Embed Size (px)

Citation preview

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 1/43

1

SUMMER PROJECT REPORT ON

INTERNAL AUDIT OF FINANCIAL STATEMENTS

Submitted to the University of Mumbai in the partial fulfillment of the

requirement for the award of the degree in

MASTERS OF MANAGEMENT STUDIES

BY:

JENIFER PEREIRA

MMS II ROLL NO.: 812009-11

Under the guidance of

Prof. Thomas Mathew (Core Faculty ± Mark eting)

St Francis Institute of Management and Research

S F I M A R

St Francis Institute of Management and Research, Mt. Poinsur,S.V.P Road, Borivali (W) Mumbai.

Year: 2009 ± 2011

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 2/43

2

CERTIFICATE

This is to certify that the project work µINTERNAL AUDIT OF FINANCIALSTATEMENTS¶ has been successfully completed by µJENIFER PEREIRA¶

during the year 2009-2011 in the partial fulfillment of the requirement for the

award of the degree in Master in Management Studies at St. Francis Institute of

Management & Research under Mumbai University. The information submitted is

true and to the best of my knowledge.

JENIFER PEREIRA

(Project Trainee)

PROF. THOMAS MATHEW

(Project Guide)

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 3/43

3

ACKNOWLEDGEMENT

I Jenifer Pereira, student of St. Francis institute of management and research is proud to submit this project to the University of Mumbai and would like to thank

University of Mumbai for motivating us towards our work by giving us this

project.

I would like to take this opportunity to express my deep sense of gratitude to my

project guide Prof. Thomas Mathew for his valuable guidance and constant support

in this endeavor. He has been a constant source of inspiration and I sincerely thank

him for his suggestions and help to prepare this project report.

I am also very much grateful to Dr. Thomas Mathew (Director ± St. Francis

Institute of Management and Research) for providing me with this unique

opportunity.

I thank all my colleagues who guided me and from whom I received the needed

information about this project during its development.

Finally I would like to thank Mr. Lalit P. Jain, and Mr. Vaidya (Partners of Jain &

Vaidya Associates), Mr. Bhushan Patil (senior accountant) and Mr. Vishal Ail(junior accountant). Their assistance in the preparation of the project made a

difficult task easier. I sincerely thank them all.

Jenifer Pereira.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 4/43

4

EXECUTIVE SUMMARY

JAIN & VAIDYA ASSOCIATES is a financial consulting firm. It has been awonderful learning experience working for such a great company. It provides

financial audit profession to ensure highest quality results and to achieve long-term

effectiveness and professionalism. The recommendations provided by them to their

clients for improvement in those areas where opportunities or deficiencies are

identified were a great learning experience for me. It will surely help me in my

future.

The main aim of the project was to study how the process of µinternal audit of

financial statements¶ helps to identify the errors and the inefficiencies in the

financial statements and finally achieve an adequate financial report. The project

also focuses on studying the significance of µinternal audit of financial statements.¶

The research was conducted to look at how the professional auditors (chartered

accountants) regard the most common issues or errors they come across in

Auditing of small scale industries and the ways to solve them.

The primary data was collected through questionnaire tool with all open endedquestions by interview technique. Simple words were used while framing the

questionnaire so that anyone would be able to understand the research.

The findings are stated on the basis of responses given by the auditors to the

questionnaire and recommendations on my personal observation.

It has indeed been a pleasure working with JAIN & VAIDYA ASSOCIATES. This

has provided me with an extremely good learning environment which helped me

gain a vast amount of practical knowledge in the field of financial management.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 5/43

5

TABLE OF CONTENTS

SR . NO. CONTENTS PAGE NO.S

1. COMPANY INTRODUCTION 6

2. PROJECT INTRODUCTION 7

3. NEED FOR THE STUDY 8

4. OBJECTIVES OF THE STUDY 8

5. LITERATURE REVIEW 9-26

6. RESEARCH METHODOLOGY 27-29

7. FINDINGS 30-37

8. COMMENTS 38

9. CONCLUSION 39

10. BIBLIOGRAPHY 40

11. WEBLIOGRAPHY 41

12. APPENDIX 42

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 6/43

6

COMPANY INTRODUCTION

Jain & Vaidya Associates, Chartered Accountants is a financial consulting and

Accounting firm. It was started by the two partners Mr. Lalit P. Jain and Mr.

Vaidya. It has eight assistant chartered accountants.

Today there is a high demand for professionalism, knowledge, integrity and

leadership in the field of Accounts. Therefore they provide accounting and audit

services. They are professional chartered accountants, practitioners of accountancy

which is the measurement, disclosure or provision of assurance about financial

information that helps managers, investors, tax authorities and other decision

makers make resource allocation decisions.

They provide internal audit services of financial statements that are the review of

the financial statements of a company, whether or not those financial statements

are relevant, accurate, complete, and fairly presented. The goal is to determine

whether these statements have been prepared in conformity with GAAP¶s.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 7/43

7

PROJECT INTRODUCTION

Finance is one of the most primary requisites of a business and the modern

management obviously depends largely on the efficient management of the

finance.

Financial statements are prepared primarily for decision making. They play a

dominant role in setting the frame work of managerial decisions. The finance

manager has to adhere to the five R¶s with regard to money. This right quantity of

money for liquidity consideration of the right quality, whether owned or borrowed

funds at the right time to preserve solvency from the right sources and at the rightcost of capital.

The term, audit of financial statements is the review of the financial statements of a

company, whether or not those financial statements are relevant, accurate,

complete, and fairly presented.

The main purpose of audit of financial statements is to ascertain the validity and

reliability of the statements. Effective recording of financial transactions, deterring

and investigating fraud, safeguarding assets, whether statements are free from

material error and compliance with laws and regulations with the goal of

highlighting organizational problems and recommending solutions.

An effective audit of the financial statements of a company will provide

information about the position, performance and changes in financial position of an

enterprise that is useful to a wide range of users in making economic decisions.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 8/43

8

NEED FOR THE STUDY

1. To analyze the different approaches used by a company to identify

inefficiencies, in order to evaluate the ways to overcome such issues in the

future financial statements.

2. To identify the most common problems occurring while auditing a financial

statements.

OBJECTIVES OF THE STUDY

1. To study how the process of µinternal audit of financial statements¶ that

helps to overcome the inadequacies in order to achieve an adequate financial

report.

2. To understand the significance of µinternal audit of financial statements¶ in

order to see the impact on the organization.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 9/43

9

LITERATURE REVIEW

AUDIT IN ACCOUNTING

Audits are performed to ascertain the validity and reliability of information; also to

provide an assessment of a system's internal control. Audit seeks to provide only

reasonable assurance that the statements are free from material error.

The term µaudit may be used to describe not only work done by accountants in

examining financial reports but also work done in reviewing (a) compliance with

applicable laws and regulations, (b) efficiency and economy of operations, and (c)

effectiveness in achieving program results.

Audit is a vital part of accounting. Traditionally, audits were mainly associated

with gaining information about financial systems and the financial records of a

company or a business. However, recent auditing has begun to include other

information about the system, such as information about security risks, information

systems performance (beyond financial systems), and environmental performance.

As a result, there are now professions conducting security audits, IS audits, and

environmental audits.

INTERNAL AUDIT

Internal auditing is a profession and activity involved in helping organizations

achieve their stated objectives. It does this by using a systematic methodology for

analyzing business processes, procedures and activities with the goal of

highlighting organizational problems and recommending solutions.

