Embed Size (px)

Citation preview

FEMA - Miscellaneous remittances, foreign

currency accounts and retention of

currencies

CA Rajesh H. Gandhi

19 April 2014

The Chamber of Tax Consultants

Agenda

2

• Overview Of Current And Capital Account Transactions

• Capital Account Regulations

• Current Account Transaction Rules

• Use of ICC/IDC

• Miscellaneous Remittances from India

• Surrender and retention of foreign exchange

• Liberalized Remittance Scheme (LRS)

• Foreign currency bank account by a resident

• Remittance facilities for Non NRIs / PIO / Foreign Nationals

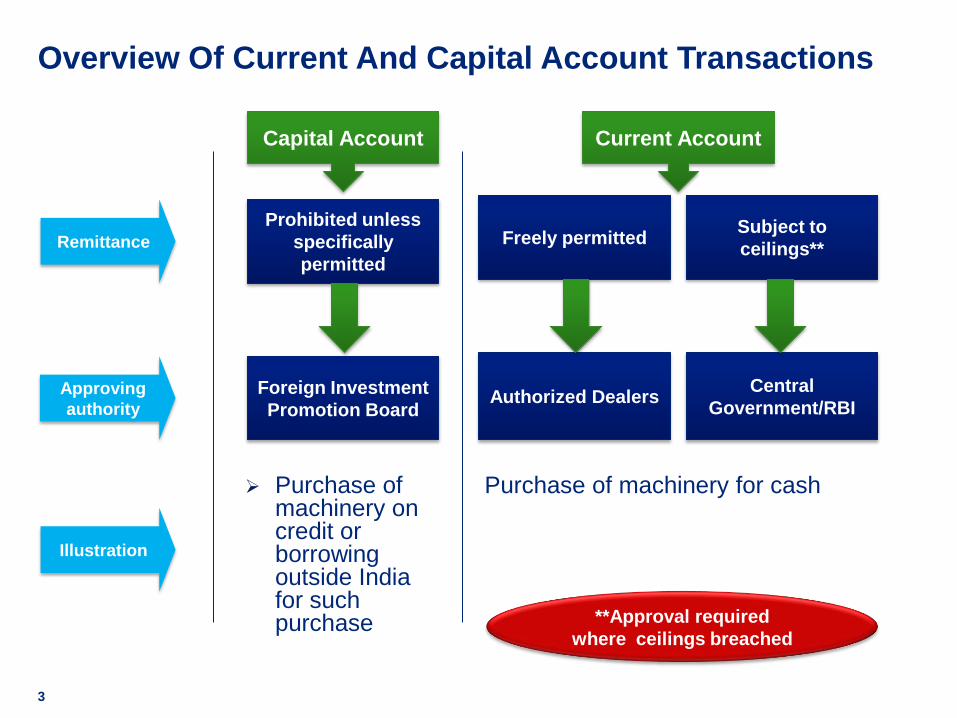

Overview Of Current And Capital Account Transactions

3

Remittance

Approving

authority

Illustration

Capital Account Current Account

Prohibited unless

specifically

permitted

Foreign Investment

Promotion Board Authorized Dealers

Subject to

ceilings** Freely permitted

Central

Government/RBI

Purchase of machinery on credit or borrowing outside India for such purchase

Purchase of machinery for cash

**Approval required

where ceilings breached

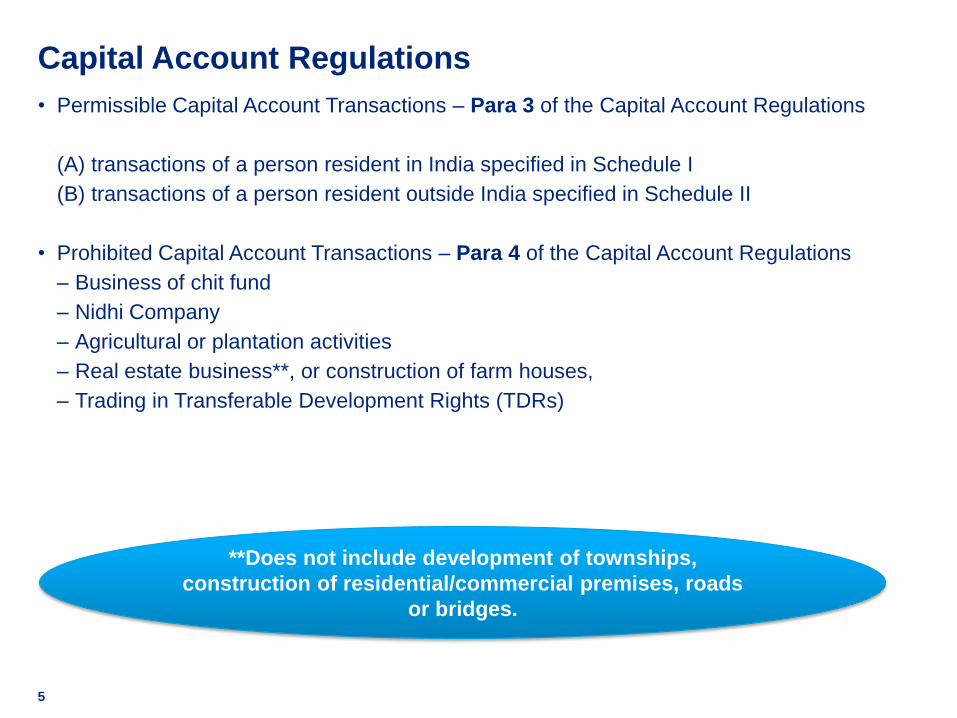

Capital Account Regulations

4

Capital Account Regulations

5

• Permissible Capital Account Transactions – Para 3 of the Capital Account Regulations

(A) transactions of a person resident in India specified in Schedule I

(B) transactions of a person resident outside India specified in Schedule II

• Prohibited Capital Account Transactions – Para 4 of the Capital Account Regulations

‒ Business of chit fund

‒ Nidhi Company

‒ Agricultural or plantation activities

‒ Real estate business**, or construction of farm houses,

‒ Trading in Transferable Development Rights (TDRs)

**Does not include development of townships,

construction of residential/commercial premises, roads

or bridges.

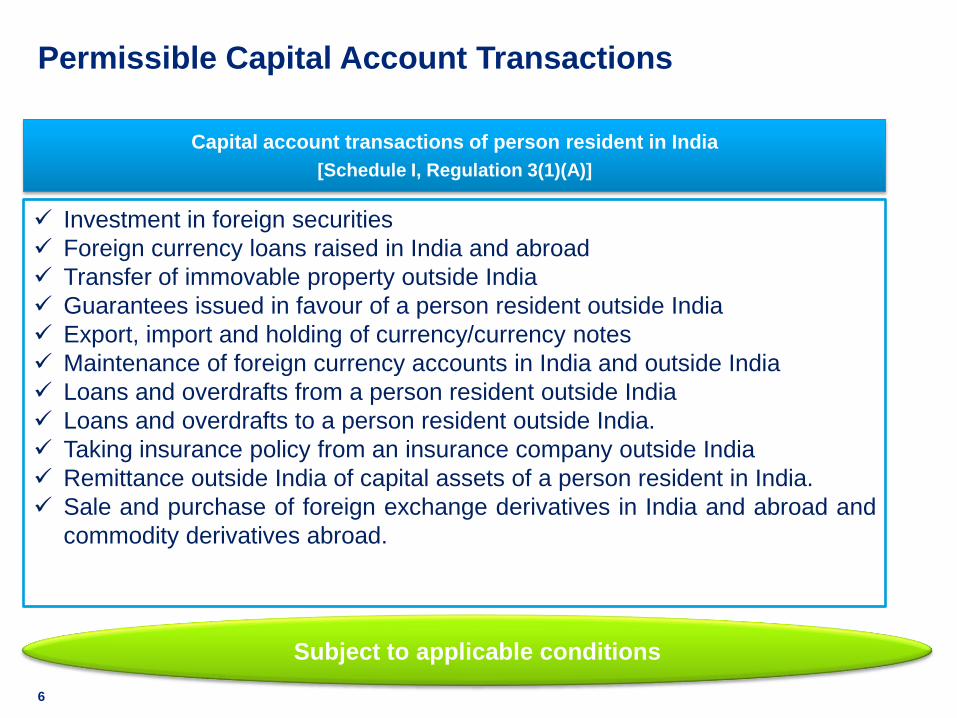

Permissible Capital Account Transactions

6

Capital account transactions of person resident in India

[Schedule I, Regulation 3(1)(A)]

Investment in foreign securities

Foreign currency loans raised in India and abroad

Transfer of immovable property outside India

Guarantees issued in favour of a person resident outside India

Export, import and holding of currency/currency notes

Maintenance of foreign currency accounts in India and outside India

Loans and overdrafts from a person resident outside India

Loans and overdrafts to a person resident outside India.

Taking insurance policy from an insurance company outside India

Remittance outside India of capital assets of a person resident in India.

Sale and purchase of foreign exchange derivatives in India and abroad and

commodity derivatives abroad.

