Embed Size (px)

Citation preview

Table of Contents

Fertilizer and Seed Sector Assessment in Niger...........................................................................21. Introduction.............................................................................................................................2

1.1 Methodology.......................................................................................................................31.2 Outline of the report............................................................................................................4

2. Fertilizer sector in Niger........................................................................................................52.1 Existing Mechanism of Fertilizer Purchase and Distribution.............................................52.2 Fertilizer pricing under CAIMA.........................................................................................72.3 Fertilizer demand and supply..............................................................................................72.4 Non – CAIMA fertilizer sources through cross-border trade.............................................82.5 Fertilizer cost build- ups.....................................................................................................92.6 Limiting factors for private sector development to CAIMA fertilizer distribution..........112.7 How to stimulate the private sector development in fertilizer market of Niger?.............12

3. The seed value chain in Niger.............................................................................................153.1 Seed research, certification and quality control activities................................................163.2 Seed multiplication activities............................................................................................173.3 Seed distribution activities................................................................................................203.4 Other seed related organizations.......................................................................................213.5 Seed market status in Niger..............................................................................................223.6 Constraints in the seed value chain...................................................................................27

List of Tables

Table 1 Estimates on Fertilizer supplied by CAIMA (Metric Tons) 8

Table 2 Details of fertilizer importation costs 9

Table 3 Quantity of fertilizer supplied and prices of fertilizer supplied through subsidy programs in Burkina Faso, Togo and Ghana

11

Table 4 Existing registered private seed firms in Niger (2014/15) 20

Table 5 Quantity of certified seeds (R1&R2) produced (kg) and distributed for major crops in 2011/12 and 2014/15

24

Table 6 Estimated certified seeds coverage under various crops in Niger (2014/15) 24

List of Figures

Figure 1 Area and production of major crops in Niger (2000-2014) (Mill Ha/ Mill Tons) 2

Figure 2 Existing System for Fertilizer importation and distribution in Niger 6

Figure 3 Public and private sector role(s) in the current seed systems in Niger 16

Figure 4 Existing seed system(s) for crops in Niger 17

Figure 5 Proportion (%) of certified seeds multiplied by seed stakeholders in in Niger 19

Figure 6 Quantity of Certified seed production (R1&R2) in Niger (2002/03 – 2014/15) 23

Figure 7 Yield of major cereal crops in Niger (2000-2014) 25

1

Fertilizer and Seed Sector Assessment in Niger

1. Introduction

Niger is a land locked country with a total geographical land area of 126.7 million hectares. The current population is approximately 17 + million people, and given that its annual population growth rate is 3.9 % (the sixth highest in the world) the population is projected to exceed 66 million by 2050. Nearly 40 per cent of Niger’s GDP is derived from the formal agriculture sector, although it has a very low proportion of arable land (13 %) that is suitable for rain fed agriculture (FAO, 2013). The agro ecology of the country is characterized as arid and semi-arid climatic types, with a very short rainy season (June – September), receiving about 600 mm of annual rainfall (in northern part – the Sahel desert receives less than 150 mm annually). Hence the agricultural activity in Niger is mainly rainfed and highly vulnerable to climate induced hazards particularly drought. The total irrigated area in Niger is around 87,870 ha (AQUASTAT, 2010), which is less than 0.5% of the total cultivable area.

Niger is the fifth largest producer of uranium in the world, and production is likely to triple by 2018. Uranium remains an important determinant of the national economic outlook, accounting for about 50 per cent of total exports. However, farming continues to be the main livelihood source for 80 % of the population in Niger. Millet and sorghum are the major rain fed subsistence crops providing more than 50 % of food source for human consumption in the country. Niger has one of the highest acreage of millet (> 7 million hectares), and an average annual consumption of 1.7 Million Tons, which is third highest in the world after India (9 Mt) and Nigeria (4.3 Mt). Agricultural production is characterized by two seasons: a rainfed season, which is determined by annual rainfall, and an irrigation season (also known as the off-season). Rainfed agricultural production is primarily for staple cereal crops, including millet, sorghum, rice, fonio, wheat, and commercial cash crops such as cowpea, peanuts, sesame, souchet, and onions. Off-season production includes rice, vegetables, and staple cereal crops.

Figure 1 Area and production of major crops in Niger (2000-2014) (Mill Ha/ Mill Tons)

2000 2002 2004 2006 2008 2010 2012 2014

0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

8000000

Cowpea

Sorghum

Millet

Are

a

2000 2002 2004 2006 2008 2010 2012 2014

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

Cowpea

Sorghum

Mil

Pro

du

ctio

n i

n T

on

s

Source: FAOSTAT, 2016

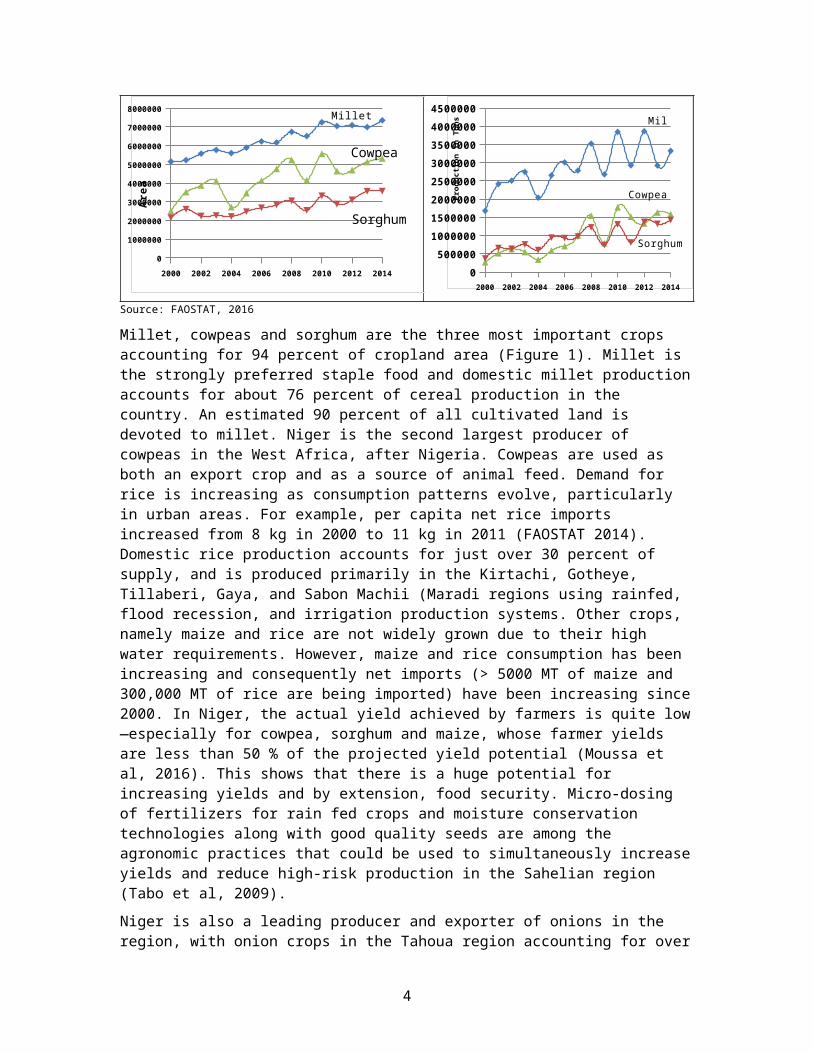

Millet, cowpeas and sorghum are the three most important crops accounting for 94 percent of cropland area (Figure 1). Millet is the strongly preferred staple food and domestic millet production accounts for about 76 percent of cereal production in the country. An estimated 90 percent of all cultivated land is devoted to millet. Niger is the second largest producer of cowpeas in the West Africa, after Nigeria. Cowpeas are used as both an export crop and as a source of animal feed. Demand for rice is increasing as consumption patterns evolve, particularly in urban

2

areas. For example, per capita net rice imports increased from 8 kg in 2000 to 11 kg in 2011 (FAOSTAT 2014). Domestic rice production accounts for just over 30 percent of supply, and is produced primarily in the Kirtachi, Gotheye, Tillaberi, Gaya, and Sabon Machii (Maradi regions using rainfed, flood recession, and irrigation production systems. Other crops, namely maize and rice are not widely grown due to their high water requirements. However, maize and rice consumption has been increasing and consequently net imports (> 5000 MT of maize and 300,000 MT of rice are being imported) have been increasing since 2000. In Niger, the actual yield achieved by farmers is quite low—especially for cowpea, sorghum and maize, whose farmer yields are less than 50 % of the projected yield potential (Moussa et al, 2016). This shows that there is a huge potential for increasing yields and by extension, food security. Micro-dosing of fertilizers for rain fed crops and moisture conservation technologies along with good quality seeds are among the agronomic practices that could be used to simultaneously increase yields and reduce high-risk production in the Sahelian region (Tabo et al, 2009).

Niger is also a leading producer and exporter of onions in the region, with onion crops in the Tahoua region accounting for over 75 percent of national production. The onion industry is a key livelihoods source for farmers across the country, and domestic production averages 500,000 tons per year, much of which is marketed in West Africa through a commercial network that supplies coastal countries in the sub region. Nigerien households consume about five percent of national production (21,000 tons, or 4.4 kilograms per person per year). Onions are produced as the primary dry season crop (> 30,200 hectares cultivated), followed by okra, eggplant, and cabbage. Nigeria is a primary consumer of Nigerien cash crops, namely cowpea, groundnut, and souchet.

The fragile agriculture environment with frequent and extended droughts combined with high population growth rates pose a huge risk in terms of providing food security to the population. It is evident that Niger crop productivity levels are quite low and there exists great potential for improving agricultural productivity, which has direct impact on the food security of the population. As elsewhere in sub-Saharan Africa, farmers in Niger have limited access to external inputs such as improved seeds and fertilizers to improve their productivity levels. In addition farmers in Niger face major constraints including: (i.) a lack of technical skills and knowledge about agricultural technologies; (ii.) poor market access; and, (iii.) above inadequate access to finances needed to purchase inputs. In this context, it is important to analyse the existing mechanisms available for distribution of fertilizers and seeds in Niger and make suitable recommendations either to streamline existing systems or to propose a series of new measures that will rectify the constraints on the efficient functioning of the input markets in Niger. The objectives of the current assessment include;

i. describe the input markets and demand and supply for seed and fertilizer in Niger;ii. identify the actors in the seed and fertilizer value chains and the constraints they

face;iii. describe the mechanics of the existing fertilizer subsidy program;iv. develop a plan for streamlining the fertilizer distribution mechanisms with

increased private sector participation; and,v. provide recommendations to improve the effectiveness and efficiency of the seed

and fertilizer value chain operations which will provide better delivery of inputs on a sustainable basis.

