Embed Size (px)

Citation preview

Increasing Customer ENGAGEMENT

Financial institutions have been using consumer data to improve and

streamline their cross-sell and up-sell opportunities for some time.

Today, new data analytics solutions are making it possible for banks

and other institutions to go deeper and understand what really makes

their customers tick.

about their customers than ever before to help guide their day-to-day

business practices and proactively deliver more personalized products

and services. By harnessing analytics, retail banks and other institutions

can create more engaging, customer-centric programs that service

consumers through a variety of channels.

John Malo, research director for CEB TowerGroup’s retail banking

practice, delved into these possibilities during a recent web seminar

hosted by the American Banker and sponsored by Envestnet® | Yodlee®.

City National Bank has been using consumer data to improve and

streamline their cross-sell and up-sell opportunities for some time.

Today, new data analytics solutions are making it possible for financial

institutions, like City National Bank, to go deeper and understand what

really makes their customers tick

Now financial services companies can draw on more insights from data

about their customers than ever before to help guide their day-to-day

business practices and proactively deliver more personalized products

and services. By harnessing analytics, City National Bank and other

institutions can create more engaging, customer-centric programs that

service consumers through a variety of channels.

John Malo, research director for CEB TowerGroup’s retail banking practice,

delved into these possibilities during a recent web seminar hosted by the

American Banker and sponsored by Envestnet® | Yodlee®.

2

A Revealing SurveyDrawing on the results of CEB TowerGroup’s annual survey of retail banking IT executives, Malo began by noting that retail banks are placing a premium on improving service through their digital channels, and that more than half of the executives surveyed indicated that this is their top priority right now. One of their key objectives, according to the survey, is to obtain a single, consistent view of their customers, which Malo called a prerequisite for improving service levels and the customer experience.

Most of the bank IT execs surveyed, he noted, strongly believe that they can improve customer adoption rates through enhancements to their digital service channels. There is, however, a disconnect at most banks

the customer experience as the number one priority by far for most banks’

operations and processes.

1© 2015 The Corporate Executive Board Company. All Rights Reserved.

WHO IS RESPONSIBLE FOR CUSTOMER EXPERIENCE?

Organizations are realizing that “Customer Experience” and “Process Simplification” are common goals.

Differences in Priorities Lie in SemanticsPrimary Drivers for Making Investments in Digital Transformation of Front-, Middle-, and Back-Offices of a Bank (%), 2015

Front-Office

Customer Experience 92.6%

Process Simplification83.3%

Capacity Augmentation52.8%

Risk Mitigation51.9%

Cost Reduction51.9%

Middle-Office

Process Simplification78.8%

Risk Mitigation70.6%

Cost Reduction64.7%

Capacity Augmentation58.8%

Customer Experience53.8%

Back-Office

Customer Experience46.3%

Process Simplification81.5%

Cost Reduction77.8%

Risk Mitigation75.9%

Capacity Augmentation50.9%

60% of negative customer experiences emanates from back-office.- Capgemini Consulting, 2014

Most negative customer experiences, meanwhile, emanate from middle and back-office processes, according to the study.

More than half of the retail bank IT executives surveyed by CEB TowerGroup indicate that improving customer service through digital channels is their top priority.

A Revealing Survey Drawing on the results of CEB TowerGroup’s annual survey of retail banking IT executives, Malo began by noting that retail banks are placing a premium on improving service through their digital channels, and that more than half of the executives surveyed indicated that this is their top priority right now. One of their key objectives, according to the survey, is to obtain a single, consistent view of their customers, which Malo called a prerequisite for improving service levels and the customer experience.

Most of the bank IT execs surveyed, he noted, strongly believe that they can improve customer adoption rates through enhancements to their digital service channels. There is, however, a disconnect at most banks between their front, middle, and back offices.

Another study cited by Malo, Capgemini’s World Retail Banking Report, identifies improving the customer experience as the number one priority by far for most banks’ front office, but the lowest priority for their middle and back offices, which places much greater stress on simplifying operations and processes.

