Country Assistance Strategy 15

house Anti-Corruption Committee has been established with representation across the sectors, and from our field-based legal staff, to serve as a focal point for integrating anti-corruption mechanisms into project design, review procurement and corruption allegations, and liaise with our internal investigations unit. Full- time staff members are now being assigned to assist task teams in the design of anti-corruption strategies, and in the investigation of possible corruption within our portfolio. It is important to recognize, of course, that while this strong combination of preventative, investigative and corrective measures is expected to significantly reduce the risk and incidence of corruption, in the near term it may not result in fewer cases of corruption being identified. More important than the number of cases is the extent to which the Bank’s practices ensure greater integrity within our own portfolio and lead to broader improved practices within Indonesia.

16 Indonesia Country Assistance Strategy

THE BANK GROUP’S ASSISTANCE PROGRAM

A. THE WORLD BANK GROUP’S STRATEGIC FOCUS

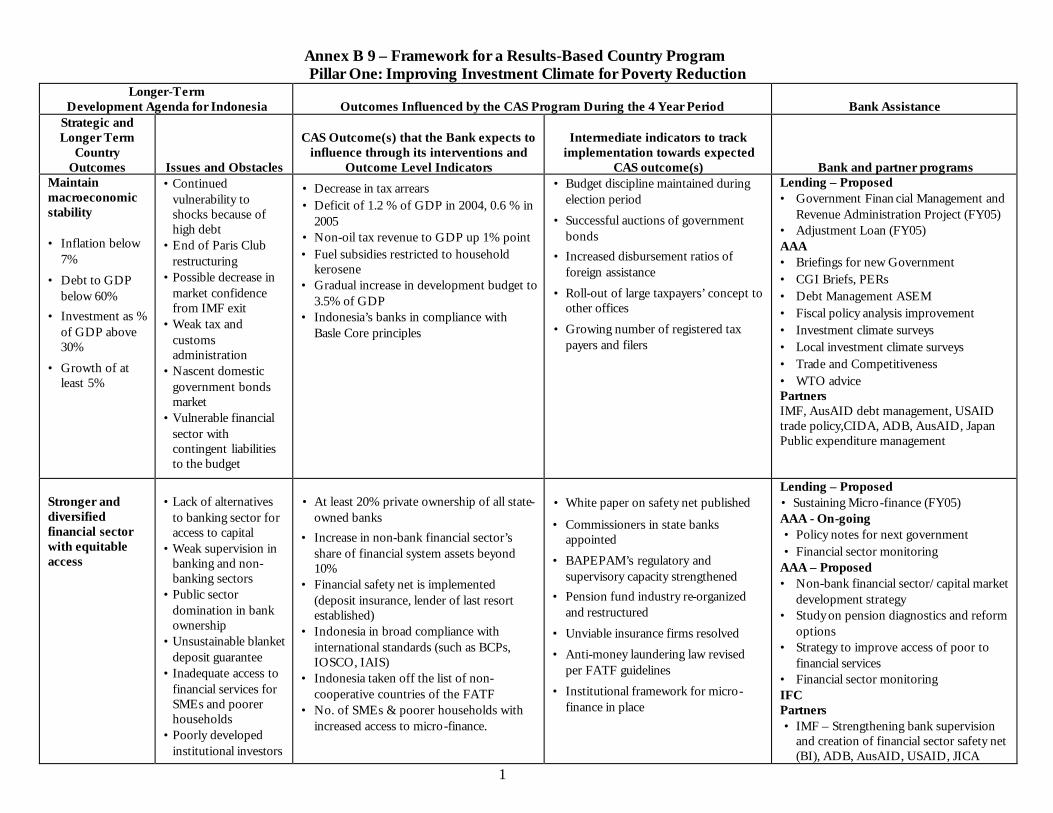

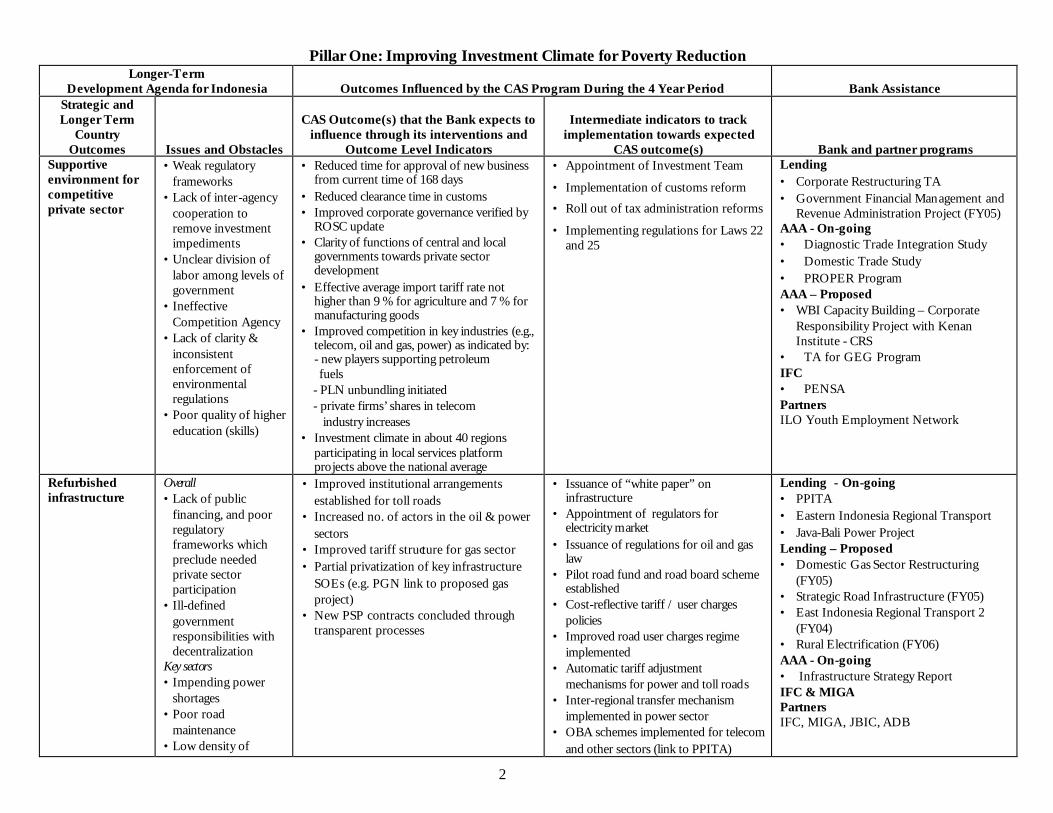

23. For the coming CAS period the Bank Group will continue to focus its program on those areas most crucial to poverty reduction. At present there are two primary constraints to further reductions in poverty. These are: first, inadequate productive employment opportunities, which result from low investment and a weak investment climate; and second, the lack of quality service delivery to poor people. Progress in these two areas, in turn, is being compromised by the underlying problem of weak governance. The World Bank Group’s strategy will be to address the objectives of strengthening the investment climate and service delivery including, critically, the key issue of governance. Four delivery platforms – corresponding to the community, local, public utility, and national levels (see next section) – will be used to deliver results in these areas (see results matrix in Annex B9).

Figure 3: The CAS Framework

Objective I: Improving the Climate for High Quality Investment

24. A weak investment climate is undermining Indonesia’s future. Indonesia’s economy has been growing over the past three years at a rate of less than 4 percent per year—lower than what is needed to absorb the 2.0-2.5 million new entrants in the labor force every year. Unemployment is rising and wages in the informal sector are stagnant. At root is the lack of investment that at the time of the crisis declined from around 30 percent of GDP to around 20 percent, where it has remained since. While maintaining the gains of macroeconomic stability will continue to be critical through the elections and the next CAS period, deepening the financial sector, fostering a regulatory and institutional environment conducive to private sector growth, building the infrastructure for growth, and ensuring that growth benefits the poor will be fundamental. The Bank Group’s support will thus be focused in five areas, with improved