1.1 Methodology

The technical team of IFDC prior to the field assessment carried out detailed literature review through extensive desktop research. With the help of Millennium Challenge Program Coordination Unit colleagues in Niamey-Niger a preliminary list of stakeholders involved in agri-

3

inputs distribution were prepared for consultations during the field trip. Further for sector specific (seed / fertilizer) related consultations, the IFDC team generated an additional list of local stakeholders involved in logistics and seed production. The field level assessment was implemented from February 7th to 12th, 2016 along with MCC-Niger staff.

During the country visit the team conducted individual interviews as well as focus group discussions with a rage of stakeholders. These engagements included face-to-face meetings (interviews), and key informant surveys to gain a broad, detailed perspective of seed and fertilizer related issues in the country, the current context of development and key intervention points to strengthen the sector. The groups were well represented by government – Ministry of Agriculture officials, farmer association representatives, agro-dealers (retail and wholesale distributors), private seed firms, fertilizer importers, seed producers association, financial institutions, logistics firms, international organizations and research scientists. During the field trip, discussions were also held with farmers to get their perception on existing inputs demand and constraints in accessing inputs through the existing system. Detailed lists of stakeholders interviewed during the field trip are enclosed in the Annexure 1.

1.2 Outline of the report

Following this section, which provides the background of the study along with the objectives and methodology adopted, section 2 describes the current fertilizer distribution mechanism, presents the supply and demand situation for fertilizers and provides suggested recommendations to stream line the existing system and offer a plan towards building an effective private sector based fertilizer sector in Niger. Section 3 provides a description of the seed value chain along with its stakeholders, supply and demand for seeds and the recommendations to improve the existing seed system. The final section presents the conclusions and policy implications concerning viable input distribution mechanisms in Niger.

4

2. Fertilizer sector in Niger

Fertilizer use in Niger is around 4 to 5 kg/ha, well below the continental average, which stands around 12 kg/ha and itself is well below targets for efficient and effective agricultural production. The target for 2015 fertilizer use adopted at the Africa Fertilizer Summit is 50 Kg/ha. In Niger fertilizers are mainly used for irrigated crops and to a very limited extent on rain fed crops. According to the FAO Report on République du Niger. Etude des fertilisants du sol. Rapport principal published in 2001, the percentage of farmers using fertilizer is more for vegetable crops (onions 80%, other veg 84%) than other irrigated crops such as maize and sorghum (35%), rice (60%) and very low for rain-fed crops as millet (1%), sorghum (5%) and cowpea (3%). The fertilizer market in Niger is very small (30,000 MT/year) compared to other countries in the region. For instance the neighboring countries such as Ghana and Burkina Faso consume an average of 250,000 MT/ year and Nigeria consumes more than 800,000 MT/ year. Niger is a land locked country and with its extensive geographical coverage, the logistics of importing and distributing to various parts of the country is not sufficiently remunerative for private firms to make investments in such systems.

2.1 Existing Mechanism of Fertilizer Purchase and Distribution

In order to improve fertilizer use by farmers in the country in 1978, Ministry of Agriculture created an exclusive agency called Central d’Aprrovisionnement (CA), to manage the fertilizers given by donors (South Africa, Nigeria, Japan etc.,) in a more efficient manner. In 2010-11, the CA became the Centrale d’Approvisionnement en Intrants et Matériels Agricoles (CAIMA) – a para-statal agency under the Ministry of Agriculture involved in distributing subsidized fertilizers and agri equipment (negligible quantities of seeds occasionally supplied through CAIMA) to farmers. CAIMA in addition to supply free fertilizers received by the donors also has an exclusive budget allocated by GoN for purchasing additional fertilizers and farm implements for distribution to farmers through MINAGRI. The overall objective is to increase agricultural productivity and food self-sufficiency in Niger.

Objectives of CAIMA

Respond to farmer demand for fertilizer not reached by donors, NGOs or the private sector.

Ensure the quality of fertilizer products distributed through CAIMA. Making fertilizer available throughout all the regions of the country. Sell fertilizers at an affordable price to farmers by distributing at subsidized rates.

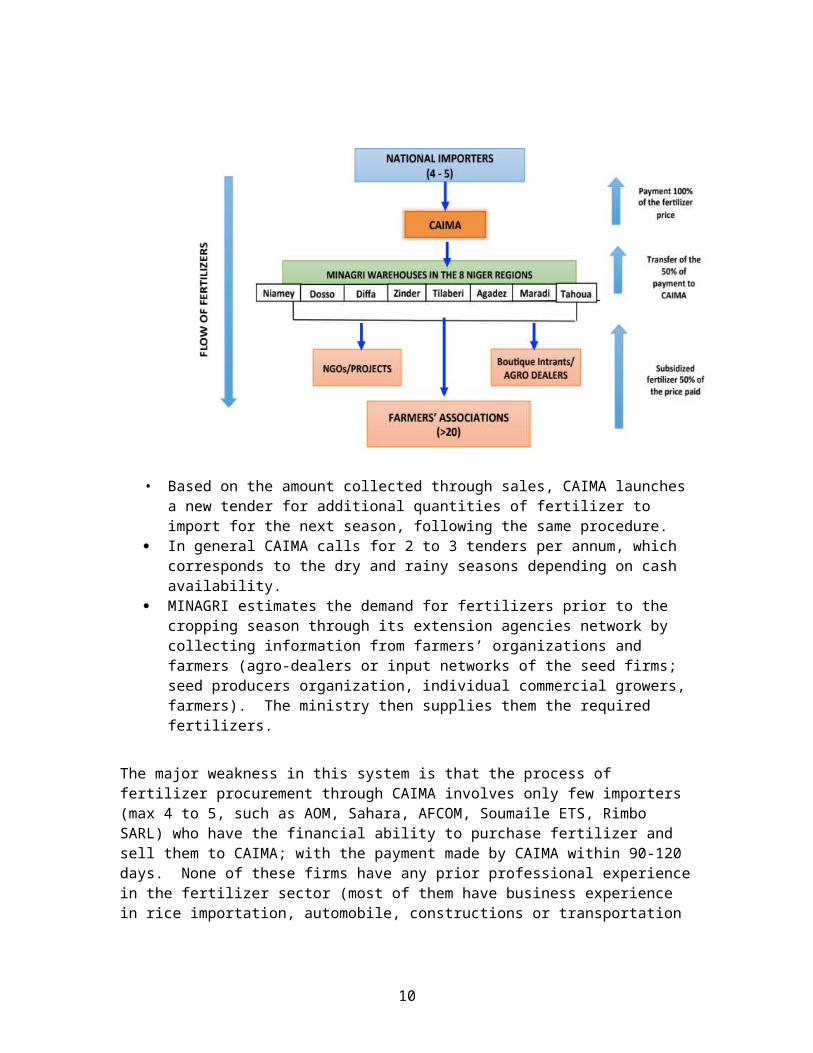

In the CAIMA mechanism, CAIMA plays a central role both as purchaser and distributor of fertilizer for the whole country. The flow of the fertilizer supply chain is as described in Figure 2 below.

CAIMA purchases fertilizer through a national tender system, which allows only the participation of firms that are registered and that pay taxes in Niger – (mostly allows only citizens of Niger).

• CAIMA receives fertilizers from the selected importers according to the budget allocated by the Ministry of Finance.

Upon importation, CAIMA distributes the fertilizer to central warehouses located in the 8 regions of Niger.

Based on demand expressed by each region, fertilizers are further distributed through village administration offices or farmers associations or different donor sponsored or

5

government aided projects (refer to figure below) by MINAGRI. At present 288 warehouses are identified as retail selling points in the country.

MINAGRI agents from regional centers sell the fertilizer at subsidized prices and transfer the money to CAIMA

Figure 2 Existing System for Fertilizer importation and distribution in Niger

• Based on the amount collected through sales, CAIMA launches a new tender for additional quantities of fertilizer to import for the next season, following the same procedure.

In general CAIMA calls for 2 to 3 tenders per annum, which corresponds to the dry and rainy seasons depending on cash availability.

MINAGRI estimates the demand for fertilizers prior to the cropping season through its extension agencies network by collecting information from farmers’ organizations and farmers (agro-dealers or input networks of the seed firms; seed producers organization, individual commercial growers, farmers). The ministry then supplies them the required fertilizers.

The major weakness in this system is that the process of fertilizer procurement through CAIMA involves only few importers (max 4 to 5, such as AOM, Sahara, AFCOM, Soumaile ETS, Rimbo SARL) who have the financial ability to purchase fertilizer and sell them to CAIMA; with the payment made by CAIMA within 90-120 days. None of these firms have any prior professional experience in the fertilizer sector (most of them have business experience in rice importation, automobile, constructions or transportation businesses and often view the fertilizer import as a business opportunity with minimum or no risk).

6

2.2 Fertilizer pricing under CAIMA

As stated above, each year the GoN budget allocates a certain budget to CAIMA to purchase fertilizers for distribution. The amount of fertilizer to be purchased through imports is decided based on the demand estimates for the fertilizer requirement collected by the Ministry of Agriculture (MinAgri). The MinAgri extension services network estimates the demand for fertilizers prior to the cropping season by collecting information from farmers’ organizations, seed firms, seed producers’ organizations, individual commercial growers and commercial farmers. Based on such estimates, the Ministry of Finance allocates a certain amount of funding for fertilizer purchases. The Ministry of Agriculture also decides the level of subsidy and the amount of fertilizer to be imported each year. It should be noted that the government of Niger (GoN) has kept the fertilizer subsidy at the same price i.e. 13,500 FCFA/50 kg bag since CAIMA started its operations in 2011. During the year 2013, CAIMA wanted to increase the fertilizer prices but it was prevented from doing so due to farmer protests. The subsidized price remains the same for all fertilizer products irrespective of their formulations (Urea, DAP, NPK) and without regard to transportation costs which may vary significantly across all 8 regions of Niger.

Payment to importers: CAIMA pays the fertilizer suppliers-importers between 1 to 4 months after fertilizer delivery. Currently only 4 or 5 firms supply fertilizers to CAIMA. From our discussions it was evident that these importers have sufficient financial strength to invest in the fertilizer importation business with less or no risk involved and they are able to make sufficient returns on this short-term investment. All the importers were satisfied with CAIMA on their terms of payment and did not have any complaints.

Payment for End users: Basically CAIMA sells all the imported fertilizer through farmers’ associations, projects sponsored by different NGOs and donors mainly to avoid engaging in a multiplicity of sales closer to a retail sales operation. Under this agreement, from the farmers’ associations or NGOs/donor projects, CAIMA can request a down payment of 50 % at delivery time and the remaining is collected at the harvest (3 to 5 months after the delivery). For regular and trusted clients a 100% cash payment can be agreed to by CAIMA. The individual farmers or small clients, who are not covered during the demand estimation time, but in need of fertilizer, can pay cash and register through their associations.

