Embed Size (px)

Citation preview

This article was downloaded by: [George Mason University]On: 06 July 2014, At: 10:17Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registered office: MortimerHouse, 37-41 Mortimer Street, London W1T 3JH, UK

Journal of International Consumer MarketingPublication details, including instructions for authors and subscription information:http://www.tandfonline.com/loi/wicm20

Factors Influencing Online and Post-purchaseBehavior and Construction of Relevant ModelsWen-Bao Lin aa Department of Business Administration , National Formosa University , Yunlin, TaiwanPublished online: 08 Sep 2008.

To cite this article: Wen-Bao Lin (2008) Factors Influencing Online and Post-purchase Behavior and Construction ofRelevant Models, Journal of International Consumer Marketing, 20:3-4, 23-38

To link to this article: http://dx.doi.org/10.1080/08961530802129151

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) containedin the publications on our platform. However, Taylor & Francis, our agents, and our licensors make norepresentations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose ofthe Content. Any opinions and views expressed in this publication are the opinions and views of the authors,and are not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be reliedupon and should be independently verified with primary sources of information. Taylor and Francis shallnot be liable for any losses, actions, claims, proceedings, demands, costs, expenses, damages, and otherliabilities whatsoever or howsoever caused arising directly or indirectly in connection with, in relation to orarising out of the use of the Content.

This article may be used for research, teaching, and private study purposes. Any substantial or systematicreproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in anyform to anyone is expressly forbidden. Terms & Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

Factors Influencing Online and Post-purchase Behaviorand Construction of Relevant Models

Wen-Bao Lin

ABSTRACT. This study is attempted to combine the decomposition theory of planned behaviorwith the theories of relationship quality and product involvement to establish a complete model forthe explanation of factors influencing online investment and post-purchase behavior. The SEM causalmodel was used to verify the capability of the model to explain the online investment and post-purchasebehavior of consumers. Consumers in the top four largest cities in Taiwan who invest in financialproducts via banks were selected, and the number of research subjects was determined by the populationof each city. The stratified random sampling method was used for the survey and 274 valid questionnaireswere returned. The SEM model was used for data verification. In the preliminary fit, the financialsupport of family members has the highest influence on the decision of consumers (subjective norm),the incorrectness of product information announced by service providers is perceived by consumersas the highest risk (perceived risk), and the attractiveness of products is the most important variableto arouse the interest of consumers to buy (product involvement). As for the actual behavior, personalrequirements for investment are the most decisive factor for consumers to take actions. The correctnessof products is the most influential factor for the gap of perceived service quality. Among the parametersunder the post-purchase behavior, the external response and internal response are most decisive forconsumers to take actions after they have made a purchase. As for the internal fit, the subjective normto actual behavior, perceived risk to actual behavior, subjective norm to post-purchase behavior, andgap of perceived service quality to post-purchase behavior reach the significant level and the overallgoodness-of-fit of the research model was satisfactory.

KEYWORDS. Decomposition theory of planned behavior, relationship quality, product involvement,structural equation model (SEM)

With the development of IT technology,many consumers use the Internet as a tool thathelps them collect information on products andservices easily and rapidly. Particularly, the real-time interactive communication of multimedia,a network technology that combines text, voice,and other media for interaction, provides a morefriendly and effective communication mecha-nism than conventional media. For financialinstitutions, the Internet not only reinforces the

Wen-Bao Lin is affiliated with the Department of Business Administration, National Formosa University,Yunlin, Taiwan.

Address correspondence to Wen-Bao Lin, Department of Business Administration, National Formosa Uni-versity, No. 64, Wunhua Road, Huwei Township, Yunlin County, Taiwan–Republic of China. E-mail: [email protected]

relationship between banks and consumers, butalso adds a new element to the marketing mixof banks. For consumers, collecting informationand feedback on investment products for theirpurchase via a plurality of routes in a mannersimilar to direct sale is a manifestation ofrelationship marketing.

In an environment in which the nationaleconomy is continually improved continually,banks and other financial institutions should,

Journal of International Consumer Marketing, Vol. 20(3–4), 2008Available online at http://jicm.haworthpress.com

C© 2008 by The Haworth Press. All rights reserved.doi: 10.1080/08961530802129151 23

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

24 JOURNAL OF INTERNATIONAL CONSUMER MARKETING

in addition to upgrading their hardware andsoftware, improve their customer relationshipmanagement to meet the coming challenges.Merely using traditional marketing strategiesand reinforcing motivations is not sufficientto improve interactive relationships with cus-tomers. Rather, how to trace the performanceof short-term transactions and convert them tolong-term relationships is a critical element forwhich service providers must take actions for itsachievement, needless to say that the cost fordeveloping new markets is much higher than thecost for retaining existing customers. Accordingto Lovelock’s (1981) classification of serviceencounters by product attributes, the bankingindustry is a branch of industries where serviceencounter is crucial for its service quality.Berry and Parasuraman (1991) also suggest thatservice providers may increase their marketshare by decreasing loss of existing customersand providing more trading approaches for theircustomers. In addition to looking for partners,service providers of banks and other financial in-stitutions should make efforts to ensure repeatedpurchase behavior of existing customers for theirsurvival in the fiercely competitive environment.The study will discuss this topic based on theconcept of relationship marketing.

Previous researches on factors that affect thewillingness to consume or consumer behavioron the Internet usually proceeded with thefollowing approaches: (1) Theories: Intention ofconsumer behavior and attitude of consumerswere discussed based on different theories.While some researchers analyzed the influenceof website system construction on the willing-ness to consume based on the Technology Ac-ceptance Model (TAM) (Moon and Kim, 2001),others applied the Theory of Planned Behavior(TPB) and Decomposed Theory of PlanningBehavior and brought up a more comprehensivedescription of the willingness to consume on theInternet and the understanding of using informa-tion technology. There are some technologicaland psychological factors affecting the Inter-net consumer. (Ajzen, 1991; Taylor and Todd,1995a); (2) Industries: The service industry wasthe focus of this approach and different theorieswere discussed to explain purchase intentionand behavior patterns (Ajzen and Driver, 1992;Henderson, Rickwood and Roberts, 1998; Liao,

Shao,Wang and Chen, 1999); (3) Website ande-Commerce: Planning of website content andconstruction of website systems or implemen-tation of e-Commerce were discussed for theirinfluence on service providers. Lai and Yang(1998), for example, proposed an IA-basedcustomized marketing system to solve the prob-lems encountered by consumers when they surfthe World Wide Web, while Bloch and Segev(1997) discussed the influence of e-Commerceimplementation on service providers from theviewpoint of the supply chain; (4) Purchase deci-sion: Factors that influence the purchase decisionof consumers were discussed. For example, theEKB model (Enge & Kollat & Blackwell model)and Howard-Sheth model (Evans and Berman,1994; Engel, Blackwell and Miniard, 1995) wereused to explain and predict the cause for and con-sequence of consumer behavior. In other words,previous research focused on the followingthree dimensions: (1) Explaining and predictingconsumer behavior based on consumer behaviortheories; (2) Stressing the influence of variousindustrial characteristics on consumer behaviorand explaining the difference; (3) Focusingon the construction of software and hardware,e.g., construction of websites and their contentfeatures.

In spite of the fact that much researchhas focused on online consumer behavior, thefollowing topics are not either touched uponor completely explained and need to be ex-plored further: (1) Factors that influence theactual online consumer behavior: Only part ofthe causal variables were discussed (Leblance,1992; Ducoffe, 1996) or described based onother models (e.g., Rogers, 1983, using theInnovation Diffusion theory to support his ar-gument of consumer behavior), and only a fewresearchers focused on the examination of thesuitability of models derived from integratedor expanded theories; (2) Most of the previousstudies focused on the intention of consumerbehavior (Hou and Lin, 1997; Ajzen and Fish-bein, 1980), and studies on factors that mayinfluence actual purchase and post-purchasebehavior were rare; (3) Most researchers usedthe Multivariate Statistical Analysis approachfor their research, but the causal model and pathanalysis of the Structural Equation Model (SEM)were rarely touched.

