Embed Size (px)

Citation preview

EARLY RELEASE FOR THE UPCOMING FDIC QUARTERLY 1

THE IMPORTANCE OF COMMUNITY BANKS IN PAYCHECK PROTECTION PROGRAM LENDING

Community banks play an important role providing financial services to local customers and small businesses.1 Despite their relatively small size and share of banking industry assets, community banks have consistently demonstrated an ability to serve their customers. Even before the COVID-19 pandemic, community banks held an outsized share of small business loans.2 At year-end 2019, community banks held about 25 percent of small business loans, well above their share of 15 percent of total banking industry loans. Community bank participation in the U.S. Small Business Administration’s Paycheck Protection Program (PPP) was also proportionately larger than their size in the banking industry. Other published analyses have discussed PPP activity in aggregate and by institution size. This article focuses on contributions of community banks to the PPP and explores how factors such as community bank location, specialty, and size affected participation.

What Is the Paycheck Protection Program?The Paycheck Protection Program (PPP) was created through Section 1102 of the Coronavirus Aid, Relief, and Emergency Services Act (CARES Act). This program—which is administered by the U.S. Small Business Administration (SBA) with support from the U.S. Department of the Treasury—made $659 billion available to small businesses in potentially forgivable loans to pay up to 24 weeks of eligible employee salaries, payroll costs, and benefits as well as other qualified expenses, such as mortgage interest, rent, and utilities. The bank forgives 100 percent of the loan if 60 percent of the funds were used for those purposes. The SBA guarantees the loans and pays banks for the forgiven loans and accrued interest as prescribed in Section 1106 of the CARES Act. Applications for PPP loans were accepted from April 3, 2020, through August 8, 2020, and more than $525 billion in loans were originated. The loans had a $10 million limit, a 1 percent interest rate, and a term of two years, or a term of up to five years for loans made on June 5, 2020, and after. Lenders received an origination fee of 1 to 5 percent, depending upon the size of the loan. The SBA began accepting applications for loan forgiveness on August 10, 2020.

