Embed Size (px)

Citation preview

Financial Liberalization and Growth: Empirical Evidence

AArrttuurroo AAlleejjaannddrroo GGuuiilllleerrmmoo GGaalliinnddoo MMiiccccoo OOrrddooññeezz11

[email protected] [email protected] [email protected]

Inter-American Development Bank

May, 2002

Abstract

This paper examines whether financial liberalization promotes economic

growth by analyzing its effects on the costs of external financing to firms. Following Rajan and Zingales’ (1998) methodology, we explore whether economic sectors that rely more on external finance grow faster than others after financial liberalization. Using this methodology and Kaminsky and Schmukler’s (2001) dataset on financial reforms, the paper shows that financial liberalization, mainly in the domestic financial sector, increases growth rates of economic sectors intensive in external funding relative to other sectors. Our results are robust to the fact that financial reform usually comes with other structural changes (e.g., trade liberalization).

1 We thank Graciela Kaminsky and Sergio Schmukler for sharing their data with us. We also thank Arturo Bris, Florencio Lopez de Silanes, Andrea Repetto and participants at the Economia Panel in Cambridge, MA, as well as participants at Banco de la República de Colombia’s brown bag seminar for useful comments and suggestions. The opinions in this paper reflect those of the authors and not necessarily those of the IADB.

2

1. - Introduction

Since the 1970s several countries have liberalized their financial systems.

Liberalization has been characterized by opening the capital account and removing

“financial repression” policies and restriction to foreign ownership. A crucial

question that deserves attention is whether these liberalizations have somehow

contributed to growth. Based on Rajan and Zingales (1998), this paper examines

whether financial liberalization reduces the cost of external finance to firms and

promotes growth. In particular, we ask whether firms that are relatively more in

need of external finance develop disproportionately faster in more liberalized

countries and during periods of high financial liberalization. We find this to be true

in our sample of 28 countries during the 1970s, 1980s and 1990s.

By the early 1970s many developing countries appeared to have slipped into

financial repression. Restrictions took the form of deposit and loan interest rate

controls, directed credit policies, and exchange and capital controls, among others.

These policies distorted the functioning of financial systems. According to Díaz-

Alejandro (1985, p. 7) financial repression leads to:

“…segmented domestic financial markets in which some obtained credit

(rationing) at very negative real interest rates, while non-favored borrowers had to

obtain funds in expensive and unstable informal credit markets. Public controls over

the banking system typically led to negative real interest rates for depositors.

Financial repression became an obstacle to domestic savings and their efficient

allocation, and financial intermediation languished.”

3

In response to adverse effects of financial restrictions, many countries have

engaged in liberalization strategies since the mid-1970s. Liberalization was

characterized by opening the capital account and by lifting restrictions on the

domestic financial system. With respect to the capital account, liberalization policies

included allowing corporations to borrow abroad and removing multiple exchange

rate mechanisms and other sorts of capital controls. Regarding the domestic

financial system, policies were aimed at removing interest rate controls (lending and

deposits), lifting other restrictions such as directed credit policies or limitations on

foreign currency deposits, allowing foreigners to own domestic equity, and

removing restrictions on repatriation of capital, dividends, and interest. Recent data

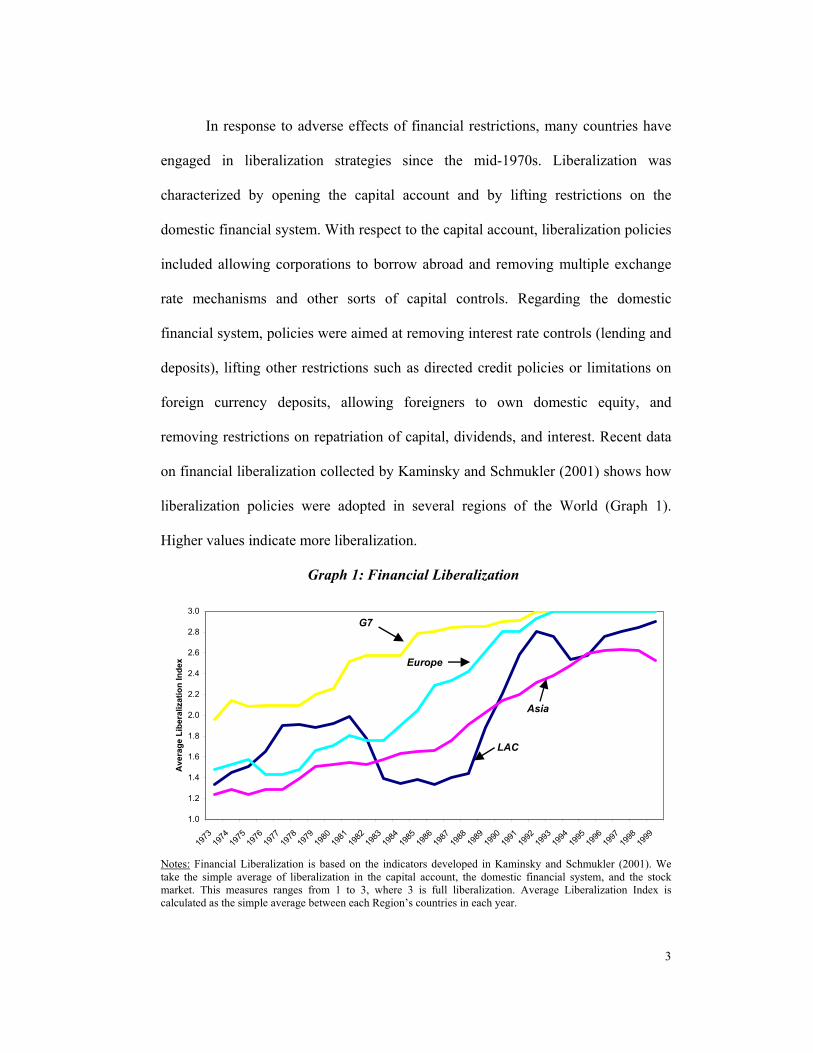

on financial liberalization collected by Kaminsky and Schmukler (2001) shows how

liberalization policies were adopted in several regions of the World (Graph 1).

Higher values indicate more liberalization.

Graph 1: Financial Liberalization

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

Ave

rage

Lib

eral

izat

ion

Inde

x

G7

Europe

LAC

Asia

Notes: Financial Liberalization is based on the indicators developed in Kaminsky and Schmukler (2001). We take the simple average of liberalization in the capital account, the domestic financial system, and the stock market. This measures ranges from 1 to 3, where 3 is full liberalization. Average Liberalization Index is calculated as the simple average between each Region’s countries in each year.

4

By the early 1970s the financial sector of most developed countries was

already significantly liberalized, while in most developing countries it was highly

repressed. The liberalization process was continuous and gradual in most regions,

except in Latin America, where an important reversal was observed in the 1980s. At

the beginning of the 1970s liberalization was rapid in Latin American countries.

This was mainly driven by the southern cone countries, which had engaged in

laissez- faire financial policies that mainly supported unrestricted private

participation in financial markets without direct government regulation. As noted by

Díaz-Alejandro (1985) this led to massive bankruptcies and a generalized financial

crisis throughout the region. Countries then abandoned laissez-faire practices,

introducing tighter regulations and restrictions to their financial systems. This came

with a de facto nationalization of the banking sector. Later, at the beginning of the

1990s, Latin America engaged once again in the liberalization strategy. The main

difference with respect to the previous liberalization wave was the implementation

of regulatory and supervision mechanisms to avoid the previous type of crisis.

A crucial question that deserves attention is whether liberalization has

somehow contributed to growth and through which channels. The literature has no

clear answer to this question, either from a theoretical or an empirical point of view.

Models of perfect markets suggest that financial liberalization should benefit

both borrowers and lenders. Starting with McKinnon (1973) and Shaw (1973), some

studies have pointed out that lifting financial restrictions can exert a positive effect

on growth rates as interest rates rise toward their competitive market equilibrium

and resources are allocated efficiently. In addition, capital account liberalization

allows firms to access cheaper foreign funds and puts pressure on the domestic

5

financial system to improve its efficiency. However, some authors claim that this

efficient-markets paradigm is misleading when applied to financial sector, in

particular to capital flows. Removing one distortion need not be welfare enhancing

when other distortions are present. Financial markets are characterized by serious

problems of asymmetric information and moral hazard issues that may undermine

the case for domestic financial liberalization (see next section for a complete

discussion of these arguments).

While theory does not give us a clear answer on the effect of financial

liberalization on growth, empirical studies are not conclusive, either. This is

particularly true in the case of capital account liberalization, which remains one of

the most controversial and least understood economic policies.2 The first reason for

this disappointing result is the lack of good and homogenous measures of financial

liberalization policies across countries and over time. A second serious issue in

virtually all studies of financial liberalization is the omitted variable problem, as the

financial liberalization process tends to be imposed and removed as part of large a

package of policies. Trade liberalization and the privatization of state enterprises, for