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

Wen-Bao Lin 25

Factors influencing the actual purchase be-havior of consumers include variables that canbe observed directly, such as marketing mixes,product features and demographics, and vari-ables that cannot be observed directly, suchas psychological, social and cultural variables(Engel et al., 1995; Teo, Vivien, and Lai, 1999;Lai, 2000). Pervious researches were capable ofexplaining factors influencing consumer behav-ior based on the Theory of Planned Behavior,Decomposition Theory of Planned Behavior andTechnology Acceptance Model (Ajzen, 1985;Davis, Bagozzi and Warshaw, 1989; Moon andKim, 2001). However, these researches wereeither involved in products to a limited extentor rarely made analysis from the viewpointof product involvement. The Study discussesthe online investment behavior and, thus, issignificantly involved in products. Since the per-ceived risk of consumers has great influence ontheir purchasing behavior, the Study is trying tocombine the Decomposition Theory of PlannedBehavior with the theories of relationship qualityand product involvement to establish a completeresearch model. The SEM causal model isused to verify the capability of the model toexplain the online investment and post-purchasebehavior of consumers.

Based on the above description, the objectivesof the study are summarized as follows based onthe above description:

1. Providing a model for factors that affectonline actual purchase behavior and post-purchasing behavior by integrating the De-composition Theory of Planned Behaviorwith the theories of relationship quality andproduct involvement.

2. Inferring management implication fromverified provider’s data based on SEM.

LITERATURE REVIEW

Decomposition Theory of PlannedBehavior

The Theory of Rational Activity (TRA) ar-gues that behavior is a controllable factor underpersonal willpower and ignores the importance

of uncontrollable factors (Ajzen,1985). Thisignorance is modified by the argumentation ofthe Theory of Planned Behavior. It emphasizesnot only personal motive and attitude towardbehavior inclination and actual purchase behav-ior, but also the influence of external factorson the subjective norm of individuals towarda certain behavior. Advocates of the Theory ofPlanned Behavior also argue that the behaviorintention and actual purchase behavior are de-pendent on whether an individual has adequateopportunities, resources and familiarity with theimplication of a certain product.

Taylor and Todd (1995a, 1995b) combinethe advantages of the Technology AcceptanceModel and Theory of Planned Behavior and ex-plain consumer behavior on a more comprehen-sive basis. Like the Theory of Planned Behavior,they find that the positive “subjective norm” andnegative “perceived risk” are important for apotential consumer to use IT systems or buyproducts. As for the factors affecting the onlineinvestment and consumer behavior as discussedin the Study, many researches find that servicefeatures of a website, such as interactivity, con-venience, informatively reliability and qualityassurance are important dimensions to attractconsumer’s attention. (Eighmey, 1997; Ducoffe,1996; Parasuraman, Zeithmal and Berry, 1988).Product involvement is another attractive aspectfor consumption (Zaichkowsky, 1985; Beattyand Smith, 1987).

The study adopts the following two dimen-sions of the Decomposition Theory of PlannedBehavior: (1) Subjective Norm: the complianceof an individual with opinions of other peopleor organizations for decision of taking actions.The Study uses the opinion of family membersor peers of a consumer on the content ofinvestment-related websites as major variables;(2) Perceived behavioral control: the assessmentof overall risks when a consumer is in a certainpurchasing situation.

Product Involvement Theory

Theoretically, observation and explanation ofproduct involvement is different depending onthe subjects and objects of the research. (1)As for subjects, Zaichkowsky (1985) finds that

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

26 JOURNAL OF INTERNATIONAL CONSUMER MARKETING

involvement “is a psychological perception ofaffairs based on inner demands, values andinterest of an individual”. When comparing thepersonal involvement of Zaichkowsky (1985)and the purchase decision of Mittal (1989),Pallister and Gorden (1998) and find that boththeories are different in the ratio of rationaland emotional involvement of a consumer. Thepersonal involvement focuses on assets man-agement of a consumer and is more rationalwhen involvement of the consumer is assessed.The purchase decision focuses on the purchasesituation that a consumer is facing and is concur-rently rational and emotional when involvementof the consumer is assessed. (2) As for enduringconcern about and efforts made for a prod-uct, Marsha and Bloch (1986) classify productinvolvement into situational involvement andenduring involvement. The former relates tothe product involvement occurring in a specialsituation (e.g., the situation of purchasing aspecial product) and is normally temporary orinfrequent. The latter relates to the enduringconcern of a consumer about a product becausethe product is important to the consumer orthe consumer has to be concerned about theproduct on a long-term basis. The enduringinvolvement indicates a steady purchase statusand great interest in the product. Both theoriesare also different in the efforts for collectionof product information and the latter is usuallyhigher than the former. Beatty and Smith (1987),for example, point out in their studies thatconsumers usually collect more informationwhen purchasing high-value or complicatedproducts to relieve financial and psychologicalrisks and show their concern about the products.The products, such as funds, stocks and otherhigh-value or complicated products, discussedin the Study are highly-involved investmentproducts and, thus, classified in the categoryof enduring involvement. Generally speaking,consumers are more rational than emotionalwhen buying financial investment products.

Relationship Quality

Parasuraman et al. (1988) create a measuringcriterion SERVQUAL for perceived servicequality of consumers. They classify the service

quality dimensions into five elements: Tangi-bility (including substantial facilities, tools forrendering service, and appearance of staffs);Reliability (the capacity of fulfilling servicecommitments correctly and reliably); Response(the capacity of staff to give feedback to con-sumers quickly); Correctness (knowledge andpoliteness of staffs to make them trustworthy toconsumers);and Care (the capacity of staffs toshow their concern for consumers).

Boulding, Kalra, Staelin and Zeithmal (1993)create the “Dynamic Process Model of ServiceQuality” and group the quality expected byconsumers into two categories: the quality levelthat should be reached by the service providerin an ideal service environment, and the qualitylevel that can be reached by the service providerin a restricted realistic environment.

Parasuraman et al. (1985) point out that actualperception of quality level is determined bycomparing expected and actual level of servicequality. He puts forward five gaps as criteriato determine the quality level. Gap1 and Gap2 result from insufficient resources, market in-formation and operating capability of the serviceprovider, Gap 3 results from insufficient on-the-job training or inappropriate attitude of staffs,Gap 4 results from exaggerated commitmentof the service provider that cannot be fulfilledto meet the requirements of consumers, andGap 5 results from the difference between theexpected quality level and actual perception ofconsumers. The first four gaps are directly re-lated to the performance of the service provider,while the fifth gap is related to an overallassessment made by consumers about the servicequality.

One of the objectives of the Study is todiscuss the factors influencing the post-purchasebehavior of consumers and, thus, Gap 5 is used asa reference for argumentation of service quality.

Establishment of an Integrated Model

Both the “Technology Acceptance Model”and “Theory of Planned Behavior “ have goodexplanation for use behavior of informationtechnology (Davis et al., 1989; Mathieson,1991; Liao et al., 1999; Bhattacherjee, 2000).However, the Technology Acceptance Model

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

Wen-Bao Lin 27

stresses more on the influence of informationsystems on consumer behavior and ignores theeffect of social and psychological factors. TheDecomposition Theory of Planned Behavior, onthe other hand, has taken these factors into con-sideration in its analysis. The Study incorporatesthe concept of product involvement as it is onemotive of consumers when they are buying. Inother words, consumers usually collect a lotof product information actively when facinghighly-involved products to make the best deci-sion and reduce risks. The Study applies the rela-tionship quality to the analysis of post-purchasebehavior as the occurrence of post-purchasebehavior is dependent on the implication ofthe relationship quality. Since maintaining thesatisfaction of consumers is the goal of therelationship quality, how to eliminate the gapin relationship quality perception of consumersis the key for enterprises to retain customers.What the Study discusses is consumer behaviorrelated to highly-involved products and, thus,overall assessment of service quality is the coreof the analysis. Reasons for putting forward anintegrated model for the Study are as follows: (1)Though there is a great number of dimensionalvariables in an integrated model, it is requiredto combine three theories for the explanationof empirical data; (2) An intergraded modelis required to clarify the causal relationshipamong variables when LISREL model is usedfor verification; (3) Combining three theories toform an integrated model is helpful for completeanalysis of relevant factors, clear definitionof inter-variable relationship, and completestructure.