Internal Auditing is an independent, objective assurance and consulting activity

designed to add value and improve an organization's operations. It helps an

organization accomplish its objectives by bringing a systematic, disciplined

approach to evaluate and improve the effectiveness of risk management, control,

and governance processes.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 10/43

10

It is the process of reviewing business activities to identify inefficiencies, reduce

costs and achieve organizational objectives. Internal audits may investigate

potential theft or fraud and ensure compliance with applicable regulations and

policies. They also assist in risk management.

Internal auditors of internal control are employed by the organization they audit.

Internal auditors perform various audit procedures, primarily related to procedures

over the effectiveness of the company's internal controls over financial reporting.

The scope of internal auditing within an organization is broad and may involve

topics such as the efficacy of operations, the reliability of financial reporting,

deterring and investigating fraud, safeguarding assets, and compliance with laws

and regulations.

Internal auditing frequently involves measuring compliance with the entity's

policies and procedures. However , internal auditors are not responsible for the

execution of company activities; they advise management and the Board of

Directors regarding how to better execute their responsibilities. As a result of their

broad scope of involvement, internal auditors may have a variety of higher

educational and professional backgrounds.

Internal Auditors are well ± disciplined in their skills and subscribe to a

professional code of ethics. They are diverse and innovative; committed togrowing and enhancing their skills; continually on the lookout for emerging risks

and trends in the profession; good thinkers. To effectively fulfill all their roles,

internal auditors must be excellent communicators who listen attentively, speak

effectively and write clearly.

R ole in internal control:

Internal auditing activity is primarily directed at improving internal control.Internal control is designed to achieve the following objectives:-

y Effectiveness and efficiency of operations.

y Reliability of financial reporting.

y Compliance with laws and regulations.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 11/43

11

Management is responsible for internal control. Managers establish policies and

processes to help the organization achieve these objectives. Internal auditors

perform audits to evaluate whether the policies and processes are designed and

operating effectively and provide recommendations for improvement.

The internal auditors are expected to provide recommendations for improvement in

those areas where opportunities or deficiencies are identified. While management

is responsible for internal controls, the internal audit activity provides assurance to

management that internal controls are effective and working as intended.

R ole in risk management:

Internal auditing professional standards require the function to monitor andevaluate the effectiveness of the organization's Risk management processes.

Internal auditors should evaluate the risks identified and advise management to set

objectives, analyze, and respond to those risks.

Internal auditors may help companies establish and maintain Risk Management

processes and help identify emerging risks.

R ole in corporate governance:

Internal auditing activity as it relates to corporate governance is generally informal,

accomplished primarily through participation in meetings and discussions with

members of the Board of Directors. Corporate governance is a combination of

processes and organizational structures implemented by the Board of Directors to

inform, direct, manage, and monitor the organization's resources, strategies and

policies towards the achievement of the organizations objectives.

A primary focus area of internal auditing as it relates to corporate governance is

helping the management perform its responsibilities effectively. This may include

reporting critical internal control problems and providing suggestions respectively.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 12/43

12

THE INTERNAL AUDIT PROCESS: -

1. Develop an understanding of the business area under review. Establish and

communicate the scope and objectives for the audit to appropriate

management.

2. Describe the key risks facing the business activities within the scope of the

audit.

3.

Identify control procedures used to ensure each key risk and transaction typeis properly controlled and monitored.

4. Develop and execute a risk-based sampling and testing approach to

determine whether the most important controls are operating as intended.

5. Report problems identified and negotiate action plans with management to

address the problems.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 13/43

13

INTERNAL AUDIT REPORTS

Internal auditors typically issue reports at the end of each audit that summarize

their findings, recommendations, and any responses or action plans to the

management and owners. Each audit finding within the body of the report maycontain five elements, sometimes called the "5 C's":

1. Condition: What is the particular problem identified?

2. Criteria: What is the standard that was not met? The standard may be a

company policy or other rules and regulations.

3. Cause: Why did the problem occur?

4. Consequence: What is the risk/negative outcome (or opportunity foregone)

because of the finding?

5. Corrective action: What should management do about the finding? What

have they agreed to do and by when?

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 14/43

14

AUDIT OF FINANCIAL STATEMENTS

An audit of financial statements is the review of the financial statements of a

company, whether or not those financial statements are relevant, accurate,

complete, and fairly presented. The goal is to determine whether these statementshave been prepared in conformity with GAAP¶s. Professionals called internal

auditors are accountants employed by organizations to perform the auditing

activity.

It determines (a) whether financial operations are properly conducted, (b) whether

the financial reports are presented fairly, and (c) whether the entity has complied

with applicable laws and regulations.

An accountant is a practitioner of accountancy, which is the measurement,

disclosure or provision of assurance about financial information that helps

managers, investors, tax authorities and other decision makers make resource

allocation decisions.

The audit is designed to reduce the possibility that a material misstatement is not

detected by audit procedures. A misstatement is defined as false or missing

information, whether caused by fraud or error. "Material" is very broadly defined

as being large enough or important enough to cause stakeholders to alter their

decisions.

Internal audit of financial statements is performed before the release of the

financial statements, typically on an annual basis before the end of the fiscal year.

Financial statement:

A financial statement (or financial report) is a formal record of the financial

activities of a business, person, or other entity. The term refers to the statementswhich the accountants prepare at the end of a period. It is often referred to as an

account, although the term financial statement is also used, particularly by

accountants.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 15/43

15

For a business enterprise, all the relevant financial information, presented in a

structured manner and in a form easy to understand, are called the financial

statements.

For large corporations, these statements are often complex and may include anextensive set of notes to the financial statements and management discussion and

analysis. The notes typically describe each item on the balance sheet, income

statement and cash flow statement in further detail. Notes to financial statements

are considered an integral part of the financial statements.

The objective of financial statements is to provide information about the financial

position, performance and changes in financial position of an enterprise that is

useful to a wide range of users in making economic decisions.

They typically include four basic financial statements:-

1. Balance sheet:

It is a statement of financial position, a summary of the financial balances of a sole

proprietorship, a business partnership or a company. A balance sheet is often

described as a "snapshot of a company's financial condition". A standard company

balance sheet has three parts:

Assets which mainly includes current assets:- Cash , Inventories, Accounts

receivable, Prepaid expenses and fixed assets:- Property, plant and equipment,

Intangible assets.

Liabilities: - Accounts payable, Provisions.

Ownership equity: - Par value of shares

The difference between the assets and the liabilities is known as equity or the net

assets or the net worth or capital of the company and according to the accounting

equation, net worth must equal assets minus liabilities.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 16/43

16

Another way to look at the same equation is that assets equal liabilities plus

owner's equity. Looking at the equation in this way shows how assets were

financed: either by borrowing money (liability) or by using the owner's money

(owner's equity). Balance sheets are usually presented with assets in one section

and liabilities and net worth in the other section with the two sections "balancing.

2. Income statement:

Income statement, also referred as profit and loss statement (P&L), earnings

statement, operating statement or statement of operations, is a company's financial

statement that indicates how the revenue (money received from the sale of

products and services before expenses are taken out)is transformed into the net

income (the result after all revenues and expenses have been accounted for). Itdisplays the revenues recognized for a specific period, and the cost and expenses

charged against these revenues, including write-offs (e.g., depreciation and

amortization of various assets) and taxes. The purpose of the income statement is

to show managers and investors whether the company made or lost money during

the period being reported.

