Embed Size (px)

DESCRIPTION

Summary useful for non-business courses graduates

Citation preview

CAPITAL STRUCTURE AND WORKING

CAPITAL MANAGEMENT

CAPITAL

amount or asset which is invested in a business. When the business is closed, after paying outside creditors, balance amount will be his capital which he can obtain.

Debt

Preferred

Equity

HOW DO WE WANT TO FINANCE OUR FIRM’S ASSETS?

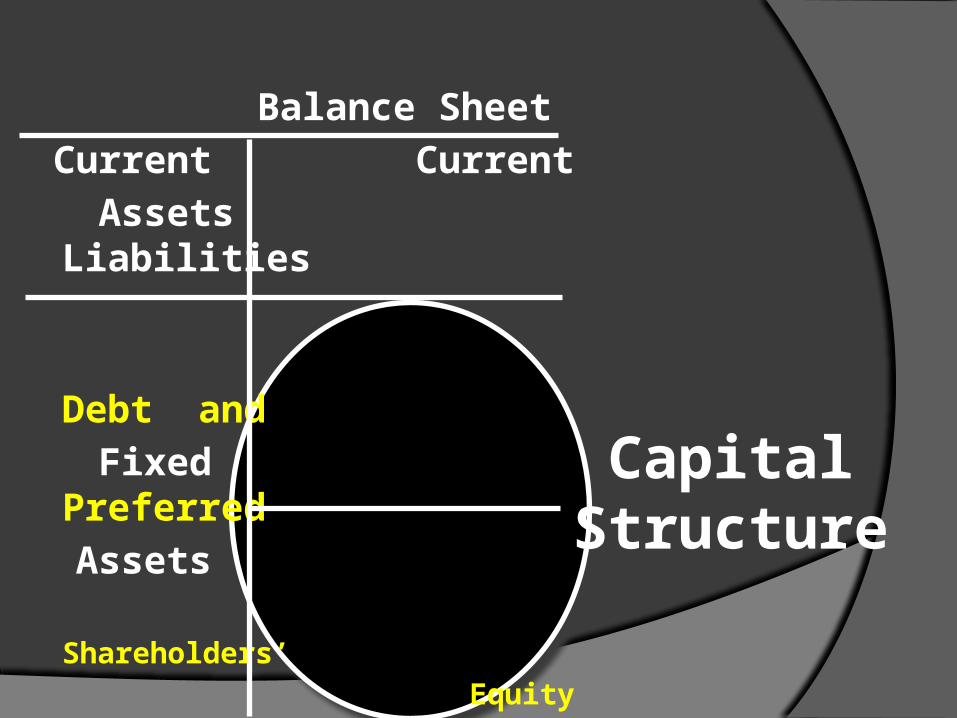

Balance Sheet Current Current Assets Liabilities

Debt and Fixed Preferred Assets Shareholders’

EQUITY

Balance Sheet

Current Current

Assets Liabilities

Debt and

Fixed Preferred

Assets

SHAREHOLDERS’

EQUITY

Balance Sheet

Current Current

Assets Liabilities

Debt and

Fixed Preferred

Assets

SHAREHOLDERS’

EQUITY

FinancialStructure

Balance Sheet

Current Current

Assets Liabilities

Debt and

Fixed Preferred

Assets

SHAREHOLDERS’

EQUITY

Balance Sheet

Current Current

Assets Liabilities

Debt and

Fixed Preferred

Assets

Shareholders’

Equity

CapitalStructure

Why is Capital Structure Important?

1) Leverage: higher financial leverage means higher returns to stockholders, but higher risk due to interest payments.

2) Cost of Capital: Each source of financing has a different cost. Capital structure affects the cost of capital.

3) The Optimal Capital Structure is the one that minimizes the firm’s cost of capital and maximizes firm value.

What is the Optimal Capital Structure?

In a “perfect world” environment with no taxes, no transaction costs and perfectly efficient financial markets, capital structure does not matter.

This is known as the Independence hypothesis: firm value is independent of capital structure.

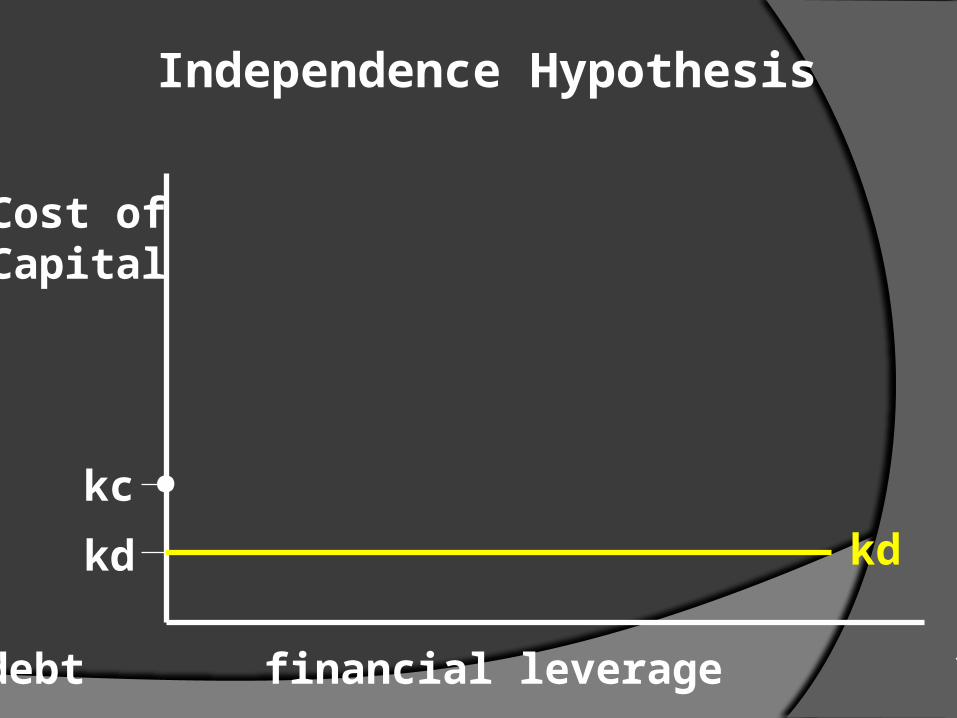

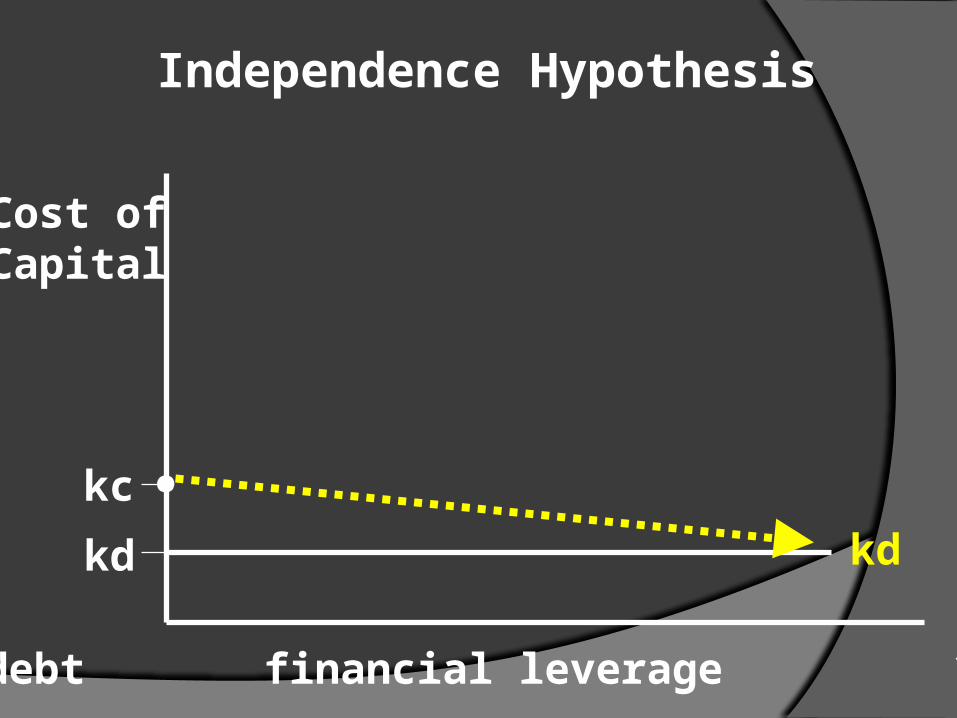

Independence Hypothesis

Firm value does not depend on capital structure.

Cost ofCapital

kc

0% debt financial leverage 100%debt

.

kc = cost of equitykd = cost of debtko = cost of capital

Independence Hypothesis

.

Independence Hypothesis

Cost ofCapital

kc

kd kd

0% debt financial leverage 100%debt

.

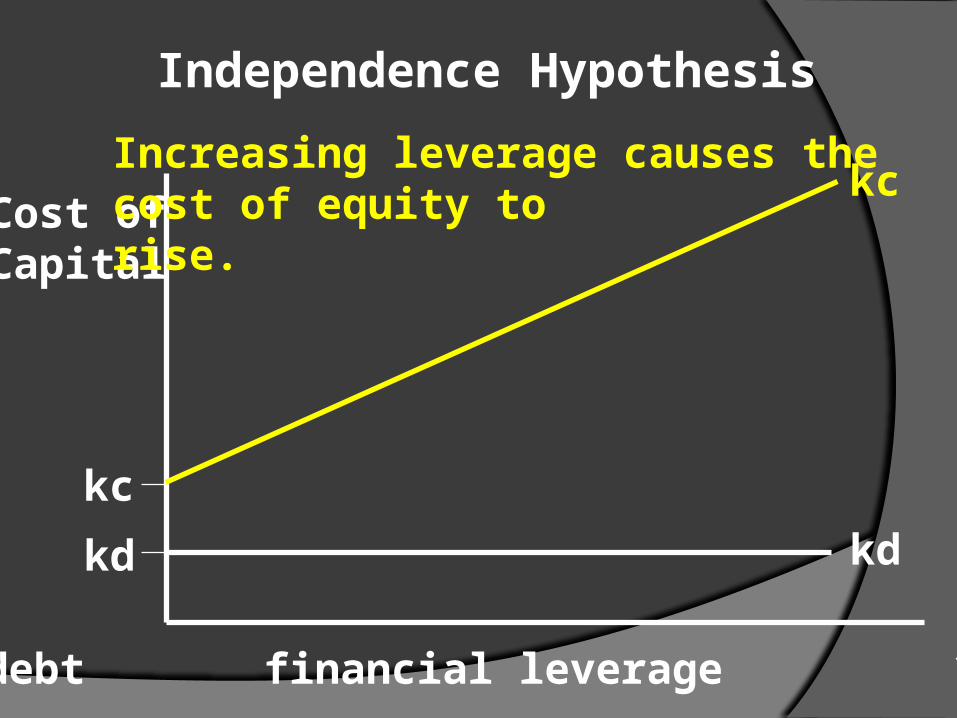

Independence Hypothesis

Cost ofCapital

kc

kd kd

0% debt financial leverage 100%debt

Increasing leverage causes thecost of equity torise.

Independence Hypothesis

Cost ofCapital

kc

kd kd

0% debt financial leverage 100%debt

Independence Hypothesis

Cost ofCapital

kc

kd

kc

kd

Increasing leverage causes thecost of equity torise.

0% debt financial leverage 100%debt

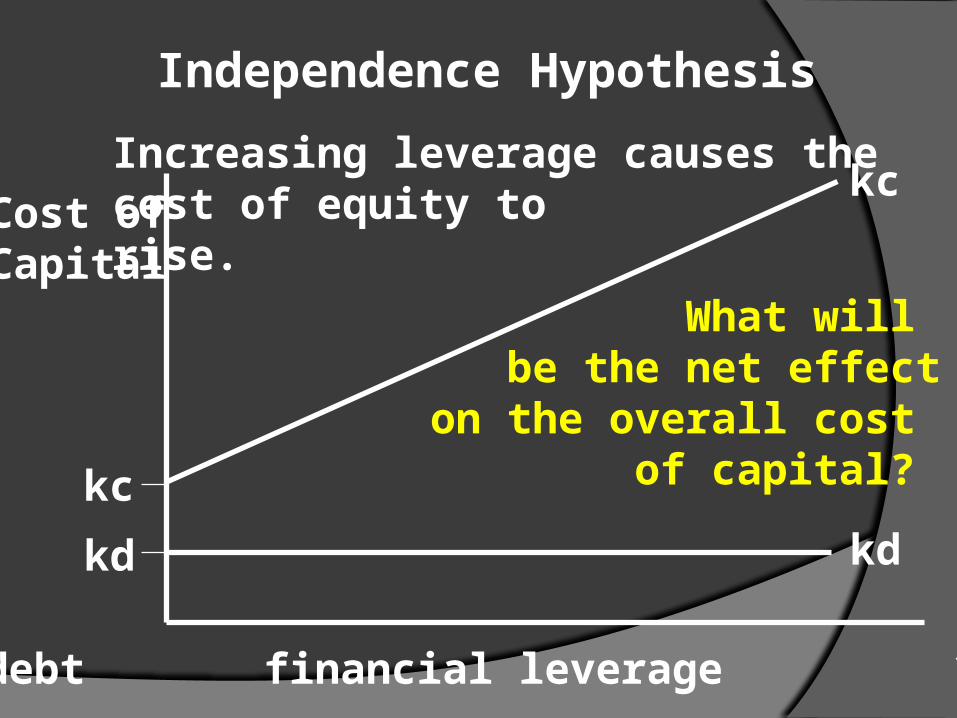

Independence Hypothesis

Cost ofCapital

kc

kd

kc

kd

Increasing leverage causes thecost of equity torise.

What will be the net effect

on the overall cost of capital?

0% debt financial leverage 100%debt

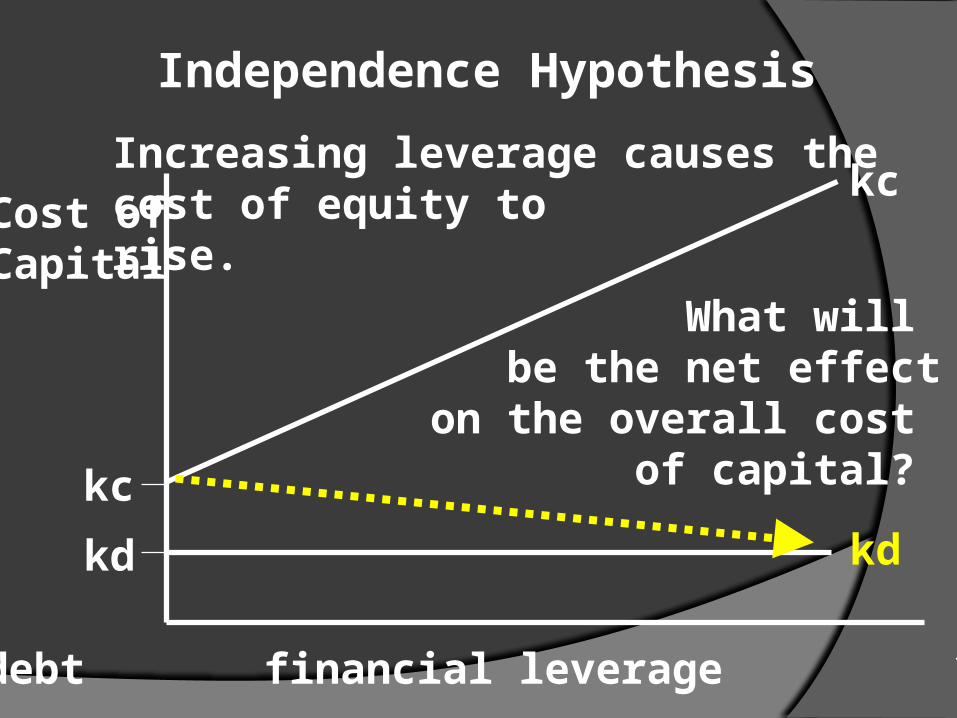

Independence Hypothesis

Cost ofCapital

kc

kd

kc

kd

Increasing leverage causes thecost of equity torise.

What will be the net effect

on the overall cost of capital?

0% debt financial leverage 100%debt

kc

kd

Independence Hypothesis

Cost ofCapital

kc

ko

kd

0% debt financial leverage 100%debt

If we have perfect capital markets, capital structure is irrelevant.

In other words, changes in capital structure do not affect firm value.

Independence Hypothesis

Dependence Hypothesis

Increasing leverage does not increase the cost of equity.

Since debt is less expensive than equity, more debt financing would provide a lower cost of capital.

A lower cost of capital would increase firm value.

Dependence Hypothesis

Cost ofCapital

kc

kd

financial leverage

kc

kd

Since the cost of debt is lowerthan the cost of equity...

Dependence Hypothesis

Since the cost of debt is lowerthan the cost of equity…increasing leverage reduces thecost of capital.

Cost ofCapital

kc

kd

financial leverage

kc

kdko

Moderate Position

The previous hypothesis examines capital structure in a “perfect market.”

The moderate position examines capital structure under more realistic conditions.

For example, what happens if we include corporate taxes?

Tax effects of financing with debt

with stock with debt

EBIT 400,000 400,000

- interest expense 0 (50,000)

EBT 400,000 350,000

- taxes (34%) (136,000) (119,000)

EAT 264,000 231,000

- dividends (50,000) 0

Retained earnings 214,000 231,000

with stock with debt

EBIT 400,000 400,000

- interest expense 0 (50,000)

EBT 400,000 350,000

- taxes (34%) (136,000) (119,000)

EAT 264,000 231,000

- dividends (50,000) 0

Retained earnings 214,000 231,000

Tax effects of financing with debt

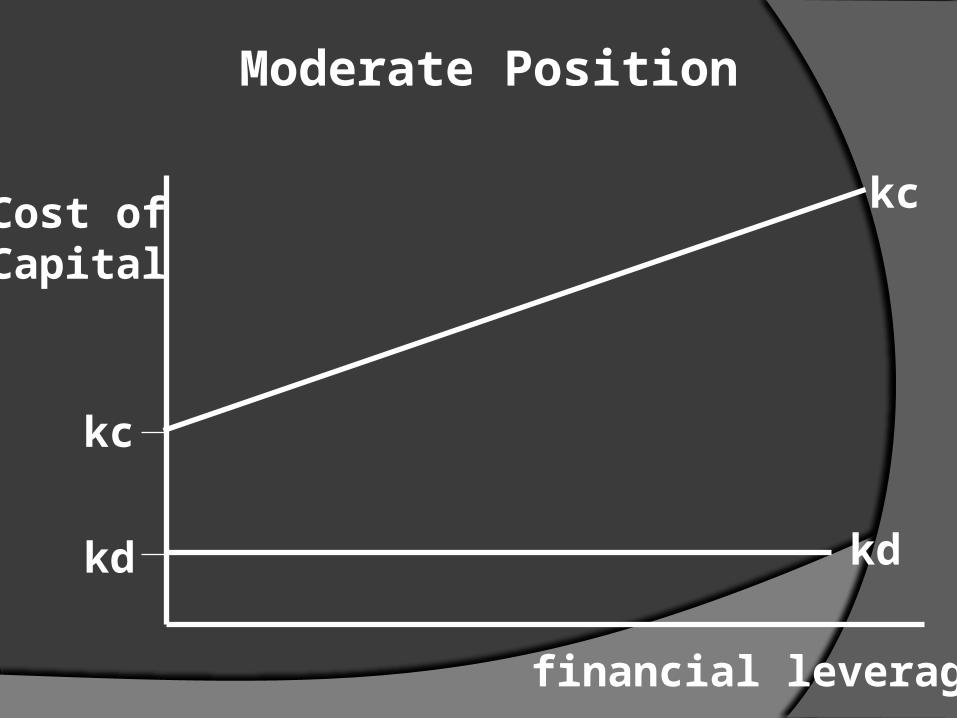

Moderate Position

Cost ofCapital

kc

kd

financial leverage

kc

kd

Moderate Position

Cost ofCapital

kc

kd

financial leverage

kc

kd

Even if the cost of equity risesas leverage increases, the cost of debt is very low...

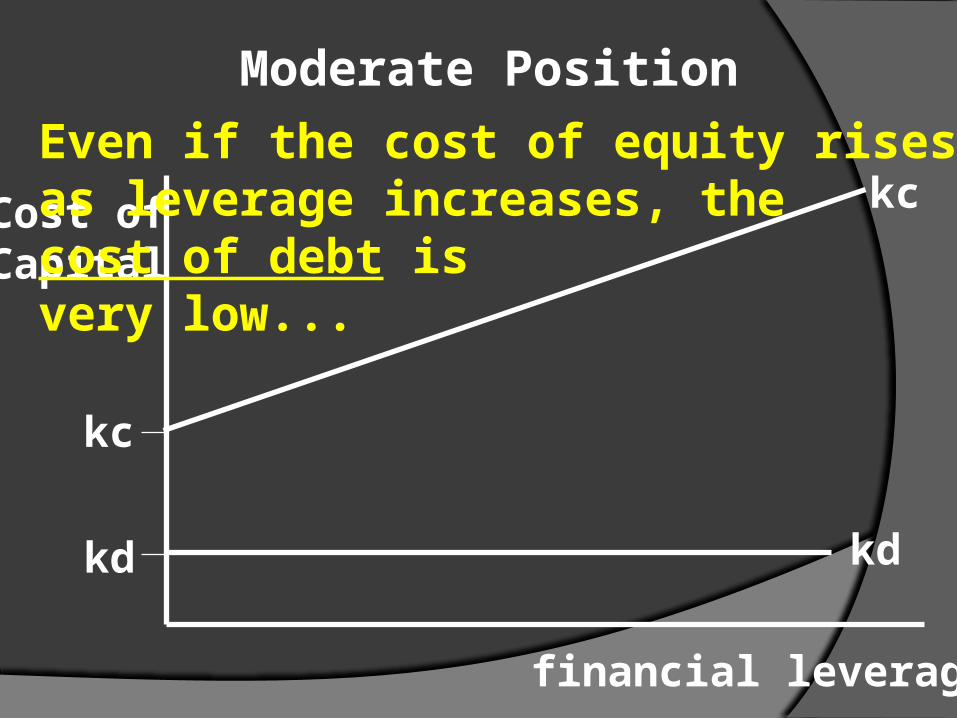

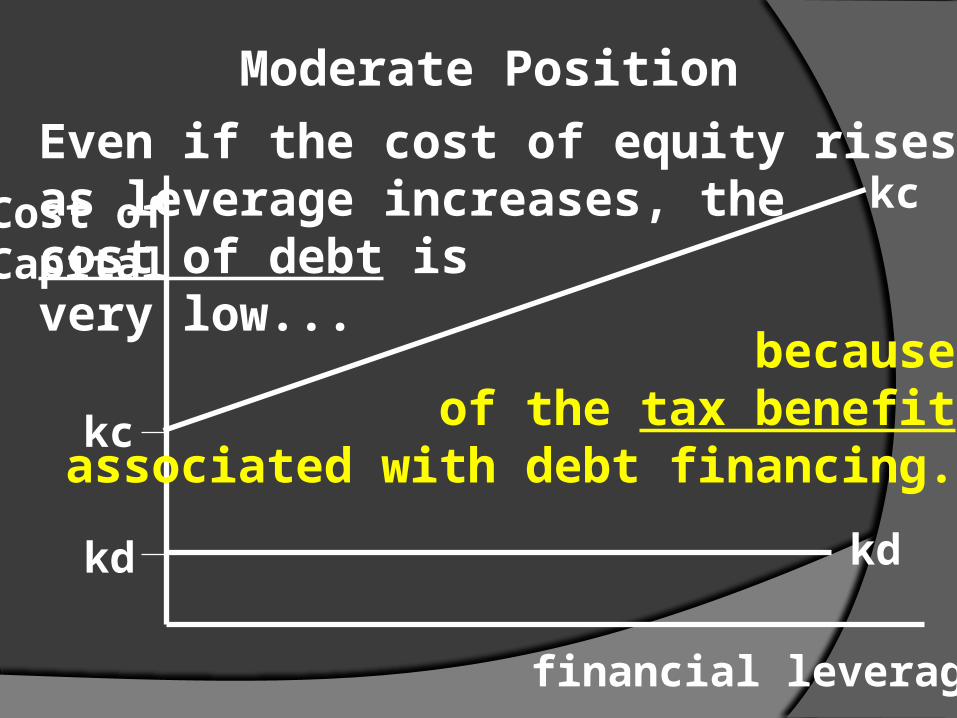

Moderate Position

Cost ofCapital

kc

kd

financial leverage

kc

kd

becauseof the tax benefit

associated with debt financing.

Even if the cost of equity risesas leverage increases, the cost of debt is very low...

Moderate Position

Cost ofCapital

kc

kd

financial leverage

kc

kd

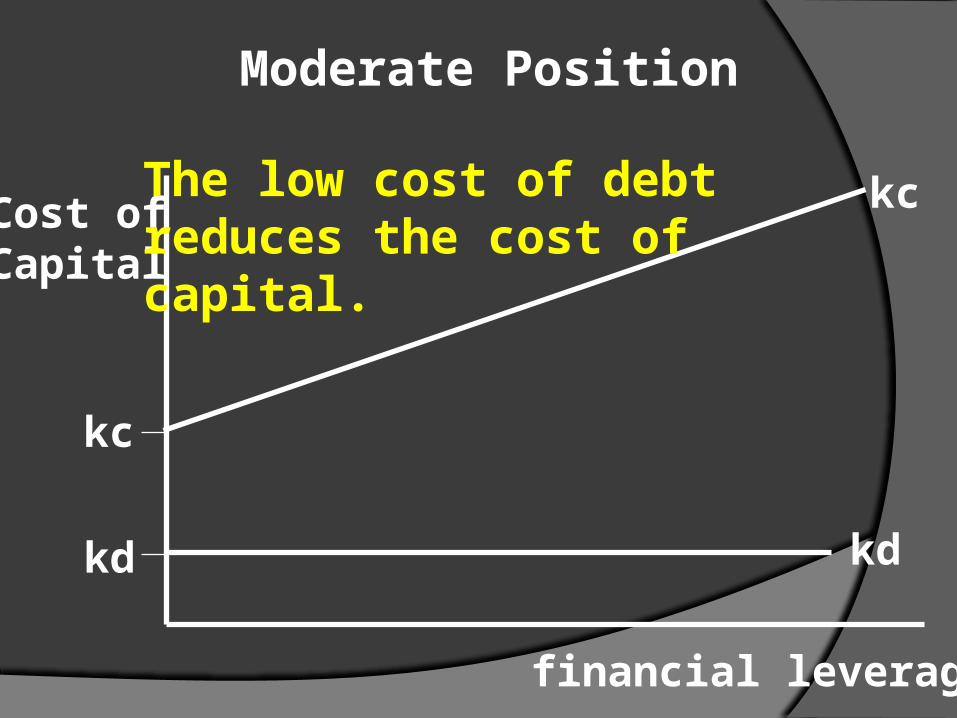

The low cost of debt reduces the cost of capital.

Moderate Position

Cost ofCapital

kc

kd

financial leverage

kc

kd

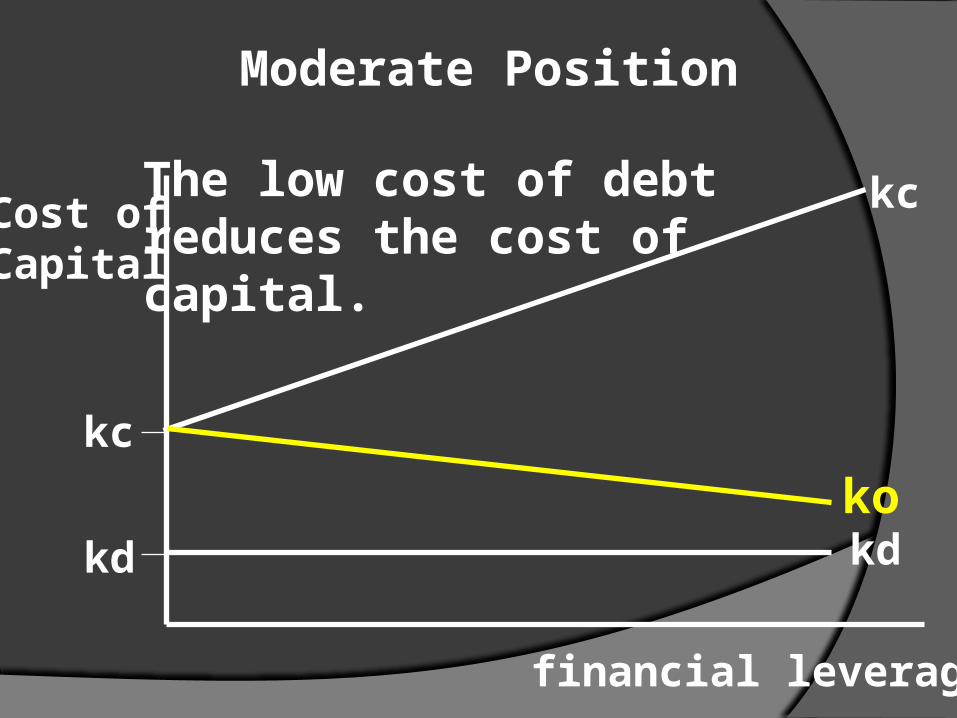

The low cost of debt reduces the cost of capital.

ko

Moderate Position

So, what does the tax benefit of debt financing mean for the value of the firm?