3

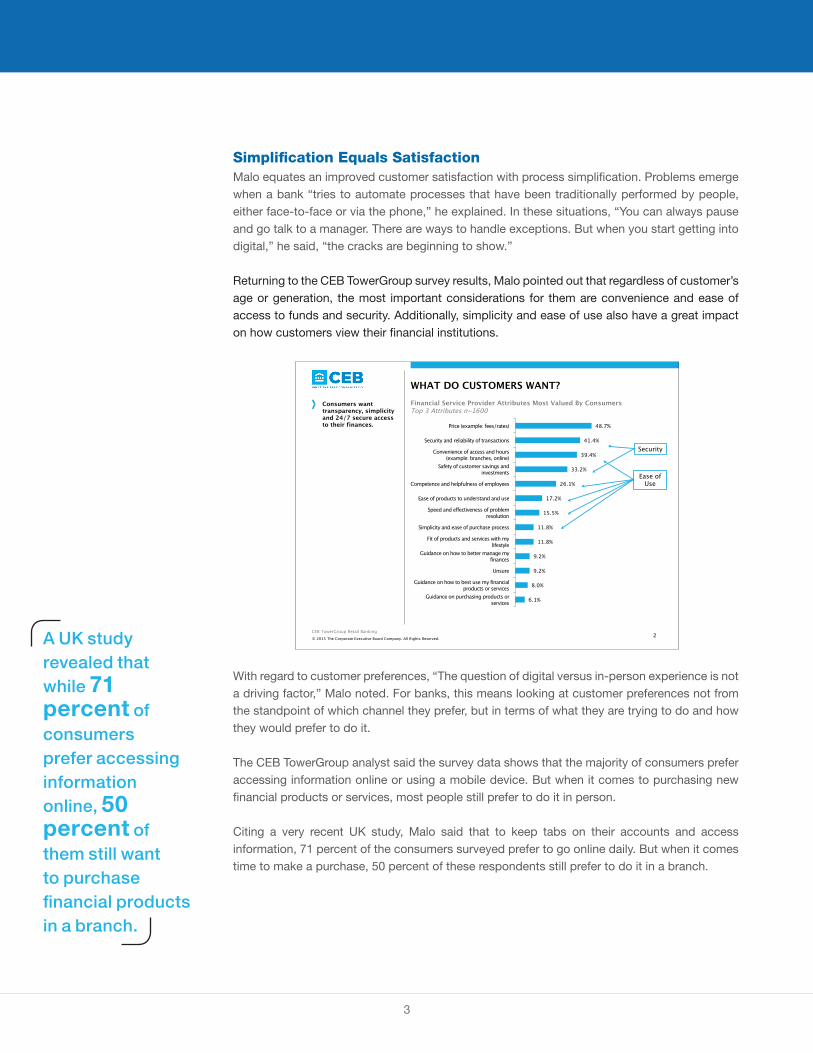

Simplification Equals Satisfaction

when a bank “tries to automate processes that have been traditionally performed by people, either face-to-face or via the phone,” he explained. In these situations, “You can always pause and go talk to a manager. There are ways to handle exceptions. But when you start getting into digital,” he said, “the cracks are beginning to show.”

Returning to the CEB TowerGroup survey results, Malo pointed out that regardless of customer’s

2© 2015 The Corporate Executive Board Company. All Rights Reserved.

CEB TowerGroup Retail Banking

WHAT DO CUSTOMERS WANT?Consumers want transparency, simplicity and 24/7 secure access to their finances.

Financial Service Provider Attributes Most Valued By ConsumersTop 3 Attributes n~1600

6.1%

8.0%

9.2%

9.2%

11.8%

11.8%

15.5%

17.2%

26.1%

33.2%

39.4%

41.4%

48.7%

Guidance on purchasing products or services

Guidance on how to best use my financial products or services

Unsure

Guidance on how to better manage my finances

Fit of products and services with my lifestyle

Simplicity and ease of purchase process

Speed and effectiveness of problem resolution

Ease of products to understand and use

Competence and helpfulness of employees

Safety of customer savings and investments

Convenience of access and hours (example: branches, online)

Security and reliability of transactions

Price (example: fees/rates)

Security

Ease of Use

standpoint of which channel they prefer, but in terms of what they are trying to do and how they would prefer to do it.