The EKB model or Decomposition Theory ofPlanned Behavior reflects the influence of inter-nal and external factors on consumer behavior.Especially, the stimuli received by consumerswhen they are shopping are identified and as-sessed via their internal information processingprocedure. Consumers will assess the contents ofpromotion activities or the tolerance of subjec-tive norms. They will also consider advantagesand disadvantages of shopping before actuallybuying products and compare the costs andbenefits that may occur after the purchase. Theywill take a positive attitude toward purchasingif the benefit is greater than the cost based on

their perceptive assessment. Otherwise, they willtake a conservative attitude. Though satisfactionof consumers with quality, features, and otheraspects of products is important for taking post-purchase actions, the attitude of reference and in-terest groups is decisive for conducting repeatedpurchase behavior or taking actions againstunsatisfactory products or service. In fact, socialgroups or social and cultural environment havegreat influence on the decision of consumers.Engel et al. (1995), for example, points out inhis research on factors affecting the decisionof consumers that consumers usually searchinformation externally when internally searchedinformation is deemed as unsatisfactory. Exter-nal searching approaches include mass mediaand social groups (including the primary relativerelationship and the secondary peers relation-ship). Schiffman and Kanuk (1987) also find thatbesides psychological factors external environ-ment (e.g., social and cultural environment) isanother factor influencing the actual purchasebehavior; in other words, subjective norms areimportant for the decision of consumers on theiractual purchase and post-purchase behavior.

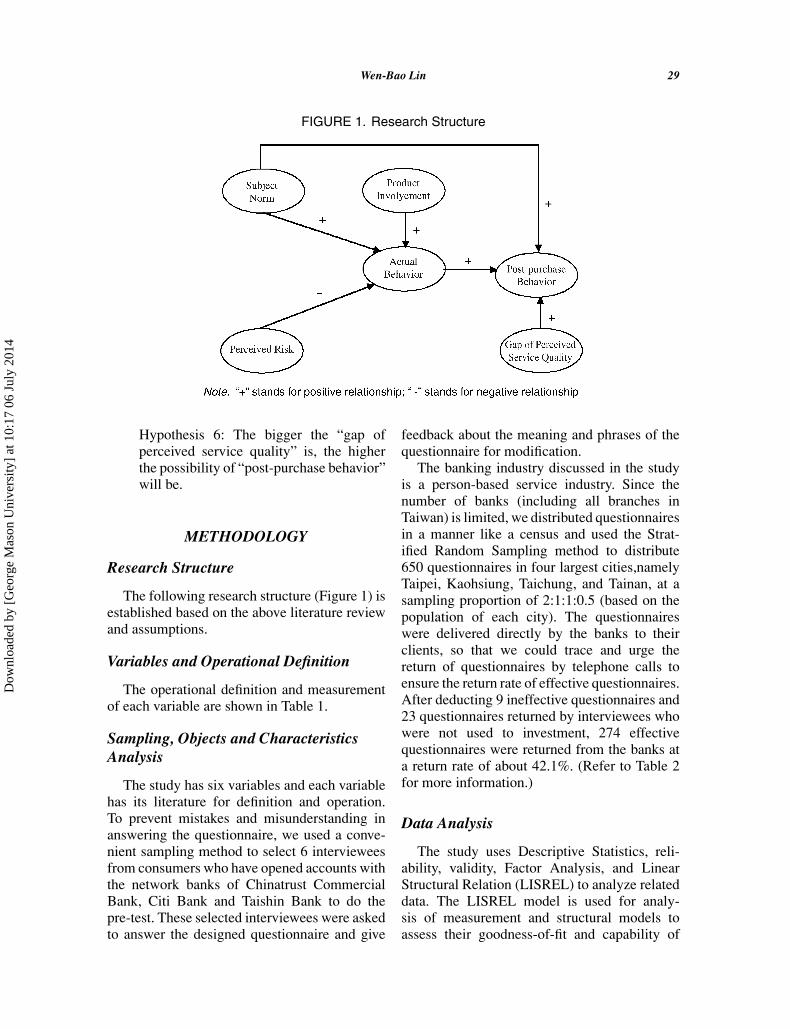

Hypothesis 1: “Subjective norm” has apositive effect on “actual behavior”

Hypothesis 2: “Subjective norm” has apositive effect on “post-purchase behavior”

According to previous studies on onlineconsumer behavior, most consumers transfer oreliminate consumption risks by means of variousmechanisms and strategies that are effectiveto reduce purchasing risks (Guseman, 1981;Boze, 1987). Tan (1999) points out that theattitude of consumers toward risks will affecttheir purchase intention and actual purchasebehavior on the Internet. Other studies alsoshow that every risk-reducing factor may affectconsumers’ willingness to buy and their pur-chase behavior (Guseman, 1981; Boze, 1987).Keeney (1999), for example, finds that assuringsecurity of transaction and protecting personaldata from disclosure have a positive effect onconsumers’ willingness to shop on the Internet.Swaminathan, Elzbieta and Bharat (1999) learnfrom their survey of online consumers for their

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

28 JOURNAL OF INTERNATIONAL CONSUMER MARKETING

experience that purchase intention or purchasebehavior is affected whenever consumers per-ceive higher purchasing risks.

Hypothesis 3: “Perceived risk” has a nega-tive effect on “actual behavior”.

When consumers perceive that the productis highly associated with their requirements,they will run into a highly involved state andcollect related product information actively,compare the difference between products andbrand names carefully, and make better decisionsto select appropriate products. The higher theassociation of an involved object with personalvalues, requirements and interest of a consumer,the more the involvement of the consumerwill be (Zaichkowsky, 1985). The consumer inthis highly involved state will be inclined toevaluate related information along the centralpath; otherwise, the consumer may evaluate theinformation along the peripheral path (Flynnand Goldsmith, 1993). The involvement ofconsumers in financial investment products asdiscussed in the Study is very high because theyare one of the tools for people to control theirincome and, thus, important for the improvementof their material life.

Hypothesis 4: The possibility of “actual be-havior” grows with the increase of “productinvolvement”.

Actual consumer behavior is affected by boththe stimuli brought by surroundings and thebehavioral intention of consumers. Like motive,the inner attitude and behavioral intention ofa consumer may affect his or her actual be-havioral models. Most consumers are hesitantor may take careful consideration before theybuy financial products, but they may run intoenduring involvement as described by Marshaand Bloch (1986) when making decision to buy,and extend their trading relationship with the ser-vice provider if the rate of return on investmentis satisfactory. Otherwise, consumers who arerational or want to make long-term investmentmay take other investment actions. The serviceprovider may contact with customers activelyin an adverse investment environment to give

acceptable reasons and consolidate the customerrelationship.

Hypothesis 5: “Actual behavior” has a pos-itive effect on “post-purchase behavior”.