The more debt financing used, the greater the tax benefit, and the greater the value of the firm.

So, this would mean that all firms should be financed with 100% debt, right?

Why are firms not financed with 100% debt?

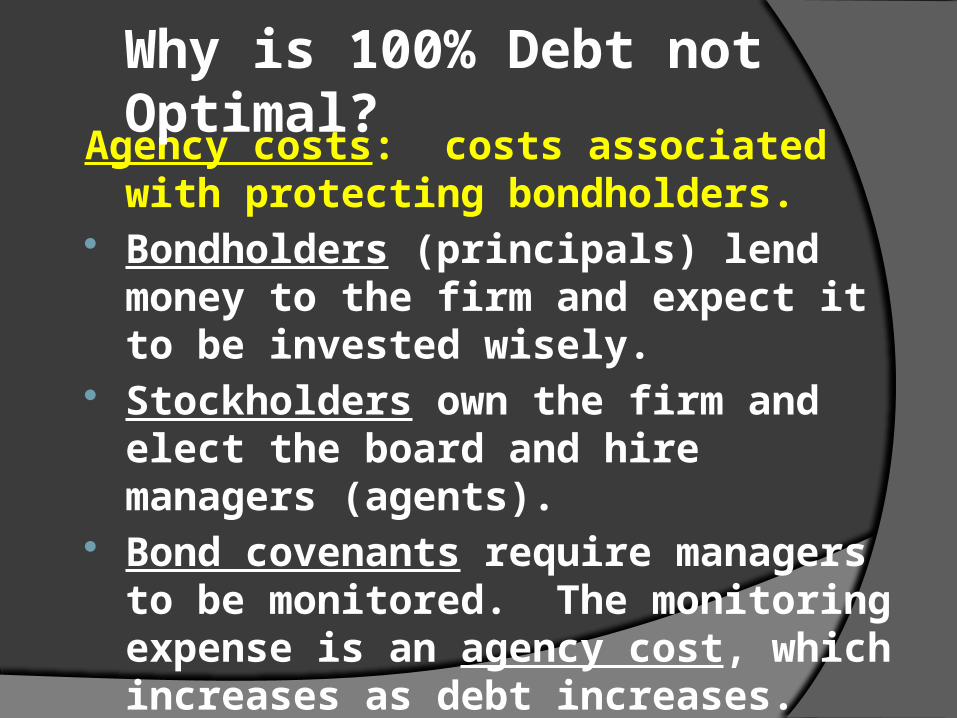

Why is 100% Debt not Optimal?Bankruptcy costs: costs of financial

distress. Financing becomes difficult to get. Customers leave due to

uncertainty. Possible restructuring or

liquidation costs if bankruptcy occurs.

Agency costs: costs associated with protecting bondholders.

Bondholders (principals) lend money to the firm and expect it to be invested wisely.

Stockholders own the firm and elect the board and hire managers (agents).

Bond covenants require managers to be monitored. The monitoring expense is an agency cost, which increases as debt increases.

Why is 100% Debt not Optimal?

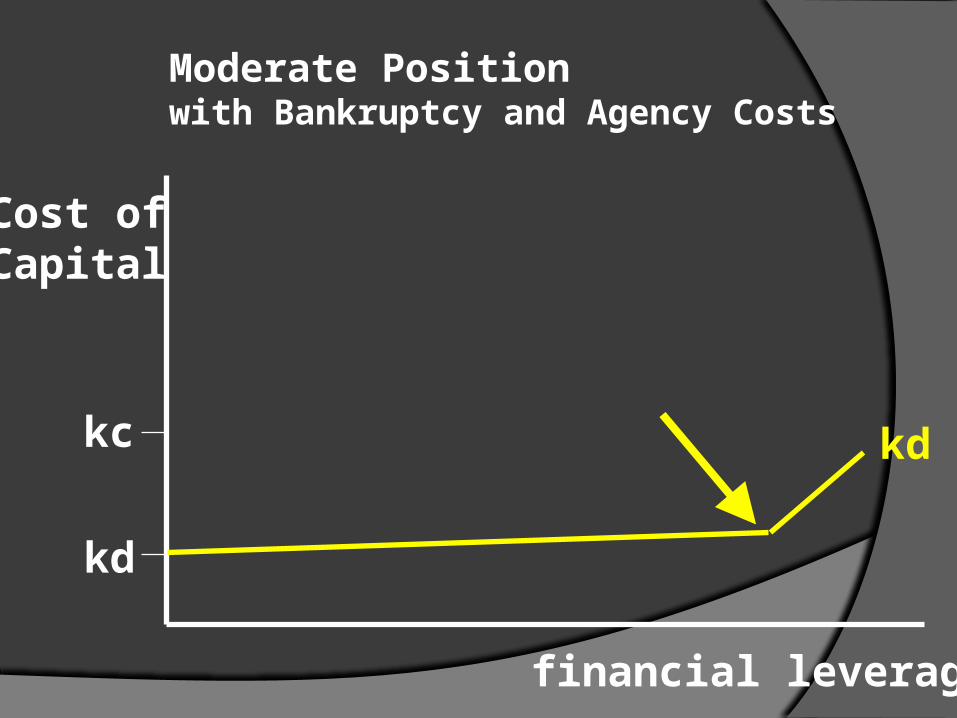

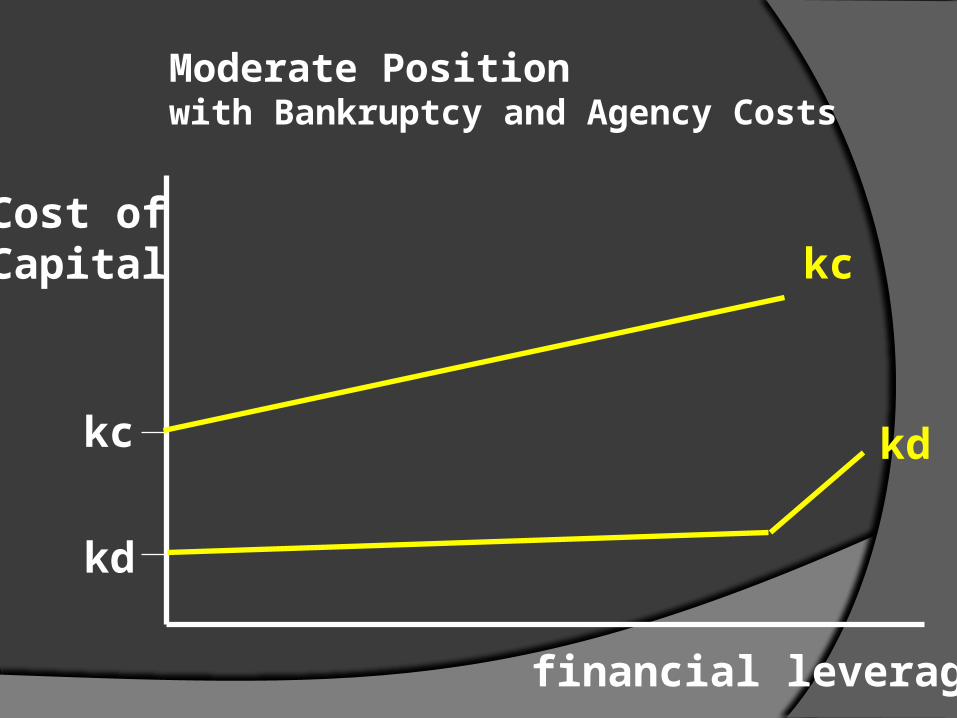

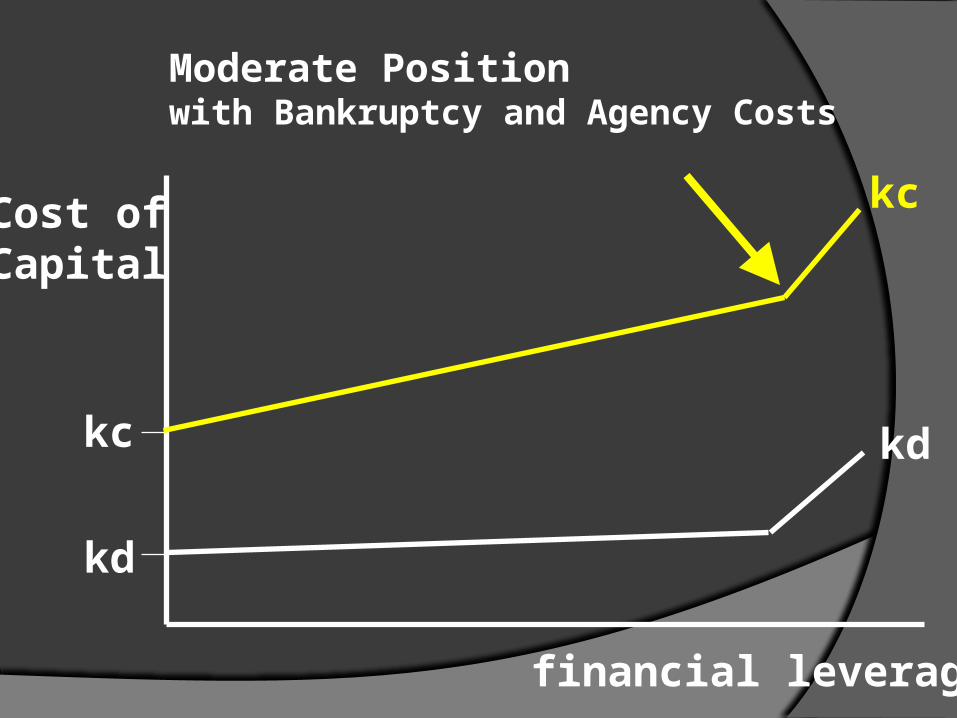

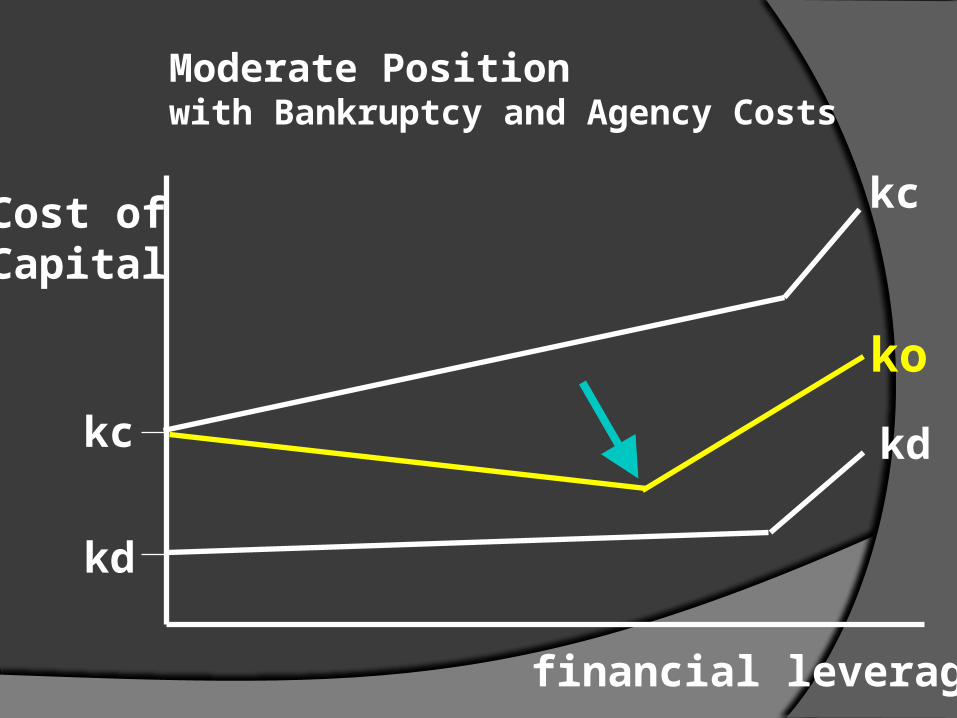

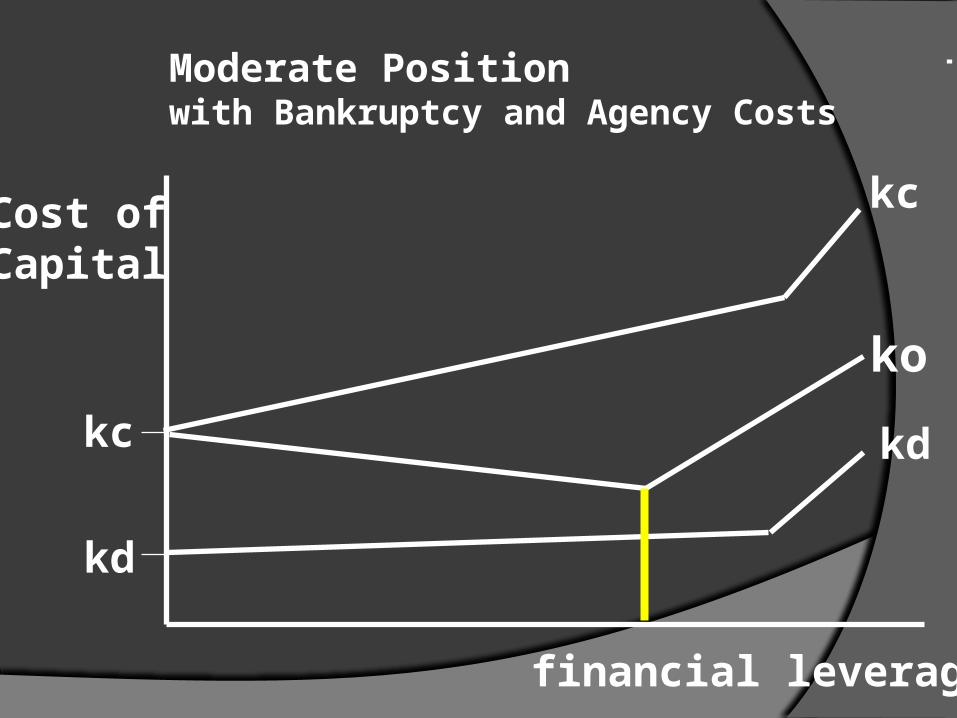

Moderate Positionwith Bankruptcy and Agency Costs

Cost ofCapital

financial leverage

kc

kd

Cost ofCapital

financial leverage

kc

kdkd

Moderate Positionwith Bankruptcy and Agency Costs

Cost ofCapital

financial leverage

kc

kd

kd

Moderate Positionwith Bankruptcy and Agency Costs

Cost ofCapital

financial leverage

kc

kd

kc

kd

Moderate Positionwith Bankruptcy and Agency Costs

Cost ofCapital

financial leverage

kc

kd

kc

kd

Moderate Positionwith Bankruptcy and Agency Costs

Cost ofCapital

financial leverage

kc

kd

kc

kd

If a firm borrows too much, thecosts of debt and equity will spike upward, due to bankruptcy costsand agency costs.

Moderate Positionwith Bankruptcy and Agency Costs

Cost ofCapital

financial leverage

kc

kd

kc

kd

Moderate Positionwith Bankruptcy and Agency Costs

Cost ofCapital

financial leverage

kc

kd

kc

kdko

Moderate Positionwith Bankruptcy and Agency Costs

Cost ofCapital

financial leverage

kc

kd

kc

kd

ko

Moderate Positionwith Bankruptcy and Agency Costs

Cost ofCapital

financial leverage

kc

kd

kc

kd

ko

Ideally, a firm should use leverageto obtain their optimum capital structure, which will minimize thefirm’s cost of capital.

Moderate Positionwith Bankruptcy and Agency Costs

Cost ofCapital

financial leverage

kc

kd

kc

kd

ko

Moderate Positionwith Bankruptcy and Agency Costs

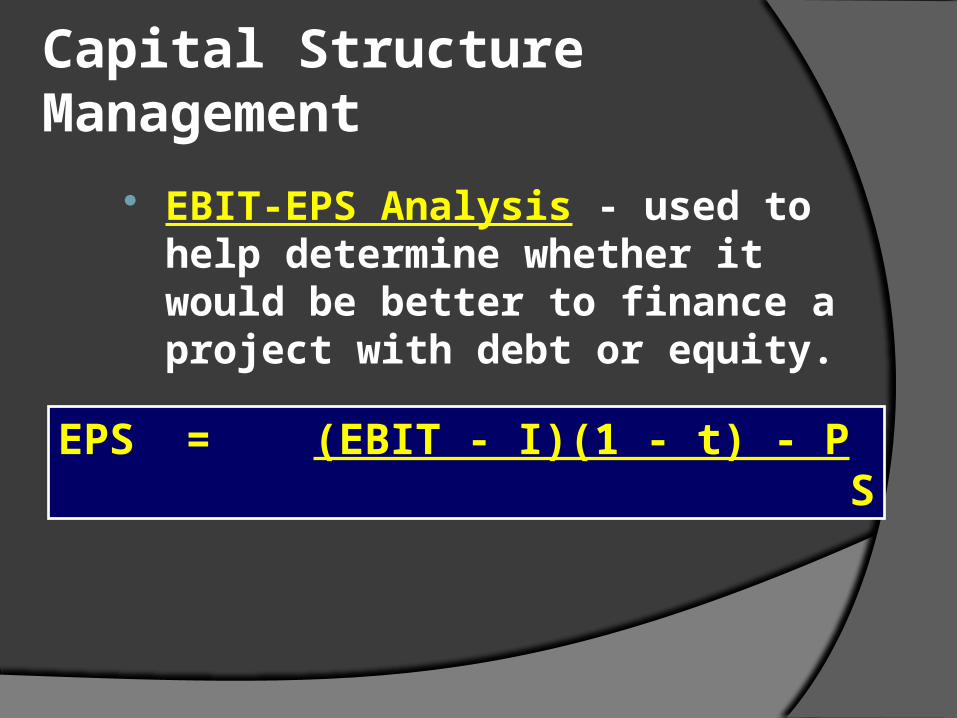

Capital Structure Management

EBIT-EPS Analysis - used to help determine whether it would be better to finance a project with debt or equity.

Capital Structure Management

EBIT-EPS Analysis - used to help determine whether it would be better to finance a project with debt or equity.

EPS = (EBIT - I)(1 - t) - P S

Capital Structure Management

EBIT-EPS Analysis - used to help determine whether it would be better to finance a project with debt or equity.

EPS = (EBIT - I)(1 - t) - P S

I = interest expense, P = preferred dividends,S = number of shares of common stock outstanding.

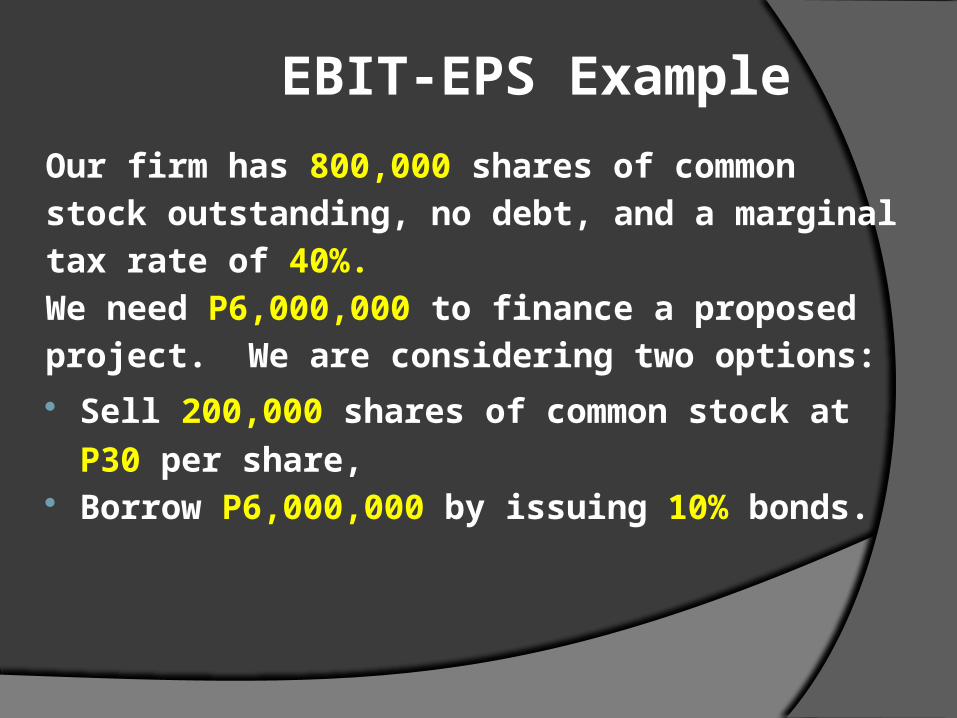

EBIT-EPS Example

Our firm has 800,000 shares of common

stock outstanding, no debt, and a marginal

tax rate of 40%.

We need P6,000,000 to finance a proposed

project. We are considering two options:

Sell 200,000 shares of common stock at

P30 per share, Borrow P6,000,000 by issuing 10% bonds.

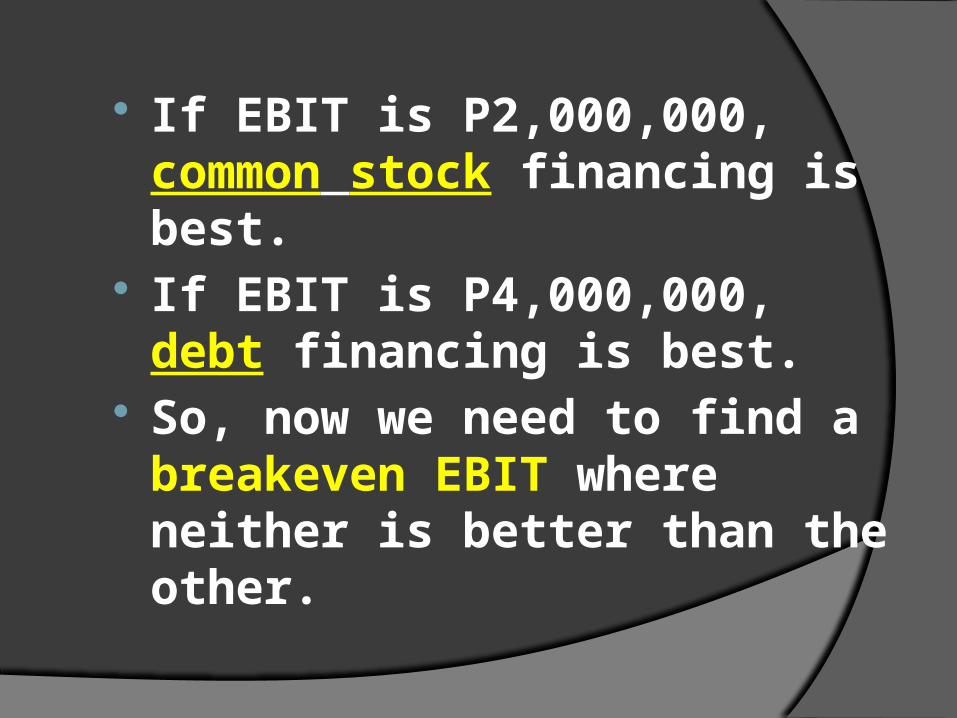

If we expect EBIT to be P2,000,000:

Financing stock debt

EBIT 2,000,000 2,000,000- interest 0 (600,000)EBT 2,000,000 1,400,000- taxes (40%) (800,000) (560,000)EAT 1,200,000 840,000# shares outst. 1,000,000 800,000EPS P1.20 P1.05

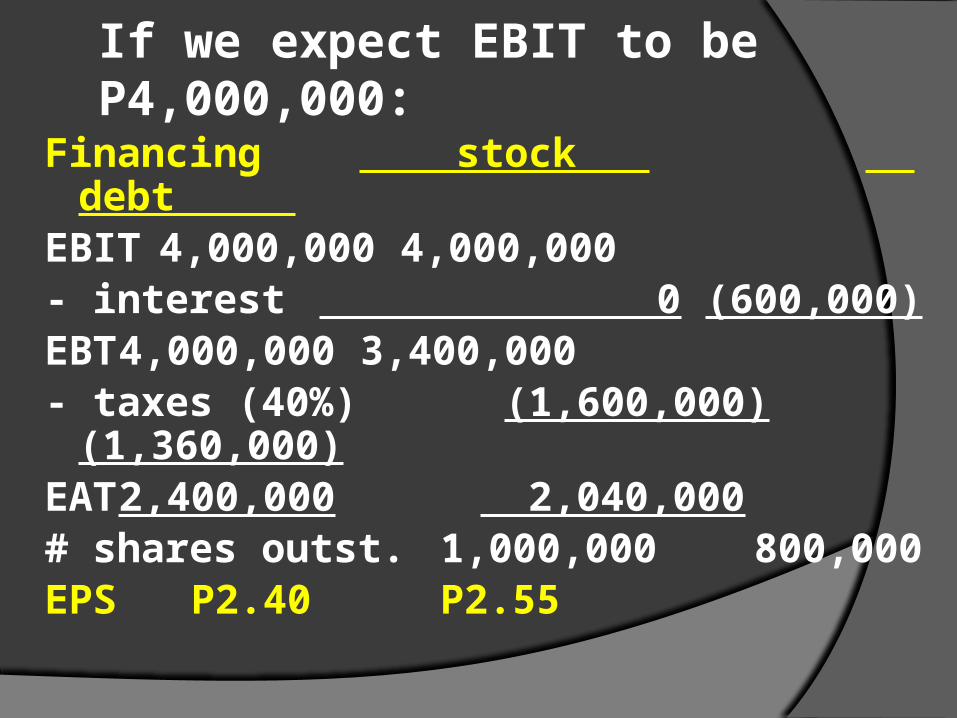

Financing stock debt EBIT 4,000,000 4,000,000- interest 0 (600,000)EBT 4,000,000 3,400,000- taxes (40%) (1,600,000)

(1,360,000)EAT 2,400,000 2,040,000# shares outst. 1,000,000 800,000EPS P2.40 P2.55

If we expect EBIT to be P4,000,000:

If EBIT is P2,000,000, common stock financing is best.

If EBIT is P4,000,000, debt financing is best.

So, now we need to find a breakeven EBIT where neither is better than the other.

