Embed Size (px)

Citation preview

FINANCIAL SECTOR ASSESSMENT PROGRAM UPDATE

BRAZIL

FINANCIAL INCLUSION IN BRAZIL: BUILDING ON SUCCESS

TECHNICAL NOTE MAY 2013

INTERNATIONAL MONETARY FUND MONETARY AND CAPITAL MARKETS DEPARTMENT

THE WORLD BANK FINANCIAL AND PRIVATE SECTOR

DEVELOPMENT VICE PRESIDENCY

LATIN AMERICA & THE CARIBBEAN REGION

VICE PRESIDENCY

Pub

lic D

iscl

osur

e A

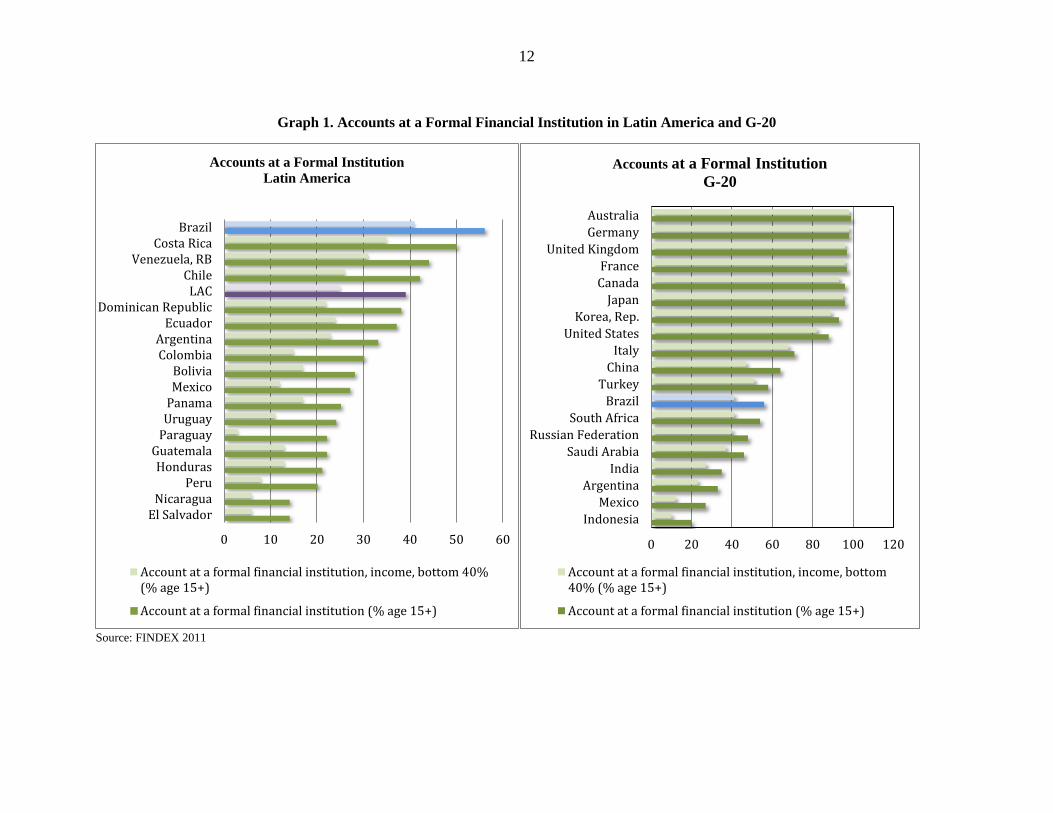