Subject to applicable conditions

Current Account Transactions

Rules

7

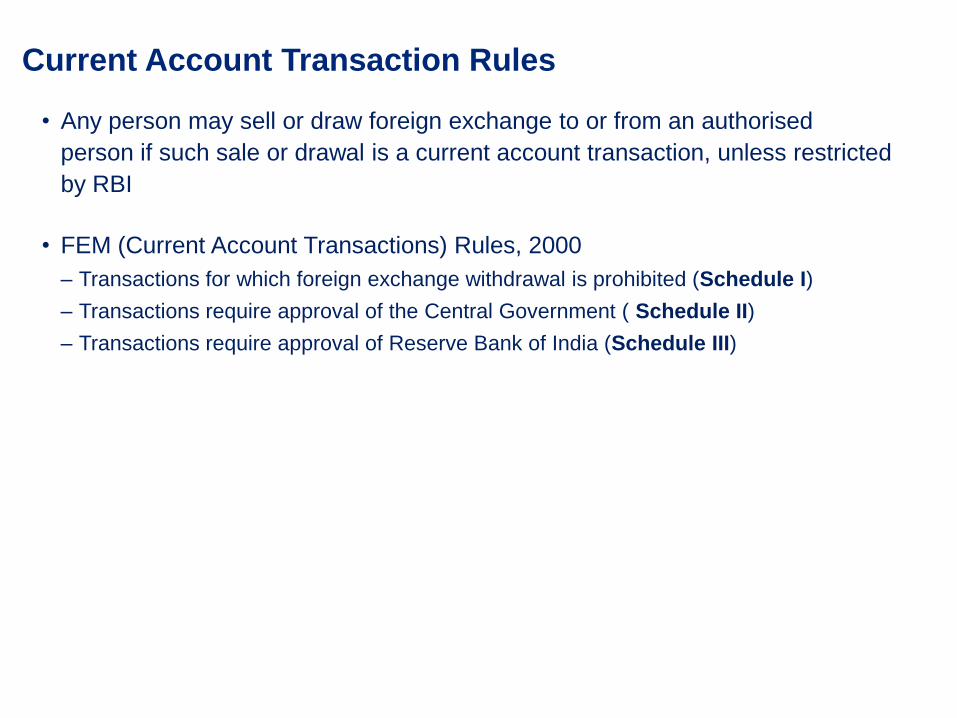

• Any person may sell or draw foreign exchange to or from an authorised

person if such sale or drawal is a current account transaction, unless restricted

by RBI

• FEM (Current Account Transactions) Rules, 2000

‒ Transactions for which foreign exchange withdrawal is prohibited (Schedule I)

‒ Transactions require approval of the Central Government ( Schedule II)

‒ Transactions require approval of Reserve Bank of India (Schedule III)

Current Account Transaction Rules

9

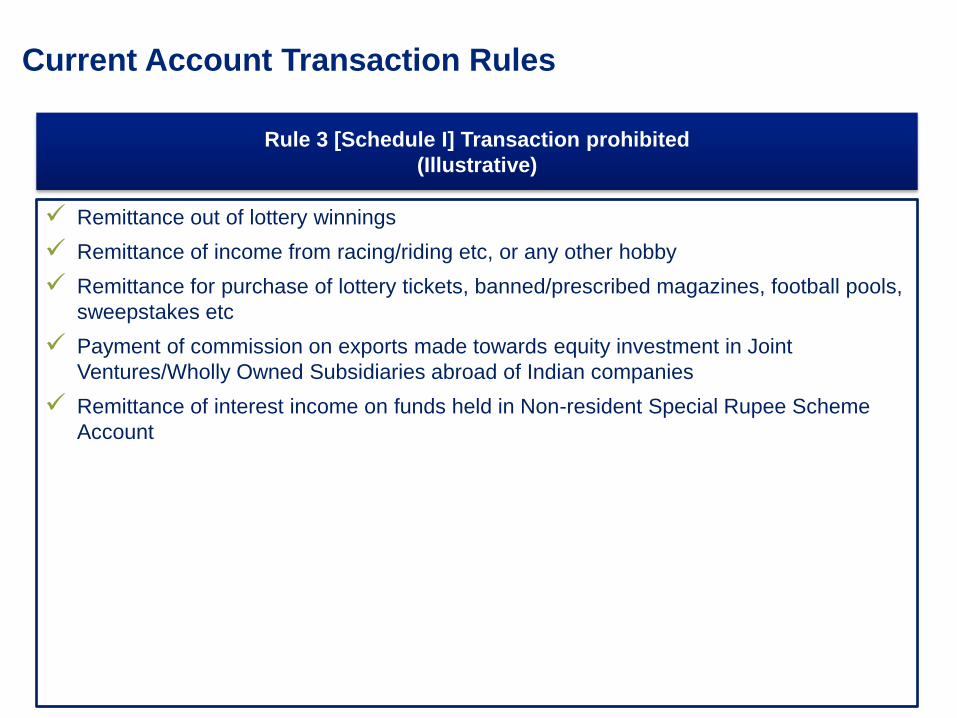

Rule 3 [Schedule I] Transaction prohibited

(Illustrative)

Remittance out of lottery winnings

Remittance of income from racing/riding etc, or any other hobby

Remittance for purchase of lottery tickets, banned/prescribed magazines, football pools,

sweepstakes etc

Payment of commission on exports made towards equity investment in Joint

Ventures/Wholly Owned Subsidiaries abroad of Indian companies

Remittance of interest income on funds held in Non-resident Special Rupee Scheme

Account

Current Account Transaction Rules

Current Account Transaction Rules

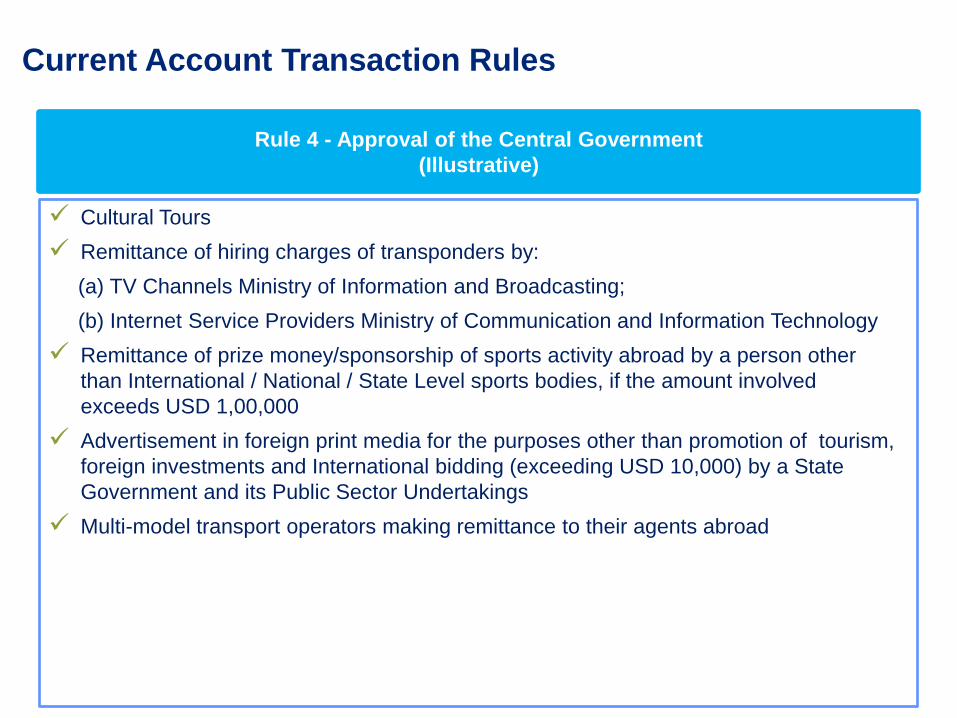

Rule 4 - Approval of the Central Government

(Illustrative)

Cultural Tours

Remittance of hiring charges of transponders by:

(a) TV Channels Ministry of Information and Broadcasting;

(b) Internet Service Providers Ministry of Communication and Information Technology

Remittance of prize money/sponsorship of sports activity abroad by a person other

than International / National / State Level sports bodies, if the amount involved

exceeds USD 1,00,000

Advertisement in foreign print media for the purposes other than promotion of tourism,

foreign investments and International bidding (exceeding USD 10,000) by a State

Government and its Public Sector Undertakings

Multi-model transport operators making remittance to their agents abroad

Current Account Transaction Rules

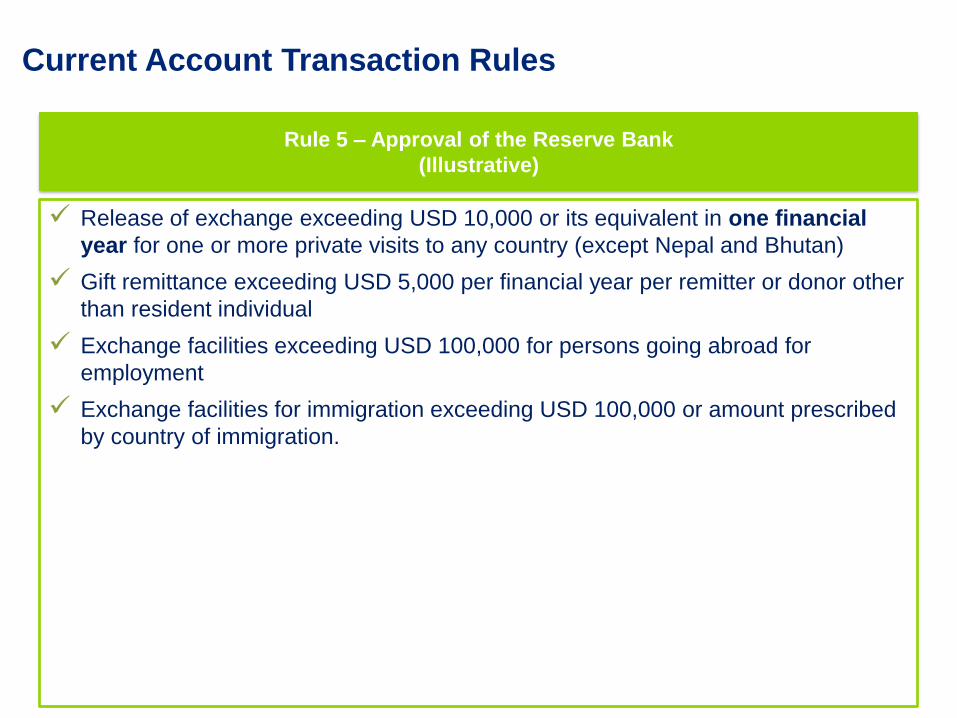

Rule 5 – Approval of the Reserve Bank

(Illustrative)

Release of exchange exceeding USD 10,000 or its equivalent in one financial

year for one or more private visits to any country (except Nepal and Bhutan)

Gift remittance exceeding USD 5,000 per financial year per remitter or donor other

than resident individual

Exchange facilities exceeding USD 100,000 for persons going abroad for

employment

Exchange facilities for immigration exceeding USD 100,000 or amount prescribed

by country of immigration.