3.

Statement of retained earnings:-

The Statement of Retained Earnings (also known as Equity Statement, Statement

of Owner's Equity for a single proprietorship, Statement of Partner's Equity for

partnership, and Statement of Retained Earnings and Stockholders' Equity for

corporation) is one of the basic financial statements as per Generally Accepted

Accounting Principles, and it explains the changes in a company's retained

earnings over the reporting period. It breaks down changes affecting the account,

such as profits or losses from operations, dividends paid, and any other items

charged or credited to retained earnings. A retained earnings statement is required by Generally Accepted Accounting Principles (GAAP) whenever comparative

balance sheets and income statements are presented. It may appear in the balance

sheet, in a combined income statement and changes in retained earnings statement,

or as a separate schedule.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 17/43

17

Therefore, the statement of retained earnings uses information from the income

statement and provides information to the balance sheet. Retained earnings are part

of the balance sheet(another basic financial statement) under "stockholders equity,"

and is mostly affected by net income earned during a period of time by the

company less any dividends paid to the company's owners / stockholders. Theretained earnings account on the balance sheet is said to represent an

"accumulation of earnings" since net profits and losses are added/subtracted from

the account from period to period.

4. Statement of cash flows:

In financial accounting, a cash flow statement, also known as statement of cash

flows or funds flow statement, is a financial statement that shows how changes in

balance sheet accounts and income affect cash and cash equivalents, and breaks the

analysis down to operating, investing, and financing activities. Essentially, the cash

flow statement is concerned with the flow of cash in and cash out of the business.

The statement captures both the current operating results and the accompanying

changes in the balance sheet. As an analytical tool, the statement of cash flows is

useful in determining the short-term viability of a company, particularly its ability

to pay bills.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 18/43

18

Purpose of financial statements:-

y Owners and managers require financial statements to make important

business decisions that affect its continued operations. Financial analysis is

then performed on these statements to provide management with a moredetailed understanding of the figures. These statements are also used as part

of management's annual report to the stockholders.

y Prospective investors make use of financial statements to assess the viability

of investing in a business for making investment decisions.

y Financial institutions (banks and other lending companies) use them to

decide whether to grant a company with fresh working capital or extend debt

securities (such as a long-term bank loan or debentures) to finance expansion

and other significant expenditures.

y Government entities (tax authorities) need financial statements to ascertain

the propriety and accuracy of taxes and other duties declared and paid by a

company.

y Vendors who extend credit to a business require financial statements to

assess the creditworthiness of the business.

STANDARDS AND REGULATIONS

Different countries have developed their own accounting principles over time,

making international comparisons of companies difficult. To ensure uniformity and

comparability between financial statements prepared by different companies, a set

of guidelines and rules are used. Commonly referred to as Generally Accepted

Accounting Principles (GAAP), these set of guidelines provide the basis in the

preparation of financial statements.

Generally Accepted Accounting Principles (GAAP) is a term used to refer to the

standard framework of guidelines for financial accounting used in any given

jurisdiction which are generally known as Accounting Standards. GAAP includes

the standards, conventions, and rules accountants follow in recording and

summarizing transactions, and in the preparation of financial statements. Financial

statements should be understandable, relevant, reliable and comparable.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 19/43

19

FINANCIAL RATIOS

A financial ratio (or accounting ratio) refers to the numerical or quantitative

relationship between two variables value taken from an enterprise's financial

statements. Often used in accounting, there are many standard ratios used to try toevaluate the overall financial condition of a corporation or other organization.

Financial ratios may be used by managers within a firm, by current and potential

shareholders (owners) of a firm, and by a firm's creditors. Security analysts use

financial ratios to compare the strengths and weaknesses in various companies.

Sources of data for financial ratios:

Values used in calculating financial ratios are taken from the balance sheet, incomestatement, statement of cash flows or (sometimes) the statement of retained

earnings. These comprise the firm's "accounting statements" or financial

statements. The statements' data is based on the accounting method and accounting

standards used by the organization.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 20/43

20

SIGNIFICANCE OF ANALYSING RATIOS IN AUDIT

Ratio analysis is a powerful tool of financial analysis useful for measuring the

performance of an organization. Ratio analysis is a process of comparison of one

accounting variable against the other, which makes a ratio to make proper analysisabout the strengths and weaknesses of the operations of an enterprise.

It helps in evaluating the firm¶s performance:

With the help of ratio analysis conclusion can be drawn regarding several aspects

such as financial health, profitability and operational efficiency of the undertaking.

Ratio points out the operating efficiency of the firm i.e. whether the management

has utilized the firm¶s assets correctly, to increase the investor¶s wealth. It ensuresa fair return to its owners and secures optimum utilization of firm¶s assets.

It helps in inter-firm comparison:

Ratio analysis helps in inter-firm comparison by providing necessary data. An

inter-firm comparison indicates relative position. It provides the relevant data for

the comparison of the performance of different departments. If comparison shows

a variance, the possible reasons of variations may be identified and if results are

negative, the action may be initiated immediately to bring them in line.

It simplifies financial statement:

The information given in the basic financial statements serves no useful Purpose

unless it s interrupted and analyzed in some comparable terms. The ratio analysis is

one of the tools in the hands of those who want to know something more from thefinancial statements in the simplified manner.

It helps in determining the financial position of the concern:

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 21/43

21

Ratio analysis facilitates the management to know whether the firm¶s financial

position is improving or deteriorating or is constant over the years by setting a

trend with the help of ratios The analysis with the help of ratio analysis can know

the direction of the trend of strategic ratio may help the management in the task of

planning, forecasting and controlling.

It is helpful in budgeting and forecasting:

Accounting ratios provide a reliable data, which can be compared, studied and

analyzed. These ratios provide sound footing for future prospectus. The ratios can

also serve as a basis for preparing budgeting future line of action.

Liquidity position:

With help of ratio analysis conclusions can be drawn regarding the Liquidity

position of a firm. The liquidity position of a firm would be satisfactory if it is able

to meet its current obligation when they become due. The ability to met short term

liabilities is reflected in the liquidity ratio of a firm.

Long term solvency:

Ratio analysis is equally for assessing the long term financial ability of the Firm.

The long term solvency is measured by the leverage or capital structure and

profitability ratio which shows the earning power and operating efficiency,

Solvency ratio shows relationship between total liability and total assets.

Operating efficiency:

Yet another dimension of usefulness or ratio analysis, relevant from the View point

of management is that it throws light on the degree efficiency in the various

activity ratios measures this kind of operational efficiency.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 22/43

22

CLASSIFICATION OF RATIOS:

Financial ratios quantify many aspects of a business and are an integral part of

financial statement analysis. Financial ratios are categorized according to the

financial aspect of the business which the ratio measures. Different ratios are usedfor different purpose these ratios can be grouped into various classes according to

the financial activity. Ratios are classified into four broad categories:-

1. Liquidity Ratio

2. Leverage Ratio

3. Profitability Ratio

4. Activity Ratio

1. Liquidity R atio: Liquidity ratio measures the firm¶s ability to meet its

current obligations i.e. ability to pay its obligations and when they become

due. Commonly used ratios are:

Current ratio:

Current ratio is the ratio, which express relationship between current asset and

current liabilities. Current asset are those which can be converted into cash withina short period of time, normally not exceeding one year. The current liabilities

which are short- term maturing to be met.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 23/43

23

Current Assets

Current Ratio =

Current liabilities

Acid test ratio:

It is often referred to as quick ratio because it is a measurement of firm¶s ability to

convert its current assets quickly into cash in order to meet its current liabilities.