Investment Climate Service

Delivery

National Platform

Public Utility Platform

Local Services Platform

CDD Platform

GOVERNANCE

Indonesia Country Assistance Strategy 17

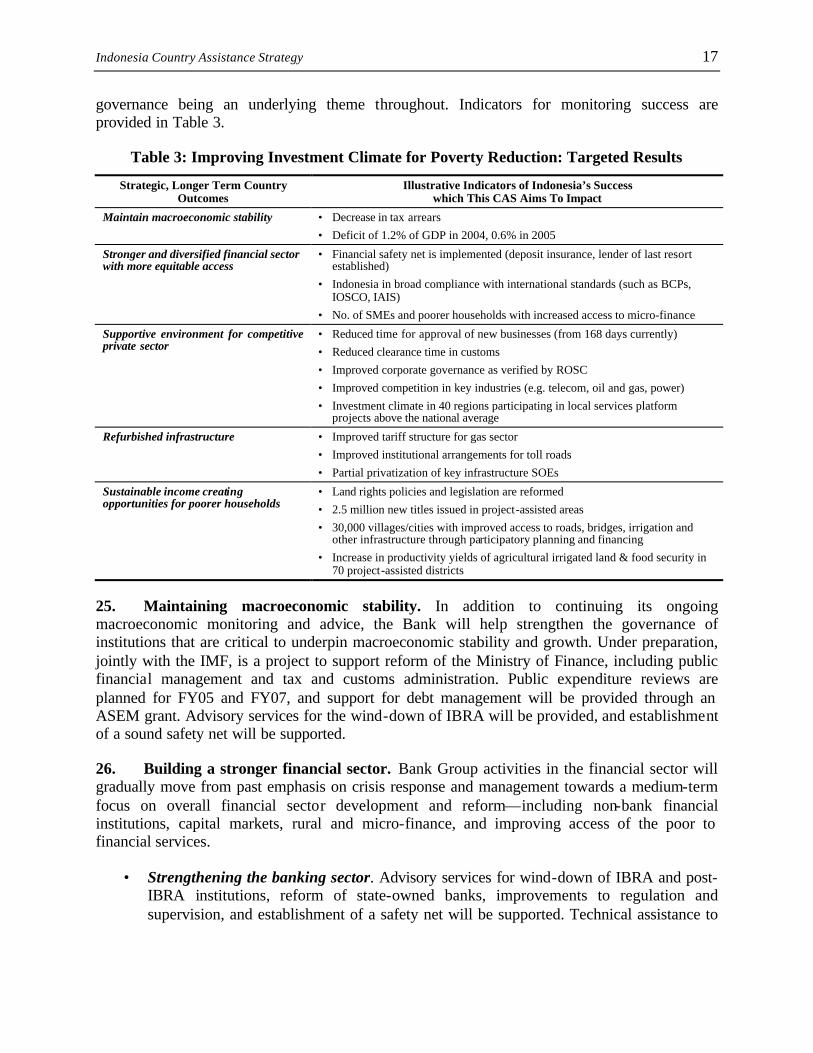

governance being an underlying theme throughout. Indicators for monitoring success are provided in Table 3.

Table 3: Improving Investment Climate for Poverty Reduction: Targeted Results

Strategic, Longer Term Country Outcomes

Illustrative Indicators of Indonesia’s Success which This CAS Aims To Impact

Maintain macroeconomic stability • Decrease in tax arrears • Deficit of 1.2% of GDP in 2004, 0.6% in 2005

Stronger and diversified financial sector with more equitable access

• Financial safety net is implemented (deposit insurance, lender of last resort established)

• Indonesia in broad compliance with international standards (such as BCPs, IOSCO, IAIS)

• No. of SMEs and poorer households with increased access to micro-finance

Supportive environment for competitive private sector

• Reduced time for approval of new businesses (from 168 days currently) • Reduced clearance time in customs • Improved corporate governance as verified by ROSC • Improved competition in key industries (e.g. telecom, oil and gas, power) • Investment climate in 40 regions participating in local services platform

projects above the national average

Refurbished infrastructure • Improved tariff structure for gas sector • Improved institutional arrangements for toll roads • Partial privatization of key infrastructure SOEs

Sustainable income creating opportunities for poorer households

• Land rights policies and legislation are reformed • 2.5 million new titles issued in project-assisted areas • 30,000 villages/cities with improved access to roads, bridges, irrigation and

other infrastructure through participatory planning and financing • Increase in productivity yields of agricultural irrigated land & food security in