Community Banks Were Active Participants in the PPP

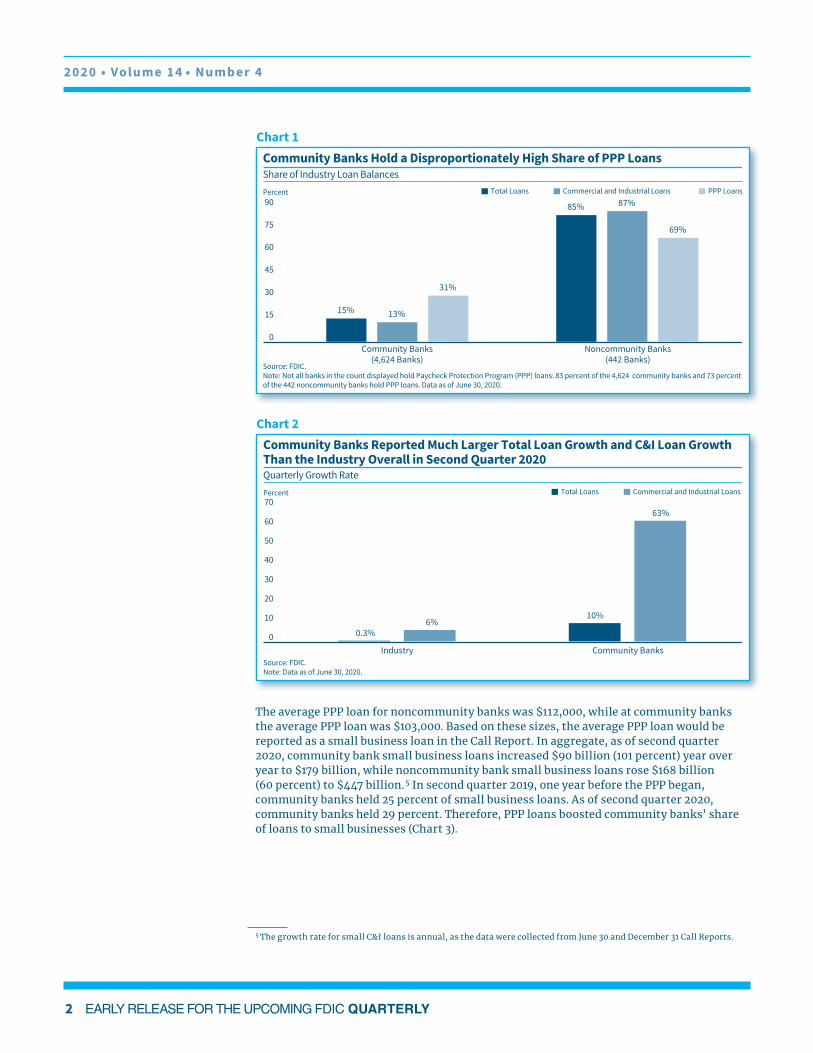

Banks hold the vast majority of the $525 billion in PPP loans made by banks and nonbanks. Community banks’ participation in the PPP outpaced noncommunity banks. As of June 30, 2020, banks held $482 billion, or 92 percent of total PPP loans. Community banks held $148 billion—28 percent of total PPP loans and 31 percent of PPP loans held by banks.3 This share is significant, as community banks held 12 percent of total industry assets and 15 percent of total industry loans as of June 30, 2020 (Chart 1).

PPP loan origination contributed to total quarterly loan growth at community banks, which outpaced quarterly loan growth in the banking industry in second quarter 2020. Industry loan growth between first and second quarter 2020 was $34 billion, or 0.3 percent (Chart 2). The banking industry’s commercial and industrial (C&I) loans, where most PPP loans were categorized, grew 6 percent quarter over quarter.4 Community banks, however, reported a quarterly loan growth rate of 10 percent in second quarter 2020 and a quarterly C&I loan growth rate of 63 percent in second quarter 2020.

1 In this article, the term community banks refers to those institutions that meet the definition created in the FDIC 2012 Community Bank Study (https://www.fdic.gov/regulations/resources/cbi/study.html). 2 In this article, small business loans are commercial and industrial (C&I) loans with original amounts of $1 million or less.3 Banks began reporting participation in the PPP starting with second quarter 2020 Consolidated Reports of Condition and Income (Call Reports). The instructions for the line item for the outstanding balance of PPP loans state “held for investment and held for sale” rather than “originated.” This line item does not report the amount of loans originated, but PPP loans reported by banks are assumed to have originated or been purchased by those banks.4 PPP loans are presumed to be predominantly C&I loans because of the lack of collateral and the loan purposes prescribed by the program.

2020 • Volume 14 • Number 4

2 EARLY RELEASE FOR THE UPCOMING FDIC QUARTERLY

0

15

30

45

60

75

90

Community Banks(4,624 Banks)

Noncommunity Banks(442 Banks)

Community Banks Hold a Disproportionately High Share of PPP LoansShare of Industry Loan Balances

Source: FDIC.Note: Not all banks in the count displayed hold Paycheck Protection Program (PPP) loans: 83 percent of the 4,624 community banks and 73 percent of the 442 noncommunity banks hold PPP loans. Data as of June 30, 2020.

Percent

15%

85%

13%

87%

31%

69%

Total Loans Commercial and Industrial Loans PPP Loans

Chart 1

Community Banks Reported Much Larger Total Loan Growth and C&I Loan Growth Than the Industry Overall in Second Quarter 2020 Quarterly Growth Rate

Source: FDIC.Note: Data as of June 30, 2020.