Quick asset

Acid test ratio =

Quick liabilities

2. Leverage or capital structure ratio: Leverage or capital structure ratios are

the ratios, which indicate the relative interest of the owners and the creditors

in an enterprise. It indicates financial structure of the organization, i.e. the

proportion of debts as compared to owner¶s fund.

Debt ±equity ratio:

Debt -equity ratio which expresses the relationship between debt and

equity. This ratio explains how far owned funds are sufficient to pay outsideliabilities. It is calculated by following formula:

Long term +short term debts +current liabilities

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 24/43

24

Debt equity ratio =

Net worth

3. Profitability ratio: Profitability ratio are the best indicators of overall

efficiency of the business concern, because they compare return of value

over and above the value put into business with sales or service carried on

by the firm with the help of assets employed. Profitability ratio can be

determined on the basis of:

y Sales

y Investment

1. Profitability ratios related to sale:

Gross profit to sales ratio:

The gross profit to sales ratio establishes relationship between gross profit and

sales to measure the relative operating efficiency of the firm to reflect pricing

policy.

Gross Profit

Gross profit to sales ratio = * 100

Net Sales

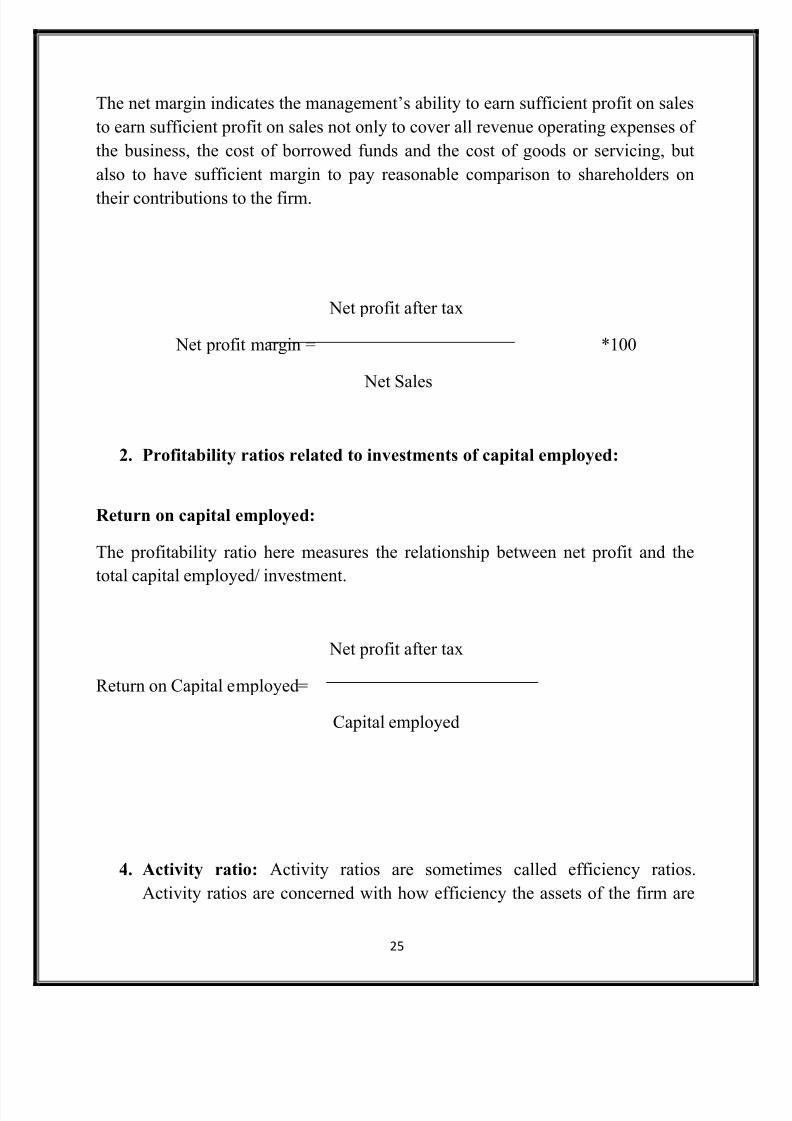

Net profit margin:

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 25/43

25

The net margin indicates the management¶s ability to earn sufficient profit on sales

to earn sufficient profit on sales not only to cover all revenue operating expenses of

the business, the cost of borrowed funds and the cost of goods or servicing, but

also to have sufficient margin to pay reasonable comparison to shareholders on

their contributions to the firm.

Net profit after tax

Net profit margin = *100

Net Sales

2. Profitability ratios related to investments of capital employed:

Return on capital employed:

The profitability ratio here measures the relationship between net profit and the

total capital employed/ investment.

Net profit after tax

Return on Capital employed=

Capital employed

4. Activity ratio: Activity ratios are sometimes called efficiency ratios.

Activity ratios are concerned with how efficiency the assets of the firm are

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 26/43

26

managed. These ratios express relationship between level of sales and the

investment in various assets inventories, receivables, fixed assets etc.

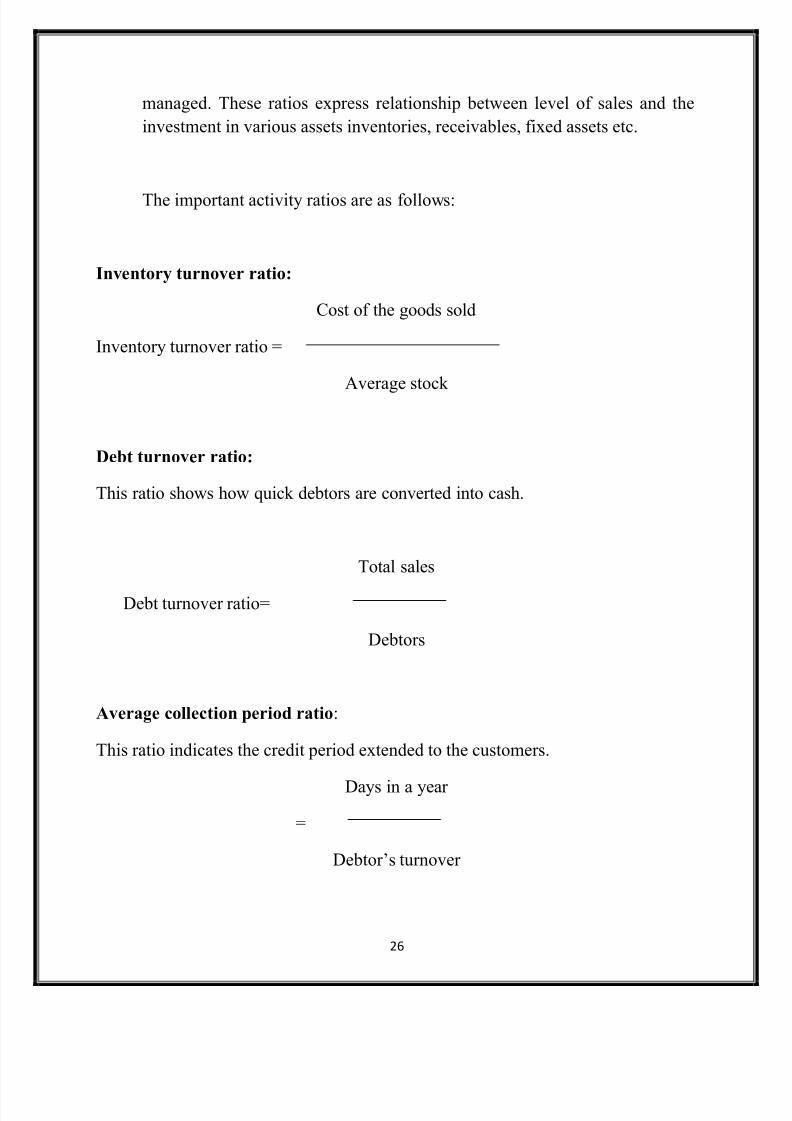

The important activity ratios are as follows:

Inventory turnover ratio:

Cost of the goods sold

Inventory turnover ratio =

Average stock

Debt turnover ratio:

This ratio shows how quick debtors are converted into cash.