Gronroos (1983) sorts the service qualityinto technical quality and functional quality byservice delivery. The former stresses whetherthe provided service can improve customersatisfaction, while the latter emphasizes whetherthe process and manner of service deliverycan improve customer satisfaction. Lovelock(1993) classifies the attribute of service productsinto person-based service and equipment-basedservice. The financial investment products asdiscussed in the Study have primarily person-based attribute with equipment as an auxiliary.Also, the service quality of these productsmainly belongs to the category of technicalquality with a few products belonging to thecategory of functional quality. Parasuraman etal. (1988) defines the service quality as the gapbetween the quality level expected by customersand the actual quality level provided by serviceproviders. The bigger the gap is, the worse theservice quality will be, and the smaller the gapis, the better the service quality will be. Bouldinget al. (1993) points out the association of servicequality with repeated purchase behavior of con-sumers. Parasuraman et al. (1996) further arguesthat service quality perceived by consumersmay have a positive or negative effect on theirrepeated purchase behavior. Consumers who donot encounter quality problems have a higherperception of service quality than those whoencounter problems, acquire satisfactory solu-tions, and do not manifest any transfer or externalresponse. However, these consumers may haveno higher intention of repeated purchase thancustomers whose quality problems are remedied.When consumers perceived negative servicequality, they could switch the brand of productand lower loyalty. In short, when perceiving abig gap of service quality, customers may feeldisappointed, reconsider post-purchase actionsor repeated purchase behavior, and, especially,request the service provider to patch up the gapby, for example, compensation or apology.

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

Wen-Bao Lin 29

FIGURE 1. Research Structure

Hypothesis 6: The bigger the “gap ofperceived service quality” is, the higherthe possibility of “post-purchase behavior”will be.

METHODOLOGY

Research Structure

The following research structure (Figure 1) isestablished based on the above literature reviewand assumptions.

Variables and Operational Definition

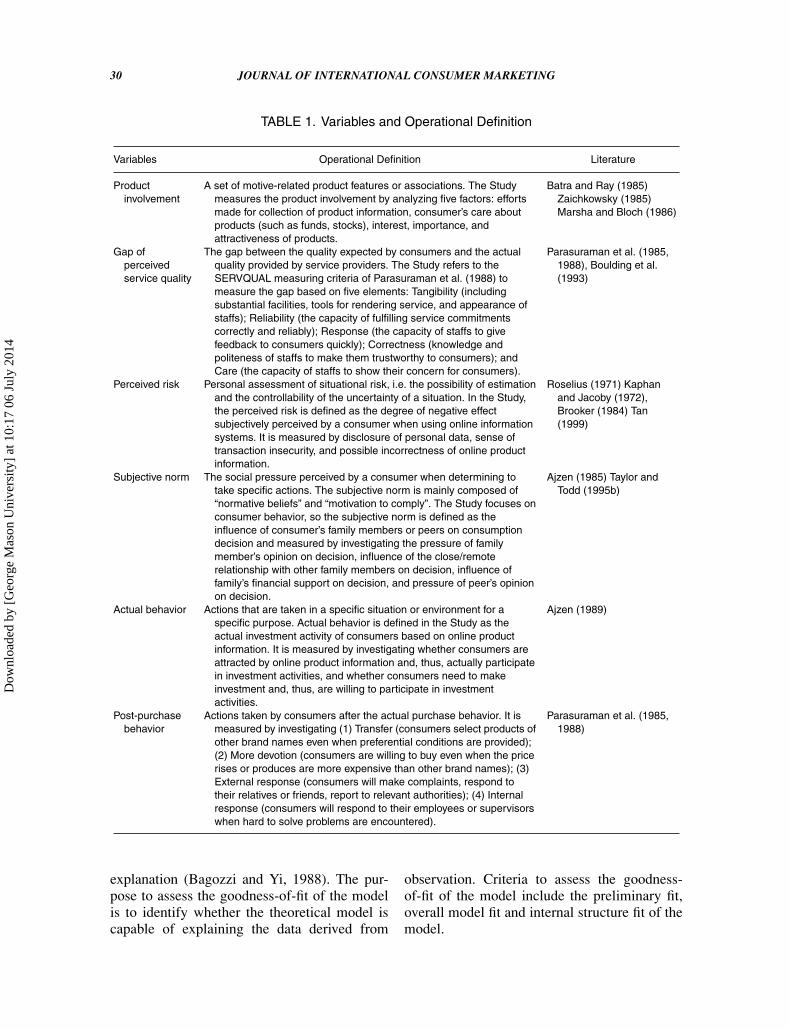

The operational definition and measurementof each variable are shown in Table 1.

Sampling, Objects and CharacteristicsAnalysis

The study has six variables and each variablehas its literature for definition and operation.To prevent mistakes and misunderstanding inanswering the questionnaire, we used a conve-nient sampling method to select 6 intervieweesfrom consumers who have opened accounts withthe network banks of Chinatrust CommercialBank, Citi Bank and Taishin Bank to do thepre-test. These selected interviewees were askedto answer the designed questionnaire and give

feedback about the meaning and phrases of thequestionnaire for modification.

The banking industry discussed in the studyis a person-based service industry. Since thenumber of banks (including all branches inTaiwan) is limited, we distributed questionnairesin a manner like a census and used the Strat-ified Random Sampling method to distribute650 questionnaires in four largest cities,namelyTaipei, Kaohsiung, Taichung, and Tainan, at asampling proportion of 2:1:1:0.5 (based on thepopulation of each city). The questionnaireswere delivered directly by the banks to theirclients, so that we could trace and urge thereturn of questionnaires by telephone calls toensure the return rate of effective questionnaires.After deducting 9 ineffective questionnaires and23 questionnaires returned by interviewees whowere not used to investment, 274 effectivequestionnaires were returned from the banks ata return rate of about 42.1%. (Refer to Table 2for more information.)

Data Analysis

The study uses Descriptive Statistics, reli-ability, validity, Factor Analysis, and LinearStructural Relation (LISREL) to analyze relateddata. The LISREL model is used for analy-sis of measurement and structural models toassess their goodness-of-fit and capability of

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

30 JOURNAL OF INTERNATIONAL CONSUMER MARKETING

TABLE 1. Variables and Operational Definition

Variables Operational Definition Literature

Productinvolvement

A set of motive-related product features or associations. The Studymeasures the product involvement by analyzing five factors: effortsmade for collection of product information, consumer’s care aboutproducts (such as funds, stocks), interest, importance, andattractiveness of products.

Batra and Ray (1985)Zaichkowsky (1985)Marsha and Bloch (1986)

Gap ofperceivedservice quality

The gap between the quality expected by consumers and the actualquality provided by service providers. The Study refers to theSERVQUAL measuring criteria of Parasuraman et al. (1988) tomeasure the gap based on five elements: Tangibility (includingsubstantial facilities, tools for rendering service, and appearance ofstaffs); Reliability (the capacity of fulfilling service commitmentscorrectly and reliably); Response (the capacity of staffs to givefeedback to consumers quickly); Correctness (knowledge andpoliteness of staffs to make them trustworthy to consumers); andCare (the capacity of staffs to show their concern for consumers).

Parasuraman et al. (1985,1988), Boulding et al.(1993)

Perceived risk Personal assessment of situational risk, i.e. the possibility of estimationand the controllability of the uncertainty of a situation. In the Study,the perceived risk is defined as the degree of negative effectsubjectively perceived by a consumer when using online informationsystems. It is measured by disclosure of personal data, sense oftransaction insecurity, and possible incorrectness of online productinformation.

Roselius (1971) Kaphanand Jacoby (1972),Brooker (1984) Tan(1999)

Subjective norm The social pressure perceived by a consumer when determining totake specific actions. The subjective norm is mainly composed of“normative beliefs” and “motivation to comply”. The Study focuses onconsumer behavior, so the subjective norm is defined as theinfluence of consumer’s family members or peers on consumptiondecision and measured by investigating the pressure of familymember’s opinion on decision, influence of the close/remoterelationship with other family members on decision, influence offamily’s financial support on decision, and pressure of peer’s opinionon decision.