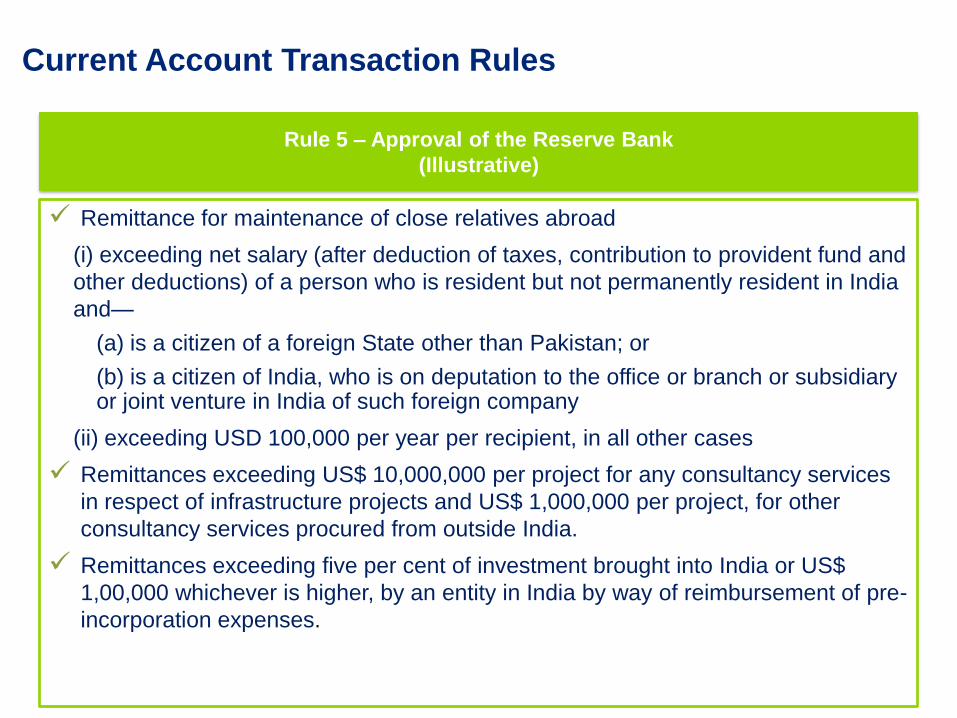

Current Account Transaction Rules

Rule 5 – Approval of the Reserve Bank

(Illustrative)

Remittance for maintenance of close relatives abroad

(i) exceeding net salary (after deduction of taxes, contribution to provident fund and

other deductions) of a person who is resident but not permanently resident in India

and—

(a) is a citizen of a foreign State other than Pakistan; or

(b) is a citizen of India, who is on deputation to the office or branch or subsidiary or joint venture in India of such foreign company

(ii) exceeding USD 100,000 per year per recipient, in all other cases

Remittances exceeding US$ 10,000,000 per project for any consultancy services

in respect of infrastructure projects and US$ 1,000,000 per project, for other

consultancy services procured from outside India.

Remittances exceeding five per cent of investment brought into India or US$

1,00,000 whichever is higher, by an entity in India by way of reimbursement of pre-

incorporation expenses.

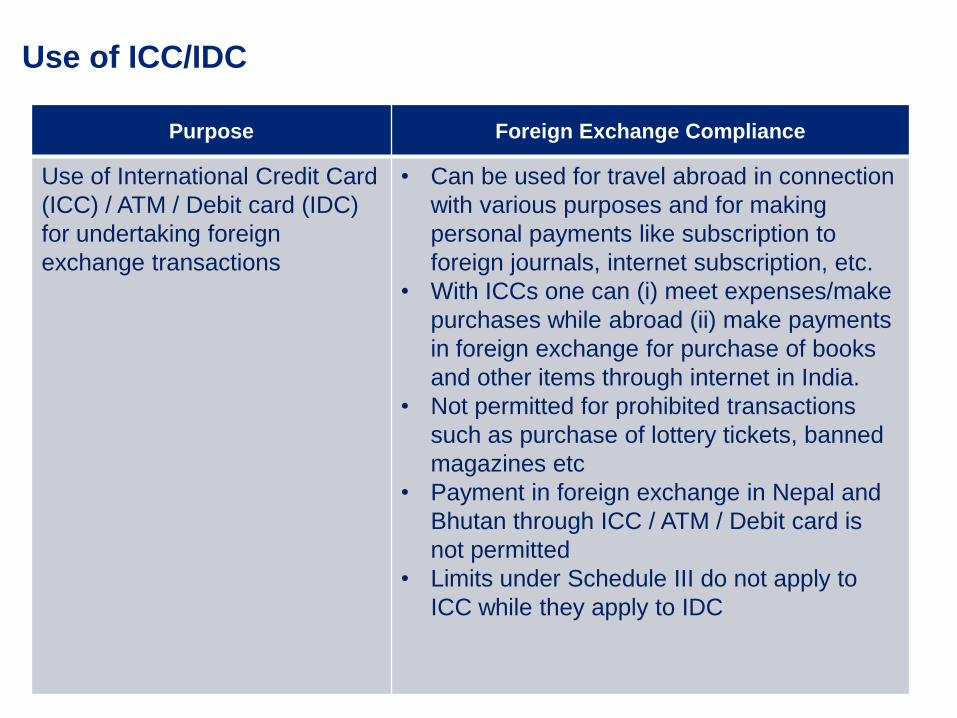

Use of ICC/IDC

13

Purpose Foreign Exchange Compliance

Use of International Credit Card

(ICC) / ATM / Debit card (IDC)

for undertaking foreign

exchange transactions

• Can be used for travel abroad in connection

with various purposes and for making

personal payments like subscription to

foreign journals, internet subscription, etc.

• With ICCs one can (i) meet expenses/make

purchases while abroad (ii) make payments

in foreign exchange for purchase of books

and other items through internet in India.

• Not permitted for prohibited transactions

such as purchase of lottery tickets, banned

magazines etc

• Payment in foreign exchange in Nepal and

Bhutan through ICC / ATM / Debit card is

not permitted

• Limits under Schedule III do not apply to

ICC while they apply to IDC

Use of ICC/IDC

Miscellaneous remittances

from India

15

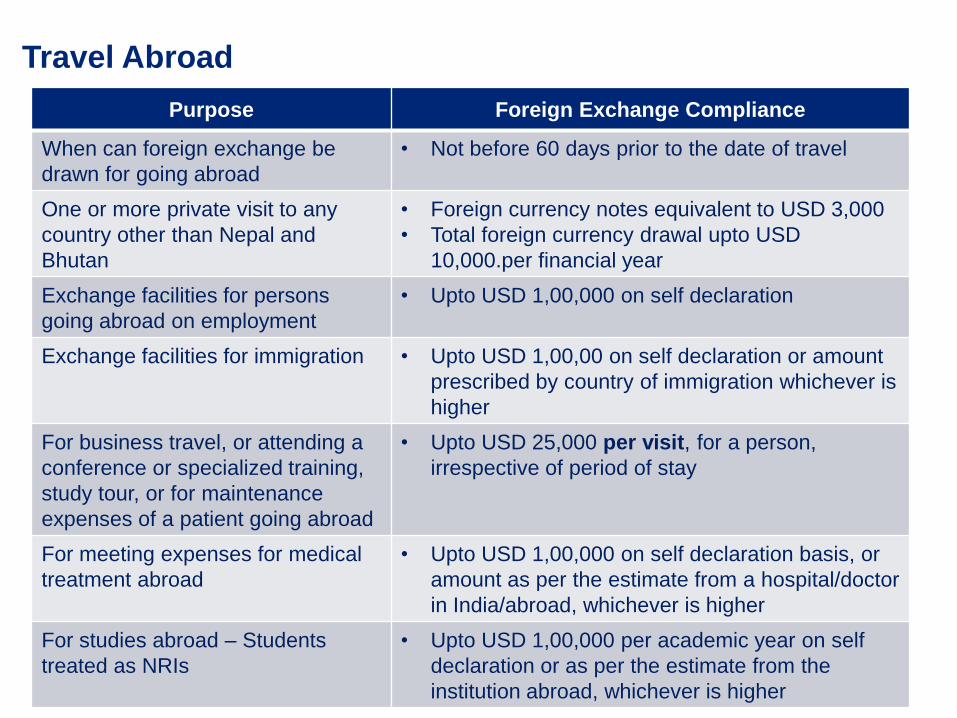

Travel Abroad

Purpose Foreign Exchange Compliance

When can foreign exchange be

drawn for going abroad

• Not before 60 days prior to the date of travel

One or more private visit to any

country other than Nepal and

Bhutan

• Foreign currency notes equivalent to USD 3,000

• Total foreign currency drawal upto USD

10,000.per financial year

Exchange facilities for persons

going abroad on employment

• Upto USD 1,00,000 on self declaration

Exchange facilities for immigration • Upto USD 1,00,00 on self declaration or amount

