Embed Size (px)

Citation preview

Financial Management

March 2008

City District Government Faisalabad, Pakistan

S.M. Khatib AlamImran Yousafzai

From Deficit to Surplus

for Good Governance

3R

s. M

illio

ns

-150

-100

-50

0

50

100

150

FY 2004-05 FY 2005-06 FY 2006-07 FY 2007-08 Projected FY 2008-09 Projected FY 2009-10 Projected

This document is produced as part of the Strengthening Decentralised Local Government in Faisalabad (SDLGF) Project for the purpose of disseminating lessons learnt from the project. The views are not necessarily those of DFID or the City District Government Faisalabad

(c) SDLGF March 2008

Parts of this case study may be reproduced for educational use, provided that such material is not printed and sold. The authors expect that, any material which is used will be acknowledged accordingly.

Layout & Designed at:

FaizBakht Printers, The Mall, Jhang (Punjab) Pakistan.

VISION

“Pre-empting Poverty, Promoting Prosperity”

MISSION STATEMENT

“We will provide high quality services which compare with the best in the country. We will work with everyone who wants a better future for our District. We will establish an efficient, effective and accountable District Local Government, which is committed to respecting and upholding women, men and children’s basic human rights, responsive towards people’s needs, committed to poverty reduction and capable of meeting the challenges of the 21st Century. Our actions will be driven by the concerns of local people”

ACKNOWLEDGMENTS

This case study is the culmination of efforts by a number of individuals from government and

the technical assistance team. Firstly it is important to thank all those who have cooperated

with the team preparing this case study not only in the last few weeks but over the course of

the last four years. They have been critical to the work and demonstrated what is possible to

achieve in government when the right set of conditions prevail.

We would also like to thank the communities and elected representatives of the district that

assisted the SPU team in implementing this project and its various components.

The authors wish to thank Rana Zahid Tauseef, City District Nazim; Maj (Retd.) Azam

Suleman Khan, District Coordination Officer; and Dr. Tariq Sardar, EDO Finance & Planning

for their valuable contribution in making this project a huge success.

We are also thankful to: Mr. Ch. Zahid Nazir, ex-District Nazim Faisalabad; Mr. Tahir Hussain,

ex-DCO Faisalabad and Mr. Athar Hussain Khan Sial, ex-DCO Faisalabad for their valuable

contribution to the success of this project. We are also thankful to: Mr. Asad Islam Mahani, ex-

EDO Finance & Planning Faisalabad and Mr. Waseem Ajmal Chaudhry, ex-EDO Finance &

Planning, Faisalabad for their valuable contribution to the success of this project.

We are further thankful to all CDGF employees (past and present) and CDGF partner

departments but we would like to specifically mention by name the following: Mr. Muhammad

Akhtar, District Accounts Officer; Mrs. Saima Raza, District Officer (DO) Finance and Budget;

Mr. Muhammad Ramzan, DO Planning; Mr. Dilmir Khan, DO Accounts; Mr. Amir Tareen, DO

Revenue; Mr. Mehmood Wazir, DDO Revenue; Mrs. Talat Qamar DDO Accounts; Mr.

Ghulam Rasool Bhawana DDO Planning and Mr. Rana Saif, Assistant Finance & Budget for

their efforts in successfully implementing reforms in their departments.

We are thankful to all DFID Project Advisers and Management that have assisted in this

project since its start and we would like to specifically thank Mr. Mosharraf Zaidi, Governance

Advisor, DFID Pakistan; Mr. Wajahat Anwar, Deputy Programme Manager, Accountability

and Empowerment team, DFID Pakistan; Ms. Jackie Charlton, DFID; Mr. Alistar Moir, DFID

Pakistan and Ms. Nighat-un-Nisa, DFID Pakistan for their continuous support and

professional technical guidance since their involvement in 2004.

Our thanks are also to Dr. James Arthur, Dr. Richard Slater and Ms. Janet Gardener for their

valuable inputs throughout the project. We would also like to thank Mr. David Gray,

Governance Advisor DFID; Mr Roy Brockman; Ms. Joji Reyes and Ms. EJ Nacpil for their

valuable contribution in completing the case study.

We are thankful to Mehreen Hosain for proof reading the document and all the SPU team

members for their dedication, hard work and the many late hours spent designing,

implementing and documenting the work of this project. These include: Nadir Ehsan,

Mahmood Akhtar, Muhammad Shahid Alvi, Muhammad Tariq, Kashif Abbas, Ajaz Durrani,

Farhan Yousaf, Muntazir Mehdi, Gul Hafeez Khokhar, Mirza Muhammad Ramzan,

Muhammad Sharif,Humaira Khan, Sumara Khan, Saima Sharif, Mubarak Ali, Adnan Akram,

Sohail Anjum, Saleem Shehzad, SamiUllah, Arooj Sultana , Mamoona Mustafa and all long

and short-term international and national consultants.

FOREWORD

The City District Government Faisalabad (CDGF) is

changing. After a period of introspective assessment we

believe that we are now moving towards becoming a more

responsive, effective and efficient Local Government

through reforms that we initiated in May 2004.

It is with great pleasure that I say we have now additional

resources which three years ago seemed difficult. Our

budget for the forthcoming year will have money that we plan

to allocate based on those whose needs are greatest in

Faisalabad. We are currently in a very good state of affairs at

all levels. Our finances are considerably better then 3 years

ago, and with a surplus budget. We now have fiscal space to

allocate resources in those sectors that we deem critical to

fighting poverty in Faisalabad especially in Education,

Health and Community Development sectors.Our budgeting

process in this quarter has been the most participatory ever,

and we believe we are a leading district in undertaking

widespread consultations which have fed into the budget.

We will be further broadening the participation process.

The availability of credible and timely information is now

helping the Finance & Planning department to correctly

inform Local Government so that discussion can be made in

a rational manner. Our information systems allow us to

present accurate information to senior management during

our monthly meetings. This information enables top

management to prioritise its needs and identify areas that

need targeted investment. The challenge ahead is clear,

how to translate this progress into good financial

management? While the CDGF continue to rely upon

provincial support, there is much that can be done at home to

offset fiscal instability.

I would like to take the opportunity to thank our City District

Nazim for his valuable support to the reforms in our district. I

would also like to congratulate my City District team

members especially all the EDOs for working to achieve the

objectives in their departmental reforms programme. Finally,

I would like to thank our major partners in development, the

Department for International Development (DFID) UK and

their management consultants GHK International Ltd., for

assisting Faisalabad City District through the project

“Strengthening Decentralized Local Government in

Faisalabad”.

Maj. (Rtd.) Azam Suleman KhanDistrict Co-ordination Officer

City District Government Faisalabad

March 2008

The Clock Tower, symbol of Faisalabad

Office of the District Co-ordination Officer, Faisalabad

PREFACE

Starting from a base where there was very limited strategic human resource management,

little or no validated data for making informed decisions, poor levels of fiscal management,

limited technical capacity within our team and an almost non-existent policy for both gender

and communication, we have made, in this very short period of time, good steady progress.

These strategic aims form the basis of improving how we govern ourselves but also

supporting a paradigm shift that leads us to becoming a more citizen friendly District

Government. The F&P department has been hard at work in improving systems, processes

and procedures that will aid to improve services in the social sectors, such as education,

health and community development.