If we choose stock financing:EPS

EBITP1m P2m P3m P4m

stock financing

0

3

2

1

If we choose bond financing:EPS

EBITP1m P2m P3m P4m

bond financing

0

3

2

1

Breakeven EBITEPS

EBITP1m P2m P3m P4m

bond financing

stock financing

0

3

2

1

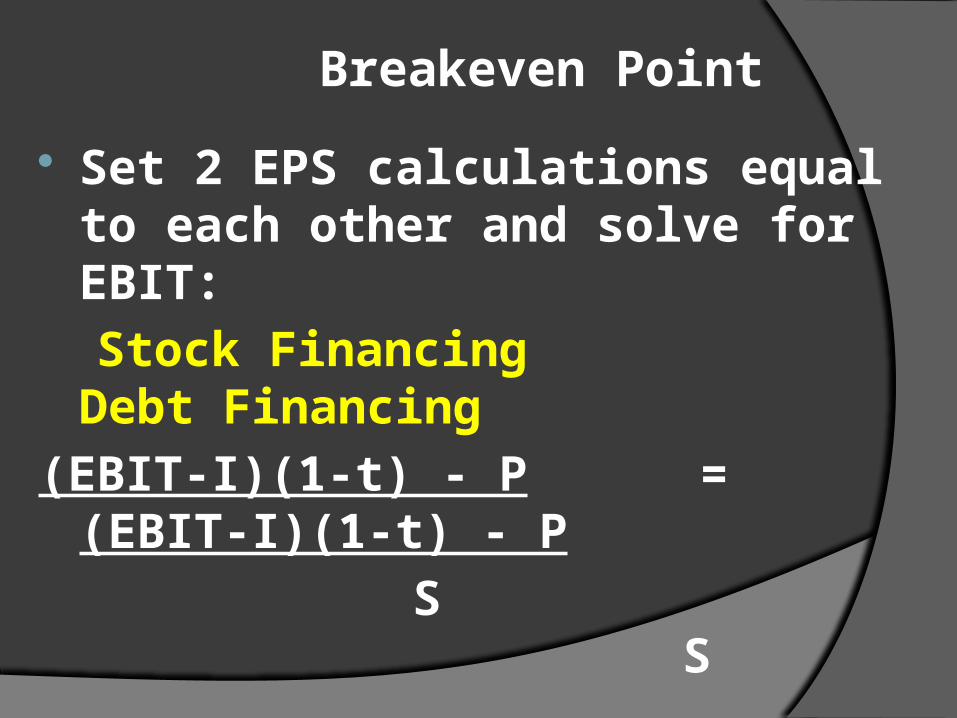

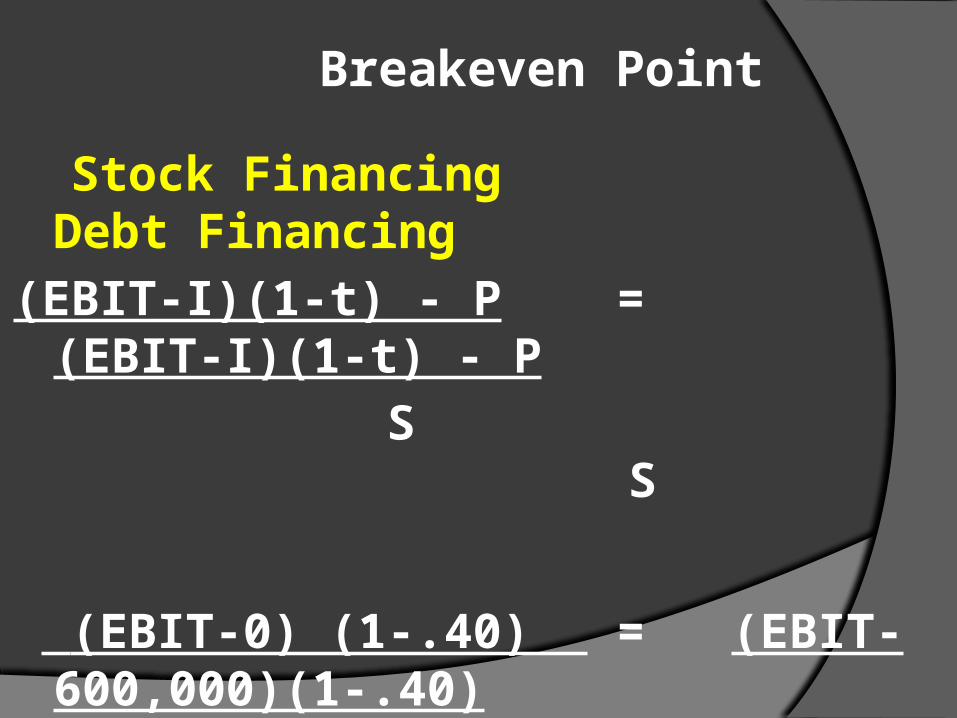

Breakeven Point

Set 2 EPS calculations equal to each other and solve for EBIT:

Stock Financing Debt Financing

(EBIT-I)(1-t) - P = (EBIT-I)(1-t) - P

S S

Breakeven Point

Stock Financing Debt Financing

(EBIT-I)(1-t) - P = (EBIT-I)(1-t) - P

S S

(EBIT-0) (1-.40) = (EBIT-600,000)(1-.40)

800,000+200,000 800,000

Breakeven Point

Stock Financing Debt Financing

.6 EBIT = .6 EBIT - 360,000

1 .8

.48 EBIT = .6 EBIT - 360,000

.12 EBIT = 360,000

EBIT = $3,000,000

Breakeven EBITEPS

EBIT 1m 2m 3m 4m

bond financing

stock financing

0

3

2

1

For EBIT up to 3 million,stock financing is best.

Breakeven EBITEPS

EBIT 1m 2m 3m 4m

bond financing

stock financing

0

3

2

1

For EBIT up to 3 million,stock financing is best.

For EBIT greaterThan 3 million,

debt financing isbest.

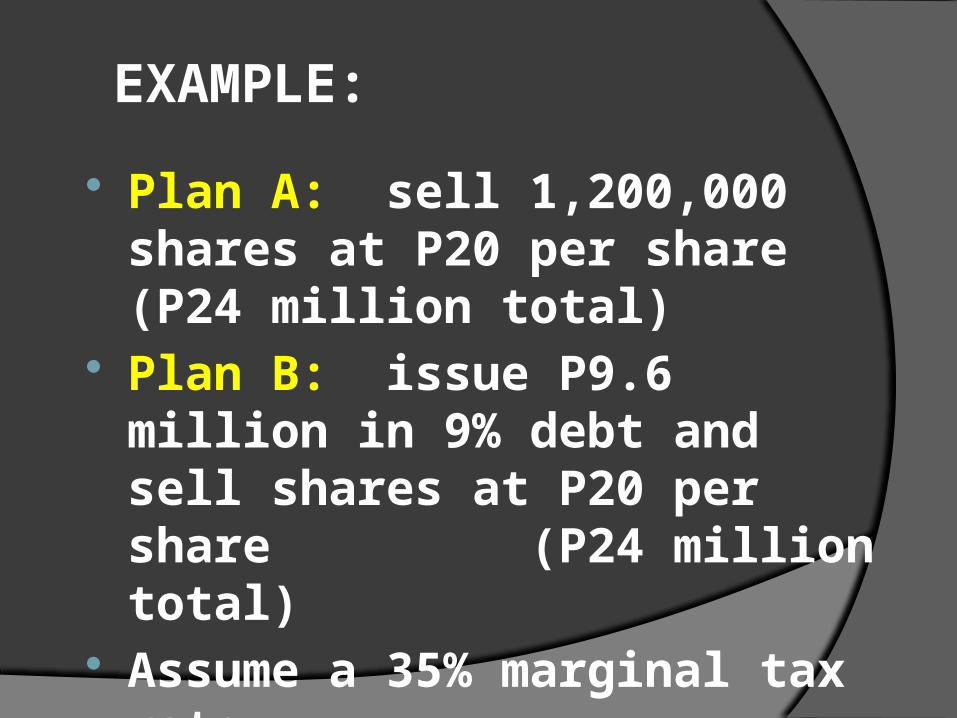

EXAMPLE:

Plan A: sell 1,200,000 shares at 10 per share (12 million total)

Plan B: issue 3.5 million in 9% debt and sell 850,000 shares at 10 per share (12 million total)

Assume a marginal tax rate of 50%.

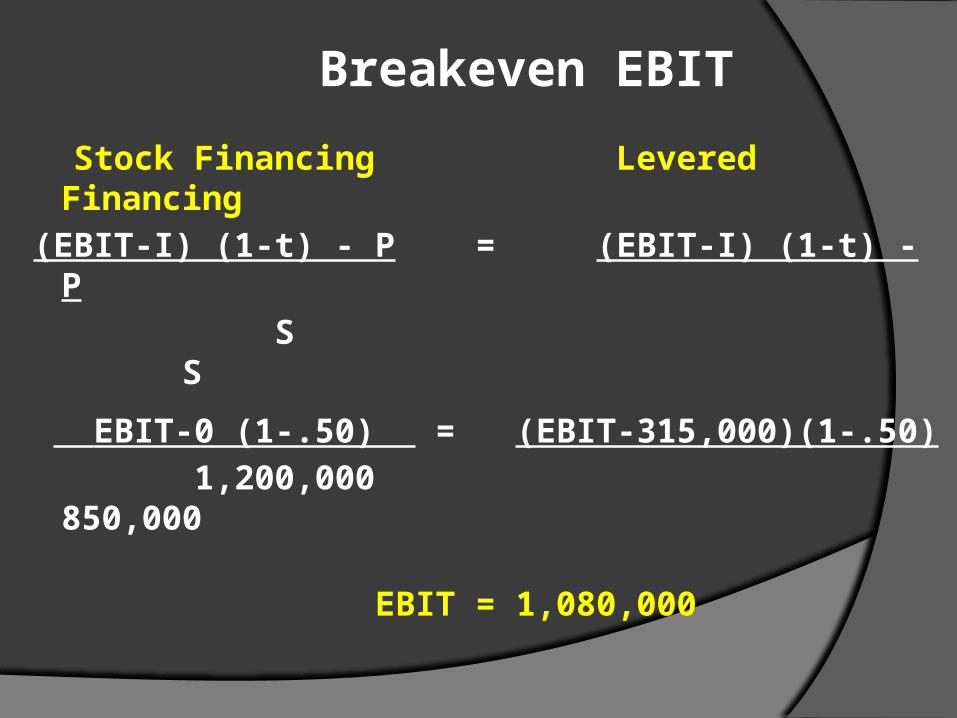

Breakeven EBIT

Stock Financing Levered Financing

(EBIT-I) (1-t) - P = (EBIT-I) (1-t) - P

S S

EBIT-0 (1-.50) = (EBIT-315,000)(1-.50)

1,200,000 850,000

EBIT = 1,080,000

Analytical Income Statement

Stock Levered

EBIT 1,080,000 1,080,000

I 0 (315,000)

EBT 1,080,000 765,000

Tax (540,000) (382,500)

NI 540,000 382,500

Shares 1,200,000 850,000

EPS .45 .45

levered financing

stock financing

EPS

EBITP.5m P1m P1.5m P2m

0

.65

.45

.25

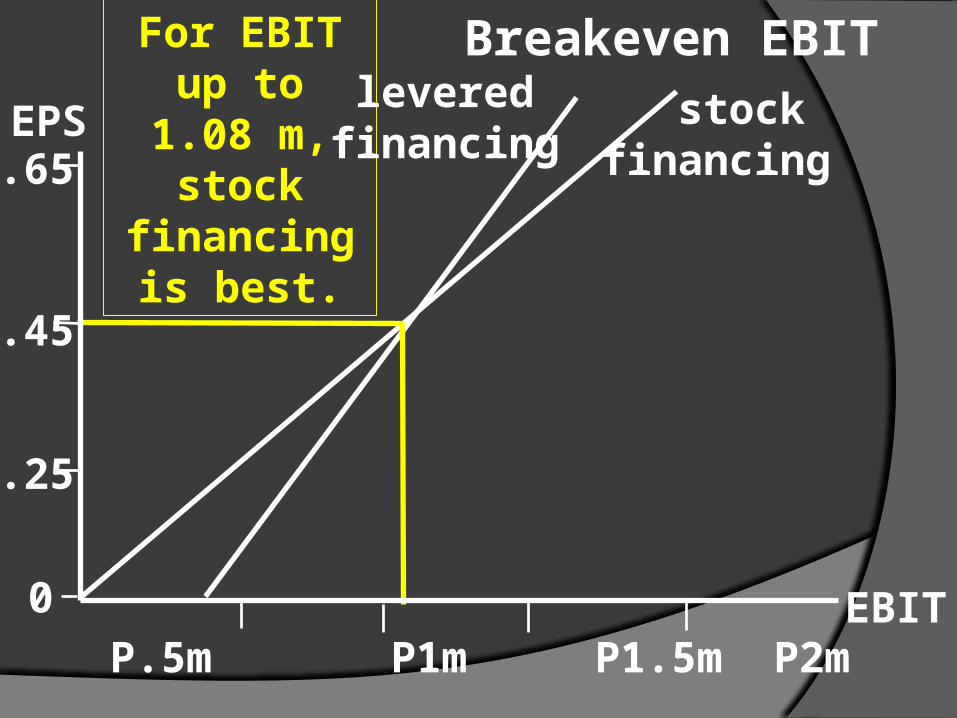

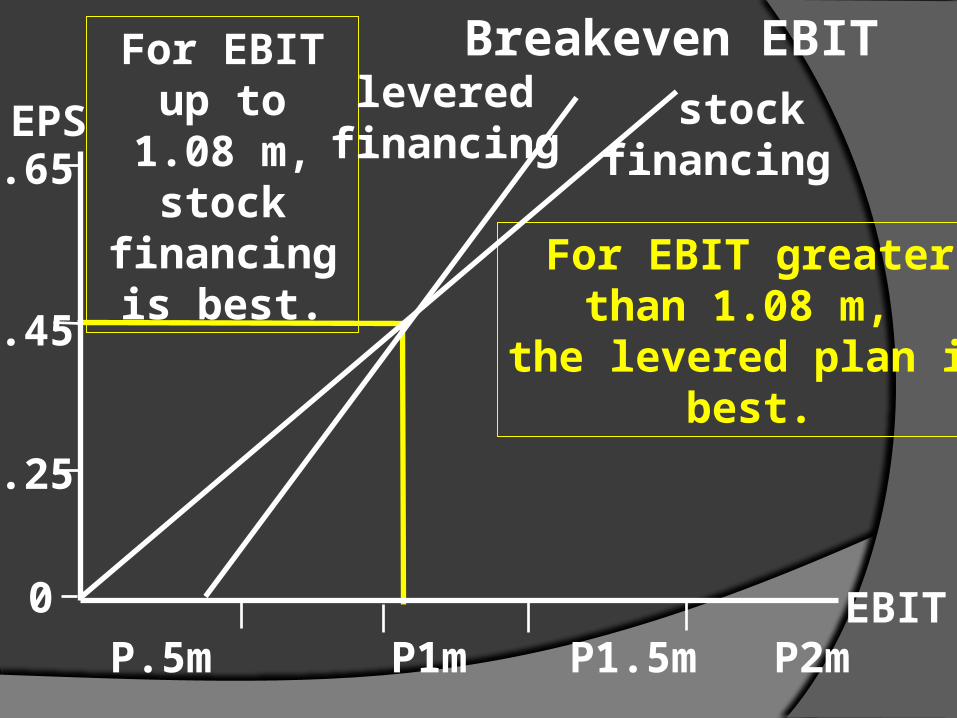

Breakeven EBIT

For EBIT up to 1.08 m,

stock financing is

best.

levered financing

stock financing

EPS

EBITP.5m P1m P1.5m P2m

0

.65

.45

.25

Breakeven EBIT

Breakeven EBITFor EBIT up to 1.08 m,

stock financing is

best. For EBIT greaterthan 1.08 m,

the levered plan isbest.

levered financing

stock financing

EPS

EBITP.5m P1m P1.5m P2m

0

.65

.45

.25

EXAMPLE:

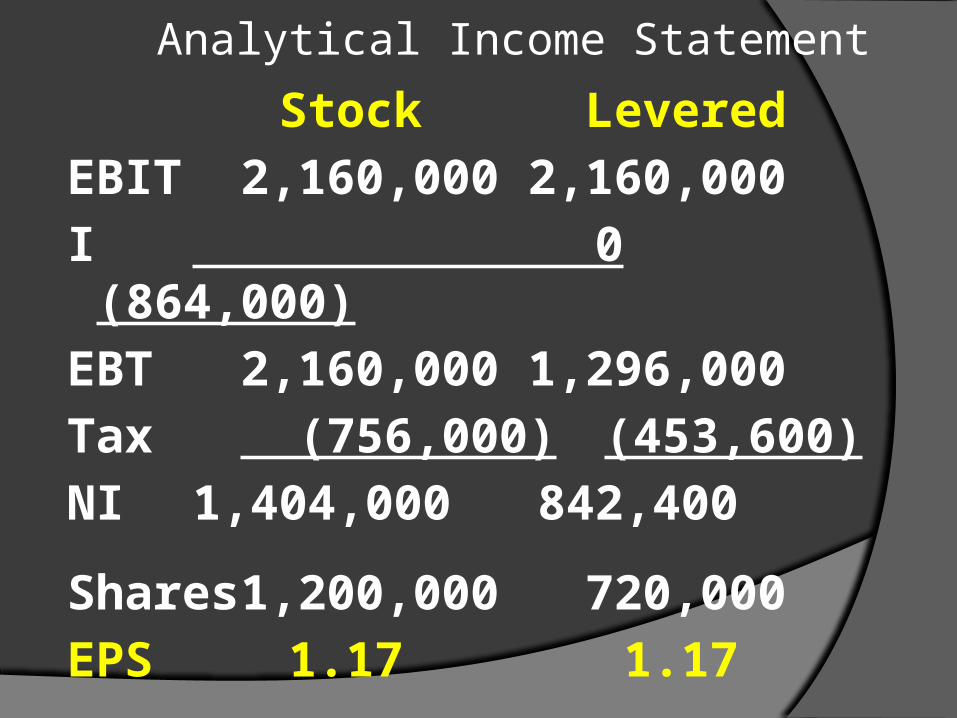

Plan A: sell 1,200,000 shares at P20 per share (P24 million total)

Plan B: issue P9.6 million in 9% debt and sell shares at P20 per share (P24 million total)

Assume a 35% marginal tax rate.

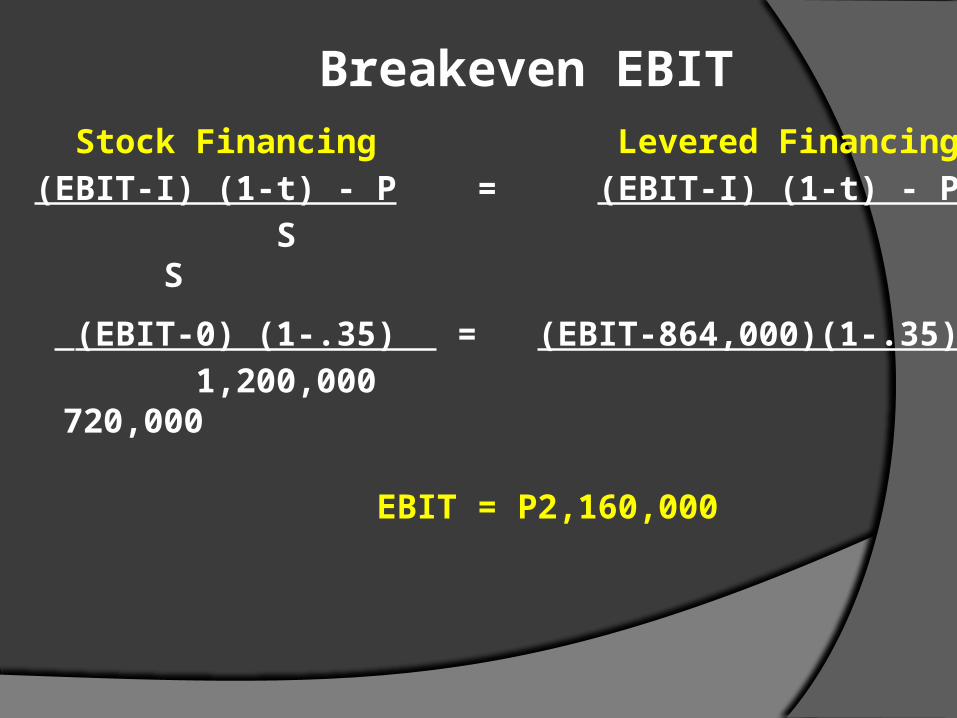

Breakeven EBIT

Stock Financing Levered Financing

(EBIT-I) (1-t) - P = (EBIT-I) (1-t) - P

S S

(EBIT-0) (1-.35) = (EBIT-864,000)(1-.35)

1,200,000 720,000

EBIT = P2,160,000

Analytical Income Statement Stock Levered

EBIT 2,160,000 2,160,000

I 0 (864,000)

EBT 2,160,000 1,296,000

Tax (756,000) (453,600)

NI 1,404,000 842,400

Shares 1,200,000 720,000

EPS 1.17 1.17

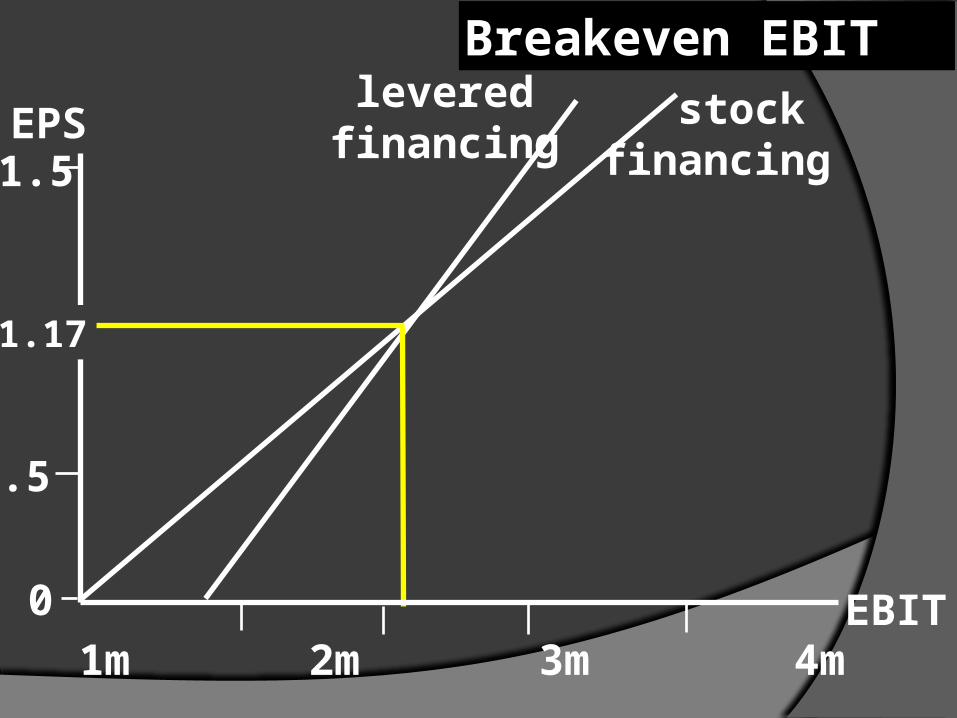

Breakeven EBITlevered

financingstock

financingEPS

EBIT 1m 2m 3m 4m

0

1.5

1.17

.5

Breakeven EBITlevered

financingstock

financingEPS

EBIT0

1.5

1.17

.5

For EBIT up to $2.16 m,

stock financing is

best.

1m 2m 3m 4m

Breakeven EBITlevered

financingstock

financingEPS

EBIT0

1.5

1.17

.5

For EBIT greaterthan $2.16 m,

the levered plan isbest.

For EBIT up to $2.16 m,

stock financing is

best.

1m 2m 3m 4m

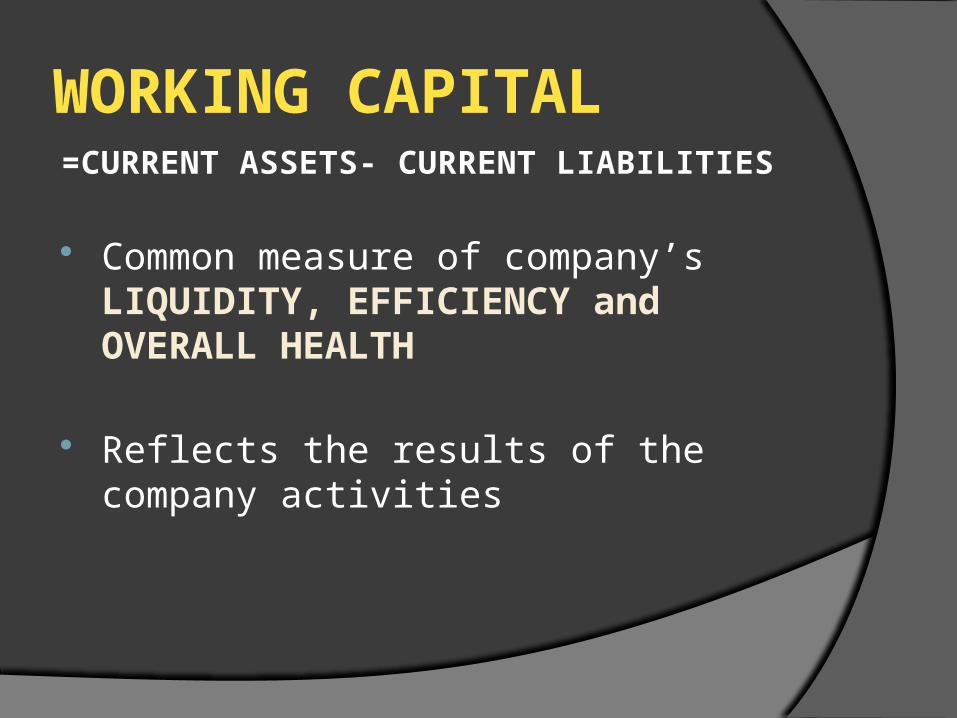

WORKING CAPITAL=CURRENT ASSETS- CURRENT LIABILITIES

Common measure of company’s LIQUIDITY, EFFICIENCY and OVERALL HEALTH

Reflects the results of the company activities

WORKING CAPITAL MANAGEMENT

the administration and control of the company’s working capital.

PRIMARY OBJECTIVE: to achieve a balance between return(profitability) and risk

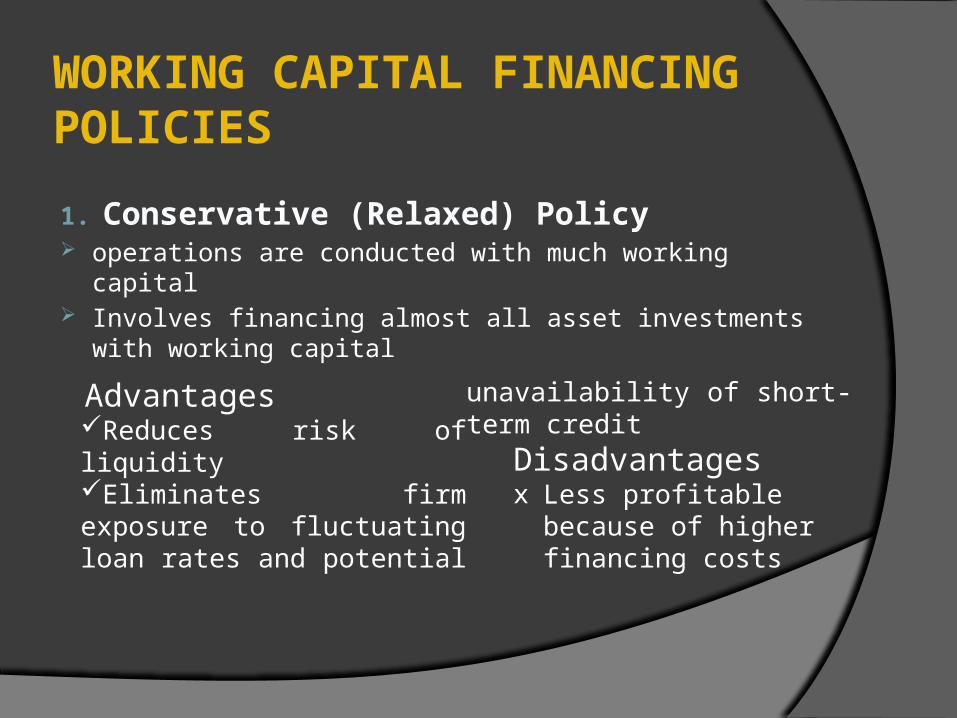

WORKING CAPITAL FINANCING POLICIES

1. Conservative (Relaxed) Policy operations are conducted with much working capital Involves financing almost all asset investments with

working capital

AdvantagesReduces risk of liquidityEliminates firm exposure to fluctuating loan rates and potential unavailability of short-term credit

Disadvantagesx Less profitable because

of higher financing costs

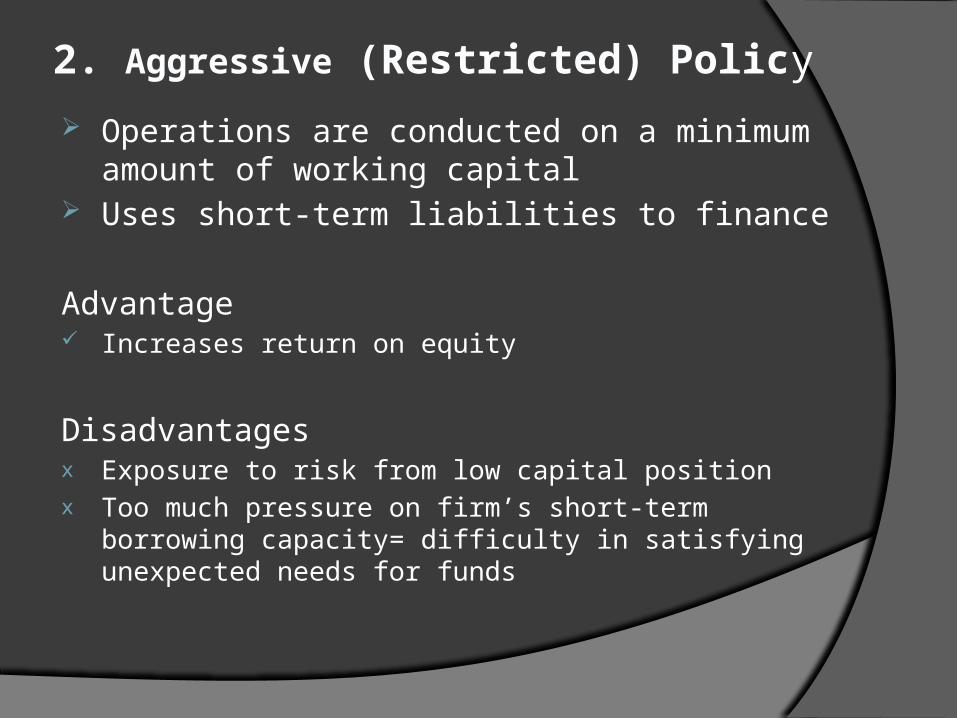

2. Aggressive (Restricted) Policy Operations are conducted on a minimum amount of

working capital Uses short-term liabilities to finance

Advantage Increases return on equity

Disadvantagesx Exposure to risk from low capital positionx Too much pressure on firm’s short-term borrowing capacity=

difficulty in satisfying unexpected needs for funds

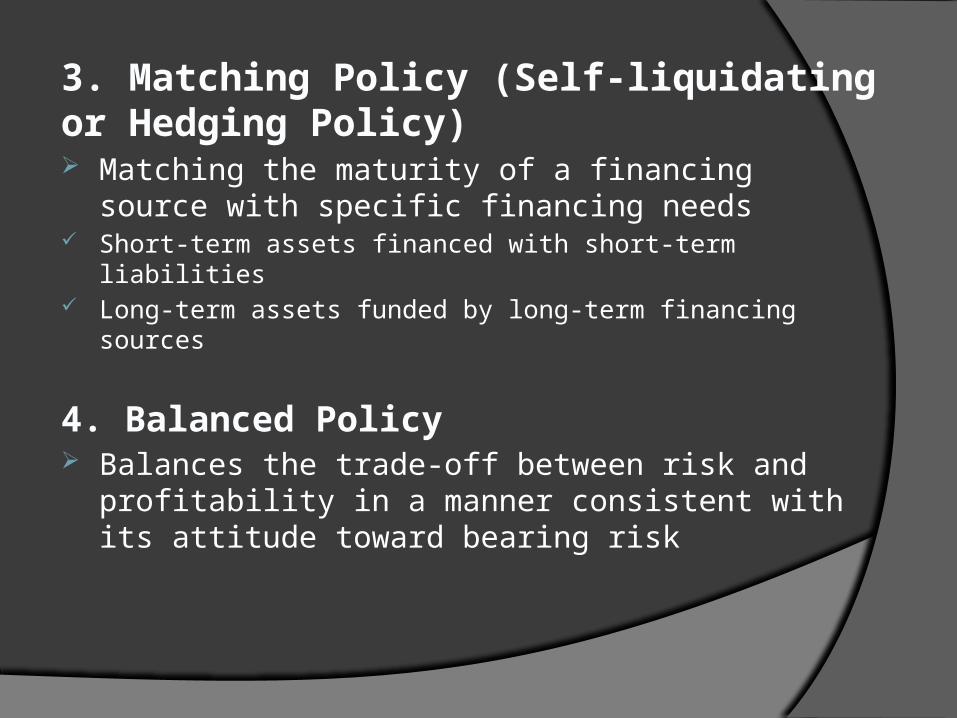

3. Matching Policy (Self-liquidating or Hedging Policy) Matching the maturity of a financing source with

specific financing needs Short-term assets financed with short-term liabilities Long-term assets funded by long-term financing sources