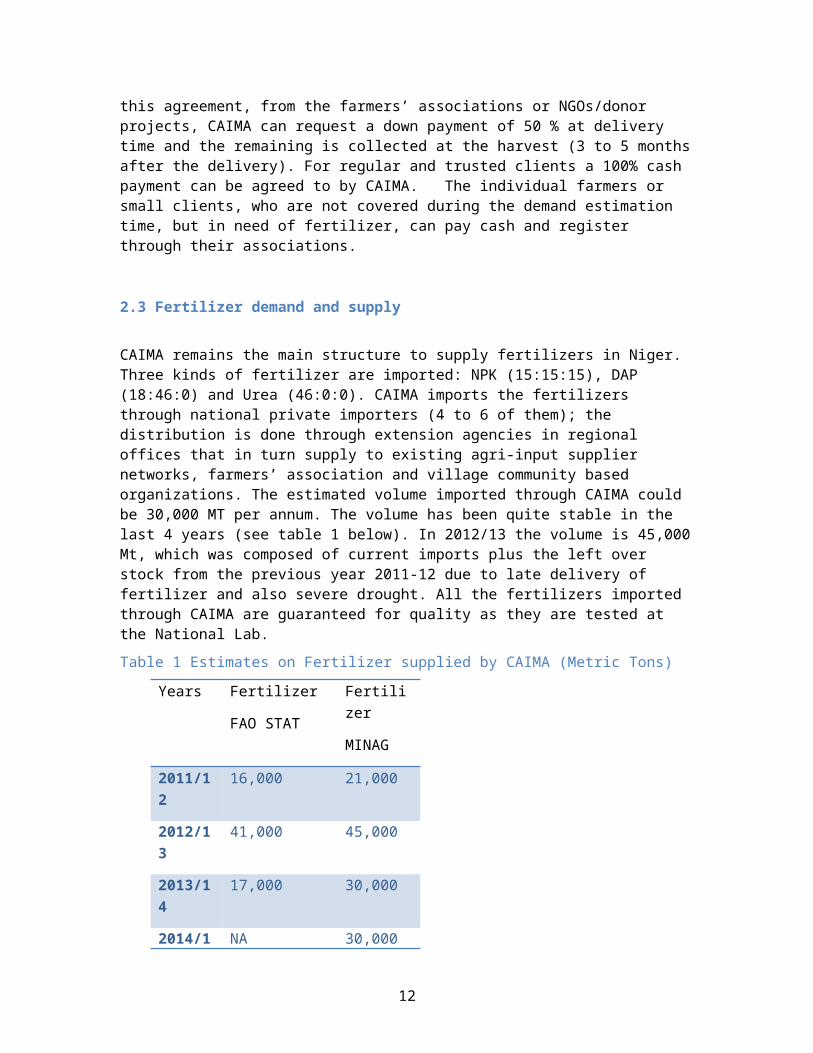

2.3 Fertilizer demand and supply

CAIMA remains the main structure to supply fertilizers in Niger. Three kinds of fertilizer are imported: NPK (15:15:15), DAP (18:46:0) and Urea (46:0:0). CAIMA imports the fertilizers through national private importers (4 to 6 of them); the distribution is done through extension agencies in regional offices that in turn supply to existing agri-input supplier networks, farmers’ association and village community based organizations. The estimated volume imported through CAIMA could be 30,000 MT per annum. The volume has been quite stable in the last 4 years (see table 1 below). In 2012/13 the volume is 45,000 Mt, which was composed of current imports plus the left over stock from the previous year 2011-12 due to late delivery of fertilizer and also severe drought. All the fertilizers imported through CAIMA are guaranteed for quality as they are tested at the National Lab.

Table 1 Estimates on Fertilizer supplied by CAIMA (Metric Tons)

Years Fertilizer Fertilizer

7

FAO STAT MINAG

2011/12 16,000 21,000

2012/13 41,000 45,000

2013/14 17,000 30,000

2014/15 NA 30,000

Source(s): MINAGRI (2016) and FAOSTAT (2016)

The fertilizer market in Niger is very small. Currently crops grown in the irrigated regions of Maradi, and Tilaberi consume most of the fertilizers –mostly for cash crops such as souchet, irrigated rice, vegetables, and onion.

2.4 Non – CAIMA fertilizer sources through cross-border trade

In addition to fertilizers supplied through CAIMA, a few private traders also import fertilizers in small quantities from Nigeria, and sell fertilizers to smallholder farmers who grow vegetables and souchet and other cash crops. These small fertilizer trades occur especially in specific areas closer to Nigeria border – Maradi and Konni areas. It is estimated that nearly 2,500-3,000 Mt of fertilizers are exchanged through non-CAIMA sources per season. However these markets thrive because of small and medium sized growers who purchase fertilizers directly from local markets and not through any organizations or pre-determined demand sources.

Fertilizers are imported from other neighboring countries by the local traders – from Benin, Burkina Faso, Togo and Nigeria who have input subsidy programs in place and as a result, lower prices than Niger –(e.g. the fertilizers from Benin are sold in Niger markets for as low as 11,000 FCFA/bag or 2,500 FCFA less than CAIMA prices). The price difference between fertilizers marketed under the Niger subsidy program and those in neighboring countries which also have subsidy programs, combined with delays in the supply of fertilizers through CAIMA during the planting season, provides a business opportunity for private traders to thrive in the market by offering lower prices and more convenient availability. The existing Niger fertilizer prices are relatively higher even after the CAIMA subsidy than prices in neighbouring countries (discussed in detail in the following section). Additionally the shortage of fertilizer that is often created by poor timing of the tenders and purchases made by CAIMA, allows some private sector firms (though not fertilizer professionals) to exploit a fertilizer business opportunity and import fertilizer from Nigeria, Togo or Ghana at a competitive price compared to the CAIMA-subsidized fertilizer. The private traders also import and sell fertilizers in small bags or quantities in local markets to smallholders, which may not be possible through CAIMA. During our interviews with fertilizer importers and suppliers it was evident that some traders also create artificial deficits in the market during the planting season, so that they can sell the fertilizers at a much higher price than CAIMA prices. A few traders also highlighted the fertilizer quality differences i.e., the fertilizers imported through private traders from other countries often have quality issues and there are instances of ‘under weighed bags’ of fertilizers.

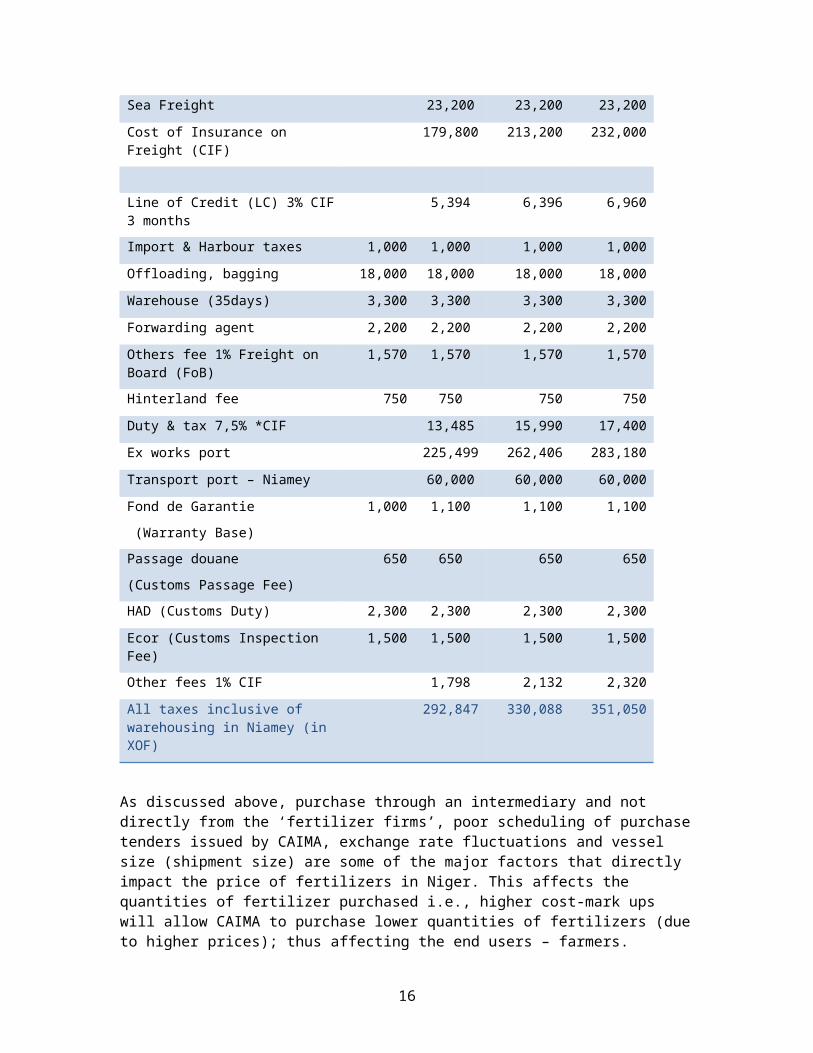

2.5 Fertilizer cost build- ups

It is always tricky to estimate the cost of fertilizers and make a comparison with the ground reality for several reasons. Exchange rate, raw materials are purchased from the international

8

market in US Dollars and the product is sold in the West African Francs i.e., XOF. The daily or monthly exchange rate fluctuations also impact the fertilizer prices up to 5 to 7%. For e.g. the exchange rate for the US dollar equivalent on February 8th, 2015 was $1 = XOF 572; the exchange rate on March 16 was $1 = XOF 620 (+ 8,4% increased).

Besides the variation of the final price of fertilizer also depends on the number of intermediaries along the fertilizer supply chain and it is safe to say that the number of intermediaries is high and there are a number of costs that accrue to fertilizer as it moves to the market in Niger that cause prices to be abnormally high by world market standards. . In the case of Niger, no importers purchase their fertilizer on the international market. They often purchase the fertilizer from ‘other importers’ located in and around the ports. The importers located in the ports of other countries would have already paid the applicable taxes, tariffs or duties for the specific country in which the product was purchased. Since the importers who supply the product to importers from Niger have already paid these taxes, the costs of acquisition of fertilizer to sell in Niger is marked up by the cost of these taxes and duties. At this stage the taxes paid through the source importers located in other country ports are not reimbursable, and so this cost is embedded into the suppliers’ cost to for brining fertilizer into the Niger market. Besides, Niger importers also have to pay the taxes, duties or tariffs that are applied to fertilizers in order to comply with Niger’s regulations. Furthermore, prices tend to be high as a result of shipments to West African ports on smaller vessels which also impacts the sea freight charges, as do unloading and demurrage charges that are often incurred in these ports.