utho

rized

Pub

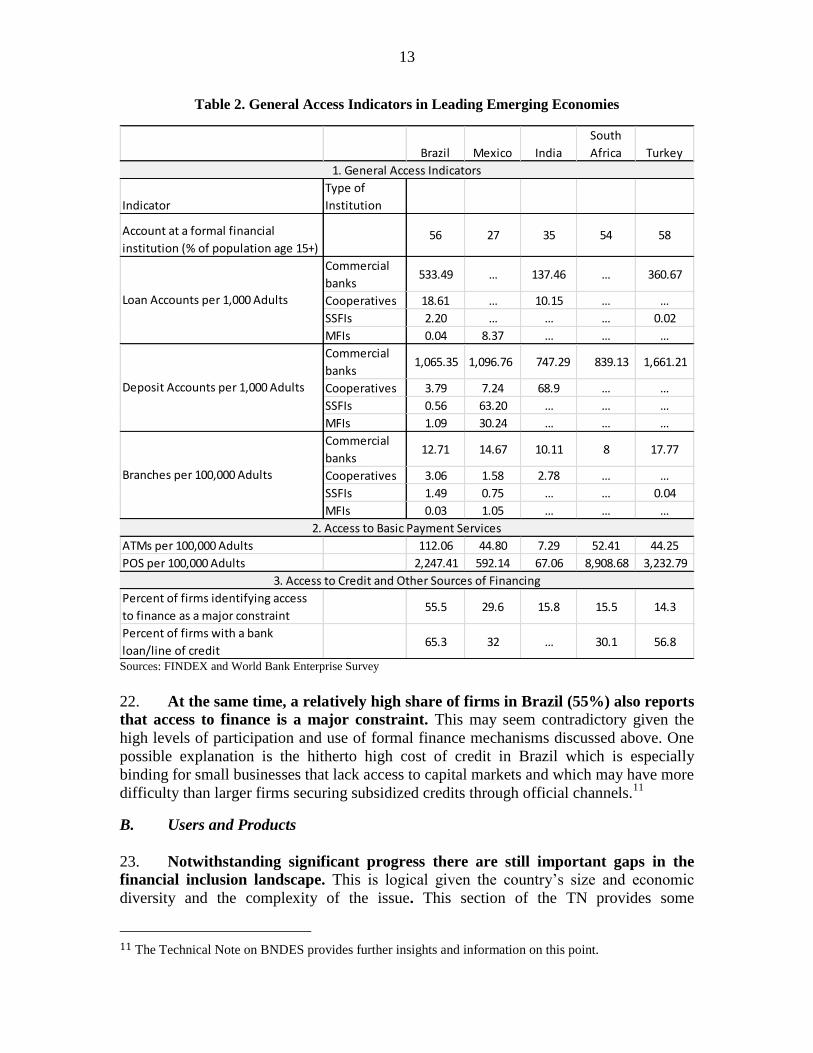

lic D

iscl

osur

e A

utho

rized

Pub

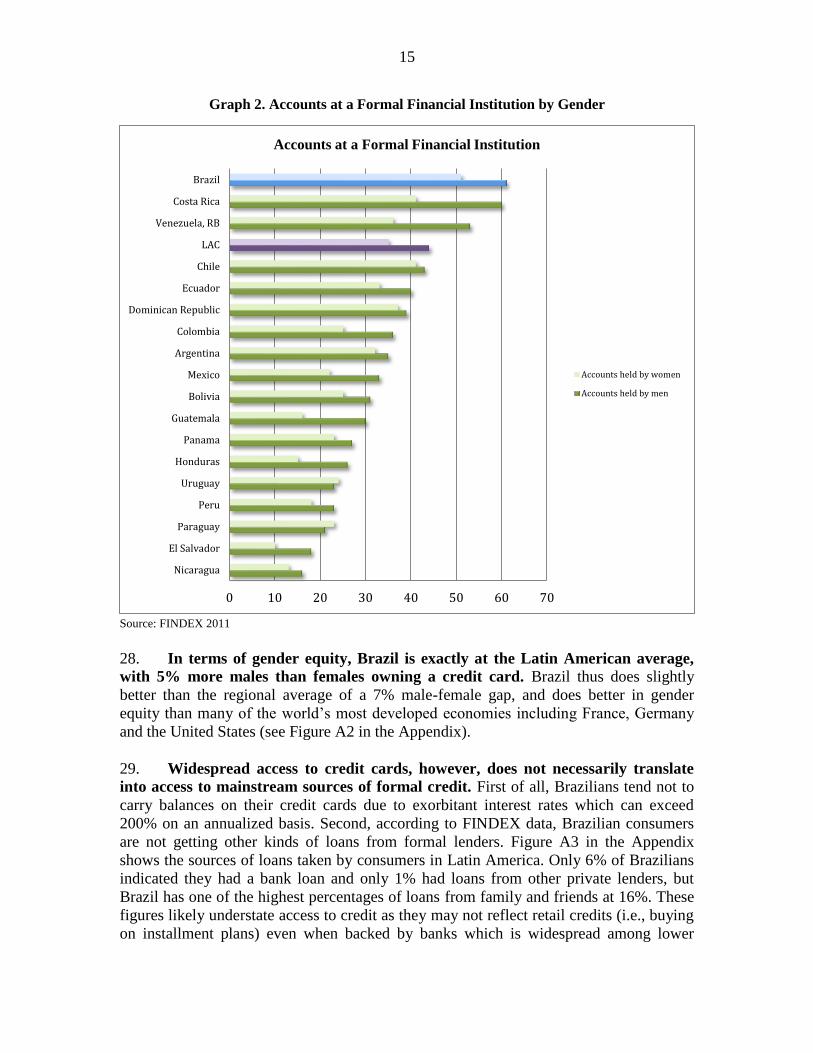

lic D

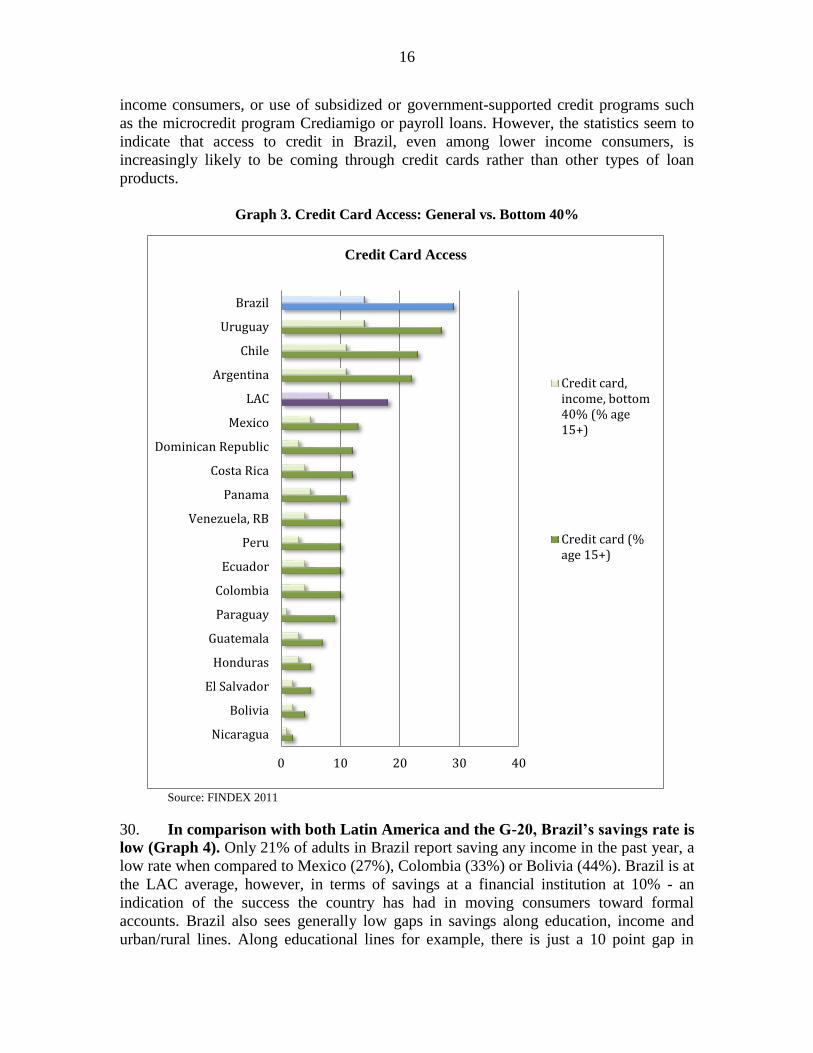

iscl

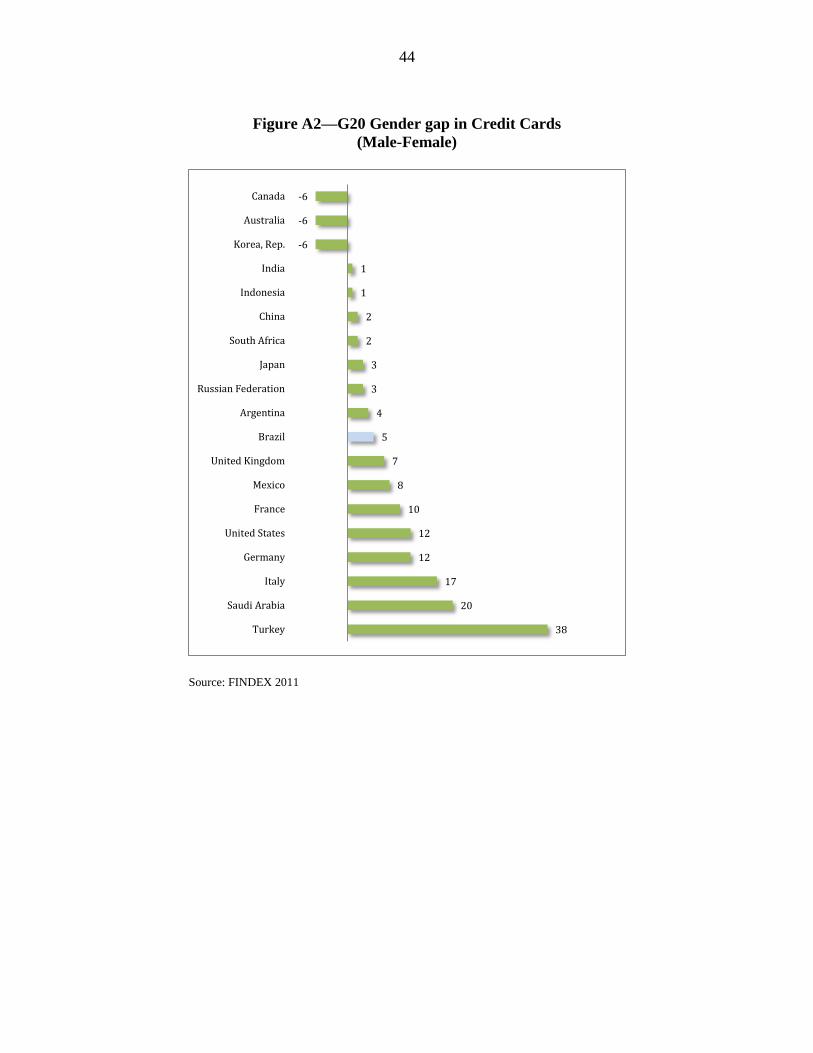

osur

e A

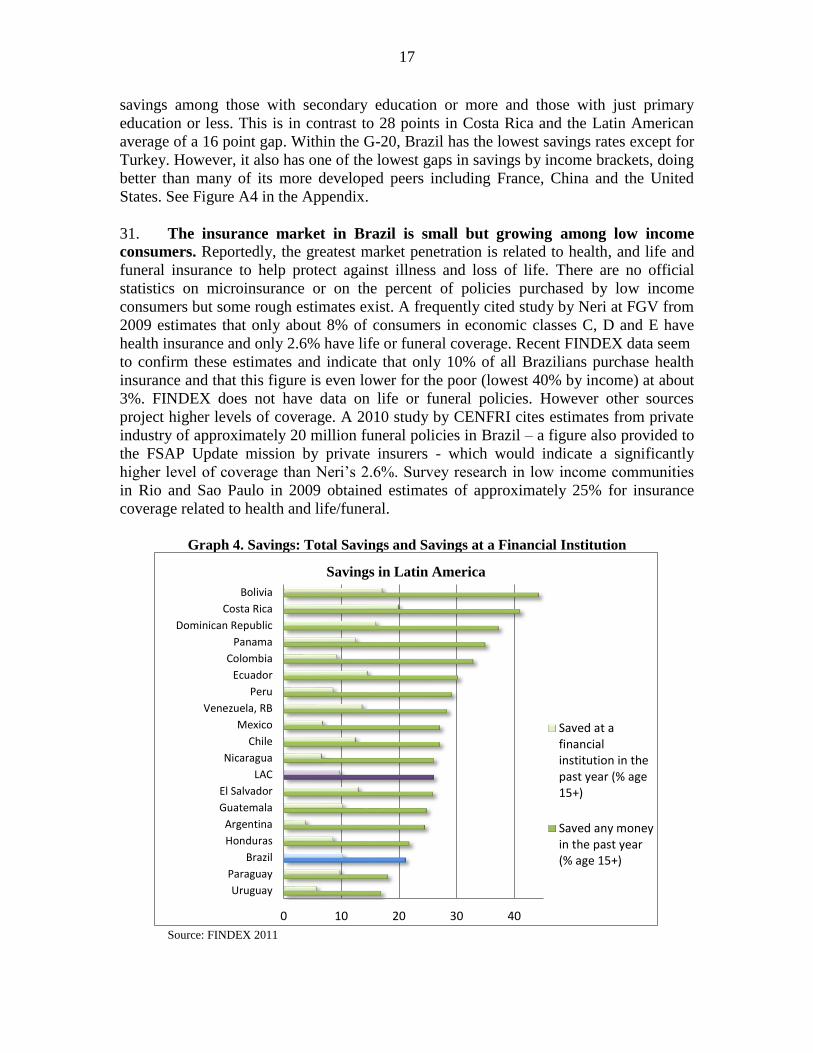

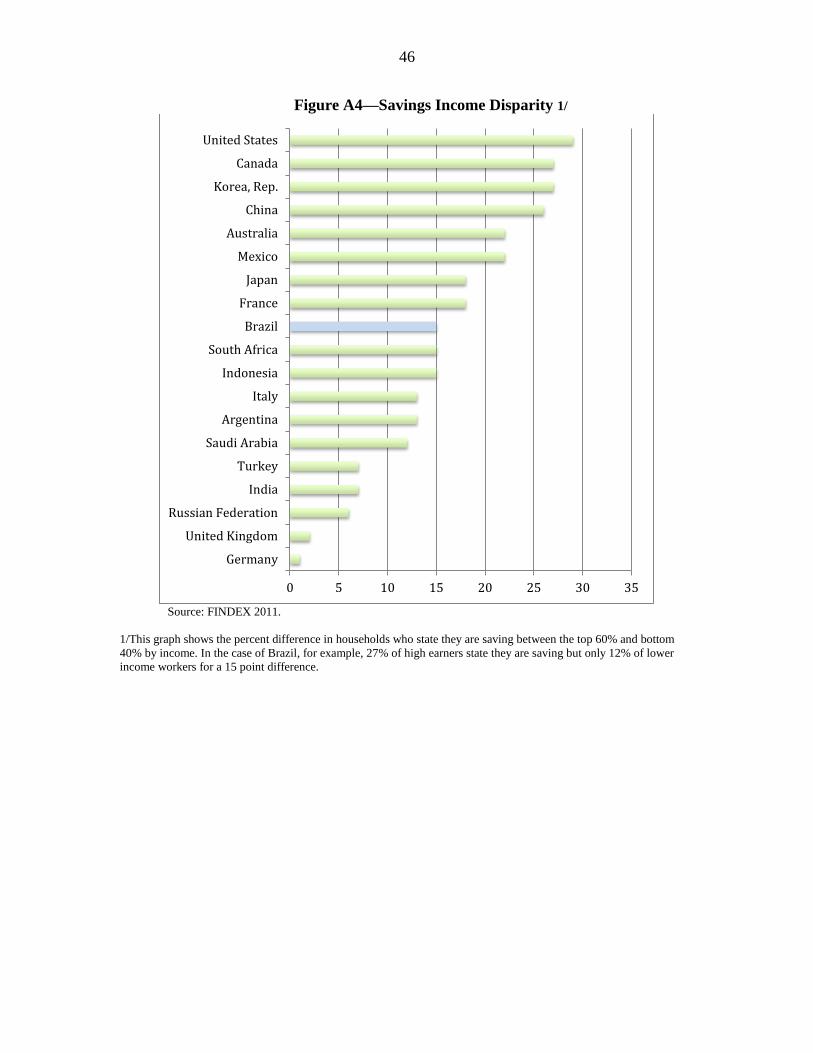

utho

rized

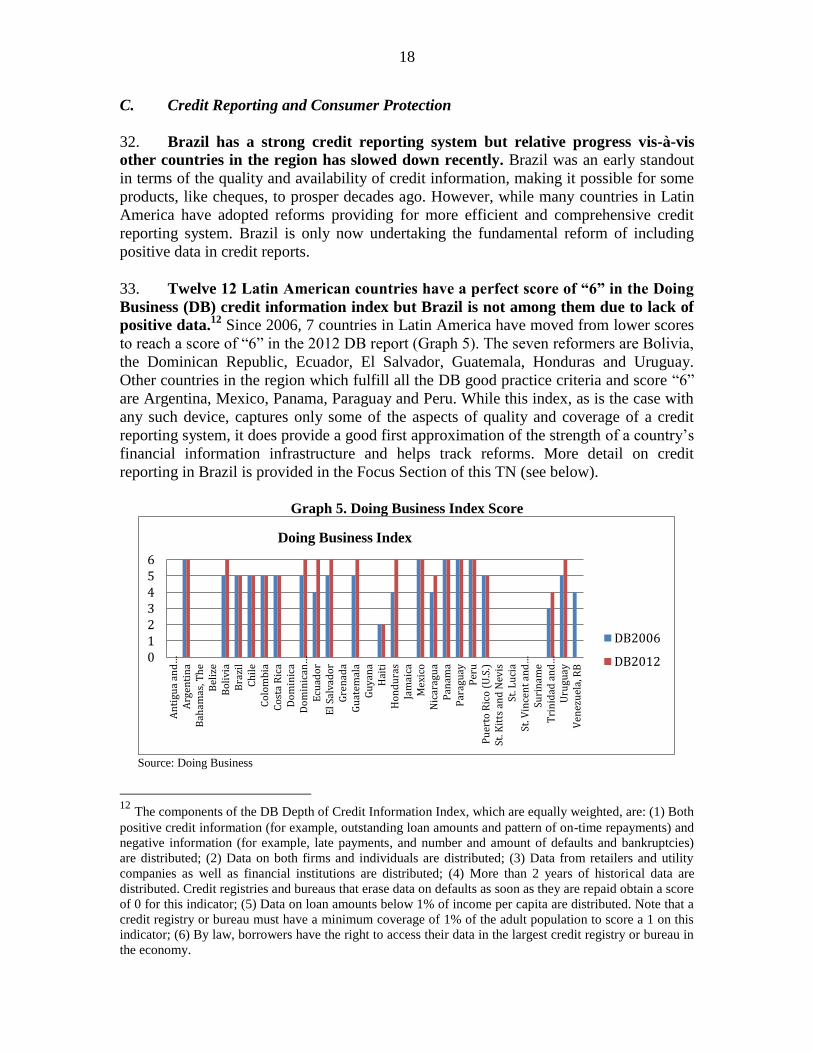

Pub

lic D