prescribed by country of immigration whichever is

higher

For business travel, or attending a

conference or specialized training,

study tour, or for maintenance

expenses of a patient going abroad

• Upto USD 25,000 per visit, for a person,

irrespective of period of stay

For meeting expenses for medical

treatment abroad

• Upto USD 1,00,000 on self declaration basis, or

amount as per the estimate from a hospital/doctor

in India/abroad, whichever is higher

For studies abroad – Students

treated as NRIs

• Upto USD 1,00,000 per academic year on self

declaration or as per the estimate from the

institution abroad, whichever is higher

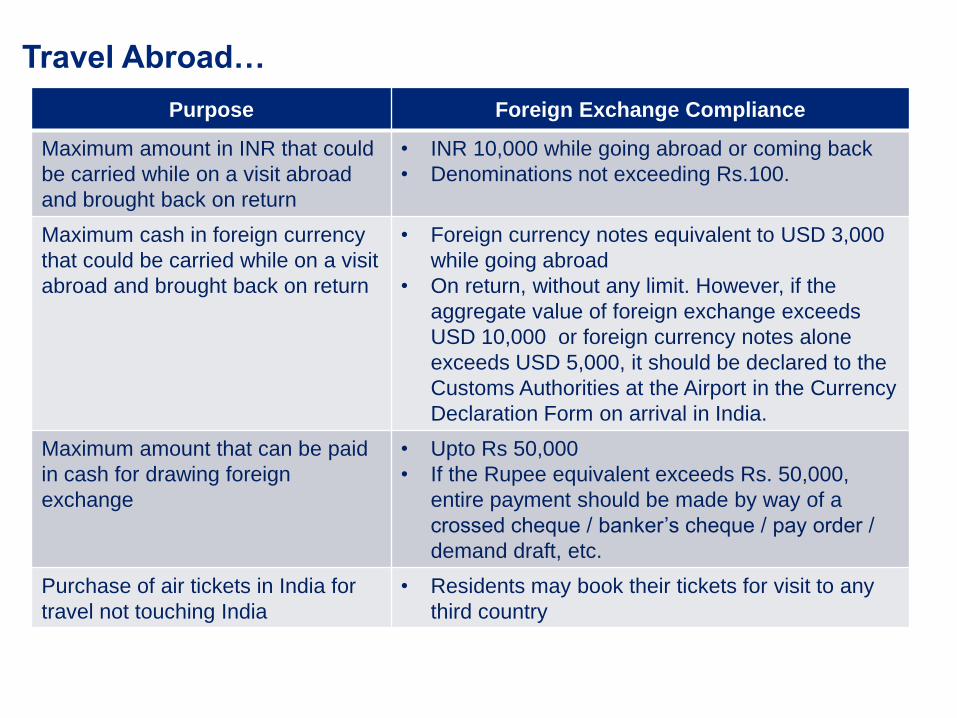

Purpose Foreign Exchange Compliance

Maximum amount in INR that could

be carried while on a visit abroad

and brought back on return

• INR 10,000 while going abroad or coming back

• Denominations not exceeding Rs.100.

Maximum cash in foreign currency

that could be carried while on a visit

abroad and brought back on return

• Foreign currency notes equivalent to USD 3,000

while going abroad

• On return, without any limit. However, if the

aggregate value of foreign exchange exceeds

USD 10,000 or foreign currency notes alone

exceeds USD 5,000, it should be declared to the

Customs Authorities at the Airport in the Currency

Declaration Form on arrival in India.

Maximum amount that can be paid

in cash for drawing foreign

exchange

• Upto Rs 50,000

• If the Rupee equivalent exceeds Rs. 50,000,

entire payment should be made by way of a

crossed cheque / banker’s cheque / pay order /

demand draft, etc.

Purchase of air tickets in India for

travel not touching India

• Residents may book their tickets for visit to any

third country

Travel Abroad…

Surrender of foreign currency

18

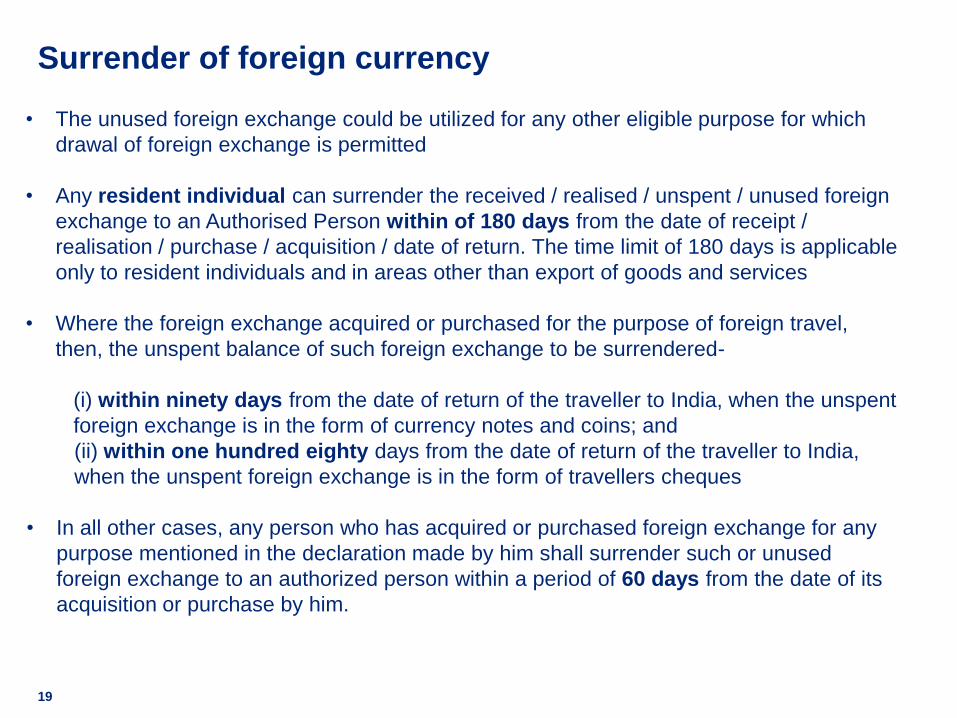

Surrender of foreign currency

19

• The unused foreign exchange could be utilized for any other eligible purpose for which

drawal of foreign exchange is permitted

• Any resident individual can surrender the received / realised / unspent / unused foreign

exchange to an Authorised Person within of 180 days from the date of receipt /

realisation / purchase / acquisition / date of return. The time limit of 180 days is applicable

only to resident individuals and in areas other than export of goods and services

• Where the foreign exchange acquired or purchased for the purpose of foreign travel,

then, the unspent balance of such foreign exchange to be surrendered-

(i) within ninety days from the date of return of the traveller to India, when the unspent

foreign exchange is in the form of currency notes and coins; and

(ii) within one hundred eighty days from the date of return of the traveller to India,

when the unspent foreign exchange is in the form of travellers cheques

• In all other cases, any person who has acquired or purchased foreign exchange for any

purpose mentioned in the declaration made by him shall surrender such or unused

foreign exchange to an authorized person within a period of 60 days from the date of its

acquisition or purchase by him.

Retention of foreign currency

20

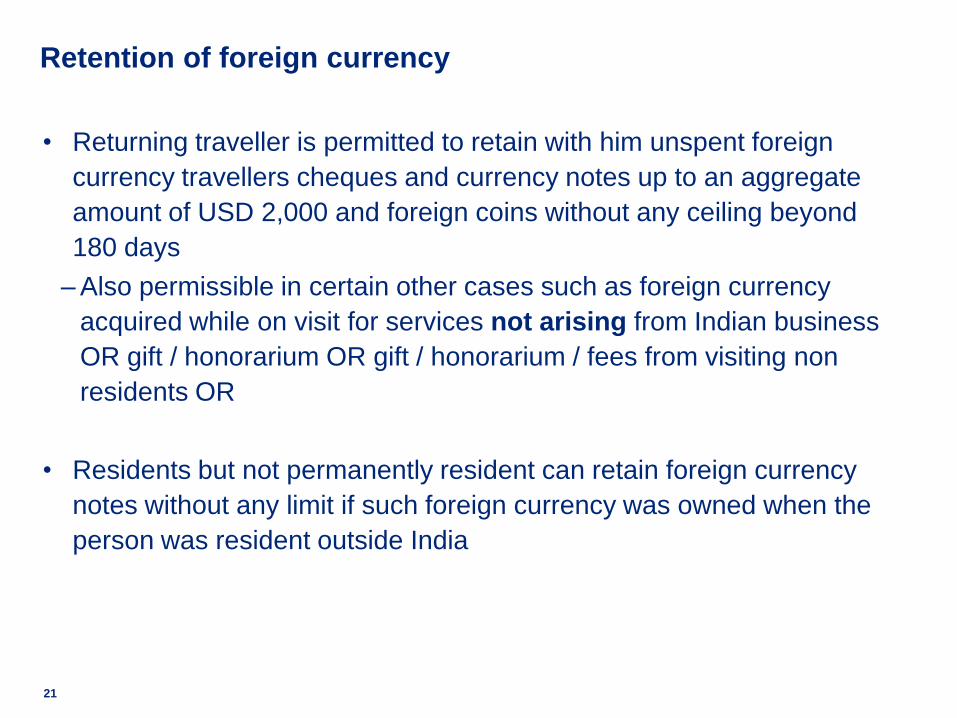

Retention of foreign currency

• Returning traveller is permitted to retain with him unspent foreign

currency travellers cheques and currency notes up to an aggregate

amount of USD 2,000 and foreign coins without any ceiling beyond

180 days

‒ Also permissible in certain other cases such as foreign currency

acquired while on visit for services not arising from Indian business

OR gift / honorarium OR gift / honorarium / fees from visiting non

residents OR

• Residents but not permanently resident can retain foreign currency

notes without any limit if such foreign currency was owned when the

person was resident outside India

21

Liberalized Remittance

Scheme

22

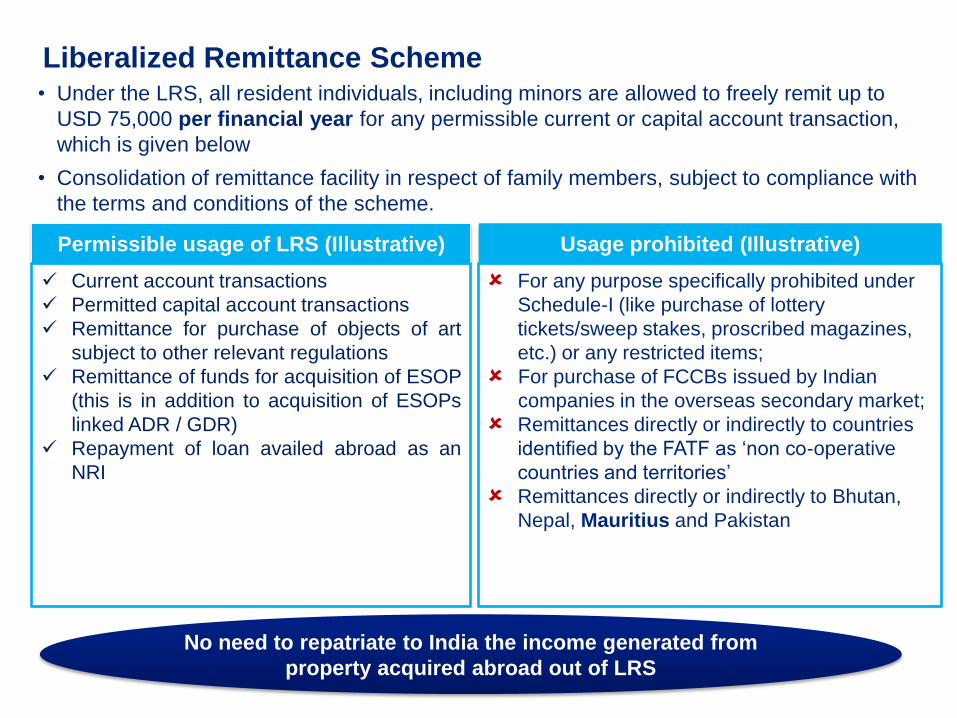

Liberalized Remittance Scheme

23

• Under the LRS, all resident individuals, including minors are allowed to freely remit up to

USD 75,000 per financial year for any permissible current or capital account transaction,

which is given below

• Consolidation of remittance facility in respect of family members, subject to compliance with

the terms and conditions of the scheme.