example, have coincided with the liberalization of the financial sector in many

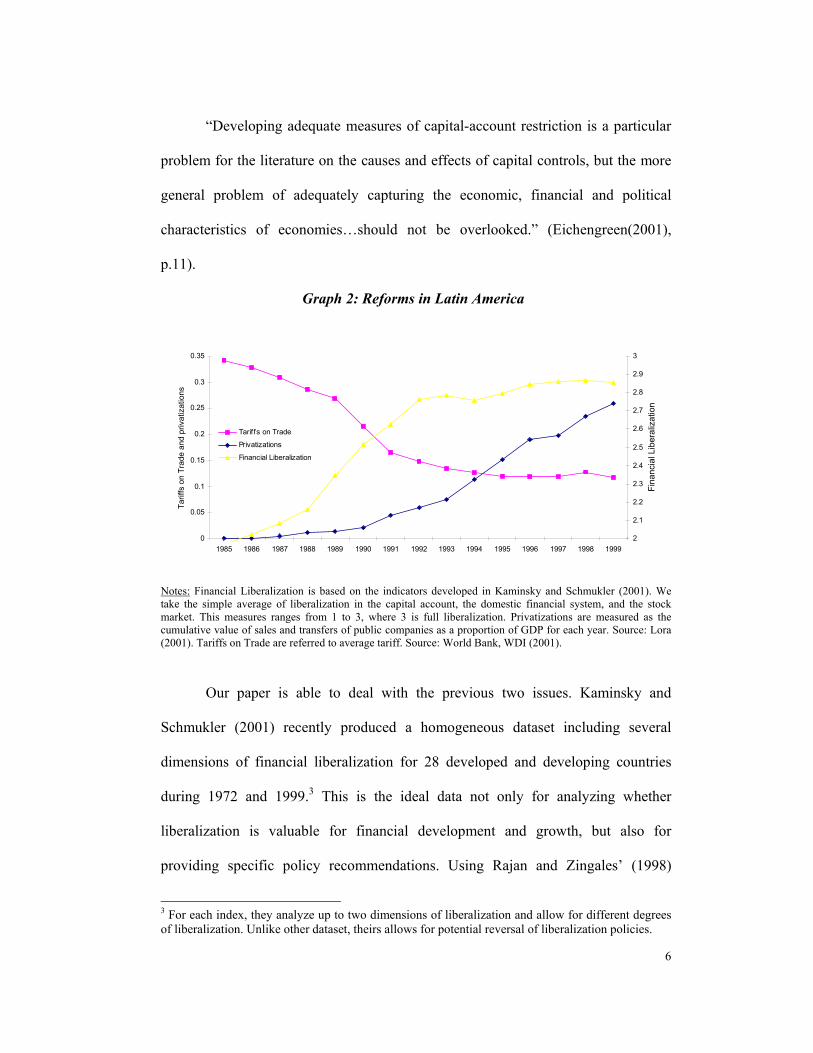

countries. As shown in Graph 2, Latin America is a clear example of this. Therefore,

it is crucial to control for all the other policy measures before to be able to conclude

about the effect of financial liberalization on growth. For the case of capital account

liberalization, Eichengreen (2001) pointed out the main challenges of this empirical

literature:

2 See Eichengreen (2001) for a survey.

6

“Developing adequate measures of capital-account restriction is a particular

problem for the literature on the causes and effects of capital controls, but the more

general problem of adequately capturing the economic, financial and political

characteristics of economies…should not be overlooked.” (Eichengreen(2001),

p.11).

Graph 2: Reforms in Latin America

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

Tarif

fs o

n Tr

ade

and

priv

atiz

atio

ns

2

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2.9

3

Fina

ncia

l Lib

eral

izat

ion

Tarif fs on Trade

Privatizations

Financial Liberalization

Notes: Financial Liberalization is based on the indicators developed in Kaminsky and Schmukler (2001). We take the simple average of liberalization in the capital account, the domestic financial system, and the stock market. This measures ranges from 1 to 3, where 3 is full liberalization. Privatizations are measured as the cumulative value of sales and transfers of public companies as a proportion of GDP for each year. Source: Lora (2001). Tariffs on Trade are referred to average tariff. Source: World Bank, WDI (2001).

Our paper is able to deal with the previous two issues. Kaminsky and

Schmukler (2001) recently produced a homogeneous dataset including several

dimensions of financial liberalization for 28 developed and developing countries

during 1972 and 1999.3 This is the ideal data not only for analyzing whether

liberalization is valuable for financial development and growth, but also for

providing specific policy recommendations. Using Rajan and Zingales’ (1998)

3 For each index, they analyze up to two dimensions of liberalization and allow for different degrees of liberalization. Unlike other dataset, theirs allows for potential reversal of liberalization policies.

7

methodology, the panel structure of the data allows us to identify the effect of

financial liberalization on growth controlling for most of the other reforms

implemented at the same time.

The theoretical underpinning of this relationship is rather simple and follows

the discussion of Rajan and Zingales (1998) on how financial development can

impact growth. They show that more developed financial systems can mitigate the

extent to which firms are affected by problems of moral hazard and adverse

selection, and hence can reduce the cost of loanable funds. This reduction in the cost

of external funds allows firms that depend more on them to grow faster. This

differential in growth across firms is the identification mechanism that allows us to

isolate the effect of financial liberalization on growth from the other reforms. In this

setup, we assume that the effect of these other reforms on firm growth is

uncorrelated with firm’ external financial dependence.

The rest of the paper is organized as follows. Section 2 presents a literature

review. Section 3 presents the data and the econometric framework. Section 4 shows

the evidence on the impact of financial liberalization on growth. Section 5 explores

the relationship between liberalization and financial sector development. Section 6

concludes.

2. - Literature Review Since the pioneering contributions of Goldsmith (1969), McKinnon (1973)

and Shaw (1973), the literature has focus on the relationship between financial

liberalization and economic growth. Financial liberalization may affect growth

through three mechanisms. First it may affect the development of the domestic

8

financial system in terms of size and efficiency, second it may affect the access of

domestic firms to foreign funds and finally it may reduce agency problems

improving corporate governance.

Several authors, starting with McKinnon (1973) and Shaw (1973), have

pointed out advantages of reducing financial repression in the domestic financial

system. They conclude that lifting financial restrictions can exert a positive effect on

growth rates as interest rates rise toward their competitive market equilibrium.

According to this tradition, ceilings on interest rates reduce savings, capital

accumulation, and discourage efficient allocation of resources. Additionally,

McKinnon points out that repression can lead to dualism in which firms that have

access to subsidized funding will tend to choose relatively capital-intensive

technologies, whereas those not favored by policy will only be able to implement

high-yield projects with short maturity.

Since then, many other authors have noted additional benefits of financial

liberalization. Foreign competition, in the form of entry of foreign institutions to the

local market (foreign banks) seems to develop the domestic financial sector and

reduces the costs of capital to domestic firms. Competition increases efficiency in

the domestic banking industry (see Claesens et al. (2001)) and allows countries to

benefit from frontier financial technologies as in Klenow and Rodríguez-Clare

(1997), and leads to increased growth. Moreover, foreign competition in the form of

access to foreign financial markets seems to reduce the costs of capital to domestic

firms (cross-listing –see Bekaert et al (2001)). This leads to higher investment and

growth (Bekaert and Harvey (2000) and Henry (2000a and 2000b)).

9

In addition, financial liberalization puts pressure to improve corporate

governance. Foreign competition may force the adoption of international accounting

and regulatory standards. These improvement may reduce the agency costs that

make it harder and more expensive for firms to raise funds in both the banking

sector and the securities market (see Claesens et al. (2001), Galindo et al (2001),

Stulz (1999) and Moel (2001)).

Laeven (2000) shows that financial liberalization can ease financial

constraints of the type described by Hubbard (1997) and Gilchrist and Himmelberg

(1998). This happens through two mechanisms. A direct one, by allowing more

capital -namely foreign- to become available, and an indirect one through an

improvement in the allocation of resources towards the sectors that were previously

more constrained. Tapping international capital markets can have significant impacts

derived from accessing a larger stock holder base, increased liquidity of stocks, and

the signaling effects of adopting international accounting standards, among other

possibilities (Sarkissian and Schill (2001)).

In summary the benefits of financial liberalization can be grouped into

increased access to domestic and international capital markets, and increased

efficiency of capital allocation.

Critics of financial liberalization policies have argued that the efficient-

markets paradigm is fundamentally misleading when applied to capital flows. In the

theory of the second best, removing one distortion need not be welfare enhancing

when other distortions are present. If capital account is liberalized while import-

competing industries are still protected for example, or if there is a downwardly-

inflexible real wage, capital may flow into sectors in which the country has a

10

comparative disadvantage, implying a reduction in welfare (Brecher and Diaz-

Alejandro (1977) and Brecher (1983).

In addition, if information asymmetries are endemic to financial markets and

transactions, in particular in countries with poor corporate governance and low legal

protections, there is no reason to think that financial liberalization, either domestic

or international, will be welfare improving (Stiglitz (2000)). Moreover, in countries

where the capacity to honor contracts and to assemble information relevant to

financial transactions is least advanced, there can be no presumption that capital will

flow into uses where its marginal product exceeds its opportunity cost.

Stiglitz (1994) argues in favor of certain forms of financial repression. He

claims that repression can have several positive effects such as: improving the

average quality of the pool of loan applicants by lowering interest rates; increasing

firm equity by lowering the price of capital; and accelerating the rate of growth if

credit is targeted towards profitable sectors such as exporters or sectors with high

technological spillovers. However, these claims can be doubtful given that they

increase the power of bureaucrats, who can be less capable than imperfect markets,

to allocate financial resources. This approach also opens doors to rent-seeking

activities.

Focusing on the development of the domestic financial sector, capital

account liberalization that allows firms to list abroad has been attributed to lead to

market fragmentation, and reduce the liquidity in the domestic market and inhibiting

its development. The inverse correlation between the amount of aggregate capital

raised by LAC corporations in the ADR market and the number of Initial Public

Offerings in Latin America seems to corroborate this argument (Moel, 2001).

11

Finally, liberalization has also been linked to macroeconomic instability. The

financial reforms carried out in several Latin American countries during the 1970s,

aimed at ending financial repression, yet led to financial crises characterized by

widespread bankruptcies, massive government interventions, nationalization of

private institutions and low domestic saving (Diaz-Alejandro (1985)). It is worth

noting that, as shown by Demirguc-Kunt and Detriagiache (1998), the likelihood of

a crisis following liberalization is decreasing in the level of institutional

development. In this sense, the arguments that Stiglitz (1994) makes in favor of

government intervention in financial markets in the form of prudential regulation

and supervision are convincing. The main argument is that the government is, de

facto, the insurer of the financial systems, and hence a financial collapse can have

significant fiscal repercussions. To the extent that regulation accompanies

liberalization, negative impacts such as those noted by Díaz-Alejandro can be

contained.

The extent to which financial liberalization affects growth remains an

empirical question. Several empirical pieces have tried to address it. Researchers

have followed two distinct empirical approaches. One proxies financial

liberalization with outcome variables, and the other focuses on explicit policy

measures. Regarding outcome variables, several measures have been posed to proxy

financial repression. Early empirical literature focused on the value of real interest

rates as an indicator of repression. The presumption was that countries with negative

real interest rates were financially repressed, while those with positive ones were

12

liberalized.4 In short they find that countries with negative real interest rates exhibit

lower growth rates than those with positive ones. However, De Gregorio and

Guidotti (1993) claim that real interest rates are not a good indicator of financial

repression, and that a better indicator of repression, or lack thereof, is the ratio of

credit to the private sector to GDP or other measures of financial development.

