Embed Size (px)

Citation preview

Exploring “Value for Money” Analysis in Low-Income

Countries Lessons learned from a PPP project in Tanzania

May 6th 2015

Lincoln Flor Bernardo Weaver

Marcelo PérezIrene Portabales

2

3

This paper presents a user-friendly two-step Value for Money (VfM) model tohelp Low-Income Countries (LICs) to understand and discuss qualitative andquantitative reasons to consider the likely implementation of a project under aPPP scheme, rather than conventional procurement.

The first section includes some reasons why governments decide to implementPPP or traditional procurement, with or without (VfM) analysis.

Why PPPs and VfM in LICs?

• Middle income countries with PPP experience see highcomplexity implementing traditional VfM analysis (PSC andtraditional approach). Other are refusing VfM analysis.

• IUK is reviewing policies and VfM approach.

• In LICs challenges preparing, procuring and monitoring ishuge:Weak institutional capacity

Constrains in fiscal space

Shallow capital markets.

limited track-record on traditional procurement and PPP deals

• Then, why and how VfM in PPPs can be addressed in LICs?

4

Follow VfMprinciples..., made it simple, practical and effective

• LICs have to discuss why a particular project has to be implement as a PPP.

• What comprise this discussion and what is the right balance, between:

• VfM provides information for the discussion and helps to take a decision.

• VfM (positive and quantitative) means: the project has to be a PPP? 5

Quantitative

Qualitative

Simplified VFM Analysis

Effectiveness

Efficiency

Economy

Motivation for PPPs are not only VfMPPPs Vs. Traditional Procurement:

What are we seeing?

PPPs• Accelerate public

investment programs• Maximize available public

funding• Is the only way to

implement the project• Achieve VfM if PPP if risks

are well allocated• Help keep maintenance

standards

Traditional Procurement

• Widely used, so all parties understand roles and concepts

• Procurement is standardized; government knows how to work

• Government retains control of the whole operation

6

VfM analysis also helps to spot disadvantages:

PPPs issues

• Contract renegotiations affect VfM if risk allocation changes

• Governments might use PPPs as a way to avoid fiscal controls

• PPPs can be more expensive than public procurement

Traditional Procurement issues

• Design and construction done in sequence by different parties

• Contractors’ expertise is not used in the design phase

• Projects are affected by short-term budget constraints

7

8

The second section describes the evolution and trends of PPPs in LICs in the past25 years.