70 project-assisted districts

25. Maintaining macroeconomic stability. In addition to continuing its ongoing macroeconomic monitoring and advice, the Bank will help strengthen the governance of institutions that are critical to underpin macroeconomic stability and growth. Under preparation, jointly with the IMF, is a project to support reform of the Ministry of Finance, including public financial management and tax and customs administration. Public expenditure reviews are planned for FY05 and FY07, and support for debt management will be provided through an ASEM grant. Advisory services for the wind-down of IBRA will be provided, and establishment of a sound safety net will be supported.

26. Building a stronger financial sector. Bank Group activities in the financial sector will gradually move from past emphasis on crisis response and management towards a medium-term focus on overall financial sector development and reform—including non-bank financial institutions, capital markets, rural and micro-finance, and improving access of the poor to financial services.

• Strengthening the banking sector. Advisory services for wind-down of IBRA and post-IBRA institutions, reform of state-owned banks, improvements to regulation and supervision, and establishment of a safety net will be supported. Technical assistance to

18 Indonesia Country Assistance Strategy

enhance financial sector skills will be provided. Ongoing financial sector monitoring will form part of the AAA agenda.

• Creating a diversified financial sector. The Bank will support non-bank financial institutions—including capital markets, insurance, and pensions—and their regulation and supervision through technical assistance, advisory services, and AAA. A lending project to support capital market infrastructure in FY05 is under discussion. A comprehensive strategy for reform of non-bank financial institutions and a diagnosis of the pension system will form part of the AAA agenda.

• Improving access of the poor to financial services. Micro-finance delivery is currently supported through the ongoing CDD and rural area development projects. A micro-finance project as well as analytical work will support increased linkages of these institutions with the formal financial sector and work with commercial banks to increase their outreach in rural areas.

• Anti-money laundering. The Bank will coordinate with other donors and provide advisory services and AAA to support Indonesia in implementing its recently revised anti-money laundering legislation.

• Joint IFC-Bank activities. IFC and the Bank will work together to assist in the development of financial market infrastructure such as credit bureaus, and key market segments such as housing finance and securitization.

27. Fostering a competitive private sector. Integrating private sector involvement into Bank projects as well as activities aimed at developing the private sector in a decentralized environment will be areas of key focus. Bank Group support will include:

• Building the institutions for a competitive economy. A policy-based loan programmed for FY05 linked to significant progress in the Government’s Economic Policy Package will support improvements in the regulatory environment that will enhance private sector competition. Support will also be aligned to improve competition in key industries, including support for the regulatory bodies in electricity, telecommunications, oil and gas. Ongoing power projects, as well as a new domestic gas project will promote unbundling and enhanced competition in the power sectors. The Bank will also seek greater clarity and predictability in the enforcement of environmental regulations, through support to the Government’s Good Environmental Governance (GEG) Program.

• Monitoring the investment climate and promoting dialogue. A program of national, local and rural business climate surveys is currently being set up, and will be supported by diagnostic work on private sector constraints, including a Diagnostic Trade Integration Study and a Domestic Trade Study. The national- level Private Sector Forum will continue to be organized by the IFC in the context of the Consultative Group meetings to enhance the dialogue between the Government and the private sector. Current topics include, for example, private investment in the power sector, mining, banking, the role of the commercial courts and corporate governance. At the local level,

Indonesia Country Assistance Strategy 19

the Bank will support improving the business climate through dialogue between private sector, including small-scale entrepreneurs, and the local government.

• Strengthening corporate governance and key oversight institutions. Corporate sector monitoring will form part of the AAA agenda. Assistance will continue to be provided to institutions such as the Competition Agency, the Corporate Directors’ Institute, and auditing and accounting bodies, and a review of corporate governance is being completed.

• Support for SME development. The IFC’s new Program for Eastern Indonesia SME Assistance (PENSA) will be the Bank Group’s main vehicle capacity building for SMEs (see Box 3). It will be supported by business climate programs through the Bank’s decentralized governance programs (see section B).

Box 3. The Program for Eastern Indonesia SME Assistance (PENSA)