Percent Total Loans Commercial and Industrial Loans

10%6%

63%

0.3%0

10

20

30

40

50

60

70

Industry Community Banks

Chart 2

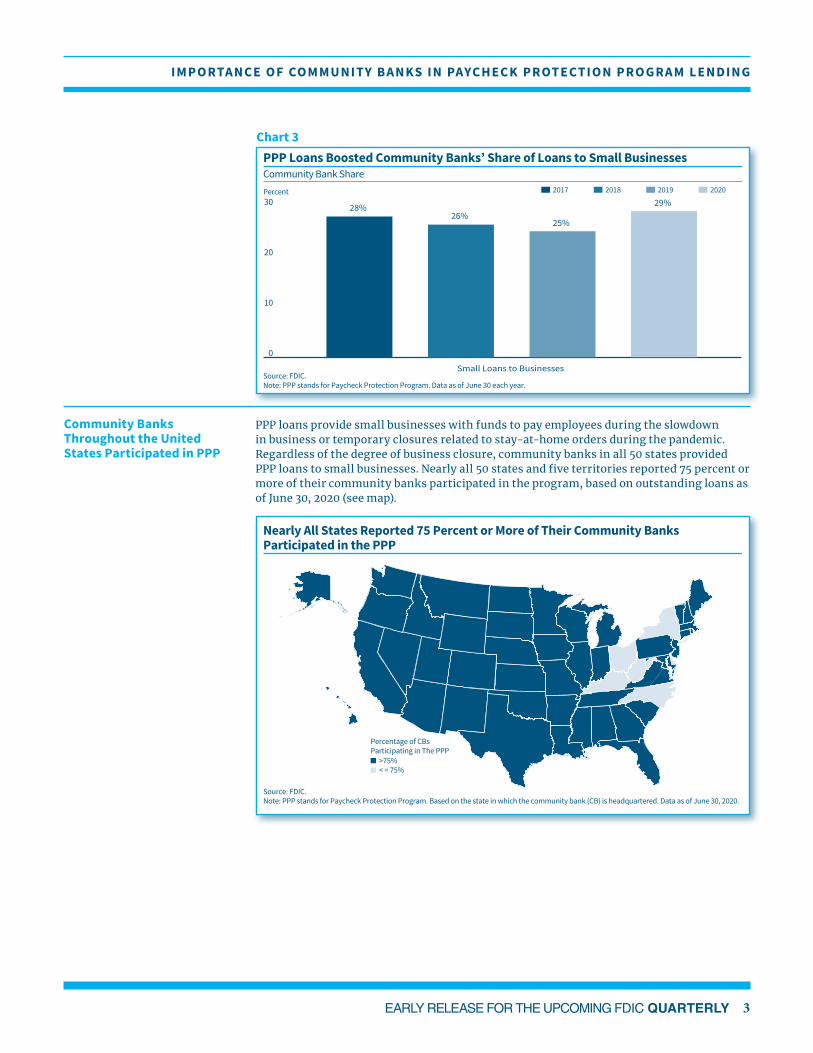

The average PPP loan for noncommunity banks was $112,000, while at community banks the average PPP loan was $103,000. Based on these sizes, the average PPP loan would be reported as a small business loan in the Call Report. In aggregate, as of second quarter 2020, community bank small business loans increased $90 billion (101 percent) year over year to $179 billion, while noncommunity bank small business loans rose $168 billion (60 percent) to $447 billion. 5 In second quarter 2019, one year before the PPP began, community banks held 25 percent of small business loans. As of second quarter 2020, community banks held 29 percent. Therefore, PPP loans boosted community banks’ share of loans to small businesses (Chart 3).

5 The growth rate for small C&I loans is annual, as the data were collected from June 30 and December 31 Call Reports.

EARLY RELEASE FOR THE UPCOMING FDIC QUARTERLY 3

IMPORTANCE OF COMMUNITY BANKS IN PAYCHECK PROTECTION PROGRAM LENDING

PPP Loans Boosted Community Banks’ Share of Loans to Small Businesses Community Bank Share

Source: FDIC.Note: PPP stands for Paycheck Protection Program. Data as of June 30 each year.