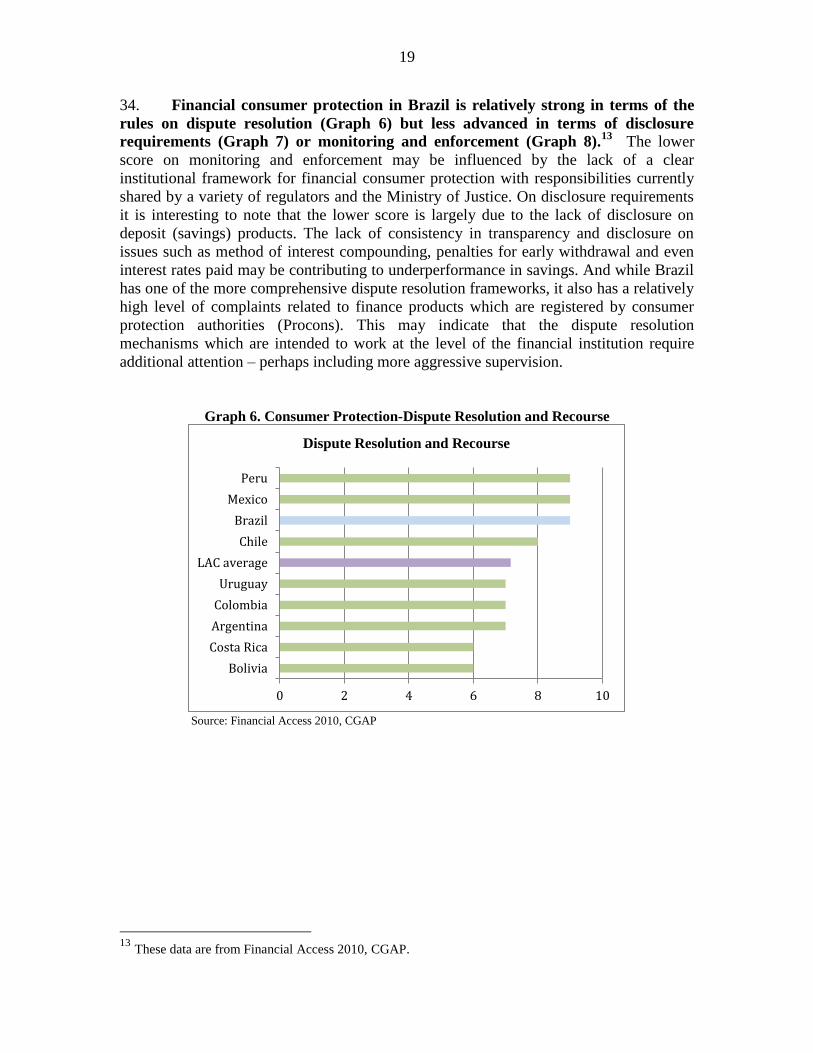

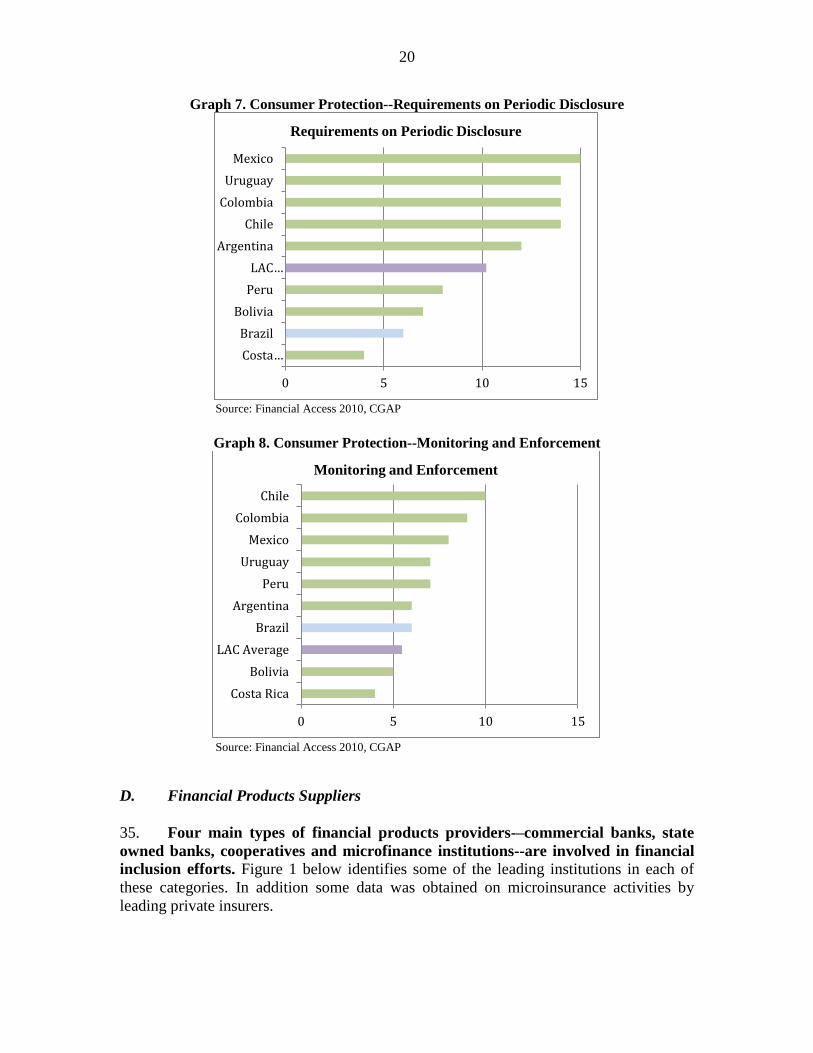

iscl

osur

e A

utho

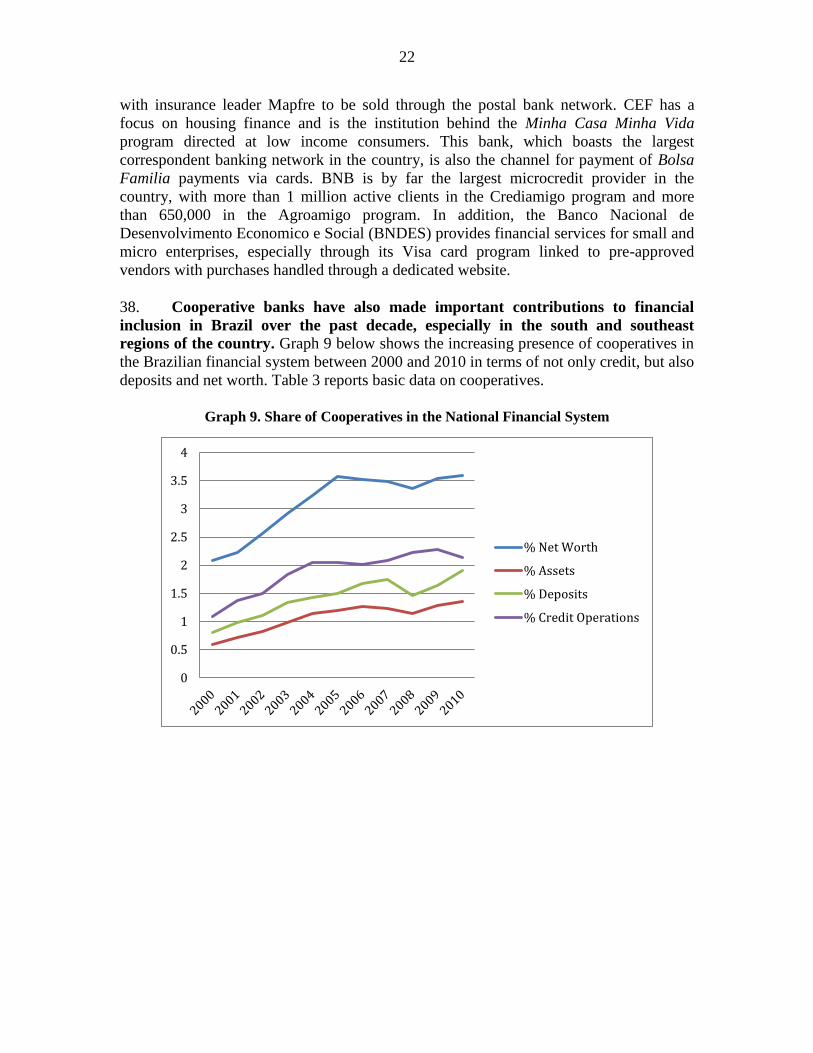

rized

2

Glossary

ATM Automated Teller Machine BB Banco do Brasil

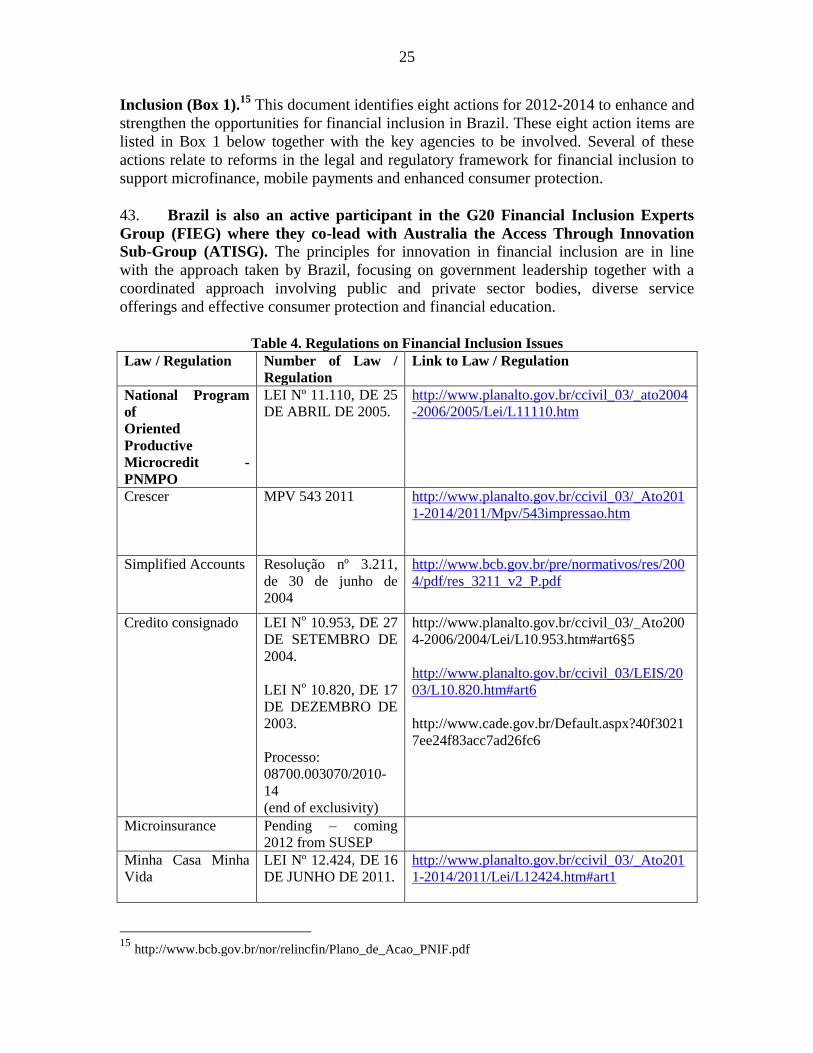

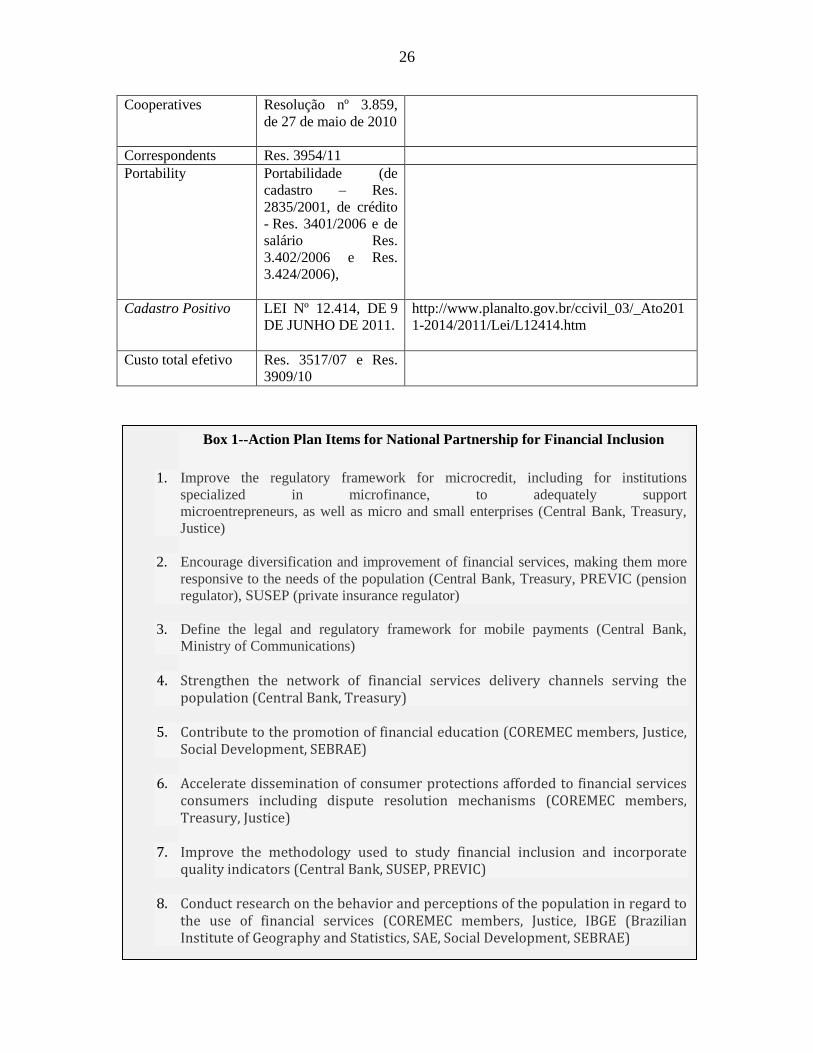

BCB Banco Central do Brasil BM&FBOVESPA Stock Market Exchange BNB Banco Nordeste do Brasil BNDES Banco Nacional de Desenvolvimento