Total sales

Debt turnover ratio=

Debtors

Average collection period ratio:

This ratio indicates the credit period extended to the customers.

Days in a year

=

Debtor¶s turnover

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 27/43

27

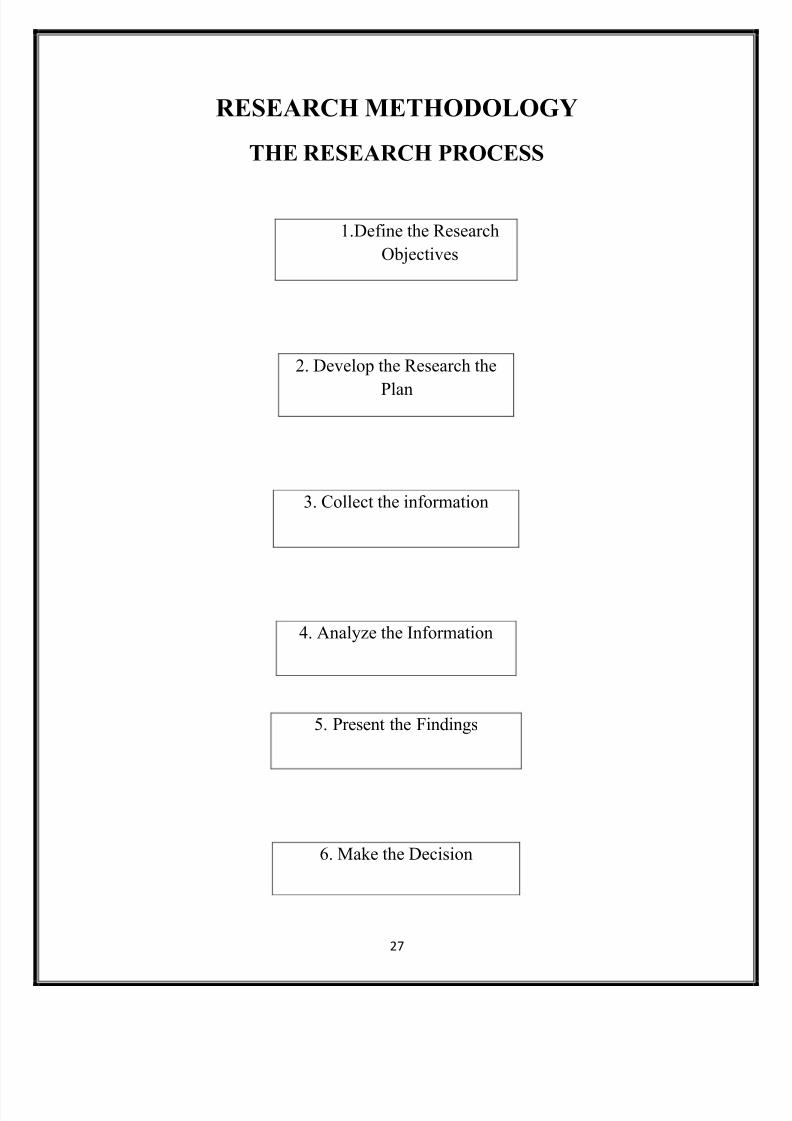

RESEARCH METHODOLOGY

THE RESEARCH PROCESS

1.Define the Research

Objectives

2. Develop the Research the

Plan

3. Collect the information

4. Analyze the Information

5. Present the Findings

6. Make the Decision

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 28/43

28

The research process involves the six steps:

STEP1: Define the Research objectives:

1. To find the reasons why an organization should audit its financial

statements.

2. To find the difference between external and internal audit and their relation.

3. To find the role of audit of financial statements in Risk management.

4. To find the auditors role in preventing, detecting and investigating fraud.

5. To find the standard guide lines followed by the auditors.

6. To find out the most common issues or errors occurring while auditing the

financial statements of small scale industries and the ways to solve them.7. To find the role of audit in Ratio analysis.

STEP2: Develop the Research Plan:

DATA SOURCES

The research involves Primary Data Collection by interviewing the charteredaccountants (auditors) in the Jain & Vaidya Associates. In order to sense the

importance of this topic and then a formal research instrument has been developed

to carry it in the company¶s operations.

RESEARCH APPROACHES

The primary data was collected through survey method.

RESEARCH INSTRUMENTS

The instrument used for the collection of Primary Data was through

Questionnaires. The questionnaire was carefully developed and tested before

administering on a large scale. The questionnaire consisted of 6 questions. The

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 29/43

29

questions were formed choosing an appropriate form, wording and sequence.

These questions are all open-ended questions.

SAMPLING PLAN

After deciding the Research Approach and Instrument, the Sampling Plan was

designed. While designing a Sampling Plan following decisions were made:

1. Sampling Size:

The Research target sample was the chartered accountants in the Jain & Vaidya

Associates. The Research was conducted on 4 chartered accountants, mainly the

two partners of the company, Mr. Lalit P. Jain and Mr. Vaidya. The two

assistant chartered accountants: Mr. Bhushan and Mr. Vishal working for the

company.

CONTACT METHODS

Once the sampling plan was determined, it was decided that the respondents be

contacted by an arranged personal interview, because it is the most versatilemethod. Where we can ask more questions and make observations of the

respondents.

STEP 3: COLLECT THE INFORMATION

The questionnaire was filled and collected in few hours. After collecting the

questionnaire it was immediately checked so that no questions were left

incomplete.

STEP 4: ANALYZE THE INFORMATION

The next step in the process was to analyze the findings from the collected data.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 30/43

30

STEP 5: PRESENT THE FINDINGS:

The last step was to present the findings that are relevant to the major decisions

facing management.

Q. 1. Why should an organization have internal auditing of financial

statements?

Mr. Lalit P. Jain : µInternal auditing bridges the gap between the company¶s

financial statements and the standards set i.e. GAAP, assesses the ethical climate

and the effectiveness and efficiency of transactions, and serves as an organization¶s

safety for compliance with rules, regulations, and overall best business practices¶.

Mr. Vaidya: A dedicated and effective internal audit activity assists the

management in fulfilling their responsibilities by bringing a systematic disciplined

approach to assessing the effectiveness of the design and execution of the system

of internal controls and risk management processes.

Mr. Vishal: Because internal auditors are experts in understanding organizational

risks and internal controls available to mitigate these risks, they assist management

in understanding these topics and provide recommendations for improvements.

Mr. Bhushan: Because of its unique and objective perspective, in-depthorganizational knowledge, and application of sound audit and consultation, a well

functioning, fully resourced and independent internal audit activity is well

positioned to provide valuable support and assurance to an organization.