We continue to focus on fiscal transparency and therefore, we have been liaising with as

many stakeholders as possible, about the way we allocate and spend money. We have been

involving our politicians to make financial decisions. Hence our efforts to educate and train

our politicians in core areas such as gender, finance, governance and expenditure

management are leading to more accurate budgeting and planning. Cash flow has improved

because of the strong financial management in CDGF. The District prepared a realistic

budget in 2007-2008 and based on our cash flow position the Finance department is

confident that in the next financial year providing there are no adverse provincial decisions

taken, the CDGF is likely to have more fiscal space for development projects.

Planning remains at the heart of good financial management. We have therefore continued to

focus on building multi-year planning capacity within the Department. Cost benefit analysis of

Financial Management Information System reveals that it has brought savings of more than

Rs.10 Million per annum. The City District administration feels it more appropriate to focus on

maximizing existing revenue sources rather than trying to identify new revenue sources.

Revenues from advertisement and commercialization remain potentially the most attractive.

They constitute 68 percent of total district receipts and the department plans to improve

revenue collection from these sources.

The road ahead will present many challenges, not least convincing sceptics that these

reforms are not only important but a necessity. Other districts in Punjab and the country will be

looking to Faisalabad to see how we develop and whether Local Governments can indeed

deliver a level of service that people deserve. The onus is on all of us to work together for a

brighter future - we owe it to all the citizens of Faisalabad.

Dr. Tariq Sardar Additional Project Director

Strengthening Decentralised Local Government in Faisalabad

March 2008

TABLE OF CONTENTS

ACKNOWLEDGMENTS

FOREWORDPREFACE

ACRONYMS

EXECUTIVE SUMMARY

BACKGROUND

OVERVIEW

THE CASE

IMPLEMENTATION AND IMPACTS

DRIVERS OF CHANGE

LESSONS & REFLECTIONS

1

4

5

7

8

Design 8

Continuing to Build Local Capacity 8

Improvement in Financial Management 9

Making the Budgeting Process Work 12

Improvement in the Release of Grants 19

Expenditure Tracking System 20

Facilitating the Reconciliation of Financial Accounts 21

Facilitating the Pensioners in CDGF 22

Asset Management 23

Information Systems 23

Increase in Revenue Mobilisations & Fiscal Efforts 25

Influence on Corporate Policy towards Reduction of Poverty 29

Strengthening the Internal Accountability Mechanisms 31

33

Provincial Government and Legal Protection 33

Leadership 33

Location, Administrative Setup and Ownership 33

Link with Non-devolved Departments and Other Donors 34

Timely Technical and Financial Support 34

Innovative System and Processes 34

35

Policy Change 35

Awareness 35

Replication 35

The Role of Survey 36

Consultation with Elected Representative 36

Availability of Technical Team 36

Financial Incentives 36

Understanding of Government Culture and Related Legislation 37

Table of Contents

Decentralisation of Revenue 37

Lack of Funds in not the Real Issue in the District 37

38

Spatial Planning Farmework 38

E-Procurement 38

PIFRA Access 38

Receipt Facilitation Centers 39

Sustainability 39

40

46

Figure 1: Improved Financial Management 10

Figure 2: Online Budgeting Process 16

Figure 3: Simplified Reconciliation system of CDGF 21

Figure 4: Financial Management Information System 24

Figure 5: Flow of Funds in the CDGF Account IV 26

Figure 6: Trends of Local Receipt from FY 2002-03 to FY 2007-08 28

Annex 1: A Case Study on Situation Analysis of CDGF’s Budget 2004-05 42

Annex 2: Comparison of PESRP Funding from 2004 to 2008 43

Annex 3: Receipt Facilitation Model 45

WAY FORWARD

CONCLUSIONS

BIBLIOGRAPHY

FIGURES

ANNEX

Figure 7: Education Department’s Development Expenditure trend from FY 2002-03

to FY 2007-08 (upto November 2007) 31

Table of Contents

ACRONYMS

AA Administrative Approval

ADP Annual Development Programme

AMC Asset Management Cell

BCL Budget Call Letter

BM Budget Management

BSF Budget Salient Features

CCBs Citizen Community Boards

CDGF City District Government Faisalabad

COs Collecting Officers

DAO District Account Office

DCC District Coordination Council

DCO District Coordination Officer

DDC District Development Committee

DDOs Deputy District Officers / Drawing and Disbursing Officers

DFI District Financial Information

DFID Department for International Development

DMS Document Management System

DO F&B District Officer Finance and Budget

DOA District Officer Accounts

DOP District Officer Planning

DOs District Officers

EDO Executive District Officer

EMIS Education Management Information System

F&P Finance and Planning

FMIS Financial Management Information System

FY Fiscal Year

GIS Geographical Information System

HRMIS Human Resource Management Information System

M&R Maintenance and Repair

MDG Millennium Development Goal

MTBF Mid-Term Budgetary Framework

NAM New Accounting Model

NBP National Bank of Pakistan

NFC National Finance Commission

PC1 Planning Commission Performa 1

PCF Provincial Consolidated Fund

PESRP Punjab Education Sector Reforms Programme

PFC Provincial Finance Commission

PIFRA Project to Improve Financial Reporting and Auditing

PLGO Punjab Local Government Ordinance

PMIU Project Management Implementation Unit

PPRSP Punjab Poverty Reduction Strategy Paper

RFC Receipt Facilitation Centre

RMIS Revenue Management Information System

SDP Strategic Development Plan

TMA Town Municipal Administration

UCs Union Councils

ZAC Zila Account Committee

Acronyms

EXECUTIVE SUMMARY

The experience of the Strategic Policy Unit (SPU) of the City District Government Faisalabad

(CDGF) demonstrates how changes in financial management practices have fuelled the

District's transformation from being a Local Government in constant fiscal crisis to being a

Local Government that can take pride in its fiscal surplus. This situation has allowed the

District Government to provide more efficient service delivery and enabled it to take vital

steps toward targeting poverty.

The last three years of the reforms programme have been a watershed for Local Government

in Faisalabad. There has been a tremendous change in the District. Who could have

envisaged three years ago that the District Government would be wholly committed to ridding

the District of deprivation and replacing earlier ad hoc and reactive policies with a firm and

sustained commitment to development and modernization? The CDGF is now saving more

time, money, and human resources, with the benefits of efficiencies being transferred to its

citizens.

On the whole the financial management reforms component has been well accepted both by

the CDGF and Provincial Government, especially, since service delivery to client

departments has improved considerably as a result of the change issues identified and then

implemented by CDGF.

The following are a brief summary of the initiatives implemented:

� The District’s first major intervention to reform the financial management process,

was to conduct a capacity development programme for financial officers, Drawing

and Disbursement Officers (DDOs), clerks and accountants to prepare the budget in

accordance with the new rules and regulations;

� Analysis of the cash flow has helped to present a macro level picture of Local

Government finances enabling management to rectify micro level issues. The

Finance and Planning Department (F&P) has been able to inform politicians of the

need to exercise fiscal discipline and to avoid new development investment as a

prelude to zero based budgeting;

� Analysis of the budget preparation process in 2005 exposed the District's ability to

manage its financial resources in a responsible manner. Close scrutiny of the process

and the way the budget had been implemented since 2003 shed light on the extent of

the financial problems facing the administration. This analysis was necessary to

inform financial managers and top administration about the current financial status of

the District and how best to use the resources available;

� The budgeting process of Faisalabad used to be cumbersome and labour-intensive.