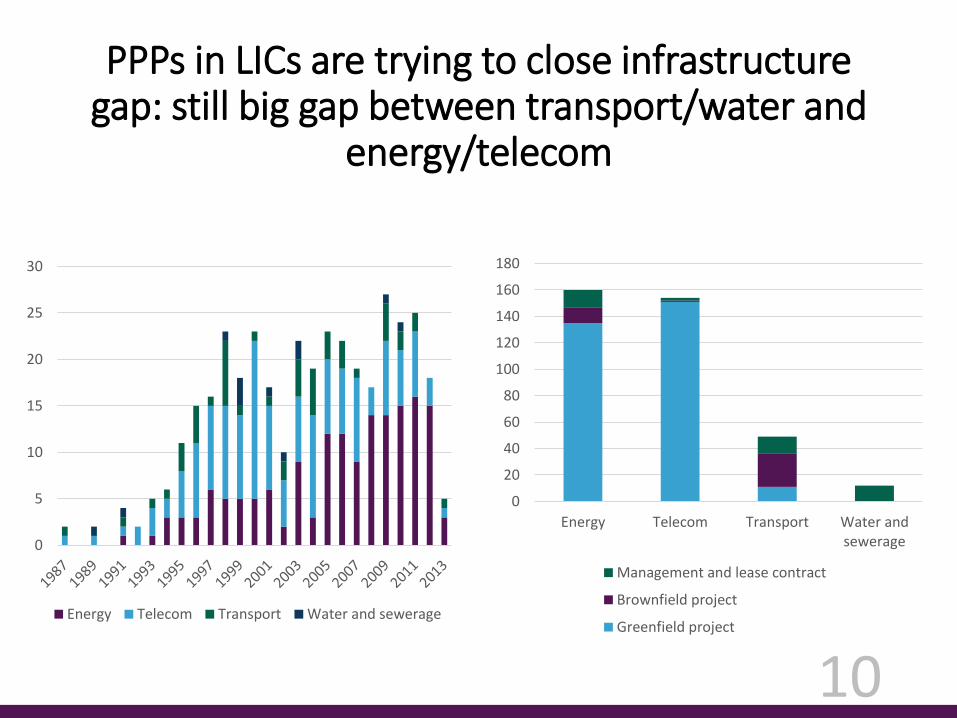

Close to 400 PPPs in LICs?(1987 to 2013, PPIAF data)

9

PPPs in LICs are trying to close infrastructure gap: still big gap between transport/water and

energy/telecom

0

5

10

15

20

25

30

Energy Telecom Transport Water and sewerage

0

20

40

60

80

100

120

140

160

180

Energy Telecom Transport Water andsewerage

Management and lease contract

Brownfield project

Greenfield project

10

11

The VfM model featured in this paper: a simple, practical and effective VfManalysis model for PPPs in LICs.

VfM Model Structure:2 Stages = Preparation and Application

12

THE MODEL PROVIDES BASE LINE INFORMATION THAT CAN BE ENHANCED BY OFFICIALS

Holistic approach: from qualitative to quantitative, step by step:

Qualitative Analysis,

interviews. If the project reaches a minimum

level, then it can continue

to the quantitative

part

Quantitative Assessment based on the

effective fiscal cost

criteria

Risk Analysis

to find within a range of

certainty if the project yields VfM

VfM Analysis,based on

qualitative and

quantitative parts

13

More Data Entered: Larger certainty

More Steps on the Analysis: More ways to check for errors

Sample Qualitative Questions and Topics Topics Questions

FinancingPayment Mechanisms – Do these boost risk management?

Amount of investment – Is the contract large enough to cover PPP transaction costs?

Bankability and

Private Sector

Appetite

Market interest – Is there appetite for the project? Do market players have the experience to deliver expected results?

Competition - Does the project structure stimulate competition? Does it lead to price reduction and higher efficiency?

Bankability – Is the project bankable? How costly are these funds? And is there access to IFIs and/or to local banks?

Implementation

Capacity and

Knowledge

Technical and operational capacity – Is there technical capacity available in the market to implement the project?

Institutional capacity – Is the government prepared to structure the project and monitor the contract?

Monitoring – Are projects inputs and outputs objective and measurable? Can they be assessed against common standards?

Risk Transfer

Risks – Are risks allocated to the party better prepared to manage and mitigate them?

Overinvestment – Is the contract structured on a manner that it does not incentivize overinvestment?

Flexibility – Is the contract flexible to mitigate demand changes? Is it structured to avoid political cycle changes?

Ability to manage risks – Can investors manage risks better than government in order to justify shifting risks?

Life cycle – Is it possible to integrate project design, construction, maintenance and operation?

Maintenance and

Rehabilitation

Economies of scale – Is rehabilitation and maintenance ensuring economies of scale for the project?

Key factor - Is maintenance and rehabilitation a key factor of the project? Is the private sector the best provider for these?

14

After all answers for theyes and no questions areentered, the MS Excelmodel will automaticallygenerate one of theseresults:

15 QUESTIONS

5 CATEGORIES

FURTHER QUESTIONS

Definition and Valuation of a general risk matrix:Sample Risk probability of occurrence and impact by

sector

15

Urban

Roads

Rural

Roads Railways

Public

Transport Energy Ports

Social Infra-

structure

PO IM PO IM PO IM PO IM PO IM PO IM PO IM

Implementation risk 90% 11% 95% 11% 92% 12% 93% 11% 94% 14% 95% 15% 96% 16%

Design risk 95% 30% 95% 30% 95% 15% 95% 30% 95% 15% 95% 15% 95% 15%

Funding risk 95% 25% 95% 25% 95% 25% 95% 25% 95% 25% 95% 25% 95% 25%

Exchange rate risk 95% 25% 95% 25% 95% 25% 95% 25% 95% 25% 95% 25% 95% 25%

Construction risk 95% 50% 95% 50% 95% 35% 95% 50% 95% 35% 95% 35% 95% 35%

Operation and performance 95% 35% 95% 35% 95% 15% 95% 35% 95% 15% 95% 15% 95% 15%