Several papers have analyzed the impact of this and other measures of

financial development on growth. There is consensus that financial development has

had a significant positive impact on the growth rates of countries.5 The extent to

which these results can be interpreted as being influenced by financial liberalization

is dubious. On the one hand, and as noted by Rajan and Zingales (1998) it is

unlikely that such empirical strategies are truly identifying the impact of financial

development on growth, due to the fact that financial development occurs at the

same time that economies go through significant structural transformations. In the

case of financial development, Rajan and Zingales (1998, p. 560) note “ …financial

development may simply be a leading indicator rather than a causal factor.”

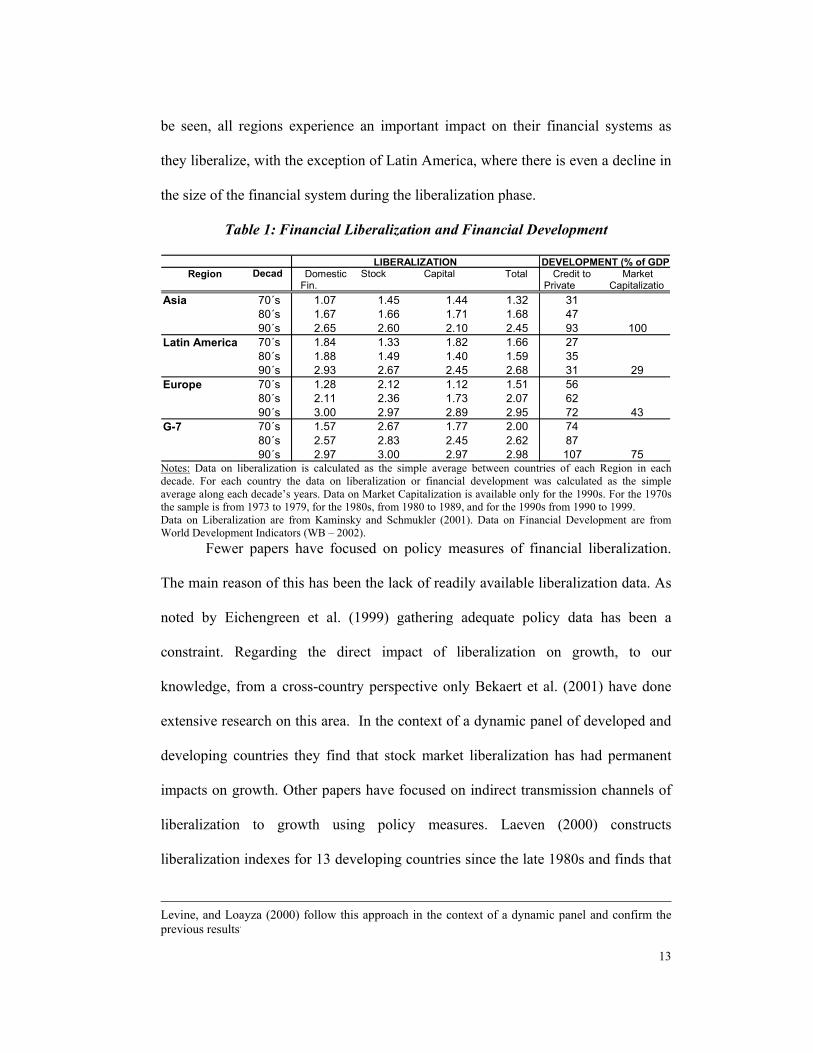

On the other hand, it is not clear either that financial liberalization has a one

to one impact on financial development. Note that it can be the case that financial

liberalization has no impact on financial development. Latin America is a clear

example of this. Table 1 shows different measures of financial development and

liberalization during the past three decades for several regions of the world. As can

4 Lanyi and Saracoglu (1983), Fry (1978), Roubini and Sala-i-Martin (1991), and World Bank (1989) are examples of this approach. 5 Ghani (1992) includes financial development in a Barro type growth equations for 50 developing countries and find significant impacts. De Gregorio and Guidotti find the same for middle and low-income countries. King and Levine (1993) expand the sample to 77 countries and add several proxies of financial development and find the same results. Levine, Loayza and Beck (1999) and Beck,

13

be seen, all regions experience an important impact on their financial systems as

they liberalize, with the exception of Latin America, where there is even a decline in

the size of the financial system during the liberalization phase.

Table 1: Financial Liberalization and Financial Development

Region Decad Domestic StockM k t

CapitalA t

Total Credit to MarketFin.S t

PrivateS t

CapitalizatioAsia 70´s 1.07 1.45 1.44 1.32 31

80´s 1.67 1.66 1.71 1.68 4790´s 2.65 2.60 2.10 2.45 93 100

Latin America 70´s 1.84 1.33 1.82 1.66 2780´s 1.88 1.49 1.40 1.59 3590´s 2.93 2.67 2.45 2.68 31 29

Europe 70´s 1.28 2.12 1.12 1.51 5680´s 2.11 2.36 1.73 2.07 6290´s 3.00 2.97 2.89 2.95 72 43

G-7 70´s 1.57 2.67 1.77 2.00 7480´s 2.57 2.83 2.45 2.62 8790´s 2.97 3.00 2.97 2.98 107 75

LIBERALIZATION DEVELOPMENT (% of GDP)

Notes: Data on liberalization is calculated as the simple average between countries of each Region in each decade. For each country the data on liberalization or financial development was calculated as the simple average along each decade’s years. Data on Market Capitalization is available only for the 1990s. For the 1970s the sample is from 1973 to 1979, for the 1980s, from 1980 to 1989, and for the 1990s from 1990 to 1999. Data on Liberalization are from Kaminsky and Schmukler (2001). Data on Financial Development are from World Development Indicators (WB – 2002).

Fewer papers have focused on policy measures of financial liberalization.

The main reason of this has been the lack of readily available liberalization data. As

noted by Eichengreen et al. (1999) gathering adequate policy data has been a

constraint. Regarding the direct impact of liberalization on growth, to our

knowledge, from a cross-country perspective only Bekaert et al. (2001) have done

extensive research on this area. In the context of a dynamic panel of developed and

developing countries they find that stock market liberalization has had permanent

impacts on growth. Other papers have focused on indirect transmission channels of

liberalization to growth using policy measures. Laeven (2000) constructs

liberalization indexes for 13 developing countries since the late 1980s and finds that

Levine, and Loayza (2000) follow this approach in the context of a dynamic panel and confirm the previous results.

14

the liberalization process in general has eased financial constraints faced by large

firms in these countries. Galindo et al. (2001) use Laeven’s data and find that

financial liberalization increases the allocative efficiency of investment.

As noted above, these papers are also subject to the identification critique.

According to Fry (1995, p. 179), the simultaneity of reforms appears binding for

researchers:

“… in practice, however, most clear cut cases of financial liberalization were

accompanied by other economic reforms (such as fiscal, international trade, and

foreign exchange reforms). In such cases it is virtually impossible to isolate the

effects of financial components of the reform package.”

Bekaert et al., as well as Galindo et al., try to isolate the impact of financial

liberalization by controlling for other reforms and macroeconomic events taking

place simultaneously. Even if this allows some identification it remains unclear if

the set of controls is large enough to isolate the effect of financial reform.

This paper improves substantially on these issues since it adopts a very clean

methodology that allows the isolation of impact of financial liberalization on

growth. As noted, there are several cross-country studies that find evidence of a

positive effect of various measures of financial development on growth. Rajan and

Zingales (1998) survey this literature. To our knowledge, however, no paper

addresses the issue of financial liberalization and growth directly from a cross-

industry-country panel data perspective. This is an additional contribution of this

work.

15

3. - Empirical Method and Data Rajan and Zingales (1998) faced problems similar to those mentioned in the

previous section when addressing the impact of development on growth. Namely,

identifying the true causal impact of financial development in a context of multiple

structural reforms rose as a challenge. In order to overcome these problems they

propose a test to identify the true impact of financial development on growth. The

basis of their test is the presumption that the development of financial markets and

institutions reduces the cost of external funds faced by firms by reducing the impact

of problems associated with moral hazard and adverse selection. From this

perspective the impact of financial development must differ according to the needs

of particular firms for external funds. Firms that rely more on external funds will be

more impacted by financial development than those that require little capital. Using

firm-level data, Rajan and Zingales identify the need for external finance (the

difference between investment and operating income) for several industries at the

ISIC three and four digit level. Given that the US market is relatively frictionless,

they assume that such technological demands for external capital would apply in

other countries once market distortions are removed.

Using this identification technique, they estimate whether development

affects industry growth by interacting several measures of financial development

with the industry demand for external funds proxy in a cross-country-industry

growth regression in which they control for country and industry-specific

characteristics. By controlling for these specific factors the omitted variable problem

is significantly reduced. Moreover, by estimating the interactive term they can fully

16

identify the impact of financial development as opposed to other events that, as

shown in the introduction, can occur simultaneously.

Since our question is subject to the same criticisms as those of the

relationship between financial liberalization and growth, our empirical methodology

follows Rajan and Zingales in a panel data context. We estimate the following

empirical model using time series of cross-industry-country data:

ijtjtijjtijtijt reqlibfinsharegrowth ελµααα +++++= − *_2110 (1)

where the dependent variable is the growth of real value added of sector i in

country j at time t, shareijt-1 is the share of industry i in country j of total value added

in manufacturing at the beginning of the period, fin_libjt is the measure of financial

liberalization of country j at time t (in some regressions we use Financial

development to replicate Rajan and Zingales), and reqi is the requirement of industry

i for external funds. Additionally we include µi,, an industry-specific fixed effect,

and λjt, a country-year effect. Finally, εijt is the error term. Our test of how financial

liberalization affects growth is mainly on the size and significance of α2.

Note that this methodology is very clean, in the sense that the inclusion of

country-year effects corrects for other types of events possible correlated with

financial liberalization, such as the general liberalization trend for Latin America

during the 1990s. This, combined with the interaction of financial liberalization with

the external dependency measure, allows for a full identification of the financial

liberalization contribution to sector growth.