CEF Caixa Economica Federal CONEF Financial Education National Committee

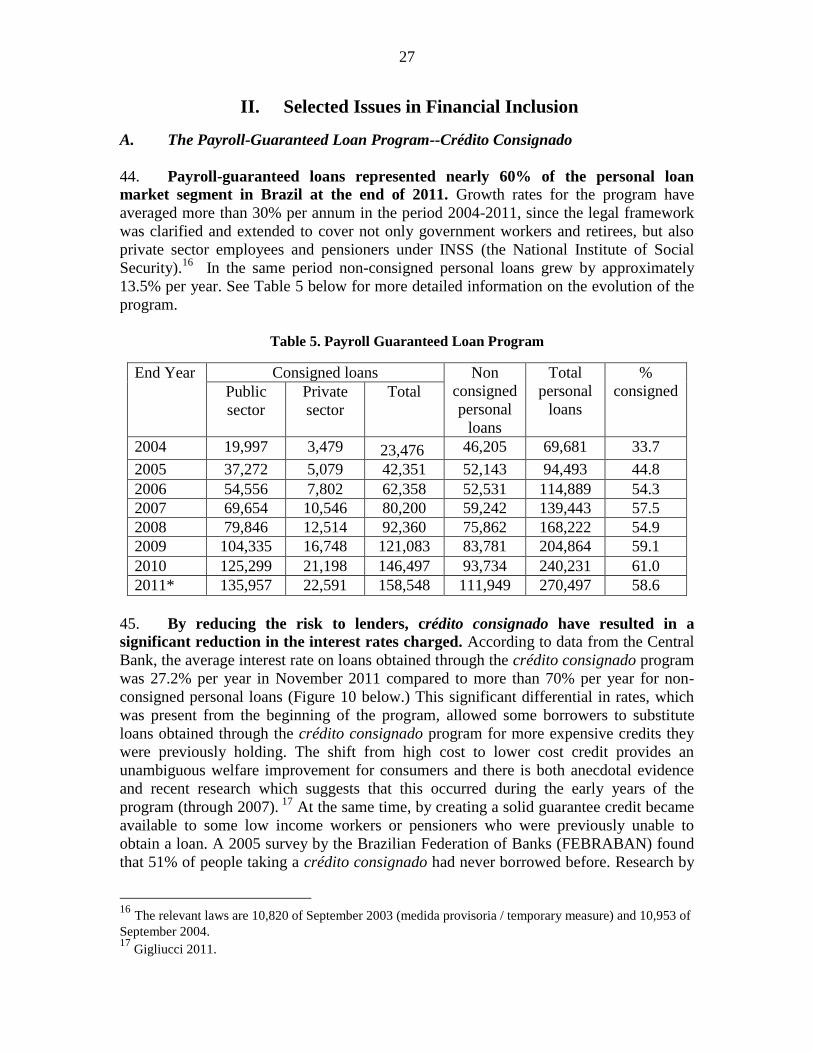

COREMEC Supervisory and Regulatory Committee of Financial Systems,

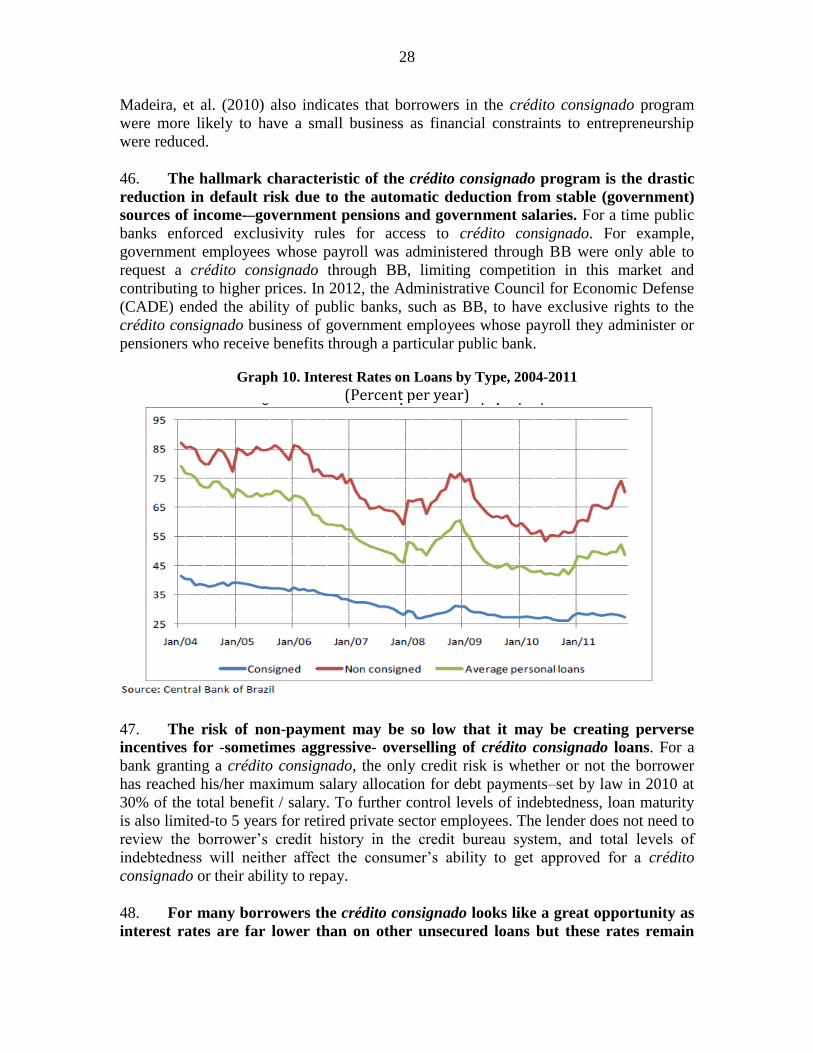

Capital Markets, Private Insurance and Social Welfare

CPL Cadastro Positivo Law

DB Doing Business

DHS Demographic and Health Surveys

ENEF National Strategy for Financial Education FEBRABAN Brazilian Banking Federation FI Financial Institution FINDEX Financial Inclusion Database

FSAP Financial Sector Assessment Program

LITS Life in Transition Survey LSMS Living Standard Measurement Surveys

MFI Microfinance Institution MSMEs Micro, Small, and Medium Enterprises

NGO Non-governmental Organization

POS Point of Sale PRONAF Program for Strengthening Family Farming

SCR Credit Information System

SCPC Serviço de Proteção de Credito

SME Small and Medium Enterprises

3

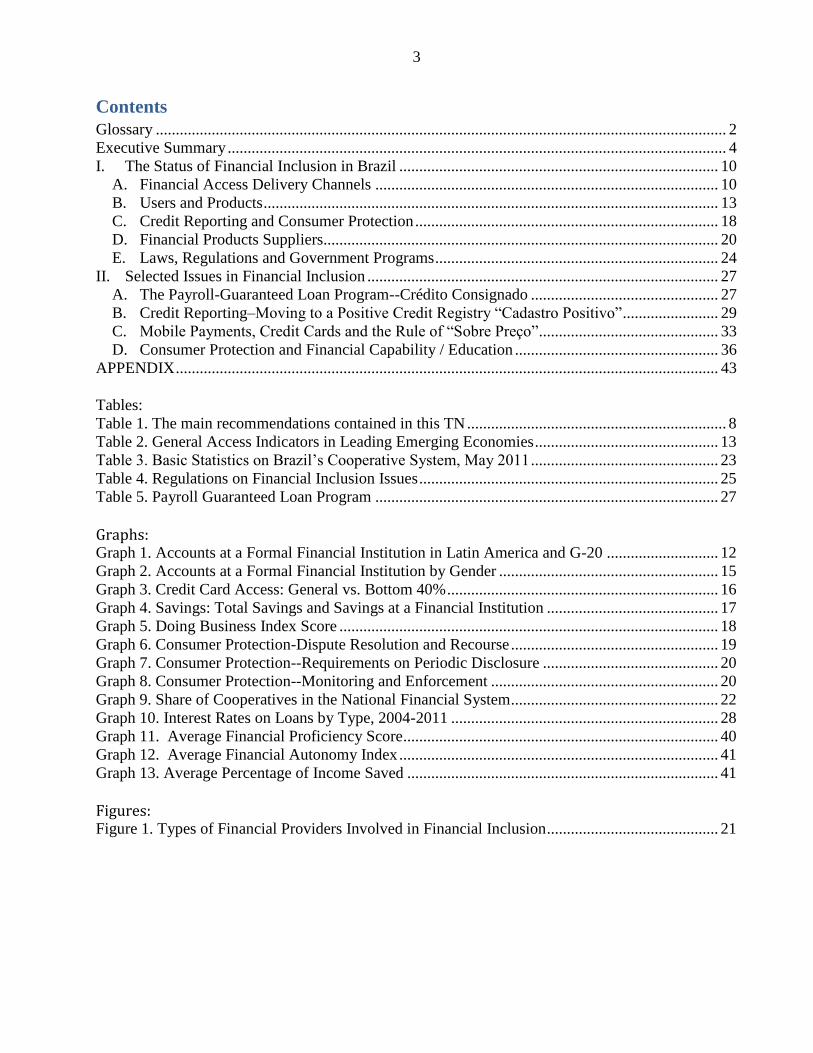

Contents

Glossary ............................................................................................................................................... 2 Executive Summary ............................................................................................................................. 4

I. The Status of Financial Inclusion in Brazil ................................................................................ 10 A. Financial Access Delivery Channels ...................................................................................... 10 B. Users and Products .................................................................................................................. 13 C. Credit Reporting and Consumer Protection ............................................................................ 18 D. Financial Products Suppliers................................................................................................... 20

E. Laws, Regulations and Government Programs ....................................................................... 24 II. Selected Issues in Financial Inclusion ........................................................................................ 27

A. The Payroll-Guaranteed Loan Program--Crédito Consignado ............................................... 27 B. Credit Reporting–Moving to a Positive Credit Registry “Cadastro Positivo” ........................ 29 C. Mobile Payments, Credit Cards and the Rule of “Sobre Preço”............................................. 33

D. Consumer Protection and Financial Capability / Education ................................................... 36

APPENDIX ........................................................................................................................................ 43

Tables:

Table 1. The main recommendations contained in this TN ................................................................. 8

Table 2. General Access Indicators in Leading Emerging Economies .............................................. 13 Table 3. Basic Statistics on Brazil’s Cooperative System, May 2011 ............................................... 23 Table 4. Regulations on Financial Inclusion Issues ........................................................................... 25

Table 5. Payroll Guaranteed Loan Program ...................................................................................... 27

Graphs: Graph 1. Accounts at a Formal Financial Institution in Latin America and G-20 ............................ 12

Graph 2. Accounts at a Formal Financial Institution by Gender ....................................................... 15 Graph 3. Credit Card Access: General vs. Bottom 40% .................................................................... 16 Graph 4. Savings: Total Savings and Savings at a Financial Institution ........................................... 17

Graph 5. Doing Business Index Score ............................................................................................... 18 Graph 6. Consumer Protection-Dispute Resolution and Recourse .................................................... 19

Graph 7. Consumer Protection--Requirements on Periodic Disclosure ............................................ 20 Graph 8. Consumer Protection--Monitoring and Enforcement ......................................................... 20 Graph 9. Share of Cooperatives in the National Financial System .................................................... 22 Graph 10. Interest Rates on Loans by Type, 2004-2011 ................................................................... 28 Graph 11. Average Financial Proficiency Score ............................................................................... 40

Graph 12. Average Financial Autonomy Index ................................................................................ 41 Graph 13. Average Percentage of Income Saved .............................................................................. 41

Figures: Figure 1. Types of Financial Providers Involved in Financial Inclusion ........................................... 21

4

Executive Summary 1. Over the past decade Brazil has made significant strides toward financial inclusion. A

full 100% of Brazilian municipalities are served by some type of facility provided by a formal

financial institution delivering a basic set of financial services1. Factors contributing to this success

include the expansion of a national correspondent banking network, growth in microfinance and

cooperatives and increasing incomes at the base of the economic pyramid due in part to well-

targeted government transfer programs such as Bolsa Familia. As a result of these policies, Brazil

has one of the highest levels of penetration of bank accounts among emerging economies – 56% of

adults in Brazil have an account according to recent FINDEX data. This compares very favorably to

other countries in the region as well as to other large, advanced developing countries globally such

as some of the other BRICs. There is still room for improvement however, to reach the levels of

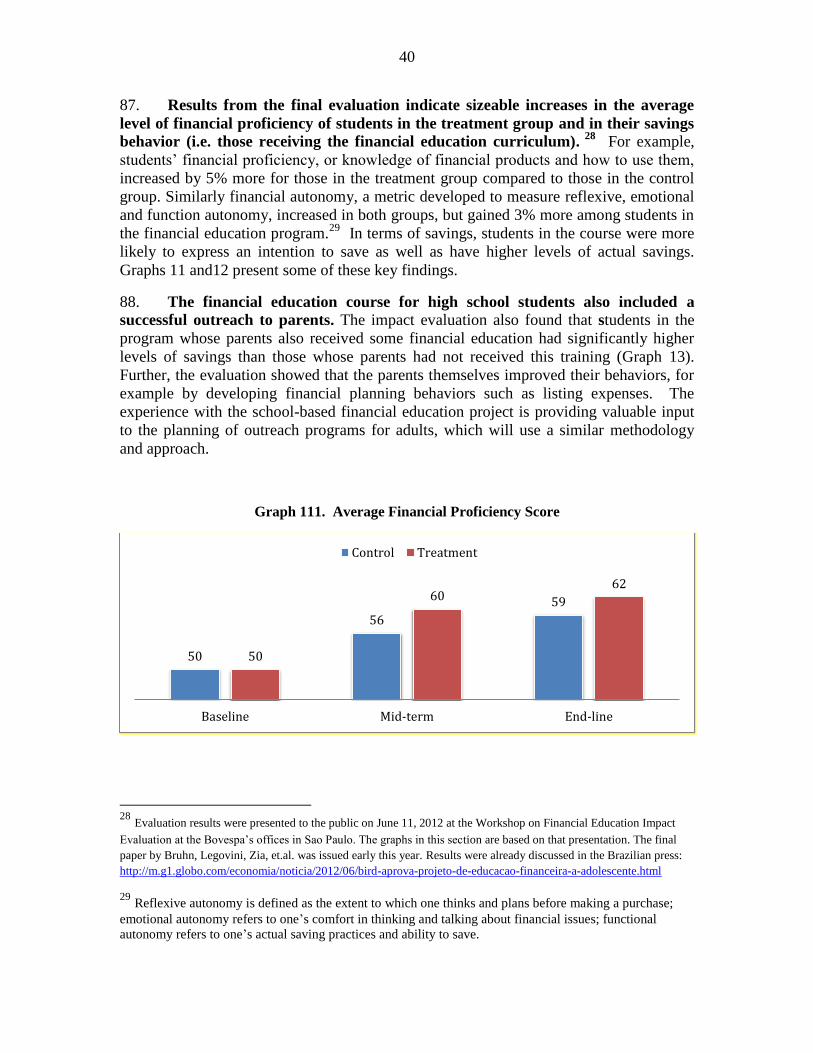

developed countries where coverage levels above 90% are common.2

2. The development of a far reaching correspondent banking network is one of the key

factors behind Brazil’s success story in financial inclusion. Between 2005 and 2011, the number

of correspondents approximately doubled to more than 160,000. The Central Bank encouraged

financial institutions to reach out to more distant consumers and to communities where they had not

previously been active, including lower income areas, through partnerships with a variety of retail

establishments including some with public ties such as the post office network and lottery agencies.

Regulators have gradually reduced restrictions on correspondent banking, such as individual

approval processes, in response to early successes with this program. The legal framework also

facilitated healthy expansion by putting the onus on regulated institutions to train and monitor their

correspondents.

3. A variety of government programs have also played a pivotal role in financial inclusion

efforts. In terms of Bolsa Familia, not only have incomes been raised--thus indirectly encouraging

access to finance--but the program itself has also been used as an instrument of financial inclusion.

All Bolsa Familia recipients receive their benefits through electronic cards from Caixa and more

than 2 million of the 13 million beneficiaries have opened a Caixa bank account. In terms of

microfinance, the vast majority (about 75%) of customers are served by the Crediamigo program at

Banco Nordeste do Brasil (BNB) which today has nearly 1 million active loan accounts. In terms of

rural credit, PRONAF, distributed in part by the Agroamigo program at BNB, is responsible for

providing access to finance for family farmers / producers – about R$ 12 billion in agricultural

credit was provided in both 2010 and 2011. Other government programs also have promoted access

to credit including notably the crédito consignado programs provided through government funded

pensions or through salaries of government employees.

4. While much has been accomplished, the financial inclusion agenda is far from

complete. Handling payments, including those related to paying utility bills and the monthly

government benefit, remains the primary service performed by many correspondent banks. The

range of financial services that people need beyond payments– including savings, credit and

insurance--is still not readily available for many low income consumers. Progress has also been

unbalanced along other dimensions. Credit products have expanded more rapidly and become more

1 Data on access points are available on the Brazilian Central Bank website: http://www.bcb.gov.br/?MICROFIN 2 See map of bank account coverage by country in Appendix, Figure A1.

5

widespread than savings products, creating a potential for unhealthy levels of indebtedness. The

expansion of access has also been tilted toward higher income regions–the South and Southeast–

especially in terms of numbers of correspondents and the growth of financial cooperatives.

Microinsurance, while growing, is still relatively underdeveloped and focused on a few limited

markets such as funeral insurance.