Ajzen (1985) Taylor andTodd (1995b)

Actual behavior Actions that are taken in a specific situation or environment for aspecific purpose. Actual behavior is defined in the Study as theactual investment activity of consumers based on online productinformation. It is measured by investigating whether consumers areattracted by online product information and, thus, actually participatein investment activities, and whether consumers need to makeinvestment and, thus, are willing to participate in investmentactivities.

Ajzen (1989)

Post-purchasebehavior

Actions taken by consumers after the actual purchase behavior. It ismeasured by investigating (1) Transfer (consumers select products ofother brand names even when preferential conditions are provided);(2) More devotion (consumers are willing to buy even when the pricerises or produces are more expensive than other brand names); (3)External response (consumers will make complaints, respond totheir relatives or friends, report to relevant authorities); (4) Internalresponse (consumers will respond to their employees or supervisorswhen hard to solve problems are encountered).

Parasuraman et al. (1985,1988)

explanation (Bagozzi and Yi, 1988). The pur-pose to assess the goodness-of-fit of the modelis to identify whether the theoretical model iscapable of explaining the data derived from

observation. Criteria to assess the goodness-of-fit of the model include the preliminary fit,overall model fit and internal structure fit of themodel.

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

Wen-Bao Lin 31

TABLE 2. Basic Data of Samples in the Study

Feature of population

Numberof

samples % Family statusNumber ofsamples %

Sex Monthly household incomeMale 102 37.2% Under 20 thousand 27 9.9%Female 172 62.8% 20∼50 thousand 92 33.6%

AgeUnder 30∼ 13 4.7% 50∼100 thousand 121 44.2%31∼40 53 19.3% 100∼150 thousand 19 6.9%41∼60 172 62.8% 150∼200 thousand 10 3.6%61 and over 36 13.2% Over 200 thousand 5 1.8%

Education Marriage and childrenJunior high school or below 3 1.1% Single 27 9.8%Senior high (vocational) school 56 20.4% Married without children 40 14.6%Bachelor 148 54.0% Married with minor children 148 54.0%Master or above 67 24.5% Married with adult children 59 21.6%

Times of investment per year Occupation1 time 6 2.2% Soldiers, civil servants, and

educational employees72 26.4%

2∼3 times 15 5.5% Dealer 62 22.6%4∼5 times 58 21.1% Private enterprises 114 41.6%Over 5 times 37 13.5% SOHO 16 5.8%Uncertain 158 57.7% None (student, housewife) 4 1.4%

Others 6 2.2%

Reliability and Validity Analysis of Samples

Since the measurement and operation of allvariables are made based on previous litera-ture and the questionnaires are completed byconsumers who buy investment portfolios frombanks, the validity of the returned samplescan be ensured. To verify the reliability ofreturned samples, we use the item analysismethod to delete the questions in high and lowgroups that have no significant difference andcalculate the Cronbach’s a value of each variableusing the principle component factor analysismethod. The result of the calculation is shown inTable 3. The Cronbach’s a value of all variablesis higher than 0.6, indicating a guaranteed levelof reliability.

In the six-factor model established in theStudy, the factor loading of 23 measurementfactors is between 0.60 and 0.85 and the factorloading of all measurement factors reachesthe significant level (P < 0.01). The factorcomposite reliability (CR) value of the six-factormodel is between 0.714 and 0.865 (Table 4)and indicates an excellent internal consistence

of the model. The Average Variance Extracted(AVE) value of each factor is greater than 0.5and meet the requirements of the suggestedvalue.

TABLE 3. Reliability Analysis of Variables

Variables QuestionsCronbach’s α

value

Subjective norm 4 0.7635Perceived risk 3 0.8217Product involvement 5 0.8134Actual behavior 2 0.7652Post-purchasebehavior�Transfer 2 0.8316�More devotion 2 0.8034�External response 3 0.7659�Internal response 2 0.7382Gap of perceivedservice quality�Tangibility 3 0.8415�Reliability 2 0.8262�Response 2 0.7933�Correctness 3 0.7851�Care 2 0.8062

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

32 JOURNAL OF INTERNATIONAL CONSUMER MARKETING

TABLE 4. CR and AVE of the Six-factor Model

Taipei Area Taichung Area Tainan Area Kaohsiung Area

Latent Variables CR AVE CR AVE CR AVE CR AVE

Productinvolvement

0.815 0.628 0.845 0.643 0.807 0.627 0.812 0.635

Gap of perceivedservice quality

0.823 0.705 0.837 0.662 0.849 0.658 0.836 0.647

Perceived risk 0.796 0.574 0.806 0.582 0.835 0.573 0.829 0.552Subjective norm 0.807 0.623 0.714 0.619 0.764 0.625 0.753 0.611Actual behavior 0.835 0.562 0.793 0.543 0.821 0.502 0.807 0.563Post-purchase

behavior0.846 0.679 0.815 0.648 0.802 0.639 0.865 0.628

Linear Structural Relation (LISREL)Analysis

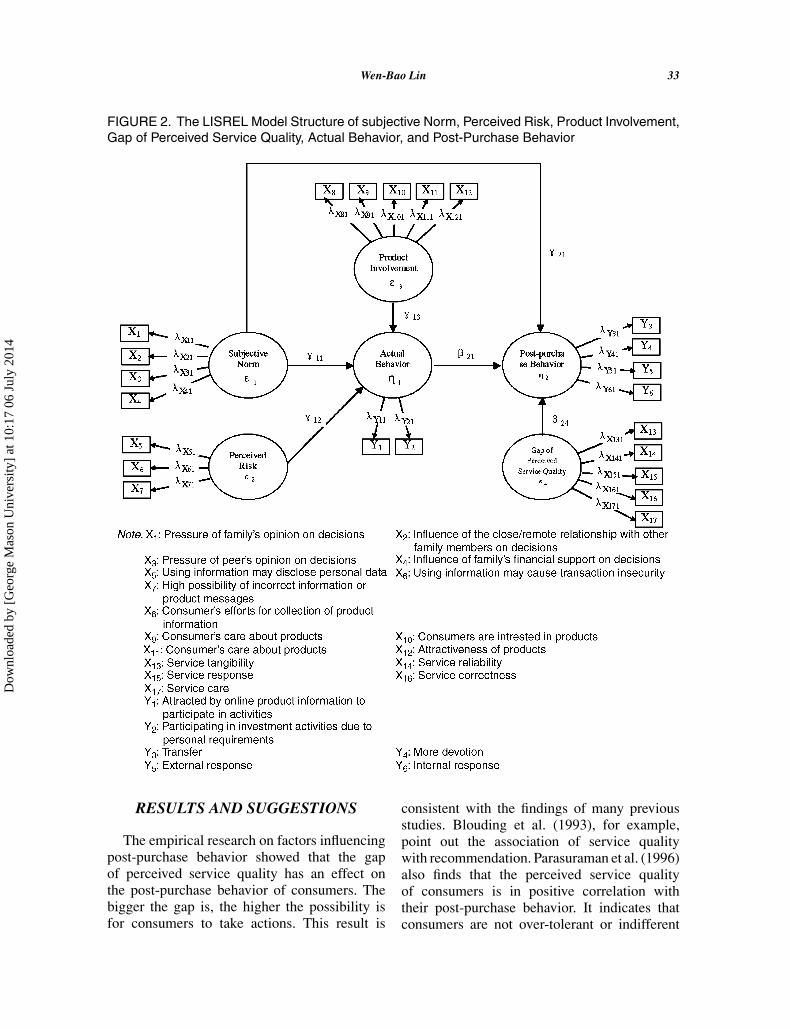

The objective of the study is to discuss factorsthat influence the actual and post-purchasebehavior of consumers. The causal relationshipamong the subjective norm, perceived risk, prod-uct involvement, actual behavior, post-purchasebehavior, and gap of perceived service quality isanalyzed based on the aforementioned literatureand LISREL model. A path drawing of theLISREL model is shown in Figure 2.