4. Balanced Policy Balances the trade-off between risk and profitability in

a manner consistent with its attitude toward bearing risk

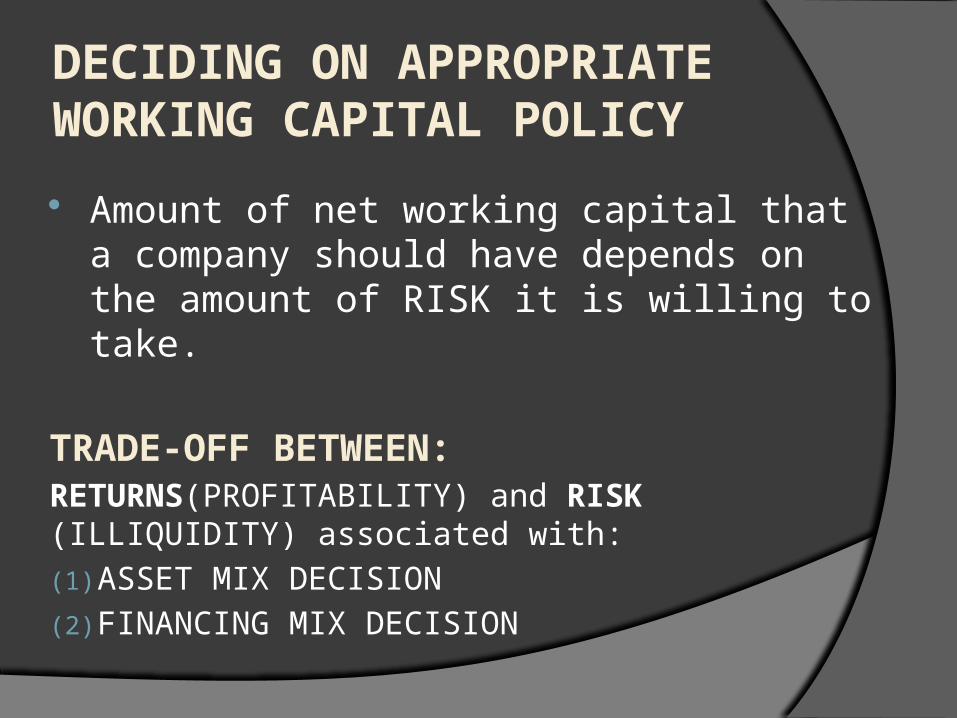

DECIDING ON APPROPRIATE WORKING CAPITAL POLICY

Amount of net working capital that a company should have depends on the amount of RISK it is willing to take.

TRADE-OFF BETWEEN:RETURNS(PROFITABILITY) and RISK (ILLIQUIDITY) associated with:

(1) ASSET MIX DECISION

(2) FINANCING MIX DECISION

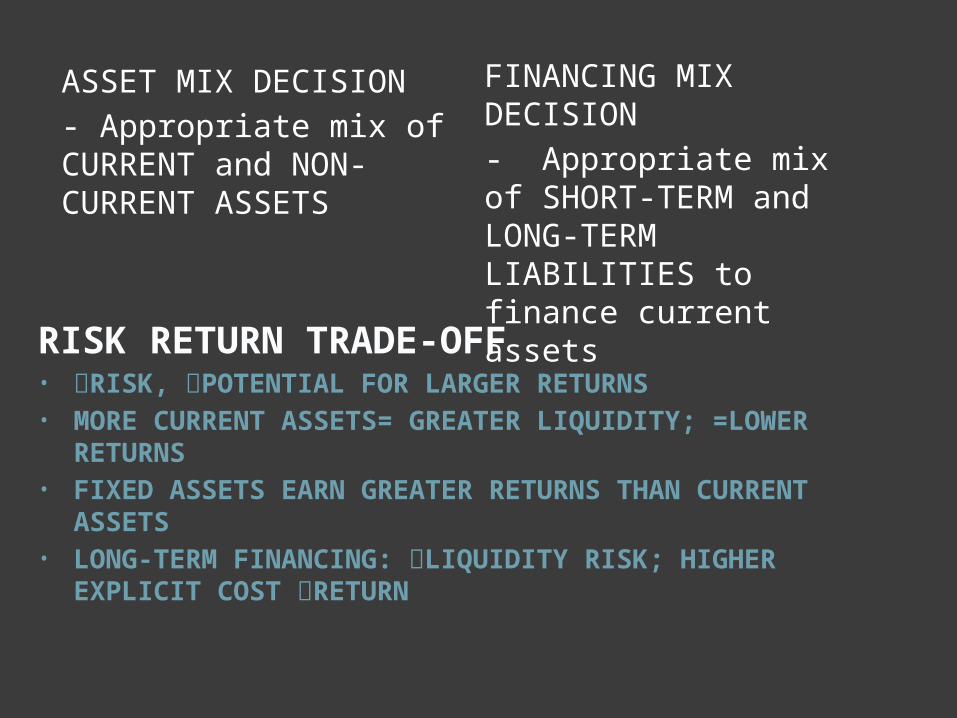

RISK RETURN TRADE-OFF• RISK, POTENTIAL FOR LARGER RETURNS• MORE CURRENT ASSETS= GREATER LIQUIDITY; =LOWER

RETURNS• FIXED ASSETS EARN GREATER RETURNS THAN CURRENT

ASSETS• LONG-TERM FINANCING: LIQUIDITY RISK; HIGHER EXPLICIT

COST RETURN

ASSET MIX DECISION

- Appropriate mix of CURRENT and NON-CURRENT ASSETS

FINANCING MIX DECISION

- Appropriate mix of SHORT-TERM and LONG-TERM LIABILITIES to finance current assets

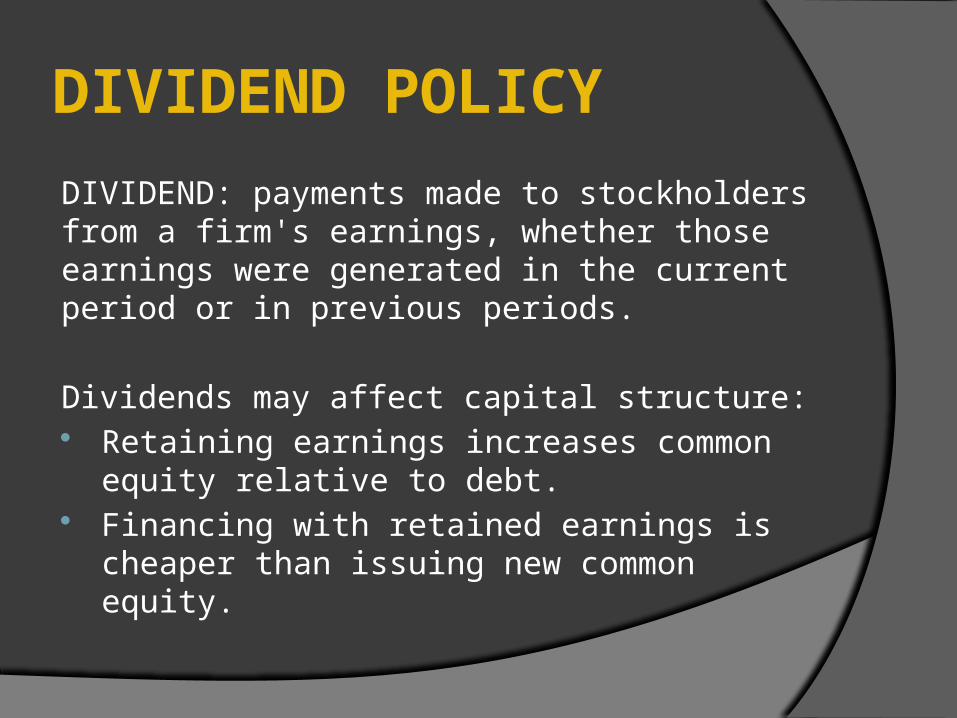

DIVIDEND POLICY

DIVIDEND: payments made to stockholders from a firm's earnings, whether those earnings were generated in the current period or in previous periods.

Dividends may affect capital structure: Retaining earnings increases common equity

relative to debt. Financing with retained earnings is cheaper than

issuing new common equity.

POLICY TYPES

Constant Dividend Payout Ratio Constant Currency Dividend Policy Residual Dividend Policy

Constant Currency (Dollar) Dividend Policy

firm pays out the same dollar amount per outstanding common share each period, say $1.25.

In practice this is by far the most common policy observed for Canadian, publicly-traded, companies that pay dividends.

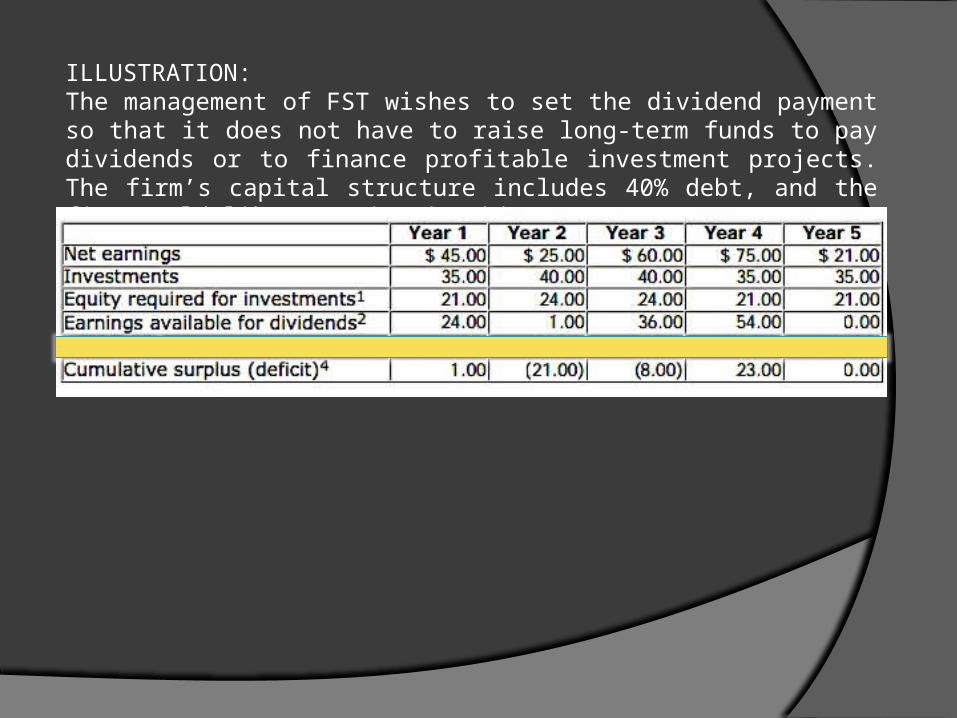

ILLUSTRATION: The management of FST wishes to set the dividend payment so that it does not have to raise long-term funds to pay dividends or to finance profitable investment projects. The firm’s capital structure includes 40% debt, and the firm would like to maintain this structure.

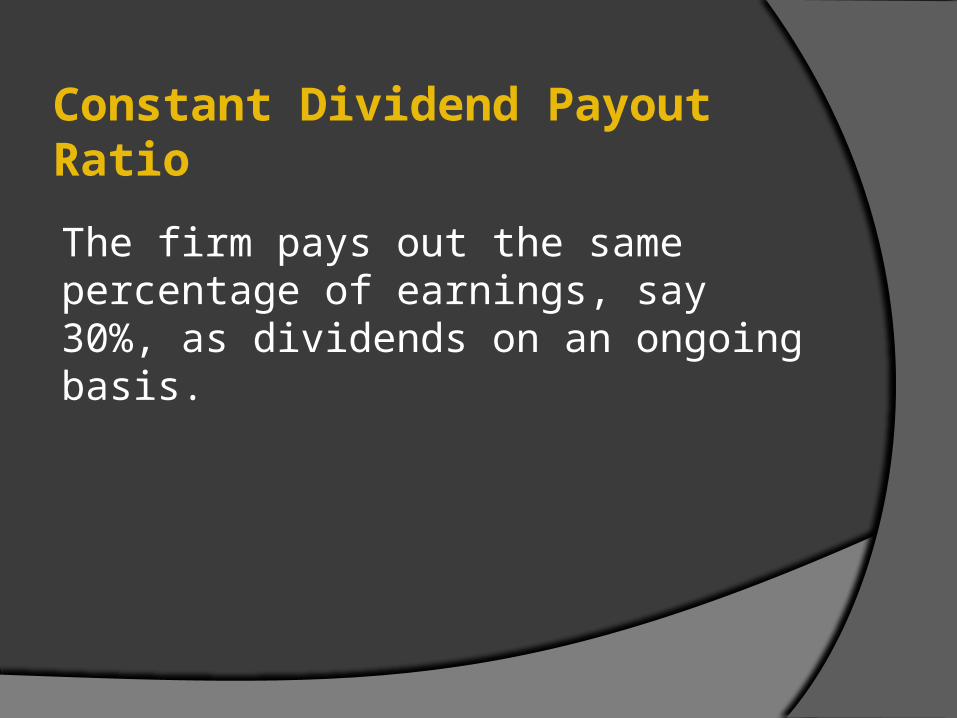

Constant Dividend Payout Ratio

The firm pays out the same percentage of earnings, say 30%, as dividends on an ongoing basis.

Illustration:

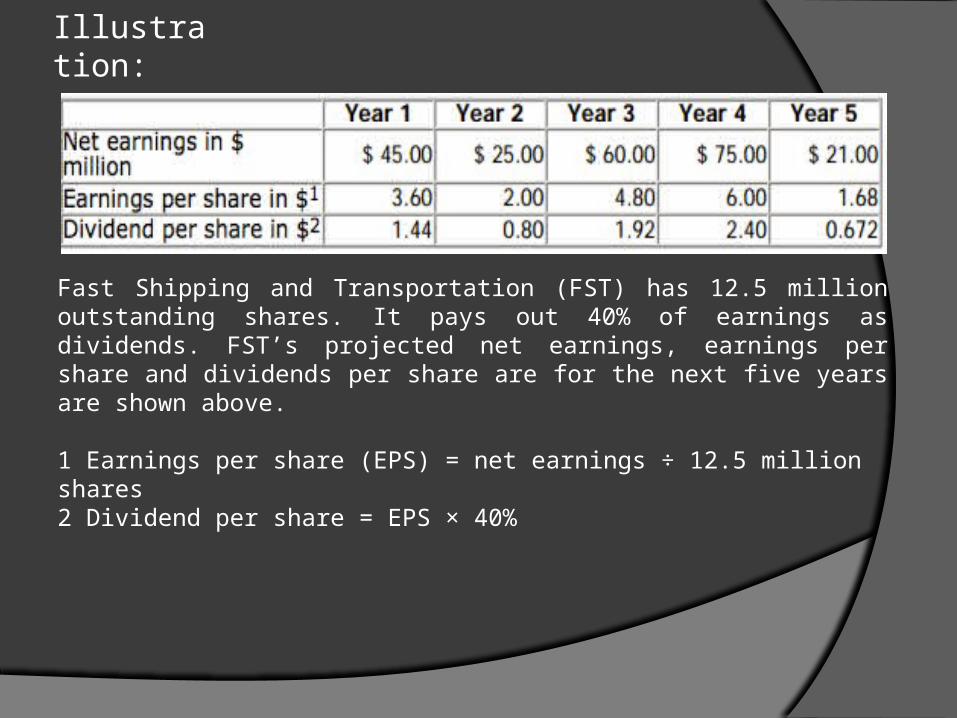

Fast Shipping and Transportation (FST) has 12.5 million outstanding shares. It pays out 40% of earnings as dividends. FST’s projected net earnings, earnings per share and dividends per share are for the next five years are shown above.

1 Earnings per share (EPS) = net earnings ÷ 12.5 million shares2 Dividend per share = EPS × 40%

Residual Dividend Policy

firm pays out dividends equal to its free cash flow.

cash flow from operations -capital expendituresFREE CASH FLOW

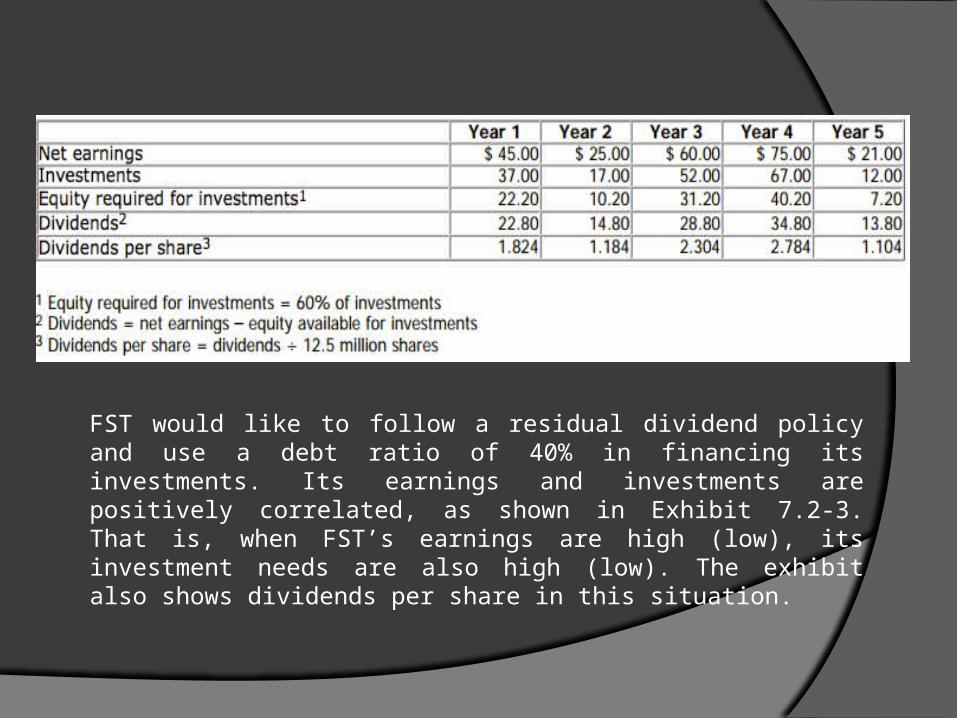

FST would like to follow a residual dividend policy and use a debt ratio of 40% in financing its investments. Its earnings and investments are positively correlated, as shown in Exhibit 7.2-3. That is, when FST’s earnings are high (low), its investment needs are also high (low). The exhibit also shows dividends per share in this situation.

MANAGEMENT OF CURRENT ASSETS

• Motives for Holding Cash• Speeding Up Cash Receipts• S-l-o-w-i-n-g D-o-w-n

Cash Payouts• Electronic Commerce

Cash and Marketable Securities Management

• Outsourcing• Cash Balances to Maintain• Investment in Marketable

Securities

Cash and Marketable Securities Management

Transactions Motive – to meet payments arising in the ordinary course of business

Speculative Motive – to take advantage of temporary opportunities

Precautionary Motive – to maintain a cushion or buffer to meet unexpected cash needs

Motives for Holding Cash

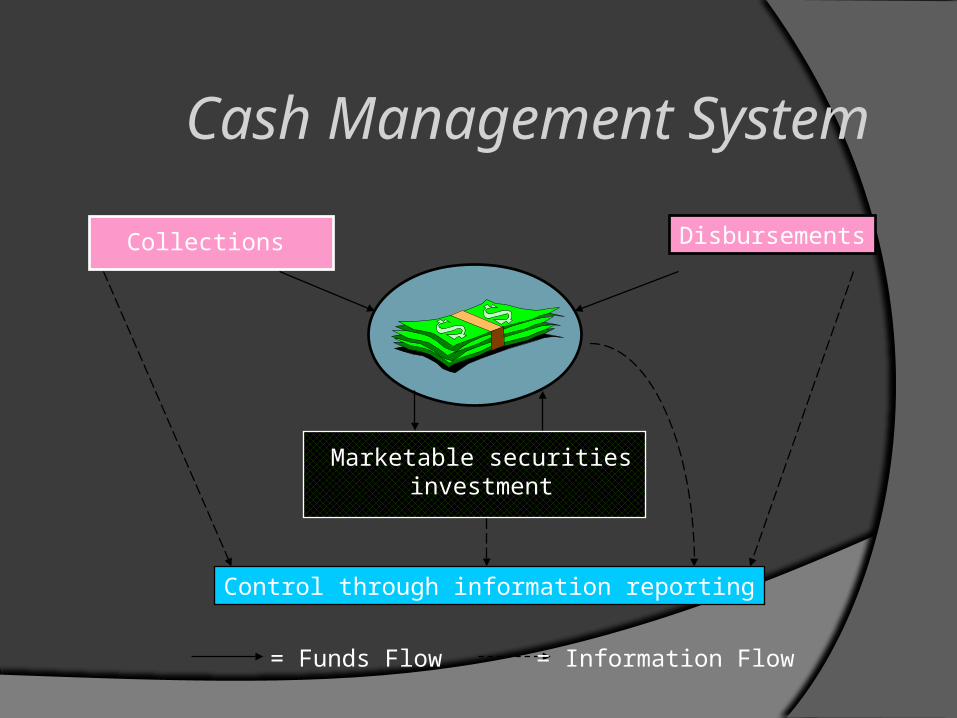

Collections Disbursements

Marketable securitiesinvestment

Control through information reporting

= Funds Flow = Information Flow

Cash Management System

• Expedite preparing and mailing the invoice• Accelerate the mailing of payments from

customers• Reduce the time during which payments

received by the firm remain uncollected

Collections

Speeding Up Cash Receipts

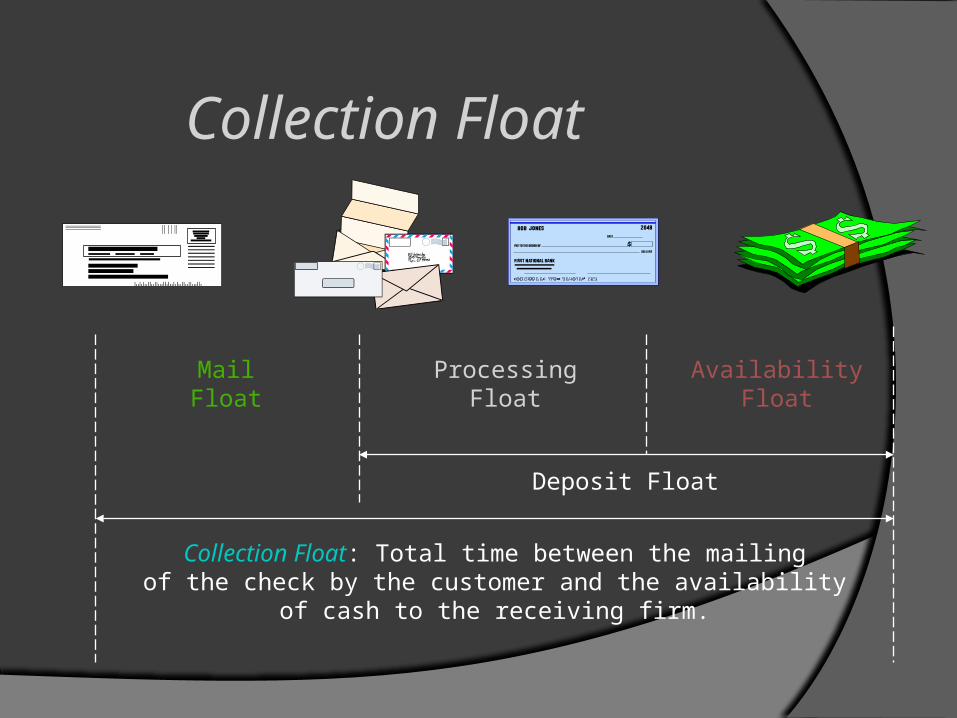

Collection Float: Total time between the mailingof the check by the customer and the availability

of cash to the receiving firm.

ProcessingFloat

AvailabilityFloat

MailFloat

Deposit Float

Collection Float

Mail Float: Time the check is in the mail.

Customer mails check

Firmreceives check

Mail Float

Processing Float: Time it takes a companyto process the check internally.

Firmdeposits check

Firmreceives check

Processing Float

Availability Float: Time consumed in clearingthe check through the banking system.

Firmdeposits check

Firm’s bankaccount credited

Availability Float

Deposit Float: Time during which the check received by the firm remains uncollected funds.

Processing Float Availability Float

Deposit Float

Accelerate preparation and mailing of invoices

• computerized billing• invoices included with shipment• invoices are faxed• advance payment requests• preauthorized debits

Earlier Billing

Preauthorized debit

The transfer of funds from a payor’s bank account on a specified date to the payee’s

bank account; the transfer is initiated by the payee with the payor’s advance authorization.

Preauthorized Payments

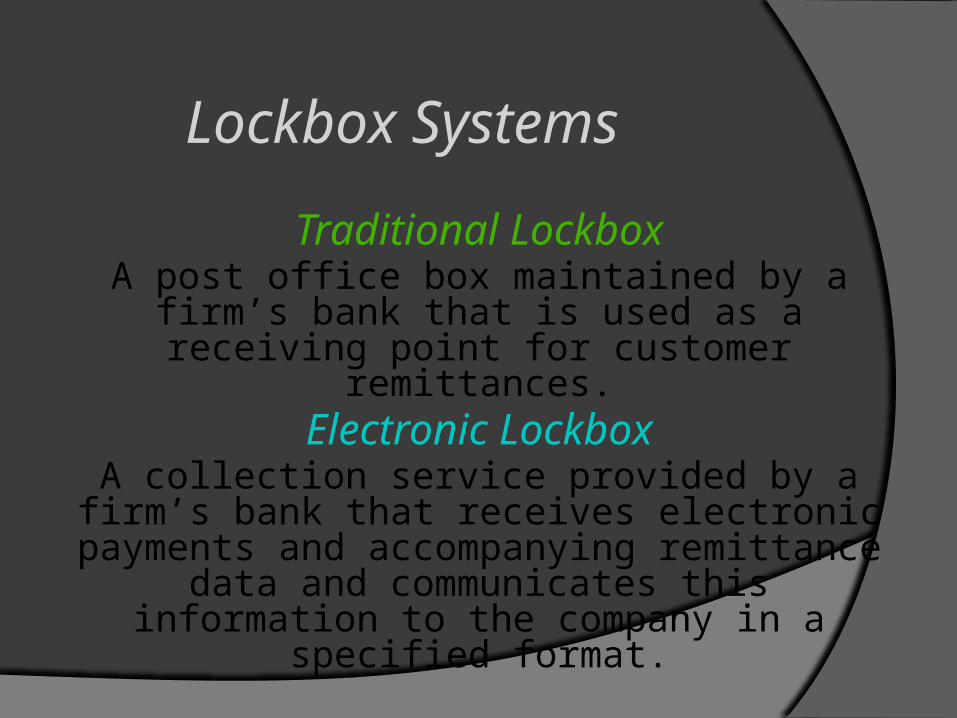

Traditional LockboxA post office box maintained by a firm’s bank that

is used as a receiving point for customer remittances.