5. Increased attention should be given to developing savings habits to further strengthen

financial inclusion while buttressing financial stability, According to 2011 Findex data, only

one-fifth of adults in Brazil reported saving any money in the previous year, and only one-tenth

saved money in a formal financial institution. As a result, 90% of savings in Brazil are generated by

the corporate sector. This situation is striking, especially given Brazil’s income level. Among upper

middle income countries more than twice as many adults usually have formal savings. Brazil’s

comparatively generous pension system is likely one factor behind low levels of personal savings,

together with widespread access to retail consumption credit and possibly still some behaviors

linked with price instability of years past. On the supply side, traditional disincentives for

promoting small savings accounts (relatively high costs) as well as high reserve requirements on

deposit accounts and access to alternative sources of financing have limited expansion of savings

products. Addressing the savings issue is thus at the heart of a number of fundamental financial

sector and fiscal reforms.

6. Rapid expansion of credit over the past four years has created the potential for

unhealthy levels of debt, especially in lower income households. Aggressive promotion of low

cost loans through Crediamigo (now even more affordable due to the Crescer program), PRONAF,

and crédito consignado programs have increased access to credit and, correspondingly, the levels of

debt. In the private sector, many low income consumers in economic class “C” have also gained

access to ubiquitous store-credits which largely finance consumption, and for those with slightly

higher incomes, to auto loans. These factors have raised concerns that some low income consumers

are getting “in over their heads” in debt and are vulnerable to a negative financial shock to the

household (e.g., loss of employment, health problem, death in the family) or to the broader

economy (e.g., recession, interest rate spike). Fully analyzing the extent of over-indebtedness is not

readily possible, as comprehensive data on the level of debt among low income consumers in Brazil

is not available. However, the rapid growth of credit programs, especially in the past 2-4 years, and

concerns among many stakeholders in the financial inclusion arena would suggest that increased

attention be given to this potential problem.

7. The regulation of the recently enacted positive credit histories law has the potential to

greatly improve market intelligence, and competition and efficiency in financial markets.

Properly implemented, the so-called Cadastro Positivo Law (CPL) should improve risk analysis and

increase competition for good borrowers, putting downward pressure on interest rates. However, the

CPL requires consumers to “opt in” to the system by authorizing their participation in writing. This

will make the positive data registry harder and more costly to construct and there will be a greater

lag in creating a comprehensive positive credit history than if the “opt out” approach had been

adopted.3 In this scenario there is a risk that the benefits of the CPL will not materialize quickly and

3 Through an “opt out” approach, consumers would be included in the database unless they took the initiative to have

their data removed (i.e. through an online process, writing a letter, signing a form at their bank or some other

mechanisms which should be fairly easy for consumers to access).

6

public perceptions will be that it has had no effect further reducing willingness to participate. How

the law is regulated and the development of a public information campaign supporting the reform

will significantly affect its impact. The addition of positive credit histories also increases the need

for an enhanced supervisory and regulatory framework for credit bureaus to strengthen public

confidence in the system and thus participation.

8. Clarifying the roles the Central Bank’s credit registry SCR could play is highly

relevant to the CPL discussions. The SCR has a very granular and extensive coverage of banking

loans with both positive and negative information, but only regulated financial institutions have

access to these data. Further, the Central Bank is not in a position to develop commercial credit

scoring models based on the SCR–one of the key offshoots/tools that such databases typically

provide to a financial market. In any case, there is a need to clearly define the SCR’s roles in the

financial system including its contribution to the supervision of regulated institutions, its direct use

for credit risk analysis by lenders, and its potential for strengthening the credit reporting industry

while fostering competition and transparency in the financial system. Other countries in the region,

for example, share some data from the public registry with private credit bureaus who meet certain

criteria such as licensing or other regulatory requirements.4

9. There has been progress in the regulation of the payment card processing industry

recently but further reforms are needed. A 2010 government report identified multiple issues on

competition in this industry.5 Some of the recommendations from this report have been

implemented, but the industry remains highly concentrated with two acquirers – Cielo and Redecard

– occupying more than 80% of the market. Market dynamics have resulted in high merchant fees as

well as very high interest rates for those consumers who carry balances. A potential area for reform,

which could put some downward pressure on card costs and reduce consumers’ incentives to use

cards, relates to restrictions on price differentiation by type of payment instrument (the so-called no-

surcharge-rule). However, the Department for Protection and Defense of Consumers understands

that allowing such price-differentiation would not be in line with the Consumer Defense Code.

Since lower income consumers are less likely to use payment cards, they are in effect cross

subsidizing consumers who are using credit cards, including high income consumers that receive

benefits through loyalty programs. This rule also reduces the ability of merchants to negotiate the

fees charged, further enhancing the market power of the large card processors. While there are

many good reasons to promote electronic payment systems on costs, efficiency, informality

reduction, and tax evasion grounds these systems should be competitive – and if they are not may

require further policy action. The development of mobile payment solutions which do not need to

be processed through the card companies and legal clarity on the use of post-dated checks would

also help stimulate competition and reduce costs in the payment and broader financial systems.

10. Virtually every financial inclusion stakeholder identified financial education as a

priority to help address issues of over-indebtedness, lack of savings, financial products selection,

and insurance products consumption. The first major financial education project undertaken by

CONEF (the national partnership for financial education) has focused on developing financial

4 Examples include Argentina and Ecuador. 5 “Report on the Brazilian Payment Card Industry 2010” by the Central Bank of Brazil, the Secretariat of Economic Law of the Ministry of Justice (SDE), and the Secretariat for Economic Monitoring of the Ministry of Finance (SEAE). http://www.bcb.gov.br/Pom/Spb/Ing/Payment_Cards_Report.pdf

7

capability in high schools, and has just completed its pilot phase. The rigorous impact evaluation of

the program recently completed found statistically significant increases in financial autonomy,

financial proficiency and savings behavior. Efforts are in the early stages to develop adult financial

education but these are not yet being implemented (likely roll out in late 2012 or 2013). Mapping

existing financial education priorities and gaps and linking these findings to the upcoming adult

education initiatives should be given priority.

11. Strengthening financial consumer protection would support sustainable access to

finance. There are a relatively high number of complaints about financial services providers

registered with the Ministry of Justice. Unlike the case of financial education, which was

championed by the committee of financial market regulators (COREMEC), responsibility for

consumer protection is mainly with a unit at the Ministry of Justice which has very limited

resources and no staff dedicated solely to financial market issues. To be sure, there have been some

recent efforts to strengthen consumer protection—e.g., this unit became a Secretary level unit in

May 2012—but more is needed, especially when it comes to new financial consumers.

12. Going forward, identifying ways to encourage innovation and competition in financial

markets – such as through mobile banking and mobile payment - will help expand inclusion

and contribute to improved product and service quality. In the specific case of mobile banking,

providing regulatory flexibility/space for more experimentation or pilots would be a useful way to

promote this channel which could be especially important for access in less populated and less well

served rural communities. Identifying ways to use public policies to create more competition in

financial products and services rather than further concentrating activities with the major state-

owned financial institutions would also help promote more efficient targeting of government funds.

13. Modest investments in more systematic, rigorous, and independent impact evaluations

of financial inclusion government programs and policies would pay large dividends in terms

of efficiency and effectiveness of the use of public funds. Some programs and policies have been

reviewed for impact, such as the aforementioned school-based financial education program.

However, external sources are typically needed to fund such evaluations. Creating even a small

fund for impact evaluation, perhaps supported by external donors who are active in this space, could

provide valuable information for better targeting limited public resources.

14. This Technical Note (TN) does not include an analysis of the causes underlying Brazil’s

continued high credit cost but many of the issues discussed here may be contributing factors. These include the lack of savings and related dependence on credit which may reduce price

elasticity in credit markets; information asymmetries which add to the cost of credit evaluation and

increase risk for lenders; and competition issues (as with mobile payments and the so-called no-

surcharge-rule on payment methods). The Aide Memoire for the FSAP Mission provides further

discussion of these important issues.

8

Table 1--Technical Note: Main Recommendations

Summary of Issues and Recommendations Issue Observations and Recommendations

Credit Incentives Numerous government programs provide highly subsidized credit for low income

consumers (microfinance, agricultural credit, housing credit, etc.) or facilitate credit

access (so called “payroll loans” backed by public sector wages or pensions). In the

case of subsidized programs, sustainability is an issue as well as market distortions

which discourage new entrants or competition. For the payroll loan program, the very

limited default risk faced by lenders creates incentives issues including the possibility

for overselling these loans to consumers who may not need them or fully understand

the cost. As a first step, further rigorous impact evaluation of these programs and their

costs and benefits would be useful in determining next steps including more narrowly

targeting subsidies, identifying other needed policies or programs and if necessary

regulatory reforms.

Savings Promotion Regulatory barriers and a generous pension system, together with increased access to

unsecured credit for consumption purchases, create a disincentive for mobilizing

savings on both the supply and demand sides. Addressing both macro and micro level

factors will be necessary to substantially increase savings in Brazil. In terms of

financial inclusion policies, actions could include strengthening basic accounts which

offer savings instruments (and determining why they have or have not worked to

promote savings in the past), identifying ways to promote and encourage savings (such

as through lotteries which are already popular), increasing financial education efforts

and enhancing disclosure on credit (so comparisons with the cost of credit vs. saving

for consumption are clearer).

Cadastro Positivo

Law (CPL)

The new CPL would promote greater transparency and competition in financial

markets and contribute to efforts to reduce the cost of credit. However, the way this law

is implemented will affect its impact. Since it requires consumers to “opt in” or

authorize their participation in writing, the public outreach campaign will be very

important as well as the specific requirements on how permission is collected and how

it relates to existing credit bureaus. Establishing a clear legal and regulatory

framework, including effective supervision/enforcement for credit reporting will be

critical for increasing consumer confidence and participation.

Mobile Payments Efforts are already underway involving the Central Bank and the Ministry of

Communications to develop regulations for mobile payments. This should help create

the clarity needed as well as the regulatory flexibility/space for more experimentation

and investments in this channel which could be especially important for access in less

populated and less well served rural communities. A related issue is the merchants’ so-

called no-surcharge-rule that prevents them from charging different prices for different

payment methods. This should be reviewed as it likely is resulting in increased market

power for leading card processors vis-à-vis merchants (especially small ones) and

transfers from low-income cash using consumers toward higher-income card using

9

consumers; market power of card processors may also be affecting the development of

alternative channels such as mobile payments.

Consumer

Protection and

Financial

Education

Consumer protection and financial education are gaining increasing attention as part of

Brazil’s financial inclusion strategy. The government has been active in developing a

thoughtful approach to financial education through a school-based financial education

program which is a global model of good practice in terms of how it was designed,

piloted and evaluated. Future work is to extend financial education to adult populations.

On the financial consumer protection front, there remains ambiguity on roles and

responsibilities. The Ministry of Justice has jurisdiction on this topic but limited

capacity or specialized knowledge. Thus far the approach has been to create

committees between Justice and the Central Bank to overcome these limitations. An

independent evaluation of the framework for financial consumer protection in Brazil

could help identify key issues and gaps and help further strengthen these efforts.

10

I. The Status of Financial Inclusion in Brazil6

15. This section compares progress on financial inclusion in Brazil with regional

comparators as well as with some nations outside Latin America with similar or higher levels

of income. Data are taken from a variety of sources7 including:

o The Global Financial Inclusion (Findex) Database which provides the first

internationally comparable survey-based demand side data on access and use of

financial products, services and infrastructure;

o Financial Access 2010 which has supply side data including detailed information on

financial consumer protection worldwide; and

o Doing Business for data related to credit information.

16. Brazil has made great strides in financial inclusion over the past decade and now leads

the region in terms of percent of population with an account in a formal financial institution

(Graph 1 and Table 2). In Brazil, 56% of the population has an account with a formal financial

institution, compared to a regional average in Latin America of only 39%. This figure is above other

middle income countries in the region which have per capita incomes significantly higher than

Brazil’s – by about 50% or more – such as Argentina (33%), Chile (42%) and Uruguay (24%).

When compared with other G-20 countries, however, Brazil still trails developed country

experiences which are typically in excess of 90% coverage (and in several cases nearly universal at

100%). Brazil is also behind China which reports 64% of the adult population is “banked”.

A. Financial Access Delivery Channels

17. Gaining access to bank accounts in Brazil has been greatly facilitated by the

correspondent banking network which numbers approximately 152,000 locations throughout

the country.8 This network complements the much smaller number of traditional bank branches

(approximately 20,000) reducing the costs and increasing the convenience of performing basic bank

transactions including opening accounts, making deposits and withdrawals, and applying for small

loans. Financial inclusion statistics on bank branches in Brazil, estimated at 12.7 per 100,000 adults,

do not capture this vast correspondent network which is unique in its size and scope.

18. In terms of access to Automated Teller Machines (ATMs) Brazil is also far ahead of

other countries in Latin America, and globally, with 121 ATMs per 100,000 adults. Comparator countries in the region – including several with higher per capita incomes - have only a

fraction as many ATMs per 100,000 adults including Argentina (42), Chile (63) and Uruguay (30).

The ATM network in Brazil is unusual in its size even by high income country standards and

exceeds those in Germany (117), France (110), Italy (99) and the U.K. (65). Only a few countries

have larger networks including the U.S. (174), Canada (220) and Korea (250). One possible

explanation for the Brazilian numbers is the fact that in the country most ATM networks are not

shared and so there is a lack of interoperability. A low level of interoperability implies a lower

average number of transactions per terminal, overlapping of ATMs, (which reduces the capillarity

of the network) and higher costs of development and maintenance.

6 This Technical Note (TN) was prepared under the March 2011 FSAP Update for Brazil by Margaret Miller (World Bank).

7 Additional country specific data on market/financial intermediary structure are available in the FSAP Aide Memoire, Chapter 2 and

in the Appendixes.