Permissible usage of LRS (Illustrative) Usage prohibited (Illustrative)

Current account transactions

Permitted capital account transactions

Remittance for purchase of objects of art

subject to other relevant regulations

Remittance of funds for acquisition of ESOP

(this is in addition to acquisition of ESOPs

linked ADR / GDR)

Repayment of loan availed abroad as an

NRI

For any purpose specifically prohibited under

Schedule-I (like purchase of lottery

tickets/sweep stakes, proscribed magazines,

etc.) or any restricted items;

For purchase of FCCBs issued by Indian

companies in the overseas secondary market;

Remittances directly or indirectly to countries

identified by the FATF as ‘non co-operative

countries and territories’

Remittances directly or indirectly to Bhutan,

Nepal, Mauritius and Pakistan

No need to repatriate to India the income generated from

property acquired abroad out of LRS

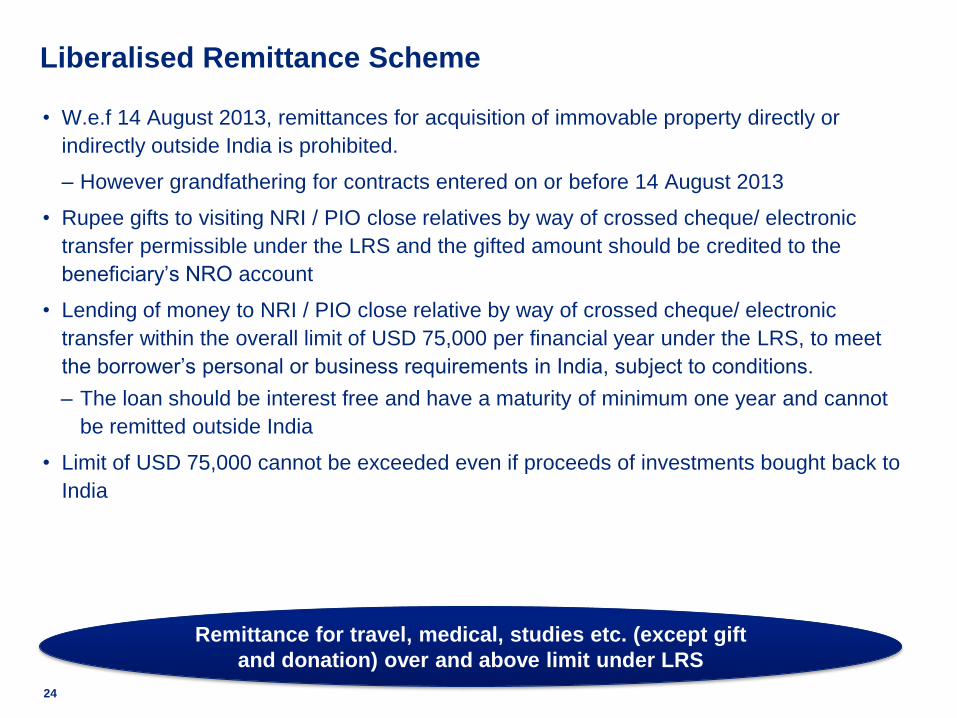

Liberalised Remittance Scheme

• W.e.f 14 August 2013, remittances for acquisition of immovable property directly or

indirectly outside India is prohibited.

‒ However grandfathering for contracts entered on or before 14 August 2013

• Rupee gifts to visiting NRI / PIO close relatives by way of crossed cheque/ electronic

transfer permissible under the LRS and the gifted amount should be credited to the

beneficiary’s NRO account

• Lending of money to NRI / PIO close relative by way of crossed cheque/ electronic

transfer within the overall limit of USD 75,000 per financial year under the LRS, to meet

the borrower’s personal or business requirements in India, subject to conditions.

‒ The loan should be interest free and have a maturity of minimum one year and cannot

be remitted outside India

• Limit of USD 75,000 cannot be exceeded even if proceeds of investments bought back to

India

24

Remittance for travel, medical, studies etc. (except gift

and donation) over and above limit under LRS

Foreign currency bank account

by a resident

25

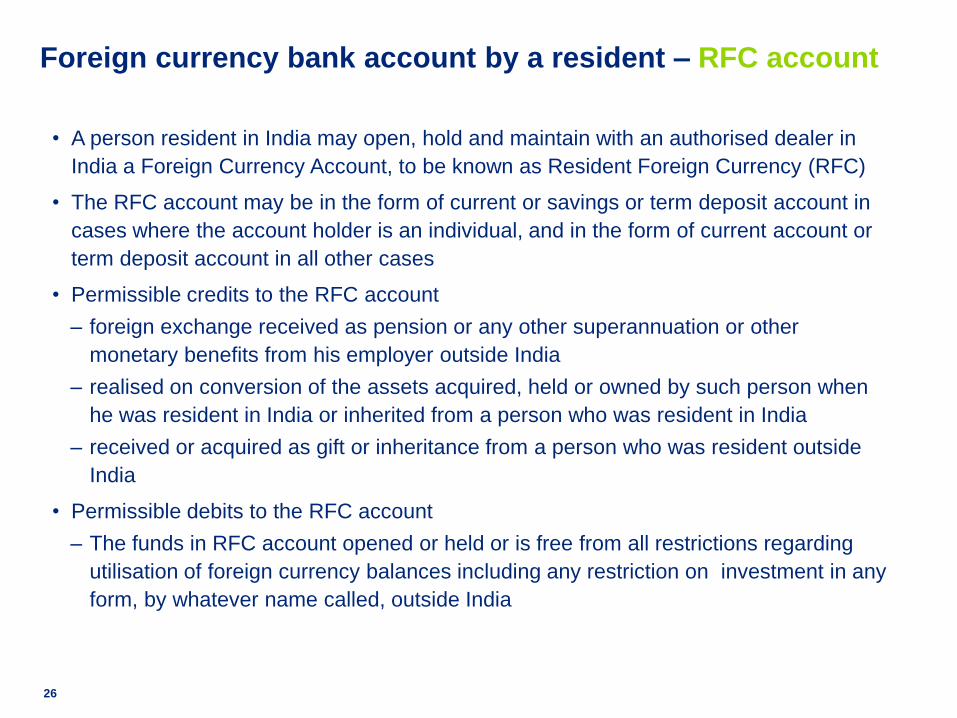

26

• A person resident in India may open, hold and maintain with an authorised dealer in

India a Foreign Currency Account, to be known as Resident Foreign Currency (RFC)

• The RFC account may be in the form of current or savings or term deposit account in

cases where the account holder is an individual, and in the form of current account or

term deposit account in all other cases

• Permissible credits to the RFC account

‒ foreign exchange received as pension or any other superannuation or other

monetary benefits from his employer outside India

‒ realised on conversion of the assets acquired, held or owned by such person when

he was resident in India or inherited from a person who was resident in India

‒ received or acquired as gift or inheritance from a person who was resident outside

India

• Permissible debits to the RFC account

‒ The funds in RFC account opened or held or is free from all restrictions regarding

utilisation of foreign currency balances including any restriction on investment in any

form, by whatever name called, outside India

Foreign currency bank account by a resident – RFC account

27

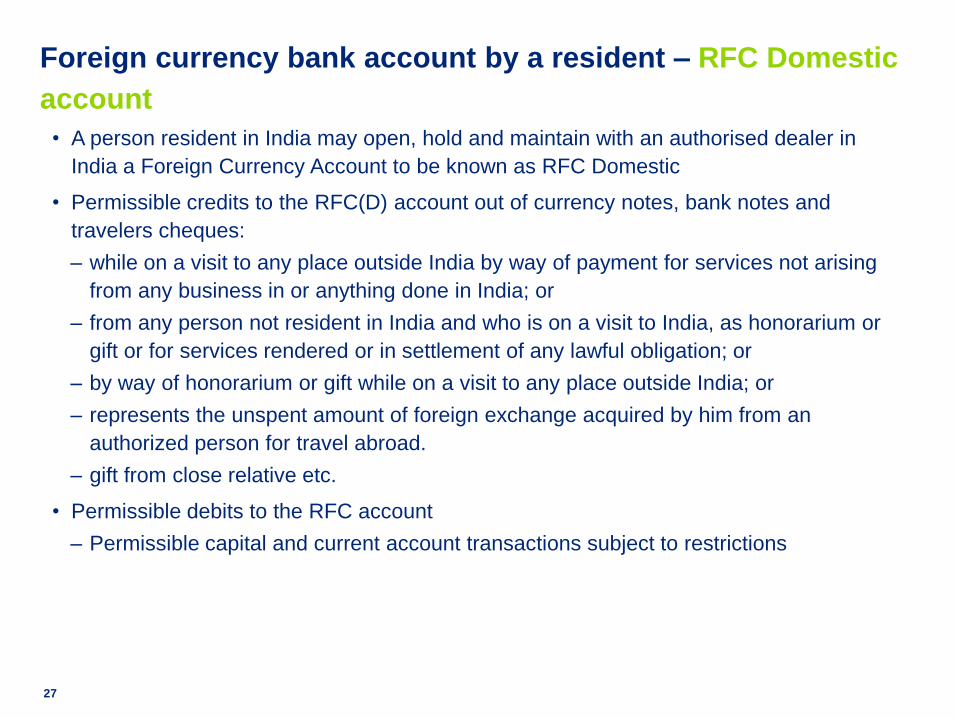

• A person resident in India may open, hold and maintain with an authorised dealer in

India a Foreign Currency Account to be known as RFC Domestic

• Permissible credits to the RFC(D) account out of currency notes, bank notes and

travelers cheques:

‒ while on a visit to any place outside India by way of payment for services not arising

from any business in or anything done in India; or

‒ from any person not resident in India and who is on a visit to India, as honorarium or

gift or for services rendered or in settlement of any lawful obligation; or

‒ by way of honorarium or gift while on a visit to any place outside India; or

‒ represents the unspent amount of foreign exchange acquired by him from an

authorized person for travel abroad.