In the last three years, the departments took huge strides in improving the traditional

budgeting process. Much of this is due to better coordination, better training provided

to the officers involved in the process and ongoing technical support from the CDGF

reform initiatives;

� Prior to the reforms process, the required data for targeting the poor was not available.

The identification of development schemes was undertaken on a highly politicised

basis with little regard for prioritising a pro-poor agenda. Elected representatives

were not conscious of poverty targeting while the majority of the Executive District

Executive Summary

“Devolution is not apposed because of capacity constraints, shortage of technical manpower, the quality of awareness of local elected leaders or any such thing. It is apposed simply because it created such a huge disruption in the political economy of corruption.”

Long Serving DMG Officer

1

Officers (EDOs) were not fully aware of the concept of poverty reduction. A key aspect

of the financial reforms process was to achieve more efficiency gains in resource

allocation to support the Punjab Poverty Reduction Strategy Paper (PPRSP);

� The procurement process of CDGF was often constrained by the outdated Delegation

of Financial Power Rules, which were issued by the Provincial Government in 1990 to

delegate and authorize approvals at various levels for the purchase of differing goods

and services from suppliers and contractors. The CDGF raised its concerns to the

Provincial Government by suggesting the changes in the rules to make the

procurement more effective. The Provincial Finance Department in year 2006 revised

the Delegation of Financial Powers Rules which helped in the improvement of

procurement of goods and services in the District;

� It has been difficult for departments to track monthly development and non-

development expenditure. The main reason has been the systems in place in the

departments were aligned to the District Accounts Office (DAO). The departments

were only preparing budgets at the departmental level while incurred expenditure

was recorded at DAO. The F&P department was thus unable to monitor expenditure

against the budget. The F&P department is now able to develop reports giving

individual line item expenditures and other components such as the Punjab

Education Sector Reform Programme (PESRP), National Programme for the

Improvement of Watercourses (NPIW), Chief Minister's Accelerated Programme,

and significantly CCB projects are now also classified;

� Reconciliation of accounts in an accurate and timely manner is critical to fiscal

discipline. Rule 67 (3) of the Budget rules 2003 clearly states that it is the joint

responsibility of all key officers to submit accurately reconciled accounts to the District

Government. The appropriation of annual account is prepared by the DAO and that

did not give the true picture of expenditure detailed object wise but only informed

about the grant wise expenditure in the District. Therefore, the CDGF for the first time

made an attempt to reconcile the June 2007 annual accounts DDO wise, grant wise

and detailed object wise with the District Account Office;

� Good strategic management relies on an organization's ability to manage its

information properly. It is only now, that the District has started to understand the

implications of having reliable information as the basis for its business decisions. For

a district as large as Faisalabad, having the right information at the right time will allow

managers to redefine Local Government services and allocate resources

accordingly;

� Revenue generation in local receipts has been constantly improving since 2002-03.

In 2007-08 the District has made considerable progress in revenue collection. Up to

November 2007, the District has collected 92 percent more revenue than the previous

financial year. This upward trend in CDGF's local receipts, combined with more

successful efforts to increase the District Government's PFC award, strongly bolsters

Faisalabad's fiscal position for the future. Faisalabad's financial reforms process has

undoubtedly brought tangible fiscal rewards to the District Government. The financial

plans and reports are being prepared on time and with fewer errors;

� Financial accounts are being reconciled allowing local policymakers to make

informed judgements and policies. Facilities for an on-line budgeting system are in

place. Financial planning and equitable resource allocation have been linked.

Commercial properties have been identified and properly valued enabling the District

Government to generate increased local revenues. The procurement process is

Executive Summary

2

being streamlined. Workshops and trainings are ongoing to continue to build a skilled,

knowledgeable, and well-motivated local work force. The Financial Management

Information System (FMIS) is at the core of the fiscal transformation.

The Finance & Planning department of CDGF through the technical assistance provided by

the reforms programme brought significant changes in the financial management practices of

the District. The Department analysed the reasons for fiscal deficit and undertook major steps

to bring improvement and efficiencies in the departmental business processes like budgeting,

expenditure tracking and release of funds etc. These efficiencies together with both the

Provincial directives and local policy changes have contributed towards the District moving

from a deficit situation to a surplus.

Keeping in view this upturn, CDGF remains optimistic that continuing with the financial

management disciplines will allow the District in the future to remain in surplus.

The fiscal space allowed the City District Government to target poverty, using evidence

based planning which built on data and information being generated at all levels. An example

of this is the District Citizen Perception Survey, which influenced the allocations in the

education and health sectors.

This wide acceptance of reforms in Faisalabad is intriguing. After all, similar or less intense

attempts to reforms in Pakistan particularly in the Punjab have been slow in producing results.

How is it then possible that reforms in Faisalabad could proceed, and were widely accepted

since 2004? Had the CDGF identified the major gaps regarding the employees’ existing

capacity and made them effective to plan an implement the proposed changes in Faisalabad’

financial management practices? Was the online budgeting systems instrumental in making

the CDGF budgeting process more efficient? How did the CDGF manage to monitor and track

the expenditure against the approved allocation and established strict financial discipline in

the district? Had the reform initiatives helped the CDGF in identifying the true potential of local

revenue? Had the CDGF improved the planning systems by developing tools to influence the

corporate policy towards targeting poverty? Had the reform initiatives changed the working

culture of the CDGF employees regarding knowledge sharing, team working, transparency

and mutual understanding?

These are just some of the issues addressed in the case study.

Executive Summary

3

BACKGROUND

The Strategic Policy Unit (SPU) was set up by the Faisalabad District Government in 2002, as

a policy think-tank. Its key aim was to act as a conduit in the district from which all reforms

programmes could be initiated. In 2004, the United Kingdom's Department for International

Development (DFID) agreed to provide technical assistance to the district through the

“Strengthening Decentralized Local Government in Faisalabad” and using the SPU as the

platform from which change would be driven.

The SPU over a four year period has acted as a key resource fostering social capital within the

City District Government and often being the focal point for local and international technical

assistance and programme development. With a cohort of key technical resources and

change management agenda it plays a key role in facilitating public sector reforms. It has

been instrumental in assisting Faisalabad to become a modern administration.

Pakistan's devolution in 2001 ushered a series of bold structural changes which created a

new tier of Local Governments comprising District Government, Town Municipal

Administration (TMA), and Union Administration. The objectives of the devolution, easily

discernible from various Government publications and ordinances, include improving the

Districts' financial management practices. Underpinning these objectives is the promise to

improve service delivery, particularly social services, and ultimately, the potential to reduce

poverty in the country.

The Government of Pakistan through devolution introduced a new system of Local

Government. But Local Governments are not a constitutional tier of Government, and are

established and assigned functional responsibilities through provincial legislatures, primarily

under the Punjab Local Government Ordinance (PLGO). District Governments have the

responsibility for delivering social and economic services, including elementary and

secondary education, primary and secondary health, agriculture and municipal services.

To make devolution function effective, the management of district and other local authorities

needed to be strengthened. Pakistan had only limited experience of Local Government and

did not have the systems, trained staff or the means of improving governance.