Q. 2. What standards guide the work of internal audit prof essionals?

Mr. Lalit P. Jain: Accounting standards vary from country to country. In India the

Institute of Chartered Accountants of India (ICAI) has formed Accounting

Standards Board (ASB) in 1977, upon which the responsibility was set to developaccounting standards to be issued and revised in the country from time to time.

They developed GAAP which refers to Generally Accepted Accounting

Principles. There are total 32 accounting standards. These are guidelines or set of

rules for financial accounting and reporting, encompassing conventions, traditions

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 31/43

31

and procedures followed in accounting industry. ASB also provides explanation

and guidance on issues arising from standards.

Q. 3. What is internal auditing role in preventing, detecting, and investigating

fraud?

Mr. Lalit P. Jain: Internal auditors support management's efforts to establish a

culture that embraces ethics, honesty, and integrity. They assist management with

the evaluation of internal controls used to detect fraud, evaluate the organization's

assessment of fraud risk, and are involved in any fraud investigations.

Q. 4. What is Enterprise R isk Management (ERM) and what role in it does

internal auditing play?

Mr. Vaidya: Enterprise Risk Management is a structured and coordinated

governance approach to identify, quantify, respond to, and monitor the

consequences of potential events. Enterprise risk management is defined as a

process, to identify potential events that may affect the entity; and manage risk to

be within its risk appetite to provide reasonable assurance regarding the

achievement of entity objectives.

Mr. Lalit P. Jain: ERM deals with risks and opportunities affecting the creation or

preservation of organizational value. Management has the primary responsibility

for identifying and managing risk and for implementing ERM in a structured,

consistent, and coordinated approach.

Implemented by management, ERM is evaluated by the internal auditors for

effectiveness and efficiency. Internal auditors play a key role in evaluating the

effectiveness of and recommending improvements to ERM.

Q. 5. How do internal and external auditors diff er and how should they relate?

Mr. Lalit P. Jain: Internal auditors are integral to the organization and provide

ongoing monitoring and assessment of all activities. On the contrary, external

auditors are independent of the organization, and provide an annual opinion on the

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 32/43

32

financial statements. The work of the internal and external auditors should be

coordinated for optimal effectiveness and efficiency.

Mr. Bhushan: Internal and external auditors have mutual interests regarding the

effectiveness of internal financial controls. Both professions adhere to codes of ethics and professional standards set by the professional associations. There are,

however, major differences with regard to their relationships to the organization,

and to their scope of work and objectives.

The internal auditors focus on future events as a result of their continuous review

and evaluation of controls and processes. They also are concerned with the

prevention of fraud in any form.

Mr. Vaidya: The primary mission of the external auditors is to provide anindependent opinion on the organization's financial statements, annually. Their

approach is historical in nature, as they assess whether the statements conform to

generally accepted accounting principles, whether they fairly present the financial

position of the organization.

Q. 6. What are the most common issues or errors occurring while auditing the

financial statements of small scale industries and the ways to solve them?

Mr. Vishal: There are many such issues, but the most common issues or errors are:

1. Bank reconciliation: Comparing and matching figures from the accounting

records against those shown on a bank statement.

2. Ledgers scrutiny: Comparing and matching the sales figures with the

debtors and purchase figures with the creditors in order to tally the closing

balance.

3. Vat audit: VAT (Value added tax) is a sales tax levied on the sale of goods

and services. We have to check whether 12.5% VAT on Sales is being paidto the government.

4. Sales return: Most of the times there is return of sales due to defective or

damaged goods. To set off the return goods amount we make credit note on

the debtors A/c.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 33/43

33

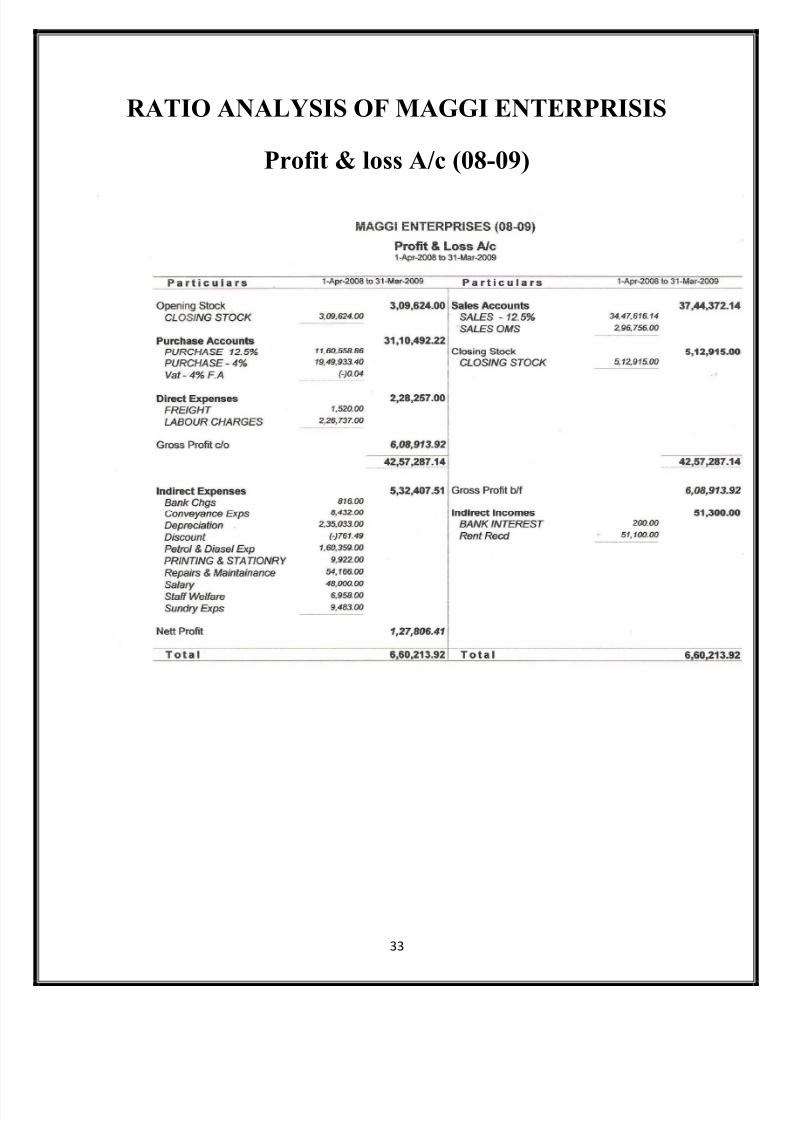

RATIO ANALYSIS OF MAGGI ENTER PRISIS

Profit & loss A/c (08-09)