Percent

28%26%

25%

29%

0

10

20

30

Small Loans to Businesses

2017 2018 2019 2020

Chart 3

Community Banks Throughout the United States Participated in PPP

PPP loans provide small businesses with funds to pay employees during the slowdown in business or temporary closures related to stay-at-home orders during the pandemic. Regardless of the degree of business closure, community banks in all 50 states provided PPP loans to small businesses. Nearly all 50 states and five territories reported 75 percent or more of their community banks participated in the program, based on outstanding loans as of June 30, 2020 (see map).

Nearly All States Reported 75 Percent or More of Their Community Banks Participated in the PPP

Source: FDIC.Note: PPP stands for Paycheck Protection Program. Based on the state in which the community bank (CB) is headquartered. Data as of June 30, 2020.

Percentage of CBsParticipating in The PPP

>75%< = 75%

2020 • Volume 14 • Number 4

4 EARLY RELEASE FOR THE UPCOMING FDIC QUARTERLY

Community banks in metropolitan, micropolitan, and rural areas hold PPP loans.6 The share of PPP loans held by community banks in micropolitan areas (63 percent) and rural areas (84 percent) closely matches their share of total loans and C&I loans in those areas. Community banks in metropolitan areas, however, hold a higher share of PPP loans than other loans. Community banks hold 26 percent of total PPP loans in metropolitan areas, well above their 10 percent share of total C&I loans in metropolitan areas (Chart 4). Community banks in metropolitan areas held the vast majority ($110 billion or 74 percent) of PPP loans in community banks nationally, and 85 percent of community banks in metropolitan areas participated in the PPP loan program.

0

15

30

45

60

75

90

Metropolitan Community Banks Hold a Greater Share of PPP Loans Than Their Share of Other Loans Community Bank Share

Source: FDIC.Note: PPP stands for Paycheck Protection Program. Numerator is community bank loan balances in area; denominator is all bank loan balances in area. Figures are based on where the bank is headquartered. Data as of June 30, 2020.

Percent Total Loans Commercial and Industrial Loans PPP Loans

12%

63%

86%

10%

63%

84%

26%

63%

84%

Metro Micro Rural

Chart 4

Commercial Lending Specialists Hold the Most PPP Loans

Among all bank lending specialty categories, commercial lenders dominated community bank PPP lending.7 Commercial specialty community banks and agriculture specialty community banks hold a total of $143 billion in PPP loans, or 96 percent of all community bank PPP loans. Most banks (61 percent) that held PPP loans as of second quarter 2020 are commercial specialty banks.8 Commercial specialty noncommunity banks hold 52 percent ($1.4 trillion) of industry C&I loans and 77 percent ($373 billion) of industry PPP loans. Commercial specialty community banks hold 22 percent ($306 billion) of the specialty’s C&I loans, yet hold 36 percent ($133 billion) of the specialty’s PPP loans (Chart 5). The next-largest specialty group holding PPP loans—by the number of banks—is the agriculture specialty group, with 24 percent of banks. Agriculture specialty banks hold 2 percent ($11 billion) of industry PPP loans and hold 1 percent of industry C&I loans.9 Almost all agriculture specialty banks (99 percent) are community banks. Agriculture

6 As defined by the U.S. Census Bureau, metropolitan areas consist of metropolitan statistical areas or counties with more than 50,000 persons; micropolitan areas consist of micropolitan statistical areas or counties with less than 50,000 but more than 10,000 persons. Rural areas are all counties that do not meet either definition. 7 Bank specialties include international, agriculture, credit card, commercial, mortgage, consumer, other less than $1 billion, all other less than $1 billion, and all other greater than $1 billion. Specialties are hierarchical, mutually exclusive, and based on percentage of assets. The percentage varies among specialty definitions. For example, credit card banks have 50 percent of assets in credit card loans, while agriculture banks have agriculture loans equal to or greater than 25 percent of loans. Specialty groups are detailed in the FDIC Quarterly Banking Profile.8 Commercial specialists are banks that are not international, agriculture, or credit card specialists, and whose commercial and industrial loans, real estate construction and development loans, and loans secured by commercial real estate exceed 25 percent of total assets.9 Since many farms are small businesses, some PPP loans were made for agricultural production purposes, although the exact dollar amount is not shown in Call Reports.