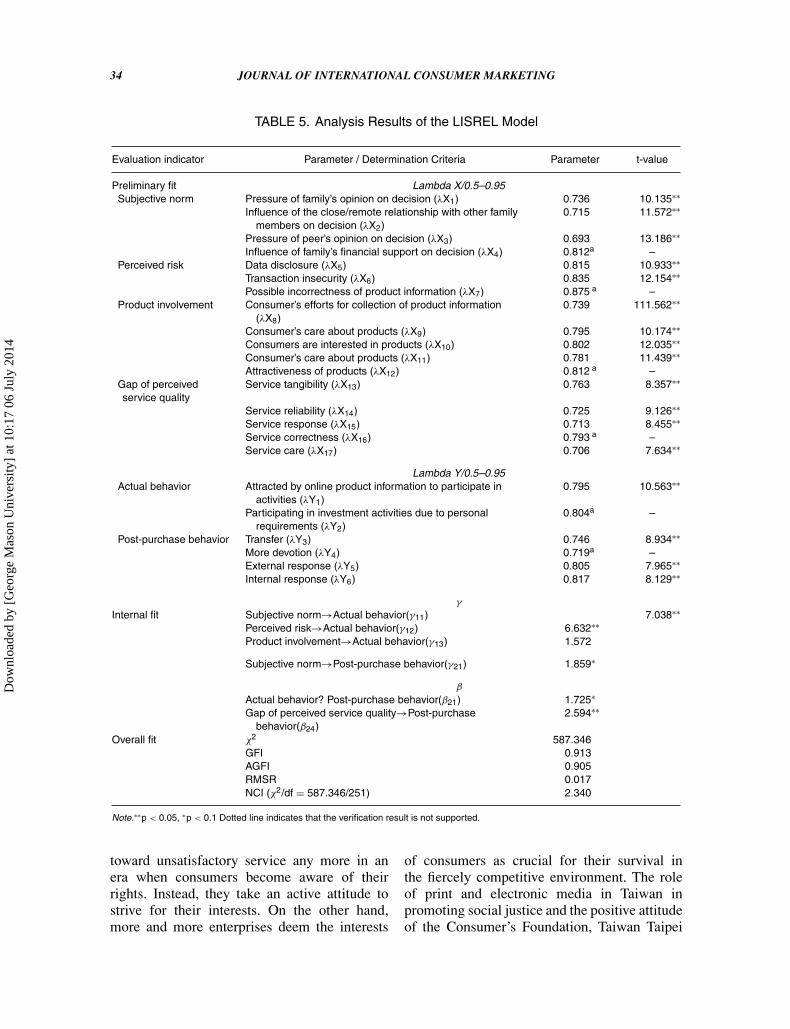

Figure 2 and Table 5 provide integrated dataof the analysis, while the verification result ofthe LISREL model is shown in Figure 3. TheLISREL model is used for analysis of mea-surement and structural models to assess theirgoodness-of-fit for assumptions. The measure-ment model includes analysis of the subjectivenorm, perceived risk, product involvement, gapof perceived service quality, and post-purchasebehavior. The influence of family’s financialsupport on decision is most significant (λX4 =0.812) among parameters under the subjectivenorm. It indicates that financial support is a veryimportant factor that consumers usually take intoconsideration when they are buying. Possible in-correctness of product information is the highestrisk (λX7 = 0.875) for consumers under the per-ceived risk, indicating that most consumers takea conservative attitude toward promotion activi-ties of service providers. Attractiveness of prod-ucts (λX12 = 0.812) is the most important vari-able under the product involvement to arouse the

interest of consumers to buy. As for actual behav-ior, personal requirements for investment (λY2= 0.804) are the most decisive factors for con-sumers to take actions. The correctness of prod-ucts (λX16 = 0.793) is the most influential factorfor the gap of perceived service quality. The anal-ysis result indicates that consumers need qualityservice from service providers and rely on theirexpertise and experience to make right decisions.Among the parameters under the post-purchasebehavior, external response (λY5 = 0.805)and internal response (λY6 = 0.817) are mostdecisive for consumers to take post-purchaseactions. It indicates that most consumers takesequential actions when they are dissatisfiedwith the service for their investment.

As for the structural model (Table 5), the γ

and β path coefficients show that the subjectivenorm to actual behavior (γ 11 = 0.634), per-ceived risk to actual behavior (γ 12 = 0.713),subjective norm to post-purchase behavior (γ 21= 0.354), and gap of perceived service qualityto post-purchase behavior (β24 = 0.533) arestatistically significant, except for the productinvolvement to actual behavior. It indicatesthat in addition to personal requirements forinvestment, the attitude of family members andfriends, and other factors, such as service level ofstaffs and problems encountered by consumersin their investment activities, may influence theactual and post-purchase behavior of consumers.In other words, the empirical result is affected byintervening variables. As a result, all hypothesesare supported except for Hypothesis 5.

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

Wen-Bao Lin 33

FIGURE 2. The LISREL Model Structure of subjective Norm, Perceived Risk, Product Involvement,Gap of Perceived Service Quality, Actual Behavior, and Post-Purchase Behavior

RESULTS AND SUGGESTIONS

The empirical research on factors influencingpost-purchase behavior showed that the gapof perceived service quality has an effect onthe post-purchase behavior of consumers. Thebigger the gap is, the higher the possibility isfor consumers to take actions. This result is

consistent with the findings of many previousstudies. Blouding et al. (1993), for example,point out the association of service qualitywith recommendation. Parasuraman et al. (1996)also finds that the perceived service qualityof consumers is in positive correlation withtheir post-purchase behavior. It indicates thatconsumers are not over-tolerant or indifferent

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

34 JOURNAL OF INTERNATIONAL CONSUMER MARKETING

TABLE 5. Analysis Results of the LISREL Model

Evaluation indicator Parameter / Determination Criteria Parameter t-value

Preliminary fit Lambda X/0.5–0.95Subjective norm Pressure of family’s opinion on decision (λX1) 0.736 10.135∗∗

Influence of the close/remote relationship with other familymembers on decision (λX2)

0.715 11.572∗∗

Pressure of peer’s opinion on decision (λX3) 0.693 13.186∗∗Influence of family’s financial support on decision (λX4) 0.812a –

Perceived risk Data disclosure (λX5) 0.815 10.933∗∗Transaction insecurity (λX6) 0.835 12.154∗∗Possible incorrectness of product information (λX7) 0.875 a –

Product involvement Consumer’s efforts for collection of product information(λX8)

0.739 111.562∗∗

Consumer’s care about products (λX9) 0.795 10.174∗∗Consumers are interested in products (λX10) 0.802 12.035∗∗Consumer’s care about products (λX11) 0.781 11.439∗∗Attractiveness of products (λX12) 0.812 a –

Gap of perceivedservice quality

Service tangibility (λX13) 0.763 8.357∗∗

Service reliability (λX14) 0.725 9.126∗∗Service response (λX15) 0.713 8.455∗∗Service correctness (λX16) 0.793 a –Service care (λX17) 0.706 7.634∗∗

Lambda Y/0.5–0.95Actual behavior Attracted by online product information to participate in

activities (λY1)0.795 10.563∗∗

Participating in investment activities due to personalrequirements (λY2)

0.804a –

Post-purchase behavior Transfer (λY3) 0.746 8.934∗∗More devotion (λY4) 0.719a –External response (λY5) 0.805 7.965∗∗Internal response (λY6) 0.817 8.129∗∗

γ

Internal fit Subjective norm→Actual behavior(γ11) 7.038∗∗Perceived risk→Actual behavior(γ12) 6.632∗∗Product involvement→Actual behavior(γ13) 1.572