‒ gift from close relative etc.

• Permissible debits to the RFC account

‒ Permissible capital and current account transactions subject to restrictions

Foreign currency bank account by a resident – RFC Domestic

account

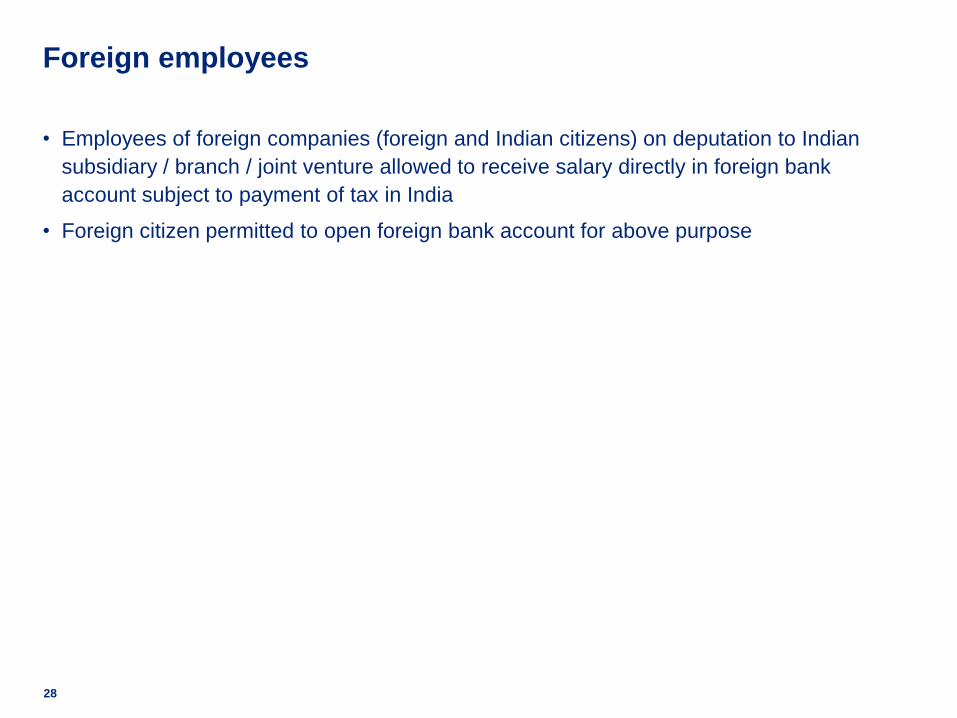

• Employees of foreign companies (foreign and Indian citizens) on deputation to Indian

subsidiary / branch / joint venture allowed to receive salary directly in foreign bank

account subject to payment of tax in India

• Foreign citizen permitted to open foreign bank account for above purpose

28

Foreign employees

Remittance facilities for Non

NRIs / PIO / Foreign Nationals

29

30

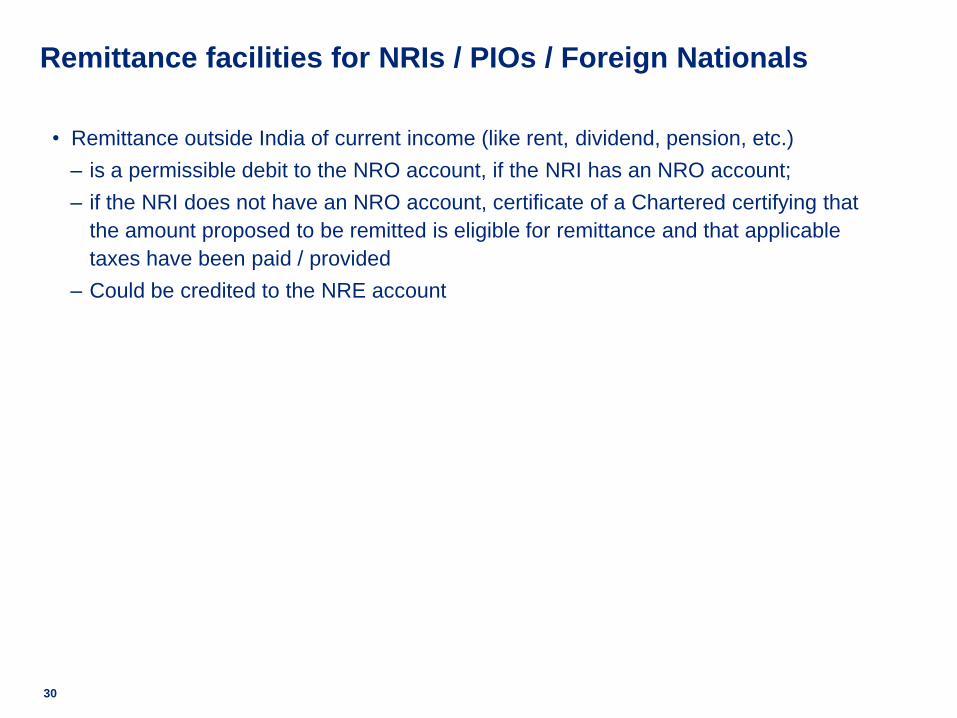

• Remittance outside India of current income (like rent, dividend, pension, etc.)

‒ is a permissible debit to the NRO account, if the NRI has an NRO account;

‒ if the NRI does not have an NRO account, certificate of a Chartered certifying that

the amount proposed to be remitted is eligible for remittance and that applicable

taxes have been paid / provided

‒ Could be credited to the NRE account

Remittance facilities for NRIs / PIOs / Foreign Nationals

31

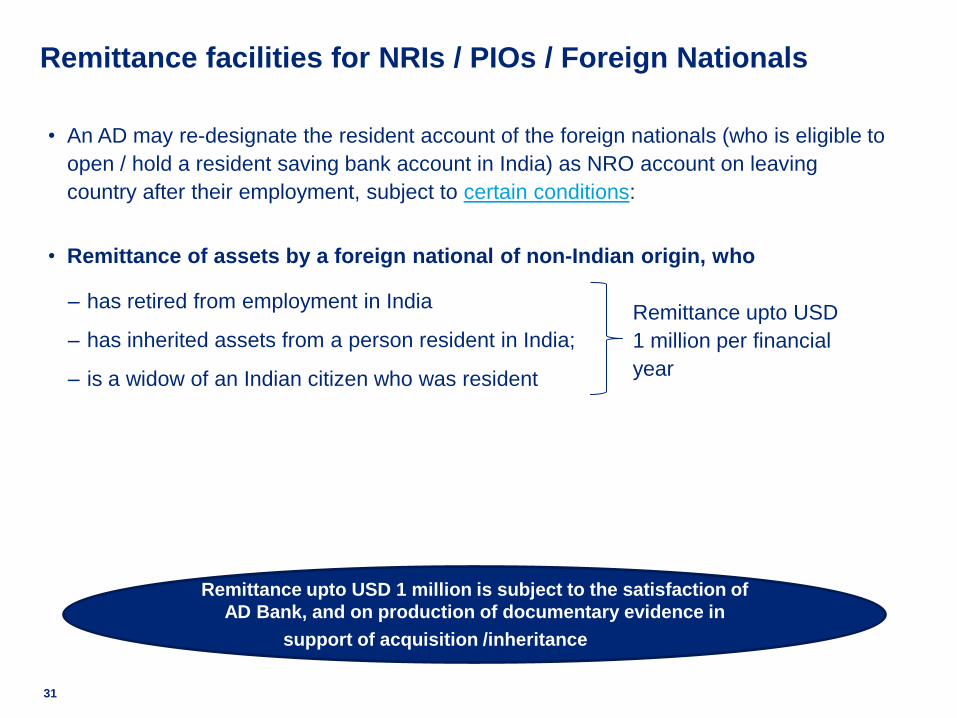

• An AD may re-designate the resident account of the foreign nationals (who is eligible to

open / hold a resident saving bank account in India) as NRO account on leaving

country after their employment, subject to certain conditions:

• Remittance of assets by a foreign national of non-Indian origin, who

Remittance facilities for NRIs / PIOs / Foreign Nationals

‒ has retired from employment in India Remittance upto USD

1 million per financial

year

‒ has inherited assets from a person resident in India;