EARLY RELEASE FOR THE UPCOMING FDIC QUARTERLY 5

IMPORTANCE OF COMMUNITY BANKS IN PAYCHECK PROTECTION PROGRAM LENDING

specialty community banks hold 94 percent ($28 billion) of the specialty’s C&I loans and 93 percent ($10 billion) of the specialty’s PPP loans. While community banks in other specialty groups also hold PPP loans and made a disproportionate share of PPP loans given their specialty’s share of industry loan balances, their aggregate total was just $5.5 billion, or 4 percent of the $148 billion total for all community banks.

Community Banks Specializing in Commercial Lending Made the Majority of Community Bank PPP Loans

Source: FDIC.Note: Community banks only. Not all banks in the count of banks hold Paycheck Protection Program (PPP) loans. Other includes mortgage, consumer, and other specialty banks. Data as of June 30, 2020.

200,071

80,238

1,158,082

$132,939

$9,928 $5,4810

300,000

600,000

900,000

1,200,000

1,500,000

Commercial(2,497 Banks)

Agriculture(1,191 Banks)

Other(936 Banks)

0

30,000

60,000

90,000

120,000

150,000

Number of Loans

Dollars of Loans

Number of PPP LoansDollars of PPP Loans (Millions)

Chart 5

Community Banks of All Sizes Participated in the PPP

Community banks, regardless of asset size, participated in the PPP. Not surprisingly, smaller community banks made smaller loans, while larger community banks made larger loans. Average PPP loan sizes ranged from $50,000 to $129,000 (Chart 6). Each size group participated in the PPP at approximately the same rate as their share of total community bank C&I loans. For example, community banks with less than $100 million in assets made 1.1 percent of the dollar volume of the community bank PPP loans. These banks hold approximately 1.5 percent of the total dollar volume of community bank C&I loans. At the other end of the spectrum, community banks with total assets greater than $1 billion hold 59 percent of the total dollar volume of community bank C&I loans and hold 57 percent of the dollar volume of community bank PPP loans.

On Average, the Smallest Community Banks Hold the Smallest PPP LoansAverage PPP Loan Size by Community Bank Asset Size

Source: FDIC.Note: Community banks only. Not all banks in the count of banks hold Paycheck Protection Program (PPP) loans. Data as of June 30, 2020.

$ Thousands

0

25

50

75

100

125

150

Less Than$100 Million(982 Banks)

$100 to $250 Million(1,377 Banks)

$250 to$500 Million

(1,032 Banks)

$500 Million to$1 Billion

(676 Banks)

Greater Than$1 Billion

(557 Banks)

Average PPP Loan Size Among Community Banks: $103,000

Chart 6

2020 • Volume 14 • Number 4

6 EARLY RELEASE FOR THE UPCOMING FDIC QUARTERLY

Summary While community banks hold a smaller share of industry-wide loans by dollar volume and number than noncommunity banks, their participation in the PPP has been larger than their share of both total loans and C&I loans. Community banks in all states participated in the PPP program, and most states had at least three quarters of community banks holding PPP loans as of June 30, 2020. Community banks headquartered in metropolitan areas drove the participation rates, reporting greater shares of PPP loans than their share of total loans or C&I loans. Commercial and agriculture specialty lenders were the most common participants in the PPP lending program, consistent with the most common borrowers in the program and the number of banks identified in these specialty bank groups. Community banks of all sizes participated in the PPP and each size group participated at approximately the same rate as their share of total community bank C&I loans. The PPP program filled a need for credit at a critical time in our nation’s financial history, and community banks’ participation in this lending was instrumental.

Authors: Margaret Hanrahan Chief, Financial Analysis Section Division of Insurance and Research

Angela Hinton Senior Financial Analyst Division of Insurance and Research