Regulatory risk 95% 10% 95% 10% 95% 10% 95% 10% 95% 10% 95% 10% 95% 10%

Risk of force majeure 95% 10% 95% 10% 95% 10% 95% 10% 95% 10% 95% 10% 95% 10%

Environmental risk 95% 10% 95% 10% 95% 10% 95% 10% 95% 10% 95% 10% 95% 10%

Demand risk 95% 20% 95% 20% 95% 20% 95% 20% 95% 20% 95% 20% 100% 20%

Political risk 95% 15% 95% 15% 95% 15% 95% 15% 95% 15% 95% 15% 95% 15%

16

BOT - No fare BOT - Fare TBOT - No fare TBOT - Fare DBOT - No fare DBOT - Fare

Public

Sector

Private

Agent

Public

Sector

Private

Agent

Public

Sector

Private

Agent

Public

Sector

Private

Agent

Public

Sector

Private

Agent

Public

Sector

Private

Agent

Implementation risk 100% 0% 100% 0% 100% 0% 100% 0% 100% 0% 100% 0%

Design risk 100% 0% 100% 0% 100% 0% 100% 0% 0% 100% 0% 100%

Funding risk 0% 100% 0% 100% 0% 100% 0% 100% 0% 100% 0% 100%

Exchange rate risk

Construction risk 0% 100% 0% 100% 0% 100% 0% 100% 0% 100% 0% 100%

Operation and performance risk 0% 100% 0% 100% 0% 100% 0% 100% 0% 100% 0% 100%

Regulatory risk 100% 0% 100% 0% 100% 0% 100% 0% 100% 0% 100% 0%

Risk of force majeure 100% 0% 100% 0% 100% 0% 100% 0% 100% 0% 100% 0%

Environmental risk 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Demand risk 100% 0% 0% 100% 100% 0% 0% 100% 100% 0% 0% 100%

Political risk 100% 0% 100% 0% 100% 0% 100% 0% 100% 0% 100% 0%

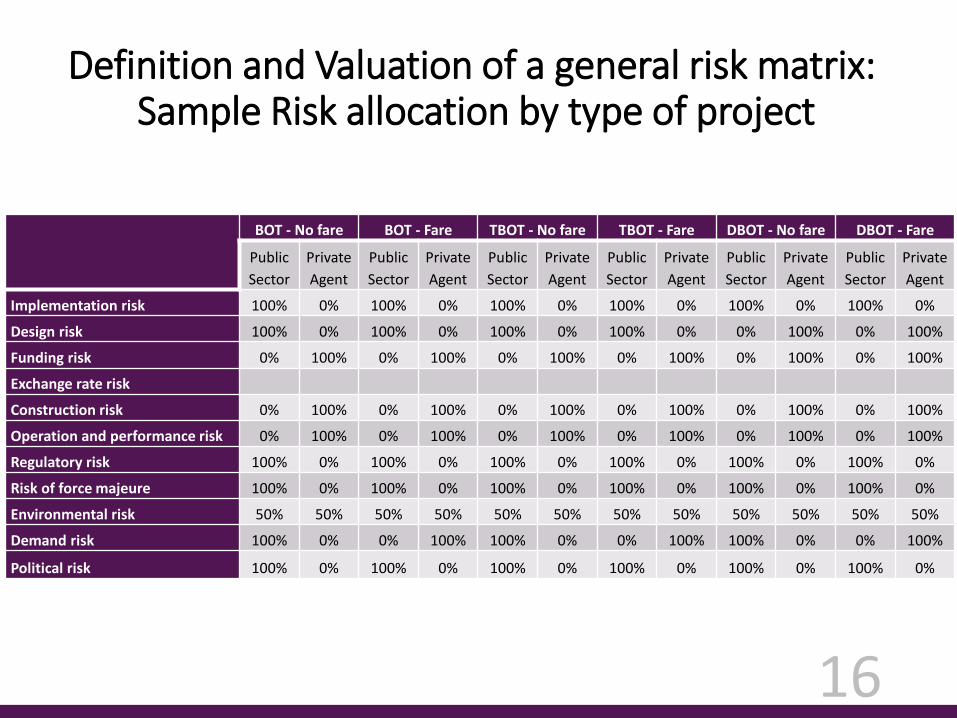

Definition and Valuation of a general risk matrix:Sample Risk allocation by type of project