Subjective norm→Post-purchase behavior(γ21) 1.859∗

β

Actual behavior? Post-purchase behavior(β21) 1.725∗Gap of perceived service quality→Post-purchase

behavior(β24)2.594∗∗

Overall fit χ2 587.346GFI 0.913AGFI 0.905RMSR 0.017NCI (χ2/df = 587.346/251) 2.340

Note.∗∗p < 0.05, ∗p < 0.1 Dotted line indicates that the verification result is not supported.

toward unsatisfactory service any more in anera when consumers become aware of theirrights. Instead, they take an active attitude tostrive for their interests. On the other hand,more and more enterprises deem the interests

of consumers as crucial for their survival inthe fiercely competitive environment. The roleof print and electronic media in Taiwan inpromoting social justice and the positive attitudeof the Consumer’s Foundation, Taiwan Taipei

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

Wen-Bao Lin 35

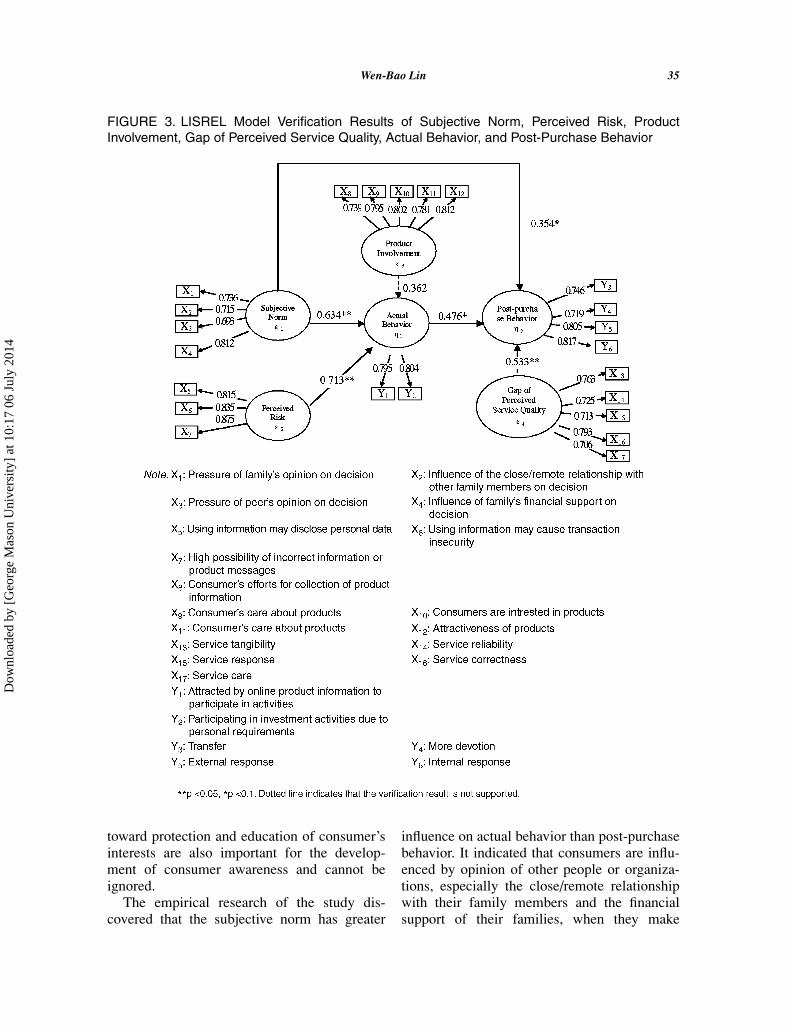

FIGURE 3. LISREL Model Verification Results of Subjective Norm, Perceived Risk, ProductInvolvement, Gap of Perceived Service Quality, Actual Behavior, and Post-Purchase Behavior

toward protection and education of consumer’sinterests are also important for the develop-ment of consumer awareness and cannot beignored.

The empirical research of the study dis-covered that the subjective norm has greater

influence on actual behavior than post-purchasebehavior. It indicated that consumers are influ-enced by opinion of other people or organiza-tions, especially the close/remote relationshipwith their family members and the financialsupport of their families, when they make

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

36 JOURNAL OF INTERNATIONAL CONSUMER MARKETING

purchase decisions. Consequently, consumerswho are not the key person in the decisionof investment strategies or have no adequatefinancial resources or supports may have lowerwillingness to buy. Since many uncertain exter-nal factors (e.g., changes to industrial structureand financial status of consumers) are involvedin the post-purchase behavior of consumers, theinfluence of the subjective norm on actual andpost-purchase behavior is different.

According to the results derived from thisstudy, the following specific suggestions formanagement are provided for reference. First,the banking industry should plan an attractivemarketing mix strategy especially for customersand their close relationship with family mem-bers. Second, the banking industry should lowerthe risk of uncertainty when consumers purchasethe on-line financial products. If the bankingindustry are willing to lower these risks, theyshould not only enhance constructions of se-curity system for transactions but also improvediverse secured transaction terms, such as en-cryption, for increasing the security modulus,which will be trusted by consumers. If thecontact window can be well set, we believe thaton-line transaction will be one of the best waysbased on the advantages that the Internet prevailsover traditional channels. Third, the banking in-dustries should frame measures with increases ofcustomer’s consumption value and enhancementof the relationship marketing strategy to build along-term business relationship with customersinstead of a price war, sacrifice of service quality,a business goal with short-term benefits. Thiswill have permanently good relationship withcustomers.

However, the product involvement does notsignificantly influence the actual behavior. Thereason for the insignificant influence is perhapsthat, in addition to the kern benefit of theproduct, the deferred value or value relevanceof the product or the percentage of expenditureto the total budget is important to consumers.Consumers usually take careful considerationbefore taking actions if the product, especiallyfinancial investment products, has high deferredvalue or expenditure.

The theoretical structure of the study is basedon the Decomposition Theory of Planned Behav-

ior combining the concept of product involve-ment and relationship quality and conformedto the three factors—personal factor, physicalfactor and situational factor—related to productinvolvement of consumers (Zaichkowsky, 1985).The result of the Study provides the followingmanagement implications for enterprises: (1) Inaddition to reinforcing the factors related to con-sumer’s personal requirements, providers of en-duringly involved financial investment productsshould develop market segmentation strategiesfor different products to expand their market do-main by meticulous deployment; (2) Providersshould reinforce the professional training of theirstaff to win the trust of consumers, improve thedeferred effect of consumers on the staff andreduce their motivation to comply, shorten thetime for decisions, and eliminate uncertainty; (3)Providers should improve their service qualityand develop a total solution to improve theperceived value of consumers to reduce post-purchase actions and improve customer loyaltyand satisfaction;(4)We can further test the re-search model, and there are may be differenceamong samples from different areas.

Since the study discusses the actual purchaseand post-purchase behavior of consumers onlybased on part of theories in this field, the argu-mentation may not be complete enough to forma comprehensive result. It is therefore suggestedthat researchers dealing with this topic mayput forward a more comprehensive model forbetter management solutions and implications.Comparative researches on other industries ormultinational surveys are also suggested to findstrategies on a global basis.

REFERENCES

Ajzen, I. 1985. From intentions to action: A theory ofplanned behavior, action-control: From congition tobehavior, Heidelberg: Springer.

Ajzen, I. 1989. Attitude, personality, and behavior, MiltonKeynes: Open University Press.

Ajzen, I. 1991. The theory of planned behavior. Organi-zational Behavior and Human Decision Processes, 50:179–211.

Ajzen, I. And B.L. Driver. 1992.Application of Simultane-ous Factor Analysis to Issues of Factorial Invariance,in Factor Analysis and Measurement in Sociologi-cal Research: A Multidimensional Perspective, D.D.