All the above issues highlight the need for the scheduling of fertilizer tenders by CAIMA on time, allow the importers to negotiate for the best fertilizer prices from the suppliers, in terms of taxes, cutting down other costs and shipment size. However one should note that in the existing system, fertilizer importation is handled through unprofessional business people, who have little or no experience in handling fertilizers. Clearly the system could be streamlined by delivering the existing quantities of imports through professionals who can negotiate for better fertilizer prices based on international prices.

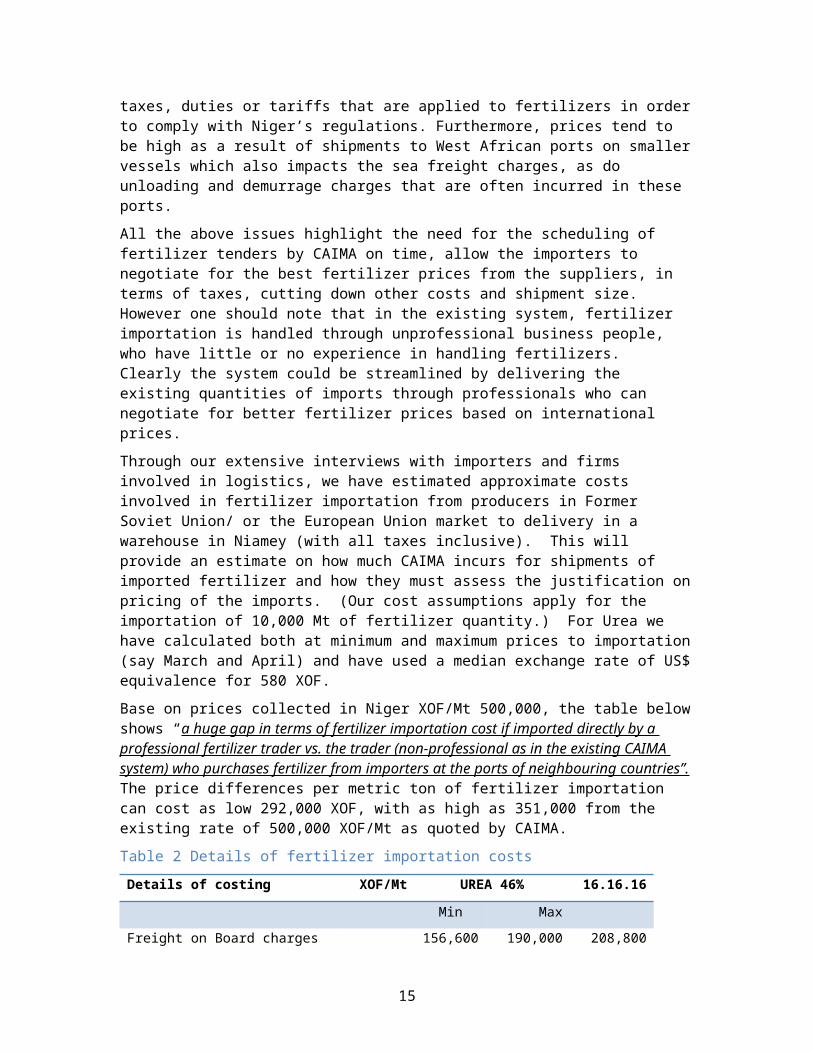

Through our extensive interviews with importers and firms involved in logistics, we have estimated approximate costs involved in fertilizer importation from producers in Former Soviet Union/ or the European Union market to delivery in a warehouse in Niamey (with all taxes inclusive). This will provide an estimate on how much CAIMA incurs for shipments of imported fertilizer and how they must assess the justification on pricing of the imports. (Our cost assumptions apply for the importation of 10,000 Mt of fertilizer quantity.) For Urea we have calculated both at minimum and maximum prices to importation (say March and April) and have used a median exchange rate of US$ equivalence for 580 XOF.

Base on prices collected in Niger XOF/Mt 500,000, the table below shows “a huge gap in terms of fertilizer importation cost if imported directly by a professional fertilizer trader vs. the trader (non-professional as in the existing CAIMA system) who purchases fertilizer from importers at the ports of neighbouring countries”. The price differences per metric ton of fertilizer importation can cost as low 292,000 XOF, with as high as 351,000 from the existing rate of 500,000 XOF/Mt as quoted by CAIMA.

Table 2 Details of fertilizer importation costs

Details of costing XOF/Mt UREA 46% 16.16.16

Min Max

Freight on Board charges 156,600 190,000 208,800

Sea Freight 23,200 23,200 23,200

9

Cost of Insurance on Freight (CIF) 179,800 213,200 232,000

Line of Credit (LC) 3% CIF 3 months 5,394 6,396 6,960

Import & Harbour taxes 1,000 1,000 1,000 1,000

Offloading, bagging 18,000 18,000 18,000 18,000

Warehouse (35days) 3,300 3,300 3,300 3,300

Forwarding agent 2,200 2,200 2,200 2,200

Others fee 1% Freight on Board (FoB) 1,570 1,570 1,570 1,570

Hinterland fee 750 750 750 750

Duty & tax 7,5% *CIF 13,485 15,990 17,400

Ex works port 225,499 262,406 283,180

Transport port – Niamey 60,000 60,000 60,000

Fond de Garantie

(Warranty Base)

1,000 1,100 1,100 1,100

Passage douane

(Customs Passage Fee)

650 650 650 650

HAD (Customs Duty) 2,300 2,300 2,300 2,300

Ecor (Customs Inspection Fee) 1,500 1,500 1,500 1,500

Other fees 1% CIF 1,798 2,132 2,320

All taxes inclusive of warehousing in Niamey (in XOF)

292,847 330,088 351,050

As discussed above, purchase through an intermediary and not directly from the ‘fertilizer firms’, poor scheduling of purchase tenders issued by CAIMA, exchange rate fluctuations and vessel size (shipment size) are some of the major factors that directly impact the price of fertilizers in Niger. This affects the quantities of fertilizer purchased i.e., higher cost-mark ups will allow CAIMA to purchase lower quantities of fertilizers (due to higher prices); thus affecting the end users – farmers.

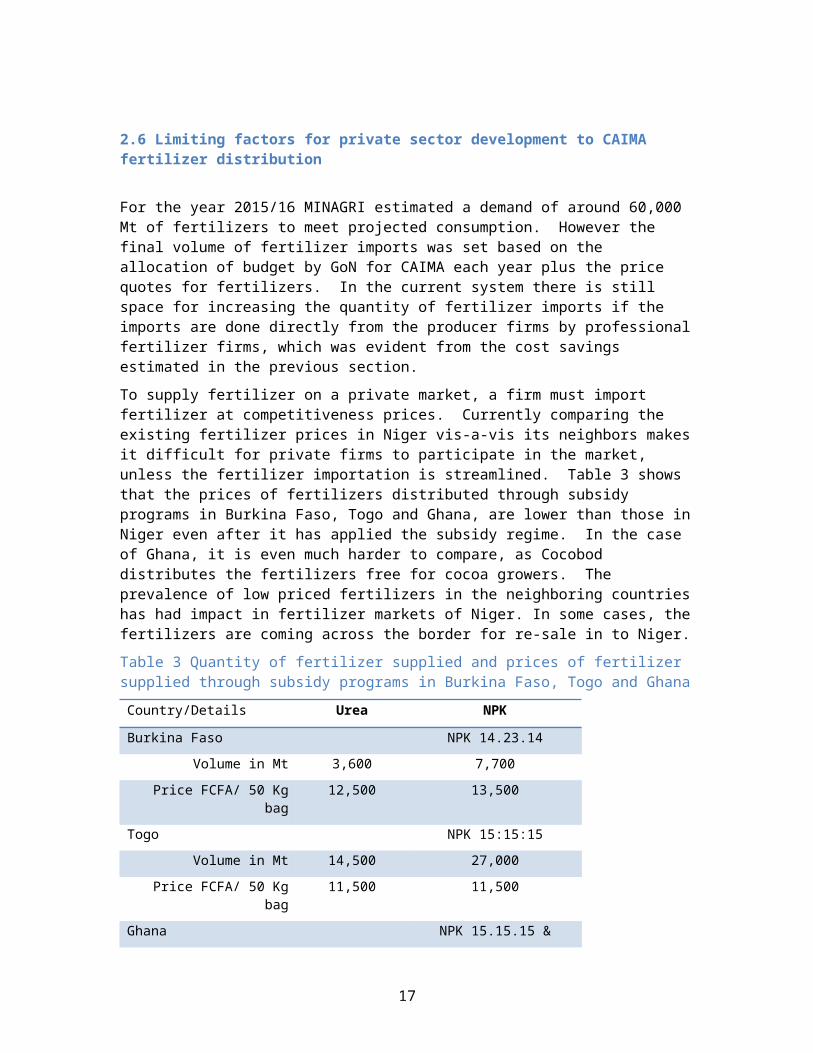

2.6 Limiting factors for private sector development to CAIMA fertilizer distribution

For the year 2015/16 MINAGRI estimated a demand of around 60,000 Mt of fertilizers to meet projected consumption. However the final volume of fertilizer imports was set based on the allocation of budget by GoN for CAIMA each year plus the price quotes for fertilizers. In the current system there is still space for increasing the quantity of fertilizer imports if the imports are done directly from the producer firms by professional fertilizer firms, which was evident from the cost savings estimated in the previous section.

10

To supply fertilizer on a private market, a firm must import fertilizer at competitiveness prices. Currently comparing the existing fertilizer prices in Niger vis-a-vis its neighbors makes it difficult for private firms to participate in the market, unless the fertilizer importation is streamlined. Table 3 shows that the prices of fertilizers distributed through subsidy programs in Burkina Faso, Togo and Ghana, are lower than those in Niger even after it has applied the subsidy regime. In the case of Ghana, it is even much harder to compare, as Cocobod distributes the fertilizers free for cocoa growers. The prevalence of low priced fertilizers in the neighboring countries has had impact in fertilizer markets of Niger. In some cases, the fertilizers are coming across the border for re-sale in to Niger.