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 34/43

34

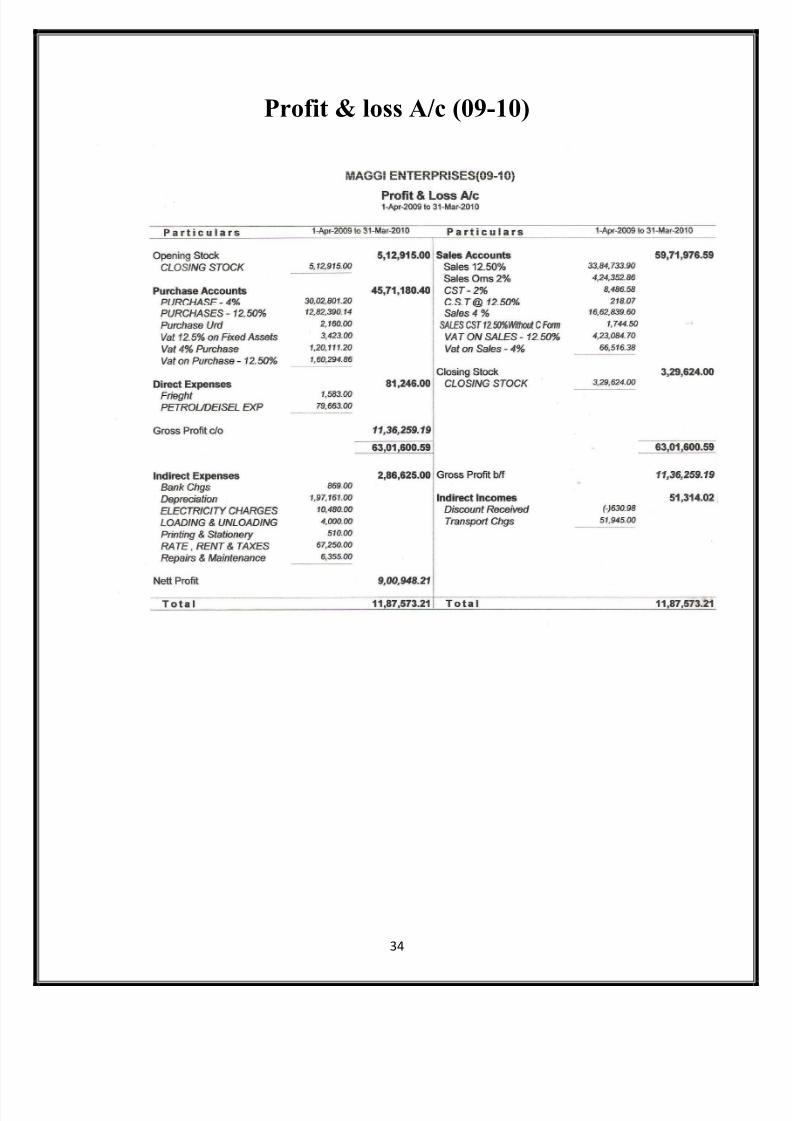

Profit & loss A/c (09-10)

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 35/43

35

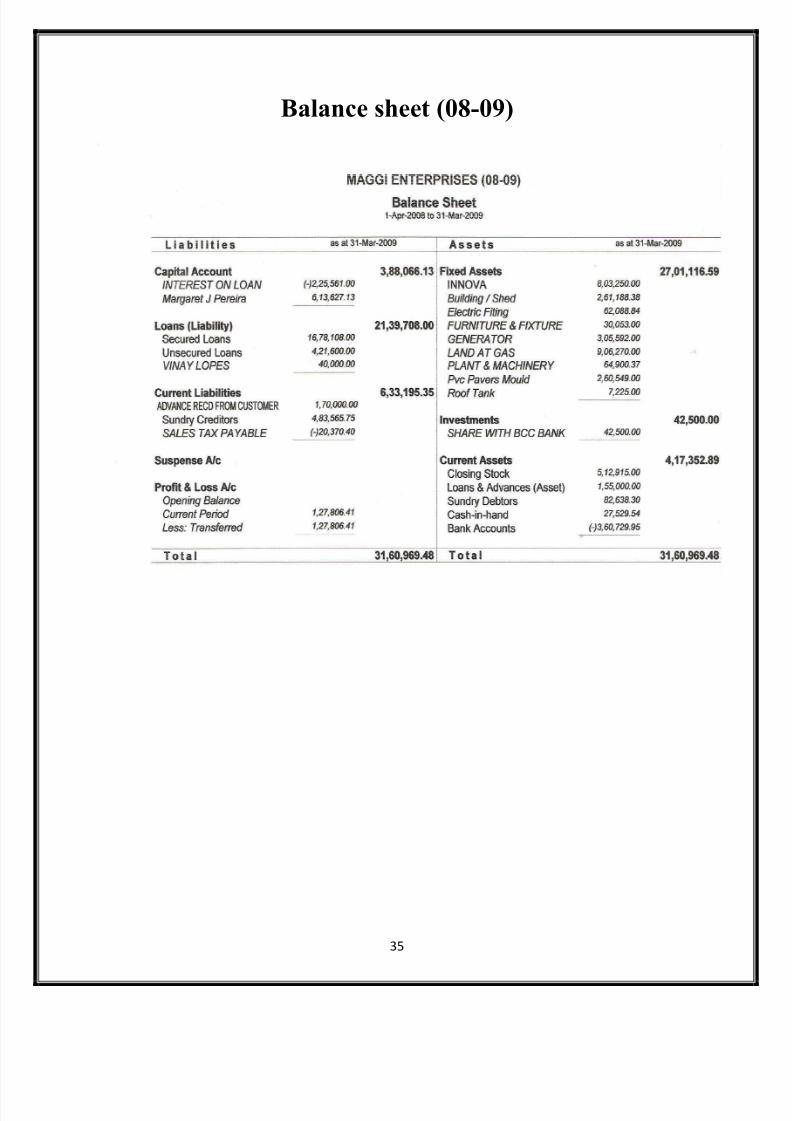

Balance sheet (08-09)

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 36/43

36

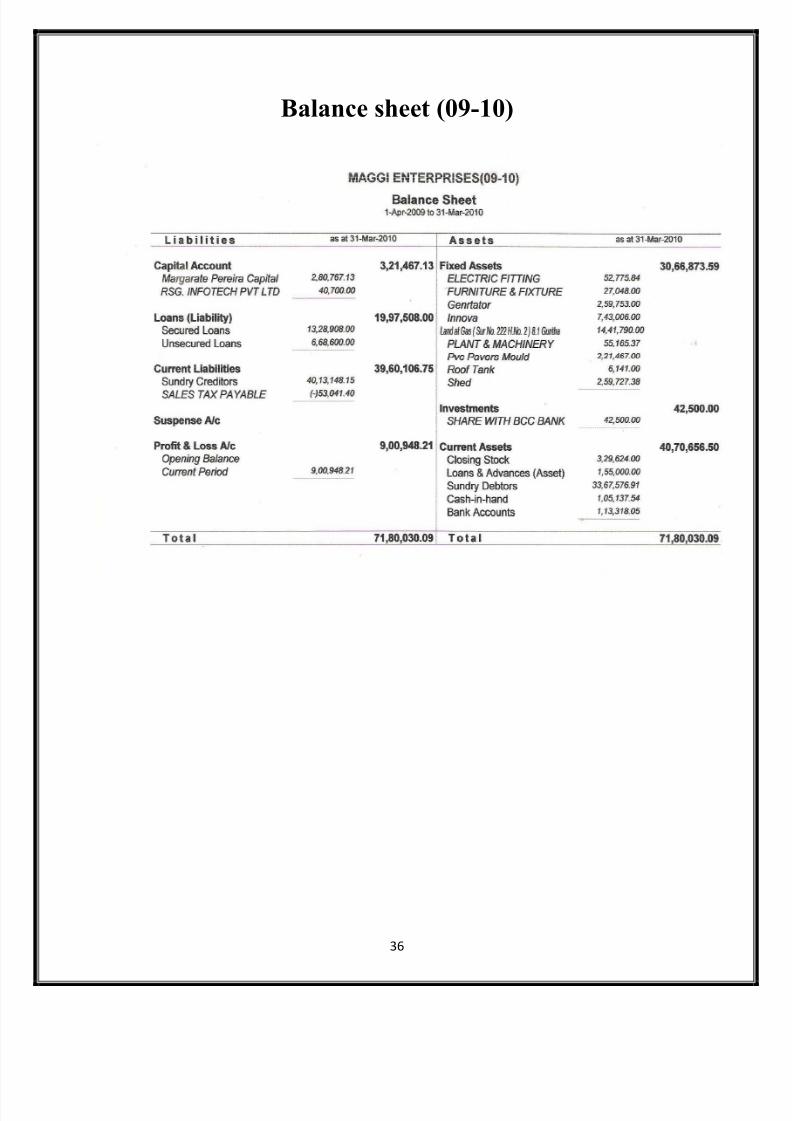

Balance sheet (09-10)