The process of devolution was undertaken quickly and many new initiatives were built into the

legislature, some powers of the Provincial Governments were decentralized to the District

level, but supporting processes and rules were not thought through sufficiently. For example,

there was a lack of in-house treasury arrangements at the District level, where a District

Accounts Officer (DAO) controls the accounting function making the Finance & Planning

(F&P) department dependent on it.

Background

4

Box 1: Financial Management Functions in the City District Governments

In the City Districts the Key Financial Management functions are undertaken by four departments:

� Finance and Planning department is responsible for budgeting, expenditure management, cash

management, reconciliation, pension, audit, development planning, enterprise and investment promotion;

� The Revenue department assesses and collects local receipts, for example, building rent, license fee, local

rates;

� The Municipal Services department assesses and collects the revenue from advertisement,

commercialization and bus stations;

� The District Accounts Office which is a non-devolved department performs the functions of treasury in the

District.

OVERVIEW

To meet the challenges of devolution in 2001, the City District Government Faisalabad

established a Strategic Policy Unit (SPU), to drive the process of reforms. The District

Government Faisalabad obtained the assistance of the Department for International

Development (DFID) in providing technical assistance to develop and improve systems and

processes. As a first step, the City District Government Faisalabad prepared five year

evidence based Departmental Strategic Operational Plans (SOPs) in 2004 in line with the

District Government's Corporate Governance Plan (2004-2009).

The Finance & Planning (F&P) and Revenue departments had undertaken a very detailed

situation analysis of the departmental activities. The situation analysis critically highlighted

the management, organizational, financial and capacity constraints of the departments. The

key strategic issues that needed to be addressed were identified:

� Financial management systems did not allow the F&P department to analyse the

District cash flow, issue an effective Budget Call Letter (BCL), track and monitor

expenditures & receipts or provide timely release of grants to the departments;

� Users were not able to have access to financial information nor did financial reporting

mechanisms exist to assist in decision making. A key issue was the need to establish

an effective Financial Management Information System (FMIS);

� Bottom-up-planning was non-existent, and most development funds were used by

councillors for local and ad hoc schemes and not for strategic district level

improvements. The City District Government was unable to plan for its capital

investment, a need essential to balance budgets and allowing the proper allocation of

money toward district functions was identified;

� Since 2001 up-to 2004, the Provincial Finance Commission (PFC) development

award was static and the increased amount from the National Finance Commission

Overview

5

Retained Account

The money in the Retained account is retained by the Provincial Government and is not distributed to the districts as part of the PFC award. This is mainly used for the Provincial Governments functions and the Provincial Government may provide funds to the districts for various projects in the form of conditional grants.

Manual budgeting system in 2004

(NFC) went into the retained account only. Local receipts were low until 2006 when

the District Government was upgraded into a City District Government where

additional revenue sources such as advertisement, commercialization and General

Bus Stands fee came under the CDGF control. But there was no fare-based record of

revenue sources available. So yearly targets set by the departments for the local

revenue sources were unrealistic;

� The Revenue department is the primary custodian of District Government assets. But

the department did not have any record of properties for which the department could

be held accountable for managing and maintaining the CDGF assets. Besides there

was no culture of asset management in the District;

� The capacity and resources of the F&P department were not adequate or fit for

purpose for the delivery of quality public services;

� The process of reconciliation of accounts needed improvement to enable

expenditure and receipts realized in line departments to be reconciled with the

District Accounts Office (DAO) and to publish financial reports of the District Officer

Accounts (DOA) on a monthly basis to be submitted to the Council for approval;

� The utilisation of development funds was less than 70 percent, which can be traced to

the ineffective and inefficient budgeting process;

� System deficiencies and lack of availability of financial data prevented top

management in determining investment priorities, leading to poor investments,

which were not effective in reducing poverty. Political will and ownership by the

District administration were needed in evaluating plans to ensure that health and

education programmes were allocated to the areas of greatest need;

� Procurement of goods and services was inefficient in the District. Outdated rules, lack

of trust of suppliers, poor Government procedures and instructions, late fund

releases and the lack of effective financial control systems were the key problems.

Overview

6

Weekly brainstorming session of F&P department to identify key issues

DO finance & budget Mrs. Saima Raza introducing FMIS to finance & planning department

THE CASE

This case study describes how the District undertook the financial reforms which are

essential to improve service delivery in critical sectors i.e. education, health, agriculture and

municipal services generally. It addresses a number of questions including the following:

What were the factors that allowed the District to become more fiscally responsible? How was

fiscal space created in becoming more transparent, accountable and efficient? How did the

FMIS help the City District Government Faisalabad in decision making? Why was it important

to improve the budgeting, reconciliation, releases and expenditure tracking systems in the

City District Government Faisalabad? Were the Provincial Government, local administration

and politicians supportive of the reforms process? How committed has the CDGF been in

their goals of investing and getting value for money on the education and health sectors?

Specifically, this case study focuses on the following areas:

a) Can one achieve efficiency by strengthening the capacity within the District

Government for effective planning and budgeting process?

b) How can improvements in the Financial Management systems help in bringing more

transparency and accountability?

c) How does the increase in revenue mobilization and fiscal efforts create more fiscal

space?

d) Did the City District Government influence the corporate policy towards reduction of

poverty?

e) Can one change departmental culture and behaviours by strengthening internal

accountability mechanisms to ensure professional integrity and financial propriety?

7

The Case

IMPLEMENTATION AND IMPACTS

Design

Continuing to Build Local Capacity

Faisalabad was committed to reforms and change and had set itself a series of challenges

that if met would result in marked improvements in local governance and public services. The

first major step was to establish a good governance framework, which underpinned the

reforms process and injected life into public services.

During the inception phase of the reforms initiatives (from May-November-04) the district

corporate plan was prepared. The Faisalabad's 'Corporate Plan' provided the overarching

policy framework for service planning and delivery. The corporate plan laid out the Mission

statement, and core values of the District. The District Corporate Plan provided a clear

indication of where Faisalabad as a District Government wants to be and the principles by

which the District want to get there.

To achieve the corporate objectives, Departmental Strategic Operational Plans (SPOs) were

prepared. The Corporate Plan and all the Departmental SOPs have not been prepared in

isolation, but have been informed in a number of ways including: seeking views from a

number of key stakeholders which included the Government, elected members, civil society

groups and monitoring committees.

The detailed situation analysis was conducted of the Finance & Planning and Revenue

departments. During the situation analysis, key change issues were identified and to address

those issues five years implementation plans were prepared highlighting the strategy,

objectives, activities, performance indicators, means of verification, time span and where

applicable, costs. These were discussed in the Zila council (district assembly) and approved

in December 2004.

Issue

The lack of service planning in the City District Government was a major cause for concern.

Poor departmental performance can often be attributed to a number of factors i.e.

interdepartmental relationships, weak reporting & management structures and a lack of

resources. However one of the most important areas is the lack of knowledge and skills

possessed by personnel on multi-year service planning and development, leaving

departments unable to plan and deliver professional services. Despite these skill gaps, the

District was still expected to deliver quality services.

Process

Realising this major gap, the F&P department organised training workshops for senior

officers, Drawing and Disbursing Officers (DDOs), Accountants / bill clerks of the City District

Government and other implementing and executing agencies.