Table 3 Quantity of fertilizer supplied and prices of fertilizer supplied through subsidy programs in Burkina Faso, Togo and Ghana

Country/Details Urea NPK

Burkina Faso NPK 14.23.14

Volume in Mt 3,600 7,700

Price FCFA/ 50 Kg bag 12,500 13,500

Togo NPK 15:15:15

Volume in Mt 14,500 27,000

Price FCFA/ 50 Kg bag 11,500 11,500

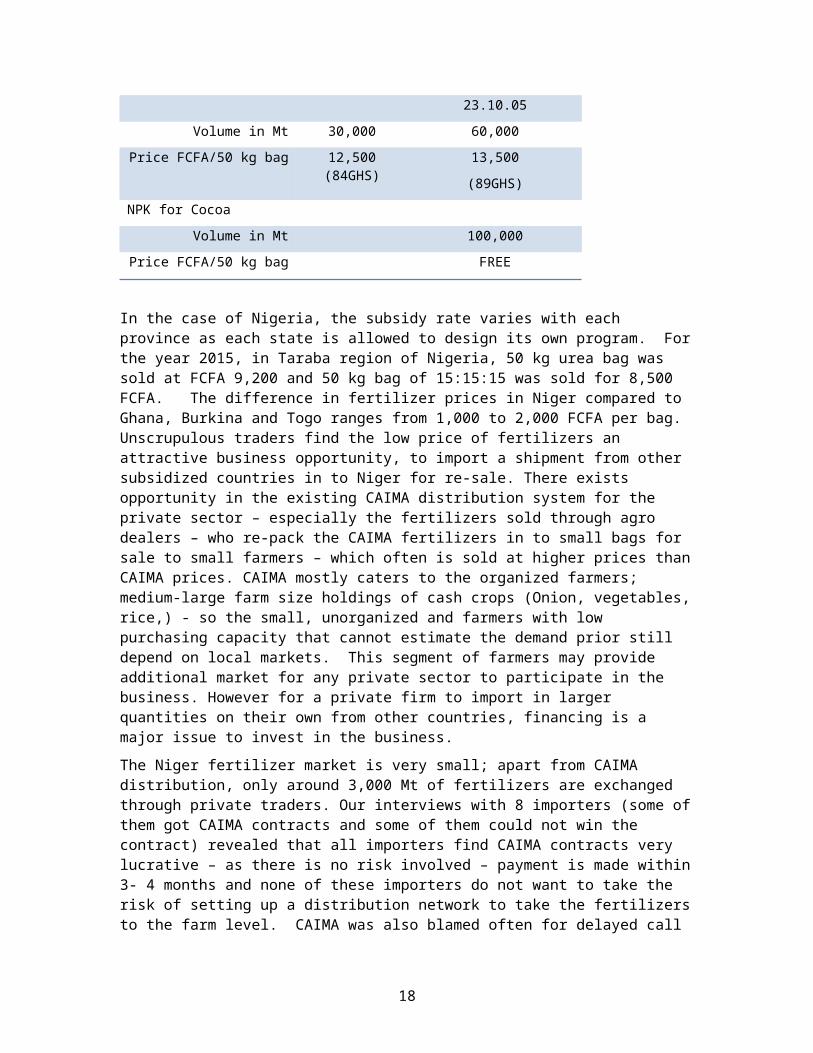

Ghana NPK 15.15.15 & 23.10.05

Volume in Mt 30,000 60,000

Price FCFA/50 kg bag 12,500 (84GHS) 13,500

(89GHS)

NPK for Cocoa

Volume in Mt 100,000

Price FCFA/50 kg bag FREE

In the case of Nigeria, the subsidy rate varies with each province as each state is allowed to design its own program. For the year 2015, in Taraba region of Nigeria, 50 kg urea bag was sold at FCFA 9,200 and 50 kg bag of 15:15:15 was sold for 8,500 FCFA. The difference in fertilizer prices in Niger compared to Ghana, Burkina and Togo ranges from 1,000 to 2,000 FCFA per bag. Unscrupulous traders find the low price of fertilizers an attractive business opportunity, to import a shipment from other subsidized countries in to Niger for re-sale. There exists opportunity in the existing CAIMA distribution system for the private sector – especially the fertilizers sold through agro dealers – who re-pack the CAIMA fertilizers in to small bags for sale to small farmers – which often is sold at higher prices than CAIMA prices. CAIMA mostly caters to the organized farmers; medium-large farm size holdings of cash crops (Onion, vegetables, rice,) - so the small, unorganized and farmers with low purchasing capacity that cannot estimate the demand prior still depend on local markets. This segment of farmers may provide additional market for any private sector to participate in the business. However for a private firm to import in larger quantities on their own from other countries, financing is a major issue to invest in the business.

The Niger fertilizer market is very small; apart from CAIMA distribution, only around 3,000 Mt of fertilizers are exchanged through private traders. Our interviews with 8 importers (some of them got CAIMA contracts and some of them could not win the contract) revealed that all

11

importers find CAIMA contracts very lucrative – as there is no risk involved – payment is made within 3- 4 months and none of these importers do not want to take the risk of setting up a distribution network to take the fertilizers to the farm level. CAIMA was also blamed often for delayed call for tender and its processing as well delayed supply of fertilizers to the end users.

The main constraints to developing a professional fertilizer private sector in Niger are:

Only cash crops consume fertilizer, which represent a small market (rice, onion, souchet and vegetables).

In addition CAIMA mostly caters to the organized farmers; medium-large farm size holdings of cash crops (Onion, vegetables, rice,). The small, unorganized farmers with low purchasing capacity still depend on local private markets. This segment of farmers is very difficult to target by the private firms.

There is no control or quality assurance of the fertilizer entering via the private sector, hence the end user is very skeptical about the quality of the non CAIMA fertilizers.

Access to credit for the private fertilizer firm is difficult to obtain due to lack of collateral.

Fertilizer business operation in Niger is very seasonal, extensive coverage required to meet the small demand – efficiency of the market is very poor.

Unfair price competition with subsidized fertilizer prices in Niger vs. neighboring countries.

There are no incentives extended from CAIMA to support private firms to import additional volume of fertilizers and use the MINAGRI distribution network.

2.7 How to stimulate the private sector development in fertilizer market of Niger?

Despite the fact that the Niger fertilizer market as such is very small, which is around 30,000 MT, some actions can be taken to address the challenges faced by the private sector.

Operating in all the 8 regions of the country, CAIMA has played a crucial role in improving the awareness of fertilizer use in the country at large and ensure quality of fertilizer. However the operational effectiveness of CAIMA could be improved further through effective private sector participation – improved competitive markets and technology transfers.

12

3. The seed value chain in Niger

The current seed sector development policy in Niger is related to the major agricultural development thrusts as initiated through the Government of Niger’s ambitious agricultural transformation plan called the 3N Initiative – Nigeriens Nourish Nigeriens since 2012. The program emphasizes food security through intensified production and the organization of the rural areas through government initiatives; and enhancing the role of the private sector and its independent economic operators through processes of liberalization and privatization.

The current institutional structure of Niger seed system includes two components viz., public and private sector. Under the current system the public sector (the service component) is responsible for research, production of breeder and foundation seeds (early generation seeds), legislation and extension, certification and quality control and the private sector is involved in operationalizing seed related activities such as multiplication of foundation seeds, distribution and marketing. The GoN approved the “Bill on Seed Plant” in 2013, and further passed the seed law with provisions for seed regulations in 2014. This enabled to an extent re-structuring the seed activities performed through public and private entities, providing more provisions for private sector participation and public-private partnership mechanisms.

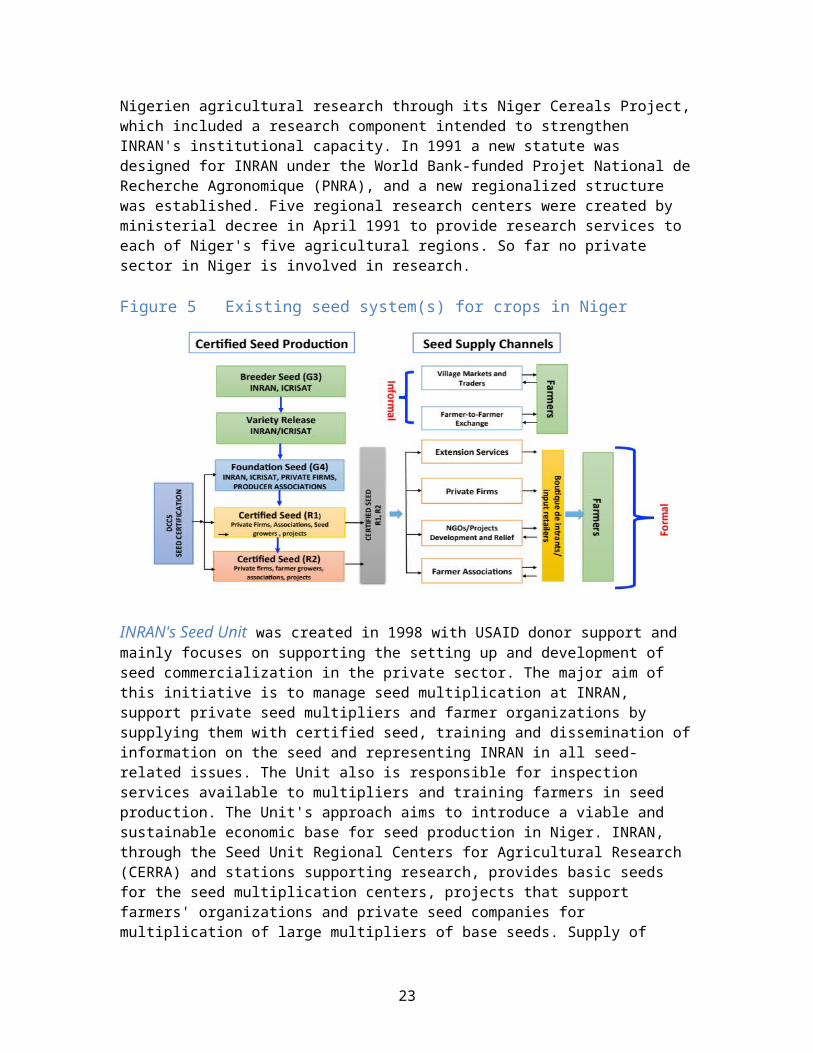

Figure 4 Public and private sector role(s) in the current seed systems in Niger

The seed value chain in Niger further could be distinguished in to actors involved in activities of seed research, seed production i.e., certified seed production vs. actors in seed supply (Fig). These channels comprise representatives of seed producers and farmer organizations, private seed firms, project (s) by donors and implemented through different NGOs, seed input shops – Boutique d’intrants, grain traders and farmers. The seed produced could be further divided in to formal and informal depending on their seed supply mechanisms. Formal systems comprise of formal actors, includes research, certified seed producers, and formal seed distributors such as projects, extension, associations, and private firms. The seeds exchanged through informal, mostly not certified and either exchanged through local markets or among farmers in their own communities, outside the formal sphere systems of operations.

In Niger less than 15 % of the seeds are supplied through formal system and the rest are through informal exchanges and own saved seeds. Though the figure below represents the general value chain for seeds of all field crops in Niger, actors vary across crops, especially towards supply. For e.g. for rice the foundation (pre-basic/basic seeds) are produced by INRAN and further multiplied through a farmer’s cooperative ‘Sadia cooperative rice farm’ and distributed through FUCOPRI – the rice growers association. Apart from Sadia, only two other private firms have been involved in producing certified seeds (HALAL and AINOMA) since 2013-14 seasons. In vegetables, private firms or projects distribute seeds directly to farmers, most of which are imported. The seeds of onion, the major cash crop of Niger are mostly planted through bulbs – either through farmer exchanges and only less than 1% of farmers purchase seeds imported from European countries and sold in Niger markets.