Our sector value-added data comes from United Nations Statistical Division

and covers the 28 countries for which Kaminsky and Schmukler (2001) have

17

information about financial liberalization during the period 1972-1998. Our measure

of sector dependence on external financing is taken from Rajan and Zingales (1998).

Their dataset covers 37 industries; 28 of them correspond to three-digit ISIC codes

and 9 correspond to four-digit ISIC code (see Data Appendix).

The following section shows our empirical results using this methodology

and data.

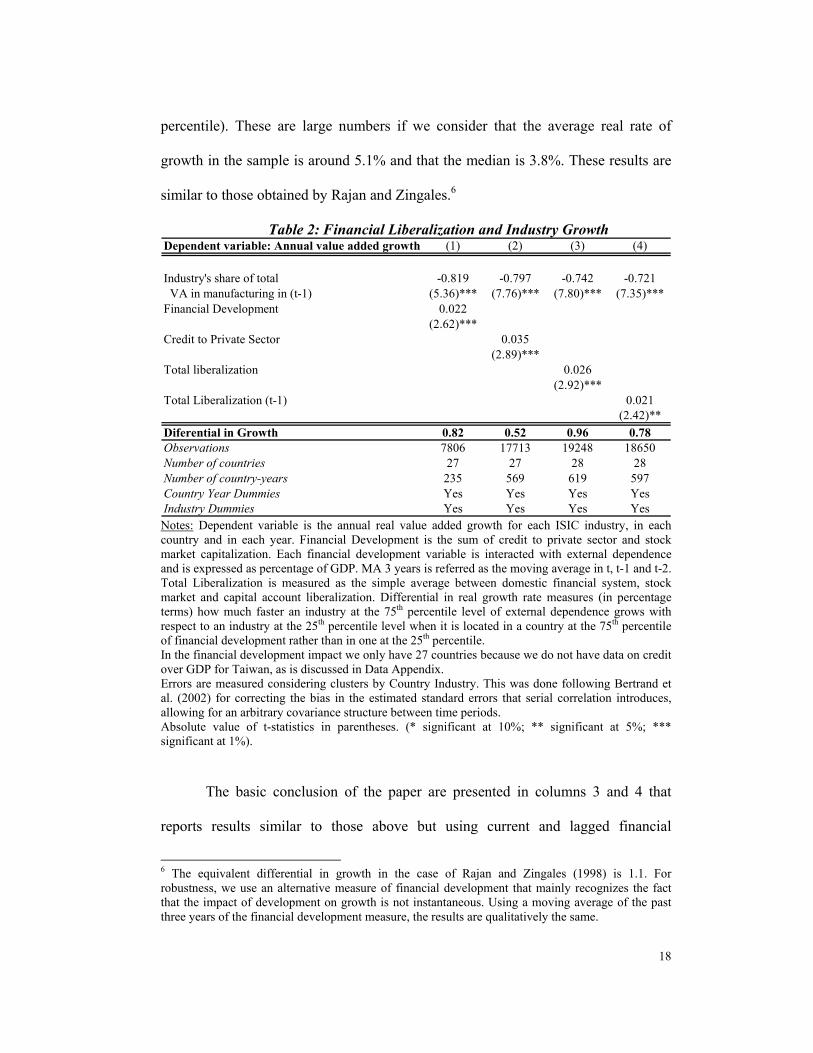

4.- Financial Liberalization and Growth

The first two columns in Table 2 replicate Rajan and Zingales’ (1998) results

using our sample in a panel data setup. As usual in this literature, our measure of

financial development is either the ratio of private credit to GDP or the ratio of

private credit plus stock market capitalization to GDP. The first column shows that

sectors with higher external dependency grow faster in countries that have well-

developed financial sectors as measured by the ratio of the sum of private credit and

stock market capitalization to GDP. The second column redoes the same exercise

using just the ratio private credit to GDP. The signs of the coefficients are positive

and significant. The line labeled differential in growth at the bottom of the table

shows the impact, according to our estimation, on growth differentials across sectors

and countries. For example, in column 1 this differential is 0.82. This should be

interpreted as follows: the relative growth rate of an industry in the 75th percentile of

external requirements relative to an industry in the 25th percentile, in a country with

high financial development (in the 75th percentile of financial development), is 0.82

percentage points higher than that in a country with a weak financial sector (25th

18

percentile). These are large numbers if we consider that the average real rate of

growth in the sample is around 5.1% and that the median is 3.8%. These results are

similar to those obtained by Rajan and Zingales.6

Table 2: Financial Liberalization and Industry Growth Dependent variable: Annual value added growth (1) (2) (3) (4)

Industry's share of total -0.819 -0.797 -0.742 -0.721 VA in manufacturing in (t-1) (5.36)*** (7.76)*** (7.80)*** (7.35)***Financial Development 0.022

(2.62)***Credit to Private Sector 0.035

(2.89)***Total liberalization 0.026

(2.92)***Total Liberalization (t-1) 0.021

(2.42)**Diferential in Growth 0.82 0.52 0.96 0.78Observations 7806 17713 19248 18650Number of countries 27 27 28 28Number of country-years 235 569 619 597Country Year Dummies Yes Yes Yes YesIndustry Dummies Yes Yes Yes Yes Notes: Dependent variable is the annual real value added growth for each ISIC industry, in each country and in each year. Financial Development is the sum of credit to private sector and stock market capitalization. Each financial development variable is interacted with external dependence and is expressed as percentage of GDP. MA 3 years is referred as the moving average in t, t-1 and t-2. Total Liberalization is measured as the simple average between domestic financial system, stock market and capital account liberalization. Differential in real growth rate measures (in percentage terms) how much faster an industry at the 75th percentile level of external dependence grows with respect to an industry at the 25th percentile level when it is located in a country at the 75th percentile of financial development rather than in one at the 25th percentile. In the financial development impact we only have 27 countries because we do not have data on credit over GDP for Taiwan, as is discussed in Data Appendix. Errors are measured considering clusters by Country Industry. This was done following Bertrand et al. (2002) for correcting the bias in the estimated standard errors that serial correlation introduces, allowing for an arbitrary covariance structure between time periods. Absolute value of t-statistics in parentheses. (* significant at 10%; ** significant at 5%; *** significant at 1%).

The basic conclusion of the paper are presented in columns 3 and 4 that

reports results similar to those above but using current and lagged financial

6 The equivalent differential in growth in the case of Rajan and Zingales (1998) is 1.1. For robustness, we use an alternative measure of financial development that mainly recognizes the fact that the impact of development on growth is not instantaneous. Using a moving average of the past three years of the financial development measure, the results are qualitatively the same.

19

liberalization instead of financial development as a regressor, respectively. These

results suggest that financial liberalization boost growth in sectors with higher

external dependency. Column 3 suggests that industries that depend on external

financing (75th percentile) grow 0.96% faster, relative to industries with low external

financing dependence, in periods of full liberalization compared to those of partial

liberalization. Once again this is a very significant figure given the average values of

sector growth in our sample.7

To obtain the long run effect of financial liberalization we have to divide its

coefficient by the lag sector-share coefficient multiplied by (-1). The results in

column 3 suggest that, in the long run, industries that depend more on external

financing (at the 75th percentile level) and are located in a fully liberalized economy

will have a share over total value added 1.6% higher than the same type of industries

located in a country that is only partially liberalized. This is an important effect if we

consider that the average sector-share in our sample is 3.3 %.

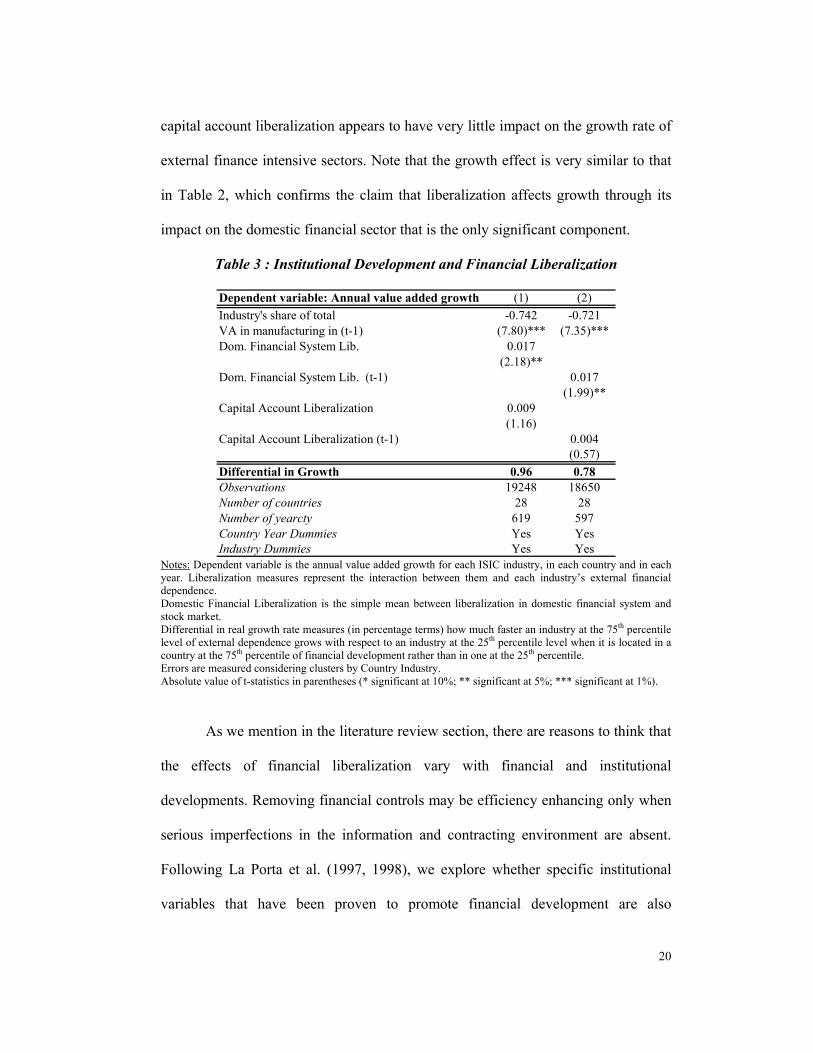

To identify the mechanism through which financial liberalization boosts

growth we open our measure in two components. On the one hand we study

liberalization on domestic financial system and on stock market, and on the other we

analyze the impact of capital account liberalization. As shown in Table 3, what

matters in our estimations is the liberalization of domestic financial markets.