‒ is a widow of an Indian citizen who was resident

Remittance upto USD 1 million is subject to the satisfaction of

AD Bank, and on production of documentary evidence in

support of acquisition /inheritance

32

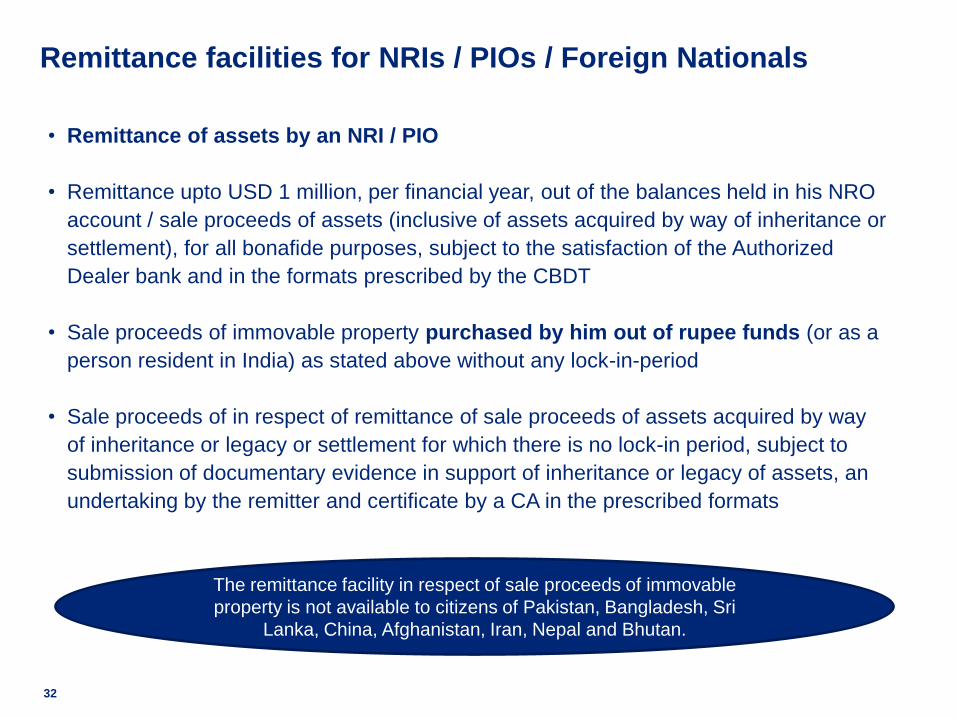

• Remittance of assets by an NRI / PIO

• Remittance upto USD 1 million, per financial year, out of the balances held in his NRO

account / sale proceeds of assets (inclusive of assets acquired by way of inheritance or

settlement), for all bonafide purposes, subject to the satisfaction of the Authorized

Dealer bank and in the formats prescribed by the CBDT

• Sale proceeds of immovable property purchased by him out of rupee funds (or as a

person resident in India) as stated above without any lock-in-period

• Sale proceeds of in respect of remittance of sale proceeds of assets acquired by way

of inheritance or legacy or settlement for which there is no lock-in period, subject to

submission of documentary evidence in support of inheritance or legacy of assets, an

undertaking by the remitter and certificate by a CA in the prescribed formats

Remittance facilities for NRIs / PIOs / Foreign Nationals

The remittance facility in respect of sale proceeds of immovable

property is not available to citizens of Pakistan, Bangladesh, Sri

Lanka, China, Afghanistan, Iran, Nepal and Bhutan.

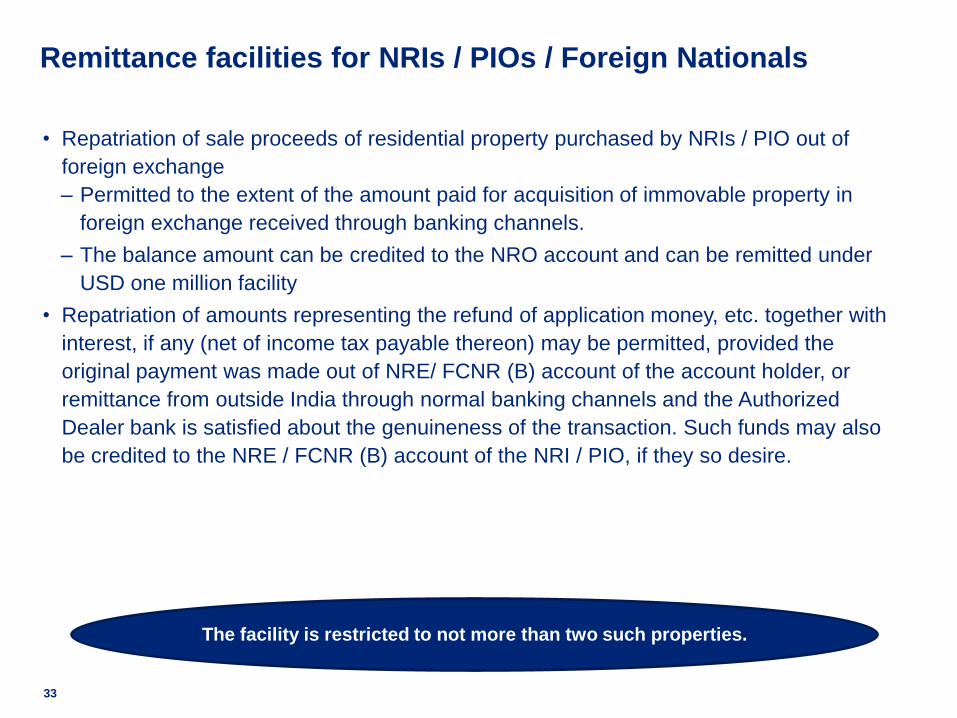

• Repatriation of sale proceeds of residential property purchased by NRIs / PIO out of

foreign exchange

‒ Permitted to the extent of the amount paid for acquisition of immovable property in

foreign exchange received through banking channels.

‒ The balance amount can be credited to the NRO account and can be remitted under

USD one million facility

• Repatriation of amounts representing the refund of application money, etc. together with

interest, if any (net of income tax payable thereon) may be permitted, provided the

original payment was made out of NRE/ FCNR (B) account of the account holder, or

remittance from outside India through normal banking channels and the Authorized

Dealer bank is satisfied about the genuineness of the transaction. Such funds may also

be credited to the NRE / FCNR (B) account of the NRI / PIO, if they so desire.

33

The facility is restricted to not more than two such properties.

Remittance facilities for NRIs / PIOs / Foreign Nationals

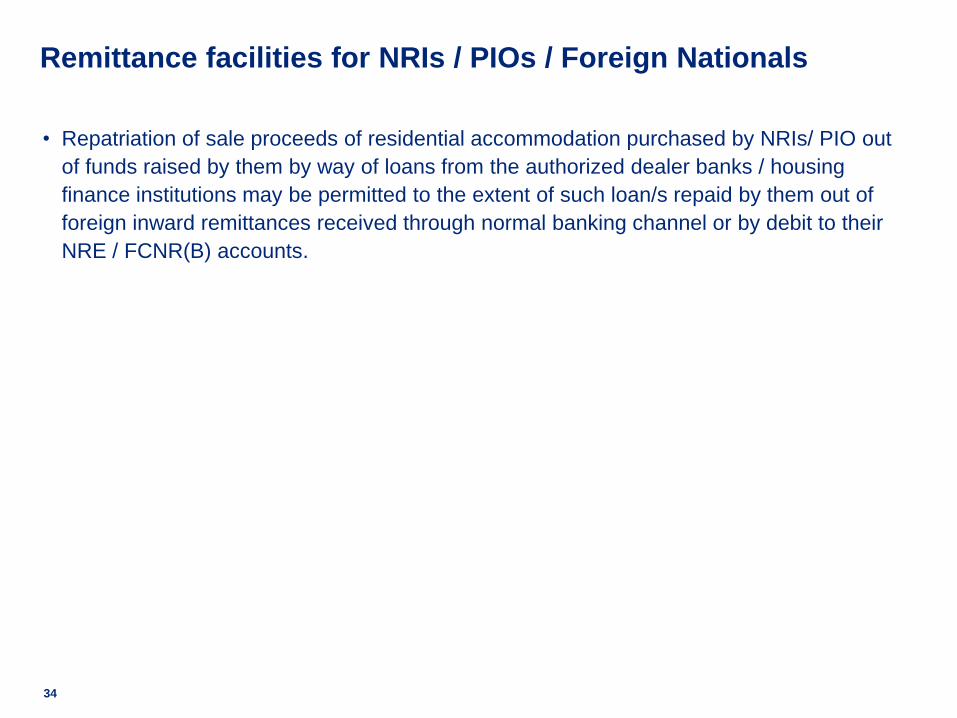

• Repatriation of sale proceeds of residential accommodation purchased by NRIs/ PIO out

of funds raised by them by way of loans from the authorized dealer banks / housing

finance institutions may be permitted to the extent of such loan/s repaid by them out of

foreign inward remittances received through normal banking channel or by debit to their

NRE / FCNR(B) accounts.

34

Remittance facilities for NRIs / PIOs / Foreign Nationals

Thank you!!!

36

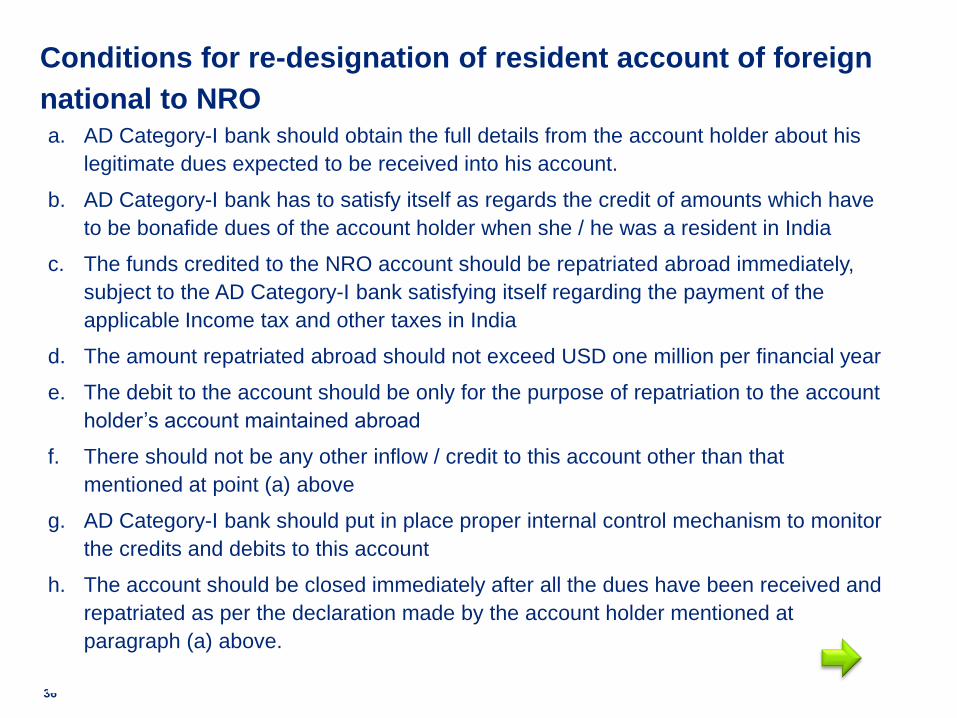

a. AD Category-I bank should obtain the full details from the account holder about his

legitimate dues expected to be received into his account.

b. AD Category-I bank has to satisfy itself as regards the credit of amounts which have

to be bonafide dues of the account holder when she / he was a resident in India

c. The funds credited to the NRO account should be repatriated abroad immediately,

subject to the AD Category-I bank satisfying itself regarding the payment of the

applicable Income tax and other taxes in India

d. The amount repatriated abroad should not exceed USD one million per financial year

e. The debit to the account should be only for the purpose of repatriation to the account

holder’s account maintained abroad

f. There should not be any other inflow / credit to this account other than that

mentioned at point (a) above

g. AD Category-I bank should put in place proper internal control mechanism to monitor

the credits and debits to this account

h. The account should be closed immediately after all the dues have been received and

repatriated as per the declaration made by the account holder mentioned at

paragraph (a) above.