Breeding, variety release,

certification, quality control

PUBLIC

Foundation seed production & distribution

PUBLIC & PRIVATE

Commercial seed multiplication

PRIVATE

Commercial seed quality control

PUBLIC

Processing, marketing and

distribution

PRIVATE AND PUBLIC

13

3.1 Seed research, certification and quality control activities

Institut National de Recherches Agronomiques du Niger (INRAN) Following its independence in 1960, Niger's agricultural research system focused on principal crops like cotton, groundnut, and oil palm. But in the mid 1970s the emphasis of research system was shifted to millet and sorghum due to 1972-74 droughts and subsequent nationalization of the agricultural research in Niger. Food crops thus became the focus of research. Local variety breeding is done primarily by the Institut National de Recherches Agronomiques du Niger (INRAN), created in 1975, the International Crops Research Institute for the Semi Arid Tropics (ICRISAT Sahelian Center), and to a lesser extent by scientists at the Abdou Moumouni University of Niamey (UAM: Faculty of Agronomy, Faculty of Sciences, Institute of Radio Isotopes). In the mid-1970s, as French researchers left the system, USAID became involved in Nigerien agricultural research through its Niger Cereals Project, which included a research component intended to strengthen INRAN's institutional capacity. In 1991 a new statute was designed for INRAN under the World Bank-funded Projet National de Recherche Agronomique (PNRA), and a new regionalized structure was established. Five regional research centers were created by ministerial decree in April 1991 to provide research services to each of Niger's five agricultural regions. So far no private sector in Niger is involved in research.

Figure 5 Existing seed system(s) for crops in Niger

INRAN's Seed Unit was created in 1998 with USAID donor support and mainly focuses on supporting the setting up and development of seed commercialization in the private sector. The major aim of this initiative is to manage seed multiplication at INRAN, support private seed multipliers and farmer organizations by supplying them with certified seed, training and dissemination of information on the seed and representing INRAN in all seed-related issues. The Unit also is responsible for inspection services available to multipliers and training farmers in seed production. The Unit's approach aims to introduce a viable and sustainable economic base for seed production in Niger. INRAN, through the Seed Unit Regional Centers for Agricultural Research (CERRA) and stations supporting research, provides basic seeds for the seed multiplication centers, projects that support farmers' organizations and private seed companies for multiplication of large multipliers of base seeds. Supply of basic seeds is often reported to fall short for producing large seed quantities of certified R1 and R2 seed categories. This deviation is

14

primarily due to financial constraints of the centers. In the current scheme, INRAN and ICRISAT both provide basic seeds for multiplication of foundation seeds through private firms, farmers associations and few donor funded projects.

Direction du controle et de la certification des semences (DCCS) previously - Service des Intrants de Controle et de Conditionment et Legislation d’Agricole (SICCLA) The Input Control, Seed Certification and seed legislation are handled through SICCLA, currently known as DCCS since December 2013, after constituting a new seed legislation. This agency is also responsible for monitoring the production and commercialization of seed in Niger. SICCLA was formed in 1990 out of the former National Seed Service of Niger. SICCLA was one of four departments of the Directorate of Agriculture. The functions include the collection and management of statistical data on seed production activities; enacting the seed laws related to seed quality and enforcement; training of seed personnel (inspectors) and monitoring the seed production programs implemented by seed centers and private producers. DCCS is directly involved in certifying seeds produced INRAN seed centers, and also offers certification services at a fee to private seed companies, and private seed producers at a nominal fee.

DCCS manages six regional seed farms for the production of foundation and certified seeds and a national laboratory for quality control and certification. There are a total of six seed farms of 60 hectares each for the production of basic and pre-basic seed. They are located in different regions including Lossa, Hamdallaye, Guéchémé, Doukou Doukou, Kouroungoussaou and Angoual Gamji. Each center has appropriate land and some of them also have irrigation facilities for seed production. They are also equipped with facilities for cleaning and storing seed. These centers are open to private producers on a contract basis. Seed produced at Lossa include cowpea, millet, sorghum and sesame. Foundation seed for multiplication usually comes from INRAN, though DCCS centers also produces some foundation seed. Further multiplication involves seed inspection, consisting of three field visits plus laboratory tests for germination and purity.

3.2 Seed multiplication activities

The certified seeds in Niger are produced by 4 major actors viz., private seed producers includes individual seed producers, farmer organizations; private seed firms (14 firms) who multiply seeds through contract farmer growers or in their own farm; the donor projects who also contract farmers to multiply seeds through different programs and FAO - international organization involved directly in seed multiplication activities through their community seed initiatives in collaboration with GoN. Almost 80-85 % of the certified seeds produced are distributed as ‘ free’ either through FAO, other donor funded projects or through government programs. Less than 10 % of the seeds multiplied by these actors – primarily by private seed firms are sold directly to farmers for cash.

15

Figure 5 Proportion (%) of certified seeds multiplied by seed stakeholders in in Niger

2010/11 2011/12 2012/13 2013/14 2014/150

10

20

30

40

50

60

70

80

90

100

FAO

Projects/NGOs

Private Firms

Private producers

Pro

por

tion

of C

S b

y se

ed a

ctor

s (%

)

Farmer seed producers/organizations Due to various seed based interventions in Niger since the late 1980s, the local capacity for seed production has increased over the years, usually through seed groups or cooperatives in various locations. Well-known seed producer groups includes Maïzabi (Saé Saboua (Maradi), Madaoua), Guidan Iddar (Konni), Tchiaguiriré (Kollo) and Tamou (Say) produce pearl millet, sorghum, groundnut and cowpea seed, Federation of rice producers cooperative union (FUCOPRI) in the Niger River Valley for rice seeds. In Guidan Iddar, Tchiaguiriré and the irrigated areas around Djirataoua, Galmi, Mouléla, Konni and Diffa, production of hybrid seeds of sorghum and maize by farmer cooperatives has clearly shown the technical feasibility of modern seed multiplication by local producers. Whilst the farmers belonging to seed groups or cooperatives have considerable skills in producing high quality seeds under favorable conditions, they remain completely dependent on donor-funded projects to find buyers for the seed produced. Where such support is lacking, farmers are unable to sell their seed, and production often ceases the following year. As such, the infrastructure created for seed production is often defunct or not functioning to its full capacity.

The seed producer organizations in Niger currently produce seeds for FAO, government, private firms and other donor projects. A regional committee headed by the regional governor and consisting of representatives from Regional Agricultural Department (DRDA) and all department heads from the Ministry of Agriculture play a key role in setting seed prices for producers. Quality control is the responsibility of the Seed Certification and Quality Control Department (DCCS) (previously SICCLA) and the regional committee. The farmer seed producer organizations are also involved extensively in the multiplication of certified seeds (R1 and R2) and also few organizations such as Moriben, FESA/SARL, FUBI also produce foundation seeds for millets (G4).

Private Seed Firms The private sector channels involvement in Niger seed sector emerged after the liberalization of input sector in the late 80’s with pressure from the World Bank. Initially the private sector traders operated by importing fertilizers and vegetable seeds to be sold in the local markets, located mainly in and around irrigated and vegetable production areas. There were few formal structures initiated by AGRIMEX (an input firm), and MANOMA (a private cooperative)

16

in the late 90s and early 2000 to operate as full fledged agri input distribution firms – that sell mainly imported vegetable seeds, pesticides and small farm implements.

With INRAN facing shortage of funds for seed production activities, and also the demand for good quality seeds, especially during and after disasters, the GoN decided to involve private growers, farmer associations and firms in the multiplication of field crop seeds for distribution to INRAN, and other government programs since mid 2000. Currently there are 14 registered private firms in 8 regions of Niger, who are involved in multiplication and distribution of seeds in the country. Of the 14 private firms, Alheri is the only seed firm with warehousing and seed processing facilities in entire Niger.

Table 4 Existing registered private seed firms in Niger (2014/15)

Registered Firms Start year

Location

1 Enterprise Alheri 2012 Doutchi2 Cigaban karkara 2013 Madoua3 Enteprise Nagarta IRI-SARL 2011 Maradi4 F S Amintchi 2011 Gucheme5 Enterprise Tatache IRI 2013 Madaoua6 F S Amathe 2010 Maradi7 Ferme Semenciere AINOMA 2006 Niamey8 Enterprise HUSA'A 2010 Dosso9 SMS IRI NAGARI 2013 Madaoua

10 Enteprise GAOH YBZ 2008 Niamey11 Enteprise Agricole Alfarey

Masaada2013 Dosso

12 Enterprise Tanadin Iri NA NA13 Enterprise Halal 2012 Maradi14 Enterprise Haraibane 2012 Wankame

Of the 14, 8 firms are involved in multiplication of certified seeds (R1 and R2) and 4 firms (Alheri, Husa, AINOMA and Halal) are involved in the production of foundation seeds of millet, sorghum, cowpea and groundnut (G4), producing nearly 15 % of foundation seeds. Since 2010, private firms produce 20 % of the total certified seeds. They are primarily involved in multiplication of millet, sorghum, cowpea, groundnut, maize, sesame and vegetables (okra, moringa). Seed is mostly purchased by projects within the Ministry or by FAO and NGOs, often for emergency seed distribution projects.

The major market for private firm seeds is government (50-55%); project of NGOs (donor funded) constitute early 30-35 % and seed sales through input outlets and directly to farmers is around 10-15%. For the year 2015 cropping season, according to APPSN, of the 50 % of seeds purchased by FAO, 40 % of the seeds were procured from the private producers.

Donor or project sponsored seed multiplication/distribution (donor funded and NGOs) In addition to seed multiplication directly through firms and seed producers’ organization, multiplication activities are also sponsored through various projects on seeds through donor funds, implemented by NGOs. These projects contract either existing seed producers/organizations/ firms directly to produce seeds of certain crops to be distributed through their projects or they organize farmers towards seed multiplication. Few key projects sponsored

17

by IFAD, USAID such as PPAAO, REGIS, PAMED are multi-year, long term projects with specific seed related activities are actively involved directly in seed multiplication activities. Other projects and NGOs who are involved in certified seed multiplication activities include PASADEM, PADSR, CR, Mercy Corps etc., The NGO/donor sponsored seed multiplication (excluding contracted through private firms) comprise nearly 35 % of total seeds multiplied and distributed in Niger (National Directory on the availability of quality seeds in Niger, 2015).

3.3 Seed distribution activities

The seed market prices are not controlled by the government – to an extent its open now. Each year the Department of Agriculture (MINAGAI) purchases seeds from the private firms, producers and farmer organizations to distribute seeds ‘free’ to different locations – mostly to seed insecure and vulnerable communities. NGOs and donors through projects also distribute seeds for different projects in small quantities, mostly free and in some cases, 35-50 % subsidized rates depending on the program.