The CEB TowerGroup analyst said the survey data shows that the majority of consumers prefer accessing information online or using a mobile device. But when it comes to purchasing new

Citing a very recent UK study, Malo said that to keep tabs on their accounts and access information, 71 percent of the consumers surveyed prefer to go online daily. But when it comes time to make a purchase, 50 percent of these respondents still prefer to do it in a branch.

A UK study revealed that while 71 percent of consumers prefer accessing information online, 50 percent of them still want to purchase financial products in a branch.

Simplification Equals SatisfactionMalo equates an improved customer satisfaction with process simplification. Problems emerge when a bank “tries to automate processes that have been traditionally performed by people, either face-to-face or via the phone,” he explained. In these situations, “You can always pause and go talk to a manager. There are ways to handle exceptions. But when you start getting into digital,” he said, “the cracks are beginning to show.”

Returning to the CEB TowerGroup survey results, Malo pointed out that regardless of customer’s age or generation, the most important considerations for them are convenience and ease of access to funds and security. Additionally, simplicity and ease of use also have a great impact on how customers view their financial institutions.

With regard to customer preferences, “The question of digital versus in-person experience is not a driving factor,” Malo noted. For banks, this means looking at customer preferences not from the standpoint of which channel they prefer, but in terms of what they are trying to do and how they would prefer to do it.

The CEB TowerGroup analyst said the survey data shows that the majority of consumers prefer accessing information online or using a mobile device. But when it comes to purchasing new financial products or services, most people still prefer to do it in person.

Citing a very recent UK study, Malo said that to keep tabs on their accounts and access information, 71 percent of the consumers surveyed prefer to go online daily. But when it comes time to make a purchase, 50 percent of these respondents still prefer to do it in a branch.