Implementation and Impacts

8

As part of the CDGF’s internal monitoring process to determine how the District is performing with respect to what is mentioned in the corporate and departmental operational plans? Faisalabad under the reforms initiatives developed the bi-annual performance reports, which presented detailed assessments for consideration by the district assembly and other stakeholders. This has allowed the CDGF to be held accountable and transparent, as well as informed all the relevant stakeholders of the issues that Faisalabad faced during the last 3 years of implementation.

DDOs training on budget & planning

Local capacity was weak, and needed to be boosted to effectively plan and implement all the

proposed changes in Faisalabad's financial management practices. Much of the success of

the reforms process was hinged on the ability of concerned staff to use the FMIS. Resource

Centres, established in the departments have provided on-line budgeting, reconciliation, and

expenditure tracking facilities for all DDOs. Training sessions were planned to cover various

modules of the FMIS.

Encouraging broad-based citizen support of the City District Government's plans and

programmes entails more participation. A trilingual approach such as English, Urdu, and

Punjabi has been used to train stakeholder groups to facilitate understanding of the basic

concepts of translating plans into financial budgets. Different workshops have been

conducted involving District Council Members to discuss the benefits of locally-evolved

planning and to help them to understand their roles in the preparation, approval and

implementation of the budget.

Impacts

A series of training workshops for the top, senior and middle management contributed to

district’s success by helping the CDGF to develop its human resources to meet its present

and future needs. It has also improved the employees' performance, provided them

professional development opportunities and became more efficient and effective in

managing the finances of the CDGF. Following are the benefits achieved through the reforms

process:

l 960 DDOs and their account clerks trained on budget and planning; The error rate in

budget preparation from more than 33 percent to less than 3 percent as a result of this

training;

l Capacity building of all EDOs and other operational officers on Mid-term Budgetary

Frame work (MTBF) enhanced the understanding of District & Tehsil Officers on

MTBF, service planning & project planning;

l Technical training on FMIS imparted to the F&P department gave opportunity to the

F&P staff to use and modify the systems without reverting to consultants and experts;

l Training of 413 members of the District Council on Gender Responsive Budgeting

and budget & planning has been carried out which helped to increase their

understanding level on budget & planning.

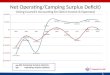

The experience of the CDGF demonstrates how politically and technically supported

changes in financial management practices can fuel a transformation from being a Local

Government in constant fiscal crisis to being a Local Government that can take pride in its

fiscal surpluses. This situation has allowed the District Government to provide more efficient

service delivery and enabled it to take the vital steps toward reducing poverty.

Improvement in Financial Management

9

Implementation and Impacts

Fiscal Space

“Fiscal space can be defined as room in a government´s budget that allows it to provide resources for a desired purpose without jeopardizing the sustainability of its financial position or the stability of the economy.”

Box 2: Identification and Training of the Master Trainers

To train over 900 government officials was a major undertaking and given the limited resources available, it was

important to decide on a delivery model that would achieve the desired outcome within a suitable time frame. The

approach that was finally adopted included the use of master trainers from various departments as key resource

persons to deliver training to the DDOs in Towns. Consultations were held with departments as part of the process

to identify master trainers and 32 master trainers were identified with the support of the other departments

especially the Education department.

Following is a description of the activities and initiatives of reforms undertaken in the F&P

department of CDGF and Figure 1 describes this process.

Issue

A fiscal assessment showed that the City District Government's weak fiscal performance can

be traced in part to the poor linkage between policy making, planning, and budgeting. A lack

of interest or may be the poor appreciation of the relevant accounting procedures and policies

seemed to be among the underlying reasons for Faisalabad's fiscal deficit in 2004. Receipts

for development and non-development expenditures were inflated and inconsistent with local

receipts. There was a gap between the City District Government's recorded bank balance

and the actual available balance.

In January 2005, close scrutiny of the CDGF's process and the way the budget had been

implemented since 2003 shed light on the extent of the financial problems facing the

administration. To this point, the City District Government had been working on the

assumption that there was more money available to the administration than actual releases.

As a result of the 2004-2005 budget analysis, the team identified that there were errors in the

budget which subsequently resulted into the deficit budget in Faisalabad.

Process

Generally, there tends to be a practice in the City District Governments that if the estimated

expenditure exceeds the estimated receipts, then for the sake of balancing the budget and

under the assumption that Provincial Government will make the loss good, an entry of grant in

aid from the Provincial Government is made on the “budget at glance sheet” of the budget

book.

The evidence suggests that due to the lack of capacity, enough care was probably not taken

and errors were made in the preparation of this important document. As an example the

situation is explained in Annex 1 where it is discussed as a short case study to learn from. The

financial situation was very tight for the CDGF and at that time of crisis, major steps were

Strengthening Fiscal Planning

Implementation and Impacts

10

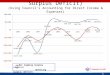

Figure 1: Improved Financial Management

Pre-empting Poverty, Promoting Prosperity

ISSUES WAY FORWARD

P A D

P A D

P A D CDGF

Sustainability

Replication

Receipts Facilitation Centers

Spatial Planning Framework

E-Procurement

REFORMS PROCESS

I proved r ic Delivery

mSe v e

Section 112 (4) (a) PLGO 2001

A budget shall not be approved if the sums required to meet estimated expenditures exceed the estimated receipts.

Pre-empting Poverty, Promoting Prosperity

ISSUES WAY FORWARD

P A D

P A D

P A D CDGF

Sustainability

Replication

Receipts Facilitation Centres

Spatial Planning Framework

E-Procurement

REFORMS PROCESS

prov d r i Del ve y

Ime Se v ce i r

taken by the administration to ensure that greater fiscal responsibility was achieved.

The City District Government's fiscal position, however, began to look up in financial year

2006-07. The following factors contributed to this upturn in fiscal fortune:

l Improved budgeting systems of the CDGF;

l Effective expenditure tracking systems;

l Timely releases of funds to the departments and executing agencies in the CDGF;

l The District started receiving more resources when in October 2005, Faisalabad was

afforded the status of City District Government which brought with it enhanced

jurisdictions and resources;

l Octroi grant of Rs. 655 million from the Provincial Government was provided to

CDGF;

l The Municipal Service department became responsible for managing resources

from advertisement, commercialization and General Bus Stands, which had a

positive impact on the fiscal surpluses of the District;

l CDGF received an increased PFC award from the Provincial Government on the

request of the City District Nazim and District Coordination Officer (DCO).

District Cash Flow analysis is a tool which helps to present a macro level picture of the Local

Government finances enabling management to rectify micro level issues. Armed with the

cash flow information, the Finance & Planning department is able to present a stronger case

on the basis of evidence, to senior and top management on the District's financial status.

Identifying and setting priorities becomes easier now in the light of information never

previously available. Cash Flow analysis is a useful tool since it allows managers to develop

numerous scenarios based on short and long-term forecasts.

Implementation and Impacts

11

Box 3: Steps Taken by the CDGF to Improve Fiscal Position

� There was no new project executed by the F&P department. District administration took very difficult decisions

on seeing the tight financial position of the District, in order to pay outstanding liabilities before taking on new

ones;

� The F&P department submitted a request to the Provincial Government that the current PFC share is not

enough to meet the development and non-development needs of the District and PFC share of the District

should be according to population and area of the District;

� A further request was made to the provincial Finance department to help City District Faisalabad by providing

funds to cover the deficit of CDGF over the coming years.