Electronic LockboxA collection service provided by a firm’s bank that receives electronic payments and accompanying

remittance data and communicates this information to the company in a specified format.

Lockbox Systems

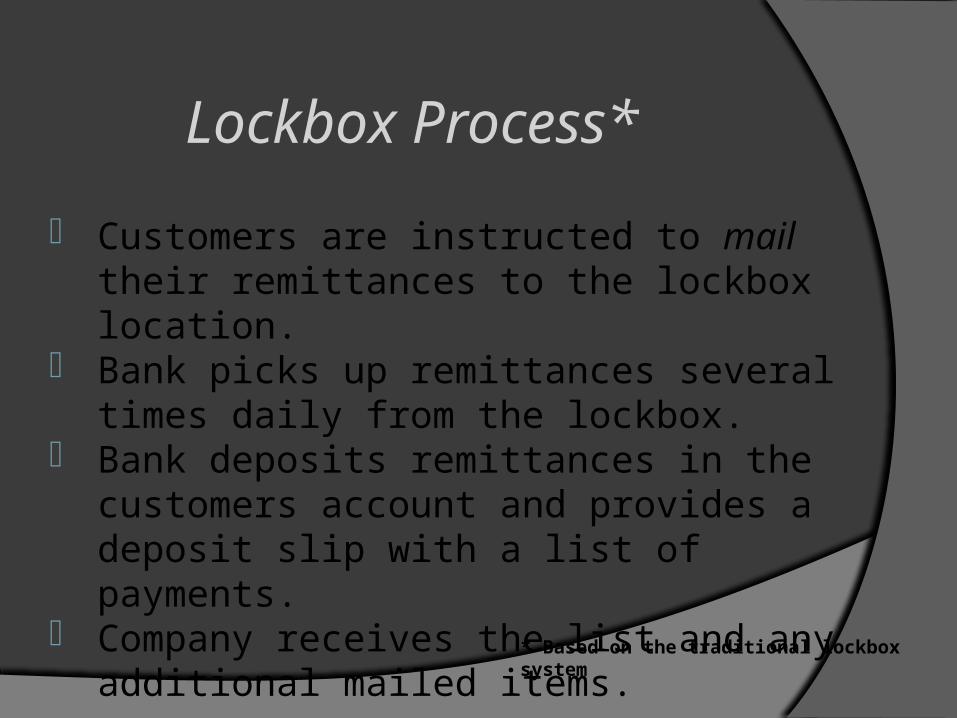

• Customers are instructed to mail their remittances to the lockbox location.

• Bank picks up remittances several times daily from the lockbox.

• Bank deposits remittances in the customers account and provides a deposit slip with a list of payments.

• Company receives the list and any additional mailed items.

* Based on the traditional lockbox system

Lockbox Process*

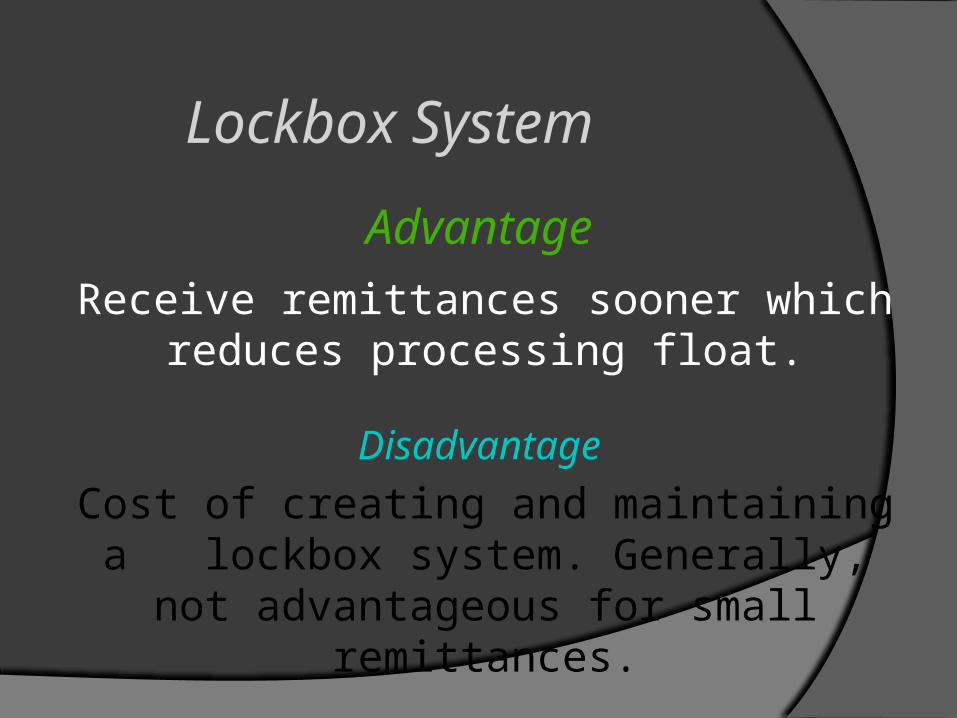

Disadvantage

Cost of creating and maintaining a lockbox system. Generally, not

advantageous for small remittances.

Advantage

Receive remittances sooner which reduces processing float.

Lockbox System

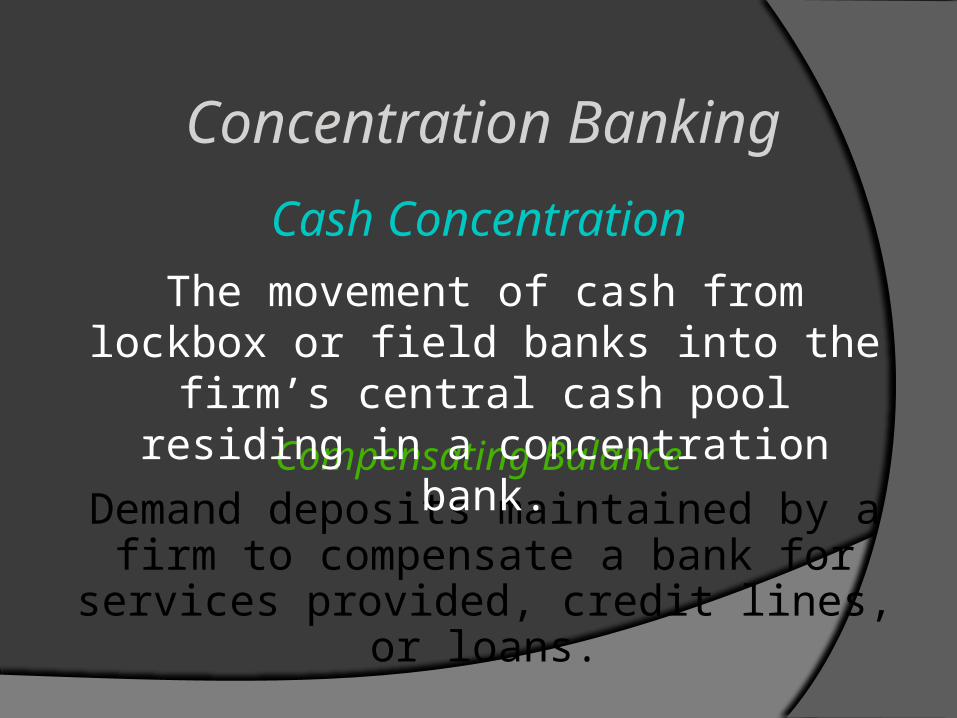

Compensating BalanceDemand deposits maintained by a firm to compensate a bank for services provided,

credit lines, or loans.

Cash Concentration

The movement of cash from lockbox or field banks into the firm’s central cash pool

residing in a concentration bank.

Concentration Banking

Reduces availability float associated with check clearing.

Accounts Receivable Conversion

A process by which paper checks are converted into ACH debits at lockboxes or

other collection sites.

So what is the Benefit of ARCs?

Collections Improvements

• Improves control over inflows and outflows of corporate cash.

• Reduces idle cash balances to a minimum.

• Allows for more effective investments by pooling excess cash balances.

Moving cash balances to a central location:

Concentration Banking

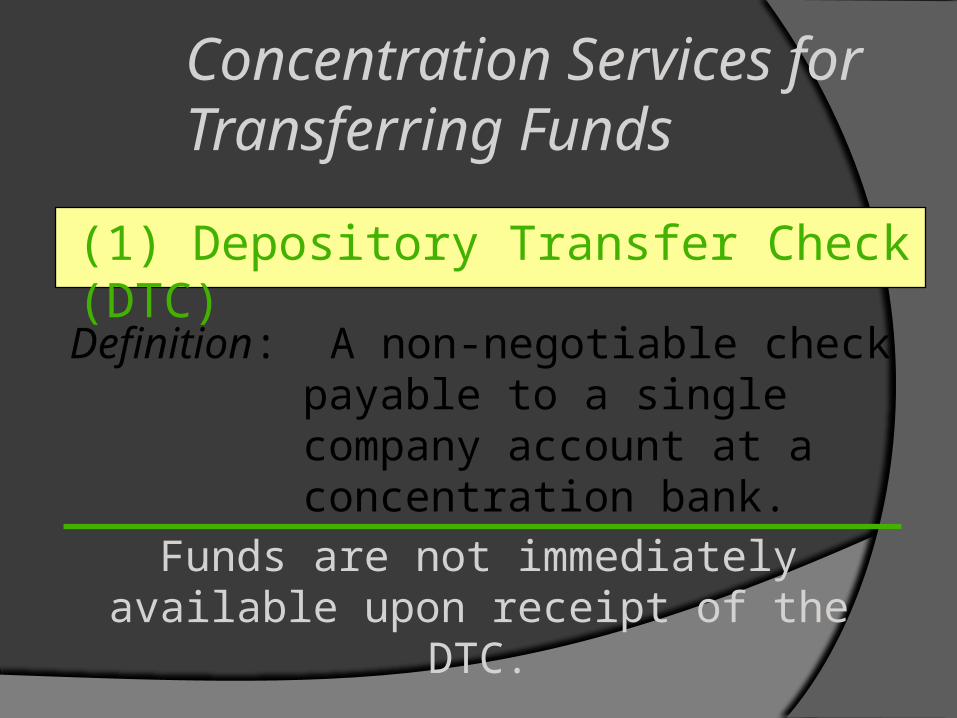

Definition: A non-negotiable check payable to a single company account at a concentration bank.

Funds are not immediately available upon receipt of the DTC.

(1) Depository Transfer Check (DTC)

Concentration Services for Transferring Funds

Definition: An electronic version of the depository transfer check (DTC).

(1) Electronic check image version of the DTC.(2) Cost is not significant and is replacing DTC.

(2) Automated Clearinghouse (ACH) Electronic Transfer

Concentration Services for Transferring Funds

Definition: A generic term for electronic funds transfer using a two-way communications system, like Fedwire.

Funds are available upon receipt of the wire transfer. Much more expensive.

(3) Wire Transfer

Concentration Services for Transferring Funds

• “Playing the Float”

• Control of Disbursements• Payable through Draft (PTD)• Payroll and Dividend

Disbursements• Zero Balance Account (ZBA)

• Remote and Controlled Disbursing

S-l-o-w-i-n-g D-o-w-n Cash Payouts

You write a check today, which is subtracted from your calculation of the account balance. The check has not cleared, which creates float. You can potentially earn

interest on money that you have “spent.”

Net Float -- The dollar difference between the balance shown in a firm’s (or individual’s)

checkbook balance and the balance on the bank’s books.

“Playing the Float”

Solution:Centralize payables into a single (smaller

number of) account(s). This provides better control of the disbursement process.

Firms should be able to:

1. shift funds quickly to banks from which disbursements are made.

2. generate daily detailed information on balances, receipts, and disbursements.

Control of Disbursements

• Delays the time to have funds on deposit to cover the draft.

• Some suppliers prefer checks.• Banks will impose a higher service charge

due to the additional handling involved.

Payable Through Draft (PTD):A check-like instrument that is drawn against the

payor and not against a bank as is a check. After a PTD is presented to a bank, the payor gets to decide

whether to honor or refuse payment.

Methods of Managing Disbursements

• Many times a separate account is set up to handle each of these types of disbursements.

• A distribution schedule is projected based on past experiences. [See the next slide]

• Funds are deposited based on expected needs.• Minimizes excessive cash balances.

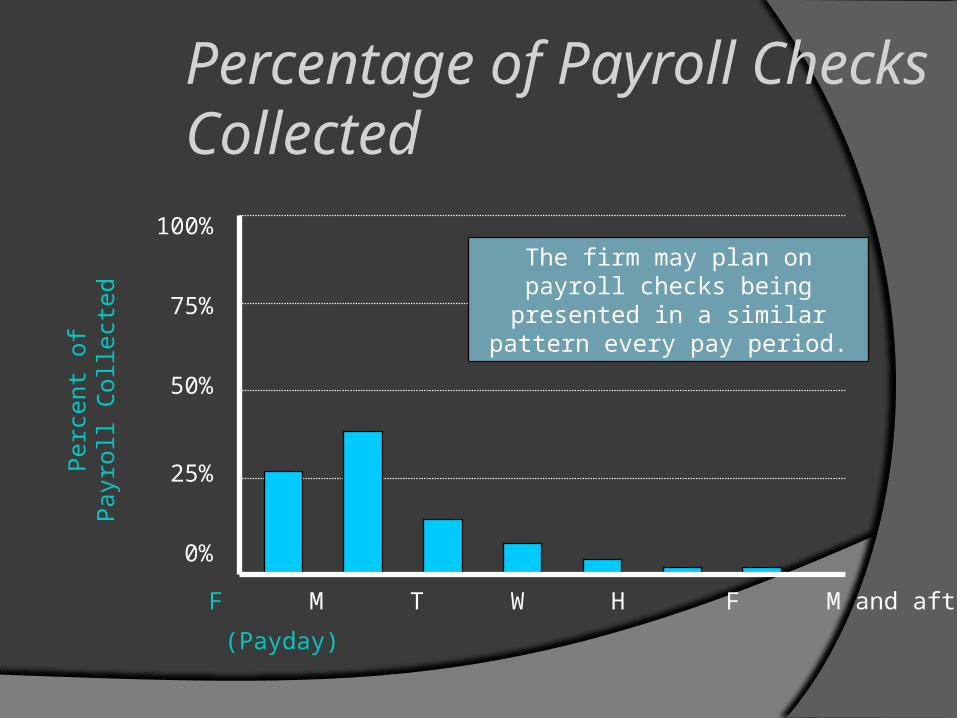

Payroll and Dividend DisbursementsThe firm attempts to determine when payroll and dividend checks will be presented for collection.

Methods of Managing Disbursements

F M T W H F M and after

(Payday)

Per

cent

of

Pay

roll

Col

lect

ed

100%

75%

50%

25%

0%

The firm may plan onpayroll checks beingpresented in a similar

pattern every pay period.

Percentage of Payroll Checks Collected

• Eliminates the need to accurately estimate each disbursement account.

• Only need to forecast overall cash needs.

Zero Balance Account (ZBA):A corporate checking account in which a zero balance is maintained. The account requires a

master (parent) account from which funds are drawn to cover negative balances or to which excess

balances are sent.

Methods of Managing Disbursements

Example: A Vermont business pays a Maine supplier with a check drawn on a bank in Montana.

This may stress supplier relations, and raises ethical issues.

Remote Disbursement – A system in which the firm directs checks to be drawn on a bank that is geographically remote from its customer so as to

maximize check-clearing time.

This maximizes disbursement float.

Remote and Controlled Disbursing

Late check presentments are minimal, which allows more accurate predicting of disbursements on a day-

to-day basis.

Controlled Disbursement – A system in which the firm directs checks to be drawn on a bank (or branch bank) that is able to give early or mid-morning notification of the total dollar amount of checks that will be presented

against its account that day.

Remote and Controlled Disbursing

Messaging systems can be:

1. Unstructured – utilize technologies such as faxes and e-mails

2. Structured – utilize technologies such as electronic data interchange (EDI).

Electronic Commerce – The exchange of business information in an electronic (non-paper) format, including over the Internet.

Electronic Commerce

Electronic Data Interchange – The movement of business data electronically in a structured,

computer-readable format.

EDIElectronic Funds Transfer (EFT)

Financial EDI (FEDI)

Electronic Data Interchange (EDI)

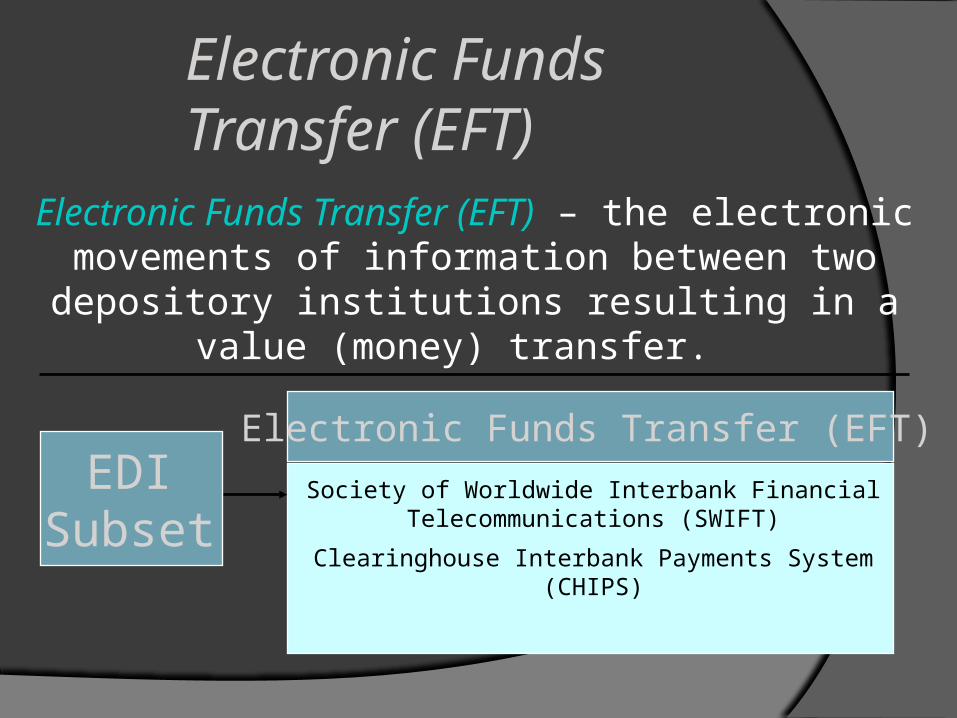

Electronic Funds Transfer (EFT) – the electronic movements of information between two depository institutions resulting in a value (money) transfer.

EDISubset

Electronic Funds Transfer (EFT)

Society of Worldwide Interbank Financial Telecommunications (SWIFT)

Clearinghouse Interbank Payments System (CHIPS)

Electronic Funds Transfer (EFT)

EFT Regulation

In January 1999, a regulation that required ALL federal government payments be made electronically.* This:

• provides more security than paper checks and• is cheaper to process for the government.

* Except tax refunds and special waiver situations

Electronic Funds Transfer (EFT)

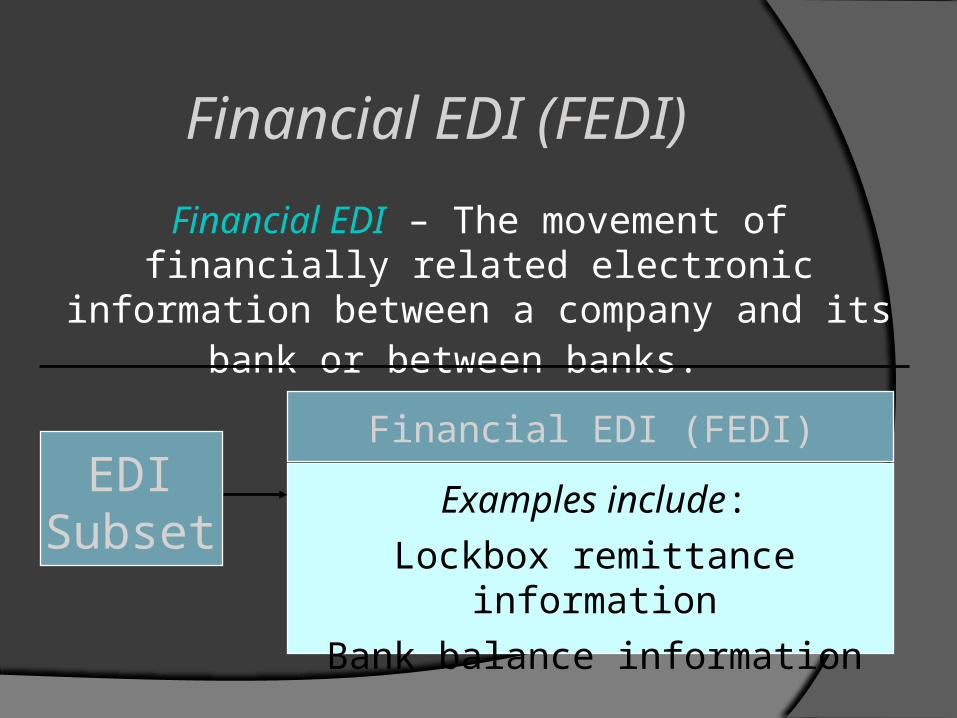

Financial EDI – The movement of financially related electronic information between a company and its

bank or between banks.

Financial EDI (FEDI)

Examples include:

Lockbox remittance information

Bank balance information

EDISubset

Financial EDI (FEDI)

Costs• Computer hardware and

software expenditures• Increased training costs to

implement and utilize an EDI system

• Additional expenses to convince suppliers and customers to use the electronic system

• Loss of float

Benefits• Information and payments

move faster and with greater reliability

• Improved cash forecasting and cash management

• Customers receive faster and more reliable service

• Reduction in mail, paper, and document storage costs

Costs and Benefits of EDI

1. Reducing and controlling operating costs 2. Improve company focus (close 2nd)3. Freeing resources for other purposes

Outsourcing – Subcontracting a certain business operation to an outside firm,

instead of doing it “in-house.”

Why might a firm outsource?*

Outsourcing

Business Process Outsourcing (BPO)

A form of outsourcing in which the entire business process is handed over to a third-

party service provider• Entire function such as accounting might be handed over to the BPO• Typically found in low labor cost countries• Many are owned by large multinationals

Outsourcing

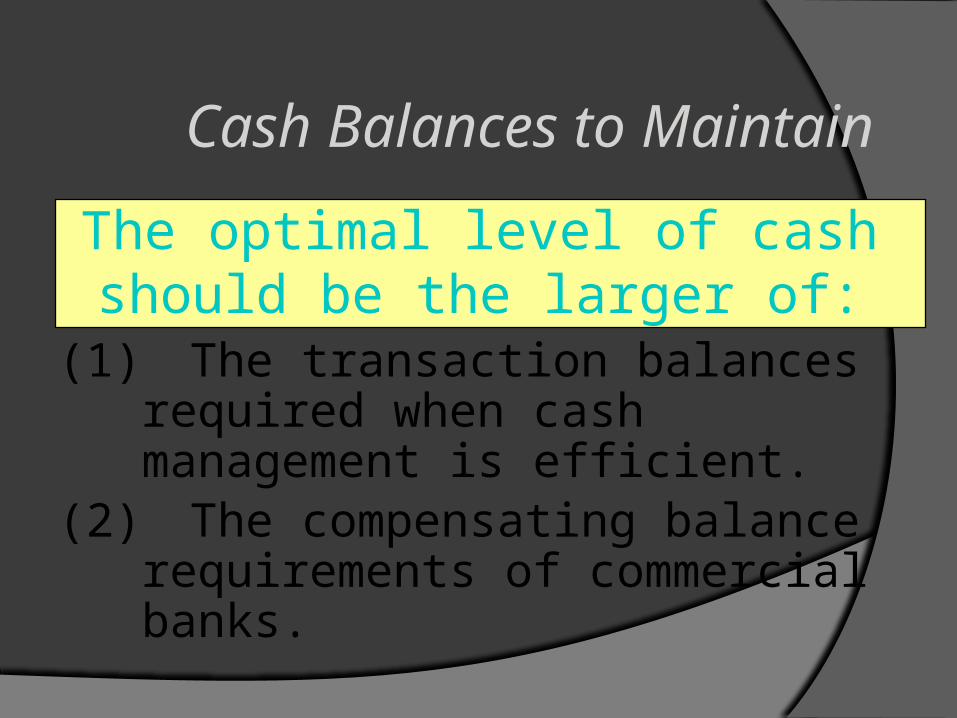

The optimal level of cash should be the larger of:

(1) The transaction balances required when cash management is efficient.

(2) The compensating balance requirements of commercial banks.

Cash Balances to Maintain

Note regarding the management of marketable securities.

Marketable Securities are shown on the balance sheet as “Short-term Investments”

Investment in Marketable Securities

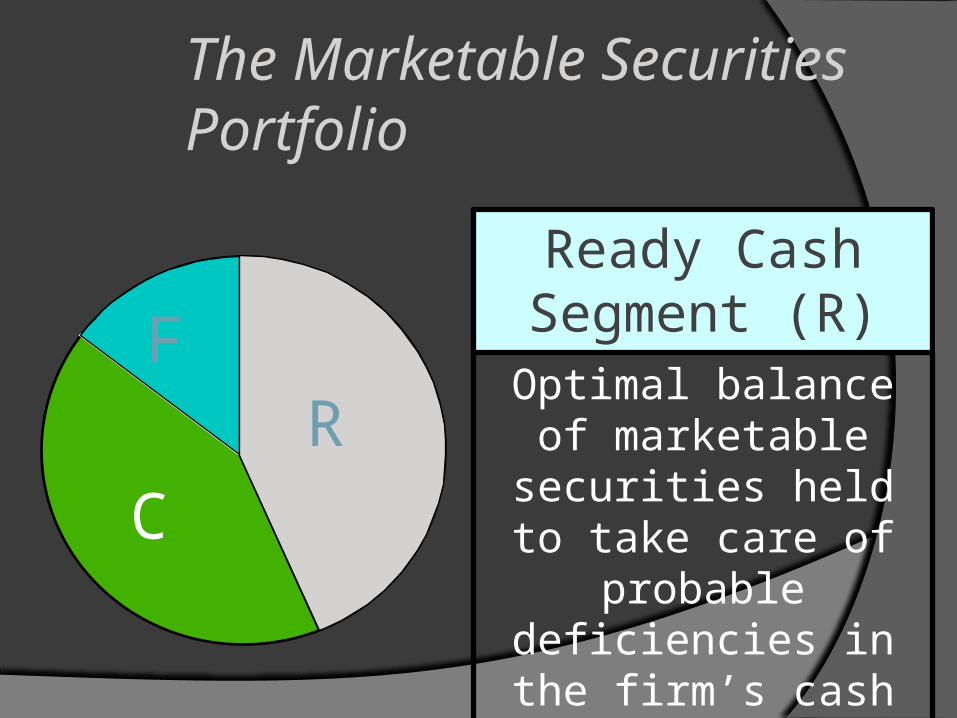

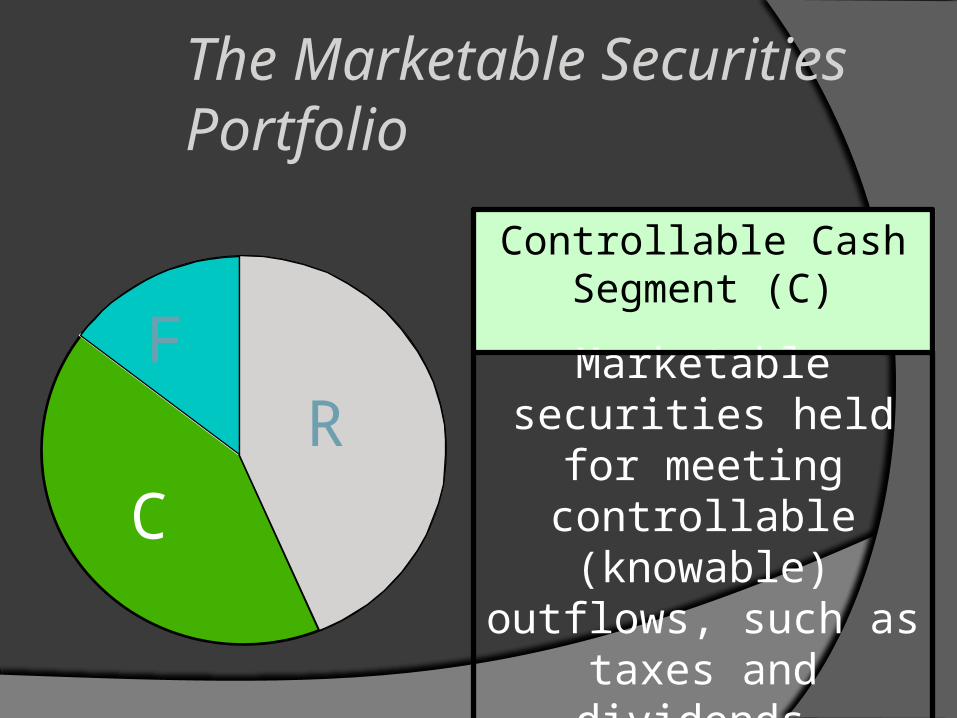

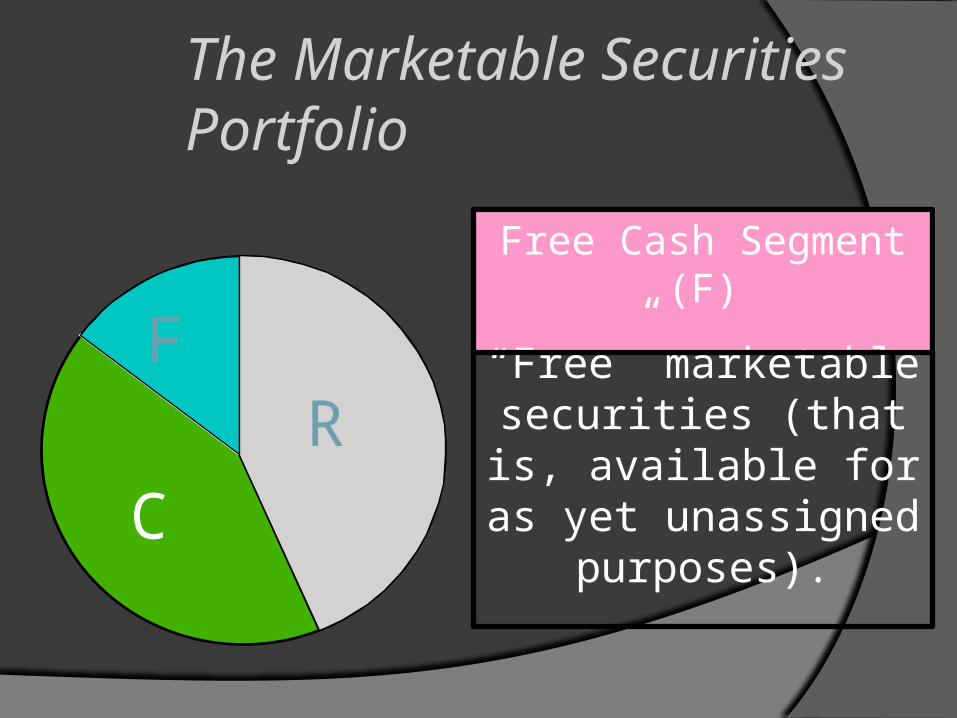

Ready Cash Segment (R)

Optimal balance of marketable securities held to take care of

probable deficiencies in the firm’s cash

account.