Conditions for re-designation of resident account of foreign

national to NRO

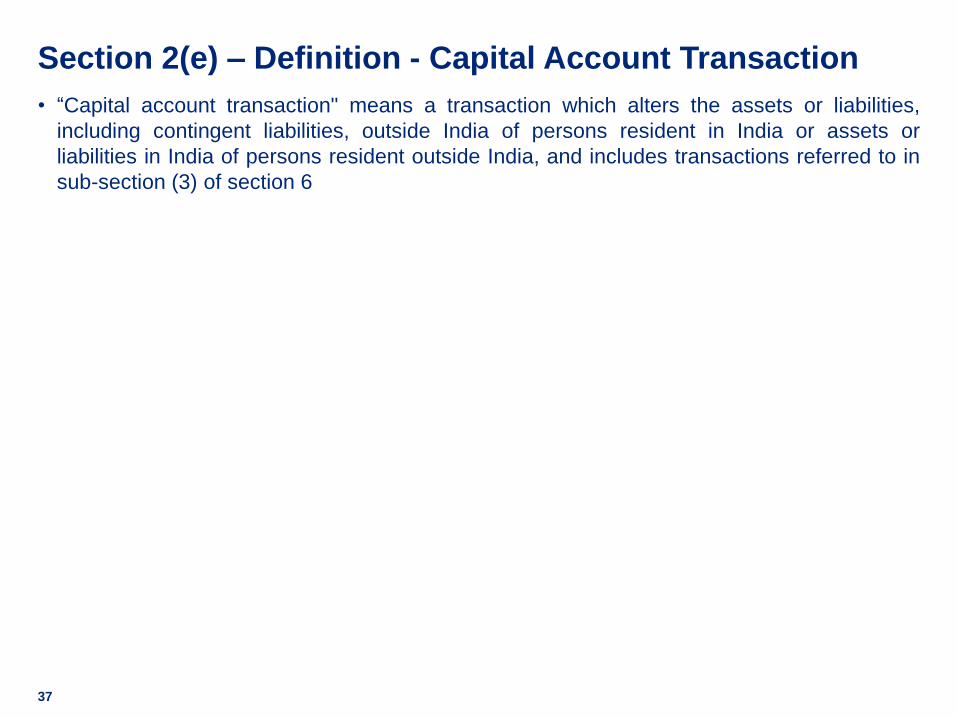

Section 2(e) – Definition - Capital Account Transaction

37

• “Capital account transaction" means a transaction which alters the assets or liabilities,

including contingent liabilities, outside India of persons resident in India or assets or

liabilities in India of persons resident outside India, and includes transactions referred to in

sub-section (3) of section 6

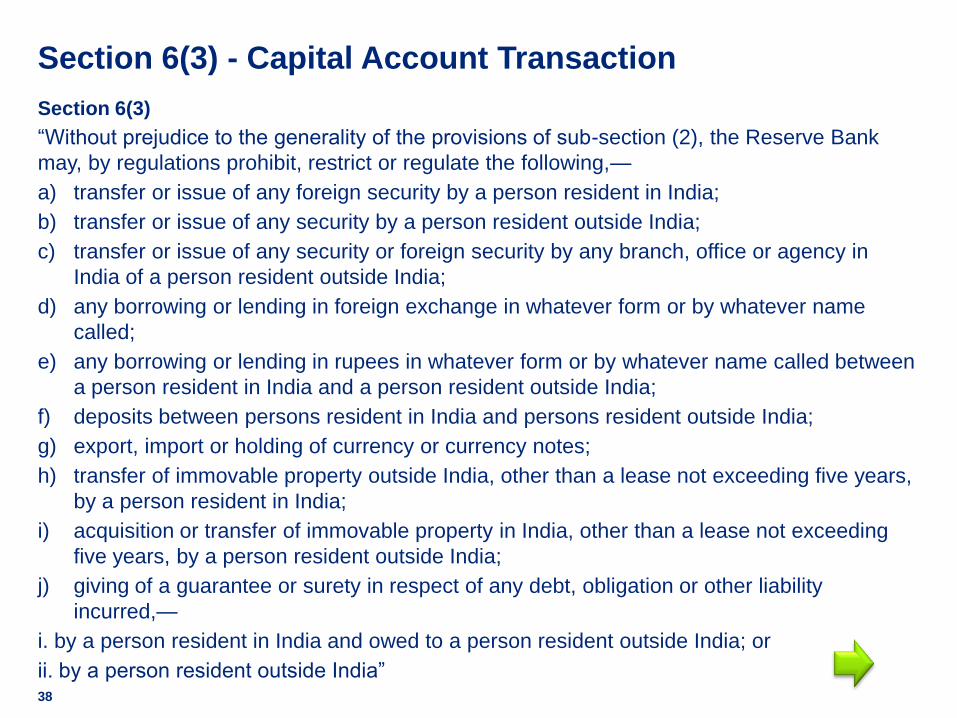

Section 6(3) - Capital Account Transaction

38

Section 6(3)

“Without prejudice to the generality of the provisions of sub-section (2), the Reserve Bank

may, by regulations prohibit, restrict or regulate the following,—

a) transfer or issue of any foreign security by a person resident in India;

b) transfer or issue of any security by a person resident outside India;

c) transfer or issue of any security or foreign security by any branch, office or agency in

India of a person resident outside India;

d) any borrowing or lending in foreign exchange in whatever form or by whatever name

called;

e) any borrowing or lending in rupees in whatever form or by whatever name called between

a person resident in India and a person resident outside India;

f) deposits between persons resident in India and persons resident outside India;

g) export, import or holding of currency or currency notes;

h) transfer of immovable property outside India, other than a lease not exceeding five years,

by a person resident in India;

i) acquisition or transfer of immovable property in India, other than a lease not exceeding

five years, by a person resident outside India;

j) giving of a guarantee or surety in respect of any debt, obligation or other liability

incurred,—

i. by a person resident in India and owed to a person resident outside India; or

ii. by a person resident outside India”

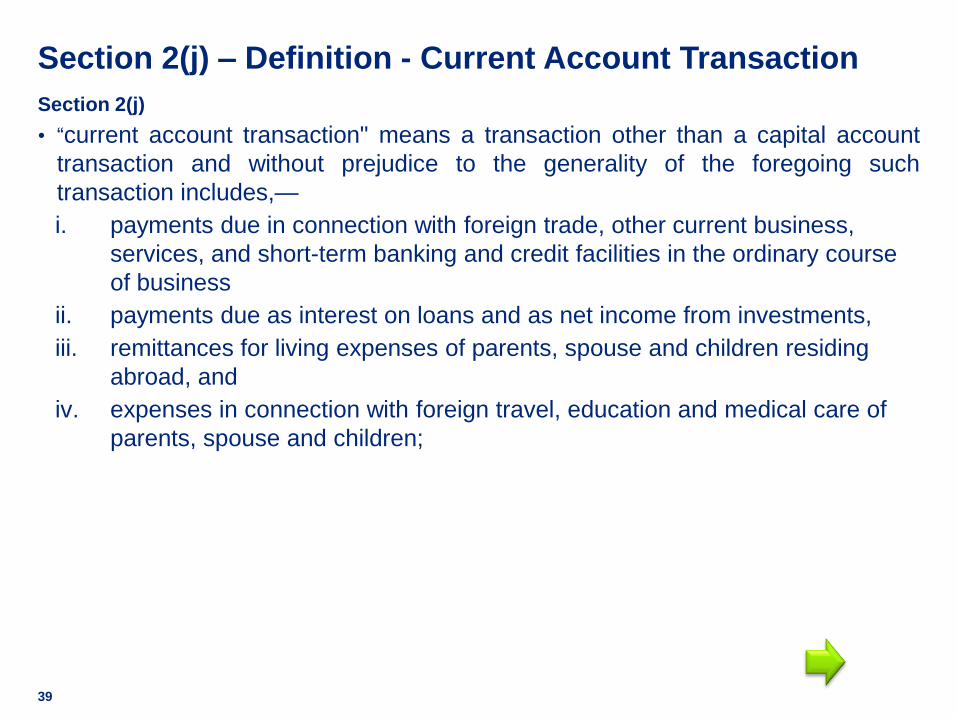

Section 2(j) – Definition - Current Account Transaction

39

Section 2(j)

• “current account transaction" means a transaction other than a capital account

transaction and without prejudice to the generality of the foregoing such

transaction includes,—

i. payments due in connection with foreign trade, other current business,

services, and short-term banking and credit facilities in the ordinary course

of business

ii. payments due as interest on loans and as net income from investments,

iii. remittances for living expenses of parents, spouse and children residing

abroad, and

iv. expenses in connection with foreign travel, education and medical care of

parents, spouse and children;