8 Data as of June 2010, from Central Bank of Brazil website: http://www.bcb.gov.br/?MICROFIN.

11

19. Brazil also stands head and shoulders above other countries in Latin America in terms

of the spread of Point of Sale (POS) technology, with 1,471 terminals per 100,000 adults.

Penetration is much higher than in other countries in the region--Chile (450), Panama (427) or

Uruguay (275). The spread of POS technology in Brazil has not reached high income country

levels, however, which often exceed 2,000 per 100,000 adults (examples include Italy, France, the

U.K., U.S. and Canada) and in a few instances even 3,000+ per 100,000 adults (Australia, Turkey).

Similarly to the ATM network, POSs do not have full interoperability which results in a high level

for the merchant discount rate compared to other countries.

20. Mobile payments via cell phones in Brazil have just barely begun to develop and are

reportedly used by only about 1% of the population. The figure for online electronic payments is

significantly higher with 6% of low income consumers using this method.9 Checks are another

common form of payment among higher income Brazilians but are less frequently available to low

income consumers – according to FINDEX data only 2% of low income Brazilians use this payment

channel.

21. While this report focuses primarily on consumer or personal finance, not enterprise

finance, it is useful to briefly review some basic statistics on finance available to micro and

small enterprises.10

Approximately two-thirds of firms in Brazil indicate that they have a bank

loan or line of credit according to data collected through the World Bank’s Enterprise Surveys

(Brazilian data from 2009). This is a relatively high share compared to other emerging economies

such as Mexico (32%), South Africa (30%) or Turkey (59%). Virtually all Brazilian firms (99.4%)

also report having a checking or savings account and almost half (48%) say that they are using

banks to finance investments.

9 Data cited are from FINDEX 2011. 10 A focus on consumer / personal finance was agreed with the Brazilian Government for this FSAP Update Financial Inclusion TN.

12

Graph 1. Accounts at a Formal Financial Institution in Latin America and G-20

Source: FINDEX 2011

0 10 20 30 40 50 60

El SalvadorNicaragua

PeruHonduras

GuatemalaParaguayUruguayPanamaMexicoBolivia

ColombiaArgentina

EcuadorDominican Republic

LACChile

Venezuela, RBCosta Rica

Brazil

Accounts at a Formal Institution

Latin America

Account at a formal financial institution, income, bottom 40%(% age 15+)

Account at a formal financial institution (% age 15+)

0 20 40 60 80 100 120

Indonesia

Mexico

Argentina

India

Saudi Arabia

Russian Federation

South Africa

Brazil

Turkey

China

Italy

United States

Korea, Rep.

Japan

Canada

France

United Kingdom

Germany

Australia

Accounts at a Formal Institution

G-20

Account at a formal financial institution, income, bottom40% (% age 15+)

Account at a formal financial institution (% age 15+)

13

Table 2. General Access Indicators in Leading Emerging Economies

Sources: FINDEX and World Bank Enterprise Survey

22. At the same time, a relatively high share of firms in Brazil (55%) also reports

that access to finance is a major constraint. This may seem contradictory given the

high levels of participation and use of formal finance mechanisms discussed above. One

possible explanation is the hitherto high cost of credit in Brazil which is especially

binding for small businesses that lack access to capital markets and which may have more

difficulty than larger firms securing subsidized credits through official channels.11

B. Users and Products

23. Notwithstanding significant progress there are still important gaps in the

financial inclusion landscape. This is logical given the country’s size and economic

diversity and the complexity of the issue. This section of the TN provides some

11 The Technical Note on BNDES provides further insights and information on this point.

Brazil Mexico India

South

Africa Turkey

Indicator

Type of

Institution

Account at a formal financial

institution (% of population age 15+)56 27 35 54 58

Commercial

banks533.49 … 137.46 … 360.67

Cooperatives 18.61 … 10.15 … …

SSFIs 2.20 … … … 0.02

MFIs 0.04 8.37 … … …

Commercial

banks1,065.35 1,096.76 747.29 839.13 1,661.21

Cooperatives 3.79 7.24 68.9 … …

SSFIs 0.56 63.20 … … …

MFIs 1.09 30.24 … … …

Commercial

banks12.71 14.67 10.11 8 17.77

Cooperatives 3.06 1.58 2.78 … …

SSFIs 1.49 0.75 … … 0.04

MFIs 0.03 1.05 … … …

ATMs per 100,000 Adults 112.06 44.80 7.29 52.41 44.25

POS per 100,000 Adults 2,247.41 592.14 67.06 8,908.68 3,232.79

Percent of firms identifying access

to finance as a major constraint55.5 29.6 15.8 15.5 14.3

Percent of firms with a bank

loan/line of credit65.3 32 … 30.1 56.8

Loan Accounts per 1,000 Adults

1. General Access Indicators

Deposit Accounts per 1,000 Adults

Branches per 100,000 Adults

2. Access to Basic Payment Services

3. Access to Credit and Other Sources of Financing

14

additional analysis of both the accomplishments and the challenges facing Brazil as it

moves toward more inclusive financial markets with discussion on who holds accounts as

well as on use of credit, savings, and insurance.

24. Brazil has made particular progress in access to accounts in formal financial

institutions. 41% of adults at the base of the economic pyramid (bottom 40%) in Brazil

have accounts compared to only 25% on average in Latin America (see Graph 1). In

general, access to accounts among the poor is limited in the region and as low as 15% for

Colombia, 12% in Mexico and 11% in Uruguay.

25. When compared against higher income countries in the G-20, however,

Brazil still has room for improvement in access to formal accounts. Graph 1 also

contrasts access to accounts in formal financial institutions for people at the bottom of the

income distribution with the average for each G-20 country. Brazil outperforms most

emerging markets in the group (with the exceptions of China and Turkey) but is still far

from the near-universal coverage (generally above 90%) of high income nations. Further,

the difference in coverage by income levels is relatively large in Brazil – 15% - when

compared with many members of the group including all of the high income countries

and many middle income countries as well such as Indonesia, India, Argentina, Russia

and Turkey. Only China (17%) and Mexico (15%) have spreads in account access

between income levels as high as Brazil.

26. There is also an important gender gap in Brazil when it comes to access

(Graph 2). The 10 percentage point gender gap is similar to the regional average of 9

percentage point gap in favor of men but it is outside the norm for Mercosur countries

where the gap is very small (2% in Chile; 3% in Argentina; and 2% more women than

men covered in Paraguay). Within the G-20, Brazil generally fares better than its

developing country peers, and is in line with the G-20 average of a roughly 10 point gap.

27. Brazil leads Latin America in the percentage of adults with a credit card at

29%, more than double the rate of most countries in the region and near the G-20

average of 33% (Graph 3). Brazil still has room to grow this market, as penetration

levels in high income countries are closer to two-thirds of the adult population; in the

U.S. for example, cards are used for approximately half of all purchases. Penetration

levels of credit card use vary significantly across the Brazilian population, reflecting the

fact that credit cards continue to be a product focused in more urban and higher income

communities. For example, 40% of higher income consumers (top 60% of incomes) have

a credit card in Brazil compared to 14% for those at the bottom of the economic pyramid

(bottom 40%). The urban / rural divide is 37% vs. 21% - the highest absolute gap in the

region.

15

Graph 2. Accounts at a Formal Financial Institution by Gender

Source: FINDEX 2011

28. In terms of gender equity, Brazil is exactly at the Latin American average,

with 5% more males than females owning a credit card. Brazil thus does slightly

better than the regional average of a 7% male-female gap, and does better in gender

equity than many of the world’s most developed economies including France, Germany

and the United States (see Figure A2 in the Appendix).

29. Widespread access to credit cards, however, does not necessarily translate

into access to mainstream sources of formal credit. First of all, Brazilians tend not to

carry balances on their credit cards due to exorbitant interest rates which can exceed

200% on an annualized basis. Second, according to FINDEX data, Brazilian consumers

are not getting other kinds of loans from formal lenders. Figure A3 in the Appendix

shows the sources of loans taken by consumers in Latin America. Only 6% of Brazilians

indicated they had a bank loan and only 1% had loans from other private lenders, but

Brazil has one of the highest percentages of loans from family and friends at 16%. These

figures likely understate access to credit as they may not reflect retail credits (i.e., buying

on installment plans) even when backed by banks which is widespread among lower

0 10 20 30 40 50 60 70

Nicaragua

El Salvador

Paraguay

Peru

Uruguay

Honduras

Panama

Guatemala

Bolivia

Mexico

Argentina

Colombia

Dominican Republic

Ecuador

Chile

LAC

Venezuela, RB

Costa Rica

Brazil

Accounts at a Formal Financial Institution

Accounts held by women

Accounts held by men

16

income consumers, or use of subsidized or government-supported credit programs such

as the microcredit program Crediamigo or payroll loans. However, the statistics seem to

indicate that access to credit in Brazil, even among lower income consumers, is

increasingly likely to be coming through credit cards rather than other types of loan

products.

Graph 3. Credit Card Access: General vs. Bottom 40%

Source: FINDEX 2011

30. In comparison with both Latin America and the G-20, Brazil’s savings rate is

low (Graph 4). Only 21% of adults in Brazil report saving any income in the past year, a

low rate when compared to Mexico (27%), Colombia (33%) or Bolivia (44%). Brazil is at

the LAC average, however, in terms of savings at a financial institution at 10% - an

indication of the success the country has had in moving consumers toward formal

accounts. Brazil also sees generally low gaps in savings along education, income and

urban/rural lines. Along educational lines for example, there is just a 10 point gap in

0 10 20 30 40

Nicaragua

Bolivia

El Salvador

Honduras

Guatemala

Paraguay

Colombia

Ecuador

Peru

Venezuela, RB

Panama

Costa Rica

Dominican Republic

Mexico

LAC

Argentina

Chile

Uruguay

Brazil

Credit Card Access

Credit card,income, bottom40% (% age15+)

Credit card (%age 15+)

17

savings among those with secondary education or more and those with just primary

education or less. This is in contrast to 28 points in Costa Rica and the Latin American

average of a 16 point gap. Within the G-20, Brazil has the lowest savings rates except for

Turkey. However, it also has one of the lowest gaps in savings by income brackets, doing

better than many of its more developed peers including France, China and the United

States. See Figure A4 in the Appendix.

31. The insurance market in Brazil is small but growing among low income

consumers. Reportedly, the greatest market penetration is related to health, and life and

funeral insurance to help protect against illness and loss of life. There are no official

statistics on microinsurance or on the percent of policies purchased by low income

consumers but some rough estimates exist. A frequently cited study by Neri at FGV from

2009 estimates that only about 8% of consumers in economic classes C, D and E have

health insurance and only 2.6% have life or funeral coverage. Recent FINDEX data seem

to confirm these estimates and indicate that only 10% of all Brazilians purchase health

insurance and that this figure is even lower for the poor (lowest 40% by income) at about

3%. FINDEX does not have data on life or funeral policies. However other sources

project higher levels of coverage. A 2010 study by CENFRI cites estimates from private

industry of approximately 20 million funeral policies in Brazil – a figure also provided to

the FSAP Update mission by private insurers - which would indicate a significantly

higher level of coverage than Neri’s 2.6%. Survey research in low income communities

in Rio and Sao Paulo in 2009 obtained estimates of approximately 25% for insurance

coverage related to health and life/funeral.

Graph 4. Savings: Total Savings and Savings at a Financial Institution

Source: FINDEX 2011

0 10 20 30 40

Uruguay

Paraguay

Brazil

Honduras

Argentina

Guatemala

El Salvador

LAC

Nicaragua

Chile

Mexico

Venezuela, RB

Peru

Ecuador

Colombia

Panama

Dominican Republic

Costa Rica

Bolivia

Savings in Latin America

Saved at afinancialinstitution in thepast year (% age15+)

Saved any moneyin the past year(% age 15+)

18

C. Credit Reporting and Consumer Protection

32. Brazil has a strong credit reporting system but relative progress vis-à-vis

other countries in the region has slowed down recently. Brazil was an early standout

in terms of the quality and availability of credit information, making it possible for some

products, like cheques, to prosper decades ago. However, while many countries in Latin

America have adopted reforms providing for more efficient and comprehensive credit

reporting system. Brazil is only now undertaking the fundamental reform of including

positive data in credit reports.

33. Twelve 12 Latin American countries have a perfect score of “6” in the Doing

Business (DB) credit information index but Brazil is not among them due to lack of

positive data.12

Since 2006, 7 countries in Latin America have moved from lower scores

to reach a score of “6” in the 2012 DB report (Graph 5). The seven reformers are Bolivia,

the Dominican Republic, Ecuador, El Salvador, Guatemala, Honduras and Uruguay.

Other countries in the region which fulfill all the DB good practice criteria and score “6”

are Argentina, Mexico, Panama, Paraguay and Peru. While this index, as is the case with

any such device, captures only some of the aspects of quality and coverage of a credit

reporting system, it does provide a good first approximation of the strength of a country’s

financial information infrastructure and helps track reforms. More detail on credit

reporting in Brazil is provided in the Focus Section of this TN (see below).

Graph 5. Doing Business Index Score

Source: Doing Business

12

The components of the DB Depth of Credit Information Index, which are equally weighted, are: (1) Both

positive credit information (for example, outstanding loan amounts and pattern of on-time repayments) and

negative information (for example, late payments, and number and amount of defaults and bankruptcies)

are distributed; (2) Data on both firms and individuals are distributed; (3) Data from retailers and utility

companies as well as financial institutions are distributed; (4) More than 2 years of historical data are

distributed. Credit registries and bureaus that erase data on defaults as soon as they are repaid obtain a score

of 0 for this indicator; (5) Data on loan amounts below 1% of income per capita are distributed. Note that a

credit registry or bureau must have a minimum coverage of 1% of the adult population to score a 1 on this

indicator; (6) By law, borrowers have the right to access their data in the largest credit registry or bureau in

the economy.