4

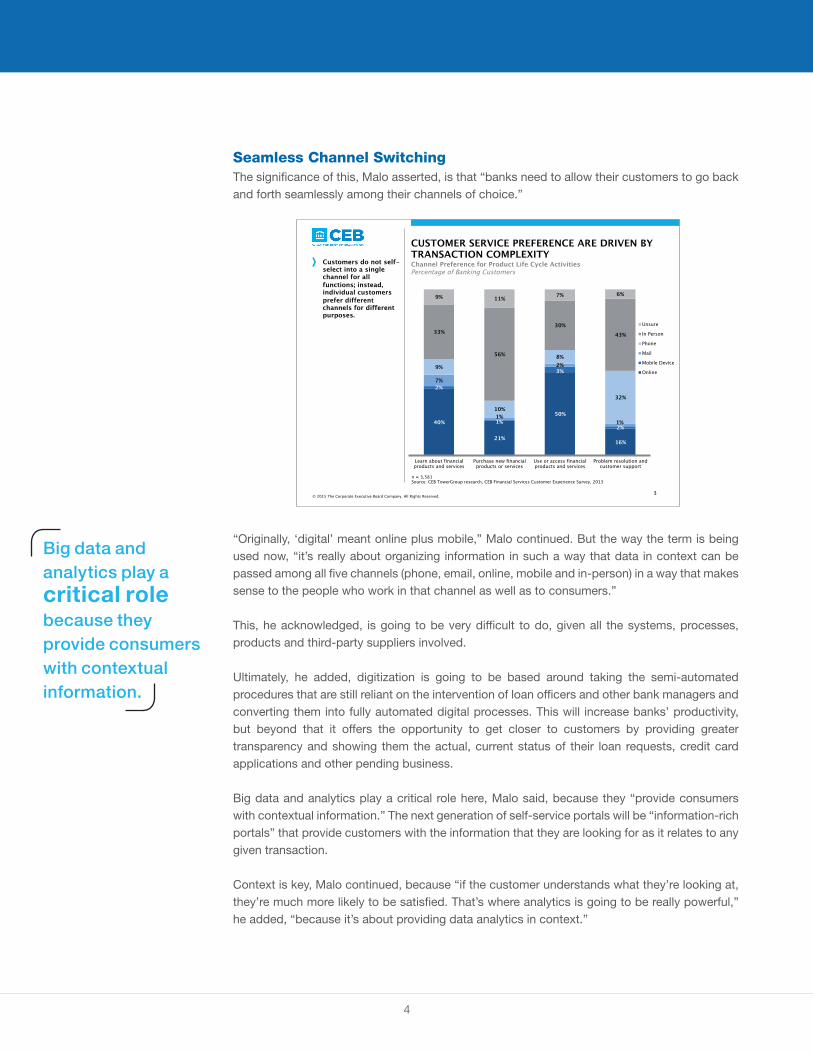

Seamless Channel Switching

forth seamlessly among their channels of choice.”

3© 2015 The Corporate Executive Board Company. All Rights Reserved.

Customers do not self- select into a single channel for all functions; instead, individual customers prefer different channels for different purposes.

Channel Preference for Product Life Cycle ActivitiesPercentage of Banking Customers

CUSTOMER SERVICE PREFERENCE ARE DRIVEN BY TRANSACTION COMPLEXITY

40%

21%

50%

16%

2%

1%

3%

2%

7%

1%

2%

1%

9%

10%

8%

32%

33%

56%

30% 43%

9% 11% 7% 6%

Learn about financial products and services

Purchase new financial products or services

Use or access financial products and services

Problem resolution and customer support

Unsure

In Person

Phone

Mobile Device

Online

n = 3,581 Source: CEB TowerGroup research, CEB Financial Services Customer Experience Survey, 2013

“Originally, ‘digital’ meant online plus mobile,” Malo continued. But the way the term is being used now, “it’s really about organizing information in such a way that data in context can be passed

the people who work in that channel as well as to consumers.”

and third-party suppliers involved.

Ultimately, he added, digitization is going to be based around taking the semi-automated bank managers and

converting them into fully automated digital processes. This will increase banks’ productivity, but beyond that it offers the opportunity to get closer to customers by providing greater transparency and showing them the actual, current status of their loan requests, credit card applications and other pending business.

Big data and analytics play a critical role here, Malo said, because they “provide consumers with contextual information.” The next generation of self-service portals will be “information-rich portals” that provide customers with the information that they are looking for as it relates to any given transaction.

Context is key, Malo continued, because “if the customer understands what they’re looking at,

added, “because it’s about providing data analytics in context.”

Big data and analytics play a critical role because they provide consumers with contextual information.

Seamless Channel SwitchingThe significance of this, Malo asserted, is that “banks need to allow their customers to go back and forth seamlessly among their channels of choice.”

“Originally, ‘digital’ meant online plus mobile,” Malo continued. But the way the term is being used now, “it’s really about organizing information in such a way that data in context can be passed among all five channels (phone, email, online, mobile and in-person) in a way that makes sense to the people who work in that channel as well as to consumers.”

This, he acknowledged, is going to be very difficult to do, given all the systems, processes, products and third-party suppliers involved.

Ultimately, he added, digitization is going to be based around taking the semi-automated procedures that are still reliant on the intervention of loan officers and other bank managers and converting them into fully automated digital processes. This will increase banks’ productivity, but beyond that it offers the opportunity to get closer to customers by providing greater transparency and showing them the actual, current status of their loan requests, credit card applications and other pending business.

Big data and analytics play a critical role here, Malo said, because they “provide consumers with contextual information.” The next generation of self-service portals will be “information-rich portals” that provide customers with the information that they are looking for as it relates to any given transaction.

Context is key, Malo continued, because “if the customer understands what they’re looking at, they’re much more likely to be satisfied. That’s where analytics is going to be really powerful,” he added, “because it’s about providing data analytics in context.”