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 37/43

37

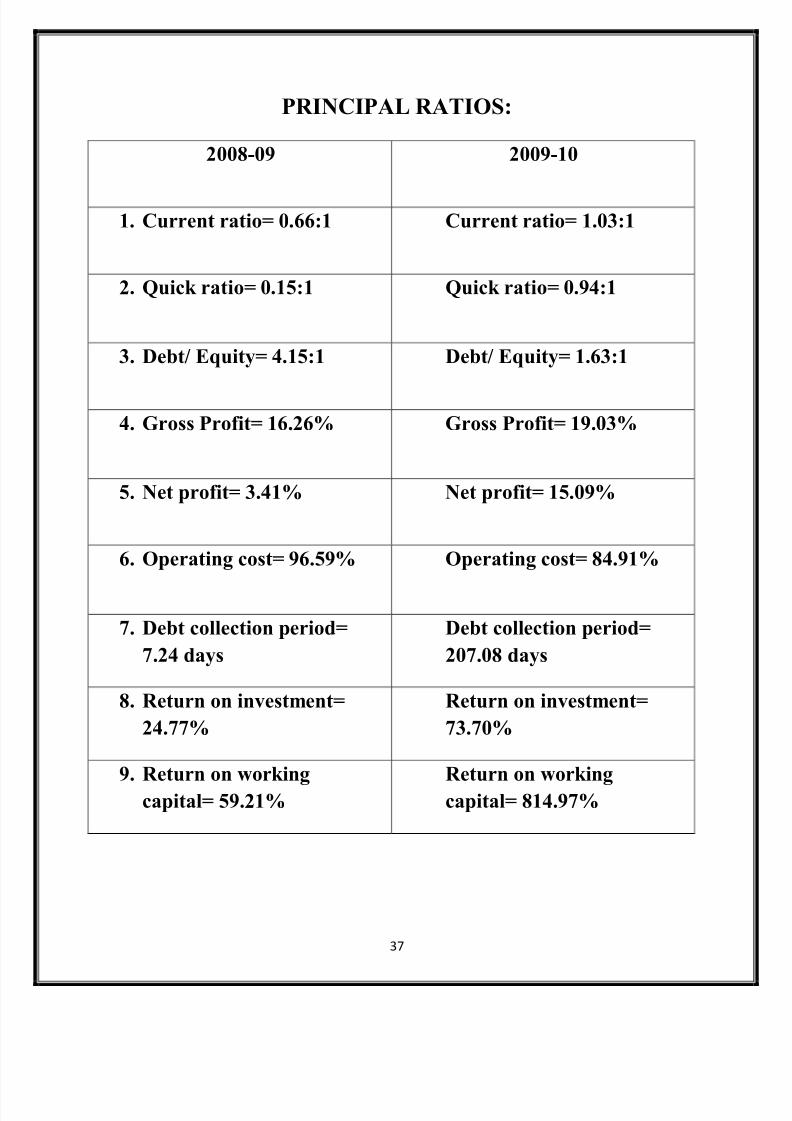

PRINCIPAL RATIOS:

2008-09 2009-10

1. Current ratio= 0.66:1 Current ratio= 1.03:1

2. Quick ratio= 0.15:1 Quick ratio= 0.94:1

3. Debt/ Equity= 4.15:1 Debt/ Equity= 1.63:1

4. Gross Profit= 16.26% Gross Profit= 19.03%

5. Net profit= 3.41% Net profit= 15.09%

6. Operating cost= 96.59% Operating cost= 84.91%

7. Debt collection period=

7.24 days

Debt collection period=

207.08 days

8. Return on investment=

24.77%

Return on investment=

73.70%

9. Return on working

capital= 59.21%

Return on working

capital= 814.97%

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 38/43

38

COMMENTS ON RATIO ANALYSIS

1. The current ratio is increased from 0.66:1 to 1.03:1. Its shows efficiency in

order to meet the standard ratio and indicates stronger financial position. The

standard ratio should be 2:1 but now a day¶s even 1.33:1 is considered.

2. The quick ratio is increased from 0.15:1 to 0.94:1. The standard ratio should

be 1:1. It shows efficiency and stronger financial position.

3. Debt-equity ratio is decreased from 4.15:1 to 1.63:1. This indicates the

company has successfully repaid their debts.

4. Gross profit ratio has increased from 16.26% to 19.03%. It indicates the

efficiency of production and operations.

5. Net profit ratio has increased from 3.41% to 15.09%. It indicates the overall

efficiency of the business.6. Operating cost ratio has decreased from 96.59% to 84.91%. It indicates

company¶s efficiency in controlling operating expenses.

7. Debt collection period has increased from 7.24 days to 207.08 days. It

indicates the company¶s inefficiency in recovery of debts from debtors.

8. Return on investment has increased from 24.77% to 73.70%. It indicates

efficiency in earning capacity and optimum utilization of funds.

9. Return on working capital has increased from 59.21% to 814.97%. It

indicates the efficiency of the company in earning capacity and optimumutilization of the assets.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 39/43

39

CONCLUSION

1. The conduct of internal audit of financial statements helps the organization

prepare financial statements in compliance with the rules and regulations set

by the ICAI.

2. Internal audit helps to identify the errors in the financial statements and

applies different approaches to solve them.

3. It helps to eliminate the inefficiencies in the financial statements in order to

get an adequate financial report.

4. It also helps the organization to identify the emerging risks key risks

involved in its future events and recommends solutions to manage the risks.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 40/43

40

BIBLIOGRAPHY

Name of the book : Financial management

Author: Arvind A. Dhond

Edition: Second Edition.

Name of the book : Mark eting management

Author: Philip K otler, Kevin Lane Keller

Edition: Twelfth Edition.

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 41/43

41

WEBLIOGRAPHY

www.google.co.in

www.wikipedia.com

www.icai.com

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 42/43

42

APPENDIX

UNIVERSITY 100 MARKS PROJECT QUESTIONNAIRE

ST. Francis Institute of Management & Research

MMS 2009-2011

NAME: JOB TITLE:

Q. 1. Why should an organization have internal auditing?

Q. 2. What standards guide the work of internal audit professionals?

Q. 3. What is internal auditing role in preventing, detecting, and investigating

fraud?

Q. 4. What is Enterprise Risk Management (ERM) and what role in it does internal

auditing play?

Q. 5. How do internal and external auditors differ and how should they relate?

Q. 6. What are the most common issues or errors which come across in Auditing of

small scale industries and the ways to solve them?

8/8/2019 Final Project - Copy - Copy

http://slidepdf.com/reader/full/final-project-copy-copy 43/43