0123456

An

tigu

a an

d…

Arg

enti

na

Bah

amas

, Th

eB

eliz

eB

oli

via

Bra

zil

Ch

ile

Co

lom

bia

Co

sta

Ric

aD

om

inic

aD

om

inic

an…

Ecu

ado

rE

l Sal

vad

or

Gre

nad

aG

uat

emal

aG

uya

na

Hai

tiH

on

du

ras

Jam

aica

Mex

ico

Nic

arag

ua

Pan

ama

Par

agu

ayP

eru

Pu

erto

Ric

o (

U.S

.)St

. Kit

ts a

nd

Nev

isSt

. Lu

cia

St. V

ince

nt

and

…Su

rin

ame

Tri

nid

ad a

nd

…U

rugu

ayV

enez

uel

a, R

B

Doing Business Index

DB2006

DB2012

19

34. Financial consumer protection in Brazil is relatively strong in terms of the

rules on dispute resolution (Graph 6) but less advanced in terms of disclosure

requirements (Graph 7) or monitoring and enforcement (Graph 8).13

The lower

score on monitoring and enforcement may be influenced by the lack of a clear

institutional framework for financial consumer protection with responsibilities currently

shared by a variety of regulators and the Ministry of Justice. On disclosure requirements

it is interesting to note that the lower score is largely due to the lack of disclosure on

deposit (savings) products. The lack of consistency in transparency and disclosure on

issues such as method of interest compounding, penalties for early withdrawal and even

interest rates paid may be contributing to underperformance in savings. And while Brazil

has one of the more comprehensive dispute resolution frameworks, it also has a relatively

high level of complaints related to finance products which are registered by consumer

protection authorities (Procons). This may indicate that the dispute resolution

mechanisms which are intended to work at the level of the financial institution require

additional attention – perhaps including more aggressive supervision.

Graph 6. Consumer Protection-Dispute Resolution and Recourse

Source: Financial Access 2010, CGAP

13

These data are from Financial Access 2010, CGAP.

0 2 4 6 8 10

Bolivia

Costa Rica

Argentina

Colombia

Uruguay

LAC average

Chile

Brazil

Mexico

Peru

Dispute Resolution and Recourse

20

Graph 7. Consumer Protection--Requirements on Periodic Disclosure

Source: Financial Access 2010, CGAP

Graph 8. Consumer Protection--Monitoring and Enforcement

Source: Financial Access 2010, CGAP

D. Financial Products Suppliers

35. Four main types of financial products providers-–commercial banks, state

owned banks, cooperatives and microfinance institutions--are involved in financial

inclusion efforts. Figure 1 below identifies some of the leading institutions in each of

these categories. In addition some data was obtained on microinsurance activities by

leading private insurers.

0 5 10 15

Costa…

Brazil

Bolivia

Peru

LAC…

Argentina

Chile

Colombia

Uruguay

Mexico

Requirements on Periodic Disclosure

0 5 10 15

Costa Rica

Bolivia

LAC Average

Brazil

Argentina

Peru

Uruguay

Mexico

Colombia

Chile

Monitoring and Enforcement

21

Figure 1. Types of Financial Providers Involved in Financial Inclusion

Source: Author

36. Leading commercial banks, including Bradesco, Santander, and BMG, are

pursuing different financial inclusion strategies. Bradesco is the second largest

commercial bank in Brazil by both assets and deposits (US$355 billion and $US 116

billion, respectively, as of December 2011). The focus of Bradesco’s efforts has been to

establish an extensive network to facilitate access through a variety of channels--

correspondents, branches and ATMs--with emphasis on credit and insurance products.14

In partnership with Caixa Economica Federal (CEF) and BB, it launched the Elo card

brand which includes both debit and credit cards with a focus on lower income clients.

The goal is to reach a 15% market share in the medium term. Santander has taken a

different approach, with investment in a dedicated microcredit institution which ranks as

one of the largest microfinance institution (MFI) operations in the country after Banco do

Nordeste do Brasil’s (BNB) programs. In 2010, according to MIX data, Santander

Microcredit had more than 95,000 active clients and a loan portfolio in excess of US$75

million. Yet another approach is a focus on payroll loans exemplified by BMG, a market

leader in this segment. It focuses almost exclusively on loans to public employees and

pensioners.

37. Three state-owned banks continue to be the main source for financial

products and services targeting low income consumers. Two of these, BB and CEF,

rank among the 5 largest banks by assets, with BB leading the nation’s banks not only in

assets but also deposits, number of branches and number of employees. The third

institution is BNB. While these institutions have a broad customer base reaching both

middle and low income consumers, they also have mandates related to financial

inclusion. BB, which is now administering the postal bank correspondents’ network, is

pursuing a multi-pronged effort on financial inclusion. BB activities include a partnership

on mobile banking with the telco firm Oi, and the launch of a microinsurance product

14 In terms of bank branches, Bradesco is second only to Banco do Brasil (BB) with 4,643 nationwide.

Between 2002 and January 2012, Bradesco managed the correspondent banks run through Banco Postal –

more than 6,000 in number. Bradesco Expresso correspondent banks number more than 38,000 nationally.

Commercial Banks

Domestic Capital

Foreign owned

State Owned Banks

Caixa Economica Federal

Banco do Brasil

Banco Nordeste do Brasil

BNDES

Cooperatives

(associations listed below)

SICOOB

SICREDI

UNICRED

Microfinance

Santander

Banco Nordeste do Brasil

Others

22

with insurance leader Mapfre to be sold through the postal bank network. CEF has a

focus on housing finance and is the institution behind the Minha Casa Minha Vida

program directed at low income consumers. This bank, which boasts the largest

correspondent banking network in the country, is also the channel for payment of Bolsa

Familia payments via cards. BNB is by far the largest microcredit provider in the

country, with more than 1 million active clients in the Crediamigo program and more

than 650,000 in the Agroamigo program. In addition, the Banco Nacional de

Desenvolvimento Economico e Social (BNDES) provides financial services for small and

micro enterprises, especially through its Visa card program linked to pre-approved

vendors with purchases handled through a dedicated website.

38. Cooperative banks have also made important contributions to financial

inclusion in Brazil over the past decade, especially in the south and southeast

regions of the country. Graph 9 below shows the increasing presence of cooperatives in

the Brazilian financial system between 2000 and 2010 in terms of not only credit, but also

deposits and net worth. Table 3 reports basic data on cooperatives.

Graph 9. Share of Cooperatives in the National Financial System

0

0.5

1

1.5

2

2.5

3

3.5

4

% Net Worth

% Assets

% Deposits

% Credit Operations

23

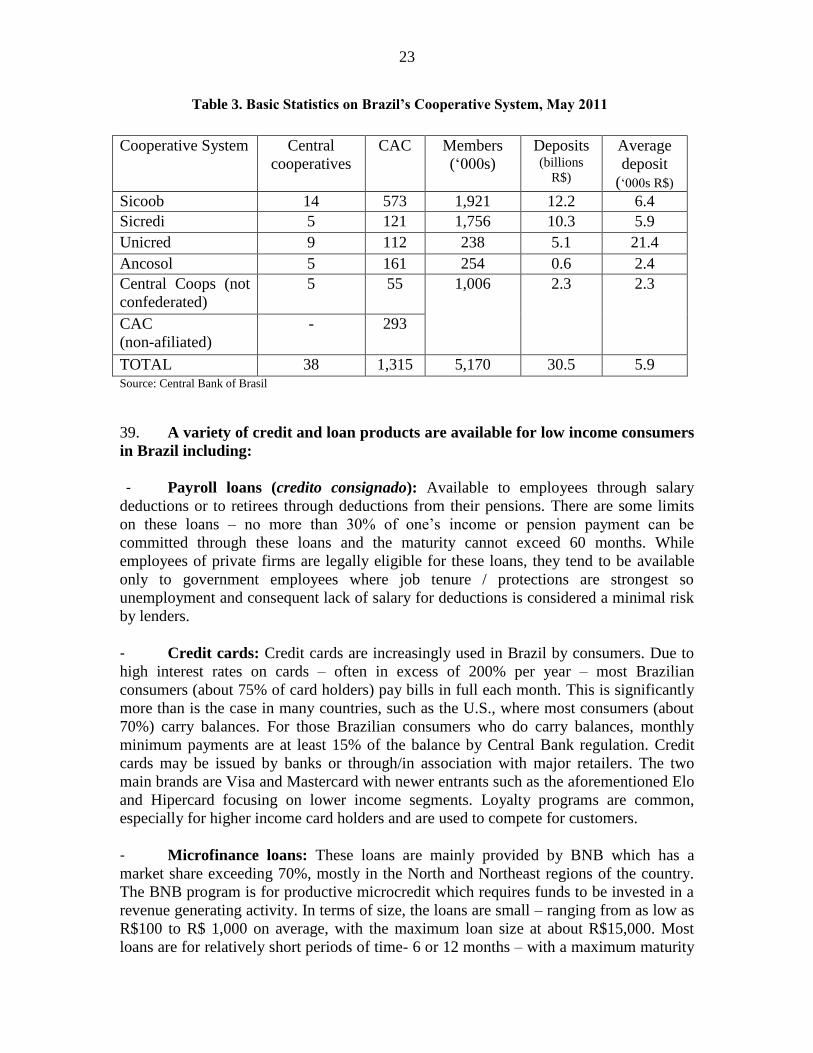

Table 3. Basic Statistics on Brazil’s Cooperative System, May 2011

Cooperative System Central

cooperatives

CAC Members

(‘000s)

Deposits (billions

R$)

Average

deposit

(‘000s R$)

Sicoob 14 573 1,921 12.2 6.4

Sicredi 5 121 1,756 10.3 5.9

Unicred 9 112 238 5.1 21.4

Ancosol 5 161 254 0.6 2.4

Central Coops (not

confederated)

5 55 1,006 2.3 2.3

CAC

(non-afiliated)

- 293

TOTAL 38 1,315 5,170 30.5 5.9 Source: Central Bank of Brasil

39. A variety of credit and loan products are available for low income consumers

in Brazil including:

- Payroll loans (credito consignado): Available to employees through salary

deductions or to retirees through deductions from their pensions. There are some limits

on these loans – no more than 30% of one’s income or pension payment can be

committed through these loans and the maturity cannot exceed 60 months. While

employees of private firms are legally eligible for these loans, they tend to be available

only to government employees where job tenure / protections are strongest so

unemployment and consequent lack of salary for deductions is considered a minimal risk

by lenders.

- Credit cards: Credit cards are increasingly used in Brazil by consumers. Due to

high interest rates on cards – often in excess of 200% per year – most Brazilian

consumers (about 75% of card holders) pay bills in full each month. This is significantly

more than is the case in many countries, such as the U.S., where most consumers (about

70%) carry balances. For those Brazilian consumers who do carry balances, monthly

minimum payments are at least 15% of the balance by Central Bank regulation. Credit

cards may be issued by banks or through/in association with major retailers. The two

main brands are Visa and Mastercard with newer entrants such as the aforementioned Elo

and Hipercard focusing on lower income segments. Loyalty programs are common,

especially for higher income card holders and are used to compete for customers.

- Microfinance loans: These loans are mainly provided by BNB which has a

market share exceeding 70%, mostly in the North and Northeast regions of the country.

The BNB program is for productive microcredit which requires funds to be invested in a

revenue generating activity. In terms of size, the loans are small – ranging from as low as

R$100 to R$ 1,000 on average, with the maximum loan size at about R$15,000. Most

loans are for relatively short periods of time- 6 or 12 months – with a maximum maturity

24

of 36 months. Interest rates are also significantly below market levels and now are as low

as 0.64% per month thanks to the Crescer program. Santander Microcredit is a distant

second in the market for microfinance, with an average loan size of about $700 USD.

- Prepaid cards: Prepaid cards enable unbanked consumers to have access to card

technology for payment. Single use prepaid cards, such as store gift cards, were joined by

general purpose reloadable (GPR) cards in 2011. The main providers are PanAmericano

Mastercard, Ourocard Visa (with BB) and Mundo Livre Visa (Banco Rendimento). These

cards may have fees for issuance, maintenance (only Mundo Livre), for adding value and

for withdrawals.

- Savings accounts: Savings accounts have traditionally been a popular investment

vehicle in Brazil because they paid a guaranteed, tax-free rate of return even during

periods of economic instability. This policy was shifted recently, however, when the

Government announced in May 2012 that the rate would drop to 70% of the SELIC

reference rate, if that rate went below 8.5%, on new deposits. Savings accounts are

commonplace – more than 100 million exist – but represent a relatively small share of

total savings in the country.

E. Laws, Regulations and Government Programs

40. The authorities have taken a strategic and forceful approach to financial

inclusion underpinned by a multi-agency “architecture”. The Central Bank sits at the

top of this architecture and established a dedicated unit for Financial Inclusion in April

2010 as part of its Financial System Regulation Department (DENOR). The Central Bank

has hosted an annual Forum for Financial Inclusion since 2009 and publishes an annual

report on the topic. Other agencies which play key roles in various aspects of the

financial inclusion strategy include the other main financial sector regulators who form

part of COREMEC (in addition to the Central Bank, CVM (securities regulator), SUSEP

(private insurance regulator) and PREVIC (pension regulator), Treasury (Fazenda), the

Ministry of Justice (especially related to consumer protection), the Ministry of Social

Development (related to financial inclusion via transfer payments through the Bolsa

Familia program), Ministry of Communications (for mobile payments) and SEBRAE

which provides support to SMEs.

41. Brazil’s approach to financial inclusion has evolved over time establishing

new programs and products and strengthening market conduct. More than a decade

ago, initial efforts to extend access to finance relied on microcredit, followed by payroll

guaranteed loans. Over time the focus broadened to include non-credit financial products

and services including microinsurance (regulations pending) and payments (especially

related to social transfers to the poor (G2P)). There is also a growing attention given to

market conduct and transparency to create incentives for innovation and competition at

the base of the pyramid. Table 4 lists some of the most important regulatory measures

taken in the last ten years.