RF

C

The Marketable Securities Portfolio

Controllable Cash Segment (C)

Marketable securities held for meeting

controllable (knowable) outflows, such as taxes

and dividends.

RF

C

The Marketable Securities Portfolio

Free Cash Segment (F)

“Free” marketable securities (that is, available for as yet

unassigned purposes).R

F

C

The Marketable Securities Portfolio

Marketability (or Liquidity)The ability to sell a significant volume of securities in a short period of time in the

secondary market without significant price concession.

SafetyRefers to the likelihood of getting back the

same number of dollars you originally invested (principal).

Variables in MarketableSecurities Selection

MaturityRefers to the remaining life of the security.

Interest Rate (or Yield) Risk

The variability in the market price of a security caused by changes in interest

rates.

Variables in Marketable Securities Selection

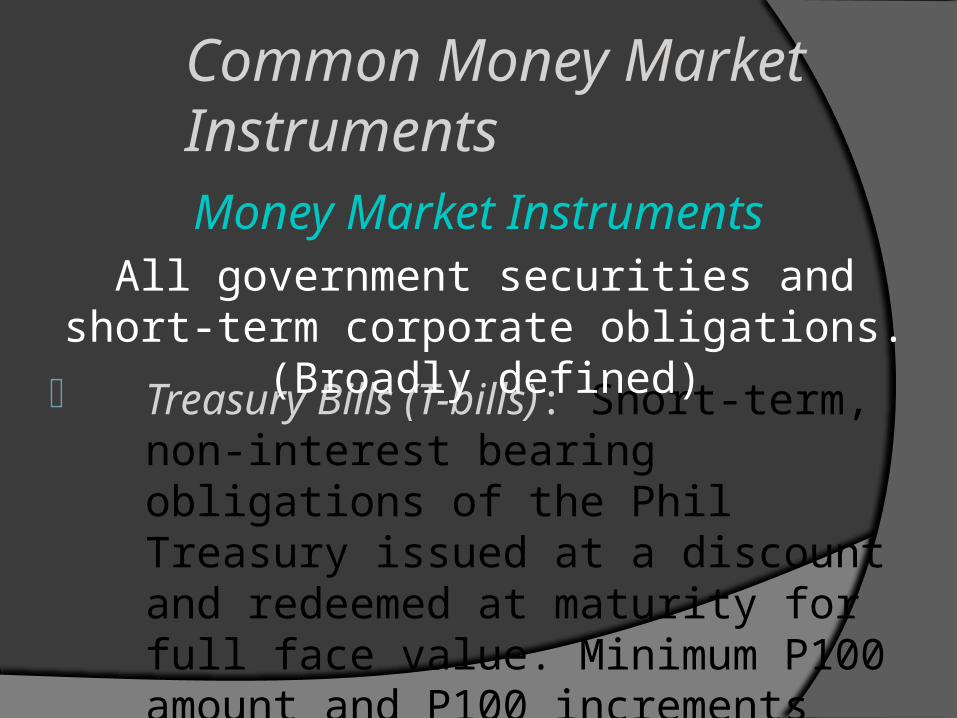

• Treasury Bills (T-bills): Short-term, non-interest bearing obligations of the Phil Treasury issued at a discount and redeemed at maturity for full face value. Minimum P100 amount and P100 increments thereafter.

Money Market InstrumentsAll government securities and short-term corporate obligations. (Broadly defined)

Common Money Market Instruments

• Bankers’ Acceptances (BAs): Short-term promissory trade notes for which a bank (by having “accepted” them) promises to pay the holder the face amount at maturity.

• Repurchase Agreements (RPs; repos): Agreements to buy securities (usually Treasury bills) and resell them at a higher price at a later date.

Common Money Market Instruments

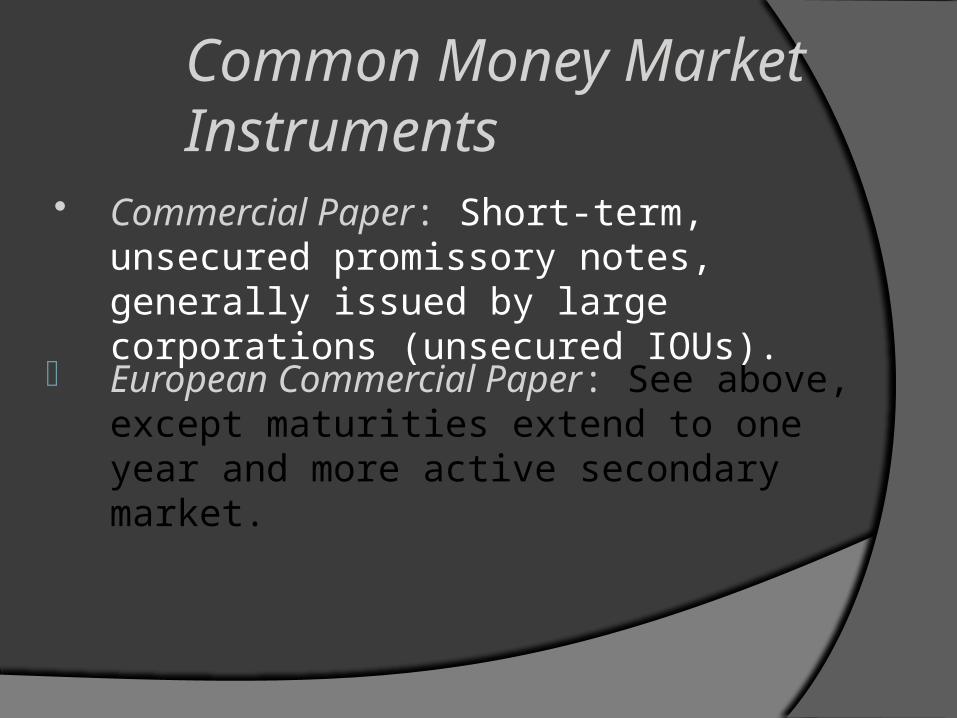

• European Commercial Paper: See above, except maturities extend to one year and more active secondary market.

• Commercial Paper: Short-term, unsecured promissory notes, generally issued by large corporations (unsecured IOUs).

Common Money Market Instruments

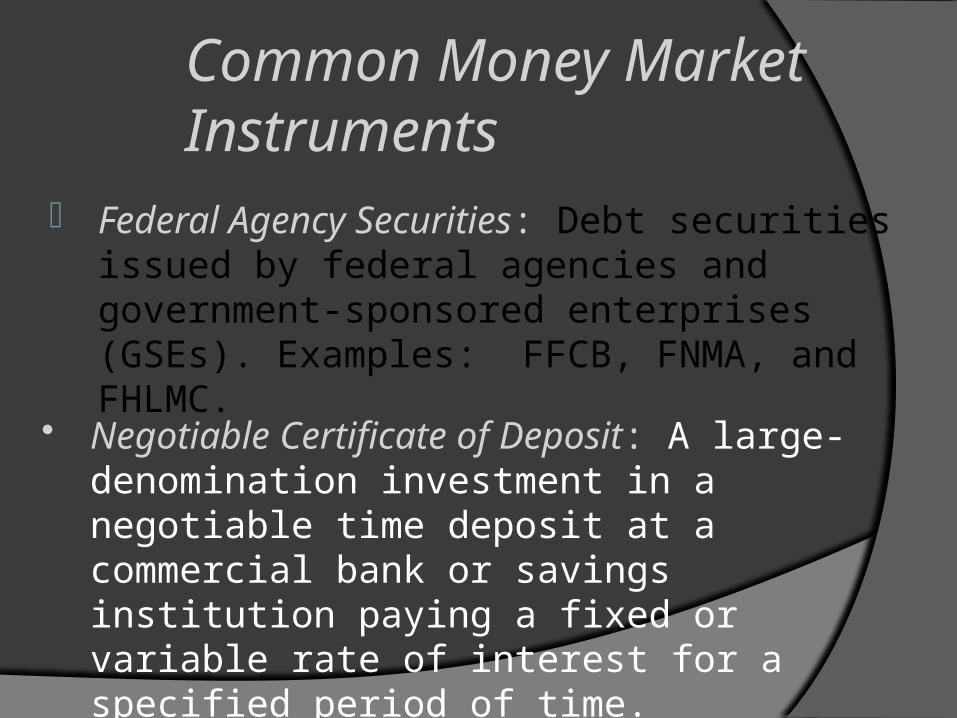

• Federal Agency Securities: Debt securities issued by federal agencies and government-sponsored enterprises (GSEs). Examples: FFCB, FNMA, and FHLMC.

• Negotiable Certificate of Deposit: A large-denomination investment in a negotiable time deposit at a commercial bank or savings institution paying a fixed or variable rate of interest for a specified period of time.

Common Money Market Instruments

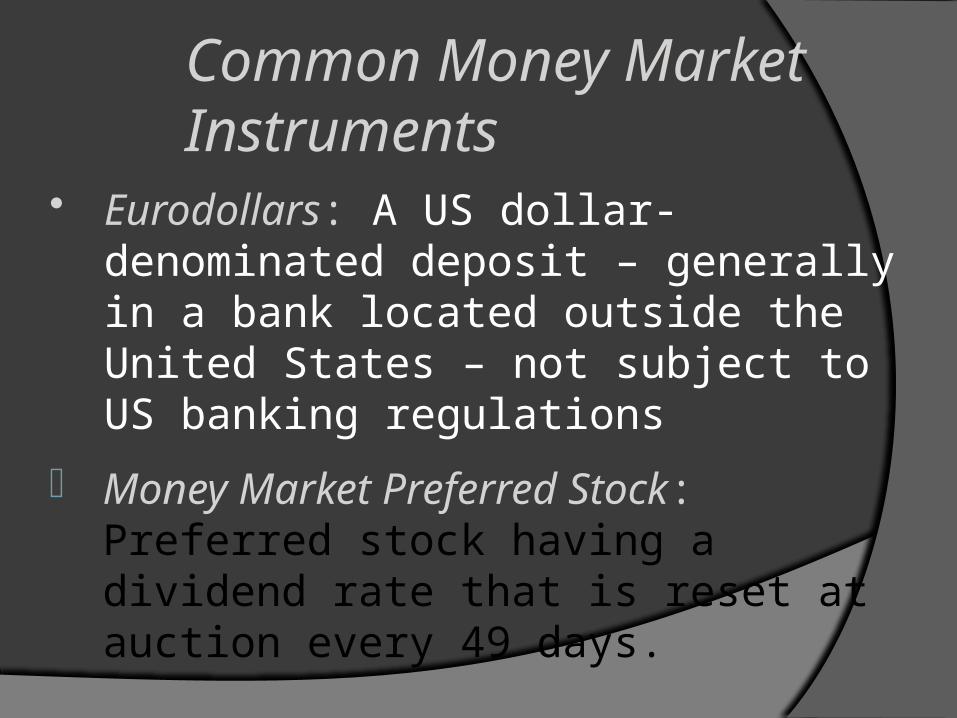

• Money Market Preferred Stock: Preferred stock having a dividend rate that is reset at auction every 49 days.

• Eurodollars: A US dollar-denominated deposit – generally in a bank located outside the United States – not subject to US banking regulations

Common Money Market Instruments

Accounts Receivable and Inventory ManagementWhy do firms accumulate accounts receivable and inventory? Given that accounts receivable and inventory are assets

that do not provide an explicit rate of return, it is important to understand why firms might still want to have these investments.

Granting credit, resulting in Accounts Receivable, is often an essential business practice and can enhance sales. (But also will increase costs.)

Holding adequate inventory is necessary to avoid loss of sales due to stock-outs and have an efficient manufacturing process.

Finding the Optimum Level of Accounts Receivable

Accounts Receivable represent your money sitting in someone else’s bank account.

So, if the firm does grant credit, how do we minimize the impact on cash flow

Firm’s managers must review the firm’s credit policies and evaluate the impact of any proposed changes in policies based on the NPV of incremental cash flows due to the proposed changes

Accounts Receivable - Terms

The terms of sale are generally stated in the form X / Y, n Z

This means that the customer can deduct X percentage if the account is paid within Y days; otherwise, the full amount must be paid within Z days.

Example: 2/10 n 30The company offers a 2% discount if the

invoice is paid in 10 days. Otherwise,Balance due in 30 days.

Average Collection Period (ACP) Old Policy; 2/10, n30

35% of customers pay in 10 days62% of customers pay in 30 days3% of customers pay in 100 daysACP=(.35x10)+(.62x30)+(.03x100)=25.1 days

New Policy; 2/10, n4035%of customers pay in 10 days60% of customers pay in 40 days5% of customers pay in 100 daysACP=(.35x10)+(.60x40)+(.05x100)=32.5 days(If sales are P1M per day, this will cost P7.4M!)

Analysis of Accts. Receivable Changes to Credit Policy Develop pro forma financial statements

for each policy under consideration. Use the pro formas to estimate

incremental cash flows by comparing forecasts to current policy cash flows.

Use the incremental cash flows to estimate the NPV of each policy change.

Choose the policy change that maximizes the value of the firm (highest NPV).

Example:ABC Corporation is considering a credit policy change from offering no credit to offering 30 days credit with no discount

Why might they do this?

-Increase sales

-Increase market share What costs will the firm incur as a result?

-Cost of carrying accounts receivable

-Potential increase in bad debts

-Credit analysis and collection costs

Analysis of Accts. Receivable Changes

Analysis of Accts. Receivable Changes

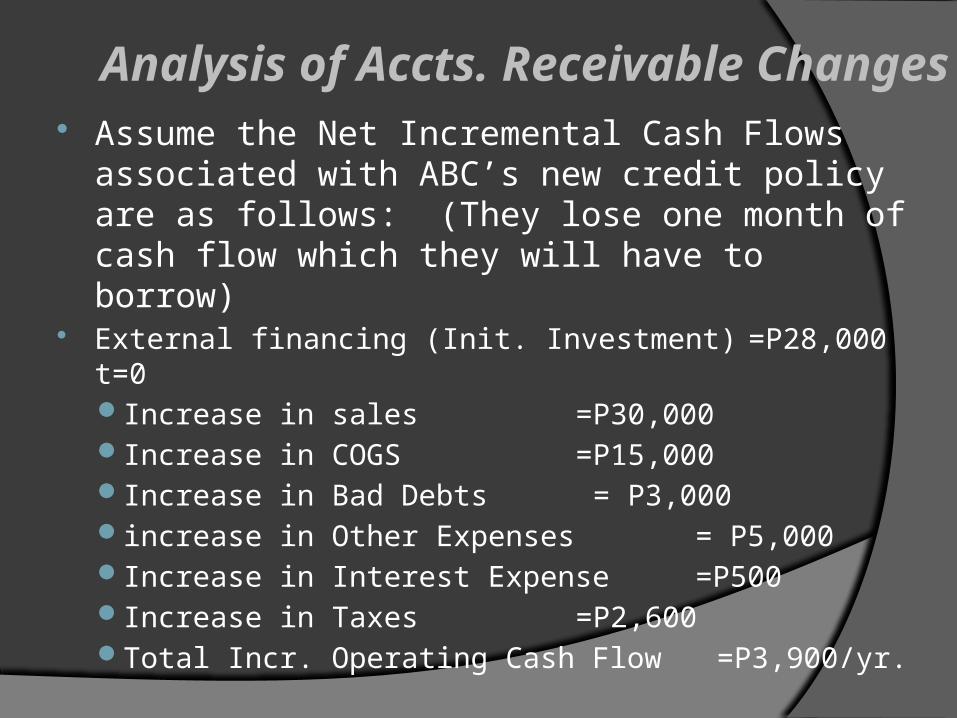

Assume the Net Incremental Cash Flows associated with ABC’s new credit policy are as follows: (They lose one month of cash flow which they will have to borrow)

External financing (Init. Investment) =P28,000 t=0Increase in sales =P30,000 Increase in COGS =P15,000 Increase in Bad Debts = P3,000increase in Other Expenses = P5,000Increase in Interest Expense =P500Increase in Taxes =P2,600Total Incr. Operating Cash Flow =P3,900/yr.

Analysis of Accts. Receivable Changes Calculate the NPV of the change (k = 12%): PV of the expected inflows of P3,900 per year

from t = 0 to infinity (perpetuity)= P3,900/.12 = P32,500

NPV = PV of inflows - initial investment= P32,500 - P28,000 = P4,500

Since NPV > 0, ABC should undertake the credit policy change

Note: If they keep the P28,000, cash flow at 12% = P3,360

Methods of Collection

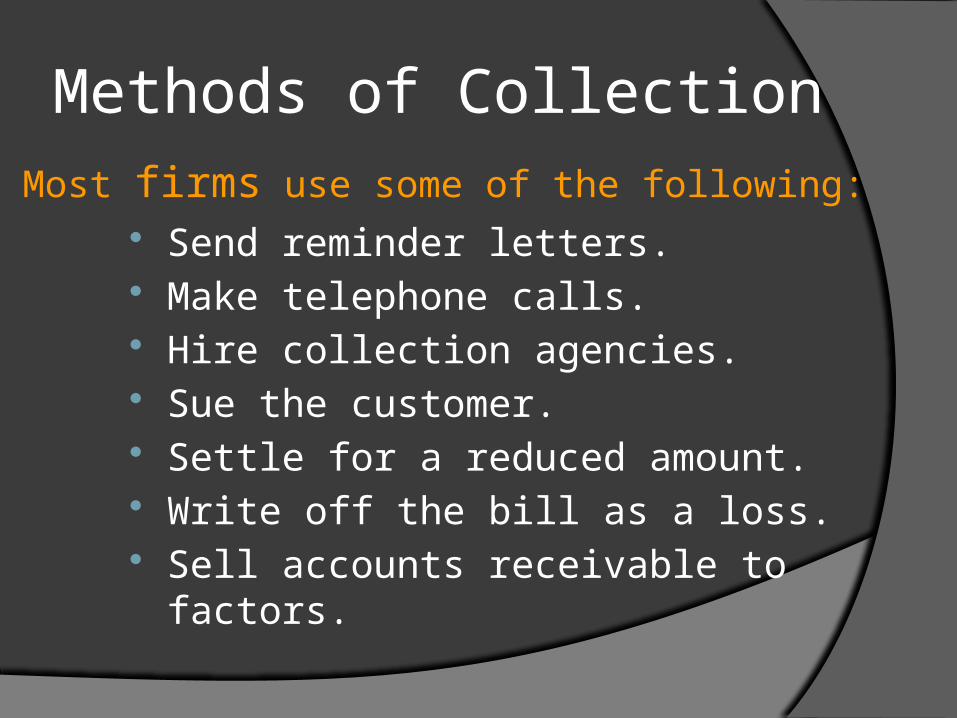

Send reminder letters. Make telephone calls. Hire collection agencies. Sue the customer. Settle for a reduced amount. Write off the bill as a loss. Sell accounts receivable to factors.

Most firms use some of the following:

Inventory Management Typically, inventory accounts for about four to five

percent of a firm's assets. In manufacturing firms, this could be 20 to 25% of the firm’s assets.

Inventory sitting on your shelf earns nothing! In fact, it costs you 20 to 30% of the value of the

inventory just to keep and maintain it. Therefore, the objective is to minimize the

investment in inventory without sacrificing production requirements

149

Inventory Mangement

In order to effectively manage the investment in inventory, two problems must be dealt with: how much to order and how often to order.

The economic order quantity (EOQ) model attempts to determine the order size that will minimize total inventory costs.

Inventory Management

Determining Optimal Inventory (where total costs are minimized)

TotalInventory

Costs =

TotalCarrying

Costs

TotalOrdering

Costs+

Note: We are not talking about the cost of the Inventory itself, but costs of holding and maintaining the inventory

151

Inventory Costs Carrying Costs

Warehouse rent, insurance, security costs,

utility costs, maintenance costs, property taxes,

move and re-arrange, obsolescence, and opportunity cost, i.e., using cash for profitable projects rather than being tied up in inventory.

Ordering costs

Clerical expense, telephone, Material Resource Planning (MRP) system, management time, receiving costs, etc.

Time

OrderQuantity

Q

InventoryLevel

(units)

The EOQ Model assumes the firm orders a fixed amount (Q) at equal intervals.

Time

OrderQuantity

Q

InventoryLevel

(units)

The EOQ Model

Average inventory = Order Quantity2

=

TotalInventory

Costs ( ) CC + ( ) OCOQ2

S OQ

Where:OQ = Order Size (order quantity)S = Annual Sales VolumeCC = Carrying Cost per UnitOC = Ordering Cost per Order

TotalInventory

Costs=

TotalCarrying

Costs

TotalOrdering

Costs+

Order Size (units)

Cost($) Ordering Costs, per unit

= ( )OC S OQ

Ordering Costs

Ordering costs per unit go down as order size increases. Assumes orderingcosts are relatively fixed.

Carrying Costs

Order Size (units)

Cost($)

Carrying Costs = ( ) CC OQ 2

= ( )OC S OQ

Ordering Costs

Carrying costs increaseas the size of the inventory increases.

Total Costs = Carrying Costs + Order CostsTotal Cost = OQ x CC + S x OC

2 OQ

Order Size (units)

Cost($)

Carrying Costs = ( ) CC OQ 2

= ( )OC S OQ

Ordering Costs

X

Y The economic order quantity is the intersection of the X and Y points where total inventory cost is minimized

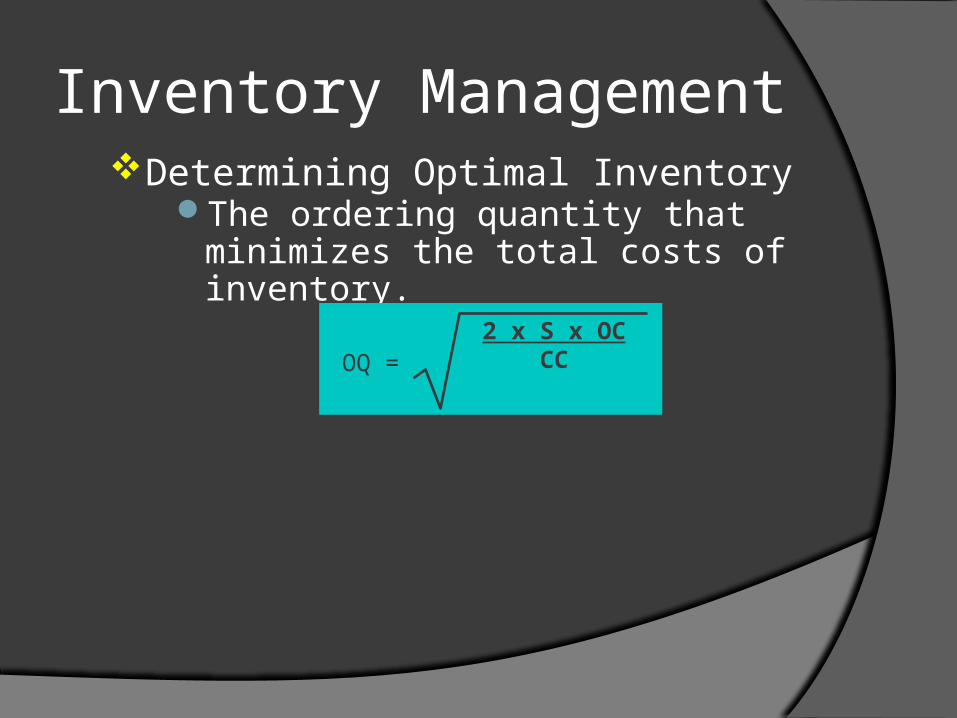

Inventory Management

The ordering quantity that minimizes the total costs of inventory.

Determining Optimal Inventory

OQ =2 x S x OC

CC

Inventory Management

Economic Order Quantity (EOQ)

Example:Awesome Autos expects to sell 1,560 new automobiles in the next year. It currently costs $40 per order placed with the manufacturer. Carrying costs amount to $50 per auto. How many autos should they order each time they place an order?

=

= 49.96 50 cars

2(1560)4050

Determining Optimal Inventory

OQ =2 x S x OC

CC

160

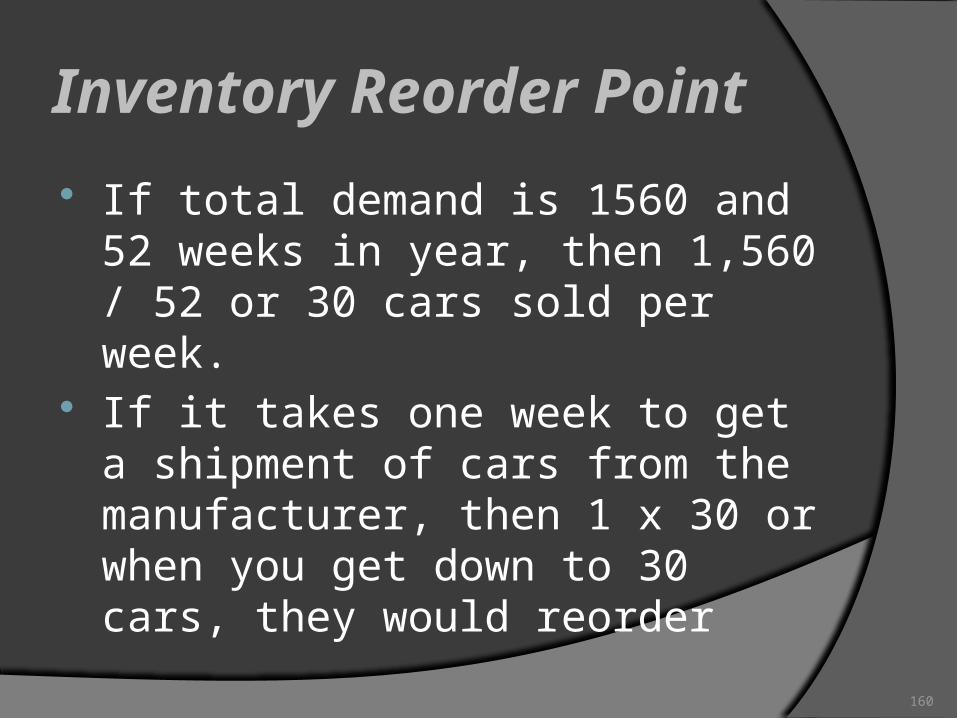

Inventory Reorder Point If total demand is 1560 and 52 weeks

in year, then 1,560 / 52 or 30 cars sold per week.