Unreported results shows that it is a very robust result: domestic financial system

liberalization is the key component regarding the impact of liberalization on growth;

7 As robustness checks, we allow for different lag structures of the financial liberalization measures and also different constructions of the liberalization variable (principal components). Results are qualitatively the same.

20

capital account liberalization appears to have very little impact on the growth rate of

external finance intensive sectors. Note that the growth effect is very similar to that

in Table 2, which confirms the claim that liberalization affects growth through its

impact on the domestic financial sector that is the only significant component.

Table 3 : Institutional Development and Financial Liberalization

Dependent variable: Annual value added growth (1) (2)Industry's share of total -0.742 -0.721VA in manufacturing in (t-1) (7.80)*** (7.35)***Dom. Financial System Lib. 0.017

(2.18)**Dom. Financial System Lib. (t-1) 0.017

(1.99)**Capital Account Liberalization 0.009

(1.16)Capital Account Liberalization (t-1) 0.004

(0.57)Differential in Growth 0.96 0.78Observations 19248 18650Number of countries 28 28Number of yearcty 619 597Country Year Dummies Yes YesIndustry Dummies Yes Yes

Notes: Dependent variable is the annual value added growth for each ISIC industry, in each country and in each year. Liberalization measures represent the interaction between them and each industry’s external financial dependence. Domestic Financial Liberalization is the simple mean between liberalization in domestic financial system and stock market. Differential in real growth rate measures (in percentage terms) how much faster an industry at the 75th percentile level of external dependence grows with respect to an industry at the 25th percentile level when it is located in a country at the 75th percentile of financial development rather than in one at the 25th percentile. Errors are measured considering clusters by Country Industry. Absolute value of t-statistics in parentheses (* significant at 10%; ** significant at 5%; *** significant at 1%).

As we mention in the literature review section, there are reasons to think that

the effects of financial liberalization vary with financial and institutional

developments. Removing financial controls may be efficiency enhancing only when

serious imperfections in the information and contracting environment are absent.

Following La Porta et al. (1997, 1998), we explore whether specific institutional

variables that have been proven to promote financial development are also

21

associated with the impact of liberalization on growth. There are several usual

suspects in this literature. The legal origin of law codes, rule of law, creditor

protection and effective creditor rights protection8 are usual candidates for

explaining cross-country differences in financial sector development.

Presumably, economies that afford weak legal protections to creditors are

less likely to benefit from liberalization. The literature has shown that these are

dominant features explaining the development of financial markets. If these

protections are not in place the liberalization of restrictions on intermediation are

dampened by the adverse effects of institutional disarrays and do not promote

financial sector development. The absence of legal protections that guarantee the

ability of creditors to minimize their financial loss in case of borrower default can

counteract the potential efficiency effects that financial liberalization can induce.

To test this hypothesis we re-estimate equation [1] including interactive

terms between the liberalization measure, and the different proxies for legal

protections. Specifically we estimate:

ijtjtijj

jjjtjjtijtijt

LegreqLegreqlibfinreqlibfinsharegrowth

ελµα

αααα

++++

+++= −

***_*_

4

32110 (2)

where Leg is any of the legal protection proxies mentioned above. α3

captures the differential effect, if any, of countries with different legal protections.

Higher values of Leg indicate greater legal protection. Hence, one would expect α3

to be positive if our claims are accurate.

8 Effective creditor rights protection is the product of the rule of law index and creditor rights. It intends to capture the extent to which creditor rights regulations can be enforced or not. See Galindo and Micco (2002) for a discussion.

22

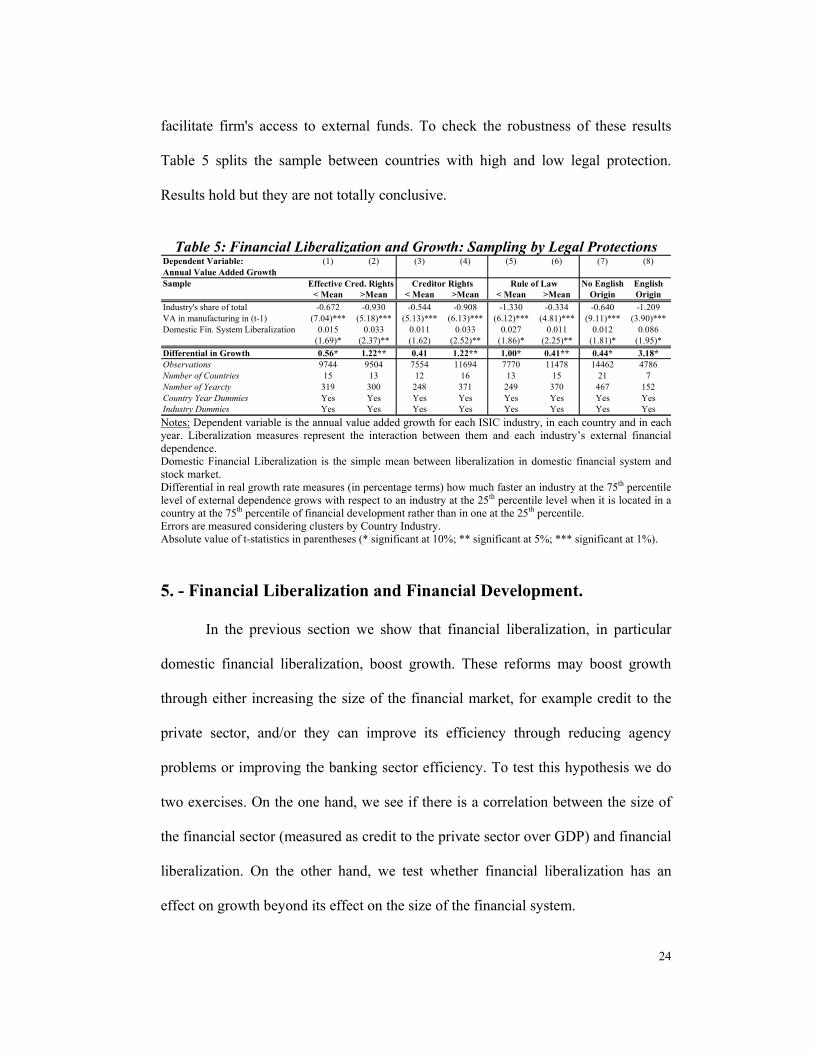

Table 4 reports our results. Column 1 reports the regression without any

interaction with the legal protections. The results are hence equivalent to those

above but now focusing only in domestic financial liberalization. Column 2 reports

the result including the interaction of the liberalization measure and effective

creditor rights. Note that the significance of both terms drops dramatically. However

this must not be interpreted as meaning that economic significance of this interaction

is lost. The loss of significance is attributed to the fact that both regressors are

importantly collinear (0.76). Hence the relevant test is one on joint significance. We

report this at the bottom of Table 4. Note that independent of the legal protection-

proxy used joint significance is always above standard level. Column 2 thus

suggests that liberalization has a greater impact in countries where creditors are

more protected. As above, we present the differential growth impact. Now we

compare this impact in countries in the 75th percentile of legal protection with those

in the 25th. The results suggest that the differential impact is higher where creditor

protections are in place. Columns 3 and 4 show the same exercises using creditor

rights and rule of law instead of effective creditor rights, respectively. The

interpretation of results follows those of effective creditor rights.

The previous three measures of legal protection have the caveat that they

could be endogenous; the need for financial development may create pressure to

improve legal protection.9 To avoid this problem, in column 5 we use legal origins

as a proxy for legal protection.10 As shown by previous research (see La Porta et al.

(1998)), common law origin countries tend to have higher protections. This result

9 In addition these measure are only available for 1998. 10 Our proxy for legal protection is a dummy variable that is one for countries with common law legal origin and zero otherwise.

23

again suggests that higher legal protections magnify the impact of financial

liberalization on growth.

Table 4: Financial Liberalization and Growth: Interactions with Legal Protections

Dependent Variable: Annual Value Added Growth (1) (3) (4) (5) (6)Industry's share of total -0.738 -0.743 -0.737 -0.762 -0.752VA in manufacturing in (t-1) (7.83)*** (7.89)*** (7.86)*** (7.85)*** (7.96)***Domestic Financial System Lib. 0.024 0.015 0.015 0.005 0.014

(3.00)** (1.69)* (1.98)** (0.18) (2.09)**Domestic Financial System Lib. 0.023 (Int. with Efective Cred. Rights) (1.07)Domestic Financial System Lib. 0.018 (Int. with Creditor Rights) (0.92)Domestic Financial System Lib. 0.019 (Int. with Rule of Law) (0.66)Domestic Financial System Lib. 0.055 (Int. with English Legal Origin) (2.08)**Differential in growth 0.9** (Institutional Measure in average)Differential in growth 0.7** 0.7*** 0.5 (Institutional Measure in percentil 25)Differential in growth 1.0*** 1.1** 0.8*** (Institutional Measure in percentil 75)Differential in growth 0.5** (No English Legal Origin)Differential in growth 2.6** (English Legal Origin)Observations 19248 19248 19248 19248 19248Number of countries 28 28 28 28 28Number of yearcty 619 619 619 619 619Country Year Dummies Yes Yes Yes Yes YesIndustry Dummies Yes Yes Yes Yes YesF test /2 3.85** 4.88*** 5.03*** 3.78**Prob > F 0.021 0.008 0.007 0.023 Notes: Dependent variable is the credit to private sector as percentage of GDP. DFSL is Domestic Financial System Liberalization measured as the simple average between domestic system and stock market liberalization. The impact of financial liberalization on financial development is measured as a percentage of GDP, both for countries at the 25th and at the 75th percentile level in each considered institutional variable. Significance level for each impact is calculated by the following linear combination test: Domestic Financial Liberalization + Domestic Financial Liberalization (Interacted with Institutional Measure) * Value of Institutional Measure (at the considered percentile) = 0 All institutional variables are normalized between 0 and 1, 1 being the better possible situation. Errors are measured considering clusters by Country Industry. Absolute value of z-statistics and t-statistics in parentheses. (* significant at 10%; ** significant at 5%; *** significant at 1%). 2 / F test: Domestic Financial Liberalization = Domestic Financial Liberalization (Interacted with Institutional Measure) = 0

Liberalization only seems to boost growth if structural legal conditions, such

as the protection of property and creditor rights, are imbedded in the law codes and

are effectively enforced. Without these requirements, liberalization does not seem to

24

facilitate firm's access to external funds. To check the robustness of these results

Table 5 splits the sample between countries with high and low legal protection.