Section 111 (5) PLGO 2001

“Conditional grants from the provincial retained amount shall be shown separately in the budget and shall be governed by conditions agreed therein”.

In addition, the Finance and Planning department developed the FMIS which was compatible

with the national Project to Improve Financial Reporting and Auditing (PIFRA) and other

management information systems already in place, allowing more accurate and timely

analysis and planning.

Due to the recent changes in the political and administrative set-up at the Provincial

Government level, the finance department has changed the policy of fiscal transfers for the

District Governments. Under the current scenario, due to decrease in the PFC award, the City

District Government expects 8% decrease in the fiscal transfers from the Provincial

Government up-to June 2008. The City District Government Faisalabad by following the

Provincial Government guidelines has changed the fiscal strategy by reducing the non-

development non-salary expenditure by 13 percent and development expenditure by 10

percent Therefore, this strategy will no doubt affect the development and the service delivery

in the District but will also save Faisalabad from deficit in the coming years.

Impacts

The financial reforms process undertaken by Faisalabad has not been easy. But, it has

transformed the City District Government into one of the most progressive Local

Governments in the country. Due to the reforms implemented, Faisalabad has turned its

finances around and succeeded in generating a fiscal surplus for the first time in three years.

The prospects are strong for more funds in the coming years. The extra fiscal flexibility that

comes with the surplus funds affords the City District Government the chance to finally

increase public expenditure on sectors previously neglected.

Issue

The Local Government Ordinance encourages a participatory budgeting process and

consulting stakeholders' is the first step in the budget cycle. Due to certain political and

administrative reasons, the City District Government Faisalabad did not follow the Budget

Rules 2003, and were issuing the Budget Call Letters (BCLs) without consulting stakeholders

(Citizens, elected members, CCBs, and NGOs).

City District Government estimates its local receipts based on historical data. In 2004-2005

the District Government Faisalabad did not have authenticated data and information to base

on and to assess the true potential of revenue. Therefore the targets set for revenue were not

realistic. Previously receipts were estimated on the forms prescribed by the Provincial

Government in the Budget Rules 2003. The District Officer Accounts was unable to track the

actual receipts against the departmental targets.

In 2004, the project identified the following major issues in the non-development budget:

� Most of the District Council members (including chairpersons monitoring committees)

did not examine the departments' non-development budget during the budget session

Making the Budgeting Process Work

Implementation and Impacts

12

Box 4: Budget Call Letter (Budget rule 11)

The Budget Call Letter shall be finalized after consultation with the relevant stakeholders. The "stakeholders"

include Councils, elected representatives, general public, women's organization, private sector, Citizen Community

Boards, Non-Governmental Organizations, Community Based Organizations, and other organizations.

Budget cell of the Finance & Planningdepartment

or prior to the budget session and yet they approved the budget;

� There was no proper training for DDOs on budget preparation under the new rules;

� In the majority of cases, budget forms were prepared by DDOs' clerks but these forms

were not checked by the DDOs themselves and yet signed by them. The possible

reason for that has been lack of capacity and interest;

� Completed forms returned by DDOs to District Officer (DO) Finance & Budget (F&B)

often contained errors and these forms were then returned to the concerned DDO for

rectification. The forms were then corrected by the DDO clerks and once again

passed to the DO F&B. If there were still errors, this process was repeated;

� Various forms often contained exactly the same information but when they were

individually completed, the information was found not to match.

Similarly on the development side during the situational analysis, the F&P department

identified the following key issues in the development budget preparation process:

� Lack of evidence based planning with most projects being identified by the local

politicians on the basis of political priorities. Often these politically motivated projects

tend not to be pro-poor or as such no conscious effort was made to identify the most

vulnerable and their needs;

� The major portion of the District Government's funds were distributed throughout the

289 Union Councils equally and the remaining funds were not distributed on the basis

of the greatest need. The Local Government Ordinance envisaged a process where

projects would be prepared with complete community participation of all 21 members

of the Union Council and general public were to be consulted in identifying local

projects. However, frequently the UC Nazims have a very strong input and influence

on project selection, thus resulting in local development schemes without honest

community participation, as was envisaged in the Ordinance;

� Budget preparation for any coming financial year should take six months to complete

from January-June in the preceding year, but in reality tends to be compressed in the

last two months. Projects tend to be identified continuously throughout January - June

without one single submission deadline. This not only increases the workload of the

F&P department but also impacts on the planning process. Projects are also identified,

at the last minute, during the budget preparation process in June, and are then

included in the budget document as “unapproved schemes”. At the end of June, the

ADP is submitted to the District Assembly and House for approval. These projects

therefore bypass the process of discussion or approval in the District Development

Committee (DDC);

� Block allocations for development projects in the ADP, with no regard for targeting

deprivation and economic opportunity;

� The volume of carried forward schemes was quite substantial and was affecting the

development programme for the next year;

� No gender responsive projects in the ADP.

Implementation and Impacts

13

Box 5: Errors in the Completion of Budget Forms

The first test to look into the DDOs' budget was to see that the total figures of the Budget Detail Others (BDO 3) is

balanced with the establishment charges of the Budget Detail Current (BDC 3) and then total of BDO 4 is balanced

with allowances of BDC 3. The second test was to verify the establishment charges and all regular allowances with

BDC 6. But in most of the cases the figures were not balanced. The assistant who made those budgets did not know

the effect of one form on the other.

Rule 57 (2) Budget Rules 2003

“The Budget based on the preliminary estimates as approved by the Nazim shall be presented to the Council for discussion as a draft budget”.

Rule 40 (1) Budget Rules 2003

“The Annual Development Programme shall classify projects by sector, function and geographic location”.

In Faisalabad, the previous accounting system up to March 2005, only recorded cash

payments and receipts on a daily basis. The problem with this system was that the recorded

inflows and outflows had no direct relationship with the actual financial performance. The

obligations to make future payments could not be properly identified. It is a mandatory

provision that the New Accounting Model (NAM) will be followed by all tiers of government in

their financial operations. The Project to Improve Financial Reporting and Auditing (PIFRA) stbased on NAM started its operations in District Faisalabad on 1 April 2005.

Process

To address the above mentioned issues, the process followed is given here:

Budget Call Letter

Budget Call Letter (BCL) is the instrument in which the Local Governments communicate the

vision/ policies/ priorities and targets fixed under various sectors/ programmes and

investments etc. Issuing the budget call letter is a legal requirement for the District

Government - it provides direction and a macro-level perspective on financial policy. This is

an outline plan of who will take responsibility for preparing the final budget.

It clarifies the steps needed to successfully complete the budget. BCL essentially sets out the

timing of events in the planning and budgeting process, the input required from other

stakeholders by the budget desk to enable the desk to compile the Local Government budget

framework and the information required by the stakeholders to enable them prepare their

input.

In 2007-2008 budget cycle, the CDGF managed to organize extensive workshops with the

departments and other stakeholders. The feedback was incorporated into the budget

preparation process and the findings shared with the District's political leadership. The

stakeholders' consultations revealed that social sector investments remain a priority for the

people of Faisalabad, with spending on education and health a primary concern.