If it takes one week to get a shipment of cars from the manufacturer, then 1 x 30 or when you get down to 30 cars, they would reorder

161

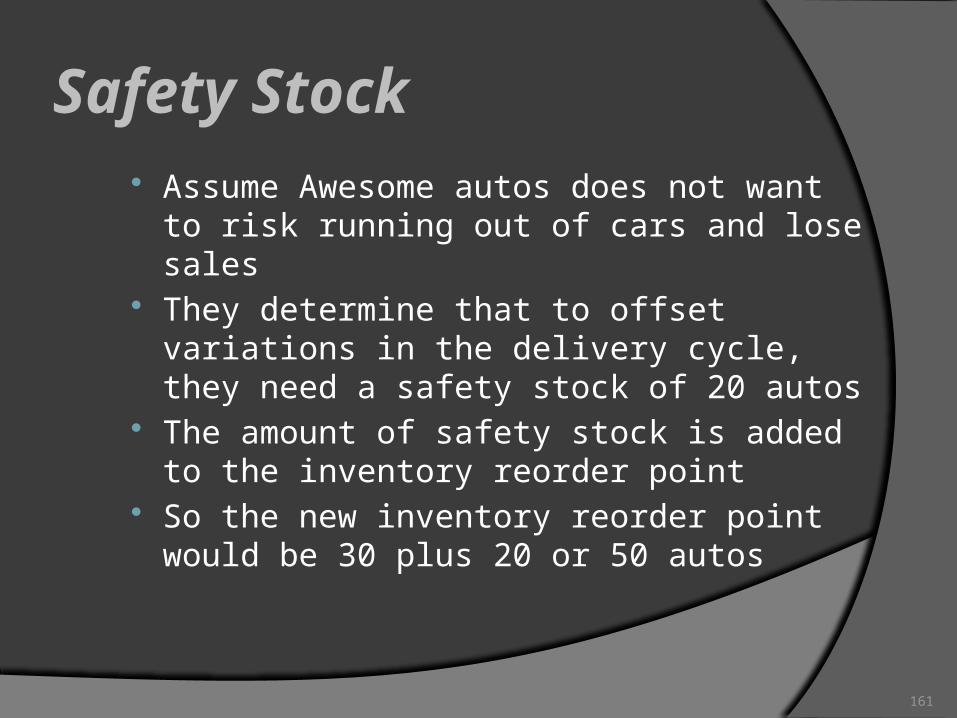

Safety Stock Assume Awesome autos does not want

to risk running out of cars and lose sales They determine that to offset variations

in the delivery cycle, they need a safety stock of 20 autos

The amount of safety stock is added to the inventory reorder point

So the new inventory reorder point would be 30 plus 20 or 50 autos

Inventory Management with Safety Stock- Order before inventory is at zero.

EOQ

Depleted StockDuring Delivery

Inventory Order Point

Actual Delivery Time

SafetyStock

Time

InventoryLevel

(units)

20

50

70

Spontaneous liabilities arise from the normal course of business.

The two major spontaneous liability sources are accounts payable and accruals.

As a firms sales increase, accounts payable and accruals increase in response to the increased purchases, wages, and taxes.

There is normally no explicit cost attached to either of these current liabilities.

Accounts Payable Management

Spontaneous Liabilities: Accounts Payable Management

Accounts payable are the major source of unsecured short-term financing for business firms.

The average payment period has two parts: The time from the purchase of raw materials until the firm

mails the payment Payment float time (the time it takes after the firm mails

its payment until the supplier has withdrawn spendable funds from the firm’s account

The firm’s goal is to pay as slowly as possible without damaging its credit rating.

Spontaneous Liabilities: Analyzing Credit Terms

Credit terms offered by suppliers allow a firm to delay payment for its purchases.

However, the supplier probably imputes the cost of offering terms in its selling price.

Therefore, the firm should analyze credit terms to determine its best credit strategy.

If a cash discount is offered, the firm has two options—to take the cash discount or to give it up.

Taking the Cash DiscountIf a firm intends to take a cash discount, it should pay

on the last day of the discount period.There is no cost associated with taking a cash discount.

Giving Up the Cash DiscountIf a firm chooses to give up the cash discount, it

should pay on the final day of the credit period.The cost of giving up a cash discount is the implied

rate of interest paid to delay payment of an account payable for an additional number of days.

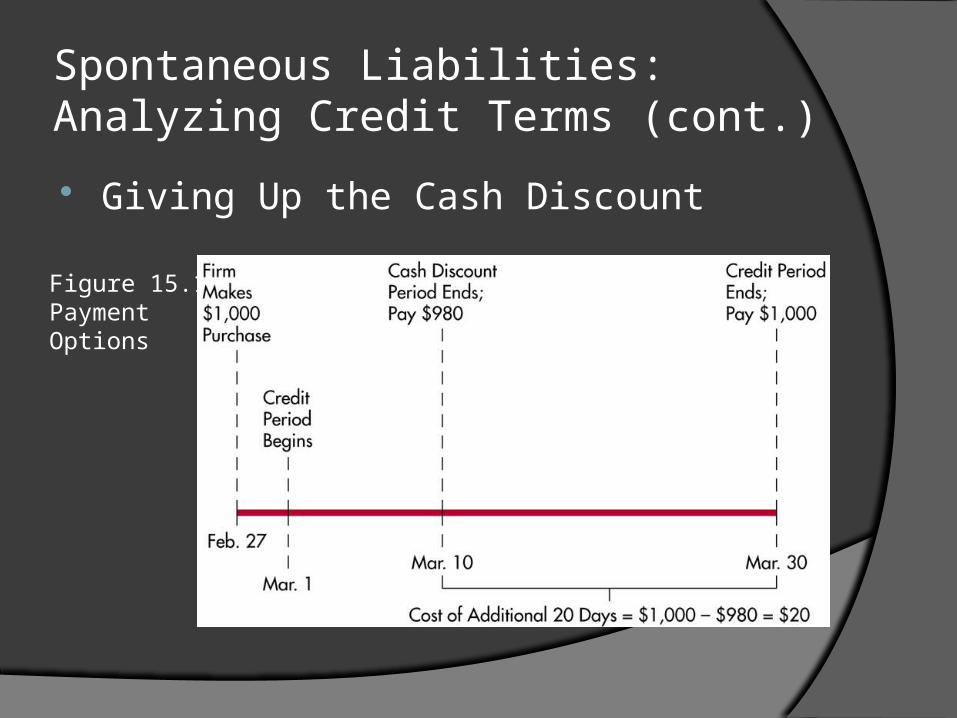

Giving Up the Cash Discount

Spontaneous Liabilities: Analyzing Credit Terms (cont.)

Figure 15.1 Payment Options

Giving Up the Cash Discount

Spontaneous Liabilities: Analyzing Credit Terms (cont.)

Cost = 2% x 365 = 37.24%

100% - 2% 30 - 10

Spontaneous Liabilities: Effects of Stretching Accounts Payable Stretching accounts payable simply

involves paying bills as late as possible without damaging credit rating.

This can reduce the cost of giving up the discount.

Copyright © 2009 Pearson Prentice Hall. All rights reserved.

15-170

Spontaneous Liabilities: Accruals Accruals are liabilities for services received

for which payment has yet to be made. The most common items accrued by a firm

are wages and taxes. While payments to the government cannot

be manipulated, payments to employees can.

This is accomplished by delaying payment of wages, or stretching the payment of wages for as long as possible.

Unsecured Sources of Short-Term Loans: Bank Loans

The major type of loan made by banks to businesses is the short-term, self-liquidating loan which are intended to carry firms through seasonal peaks in financing needs.

These loans are generally obtained as companies build up inventory and experience growth in accounts receivable.

As receivables and inventories are converted into cash, the loans are then retired.

These loans come in three basic forms: single-payment notes, lines of credit, and revolving credit agreements.

Unsecured Sources of Short-Term Loans: Bank Loans (cont.)

Loan Interest RatesMost banks loans are based on the prime

rate of interest which is the lowest rate of interest charged by the nation’s leading banks on loans to their most reliable business borrowers.

Banks generally determine the rate to be charged to various borrowers by adding a premium to the prime rate to adjust it for the borrowers “riskiness.”

Unsecured Sources of Short-Term Loans: Bank Loans (cont.)

Fixed & Floating-Rate LoansOn a fixed-rate loan, the rate of interest is

determined at a set increment above the prime rate and remains at that rate until maturity.

On a floating-rate loan, the increment above the prime rate is initially established and is then allowed to float with prime until maturity.

Like ARMs, the increment above prime is generally lower on floating rate loans than on fixed-rate loans.

Unsecured Sources of Short-Term Loans: Bank Loans (cont.)

Method of Computing InterestOnce the nominal (stated) rate of interest is

established, the method of computing interest is determined.

Interest can be paid either when a loan matures or in advance.

If interest is paid at maturity, the effective (true) rate of interest—assuming the loan is outstanding for exactly one year—may be computed as follows:

Unsecured Sources of Short-Term Loans: Bank Loans (cont.)

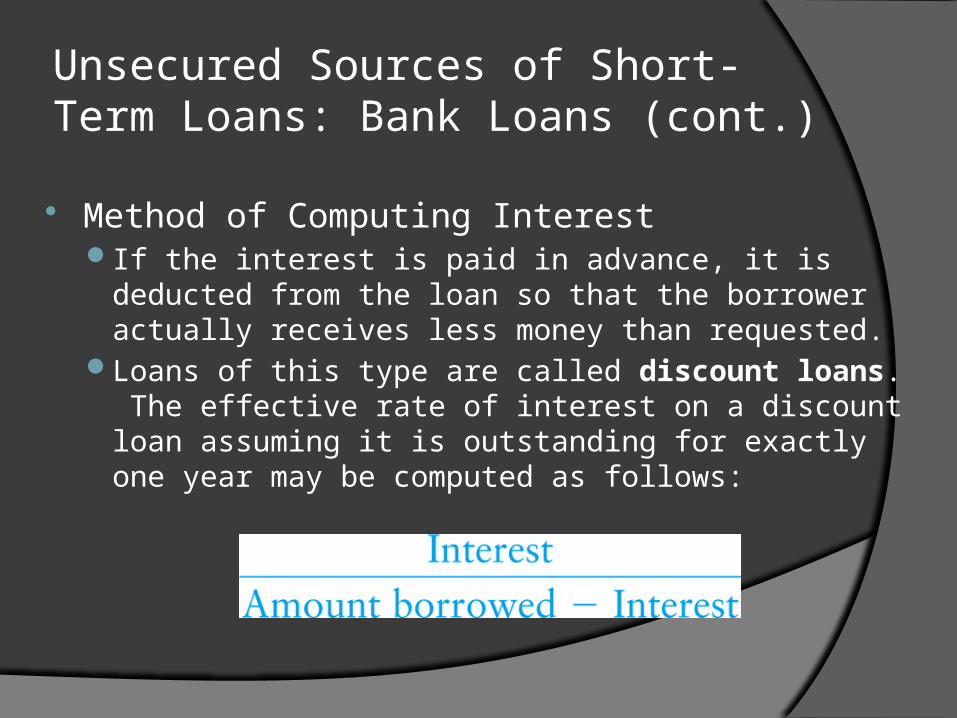

Method of Computing InterestIf the interest is paid in advance, it is deducted from the

loan so that the borrower actually receives less money than requested.

Loans of this type are called discount loans. The effective rate of interest on a discount loan assuming it is outstanding for exactly one year may be computed as follows:

Unsecured Sources of Short-Term Loans: Bank Loans (cont.)

Single Payment NotesA single-payment note is a short-term, one-time

loan payable as a single amount at its maturity.

The “note” states the terms of the loan, which include the length of the loan as well as the interest rate.

Most have maturities of 30 days to 9 or more months.

The interest is usually tied to prime and may be either fixed or floating.

Unsecured Sources of Short-Term Loans: Bank Loans (cont.)

Line of Credit (LOC)A line of credit is an agreement between a

commercial bank and a business specifying the amount of unsecured short-term borrowing the bank will make available to the firm over a given period of time.

It is usually made for a period of 1 year and often places various constraints on borrowers.

Although not guaranteed, the amount of a LOC is the maximum amount the firm can owe the bank at any point in time.

Unsecured Sources of Short-Term Loans: Bank Loans (cont.)

Line of Credit (LOC)In order to obtain the LOC, the borrower may be

required to submit a number of documents including a cash budget, and recent (and pro forma) financial statements.

The interest rate on a LOC is normally floating and pegged to prime.

In addition, banks may impose operating restrictions giving it the right to revoke the LOC if the firm’s financial condition changes.

Unsecured Sources of Short-Term Loans: Bank Loans (cont.)

Line of Credit (LOC)Both LOCs and revolving credit agreements

often require the borrower to maintain compensating balances.

A compensating balance is simply a certain checking account balance equal to a certain percentage of the amount borrowed (typically 10 to 20 percent).

This requirement effectively increases the cost of the loan to the borrower.

Unsecured Sources of Short-Term Loans: Bank Loans (cont.)

Revolving Credit Agreement (RCA)A RCA is nothing more than a guaranteed line

of credit.Because the bank guarantees the funds will be

available, they typically charge a commitment fee which applies to the unused portion of of the borrowers credit line.

A typical fee is around 0.5% of the average unused portion of the funds.

Although more expensive than the LOC, the RCA is less risky from the borrowers perspective.

FINANCING DECISIONS

Short-Term Financing

Spontaneous Financing Negotiated Financing Factoring Accounts Receivable Composition of Short-Term

Financing

Spontaneous Financing

Accounts Payable (Trade Credit from Suppliers)Accrued Expenses

Types of spontaneous financing

Spontaneous Financing

Open Accounts: the seller ships goods to the buyer with an invoice specifying goods shipped, total amount due, and terms of the sale.

Notes Payable: the buyer signs a note that evidences a debt to the seller.

Trade Credit -- credit granted from one business to another.

Examples of trade credit are:

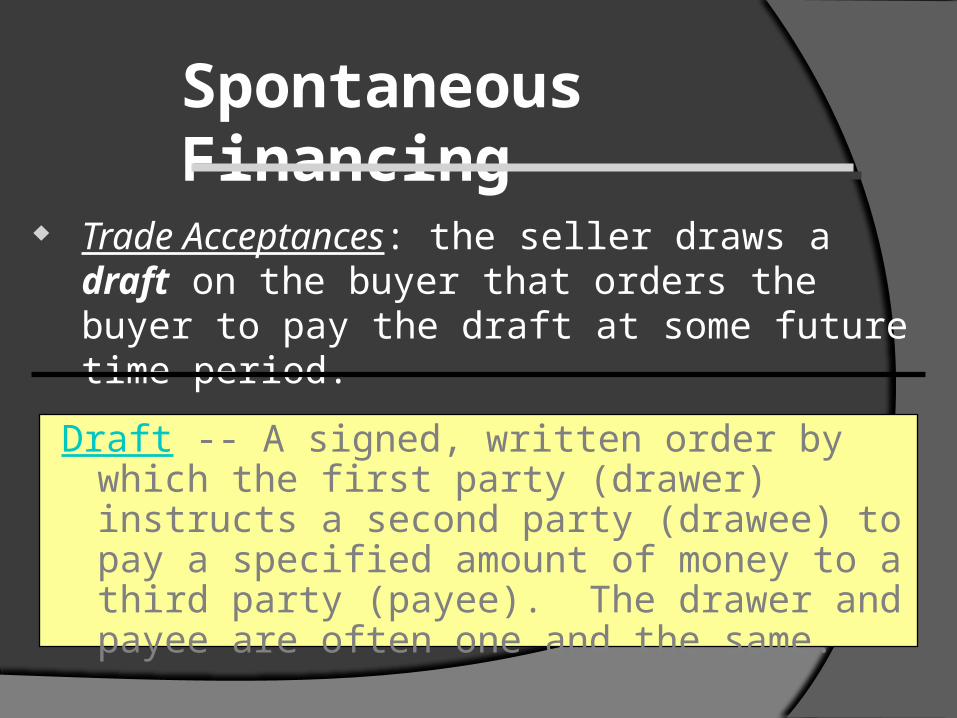

Spontaneous Financing

Draft -- A signed, written order by which the first party (drawer) instructs a second party (drawee) to pay a specified amount of money to a third party (payee). The drawer and payee are often one and the same.

Trade Acceptances: the seller draws a draft on the buyer that orders the buyer to pay the draft at some future time period.

Terms of the Sale

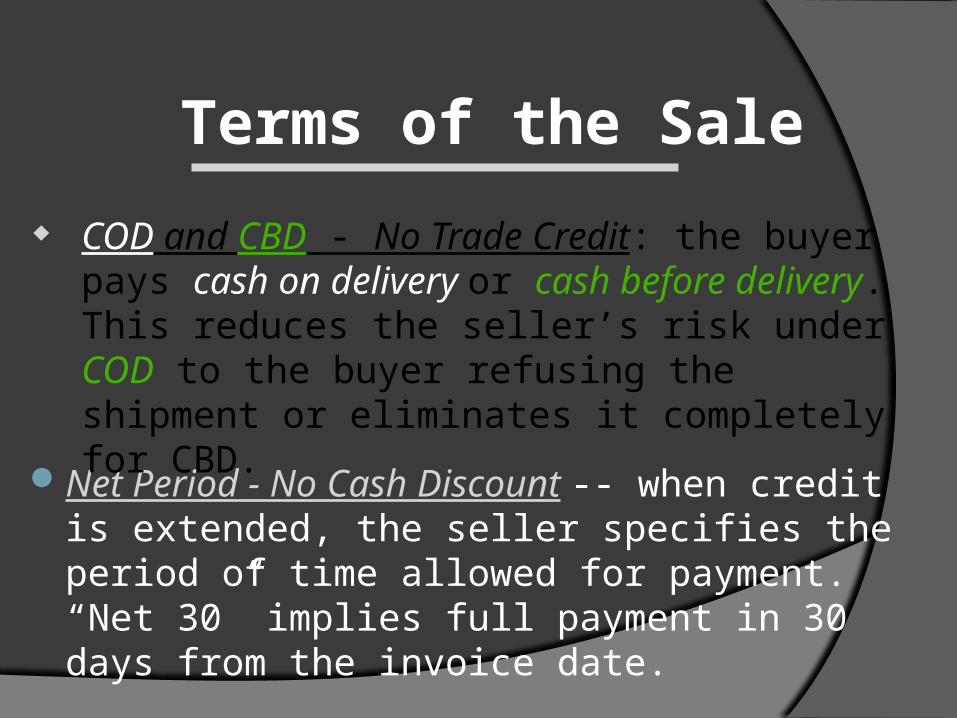

Net Period - No Cash Discount -- when credit is extended, the seller specifies the period of time allowed for payment. “Net 30” implies full payment in 30 days from the invoice date.

COD and CBD - No Trade Credit: the buyer pays cash on delivery or cash before delivery. This reduces the seller’s risk under COD to the buyer refusing the shipment or eliminates it completely for CBD.

Terms of the Sale

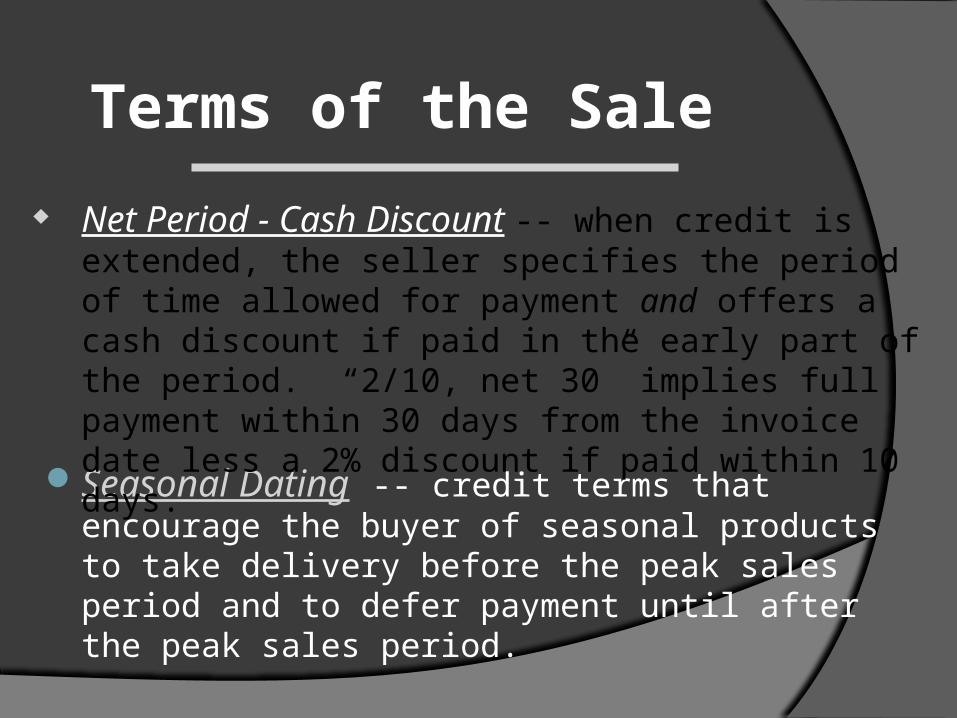

Seasonal Dating -- credit terms that encourage the buyer of seasonal products to take delivery before the peak sales period and to defer payment until after the peak sales period.

Net Period - Cash Discount -- when credit is extended, the seller specifies the period of time allowed for payment and offers a cash discount if paid in the early part of the period. “2/10, net 30” implies full payment within 30 days from the invoice date less a 2% discount if paid within 10 days.

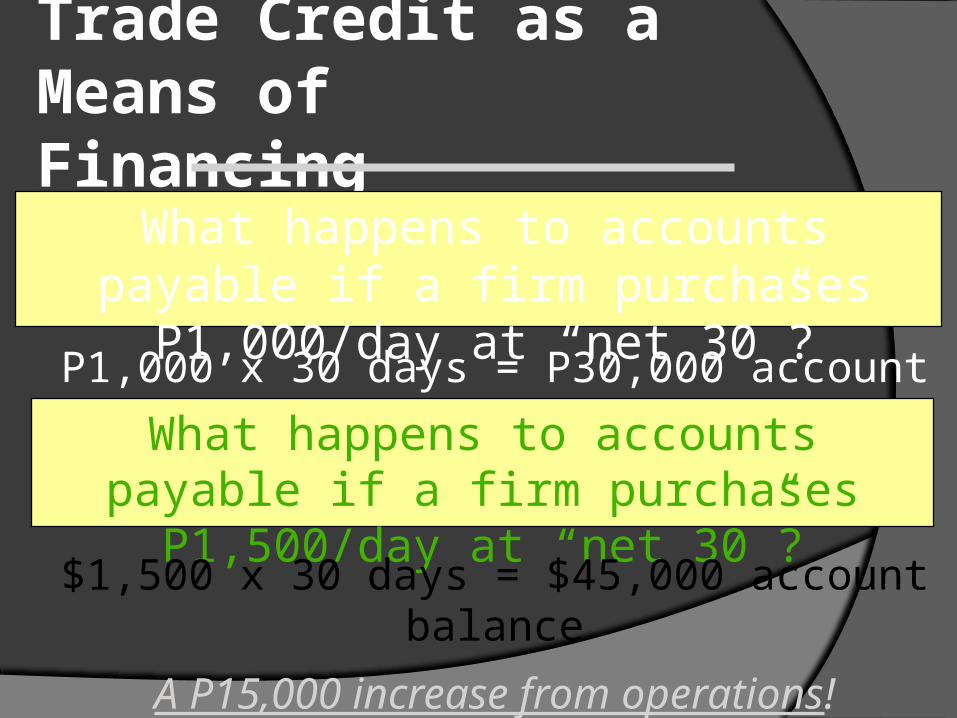

Trade Credit as a Means of Financing

P1,000 x 30 days = P30,000 account balance

What happens to accounts payable if a firm purchases P1,000/day at “net 30”?

What happens to accounts payable if a firm purchases P1,500/day at “net 30”?

$1,500 x 30 days = $45,000 account balance

A P15,000 increase from operations!

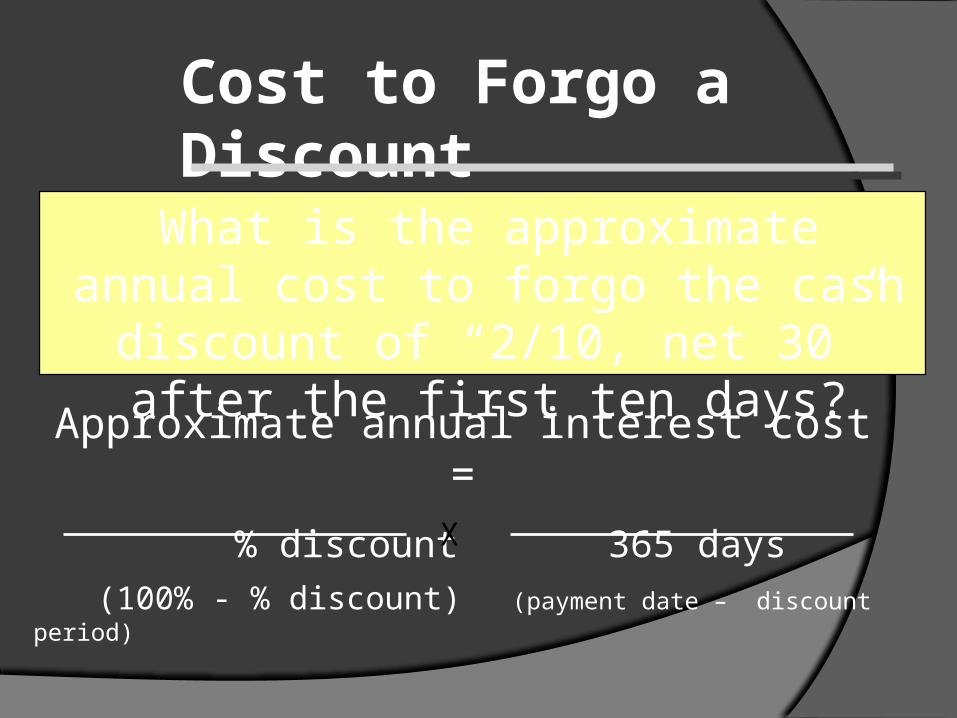

Cost to Forgo a Discount

Approximate annual interest cost =

% discount 365 days

(100% - % discount) (payment date – discount period)

What is the approximate annual cost to forgo the cash discount of “2/10, net 30”

after the first ten days?

X

Cost to Forgo a Discount

Approximate annual interest cost =

2% 365 days

(100% - 2%) (30 days - 10 days)

= (2/98) x (365/20) = 37.2%

What is the approximate annual cost to forgo the cash discount of “2/10, net 30,” and pay

at the end of the credit period?

X

Payment Date* Annual rate of interest

11 744.9% 20 74.5 30 37.2 60 14.9 90 9.3

* days from invoice date

Cost to Forgo a Discount

The approximate interest cost over a variety of payment decisions for “2/10,

net ____.”

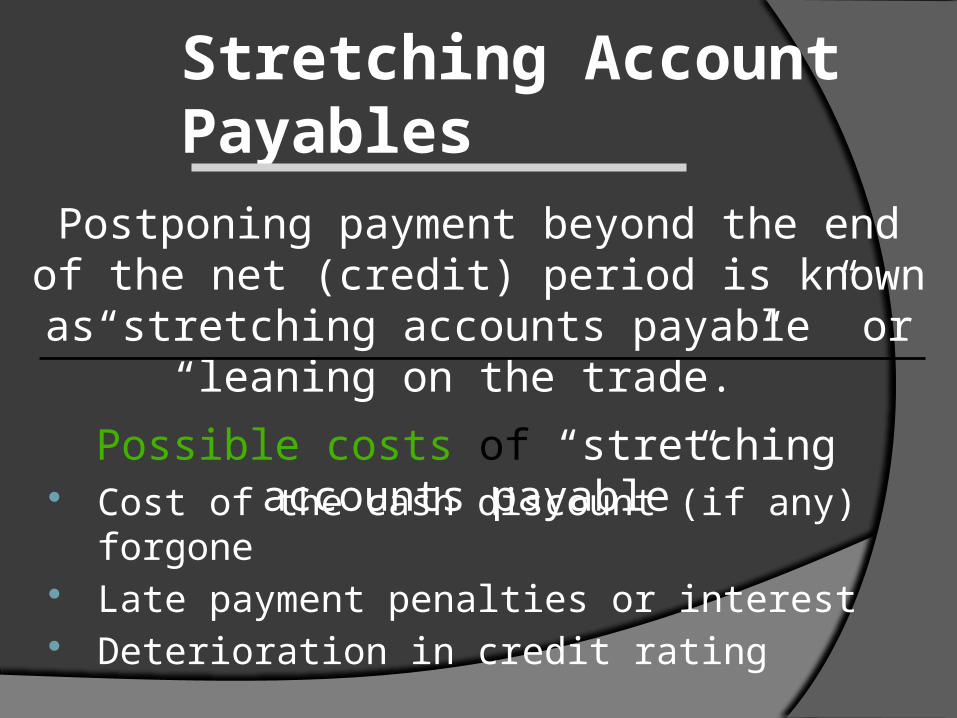

Stretching Account Payables

Cost of the cash discount (if any) forgone Late payment penalties or interest Deterioration in credit rating

Postponing payment beyond the end of the net (credit) period is known as“stretching accounts

payable” or “leaning on the trade.”