Results hold but they are not totally conclusive.

Table 5: Financial Liberalization and Growth: Sampling by Legal Protections

Dependent Variable: (1) (2) (3) (4) (5) (6) (7) (8)Annual Value Added GrowthSample No English English

< Mean >Mean < Mean >Mean < Mean >Mean Origin OriginIndustry's share of total -0.672 -0.930 -0.544 -0.908 -1.330 -0.334 -0.640 -1.209VA in manufacturing in (t-1) (7.04)*** (5.18)*** (5.13)*** (6.13)*** (6.12)*** (4.81)*** (9.11)*** (3.90)***Domestic Fin. System Liberalization 0.015 0.033 0.011 0.033 0.027 0.011 0.012 0.086

(1.69)* (2.37)** (1.62) (2.52)** (1.86)* (2.25)** (1.81)* (1.95)*Differential in Growth 0.56* 1.22** 0.41 1.22** 1.00* 0.41** 0.44* 3.18*Observations 9744 9504 7554 11694 7770 11478 14462 4786Number of Countries 15 13 12 16 13 15 21 7Number of Yearcty 319 300 248 371 249 370 467 152Country Year Dummies Yes Yes Yes Yes Yes Yes Yes YesIndustry Dummies Yes Yes Yes Yes Yes Yes Yes Yes

Effective Cred. Rights Creditor Rights Rule of Law

Notes: Dependent variable is the annual value added growth for each ISIC industry, in each country and in each year. Liberalization measures represent the interaction between them and each industry’s external financial dependence. Domestic Financial Liberalization is the simple mean between liberalization in domestic financial system and stock market. Differential in real growth rate measures (in percentage terms) how much faster an industry at the 75th percentile level of external dependence grows with respect to an industry at the 25th percentile level when it is located in a country at the 75th percentile of financial development rather than in one at the 25th percentile. Errors are measured considering clusters by Country Industry. Absolute value of t-statistics in parentheses (* significant at 10%; ** significant at 5%; *** significant at 1%).

5. - Financial Liberalization and Financial Development.

In the previous section we show that financial liberalization, in particular

domestic financial liberalization, boost growth. These reforms may boost growth

through either increasing the size of the financial market, for example credit to the

private sector, and/or they can improve its efficiency through reducing agency

problems or improving the banking sector efficiency. To test this hypothesis we do

two exercises. On the one hand, we see if there is a correlation between the size of

the financial sector (measured as credit to the private sector over GDP) and financial

liberalization. On the other hand, we test whether financial liberalization has an

effect on growth beyond its effect on the size of the financial system.

25

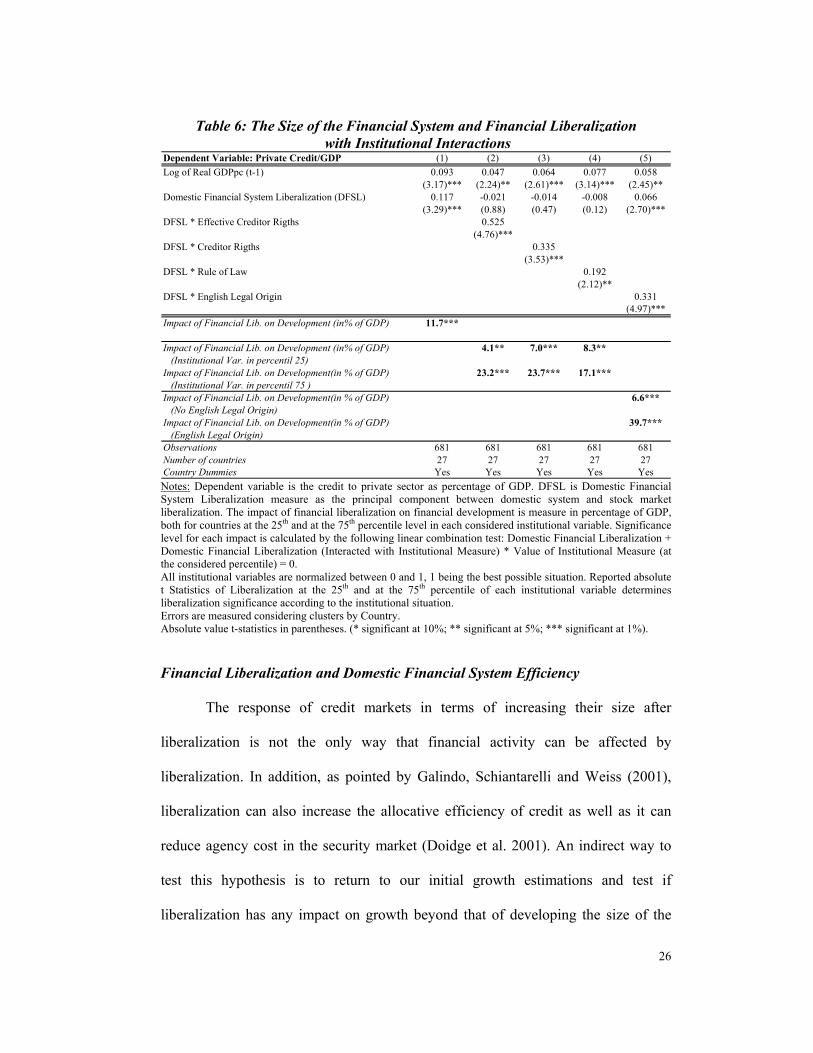

Financial Liberalization and the Size of the Financial System

Table 6 reports the correlation between financial liberalization and the size

of the financial system. We include interactive terms between the liberalization

measure, and the different proxies for legal protections of creditors. Beside these

variables, we include the lag of log GDP per capita and country fixed effects as

controls. Our measure for the financial system size is the current ratio of credit to the

private system over GDP.

Results suggest that financial liberalization increases the size of the financial

system in countries with more developed institutions. Specifically, we find that

countries with low creditor protections do not take complete advantage of possible

effects of liberalization. On the bottom of the Table 6 we include estimates of the

impact of financial liberalization on the financial system size in the extreme

countries. For example, in column 2 we show that in a country with low effective

creditor rights (in the 25th percentile) liberalization has a minimum correlation with

credit market development. An increase in liberalization leads to a 4.1 percentage

points of GDP increase of credit markets. On the other hand, if creditor rights are

highly protected (in the 75th percentile) an increase in liberalization leads to a 23.2

percentage points of GDP increase in the size of credit markets. We obtain similar

results for the case of creditor right and rule of law.

Finally, column 5 reports the same results using a completely exogenous

proxy for legal protections: the origin of the legal code. Not surprisingly, the results

suggest that common law countries tend to have advantages from liberalizing due to

the fact that they are more oriented toward creditor protection.

26

Table 6: The Size of the Financial System and Financial Liberalization with Institutional Interactions

Dependent Variable: Private Credit/GDP (1) (2) (3) (4) (5)Log of Real GDPpc (t-1) 0.093 0.047 0.064 0.077 0.058

(3.17)*** (2.24)** (2.61)*** (3.14)*** (2.45)**Domestic Financial System Liberalization (DFSL) 0.117 -0.021 -0.014 -0.008 0.066

(3.29)*** (0.88) (0.47) (0.12) (2.70)***DFSL * Effective Creditor Rigths 0.525

(4.76)***DFSL * Creditor Rigths 0.335

(3.53)***DFSL * Rule of Law 0.192

(2.12)**DFSL * English Legal Origin 0.331

(4.97)***Impact of Financial Lib. on Development (in% of GDP) 11.7***

Impact of Financial Lib. on Development (in% of GDP) 4.1** 7.0*** 8.3** (Institutional Var. in percentil 25)Impact of Financial Lib. on Development(in % of GDP) 23.2*** 23.7*** 17.1*** (Institutional Var. in percentil 75 )Impact of Financial Lib. on Development(in % of GDP) 6.6*** (No English Legal Origin)Impact of Financial Lib. on Development(in % of GDP) 39.7*** (English Legal Origin)Observations 681 681 681 681 681Number of countries 27 27 27 27 27Country Dummies Yes Yes Yes Yes Yes Notes: Dependent variable is the credit to private sector as percentage of GDP. DFSL is Domestic Financial System Liberalization measure as the principal component between domestic system and stock market liberalization. The impact of financial liberalization on financial development is measure in percentage of GDP, both for countries at the 25th and at the 75th percentile level in each considered institutional variable. Significance level for each impact is calculated by the following linear combination test: Domestic Financial Liberalization + Domestic Financial Liberalization (Interacted with Institutional Measure) * Value of Institutional Measure (at the considered percentile) = 0. All institutional variables are normalized between 0 and 1, 1 being the best possible situation. Reported absolute t Statistics of Liberalization at the 25th and at the 75th percentile of each institutional variable determines liberalization significance according to the institutional situation. Errors are measured considering clusters by Country. Absolute value t-statistics in parentheses. (* significant at 10%; ** significant at 5%; *** significant at 1%). Financial Liberalization and Domestic Financial System Efficiency

The response of credit markets in terms of increasing their size after

liberalization is not the only way that financial activity can be affected by

liberalization. In addition, as pointed by Galindo, Schiantarelli and Weiss (2001),

liberalization can also increase the allocative efficiency of credit as well as it can

reduce agency cost in the security market (Doidge et al. 2001). An indirect way to

test this hypothesis is to return to our initial growth estimations and test if

liberalization has any impact on growth beyond that of developing the size of the