The fiscal surplus resulting from improved processes and prudent financial management

allowed the City District Government to target poverty, using evidence based planning which

built on the data and information being generated at all levels. An example of this is the

District’s Citizen Perception Survey, which influenced the allocations in the education and

health sectors. Hence the budget 2007-2008 was more participatory and for the first time

spending limits were set for various sectors, departments were advised to follow the PPRSP

indicators and the Millennium Development Goals (MDGs) in planning their resources for

various sectors.

Gender Responsive Budgeting was also introduced in the BCL as of 2006-07 and

departments and politicians were advised to submit budgets that are more gender responsive.

This is expected to help the District administration in setting a budget which is more citizens

focused and gender responsive. The consultations also included an element of training, to

ensure that stakeholders understood the budgeting process clearly. Similarly, departments

and other stakeholders such as NGOs and elected representatives have been trained on

participatory and gender responsive approaches. All this bolsters their capacity to respond to

community needs and ensures targeted approaches to address poverty and marginalization.

Implementation and Impacts

14

Millennium Development Goals

By 2015 all United Nations member states, including the Government of Pakistan, have pledged to meet the following goals to:� Eradicate extreme poverty

and hunger� Achieve universal primary

education� Promote Gender Equality

and empower women� Reduce Child Mortality� Improve Maternal Health� Combat HIV/AIDS,

malaria and other diseases� Ensure environmental

sustainability� Develop a global

partnership for development

Rule 8 (2) Budget Rules 2003

“The Nazim shall ensure that the needs of the disadvantaged groups are reflected in the priorities and gender issues are adequately addressed”.

Rule 11 (6) Budget Rules 2003

“Each Head of Offices shall prepare its budget in accordance with the Budget Call Letter approved by the Nazim”.

Chart of Accounts

The Chart of Accounts is an essential component of the accounting framework. It provides the structure by which accounting transactions are coded, and thus used in financial reporting.

Gender Responsive Budgeting training for district council members

Estimation of Receipts

The District Government bases its budget on the following types of receipts;

� PFC award from the Provincial Government

� Octroi Grant from the Provincial Government

� Local receipts

� Donors' money

Physical surveys were conducted to assess the true potential of the local sources of revenue

and computerized Budget Detailed Receipts (BDR) forms were generated and the

departments were advised to fill in the electronic forms by using the Collecting Officer (CO)

codes and new Chart of Accounts (CoA). This has helped the F&P department in setting

realistic targets and tracking the departments' receipts against their targets on a monthly

basis.

Non-Development Budget

The Finance & Budget officer is responsible for preparing the non-development budget

according to the new Budget Rules. The non-development budget is more than 85 percent of

the total budget in City District Faisalabad, and includes the following:

� Establishment charges

� Purchase of durable goods

� Repair & Maintenance of durable goods

� Commodities and services

� Transfer payments

� Miscellaneous items

The budgeting process of Faisalabad used to be excessively cumbersome and labour

intensive. In the past, it used to take at least 9,000 man-days from the numerous service

officers involved to prepare and finalise the budget. The error rate was more than 30 percent.

In reality, the process was typically compressed during the last two months of the financial

year, resulting not only in the workload of the F&P department surging during this period but

also in substantive delays in project implementation.

In the last three years, the departments took huge strides in improving the traditional

budgeting process. Much of this is due to better coordination, training provided to the officers

involved in the process and on-going technical support from the SPU team. The F&P

department has established a fully equipped Budget Cell in the DCO complex and 40

Resource Centres throughout the District. These Resource Centres are providing support to

the DDOs at their door step and they now do not need to visit the F&P Department for the

submission of budgets (Figure 2).

CDGF now has an on-line budgeting system which has translated into fiscal planning and

operational efficiencies for the City District Government. Embedded as a distinct module in

the FMIS, Faisalabad's on-line budgeting system allows for highly effective budgeting and

timely approval of the budget by the City District Council.

Implementation and Impacts

15

Figure 2 : Online Budgeting Process

Performance Based Budgeting

Prior to FY 2007-2008, the CDGF could not measure the performance of departments

against the annual targets. To make the departments more accountable and improve service

delivery in the District, the CDGF in 2007-2008 introduced the concept of performance based

budgeting. All the departments were requested to submit annual targets against the

requested budget lines on Budget Salient Features (BSF) forms. This is now approved from

the District Council and is an integral part of the budget document. The EDOs of all

departments report the monthly progress against the BSF targets on the Budget

Management (BM) forms that bring more transparency and accountability in financial

management operations.

As an example, to improve the performance of the Education Department, especially the

elementary section of the Education Department and quality of primary education in the

District, the CDGF introduced the concept of school based budgeting.

The concept of school based budgeting is very new in Pakistan. Under the current set-up, on

the elementary side of the Education department, the Deputy District Officer (DDO)

Education is responsible for more than 300 schools. He or she also exercises financial

powers for those schools. Previously block allocations were made for these schools, and

therefore there was no criterion for the distribution of budgets to the individual schools.

To address this issue the F&P department introduced school based budgeting in Jaranwala

town as a pilot. Jaranwala town comprises 736 primary schools. All the schools were given

separate budget lines for few items. This is expected to provide an opportunity for more local

control and greater fiscal independence for primary schools, with resulting improvements in

the quality of education in the District. This will also help the Finance department of the CDGF

to work out the cost per child in the primary education system. The purpose is not to reduce

the cost at the expense of quality education but to improve the quality of primary education by

effective resource planning and strengthen the accountability mechanisms in the education

department.

Implementation and Impacts

16

Resource Centres (RCs)40 RCs helping 600 DDOs

DDO wise budget data entered & storedSubmitted to the Main server in web based FMIS

Head of Offices

Departments' own data entered & stored

Scrutiny and verification of RCs data

Verified data submitted to the main server

in web based FMIS

F&P Department

Retrieval of verified data

Consolidation of budget data

Finalization of Draft Budget

Council

Approval of final budget

BSF & BM8-9 Forms

BSF forms mean Budget Salient Features forms and these forms are used for setting the annual targets for the sector/ departments. BM8-9 forms mean the Budget Management forms and are used for monitoring the progress against the targets given in the BSF forms.

However, the Education department is still facing problems in the disbursement of money.

According to the DDOs, handbook in which all the categories of the employees are mentioned

who could exercise the powers of the Drawing and Disbursing Officers, the majorities of

primary school head-teachers do not belong to these categories and are therefore unable to

utilise the budget. As a result, the office of the DO assumes the power to process the bills for

those schools. According to the treasury and audit rules, if one person exercises the power for

the procurement of many cost centres, they have to undertake bulk purchases to achieve

economy. At the same time in accordance with rules, from the DAO, for every item in the cost

centre, separate bills per item per cost centre have to be produced. These inconsistent rules

are one of many challenges currently faced by the Education and F&P departments.

Development Budget

In the Annual Development Programme (ADP) process, the identification of development

projects is very important and initiated at the Union Council (UC) level by UC Nazims, the

District Nazim and EDOs. The elected member of the District Council (Zila council) submit his

project proposal to the District Nazim or to any other of the senior administration officers. The

proposal is then forwarded to the appropriate EDO i.e. education or Works and Services etc.