Possible costs of “stretching accounts payable”

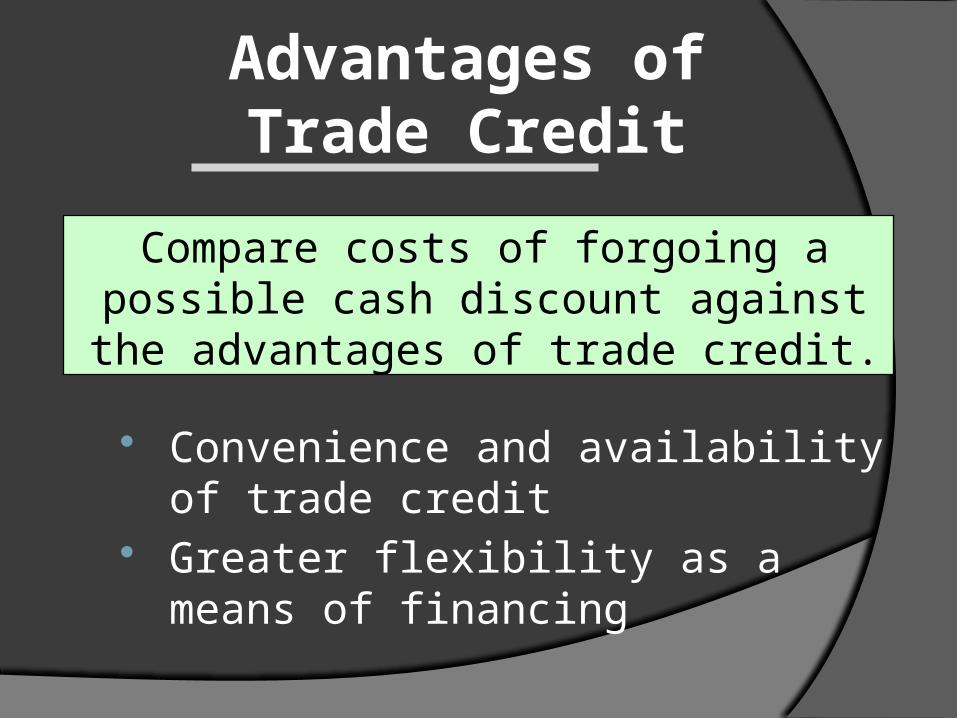

Advantages of Trade Credit

Convenience and availability of trade credit

Greater flexibility as a means of financing

Compare costs of forgoing a possible cash discount against the advantages of

trade credit.

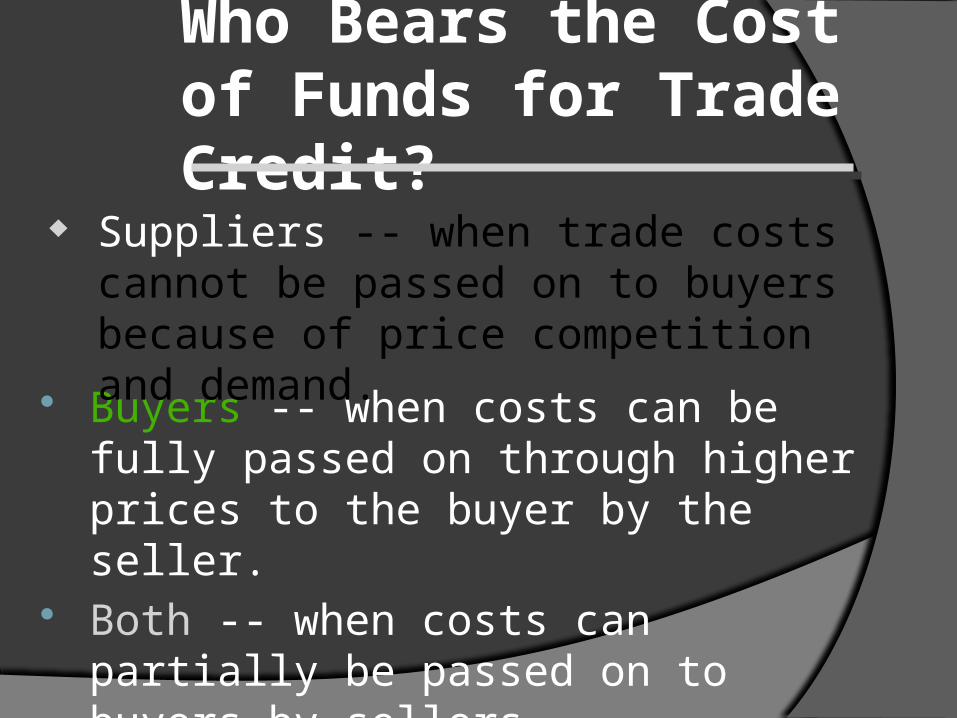

Who Bears the Cost of Funds for Trade Credit?

Buyers -- when costs can be fully passed on through higher prices to the buyer by the seller.

Both -- when costs can partially be passed on to buyers by sellers.

Suppliers -- when trade costs cannot be passed on to buyers because of price competition and demand.

Accrued Expenses

Wages -- Benefits accrue via no direct cash costs, but costs can develop by reduced employee morale and efficiency.

Taxes -- Benefits accrue until the due date, but costs of penalties and interest beyond the due date reduce the benefits.

Accrued Expenses -- Amounts owed but not yet paid for wages, taxes, interest, and dividends. The accrued expenses account is a short-term liability.

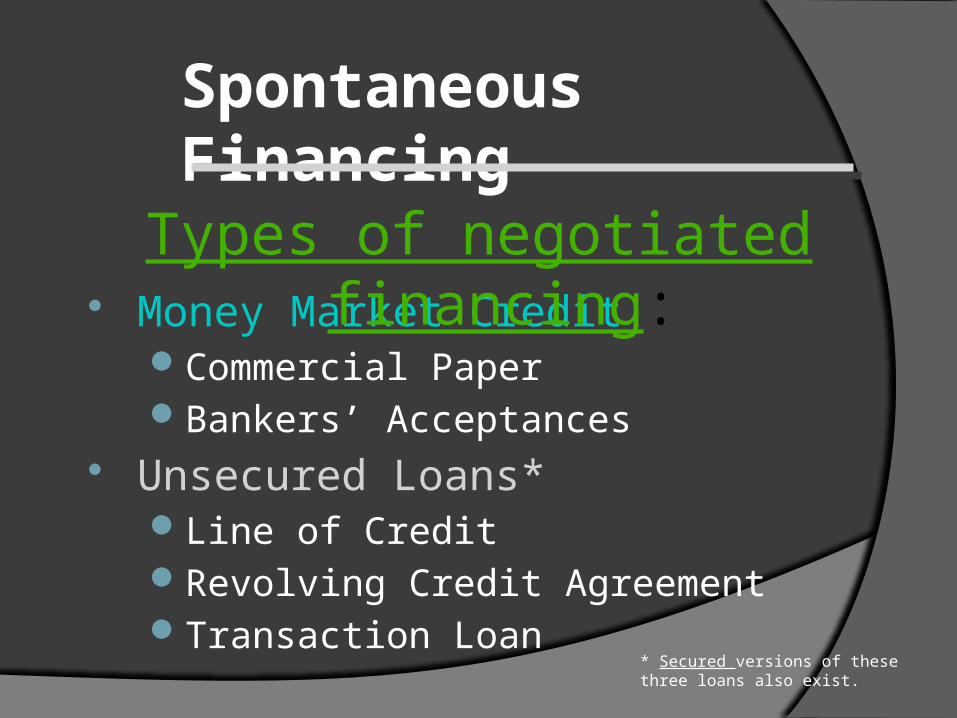

Spontaneous Financing

Money Market CreditCommercial PaperBankers’ Acceptances

Unsecured Loans*Line of CreditRevolving Credit AgreementTransaction Loan

Types of negotiated financing:

* Secured versions of these three loans also exist.

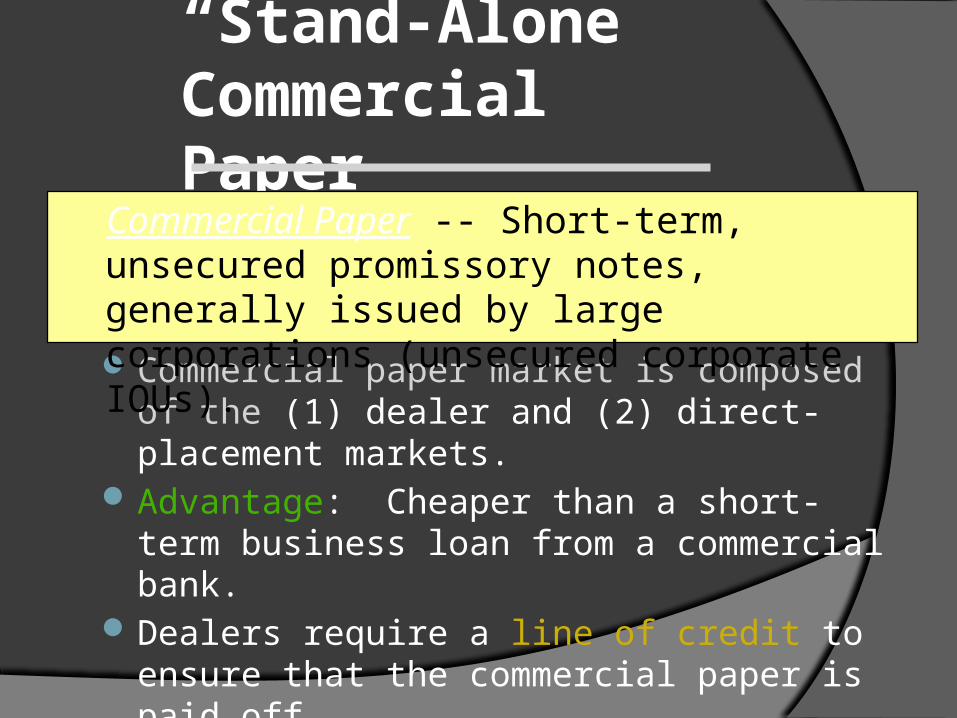

“Stand-Alone” Commercial Paper

Commercial paper market is composed of the (1) dealer and (2) direct-placement markets.

Advantage: Cheaper than a short-term business loan from a commercial bank.

Dealers require a line of credit to ensure that the commercial paper is paid off.

Commercial Paper -- Short-term, unsecured promissory notes, generally issued by large corporations (unsecured corporate IOUs).

“Bank-Supported” Commercial Paper

Letter of credit (L/C) -- A promise from a third party (usually a bank) for payment in the event that certain conditions are met. It is frequently used to guarantee payment of an obligation.

Best for lesser-known firms to access lower cost funds.

A bank provides a letter of credit, for a fee, guaranteeing the investor that the company’s obligation will be paid.

Bankers’ Acceptances

Used to facilitate foreign trade or the shipment of certain marketable goods.

Liquid market provides rates similar to commercial paper rates.

Bankers’ Acceptances -- Short-term promissory trade notes for which a bank (by having “accepted” them) promises to pay the holder the face amount at maturity.

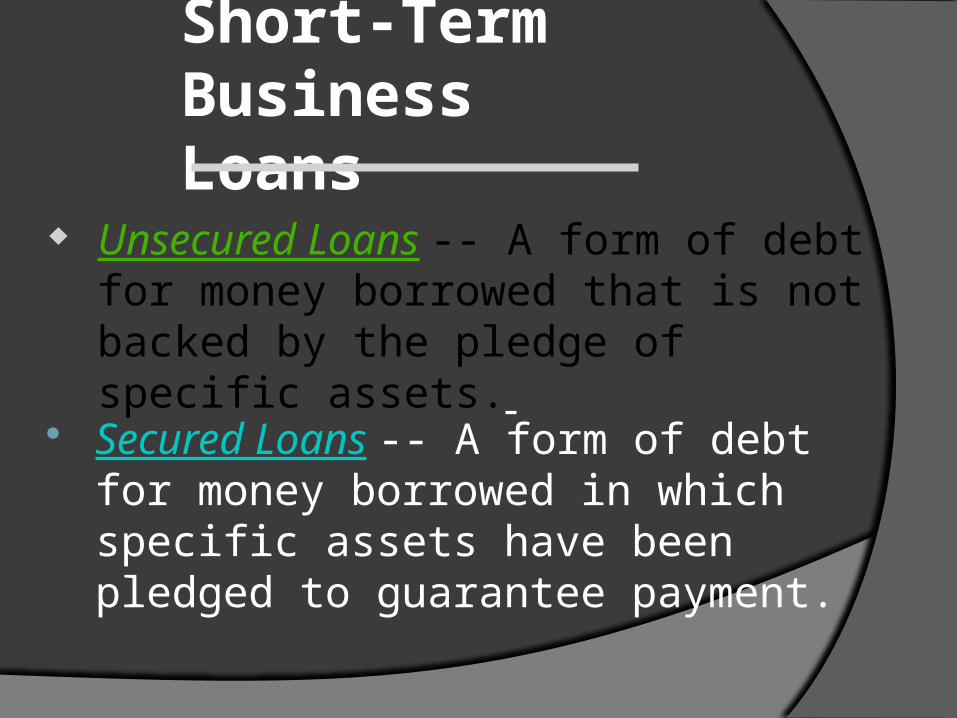

Short-Term Business Loans

Secured Loans -- A form of debt for money borrowed in which specific assets have been pledged to guarantee payment.

Unsecured Loans -- A form of debt for money borrowed that is not backed by the pledge of specific assets.

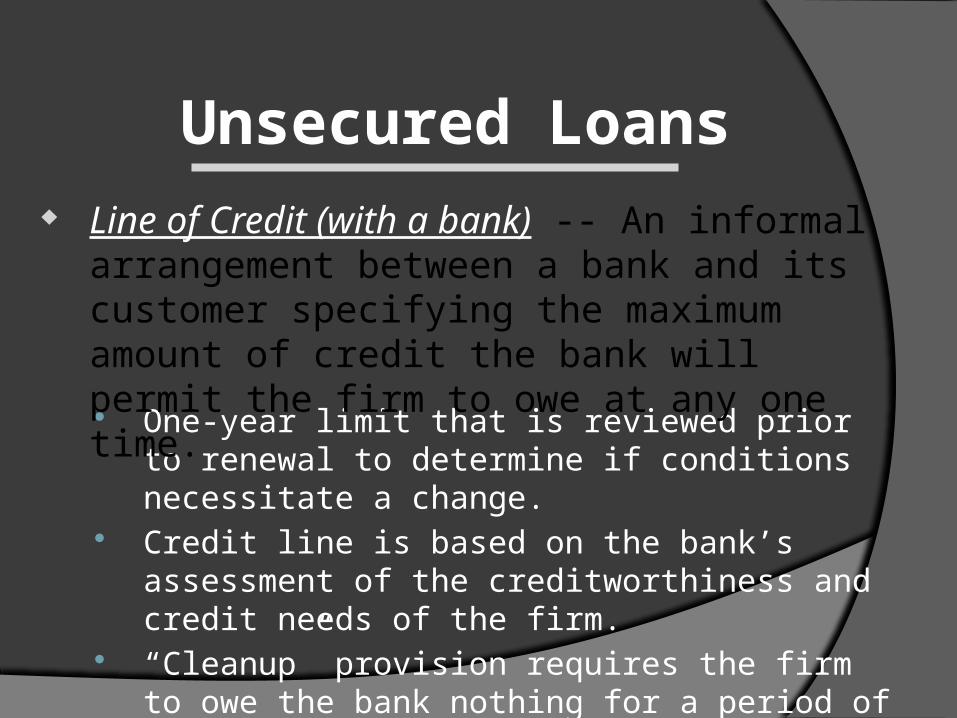

Unsecured Loans

One-year limit that is reviewed prior to renewal to determine if conditions necessitate a change.

Credit line is based on the bank’s assessment of the creditworthiness and credit needs of the firm.

“Cleanup” provision requires the firm to owe the bank nothing for a period of time.

Line of Credit (with a bank) -- An informal arrangement between a bank and its customer specifying the maximum amount of credit the bank will permit the firm to owe at any one time.

Unsecured Loans

Firm receives revolving credit by paying a commitment fee on any unused portion of the maximum amount of credit. Commitment fee -- A fee charged by the lender for

agreeing to hold credit available. Agreements frequently extend beyond 1 year.

Revolving Credit Agreement -- A formal, legal commitment to extend credit up to some maximum

amount over a stated period of time.

Unsecured Loans

Each request is handled as a separate transaction by the bank, and project loan determination is based on the cash-flow ability of the borrower.

The loan is paid off at the completion of the project by the firm from resulting cash flows.

Transaction Loan -- A loan agreement that meets the short-term funds needs of the firm for a single, specific purpose.

Secured (or Asset-Based) Loans

Marketability Life Riskiness

Security (collateral) -- Asset (s) pledged by a borrower to ensure repayment of a loan. If the borrower defaults, the lender may sell the security to pay off the loan.

Collateral value depends on:

Accounts-Receivable-Backed Loans

Quality: not all individual accounts have to be accepted (may reject on aging).

Size: small accounts may be rejected as being too costly (per dollar of loan) to handle by the institution.

One of the most liquid asset accounts. Loans by commercial banks or finance

companies (banks offer lower interest rates).

Loan evaluations are made on:

Accounts-Receivable-Backed Loans

Notification -- firm customers are notified that their accounts have been pledged to the lender and remittances are made directly to the lending institution.

Types of receivable loan arrangements: Nonnotification -- firm customers are not notified

that their accounts have been pledged to the lender. The firm forwards all payments from pledged accounts to the lender.

Inventory-Backed Loans

Marketability Perishability Price stability Difficulty and expense of selling for loan

satisfaction Cash-flow ability

Relatively liquid asset accounts

Loan evaluations are made on:

Types of Inventory-Backed Loans

Floating Lien -- A general, or blanket, lien against a group of assets, such as inventory or receivables, without the assets being specifically identified.

Chattel Mortgage -- A lien on specifically identified personal property (assets other than real estate) backing a loan.

Types of Inventory-Backed Loans

Trust Receipt -- A security device acknowledging that the borrower holds specifically identified inventory and proceeds from its sale in trust for the lender.

Terminal Warehouse Receipt -- A receipt for the deposit of goods in a public warehouse that a lender holds as collateral for a loan.

Types of Inventory-Backed Loans

Field Warehouse Receipt -- A receipt for goods segregated and stored on the borrower’s premises (but under the control of an independent warehousing company) that a lender holds as collateral for a loan.

Factoring Accounts Receivable

Factor is often a subsidiary of a bank holding company.

Factor maintains a credit department and performs credit checks on accounts.

Allows firm to eliminate their credit department and the associated costs.

Contracts are usually for 1 year, but are renewable.

Factoring -- The selling of receivables to a financial institution, the factor, usually “without recourse.”

Factoring Accounts Receivable

Factor receives a commission on the face value of the receivables (typically <1% but as much as 3%).

Cash payment is usually made on the actual or average due date of the receivables.

If the factor advances money to the firm, then the firm must pay interest on the advance.

Total cost of factoring is composed of a factoring fee plus an interest charge on any cash advance.

Although expensive, it provides the firm with substantial flexibility.

Factoring Costs

Composition of Short-Term Financing

Cost of the financing method Availability of funds Timing Flexibility Degree to which the assets are

encumbered

The best mix of short-term financing depends on:

Long-Term Financing A corporation has many stakeholders with conflicting

desires. Wealth creation for the shareholders is our goal. Accounting income is not a sufficient measure of

performance because it ignores risk and the cost of the invested funds.

Economic profit and net present value are two ways we measure wealth creation in a single period and multiple periods.

Capital projects create most of the wealth for the firm but not all projects are equal or should even be considered.

Strategy and competive advantage should guide the capital budgeting process.

Need for long term Finance

Long term vs. short term(working capital) funds requirements

For modernisation, expansion, diversification; huge quantities reqd., irreversible decision

Asset-liability mismatch, interest rate risk, liquidity risk, if LT reqts.met by ST funds

Equity Capital Authorised, Issued, Subscribed and Paid

up capital Par/face value, Issue Price, Book value

and Market Value Rights of equity shareholders

-Right to Income :PAT less preferred dividends-Right to Control: voting rights-Pre-emptive Right: for additional issues, rights issue in the same proportion-Right in liquidation: residual claim over assets

Pros and cons of equity Capital

Advantages No fixed

maturity, no obligation to redeem

No compulsion to pay dividends

Provides leverage capacity

Dividends tax exempt for investors

Disadvantages Dilution of control of

existing owners High Cost: rate of

return expected by equityholders higher than debtholders

Dividends are not tax deductible: hence cost is higher

Issue costs higher: underwriting, brokerage, other issue expenses

Internal Accruals

Pros Readily available, no

talking to outsiders Effectively additional

equity capital, however no issue costs of loss due to underpricing

No dilution of control No expansion in

equity base, hence no dilution of EPS, BV per share etc.

Cons Quantum very limited High Opportunity

costs: dividends forgone by equity holders

Requires careful attention to NPV of projects

Consists of retained earnings and depreciation charges

Preference Capital Is a hybrid form of financing, payment after debt but

before equity Equity features:

-out of distributable profits -not an obligatory payment

-dividends not tax deductible Debt features:

-dividend rate is fixed-capital is redeemable-normally no right to vote

Can have other features like cumulative, convertible, participating

Preference CapitalPros

No obligation to pay dividend, no bankruptcy or legal action for non payment

Financial distress of redemption obligation not very high Part of net worth, hence increases its creditworthiness/

leverage capacity No dilution of control No pledging of assets required

Cons Expensive source since dividends not tax deductible Though no legal consequences, liability to pay

dividends stands, can spoil company’s image Can acquire voting rights in some cases Have claim prior to equity holders

Term Loans Provided by FIs/banks Can be in domestic/foreign currency, liability on

FC loans translated to rupees for payment Are typically secured against fixed assets/

hypothecation of movable properties, prime security/ collateral security

Definite obligations on interest and principal repayment; interest paid periodically; based on credit risk and pegged to a floor rate

Carry restrictive covenants for future financial and operational decisions of the company, its management, future fund raising, projects, periodic reports called for

Term LoansPros

Interest on debt is tax deductible Does not result in dilution of control Do not partake in value created by the firm Issue costs of debt is lower Interest cost is normally fixed, protection against

high unexpected inflation Has a disciplining effect on management

Cons Entails fixed obligation for interest and principal, non

payment can even lead to bankruptcy/ legal action Debt contracts impose restrictions on firm’s financial

and operational flexibility Increases financial leverage, excess raises cost of

equity to the firm If inflation rate dips, cost of debt higher than

expected

Debentures Like promissory notes, are instruments for raising LT

debt More flexible compared to term loans as they offer

variety of choices as regards maturity, interest rate, security, repayment and other special features

Interest rate can be fixed/floating/deep discount Convertibility : Can be FCDs, NCDs, PCDs Warrants : Can have warrants attached, detachable or

non detachable, detachable traded separately Option : Can be with call or put option Redemption: Bullet payment or redeemed in instalments Security: Secured or unsecured Credit rating: Need to have a credit rating by a credit

rating agency Trustee: Need to appoint a trustee to ensure fulfilment of

contractual obligations by company DRR: Company needs to create a DRR if maturity more

than 18 months

Other forms of Finance Leasing: asset leased out in lieu of lease rentals, title

not transferred, only economic use of assets given; can be financial lease or operating (service) lease

Hire Purchase: ownership transferred to the buyer after all the installments paid up

Securitisation: assets involving financial claims pooled and financial instruments created, thus creating cash out of receivables

Government Subsidies: central and state govts offer cash subsidies to units in backward areas, classified in three categories

Sales tax deferments and exemptions: payment deferred for a fixed period, like interest free loan; or exemptions given for certain no. of years

Suppliers credit: available from suppliers of machinery, other fixed assets, terms devised to defer payment, or pay in installments over a period of time

Leasing vs. Hire Purchase

Leasing Ownership not transferred to lessee Depreciation benefit to lessor

Magnitude of funds high, for big ticket items No margin money/down payment required Maintenance of asset by lessor in operating lease Tax benefits of depreciation taken by lessor; lessee gets tax shield on lease

rentals Considered off balance sheet mode of financing, as no asset or liability

figures in balance sheet

Hire-Purchase Ownership transferred to hirer on payment of all instalments Depreciation shield available to hirer Maybe for smaller value capital goods Some down payment reqd

Maintenance cost borne by hirer

Hirer allowed depreciation claim and finance charge for taxation; seller may claim interest on amount borrowed to acquire asset

Asset figures in balance sheet on complete of purchase

Raising Long Term Finance

Initial Public Offer (IPO) Secondary Public offer Rights Issue Bought out deals Euro Issues Private Placement Preferential allotment Venture Capital/ Private Equity

transactions Obtaining a term loan

Initial Public OfferPros

Access to larger amount of funds Further growth limited companies not using this route Listing: provides exit route to promoters; ensures marketability of

existing shares Encash on value created in the firm Recognition in market Stock prices provide useful indicators to management Sometimes stipulated by private investors in the company

Cons Pricing may have to be attractive to lure

investors Loss of flexibility Higher accountability More disclosure requirements to be met Visibility in market Cost of making a public issue quite high

Other aspects of a public issue

Eligibility criteria defined: net worth, track record of profitability, issue in same year; secondary issues have no such restrictions

Book Building process: process of tendering quantities at prices within a band

Issue expenses: underwriting, brokerage commissions, fees to managers to the issue, registrars, printers, advertisers, listing fees, stamp duty

Issue pricing: free pricing, disclose basis for issue price

Public issue of debt: appointment of debenture trustee, creation of DRR, credit rating reqd., security to be created

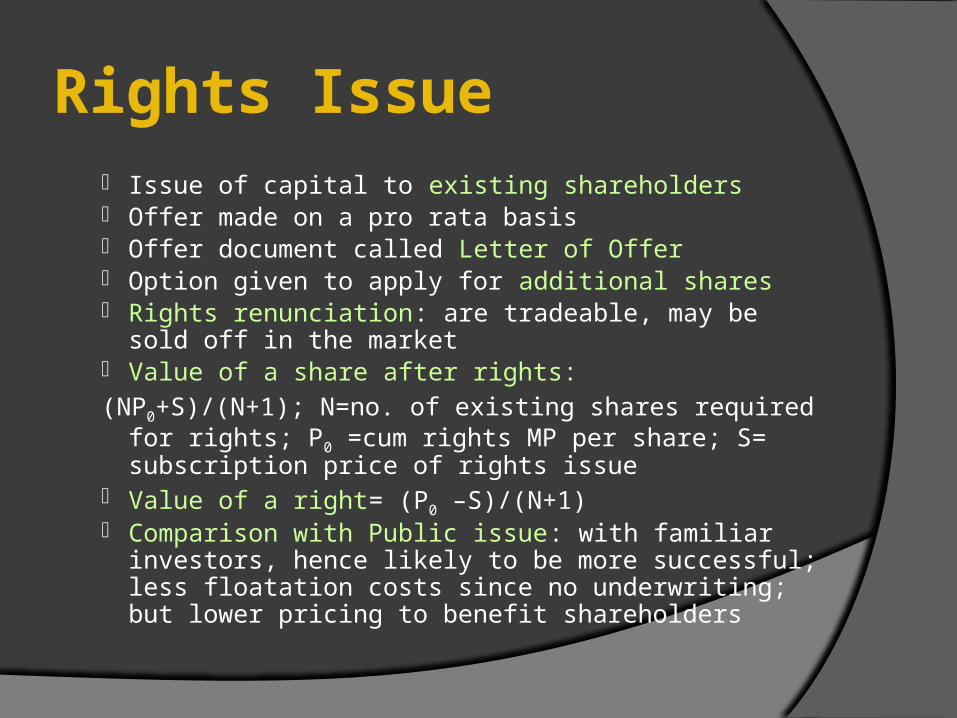

Rights Issue• Issue of capital to existing shareholders• Offer made on a pro rata basis• Offer document called Letter of Offer• Option given to apply for additional shares• Rights renunciation: are tradeable, may be sold off

in the market• Value of a share after rights:(NP0+S)/(N+1); N=no. of existing shares required for

rights; P0 =cum rights MP per share; S= subscription price of rights issue

• Value of a right= (P0 –S)/(N+1)• Comparison with Public issue: with familiar

investors, hence likely to be more successful; less floatation costs since no underwriting; but lower pricing to benefit shareholders

![[PPT]Introduction to Financial Management - San Francisco …user · Web viewFIN 819: Financial Management Administrative Issues Course Overview FIN 819: Lecture 1 FIN 819: Lecture](https://img.pdfslide.net/doc/110x75/5ac81c047f8b9acb7c8c5f54/pptintroduction-to-financial-management-san-francisco-viewfin-819-financial.jpg)