27

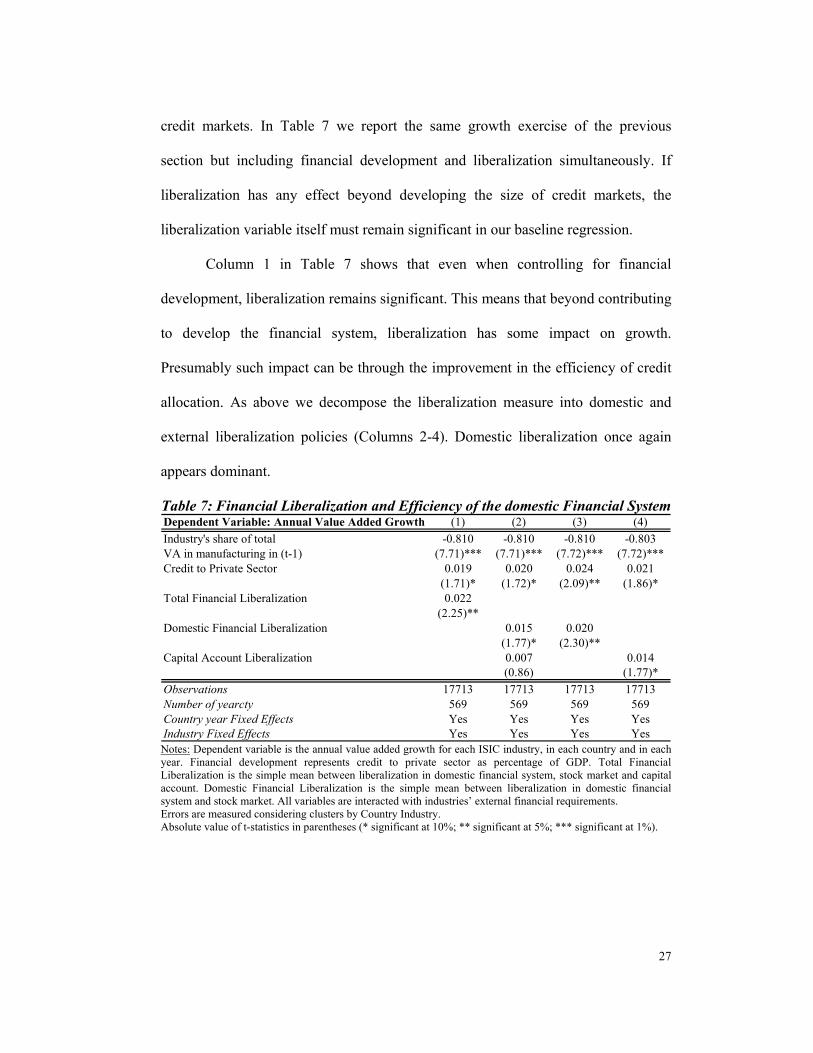

credit markets. In Table 7 we report the same growth exercise of the previous

section but including financial development and liberalization simultaneously. If

liberalization has any effect beyond developing the size of credit markets, the

liberalization variable itself must remain significant in our baseline regression.

Column 1 in Table 7 shows that even when controlling for financial

development, liberalization remains significant. This means that beyond contributing

to develop the financial system, liberalization has some impact on growth.

Presumably such impact can be through the improvement in the efficiency of credit

allocation. As above we decompose the liberalization measure into domestic and

external liberalization policies (Columns 2-4). Domestic liberalization once again

appears dominant.

Table 7: Financial Liberalization and Efficiency of the domestic Financial System Dependent Variable: Annual Value Added Growth (1) (2) (3) (4)Industry's share of total -0.810 -0.810 -0.810 -0.803VA in manufacturing in (t-1) (7.71)*** (7.71)*** (7.72)*** (7.72)***Credit to Private Sector 0.019 0.020 0.024 0.021

(1.71)* (1.72)* (2.09)** (1.86)*Total Financial Liberalization 0.022

(2.25)**Domestic Financial Liberalization 0.015 0.020

(1.77)* (2.30)**Capital Account Liberalization 0.007 0.014

(0.86) (1.77)*Observations 17713 17713 17713 17713Number of yearcty 569 569 569 569Country year Fixed Effects Yes Yes Yes YesIndustry Fixed Effects Yes Yes Yes Yes Notes: Dependent variable is the annual value added growth for each ISIC industry, in each country and in each year. Financial development represents credit to private sector as percentage of GDP. Total Financial Liberalization is the simple mean between liberalization in domestic financial system, stock market and capital account. Domestic Financial Liberalization is the simple mean between liberalization in domestic financial system and stock market. All variables are interacted with industries’ external financial requirements. Errors are measured considering clusters by Country Industry. Absolute value of t-statistics in parentheses (* significant at 10%; ** significant at 5%; *** significant at 1%).

28

6. - Conclusions As found in previous work by Rajan and Zingales, financial development

allows for the provision of cheaper funds which tend to benefit and stimulate the

growth of economic sectors that are dependent on external funding. We find that

financial liberalization is an instrument that, under certain conditions, promotes

financial sector development and through it can stimulate the relative growth rate of

sectors that rely on external funding. In order to promote development, though, other

structural reforms that support the proper behavior of financial markets have to be in

place. Hence even if systems reach full liberalization, the impact of liberalization on

domestic credit market growth can be null if rules and institutions that support

creditor rights are not in place. If the proper legal setup is in place, the impact of

liberalization on growth can be notable. Finally, it is worth to note that, like Rodrik

(1998), we find that, contrary to policies which reduce domestic “financial

repression,” capital account liberalization does not seem to boost growth.

29

Data Appendix Our sample includes the 28 countries that have data on financial liberation

from Kaminsky and Schmukler (2001) for the period 1973-1998. This data includes

information on capital account, domestic financial sector and stock market

liberalization. For capital markets liberalization they study whether corporations are

allowed to borrow abroad and if multiple exchange rate mechanisms or other sorts

of capital controls are in place. Regarding financial liberalization they explore

interest rate controls (lending and deposits) and other restrictions such as directed

credit policies or limitations on foreign currency deposits. With respect to stock

market liberalization they analyze the degree to which foreigners are allowed to own

domestic equity and restrictions on repatriation of capital, dividends, and interest.

Each area of interest has an index ranging from 1 to 3. Higher values indicate higher

liberalization. The average for different regions is reported in Table 1. The last

column in that table presents a financial liberalization index that averages the three

independent measures. The countries and regions with information are the ones

shown in Table 7 at the end of this Appendix.

Our measure of sector dependence on external financing is taken from Rajan

and Zingales (1998). Their dataset covers 37 industries; 28 of them correspond to

three-digit ISIC codes and 9 correspond to four-digit ISIC code.

Data on value added for each industry in each country were obtained from

three different sources. The first of them was the Industrial Statistics Yearbook

database put together by the United Nations Statistical Division (UNIDO, 2001). To

deflate our series we follows Rajan and Zingales (1998). The rate of growth of each

30

industry’s real value added is the difference between its rate of growth in nominal

terms minus the deflator rate of growth for the entire manufacturing sector. The

manufacturing deflator was calculated by the difference between the growth in

manufacturing nominal value added minus the rate of growth of the industrial

production index, obtained from the IMF’s International Finance Statistics (IFS)

database. Data of industrial production for Taiwan was obtained from its

Government web page http://www.stat.gov.tw/.

The second information source for value added was the “Programa de

Análisis de la Dinámica Industrial” (PADI-2000) database constructed by the

Division de Desarrollo Productivo y Empresarial - CEPAL. This database only

provides information for Latin American countries but is much more complete than

UNIDO information for these countries.

Finally, we also used the OECD STAN database for Industrial Analysis

edited by OECD in 1998. This dataset has information for all OECD countries and is

also available for our sample years.

From these three databases we constructed two different datasets. The first

dataset is just the UNIDO database that has information for all the countries in our

sample. The alternative dataset is a combination of the information of UNIDO,

PADI and OECD databases, though we used data of PADI and OECD whenever it

was possible. The databases mix was just across countries (data on each country has

only one information source for all the considered years). For this last dataset, 55%

of the observations come from the OECD database, 20% from PADI and 25% from

UNIDO.

31

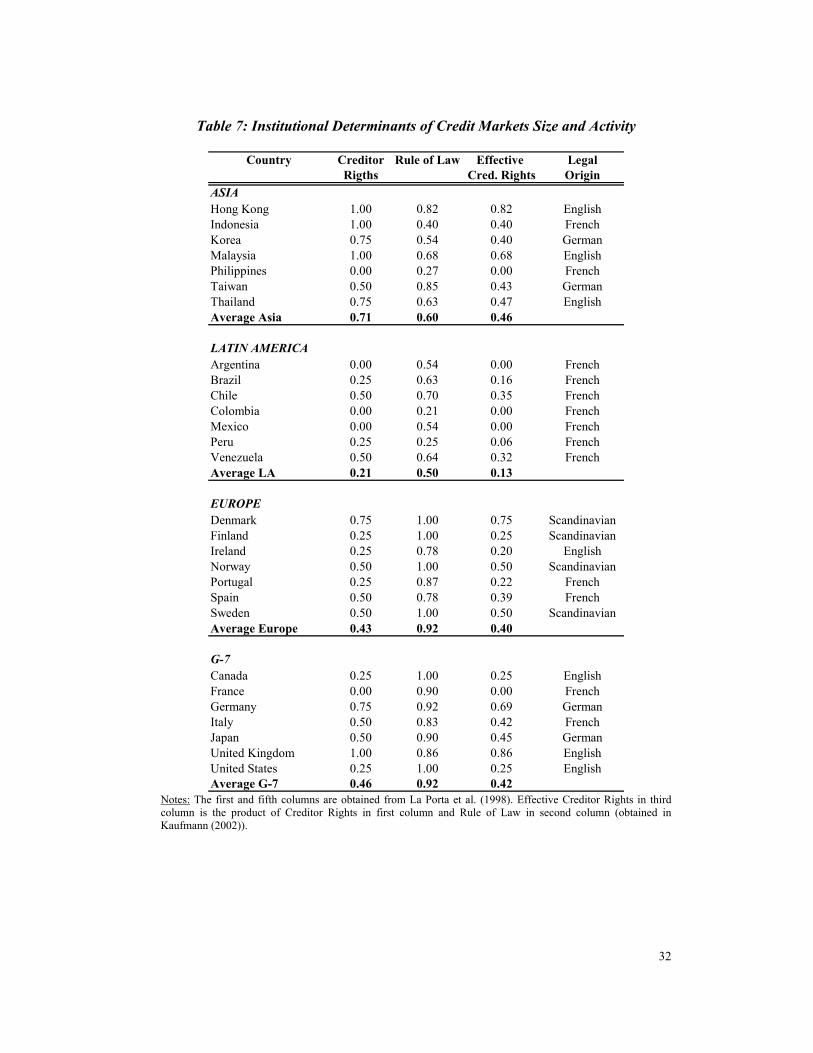

Our measure of financial development is Credit to Private Sector and Market

Capitalization of listed firms (both in percent of GDP). Both variables come from

World Development Indicators CD-ROM (2001). We do not consider Taiwan in the

analysis of financial development because data on this country is not present in the

World Bank database. These measures are reported in Table 1.