42. In May 2012 Brazil published the “Action Plan to Strengthen the

Institutional Environment” as part of the National Partnership for Financial

25

Inclusion (Box 1).15

This document identifies eight actions for 2012-2014 to enhance and

strengthen the opportunities for financial inclusion in Brazil. These eight action items are

listed in Box 1 below together with the key agencies to be involved. Several of these

actions relate to reforms in the legal and regulatory framework for financial inclusion to

support microfinance, mobile payments and enhanced consumer protection.

43. Brazil is also an active participant in the G20 Financial Inclusion Experts

Group (FIEG) where they co-lead with Australia the Access Through Innovation

Sub-Group (ATISG). The principles for innovation in financial inclusion are in line

with the approach taken by Brazil, focusing on government leadership together with a

coordinated approach involving public and private sector bodies, diverse service

offerings and effective consumer protection and financial education.

Table 4. Regulations on Financial Inclusion Issues

Law / Regulation Number of Law /

Regulation

Link to Law / Regulation

National Program

of

Oriented

Productive

Microcredit -

PNMPO

LEI Nº 11.110, DE 25

DE ABRIL DE 2005.

http://www.planalto.gov.br/ccivil_03/_ato2004

-2006/2005/Lei/L11110.htm

Crescer MPV 543 2011 http://www.planalto.gov.br/ccivil_03/_Ato201

1-2014/2011/Mpv/543impressao.htm

Simplified Accounts Resolução nº 3.211,

de 30 de junho de

2004

http://www.bcb.gov.br/pre/normativos/res/200

4/pdf/res_3211_v2_P.pdf

Credito consignado LEI No 10.953, DE 27

DE SETEMBRO DE

2004.

LEI No 10.820, DE 17

DE DEZEMBRO DE

2003.

Processo:

08700.003070/2010-

14

(end of exclusivity)

http://www.planalto.gov.br/ccivil_03/_Ato200

4-2006/2004/Lei/L10.953.htm#art6§5

http://www.planalto.gov.br/ccivil_03/LEIS/20

03/L10.820.htm#art6

http://www.cade.gov.br/Default.aspx?40f3021

7ee24f83acc7ad26fc6

Microinsurance Pending – coming

2012 from SUSEP

Minha Casa Minha

Vida

LEI Nº 12.424, DE 16

DE JUNHO DE 2011.

http://www.planalto.gov.br/ccivil_03/_Ato201

1-2014/2011/Lei/L12424.htm#art1

15

http://www.bcb.gov.br/nor/relincfin/Plano_de_Acao_PNIF.pdf

26

Cooperatives Resolução nº 3.859,

de 27 de maio de 2010

Correspondents Res. 3954/11

Portability Portabilidade (de

cadastro – Res.

2835/2001, de crédito

- Res. 3401/2006 e de

salário Res.

3.402/2006 e Res.

3.424/2006),

Cadastro Positivo LEI Nº 12.414, DE 9

DE JUNHO DE 2011.

http://www.planalto.gov.br/ccivil_03/_Ato201

1-2014/2011/Lei/L12414.htm

Custo total efetivo Res. 3517/07 e Res.

3909/10

Box 1--Action Plan Items for National Partnership for Financial Inclusion

1. Improve the regulatory framework for microcredit, including for institutions

specialized in microfinance, to adequately support

microentrepreneurs, as well as micro and small enterprises (Central Bank, Treasury,

Justice)

2. Encourage diversification and improvement of financial services, making them more

responsive to the needs of the population (Central Bank, Treasury, PREVIC (pension

regulator), SUSEP (private insurance regulator)

3. Define the legal and regulatory framework for mobile payments (Central Bank,

Ministry of Communications)

4. Strengthen the network of financial services delivery channels serving the

population (Central Bank, Treasury)

5. Contribute to the promotion of financial education (COREMEC members, Justice, Social Development, SEBRAE)

6. Accelerate dissemination of consumer protections afforded to financial services consumers including dispute resolution mechanisms (COREMEC members, Treasury, Justice)

7. Improve the methodology used to study financial inclusion and incorporate quality indicators (Central Bank, SUSEP, PREVIC)

8. Conduct research on the behavior and perceptions of the population in regard to the use of financial services (COREMEC members, Justice, IBGE (Brazilian Institute of Geography and Statistics, SAE, Social Development, SEBRAE)

27

II. Selected Issues in Financial Inclusion

A. The Payroll-Guaranteed Loan Program--Crédito Consignado

44. Payroll-guaranteed loans represented nearly 60% of the personal loan

market segment in Brazil at the end of 2011. Growth rates for the program have

averaged more than 30% per annum in the period 2004-2011, since the legal framework

was clarified and extended to cover not only government workers and retirees, but also

private sector employees and pensioners under INSS (the National Institute of Social

Security).16

In the same period non-consigned personal loans grew by approximately

13.5% per year. See Table 5 below for more detailed information on the evolution of the

program.

Table 5. Payroll Guaranteed Loan Program

End Year Consigned loans Non

consigned

personal

loans

Total

personal

loans

%

consigned Public

sector

Private

sector

Total

2004 19,997 3,479 23,476

46,205 69,681 33.7

2005 37,272 5,079 42,351 52,143 94,493 44.8

2006 54,556 7,802 62,358 52,531 114,889 54.3

2007 69,654 10,546 80,200 59,242 139,443 57.5

2008 79,846 12,514 92,360 75,862 168,222 54.9

2009 104,335 16,748 121,083 83,781 204,864 59.1

2010 125,299 21,198 146,497 93,734 240,231 61.0

2011* 135,957 22,591 158,548 111,949 270,497 58.6

45. By reducing the risk to lenders, crédito consignado have resulted in a

significant reduction in the interest rates charged. According to data from the Central

Bank, the average interest rate on loans obtained through the crédito consignado program

was 27.2% per year in November 2011 compared to more than 70% per year for non-

consigned personal loans (Figure 10 below.) This significant differential in rates, which

was present from the beginning of the program, allowed some borrowers to substitute

loans obtained through the crédito consignado program for more expensive credits they

were previously holding. The shift from high cost to lower cost credit provides an

unambiguous welfare improvement for consumers and there is both anecdotal evidence

and recent research which suggests that this occurred during the early years of the

program (through 2007). 17

At the same time, by creating a solid guarantee credit became

available to some low income workers or pensioners who were previously unable to

obtain a loan. A 2005 survey by the Brazilian Federation of Banks (FEBRABAN) found

that 51% of people taking a crédito consignado had never borrowed before. Research by

16

The relevant laws are 10,820 of September 2003 (medida provisoria / temporary measure) and 10,953 of

September 2004. 17

Gigliucci 2011.

28

Madeira, et al. (2010) also indicates that borrowers in the crédito consignado program

were more likely to have a small business as financial constraints to entrepreneurship

were reduced.

46. The hallmark characteristic of the crédito consignado program is the drastic

reduction in default risk due to the automatic deduction from stable (government)

sources of income-–government pensions and government salaries. For a time public

banks enforced exclusivity rules for access to crédito consignado. For example,

government employees whose payroll was administered through BB were only able to

request a crédito consignado through BB, limiting competition in this market and

contributing to higher prices. In 2012, the Administrative Council for Economic Defense

(CADE) ended the ability of public banks, such as BB, to have exclusive rights to the

crédito consignado business of government employees whose payroll they administer or

pensioners who receive benefits through a particular public bank.

Graph 10. Interest Rates on Loans by Type, 2004-2011

(Percent per year)

47. The risk of non-payment may be so low that it may be creating perverse

incentives for -sometimes aggressive- overselling of crédito consignado loans. For a

bank granting a crédito consignado, the only credit risk is whether or not the borrower

has reached his/her maximum salary allocation for debt payments–set by law in 2010 at

30% of the total benefit / salary. To further control levels of indebtedness, loan maturity

is also limited-to 5 years for retired private sector employees. The lender does not need to

review the borrower’s credit history in the credit bureau system, and total levels of

indebtedness will neither affect the consumer’s ability to get approved for a crédito

consignado or their ability to repay.

48. For many borrowers the crédito consignado looks like a great opportunity as

interest rates are far lower than on other unsecured loans but these rates remain

29

high in real terms. Price inflation in Brazil has only hovered between 3 and 7 percent

per annum since 2007. According to information provided by INSS (the National

Institute for Social Security), a higher share of pensioners take these loans in lower

income states, such as those in the North and Northeast, while they are less popular in the

Federal District or south. Further, pensioners typically are taking the maximum loan

amount and carrying this positive balance indefinitely, thus reducing their income level

by as much as 30%.

49. Going forward attention should be paid to how government workers and

pensioners are marketed these loans and the impact on their welfare should be

evaluated. Efforts to reduce overly aggressive sales techniques have begun including be

setting training requirements for agents. However, given the incentive structure in the

industry, where agents are only paid for loans they make, these steps may not be

sufficient. Looking at ways to involve the banks making the loans in the risk of non-

payment would help to curb over-selling but would also likely increase the rate charged

and reduce the access to credit for some borrowers. Impact evaluation of the program

should also be prioritized to see whether borrowers are benefiting from access to credit –

improved health outcomes, investments in productive investments or education for family

members, etc.

B. Credit Reporting–Moving to a Positive Credit Registry “Cadastro Positivo”

50. Brazil has traditionally had a strong credit information culture in terms of

negative data. SERASA is the country’s leading private credit bureau and was originally

founded in 1968 by Brazil’s domestic banks, decades before many other Latin American

countries established private bureaus. SERASA began operations focusing on the

collection of negative credit data from its members, but over time extended its scope to

include data from other public and private data sources. The other main source of credit

information in Brazil historically was the SCPC (Serviço Central de Proteção ao

Crédito), a service run by the Sao Paulo Chamber of Commerce which links to data from

retailers across the country. The Central Bank has also played an important role in credit

information. For example, the wide use of post-dated checks in Brazil was possible

because of easy and low-cost access to information on bounced checks provided by the

Central Bank. This service made it possible to use post-dated checks as a type of retail

credit as well as a payment mechanism.

Major changes in credit reporting in Brazil—From 2007 to the present

51. SERASA was the fourth largest bureau globally (trailing only the “Big

Three” international bureaus Experian, TransUnion and Equifax) when it was a

acquired by Experian in 2007. Experian is the majority shareholder, with two of

Brazil’s largest banks – Itaú Unibanco and Bradesco - holding the remaining minority

shares. The acquisition was important for several reasons. It provided access to

international capital as well as to Experian’s global technology for data management and

analytical solutions. The new ownership structure also put the firm in line with global

good practices for the industry by removing the banks (the primary providers and users of

30

data) from management of the firm. Third party ownership of credit reporting firms helps

to align incentives toward expansion of the database and its use by a broader set of

financial and commercial firms. On a related point, it also is likely to increase the

quantity and quality of decision tools offered by the bureau, creating a more level playing

field for credit analytics. (When banks own a credit bureau they may try to limit the data

collected to client segments that are of greatest interest or limit access and use of the data

– including the spread of credit scores and other analytical tools - by potential

competitors who are not owners of the bureau.)

52. The other main private bureau today is Boa Vista/Equifax which is

significantly smaller than SERASA, but growing. Boa Vista / Equifax was created in

2010 through a partnership between the Chambers of Commerce of Sao Paulo, Rio de

Janeiro, Paraná and Porto Alegre, together with the investment fund TMG Capital and the

international credit bureau firm Equifax. In addition to collecting data from banks, firms

and other sources, Boa Vista commercializes data from the SCPC. This is an important

strategic advantage for the firm as it seeks to build market share. It also brings investment

capital and technical know-how to the management and distribution of this rich dataset,

increasing its value to financial providers through decision tools and analytics.18

53. There is also a public credit registry managed by the Central Bank of Brasil. Known as the SCR or Credit Information System, it includes both positive and negative

data on all customers with loans in excess of R$ 1,000 at regulated financial institutions.

The lower bound on loans reported was recently changed to R$ 1,000 from R$ 5,000 to

include more small borrowers in the public registry. The main objective behind this

change was to make it easier for both lenders and regulators to accurately measure

indebtedness levels for a larger share of the population, so as to promote wiser use of

credit. In addition to loan amount, lenders provide information on the status of the loan,

indicating whether payments are on time, late or in default. Since private bureaus only

collect negative data at this time (i.e. information on loans where there are late payments

or defaults), this is the only source of reliable information on levels of credit exposure

(i.e. total indebtedness which includes loans in good standing). Only regulated financial

institutions can access these data through their dedicated communication lines with the

Central Bank, and they pay a very small fee for this access. Private credit bureaus and

other private firms providing credit analysis and credit decision tools do not have access

to the data in the SCR. The CPL allows the sharing of details of the credit transactions

with other sectors of the economy.

Seizing the opportunity --Cadastro Positivo

54. Recent changes in the credit reporting industry in Brazil have created a solid

foundation for growth and for the sector to play an increasingly strategic role in

financial markets. These include the aforementioned change in ownership of the

dominant bureau SERASA; the strengthening of the secondary credit bureau BoaVista

18

Some of the local retailer associations under CNDL did not join the BoaVista partnership and have since

entered into a partnership with SERASA to disseminate their data.

31

Equifax through a partnerships with leading Chambers of Commerce and the

commercialization of SCPC data through Boa Vista (offering a more technologically

advanced platform and credit tools); and the expansion of the SCR to include small loans

to a minimum size of R$ 1,000. The next major reform, which is poised to take effect in

mid-2012, is the development of the “cadastro positivo” or positive credit data in Brazil.

55. Brazil has lagged behind the global trend--and internationally recognized

good practice--of collecting and distributing both positive and negative credit data. The lack of positive credit information is the reason that Brazil scores 5 out of 6 on the

Doing Business “Depth of Credit Information” index – below the regional average of 5.4.