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

Wen-Bao Lin 37

Jackson and E.P. Borgatta (eds), CA: Sage Beverly Hill,249–280.

Ajzen, I. And M. Fishbein. 1980. Understanding Attitudesand Predicting Social Behavior, Engelwood Cliffs, NJ:Prentice-Hall.

Bagozzi, R.P. and Yi, Y. 1988. On the evaluation of structureequations models. Academic of Marketing Science, 16:76–94.

Batra, R. and M. Ray. 1985. Affective response medi-ating acception of advertising. Journal of ConsumerResearch, 3: 234–249.

Beatty, S.E. and S.M. Smith. 1987. External search effort:An investigation across several product categories.Journal of Consumer Research, 14: 83–95.

Berry, L.L. and A. Parasuraman. 1991. Marketing Service:Competing Through Quality, New York: Free Press.

Bhattacherjee, A. 2000. Acceptance of Internet Applica-tions Service: the Case of Electronic Brokerages. IEEETransactions on Systems, Man, and Cybernetics-Part A:Systems and Humans, 30(4): 441–420.

Bloch, M. and A. Segev. 1997. The impact of electroniccommerce on the travel industry. Proceedings, Hawaii:HICSS 31.

Boulding, W., A. Kalra, R., Staelin, V.A. Zeithaml.1993. A Dynamic Process Model of Service Quality:from Expectations to Behavioral Intentions. Journal ofMarketing Research, 30(1): 7–27.

Boze, B.V. 1987. Selection of legal service: An investiga-tion of perceived risk. Journal of Professional ServiceMarketing, 3(2): 287–297.

Brooker, G. 1984. An Assessment of an expended measureof perceived risk in Thomas, C. and U. Kinnear,(Ed.), Advances in Consumer Research, Advances inConsumer Research, II, 439–491.

Davis, F.D., R.P., Bagozzi, and P.R. Warshaw. 1989. UserAcceptance of Computer Technology: A Comparison ofTwo Theoretical Models: Management Science, 35(8):982–1003.

Ducoffe, R.H. 1996. Advertising Value and Advertisingon the Web. Journal of Advertising Research, Septem-ber/October, 21–35.

Eighmey, J. 1997. Profiling User Responses to CommercialWeb Sites, Journal of Advertising Research, 37(3):59–66.

Engel, J. F. R. D. Blackwell and P.W. Miniard. 1995.Consumer Behavior, 8th ed., Chicago: Dryden Press.

Evans, J.R. and B Berman, 1994. Marketing, 6th ed.,MacMillan, Pub. Co.

Flynn, L.R, and R, E, Goldsmith. 1993. Applicationof the personal involvement inventory in marketing.Psychology & Marketing, 10(4): 357–366.

Gronroos, C. 1983. Strategic Management and Marketingin the Service Sector. Boston: Marketing ScienceInstruct, (May 63).

Guseman, D. 1981. Risk Perception and Risk Reductionin Consumer Service”, in Donnelly, J. and W. George,

(Eds.), Marketing of Service, American MarketingAssociation, 200–224.

Henderson, R. D. Rickwood and P. Roberts. 1998. TheBeta Test of an Electronic Supermarket. Interacting withComputers, 10: 385–399.

Hou, J.S. and C.I. Lin. 1997. “The National Park TourismIntention of College Students: A Theory of FishbeinBehavioral Intention Model, ” in Leisure Behavior, TheOutdoor Recreation Association of R.O.C. (eds), Taipei:Garden City, 19–34 (In Chinese).

Kaphan, L.B. and Jacoby, J. 1972. “The Components ofPerceived Risk”, In Proceedings, Third Annual Confer-ence (Ed.), M. Venkatesan, Urbans, IL: Association forConsumer Research.

Keeney, R.L.1999. The Value of Internet Commerce to theCustomer. Management Science, 45(4): 533–542.

Lai, H. and T., Yang. 1998. A system architecture ofintelligent-guided browsing on the Web. Hawaii Inter-national Conference on System Sciences.

Lai, H.C. 2000. Intermarketing in Electronic CommerceTheory and Practice, T.P. Liang, (eds), Taipei: Hwtai,273–323 (in Chinese).

Leblance, G. 1992. Factor Affecting Customer Evaluationof Service Quality in Travel Agencies: An Investigationof Customer Perceptions. Journal of Travel Research,30: 10–16.

Liao, S., Y.P. Shao, H. Wang and A. Chen. 1999.The adoption of virtual banking: An empirical study,International Journal of Information Management, 19:63–74.

Lovelock, C.H. 1981.“Why Marketing Management Needsto Different for Service,” Marketing of Service, J.Donnelly, and W. George (rds.), Chicago: AmericanMarketing Association, 5–9.

Marsha, R.L. and P.H. Bloch. 1986. After the new wears off:The temporal context of product involvement. Journalof Consumer Research, 13: 280–285.

Mathieson, K. 1991. Predicting User Intentions: Compar-ing the Technology Acceptance Model with the Theoryof Planned Behavior. Information Systems Research,2(3): 173–191.

Mittal, Bonwari. 1989. Measuring purchase-decisioninvolvement. Psychology & Marketing, 6(2): 147–163.

Moon, J.W. and Y.G. Kim. 2001. Extending the ATM fora World-Wide-Web Context. Information and Manage-ment, 38: 217–230.

Pallister, J.G. and G.R. Gorden.1998. Measuring purchasedecision involvement for financial service: Comparsionof the Zaichkowsky and Mittal Scales. The Inter-national Journal of Bank Marketing, 16(5): 180–193.

Parasuraman, A., V.A. Zeithmal, and L.L. Berry. 1985.A conceptual model of service quality and its impli-cation for future research. Journal of Marketing, 49:41–45.

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014

38 JOURNAL OF INTERNATIONAL CONSUMER MARKETING

Parasuraman, A., V.A. Zeithmal, and L.L. Berry. 1988.SERVQVAL: A multiple-item scale for measuringconsumer perceptions. Journal of Retailing, 64: 12–40.

Parasurman, A., V.A. Zeichaml, and L.L. Berry. 1996. TheBehavioral Consequences of Service Quality. Journalof Marketing, April: 31–46.

Rogers, E.M. 1983. Diffusion of Innovations, 3th ed.,New York: The Free Press.

Roselius, T. 1971. Consumer rankings of risk reductionmethods, Journal of Marketing, 35: 56–61.

Schiffman, L.G. and L.L. Kaunk 1987. A markets seg-ments. Marketing, 59–62.

Swaminathan, V., Lepkowska-White Elzbieta, and P.R.Bharat. 1999. Browsers or Buyers in Cyberspace?Journal of Computer-Mediated Communication, 5(2):56–68.

Tan, S.J. 1999. Strategies for reducing consumers’ riskaversion in internet shopping. Journal of ConsumerMarketing, 16(2): 163–180.

Taylor, S. and P.A. Todd. 1995a. Understanding informa-tion technology usage: A test of competing models.Information System Research, 6(2): 144–176.

Taylor, S. and P.A. Todd. 1995b. Decomposition andCrossover Effects in the Theory of Planned Behavior:A Study of Consumer Adoption Intentions. Interna-tional Journal of Research in Marketing, 12: 137–155.

Teo, T.S.H., K.G. Vivien, and R.Y.C. Lai. 1999. Intrinsicand extrinsic motivation in internet usage. Omega,27(1): 25.

Zaichkowsky, J.L. 1985. Measuring the involvementconstruct. Journal of Commer Research, 12: 341–352.

SUBMITTED: September 2005FIRST REVISION: March 2006

SECOND REVISION: March 2007ACCEPTED: June 2007

Dow

nloa

ded

by [

Geo

rge

Mas

on U

nive

rsity

] at

10:

17 0

6 Ju

ly 2

014