Measures of institutional development such as Creditor Rights, Rule of Law,

Risk of Expropriation and Legal Origin were obtained from La Porta et al. (1998)

and Kaufmann et al. (2002). These measures are between 0 (complete lack of those

properties) and 1 (total presence). We present these indicators in Table 7.

32

Table 7: Institutional Determinants of Credit Markets Size and Activity

Country Creditor Rule of Law Effective LegalRigths Cred. Rights Origin

ASIAHong Kong 1.00 0.82 0.82 EnglishIndonesia 1.00 0.40 0.40 FrenchKorea 0.75 0.54 0.40 GermanMalaysia 1.00 0.68 0.68 EnglishPhilippines 0.00 0.27 0.00 FrenchTaiwan 0.50 0.85 0.43 GermanThailand 0.75 0.63 0.47 EnglishAverage Asia 0.71 0.60 0.46

LATIN AMERICAArgentina 0.00 0.54 0.00 FrenchBrazil 0.25 0.63 0.16 FrenchChile 0.50 0.70 0.35 FrenchColombia 0.00 0.21 0.00 FrenchMexico 0.00 0.54 0.00 FrenchPeru 0.25 0.25 0.06 FrenchVenezuela 0.50 0.64 0.32 FrenchAverage LA 0.21 0.50 0.13

EUROPEDenmark 0.75 1.00 0.75 ScandinavianFinland 0.25 1.00 0.25 ScandinavianIreland 0.25 0.78 0.20 EnglishNorway 0.50 1.00 0.50 ScandinavianPortugal 0.25 0.87 0.22 FrenchSpain 0.50 0.78 0.39 FrenchSweden 0.50 1.00 0.50 ScandinavianAverage Europe 0.43 0.92 0.40

G-7Canada 0.25 1.00 0.25 EnglishFrance 0.00 0.90 0.00 FrenchGermany 0.75 0.92 0.69 GermanItaly 0.50 0.83 0.42 FrenchJapan 0.50 0.90 0.45 GermanUnited Kingdom 1.00 0.86 0.86 EnglishUnited States 0.25 1.00 0.25 EnglishAverage G-7 0.46 0.92 0.42

Notes: The first and fifth columns are obtained from La Porta et al. (1998). Effective Creditor Rights in third column is the product of Creditor Rights in first column and Rule of Law in second column (obtained in Kaufmann (2002)).

33

8. References Beck, T.; Levine, R. and N. Loayza (2000) "Finance and the Sources of Growth"

Journal of Financial Economics, 58, pp. 261-300. Bekaert, G, and C. Harvey (2000) “Foreign Speculators and Emerging Equity

markets”, Journal of Finance 55, pp. 565-614. Bekaert, G, Harvey, C and C. Lundblad. (2001) “Does Financial Liberalization Spur

Growth”, NBER Working Paper # 8245. Bertrand, M.; Duflo, E. and S. Mullainathan. (2002) “How Much Should We Trust

in Differences-in-Differences Estimates?” NBER Working Paper # 8841. Brecher, R. and C. Díaz-Alejandro. (1977) “ Tariffs, Foreign Capital and

Immiserizing Growth” Journal of International Economics 7, pp. 317-322. Brecher, R. (1983), “Second-Best Policy for International Trade and Investment”.

Journal of International Economics 14, pp. 313-320 CEPAL. Programa de analisis de dinamica industrial. (2000) - CD-ROM Claessens, S.; Demirguc-Kunt, A. and H. Huizinga. (2001). “How Does Foreign

Entry Affect Domestic Banking Markets?” Journal of Banking and Finance. 25, pp. 891-911.

De Gregorio, J. and P. Guidotti. (1993). “Financial Development and Economic Growth”. Washington DC. International Monetary Fund, July.

Demirguc-Kunt, A. and E. Detriagiache. (1998) "Financial Liberalization and Financial Fragility". World Bank Working Paper.

Díaz-Alejandro, C. (1985) “Good-Bye Financial Repression, Hello Financial Crash” Journal of Development Economics, 19 (1-2, September-October); pp. 1-24

Doidge, C.; Karolyi, A. and R. Stulz. (2001). “Why are Foreign Firms Listed in the US Worth More”. Ohio State University. Photocopy.

Eichengreen, B and A. Rose. (1999) “Contagious Currency Crises: Channels of Conveyance” in Takatoshi Ito and Anne Krueger (eds), Changes in Exchange Rates in Rapidly Developing Economies, Chicago: University of Chicago Press; pp. 29-56.

Eichengreen, B. (2001) “Capital Account Liberalization: What Do the Cross Country Studies Tell Us”. University of California, Berkeley, Photocopy.

Fry, M. (1978). “Money and Capital or Financial Deepening in Economic Development?” Journal of Money, Credit and Banking, 10 (4, November), pp. 464-475.

Fry, M. (1995). Money, Interest and banking in Economic Development. The Johns Hopkins University Press. Second Edition.

Galindo, A., F. Schiantarelli and A. Weiss. (2001) "Does Financial Liberalization Improve the Allocation of Investment? Micro Evidence from Developing Countries" Mimeo. IDB.

Galindo, A. and A. Micco. (2002) “ Legal Protection and Credit Cycles: Theory and Evidence”. IDB Working Paper # 443.

Ghani, E. (1992). “How Financial Markets Affect Long-Run Growth: A Cross-Country Study” Washington DC: World Bank, Country Operations, PR Working Paper WPS 843, January.

34

Gilchrist, S. and C. Himmelberg. (1998). Investment, Fundamentals and Finance. NBER Macroeconomics Annual, MIT Press.

Goldsmith, R. (1969). “Financial Structure and Development”. New Haven, CN, Yale University Press.

Henry, P. (2000a). “Stock Market Liberalization, Economic Reform and Emerging Markets Equity Prices”. Journal of Finance, 55, pp. 529-564.

Henry, P. (2000b). “Do Market Liberalization Cause Investment Booms”. Journal of Financial Economics.

Hubbard, G. (1997). “Capital Market imperfections and investment”, Journal of Economic Literature 36 (3), pp. 193-225.

International Monetary Fund. International Financial Statistics (2002). CD-ROM. Kaminsky, G. and S. Schmukler (2001). "On Booms and Crashes: Financial

Liberalization and Stock Market Cycles". World Bank Working Paper. King, R. and R. Levine. (1993). “Finance and Growth: Schumpeter Might Be Right”

Quaterly Journal of Economics, 108(3, August); pp. 717-737. Klenow, P. and A. Rodriguez-Clare. (1997). “Economic Growth: A Review Essay”,

Journal of Monetary Economics 40, pp. 597-617. La Porta, R.; Lopez-de-Silanes, F. and R. Vishny. (1997) “Legal Determinants of

External Finance”. Journal of Finance 52(3): pp. 1131-1150. La Porta, R.; Lopez-de-Silanes, F. and R. Vishny. (1998). “Law and Finance”.

Journal of Political Economy 106(6), pp. 1113-1155. Laeven, L. (2000), “Does Financial Liberalization Reduce Financial Constraints?”,

World Bank Working Paper. Lanyi, A. and R. Saracoglu (1983). “The importance of Interest Rates in Developing

Economies”. Finance and Development, 20(2), pp. 20-23. Levine, R; Loayza, N and T. Beck. (1999). “Financial Intermediation and Growth:

Causalty and Causes”. World Bank Working Papers # 2059. Lora, E. (2001). “Structural Reforms in Latin America: What has Been Reformed

and How to Measure It”. IDB Working Paper # 466. McKinnon, R (1973) Money and capital in Economic Development. Washington,

DC: Brookings Institution. Moel, A. (2001). “On American Depositary Receipts and Emerging Markets”.

Economía 2(1), pp. 209-273. OECD STAN Database for Industrial Analysis. (1999). Rajan, R. and L.Zingales (1998) "Financial Dependence and Growth". American

Economic Review. 88(3), pp. 559-586. Rodrick, D. (1998) “Who Needs Capital-Account Convertibility?” in Peter Kenen

(ed). Should the IMF Pursue Capital Account Convertibility? Essays in International Finance # 207. Princeton: Princeton University Press.

Roubini, N and X. Sala i Martin. (1991). “Financial Development, the Trade Regime and Economic Growth”. NBER Working Paper # 3876.

Sarkissian, S. and M. Schill (2001). “The Overseas Listing Decisions: New Evidence of Proximity Preference”. Photocopy.

Shaw, E. (1973) Financial Deepening in Economic Development. New York: Oxford University Press.

Stiglitz, J. (1994), “The Role of the State in Financial Markets” In Proceedings of the World Bank Annual Bank Conference on Development Economics 1993.

35

Edited by Michael Bruno and Boris Pleskovic, Washington DC, World bank, pp. 19-52.

Stiglitz, J. (2000), “Capital Market Liberalization, Economic Growth and Instability”, World Development 28, pp. 1075-1086.

Stulz, R. (1999). “Globalization of Equity Markets and the Cost of Capital”. NBER Working Paper # 7021.

UNIDO (United Nations). Industrial Statistics Database (2000) – CD-ROM World Bank (1989) World Development Report 1989. New York. Oxford University

Press for the World Bank. World Bank. World Development Indicators (2001) – CD-ROM