17

VfM under quantitative analysis

Private provision

Public provision cost adjusted by risk

allocation

Private provision cost adjusted by risk

allocationVFM

VFM > 0?

Public provision

Private provision

Yes

No

Value for Money Map

VfM MAPQUANTITATIVE EVALUATION

0-20% 20-40% 40-60% 60-80% 80-100%

QU

ALI

TATI

VE

EVA

LUA

TIO

N

Generates high

Generates

moderate

Generates low

Generates

minimum

Does not Generate

18

PUBLIC

PROCUREMENT

PPP

19

INITIAL SIMPLIFIED

MODEL

Increasenumber of questions

Weightquestions

Deeper risk analysis

...

Adding complexity modularly

This model was designed using a bottom-up approach. As this is an initial dualand simplified model embodying the principles of VfM, where complexity canbe incorporated modularly. If a more sophisticated analysis is desired,governments could add complexity as human capital is strengthened andproject data is more reliable.

20

The fourth section presents the application in a BRT project in Tanzania. In thiscase, the results show a 62 percent chance that the given project wouldgenerate VfM. This figure can vary, depending on risk distribution and valueinputs. After a qualitative and quantitative analysis and simulations, the BRT inTanzania would yield VfM for the local government.

The case of Tanzania: BRT project: lacking the following• Sound PPP policy;

• Human capital to design and implement projects;

• Long-term financing and guarantees;

• Negotiations, contract supervision, and implementation and management capacity;

• Risk-sharing mechanisms, guarantees;

• Mechanisms to recover capital from private investors;

• Lack of public awareness of PPPs and their benefits; and

• Role of Ministry of Finance.

21

Who do what in PPPs in Tanzania?Institution PPP projects role

Contracting Authority (CA)

CAs are the actual “project owners,” usually a line ministry, a developing agency, or a multilateral development agency.

Their staff takes the lead on the project.

Project Development Team (PDT)

CA’s PDT chooses which project should be done, and

conducts pre-feasibility studies and procurement.

Line Minister (LM)

LM interacts with PDT along the project; reviews and

approves feasibility study for the PPP coordination unit and

the finance unit.

Accounting Officer (AO) AO negotiates and designs the agreement.

Project Management Team (PMT) PMT carries out contract management tasks.

Tanzania Investment Centre PPP Coordination Unit (PPPCU)PPPCU Advises and recommends pre-feasibility/feasibility

studies submitted by CA.

Ministry of Finance

Reviews and approves key aspects of the PPP project cycle.

Minister of Finance MoF gives final approval before procurement.

PPP Finance Unit (PPPFU)

PPPFU receives PPP draft agreement, decides on its

approval before sending it to MoF for final approval.

Attorney-General´s Office (AGO)AGO reviews draft contract to issue legal opinion.

Regulatory Authorities (RA)RA provides advice to CA on project implementation.