The department then begins the process of preparing cost estimates for the projects, which

culminates in a BDD-4 form (PC-1). All projects that contain a building, roads or other

infrastructure component involve the EDO Works & Services. Once estimates are prepared,

the proposal is then routed to the EDO F&P's team, where a working paper for the proposals

is prepared for submission to the District Development Committee (DDC). Proposals

successful at this stage are then “approved schemes” and included in the budget for the

following financial year.

In the past, block allocations were made as a result of which many sectors remained

neglected. Therefore, the CDGF in the Budget for 2007-08 made adjustments and in the

development allocation, the F&P department by following the Punjab Poverty Reduction

Strategy Paper (PPRSP) indicators has allocated a 5 percent increase over the previous

year's allocation for agriculture, 8 percent increase in community development, 11 percent

increase in education and 7 percent increase in the primary and secondary health care sector.

There has been a visible move towards ensuring that allocations and expenditures are pro-

poor, and reflect the District's commitments to achieving the Millennium Development Goals.

The CDGF's improved fiscal position and the timely release of development funds has

resulted in the timely execution of development projects. Further, it has reduced the number

of throw forward schemes from more than 3,000 in FY 2004-2005 to 1,468 in FY 2007-2008.

In the Finance & Planning department there was a need to have consistency in the

Implementation and Impacts

17

Box 7: Budget Rules and Block Allocation

According to Budget Rules 2003 Section 58(3), No lump sum provisions shall be made in the budget the details of

which cannot be explained.

Box 6: Steps Taken by the Planning Wing of the F&P Department

� Organized comprehensive training programme for elected representatives on budget and planning and

gender responsive budgeting.

� Identification of schemes through the elected members in February with the Department attempting to submit

the draft budget in April 2008.

� Development of the Planning module of the FMIS, which will reduce the times for budget processing,

preparing the working paper for the DDC and also for issuing the minutes of the DDC meeting.

PC 1

“PC1 stands for the Planning Commission 1. That is the form which is used for the submission of development projects”.

Rule 64 (1)(IV) Budget Rules 2003

“Each Local Government shall efficiently and effectively manage the resources made available to the Local Government”.

development project numbers. This issue was addressed by the planning wing of the F&P

department and allocated project numbers which were unique and consistent with the project

numbers used in PIFRA by the District Accounts office. Therefore, the Planning wing not only

allocated unique project numbers but also started tagging the individual development

schemes with the Geographical Information System (GIS). This will allow the F&P

department to assess the individual schemes according to the Provincial Government

Planning and Development (P&D) department’s prescribed planning and engineering criteria .

However, there is a need to develop synergy with planning at the UC and District levels. Once

this is achieved then it will be easier for the F&P department to understand local needs and

development priorities before approving projects at the DDC stage. If Town level and UC level

information was available, then the allocation of resources could be made on a priority basis.

At the moment, projects at the UC level are approved arbitrarily and not using official planning

guidelines.

New Accounting Model

In NAM, the concept of Modified Cash-Based Accounting was introduced. Transactions

regarding future commitment can now be recorded through NAM. By keeping a record of

future commitments that have been entered into, the budget position can be effectively

monitored and expenditures that may arise as a result of possible overspending in the budget

can be readily identified.

Impacts

Improved Financial Management has brought greater efficiency in the CDGF budgeting

process. It allowed the departments to evaluate the progress and asses where resources are

needed to be aligned in order to complete district's commitments. The CDGF is now in a

better position to identify the priority projects by sector and location by introducing the pro-

poor budgeting in the District. Following are the impacts of improved budgeting process in the

City District Government Faisalabad:

� Consultation workshops were organised with departments, NGOs, CCBs, and

elected representatives for the budget 2007-2008 and 2008-2009;

� An effective BCL was issued. In BCL 2007-2008 PPRSP indicators were strictly

followed. The concept of Gender Responsive Budgeting was introduced;

� Greater fiscal space was achieved (for the first time the City District Faisalabad

produced a surplus budget);

� A significant reduction in the budgeting process from inputs of 9000 man days to

3000 man days and a time-line of 45 to 9 days has resulted in savings of Rs.10

million;

� School based budgeting was introduced in Jaranwala Town as a pilot;

� The concept of performance based budgeting has been embedded into CDGF, and

EDOs have to report to the DCO on a quarterly basis;

� The Planning module of the FMIS is helping the planning wing of the F&P department

in preparing the working paper to be submitted in the District Development

Committee, and has reduced the time needed for this process from two weeks to one

day.

Implementation and Impacts

18

New Accounting Model

The New Accounting Model (NAM) has been adopted as the New Accounting Model for Pakistan that not only allows modified cash based accounting but also allows the commitments against budget and allowing statements of receipts and payments, asset and liabilities and cash flow statement.

Training on New Accounting Model

Improvement in the Release of Grants

Issue

In the past, releases for non-development expenditure were given to departments through

the respective EDO before being received by a DDO. Access to funds would often depend on

the nature of the relationship between a particular DDO and EDO, if strained then delays

often occurred.

On the development side there was a practice to release 30 percent of funds against the

approved allocation of individual projects. The large proportion of the majority of the individual

projects were less than Rs 50,000 and the contractors were not willing to work on the 30

percent releases against those projects. This has resulted in delays in starting development

projects and also affected utilisation. Most projects would not be completed and would spill

over to the next year's budget (ADP).

Process

A very large proportion of receipts emanate from the Provincial Government’s PFC award.

This award is received in 12 monthly equal installments; the problem with this arrangement is

that enough money is not available for releasing to DDOs in order to cater their spending

requirements. There was no criterion for the release of funds. This has led to the development

of a criterion for releasing funds which makes money available directly to the DDO, so that

they can use the funds immediately. The process bypasses EDOs, though they are kept

informed of the releases, gives enough flexibility to managers in spending money and cuts

additional bureaucracy.

Executing agencies tend to complain that the finance and planning department does not

release funds and therefore they are unable to complete their work within time and budget.

However, the evidence does not support this claim; executing agencies do tend to be

provided with funds. On the development side, the process of releases has now been

streamlined; 100 percent funds are released and Administrative Approval (AA) issued for

those projects which are approved in the DDC. The timely release of funds has not only

restored the confidence of contractors in the market but also improved the utilisation rate.

Impacts

The mechanism for releasing funds to departments lacked clarity in the past. This has led to

the development of criterion for releasing funds which ensures the availability of money to the

managers, so that they can use the funds immediately. The improved release process saves

time and consumes less human resources. The CDGF improved release policy has the

following benefits:

� The timely release of funds has improved service delivery in the departments and will

help the executing agencies in completing projects on time;

� Online direct releases to the DDOs, has also improved service delivery and the

utilisation rates especially in the education department.

Implementation and Impacts

19

Rule 64 (3) Budget Rules 2003

“Delay in payment of money due from a Local Government shall be avoided”.

Expenditure Tracking System

Issue

Previously it has been difficult for departments to track monthly development and non

development expenditure. The main reason has been that the systems in placed in the

departments were not aligned to the DAO. The departments were only preparing budgets at

the departmental level while incurred expenditure was recorded at DAO. The F&P

department was unable to monitor expenditure against the approved budget.

Process

In the expenditure tracking system which was previously followed, the DAO was sending

expenditure details to the office of the EDO F&P and the expenditure statements were not

disseminated further to the relevant DDOs and the concerned executing agencies. The