Government is the biggest market for seed producers and firms. Situation has improved in Niger with regard to ‘free’ or ‘relief seeds procurement and distribution’ since 2007-08 due to i) private sector participation – the NGO projects and donor projects procures directly from the private firms ii) the government procures ‘seeds’ directly from the private seed firms and seed producers/ organizations – quality is ensured through seed quality control and regulations.

Commercial inputs shops (Agro-dealers) Seed firms retain small stocks, depending on the season to be sold through their own outlets. 6 out of 14 private firms involved in seed multiplication also have their own seed retail outlets to enable direct seed purchases of farmers. The firms with their own retail outlets are Alheri, Husaa, Ainoma, Agrimex, FESA,Halal. For example Alheri seeds sell their seeds through 80 sales point or input outlets located in Tahoua, Dosso and Niamey; Husaa firms operates through 33 sale points in Dosso, Niamey and Tahoua and AGRIMEX operates through 20 agro-input shops in Maradi, Tahoua, Niamey and Gaya. AGRA has trained few dealers (120 dealers in 2 phases) through their agro dealer development program in eastern and western region since 2010 and in operation in Tahoua, Maradi and Zinder. For the year 2016, it is expected that 265 additional agro dealers will be trained through AGRA program on agro dealer development. The program through AGRA also encouraged establishing an agro dealer association in Niger (Association des Distributeurs des Produits Phytosanitaires du Niger (ADPHYTO)). However the association could not function as expected and it is being revived under the current management.

Community-managed input shops (Boutiques d’Intrants (BI)) The concept of community-managed input stores (Boutiques d’Intrants, BI) was initiated by an FAO project in 1999. In contrast to the concept of input banks, which were based on the distribution of free or subsidized inputs on credit, cash sales are encouraged in BI to ensure their financial security. Profit, however, is not the major motive of the BI organization, and they tend not to be run on a commercial basis. The BIs are cooperatives or associations that are autonomous, either grouped as networks, owned by producer organizations or unions or federations. Funding provided by donors through FAO provides initial capacity building and some construction materials to build a store at the community level.

The following are among the main owners of a number of input shops: Mooriben, Fédération des coopératives maraîchères du Niger (FCMN-NIYA), Dadin Karkara, Marhaba, Fédération des Unions de Boutiques d’Intrants de Zinder (FUBI), Fédération des producteurs de Tahoua

18

(FUCAP), Fédération des Unions de producteurs de Maradi (FUMA), Fédération des producteurs de Souchet SA’A, Union des Coopératives Maraîchères de l’Aïr (UCMA).

Between 1999 and 2008, the Inputs Project and partners helped to set up a number of input shops in Niger. Between 2009 and up until 2012, the Intensifying Agriculture by Strengthening Cooperative Input Shops (IARBIC) project and other rural initiatives continued to set up and rehabilitate input shops. The number of input shops has constantly grown in Niger since 1999 (the year that the Inputs Project was launched). Some 935 shops had been registered throughout the country by the close of 2014. However the evaluation of BIs in September 2015 by FAO found that only 720 shops are in operation, with 20 % or more shops are not operating due to mismanagement issues.

The BI project also trains community members in new agricultural technologies, safe handling of pesticides and how to negotiate prices, etc. The BI are designed to be self-sufficient so that they can sustain their working capital requirements as well as promote regular supply of necessary inputs on time. The major strengths of the BI program are in meeting the demand of the local communities by providing easy access to key inputs at affordable prices. In Niger, as in other countries of the Sahel, lack of availability of quality inputs in the right place, at the right time and in small packs is one of the main reasons for low levels of use. The BI inputs shops repackage inputs into small quantities (packages of 0.5 to 1 kg of fertilizers or seed) to allow farmers the purchase of quantities they can afford. Other advantages included the proliferation of various activities through BIs and their initiatives such as Farmer Field Schools, farm demonstrations, provision of timely information through rural radio and billboards, and income-generating activities such as warrantage, processing, and seed multiplication in the communities.

Grain traders (informal seed markets) Discussions with farmers and other stakeholders provided information on the exchange of planting materials through grain markets. The markets are mainly meant for grain sales but contractors for government or NGO seed projects during ‘emergency or disaster times’ come to purchase prior to the planting season for relief seed distribution due to heavy demand. The distinction between ‘grain’ and ‘seed’ was negligible and in some cases there was a slight price difference between the categories, though this does not necessarily imply any difference in quality. The traders in four major grain markets in Maradi, Zinder, Konni towns, and Serkan Haoussa are known to sell seeds during the planting season though the quality of such ‘seeds’ are often questionable.

3.4 Other seed related organizations

Seed Producers’ Association of Niger (l'Association de Producteurs Privés de Semence du Niger, (APPSN)) The Private Seed Producers' Association of Niger (l'Association de Producteurs Privés de Semence du Niger, APPSN) is a national association of private seed producers set up in 1999 on the initiative of producers interested in modern seed techniques and a professionalization of its activities. The APPSN has gradually increased its membership in the country, and it has developed a special relationship with the national authorities as far as seed distribution is concerned. Currently there are 9 private firms and 63 farmer organizations that have been the members of APPSN. The members of the association are of two types, one is a seed firm; and other type includes seed growers or farmers. The association members also represents in the current national seed committee and in varietal release committee of Niger.

Federation des Unions de Cooperatives de Producteurs de Riz (FUCOPRI) This is a rice growers federation comprising 9 unions of cooperatives and 4 unions of women parboilers, established in 2001 with 37 cooperatives and 26,691 farmers as members. The geographical coverage includes Tillabery, Dosso and Niamey – the Nile river basin. FUCOPRI is the biggest rice producers

19

association in Niger, with rice cultivation in 8,500 ha of land. They are a well-organized rice value chain taking care of both input and output end of the system. In terms of input access, particularly credit and fertilizers are channelled through CAIMA with a guaranteed credit facility. From 2012 to 2014, FUCOPRI assisted the cooperatives in purchases amounting to 9,61 tons of fertilizer, 77.7% of which was bought through partnerships with banking institutions. The cooperatives and their federation have established credibility within the Nigerien banking system. FUCOPRI’s experience shows that the existence of guaranteed market is a key success factor. The improved variety seeds of rice are obtained through Sangia seed farms by FUCOPRI, though mostly farmers use farm saved seeds for cultivation. The most popular rice varieties grown by Nigerian farmers include Gambiaca, IR varieties. FUCOPRI recommends farmers to renew their varieties every 4 years. Our discussions with FUCOPRI highlighted the need for quality seeds and new cultivars of rice to improve the productivity.

3.5 Seed market status in Niger

Currently Government programs are the major source of market for certified seeds. The Government purchases constitute 50-55% of certified seeds multiplied by various stakeholders; 35-40 % of the seeds are consumed by NGO projects funded through donors; and only 5-10 % is being ‘sold’ as seeds by firms involved in seed multiplication. The seeds purchased by government are distributed as ‘free seeds’ to different farming communities – mostly vulnerable through various development programs.

Figure 6 Quantity of Certified seed production (R1&R2) in Niger (2002/03 – 2014/15)

2002/03 2005/06 2010/11 2011/12 2012/13 2013/14 2014/15

0

2000

4000

6000

8000

10000

12000

14000

1,013 607

3,500

5,500

10,199

11,92412,719

Ton

s of

Cer

tifi

ed S

eed

s P

rod

uce

d

Source(s): National directory of seeds in Niger (2010-11 to 2014-15), MINAGRI, Niger; for 2002/03 and 2005/06 – Ministère du Developement Agricole, 2005.

3.5.1 Seed supply Currently INRAN, through the Seed Unit Regional Centers for Agricultural Research (CERRA) and stations supporting research, provides basic seeds (G3 and G4) for the seed multiplication centers, projects that support farmers' organizations and private seed companies for large-scale multiplication basic and pre-basic seeds. ICRISAT also contributes to an extent towards multiplying basic seeds through their seed production farms. Supply of basic seeds is often reported to fall short for producing large seed quantities of certified R1 and R2 seed categories. This deviation is primarily due to financial constraints of the centers.

20

The certified seed production in Niger covers cereal crops such as millet, sorghum, maize and rice; the oil seed crops of groundnut and sesame; legume crop cowpea; and vegetable seeds of moringa, okra, and pumpkin. Prior to 2010, the only formal organization that produced certified seeds for distribution was INRAN through its farmer organization and seed farms. The quantity of certified seed production was very low at the beginning of 2000 and it gradually increased to 12,000 tons of seeds for the cropping season 2014-15.

Table 6 Quantity of certified seeds (R1&R2) produced (kg) and distributed for major crops in 2011/12 and 2014/15

Crop seeds 2011-12 % to total 2014/15 % to totalMillet 4,232,400 76.3% 8,302,592 65.3%Sorghum 349,200 6.3% 1,090,295 8.6%Rice 38,400 0.7% 329,000 2.6%Maize 1,500 0.03% 8,049 0.1%Cowpea 582,400 10.5% 2,717,662 21.4%Groundnut 312,600 5.6% 243,302 1.9%

Source: National directory of seeds, MINAGRI.

The quantity of certified seeds produced vary across crops; depending on acreage and demand for seed among farmers. Among the cereal crops millet and sorghum seeds are the major seeds multiplied by all the stakeholders in the chain; followed by cowpea, groundnut, maize, rice and sesame. During the year 2014/15 cropping season, of the 12,700 tons of seeds, 8300 ton of seeds were for millet (65 % of certified seeds); followed by cowpea (21%); sorghum (9%) and the rest by all other crops. The production of rice and maize seeds have improved significantly in the recent years based on the demand and acreage under these crops. Cowpea seed requirement also have gone up substantially with more importance given to legume crop production through focused activities of donors (Gates Foundation and USAID investments). Also Niger leads the cowpea production and acreage in the West African region and there is huge potential to improve its productivity through improved seed systems and varietal use.

In order to improve the supply of quality seeds, and to achieve an increased adoption of improved varieties among farmers, since 2010 season INRAN began providing basic seeds of cowpea, millet and sorghum for multiplication through private firms, farmer associations and other projects involved in seed production. From involving as low as 20 stakeholders towards certified seed production, currently there are as many as 50 actors involved in certified seed production of major cereals, oilseeds and legume crops.

Increase in certified seed production also has significant impact in the adoption or use of improved varieties among farmers. The adoption of improved varieties have improved since early 2000; the adoption was around 4 % in 2008; 6 % in 2010/11 and currently it is around 10 -11 % among farmers (National directory of seeds in Niger, 2010 and 2015).

3.5.2 Demand for seeds From the total certified seeds produced in the country vs. the cultivated area under each crops one could estimate the coverage of certified seeds under different crops in Niger. From the table it is seen that except rice, all the other major crops have very low coverage of certified seeds. Though the certified seed usage is still higher than 2010/11 figures (in parenthesis col 5 in table), still there exists a huge potential in coverage under quality seeds.