5

Summarizing his key points, the CEB TowerGroup analyst told the webinar attendees that “Information is what’s going to be important. We can look for one piece of data in a large database. But if all we do is multiply the size of the database and we’re still looking for the same data point, we’re looking for a needle in a haystack.”

Ultimately, he said, “it’s about delivering the experience to the consumer in their preferred channel for whatever they’re trying to get done, and ensuring that if they move from one channel to another, the bank can provide continuity and not just replicate the data.”

The Envestnet | Yodlee Platform

innovation and provides many of the tools banks need to build out the sort of digital customer experience described by Malo. The Envestnet | Yodlee Financial Cloud is an open technology

Envestnet | Yodlee’s Senior Vice President for Product Marketing and Alliances.

Ultimately, Envestnet | Yodlee can help banks provide their customers with a comprehensive

said. In tandem with Envestnet | Yodlee’s suite of applications, this allows customers to access,

banks to deliver the right information to their customers at the right time, and transform the customer experience in the process.

An example of this is Envestnet | Yodlee’s Transaction Data Enrichment (TDE) solution. This new product-set adds important attributes to the data generated by bank, credit card and debit card transactions, making it much more useful. The enhanced data includes optimizations like natural language descriptions of the transaction, geo-location and other identifying characteristics of the merchant, which allows and their customers to easily identify and assess the nature of the transaction.

Used in this way, the Yodlee TDE solution helps to reduce call center volumes and false fraud alerts, while also making it easier for both the institutions and their customers to monitor spending habits and preferences. Since understanding consumers is the basis for building a sustainable competitive advantage in banking, Yodlee’s TDE gives banks the ability to improve their offerings, deepen their customer relationships, improve their customer retention and more effectively acquire new customers.

The Envestnet | Yodlee Financial Cloud is an open technology platform that underpins the digital financial solutions for over 900 companies.

Summarizing his key points, the CEB TowerGroup analyst told the webinar attendees that “Information is what’s going to be important. We can look for one piece of data in a large database. But if all we do is multiply the size of the database and we’re still looking for the same data point, we’re looking for a needle in a haystack.”

Ultimately, he said, “it’s about delivering the experience to the consumer in their preferred channel for whatever they’re trying to get done, and ensuring that if they move from one channel to another, the bank can provide continuity and not just replicate the data.”king for as it relates to any given transaction.

The Envestnet | Yodlee PlatformEnvestnet | Yodlee, the webinar’s sponsor, and its cloud-based Financial Data Platform drives digital financial innovation and provides many of the tools City National Bank needs to build out the sort of digital customer experience described by Malo. The Envestnet | Yodlee Financial Cloud is an open technology platform that underpins the digital financial solutions for over 950 companies, said John Bird, Envestnet | Yodlee’s Senior Vice President for Product Marketing and Alliances.

Ultimately, Envestnet | Yodlee can help City National Bank provide their customers with a comprehensive view of all their financial data in real-time – including data provided by other institutions, Bird said. In tandem with Envestnet | Yodlee’s suite of applications, this allows customers to access, comprehend and interact more effectively with their finances.

Key to the Financial Data Platform is the data intelligence and analytics firepower that can enable City National Bank to deliver the right information to their customers at the right time, and transform the customer experience in the process.

An example of this is Envestnet | Yodlee’s Transaction Data Enrichment (TDE) solution. This new product-set adds important attributes to the data generated by bank, credit card and debit card transactions, making it much more useful. The enhanced data includes optimizations like natural language descriptions of the transaction, geo-location and other identifying characteristics of the merchant, which allows City National Bank and their customers to easily identify and assess the nature of the transaction.

Used in this way, the Yodlee TDE solution helps to reduce call center volumes and false fraud alerts, while also making it easier for both the institutions and their customers to monitor spending habits and preferences. Since understanding consumers is the basis for building a sustainable competitive advantage in banking, Yodlee’s TDE gives City National Bank the ability to improve their offerings, deepen their customer relationships, improve their customer retention and more effectively acquire new customers.