22

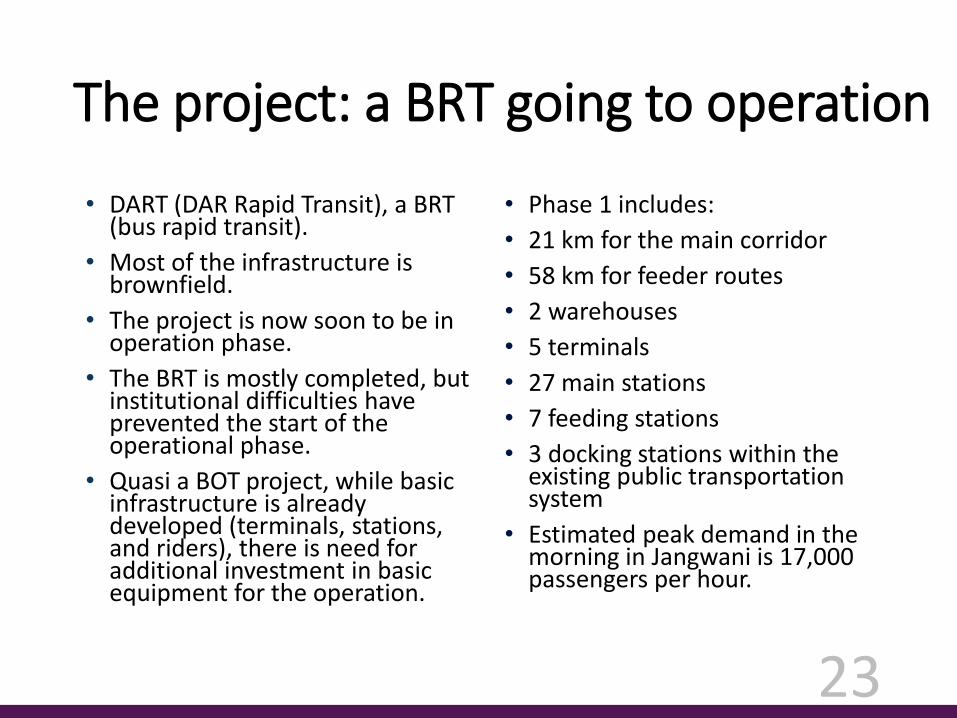

The project: a BRT going to operation

• DART (DAR Rapid Transit), a BRT (bus rapid transit).

• Most of the infrastructure is brownfield.

• The project is now soon to be in operation phase.

• The BRT is mostly completed, but institutional difficulties have prevented the start of the operational phase.

• Quasi a BOT project, while basic infrastructure is already developed (terminals, stations, and riders), there is need for additional investment in basic equipment for the operation.

• Phase 1 includes:

• 21 km for the main corridor

• 58 km for feeder routes

• 2 warehouses

• 5 terminals

• 27 main stations

• 7 feeding stations

• 3 docking stations within the existing public transportation system

• Estimated peak demand in the morning in Jangwani is 17,000 passengers per hour.

23

VfM qualitative: moderate, go to next step

24

Quantitative VfM: high

25

Value for money map for the project

26

VfM MAPQUANTITATIVE EVALUATION

0-20% 20-40% 40-60% 60-80% 80-100%

QU

ALI

TATI

VE

EVA

LUA

TIO

N

Generates high

Generates

moderate

Generates low

Generates

minimum

Does not Generate

PUBLIC

PROCUREMENT

PPP

PPP

PPP

Tanzania

BRT

27

Finally, based on the case some key lessons learned are identified.

The model’s main advantage is its simplicity.

The model has the capacity to provide valid information to discuss if a project can be implemented as a PPP or traditional procurement.

It can be useful in LIC but also in countries with weak institutional capacity (including some subnational governments in MICs).

A key factor for guaranteeing the applicability of this model to find an appropriate balance between the qualitative and quantitative analysis.

The model can have more complexity added modularly. Application of a bottom-up approach.

Importance of a two stages approach, one for preparation and one for application.

On Stage One, the profile of respondents is crucial to avoid conflict of interest. (balance of multiple expertise, no conflict of interest, etc.) 28

The initial use of pre-stablished parameters for the risk analysis is an appropriate approach to mitigate the risks of lack of project data, as well as of data manipulation.

More accurate and better information should help LICs government officials and their advisors produce important decisions with a higher degree of certainty.

Reducing government mistakes can be an important step in enhancing accuracy of infrastructure assets and services delivery to the population.

Infrastructure projects accuracy should be especially important because of the well-known social impact of many of these projects and the sheer size of these economic interventions.

29

Thank you!Lincoln Flor

Bernardo Weaver

Marcelo Pérez

Irene Portabales

However, more research efforts and discussions areneeded to continue improving VfM approaches and toolsto select the right PPP project. This is an ongoing work…

Sample Risk Analysis – Crystal Ball Simulation

31