Table 7 Estimated certified seeds coverage under various crops in Niger (2014/15)Crops Total area Certified Seeds % to total area *

21

cultivated Available Coverage Millet 7,358,242 8,302,592 830,259 11.30%

(6%)Sorghum 3,572,331 1,090,295 109,030 3.10%

(2.4%)Rice 11,016 329,000 4,113 37.30%

(5.5%)Maize 11,975 8,049 402 3.40%

(0.9)Cowpea 5,320,780 2,717,662 135,883 2.60%

(0.6%)Groundnut 778,929 243,302 4,055 0.50%Sesame 131,575 22,130 4,426 3.40%

Note: * Figures in parenthesis indicates proportional certified usage in 2010/11

Projected demand: According to MINAGRI officials, the GoN aims to achieve 30 % cultivable land under improved seeds of better varieties in the next 5 years. The official statistics of the government estimates that with existing cultivable area under various crops, the market for certified seeds are as high as 30,000 tons per year. A study conducted by IFC-World Bank in 2013 estimated based on area of cultivable land Niger needs 100,000 tons of various seeds (vs. the existing 12,750 tons). Still there is gap in supply and demand exists for high yielding and quality seeds and concerted efforts needed to the growing seed requirements in the country.

Crop- seeds of demand (in the order of purchases and seed replacement)

Farmers in Niger often save their own saved seed to use the following year, and they replace them with new purchased seed on loosing the seeds due to drought, or pest and disease problems or when their own stock is not of good quality. The seed replacement in Niger is relatively better than any other countries as Niger is vulnerable to extended drought periods (and sometimes locust damage) more often and the extent of damage is much higher. Hence farmers are forced to replace and renew their stock of seeds. The relief seeds are another mechanism through which farmers also renew their seeds, though most of the relief seed quality is of poor quality till now and becoming better due to policy measures. In general the frequency of seed replacement that farmers typically use in Niger is listed below.

Cowpea (once in 2 seasons) Millet (3-4 seasons) Rice (3-4 seasons- depending on the association requirement, only 3 varieties dominate +

few local cultivars) Groundnut (every 2 to 3 years) Sorghum (3 to 4 years) Vegetables (farmers purchase every year – seed saving is observed only in bulb crops like

Onion – due to varietal preferences, Souchet (sweet pea)Note: All seeds are OPVs (open pollinated varieties) – millet, sorghum, rice, vegetables (hybrids – farmers do purchase every year); sesame, cowpea, and groundnut.

3.5.3 Potential markets for seeds The figure below shows trends in the productivity of key crops over the last 15 years. Almost all the cereal crops exhibit low yield levels and high fluctuations in their productivity trends. The fluctuation in production, mainly for rain fed crops coincide with rainfall/drought patterns in Niger; with substantial drops in 2005, 2007 and 2010 years, due to extended drought periods. Introduction of hybrid millet, sorghum and maize and high yielding cultivars for rice would generate additional demand for seeds especially for irrigated and upland irrigated regions. Also

22

the big reduction in yields of rice and other crops are mainly due to drop in production levels rather than yield. In Niger, the area under cereal crops are expanding annually without improvement in yields – hence the increase in production is based on extensive cultivation than improved yields of the crop in question.

Figure 8 Yield of major cereal crops in Niger (2000-2014)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

SorgYieldMil Yield

Maize yld

Rice Yield

Source: FAO, 2016

Millet Hybrids: The ICRISAT/INRAN scientists have been testing 2 millet hybrids over the last few seasons and now are at the final stages of testing - at farmers’ fields. These hybrids have significant yield potential – almost doubled yields than the existing cultivars – which yield around 300-400 kg/ha under farmer’s field conditions. The hybrids also can yield heavily under minimum irrigation i.e., suitable for ‘uplands cultivation’ in the Niger River basin.

Nutritious seeds Iron-rich pearl millet is being developed using conventional breeding by the International Crops Research Institute for the Semi-Arid Tropics (ICRISAT) as part of the HarvestPlus program. The first iron-rich pearl millet variety (ICTP-8203Fe) was commercialized in 2012 in India. It also provides more zinc, is high yielding and is disease and drought tolerant. Results from a research study in India indicate that children could get their full daily iron needs from just 100 grams of this pearl millet flour. Children aged below two, who might eat less, would still benefit substantially from eating iron-rich pearl millet. Another study conducted among Benin women indicate that less than 160 grams of iron-rich pearl millet flour daily is enough to provide Beninese women aged 18-45 with more than 70 percent of their daily iron needs. ICRISAT – Sadore research center in Niger has been conducting trials in Niger with ICTP-8203Fe lines and derivatives for a proper selection of suitable cultivars. Pearl millet is grown extensively in around 7.5 million hectares in Niger. The area under pearl millet has been almost steady in Niger compared to other countries in the region due to strong preference of Nigerians towards millet consumption. The opportunity to multiply and distribute seeds of enriched pearl millet and coverage under improved seeds will not only improve the production but improves the ‘nutritional security’ of the households. In the recently concluded field days for stakeholders in Sadore, ICRISAT introduced participants for high iron content pearl millet cultivars (iniari type). The phenotypic performance of recently introduced biofortified (high-iron) pearl millet variety ICTP 8203 and new single-cross hybrids ICMH IS 14002 and ICMH IS 14012 were great attractions to private firms and farmers. The Harvest Plus and ICRISAT are planning to further advance the trials of Iron rich pearl millet cultivars suitable for Niger and other countries in the region from 2016 season.

According to scientists from ICRISAT and INRAN, with better seed quality and crop management practices the pearl millet yields could be improved to 1.5 to 2 tons/hectare. The existing cultivars are OPVs (open pollinated) and there exists a huge potential for introducing

23

pearl millet hybrids in to the system. The demand for such hybrids will be higher among farmers for two reasons; 1) the quality of hybrid seeds are very high, with great vigor – the seed rate requirement is very low (requires only 3-4 kg/ha vs. 15 kg/ha with repeated sowing); 2) Millet being the staple food crop and most of the cultivable (rainfed) land is now locked under millet, any improvement in their yield levels will have a significant impact on the food security of the population.

Maize Hybrids: The acreage under maize has been increasing in the recent years, currently occupying around 11,000 hectares. AGRIMEX, a private seed firm has been selling hybrid maize seeds (from Burkina Faso) since 2012 – Komasaya Maize Hybrid. AGRIMEX sold 10 MT of hybrid maize seeds to farmers in Dosso region (for irrigated tracts) during 2015 season alone and they expect the demand to increase around 20 MT during the 2016 season. The demand for maize is twofold –green maize and dry maize for human consumption.

Rice seeds: Niger has been importing nearly 300,000 tons of rice annually from other countries, and the consumption of rice has been increasing among local population. Potential to extend irrigated acreage and demand for good quality seeds for rice and also new high yielding cultivars of rice exists in the irrigated regions of Dosso, Niamey and Tillabery.

In Tillabery rice growing region, the seed farm of Saguia, under the responsibility of the ONAHA, is the main and only source of certified rice seed for local farmers’ unions, who united into a federation of rice farmers’ unions of Niger (FUCOPRI). It is clear that the lack of other seed companies competing with the Saguia Farm has had a negative impact on the rice seed sub-sector of Niger. This monopoly cannot be however the sole explanation for the shortage of certified seeds to reach small-scale farmers in the country.

The official rice seed supply in Niger has undergone changes during the last 20 years (from state-led intervention to farmers’ association-led intervention) but with less impact than expected. In addition to the lack of competition, this situation is affected by the shortage of qualified seed inspectors and a clear and strict national seed policy to ensure access to quality seed by smallholders. The promotion and creation of small private seed enterprises could gradually enhance farmers’ access to seed and may revitalize the rice seed system and complement the local informal seed supply. In summary, Niger must implement a national seed policy that restructures the formal seed sector and opens it to non-government organizations and small private enterprises. Additionally, staff of Saguia seed farm, seed producers of local farmers’ association, as well as seed inspectors should be trained in appropriate seed production and policies.

3.6 Constraints in the seed value chain

The description of the seed value chain highlights various technical, marketing and policy constraints in the current system. In general seed demand estimation by the government is very poor – government often underestimates the demand, which affects the seed multiplication of seeds.

Technical constraints relate to the capacity of farmers to produce good quality seeds and the implementation of seed quality control procedures. In general, those farmers who have been involved in well-established seed production schemes, e.g. those near the seed processing centers such as Douku-Douku, have the capacity to produce quality seed, but not all farmers are able to produce good quality seed. The current seed system lacks basic quality control measures, and there is a shortage of technical staff to ensure that basic quality standards are maintained. Very little emphasis has been placed on seed quality aspects since most of the ‘seeds’ produced are

24

destined for the relief seed market. Fake seeds entry from Nigeria is another problem faced by seed users and seed firms (who distort the prices) and warrant more quality control mechanisms in place at the border especially during the planting season.

Marketing constraints are apparent in the fact that seed producers are entirely dependent on either seed service centers or ‘projects’ to sell seed for them. Since farmers buy in small quantities only, the seed producers feel that seed production is a viable enterprise only if there is a donor-funded project to purchase the seed. The fact that the community-managed input stores or BI are not run on a commercial basis and rarely stock seed is also an indication of marketing constraints, as is the lack of functional input shops selling seeds. Marketing

constraints relate to the fact that almost all seed sales in Niger revolve around donor-funded projects, often involving relief seed, which is then distributed for free to farmers affected by drought. The dominance of the relief seed market has contributed towards inhibiting the development of an effective commercial seed system. Another reason for the limited development of commercial seed systems in Niger relates to a problem that is common throughout Africa, in which national seed markets are too small to support significant commercial investment, especially for most secondary crops.

Private firms also complained delayed payment (9 months to a year delay) for seed purchases by the government which in turn affects firms’ ability to pay the out growers on time. 2 seed firms – the largest suppliers to government still await for 400 million FCFA – for the seeds supplied last year. The private firms also have major issues to access commercial finance for business purposes. The interest rates are high and100 % collateral is required to access finance. In the case of micro financing institutions (MFIs) the interest rates are as high as 24-26% per annum though requires very minimum collaterals. There are no exclusive schemes or programs from the government towards developing commercial seed sector.

Discussion with farmers – seed users revealed delayed distribution of seeds, i.e., seeds are not distributed on time for planting and the quality is very poor. Farmers commented – “ if they allow us to use the vouchers to buy directly from the private firms or seed producers”. Technical information or seed varietal information is also not provided when the government provides the seeds free to farmers.

Most of input retailers (either BI or seed firm based outlets) are single-input based – either they sell fertilizers or seeds or pesticides alone. The concept of selling all three inputs in one shop – is slowly catching up – but a long way to go – as this involves resolving financial constraints – input credit related issues and also interface between CAIMA –inputs distribution and the existing seed system!

25